an overview of indian pharmaceutical...

TRANSCRIPT

1

AN OVERVIEW OF INDIAN PHARMACEUTICAL

INDUSTRY

The Indian Pharmaceutical industry is in the front rank of India’s science based industries

with wide ranging capabilities in the complex field of drug manufacture and technology.

Pharmaceutical Industry in India is one of the largest and most advanced among the

developing countries. The growth of the pharmaceutical industry in India is quite

phenomenal. Today the Indian Pharmaceutical industry is capable of meeting the country’s

demand for each and every drug. But with the development of pharmaceutical Industry,

pharmaceutical malpractices are also increasing. Pharmaceutical malpractices mean that a

drug company caused injury or death to a consumer by failing to act within the applicable

standard of care. The consumers have been exploited by the manufacturers and the traders.

The traders are dominating the market and the consumers are not united. Therefore, in such a

situation traders do not hesitate to indulge in various undesirable and immoral trade practices.

It is an undeniable fact that access to health care is one of the most basic needs and an

inviolable right of every human being. Today Pharmaceutical industry is forced to work in

an environment of stiff competition. The complexion of the pharmaceutical sector has thus

undergone a significant change in terms of trade and marketing practices. Pharmaceutical

companies found themselves in a market where the customer has more options than ever

before and firms while competing with one another adopt restrictive or unfair practices,

which are derogatory to the core of a competitive market. In the pursuit of profit making,

business failed to discharge social responsibilities of maintaining and charging fair prices,

supplying quality and standard goods and providing other services to the customer.

Adulterated stuffs and eatables poisoned by industrial pollution found their way into the

markets1.

Globally, the drug sector has been known for practices thwarting the spirit of

competition and regulation. Anti competitive system include price fixing abuse of

dominance, collusive agreements and tied selling2. Even practices such as kickbacks to

doctors and pharmacists may be deemed as unfair trade as they result in depriving patients of

the best possible prices. The primary effect of anticompetitive practices in the health sector

is that medicines and services are rendered costlier. Hospitals are an important part of the

2

health delivery system. But they are also known to exploit consumers, and enter into

agreements with drug manufacturers. Some drug companies offer incentives to doctors to

prescribe off label. All types of fraudulent products, unsafe or defective products, even

spurious drugs without proper regard for consumer health were pumped into the market.

Historically, Major pharmaceutical companies marketed their drug offering to patient

gatekeepers – physicians and health care professionals since the Food Drug and Alcohol

Administration (FDA) of USA prohibited advertising prescription drugs to consumers.

Companies used sales representatives to ‘detail’ doctors by educating them and promoting

prescription drugs. The companies also provided drug samples to the gatekeepers to

indirectly gain exposure to and trial by patients. In 1985 FDA legalized the marketing of

prescription drugs to consumers with the mandate that advertisement could not make false or

misleading claims and all side effects must be listed in detail with the products benefits.

Direct-to-consumers advertising of prescription drugs become more prominent in 1997 when

FDA issued less stringent guidelines, although FDA still prohibited misrepresentation or

false claims. But in order to gain more demand and attention of consumers, companies are

making advertisements with false claims and misleads. Doctors start selling the sample

medicines to the patients and companies start offering kickbacks to the doctors for giving

prescription of their drugs. Some other unfair trade practices are also prevailing in the market

like tied selling, attention deficit disorder (ADD), false advertisement, misrepresentation,

False offer or claims etc. these types of unfair and restrictive practices harm both customers

and economy. In this way pharmaceutical companies are adopting different unfair means to

increase the profits. For example an injection (Irinotecan salt based) used for treating cancer

is being sold in the market by a major pharmaceutical company for around Rs. 15000 when

the injection, made out of the same salt, is available under different brands for just Rs. 1500.

There are numerous cases like this where the patients are unaware of cheaper alternatives

with same salt. Officials in the government said that the companies, which sold higher

priced medicines offered a better share of profits for the chemists and retailers. Even if a

chemist offered a cheaper alternative with same salt, he would do so at the risk of losing his

license because the rules bind him to follow doctor’s prescription.

3

The protection of consumers from the undesirable, unethical or immoral trade

practices has both social and monetary benefits. As per the law, the consumer is to be

charged the minimum cost and while profits are the soul of the businesses it should not turn

into profiteering. Mahatma Gandhi had said, “There is enough in this world to meet every

man’s need but not enough in this world to satisfy every man’s greed. Display of wealth is

necessary for a man’s ego. But it is wrong to convert that ego into class struggle. Profit is

not a dirty word, but profiteering is.3”

NEED OF UNFAIR TRADE PRACTICES ACT

Unfair Trade Practices Act helps in protecting consumers from injuries caused by deceptive

trade practices, the remedies provided to redress such injuries are available only to business

entities and proprietors. Consumers who are injured by deceptive trade practices must avail

themselves of the remedies provided by unfair trade practices Act. Unfair Trade Practices

Act took on the role of a watchdog of consumer interest. In the new corporate and business

world today where there is cut throat competition, the business persons daringly use UTP to

edge over the other. Misleading and deceptive conduct is one of the most important

consumer parts of the Act. Unfair Trade Practices Act protects from five types of practices

which are regarded as unfair trade practices in certain situations. These practices are:

a) Misleading advertisements and false representations

b) Bargain sale

c) Offering gifts or prizes and conducting promotional contests

d) Supplying goods not adapting to product safety standards

e) Hording or destruction of goods, or refusal to sell the goods.

FIVE MAJOR FORCES OF DRIVING COMPETITION IN

THE PHARMACEUTICAL MARKET IN INDIA

1. Buyer Power: Over recent years, the hospital segment has experienced a reduced

share in market sales, with other sources such as pharmacies taking a larger share.

This reduces buyer power as pharmaceutical companies are supplying to different

4

sources. Many drugs are unavailable without prescription. Furthermore

pharmaceutical companies market their products largely through physicians, meaning

individual consumers have little control over what pharmaceuticals are at their

disposal. There are often multiple drug treatments available for a given medical

condition. This means that buyer power is reduced further as the manufacturer can

differentiate its product from others by demonstrating the genuine clinical benefits of

its branded and patented product. However, generic equivalents of branded drugs do

exist meaning that there is increased differentiation of prescription drugs, which

serves to increase buyer power. Additionally end users may be given a choice of

treatment medicine and so the buyer power is enhanced to some extent. Switching

costs can often be considerably high.

2. Supplier power: Main supplier to the pharmaceutical industry are manufacturers

who provide active pharmaceutical Ingredients(API). API’s are needed by

pharmaceutical companies in their development of drugs, as such the market player is

in a weaker position. Most large multinational pharmaceutical companies have major

investments in fine chemical manufacturing, providing them a degree of self-

sufficiency. However due to pharmaceutical companies requiring a wide range of

chemicals, power remains with the supplier. It is unlikely that suppliers would

forward integrate into the pharmaceutical market; however their capabilities in

chemical synthesis make them ideal candidates for forward integration into the

manufacture of generic drugs. Over recent years, larger pharmaceutical companies

have turned to produce their own chemicals in a bid to enhance profits. However

smaller companies lack the resources required to do this and remain reliant on API

manufacturers. APIs are supplied on a contractual basis. Pharmaceutical companies

are likely to risk high switching costs if they consider taking their business elsewhere.

This serves to increase supplier power further. In turn, pharmaceutical companies

employ sourcing managers to minimize costs in the purchase of APIs and mitigate

supplier power. The development of new therapeutic agents requires the sourcing of

newer APIs, for which chemical manufacturers can charge pharmaceutical companies

high prices. If the novel drug successfully reaches the market, the supplier of the API

5

can make a large amount of money. Supplier power with respect to the

pharmaceutical market is considered to be strong.

3. New Entrants: The cost of developing a novel prescription drug is in the

excess of millions. Vigorous and extensive clinical trials are required to satisfy the

safety protocols of regulatory bodies. A high level of proprietary knowledge is

required to compete successfully in this market, as established companies usually

keep their drug discovery processes very secretive. This can prove off putting to new

entrants. Additionally the process of developing a new drug is fraught with problems

and is a risk to financiers. Players may yield poor revenues due to leading

incumbents such as Cipla Ltd., GlaxoSmithKline Plc, Ranbaxy Laboratories Limited,

Piramal Healthcare(PHL) etc. dominates the market and the development of

substitute therapies, which are considered as a weak threat to prescription

pharmaceuticals. However patents for new drugs protect the interests of the

developer, allowing the recouping of development expenses, and ensuring

profitability. As well as this strong market growth is seen as enticing new entrants.

Recently, Asia has become vital in pharmaceutical outsourcing. Leading

international incumbents are processing their products in India over the European and

US markets.

4. Threats of substitutes: Generic substitutes of branded drugs exist in the

market. However there are very few viable substitutes for ethical pharmaceuticals

overall. Recently, there has been a growth in the popularity of alternative therapies

which prove cheaper than some drugs. The medical community heavily disputes the

benefits of these alternatives, claiming them to lack the rigorous clinical testing

required for all pharmaceutical products. Additionally, alternative therapies are

claimed not to target medical problems specifically unlike their pharmaceutical

counterpart. OTC medicines are threatened by alternative therapies more than

prescription medicines. It is the individual consumer who purchases alternative

therapies, whereas the price of most ethical drugs to the patient is heavily subsidized

by either the state or health insurers. It is these substitutes which are regarded as

more expensive.

6

5. Degree of Rivalry: The key players in the pharmaceutical market are usually

large multinational companies who own a high level of capital investment. Large

companies are likely to keep their leading position for this reason, as new entrants are

less likely to have the same degree of capital investment. The Indian market is

relatively fragmented with four major companies sharing 22% of the total market

value. Rivalry is intensified further by the high fixed and exit costs from suppliers.

The market is highly competitive for a number of reasons. Firstly the development

costs for a prescription drug are high. Secondly, there are often other drugs

competing for a market share of a given therapeutic area. Furthermore, there are no

switching costs for practitioners. These reasons mean that rivalry between key

players is high. Excellent market growth serves to ease rivalry to some extent. Key

players must invest in marketing and sales operations in order to maximize their

revenues. Overall, the pharmaceutical market displays a strong level of rivalry.

INDIAN PHARMACEUTICAL INDUSTRY

Medicines contribute enormously to the health of the nation. The discovery, development

and effective use of drugs have improved many people’s quality of life, reduced the need for

surgical intervention and the length of time spent in hospital and saved many lives. Over the

years pharmacy has grown in the form of pharmaceuticals sciences through research and

development processes. It is related to product as well as services. The various drugs

discovered and developed are its products and the healthcare it provides comes under the

category of services. Pharmacy involves all the stages that are associated with the drugs, i.e.

discovery, development, action, safety, formulation, use, quality control, packaging, storage,

marketing etc.

The Indian pharmaceutical industry is a successful, high-technology-based industry that has

witnessed consistent growth over the past three decades. Indian Pharmaceutical Industry has

an important role in promoting public health. The origin of the Indian pharmaceutical

Industry may be traced to the establishment of the Bengal Chemicals and Pharmaceutical

works, which exist today as one of 5 government owned drug manufacturers, in Calcutta in

1930.4 For the next 60 years, most of the drugs in India were imported by multinationals

7

either in fully formulated or bulk form. The government started to encourage the growth of

drug manufacturing by Indian companies in the early 1960s and with the patent Act in 1970,

enabled the Industry to become what it is today. This patent act removed composition

patents from food and drugs and though it kept process patents, these were shortened to a

period of five to seven years. The lack of patent protection made the Indian market

undesirable to the multinational companies that had dominated the market, and while they

streamed out, Indian companies started to take their places. They carved a niche in both the

Indian and world markets with their expertise in reverse engineering new processes for

manufacturing drugs at low costs. Although some of the larger companies have taken baby

steps towards drugs innovation, the industry as a whole has been following this business

model until the present.

CLASSIFICATION OF PHARMACEUTICAL INDUSTRY

The global pharmaceutical industry structure can be divided into two:

• Bulk drugs (20%) The bulk drug segment of the market has increased in the past decade at

around 20% annual growth rate.

• Formulations (80%) Production of formulations has increased by around 15% annually.

The Indian Pharmaceutical Industry is among the top five producers of bulk drugs in the

world. The largest firms account for the majority of the R& D investment in the industry and

hold the majority of the patents. A small number of multinational enterprises (MNEs)

dominate the global pharmaceutical industry; top twenty-five MNEs having accounted for

64.5 percent of the world (2003) Firms can be either in production of bulk drugs or

formulations or may manufacture both. Firms in to formulations may be further classified

into innovating firms and non- innovating firms. However, R&D is insignificant when

compared to MNEs. There are about 8174 bulk drug manufacturing units and 2389

formulations units spread across India. Total: 10563 units.

Statistics

The net worth of the industry is about 8 Billion Dollars with a growth rate of 8-9% PA. It

exports to nearly 212 countries.5 In 2002, over 20,000 registered drug manufacturers in India

8

sold $9 billion worth of formulations and bulk drugs. 85% of these formulations were sold in

India while over 60% of the bulk drugs were exported, mostly to the United States and

Russia. Most of the players in the market are small-to-medium enterprises; 250 of the largest

companies control 70% of the Indian market. Multinationals represent only 35% of the

market, down from 70% thirty years ago.

Most pharmaceutical companies operating in India, even the multinationals, employ Indians

almost exclusively from the lowest ranks to high level management. Mirroring the social

structure, firms are very hierarchical. Homegrown pharmaceuticals, like many other

businesses in India, are often a mix of public and private enterprises. Although many of these

companies are publicly owned, leadership passes from father to son and the founding family

holds a majority share.

In terms of the global market, India currently holds a modest 1-2% share, but it has been

growing at approximately 10% per year. India gained its foothold on the global scene with its

innovatively-engineered generic drugs and active pharmaceutical ingredients (API), and it is

now seeking to become a major player in outsourced clinical research as well as contract

manufacturing and research. There are 74 U.S. FDA-approved manufacturing facilities in

India, more than in any other country outside the U.S, and in 2005, almost 20% of all

Abbreviated New Drug Applications (ANDA) to the FDA are expected to be filed by Indian

companies. Growth in other fields notwithstanding, generics is still a large part of the picture.

The pharmaceutical market generated total revenue of $ 10838.7 million in 2009,

representing a compound annual growth rate of 11.3% for the period spanning 2005-2009.

Alimentary/metabolism sales proved the most profitable for the Indian pharmaceuticals

market in 2009, generating total revenues of $1498.8 million equivalent to 13.8% of the

market’s overall value. India accounts for 8.7% of the Asia-Pacific pharmaceuticals market’s

value. Japan leads the Asia-Pacific pharmaceuticals market, accounting for 53.8% of

market’s value.

9

GROWTH OF INDIAN PHARMACEUTICAL INDUSTRY

The Indian Pharmaceutical industry today is in the front rank of India’s science-based

industries with wide ranging capabilities in the complex field of drug manufacture and

technology. Pharmaceutical Industry in India is one of the largest and most advanced among

the developing countries. It provides employment to million and ensure that essential drugs

at affordable prices are available to the vast population of India. Indian Pharmaceutical

Industry has attained wide ranging capabilities in the complex field of drug manufacture and

technology. From simple pain killer to sophisticated antibiotics and complex cardiac

compounds, almost every type of drug is now made indigenously. A highly organized sector,

the Indian Pharmaceutical Industry is estimated to be worth $ 7.8 billion, growing at about 8

to 9 percent annually.

The growth of the pharmaceutical industry in India is quite phenomenal. From small

beginnings during the first post-independence decade, the industry has come a long way and

become very robust today. This industry is able to weather the impact of the three F’s –

Finance (inflation in the economy), Fuel price escalation and food shortage on the

pharmaceutical sector reflect robustness, as the prices are hardly hit despite the rapid fall of

the sensex. The pharmaceutical industry produces valuable life-saving drugs along with

numerous over-the-counter drugs such as paracetamol. The growth of an industry is highly

dependent on the regulatory environment. India had a product patent regime for all

inventions under the Patents and Designs Act 1911. However, in 1970, the government

introduced the new Patents Act, which excluded pharmaceuticals and agrochemical products

from eligibility for patents. This exclusion was introduced to break away India’s dependence

on imports for bulk drugs and formulations and provide for development of a self-reliant

indigenous pharmaceutical industry and the same helped in6-

1. Reduction in the manufacturing costs in terms of license fee.

2. Reduction in the costs involved in R&D.

3. Diffusion of technology and knowledge through reverse engineering.

10

The lack of protection for product patents in pharmaceuticals and agrochemicals had a

significant impact on the Indian pharmaceutical industry and resulted in the development of

considerable expertise in reverse engineering of drugs that are patentable as products

throughout the industrialized world but unprotect able in India. As a result of this, the Indian

pharmaceutical industry grew rapidly by developing cheaper versions of a number of drugs

patented for the domestic market and eventually moved aggressively into the international

market with generic drugs once the international patents expired. Till 1970, the growth of the

Indian pharmaceutical industry was very slow and after that government investment in the

pharmaceutical industry infused life into the domestic pharmaceutical sector. In addition, the

Patents Act provides a number of safeguards to prevent abuse of patent rights and provide

better access to drugs. The Indian Patents (Amendment) Act, 2005 introduced product

Patents in India and marked the beginning of a new patent regime aimed at protecting the

Intellectual property rights of patent holders. The Act was in fulfillment of India’s

Commitment to World Trade Organization (WTO) on matters relating to Agreement on

Trade Related Aspects of Intellectual Property Rights (TRIPS Agreement). Product patents

for pharmaceuticals, food and agro-chemicals were removed by the Act, allowing patents

only for production processes. Automatic licensing was put in place and the statutory terms

was shortened to seven years on drug patents. This led to the era of reverse engineering,

where new products were developed by a firm by changing their production processes.

During the last three decades, the private Indian pharmaceutical firms focused their efforts on

reverse engineering-oriented research and development, and this activity was very much

limited to applying known knowledge, or to making minor adjustments and modifications.

In addition, a few public sector laboratories operated in pharmaceutical research and

development under the Council of Scientific and Industrial Research (CSIR). Thus, the lag

period between the launch of a new product in its maiden market abroad and in India was

reduced in some cases to two years low, as a result of well-mastered production

technologies.7

Indian Pharmaceutical Industry plays an important role in the country to improve the quality

of life of the people by way of manufacturing host of drugs and pharmaceuticals for the

health of the citizens. The primary objective of the industry is to ensure the availability of

11

quality medicines for the masses including essential and life saving drugs and formulations at

reasonable prices. The foundation of the modern Indian Pharmaceutical Industry was laid in

the beginning of the current century when in 1901 a small factory known as M/s. Bengal

Chemical & Pharmaceutical Works was established in Calcutta. In the period immediately

after independence, the industry was totally dependent upon imports and by 1960s a number

of bulk drugs were produced in the country. During the period 1960 to 1970, the Indian

companies along with multinational companies laid the foundation of a truly modern

pharmaceutical industry.8

Advantage India:

India does have quite a few advantages, but the pharmaceutical industry needs a proper

marketing strategy to be put in place before banking on the government for concessions9.

The advantages India has are:

Cost – effective chemical synthesis: Implementation of value engineering in

chemical synthesis of various drug molecules drastically improves cost benefit. Fast

development track record

Provides bulk drugs: Provides a vast variety of bulk drugs and also enhances

exports of sophisticated bulk drugs.

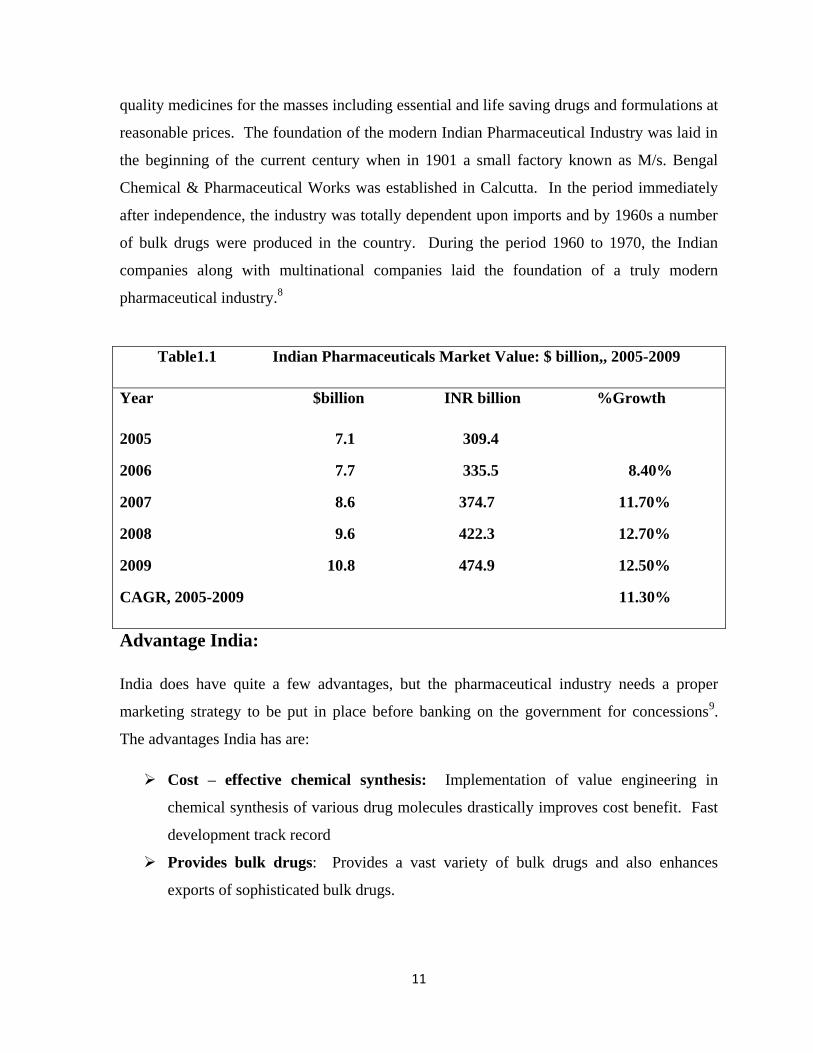

Table1.1 Indian Pharmaceuticals Market Value: $ billion,, 2005-2009

Year $billion INR billion %Growth

2005 7.1 309.4

2006 7.7 335.5 8.40%

2007 8.6 374.7 11.70%

2008 9.6 422.3 12.70%

2009 10.8 474.9 12.50%

CAGR, 2005-2009 11.30%

12

Competent workforce: India has a pool of easily available professional expertise

with high managerial and technical competence and these professionals are proficient

in English and other international languages, which facilitates international trading.

Legal and financial framework: A successful 60-year-old democracy of India

supports a strong legal framework and financial markets. Established international

industry and business s community also provide development framework.

Globalization: India has a free market economy and supports globalization.

Consolidation: India is now generating great opportunities from international

pharmaceutical industries.

Above all India has a huge population (16% of the world’s population), which is really in

need of good health. The prescription audit revealed the following information on the types

and category of drugs being prescribed generic(50.57%), branded (49.43%) and fixed dose

combination (18.27%) antibiotics (22.76%), analgesics(21.76%), anti-histaminies (12.56%),

drugs for gastro intestinal tract diseases (9.47%) steroids (3.57%) and drug for

cardiovascular diseases (3.16%) were prescribed. Doses were mentioned correctly for

19.28% of the antibiotics prescribed.10

SWOT ANALYSIS11

Strengths

Cost Competitiveness

Table No:1.2 Category – wise sale of Pharmaceutical Products in India (By

value)

Category % Sales

Anti-infectives 18

Alimentary/metabolism 11

Cardiovascular 10

Respiratory 9

Central Nervous System 5

Others 47

Total 100

13

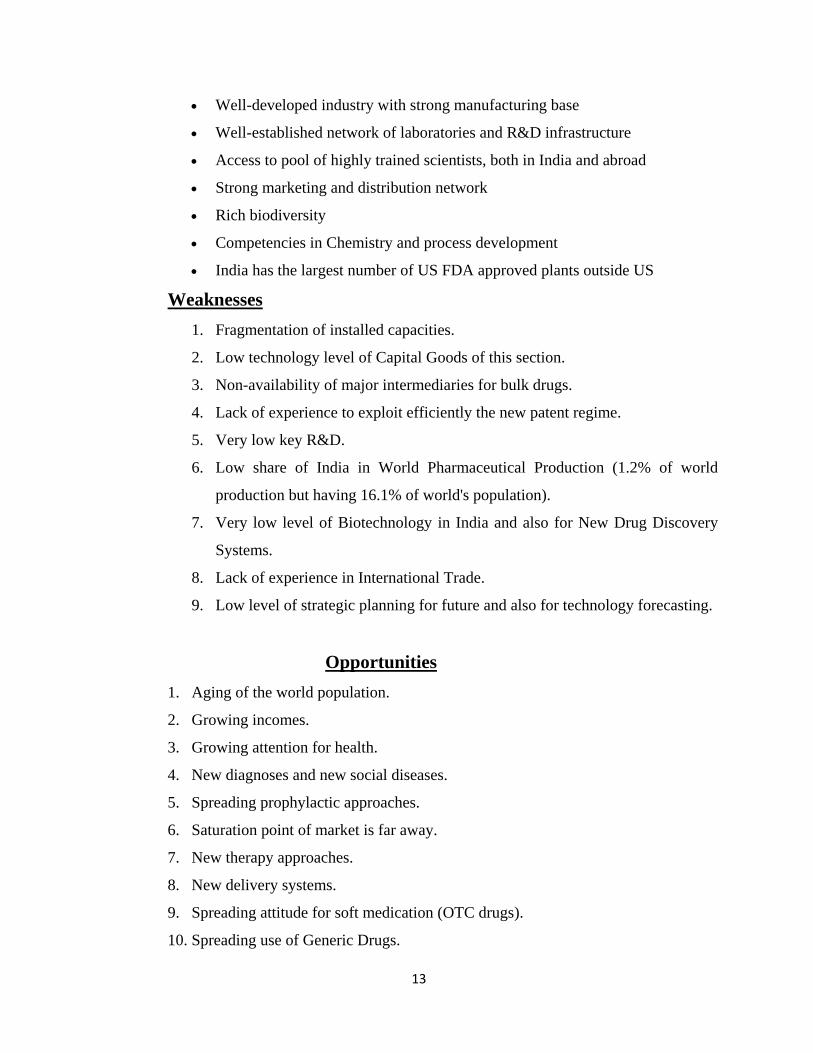

Well-developed industry with strong manufacturing base

Well-established network of laboratories and R&D infrastructure

Access to pool of highly trained scientists, both in India and abroad

Strong marketing and distribution network

Rich biodiversity

Competencies in Chemistry and process development

India has the largest number of US FDA approved plants outside US

Weaknesses

1. Fragmentation of installed capacities.

2. Low technology level of Capital Goods of this section.

3. Non-availability of major intermediaries for bulk drugs.

4. Lack of experience to exploit efficiently the new patent regime.

5. Very low key R&D.

6. Low share of India in World Pharmaceutical Production (1.2% of world

production but having 16.1% of world's population).

7. Very low level of Biotechnology in India and also for New Drug Discovery

Systems.

8. Lack of experience in International Trade.

9. Low level of strategic planning for future and also for technology forecasting.

Opportunities

1. Aging of the world population.

2. Growing incomes.

3. Growing attention for health.

4. New diagnoses and new social diseases.

5. Spreading prophylactic approaches.

6. Saturation point of market is far away.

7. New therapy approaches.

8. New delivery systems.

9. Spreading attitude for soft medication (OTC drugs).

10. Spreading use of Generic Drugs.

14

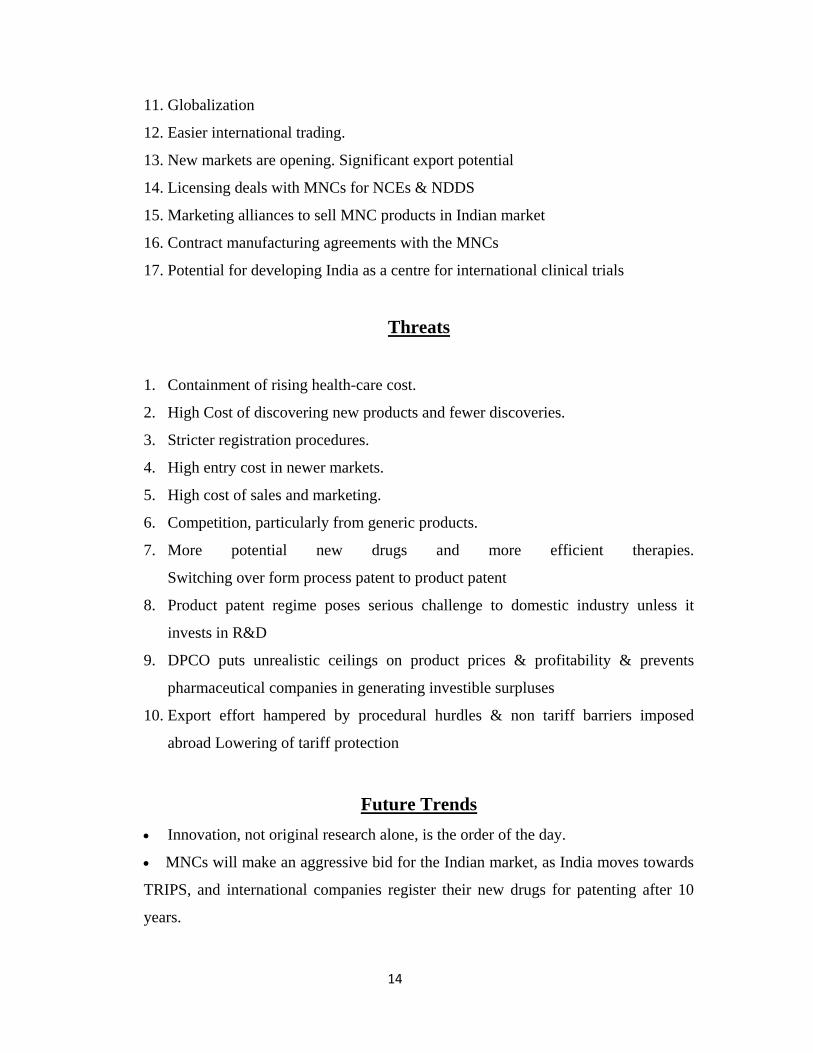

11. Globalization

12. Easier international trading.

13. New markets are opening. Significant export potential

14. Licensing deals with MNCs for NCEs & NDDS

15. Marketing alliances to sell MNC products in Indian market

16. Contract manufacturing agreements with the MNCs

17. Potential for developing India as a centre for international clinical trials

Threats

1. Containment of rising health-care cost.

2. High Cost of discovering new products and fewer discoveries.

3. Stricter registration procedures.

4. High entry cost in newer markets.

5. High cost of sales and marketing.

6. Competition, particularly from generic products.

7. More potential new drugs and more efficient therapies.

Switching over form process patent to product patent

8. Product patent regime poses serious challenge to domestic industry unless it

invests in R&D

9. DPCO puts unrealistic ceilings on product prices & profitability & prevents

pharmaceutical companies in generating investible surpluses

10. Export effort hampered by procedural hurdles & non tariff barriers imposed

abroad Lowering of tariff protection

Future Trends

Innovation, not original research alone, is the order of the day.

MNCs will make an aggressive bid for the Indian market, as India moves towards

TRIPS, and international companies register their new drugs for patenting after 10

years.

15

Smaller companies, which had so far benefited from the protective regime, may

be forced to become contracting units, or close shop.

Generics will have a huge demand.

Increasing R&D costs will lead to more consolidation among international

companies. Within 5 years, the top ten pharmaceutical companies will control over

60% of the world market.

International companies could set up their own R&D labs in India and develop

drugs for tropical diseases.

Innovations in R&D process such as genomics and combinatorial chemistry.

Indian pharmaceutical companies are expected to move up the value chain from

merely being reverse engineers to developers of proprietary products in the US

market.

10 MAJOR INDIAN DRUG COMPANIES

1) Dr. Reddy’s Laboratories Ltd.

2) Ranbaxy Laboratories Ltd.

3) Lupin Ltd.

4) Sun Pharmaceutical industries Ltd.

5) Cipla Ltd.

6) Orchid Chemicals & Pharmaceuticals Ltd.

7) Nicholas Piramal India Ltd.

8) Wockhardt Ltd.

9) IPCA Laboratories Limited

10) Cadila Healthcare Limited

1) Dr. Reddy’s Laboratories Ltd.: Dr. Reddy Laboratories was incorporated in

India by Dr. K. Anil in 1984. The company went public in 1985 was listed on the Indian

Stock Exchange in 1986. Dr. Reddy’s Laboratories is a global pharmaceutical company.

The company produces and distributes finished dosage forms, active ingredients and

intermediates and biotechnology products. It also conducts research in the areas of cancer,

16

diabetes, cardiovascular, inflammation and bacterial infection. The company primarily

operates in India, the US, Europe and Russia. It is headquartered in Hyderabad, India and

employs around 11228 people. It was listed on the New York Stock Exchange in 2001. Dr.

Reddy Laboratories specializes in the production of generic and branded drugs. The

company’s key products and services are:

PRODUCTS

Active pharma ingredients

Custom pharma Services

Generic biopharmaceuticals

Generics

New chemical entities and differentiated formulations

SERVICES

Custom chemical Services

Drug Research and development Services

The company recorded revenues of $ 8727 million in the Fiscal year ended Mar. 2009, an

increase of 20.1% over 2008.

2) Ranbaxy Laboratories Ltd.:

Ranbaxy company was incorporated in 1961. Ranbaxy was registered as private sector

company in 1973 and start a multi purpose chemical plant for manufacturing APIs at Mohali

in India. In 1985 Ranbaxy research foundation was established. Ranbaxy is the largest

generic pharmaceutical company in India. The company’s operations are divided into two

business segments: dosage forms and APIs. The dosage forms produced by the company

include a range of prescription and non- prescription drugs. The division places a particular

emphasis on anti-infective and anti bacterial. API division has a portfolio of over 50

products covering a wide therapeutic range such as anti infective, anti ulcer ants, anti

diabetics etc. the other products includes therapeutics for orthopedics, pain management,

17

nutritional, multivitamins, central nervous system disorders etc. Ranbaxy today has global

footprint in 46 countries, world-class manufacturing facilities in 7 countries and serves

customers in over 125 countries. It is headquartered in Gurgaon.

For the year 2009, the company recorded Global sales of US $ 1519 mn. The company has a

balanced mix of revenues from emerging and developed markets that contribute 54% and

39% respectively. In 2009, North America, the company’s largest market contributed sales

of US $ 397 Mn, followed by Europe garnering US $ 269 Mn and Asia clocking sales of

around US $ 441 Mn.

3) Lupin Ltd.:

Lupin Pharmaceuticals, Inc. is the U.S. wholly owned subsidiary of Lupin Limited, which is

among the top six pharmaceutical companies in India. Through our sales and marketing

headquarters in Baltimore, MD, Lupin Pharmaceuticals, Inc. is dedicated to deliver high-

quality, branded and generic medications trusted by healthcare professionals and patients

across geographies.

Lupin Limited, headquartered in Mumbai, India, is strongly research focused. It has a

program for developing New Chemical Entities. The company has a state-of-the-art R&D

center in Pune and is a leading global player in Anti-TB, Cephalosporins (anti-infectives) and

Cardiovascular drugs (ACE-inhibitors and cholestrol reducing agents) and has a notable

presence in the areas of diabetes, anti-inflammatory and respiratory therapy.

4) Sun Pharmaceutical industries Ltd.

Sun Pharma began in 1983 with just 5 products to treat psychiatry ailments. Sales were

initially limited to 2 states - West Bengal and Bihar. Sales were rolled out nationally in 1985.

Products that are used in cardiology were introduced in 1987, and Monotrate, one of the first

products launched at that time has since become one of the largest selling products.

Important products in Cardiology were then added; several of these were introduced for the

first time in India. Realizing the fact that research is a critical growth driver, we established

research center SPARC in 1993 and this created a base of strong product and process

18

development skills. Sun Pharma was listed on the main stock exchanges in India in 1994;

first API manufacturing plant was built in Panoli in 1995, for access to high quality actives

ahead of competition, and to tap the vast international opportunity for specialty APIs.

The tally at the end of 2008:

17 manufacturing plants in 3 continents

8000 employees

World class research centers

Brand selling in markets worldwide

A growing presence in the US generic market

Company makes specialty pharmaceuticals and active pharmaceutical ingredients. Our

brands are prescribed in chronic therapy areas like cardiology, psychiatry, neurology,

gastroenterology, diabetology and respiratory and dermatology.

5) Cipla Ltd.: Khwaja Abdul Hamied, the founder of Cipla. In 1935, he set up The

Chemical, Industrial & Pharmaceutical Laboratories, which came to be popularly known as

Cipla. He gave the company all his patent and proprietary formulas for several drugs and

medicines, without charging any royalty. On August 17, 1935, Cipla was registered as a

public limited company with an authorised capital of Rs 6 lakhs.

The search for suitable premises ended at 289, Bellasis Road (the present corporate office)

where a small bungalow with a few rooms was taken on lease for 20 years for Rs 350 a

month.

Cipla was officially opened on September 22, 1937 when the first products were ready for

the market. The Sunday Standard wrote: "The birth of Cipla which was launched into the

world by Dr K A Hamied will be a red letter day in the annals of Bombay Industries. The

first city in India can now boast of a concern, which will supersede all existing firms in the

magnitude of its operations. India has lagged behind in the march of science but she is now

awakening from her lethargy. The new company has mapped out an ambitious programme

19

and with intelligent direction and skillful production bids fair to establish a great reputation

in the East. "

6) Orchid Chemicals & Pharmaceuticals Ltd.:

Orchid Chemicals & Pharmaceuticals Ltd (Orchid) was established in 1992 as a 100%

Export Oriented Unit (EOU). Commencing operations in 1994, Orchid has achieved amazing

and consistent growth, quantitatively and qualitatively to emerge among the Top-15

companies in the Indian pharmaceutical industry in a short span of fifteen years of

operations. Orchid employs over 4000 people, of which over 700 are scientists, technologists

and other professionals.

Orchid's growth and positioning in the global pharmaceutical industry are indeed distinctive.

A robust leadership position in the antibiotics space, a core competence in oral and sterile

manufacturing, a broad-based multi-therapeutic coverage and an end-to-end connectivity

over the pharmaceutical value chain, from discovery to delivery, have positioned Orchid

uniquely.

Orchid has two manufacturing sites for APIs (at Alathur near Chennai and at Aurangabad,

near Mumbai) and three manufacturing sites for Dosage forms (at Irungattukottai and Alathur

in Chennai), besides a world-class R&D centre (at Sholinganallur, Chennai). Orchid’s

facilities are state-of-the-art and have several international regulatory approvals, including

the US FDA and UK MHRA. Orchid’s API facilities are ISO certified for their quality,

environmental management and operational health and safety systems. Orchid has a Joint

Venture in China for manufacturing sterile APIs.

Orchid’s scientific and technical strengths have made it a partner of choice for several

multinational corporations. Orchid has long-term exclusive marketing alliances with reputed

global companies for distribution of its products in the advanced markets.

20

7) Nicholas Piramal India Ltd.:

Piramal Healthcare (PHL) (formerly Nicholas Piramal India) was incorporated in 1947,

under the name Indian Schering; Later changing to Nicholas Laboratories India in 1979. The

name of the company changed to Nicholas Piramal India, in 1992. In May 2008, the

company again changed its name to Piramal Health care Limited. PHL manufactures

antibiotics, nutritionals products and general medicines under the brands such as phensedyl,

Haemaccel, stemetil, Tixlix, Ismo etc. Piramal Health care primarily operated in India,

headquarted in Mumbai. The company’s business operations are divided into pharmaceutical

business and other business. Piramal Health care ltd.’s pharmaceutical business segment

consists of the manufacture and trading of bulk durgs and formulations. It manufactures

creams and powder, tablets, capsules, liquids, ointments, bulk drugs and intermediates.

PHL and Minrad, a provider of generic inhalation anesthetics signed a definitive merger and

agreement fro PHL to acquire Minrad in Dec 2009. Piramal Health care generated revenue of

$ 750 million in the financial year (FY) ended March 2009, an increase of 14.2% over FY

2008. The company’s net income totaled $ 72.2 million in FY 2009, a decrease of 5.3% over

FY 2008. India accounted for 59.9% of the total revenue generated I FY 2009. Revenues

from India reached $ 449.8 million in FY 2009, an increase of 20.9% over 2008.

8) Wockhardt Ltd.

Wockhardt is a global, pharmaceutical and biotechnology company that has grown by

leveraging two powerful trends impacting the world of medicine - globalization and

biotechnology.

The Company has a market capitalization of over US$ 1 billion and an annual turnover of

US$ 650 million. Wockhardt’s pace of growth and momentum permeates every mindset,

system and technology within the organization.

Wockhardt today, is distinguished by a strong and growing presence in the world’s leading

markets, with more than 65% of its revenue coming from Europe and the United States.

Wockhardt’s market presence covers formulations, biopharmaceuticals, nutrition products,

21

vaccines and active pharmaceutical ingredients (APIs). The Company has its headquarters in

India, and has 14 manufacturing plants in India, UK, Ireland, France and US Subsidiaries in

US, UK, Ireland and France Marketing offices in Africa, Russia, Central and South East

Asia.

Wockhardt has a strong track record in acquisition management, with five successful

acquisitions in the European market. These acquisitions have strengthened Wockhardt’s

position in the high-potential markets of Europe, and have expanded the global reach of the

organisation.

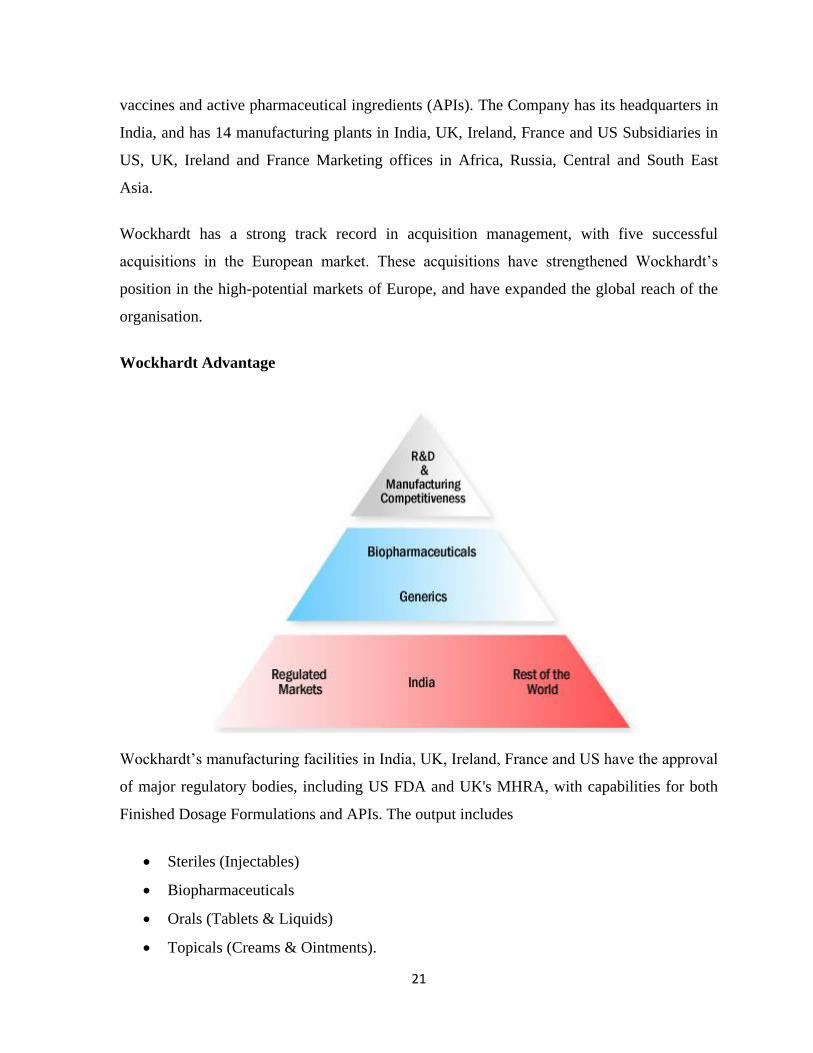

Wockhardt Advantage

Wockhardt’s manufacturing facilities in India, UK, Ireland, France and US have the approval

of major regulatory bodies, including US FDA and UK's MHRA, with capabilities for both

Finished Dosage Formulations and APIs. The output includes

Steriles (Injectables)

Biopharmaceuticals

Orals (Tablets & Liquids)

Topicals (Creams & Ointments).

22

Wockhardt is a partner of choice for manufacturing, having entered into manufacturing

alliances with leading pharmaceutical and biotechnology majors, including

Astra Zeneca

Aventis

Schering-Plough

Cell Therapeutics

AFT, New Zealand

Lab Aguettant

Amylin

Eisai

LSI, UK

Ebewe, Austria

A key growth driver at Wockhardt is its state-of-the-art, multi-disciplinary research

capability backed by a team of 500 skilled scientists. Consistent efforts have resulted in six

breakthrough biotechnology products, 750+ patent filings and a pipeline of promising new

molecules.

Wockhardt’s strategies are aligned towards being a significant player in the emerging global

biopharmaceuticals market. In order to achieve this goal, the company has set up the

Wockhardt Biotech Park, India’s largest biopharmaceuticals complex, with six dedicated

plants built to international standards.

9) IPCA Laboratories Limited

One of the first modern pharma factory of yesteryears was commissioned by Ipca at

Mumbai in 1969. The company was originally promoted by a group of medical

professionals and businessmen and was incorporated as 'The Indian Pharmaceutical

Combine Association Limited.' in October 1949. Ipca is a fully integrated, rapidly

growing Indian pharmaceutical company with a strong thrust on exports. Ipca's APIs and

23

Formulations produced at world class manufacturing facilities are approved by leading

drug regulatory authorities including the US-Food and Drug Administration (FDA), UK-

Medicines and Healthcare products Regulatory Agency (MHRA), South Africa-Medicines

Control Council (MCC), Brazil-Brazilian National Health Vigilance Agency (ANVISA)

and Australia-Therapeutic Goods Administration (TGA). With operations in over 100

countries, exports account for over 52% of the company's income.

Forbes, a leading US business magazine, selected Ipca in 2003 among its top 200

successful, rising companies outside USA, with sales under USD 1 Billion. Over 19,000

companies were considered by Forbes, and of the 18 companies from India that figured in

this list, only four were from the 'Indian Pharmaceutical Sector'. Ipca happens to be one of

them. Subsequently, Ipca was selected by FORBES in this prestigious list for two

consecutive years; 2004 and 2005.

From a modest income of Rs. 0.54 crores in 1975-76, the net income has soared to Rs.

753.30 crores in 2005-06 with exports accounting for Rs. 401.83 crores. The net profit for

the year ending 31st March, 2006 stood at Rs. 63.98 crores. Formulations constitute 67

percent of the total income for 2005-06. Today, Ipca is one of the biggest manufacturers

in the world of APIs Atenolol (Antihypertensive), Chloroquine Phosphate (Antimalarial),

Furosemide (Diuretic) and Pyrantel Salts (Anthelmintic) right from the basic stage. Ipca is

also one of the largest suppliers of these APIs and their intermediates world over.

10) Cadila Healthcare Limited:

'Cadila Healthcare' is an Indian pharmaceutical company head quartered at Ahmedabad in

Gujarat state of western India. The company is the fifth largest pharmaceutical company in

India, with US$290m in turnover in 2004. It is a significant manufacturer of generic drugs.

Cadila Pharma have developed a drug named Roserin which has reduced the cost of curing

TB by 33%. Cadila Laboratories was founded in 1952 by Ramanbhai Patel (1925-2001),

formerly a lecturer in the L.M. College of Pharmacy, and his business partner Shri

Indravadan Modi. The company evolved over the next four decades into one of India's

established pharmaceutical companies.

24

STEPS REQUIRED TO BOOST THE COMPETITIVENESS OF

THE PHARMA -INDUSTRY

• Extension of deduction of 150% of R&D expenses. This would encourage more

and more companies to invest in R&D. The government has earmarked 150 crores for R&D.

This is just not enough. It should be augmented to at least 2000 crores.

• To rationalize Drug Price Control Order (DPCO). The objective of the price

control was to ensure adequate availability of quality medicines at affordable prices. The

product patent regime will make it obligatory for Indian companies to compete in R&D if

they want to survive. Similarly, WTO led global trading system will result in import tariffs

coming down. For Indian companies to compete with cheap imports, they will have to invest

in cost effective technology and processes. Therefore, it is imperative that the pharma

industry has surplus for investment. In this context, a liberalized price control regime

becomes more important.

• An academic –industrial relationship can be further explored, on the lines of

the US model, where the universities are the sites of innovation and the industry

commercializes the product. The universities are permitted to own the Intellectual Property

Rights (IPR) and get a share of the profits. Academic institutions will then become the

engines of entrepreneurship. This also requires setting up of greater number of centers of

academic excellence throughout India in different states, so that people from across the

country can avail of such education and make their contributions without feeling the need to

look beyond India for achieving academic excellence.

• Income tax exemptions should be given on clinical trials and contract

research done outside the company and abroad. This is because India is seen as

emerging as a major center for outsourcing of clinical trials for the Pharmaceutical MNCs.

• The problem of spurious drugs has to be tackled. The procedure for

procurement of licence should be made more stringent, including extensive disclosure of

detailed personal, financial and business information and a thorough background check.

25

There is a strong need to strengthen and streamline the Central and State Drug Control

Organizations. State drug controllers should take measures like setting up of separate

intelligence-cum-legal machinery with police assistance. Faking should be made non-bailable

and cognizable offence and the prosecution should be instituted by any police or Central

Bureau of Investigation officer not less than the rank of a sub-inspector (instead of an

inspector in the extant provision). Most of the cases relating to spurious drugs remain

undecided for years. Hence there is a strong need for setting up separate courts for speedy

trials of such offences. The case should be tried by the court of the rank of a Session Judge or

above whereas the extant provision provides for a trial by a metropolitan magistrate or a first

class judicial magistrate or above. Each state should set up accredited testing laboratories

that are well equipped and adequately staffed. The staff should be trained well for drawing

samples for test and monitoring the quality of drugs and cosmetics moving in the State. It is

most important and essential to have training programmes for technical staff of central and

state drug control laboratories and private testing laboratories as it is based on the report of

these testing laboratories that a manufacturer releases his product or otherwise. Legal action

against the manufacturer is likely to be taken on the basis of the test report given by a

government analyst.

• India should exploit its know-how in herbal medicines. Since these medicines

do not come under the purview of the TRIPS regime and the research in new chemical

entities involves millions of dollars of investment, the Indian companies should engage in

R&D in herbal medicine. The companies should try to exploit the Indian traditional

knowledge in ayurveda and herbal cures and file as many patents for herbal medicine as they

can. For this the government should set up R&D laboratories undertaking research

exclusively in the area of herbal medicines and support the companies in their research and

patent filing.

• The government should encourage setting up of USFDA-compliant plants

by providing tax holidays for a specified period (as given in regions like

Baddi), so that the Indian companies can exploit the opportunity arising out of patented

drugs and take up marketing of generics in the developed countries like USA.

26

SIGNIFICANCE OF THE STUDY

According to the World Bank “Competition” is “a situation in a market in which firms or

sellers independently strive for the buyers” patronage in order to achieve a particular

business objective for example profits, sales or market share.” Sometimes firms while

competing with one another, adopt restrictive or unfair practices, which are derogatory to the

core of a competitive market.

Today unfair trade practices are increasing day by day. The provisions pertaining to unfair

trade practices are applicable to any person, trader, business, or industry etc. excepting to

certain undertakings or trade associations. These include: 1) any undertaking owned or

controlled by a Government company; 2) any undertaking owned or controlled by the

Government Company; 3) any undertaking owned or controlled by a corporation (not being

a company) established by or under any central, provincial or State Act; 4) any trade union

or other association of workmen or employees formed for their own reasonable protection as

such workmen or employees; 5) any undertaking engaged in any industry the management

of which has been taken over by any person or body of persons in pursuance of any

authorization made by the central Government under any law for the time being in force; 6)

any undertaking owned by a co-operative society formed and registered under any central,

provincial or state Act relating to co-operative societies; and 7) any financial institution.

This research highlights the unfair trade practices done in the pharmaceutical sector and also

highlights the steps that should be taken to remove the unfair trade practices.

SCOPE OF THE STUDY

To achieve the above objectives this study a set of questions were asked from Doctors,

Patients and Wholesalers & retailers of different pharmaceutical companies. In this

Researcher has found what type of unfair trade practices are conducted in Pharmaceutical

sector in India. The study covers data over the period ranging from 1998-99 to 2008-09.

However, in some of the cases where the secondary data for those years could not be made

available, the range of period has been shifted.

27

CONTRIBUTION OF THE STUDY

The finding of the present research endeavor will be of interest to pharmaceutical companies,

academicians, managers of pharmaceutical companies, distribution channels, doctors and

customers. An attempt has been made to add to the knowledge about what type of unfair

trade practices are there in present competitive scenario. This study also checks the

awareness of the customers towards these practices. This study will tell the customers how

they are cheated in the market and what steps can be taken by them so that they don’t let

others to cheat them. This study will throw light on the process of filing complain under

Unfair Trade Practices Act.

LIMITATIONS OF THE STUDY

The present study is made to analyze Unfair Trade Practices in Pharmaceutical Industry.

Lack of relevant research work special on Unfair Trade Practices in Pharmaceutical Industry

has been the greatest limitation of the study as this absence created problems in collecting

qualitative information pertaining to various areas of Unfair Trade Practices.

It is important to highlight the limitations of a work especially in case of a research. The

limitations help us to understand and appreciate the work in proper perspective.

The research work has been completed under the following other main limitations:

(i) For the individual researcher certainly some constraints and restraint of time money

and sufficient authority to enquire about information.

(ii) Techniques used in the study are subject to their own limitation, which might have

affected the finding of the study.

(iii) In the collection of first hand information some respondents tried to conceal the

actual facts regarding unfair trade practices followed by them.

(iv) The non-availability of detailed operational data from the individual branch has been

greatest limitation to the present study.

(v) There is no free access to the records; most of the information has been taken to be

true on the basis of the questionnaire.

28

(vi) Self-structured questionnaires have own limitation because such type of

questionnaires never used in previous research.

(vii) The present study is a study of sample. Alternatively, the complete universe

would have been studied. This has not been done because of two reasons.

First, it was not possible to study the entire universe with the limited resources and

time available at hand. Secondly, it is well established fact that the study of universe

and representative sample would provide similar results. It is in this background that

a sample study was opted. It is hoped that the results obtained would be appropriate

for the strata studied as well as the universe.

Of course, every possible effort has been made to achieve the goal of the present

study. Despite these limitations, researcher has tried to find out the significant conclusions on

the subject to the study.

29

REFERENCES

1) Chaudhary Harish Chandra, Consumerism and consumer Protection: A Paper presented

at all India Seminar on Government and Business Environment in India at Jaipur

(Rajasthan)

2) “Dealing with anti-competitive practices in the Indian pharmaceuticals and the health

delivery sector”, “CUTS C-CISR” No. 5/2008

3) http://www.blogandearn.in/blogs/unfair-and-restrictiver-trade-practices-by

Yaduvanshi1974

4) http://en.wikipedia.org/wiki/Pharmaceuticals_in_India

5) M S Nair, India: Product patent regime & Pharmaceutical industry in India- The

Challenges ahead, LEX ORBIS, Jan 2007, 58-65.

6) ZafarMirza, WTO/TRIPs, Pharmaceuticals and Health: Impacts and strategies, The

Society for International Development, SAGE Publications.

7) Gester Richard, “The phenomenal Growth of pharma Industries in India”, Marketing

mastermind, September 2008.

8) “Pharmaceutical Industry in India”, iNDExTB-Industrial Extention Bureau (A

Government of GujratOrganisation)

9) http://www.pharmaceutical-drug-manufacturers.com/pharmaceutical-industry/

10) Research on Rational drug use in India: A Glimpse; Delhi Society for promotion of

Rational use of drugs & India-WHO essential drug programme, study conducted at

Punjab university Health centre (PUHC), chandigarh

11) http://www.pharmabiz.com/article/detnews.aspşarticleid=167382sectionid=50