an opportunity for all: financial education in africa

TRANSCRIPT

MULTIMEDIA PILOT TRIAL

WHITE PAPER

OPPOR TUNIT Y INTERNATIONAL GLOBAL IMPAC T

Afr ica

OpportunityInternationalAfrica Region

‘An Opportunity for All: Financial Education in Africa’Opportunity International

2

Acknowledgements‘An Opportunity for All: Financial Education in Africa’ Multimedia Pilot Project has benefitted from generous contributions of time and effort by many individuals and organisations to which we say a special thanks.

The Financial Education Fund (FEF) funded by the United Kingdom’s Department for International Development is recognised for their contribution to the Financial Education work of Opportunity International in Malawi, Uganda, Mozambique and Ghana; to support the financial empowerment of poor people through impartation of skills, knowledge and confidence to manage their finances effectively and protect them from exploitation.

We are grateful to the theoretical and practical guidance, feedback and support from Alyna Wyatt Team Leader FEF and the FEF team throughout the design , implementation and data quality control of the evaluation activities.

Also acknowledged are the Chief Executive Officers in each country, namely Mr Aleksandr Kalanda of Opportunity International Bank of Malawi (OIBM), Mr Archie Mears of Opportunity International Uganda, Mr Cosmos Kowouche of Opportunity International Savings and Loans Ghana (OISL) and Mr Ian Campbell of Banco Oportunidade de Mocambique (BOM) Mozambique. A special mention is provided for the Transformation Managers Mr Luckwell Ng’ambi of OIBM, Mrs Linda Godinho of BOM, Mr Kojo Mbir of OISL, and Margaret Namazzi of Opportunity International Uganda and their respective teams who have worked so hard not only to make available financial education to clients and their communities, but also to protect the integrity of the research process.

The external evaluation and writing of the ‘Impact Evaluation Report’ (referred to within section 3 of this paper) was led by Mary Pennington; with Statistical Review and Data Quality Checks performed by Helen Gustafson. Mike Quaye, Regional MIS Project Consultant (Africa) on behalf of Opportunity International United Kingdom, facilitated the capture of MIS and transaction data across the 16 pilot branches contributing significantly in determining the total outreach numbers of this pilot project.

Special thanks is extended to Rebecca Ngo, Programme Manager Opportunity International United Kingdom for her tireless work behind the scenes from project commencement, and to Deborah Foy, International Programme Director, Opportunity International United Kingdom for providing great support and making generous contributions throughout the life of the project.

Finally, we acknowledge, thank and celebrate the 2052 clients across the four participating countries who provided invaluable insights and helped us access critical data and information on their financial capability and experience with the multimedia financial education pilot.

Robyn Robertson Lead Consultant & Project Manager ‘An Opportunity for All: Financial Education in Africa’

DATE October 2011

AUTHOR Robyn Robertson Lead ConsultantProject Manager

CONTACT INFORMATIONOpportunity International United Kingdom

Angel Court, 81 St Clements

Oxford OX4 1AWUnited Kingdom

Tel: +44 01865725304 (Oxford)

www.opportunity.org.uk

3

Table of ContentsExecutive Summary Theory of Change 4

Section 1: Design, Development & Building Process Process: Client Needs Analysis, Focus Group Discussions, Interviews 7 Design: Syllabus & Content Development Phase 7 Create: Scope, Style and Formula of emerging multimedia FE tools 8 Evolve: The evolution of the ‘formula’ for the multimedia concept 9 Key Considerations for designing, building and disseminating multimedia FE resources 11

Section 2: Engagement and Access Designed Dissemination Strategies verse emergence of Client Demanded Access Channels 12 Staff Financial Capability and Financial Literacy Capacity Development – The Key to Impact 14 Key Insights – Enhancing the quality of the transformational environment for dissemination 15

Section 3: Overall Assessment of Impact – The Evidence Pilot & Initiatives doing things differently and testing new concepts 16 Research Design, data collection instruments development, impact evaluation methodology, execution 16 The Most Significant Changes identified and attributable to the pilot 17 Outcomes & Recommendations for taking multimedia financial education efforts forward... 19

Section 4: Institutional Capacity Utilization: How to make best use of multimedia FE tools to enhance the impact of

your financial education 21

Closing Comments & Recommendations In Conclusion – Is financial education via suite of multimedia resources and dissemination

channels an effective approach to improving financial capabilities? 22 The Final Word... 24

Appendices The Overview 27 Pilot Sites 28 Unique Client Numbers 29 Objectives & Indicators 33 Indicator Results per Country 35 Syllabus & DVD Content per Country 37

44

Executive SummaryThis White Paper is a report on ‘An Opportunity for All: Financial Education in Africa’ Multimedia Pilot trial, which describes the process, implementation, outcomes, learning and discussion of results culminating in a final conclusion which answers the question ‘Is financial education delivered via a suite of interactive multimedia resources and technology driven dissemination channels an effective approach to improving financial capabilities?’ [See Appendix: The Overview]

Opportunity International has been present in the microfinance sector for over 40 years, driven by a conviction that escaping the poverty trap requires three things: passion, tools and skills.

Opportunity has continued to work hard over the years to create and provide a range of useful microfinance tools: Small Business Expansion Loans, Individual Savings Accounts, Agricultural and Insurance Products specifically tailored to assist really poor people to step up out of poverty. However a tool is only as good as one’s ability to use it! For most MFI clients’, their ability to use these tools is often hampered by low levels of literacy and limited education.

Whilst basic access to most financial services is rapidly increasing even for the poor, the majority are not sufficiently financially literate to leverage those services to their fullest gain, or to make informed, responsible or confident decisions about personal financial management.

In the recently released ‘Opportunities and Obstacles’ Report by the Centre for Financial Inclusion1, 301 microfinance industry stakeholders were asked to rank the top opportunities to generate financial inclusion for the poor – the number one existing opportunity cited across the board was in the provision of financial education. The biggest obstacle impacting the consumers’ ability to successfully navigate their journey toward financial inclusion and empowerment cited as low or limited financial literacy.

While rapidly emerging technology platforms provide new avenues to increase and improve financial inclusion of the poor (presenting particular benefits to consumers in remote areas), this technology driven push also present challenges to MFI client development and transformation efforts, reducing person-to-person touch points and impacting learning opportunities.

Acutely aware that the most important financial tool is not a product rather knowledge, skills and confidence; Opportunity International was keen to explore how technology could be leveraged cost effectively to enhance consumer’s financial capabilities, overcome disadvantage and risk by empowering clients to make best use of the microfinance tools on offer.

Whilst Opportunity clients engaged in group lending methodology, typically had some exposure to basic financial education training inputs, savers (often new to the formal financial system) and individual client (who typically and increasingly engage and access the MFI on their own terms and degree of frequency), were either inadequately or not catered for when it came to financial education, financial capability development and financial management training.

TH

E N

EE

D

1http://centerforfinancialinclusionblog.files.wordpress.com/2011/07/opportunities-and-obstacles-to-financial-inclusion_110708_final.pdf

5

At the pilot project formulation stage, assumptions play a key role. Where the platform of past experience and data are either not available or not consolidated and comprehensive, extrapolating from existing knowledge requires the complimentary use of assumptions to fill in the gaps. If these assumptions are not appropriately set up, the nature of the situation is distorted, and the problem cannot be solved appropriately.

‘An Opportunity for All: Financial Education in Africa’ articulated the following assumptions as playing a key role: Opportunity International Clients have low levels of financial literacy We can respond to low levels of financial literacy through client training We believe there could be real benefit for the client and the institution in delivering client

financial education training via suite of interacting multimedia resources and dissemination channels (Content Quality, Client Engagement Potential, Time Efficiency, Economies of Scale and Reliability)

Individual Clients and Voluntary Savers could be effectively reached primarily through ‘In Branch’ dissemination and subsequently via a range of ‘portable devices’ and complementary support materials allowing dissemination into market and community.

We could reach a target audience of over 110,000 low income individuals from the 16 pilot branches across the 4 participating countries during the project

An indication of a successful financial education intervention resulting in behaviour change would be evidence of the increased uptake by target segment of formal financial products and services.

An Opportunity for All: Financial Education in Africa pilot set out to find a high impact, cost effective approach for quality dissemination of Financial Education across the hard to reach target segment of individual loan and voluntary savings clients. The desired result: to offer financial education in such a way that it builds the confidence and capability of target audience, their families and communities to exercise initiative and engage in financial decisions with a sense of informed choice, leading to increased financial service penetration.

The project’s impact objectives were to evaluate whether the delivery of financial education via DVD and multimedia was an effective approach to improving financial capability, namely measured through four (4) objectives:[1] Increase the awareness of the target audience on a wide range of financial services; [2] Increase usage of savings accounts and insurance products by low income people;[3] Promote better management of credit and increased awareness of the dangers related to

multiple borrowing; and [4] Encourage a diversification of asset storage away from cash, particularly though the use

of ICT-based financial services.

The project deliverables were a unique set of 10 multi-media financial literacy training modules for each of the four (4) countries participating (designed and developed from detailed input generated from the Client Needs Analysis and FGD at the baseline).

The dissemination deliverables specified for the project pilot to roll out over sixteen (16) urban and rural branch locations in Ghana, Uganda, Malawi and Mozambique. [See Appendix: Pilot Sites] The Financial Education DVD resources were to be disseminated via plasma screens in Banking Halls and through portable devices to reach pilot branch clients in community, market and more rural locations. The project outreach target was to deliver Financial Education to over 110,000 low-income individuals across the life of the project.

AS

SU

MP

TIO

NS

DE

SIR

ED

R

ES

UL

TS

OB

JE

CT

IVE

S &

L

IVE

RA

BL

ES

6

The following factors held potential to influence the pilot project’s ability to create or capture change. These included: Human Capacity – Experience, Bandwidth & Confidence Contextualization – Cultural detail captured within Content Development Design and level of detail within Dissemination Strategy Dissemination Infrastructure Selection Institutional Buy-in Market Competition – Financial Products & Services + Financial Education Environmental and Man Made Disasters Relationship between MFI and Client

Evaluating the impact of the delivery mechanism and content of materials was a key component of the project. The project objectives and impact indicators were derived from a systematic evaluation approach based on the financial capability theory of change: knowledge; skills; attitudes and behaviour.

The project’s Impact Evaluation was based on a longitudinal study across the 16 pilot sites and 4 comparison sites across the 4 participating countries. A robust sample of 5% precision confidence was built with an initial 25% loading for dropouts - resulting in 2,052 Savers and Individual Loan Clients observed over the complete course of the study. A combination of qualitative and quantitative measurement techniques were used to evoke both a detailed understanding and derive generalized quantifiable findings. Survey Data – Collected at Baseline and Endpoint MIS Transaction Data Qualitative Methods – Needs Assessment, External midpoint in-country visits & focus groups

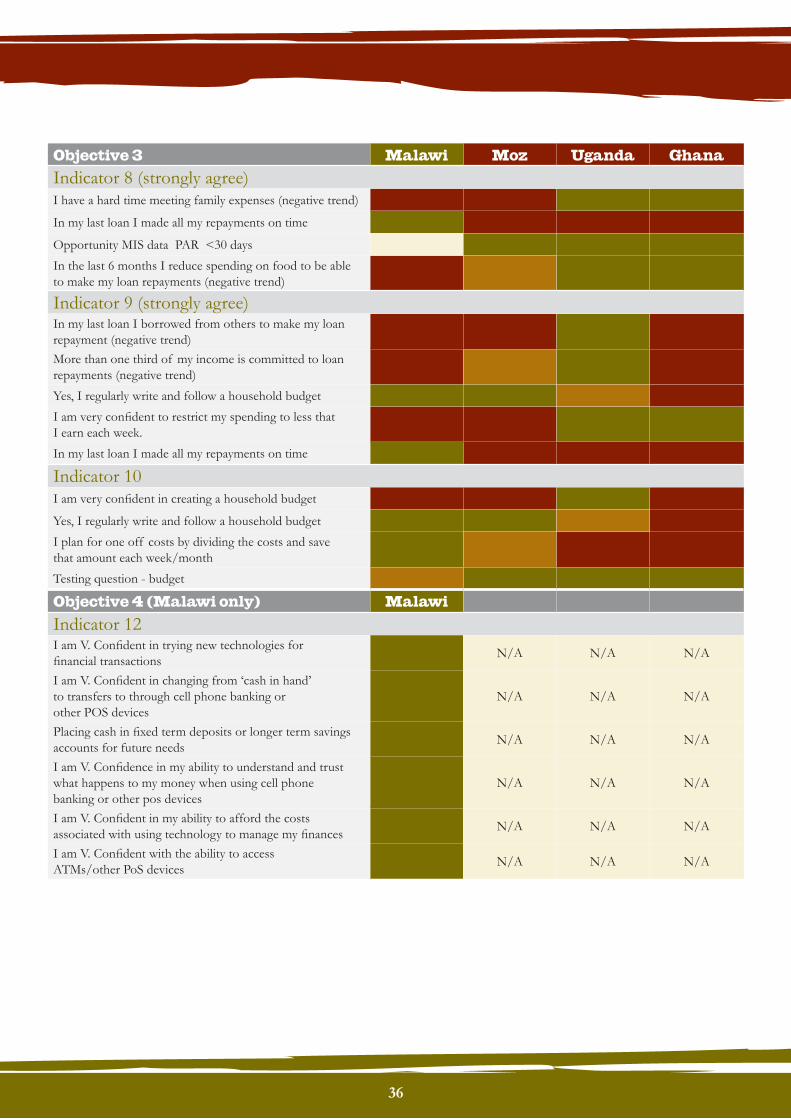

The project had four (4) objectives measured by twelve (12) impact indicators testing all four elements of the financial capability theory of change. [See Appendix: Objectives & Indicators] The impact evaluation analysed performance against these pre determined objectives and indicators.

‘An Opportunity for All: Financial Education in Africa’ Pilot was provided with £352,908. These funds were used to resource and achieved the following results: 2,052 Clients were studied across 4 countries in a longitudinal study 4 bespoke local language DVDs of 9-10 units were developed Hard Copy Support Materials (Comics and Board Games) were produced Pilot Branch Staff Capacity Development Training to over 350 Client Facing Staff Unique Pilot Branch Client Footfall (April – June 2011): 167,607 Clients Reached + Unique

Individuals Reached with Portable Equipment (April 2010 – June 2011): 122,629 = Grand Total 290,236 Unique Client/Individual Reached in Pilot Project

Pilot Branch Repeat Exposure (January 2011 – March 2011) – 227,752 Clients Total Unique Non Pilot Branch Footfall (January 2011 – March 2011) – 362,560 Clients Objectives 1,3 and 4 were met by individual Countries Investment into ‘An Opportunity for All: Financial Education in Africa’: £ 352,908 Cost per Unique Client Reach for this pilot Intervention £1.21 per person

INF

LU

EN

TIA

L

FA

CT

OR

SIM

PA

CT

E

VA

LU

AT

ION

RE

SU

LT

S

7

Section 1: Design, Development & Building Process Process Client Needs Assessment, Focus Group Discussions, Interviews Reliable information sets the scene for well founded syllabus and content development decisions. ‘An Opportunity for All: Financial Education in Africa’ pilot began with Target Client Segment Needs Analysis and Focus Group discussions. The intended outcome of this exercise was to ensure each project manager had exposure directly to the client target segment to gain a strong sense of where to focus the client financial education content. Further, to provide for each project manager an opportunity to unpack and examine individual client and cultural commonalities and differences related to financial management (attitudes, beliefs or habits) which could be drawn upon for inspiration to creatively develop contextualized client financial education training content.

The key insight gained from the client needs assessment and focus group discussion conducted in each of the participating countries, further confirmed through input gained from frontline staff interviews, was the need to actively avoid a ‘one size fits all’ construction of DVD content in preference of four (4) bespoke financial education DVDs given the emergence of cultural, content and creative differences.

Design Syllabus & Content Development Phase Employing multimedia tools into the learning environment has an array of benefits, but developing solid content and strong teaching elements within these tools is a challenging and complex task. The instructional design of the resource should be based upon careful examination and analysis of many factors, both human and technical, related to both adult education principles and the keys to visual learning.

The first factor considered was how the content of the resource will provide timely and responsive client solutions to expressed or demonstrated need. For ‘An Opportunity for All: Financial Education in Africa’ project, the following represent a collation of the key content themes which emerged from each participating countries Client Needs Assessment and Focus Group Discussions. [Appendix ‘Syllabus & DVD Content’ per Participating Country] Financial goal setting Basics of financial planning (budget & cash flow)

Knowing the true state of your finances Understanding and using credit wisely Debt management Understanding how formal savings products work Strategies for successful savings Managing the financial impact of risk Understanding new technology driven bank products Increasing financial security

The second aspect considered related to the client goals and motivation for self directed engagement with learning opportunities. Key questions clients ask when exposed to learning include: What is the content presented? What does this mean? How does this relate to what I know? How can I apply this to the situation I am in right now? Adults within the target client segments expressed belief that the strongest motivation for learning and applying was generated by internal or immediate crisis or pressure and the ability to access ‘just enough’ information ‘just in time’. Understanding this dynamic requires resource developers to ask themselves: What prior experience of the audience needs to be recognised? What will be the right mix and degree of complexity of content to present? What are the important content elements that will require cultural contextualization? How will the resource offer a link between financial management theory and real life situation application? How will the audience access the information immediately upon realization of a problem or challenge?

Finally, the last key aspect to consider is the visual elements as they relate to the content themes. When is sound more meaningful than a picture? How much text or copy is too much? Does the graphic or image overwhelm the screen and distract from the central message attempting to convey? Visuals must be congruent, relevant and consistent with other information presented in order to be effective. Care needs to be taken when using visuals simply for aesthetic reasons. The misuse of even a single visual element can cause misrepresentation of information and become a barrier to content and impede learning even if the program overall may, in all other aspects, follow the principles of instructional design.

Example: The OISL Ghana DVD included a proverb titled ‘The Ant and the Vulture: The story of procrastination

8

and denial’ within the unit on Financial Planning and Financial Denial. During production week, the opportunity to capture a ‘vulture’ or even a Ghanaian bird as a suitable substitute did not present itself. Footage had been captured of the Marabou (large ugly version of a stork) while in Uganda, so a decision was made to substitute the ideal footage of a vulture for what was already on file. Whilst the end resource looks visually effective and the content and metaphor convey the financial principal contained within the proverb; clients during mid point evaluation focus groups consistently provided feedback that while they found such humour in the bird selection, they were unable to recall the proverb let alone the meaning intended to be conveyed through the clip.

Create Scope, Style and Formula of emerging multimedia FE Tools Multimedia simultaneously weaves a combination of various formats into a single learning environment: text, video, photography, sound, graphics, illustration and animation. With multimedia the process of learning can become more participatory, enabling the role of teacher to evolve into the role of facilitator with the client much more responsible for their own exploration, discovery and learning experience.

The desired outcome for this multimedia Financial Education project was to achieve sustained change through addressing knowledge and skill development, attitude and emotional change, and behavioural change towards creation of positive financial habits.

Language Used in Training Choosing which language to film content in and/or provide subtitles for (out of multiple official languages or regionally specific sub dialects possible) was a key consideration and challenge for the overall project as much as for each participating MFI. For budget reasons, each participating country was asked to select a single language most able to facilitate client’s ability to engage and understand the training content of the DVD in the pilot branch locations. For Malawi and Ghana, whilst multiple language options existed, given the regional specificity of languages and corresponding location of pilot sites, the decision was relatively straightforward. However upon analysis of the midpoint and endpoint impact evaluation data, the language chosen in Uganda and Mozambique may not have correlated closely

The Formula

The pedagogical framework used by ‘An Opportunity for All: Financial Education in Africa’ followed a simple yet powerful ‘formula’ for change...

Start where people are currently at! Catch the ‘voice on the street’. Allow the audience to hear a range of people just like them describe behaviours, attitudes and beliefs around key financial themes, connecting and engaging the audience within the dialogue.

Next, know where the target audience gaps, questions and confusion points are within each financial education theme (ascertained from the Client Focus Group discussions and Needs Assessment). Provide information, demonstration, examples of application to impart knowledge which is directly connected to this immediate need. Connect new knowledge, information or skills to something the audience can immediately take and use to solve a current issue they face.

To finish, provide a powerful motivator. Understand the question clients frequently ask, ensuring the client testimony presented clearly builds the case for each viewer to consider making changes. Use people from the target population to share their testimony. Provide the answer... ‘If you do embrace these changes, your future reality could be significantly better than your current reality!’

Breaking the financial education themes down into multifaceted multimedia presentation certainly can act as a catalyst for new discovery by clients, but unless consumption is followed by a chance to use new discoveries, rehearse ideas or demonstrate what was learnt, the knowledge acquired soon becomes knowledge forgotten. The augmentation of comics, board game and flipcharts alongside capacity development of client facing staff to effectively interact with the audience around DVD content was always going to be a critical aspect of optimizing impact.

9

enough with selection of project pilot sites, potentially adversely affected the impact of the training.

Client from two (2) of the four (4) pilot sites selected in Uganda indicated that while able to understand Lugandan they want resources in their specific language or regional dialect when it comes to absorbing important information or learning.

In Mozambique the client needs assessment indicated that the DVD should be filmed in Portuguese with English subtitles. However midpoint client feedback later determined that Portuguese is not spoken as widely as first reported in the northern rural pilot branches. In Tete, for example, it is estimated that only 40% of the population speak Portuguese well enough to understand the existing DVD. This factor alone is significant enough to singlehandedly be responsible for a loss in client interest in the multimedia training as it was not their preferred language and thus confusing.

Evolve The evolution of the ‘formula’ for the multimedia concept The suite of resources developed through the pilot ‘An Opportunity for All: Financial Education in Africa’ are highly designed at the back end to ensure they capture core content in accurate, concise and engaging ways and skip right over low literacy and formal education obstacles.

The role of Symbols, Narration and Characterization Multimedia resources should benefit the user by being easy to use, enhanced by a well designed personal interactive interface. Opportunity Uganda took a creative step forward from the original design used to build the Financial Education DVD’s (in Malawi, Mozambique and Ghana) and added a ‘sticking agent’.

The Transformation Project Manager for Opportunity Uganda, through insights gained during the client focus group discussions, initiated exploration of the possible value of linking training segments and client stories to a narration element or lead character. The rationale for this was to attempt to find a way to bring the richness of African Storytelling into the way we were attempting to deliver training - in an effort to ensure the development of a more culturally appropriate training tool whilst enabling greater client engagement with and retention of the content.

As a result of this initial conversation, the concept of going on a financial ‘journey’ was born. The goal of the script development team, was not only to find a way to deliver the ‘what’ of financial literacy and money management, but to explore a way to link all the segments of training together so people actually discovered ‘why’ they should care about the content of the training and mobilize them toward ‘going further on their own financial journey.’

The inclusion of a series of short narration segments presented by a central character Mr Mutambuze (meaning ‘Journeyman’ or ‘Sojourner’) provided the audience with a personal guide for their financial journey. This character has a quirky edge, achieved through life size cartoon figure filmed through stop gap animation and real time pieces to camera, combined with animation and one dimensional cartoon elements. His content delivered via carefully selected and field tested voice over.

Animation was used to enhance demonstration of ideas or illustrate a concept of rapid sequence more effectively than video from real life could deliver. Further, in an effort to overcome low literacy levels, Opportunity Uganda explored the use of key symbols linked to each Financial Education theme to achieve visual connection between the DVD and the suite of additional multimedia financial education resources.

Mr Mutambuze and Bwabye Hanifa (blue), Opportunity Uganda Client

10

The incorporation of narrative interactivity and strong use of visual cues for content linkage aided and enhanced client content acquisition speed. Clients demonstrated capacity to accurately tap into their recognition memory recalling with very high levels of detail colour, form, visual sequence, illustrations and pictures used as metaphors – that contrasted sharply with the same client’s limited recall of training which relied on plain text or stand alone audio content.

Mr Mutambuze and Bwabye Hanifa (blue), Opportunity Uganda Client

Emergence of an additional Suite of Multimedia Financial Education Resources In addition to the video component, augmenting training tools emerged over the course of the pilot which included:

Comics - that supported content recall and encourage the audience to immediately put new and relevant knowledge and skills into practice

In order to reinforce the key concepts and highlight the flow of thought underpinning the DVD training segments, ‘An Opportunity for All: Financial Education in Africa’ Project embarked on

exploration of various ways hard copy resources (such as ‘comic strips’ and ‘cartoons’) could be utilised.

Character based cartoons were developed to capture the features of staff and clients featured in the video, and mirror the teaching segments on the DVD, and even where appropriate to be incorporated as B Roll footage (additional visual support footage) within the edit phase of the DVD’s to serve to create visual and conceptual learning links for client audiences.

Once the artwork was developed, the graphics and English comic strip script was circulated between participating Institutions, and simply translated into local vernacular and printed as hard copy resources (fliers) which Client facing staff or customer service staff then made available to inquiring clients.

Financial Education Board Game – designed from a cognitive behavioural therapy framework, that brings the Financial Education DVD content alive through discussion, humour and competition

11

Storyboards Flip Charts – that field staff can use which capture the visual and key message content of the video in hard copy to take out beyond the technology reach

BOM Mozambique: Using Comics and Flip Charts to complement the Financial Education DVD screening in the marketplace

Multimedia Staff Training Workshops – As with any innovation, the installation of new technology, new resources and new training methodology inevitably brings with it the need for staff development to support optimal utilization of resources. To ensure staff could appropriately facilitate and support client engagement with the suite of multimedia financial education tools, multimedia staff training workshops were rolled out across the pilot branches.

The value of staff training should not be overlooked. The full potential for multimedia based client training can only be realized after there has been a re-engineering of the training techniques and understanding of the desired learning environment staff should be offering.

Key Considerations for designing, building and disseminating multimedia FE resources Client Needs Assessment and Focus Group

Discussions are foundational to any syllabus formation and content creation

Carefully create ‘copy’ to integrate intentionally with the design and selection of visual inclusion as these act as the keystone tying all other resource elements together

Use familiar metaphors and analogies, feedback and personalization to augment client motivation

Multimedia should be designed to support, relate to or extend learning not just as embellishment

An integrated suite of resources presented simultaneously rather than consecutively to audience, ensures the Financial Education Multimedia Intervention achieved both broad and focused financial education impact with greatest potential for content reinforcement

There is a correlation between the rich African heritage of storytelling and inclusion of character driven messaging

Given the literacy rates of the target client segment, there is significant value in designing communication which transcends language obstacles and consistently utilizes symbols as reinforcement, visual linkage and information pegs

The greater the cultural detail and bespoke the content, the greater the engagement by audience

12

Section 2: Engagement and Access Learning requires personal integration and the ability to make sense of the new information at the same time apply it in ones daily life. Creation of a truly effective multimedia learning experience requires careful consideration of how exposure to the resource can be supported by opportunities for interaction, feedback, rehearsal and the ability to connect with content on multiple occasions to strengthen the learning over time. The degree of consideration given to engagement and access aspects of any multimedia training model will determine how effective it is as a learning format and how consistently achieved the learning outcomes.

Designed Dissemination Strategies verse emergence of Client Demanded Access ChannelsThe initial DFID FEF An Opportunity for All: Financial Education for All application identified plasma screens and DVD players as the primary channel for equipping brick and mortar branches to offer the individual voluntary saver or individual loan client access to multimedia financial education. Further, portable devices were identified as a secondary channel to ensure a complimentary mix of technology was on offer and able to maximize the reach and frequency of access to the DVDs by the target population.

Upon analysis of Client Needs Assessment, a unique dissemination strategy was developed for each participating pilot branch, which specified the optimal and most appropriate mix of infrastructure; permitted given that the key focus of this project was to test the effectiveness and impact from delivery of client financial education via a multi media suite of resources (revolving around the10 unit financial education DVD series), not exclusively to test the effectiveness of plasma screens installed within banking halls.

Banking Hall foot flow at OIBM Branches across Malawi

Pilot Project Assumption proves Incorrect: One of the key assumptions made by An Opportunity for All: Financial Education in Africa pilot was that individual client target segments would be most effectively and primarily reached through In-Branch delivery channels (plasma screens).

In heavily subscribed densely populated branches with large individual client portfolios, clients reaffirmed efforts to disseminate financial education through In-Branch delivery channels while they waited for a transaction or assistance (especially in Malawi).

However in Ghana, Uganda and Mozambique (despite initial confirmation of the assumptions related to client footfall and duration of exposure to banking hall screening coming from the Baseline Client Needs Assessment) once the pilot began the dissemination phase, feedback from target client segments began to emerge that they did not spend long enough in the banking halls to be able to watch complete segments of the DVD, although several clients within the mid project evaluation focus group discussion did report that they had intentionally stayed back at their branch especially

13

to watch the entire film of 90+ minutes in duration to ensure they did not miss out on the information being provided for free.

It is worth highlighting that a DVD training segment averages 9 to 12 minutes in duration (broken into components of 2 minute drama or vox pop street interviews + 4-6 minute teaching or skill demonstration + 3-5 minute client story).

In addition, where solidarity group footfall was reviewed, it was determined that only the group leaders were regularly coming into the banking halls on the day of payment on behalf of the group with the majority of group members never or seldom enter the branch.

This deeper understanding of client footfall and access trends highlighted the need to place greater and equal emphasis on optimising portable delivery channels, as opposed to relying as heavily upon in branch delivery.

Opportunity International Uganda: Mobile Lending Van & Financial Education Training

BOM Mozambique: Agricultural Farmer Financial Education Training Outreach

Opportunity International Uganda: Community Financial Education Sensitization Church Partnership

Opportunity International Uganda: Community Financial Education Sensitization Church Partnership

Emergence of Client Demanded Access Channels Although the dissemination strategies for this financial education DVD were developed from and responsive to gathered client and staff input, the majority of training opportunities were (in hindsight) still largely determined and dictated to clients by the institution (such as how long the DVD was put on loop in the banking halls, when the multimedia portable screenings would occur in the village or house where a group meeting was going on, or how frequently partnerships with other non government organizations would provide Opportunity the chance to piggyback on their event for dissemination).

Allowing clients to control, manipulate and explore resources autonomously was not something deeply considered at the multimedia pilot trial design phase. However two interesting events happened which highlighted the significant client demand for increased opportunities for self initiated learning and client determined access.

14

Event 1: In Malawi, clients who frequented branches not screening the Financial Education DVD, discovered via word of mouth that OIBM was offering new ‘information’ in the next community, and went to the trouble of getting private transport so as to make the 50km journey to simply view the ‘money information’ as they didn’t want to miss out on anything which may help them come up in life.

Event 2: In Ghana, clients managed to get a hold of a single copy of the official Financial Education DVD, and burn multiple rough copies. These entrepreneurs then decided to create a Financial Education video lending library business. OISL field staff rectified the issue of charging other clients to access Financial Education, whilst praising the initiative and passion. As a result the creation of ‘Financial Education Champion Clients’ with the responsibility to administer the ‘free’ Financial Education DVD take home lending library through their existing shops or stalls.

An Opportunity for All: Financial Education in Africa Pilot made an initial assumption that the banking halls would be a convenient location for clients’ self determining their access to financial education through frequenting the banking halls and branches. However qualitative feedback gathered throughout the programme portrays that the initial project assumption may be misplaced, and could be a significant confounding factor to consider when analysing the impact results.

Institutional designed dissemination strategies need complementary client driven access opportunities. Clients in all countries commented that they wanted

the DVD taken out to their communities to watch in the market place or church halls and many said they would like to have their own copy. Further, Clients have suggested that the financial literacy material is made available to their children whilst still at school to better equip them for adulthood, and in all locations, clients were eager for the materials to be more accessible in their home and work locations.

Staff Financial Capability & Literacy Capacity Development – The Key to ImpactAn Opportunity for All: Financial Education in Africa pilot intentionally focused on enhancing the environment into which a client would enter and engage with the Financial Education multimedia.

In order to design and build appropriate client facing staff capacity a Staff Financial Education Knowledge, Skill and Confidence Audit was undertaken. Staff identified for this review and specific training included but are not limited to Teller Staff, Field Staff, Client Relationship Officers, Customer Service Staff, Mobile Banking Staff, Satellite Staff, Area Managers and Loan Officers in each pilot site.

Specific capacity development training was then developed which focused on exploring how staff through their respective job functions could build safe, supportive, empowering learning environments and enhance client engagement with and learning from the DVD training resource (including enhancing staff capacity for effective use of any supporting hard copy training tools with clients).

A generic Staff Capacity Development Training Script and Lesson Plan was developed as a template for local Project Teams, to guide the specific training.

Attitudes & Beliefs Examination To create and grow a supportive conversational

learning environment which offers personal challenge points for clients toward making positive financial behavioural change

To deepen clients self awareness of their financial attitudes and behaviours (through strategic questioning approach)

To support clients (through optimizing dialogue opportunities), to examine, negate or avoid attitudes or beliefs which would maintain their poverty exposure or make them more financially vulnerable

15

Information & Knowledge Acquisition To confirm (or clarify) for clients their previous

financial education learning (group or workshop trainings or personal coaching)

To provide reinforcement to clients of key principles and concepts supporting the financial training content delivered through multimedia channels

To offer additional motivational support for clients to engage with the multimedia training materials so as to acquire additional financial information or knowledge

Experiences & Behaviour Change To work towards increasing one to one connection

between staff and clients – so staff can effectively facilitate and empower clients progress toward personal financial objectives and individual implementation of relevant key learning (either directly or through referral to customer service staff)

To assist clients to successfully navigate any barriers encountered while seeking to implement new financial learning

It is important to note, that staff underwent training to enhance their facilitation skills and handling client FE DVD related questions. Many staff members said that they had benefitted personally from the lessons in the DVD specifically in relation to Savings and Budgeting. All staff was enthusiastic about the prospect of using the DVD in Client communities. However, it is important to note that there was a proportion of staff which remained anxious or not confident to engage in dialogue with Clients, and some who even actively avoided client engagement around financial literacy. In instances where such interpersonal dynamics surfaced there was obviously potential limitation on Financial Education optimization.

Case Study: Both Stelson Ashaba and Stephen Senyonjo work at Opportunity Uganda as Relationship Officers, in Masaka and Iganga branch respectively. Before attending financial education training at opportunity Uganda, they had no idea of spending their monies and using their salaries wisely, which exposed them to the dangerous cycle of multi borrowing from colleagues and shop attendants. Since attending the Staff Financial Education training, both have changed their spending habits and have worked their way out of the debt trap. Stelson has since reduced his huge expenses by cutting

on the number of trips to Kampala from four to two a month, cutting air time from $40US dollars per month (100,000 Ugsh) to half and shifting to a relatively cheaper house. While Stephen has stopped impulse buying and now he sticks to his monthly budget. By cutting down on their expenses they are able to live within their monthly incomes and have money set aside for saving.

Key Insights – Enhancing the quality of transformational environment around dissemination Client facing staff capability development training

is a ‘must’. Without this training, where client facing staff confidence is low, financial education learning optimization and impact is significantly reduced. Training has shown to increase the experience of a safe learning environment for clients, where dialogue, rehearsal, question and answer opportunities and support is provided.

Staff also require and benefit from Financial Education There is a need for a mix between Institution

designed and driven Financial Education dissemination strategies and client controlled access channels

Staff need to be trained how to encourage clients to actively process and integrate learning rather than receive passively

Multimedia Financial Education Resources lend themselves well to a host of strategic dissemination partnerships (with or without owner institution presence) to leverage initial investment

16

Section 3: Overall Assessment of Impact – ‘The Evidence’Pilot & Initiatives An Opportunity for All: Financial Education in Africa’ pilot, did not seek to measure success or failure, rather to remain focused on uncovering, using and sharing information about what was effective at empowering people to do more with the money they have, and to overcome disadvantage and risk by showing them how to make best use of formal financial products available. Further, the project sought to document and explore delivered outputs, outcomes and impact so as to reduce assumptions and increase knowledge about financial education interventions; necessary for successive evolution of the idea that multimedia resources and technology driven dissemination channels hold the key to increasing financial capability and behavioural change effectively.

Peter Drucker (1998)2 emphasises that the progress of innovation is uneven rather than continuous and the payoff is rarely immediate. An effective innovation must be approached from a position of openness to learn at least as much from aspects of apparent failure or what works in ways different from anticipated as from what works as hoped or expected.

In the paper ‘Can Financial Education Change Behaviour? Lessons from Bolivia and Sri Lanka’ (2009)3 Gray & Sebstad suggest that assessing the outcomes of financial education requires paying attention to more than just the indicators of behavioural change or looking solely at the influence of financial education on the uptake of particular financial products. Rather, that assessing the outcomes of financial education requires understanding the fluidity of financial behaviours influenced by ever changing internal and external factors; and exploring the factors that make financial education most effective: Quality and frequency of the education Relevance of the education to the target population Opportunity to use the education Context in which people can exercise their new

wound financial behaviours and Appropriateness of use of a financial products

on offer

Research DesignEvaluating the impact of the delivery mechanism and content of materials was a key component of the

project. The project objectives and impact indicators were derived from a systematic evaluation approach based on the financial capability theory of change: knowledge; skills; attitudes and behaviour.

The project’s Impact Evaluation was based on a longitudinal study across 16 pilot sites and 4 comparison sites across the 4 participating countries. Where possible both rural and urban branches were used to allow comparison. [See Appendix Pilot Sites]

A robust sample of 5% precision confidence was built with an initial 25% loading for dropouts - resulting in 2,052 Savers and Individual Loan Clients observed over the complete course of the study. A combination of qualitative and quantitative measurement techniques were used to evoke both a detailed understanding and derive generalized quantifiable findings. Survey Data – Collected at Baseline and Endpoint MIS Transaction Data Qualitative Methods – Needs Assessment, External

midpoint in-country visits & focus groups

The project had four (4) Objectives measured by twelve (12) Impact indicators testing all four elements of the theory of change. The impact evaluation analysed performance against these pre determined objectives and indicators. [See Appendix: Objectives & Indicators]

A bespoke Financial Education Survey was designed and tailored to measure the project objectives and indicators. This was conducted at the baseline (April 2010) to establish a clear position of clients financial capability of both the test and comparison sites. It was conducted again at the endpoint (April 2011) to measure any change.To support the self-reporting questions in the Survey, MIS data, capturing clients banking transactions, was extracted within the longitudinal process to cross reference these statements. This is predominantly in relation to clients savings behaviour. MIS Client Transaction Data includes: Frequency of withdrawals; Number of voluntary saving accounts; Amount on deposit; Deliquency rates.

2Drucker, P. F. (1998, Nov-Dec) ‘The Discipline of Innovation’, Harvard Business Review 76(6): 149-156. 3Gray, B., Sebstad, J. et al (2009) Can Financial Education Change Behaviour? Lessons from Bolivia and SriLanka

17

Due to the importance of reliable data, an External Statistician was used to ensure data quality control, undertaking a data quality check and statistical summary of the baseline and end point raw data and statistical analysis and cursory review of the report findings.

An initial Client Needs Assessment through focus group discussions with clients was carried out in the participating institutions to ensure that the material responds to the needs of the clients.

An External Midpoint Visit was carried out to evaluate the deployment of the DVD in each of the test sites. This gathered an understanding of the quality, relevance and perceived success of the intervention. It consisted of key stakeholder interviews and focus groups generating feedback from over 135 staff and 242 clients, resulting in a Midpoint Report submitted to the Department for International Development in Q1, 2011.

A Project Team Workshop was held to address the questions, to help understand and to complement the information emerging from the end line results. The workshop consisted of the Lead Consultant/Project Manager, each of the in-country Transformation Managers and an Operational Staff Member from each participating institution.

Impact Evaluation conclusions from this quasi-experimental approach compared the mean (or average) of the experimental pilot group with that of the comparison group to determine the percentage change from Baseline to Endpoint per Objective. If there was more than a 5% or greater positive change, the objective was declared ‘met’. The implicit assumption, that the larger the percentage result on a criteria the better the benefit and the more successful the intervention. [See ‘An Opportunity for All: Financial Education in Africa Impact Assessment Report]

Clients in the Focus Group in Chimoio, Mozambique

The Most Significant Changes identified and attributable to the pilot

After minimum of 9 months and maximum of 11 months exposure to the multimedia financial education resources (due to staggered Go Live phase), we see evidence of small yet statistically significant signs that the intervention produced positive steps forward toward achievement of financial capability and literacy impact; increasing client’s ability for financial planning (primarily through budget creation and use) as well as contributing to clients ability and confidence to make informed choices around the selection of formal financial products. Further, we also see evidence that the financial education intervention contributed to an increase of confidence and willingness to build foundational financial disciplines such as restricting spending, building savings and more fully utilizing existing financial products.

18

‘An Opportunity for All: Financial Education in Africa’ Impact Evaluation demonstrated the following results for each objective:

Objective #1To increase awareness of target audience on wide range of financial services available to them

Objective 1 was met in Uganda.

Objective #2 To increase usage of savings accounts and insurance products.Objective 2 was not met in any country.

Objective #3To promote better management of credit and increased awareness of the dangers relating to multiple borrowing

Objective 3 was met in Malawi.

Objective #4 To encourage diversification of asset storage away from cash, particularly through the use of ICT - based financial services (Smart Cards, ATM’s and POS devices).

Objective 4 was met in Malawi

However, mean scores invariably hide the true meaning found in analysis of the results at the indicator level as well as individual questions within each indicator. To this end it is important to show the breakdowns.

Ghana

The DVD has contributed to an increase in client’s ability to...

Determine the features of an insurance product Deposit their savings into formal savings product

The DVD has contributed to an increase in the client’s confidence to...

Restrict spending to less than they earn

Uganda

The DVD has contributed to an increase in client’s ability to...

Determine the features of a loan product Effectively use an insurance product

The DVD has contributed to an increase in the client’s confidence to...

Ask questions about products at a Bank or MFI Make complaints at a Bank about products & services Restrict their spending to less than they earn

The DVD has contributed to an increase in the client’s willingness to...

Deposit their savings into formal savings products

Malawi

The DVD has contributed to an increase in client’s ability to...

Determine the features of an insurance product Determine the features of a savings product

The DVD has contributed to an increase in the client’s confidence to...

Deposit savings into formal savings products

The DVD has contributed to an increase in the clients willingness to...

Save more regularly and withdraw savings only for immediate needs

Mozambique

The DVD has contributed to an increase in client’s ability to...

Effectively use an insurance product Correctly create and use a household budget

The DVD has contributed to an increase in the client’s confidence to...

Determine the features of a savings product

[See Appendix Indicator Results Per Country]

The project set out to determine whether the delivery of financial education via DVD/multimedia is an effective approach to improving financial capability. Data suggest that where messages were reinforced and repeated in more than one training unit, there was a greater impact on clients’ ability to understand and use the information. For example, in Uganda 4 of the nine modules focused on understanding financial products and terminology, thus resulted in Uganda meeting Objective 1 which measures the increase in Clients’ awareness on the range of financial services available to them.

19

Whereas OIBM in Malawi, as a savings led organisation with a reputation for innovation and being ahead of the technology curve, targeted 3 of the 9 financial education DVD units around M-Banking and familiarization with technology, which resulted in an overwhelming meeting of Objective 4.

Contemporary learning theorists such as Bereiter4, Brown5 and Spiro6 believe that a key goal of educators working outside traditional educational fields, is to provide opportunities for learners to develop mastery in the areas of life they are each involved but lacking confidence to embrace. Contemporary learning theory goes on to suggest that confidence is achieved through the development of clear simple mental models that effectively represent reality.

In the case of the OIBM Malawi financial education DVD, instruction on how ATM, Cell Phone Banking and Point of Sale Devices that helped clients build accurate yet simple mental models around how these products work, what happens to the cash and what to do if issues surface, enables clients to trust and engage confidently with new technology driven baking. This reinforced the hypothesis that some financial education topics are more effectively conveyed through presentation of content and visual overlay simultaneously and via rapid visual sequencing (real life overlay or animated graphics) rather than consecutively or via audio or text in isolation.

Whilst the results in Mozambique and Ghana suggest that they haven’t met the project objectives, the achievements within individual project indicators suggest that the training has increased clients’ financial capability.

Key achievements for Mozambique include an increase clients’ ability to determine the features of a savings product and an increase in clients’ ability to correctly create a household budget.

Key achievements for Ghana include an increase in clients’ ability to determine the features of an insurance product, an increase in clients’ ability to deposit their savings into formal savings products and an increase in clients’ ability to correctly create a household budget.

In response to the overall question ‘Is financial education delivered via a suite of interactive multimedia resources and technology driven dissemination channels an effective approach to improving financial capabilities?’, the overall results suggest that the financial education training via DVD is an effective approach to improving financial capability.

☑ The DVD training has exceeded the targeted outreach numbers of 110,000 clients. Unique Client Pilot Branch Footfall (April – June 2011): 167,607 Clients Reached + Unique Individuals Reached with Portable Equipment (April 2010 – June 2011): 122,629 = Grand Total 290,236 Unique Client/Individual Reached in Pilot Project

☑ The content of the training material has proved easy to understand, tailored to the audiences’ need and has had a demonstrable impact on improving clients’ financial capability, albeit with the results varying across the countries.

☑ Objective results that portray an increase in financial capability are clearly visible and have been met in Uganda and Malawi

☑ Objective results for Mozambique and Ghana are less evident but indicator results remain significant to suggest a trend toward an increase in financial capability.

Outcomes & RecommendationsAs this was a pilot project, a number of operational and implementation issues were identified that could be worked on to improve future versions of this concept. These include:

Re-evaluation of the cost benefit analysis for Quasi Random Control Trial to determine impact given the disproportionate allocation of budget, time and human resource compared to potential benefits of scaling back the impact evaluation in favour of redirecting resources into the design, development and dissemination elements of the project

Behaviour change indicators were less successful than the indicators measuring confidence or knowledge gain however given the short exposure phase, a key learning is that more client exposure to

4Bereiter, C., and M. Scardamalia (1996) Rethinking learning. In D. Olson & N Torrance (eds) Handbook of education and human development: New models of learning, teaching and schooling (485 – 513) 5Brown, J.S. and P. Duguid (1989) Situated cognition and the culture of learning. Educational Researcher, 18(1), 32-42 6Spiro, R.J., M.J.Feltovich, and R.J.Coulson (1991). Cognitive flexibility, constructivism and hypertext: Random access instruction for advanced knowledge acquisition in ill-structured domains. Educational Technology, May. 24-33

20

resources time is needed (minimum of 12 months) to translate information and knowledge acquisition into a clear, positive trend towards behaviour change, a position widely supported by industry stakeholders.

Review of key assumption, specifically: (1) that primary dissemination channel for individual loan clients and voluntary savers would be via in branch screening; (2) that success of Financial Education intervention would result in an increased uptake from target segment of formal financial products and services

Ensure Project Indicators only measure one rather than multiple elements

Refine the number of survey questions under each indicator and ensure superfluous questions are removed

Test survey instrument not only in field with clients, but from an analysis aspect

Re-sequencing of the project phases to ensure design, development and dissemination aspects interfaced more effectively

Greater investment into adequately researched then designed dissemination strategies

Increasing emphasis on enhancing the quality of the ‘environment’ into which Financial Education resources are injected

21

Section 4: Institutional CapacityUtilization: How to make best use of the multimedia FE tools to enhance the impact of your financial educationTo optimize the potential impact of multimedia financial education resources, an institutional appetite for innovation; capacity to create a conducive learning environment, investment into building a competent front line staff client interface and an effective dissemination strategy is required.

Effective dissemination is contingent upon all internal stakeholders being aligned behind a single strategy. It is essential the institution has widespread understanding of the links between client financial education, consumer protection and overall strong institutional performance. This understanding ensures consistant key messaging that Client (consumer) financial education is critical and much more than simply a ‘nice to have’ additional activity outside of the institutions core business. Optimal impact is achieved where an institution has ‘across the board’ buy-in cascading from the top executive or management down to the front line staff client interface.

The following are key challenges to carefully consider so no unnecessary risk threatens or limits the potential impact of your multimedia financial education intervention.

The degree of intentional consideration of dissemination objectives within the strategic planning processes, core business and core operational processes affects dissemination effectiveness and overall impact. Planning exercises or strategic executive management decisions should be well informed of the financial education project developments and trajectory to ensure every opportunity for supporting, leveraging, integrating or piggybacking the financial education objectives with overall institutional direction can be achieved.

Importance should be placed on ensuring effective communication and coordination between Project (Transformation) Officer, Management and Branch Management. Where limited dialogue or ineffective communication between the Project Officer (Transformation Manager) and Senior Management and Pilot Sites (Branch Managers) occurs, potential exists for different interpretation of targets, approaches and commitment to dissemination objectives.

Prioritizing Financial Education in a Resource Limited Environment – The reality is often a gap between activities described in plans and what is required to translate plans into effective implementation on the ground. The gap is more likely to occur when institutional planning sets objectives and activities to achieve, with limited knowledge or consideration of the resources available or the logistics required. Prioritization processes in a limited resource environment are often overlooked during a pilot planning process and therefore become the silent ‘white ants’ to the dissemination strategies chances of success. Alignment and integration of the dissemination strategy to the overall institutions strategic and business plans and objectives is an important consideration to take into account as early in the planning process as possible.

Emerging Capacity needs Supporting – The level of skill, experience and capacity required to design, create and develop financial education resources is an element of the program often under-appreciated and under resourced. Further, when it comes to the elements and demands upon project managers to effectively mobilize dissemination, capacity gaps or limitations are not only under resourced but often underestimated. Skill and capability is needed to motivate, mobilize, monitor, ensuring compliance, proactively anticipate and navigate roll out obstacles - without such capacity the dissemination strategy is impeded.

The importance of Hands on Monitoring – Often the tendency is to take the hands off the wheel when it comes to the dissemination phase, as the deadlines for deliverables are further away (ie. evaluation activities only requiring attention towards the end of the pilot phase), however a successful dissemination strategy requires inbuilt regular review and monitoring to ensure progress is tracked, required changes are made, dissemination targets are achieved and return on investment is delivered.

The value and importance of Executive or Management buy in and support for the initiative during the pilot phase even before the cost benefit analysis and impact evaluation is available – There are valid reasons why an Institutions Management may want to restrict enthusiastic support of a pilot until the external

22

evaluation has been produced, however there are times where such a decision to postpone buy-in or delay institution wide extension of support could confuse the key messages disseminated within the Institution as to whether the initiative is officially supported or not. Impact Evaluation data should always proceed additional major investment into expansion of a pilot, however in some situations lack of vision or lack of executive or management ‘will’ to try something new is the actual obstacle to maximizing impact.

Conclusion...Is financial education delivered via a suite of interactive multimedia resources and technology driven dissemination channels an effective approach to improving financial capabilities?’There are many ways to determine effectiveness. For the purposes of this paper, three major criteria have been selected to determine if ‘An Opportunity for All: Financial Education in Africa’ can be categorized as an effective intervention: (1) The extent to which it responded to the identified need; (2) The degree to which the pilot met objectives and demonstrated impact (Increased Financial Capability and Behaviour Change for Target Segment); and (3) The extent to which it represents a triple bottom line return on investment (Scale, Sustainability and Transformation).

1) The extent to which it responded to the identified needs

The driver behind ‘An Opportunity for All: Financial Education in Africa’ was to find an effective approach targeting low income savers and individual loan client with financial education, financial capability development, consumer protection and financial management training.

With client’s growing impatience with more traditional longer workshop style training interventions disseminating financial education via technology driven delivery channels provided clients new vibrant learning experiences that continued to expose and re-expose them, achieving multiple reinforcement on each given topic, primarily on client terms.

When properly designed, multimedia is effective not only because it delivers a message through two basic

channels (verbal and visual), but because in its very nature of being multifaceted, it appeals more readily to diverse learning preferences across client segments taking advantage of the fact that most people access information in non linear ways.

Learning takes place in context at the moment knowledge is required, on client terms

Less time required by clients to access, participate, receive and complete foundational financial management syllabus

More consistency in delivery of content compared to in person workshop instructor or trainer approach

If poorly designed or inappropriately disseminated, multimedia financial education can also be ineffective, even detrimental or discourage client engagement with content.

(2) The degree to which it met pilot objectives and demonstrated impact;

The overall results suggest that multimedia financial education training is an effective approach to improving financial capability, with Objectives 1, 3 and 4 met by individual countries.

The content of the training material has proved easy to understand, tailored to the audiences’ need and has had a demonstrable impact on improving clients’ financial capability, albeit with the results varying across the countries.

Objective results that portray an increase in financial capability clearly visible and have been met in Uganda and Malawi

Objective results for Mozambique and Ghana are less evident but indicator results remain significant to prove this project effective.

(3) The extent to which it represents a triple bottom line Return on Investment (Scale, Sustainability and Transformation). An Opportunity for All: Financial Education in Africa Pilot delivered a triple bottom line return on investment.

Scale Opportunity International selected multimedia

as its central tool, because of its advantages for transmitting consistent standard of information, knowledge and skills to both the client, the staff

23

and the general community and to offer a training solution able to keep pace with large scale growth.

Not only was the dissemination target met, but was exceeded. To date, this project has extended Financial Education Multimedia based training to 290,236 low income individuals as we continue to work towards the goal of Financial Education for All.

In addition... Total Unique Non Pilot Branch Footfall (January

2011 – March 2011) – 362,560 Clients, made possible by Malawi having existing infrastructure able to screen the DVD in 11 additional Banking Halls and Ghana screening the DVD in 6 additional Banking Halls.

There was an element of gradual growth of footfall into the 16 pilot banking halls per month across each quarter, however the trend accelerated toward much greater scale when it came to utilization of portable players and mobile devices to take the multimedia tools out of the banking hall and into the communities and to the clients.

Sustainability The entire process for An Opportunity for All: Financial Education in Africa Multimedia Financial Education Pilot was completed in less than 18 months required an investment of £352,908. This investment covered Client Needs Assessment; Syllabus Design and Content Development; Staff Capacity Development; Financial Education Dissemination and Impact Evaluation for Pilot Sites in Uganda, Malawi, Mozambique and Ghana. The pilot had a Unique Branch Footfall and Portable Device Outreach of 290,236 clients and individuals over the dissemination period, which converts to a cost per client of £1.21.

Whilst traditional classroom or workshop style financial education has a significantly lower start-up cost, costs remain constant for each student each time the training is delivered. However for multimedia based financial education, despite the higher up front resource development costs, the cost per person declines as the number of clients accessing the resources increases.

Consider ‘Non Pilot Branch Dissemination’ plus ‘Repeat Client’ and ‘Community Exposure’

dimensions to this intervention for little additional logistical outlay, and the cost per client drops considerably to almost nil. Considering the suite of multimedia resources created during An Opportunity for All: Financial Education in Africa pilot are evergreen, the potential roll out beyond the 16 pilot branches over many years, presents an exciting cost effective alternative to more traditional Client Training approaches.

At various times in history, technology is introduced in the hope it would enhance and extend learning possibilities. Just like the introduction of the blackboard into schools, the advent of Information Communication Technology (ICT) and rise in new applications for multimedia have rapidly expanded learning approaches and possibilities toward the intersection of education and entertainment (‘edu-tainment’). Further, with Sub Sahara and East Africa’s rapid transition from one of the slowest entrants into the world of ICT to now 5 years on becoming one of the most aggressive competitive technology forward regions in the world (where cell phone subscribers are signing up with mobile phone services at a rate greater than one every second), Africa is rapidly closing the digital divide reaching out and utilizing technology and devices to access information at a pace never imagined. Simultaneously, the rapidly reducing cost of technology (including portable smart and tablet devices) coinciding with the hot competition necessary to drive excellent customer service (attempts to satisfy customer needs at a price customers can afford and institutions can sustain), should position multimedia financial education at the front of mind and be of particular interest to MFIs across Africa.

Transformation Whilst only a trial, all participating institution have already requested additional funding to roll out the training materials across the spectrum of their respective footprints through a variety of dissemination strategies including:

Infrastructure to ensure dissemination across the full institutional footprint

Financial Education DVD lending library;

Financial Education night time cinema for rural delivery;

24

Financial Education (Client) Champions Network as distribution points throughout client

footprint able to provide DVDs and Comics, support and coaching upon client request;

Web based upload to access via internet outlets and browsing centres;

Television and Radio Mass Broadcasting.

In addition, a number of local NGOs and community groups have requested either strategic dissemination partnerships or access to the material after witnessing the engagement and impact of the resources.

The Final Word...DfID Financial Education Fund afforded Opportunity International the resources needed to use An Opportunity for All: Financial Education in Africa pilot project to build a model that has demonstrated effectiveness at delivering financial education via a suite of multimedia resources.

Opportunity International has been committed to the education of its clients since the outset in 1971. This pilot programme reflects our ongoing dedication to ensuring that people living in poverty are given the wherewithal to make the best financial decisions for themselves and their family. However this level of commitment is not limited to Sub Sahara Africa. Over the past 2 years, Opportunity International has been building resources, partnerships and a body of impact evaluation data to ensure effective extension of our suite of bespoke multimedia financial education resources across and throughout the Opportunity International global footprint. Innovation and pilot trials are underway or into phase two for: Uganda, Ghana, Malawi, Mozambique, Colombia, India, Philippines and now Rwanda, Kenya, Tanzania and DRC. At Opportunity International, we are constantly trying to improve our cost effectiveness, outreach and impact. Opportunity International will always strive toward the leading edge of innovation.

25

‘An Opportunity for All: Financial Education in Africa’ pilot programme reflects Opportunity International’s ongoing dedication to ensuring that people living in poverty are given the wherewithal to make the best financial decisions for themselves and their family.

As a Network, we have been committed to the education of our clients since our outset in 1971 – whether this training is delivered through induction meetings, street theatre, mass media campaigns, or through training and mobilising community leaders to be peer trainers. We will continue to develop our financial education curriculum over the coming months and years, making sure we focus our efforts on the following five priorities:

1. We will increasingly listen to our clients. We will segment our client base to ensure we are having maximum impact with our financial education programmes. We recognise that a “one size fits all” approach will not work since the need for financial education depends on a wide number of variables, including client life cycles and the availability of “teachable moments”.

2. We will continue to build the financial capability of our front line staff. We recognise that investing in our staff is a key way to optimise our ability to deliver effective financial education programmes to our clients.

3. We will to continue to innovate, to pilot test new approaches and to collect more data of what works and where, especially in geographies where we are increasingly offering branchless banking services to the poor (e.g. for remittances, mobile payments, cash transfers) or where we are serving new client groups (e.g. youth, remittances recipients and smallholder farmers). These new forms of financial access necessitate new models of delivering financial education training.

4. We will continue to make use of new technologies as they become available, in order to increase the coverage of our financial education programmes and to reduce unit costs.

5. We will endeavour to further develop a business case for financial education (looking at the effectiveness in terms of impact, as well as possibilities for cost recovery). Cost recovery will come through a number of means, including reduced risk of non-repayments, increased possibilities for cross-selling products and services, increased client retention rates and enhanced branding.

We continue to believe that building the financial capability of our clients is critical and that this has to go hand-in-hand with delivering increased access to financial services and products if we are to achieve economic transformation in the lives of poor and excluded populations. This is why Opportunity International will always be found at the leading edge of innovation.

Harry Turner CEO of Global Microfinance Operations Opportunity International Network

A message from the CEO

MULTIMEDIA PILOT TRIAL

ATTACHMENTS

27

The OverviewThe Model DVD Resource used as a tool to present financial education to individual clients and voluntary savings clients

Primary Objective To find a high impact cost effective approach for quality dissemination of FE across target segment of individual loan and voluntary savings clients