analysis of exchange rate risk & hedging strategies

TRANSCRIPT

Analysis of Exchange Rate Risk & Hedging Strategies - Study

on Dutch Listed Firms

Author: Akash Kumar (11133317)

Contact: [email protected]

Supervisor: Prof. Jeroen Ligterink

Program: Amsterdam MBA (Full Time – 2016-17)

Analysis of Exchange Rate Risk & Hedging Strategies

ABSTRACT

Currency risk arises from a combination of foreign currency exposure and volatility in foreign

currency exchange rate with respect to domestic currency. As the firms may experience

considerable exposure to foreign exchange rate risk because of foreign currency based activities

and international competition. Many currencies are volatile as they show high fluctuations in the

value due to various factors, such as trading speculation, change in global political and economic

scenario, policy of central banks and many other factors. To minimize the effect of exchange rate

risk, many firms use hedging techniques to over exposed risk, which may help to minimize the

effects of exchange rate risk. In this paper, some hedging strategies will be discussed, for

minimizing the firm’s exposure due to exchange rate fluctuations and test whether hedging

diminishes the firm’s exposure.

We analyse the relationship between the change of exchange rate and stock returns of 17 Dutch

firms over a period of 10 years (2006-2016). We find that 41% of the firms are significantly

exposed to exchange rate risk. We also examined the relationship between the coefficient of

exchange rate exposure and foreign currency derivatives used by the firm to hedge the currency

exposure. We were not able to any significant relationship between coefficient of exchange rate

exposure and foreign currency derivatives.

CONTENTS

Abstract

List of Abbreviations

I. Introduction …………………………………………………………………………. 1

A. Background ………………………………………………………………… 1

B. Research Objective …………………………………………………………. 4

II. Conceptual Framework : Theory Review, Tools & Framework ……………………. 7

A. Foreign Exchange Risk ……………………………………………………... 7

B. Type of Foreign Exchange Risk ……………………………………………. 7

C. Factors Affecting Exchange Rate Fluctuations ……………………………... 9

D. Hedging ……………………………………………………………………. 10

E. Hedging Instruments ………………………………………………………. 12

a. Currency Forwards ………………………………………………… 12

b. Currency Futures …………………………………………………... 13

c. Currency Options ………………………………………………….. 13

d. Currency Swaps …………………………………………………... 14

F. Literature Review ………………………………………………………….. 15

III. Framework ………………………………………………………………………… 18

A. Exchange Rate Fluctuations and Stock Return …………………………..... 19

B. Currency Derivative and Exchange Rate Exposure ……………………….. 21

C. Empirical Findings ………………………………………………………… 21

IV. Managerial Implications …………………………………………………………... 25

V. Conclusion ……………………………………………………………………….... 29

VI. References …………………………………………………………………………. 31

LIST OF ABBREVIATIONS / KEY WORDS

Forex / FX – an abbreviation of ‘foreign exchange’

Euro (€) – Currency of 19 Eurozone countries

USD (US$) – United States Dollar, currency of U.S.

Foreign Exchange Fluctuation – The change in value of one currency with respect to another

currency.

Domestic currency – the currency issued for use in a particular jurisdiction. For example, for

Netherlands it would be Euro

Forward exchange contract – an agreement to exchange one currency for another currency on an

agreed date (for any date other than the ‘spot’ date)

Hedging – A transaction which protects an asset or liability against a fluctuation in the value of

foreign currency.

option – A derivative instrument.

A call option is in the money if its strike price is below the current spot price.

A put option is in the money if its strike price is above the current spot price.

Spot rate – Arrangement to exchange currencies in two working days.

Bid – the rate at which a dealer is willing to buy the base currency.

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 1

I. Introduction

A. Background:

An exchange rate of two currencies is the rate at which one currency can be exchanged for another

currency or simply the value of one country’s currency with another country’s currency.

Currency trading has been prevailing since the ancient times. During the early time, Byzantine

government kept a monopoly on the exchange of currency (Hasebroek, 1933: 155-157). The trade

was taking place in the ancient world and different kingdoms used different currency (mostly made

of gold or silver), the value of this currency was determined by the amount of gold/silver in one

kingdoms coin with respect to another kingdom’s. The coin with less gold was cheaper, hence

more coins had to be paid for the lower value coins.

During the 15th century, Italian Banks, such as those run by the Medici family, started to open

foreign branches to effect payments and currency exchange for their clients (Smith, Walter,

DeLong, 2012: 3). In order to facilitate currency exchange and international payments Nostro and

Vostro bank accounts were started during this time (Roover, 1999: 130). These accounts are even

used today by firms doing international transactions.

During the modern era, Bretton Woods Accord was signed in 1944. Under this system, each

country was obligated to maintain its currency fluctuations within a range of ±1% from the

currency’s par exchange rate. The member states were required to control their country’s currency

within the ±1% parity by intervening in their foreign exchange markets. This gave rise to pegged

rate currency regime, wherein different currencies were pegged to dollar and the dollar was linked

to gold at the rate of $35 per ounce.

Bretton Woods system ended in 1971, after the United States unilaterally terminated convertibility

of the US dollar to gold. This was the starting of free floating exchange rate regime, wherein most

of the currencies were determined by the market conditions. The central bank could only control

their local currency rate by intervening in the market (by purchasing or selling the currency).

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 2

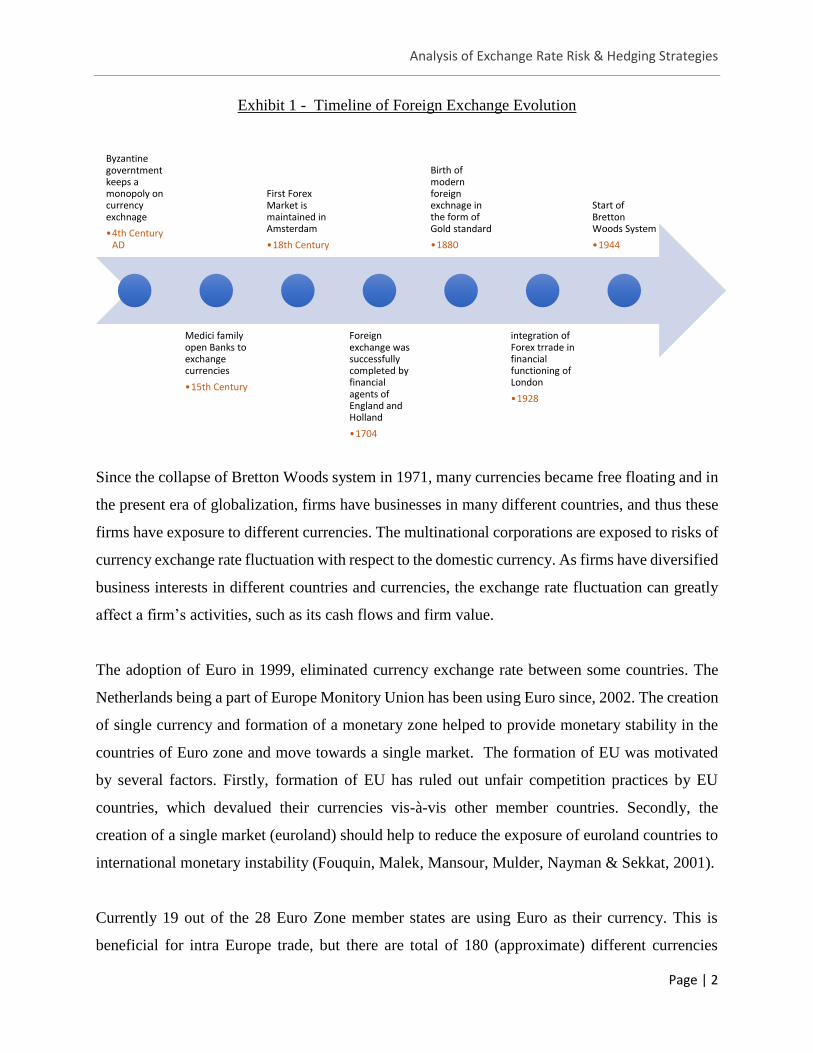

Exhibit 1 - Timeline of Foreign Exchange Evolution

Since the collapse of Bretton Woods system in 1971, many currencies became free floating and in

the present era of globalization, firms have businesses in many different countries, and thus these

firms have exposure to different currencies. The multinational corporations are exposed to risks of

currency exchange rate fluctuation with respect to the domestic currency. As firms have diversified

business interests in different countries and currencies, the exchange rate fluctuation can greatly

affect a firm’s activities, such as its cash flows and firm value.

The adoption of Euro in 1999, eliminated currency exchange rate between some countries. The

Netherlands being a part of Europe Monitory Union has been using Euro since, 2002. The creation

of single currency and formation of a monetary zone helped to provide monetary stability in the

countries of Euro zone and move towards a single market. The formation of EU was motivated

by several factors. Firstly, formation of EU has ruled out unfair competition practices by EU

countries, which devalued their currencies vis-à-vis other member countries. Secondly, the

creation of a single market (euroland) should help to reduce the exposure of euroland countries to

international monetary instability (Fouquin, Malek, Mansour, Mulder, Nayman & Sekkat, 2001).

Currently 19 out of the 28 Euro Zone member states are using Euro as their currency. This is

beneficial for intra Europe trade, but there are total of 180 (approximate) different currencies

Byzantine governtment keeps a monopoly on currency exchnage

•4th Century AD

Medici family open Banks to exchange currencies

•15th Century

First Forex Market is maintained in Amsterdam

•18th Century

Foreign exchange was successfully completed by financial agents of England and Holland

•1704

Birth of modern foreign exchnage in the form of Gold standard

•1880

integration of Forex trrade in financial functioning of London

•1928

Start of Bretton Woods System

•1944

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 3

worldwide, many of which may expose a firm to exchange rate fluctuations. The single currency

has helped to eliminate the exchange rate fluctuation risk within the Euroland countries, but the

single currency is still vulnerable to the exchange rate fluctuations of the other major currencies,

such as the US Dollar, Pond Sterling, Yen and currencies of other major trading

partners(countries).

Exchange rate fluctuations have a substantial effect on firms. The fluctuation of foreign exchange

rates affects both the cash flow and discount rate and hence the value of the firm. We will try to

analyze the impact of exchange rate on the firm’s value by means of impact of foreign currency

exchange rate on the share price of the firm. Exposure represented the sensitivity of the value of

the firm to the exchange rate movements and can be measured by the regression coefficient of the

change in the value of firm on the change in exchange rate (Jorian, 1990).

Some of the most common factors which affect the value of a country’s currency are:

(Which in case of our study are factors faced by Euro Monitory Union combined and as guided by

ECB):

a. Current account deficit of the country.

b. Public debt of the country.

c. Political stability and economic performance.

d. Rate of inflation for the country

e. Interest rates

The exchange rate risk is a mixture of exposure to a currency and its volatility. As the firms may

experience considerable exposure to foreign exchange rate risk because of foreign currency based

activities and international competition. The volatility can be understood as the amount of

fluctuation in the value of currency due to market conditions (It is assumed the market has factored

in all factors impacting the exchange rate). Some of the most volatile currency pairs are US dollar

and Mexican peso, US dollar and Turkish lira (Fouquin et al., 2001).

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 4

As we see, firms may have exposure to many different currencies and the exchange rate

fluctuations of these currency can affect the firm’s cash flow and value. In order to minimize the

effect of exchange rate risk and safeguard itself from the currency fluctuations, firms use hedging.

Hedging is a financial instrument which reduces the risk of adverse price movements in an asset.

In more simple words hedge is an investment position used to reduce any substantial gain or losses

that can be gained or suffered by a firm.

Hedging can be seen like an insurance policy. While taking an insurance policy someone does not

know if the specific scenario will occur or not, but to protect the assets from the worst scenario, a

person takes the insurance policy and pays a certain premium for the same. There is an inherent

risk-reward tradeoff in hedging, while it reduces the potential risks, it also takes away any potential

gains that may occur. The method to reduce/eliminate a company’s foreign exchange risk resulting

from transactions in foreign currencies is called as foreign exchange hedge. Forward covers are

used widely as a hedging instrument for offsetting the currency exposure.

Different strategies can be used to hedge the foreign exchange risk, many financial instruments are

also used for hedging the foreign exchange risk. Hedge is a type of derivative or financial

instrument, that derives its value from the underlying asset. Some of the most common hedging

strategies are natural hedging, use of derivatives such as forward and options. It is important to

understand that, as there is an inherent risk-reward tradeoff in hedging and also there are certain

costs associated with the hedging. So, it is important for firms to find an optimum balance, where

in they need to also check the potential gains of hedging with the cost of hedging.

B. Research Objective

This paper addresses the key issues mentioned above. Firstly, we will find the effect of foreign

exchange exposure on firms listed in Dutch stock market by analyzing the effect of exchange rate

fluctuations on the stock returns of the firms. For this, we will use the 17 firms listed on Euronext,

AMX Index (Appendix - 1). These firms have assets in different countries and some of these firms

are also listed in different stock exchanges, which makes them exposed to exchange rate

fluctuations. When foreign currencies appreciate/depreciate, it affects the earnings of Dutch listed

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 5

firms. Adler and Dumas (1984) defined the exchange rate exposure as the extent to which the stock

market value of a firm varies with changes in exchange rates.

The Netherlands is one of the most open economies in the world. In 2016, the imports and exports

of the Netherlands were 69.9% and 80.8% of GDP, respectively. In comparison the imports and

exports of US were 15.4% and 12.5% of GCP. The other European Union power Germany was

even lagging behind the Netherlands, as imports and exports of Germany were 30.3% and 45.9%

of the GDP (World bank) respectively. This shows that the Dutch listed firms with operations in

multiple countries combined with the trade openness of the Netherlands will significantly make

firms more exposed to the exchange rate risk as compared to firms of other countries.

In the second part of this paper, we will test whether hedging helps in diminishing firm’s exchange

rate exposure. Hedging, by definition, is the strategy of minimizing or eliminating risk, mostly

using financial instruments. As we have discussed earlier hedging is like an insurance cover,

insuree/s pays a certain amount of premium to the insurer for cover provided by the insurer against

certain kind of risks. If the risk occurs, then the underwriter, which is the insurer, pays the

compensation towards the losses incurred by the insuree/s upto the limit covered in the policy. But

on the flip side if the risks don’t occur than the insuree/s ends up paying the premium, with no

return on the premium, this premium is the cost associated with the insurance.

The same is also true for the certain derivative products such as FX options. Currency option is an

agreement that provides its holder the right but not obligation to purchase or sell an amount of one

currency into another currency at pre-determined price at a specified time in the future. The holder

of option has to pay premium to the broker/firm/individual who executes orders of currency option

contracts on the behalf of holder. The advantage of FX option is that if the foreign currency

strengthens, the can still benefit fully from this move, as holder do not have the obligation to

exercise the option and will only loose the premium paid. Another derivative product regularly

used is the forward contract, wherein two parties or more enter into a contract with the intention

of exchanging one currency for another at an agreed upon rate and at a certain quantity on a

specified future date. It is a non-standardised contract. As the forward contract is a legally binding

contract, if the exchange rate moves against the holder’s interest, then the holder is not allowed to

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 6

gain from the profitable rate movement and holder may have to pay a relatively high cancellation

cost.

One of the main reasons for undertaking hedging is for shielding the revenue stream, balance sheet

and profitability of the company against adverse price movements (Allayannis & Ofek, 2001). For

the hedging strategy to be most effective, companies should get a clear picture of their risk profile,

their risk appetite and benefits from risk aversion by hedging. Hedging does not eliminate risks

but helps to transfer risks to someone who is well equipped to manage the risk or is ready to risk

in return for higher returns. A properly designed hedging strategy enables corporations to reduce

risks (Lewent & Kearney, 1990).

As we have discussed earlier, Firms may use different hedging tools to safeguard themselves from

different risks, we will discuss about the various hedging strategies and tools available for

protecting against currency fluctuations. Some of the tools and strategies used for currency

hedging are, hedging the cash flow by using natural hedge to offset their currency exposure, or by

use of forward contract to lock the future currency rate, such as in case of receivables. Apart from

these, there are other hedging tools available such as, futures, options and swaps.

As we have discussed, the firms may experience considerable exposure to foreign exchange rate

risk because of foreign currency based activities and international competition. Due to highly

volatile nature of the foreign exchange market, there is a considerable movement in the value of

different currencies which makes the firms exposed to exchange rate risk. In this paper we will

find the effect of foreign exchange exposure on firms listed in Dutch stock market by analyzing

the effect of exchange rate fluctuations on the stock return of the firm. We will also test whether

hedging actually diminishes the firm’s exposure.

This paper is organized as follows. Section II discussed the conceptual framework, which

encompasses different theories on Currency risk, hedging strategies and hedging instruments.

section III is the framework, where we discuss about the data and model used for analysis, we will

also show the empirical findings in this section. Section IV deals with the managerial implications

of the research followed by Section V and VI, conclusion and references respectively.

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 7

II. Conceptual Framework : Theory Review, Tools & Framework

A. Foreign Exchange Risk

Foreign exchange risk is the risk that affects financial performance or position of a firm by

fluctuations in the exchange rates between currencies. Currency risk is the mixture of exposure

and volatility of the currency.

There are different modes through which firms can be exposed to exchange rate risks. For instance,

a firm which exports its products, is susceptible to exchange rate risk, because when exchange rate

of the buyer country with respect to the domestic currency changes than this will affect the

receivable of the firm. Some firms can also import resources from abroad, in such a scenario the

change in exchange rate will affect the payables of the firm. In case of receivable appreciation of

domestic currency will reduce the receivable of the firm, where in case of payables, depreciation

of currency will increase the payable of the firm. Usually both the scenarios can substantially affect

the cash flow of the firm.

Another scenario is for a multinational firm, which are substantial assets and liabilities abroad.

Firms need to prepare a consolidated Financial statement for reporting purposes, in case of firms

with overseas assets and liabilities need to translate these or the foreign subsidiaries financial

statement needs to be changed to domestic currency and consolidate in firms financial statement.

This could greatly affect reported earnings and hence the stock price.

B. Type of Foreign Exchange Risk

The three main types of exchange rate risk are (Papaioannou, 2006):

1. Transaction risk – It is the cash flow risk and deals with the effect of exchange rate

exposure, related to receivables (export), payables (Import) or repatriation of

dividends. Change in exchange rate in the currency of denomination (which is usually

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 8

the foreign currency) of any such contract will result in a direct transaction exchange

rate risk to the firm.

An easy example would be a Dutch carpet showroom importing carpet from India. In

such a case there exists a transactional risk in the contract for example is the Euro/INR

exchange rate at the time of contract stands at INR 70 for € 1 and the Dutch importer

makes a contract for buying carpets worth € 10,000 in the month of December 2017.

The transaction risk is the uncertainty of the same Euro/INR rate as on the date of

contract. If the Euro/INR rate moves to INR 35 for every euro than the Dutch buyer

will end up paying twice the amount. This situation makes parties involved in the

international trade exposed to currency risk.

2. Translation risk – This risk is related to the valuation of foreign assets and liabilities

of a foreign subsidiary which in turn can affect the parent company’s balance sheet.

Translation risk for a foreign subsidiary is usually measured by the exposure of net

assets (assets less liabilities) to potential exchange rate moves. Translational risk is

also known as an accounting risk and it might not affect the cash flow of the firm, but

it can have significant impact on the firm’s reported earnings and value which can

impact the stock price.

An example of translational risk could be by looking at the consolidated financial

statement and balance sheet of Philips, Dutch multinational. Philips have many

subsidiaries all over the world, and after the end of each financial year, the corporate

head office of Philips global has to present a consolidated balance sheet, which will

have assets and liabilities of its global subsidiaries in a single currency. While reporting

the consolidated position Philips needs to convert assets of subsidiaries from local

currency to parent company’s currency. This gives rise to translation risk, as Philips

will witness foreign currency gains or losses when its assets, liabilities and financial

obligations are converted in currency of parent company.

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 9

3. Economic risk - it is the risk to the firm’s present value of future cash flows from

exchange rate movements. It is the effect of exchange rate fluctuations on revenues

(domestic sales and exports) and operating expenses (cost of domestic inputs and

imports). Economic risk is usually applied to the present value of future cash flow

operations of a firm’s parent company and foreign subsidiaries.

C. Factors Affecting Exchange Rate Fluctuations

There are a number of factors which can be attributed as factors which determine the volatility or

fluctuations in exchange rate. These factors range from economic indicators to international

factors.

Exchange rate system is a system in which one currency say Euro exchanges with other currencies

or indices denominated in foreign currency. With the collapse of Bretton Woods system and later

on the Smithonian Agreement and the formation of Euro, countries started to move towards free

floatation of their currencies. There are various factors affecting the currency exchange rate, these

are:

1. Inflation – Inflation plays an important role currency exchange rates. Lower inflation rates

in a country helps to appreciate the currency value of that country. For example if rate of

inflation in India is lower that other countries this will help India to increase its exports.

This will also help to increase the demand for rupees to buy Indian goods. As the increase

demand for Indian currency will appreciate the value of Rupee and the imports will become

cheaper. Therefore, lower inflation helps to appreciate the value of currency.

2. Interest Rate – it is important to know that interest rate, inflation and forex rates are highly

correlated. A country with interest rates higher that others will attract more foreign capital,

as foreign investors will get higher returns on their investments and this will cause the

exchange rate to rise.

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 10

3. Current Account Deficit – Current account is the balance of payment between country and

its trading partners. A current account deficit indicated that the country is spending more

on foreign trade than it is earning, in other words country is importing more than exporting

higher imports resulting in shortage of foreign currency. This excess demand of foreign

currency lowers the domestic currency of the country.

4. Public Debt – Countries spending on public sector projects and other social funds through

deficit financing becomes less attractive for foreign investors. As the such countries face

the problem of higher inflation. A important determinant in this sector is the debt rating

provided by rating agencies to the country. A country with lower rating has the risk of

defaulting, which will stop foreign investors to hold debt in that currency as the country

might default. Hence, rating provided to a countries debt is an important determinant of the

exchange rates.

5. Political Stability and Economic Performance – Countries with stable political government

and strong economic performance attracts foreign investors. As a stable government can

give strong economic performance through completion of projects and initiating new

developments projects.

As we have seen, there are different type of exchange risks to which a firm may be exposed, due

to its business activity and geographical distribution. We have also seen that there are many factors

which affect the currency exchange rate, it can be seen that these factors can substantially affect

the value of currency. In the next sections, we will discuss about the hedging strategies and tools

which can be used by the firms to protect themselves against currency risks.

D. Hedging

Hedging is a risk management technique which is used to reduce or eliminate losses due to adverse

movements. It is one of the most common methods that firms use to eliminate financial risks. There

are different kind of hedging strategies and tools which are used for mitigating various risks, such

as the operational risk, credit risks and other financial risk. This paper is focusing on currency

exchange risk, and how that affects the value of the firm. Hence, we will discuss about tools

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 11

available for hedging foreign exchange risk and test weather hedging helps to reduce the currency

risk.

Firms use different financial hedging products, such as future contracts, forward contract, options,

currency swaps and others, for minimizing the effect of currency risk. Currently there is an

availability of large number of hedging instruments, their variety and complexity has increased the

specific hedging needs of the modern firm (Hakala and Wystup, 2002; Jacque, 1996; Shapiro,

1996). Apart from regular hedging instruments, treasuries are developing efficient hedging

strategies as a more integrated approach to hedge currency risk than using normal forward covers

to hedge certain foreign exchange exposure (Kritzman, 1993). From the perspective of corporate

manager, currency risk management is viewed as a sensible approach to reduce vulnerabilities of

a firm from major exchange rate movements (Van Deventer, Imai, and Mesler, 2004).

Previous studies (Allen, 2003 & Jacque,1996) have found that firms with significant exchange rate

exposure often need to establish an operational framework of best practices. They further

recommended that these strategy should revolve around 5 points namely –

1. Identification and measurement of exchange rate risk – Firms need to identify the

type/s of currency risk it is exposed to, such as transaction, translational and

economic risk and also specific currencies to which they are exposed. In addition,

they need to measure these currency risks, this can be accomplished by using

models, such as the VaR (Value at Risk).

2. Development of exchange rate risk management strategy – Firm need to develop a

strategy for dealing with the currency risk. This strategy should be able to answer

some basic questions, such as if the firm need to fully or partially hedge the

currency exposure, what are the different instruments that firm needs to use under

specific cases and how the firm will monitor the hedge positions.

3. Creation of a centralized team - To deal with the practical aspects of currency risk

hedging execution, a centralized entity should be created in the firm’s treasury. The

entity will be responsible for mechanism of hedging, cost of hedging, accounting

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 12

procedure for hedging, forecasting of exchange rates, establishing benchmark for

currency hedging performance management and other tasks related to hedging.

4. Developing monitoring mechanism - Firm’s needs to develop a set of controls for

monitoring the currency risk in the firm. This should include position limits for

each hedging instrument should be set, for periodic monitoring of hedging

performance benchmarks should be established.

5. Establishing risk oversight committee – This committee would review risk

management policy on regular basis. They will approve limits on position taking

and check the appropriateness of hedging instruments.

E. Hedging Instruments

In this section we will discuss about the various hedging instruments which are available for a firm

to hedge their currency risks. Currency hedging is defined as protecting a firm against movement

of exchange rate in the direction opposite to their position in the market by taking an offsetting

position in that currency.

There is an availability of large number of complex hedging instruments. These include both OTC

(Over the counter) and exchange traded products. In this paper we discuss about the four widely

used hedging instruments. Currency forward and cross currency swaps are OTC hedging

instruments whereas currency futures and currency options are exchange traded hedging

instruments.

a. Currency Forwards

It is a contract between two or more parties to buy or to sell certain amount of currency (asset) at

an agreed upon price on a specific future date.

As forward contract is an non-standardized contract, this makes it highly customised which makes

it apt for hedging. The contract can be customized according to the needs of parties and they can

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 13

decide on delivery date, quantity and price. Many firms use forward contract to hedge their

currency risk. As forwards traded over the counter and not in exchange, they possess a high degree

of default risk.

b. Currency Futures

It is a contract to exchange one currency for another at an pre-determined price (exchange rate) on

a specified future date.

Future contracts are an standardized exchange traded contracts and can be seen as an upgradation

of forward contracts, designed to solve problems encountered in forwards. Future contracts have

a number of standardized features such as maturity date, contract size, quoting convention (i.e:

EUR/USD), price limit (i.e. daily maximum price fluctuation ) and position limits (number of

contracts a party is allowed to buy or sell). The delivery price on future contract is determined on

an exchange as it primarily relies on the market demands.

Another change from the forward contract is the deposit of security amount in futures. There is no

need to deposit cash in a forward contract, whereas in future, traders are required to open a futures

account, where both (buyer and seller) need to make a security deposit, this provides guarantee

that the traders will fulfill their contractual obligations.

c. Currency Options

It is an agreement that provides the holder the right but not the obligation to exchange one currency

into another currency at a pre-agreed rate on a specified date in the future.

As the option holder has the right but not the obligation to exercise the contract, the holder has to

pay a premium for this right to choose. Options trading is not and is not heavily regulated and they

are traded in exchanges such as International Securities Exchange . Premium is regarded as the

upfront cost which the holder is required to pay upfront to gain the possession of option, regardless

of whether option will be exercised or not.

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 14

Depending on buying or selling of currency option can be classifies into call option and put option.

Call option gives holder the right to buy specific quantity of currency at a fixed date and price,

whereas put option give holder right to sell an specific quantity of currency at a fixed date and

time.

d. Currency Swaps

It is also known as cross currency swap. It is an agreement between two parties to exchange interest

payments and sometime principal denominated in one currency into another currency at an agreed

upon exchange rate for a specific period of time.

Apart from helping in hedge against forward exchange rate fluctuations currency swaps may help

to secure cheaper debt, as the company can borrow at the best available rate regardless of currency

and then swapping for debt in desired currency.

One of the major drawback of swap is default and creditworthiness risk of the counterparty. If one

party fails to meet the financial obligation on maturity date than the other party may also face

situation of default on principal payment along with interest.

As we have discussed earlier, there are many different factors which affect the foreign exchange

rates. In the last two decades the world has seen many currency crisis such as economic crisis in

Mexico (1994), Asian Financial Crisis (1997), Russian financial crisis (1998) and the Argentine

economic crisis (1999-2002). Apart from these there are many different events which affected the

currency rates. The 2008 European debt crisis, wherein countries had to be bailed out of debt, this

lead to recession and economic instability. The Euro and other European currencies fluctuated

during the crisis. More recently following the Brexit, GBP depreciated by 10% in value. We can

see there are many events which influence the currency rates and the fluctuations can substantially

effect the firm’s cash flow and firm value. In order safeguard gains adverse price movements, it is

important for firms to hedge their currency positions.

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 15

F. Literature Review

Various studies have shown that the effect of Foreign exchange risk on a firm’s stock price depend

on a variety of firm characteristics. A sample of 287 U.S. multinationals was analyzed by Jorion

(1990) and found that the ratio of foreign sales is a significant determinant of a firm’s exchange

rate exposure and the ratio of foreign sales and total sales is positively related with depreciation of

the US dollar. Adler and Dumas (1984) define exchange rate exposure as the effect of exchange

rate changes on the value of a firm.

By analyzing a sample of automotive firms from the United States and Japan, it is reported that

foreign sales increased the exposure to currency risk whereas foreign operations reduced the

exposure (Williamson, 2001). He also found that industry competition and the structure of the

firm's operations play vital roles in the exchange rate exposure to firm-value relation. For instance,

if a firms exports its product to an overseas market and does not directly compete with the firms

in that market, than exposure of the firm is simply a function of its foreign currency revenues. If

the foreign firm faces competition in the local market, than the exposure is a function of its foreign

currency revenues and also to the elasticity of its own and its competitor's product (Williamson,

2001). It is also reported that domestic competition from foreign firms is an important determinant

of exposure. The results of the research have shown the U.S automotive firms have significant

exposure to the Japanese yen, which the home country currency of their major competitors. As the

sales in Japan is low for U.S firms, the source of exposure should be from the Japanese firm's U.S

sales and not from U.S. firm's sales in Japan.

It is reported that exposure can cause revenue of MNC’s to increase (decrease) when foreign

currencies appreciate (depreciate) because goods and services produces domestically become

relatively less (more) expensive. Alternatively, appreciation (depreciation) in the foreign

currencies could lead to increased (decreased) cost due to exposure because the foreign-sourced

inputs and foreign-denominated debt become relatively more (less) expensive (Martin Madura,

Akhigbe, 1990).

Some studies of foreign exchange rate exposure are done in some specific industry sector.

Allayannis (1996) studies he effect of exchange rate exposure in U.S manufacturing industries and

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 16

found that the exposure has to do with the level of export and import. The study also found a

relationship between exchange rates and time. In this study, the stock return is used as a proxy for

a firm’s value and a strong evidence was found that the industry exchange rate exposure varies

over time in a systematic way with the share of imports and exports in the industry.

Study was conducted about the exposure of exchange rate changes of large firms in UK, France

and Germany in the pre-Euro setting. The exchange rate sensitivity was found to be considerably

strong. For the firms of all three countries, firms gain value when local currency depreciates against

the US dollar (William & Sanjay, 2005).

Euro was adopted in 1995 and introduced as an accounting currency in 1999. This eliminated

exchange rate variability between some member Eurozone countries. The physical Euro currency

(bank notes and coins) entered into circulation in 2001 and by May, 2002, Euro had completely

replaced former currencies. Currently 19 out of the 28 euro member states are using Euro. Bartram

and Karolyi (2006) studied the effect of the introduction of the Euro as a common currency which

affected 3220 corporations in 20 countries around the world. They found that a common currency

leads to lower foreign exchange rate risk and, thus, lower foreign exchange rate exposures of

nonfinancial firms.

Jong et al (2006) studies about foreign exchange rate exposure of Dutch MNC’s (non-financial

firms)finds that over a period 1994-1998, over 50 percent of a sample of Dutch firms are

significantly exposed to foreign exchange risk. They also found that firms with significant

exposure benefit from a depreciation of the Dutch guilder relative to a trade-weighted currency

index and that the firm size and the foreign sales ratio are significantly and positively related to

exchange rate exposure.

Some studies such as by Jorion (1990) found only a small number of firms with significant

exchange rate exposure. As a consequence, somewhat surprisingly, researchers concluded that, the

effect of exchange rate changes on firms value is economically and statistically small (Griffin and

Stulz, 2001).

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 17

Two models which are used by prior researchers for measuring exchange rate exposure are

discussed by Bodnar and Wong (2003). In the first model, the coefficient on the exchange rate

variable in a linear regression between the return on stock of the firm and the change (percentage)

in an exchange rate (home currency price of foreign currency) variable gives the exposure

elasticity. In the second model return to the market portfolio is added with the exchange rate

variable to control for the common “macroeconomic” influences on “total” exposure elasticities.

The market portfolio return improves the precision of the exposure estimates by reducing the

residual variance of the model, hence, it is a commonly estimated exposure model.

Study (Doidge, Griffin & Williamson, 2006) assessed the economic magnitude of exchange rate

exposure by using a new approach, known as portfolio approach to measure the economic

importance of exposure. According to this model, the wealth is allocated among alternative assets

including domestic money, domestic bonds and equities and foreign securities (Phylaktis,

Ravazzolo, 2005). Their result shows that the exchange rates play an important role in explaining

stock returns. Bodnar and Wong (2002) show that the different constructions of a market portfolio

have different exposures to exchange rates due to a significant size effect in exchange rate

exposures. They claim a significant inverse relation between firm size and exchange rate exposure.

Many research paper encounter methodological shortcoming in the research. Alayannis & ofek

(2001) compare financial hedging versus operational hedging. They used several alternative

measures of geographical distribution of subsidiary companies as a proxy for the level of

operational hedging of a firm. They found that the dispersion of subsidiaries across multiple

countries does not reduce exchange-rate exposure. Bodnar and Marston (2000) find that foreign

exchange exposure is low for the majority of 103 US firms surveyed, because these firms make

effective use of operational hedging (matching foreign currency receivable and payables). The

conclusion of Bodnar is in direct conflict with the conclusion of Alayannis. The biased result of

Bodnar may be because, only those firms that do have a good track record with respect to exchange

rate exposure participate in the survey, this is a shortcoming of the survey method.

He and Ng (1998) conducted research on 171 Japanese companies to investigate the incentives of

hedging. They found that firms with high financial leverage or firms with weak short-term liquidity

positions have more incentive to hedge and have smaller exchange rate exposures. “Within the

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 18

framework of hedging the exchange rate risk in a consolidated balance sheet, the issue of hedging

a firm’s debt profile is also of paramount importance”, (Marrison, 2002; Jorion and Khoury, 1996).

Allayannis and Ofek (2001) examine whether firms use foreign currency derivatives for hedging

or for speculative purpose by using a sample of S&P 500 nonfinancial firms for 1993. They find

evidence that firms use currency derivatives for hedging to significantly reduce the exchange rate

exposure. They also find that the decision to use currency derivatives depends on exposure factors

such as foreign sales and variables largely associated with theories of optimal hedging such as

R&D expenditures; the level of derivatives used depends only on a firm’s exposure through foreign

sales.

Sarah et al (1998) examines currency exchange risk to financial institutions which are doing

business internationally. The research concluded that financial institutions are increasingly facing

foreign currency exposure and recommending hedging and financial strategies. Papaioannou

(2006), discusses about various risk management tools for calculation of currency risk and also

discusses the general hedging strategies for translational, transactional and economic risks. Further

various hedging instruments such as forward, future, options and swaps are discussed.

Papaioannou(2006) also finds that, based on the reported U.S. data, it is observed that the larger

the size of a firm the more likely it is to use derivative instruments in hedging its exchange rate

risk exposure; the primary goal of U.S. firms’ exchange rate risk hedging operations is to minimize

the variability in their cash flow and earning accounts.

III. Framework

The paper consists of two parts. Firstly, we will find the relationship between change in foreign

exchange rate and return on stocks. Secondly, we will check if the hedging helps to minimize the

effect of exchange rate fluctuations.

The first part will be analyzed using the regression test, to find the relationship between exchange

rate and return on stock value. The sample for our research contains 17 firms listed in Euronext,

AMX Index. All of these firms have operations in different geographical locations, and they deal

in different currencies which makes them exposed to currency risk.

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 19

The study covers a period of 10 years (2006-2016). The time period have seen some global events

taking place, causing a substantial fluctuations in the different exchange rates. In the second part

the relationship between ratio of foreign currency derivate and total assets in a firm will be checked

with the exchange rate exposure. The length of the return measurement horizon, is taken to be one

month (Bodnar and Wong, 2003). They also state that “exchange rate exposure estimates are more

statistically significant at longer horizons. However, lengthening the horizon beyond one month

does not reduce the model sensitivity of the exposure estimates arising from the relation between

exposure and firm size”.

A. Exchange rate fluctuations and stock returns

Floating rate has bought unanticipated exchange rate movements in the international business

environment. It is also known that these unanticipated movements in currency value create risks

for multinational companies, forcing company managers to take actions to prevent or avoid the

risk. The value of Firms operating in multiple countries are affected by the changing exchange

rates. When foreign currencies appreciate, the sales and earnings of operations in those currencies

translate into more parent currencies, thus, increasing consolidated sales and earnings. Dumas

(1978), Adler and Dumas (1984) and Hodder (1982) defined the exchange rate exposure as the

extent to which the stock-market value of a firm varies with changes in exchange rates.

The exchange rate exposure of a firm is the way in which value of the company changes, as real

value of local currency changes. The currency exposure of a firm can be calculated by regressing

the firm’s stock return with the change in local currencies value. In accordance with He and NG

(1997), the following regression model will be used to measure the exposure. The model was used

in earlier researches by Adler and Dumas (1984), Jorion (1990), Allayannis (1996)

Rit = β0 + βix Rxt + βim Rmt + εit ……………………………………………………… (1)

Rit is the return on the ith corporation’s stock, β0 is the intercept, Rxt is the return on nominal

effective weighted exchange rate index and Rmt is the return on a market portfolio in time t. βix

measures the exchange rate exposure. εit is the error term.

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 20

As a sample we initially started with 17 firms listed on Euronext, AMX Index. Out of the 25 firms,

we took 17 firms(Table 1, Appendix) for our research, as there was non-availability of data for the

other 8 firms. The firms not included in the research were newly inducted in the AMX index, hence

we were unable to gather data for the complete duration of 10 years for these firm (2006-2016).

The monthly return on exchange rate is calculated using nominal effective exchange rates of the

euro as calculated by the European Central Bank (ECB). The nominal effective exchange rate is a

weighted average of nominal bilateral rates between the euro and a basket of foreign currencies

(19 trading partners).

As is the common practise in studies of exchange rate exposure, we use return on market index as

a proxy which helps to reduce noise. The index selected is, AMX index of Euronext, which was

started in 1995. It is a midcap market index and encompasses 25 Dutch companies which are

traded on Euronext. It is a free float market capitalization weighted index, with total market

capitalization of €58.10 billion. We calculate returns on monthly basis. For the monthly data we

use data on the 15th day of every month, taking January, 2006 as a base year. In case 15th day of

the month is a holiday, than we selected the next working day for calculations of returns.

Exhibit 2 – Return on market portfolio and change of nominal exchange rate

-0.6000

-0.4000

-0.2000

0.0000

0.2000

0.4000

0.6000

16

/01

/20

06

15

/06

/20

06

15

/11

/20

06

16

/04

/20

07

17

/09

/20

07

15

/02

/20

08

15

/07

/20

08

17

/12

/20

08

15

/05

/20

09

15

/10

/20

09

15

/03

/20

10

16

/08

/20

10

17

/01

/20

11

15

/06

/20

11

15

/11

/20

11

16

/04

/20

12

17

/09

/20

12

15

/02

/20

13

15

/07

/20

13

16

/12

/20

13

15

/05

/20

14

15

/10

/20

14

16

/03

/20

15

17

/08

/20

15

15

/01

/20

16

15

/06

/20

16

15

/11

/20

16

Chart Title

Rate of return on market portfolio (Rmt) rate of change of exchange rate(Rxt)

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 21

Exhibit 2 shows the variation of return on market portfolio and change of exchange rate over a

period of 10 years (2006 – 2016), which is also the duration of our research. It can be seen that

there is a relationship between the two. The two independent variable seem to be correlated. The

coefficient is calculated to be -0,38, implying that return on market portfolio and return on

exchange rate have a moderate negative linear relationship. There was no significant

multicollinearity found in the model.

B. Currency Derivative and Exchange Rate Exposure

In this part we will examine the impact of firms use of currency derivatives and its exchange rate

exposure. The exchange rate exposure of a firm is determined by its financial hedging. Therefore,

we use the following equation

βix = α + ϒi (FCD/TA) ……………………………………………………………(2)

βix is the firms exchange rate exposure as measure in (1), FCD/TA is the ratio of nominal value of

foreign currency derivatives to the total assets of the firm, ϒi measures the effectiveness of

hedging against currency exposure. Here βix is the coefficient of currency exposure that we will

find from equation (1), and use liner regression to find the coefficient of currency derivative ϒi

i.e. (FCT/TA)

C. Empirical Findings

Exchange rate fluctuations and stock returns

We estimate equation (1), for each firm in our sample using liner regression. Table 1 represents

the regression of changes in the ECB’s nominal effective weighted exchange rate and returns on

stock at 0.05 level.

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 22

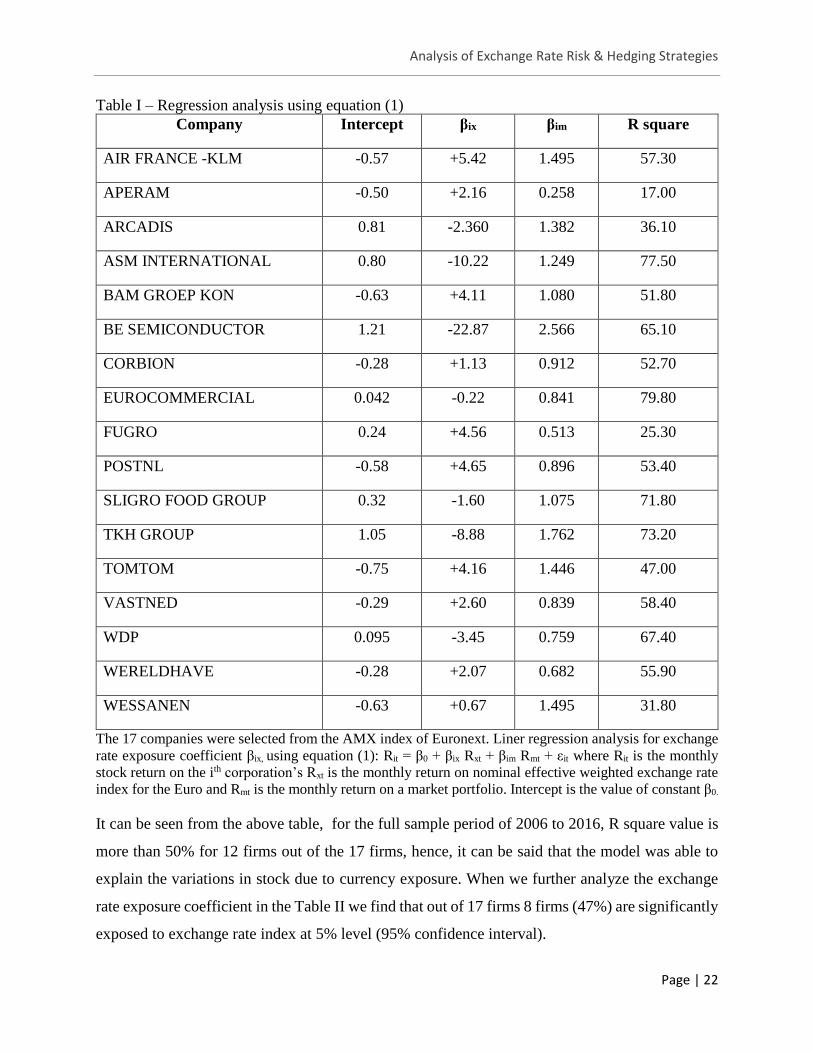

Table I – Regression analysis using equation (1)

Company Intercept βix βim R square

AIR FRANCE -KLM -0.57 +5.42 1.495 57.30

APERAM -0.50 +2.16 0.258 17.00

ARCADIS 0.81 -2.360 1.382 36.10

ASM INTERNATIONAL 0.80 -10.22 1.249 77.50

BAM GROEP KON -0.63 +4.11 1.080 51.80

BE SEMICONDUCTOR 1.21 -22.87 2.566 65.10

CORBION -0.28 +1.13 0.912 52.70

EUROCOMMERCIAL 0.042 -0.22 0.841 79.80

FUGRO 0.24 +4.56 0.513 25.30

POSTNL -0.58 +4.65 0.896 53.40

SLIGRO FOOD GROUP 0.32 -1.60 1.075 71.80

TKH GROUP 1.05 -8.88 1.762 73.20

TOMTOM -0.75 +4.16 1.446 47.00

VASTNED -0.29 +2.60 0.839 58.40

WDP 0.095 -3.45 0.759 67.40

WERELDHAVE -0.28 +2.07 0.682 55.90

WESSANEN -0.63 +0.67 1.495 31.80

The 17 companies were selected from the AMX index of Euronext. Liner regression analysis for exchange

rate exposure coefficient βix, using equation (1): Rit = β0 + βix Rxt + βim Rmt + εit where Rit is the monthly

stock return on the ith corporation’s Rxt is the monthly return on nominal effective weighted exchange rate

index for the Euro and Rmt is the monthly return on a market portfolio. Intercept is the value of constant β0.

It can be seen from the above table, for the full sample period of 2006 to 2016, R square value is

more than 50% for 12 firms out of the 17 firms, hence, it can be said that the model was able to

explain the variations in stock due to currency exposure. When we further analyze the exchange

rate exposure coefficient in the Table II we find that out of 17 firms 8 firms (47%) are significantly

exposed to exchange rate index at 5% level (95% confidence interval).

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 23

Table II. Descriptive Statistics of Exchange Rate Exposure Coefficient

Statistic

Beta Minimum -22.8660

First quartile -2.360

Median 1.130

Third quartile 4.108

Maximum 5.419

Mean -1.063

Standard deviation 7.203

Firms with significant exposure at 95%

confidence interval 7 ( 41%)

Firms with significant positive exposure

at 95% confidence interval 4 (24%)

Firms with significant negative exposure

at 95% confidence interval 3 (18%)

Liner regression analysis for exchange rate exposure coefficient βix, using equation (1): Rit = β0 + βix Rxt +

βim Rmt + εit where Rit is the monthly stock return on the ith corporation’s stock, α is the intercept, Rxt is the

monthly return on nominal effective weighted exchange rate index for the Euro and Rmt is the monthly

return on a market portfolio of the market capitalized weighted AMX index of Dutch stock market in time

t. βix measures the exchange rate exposure. εit is the error term.

There are 4 firms with significant positive value of exchange rate coefficient (βix). On the other

hand there are 3 (18%) firms with significant negative exchange rate coefficient. Overall 41% of

the Dutch listed firms are exposed to exchange rate exposure. This results are similar to previous

study conducted by Jong et al (2006), they found more than 50% of the Dutch firms exposed to

currency exposure for Dutch guilder. But our results, to an extent also support the results of

Bartram and Karolyi (2006) who study the introduction of Euro on exchange rate risk exposure.

They found that common currency leads to lower foreign exchange rate risk and, thus, lower

foreign exchange rate exposures of firms. Jong et al (2006) found more than 50% of the Dutch

firms exposed to currency exposure whereas in our research it has decreased 41%.

The mean of exposure coefficient is -1.063, the negative is due to a presence of an outlier. After

removing the outlier, if we check again, we find the mean value of exposure coefficient to be 0.30,

showing that if Euro depreciates with 1 percent average Dutch firms of the sample gain 0.30 per

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 24

cent. The positive value of currency exposure coefficient suggest that depreciation of Euro against

basket of currency has a positive impact on the stock returns of the Dutch firms. The negative

value of coefficient implies that depreciation of Euro has a negative impact on the value of firms.

There are 4 (24%) firms with significant positive exposure coefficient, ranging from 0.67 to 2.60.

These firms are exporters, a possible explanation can be that these firms have assets in foreign

currency and when the Euro depreciates, it cases positive impact on their consolidated books.

These firms can also be very big firms, and they can be net exporter of goods or services. The

results show that almost 41% of the firms in sample are exposed to currency exposure, which is

more than other researches.

Currency Derivative and Exchange Rate Exposure

We use equation (2), to find the potential impact of a firm’s currency derivative use on its

exchange-rate exposure. We calculated the coefficient of currency exposure by equation (1).

Foreign currency derivate is the nominal value of Forward contracts and options which companies

use to hedge their risk. Total assets and nominal value of currency derivatives can be found in the

financial statement of the firm for the year 2012.

Table III – Descriptive statistics

βix

FCD

Total

Assets

FCD/TA

Beta Minimum -22.8660 0.00 689 0.00

First quartile -2.360 11.72 1638 0.53

Median 1.130 64 2182 2,80

Third quartile 4.108 170 3749 4.72

Maximum 5.419 6934 22932 30.24

Mean -1.063 540 3879 5.22

Standard deviation 7.203 1770.47 5413 7.97

Linear regression for coefficient of currency derivative ϒi using equation (2): βix = α + ϒi (FCD/TA) βix is

the firms exchange rate exposure as measured in (1), (FCD/TA) is the ratio of nominal value of foreign

currency derivatives to the total assets of the firm, ϒi measures the effectiveness of hedging against

currency exposure.

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 25

Table III, see the statistical analysis of dependent and independent variable of equation (2). On

performing the regression analysis we find that coefficient of foreign currency derivatives is +0.39,

implying that ϒi is positively related to exchange rate exposure (βix ).

As shown by Allayannis and Ofek (2001), If firms use foreign currency derivatives to hedge

against currency fluctuation, then use of derivatives should reduce the currency exposure. We can

also say that the use of derivatives should decrease exchange-rate exposure for firms with positive

exposures and increase (decrease in absolute value) exchange-rate exposure for firms with negative

exposures. Therefore, the absolute values of derivatives used should be negatively related to the

absolute values currency exposure (βix ). A positive relation between the absolute values of

derivatives used and the absolute values currency exposure (βix), implies, that firms are using

derivatives to speculate in the foreign exchange market.

We have a positive relationship between the absolute value of currency exposure and absolute

value of the percentage use of foreign currency derivative. This implies that the Dutch listed firms

use currency derivative products for the purpose of speculating in the foreign exchange market.

this statement is not consistent with our sample, as all the companies in the sample are non-

financial firms. Other factors which may have biased our results and influenced the value of ϒi,

can be due to the small size of our sample, another important factor is that we only tool foreign

currency forward/futures and options as foreign currency derivative and excluded the swaps.

IV. Managerial Implications

Exchange rate fluctuations and stock returns

Currency risk arises from a combination of currency exposure and currency volatility. Firms may

experience considerable exposure to foreign exchange rate risk because of foreign currency based

activities and international competition. The exchange rate fluctuation has a substantial effect on

firms. The fluctuation of foreign exchange rates affects both the cash flow and discount rate and

hence the value of the firm.

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 26

The adoption of Euro in 1999, eliminated exchange rate variability between major trading

countries in the Eurozone. Netherlands being a part of Europe is using euro since, 2002. Currently

19 out of the 28 euro member states are using Euro. This is beneficial for intra Europe trade, but

there are a total of approx. 180 different currencies worldwide, many of which may expose a firm

to exchange rate fluctuations. We found that 41% of the of the 17 firms listed on the Dutch stock

market are exposed to exchange rate fluctuations.

Firms with open economies exhibit more exposure to exchange rate as compare to closed/partially

closed economies. As most of the previous studies such as by Jorion (1990) and Choi and Prasad

(1995) studied on US firms. These results of these studies a low number of firms which are exposed

to currency fluctuation. Netherlands being a more open, show a large number of firms which are

exposed to currency fluctuation.

Currency fluctuations is like a two sided sword, it can be beneficial for a firm and may give

favorable outcomes, but on the flip side, it can also have very unfavorable effects on the firm. One

of the currency which lately saw high volatility is the British Pound (GBP). Post the Brexit

referendum, GBP depreciated more than 10% in value. Any Dutch firm having assets in Britain

would had suffered badly because of the depreciation of GBP. Firms exporting products to Britain,

would receive less Euros, as Euro would have appreciated, whereas it is beneficial for importers.

As suggested by Jong et al (2006), 24 out of 47 firms (more than 50%) had a positive exposure

coefficient, implying, Dutch firms are net exporters. We found that 24% of the firms have

significant positive exposure coefficient. Hence, If these firms were exporting to Britain, or have

assets, then they would have had a significant effect on the value of firm.

Earlier we had discussed about various types of currency exchange risk that a firm might have to

face, such as the transaction risk, translation risk and economic risk. The most common source of

these risks is explained in Exhibit 3.

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 27

Exhibit 3

Source: Export Development Canada

It can be clearly seen that in case of a trading or manufacturing firm, risk arises at the time of order

initiation itself and then on different phases of different types of risk arise.As we have discussed

how currency risk can have substantial effect on the value of the firm. In line with previous

researches, we also collaborated that the Dutch firms are more exposed to currency exposure.

Considering all the things, it is important for the corporate managers, to develop a strategy and if

required hedging instruments, in-order to tackle the issue to currency exposure risk.

Exhibit 4 – Currency risk management approach

Source: Export Development Canada

Firms usually use hedging instrument to reduce the effects of currency rate fluctuations. These

instruments takes away the possible losses that the firm might incur due to currency exposure, but

hedging also takes away the possible gains, which a firm might get due to favorable movement of

currency rates. Van Deventer, Imai, and Mesler (2004) suggested currency risk management, as a

sensible approach to reduce vulnerabilities of a firm from major exchange rate movements. These

approach are better suited because they form the basis of currency risk management policy of the

firm. A proposed currency risk management approach is represented by Exhibit 3. It is self-

explanatory, it is similar to operational framework of best practices for firms with significant

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 28

exchange rate exposure(Allen, 2003 and Jacque’s,1996). The framework works as a currency risk

management policy. Exhibit 4 represents the framework.

Exhibit 4- Operational framework of best practices

Lewent and Kearney (1990) in their paper also considered an alternative approach to the financial

hedging. This approach involves the following 5 steps:

1. Exchange Forecast – The firm needs to project the exchange rate volatility and needs to

understand the factors which guide the exchange rate movements, such as the economic

indicators, target area of government policies and other forecasters. Firm needs to develop

a model incorporating different factors, to forecast the exchange rate volatility.

2. Strategic Plan Impact – Firm needs to access the impact of adverse exchange rate

fluctuations on its long term plan. Firm can compare their cash flow and earnings projects

with the expected and adverse price movements.

Identification/review and measurement of

currency risk

Developing/updating risk management

strategy

Creating a core teamDeveloping/updating

monitoring and controling mechanism

Risk Oversight committee

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 29

3. Hedging Rationale – the firm needs to decide if it needs to hedge the currency volatility or

not and to which extend they want to hedge the currency risk. Many companies, if not sure

about the currency movement, do not completely hedge their currency exposure, as it may

take away the possible gains due to favorable price movements.

4. Financial instrument – The firm needs to select the suitable instruments for hedging the

risk. Forward contracts, foreign currency debt, and currency swaps all effectively fix the

value of the amount hedged regardless of currency movements. Whereas options, retains

the opportunity to benefit from natural position, although at a cost equal to the premium

paid for the option.

5. Hedging Program – This will involve taking decisions about hedging such as analysing

every year the position of hedge and find the optimum instruments, the amount which needs

to be hedges, varying the strike price of options for reducing the hedging costs.

V. Conclusion

The relationship between exchange rate changes and stock returns for a sample of 17 Dutch firms

was examined over a period of 10 years (2006-2016). It was found that 41% of 17 firms are

significantly exposed to exchange rate risk. 24% of firms have significant positive exposure and

18% have significant negative exposure. Firms with positive exposure benefit from the

depreciation of Euro. We also tested if hedging helps to diminish firms currency exposure. No

significant effect on currency exposure was observed by the use of foreign currency derivative.

One of the possible may be because we used single factor usage of foreign currency derivative

has no significant effect on the exposure.

This study uses trade weighted exchange rate index by European central bank. The weights in trade

weighted index is derived from trade figures with foreign countries and when we use such a index,

it is assumed that individual firms will also be having similar characteristics. To find the effect of

foreign currency derivative on the exposure, we used nominal value of Forward contracts and

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 30

options as currency derivative. A possible source of bias can that the firms also use foreign debt

as a way to hedge their currency exposure.

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 31

VI. References

• J Hasebroek. 1933. Trade and Politics in Ancient Greece. Biblo & Tannen Publishers,

page 155-157.

• RC Smith, I Walter & G DeLong. 1999. Global Banking. Oxford University Press, 3.

• R.A. De Roover. 1999. The Rise and Decline of the Medici Bank: 1397-1494. Beard

Books, page -130.

• Shapiro, A.C, 1996. Multinational Financial Management, 5th ed.. Wiley, New Jersey.

• Van Deventer, D.R., K. Imai, & M. Mesler, 2004. Advanced Financial Risk

Management: Tools and Techniques for Integrated Credit Risk and Interest Rate Risk

Management. Wiley, New Jersey.

• Fouquin, M., K. Sekkat, J. Malek Mansour, Nanno Mulder & Laurence Nayman. 2001.

Sector Sensitivity to Exchange Rate Fluctuations. CEPII, Document de travail n° 01-11.

• Bodnar, G.M. & F. Wong. 2003. Estimating Exchange Rate Exposures: Issues in Model

Structure. Financial Management, 32(1): 35–67.

• Michael Papaioannou. 2006. Exchange Rate Risk Measurement and Management: Issues

and Approaches for Firms. International Monetary Fund.

• Jorion, P. 1990. The Exchange-Rate Exposure of US Multinationals. Journal of

Business, 63(3): 331–345.

• Adler, M. & B. Dumas. 1984. Exposure to Currency Risk: Definition and Measurement.

Financial Management, 13: 41–50.

• Allayanis, G. & E. Ofek. 2001. Exchange Rate Exposure, Hedging, and the Use of

Foreign Currency Derivatives. Journal of International Money and Finance, 20: 273–

296.

• Judy C. Lewent and A. John Kearney. 1990. Identifying, Measuring, and Hedging

Currency Risk at Merck, Journal of Applied Corporate Finance, 2.4: 19-28.

• Hakala, J. & U. Wystup. 2002, Foreign Exchange Risk: Models, Instruments, and

Strategies. Risk Publications.

• Kritzman, M., 1993. The Optimal Currency Hedging Policy with Biased Forward Rates.

Journal of Portfolio Management, 19 (4): 94–10.

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 32

• Allen, S.L.. 2003. Financial Risk Management: A Practitioner’s Guide to Managing

Market and Credit Risk, Wiley, New Jersey.

• Jacque, L., 1996, Management and Control of Foreign Exchange Risk, Kluwer Academic

Publishers, Massachusetts.

• Williamson R. 2001. Exchange rate exposure and competition: evidence from the

automotive industry, Journal of Financial Economics, 59: 441-475.

• Martin, J. Madura, A. Akhigbe. 1999. Economic Exchange Rate Exposure of U.S.-Based

MNCs Operating in Europe. The Financial Review, 3: 21-36.

• Allayannis, G. 1996. The time-variation of the exchange rate exposure: an industry

analysis. Unpublished Working Paper, New York University, NY.

• William R, Sanjay U. 2005. Exchange rate exposure among European firms: evidence

from France, Germany and the UK. Accounting and Finance, 45: 479–497.

• Bartram S.M & Karolyi G.A. 2006. The impact of the introduction of the Euro on foreign

exchange rate risk exposures. Journal of Empirical Finance, 13: 519–549.

• Griffin, J.M., Stulz, R.M., 2001. International competition and exchange rate shocks: a

crosscountry industry analysis of stock returns. Review of Financial Studies, 14(1): 215–

241.

• Doidge, C. Griffin, J and Williamson. 2006. Measuring the economic importance of

exchange rate exposure, Journal of Empirical Finance, 13: 550-576.

• Phylaktis,K and Ravazzolo. 2005. Stock Prices and exchange rate dynamics. Journal of

International Money and Finance, 24: 1031-105.

• Jia He and Lilian K. Ng. 1998. The Foreign Exchange Exposure of Japanese

Multinational Corporations. The Journal of Finance. 53(2): 733-753.

• Jorion, P., and S.J. Khoury. 1996. Financial Risk Management: Domestic and

International Dimensions, Blackwell Publishers, Massachusetts.

• Sarah K & Spiros H. 1998. Multi-currency options and Financial institutions’ hedging,

office

• of thrift Supervision-USA and University of Cyprus. International Atlantic Economic

Conference.

• Dumas and Bernard. 1978. The theory of the trading firm revisited, Journal of Finance

33: 1019– 1029.

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 33

• Hodder, J. 1982. Exposure to exchange rate movements, Journal of International

Economics,13: 375–386.

• De Jong A, Ligterrink J. and Macrae, V. 2006. A Firm –Specific Analysis of the

Exchange-Rate Exposure of Dutch Firms, Journal of International Financial

Management and Accounting, 17:1.

• Choi, J.J. & A.M. Prasad. 1995. Exchange Risk Sensitivity and its Determinants: A Firm

and Industry Analysis of US Multinationals, Financial Management, 24: 77–88.

• Van Deventer, D.R., K. Imai, and M. Mesler. 2004. Advanced Financial Risk

Management: Tools and Techniques for Integrated Credit Risk and Interest Rate Risk

Management, Wiley, New Jersey.

Websites

• www.forexnewsnow.com/forex-analysis/currency/volatile-currency-pairs-2017/

• data.worldbank.org/topic/trade

Analysis of Exchange Rate Risk & Hedging Strategies

Page | 34

Appendix - 1

Sr. No. Company

1 AIR FRANCE -KLM

2 APERAM

3 ARCADIS

4 ASM INTERNATIONAL

5 BAM GROEP KON

6 BE SEMICONDUCTOR

7 CORBION

8 EUROCOMMERCIAL

9 FUGRO

10 POSTNL

11 SLIGRO FOOD GROUP

12 TKH GROUP

13 TOMTOM

14 VASTNED

15 WDP

16 WERELDHAVE

17 WESSANEN