analysis of booming pharmaceutical sector in india

TRANSCRIPT

HISTORY OF INDIAN PHARMACEUTICAL COMPANIES

22

Contents

� Growing Indian Economy

� Growing Middle Class with Higher Purchasing Power

� Changing Disease Profile

� Government Policies

� HealthCare Insurance

Strong Macro-Economics over the Next Decade

Growing Middle Class with Higher Purchasing Power• India’s population is currently around 1.2 billion and is projected to rise to 1.7 billion by 2050 – a 41.66% increase that will see it

outstrip China as the world’s most populous state. Besides, India has a huge middle class population (households with annual incomes of US$4762 to US$23,810 at 2001-02 prices), which has grown rapidly, from 25 million people in 1996 to 159 million people in 2013. If the economy continues to grow fast and literacy rates keep rising, around a third of the population (34%) is expected to join the middle class in the near future. The middle class population is rapidly acquiring the purchasing power necessary to afford quality western medicine due to an increase in disposable income.

The Indian population spent 7% of

its disposable income on healthcare

in 2005; this number is expected to

nearly double, to 13%, by 2025

Changing Disease ProfileThe Indian population is experiencing a shift in disease profilesTraditionally, the acute disease segment held a significant share ofthe Indian pharmaceutical market. This segment will continue togrow at a steady rate, due to issues relating to public hygiene andsanitation. But, with increase in affluence, rise in life expectancyand the onset of lifestyle related conditions, the disease profile isgradually shifting towards a growth in the chronic diseasessegment. India has the largest pool of diabetic patients in theworld, with more than 41 million people suffering from thedisease; this is projected to reach 73.5 million in 2025. IMS Healthindicates that some of the fastest growing therapeutic segmentsin the Indian Pharma space today are chronic disease-relatedtherapeutic segments. The anti-diabetic segment grew 29% in the12 months ending July 2010. Cardio-vascular medication andnervous system disorder medication grew at 22% for the sameperiod of time, indicating rapid growth. The growing size of theIndian geriatric population will be a key factor in influencing thegrowth of the chronic segment. By 2028, an estimated 199 millionIndians will be age 60 or older, up from about 91 million in2008.Along with chronic, in the last year there has been a reboundin sales in the acute diseases segment. This trend is likely tocontinue over the next few years, as we see companies wideningtheir reach into newer markets, which have a relatively highernumber of treatment naïve patients requiring basic treatment,thus, creating new demand for drugs of the acute therapiessegment.

• Government Policies

The Indian government has been making efforts toimprove nationwide provision of healthcare. It haslaunched policies that are aimed at:

• building more hospitals,

• boosting local access to healthcare,

• improving the quality of medical training,

• increasing public expenditure on healthcare to 2-3%of GDP, up from a current low of 1%.

Some of the significant government allocations onhealthcare spend include a five year tax break foropening hospitals anywhere in India, with an addedfocus on tier II and tier III markets, both in the 2008-09Union Budget plans to spend US$373 million on thepromotion of healthcare through programmes for theprevention and cure of diseases such as cancer,diabetes, heart ailments and stroke in 2014-15.

Diabetes, hypertension and non- communicabledisease patients will be screened under the NationalProgramme for Prevention and Control of Cancer,Diabetes, Cardiovascular Diseases and Stroke(NPCDCS). The programme is likely to cover more than70 million adults across 100 districts in 15 states andunion territories of the country

• Healthcare Insurance

India’s healthcare insurance industry is currently small and limited, but is expected to grow at a CAGR of 15% till 201. Around 80% of India’s healthcare expenditure is financed out of pocket. This limits the propensity of Indians to spend on healthcare, particularly in lower and middle income groups which comprise around 95% of population.The small percentage of Indians who do have some insurance, the main provider is the Government-run General Insurance Company (GIC). Private insurance only came into the market post 2007, when the Insurance Regulatory and Development Authority (IRDA) eliminated tariffs on general insurance. Apollo was the first private healthcare insurance provider in the country; other private entrants are ICICI Lombard, Tata AIG, Royal Sundaram, Star Allied Health Insurance, Cholamandalam DBS and Bajaj Allianz Apollo

$15.6 billionPharma Exports in FY13

$16.4 billionDomestic Pharma Market in FY13

60%Share of Urban Regions in the

Domestic Pharma Market in 2013

5%Pharma FDI as a Share of Total

FDI in India in FY14

73%Share of Indian Companies in

the Pharma Market in 2013

India‟s pharma sector at a glance

$84.9 billionEstimated Pharma Market Size

in 2020

STRUCTURE OF THE

PHARMA SECTOR

PHARMA

Active PharmaceuticalIngredients / Bulk Drugs Formulations

Pharma sector in India is broadly classified into two segments: Active Pharmaceutical

Ingredients/Bulk Drugs and Formulations

Branded Generic Chronic Acute

�Cardiovascular

�Neurological

�Anti-diabetes

�Gastro-intestinal

�Anti-infectives

�Respiratory

�Pain

�Gynecology

By therapeutic segments

Advantage India

AdvantageIndia

Cost Efficiency

• Lowcost of production and R&Dboosts efficiencyof Indianpharmacompanies

• Comparative cost advantageenhances Indianpharmaexports

EconomicDrivers

• Economicprosperity toimproveaffordabilityof drugs

• Increasingpenetration ofhealth insurance

Diversified Portfolio

• Accounts for over10per cent ofglobal pharmaceutical production

• Over60,000 generic brands across60 therapeutic categories

• Manufactures more than 400different APIs

Policy Support

• Government unveiled‘PharmaVision2020’aimedat makingIndiaagloballeader in end-to-enddrugmanufacture

• Reducedapproval time for newfacilities to boost investments

Market size:USD35.9billion

2016F

Market size:USD15.6billion

2011

Source: BMI, Aranca Research2016 revenueforecasts are estimates of BMI, United States Food and Drug

Association (USFDA), BMI stands for Business Monitor International,API stands for Active Pharmaceutical Ingredients

Evolution of the Indian pharmaceuticalsector

• Indiancompaniesincreasinglylaunchoperations in foreigncountries

• Indiaamajordestination forgeneric drugmanufacture

• Higher spendingon R&Ddueto theintroductionofproductpatents

• Liberalisedmarket• Domesticplayers

expandaggressively

• Increasedpropensity forR&D

• IndianPatent Actpassed in 1970

• Several domesticcompanies startoperations

• Development ofproductioninfrastructure

• Export initiativestaken

• Marketdominatedbyforeigncompanies,withlittledomesticparticipation

2005 onwards

1990-2005

1970-1990

Before 1970

Notable Trends in Indian Pharmaceutical sector

Research anddevelopment

• Indianpharma companies spend 2 per cent of their total turnover on R&D

• Expenditure on R&D is likely to increase due to the introduction of productpatents; companies need to develop new drugs to boost sales

Clinical trials

• Due to its cost advantage, India is increasingly becoming a hub for clinical trials. Clinical

trials market is estimated to be worth USD485million in 2010 and is projected to grow at 17

per cent CAGR over2009-15.

Export revenue

• The pharmaceutical export market in Indiais thrivingdue to strong presencein thegeneric

space

Joint ventures

• Several multinational companies are collaborating with Indian pharma firms to develop

new drugs

• Pfizer partnered with Aurobindo Pharmato developgeneric medicines

Product patents• The introduction of product patents in India in 2005 has boosted the discovery of new

drugs

• Indiahas reiterated its commitment to IP protection following the introduction of product

patents

• Due to its cost advantage, India is increasingly becoming a hub for clinical trials. Clinical trials

market is estimated to be worth USD585million in 2015 and is projected to grow at 17 per cent

CAGR over 2015-2020

• The pharmaceutical export market in India is thriving due to strong presence in

the generic space

• Several multinational companies are collaborating with Indian pharma firms to develop

new drugs

• Pfizer partnered with Aurobindo Pharmato develop generic medicines

• The introduction of product patents in India in 2005 has boosted the discovery of

new drugs

• India has reiterated its commitment to IP protection following the introduction of

productpatents

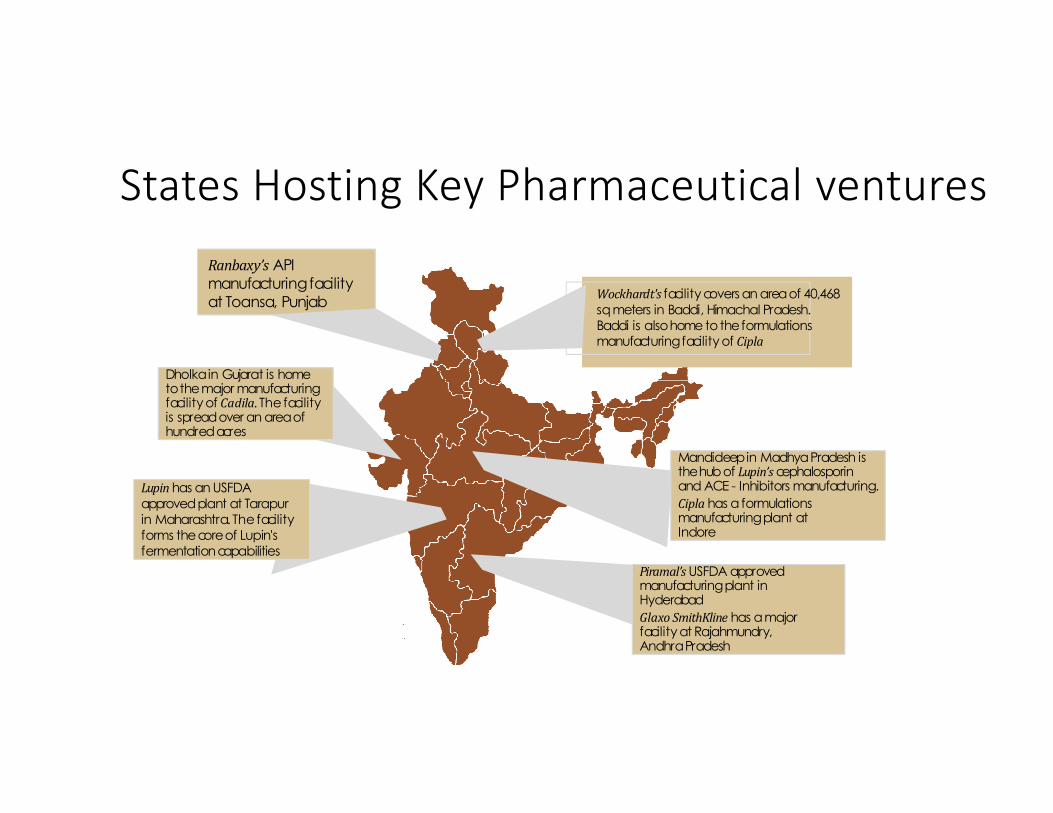

Dholkain Gujarat is hometothemajor manufacturingfacility of Cadila. The facilityis spreadover an areaofhundredacres

Wockhardt's facility covers an areaof 40,468sqmeters in Baddi, Himachal Pradesh.Baddi is alsohome totheformulationsmanufacturingfacility of Cipla

Ranbaxy’s APImanufacturingfacilityat Toansa, Punjab

Piramal’sUSFDA approvedmanufacturingplant in Hyderabad

Glaxo SmithKline has amajorfacility at Rajahmundry,AndhraPradesh

Mandideepin MadhyaPradesh isthehubof Lupin’scephalosporinand ACE - Inhibitors manufacturing.

Cipla has aformulationsmanufacturingplant atIndore

Lupinhas an USFDAapprovedplant at Tarapurin Maharashtra. Thefacilityforms thecoreof Lupin's fermentationcapabilities

States Hosting Key Pharmaceutical venturesStates hosting key pharmaceuticalventures

18.720.5

27.3

23.8

31.9

FY09 FY10 FY11 FY12 FY13

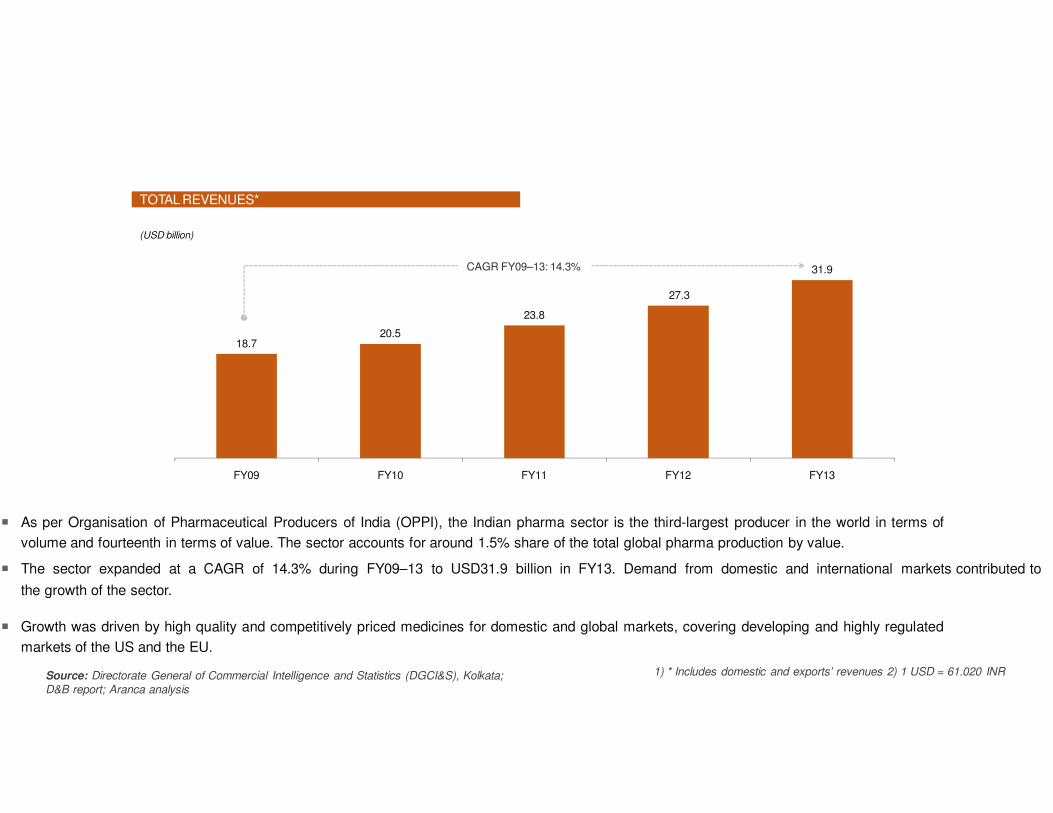

� As per Organisation of Pharmaceutical Producers of India (OPPI), the Indian pharma sector is the third-largest producer in the world in terms of

volume and fourteenth in terms of value. The sector accounts for around 1.5% share of the total global pharma production by value.

� The sector expanded at a CAGR of 14.3% during FY09–13 to USD31.9 billion in FY13. Demand from domestic and international markets contributed to

the growth of the sector.

� Growth was driven by high quality and competitively priced medicines for domestic and global markets, covering developing and highly regulated

markets of the US and the EU.

TOTAL REVENUES*

(USD billion)

India‟s pharma sector stood at USD31.9 billion in FY13, registering a CAGR of 14.3%

over FY09–13

CAGR FY09–13: 14.3%

Source: Directorate General of Commercial Intelligence and Statistics (DGCI&S), Kolkata;

D&B report; Aranca analysis

1) * Includes domestic and exports’ revenues 2) 1 USD = 61.020 INR

CAGR FY09–13: 10.8%

10.9

Source: DGCI&S, Kolkata; Department of Pharmaceuticals annual report 2011–12; Centre for Monitoring Indian Economy (CMIE) report; ICRA report

12.2

14.214.9

16.4

FY09 FY10 FY11 FY12 FY13

DOMESTIC REVENUES

(USD billion)

During FY09–13, domestic pharma market expanded at a CAGR of 10.8% to USD16.4

billion in FY13

� The domestic pharma market rose at a CAGR of 10.8% during

FY09–13, driven by increasing sales of generic medicines,

continued growth in chronic therapies, and greater

penetration in rural markets.

� Other key factors driving growth include favorable

demographics, rising income levels, growing health

awareness, increasing incidence of lifestyle diseases, and

insurance coverage.

EXPORT REVENUES EXPORT REVENUES – BY REGION

� The exports market performed well, with exports increasing from USD7.8 billion in FY09 to USD15.6 billion in FY13.

� The Americas accounted for ~34% of Indian pharma exports in FY13, followed by Europe (~26%) and Asia (~20%). The US had a ~26%

share, making it the single-largest export destination.

� Exports to Africa increased at a CAGR of 21% from FY09 to FY13, contributed mainly by export of anti-malarial and anti-retroviral drugs.

� Europe's share in Indian pharma exports has declined during FY09-13.

(USD billion)

Exports rose at 18.9% CAGR to USD15.6 billion; Americas had majority share in

India‟s exports, with US accounting for ~26%

7.88.3

12.4

9.6

15.6

FY09 FY10 FY11 FY12 FY13

CAGR FY09–13: 18.9%

Source: DGCI&S, Kolkata; CMIE report; India Ratings & Research (Ind-Ra) report, Aranca analysis

Year Americas Asia Europe Africa Oceania Others

FY09 28.8% 21.5% 31.6% 16.9% 1.1% 0.1%

FY10 31.6% 22.8% 27.3% 16.7% 1.5% 0.1%

FY11 32.5% 20.9% 27.0% 18.0% 1.5% 0.1%

FY12 33.6% 20.0% 26.4% 17.9% 1.7% 0.3%

FY13 34.3% 19.8% 25.5% 18.4% 1.6% 0.4%

CAGR

(FY09–13)

23.6% 15.9% 12.2% 21.1% 30.0% 71.9%

1.7

2.4� China has overtaken India as the main source of APIs for other

2.9

4.6

FY09 FY10 FY11 FY12

IMPORTS

(USD billion)

India imported APIs and intermediates at increased CAGR of 39.3% during FY09–12;

China has been its main source region

� Active pharmaceutical ingredients (APIs) and intermediates worth

USD4.6 billion were imported in FY12.

� The sector has been mainly importing from China as it provides low-

cost products which help the Indian formulation manufacturers to

mitigate rising production cost and increasing pressure on margins.

countries as well due to planned and sustained support from its

government in terms of infrastructure, subsidies, cheap

power, transportation, dedicated capacities in voluminous

manufacturing, effluent treatment facilities, industry-friendly labor

laws, etc.

CAGR FY09–12: 39.3%

Source: DGCI&S, Kolkata; Department of Pharmaceuticals annual report 2011–12; Business Standard; The Economic Times; Aranca analysis

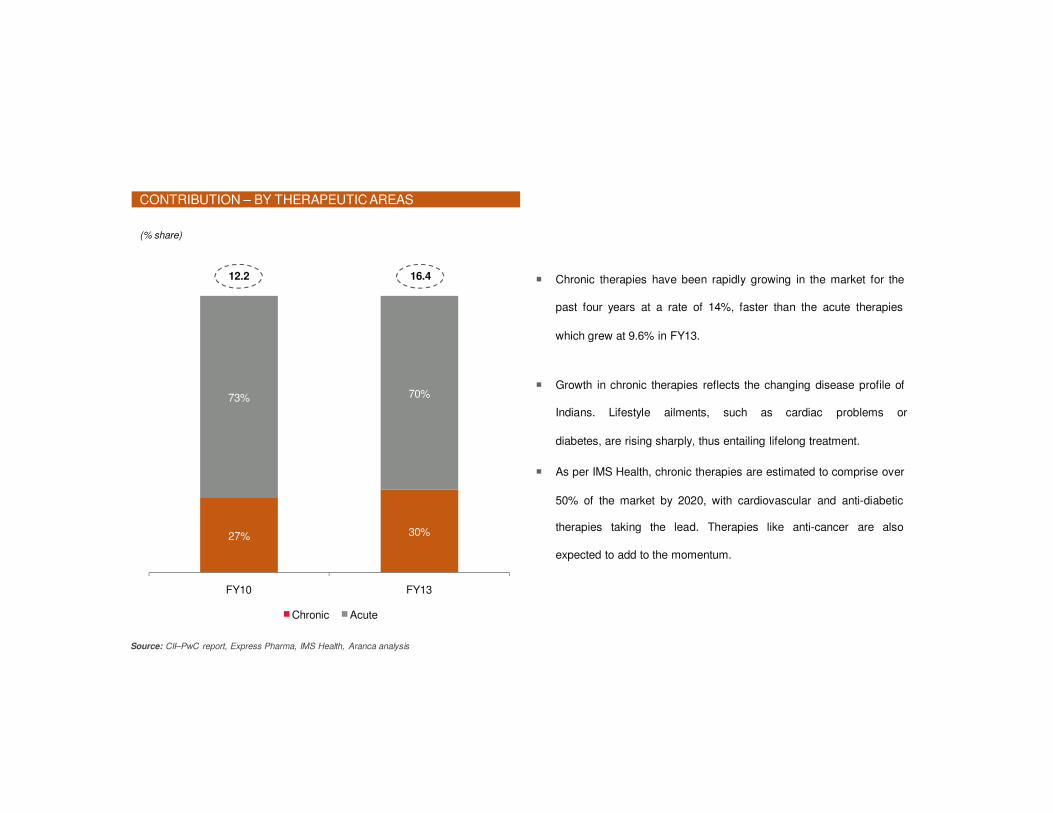

CONTRIBUTION – BY THERAPEUTIC AREAS

(% share)

Contribution by acute therapies decreased from FY10 to FY13 while that of chronic

therapies has risen during the same period

� Chronic therapies have been rapidly growing in the market for the

past four years at a rate of 14%, faster than the acute therapies

which grew at 9.6% in FY13.

� Growth in chronic therapies reflects the changing disease profile of

Indians. Lifestyle ailments, such as cardiac problems or

diabetes, are rising sharply, thus entailing lifelong treatment.

� As per IMS Health, chronic therapies are estimated to comprise over

50% of the market by 2020, with cardiovascular and anti-diabetic

therapies taking the lead. Therapies like anti-cancer are also

expected to add to the momentum.

27% 30%

73% 70%

FY10 FY13

Chronic Acute

12.2 16.4

Source: CII–PwC report, Express Pharma, IMS Health, Aranca analysis

31%

Source: CII–PwC report, Business Standard, Aranca analysis

30%

19%

USD16.4billion

20%

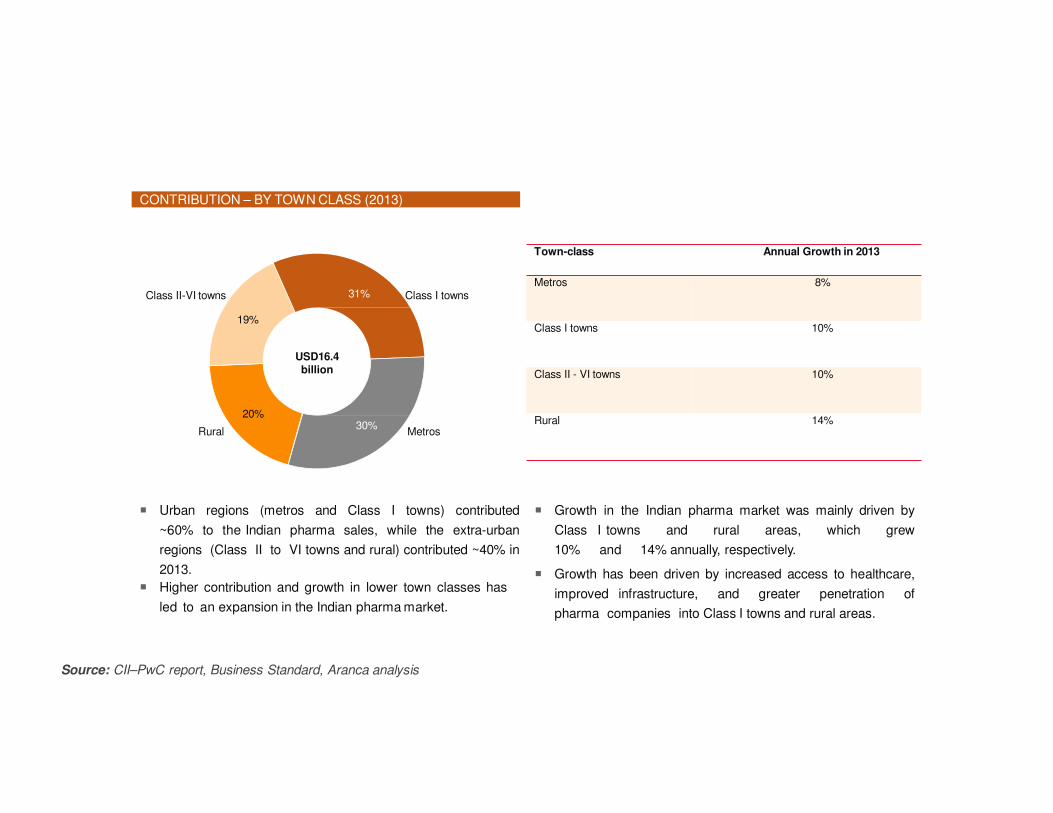

CONTRIBUTION – BY TOWN CLASS (2013)

Metros and Class I towns account for a majority share (~60%) of the Indian pharma

market; rural areas have witnessed the highest growth in contribution

MetrosRural

Class II-VI towns Class I towns

� Urban regions (metros and Class I towns) contributed

~60% to the Indian pharma sales, while the extra-urban

regions (Class II to VI towns and rural) contributed ~40% in

2013.

� Higher contribution and growth in lower town classes has

led to an expansion in the Indian pharma market.

� Growth in the Indian pharma market was mainly driven by

Class I towns and rural areas, which grew

10% and 14% annually, respectively.

� Growth has been driven by increased access to healthcare,

improved infrastructure, and greater penetration of

pharma companies into Class I towns and rural areas.

Town-class Annual Growth in 2013

Metros 8%

Class I towns 10%

Class II - VI towns 10%

Rural 14%

GLOBAL BIOLOGICS SPENDING BIOLOGICS – SHARE OF SALES BY REGION (2012)

� According to IMS Health forecasts, the global biologics market is estimated to grow to USD250 billion by 2020 from USD169 billion in 2012.

� Biosimilars and non-original biologics would represent 4–10% (USD10–25 billion) of the market by 2020, depending on the number of new

biosimilars introduced, especially in the US.

� The global biologics market is largely driven by mature markets. The US constituted approximately 49%, while the European Union (EU) accounted for

approximately 22% of the market in 2012.

� The pharmerging markets accounted for only approximately 8% share.

(USD billion)

Global biologics market is estimated to expand at 5% CAGR to USD250 billion during

2012–20

2007 2012

Biosimilars/Non-Original Biologics

2020

Other Biologics

48.6%

7.5%21.6%

13.2%

9.1%

Pharmerging (Includes

Brazil, Russia, India, China, an d Mexico, Turkey, among

others)

European Union (EU)

Rest of World (ROW)

US

USD169billion

106

169

250

105.4

Source: IMS Health, MIDAS, MAT Dec 2012; Aranca analysis

166.5

225–239

0.6 2.5 10–25

Japan

Strengths Weaknesses Opportunities Threats

•Low cost of skilled

manpower

•Access to large pool of

highly trained scientists

•Strong marketing and

distribution network

•Proven track record in

design of high technology

manufacturing devices

•Low cost of innovation,

manufacturing and

operations

•Higher GDP growth leading

to increased disposable

income in the hands of

general public and their

positive attitude towards

spending on healthcare

•Stringent pricing

regulations

•Poor transport and medical

infrastructure

•Lack of data protection

•Very competitive

environment

•Poor health insurance

coverage

•Production of low quality

drugs tarnishes image of

industry abroad

•Low investment in

innovative R&D

•Increase in per capita

income

•Global demand for

generics rising

•Increasing population with

more sedentary lifestyle

•Increasing health

insurance sector

•Significant investment

from MNCs

•Medical tourism

•Cheap, diverse clinical

trials

•Global outsourcing hub

due to low cost of skilled

labor

•Other low cost countries

affecting demand

•Government regulations

changing

•Expanding of Drugs Price

Control Order

•Lack of investment in

infrastructure

•Wage inflation

•R&D restricted by lack of

animal testing and

outdated patient office

•Counterfeiting threat

SWOT Analysis Of Indian Pharmaceutical Industry

Indian pharma sector is highly fragmented; domestic players account for a lion‟s share

KEY PLAYERS IN THE INDIAN PHARMA SECTOR

73%

27%

Cipla

Ranbaxy

Dr. Reddy‟s

GlaxoSmithKline

Market share for 2013Key International Players

Key Domestic Players

Sun Pharma

Lupin Limited

Abbott Laboratories

GlaxoSmithKline

Pfizer

Source: Company websites, The Economic Times, Aranca analysis, PwC report

� Currently, Abbott Laboratories leads the

market in therapies with a 6.5% share.

� With Sun Pharma’s acquiring Ranbaxy in

2014, market share of Indian companies is

forecasted to increase to 77% from the

current 73%.

� The combined entity is estimated to replace

Abbott Laboratories’ market share by

holding a combined market share of ~9.3%.

Indian

companies

Multinational

Corporations

Key Recent Trends In Pharma Industries

Acquisition and MergerSo the question arises what these terms actually mean.

• A merger is said to occur when 2 or more companies combine to form a singlecompany. A very well known example is Glaxosmithkline(By merging ofGlaxoWellcome and Smithkline Beecham)

• Acquisition may be defined as an act of acquiring effective control by one companyover assets and management of other company. A recent is example of acquisition ofRanbaxy by Sun pharma

• Mergers and Acquisitions (M&A) seem to be the flavor of the season. Sun Pharmatook over Ranbaxy and Bayer acquired Merck's consumer healthcare business. Thefirst was the $3.2 billion deal in early April, by which Sun Pharma acquired Ranbaxy,making the combined entity the fifth-largest generics company in the world and thelargest in India. Sun Pharma had made 16 other acquisitions before, but this dealwas larger than all of them put together. Another one was the realignment ofbusiness interests by Novartis and GlaxoSmithKline (GSK) in late April, by whichNovartis sold almost its entire vaccine business to GSK, while buying up the latter'soncology drugs business

Source: Company websites, Grant Thornton, Business Standard, Thomson Banker, Aranca research Note: Only key deals for 2013 & 2014 mentioned

USD3.2 billion

2014

Acquires

The combined entity would be

India’s largest pharma company

and world’s fifth largest generic

drugs maker

NA

2014

Acquires

The acquisition helps Lupin

expand into the Latin American

market and build its global

specialty business

USD321.6 million

2013

Acquires

The transaction would

strengthen Torrent’s position in

the women healthcare, pain

management and

vitamins/nutrition segments

USD512 million

2013

Acquires

The deal with Medpro would

help Cipla to strengthen its

African operations

The acquisition would

strengthen Mylan’s global

injectables platform and create

a global injectables leader

USD 1.75 billion

2013

Acquires

2013

Acquires

Finoso would become Vivimed’s

research and development unit

to support innovators, generics

and licensing efforts

NA

2013

Acquires

With Indchem’s excellent

customer service and technical

support, IMCD would be able to

further strengthen its presence

in the Indian market

Recent Major Acquisition And Mergers

USD 2.8 million

Why India??• The answer to which is very simple. It is because Indian companies have strengths that are

hard to ignore for any global player seeking scale. India ranks very high in the third world, interms of technology, quality and range of medicines manufactured. From simple headachepills to sophisticated antibiotics and complex cardiac compounds, almost every type ofmedicine is now made indigenously. Playing a key role in promoting and sustainingdevelopment in the vital field of medicines,

• As the global blockbuster boom of the 1980s and 1990s ran out of steam and patentexpiries started accelerating, big pharma has been forced to cut down on inefficiencies andfocus on core competencies. Hence, there has been (and will continue to be) significantconsolidation in the global pharma industry. The pharma industry globally is going througha challenging time with increasing public scrutiny and immense pressure on pricing. Againstthe backdrop of subdued growth in developed markets such as the US and the Europe,pharma emerging markets continue to show a robust growth. Two categories of companieswould drive out the benefits .The first category would consist of Indian companies whohave low-cost and world-class R&D as well as manufacturing capabilities, such thatpotential bidders can leverage the Indian infrastructure as global (or regional) supply bases.The second category would consist of companies who have market-leading positions in thedomestic branded formulations market, in high-growth chronic specialties like cardiology,endocrinology, chronic pain, chronic respiratory and oncology

A Market dominated by Branded generics• In the global context, IMS Health, which began tracking and reporting on branded generics in 2002, defines

the category as including “prescription products that are either novel dosage forms of off-patent productsproduced by a manufacturer that is not the originator of the molecule, or a molecule copy of an off-patentproduct with a trade name.” This definition is used by both the United States of America’s Food and DrugAdministration (FDA) and the United Kingdom’s National Health Service (NHS). It does not include authorizedgenerics, which are drugs made by or under license from the innovator company and sold without a brand name.

• In India, any non patented molecule with a brand name other than the innovator’s name is termed as a brandedgeneric. Chemically, branded generics are identical, or bioequivalent to innovator drugs. It is the share of voicethe brand commands by getting repeatedly prescribed by the physicians, due to some degree of recall andpreference over the other brands. In the global context, substitution – whenan innovator product goes off-patent - is the key driver for generics. In India, it’s about driving a difference using the core equity of a brand,over a competitor’s product.

Patented Product• The market size for patented drugs as of today is very small. Only about 1-2% of the market is

made up of patented drugs, which are being sold by multinational innovators. There are multiple Indian companies that have drugs in the pipeline, with a greater focus on R&D, but estimates suggest that it would be at least 7 to 10 years before these begin to have a serious impact on the industry. Industry experts believe that the current size of the patented drug market is estimated at US$120-130 million. Due to weak patent laws in the past, and multiple, cheap generic versions of drugs present in the market, multinational players were hesitant to introduce their patented products. In the future, with growing affordability, deepening of health insurance and steady improvement in Intellectual Property Rights (IPR), patented product launches should increase.

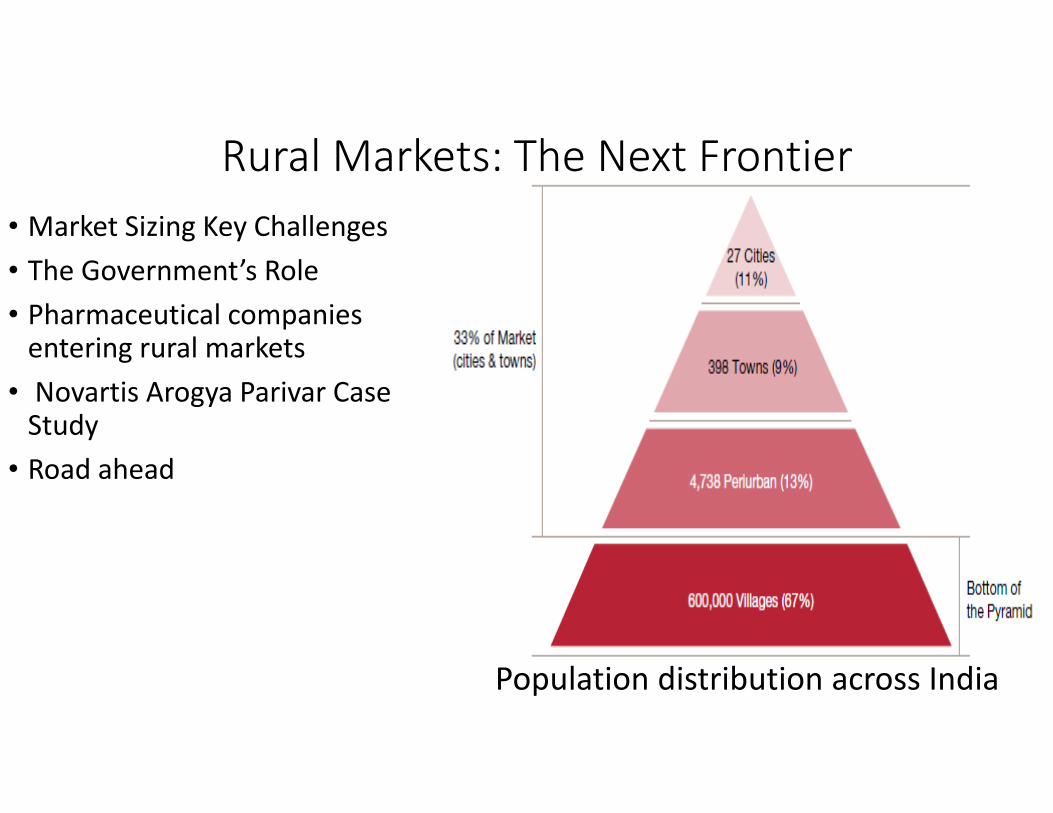

Rural Markets: The Next Frontier

• Market Sizing Key Challenges

• The Government’s Role

• Pharmaceutical companies entering rural markets

• Novartis Arogya Parivar Case Study

• Road ahead

Population distribution across India

Market Sizing• Majority of the Pharma market’s growth is

driven by the urban markets, that is, areas thatare classified as metros or tier I cities . Tier II totier VI is classified as peri urban, while rural isthe bottom of the pyramid, which constitutes67% of India’s population (600,000 villages). Asper IMS Health, peri-urban markets account for38% of total industry sales, being valued atUS$3.4 billion, while, rural markets account for17% of total industry sales, being valued atUS$2 billion, in 2010.

• PwC estimates that over the next ten years,rural markets will grow at a CAGR ranging froma conservative 15% to an aggressive 20%,reaching an expected valuation of betweenUS$8 billion and US$12 billion, depending onthe implementation of growth drivers

• The Opportunity

Around 742 million people reside in rural areas. There is a significant gap between the number of people residing in villages that require treatment, and quality treatment and medicines reaching these villages. Accessibility of medication in rural areas is very poor, with less than 20% of the population having access. This gap represents a huge opportunity for pharmaceutical companies to expand, and we believe that these markets will be the future volume drivers of the industry

Key Challenges of the Rural Market• Low government spend on healthcare

India has a low level of government spending on healthcare, at 1% of the GDP, putting the country in the lowest 20% of those that contribute significantly low levels of public spending to health. Business Monitor International reported that healthcare expenditure in India increased from US$49.7 billion to US$86.9 billion between 2009 and 2014, a rise of 75%.

• Poor Infrastructure

Healthcare infrastructure is poor, compared to urban areas. The doctor patient ratio in rural areas is 1:20,000, versus the urban ratio of 1:2000 [India requires 600,000 doctors in order to meet the statutory 1:250 ratio that is a World Health Organization (WHO) norm]. Doctors are not qualified, as most of them in villages have Bachelor of Health Sciences (BHS) & Bachelor of Ayurvedic Medicine and Surgery (BAMS) degrees. The quality and availability of medicines in rural areas is dubious, as there are many cases of counterfeiting and spurious drugs that have been exposed. Majority of the patients earn a basic daily wage, and affordability is very low.

• Limited affordability

Healthcare is a low priority when it comes to income allocation, with average consumer expenditure on healthcare at just 7%.(6) 80% of the rural population is on a daily wage, income levels are as low as <US$1.78 per day.

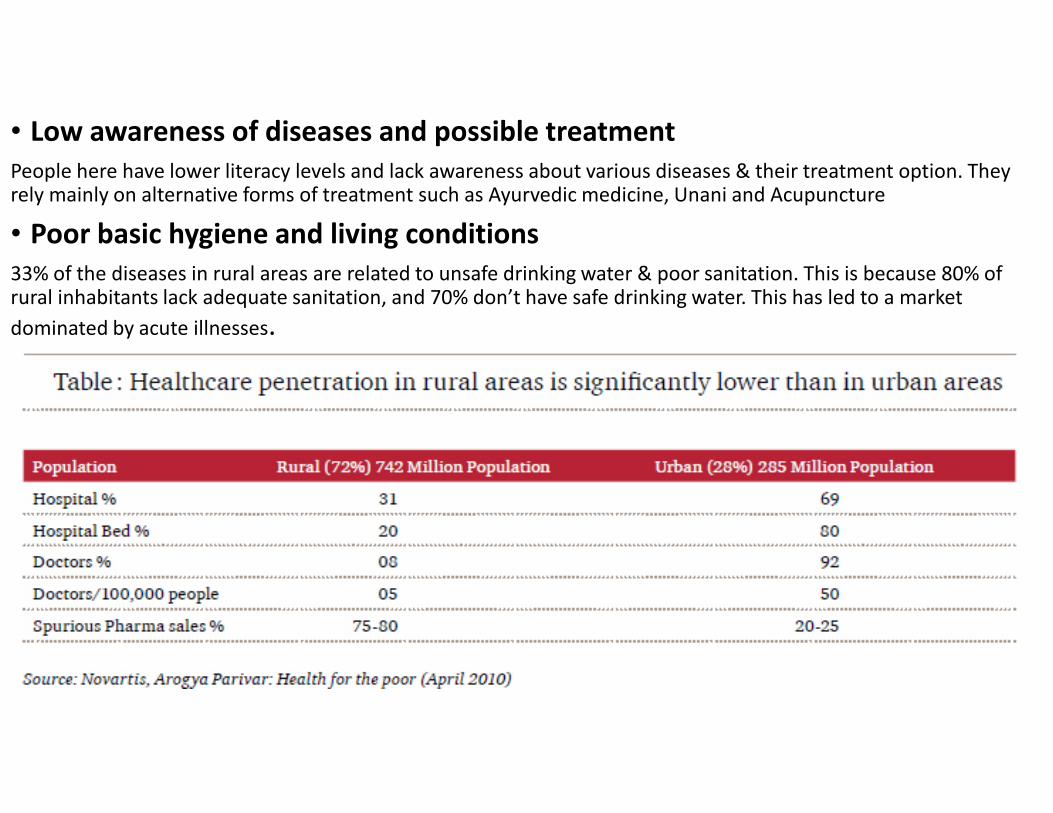

• Low awareness of diseases and possible treatment

People here have lower literacy levels and lack awareness about various diseases & their treatment option. They rely mainly on alternative forms of treatment such as Ayurvedic medicine, Unani and Acupuncture

• Poor basic hygiene and living conditions

33% of the diseases in rural areas are related to unsafe drinking water & poor sanitation. This is because 80% of rural inhabitants lack adequate sanitation, and 70% don’t have safe drinking water. This has led to a market

dominated by acute illnesses.

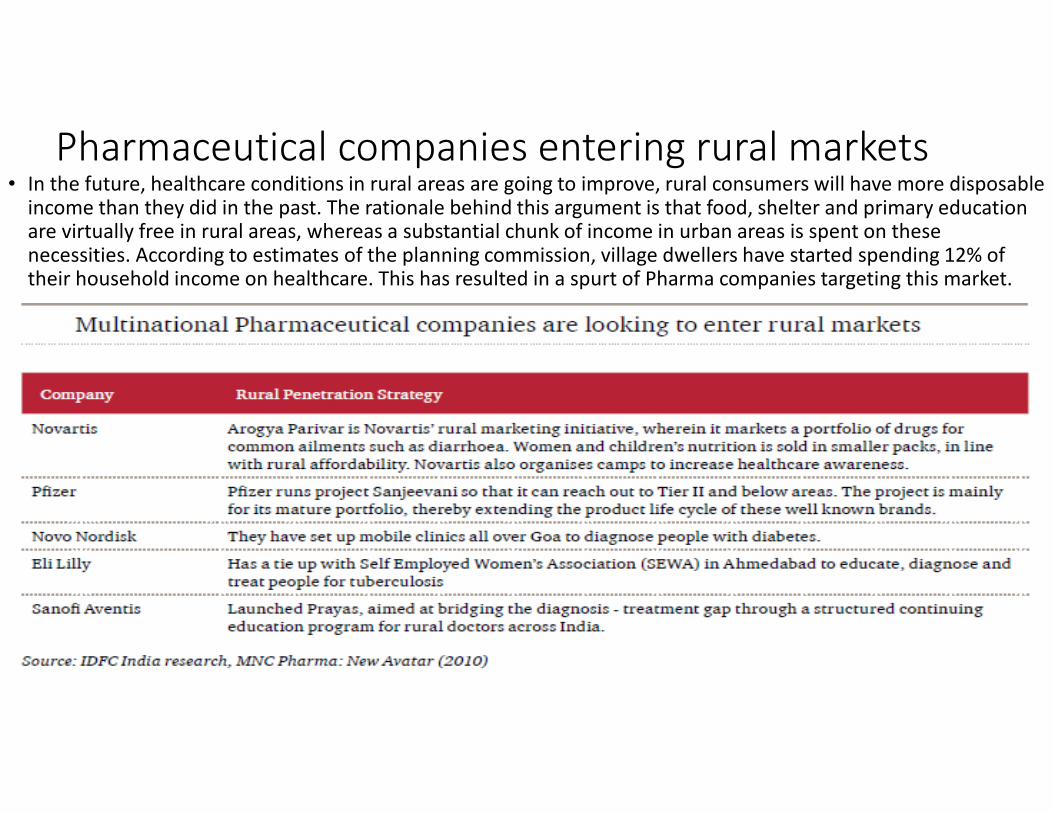

Pharmaceutical companies entering rural markets• In the future, healthcare conditions in rural areas are going to improve, rural consumers will have more disposable

income than they did in the past. The rationale behind this argument is that food, shelter and primary education are virtually free in rural areas, whereas a substantial chunk of income in urban areas is spent on these necessities. According to estimates of the planning commission, village dwellers have started spending 12% of their household income on healthcare. This has resulted in a spurt of Pharma companies targeting this market.

Novartis Arogya Parivar Case StudyArogya Parivar is a social innovation to improve healthcare for the poor in rural areas by promoting disease prevention through a healthy lifestyle and laying focus on Community Education & not ‘sell-in’ to stockists. It also aims to form partnerships with NGOs & healthcare companies to implement a complete healthcare program.Works

on 4 principles: Arogya uses the 4 A’s: awareness, affordability, availability (access), and adaptibility.

Awareness

Community Education meetings

Physician knowledge sharing [BAMS/BHMS]

Adaptability

Rural specific solutions [oral rehydration

solutions (ORS)/Zinc]

Vernacular communication [local

dialect]

Availability

Linkages to city supply points

Mobile Health camps

Affordability

Custom small packs

Arogya Parivar’s Business model

2004 2014

Source: Sun Pharma website

Among thetopfive

Indian pharma

companies

Strong presencein

generics market

Over half thesales fromNorth America

Market capitalisation of USD15.1billion

Revenuebaseof about

USD1.7 billion

Commencedoperations in

Calcutta

Nationwidemarketing

operations rolledout

Built thefirst APIplant

Firstinternationalacquisition:

NicheBrand intheUS

AcquiredRanbaxy for $3..2

bn

Organicgrowthphase

All-Indiaoperations begin

Focuson R&D

Acquisitions acrosstheglobe

1983 1987 1995

256 approvedproducts and 391filed for approval

23 manufacturingsites worldwide

Sun Pharma: Leveraging its genericmarket capabilities

44%

15%

41% USD1.4billion

India

US

Rest of the World

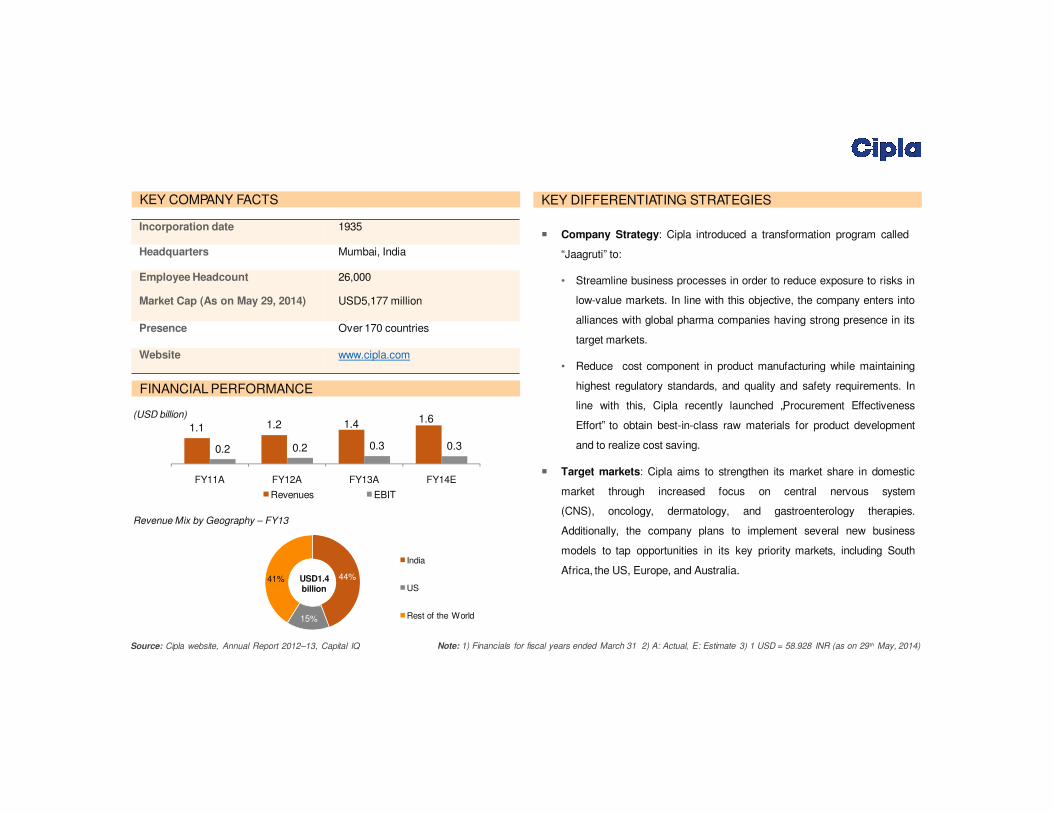

Case Study 1: Cipla Limited

Source: Cipla website, Annual Report 2012–13, Capital IQ

1.1 1.2 1.4

0.2 0.2 0.3 0.3

FY11A FY12A

Revenues

FY13A

EBIT

FY14E

(USD billion)

KEY COMPANY FACTS

FINANCIAL PERFORMANCE

KEY DIFFERENTIATING STRATEGIES

� Company Strategy: Cipla introduced a transformation program called

“Jaagruti” to:

• Streamline business processes in order to reduce exposure to risks in

low-value markets. In line with this objective, the company enters into

alliances with global pharma companies having strong presence in its

target markets.

• Reduce cost component in product manufacturing while maintaining

highest regulatory standards, and quality and safety requirements. In

line with this, Cipla recently launched „Procurement Effectiveness

Effort‟ to obtain best-in-class raw materials for product development

and to realize cost saving.

� Target markets: Cipla aims to strengthen its market share in domestic

market through increased focus on central nervous system

(CNS), oncology, dermatology, and gastroenterology therapies.

Additionally, the company plans to implement several new business

models to tap opportunities in its key priority markets, including South

Africa, the US, Europe, and Australia.

Revenue Mix by Geography – FY13

1.6

Note: 1) Financials for fiscal years ended March 31 2) A: Actual, E: Estimate 3) 1 USD = 58.928 INR (as on 29th May, 2014)

Incorporation date 1935

Headquarters Mumbai, India

Employee Headcount 26,000

Market Cap (As on May 29, 2014) USD5,177 million

Presence Over 170 countries

Website www.cipla.com

27%

39%

14%

20%India

US

Japan

Others

Case Study 2: Lupin Limited

Source: Lupin website, Annual Report 2012–13, Capital IQ

(USD billion)

KEY COMPANY FACTS

FINANCIAL PERFORMANCE

KEY DIFFERENTIATING STRATEGIES

� Competitive advantage: Lupin positions itself in the global pharma

market by leveraging opportunities in new markets, new therapies, new

businesses, and product mix. This has enabled the company to gain

competitive advantage over peers with singular focus market.

� Focus on innovative offerings: Lupin strives to offer innovative

products through R&D investments. The company‟s capacity to invest in

innovations and ability to remain invested for a long period of time

differentiates it from competitors.

licensing products and entering into strategic alliances with leading

product portfolio as well as tap the unaddressed demand.

� Creation of sales force: Lupin is committed to create and develop a

specialty product marketing and sales team with talented and

experienced professionals. This would enable the company to cater to

the complex needs of niche markets.

� Leveraging geographic reach: Lupin has combined the benefits of its

nationwide presence with a short mind-to-market cycle, enabling the

company to operate locally as well as benefit from local opportunities in

global markets.

Revenue Mix by Geography – FY14

USD 1.9

billion

1.0 1.2

0.2 0.2 0.3 0.5

FY11A FY12A

Revenues

FY13A

EBIT

FY14A

Note: 1) Financials for fiscal years ended March 31 2) A: Actual 3) 1 USD = 58.928 INR (as on 29th May, 2014)

1.91.6

Incorporation date 1968

Headquarters Mumbai, India

Employee Headcount 12,710

Market Cap (As on May 29, 2014) USD7,079 million

Presence Global

Website www.lupinworld.com

Source: Sun Pharma annual report 2013, PwC report, Aranca research

Particulars Description Implications

National Pharmaceutical Pricing

Policy (NPPP) 2012� The Indian government introduced NPPP in 2012 to regulate the prices

of 348 essential drugs, based on their strengths and dosages.

� Manufacturers are allowed to sell these drugs on or below

the ceiling price fixed by the government.

� The policy is applicable to imported drugs as well.

� Implementation of NPPP resulted in decline of profit margins for

products under regulation from 20% to 16% and 10% to 8% for retailers

and stockists, respectively, during 2012–13.

� The policy has resulted in significant uncertainty among stockists on

whether to continue with the business amid low profits and margin reduction.

Foreign Direct Investment

(FDI) policy� In 2001, 100% FDI was allowed through the automatic approval route in

the pharma sector.

� Post November 2011, 100% FDI is allowed in Greenfield projects through

the automatic route, while 100% FDI is allowed in Brownfield projects with

the approval of the Foreign Investment Promotion Board (FIPB).

� As per the Department of Industrial Policy & Promotion (DIPP), the

pharma sector attracted cumulative FDI investments of approximately

USD11.6 billion between April 2000 and February 2014.

Medical Council of India (MCI)

guidelines on sales andmarketing practices

� MCI guidelines were issued to ensure transparency in sales

and prevent unethical practices of some doctors.

� MCI aimed to stop medical professionals from prescribing drugs in exchange

of bribe from drug manufacturers.

� Tax authorities use the Central Board of Direct Taxes (CBDT) circular

based on MCI guidelines to decide on permissible sales and marketing

expenses.

Regulatory Framework

…in addition to DoP uniform code, compulsory licensing, and clinical trial regulationsParticulars Description Implications

Department of Pharmaceuticals

(DoP) uniform code on sales and marketing

� In 2011, DoP laid down a code of marketing practices for the pharma sector to

streamline marketing efforts.

� The DoP code lays down guidelines for exaggerated claims; audiovisual

promotions; activities of medical representatives; and provision of samples,

gifts, hospitality, and sponsorships by pharma companies.

� The adoption of DoP code is voluntary. However, in recent times, the pharma

sector has agreed to enforce the code.

� DoP would review its implementation and after a set interval of time if it

is discovered that the code has not been implemented by pharma

associations or companies, it would consider making it a statutory code.

Compulsory licensing � India has adopted compulsory licensing on the following grounds under

Section 84 of the Indian Patent Act: (1) the drug did not meet reasonable

requirements of the citizens,

(2) the drug was not reasonably priced, and (3) the patent was not locally

manufactured.

� The imposition of this regulation paved way for production of low-cost generic

medicines of the branded patent drugs. Thus, costly, branded life saving drugs

are available at a cheaper rates to the Indian population.

� The regulation affects the brand value of branded drugs manufactured by

MNCs, and thus has been opposed by them.

Clinical trial regulations � As per new regulations introduced in 2013, all clinical trials need to be

approved by a government committee and at least half of each trial needs to

be run in a government-run hospital.

� Pharma companies need to have the videotaped consent of each test subject.

� Stringent regulations increase the duration of the approval process; hence, the

number of clinical trials has dropped to 19 in 2013 from 500 in 2011.

� It also has projected India as a less favorable option to conduct clinical

trials.

Biosimilars in India are regulated by Central Drugs Standard Control Organization and

Department of BiotechnologyParticulars Description Implications

Biosimilar Guidelines � The “Guidelines on Similar Biologics” prepared by Central Drugs Standard

Control Organization and Department of Biotechnology in 2012 laid down the

regulatory pathway for a biologic claiming to be similar to an already authorized

reference biologic.

� The guidelines address the regulatory pathway regarding manufacturing

process and quality aspects for similar biologics.

� These guidelines also address the pre-market regulatory requirements

including comparability exercise for quality, preclinical and clinical studies, and

post-market regulatory requirements for similar biologics.

� The new guideline creates a pathway for local and international

companies to invest in biosimilar development with manufacturing in India.

� The introduction of a similar biologic or biosimilar into the market would result

in significant reduction in costs.

� This introduction would also help address local patients‟ access to expensive

drugs.

Reduction in approvaltimefor new facilities

• Steps taken toreduceapproval timefor new facilities

• NOCfor export license issued in twoweeks comparedto 12 weeks earlier

Collaborations• MOUs with USFDA, WHO,Health Canada, etc. to boost growth of the Indian

Pharmasector by benefitingfromtheir expertise

Support fortechnology upgrades

and FDIs

• Zeroduty for technology upgrades in the pharmaceutical sector through the

Export Promotion Capital Goods (EPCG)Scheme

• Government is planningto relax FDI norms in the pharmaceuticals sector

Industryinfrastructure

• Government of Indiaplans to set upaUSD640 million VCfund to boost drug

discoveryand strengthenthe pharmainfrastructure

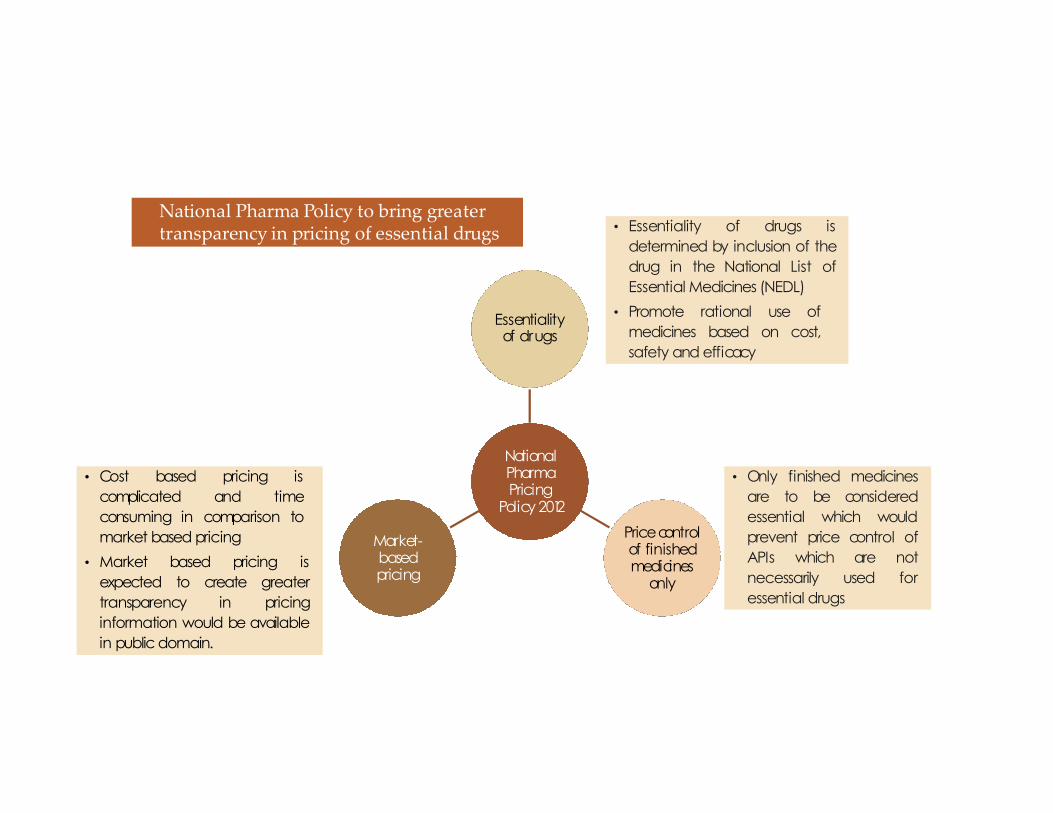

Pharmavision 2020• PharmaVision 2020 by the government’s Department of Pharmaceuticals aims to

makeIndiaamajor hubfor end-to-enddrugdiscovery

Notes: NOC- No objection certificate; VC - Venture CapitalMOU - Memorandum of Understanding

Favourable policy measures supportgrowth

Favourable Policy Measures Support Growth

NationalPharmaPricing

Policy 2012

Essentialityof drugs

Pricecontrolof finishedmedicines

only

Market-basedpricing

• Cost based pricing is

complicated and time

consuming in comparison to

market based pricing

• Market based pricing is

expected to create greater

transparency in pricing

information would be available

in public domain.

• Essentiality of drugs is

determined by inclusion of the

drug in the National List of

Essential Medicines (NEDL)

• Promote rational use of

medicines based on cost,

safety and efficacy

• Only finished medicines

are to be considered

essential which would

prevent price control of

APIs which are not

necessarily used for

essential drugs

National Pharma Policy to bring greatertransparency in pricing of essential drugs

Challenges• Price Control

Price controls are broadly cited as the most critical challenge thatcompanies face in the Indian market. India is one of the mostprice-controlled markets in the world, as under the DPCO, pricesand margins are monitored carefully. The DPCO is beingsupervised by the NPPA. There were originally 347 pricecontrolled drugs included in 1979, which were then reduced to143 in 1987 (35) and currently, there are 76 bulk drugs under theDPCO.(36) Price controlled drugs are essential medicines, such asantibiotics and painkillers, and drugs used for the treatment ofdiseases such as cancer and asthma. Such medicines contain bulkdrugs, or raw materials, whose prices are controlled by the NPPA- manufacturers cannot hike prices on their own. However, 90%of drugs are currently outside of any price controls in India.Consumer organizations maintain their stance of urging thegovernment to continue to expand the umbrella of the DPCO,but the industry believes that there is enough competition for theprices to be modulated by the market itself. They believe thatprice caps would inhibit the development of R&D in the countryas companies would be less inclined to invest in R&D without thepossibility of high returns.

• Infrastructure

Infrastructure has always beenmentioned as a barrier to growth of thePharma industry in India. Poor energyand transport infrastructure hastraditionally posed a problem forcompanies. Some areas lack basic hotelfacilities, preventing reach andpenetration. With the governmentgradually increasing investment ininfrastructure, the situation isimproving, but it is still seen as aninvestment opportunity in India

• CounterfeitingCounterfeiting of drugs has been a major issue in the Indian Pharma space. The inherent nature of the Indian market makes it difficult for asystematic study that quantifies the extent of counterfeiting, to be carried out. There have been multiple reports suggesting various figures as therate of counterfeiting. A good indicator may be a large scale survey that was published in December 2009 by the health ministry that reportedthat spurious drug prevalence is much lower than otherwise suggested. The report found that only 0.046% of all medicines sold containedevidence of being spurious. This is in contrast to other reports, for example one conducted by the International Pharmaceutical Federation andfinanced by the WHO that said 3.1% of all drugs sold in India were spurious. These reports suggesting lower numbers than earlier ones may beencouraging, but leading players are still weary of the threat of spurious drugs. Steps taken by the industry to counter the threat of counterfeitinginclude investing in innovative packaging, using authenticity markers and sponsoring programmes to increase awareness amongst patients andhealthcare workers. The Organization of Pharmaceutical Producers of India (OPPI) has also carried out various initiatives to combat the situationlike organizing seminars and working with the Ministry of Health towards the development of policies against spurious drugs.

• LabourThere is an increasing concern in the domestic industry regarding a shortage of skilled labour in critical areas. This causes a demand-supplyimbalance, and has led to an increased rate of wage inflation

• Intellectual PropertyIndia has accepted and made a commitment to the Trade-Related Aspects of Intellectual Property Rights (TRIPS) in 1995, and keepingwith this commitment, implemented the Patent (Amendment) Act in 2005. Although this act does not apply for drugs patented before1995, it is a major step forward on the earlier patent scenario. Since then, recommendations have been made to the governmentregarding improvement and expansion of the Patent (Amendment) Act, by the Satwant Reddy committee and the Mashelkar report.These reports highlighted the need for data exclusivity and the prevention of ‘evergreening’. Domestic and global Pharma companies areshowing an increased confidence in the patent laws, and we expect an increase in the number of launches of patented products in theIndian market in the future. Resolution of data exclusivity laws and capacity building at patent offices will help in increasing confidenceamong foreign companies

India and USFDA(U.S. Food and Drug Administration)

• Since 2013 USFDA has banned 27 Indian units for violations. This year till now, USFDAhas already crackdown on 7 manufacturing units, the big name in the list being SunPharma’s 2 units Kharkadi plant and Halol plant in Gujarat and IPCA laboratoriesRatlam(API Division).Talking to a senior official at Ipca Laboratories said that the thiswould have impact on the company's formulations export business to the US marketsince it's formulations manufacturing units situated at Silvassa and SEZ Indore use theAPls manufactured from the Ratlam facility for manufacturing formulations for theAmerican market.

• Units of Ranbaxy Laboratories Ltd(Poanta Sahib in Himachal Pradesh and Dewas inMadhya Pradesh in 2009) and Wockhardt Ltd(Aurangabad Unit in 2013), were barredfrom exporting to the US.

• And one consistent problem that USFDA has been finding at almost all of the units isthat of data integrity, where USFDA has found instances of faking data, incompleterecords, retesting to match results. Experts say there is a need for Indianmanufacturers to keenly resolve these issues as even other regulators are likely totake a closer look at data integrity, besides GMP, in future

So is it that USFDA hates India!!!The answer is a straight no.• A closer look will reveal that it is not just Indian drug majors that are under the

US FDA scanner ,warning letters about violations have been sent out to drugcompanies in Australia, Canada, China, Austria, Germany, Netherlands, Ireland,and Spain

• In fact, the regulator has doled out the largest number of warning letters tohome-grown pharma companies; 114 US-based pharma companies were servedwith warnings and censured for marketing-related offences and nine for faultymanufacturing processes.

• Stating that the cost of compliance of Indian pharma companies has doubledover the past five years, the report noted that drug companies would have toinvest to ensure that compliance processes were up to speed. The large Indiandrug makers had the ability to bear the increased cost of compliance as well asthe financial flexibility to do so, and would continue to remain competitive inthe US market.

Lifestyle-related ailments, urbanization, and increasing health insurance are key drivers;

price control, low clinical trials, and fragmented supply chain are key concerns

Source: Sun Pharma Annual Report 2013, PwC, McKinsey & Company, Deloitte, Aranca research

KEY GROWTH ENGINES

� Changing disease profile and favorable demographics

• Change in patient demographics and increased lifestyle-related ailments are

likely to boost demand for quality and affordable drugs.

• Indian population‟s lifestyle has changed over the years due to socio-economic

factors and growing urbanization. This has led an increase in lifestyle-related

ailments such as obesity, heart disease, stroke, cancer, and diabetes.

• India is estimated to have a patient pool of 20% by 2020 due to ~1.3%

population growth per year and increased disease burden.

� Rapid urbanization

• The Indian pharma sector is poised to benefit from increased contribution from

metros and Class I towns, mainly due to growing urbanization and economic

development.

• According to McKinsey and BNP Paribas‟s estimates, India‟s urbanization is

projected to accelerate at a rate and scale comparable only to China, reaching

40% by 2030.

• Rapid urbanization would lead to growth in India's medical

infrastructure, thereby enabling companies to reach inaccessible and untapped

markets.

� Increasing health insurance coverage

• Increased penetration of health insurance in India is likely to solve the

affordability issue in the Indian pharma sector, thereby boosting demand.

• As of 2013, only 30% of population in India had health insurance coverage; the

remaining70% paid for healthcare expenses from their own savings.

• Health insurance penetration is estimated to reach ~45% by 2020.

KEY GROWTH INHIBITORS

� Drug price control

• The Indian government increased the number of drugs under price control

from 74 to 348 in 2013, thereby adversely impacting retail price of drugs.

• The move is said to have far-reaching implications on branded pharma

manufacturers with patented products rather than generics manufacturers

which are mostly domestic companies already selling products at relatively low

prices.

� Growing concern regarding clinical trials

• Clinical trials play a vital role in drug development. India accounts for less than

2% of global clinical trials.

• Growth in the number of clinical trials in India has been low primarily due to

regulatory uncertainty with regard to the conduct of clinical trials.

• Unethical practices, delay in approvals, corruption, etc., have led pharma

companies to shift their focus from India to other geographies like Malaysia

and East European countries like Poland for clinical trials.

� Fragmented supply chain

• The Indian pharma market is highly fragmented in manufacturing as well as

distribution. This has led to several inefficiencies in the sector.

• Fragmented supply chain leads to ineffective inventory management

systems, resulting in high inventory holding costs, thereby increasing

operating costs.

• On the distribution front, dominance of small chemists leads to lack of

economies of scale and consumers having to pay high prices.

Summing up the Entire Analysis

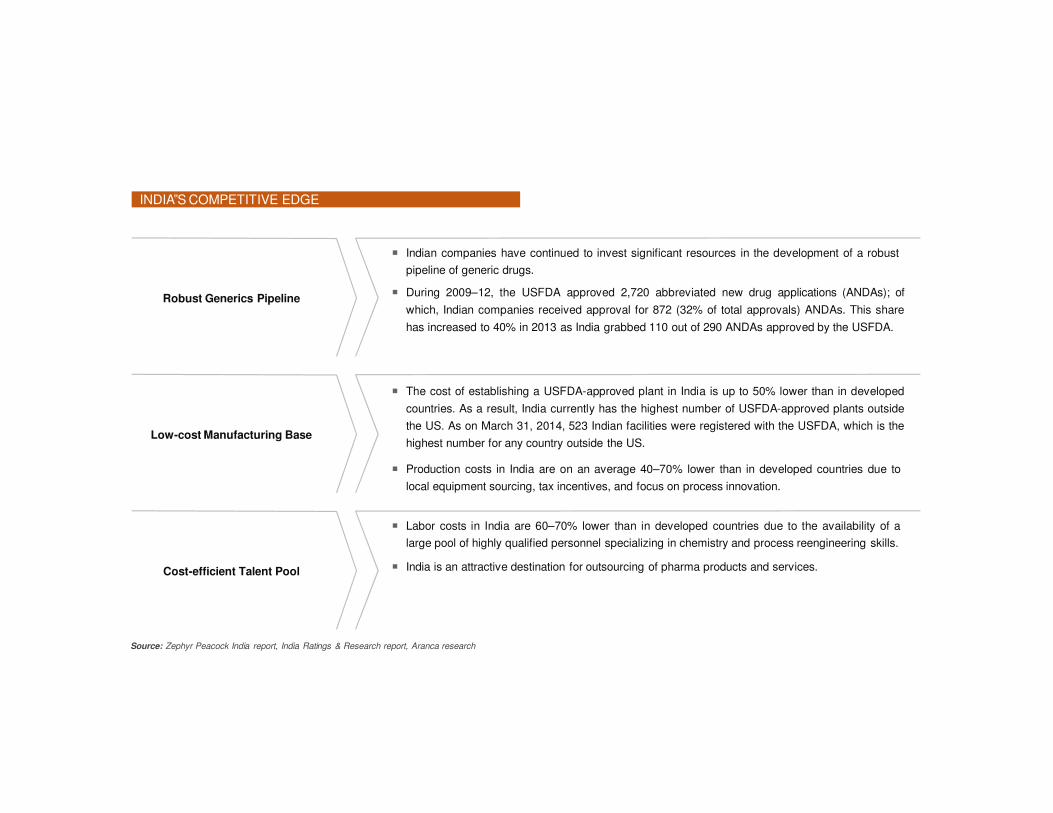

INDIA‟S COMPETITIVE EDGE

Source: Zephyr Peacock India report, India Ratings & Research report, Aranca research

Robust generics pipeline, low cost production, and cost-efficient labor give India‟s

pharma sector a leading edge over peers

Robust Generics Pipeline

� Indian companies have continued to invest significant resources in the development of a robust

pipeline of generic drugs.

� During 2009–12, the USFDA approved 2,720 abbreviated new drug applications (ANDAs); of

which, Indian companies received approval for 872 (32% of total approvals) ANDAs. This share

has increased to 40% in 2013 as India grabbed 110 out of 290 ANDAs approved by the USFDA.

Low-cost Manufacturing Base

� The cost of establishing a USFDA-approved plant in India is up to 50% lower than in developed

countries. As a result, India currently has the highest number of USFDA-approved plants outside

the US. As on March 31, 2014, 523 Indian facilities were registered with the USFDA, which is the

highest number for any country outside the US.

� Production costs in India are on an average 40–70% lower than in developed countries due to

local equipment sourcing, tax incentives, and focus on process innovation.

Cost-efficient Talent Pool

� Labor costs in India are 60–70% lower than in developed countries due to the availability of a

large pool of highly qualified personnel specializing in chemistry and process reengineering skills.

� India is an attractive destination for outsourcing of pharma products and services.

Source: Express Pharma, Aranca research

Rural India

Exports

US

Contract research and manufacturing

services (CRAMS)

Generics

� Generic opportunities in the US would

continue to drive revenue growth for the

Indian pharma companies. This would be

an outcome of:

• sizeable generic opportunity (drugs with

brand value of USD80 billion are expected to

face generic competition) over 2013–15.

• strong product pipeline of pending

ANDAs, with high increasing proportion of

complex generics.

• market share improvement given the

relatively small base (share of leading Indian

companies is less than 10% in the US

generics market).

� Indian pharma companies havecapitalized on exports in regulated

and semi-regulated markets

� Currently India is the third-largestexporter of APIs.

� Indian pharma exports are expectedto grow and developed markets likethe US and Europe would act as the

growth drivers.

� The CRAMS industry is estimated to

generate USD850 millionannually.

� A large number of specialty hospitals with

state-of-the-art facilities, large English

speaking population and rich talent

pool, diverse population and gene

pool, and increasing number of chronic

diseases are expected to boost the

CRAMS industry.

� Pharma companies are shifting focus on rural

markets purely to ramp up volumes.

� Although urban markets are more lucrative and

would continue to be the focus for the

sector, untapped potential of Indian rural

markets is now seen as the next volume driver.

� Generics is opening up a stupendous

opportunity globally.

� The global generic spending is

estimated to increase to USD400–

430 billion by 2016 from USD242

billion in 2011, mainly due to patent

expiries and government efforts to

control healthcare costs across the

world.

� India is expected to become one of

the top three generic drug makers in

the world by 2020.

AttractiveOpportunities

Contract research and manufacturing services, exports, generics, rural India, and the

US market represent lucrative growth opportunities for Indian pharma sector