analyisis of scoring in peer-to- peer lending...peer-to-peer-lending (also known as person-to-person...

TRANSCRIPT

ANALYISIS OF SCORING IN PEER-TO-

PEER LENDING DETERMINANTS OF LOAN DEFAULT

Aantal woorden/ Word count: 12.659

Davy Lust Stamnummer/ Student number : 01201013

Promotor/ Supervisor: Prof. dr. Rudi Vander Vennet

Masterproef voorgedragen tot het bekomen van de graad van:

Master’s Dissertation submitted to obtain the degree of:

Master of Science in Business Engineering

Academiejaar/ Academic year: 2016 - 2017

ANALYISIS OF SCORING IN PEER-TO-

PEER LENDING DETERMINANTS OF LOAN DEFAULT

Aantal woorden/ Word count: 12.659

Davy Lust Stamnummer/ Student number : 01201013

Promotor/ Supervisor: Prof. dr. Rudi Vander Vennet

Masterproef voorgedragen tot het bekomen van de graad van:

Master’s Dissertation submitted to obtain the degree of:

Master of Science in Business Engineering

Academiejaar/ Academic year: 2016 - 2017

VERTROUWELIJKHEIDSCLAUSULE/ CONFIDENTIALITY AGREEMENT

PERMISSION

Ondergetekende verklaart dat de inhoud van deze masterproef mag geraadpleegd en/of

gereproduceerd worden, mits bronvermelding.

I declare that the content of this Master’s Dissertation may be consulted and/or reproduced,

provided that the source is referenced.

Naam student/name student:

Davy Lust

Handtekening/signature

II

Dutch summary

Deze thesis is gericht op het bepalen van de kredietwaardigheid van een ontlener in de peer-

to-peer-leningenmarkt. Hierbij wordt in de eerste plaats aandacht besteed aan het bepalen van

de voornaamste determinanten van een ‘loan default’, of de situatie waarbij de ontlener niet

meer aan zijn financiële verplichtingen kan voldoen. Om dit te doen, maken we gebruik van

een dataset van het grootste Amerikaanse P2P-Lending platform, namelijk Lending Club.

Hierin zijn alle gegevens met betrekking tot de op het platform uitgegeven leningen terug te

vinden. Aan de hand van deze dataset stellen we een statistisch model op, dat de status van de

lening (default of niet) op het eind van de looptijd relateert aan de verschillende gegevens met

betrekking tot de ontlener, zoals bijvoorbeeld zijn inkomen, huidige schulden en

betalingsverleden. Op die manier kan worden vastgesteld welke variabelen een invloed

uitoefenen op het zich al dan niet voordoen van een loan default, en hoe deze variabelen aan

deze waarschijnlijkheid zijn gerelateerd.

De thesis vangt aan met een beschrijving van het concept ‘peer-to-peer lending’, waarbij ook

de voor- en nadelen voor zowel de ontlener als de investeerder worden besproken. Vervolgens

wordt de huidige situatie op de Europese, Amerikaanse en Aziatische P2P-Lending markt

besproken, en wordt er dieper ingegaan op hoe ‘credit scoring’ in deze financiële markten

doorgaans in z’n werk gaat.

De paper gaat verder met het beschrijven van de gebruikte data, en hoe deze data is verwerkt

om in het statistisch model opgenomen te kunnen worden. Hierna wordt dieper ingegaan op

het toegepaste statistische model, meer bepaald het logit model, de karakteristieken van dit

model, en welke invloed dit heeft op onze analyse.

Ten slotte worden de resultaten van het onderzoek weergegeven. Deze resultaten worden

vergeleken met de huidige literatuur rond ‘credit scoring’, alsook met gelijkaardige studies, om

zinvolle conclusies te kunnen trekken. Verder worden er voor elk van de bevindingen

economisch gerelateerde verklaringen gezocht.

III

Foreword

This master’s dissertation serves as the conclusion of five years of intensive academic and

personal development, and is the final stepping stone towards a promising future as a graduate

in Business Engineering.

I would like to take this opportunity to first of all thank my parents for their continuous

support, both mentally and financially, during this important period in my life. Secondly, I

want to thank prof. dr. Rudi Vander Vennet, for granting me the opportunity to work on this

fascinating and challenging topic, as well as Thomas Present, for his excellent guidance during

the development of this thesis. Finally, I want to express my heartfelt gratitude towards my

girlfriend, for her everlasting motivation and continuous belief in me.

IV

Table of content

Dutch summary ......................................................................................................................... II

Foreword .................................................................................................................................. III

Table of content ........................................................................................................................ IV

List of used abbreviations ........................................................................................................ VI

List of Figures and Tables ....................................................................................................... VII

1 Introduction ......................................................................................................................... 1

2 Theoretical Background ...................................................................................................... 2

2.1 What is Peer-To-Peer-Lending? .................................................................................. 2

2.2 Advantages of P2P-Lending ........................................................................................ 2

2.2.1 Advantages for the lender ........................................................................................ 3

2.2.2 Advantages for the borrower ................................................................................... 3

2.3 Disadvantages of P2P-Lending ................................................................................... 4

2.4 Market overview .......................................................................................................... 5

2.4.1 American market - USA ........................................................................................... 5

2.4.2 Asian market ............................................................................................................ 6

2.4.3 European market ..................................................................................................... 6

2.5 Credit Scoring .............................................................................................................. 7

2.5.1 Credit Scoring in general ......................................................................................... 7

2.5.2 Credit Scoring in P2P-Lending ................................................................................ 8

3 Data Description ............................................................................................................... 10

3.1 Data set and variables ................................................................................................ 10

3.1.1 Dependent variable .................................................................................................12

3.1.2 Predictor variables ..................................................................................................12

3.2 Descriptive statistics and correlation matrix ............................................................. 15

4 Econometrical Methodology .............................................................................................. 17

4.1 Model selection ........................................................................................................... 17

4.2 Model characteristics ................................................................................................. 18

V

4.2.1 Goodness of Fit .......................................................................................................19

4.2.2 Model significance ................................................................................................. 20

4.2.3 Significance of variables ........................................................................................ 20

4.2.4 Coefficient interpretation .......................................................................................21

5 Specification Adjustments ................................................................................................ 22

5.1 Employment length ................................................................................................... 22

5.2 Open Accounts & Total Accounts .............................................................................. 23

5.3 Public records & Months since last record ................................................................ 23

6 Empirical Results .............................................................................................................. 26

6.1 Non-significant variables .......................................................................................... 26

6.2 Significant variables .................................................................................................. 28

7 Conclusion ........................................................................................................................ 33

8 Further Research .............................................................................................................. 34

References ................................................................................................................................... I

Appendices ............................................................................................................................... IV

VI

List of used abbreviations

Abbreviation

Meaning

P2P-Lending Peer-To-Peer Lending

EU European Union

USA United States of America

UK United Kingdom

SME Small and Medium-sized Enterprises

FICO Fair Isaac Corporation

DTI Debt-To-Income

LC Lending Club

LPM Linear Probability Model

MLE Maximum Likelihood Estimation

LR Likelihood Ratio

OLS Ordinary Least Squares

VII

List of Figures and Tables

Figure 1: FICO-score Components ............................................................................................. 8

Figure 2: VantageScore 3.0 Influences ...................................................................................... 9

Table 1: Model Variables and Description ................................................................................ 11

Table 2: Descriptive statistics of numerical variables ............................................................... 15

Table 3: Correlation matrix of numerical variables ..................................................................16

Table 4: Regression results initial model - coefficients and odds ratios...................................19

Figure 3: Regression coefficients employment length, including linear trendline .................. 22

Table 5: Regression results Final Model .................................................................................. 24

Table 6: Regression coefficients for different specifications ................................................... 25

1

1 Introduction

In today’s ever changing, global society where individualism and self-interest are frowned

upon, and the prosperity of the community and the globe is becoming a core value in the policy

of the future, we can observe the emergence of all kinds of social initiatives. This is also the

case in the financial market, where actors often happily exchange the lack of connectedness or

the institutional and authoritarian structures of mainstream financial institutions for more

social, transparent and relational alternatives (Hulme & Wright, 2006). The emergence of

social lending is a clear example of this current trend.

The main part of this paper aims at analysing the scoring of loans in the peer-to-peer lending

market, based on data provided by Lending Club. This data is used to develop a model relating

the probability of default of borrowers to personal information provided during the loan

application, in order to define the main determinants of loan default in the P2P-Lending

market.

In the first part of this paper, we shortly introduce the concept of P2P-Lending, its

characteristics, advantages and disadvantages compared to traditional investment or

borrowing opportunities, and the influences on the financial market. This allows us to

determine the need for adequate credit scoring in social lending. We further describe the

emergence of P2P-Lending in the financial market, followed by an overview of the American,

Asian and European P2P-Lending markets.

The paper continues with a description and interpretation of the data used in our analysis, and

how this data will be incorporated into our model. We further describe the econometrical

methodology, as well as its characteristics and implications on the use and interpretation of

our model.

Subsequently, the empirical results of this research are described and compared with the

findings in current literature and similar studies on credit scoring in P2P-Lending, in order to

draw meaningful conclusions. Finally, these conclusions, as well as the rest of this paper, are

summarized.

2

2 Theoretical Background

2.1 What is Peer-To-Peer-Lending?

Peer-To-Peer-Lending (also known as person-to-person lending, social lending or P2P-

Lending) is a type of consumer lending where one individual lends money to another

individual, without the intervention of a financial institution acting as an intermediary

(Investopedia, n.d.). Consumer lending generally consists of loans such as debt consolidation

and refinancing, medical loans, auto loans and loans for home improvements or major

purchases (Mateeschu, 2015). More recent trends show that the P2P-Lending market has

broadened in terms of loan types, covering not only consumer loans, but other types of loans

such as small business loans, student loans and real estate loans as well. The P2P-Lending

market generally consists of online marketplaces or platforms (Mateeschu, 2015), acting as

facilitators for both parties in the transaction (Bajpai, 2015). However, it needs to be noted

that technically speaking, the act where one individual lends money to another individual

without the use of an online marketplace or platform can be described as P2P-Lending as well.

In P2P-Lending, both parties often don’t know each other and have no direct relationship

(Renton, 2012). The main reason these individuals engage in the financial transaction with

each other is their matching preferences in terms of the loan characteristics related to the

lending or borrowing of an amount of money. The role of the lending platform in this situation

is limited to the following tasks: (1) authenticating the participants, (2) managing the money

movement and loan repayment, and (3) providing the users of the platform with detailed

reports (Emekter, Tu, Jirasakuldechc, & Lu, 2015). Next to this, the platform can offer certain

services in case of a default.

Loans in the P2P-Lending market are unsecured, which means that there is no collateral to

support the loan in case of a default, and consequently, the security of the loan only depends

on the creditworthiness of the borrower. (Investopedia, n.d.). This implies that the risk for the

investor is often far greater than in the case where he deposits his capital on a bank savings

account, due to the fact that, in most cases, these accounts are protected by a deposit guarantee

scheme in case of default of the financial institution (Directive 2014/49/EU).

2.2 Advantages of P2P-Lending

The reason why P2P-Lending exists, is because it “provides an alternative and more efficient

lending model compared to mainstream financial institutions” acting as an intermediary

(Mateeschu, 2015). In what follows, these advantages are described for both the lender and the

borrower.

3

2.2.1 Advantages for the lender

The lender (or investor) as a first party in the P2P-Lending market has some clear advantages

compared to the traditional investment options provided by mainstream financial institutions.

Firstly, by disintermediation, or cutting out the middle man (in this case the financial

institution), the investors can become a higher interest rate as a return on their investment

(Renton, 2012) & (Mateeschu, 2015). This is due to several reasons. The first reason is that

P2P-Lending takes place online. Therefore, there are no operating costs with respect to

physical locations, as opposed to the traditional financial institutions which most of the time

operate mainly according to a brick-and-mortar business model. The second reason is that

online P2P-Lending platforms often operate in a more efficient and faster way in terms of the

loan application process. This is due to the fact that these platforms operate online, avoiding

slow paperwork and a delaying bureaucratic policy.

A second advantage is that P2P-Lending platforms work in a transparent way (Mateeschu,

2015). Most of the platforms provide their users with all sort of historical and statistical data,

allowing them to conduct their own analysis on the investment opportunities. This gives

investors more authority over their investments, an enables them to gain a better

understanding of what they invest in and what actually happens with their money.

Thirdly, P2P-Lending provides alternative opportunities for the investors to diversify their

investment portfolio and thus reduce the overall risk of their investments (Renton, 2012) &

(Rind, 2016).

Fourthly, the investment process on P2P-Lending platforms is generally much easier, quicker,

and more approachable for individual investors compared to that of mainstream financial

institutions (Rind, 2016). It is easy to create an online investment account and initial

investments often have a very low minimum investment requirement.

Finally, because online P2P-Lending companies use more credit variables than the mainstream

financial institutions when assessing the credit risk of a borrower, this credit risk is claimed to

be presented more accurately in P2P-Lending (Mateeschu, 2015). This benefits the investors

due to the fact that this enables them to base their investment decision on more truthful

information.

2.2.2 Advantages for the borrower

Next to the advantages for the lender, the borrower as well has some clear incentives to enter

the P2P-Lending market.

First of all, the biggest advantage for the borrower is the lower cost of credit compared to the

cost associated with the borrowing options at mainstream financial institutions or credit card

companies (Renton, 2012), (Rind, 2016) & (Mateeschu, 2015). This is mainly due to the same

reasons the investors can obtain a higher rate of return on their investment, namely lower

operating costs and a more efficient processing procedure.

4

A second big advantage for the borrowers is that obtaining a loan is less difficult in the P2P-

Lending market, compared to the financial institutions (Renton, 2012), (Rind, 2016) &

(Mateeschu, 2015). This has several reasons. Firstly, financial institutions are relatively strict

in the loans they grant. Due to the more stringent regulations resulting from the financial crisis,

banks are even more restricted in how much risk they can bear, and this has impacted their

loan granting behaviour over the last couple of years (Finger, 2013). Secondly, financial

institutions often require collateral when granting a loan. A lot of the borrowers are not able to

provide the necessary collateral to get their loan request approved. In the P2P-Lending market,

loans are unsecured, which means they are not backed up by collateral. This makes it easier for

some borrowers to get approval for their loan request (Renton, 2012) & (Rind, 2016).

A third and final advantage is the fact that applying for a loan in the P2P-Lending market does

not affect the credit score of the inquirer. This is because a credit application in the P2P-

Lending market counts as a so called “soft inquiry”, which means the application does not

negatively impact the borrower’s credit score (Woodruff, 2014).

2.3 Disadvantages of P2P-Lending

P2P-Lending doesn’t only have advantages. There are also some disadvantages compared to

the lending or investment options provided by traditional financial institutions.

Firstly, for borrowers with a low credit score, interest rates are often very high (25%-35%),

resulting in a high cost of lending (Rind, 2016). This makes it harder to keep fulfilling

repayment obligations, which may damage the credit score even more in case of missed

payments or loan defaults.

Secondly, unlike in the case where an individual invests his capital in a bank savings account,

the investment of investors in P2P-Lending is definitive, and can’t be reimbursed before the

loan expires.

Thirdly, the loans in a P2P-Lending market are unsecured, and don’t have a deposit insurance,

in contrast to deposits made with most financial institutions (Wright, 2015). Therefore,

inability of the lender to fulfil his payment obligations or a loan default has the effect that the

investor completely loses his investment and incomplete interest payments.

Fourthly, the concept of information asymmetry, or the situation where the parties engaging

in an economic transaction do not possess equal material knowledge on each other or the

transaction details (Investopedia, n.d.), is heavily present in the P2P-Lending market (Lin,

Prabhala, & Viswanathan, 2013). Although some information on the reasons of the borrower

to apply for a loan in the P2P-Lending market is presented to the investors, in most cases this

information is incomplete. This may result in adverse selection, or the situation where one of

the parties engages in an undesired transaction unknowingly, due to this information

asymmetry (Nickolas, 2015). Due to the lack of information on some aspects, combined with

possible wrong or deceiving information (for example the real reason as to why the lender

5

needs money), investors can be misled and invest in a loan request they would normally not

invest in if they were in possession of truthful information (Berger & Gleisner, 2009). Next to

this, the information asymmetry could lead to moral hazard, or the situation where the

borrower changes his behaviour or intentions after the deal has been made, adding risk that

was previously not present or known by the other party. Therefore, investors might invest in

loan request that can possibly harm their investment portfolio in terms of diversification or

desired level of risk.

These disadvantages, and especially the information asymmetry and its consequences, make it

clear that adequate risk evaluation is a crucial but challenging element in the P2P-Lending

market. Individual investors often lack the knowledge necessary to appropriately evaluate the

risk of investing in loans offered on P2P-Lending platforms. This paper therefore tries to

discover signals of possible loan default by identifying its main determinants based on

historical data provided by Lending Club.

2.4 Market overview

The following section first describes the emergence of P2P-Lending in the financial sector,

followed by an overview of the current situation in the American, European and Asian P2P-

Lending market.

The first online P2P-Lending platform, Zopa, was founded in 2004 and launched in 2005 in

the UK. The founders based their company strategy on one simple problem: borrowers were

being charged high borrowing rates and investors were receiving low returns on their

investments (Zopa, 2016). This problem could, by their believe, easily be solved by matching

borrowers and investors directly through an online platform, and like that, Zopa was founded.

Since then, over 100 platforms have risen and fallen in the UK alone (Gurney, 2017), and many

more all over the world adopted the same business idea and entered the peer-to-peer lending

market.

2.4.1 American market - USA

The American peer-to-peer lending market is currently dominated by three players, Lending

Club, SoFi and Prosper, with Lending Club, founded by Renaud Laplanche in 2007, being the

market leader. Lending Club reported at the end of 2016 that the company has funded over

24.5 billion dollars in loans since their launch in 2007, with close to 2 billion dollars in the last

quarter of 2016 alone (LendingClub Corporation, 2017). Prosper on the other hand reports to

have funded over 9 billion dollars in loans (Prosper Marketplace, Inc, 2017), where Sofi claims

to have funded loans for a value of over 18 billion dollars (Social Finance, Inc, 2017). Next to

these three big players, other P2P-Lending platforms are active in the American market,

including Peerform, founded in 2010 by Wall Street executives, Upstart, founded in 2012 by

6

ex-Googlers, and Funding Circle, a company founded in the UK in 2010 with an exclusive focus

on SME’s.

2.4.2 Asian market

The P2P-Lending market in Asia is still in its infancy, but a number of start-ups have emerged,

being active in different regions in the continent (Fintechnews Singapore, 2016). According to

Fintech News, a news outlet focusing on Digital Finance, the following companies are among

the top players in the Asian P2P-Lending market. Crowdo, a Malaysian company founded in

2013, offers various crowdfunding solutions. Funding Societies, an Indonesian company

founded in 2015 and active in Indonesia and Singapore, connects smaller businesses with both

institutional and individual investors. MoolahSense, a Singaporean P2P-Lending platform

founded in 2013, brings investors and local SME’s together on their online platform. WeLab

Holdings, a company founded in Hong Kong in 2013, is the owner of WeLend.hk, an online

lending platform in Hong Kong, and Wolaidai, one of the largest mobile lending platforms in

China. Another big player in China is CreditEase, a P2P-Lending and microfinance platform

founded in 2006, aimed at democratizing credit in China. Next to this, the company is the

owner of the online lending platform Yirendai. In the Japanese P2P-Lending market, Maneo

takes the place of the largest P2P-Lending platform, allowing SME’s to receive funding from

investors. Crowdcredit, another Japanese company launched in 2014, offers the ability to lend

money to SME’s and individuals in countries all over the world, including Estonia, Spain, Italy,

Finland, Cameroon, and Peru.

2.4.3 European market

According to Fintech News, more than 84% of the European P2P-Lending activity is

concentrated in the UK (Fintechnews Switzerland, 2016). Evelyn Bidenko, a finance coach and

mentor with more than 12 years of experience working in the financial industry in London,

states that this market is dominated by three players: Zopa, RateSetter and Funding Circle.

Zopa, as stated above, was the first online P2P-Lending platform to ever have launched. Since

its launch in 2005, it has lent more than 2.25 billion British pounds (equivalent to

approximately 2.9 billion dollars or 2.65 billion euros) to consumers in the UK. RateSetter,

founded in 2010, claims to be the biggest P2P-Lending platform in the UK, and has recorded

over 1.8 billion British pound (approximately 2.3 billion dollars or 2.1 billion euros). The

company states that thanks to their Provision Fund and 100% track record, investors haven’t

lost a single penny. Funding Circle, founded in 2010, focuses on small businesses instead of

individuals, and states to have lent to more than 23 700 businesses, providing close to 2.25

billion British pounds to date.

In other countries in Europe, the P2P-Lending market is far less developed. According to

Frédéric Dujeux, co-founder of the Belgian fintech company Mozenno founded in December

7

2015, this is due to the European Prospectus Law that implies that individuals are prohibited

to raise funds publicly (Dujeux, 2017). This law makes it very difficult for start-ups to set up a

P2P-Lending platform. Nevertheless, some companies have managed to set up a platform and

stay within the laws of their country. In Germany, a company named Auxmoney, is active on

the P2P-Lending market since 2006, and has a user base of over 2.1 million users. Younited

Credit, formerly known as Prét d’Union, is a France fintech company founded in 2009, and

operates the biggest P2P-Lending platform in France. To date, it has funded close to 60 000

loans for a total amount of over 433 million euros, and the company plans to expand to other

countries as well.

2.5 Credit Scoring

2.5.1 Credit Scoring in general

Credit scoring is the act of statistically determining and assigning a score or a grade to an

individual, that represents the creditworthiness of that individual (Investopedia, n.d.).

Subsequently, the score is equivalent with the probability that the individual fulfils his financial

obligations, and per definition not defaults on his payments.

Credit scoring is a widely used technique in almost every financial institution. However, there

is no standardized way of calculating a credit score. Nevertheless, there are a few well-

developed techniques that have gained popularity and are seen as standards in the credit

scoring industry.

Probably the most famous scoring technique is the one developed by the Fair Isaac

Corporation, known as the FICO-score. According to the company, the score is used by 90% of

the lenders. The FICO scoring technique was invented in 1989, and adopted in 1991 by the

three biggest U.S. credit reporting agencies: Equifax, TransUnion and Experian (Fair Isaac

Corporation, 2017). However, each credit reporting agency uses a different version of the

FICO-score, accommodating for the structural differences in the databases of the agencies

(Fair Isaac Corporation, 2017). Due to this difference, it is rather difficult to compare the scores

reported by the agencies.

The FICO-score ranges from 300 to 850, and although the exact calculation of the score is a

well-kept company secret, there is some information on the type of factors that influence the

score, as illustrated by Figure 1. The payment history of the borrower plays the most

important role in calculating the score, with an estimated weight of approximately 35%. The

amount of debt contributes approximately 30% to the score calculation, and the length of the

credit history determines on average 15% of the score. The final two components, new credit

and the credit mix, each have a weight of approximately 10% in the calculation of the score.

8

Figure 1: FICO-score Components

Source: Website FICO

In reaction to the dominant market position of the FICO-score, as well as the inability to

compare their scores with one another, the three previously mentioned U.S. credit reporting

agencies have developed their own credit rating score, the VantageScore, launched in 2006.

The latest version of the score, VantageScore 3.0, released in 2013, uses the same scale as the

FICO-score, ranging from 300 to 850. The factors that influence the score are similar to those

of the FICO-score (VantageScore Solutions, LLC, 2017). From Figure 2 we can learn that

payment history has the biggest impact on your score, followed by the age and type of your

credit, and the percentage of your total credit limit you use. Your balance to debt ratio

moderately influences your VantageScore credit score, and the factors ‘available credit’ and

‘recent credit behaviour and inquiries’ are the least influential when it comes to determining

your credit score according to the VantageScore credit scoring model.

2.5.2 Credit Scoring in P2P-Lending

Credit scoring in the P2P-Lending market is very similar to how mainstream financial

institutions conduct their credit scoring. Lending Club uses the self-reported FICO-score of the

borrower to conduct an initial screening and provide an estimate of the borrowing interest rate.

When the borrower decides to apply for a loan, Lending Club gathers all the information it

deems relevant to truthfully assess the creditworthiness of the borrower. In most cases, critical

information such as yearly reported income is verified by Lending Club before the loan is

approved or declined. An approved loan will be assigned a loan grade ranging from A to G,

9

each of which is subdivided into 5 subgrades, ranging from 1 to 5. Each subgrade corresponds

to an interest rate, where current macroeconomic factors such as the current risk-free rate are

taken into account as well.

Other P2P-Lending platforms such as Zopa and Prosper conduct their credit scoring process

in a similar way, basing their scoring on the information provided by credit rating agencies

such as Equifax, in combination with their own analysis based on provided and self-gathered

information on the borrower.

Figure 2: VantageScore 3.0 Influences

Source: Website VantageScore

10

3 Data Description

3.1 Data set and variables

The goal of this paper is to develop a model that relates the probability of default of a borrower

to certain borrower characteristics, based on the information provided during the loan

application. This enables us to identify the main determinants of loan default in the P2P-

Lending market. We define a defaulted loan as a loan on which the payments are late for more

than 120 days.

To estimate our model, we use a data set provided by Lending Club, which can be found and

downloaded on their website1. The data set contains all the information gathered by Lending

Club during the loan application process, as well as during the maturity of the loan. To develop

our model, we only use the information provided and gathered during the loan application

process. The dependant variable, however, will be the loan status at the end of maturity.

The Lending Club offers loans with a maturity of 36 months and 60 months. For consistency

purposes, we will focus on loans with a maturity of 36 months, and only include loans for which

the maturity has ended. This gives us a sample of 175037 observations (after corrections, see

following sections), consisting of loans initiated between June 2007 and December 2013.

The data set contains for each observation 115 variables, of which the full list can be found in

Appendix 1. However, a big part of these variables can’t be used in our model, due to several

reasons. A first reason is that several variables are introduced during the period the lending

platform was operational and improving, which results in the fact that the early loans have no

information concerning these variables. A second reason is that some variables gather non-

standardized, user-generated info. This is for example the case for the variables ‘job title’ and

‘loan description’. As a result, these variables can’t be included in a statistical model. A third

reason is that some variables are based on information gathered during the duration of the

loan. Our model tries to relate loan default to borrower characteristics based on the

information gathered during the loan application process, and consequently, variables that fall

under the category described above can’t be included in our model. A fourth and final reason

that limits us in the use of the available variables is the fact that some variables in the data set

are variables that have been developed by Lending Club, based on the information the loan

applicant has provided. A few examples of these variables are the loan grade and subgrade, the

interest rate applicable to the loan, and the monthly installment.

All of the limitations described above result in a new data set, consisting of 16 predictor

variables and one dependant variable, as described in Table 1.

1 https://www.lendingclub.com/info/download-data.action

11

Variable Description

Dependent variable

Loan Status Current status of the loan

Predictor variables

Loan Amount The listed amount of the loan applied for by the borrower. If at some point in time, the credit department reduces the loan amount, then it will be reflected in this value.

Employment Length Employment length in years. Possible values are between 0 and 10 where 0 means less than one year and 10 means ten or more years.

Home Ownership The home ownership status provided by the borrower during registration or obtained from the credit report. Our values are: RENT, OWN, MORTGAGE, OTHER

Annual Income The self-reported annual income provided by the borrower during registration.

Debt-to-Income Ratio A ratio calculated using the borrower’s total monthly debt payments on the total debt obligations, excluding mortgage and the requested LC loan, divided by the borrower’s self-reported monthly income.

Delinquencies 2 years The number of 30+ days past-due incidences of delinquency in the borrower's credit file for the past 2 years

Earliest Credit Line The month the borrower's earliest reported credit line was opened

Inquiries last 6 months The number of inquiries in past 6 months (excluding auto and mortgage inquiries)

Months since last delinquency

The number of months since the borrower's last delinquency.

Months since last record

The number of months since the last public record.

Open Accounts The number of open credit lines in the borrower's credit file.

Public Records Number of derogatory public records

Revolving Balance Total credit revolving balance

Revolving Utilization Revolving line utilization rate, or the amount of credit the borrower is using relative to all available revolving credit.

Total Accounts The total number of credit lines currently in the borrower's credit file

Initial Listing Status The initial listing status of the loan. Possible values are – W (whole) , F (fractional)

Table 1: Model Variables and Description

Source: Data Dictionary from Lending Club Statistics webpage

12

3.1.1 Dependent variable

The dependent variable in our model is the status of the loan at the end of maturity. This status

can either be “Fully paid”, which means that all the financial obligations have been fulfilled, or

“Charged off”, meaning that there is no expectation of further payments, and the borrower has

defaulted. We will model this variable as a dummy variable, ‘dummy loan status’, where a value

of 0 indicates a loan status “Fully paid”, and a value of 1 indicates a loan status “Charged off”.

3.1.2 Predictor variables

3.1.2.1 Loan Amount

The variable ‘loan amount’ represents the amount (in US dollar) the borrower applied for in

his loan application, and that has been approved by the credit department of Lending Club.

This is a numerical variable, and will be integrated into the model in this form.

3.1.2.2 Employment Length

The variable ‘employment length’ tells us how many years the borrower is employed in his

current job. The variable ranges from values between 0 and 10, 0 meaning less than one year,

and 10 meaning ten or more years. If there is no value for this variable, or the value is ‘n/a’, the

borrower is unemployed.

To make the interpretation of this variable more meaningful, as well as to allow testing for

multiple relations (linear, exponential, …) between the variable ‘employment length’ and the

dependent variable, we have decided to remodel this variable into 11 dummy variables. These

dummy variables are ‘dummy_<1y’, ‘dummy_1y’, dummy_2y’, … , ‘dummy_9y’,

‘dummy_10+y, where the first dummy variable takes a value of 1 if the borrower is employed

for less than 1 year, and a value of 0 otherwise. The second till tenth dummy variables have a

value of 1 for an employment of 1 till 9 years, respectively, and a value of 0 otherwise. The final

dummy variable, ‘dummy_10+y’, takes a value of 1 if the borrower is employed for 10 or more

years, and a value of 0 otherwise. If all dummy variables have a value of 0, the borrower is

unemployed.

3.1.2.3 Home Ownership

The variable ‘home ownership’ is a qualitative, categorical variable, that takes 5 different values

in the data set, being ‘OWN’, ‘MORTGAGE’, ‘RENT’, ‘NONE’, and ‘OTHER’. The first three

values speak for themselves in terms of meaning, but the values ‘NONE’ and ‘OTHER’ are not

clearly defined. When analysing the observations, we can determine that out of the 175251

observations, 39 have a value ‘NONE’, and 175 have a value ‘OTHER’. For interpretation

purposes, we therefore have decided to omit these observations from the data set.

We again have created dummy variables to transform this qualitative, categorical variable into

a usable form in our model. Two new variables are introduced, ‘dummy home mortgage’ and

13

‘dummy home rent’, taking a value of 1 in the borrower has a mortgage on his home or rents

his home, respectively, and taking a value of 0 otherwise. In the case where both these

dummies take a value of 0, the borrower is the owner of his home.

3.1.2.4 Annual Income

The variable ‘annual income’ is a numerical variable representing the annual income (in dollar)

of the borrower at the time of initiating the loan. No transformation is required to use this

variable in our model.

3.1.2.5 Debt-to-Income Ratio

The variable ‘debt-to-income ratio’ represents, in the words of Lending Club (2017), “a ratio

calculated using the borrower’s total monthly debt payments on the total debt obligations,

excluding mortgage and the requested LC loan, divided by the borrower’s self-reported

monthly income.” This is a numerical variable, defined with an accuracy of two decimals, and

can therefore be integrated into our model without transformation.

3.1.2.6 Delinquency 2 years

The variable ‘delinquency 2 years’ is a numerical variable that represents the amount of

delinquencies reported in the credit file of the borrower for the past 2 years. We define a

delinquency as a payment that is more than 30 days past-due. This numerical variable can be

integrated into our model in this form.

3.1.2.7 Earliest Credit Line

The variable ‘earliest credit line’ is a numerical variable in the form of a date that represents

the month and year in which the borrower has opened his first credit line. Because of the fact

that Stata, the statistical software package used to estimate our model, is capable of correctly

interpreting and using a date variable, no transformation is needed to integrate this variable

into our model.

3.1.2.8 Inquiries last 6 months

The variable ‘inquiries last 6 months’ represents in numerical form the amount of hard

inquiries on the credit report of the borrower during the last 6 months. A hard inquiry is

defined as the situation where a financial institution checks the credit report when it has to

make a lending decision, as a result of a loan application by the borrower (Irby, 2016). This

numerical variable can be integrated into our model without a transformation.

3.1.2.9 Months since last delinquency

The variable ‘months since last delinquency’ represents the number of months since the

borrower had a delinquency for the last time, as reported by his credit history file. A value of 0

means there is no recorded delinquency in the credit file of the borrower. To capture the effect

of having no recorded delinquencies, we introduce an additional dummy variable, labelled

14

‘dummy delinquencies’, which has a value of 1 if there are recorded delinquencies in the credit

file of the borrower, and a value of 0 otherwise.

3.1.2.10 Months since last record

The variable ‘months since last record’ reports the number of months since the last time a

public record was registered in the credit history file of the borrower. A credit report usually

can contain three types of public records, namely (1) bankruptcy filings, (2) tax liens, and (3)

civil judgement (Irby, 2016). Similarly to the previously described variable, a value of 0 means

there are no public records in the credit report of the borrower. We again create an additional

dummy variable, ‘dummy public records’, taking a value of 1 if there are public records in the

credit report, and a value of 0 otherwise.

3.1.2.11 Open Accounts

The numerical variable ‘open accounts’ represents the number of currently open credit lines in

the credit file of the borrower. This variable can be integrated into the model without a

transformation.

3.1.2.12 Public Records

The variable ‘public records’ is a numerical variable that represents the total amount of

derogatory public records in the credit file of the borrower. This variable needs no

transformation to be integrated into our model.

3.1.2.13 Revolving Balance

The variable ‘revolving balance’ is a numerical variable that represents the total credit

revolving balance (in US dollar) over the lifetime of the borrower, as recorded by his credit

history. Revolving balance, or revolving credit, is the amount of credit that goes unpaid at the

end of a billing cycle. This numerical variable can be integrated into our model without a

transformation.

3.1.2.14 Revolving Utilization

The numerical variable ‘revolving utilization’ represents the utilization rate of the total

available credit of the borrower. In other words, this variable is the ratio between the average

monthly credit use to the total available monthly credit, given in a percentage. This variable

can be integrated into our model in this form.

3.1.2.15 Total Accounts

The variable ‘total accounts’ is a numerical variable that represents the total number of credit

lines that are now available to the borrower, or have been available to the borrower in the past,

as currently stated in the credit file. This numerical variable requires no transformations to be

integrated into our model.

15

3.1.2.16 Initial listing status

Finally, the qualitative, categorical variable ‘initial listing status’ represents the listing status

of the loan at the time of approving and listing the loan. The variable can take two values, ‘f’

and ‘w’, where ‘f’ represents a listing status ‘fractional’, and ‘w’ a listing status ‘whole’. A

fractional loan can be funded by multiple investors on the platform whereas a loan with a

listing status ‘whole’ can only be fully funded by one investor. To use the information of this

variable in our model, we introduce a dummy variable, ‘listing status’, which has a value of 1 if

the initial listing status of the loan was ‘fractional’, and a 0 in the case where this status was

‘whole’.

3.2 Descriptive statistics and correlation matrix

In Table 2 we can find for each numerical variable described above some descriptive statistics,

namely the mean, standard deviation, minimum and maximum value.

VARIABLES N Mean Std Dev Min Max

Loan Amount 175,037 11,862 7,202 500 35,000

Employment Length 175,037 5.490 3.644 0 10

Annual Income 175,037 69,423 55,528 1,896 7,141,778

Debt-to-Income Ratio 175,037 16.06 7.604 0 34.99

Delinquencies last 2 years 175,037 0.220 0.675 0 29

Inquiries last 6 months 175,037 0.836 1.147 0 33

Months since last delinquency 175,037 14.66 22.29 0 152

Months since last record 175,037 7.650 25.72 0 129

Open Accounts 175,037 10.53 4.601 1 62

Public Records 175,037 0.101 0.397 0 54

Revolving Balance 175,037 15,012 20,060 0 2,568,995

Revolving Utilization 175,037 0.558 0.245 0 1.404

Total Accounts 175,037 23.45 11.15 1 105

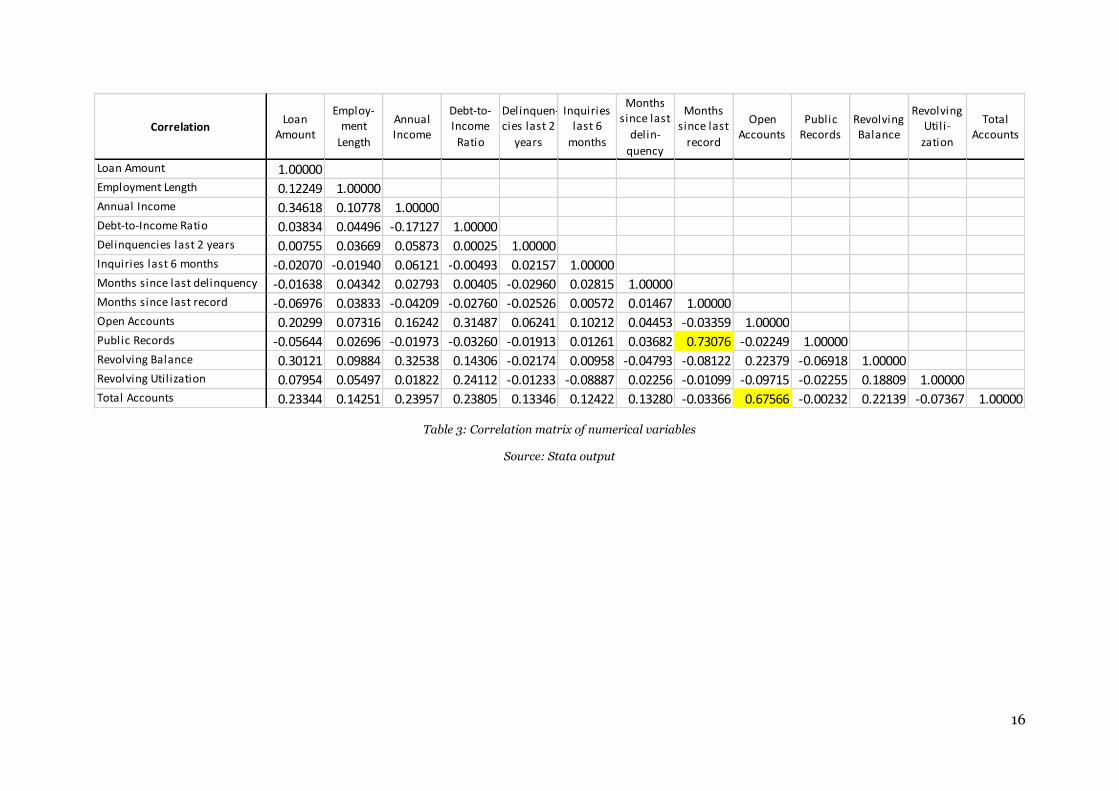

Table 3 represents the correlation matrix for the numerical variables. Variables with a high

correlation can cause some estimation problems. This will be addressed later in this paper.

Table 2: Descriptive statistics of numerical variables

Source: Stata output

16

CorrelationLoan

Amount

Employ-ment

Length

Annual Income

Debt-to-Income

Ratio

Delinquen-cies last 2

years

Inquiries last 6

months

Months since last

delin-

quency

Months since last

record

Open Accounts

Public Records

Revolving Balance

Revolving Util i-

zation

Total Accounts

Loan Amount 1.00000Employment Length 0.12249 1.00000Annual Income 0.34618 0.10778 1.00000Debt-to-Income Ratio 0.03834 0.04496 -0.17127 1.00000Delinquencies last 2 years 0.00755 0.03669 0.05873 0.00025 1.00000Inquiries last 6 months -0.02070 -0.01940 0.06121 -0.00493 0.02157 1.00000Months since last delinquency -0.01638 0.04342 0.02793 0.00405 -0.02960 0.02815 1.00000Months since last record -0.06976 0.03833 -0.04209 -0.02760 -0.02526 0.00572 0.01467 1.00000Open Accounts 0.20299 0.07316 0.16242 0.31487 0.06241 0.10212 0.04453 -0.03359 1.00000Public Records -0.05644 0.02696 -0.01973 -0.03260 -0.01913 0.01261 0.03682 0.73076 -0.02249 1.00000Revolving Balance 0.30121 0.09884 0.32538 0.14306 -0.02174 0.00958 -0.04793 -0.08122 0.22379 -0.06918 1.00000Revolving Util ization 0.07954 0.05497 0.01822 0.24112 -0.01233 -0.08887 0.02256 -0.01099 -0.09715 -0.02255 0.18809 1.00000Total Accounts 0.23344 0.14251 0.23957 0.23805 0.13346 0.12422 0.13280 -0.03366 0.67566 -0.00232 0.22139 -0.07367 1.00000

Table 3: Correlation matrix of numerical variables

Source: Stata output

17

4 Econometrical Methodology

4.1 Model selection

To use our available data and estimate a model relating the probability of default of the loan to

the borrower characteristics, we need to define the model specification and functional form

that best fits this goal and our data. According to Bolton (2009), the first step in this process is

to analyse the dependent variable. In this case, the dependent variable is the loan status at the

end of maturity. This variable can take two values, ‘Fully Paid’ or ‘Charged Off’, and is therefore

by definition a dichotomous or binary dependent variable (Wooldridge, 2002). According to

Wooldridge (2002), the most simple model to estimate and use in this situation is the linear

probability model (LPM), which is basically a multiple linear regression model where the

dependent variable is a binary variable. The model specification is defined by equation 4.1.

𝑃(𝑦 = 1|𝑥) = 𝛽0 + 𝛽1𝑥1 + ⋯ + 𝛽𝑘𝑥𝑘

In this model, the regression coefficient 𝛽𝑗 measures the change in the probability of the

occurrence of the event depicted by the dependent variable, in our case a loan default, for a

change in the predictive variable 𝑥𝑗 of 1 unit, ceteris paribus. The results of this regression can

be found in Appendix 2.

Although this model seems to fit the requirements of our case, there are some limitations that

have to be taken into account. First of all, in this model, the fitted probabilities, or the

probabilities that are a result of filling in variable values based on the observations, can be

greater than 1 and less than 0. Next to this, the partial effect of the predictor variables is

constant (Wooldridge, 2002). Finally, the error terms in the regression usually present

themselves with non-normality and heteroscedasticity, making it difficult to perform truthful

hypothesis tests based on the t-statistics the regression generates (Verbeek, 2012). These three

disadvantages of the model motivate us to explore other options.

Another binary choice model similar to the LPM is the logit model, based on the idea of

applying a transformation G on the linear relation defined by the LPM. This gives us a general

form as depicted by equation 4.2.

𝑃(𝑦 = 1|𝑥) = 𝐺(𝛽0 + 𝛽1𝑥1 + ⋯ + 𝛽𝑘𝑥𝑘)

In a logit model, this transformation G is the logistic transformation, as defined by equation

4.3. This generates a function ranging between 0 and 1 for all real numbers 𝑧 (Wooldridge,

2002).

𝐺(𝑧) = 𝑒𝑧

1 + 𝑒𝑧

(4.1)

(4.2)

(4.3)

18

If we now define 𝜋(𝑥) = 𝑃(𝑦 = 1|𝑥), and 𝑧 = (𝛽0 + 𝛽1𝑥1 + ⋯ + 𝛽𝑘𝑥𝑘), then our model

becomes:

𝜋(𝑥) = 𝑒𝛽0+ 𝛽1𝑥1+⋯+ 𝛽𝑘𝑥𝑘

1 + 𝑒𝛽0+ 𝛽1𝑥1+⋯+ 𝛽𝑘𝑥𝑘

Rearranging this to make the right hand side linear gives us equation 4.5, which is the logit

regression model we will use.

ln (𝜋(𝑥)

1 − 𝜋(𝑥)) = 𝛽0 + 𝛽1𝑥1 + ⋯ + 𝛽𝑘𝑥𝑘

To fit this model, we make use of the Maximum Likelihood Estimation, which is a method to

estimate the regression coefficients of the model by determining the combination of

coefficients or parameters that maximizes the likelihood that these estimated parameters fit

the actual population parameters, based on the observations in the sample (Wooldridge,

2002). This method defines a likelihood function that needs to be optimized iteratively, in

order to obtain the estimated parameters. In practice, we usually work with the log-likelihood

function, as it is more convenient to use (Verbeek, 2012). This log-likelihood function is

defined by equation 4.6, where 𝐹(𝑥′𝑖𝛽) = 𝑃(𝑦𝑖 = 1|𝑥𝑖; 𝛽).

log 𝐿(𝛽) = ∑ 𝑦𝑖log (𝐹(𝑥′𝑖𝛽))

𝑁

𝑖=1

+ ∑(1 − 𝑦𝑖)log (1 − 𝐹(𝑥′𝑖𝛽))

𝑁

𝑖=1

Maximizing this function gives us the estimated parameters of the model.

This model and the corresponding estimation method adequately fit the requirements of our

case. Although other models, like the tobit or probit models, would qualify as well, we decide

to use the logit model, due to the fact that this model is commonly accepted as the standard

model in credit scoring and default prediction.

4.2 Model characteristics

We now use a statistical software package, namely Stata, to estimate this model based on the

dataset we composed. Stata estimates the logit model by executing the MLE method based on

the log-likelihood function, and reports the estimated parameters, as well as some information

with respect to statistical tests. The results can be found in Table 4. The Stata command can

be found in Appendix 3.1.

Before interpreting the results, it’s important to test the characteristics of the model and its

variables.

(4.4)

(4.5)

(4.6)

19

VARIABLES Coeff Std Error

Coeff z p-value Odds Ratio

Std Error OR

Loan Amount 0.0000 0.0000 9.0224 0.000 1.0000 0.0000

Employment Length < 1 year -0.4254 0.0403 -10.5576 0.000 0.6535 0.0263

Employment Length 1 year -0.4722 0.0422 -11.1850 0.000 0.6236 0.0263

Employment Length 2 years -0.4478 0.0397 -11.2851 0.000 0.6390 0.0254

Employment Length 3 years -0.4258 0.0407 -10.4689 0.000 0.6533 0.0266

Employment Length 4 years -0.4471 0.0429 -10.4181 0.000 0.6395 0.0274

Employment Length 5 years -0.4390 0.0412 -10.6594 0.000 0.6447 0.0266

Employment Length 6 years -0.3596 0.0426 -8.4440 0.000 0.6980 0.0297

Employment Length 7 years -0.3590 0.0438 -8.2029 0.000 0.6984 0.0306

Employment Length 8 years -0.3817 0.0465 -8.2153 0.000 0.6827 0.0317

Employment Length 9 years -0.4058 0.0501 -8.0948 0.000 0.6665 0.0334

Employment Length 10+ years -0.3955 0.0342 -11.5521 0.000 0.6734 0.0231

Dummy Home Mortgage -0.1521 0.0274 -5.5406 0.000 0.8589 0.0236

Dummy Home Rent 0.1052 0.0268 3.9247 0.000 1.1109 0.0298

Annual Income 0.0000 0.0000 -21.0859 0.000 1.0000 0.0000

Debt-to-Income Ratio 0.0128 0.0011 11.3438 0.000 1.0129 0.0011

Delinquencies 2 years 0.0557 0.0135 4.1443 0.000 1.0573 0.0142

Earliest Credit Line 0.0000 0.0000 6.9047 0.000 1.0000 0.0000

Inquiries last 6 months 0.2111 0.0059 36.0733 0.000 1.2350 0.0072

Months since last delinquency -0.0005 0.0006 -0.7065 0.480 0.9995 0.0006

Dummy Delinquencies 0.0999 0.0316 3.1591 0.002 1.1051 0.0350

Months since last record 0.0003 0.0010 0.2806 0.779 1.0003 0.0010

Dummy Public Records 0.0844 0.1043 0.8085 0.419 1.0880 0.1135

Open Accounts 0.0248 0.0023 10.8474 0.000 1.0251 0.0023

Public Records 0.0049 0.0326 0.1493 0.881 1.0049 0.0328

Revolving Balance 0.0000 0.0000 -0.5469 0.584 1.0000 0.0000

Revolving Utilization 0.8345 0.0339 24.6008 0.000 2.3037 0.0781

Total Accounts -0.0115 0.0010 -11.0940 0.000 0.9886 0.0010

Listing Status 0.0768 0.0197 3.9060 0.000 1.0798 0.0212

Constant -2.5773 0.0682 -37.7908 0.000 0.0760 0.0052

4.2.1 Goodness of Fit

To estimate the goodness of fit of our model, or how well the model fits the observed data

(Verbeek, 2012), we analyse the pseudo R-squared statistic of the model, which is a statistic

ranging from 0 to 1. There are several ways to calculate the pseudo R-squared of a logit model,

but there is no agreement on which one of them is the preferred one to use.

Table 4: Regression results initial model - coefficients and odds ratios

Source: Stata output

20

The pseudo R-squared of our model, reported by Stata, is 0.0301. Although a single pseudo R-

squared statistic of a logit model can’t be accurately interpreted on its own, this value clearly

indicates that our model performs poorly in its ability to fit the data. This could be the result

of the possibility that the model is incomplete, and that we require other variables to more

accurately predict the probability of default. Unfortunately, we are restricted by our data set,

and therefore, no other variables are available.

However, in logit models, the goodness of fit of the model is relatively unimportant compared

to the statistical and economic significance of the model and its predictor variables

(Wooldridge, 2002). We therefore leave these findings out of account in the remainder of this

analysis, and focus on the estimated regression coefficients and their interpretation.

4.2.2 Model significance

Assessing the significance of a logit model essentially comes down to comparing the full model

to the model where the only predictor variable is a constant, and determining whether the log-

likelihood of the full model is statistically significantly greater than the log-likelihood of the

restricted model. According to the likelihood ratio test, as described by Wooldridge (2002), a

likelihood ratio (LR) test statistic is calculated, as illustrated by equation 4.7.

𝐿𝑅 = 2(ℒ𝑓𝑢𝑙𝑙 − ℒ𝑟𝑒𝑠𝑡𝑟𝑖𝑐𝑡𝑒𝑑)

This test statistic has a chi-square distribution of which the number of degrees of freedom is

equal to the difference between the number of predictor variables in the full model and the

number of predictor variables in the restricted model.

Calculating the LR test statistic of our model gives us a value of 3990.604. The critical chi-

square value with a significance level of 1% and 29 degrees of freedom is approximately 49.59.

The test statistic exceeds this value, and we can therefore conclude that the model is

statistically significant on a significance level of 1%.

4.2.3 Significance of variables

Assessing the significance of the variables in our model can be done by testing whether the

regression coefficient corresponding to each predictor variable is statistically significantly

different from 0. The easiest way to do this is by looking at the p-values of the coefficients. A

p-value represents the strongest significance level on which the null hypothesis of the

coefficient being statistically not significantly different from 0 can be rejected (Wooldridge,

2002). In other words, it represents the strongest significance level on which the coefficient is

significantly different from 0.

Based on the model output in Table 4, we can observe that most of the coefficients are

statistically significantly different from 0, with p-values close to or equal to zero. There are 5

(4.7)

21

coefficients, however, of which the p-value indicates that they are not statistically significantly

different from 0. These coefficients are the ones corresponding to the variables ‘months since

last delinquency’, ‘months since last record’, ‘dummy public records’, ‘public records’ and

‘revolving balance’. The economic implications of these findings will be discussed in a later

section, where the results of this research are analysed.

4.2.4 Coefficient interpretation

The interpretation of the regression coefficients of a logistic regression is rather different from

that of an OLS regression. As can be derived from the model depicted by equation 4.5, a

regression coefficient represents the increase in the logarithmic odds of the occurrence of the

event coded in the dependent variable, in our case a loan default, for an increase of the

predictor variable of 1 unit, all other variables remaining constant (Verbeek, 2012). This

relation is rather difficult to interpret, and we therefore generate odds ratios for each predictor

variable. To do so, we simply raise the mathematical constant e to the power of the coefficient

corresponding to each variable, as illustrated by equation 4.8. This can be done in Stata by

using the ‘logistic’ command, as illustrated in Appendix 3.2. The results have been added to

Table 4.

𝑂𝑅𝑖 = 𝑒𝛽𝑖

In our model, the odds ratio corresponding to a certain predictor variable is the ratio of the

odds that a loan will default to the odds that it will not, for a one-unit increase in the value of

the predictor variable. In other words, it represents the multiplicator that defines the change

in the odds of a loan default for a one-unit increase in the value of the predictor variable.

An odds ratio typically ranges from zero to positive infinity. A value lower than 1 represents a

decrease in the odds of the probability of default, and therefore corresponds to a negative

relation between the dependent variable and the predictor variable. An odds ratio of exactly 1

implies no relation between the dependent variable and the predictor variable. Note that an

odds ratio of 1 corresponds to a regression coefficient of 0, or by definition a statistically

insignificant regression coefficient An odds ratio greater than 1 corresponds to a positive

relation between the dependent variable and the predictor variable.

The odds ratios corresponding to each predictor variable, and their implications in our model,

will be discussed in a following section.

(4.8)

22

5 Specification Adjustments

Before we can correctly interpret the results of our model, some adjustments need to be made

to our initial specification. These adjustments, the reason behind them, and their implications

for our model are discussed in this section.

5.1 Employment length

As previously mentioned, the variable ‘employment length’ has been recoded into 11 dummy

variables, primarily to test for multiple relations between this variable and the probability of

default. The regression coefficients of these dummy variables, including a linear trendline, are

displayed in Figure 3.

At first sight, there seems to be no clear positive or negative relation between the increase or

decrease of employment length of the borrower and his probability of default. The trendline

doesn’t give a definitive answer as well, showing only a marginally positive2 relation. This

initial finding corresponds with the findings in the study conducted by Serrano-Cinca,

Gutiérrez-Nieto & López-Palacios (2015), where no significant relation was found as well. We

can therefore conclude that employment length doesn’t have a significant impact on the

probability of default of the borrower.

2 This positive relation is counter-intuitive, because it indicates that the probability of default is higher when the borrower is employed for a longer time.

Figure 3: Regression coefficients employment length, including linear trendline

Source: Stata output, own calculations

-0.5

-0.45

-0.4

-0.35

-0.3

-0.25

-0.2

-0.15

-0.1

-0.05

0

<1y 1y 2y 3y 4y 5y 6y 7y 8y 9y 10+y

Co

effi

cien

t

Employment Length

Regression coefficients Employment Length

23

However, due to the fact that every regression coefficient is statistically significantly different

from zero, the employment status of the borrower does seem to have an impact. The data points

towards the possibility that a borrower with a job has a significantly lower probability of default

than an unemployed borrower. We can test this by replacing the 11 dummy variables in our

model with a single new dummy variable, ‘employment’, representing whether or not the

borrower is employed. A value of 1 indicates employment, a value of 0 represents

unemployment.

Comparing the new model with the initial model by the use of the LR test will teach us if there

is a statistical difference between these two models. No statistical difference points towards no

loss of information and predictive power of the model, and therefore a valid replacement of

variables.

The LR test statistic, calculated according to equation 4.7, equals 17.82. The critical chi-square

value with a significance level of 1% and 10 degrees of freedom amounts to approximately

23.21. The test statistic doesn’t exceed the critical value, which means the null hypothesis of no

statistical difference between the models can’t be rejected. Our replacement of variables is

therefore valid, and the adjusted specification can be used. The results of this regression can

be found in Table 6, in the column of Model 1.

5.2 Open Accounts & Total Accounts

As can be seen in Table 3, we found a relatively high correlation (0.67566) between the

variables ‘open accounts’ and ‘total accounts’. This high correlation could result in a biased

estimation of the corresponding regression coefficients. We therefore execute the regression

twice, where each of these two variables will be integrated individually. This has given rise to

the results that can be found in Table 6, labelled as Model 2 and Model 3.

Based on these results, we can conclude the following. Both variables remain statistically

significant, and their relation with the dependent variable remains the same as in the initial

model. Only the actual value of the regression coefficients slightly differs from those of the

initial specification, as can be expected. We therefore decide to keep both variables in the

model.

5.3 Public records & Months since last record

Table 3 shows us that the variables ‘public records’ and ‘months since last record’ are highly

correlated as well, with a correlation of 0.73076. We therefore again execute two regressions,

each containing one of the highly correlated variables. The results of these regressions can be

found in Table 6, in the column of Model 4 and Model 5.

24

These results show us that the variable ‘months since last record’ and its corresponding dummy

variable remain statistically not significant, whereas the variable ‘public records’ becomes

significant when integrated separately into our model. We therefore decide to only keep the

significant variable ‘public records’ in our model.

The regression coefficients of each of the models used in this section are summarised in Table

6. Model 1 is the full model, where the dummy variables for employment length have been

replaced with a single dummy variable representing the employment status of the borrower.

This model serves as the basis for the following adaptions. In Model 2, the variable ‘total

accounts’ has been left out, and in Model 3, the same has been done for the variable ‘open

accounts’. In Model 4, the variables ‘months since last record’ and ‘dummy public records’ have

been omitted, and in Model 5, this is the case for the variable ‘public records’.

In conclusion, the final model that will serve as the base for our analysis is the model as

presented in Table 5, where the dummy variable ‘employment’ has been introduced as a

replacement for the dummies of the variable ‘employment length’. Next to this, the variables

‘months since last record’ and ‘dummy public records’ have been omitted due to their high

correlation with ‘public records’ and their statistical insignificance, and the variables ‘months

since last delinquency’ and ‘revolving balance’ have been omitted due to their statistical

insignificance.

VARIABLES Coeff Std Dev z p-value Odds Ratio

Std Dev OR

Loan Amount 0.0000110 1.21e-6 9.0713 0.000 1.0000110 1.21e-6

Employment -0.4142 0.0323 -12.8412 0.000 0.6609 0.0213

Dummy Home Mortgage -0.1475 0.0274 -5.3791 0.000 0.8629 0.0237

Dummy Home Rent 0.1011 0.0267 3.7811 0.000 1.1064 0.0296

Annual Income -0.0000062 2.8e-7 -22.1264 0.000 0.9999938 2.8e-7

Debt-to-Income Ratio 0.0128 0.0011 11.4887 0.000 1.0129 0.0011

Delinquencies 2 years 0.0602 0.0111 5.4421 0.000 1.0620 0.0117

Earliest Credit Line 0.0000216 3.22e-6 6.7201 0.000 1.0000216 3.22e-6

Inquiries last 6 months 0.2104 0.0058 36.0289 0.000 1.2342 0.0072

Dummy Delinquencies 0.0827 0.0164 5.0349 0.000 1.0862 0.0178

Open accounts 0.0243 0.0023 10.7526 0.000 1.0246 0.0023

Public records 0.0622 0.0170 3.6682 0.000 1.0642 0.0180

Revolving utilization 0.8330 0.0332 25.0895 0.000 2.3002 0.0764

Total Accounts -0.0114 0.0010 -11.0754 0.000 0.9887 0.0010

Listing Status 0.0737 0.0196 3.7541 0.000 1.0765 0.0211

Constant -2.5489 0.0675 -37.7650 0.000 0.0782 0.0053

Table 5: Regression results Final Model

Source: Stata output

25

(1) (2) (3) (4) (5)

VARIABLES Model 1 Model 2 Model 3 Model 4 Model 5

Loan Amount 1.12e-05*** 1.07e-05*** 1.15e-05*** 1.11e-05*** 1.12e-05***

(1.22e-06) (1.22e-06) (1.22e-06) (1.22e-06) (1.22e-06)

Employment -0.411*** -0.411*** -0.398*** -0.414*** -0.411***

(0.0323) (0.0323) (0.0322) (0.0323) (0.0323)

Dummy Home Mortgage -0.149*** -0.168*** -0.151*** -0.147*** -0.149***

(0.0274) (0.0274) (0.0274) (0.0274) (0.0274)

Dummy Home Rent 0.100*** 0.105*** 0.104*** 0.101*** 0.100***

(0.0268) (0.0267) (0.0267) (0.0268) (0.0268)

Annual Income -6.13e-06*** -6.64e-06*** -5.99e-06*** -6.14e-06*** -6.13e-06***

(2.91e-07) (2.90e-07) (2.89e-07) (2.91e-07) (2.91e-07)

Debt-to-Income Ratio 0.0130*** 0.0113*** 0.0156*** 0.0129*** 0.0130***

(0.00113) (0.00112) (0.00110) (0.00113) (0.00113)

Delinquencies 2 years 0.0553*** 0.0509*** 0.0561*** 0.0551*** 0.0553***

(0.0134) (0.0134) (0.0134) (0.0134) (0.0134)

Earliest Credit Line 2.18e-05*** 2.98e-05*** 2.54e-05*** 2.13e-05*** 2.18e-05***

(3.27e-06) (3.22e-06) (3.26e-06) (3.26e-06) (3.27e-06)

Inquiries last 6 months 0.210*** 0.206*** 0.211*** 0.210*** 0.210***

(0.00584) (0.00582) (0.00583) (0.00584) (0.00584)

Months since last delinquency -0.000431 -0.000379 -0.000336 -0.000406 -0.000431

(0.000640) (0.000641) (0.000640) (0.000640) (0.000640)

Dummy Delinquencies 0.100*** 0.0702** 0.0876*** 0.0983*** 0.100***

(0.0316) (0.0315) (0.0316) (0.0316) (0.0316)

Months since last record 0.000356 0.00142 0.000881 0.000317

(0.000975) (0.000967) (0.000972) (0.000945)

Dummy public records 0.0816 -0.0245 0.0289 0.0909

(0.104) (0.101) (0.102) (0.0867)

Open accounts 0.0245*** 0.00955*** 0.0245*** 0.0245***

(0.00228) (0.00184) (0.00228) (0.00228)

Public records 0.00527 0.0142 0.0101 0.0617***

(0.0324) (0.0292) (0.0308) (0.0170) Revolving balance -3.15e-07 -2.77e-07 2.98e-07 -4.16e-07 -3.16e-07

(5.87e-07) (5.92e-07) (5.50e-07) (5.91e-07) (5.87e-07)

Revolving utilization 0.838*** 0.854*** 0.773*** 0.838*** 0.838***

(0.0339) (0.0339) (0.0331) (0.0339) (0.0339)

Total Accounts -0.0114*** -0.00494*** -0.0114*** -0.0114***

(0.00103) (0.000827) (0.00103) (0.00103)

Listing Status 0.0753*** 0.0769*** 0.0719*** 0.0739*** 0.0753***

(0.0196) (0.0196) (0.0196) (0.0196) (0.0196)

Constant -2.568*** -2.708*** -2.545*** -2.548*** -2.568***

(0.0678) (0.0670) (0.0679) (0.0675) (0.0678)

Observations 175,037 175,037 175,037 175,037 175,037

Standard errors in parentheses *** p<0.01, ** p<0.05, * p<0.1

Table 6: Regression coefficients for different specifications

Source: Stata output

26

6 Empirical Results

This section analyses the results of the regression by interpreting the regression coefficients

and odds ratios corresponding to the variables incorporated into our model. These results can

be found in Table 5. We compare these findings with those of similar studies and the current

literature on credit scoring in P2P-Lending, and consequently draw conclusions.

As previously described, the model defines a relation between the probability of default of a

loan issued by Lending Club on the one hand, and a set of predictor variables gathered by

Lending Club during the loan application process on the other hand. Therefore, when we talk

about the probability of default, we are referring to the probability of the borrower defaulting

on his loan at Lending Club.

6.1 Non-significant variables

We first take a look at the variables for which we previously found that their regression

coefficients are statistically not significantly different from zero. As mentioned above, these

variables are ‘months since last delinquency’, ‘months since last record’, ‘dummy months since

last record’ and ‘revolving balance’. Note that the variable ‘public records’ has become

statistically significant after the removal of the highly correlated variable ‘months since last

record’ from our model.

Delinquencies

The coefficient of the variable ‘months since last delinquency’ is, according to our model,

statistically not significantly different from zero. This implies that how long ago a borrower

had his last delinquency doesn’t impact his probability of defaulting on his loan at Lending

Club. If we analyse ‘dummy months since last delinquency’, the corresponding dummy variable

we created to capture the effect of the difference between ever having had a delinquency or not,

we can conclude the following. The dummy variable is statistically significantly different from

zero, which implies that whether or not the borrower ever had a delinquency, does impact his

probability of default. The odds ratio of this dummy variable amounts to 1.0862. This points

towards a positive relation between the borrower having a delinquency recorded on his credit

file and the probability of default, and indicates that the odds of default are approximately

8.62% higher if the borrower ever had a delinquency, compared to never having had a

delinquency.

The variable ‘delinquencies 2 years’, representing the amount of delinquencies in the past two

years, has a significant coefficient as well. According to the odds ratio corresponding to this

variable, which is equal to 1.0620, each additional delinquency in the past two years increases

the odds of a default on the loan of the borrower with approximately 6.20%.

27

These findings are in line with what has been found in previous studies. As can be expected,

borrowers who have had delinquencies in the past, are more likely to miss payments or default

on their loan in the future (Nefer, 2010). The Fair Isaac Corporation, developer of the FICO-

score, states that historical payment behaviour determines 35% of a borrower’s credit score

(Fair Isaac Corporation, 2017). Next to this, Serrano-Cinca, Gutiérrez-Nieto and López-

Palacios (2015) also found a positive relation between the amount of delinquencies and the

probability of default, and no statistical relation between the number of months since the

borrower’s last delinquency and his probability of default.

Public records

The next set of variables we will discuss are the variables relating to public records in the credit

file of the borrower. These variables are ‘public records’, ‘months since last record’ and ‘dummy

records’. As previously mentioned, the variables ‘months since last record’ and ‘dummy