an investigation of consumer preferences towards store...

TRANSCRIPT

AN INVESTIGATION OF CONSUMER

PREFERENCES TOWARDS STORE BRANDS

PURCHASE IN MADURAI DISTRICT

A THESIS

Submitted by

C. R. MATHURAVALLI

Register No: 200702205

In partial fulfillment for the award of the degree of

DOCTOR OF PHILOSOPHY

Under the Supervision of

Dr. S. SAKTHIVEL RANI

Head of the Department

Department of Business Administration

Kalasalingam University

DEPARTMENT OF BUSINESS ADMINISTRATION

KALASALINGAM UNIVERSITY

KALASALINGAM ACADEMY OF RESEARCH AND EDUCATION

ANAND NAGAR

KRISHNANKOIL – 626 126

JUNE 2013

ii

CERTIFICATE

This is to certify that all corrections and suggestions pointed by the

Indian/Foreign Examiner(s) are incorporate in the thesis title “AN

INVESTIGATION OF CONSUMER PREFERENCES TOWARDS STORE

BRANDS PURCHASE IN MADURAI DISTRICT” submitted by Mr./Ms

……C.R.MATHURAVALLI……………………………………..

Place:Krishnankoil Dr. S. SAKTHIVEL RANI

Date:22.04.2015 SUPERVISOR

Head of the Department,

Department of Business

Administration,

Kalasalingam University,

Krishnankoil,

Tamil Nadu, India.

iii

iv

KALASALINGAM UNIVERSITY

KRISHNANKOIL - 626 126

BONAFIDE CERTIFICATE

This is to certify that the thesis titled “An Investigation on Consumer

Preferences towards Store Brands Purchase in Madurai District” is the

bonafide work of Mrs.C.R.MathuraValli, who carried out the research under

my supervision. Certified further, that to the best of my knowledge the work

reported here in has not been part of any other thesis or dissertation on the

basis of which a degree or award was conferred on an earlier occasion on this

title by any other scholar.

Dr. S. SAKTHIVEL RANI

SUPERVISOR

Head of the Department,

Department of Business Administration,

Kalasalingam University,

Krishnankoil,

Tamil Nadu, India.

v

ABSTRACT

The retail industry has seen a tremendous growth in the size and

market dominance of larger players, with greater store size, increased retail

concentration, and utilization of a range of formats. With the inception of

retailing recent years, various types of sophisticated and complex formats

have originated in the retailing scenario of India. Each type of retailer is

trying to survive and prosper by satisfying a group of customers` needs and

expectations more effectively than its competitors. As a result a greater

emphasis is on how to ensure complete consumer engagement and

convenience which result in maximum footfalls on this emphasis. The

retailers have succeeded in their endeavor to a great extent. The growth of an

organized retailing is predominant across the globe. Organized retail is on the

threshold of a boom in India. Branding is an important element in the retailing

industry to influence customer perceptions and to drive store choice and

loyalty. With the manifold increase of organized retailing in the urban and

semi-urban areas, there is a necessity for the retailers to brand their retail

outlet. Whether the retailers are textile or grocery or mobile phone sector, it is

unavoidable for them to brand the services. Even many multinational

companies are waiting to get the Government nod for FDI to enter into Indian

market. In such a scenario, the competing retail outlets are going to

differentiate the services towards the consumers, only by branding. The

worldwide observation shows that, as retailers become more powerful, they

have increasingly focused on their own brands at the expense of manufacturer

brands. Store brand label goods and services are available in a wide range of

industries from food and cosmetics to web hosting. Store brands, also called

private labels, are made by the retailer or a third-party supplier to the retailer's

specifications. They are those owned and sold by the retailers in stores

typically at a lower price because of minimal marketing and advertising

vi

expenses. Historically, store brands are seen as low-priced and low-quality

products. In recent years, however, companies have started using store brands

to market higher quality items, and many believe that high-quality store brand

will increase their present market. The battle is likely to change the face of the

industry between the manufacturer brands and the retail chains’ store brands.

Consequently, the progress of store brands is in a rapid pace.

The retailing business is greatly affected by the patronage

behaviour orientations of shoppers. One important factor affecting consumer

choice is the store image, an image shaped by store attributes. Due to the

rapid growth of store brand market shares, researchers have looked into

different influential factors, attempting to find out the reasons behind the

success of these store products. There is a growing need to evaluate the

drivers of retail store choice behavior in the Indian context. The study of

consumer helps the retail outlets to improve the marketing strategies by

understanding, how consumers consider different attributes and make

purchase decision that differ among various retail outlets, based on the level

of importance and interest.

It is imperative to study the consumers’ perceptions towards store

brands of various retail formats. This research work is an attempt to identify

the consumers’ perception and the store choice behaviour towards stores,

store brands and store loyalty in the Madurai district. The research also aims

at finding various parameters that influences consumer’s purchase decisions

on the store brand products. The research finds the correlation between the

satisfied customers with the stores and the reflection of store brands loyalty

towards stores. The purpose of this study is to ascertain the linkages between

store image, customer satisfaction, store brand factors and customer loyalty

towards stores especially in Madurai district.

vii

This study is an attempt to address issues related to store attributes

and their relevance in the store selection process. Identified factors and

recommendations in the research work would be of use to the retailers in

designing their outlets with store attributes that would meet the expectations

of shoppers thereby motivate them towards store patronage decisions. Then it

focuses on the insight of consumers on store brands and the various

perceptual factors that influence them to select retail brand.

The study is descriptive in nature and is well structured. Self-

administered questionnaire is developed on the basis of review of the

literature and the store –intercept has been conducted. The data has been

collected from 488 respondents of four major retail outlets in Madurai city.

The percentage analysis, ANOVA Test and Independent t-Test are used to

analyze the data and to examine the relationship between store image, store

brand factors, consumer satisfaction and store loyalty. Finally, structural

equation modeling using partial disaggregation method is performed to test

the whole structured model. The results from structural equation modeling

method confirm significant relationships among the constructs in the model.

All major fit indices from structural equation modeling analysis show

satisfactory results for both the measurement models and the structural model.

The results indicate that perceived risk and attitude determinants such as

quality variability; price consciousness; price-quality association and

convenience influence significantly on consumers’ propensities to buy store

brands.

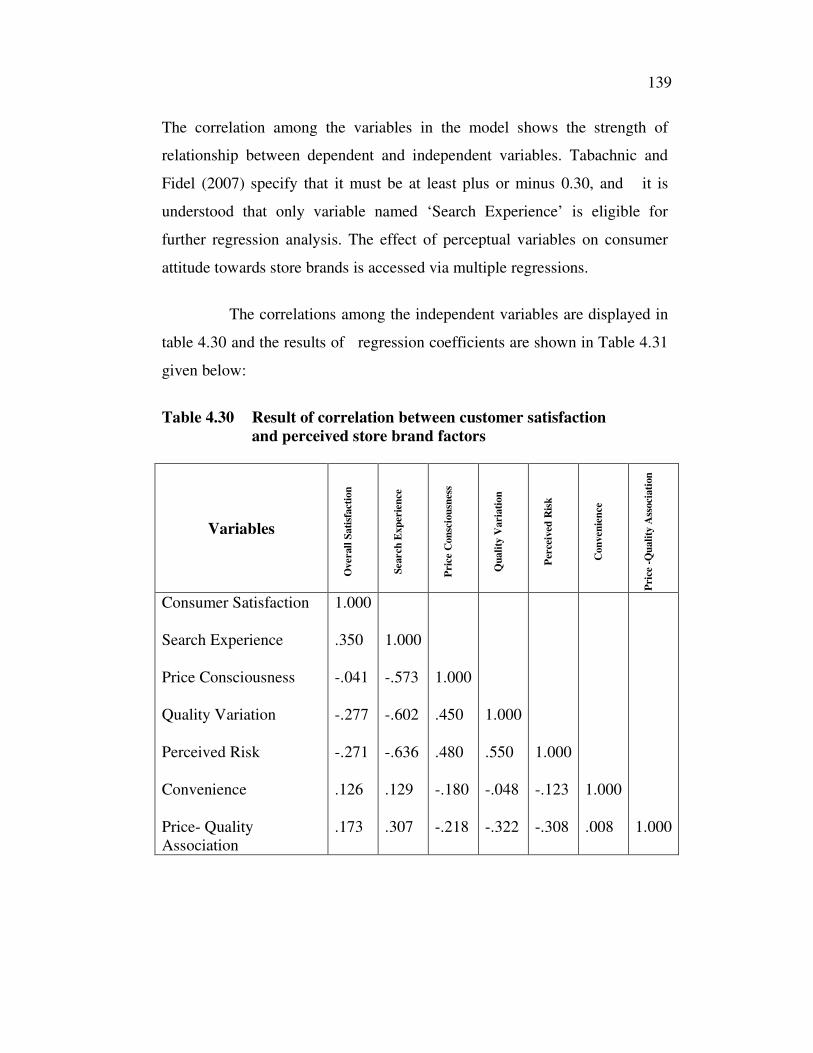

The research identified that value for money, wide range of

promotional offers and extensive varieties of products are the important store

choice attributes. Finally, the research work implies that the positive

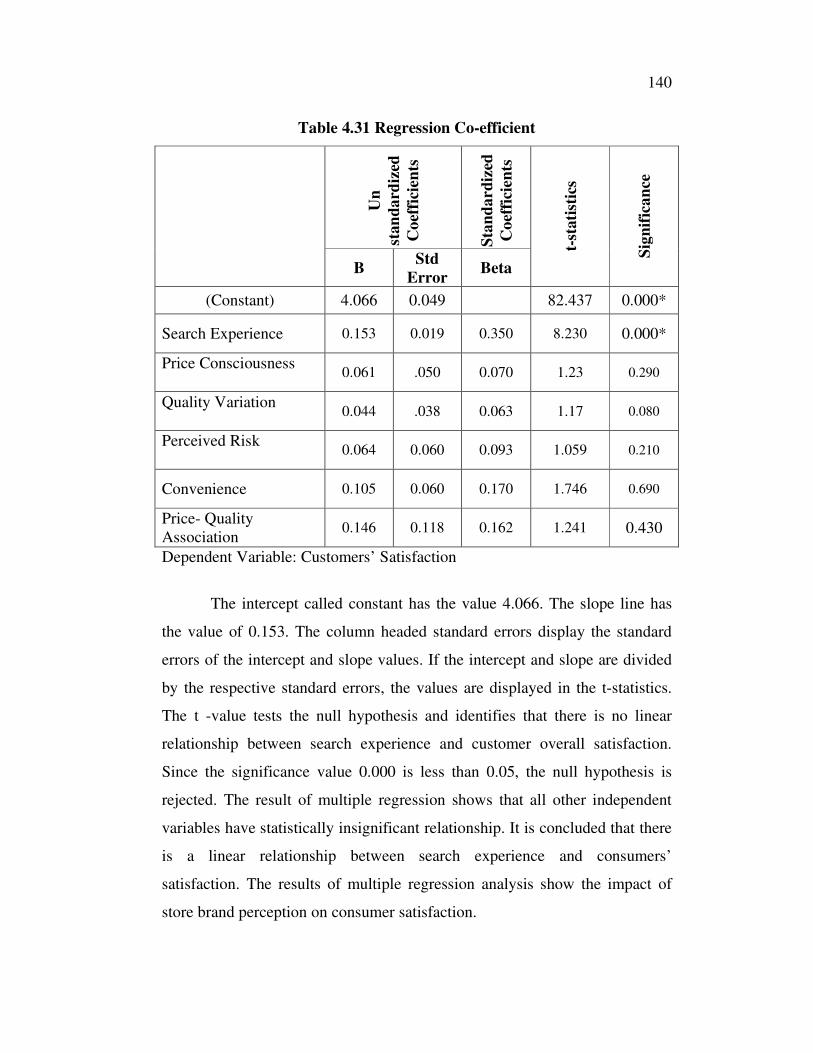

association exists in store image, consumer satisfaction and store loyalty but

not with store brands. The research has implications for organized retailers in

terms of store choice and store brand strategy which also have impact on

viii

consumer satisfaction and loyalty towards store brands in future time period.

The retailers should specifically consider aspects of store image that are

relevant to the store brands they offer, when designing activities to develop

and enhance strategies to promote their own brand and unique store

positioning.

Keywords: Store brand, store attributes, customer satisfaction and store

loyalty.

ix

ACKNOWLEDGEMENTS

My sincere thanks to our Chairman Kalvivallal

Mr. T. Kalasalingam, Illayavallal Mr. K. Sridharan Chancellor,

Dr. S. Saravana Sankar, the Vice-Chancellor Kalasalingam University, for

having permitted me to undertake the research work.

Dr. S. Sakthivelrani, my mentor and supervisor has extended her

valuable guidance and motivation throughout this research. She has been an

inspiration to me from the very beginning. Her approach and kindness

motivated me to execute this research lively. Only because of her extreme

care, trust and offered liberty, I was able to maintain quality throughout my

research. I extend my sincere thanks to her who has provided all moral

support behind the screen.

I place my deep sense of gratitude to my husband and other family

members who supported me in all efforts and for the pain they have taken in

this regard. My heartful thanks to my dear friends, and well wishers, who

have helped to finish this work successfully. I thank the Almighty for the

blessing, grace and mercy. He has showered on me and for leading me

successfully through the various stages of this work.

I acknowledge my gratitude to the respondents who readily

responded to my questionnaire for the study. I whole heartedly thank the

persons who have helped me directly and indirectly to complete this research.

C.R.MATHURAVALLI

x

CONTENTS

CHAPTER TITLE PAGE

NO. NO.

ABSTRACT v

LIST OF TABLES xviii

LIST OF FIGURES xxi

ABBREVIATIONS xxii

1 DESIGN OF THE STUDY 1

1.1 INTRODUCTION 1

1.2 STORE BRANDS – AN OVERVIEW 2

1.3 RETAILING IN INDIA – AN OVERVIEW 5

1.4 THE FACTORS DRIVING THE GROWTH OF

RETAIL SECTOR IN INDIA 6

1.5 ORGANISED AND UNORGANISED RETAIL

IN INDIA 7

1.5 .1 Unorganised Retail Sector in India 7

1.5.2 Organised Retail Sector in India 8

1.6 TRANSFORMATION OF RETAILERS IN

THE STORE BRAND 10

1.7 THE IMPORTANCE OF STORE BRANDS IN

THE RETAILING INDUSTRY 12

1.8 MODERN RETAIL FORMATS IN INDIA 14

1.9 PROFILE OF THE STUDY AREA 16

1.10 MAJOR RETAILERS IN MADURAI 16

1.10.1 Aditya Birla Retail Limited 16

1.10.2 Reliance Retail Limited 17

1.10.3 Spencer's Retail Limited 18

1.10.4 Shri Kannan Departmental store 19

xi

CHAPTER TITLE PAGE

NO. NO.

1.11 OPERATIONAL DEFINITIONS 20

1.11.1 Retail 20

1.11.2 Retailing 20

1.11.3 Organized Retailing 21

1.11.4 Unorganized Retailing 21

1.11.5 Brand 21

1.11.6 Store Brands 22

1.11.7 Perceived Risk 23

1.11.8 Quality Variable 23

1.11.9 Price Consciousness 23

1.11.10 Price-Quality Association 23

1.11.11 Search Experience attribute 23

1.11.12 Store Image 24

1.11.13 Store Loyalty 24

1.11.14 Brand Loyalty 24

1.11.15 Customer Satisfaction 24

1.12 BACKGROUND OF THE RESEARCH 25

1.13 THE RESEARCH PROBLEM 26

1.14 OBJECTIVES OF THE RESEARCH 26

1.15 JUSTIFICATION OF THE RESEARCH 27

1.16 METHODOLOGY 30

1.17 CHAPTERISATION OF THE RESEARCH

WORK 31

1.18 SUMMARY 31

xii

CHAPTER TITLE PAGE

NO. NO.

2 LITERATURE REVIEW 33

2.1 INTRODUCTION 33

2.2 STORE BRAND 33

2.3 DETERMINANTS AND CONSUMER

ATTITUDES TO STORE BRANDS 34

2.3.1 Perceived Risk 36

2.3.2 Quality Variable 39

2.3.3 Price Consciousness 42

2.3.4 Price-Quality Association 44

2.3.5 Search Experience 48

2.3.6 Convenience 50

2.4 STORE IMAGE 51

2.4.1 The store image constructs 51

2.4.2 The effect of store brands on store image 54

2.4.3 The effect of store image on store brands 55

2.5 RELATIONSHIP BETWEEN STORE IMAGE

WITH CUSTOMER SATISFACTION AND

LOYALTY 57

2.5.1 Customer Satisfaction 57

2.5.2 Store Loyalty 57

2.5.3 Brand Loyalty 58

2.6 THE RESEARCH GAP 60

2.7 SUMMARY 62

3 METHODOLOGY OF THE STUDY 64

3.1 INTRODUCTION 64

3.2 RESEARCH METHODOLOGY 64

3.3 RESEARCH DESIGN OF THE STUDY 65

xiii

CHAPTER TITLE PAGE

NO. NO.

3.3.1 Justification for the research design 65

3.4 RESEARCH METHODS 66

3.4.1 Scale development 66

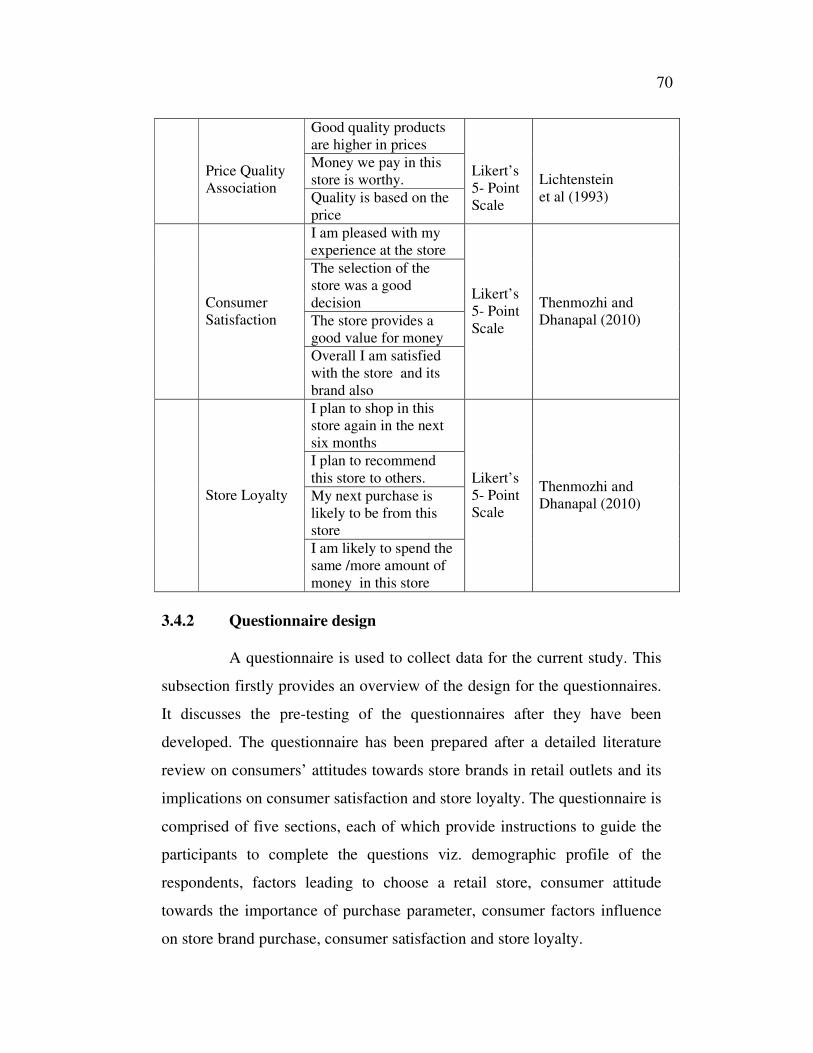

3.4.2 Questionnaire design 70

3.4.3 Pre-testing of the questionnaire 72

3.4.4 Sampling frame work and design 73

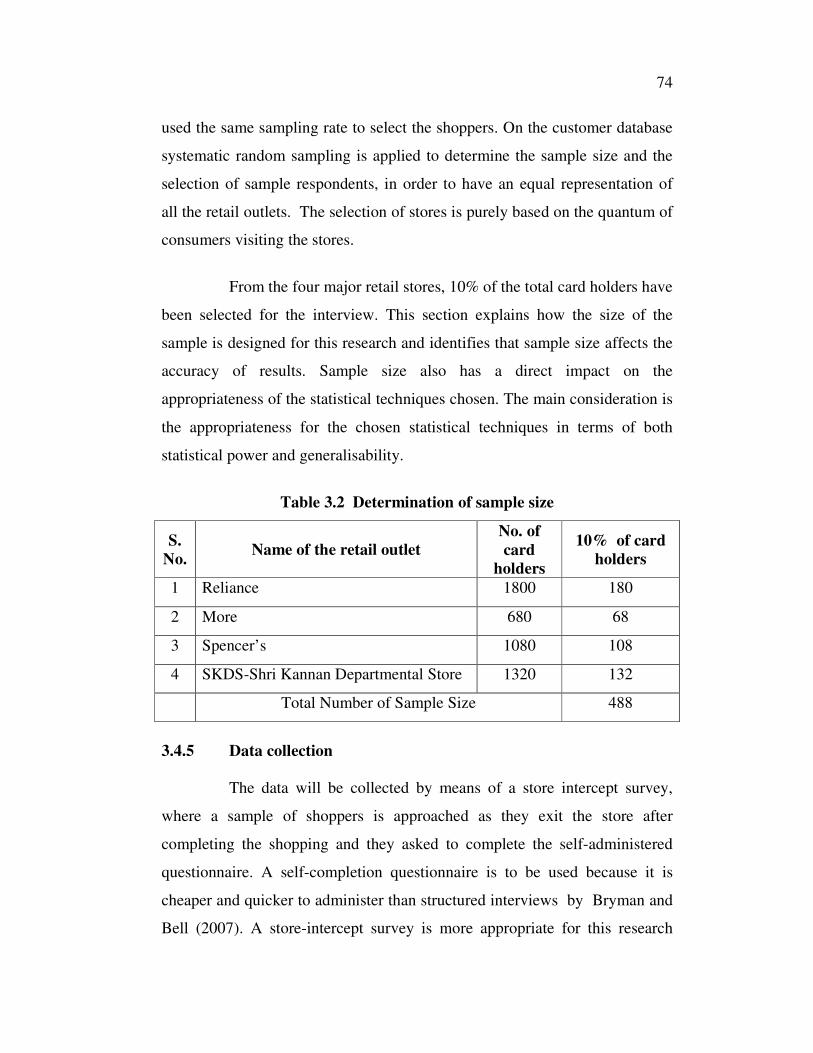

3.4.5 Data collection 74

3.4.6 Reliability test 75

3.5 DATA ANALYSIS 76

3.5.1 Factor analysis 76

3.5.2 Multiple Regression Analysis 77

3.5.3 Analysis of Variance 78

3.5.4 Independent t- test 79

3.5.5 Measures of central tendency 79

3.5.6 Structural Equation Model 81

3.6 SUMMARY 83

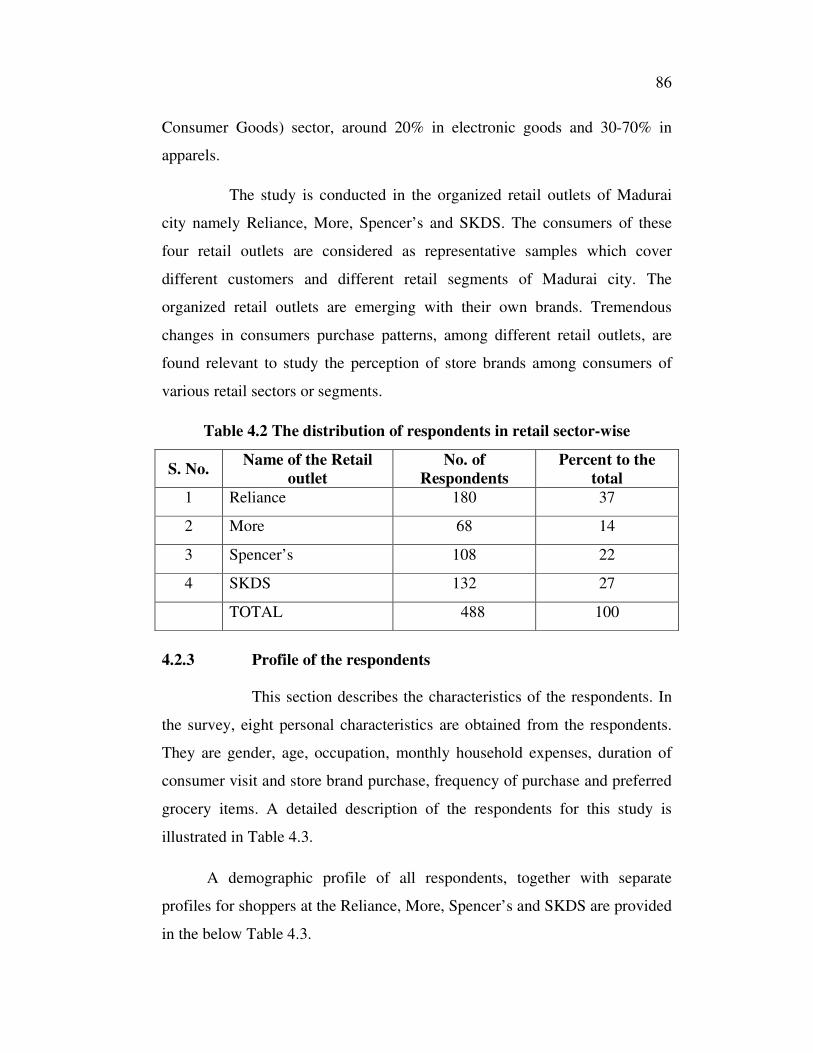

4 ANALYSIS OF DATA 84

4.1 INTRODUCTION 84

4.2 PRELIMINARY EXAMINATION OF

THE DATA 84

4.2.1 Response rate 84

4.2.2 The distribution and profile of the

respondents in each retail outlet 85

4.2.3 Profile of the respondents 86

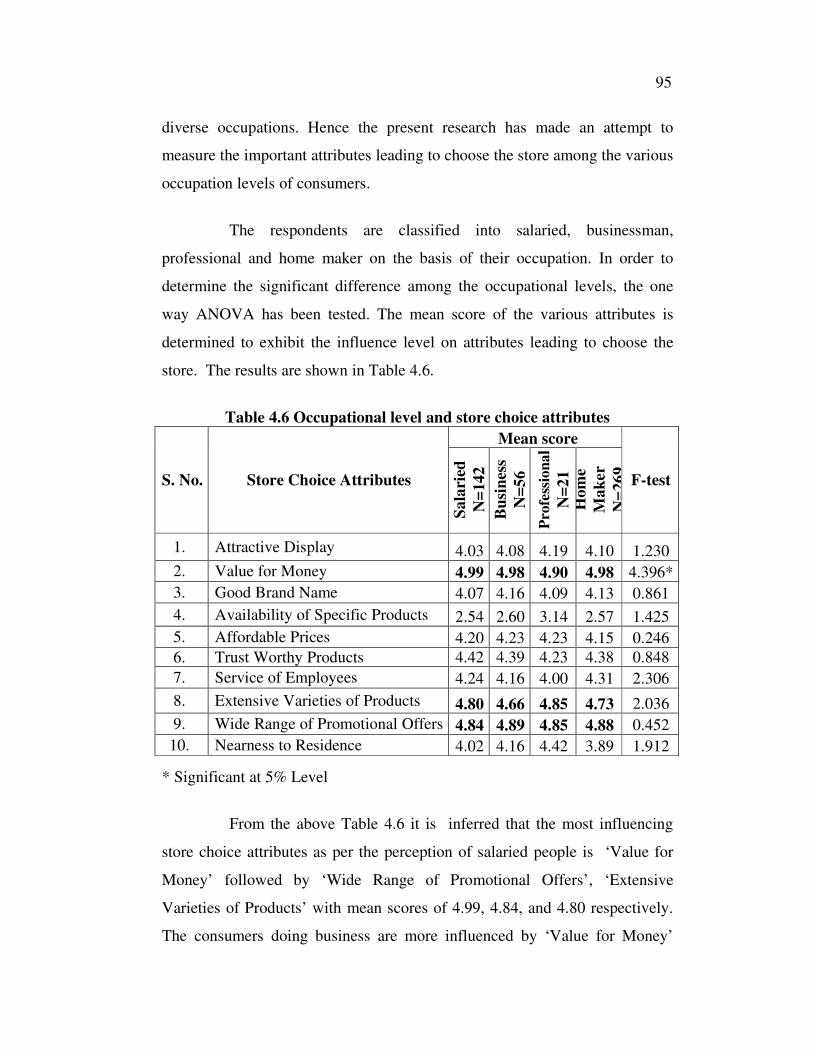

4.3 STORE CHOICE BEHAVIOUR AMONG THE

CONSUMERS 88

xiv

CHAPTER TITLE PAGE

NO. NO.

4.3.1 Attributes leading to choose the store

among gender wise classification 91

4.3.2 Attributes considered choosing the

Store among the different age group of

the consumers 92

4.3.3 Attributes considered to choose the store

among the occupational level of the

consumers 94

4.3.4 Expenditure for monthly grocery

purchase and store choice

attributes 96

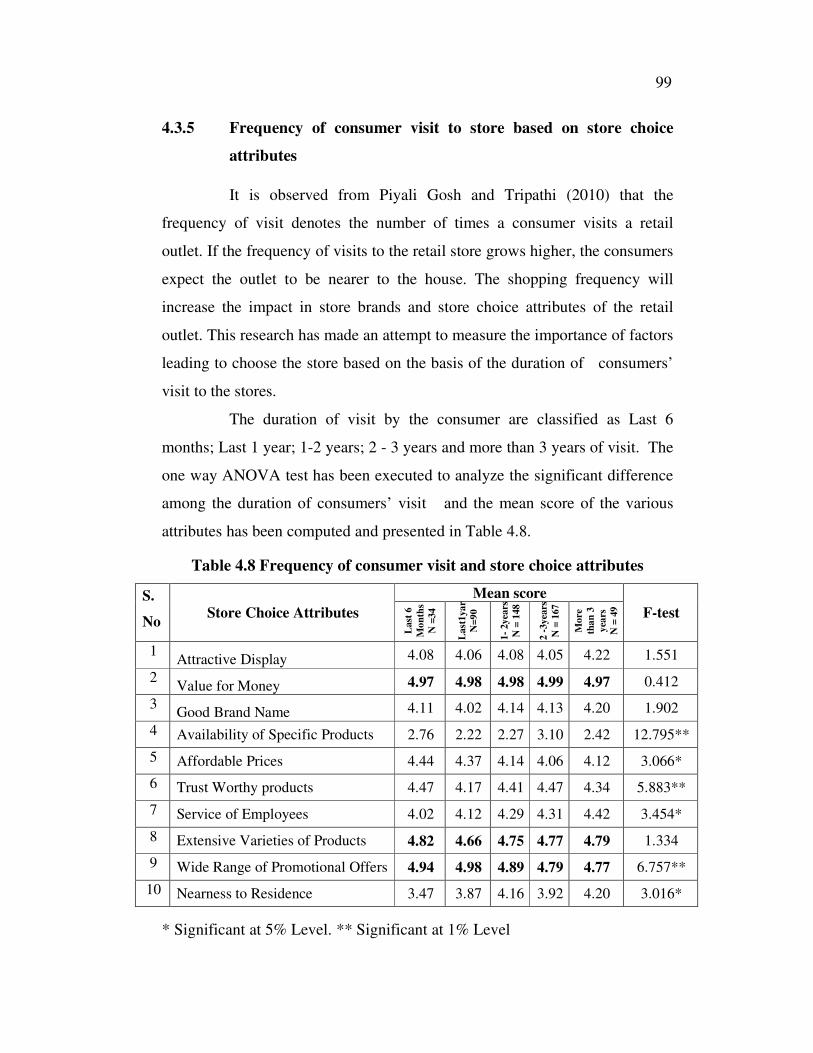

4.3.5 Frequency of consumer visit to store

based on store choice attributes 99

4.3.6 Attributes considered choosing the

store with frequency of purchase 100

4.3.7 Preference of grocery items and

store choice attributes 102

4.3.8 Frequency of store brand purchase and

store choice attributes 104

4.3.9 Consumer preference on store choice

attributes of retail outlets 105

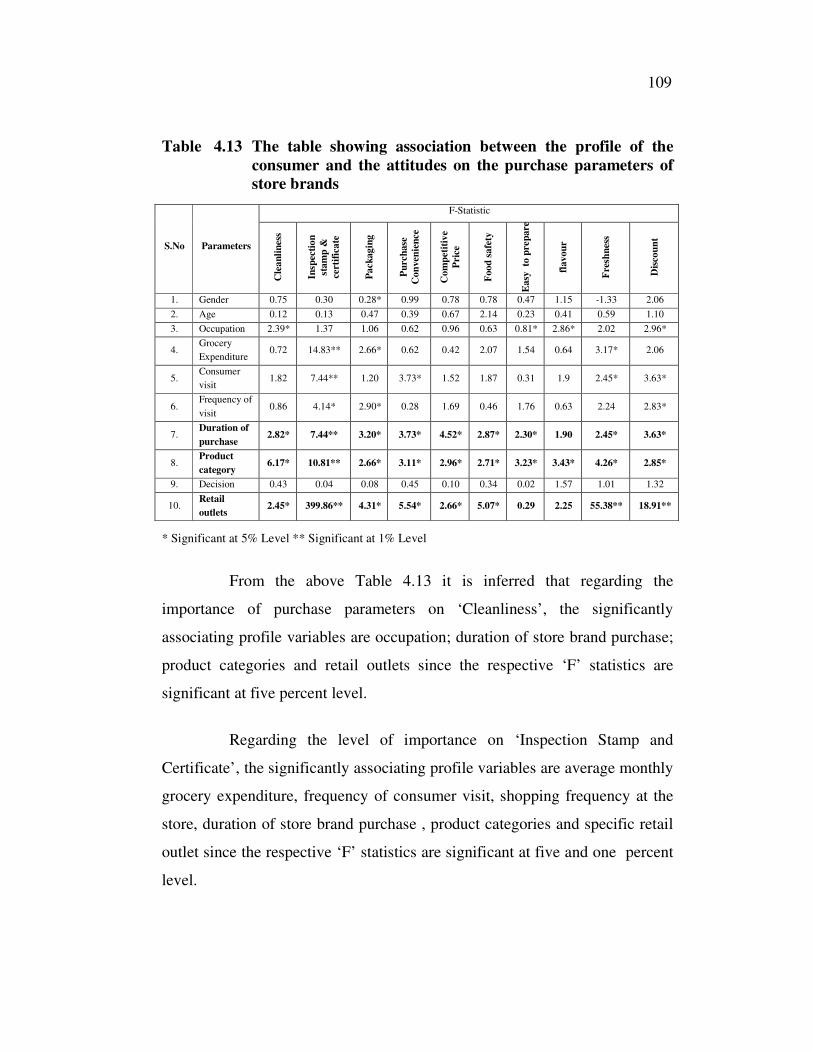

4.4 ASSOCIATION BETWEEN PROFILE OF

CONSUMER AND THE ATTITUDE

TOWARDS THE IMPORTANCE OF

PURCHASE PARAMETERS OF STORE

BRANDS 107

xv

CHAPTER TITLE PAGE

NO. NO.

4.5 CONSUMER ATTITUDES TOWARDS STORE

BRAND PURCHASE 111

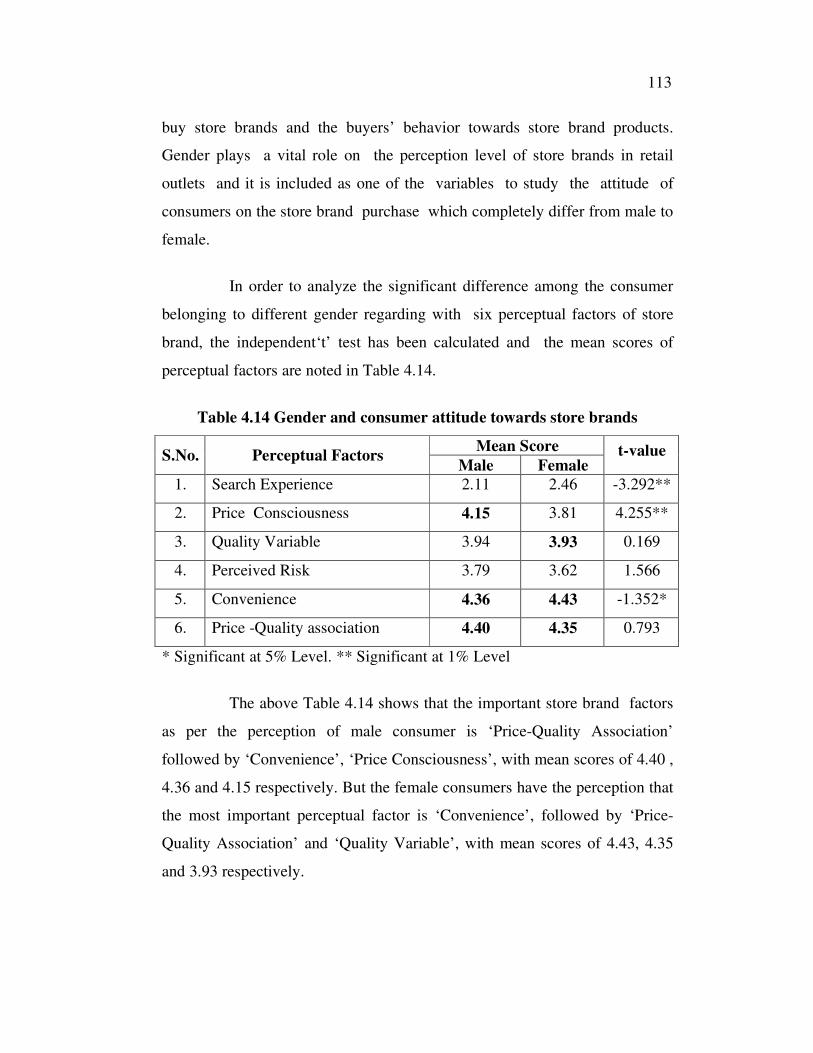

4.5.1 Variables and measures 112

4.5.2 Gender and consumer attitude towards

store brands 112

4.5.3 Age and consumer attitude towards

store brands 114

4.5.4 Occupational level and consumer

attitude towards store brands 115

4.5.5 Monthly grocery expenditure and

consumer attitude towards store brands 117

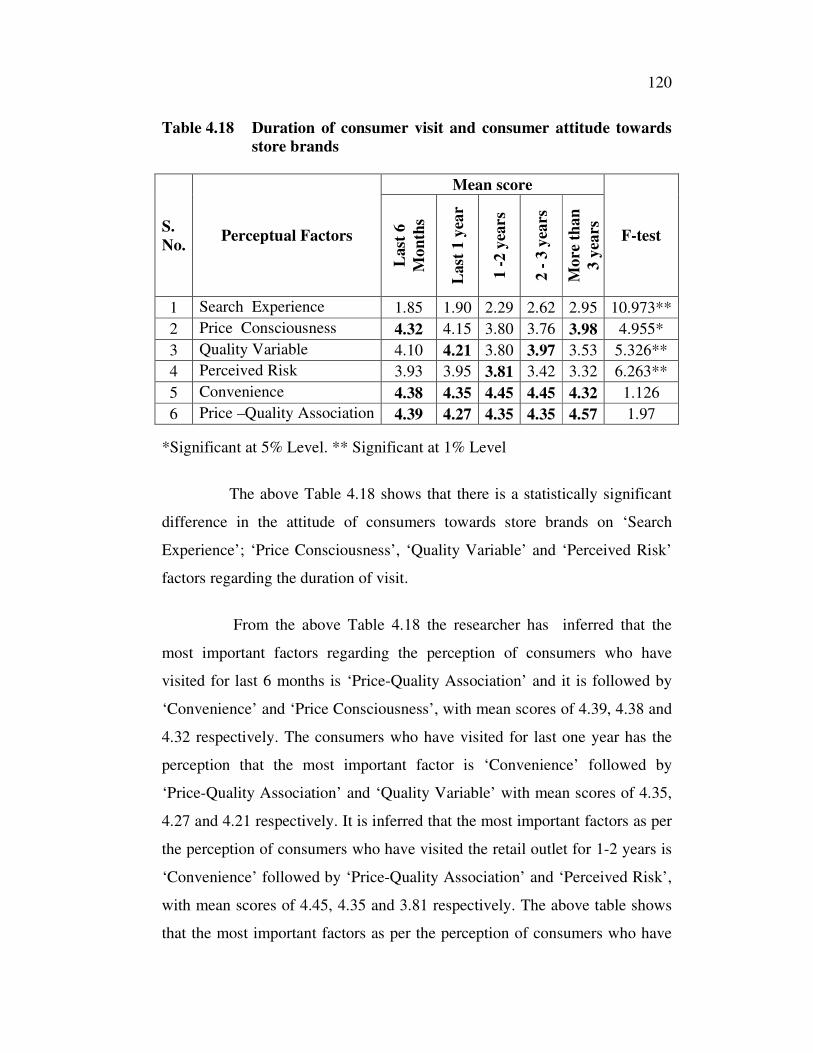

4.5.6 Duration of consumer visit and

consumer attitudes towards store brands 119

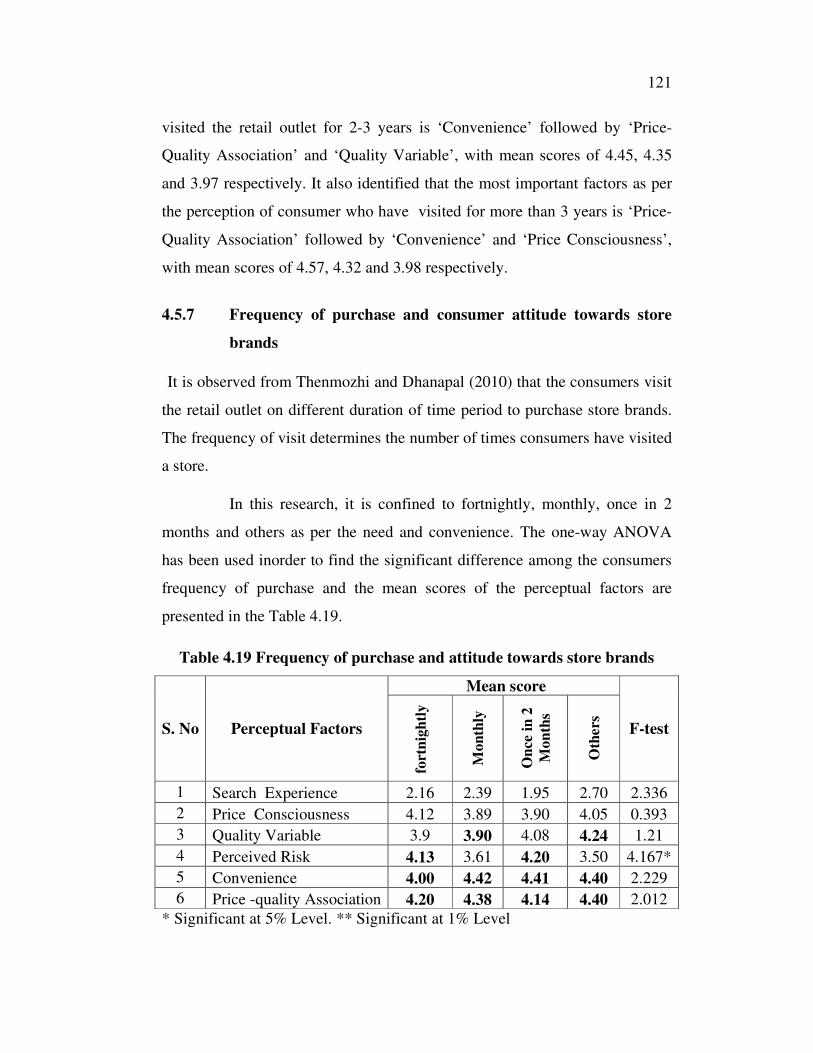

4.5.7 Frequency of purchase and consumer

attitude towards store brands 121

4.5.8 Preference of grocery item and

consumer attitude towards store brands 122

4.5.9 Duration of store brand purchase and

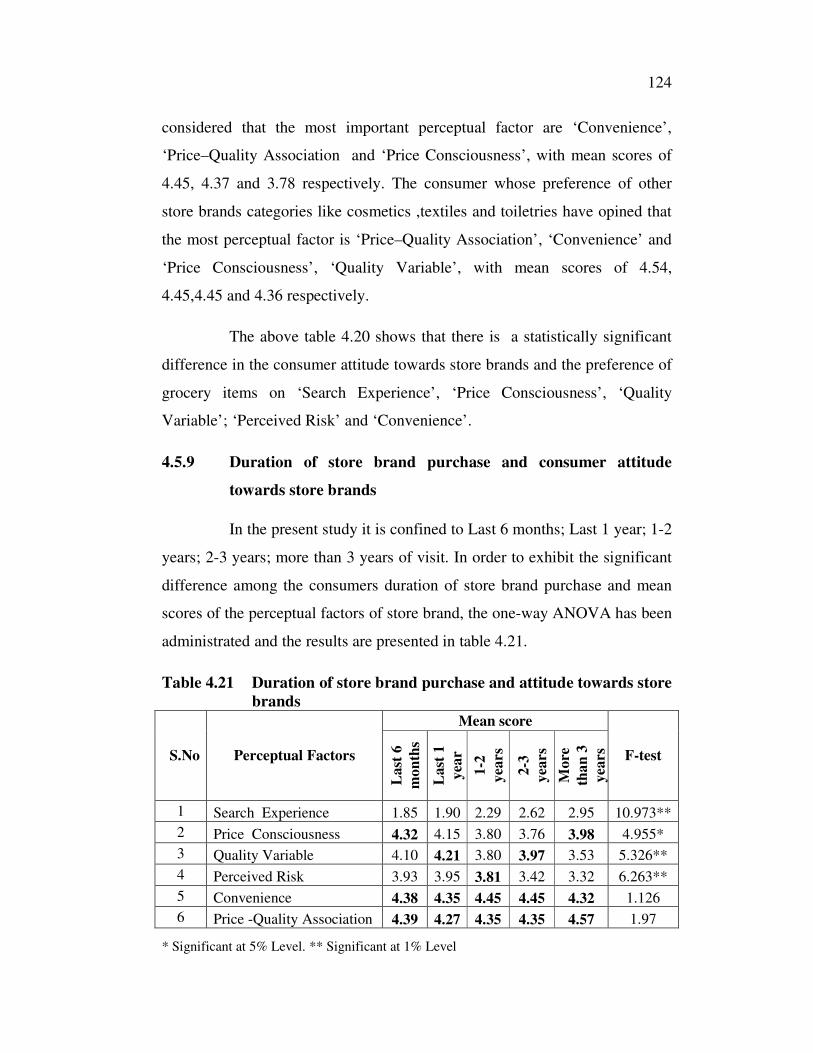

consumer attitude towards store brands 124

4.5.10 Consumer attitude towards store brands

in retail outlets 125

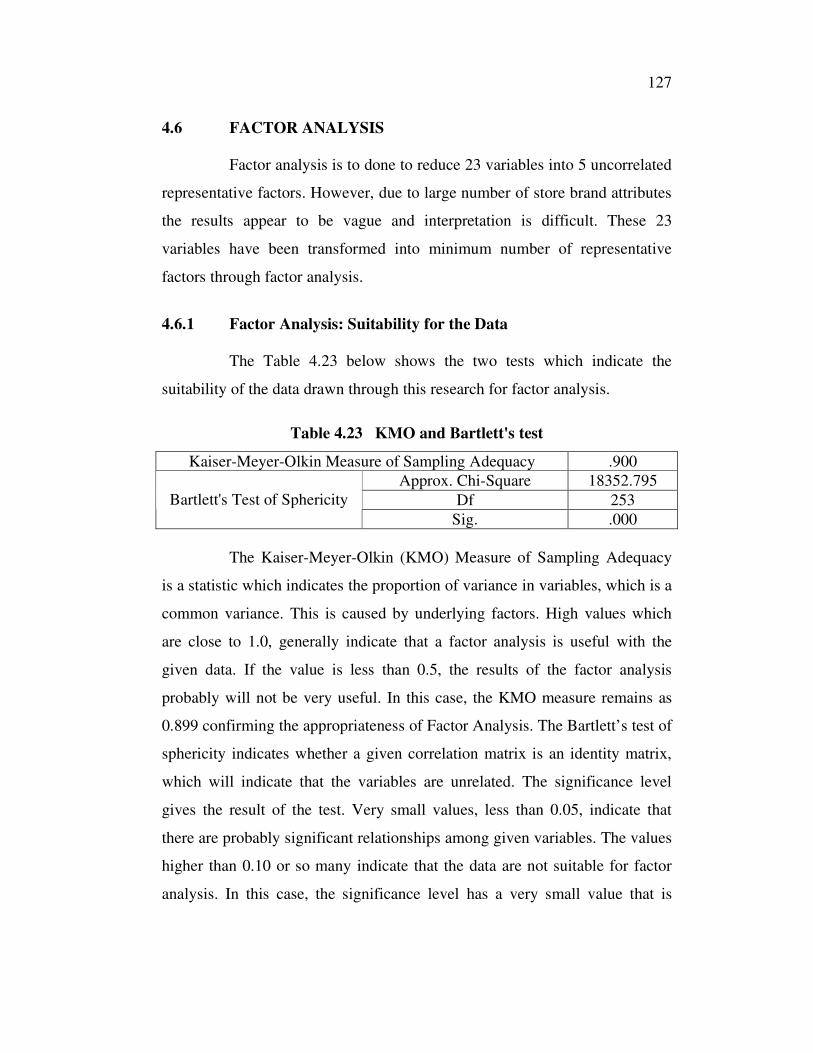

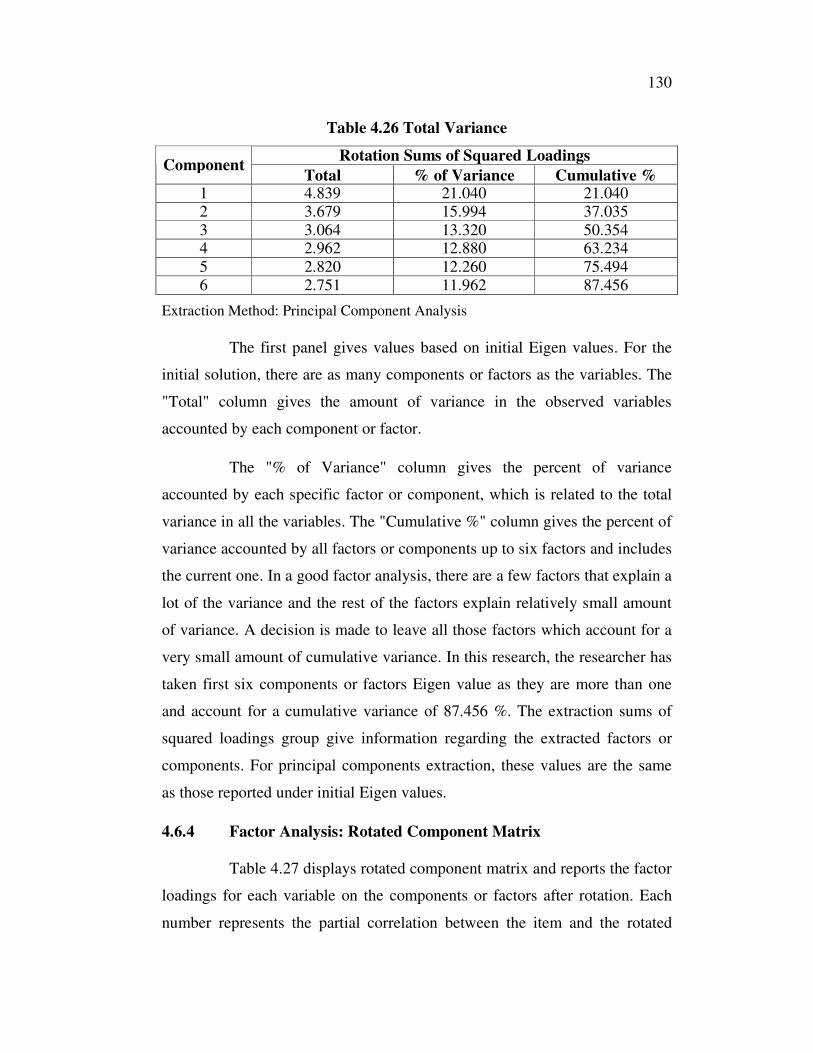

4.6 FACTOR ANALYSIS 127

4.6.1 Factor Analysis: Suitability for the data 127

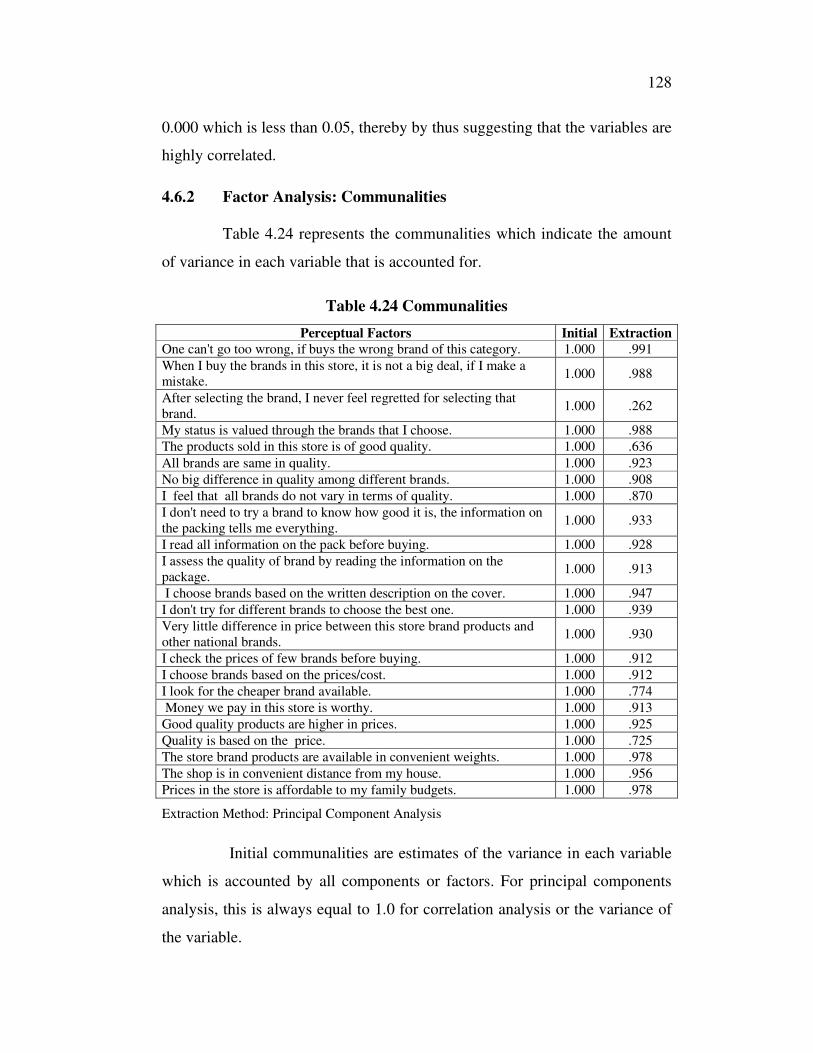

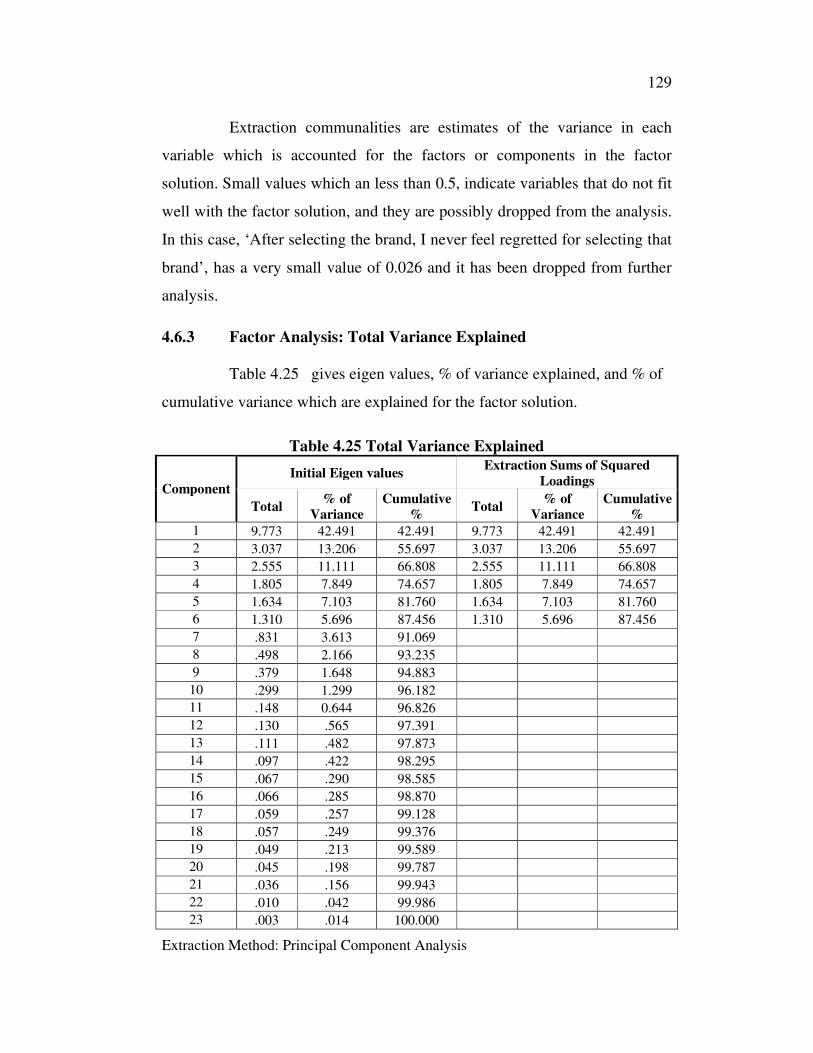

4.6.2 Factor Analysis: Communalities 128

4.6.3 Factor Analysis: Total Variance

Explained 129

4.6.4 Factor Analysis: Rotated Component

Matrix 130

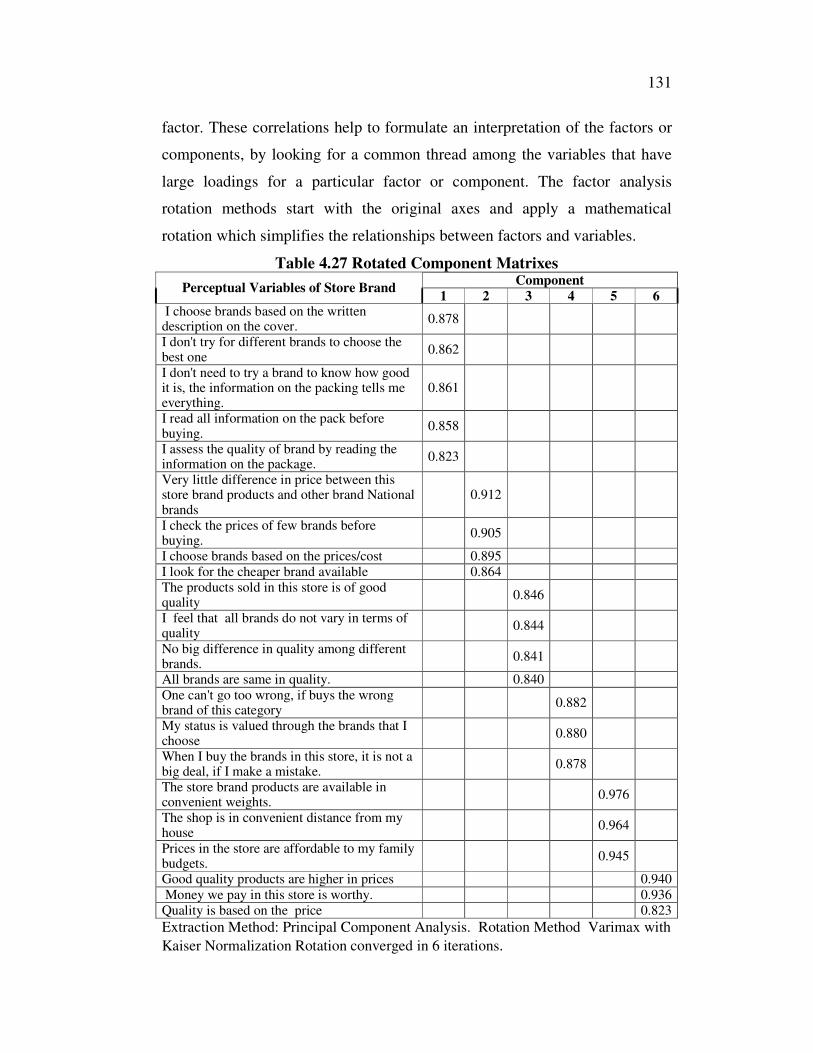

xvi

CHAPTER TITLE PAGE

NO. NO.

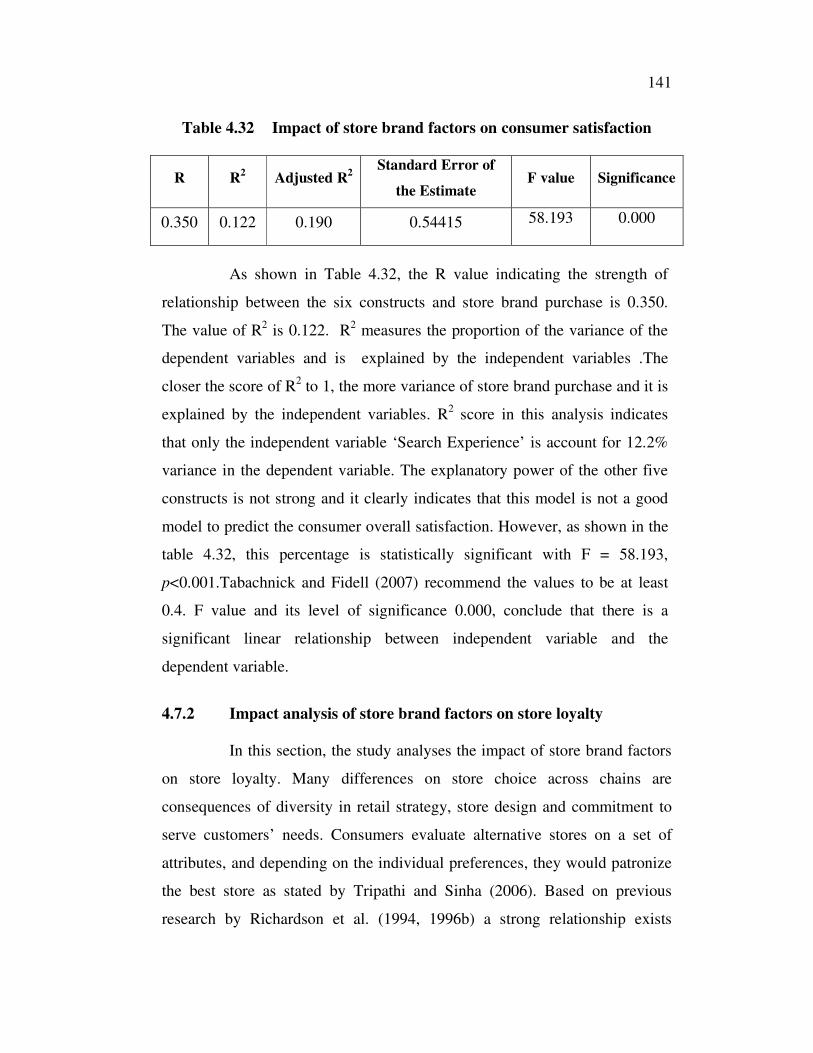

4.7 MULTIPLE REGRESSION ANALYSIS 137

4.7.1 Impact analysis of store brand factors

on consumer satisfaction 137

4.7.2 Impact analysis of store brand factors

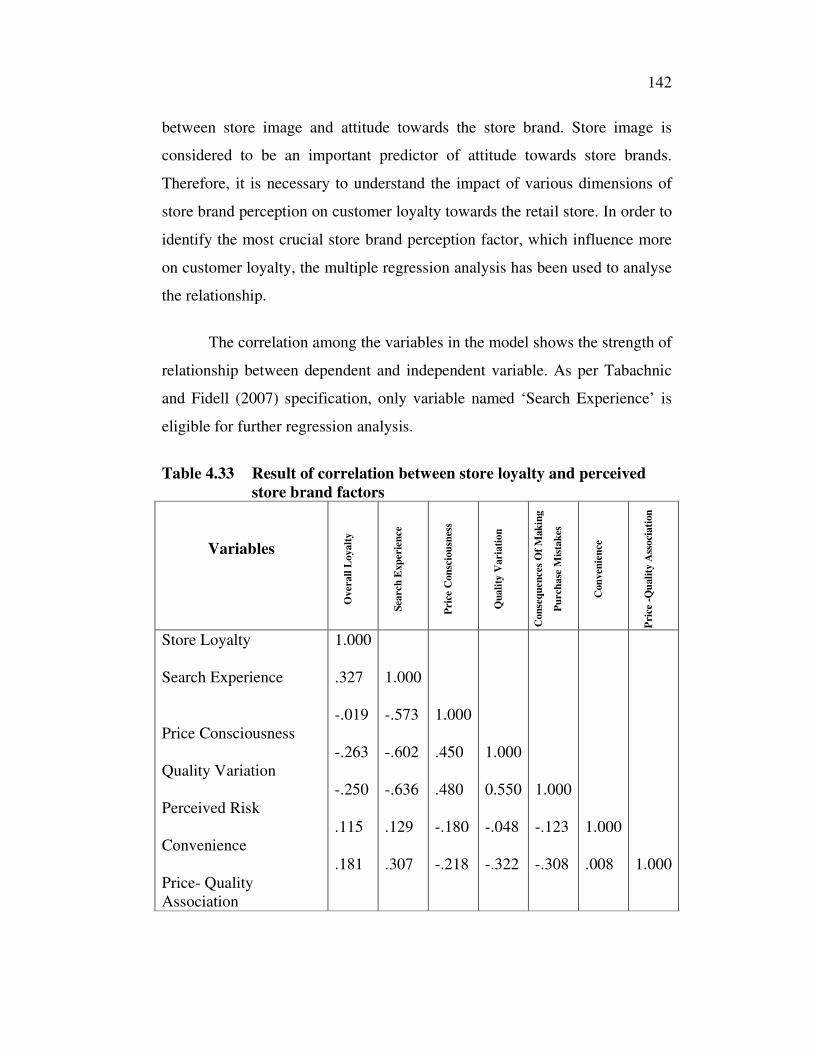

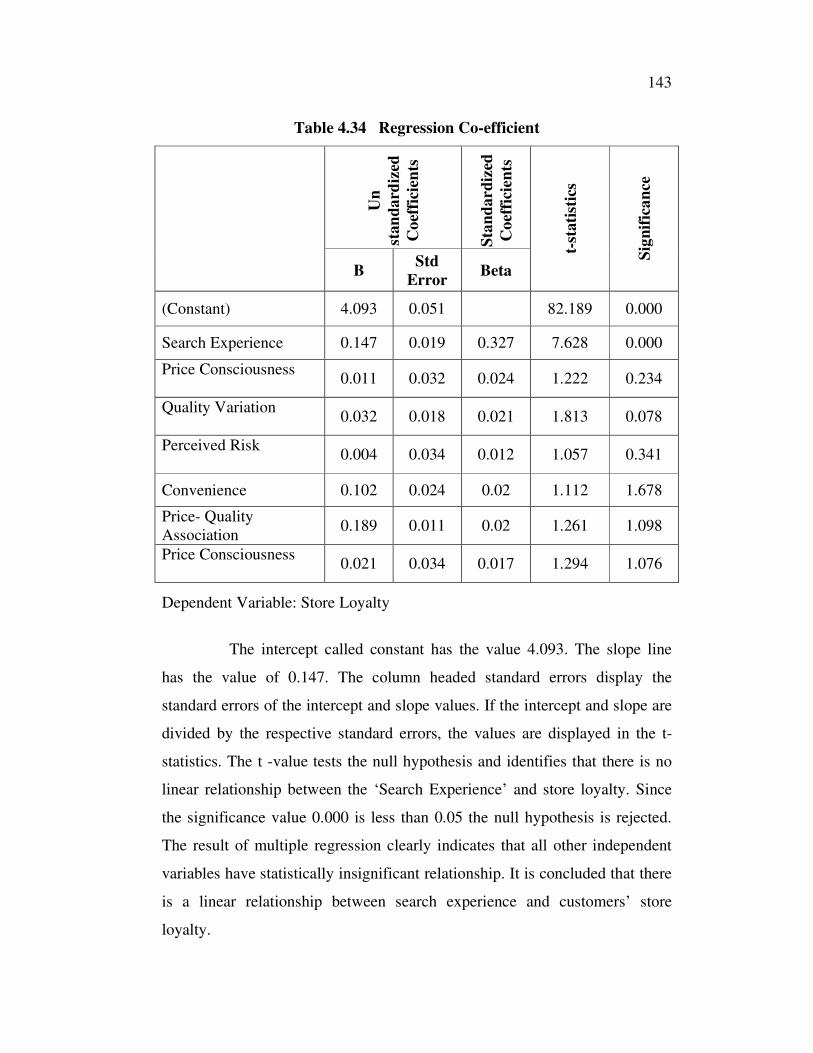

on store loyalty 141

4.7.3 Impact analysis of consumer satisfaction

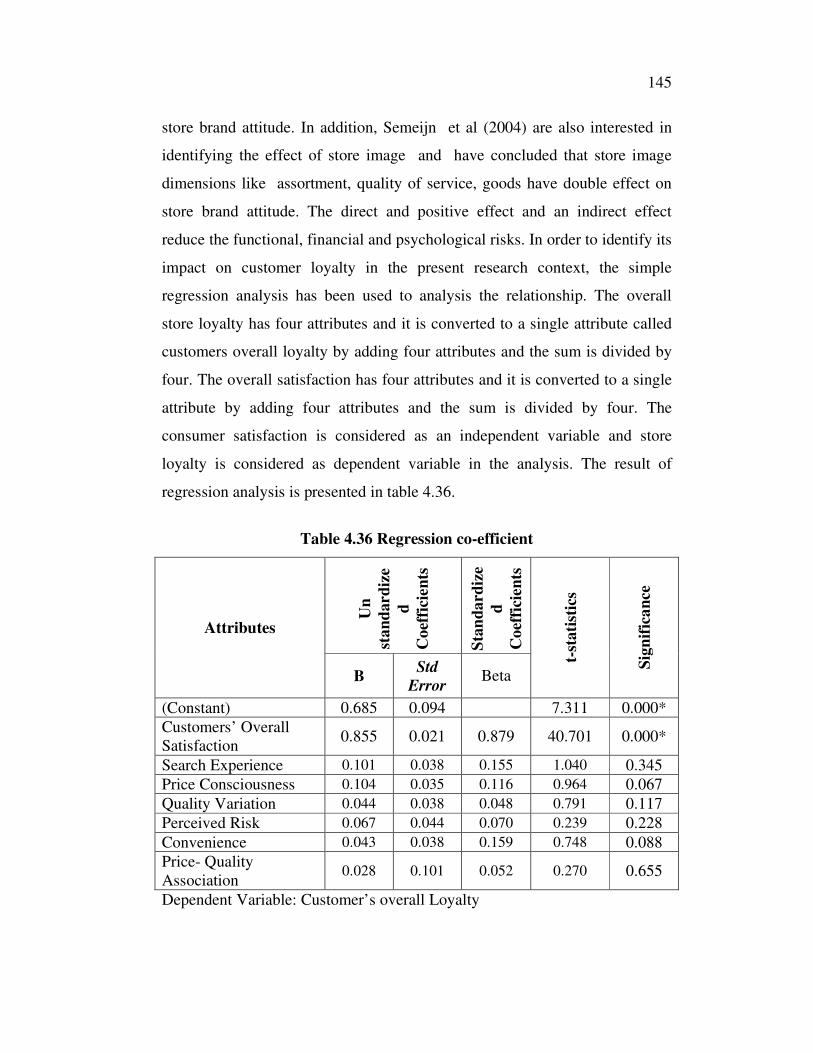

on store loyalty 144

4.8 CONSUMER SATISFACTION AND STORE

LOYALTY 147

4.9 MEASUREMENT MODEL ANALYSIS 152

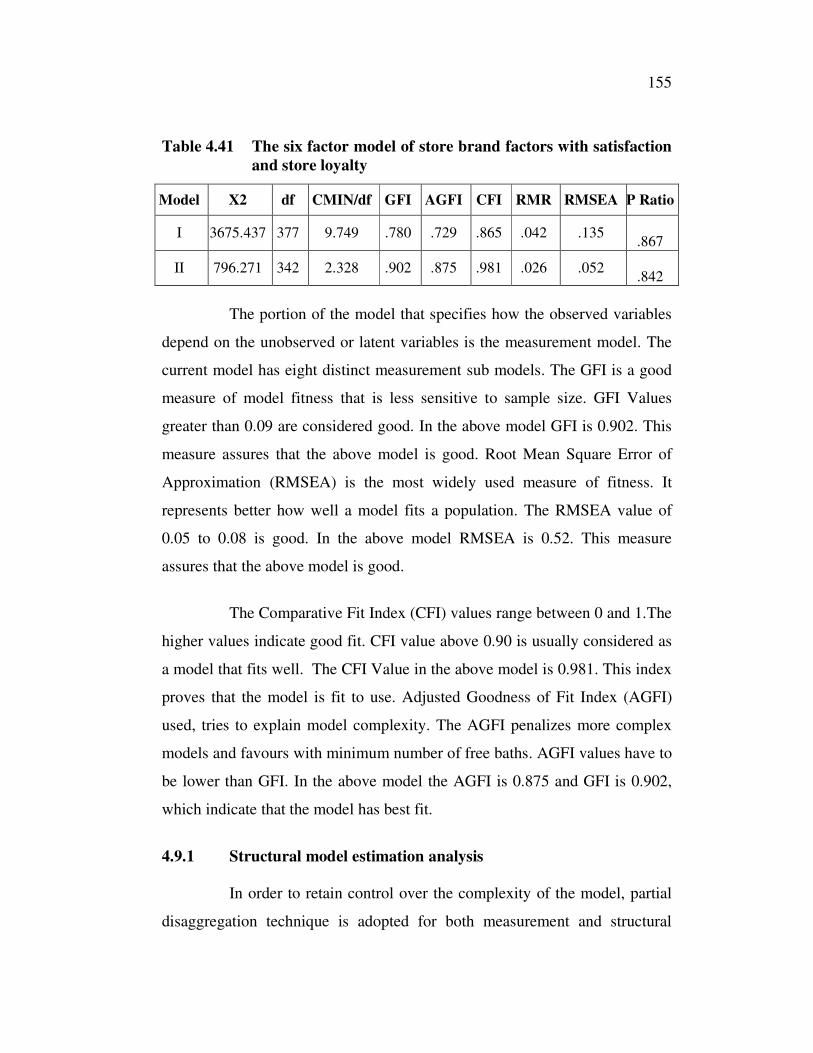

4.9.1 Structural model estimation analysis 155

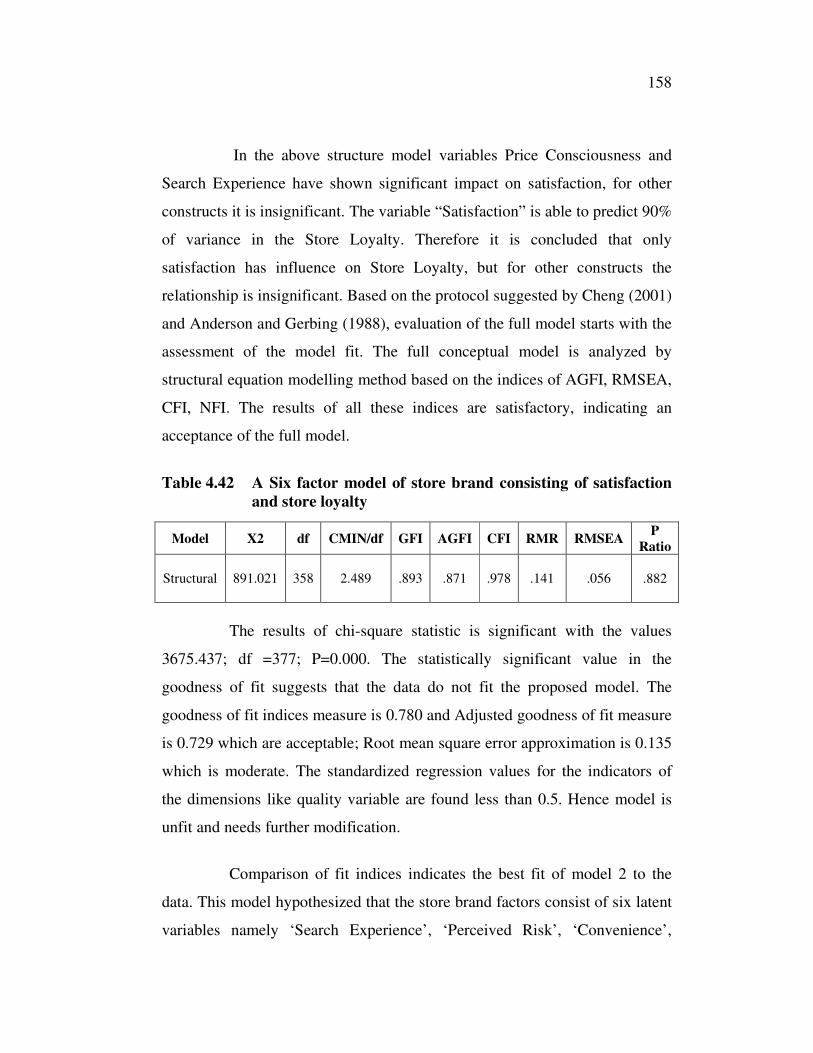

4.9.2 Evaluation of the full structure model 156

4.10 SUMMARY 159

5 FINDINGS, CONCLUSIONS AND IMPLICATIONS 161

5.1 INTRODUCTION 161

5.2 SIGNIFICANCE OF FINDINGS 162

5.3 CONSUMER FACTORS INFLUENCE STORE

BRAND PURCHASE 167

5.3.1 Price Consciousness 167

5.3.2 Quality Variable 167

5.3.3 Price–Quality Association 168

5.3.4 Search Experience 169

5.3.5 Perceived Risk 169

5.3.6 Convenience 171

5.4 CONSUMER SATISFACTION AND

LOYALTY TOWARDS RETAIL OUTLETS 172

xvii

CHAPTER TITLE PAGE

NO. NO.

5.5 IMPACT ANALYSIS OF STORE

BRAND FACTORS, STORE IMAGE

ON CONSUMER SATISFACTION

AND STORE LOYALTY 172

5.6 CONCLUSIONS ABOUT THE RESEARCH

PROBLEM 173

5.7 IMPLICATIONS FOR THEORY 174

5.7.1 Contribution to academic theory 174

5.7.2 Contribution to organized retail sector 175

5.8 MANAGERIAL IMPLICATION 176

5.8.1 Recommendations to specific retail

outlets 178

5.8.2 Suggestions to develop Store Brands 180

5.9 FURTURE RESEARCH 184

5.10 CONCLUSION 185

APPENDIX

QUESTIONNAIRE 187

STORE BRAND PRODUCTS 191

REFERENCES 195

LIST OF PUBLICATIONS 221

CURRICULUM VITAE 222

xviii

LIST OF TABLES

TABLE TITLE PAGE

NO. NO.

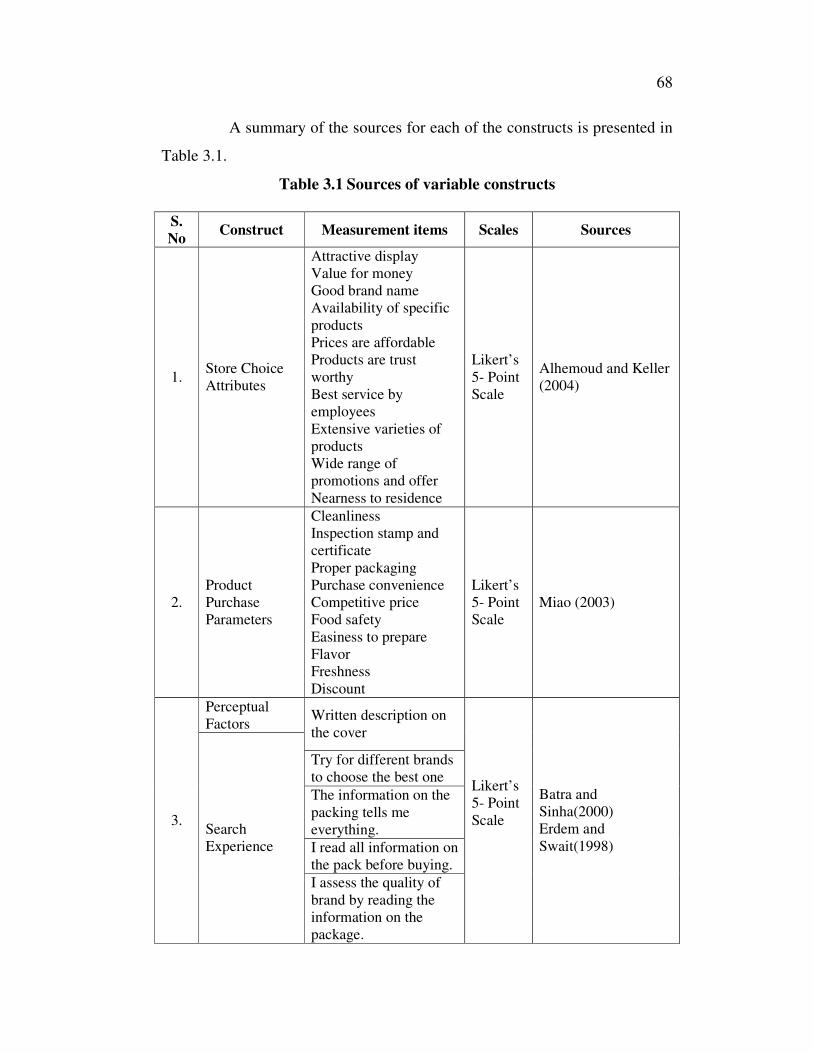

3.1 Sources of variable constructs 68

3.2 Determination of sample size 74

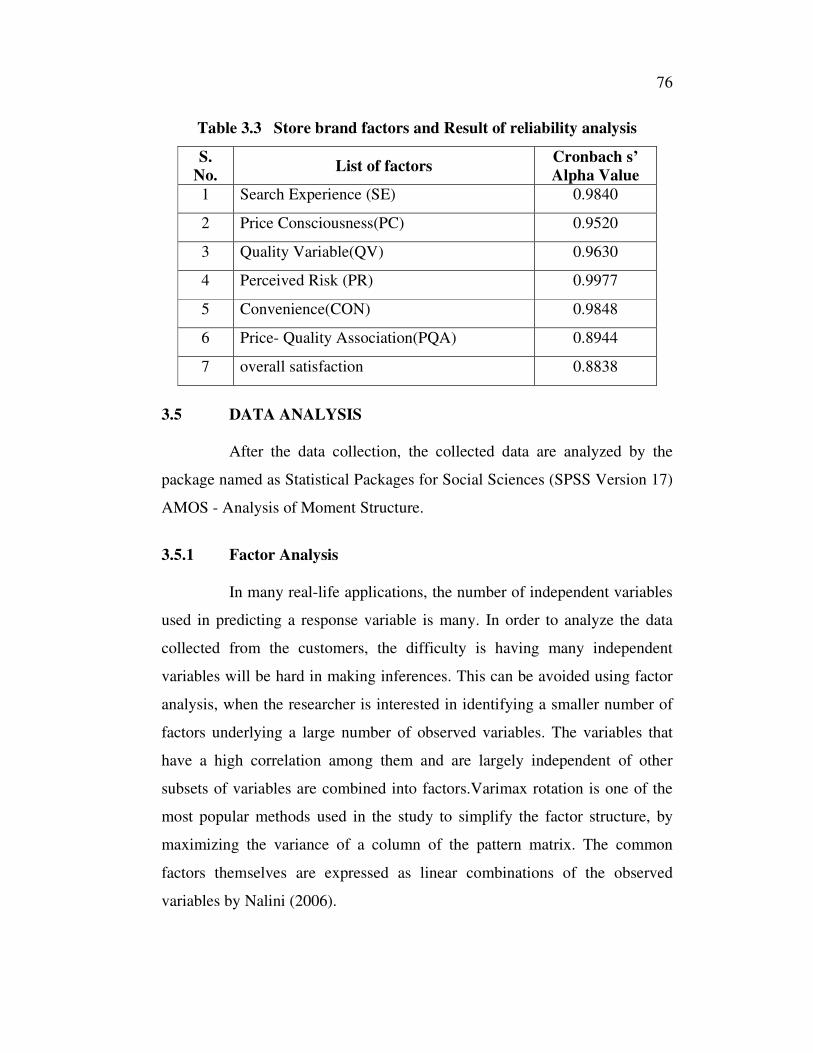

3.3 Store brand factors and Result of reliability analysis 76

4.1 Response rate 85

4.2 The distribution of respondents in retail sector-wise 86

4.3 Profile of the respondents 87

4.4 Gender and store choice attributes 92

4.5 Age group and store choice attributes 93

4.6 Occupational level and store choice attributes 95

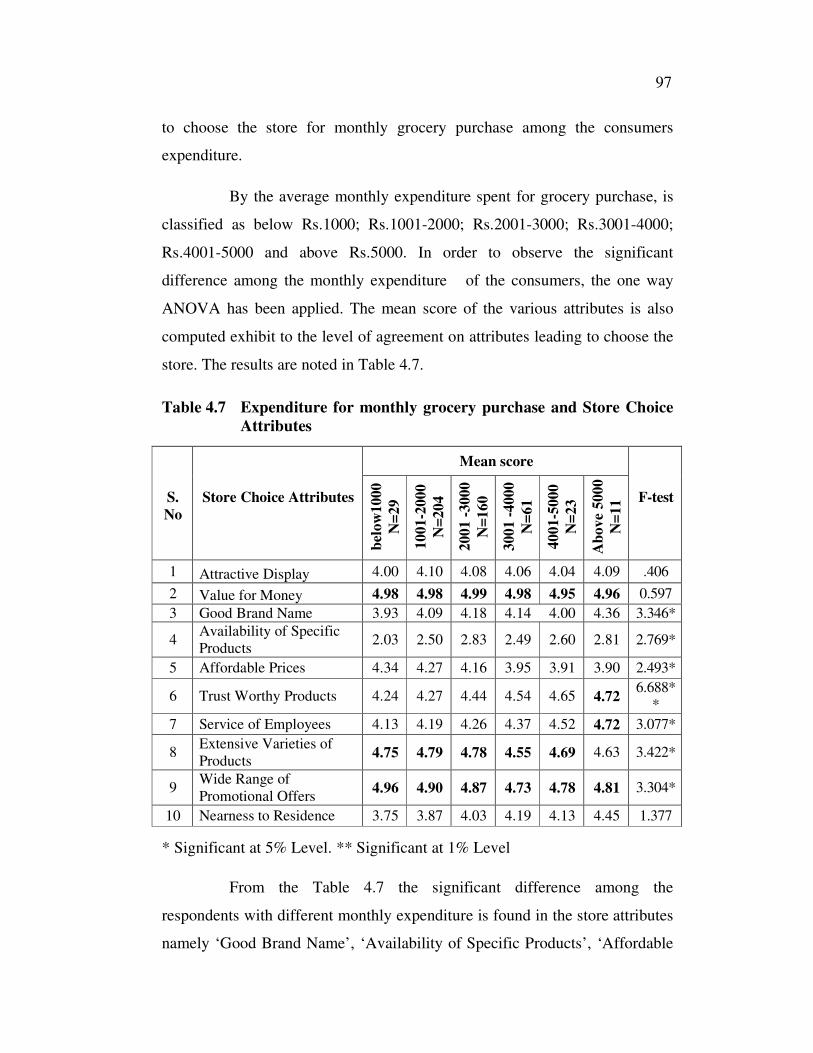

4.7 Expenditure for monthly grocery purchase and store choice

attributes 97

4.8 Frequency of consumer visit and store choice attributes 99

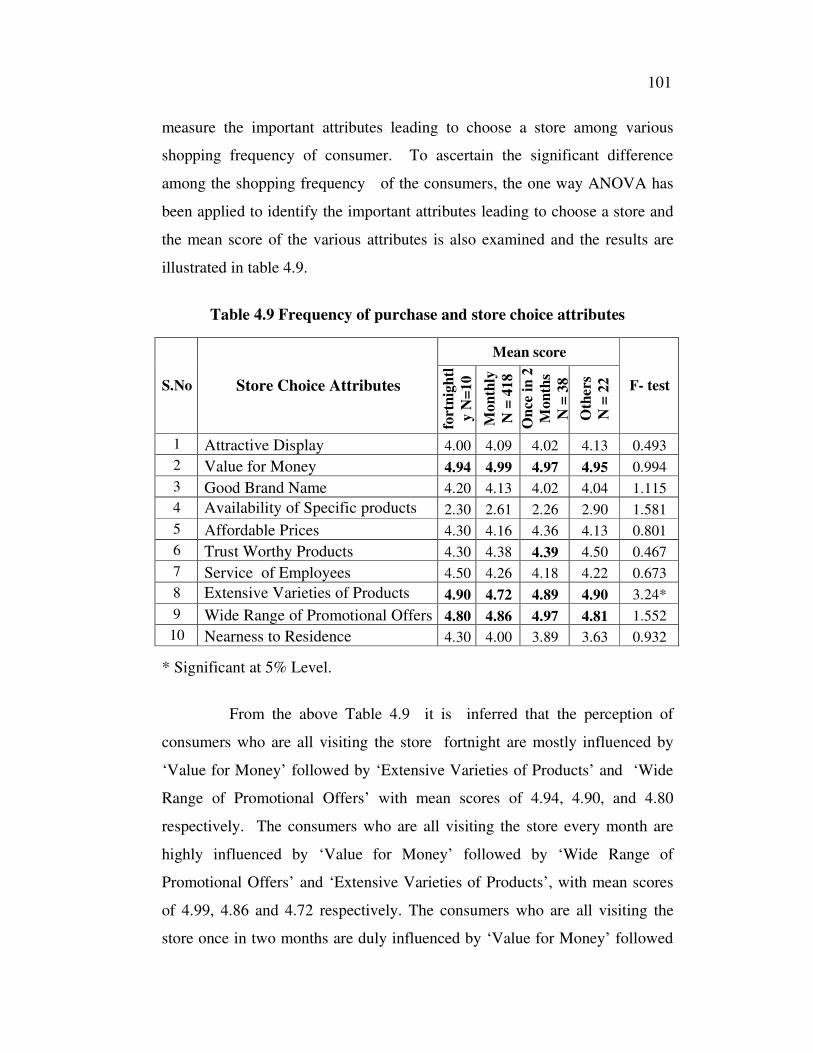

4.9 Frequency of purchase and store choice attributes 101

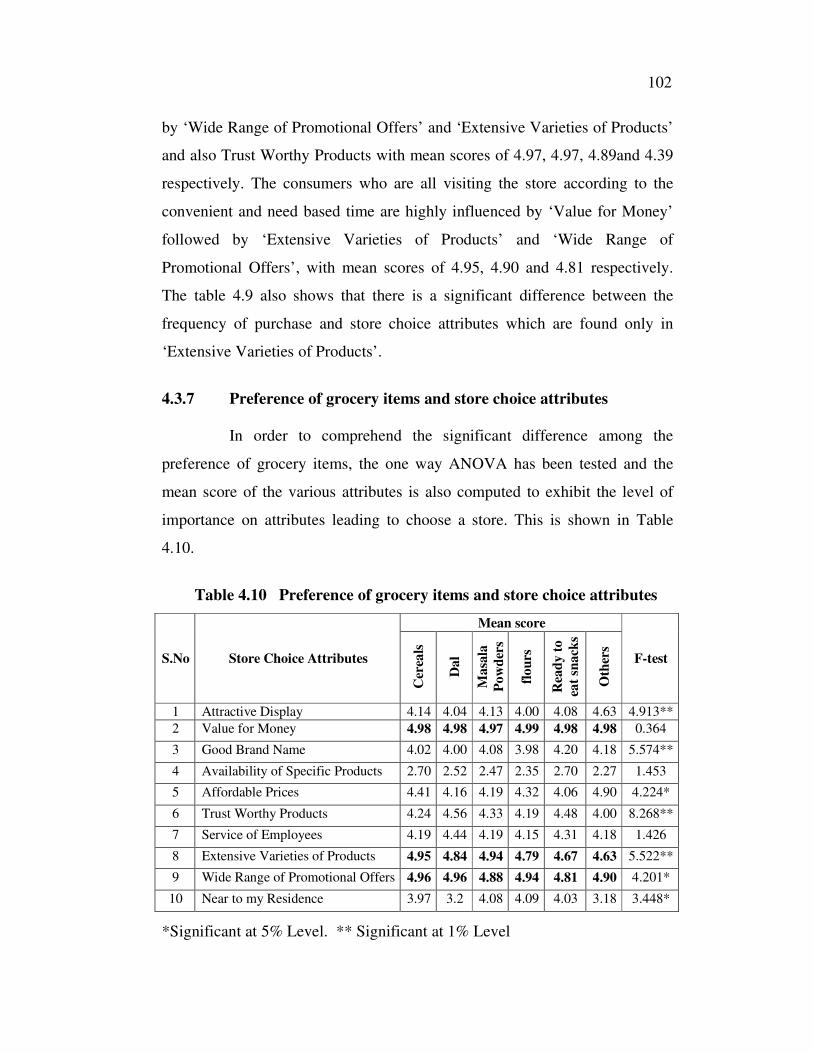

4.10 Preference of grocery items and store choice attributes 102

4.11 Frequency of store brand purchase and store choice

attributes 104

4.12 Consumer preference on store choice attributes of retail

outlet 106

4.13 The table showing association between the profile of the

consumer and the attitudes on the purchase parameters of

store brands 109

4.14 Gender and consumer attitude towards store brands 113

4.15 Age and consumer attitude towards store brands 114

4.16 Occupational level and consumer attitude towards store

brands 116

xix

TABLE TITLE PAGE

NO. NO.

4.17 Monthly grocery expenditure and consumer attitude

towards store brands 118

4.18 Duration of consumer visit and consumer attitude

towards store brands 120

4.19 Frequency of purchase and attitude towards store brands 121

4.20 Preference of grocery item and attitude towards store

brands 123

4.21 Duration of store brand purchase and attitude towards

store brands 124

4.22 Consumer attitude towards store brands in retail outlets 126

4.23 KMO and Bartlett's test 127

4.24 Communalities 128

4.25 Total Variance Explained 129

4.26 Total Variance 130

4.27 Rotated Component Matrixes 131

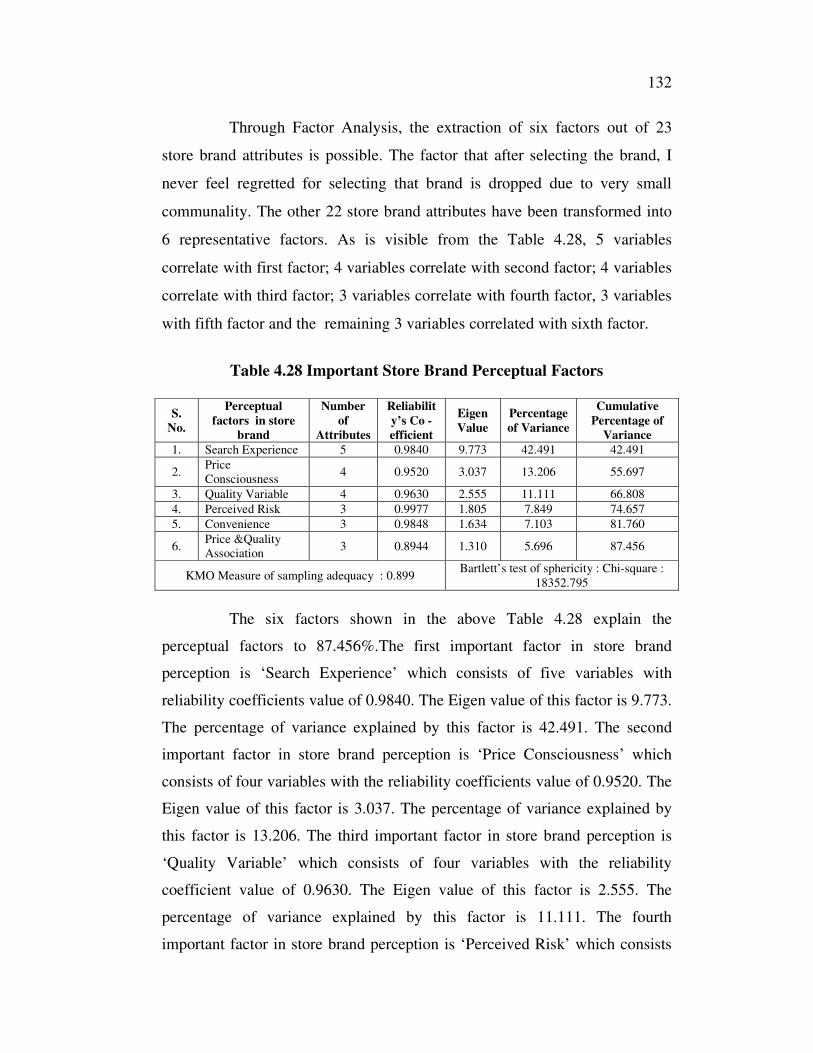

4.28 Important Store Brand Perceptual Factors 132

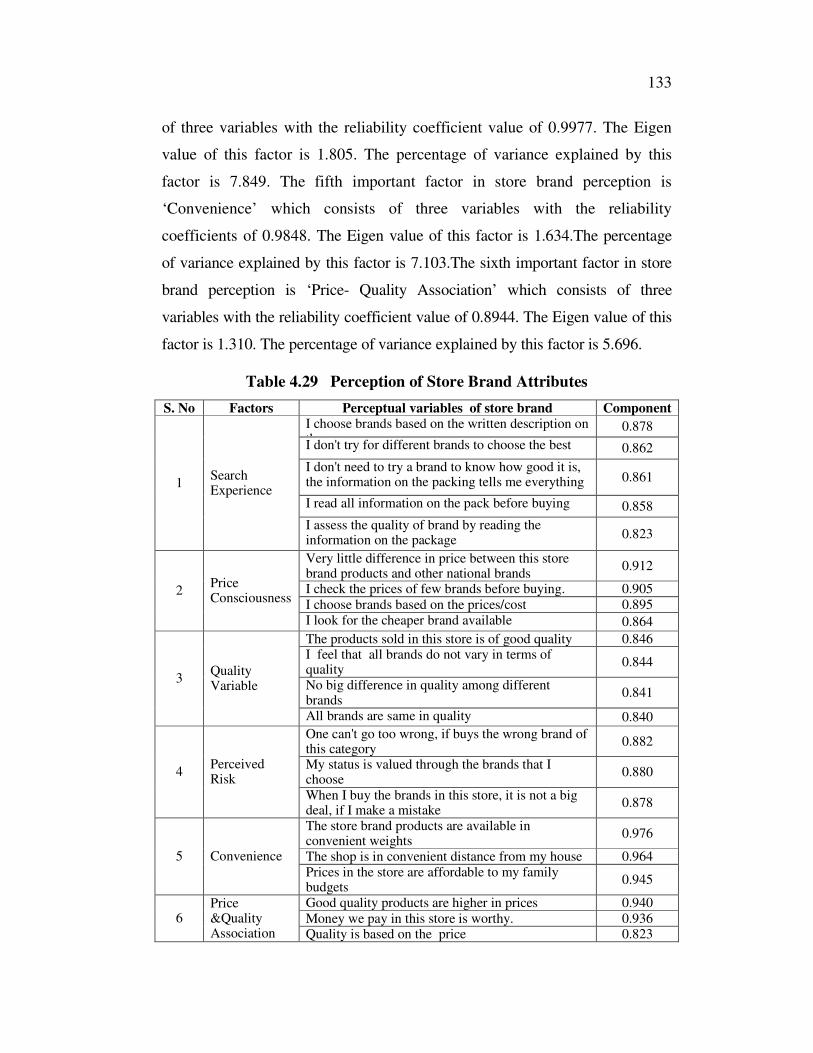

4.29 Perception of Store Brand Attributes 133

4.30 Result of correlation between customer satisfaction and

perceived store brand factors 139

4.31 Regression co-efficient 140

4.32 Impact of store brand factors on consumer satisfaction 141

4.33 Result of correlation between store loyalty and perceived

store brand factor 142

4.34 Regression co-efficient 143

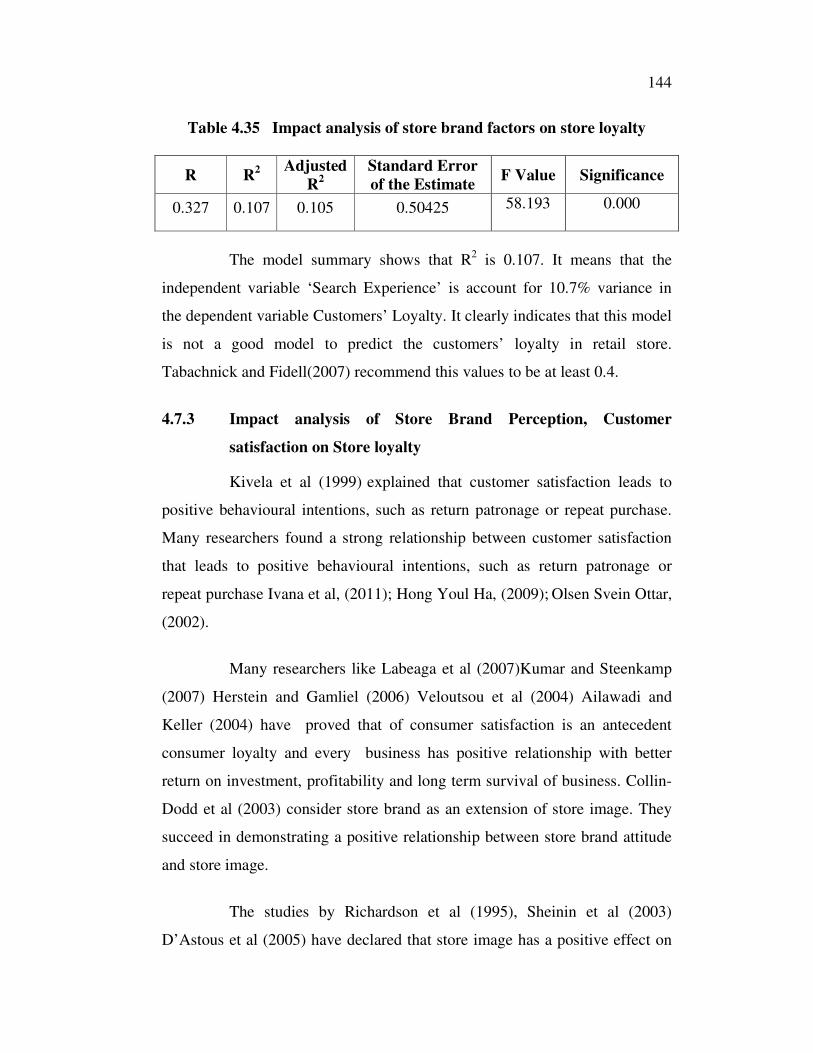

4.35 Impact analysis of store brand factors on store loyalty 144

4.36 Regression co-efficient 145

4.37 Impact analysis of consumer satisfaction on store loyalty 146

4.38 Consumer satisfaction score of the retail outlets 148

xx

TABLE TITLE PAGE

NO. NO.

4.39 Store loyalty score of the retail outlets 150

4.40 Variables of store brand perceptual factors, consumer

satisfaction and store loyalty 153

4.41 The six factor model of store brand factors with

Satisfaction and store loyalty 155

4.42 A six factor model of store brand consisting of

satisfaction and store loyalty 158

xxi

LIST OF FIGURES

FIGURE TITLE PAGE

NO. NO.

1.1 Research model 62

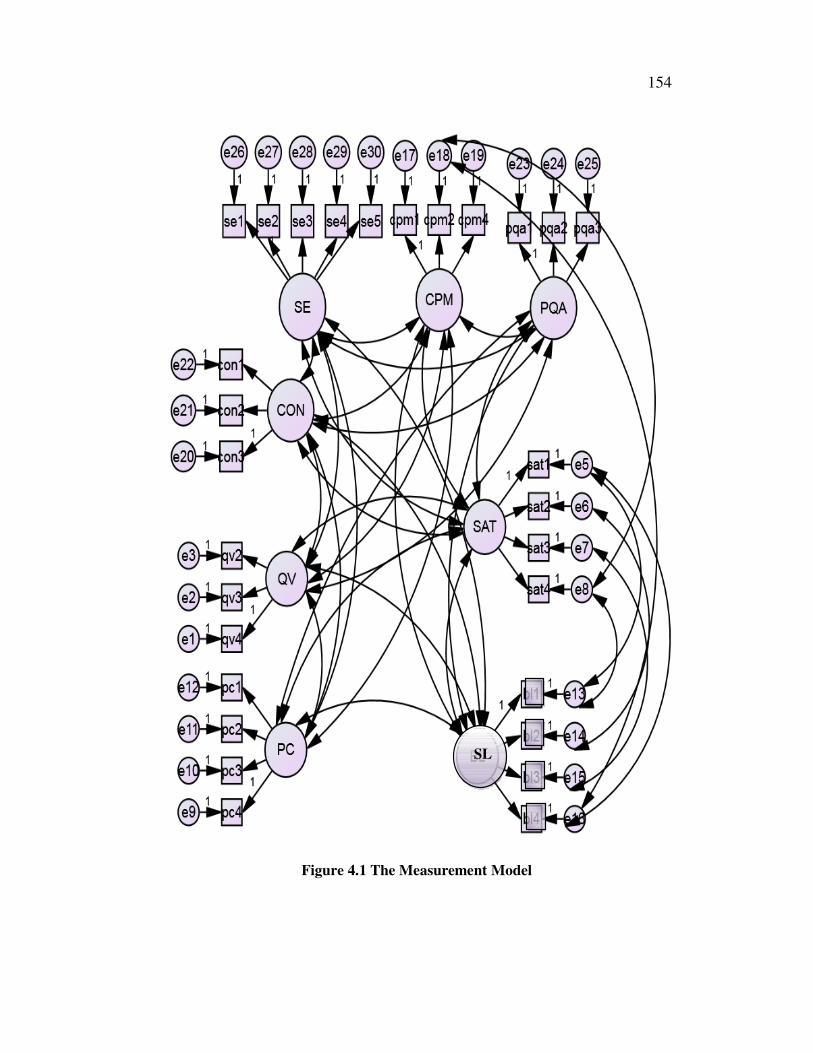

4.1 The Measurement Model 154

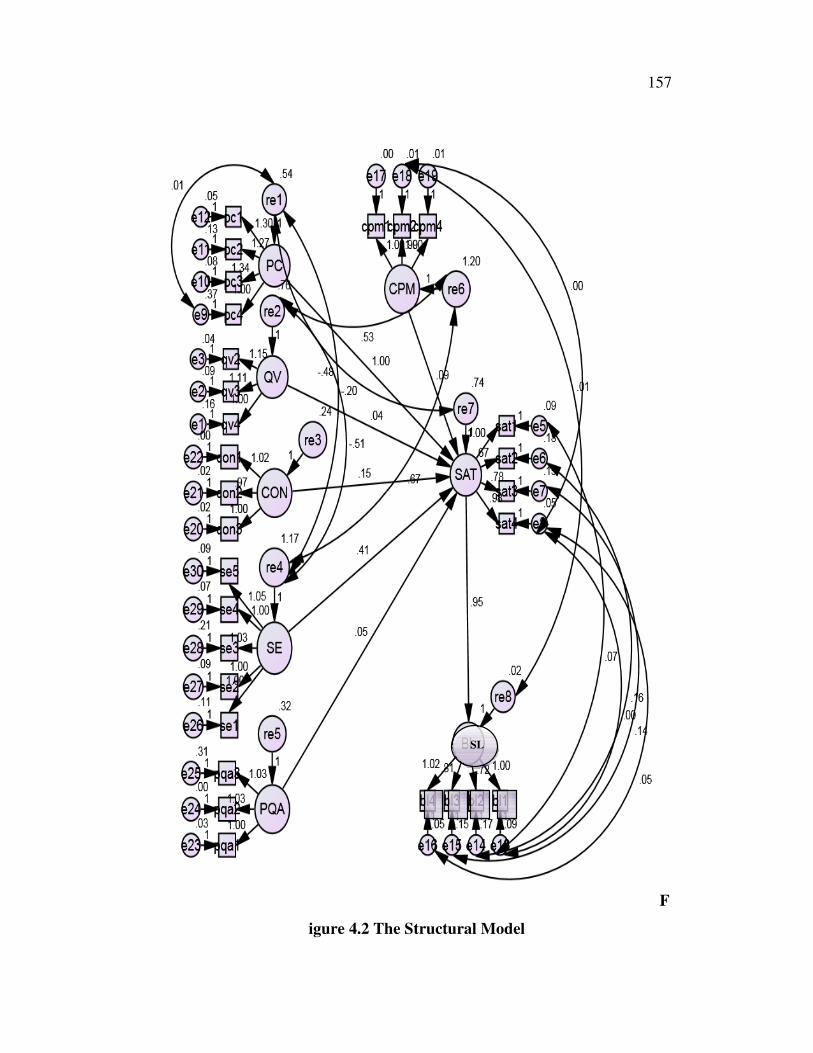

4.2 The Structural Model 157

xxii

LIST OF ABBREVIATIONS

1. AGFI – Adjusted goodness of fit index

2. AMA – American Marketing Association

3. AMOS – Analysis of Moment Structure

4. CAGR – Compound Annual Growth Rate

5. CFA – Confirmatory factor analysis

6. CFI – Comparative Fit Index

7. CON – Convenience

8. EFA – Exploratory Factor Analysis

9. FDI – Foreign Direct Investment

10. FMCG _ Fast Moving Consumer Goods

11. GDP – Gross Domestic Product

12. GFI – Goodness of fit index

13. ICRIER – Indian Council for Research on International

Economic Relations

14. KMO – Kaiser Meyer Olkin

15. MBO – Multi Brand Outlets

16. PC – Price Consciousness

17. PLMA – Private Label Manufacturers’ Association

18. PQA – Price-Quality Association

19. PR – Perceived Risk

20. QV – Quality Variable

21. RMSEA – Root Mean Square Error of Approximation

22. RRL – Reliance Retail Limited

23. S.E – Standard Error

24. SE – Search Experience

25. SEM – Structural Equation Model

26. SKDS – Shri Kannan Departmental Store

27. SPSS – Statistical packages for Social Sciences

1

CHAPTER I

DESIGN OF THE STUDY

1.1 INTRODUCTION

The organized retail sector is growing at a faster pace. Organized

retail sector in India is at the nascent stage and has tremendous potential with

respect to all the types of formats. The competition in the organized retail

sector is increasing day by day. To keep up the competition, retail marketers

find out various ways and methods to survive in today’s cut-throat

competition. Enhancing the effectiveness of retail organization is possible

with a differentiating factor. Store brands give an edge to create a favorable

impact on consumers. Every retailer today wants to capitalize on its product

offering. Store brand is a strategic tool which every retailer in the organized

sector capitalizes. In the retail competitive or world, store brand is emerging

as a new business concept and is gaining momentum. Many of the large

retailers have a wide range of store brands, irrespective of the product

category that they deal in retail marketers. Now-a-days they are managing

their proprietary brands with the same combination of care and innovation as

manufacturers of national brands. Currently, retailers have been liberating

themselves from the traditional definition of store brand marketing as poor

compared to the national brand consumer goods and thus opening up large

opportunities for store brands branding. These opportunities require adoption

of different set of marketing and branding practices to support and propel the

retailers’ business and marketing ideas for store brands.

2

1.2 STORE BRANDS – AN OVERVIEW

Store brand products are typically those manufactured or provided

by one company for offer under another company's brand. Store brand goods

are available in a wide range of industries from food to cosmetics to car care.

Now-a-days major supermarkets, hypermarkets, drug stores and discounters

offer many products under the retailer's brand.

For the store brand owners advantages are very significant and

numerous. Some of the benefits are full control over the brand and its

positioning, increased freedom in pricing strategy, more flexibility and shorter

time-to-market for innovative products, reduced producer domination in the

marketplace, improved control over stock levels, increased client dependence

and customer loyalty, deduced supplier dependence, increased sales

possibilities, opportunity to differentiate and provide variety, positive image

building and marketing efforts. These are the benefits to oneself, not to that of

competitors. For the end-user, storebrands represent the choice and

opportunity to regular purchase quality products in savings, compared to

manufacturer brands, without waiting for promotional pricing. Store brands

items consist of the same or better ingredients than the manufacturer’s brands.

As the vendor’s name or symbol is on the package, the end-user is assured

that the product meets the vendor’s quality standards and specifications.

The American Marketing Association describes store brands as “a

brand that is owned by the product's reseller rather than by its manufacturer”

(p.33). In rare instances, the reseller may be the manufacturer as well. The

term is often associated with advertised brand versus unadvertised brand, a

private brand which is unadvertised and national brand versus regional brand

3

or local brand, a private brand which is usually less than national. These

distinctions have become clouded by large retail and wholesale organizations

like Sears, Kroger, Kmart, Ace, who advertise their private brands and market

them nationally and internationally. A brand name or label name is attached

to or used in the marketing of a product other than by the product

manufacturers usually by a retailer.

Store brands are called by different names in different context such

as store brands, own brands, own labels, private brands, retailer’s brands and

home brands as stated by Pedro Galvan Guijo (2007). Baltas (1997) defines

store brands as “brands owned, controlled, and sold exclusively by a retailer”

(p.3). Store brands are products that are developed by retailers and made

available for sale only through retailers.

The store brand revolution was first observed in Europe and

Canada. Store brands that were first introduced over 100 years ago in few

product categories had tremendous growth over a period of time as stated by

Tarzijan (2004). One of the early motivations for retailers to introduce store

brands was to improve retailer’s gross margins. Hoch and Banerji (1993)

have observed that retailer’s gross margins on store brands were 20 to 30 %

higher than on national brands. Raju (1995) has found that store brands add

diversity to the product line in a retail category.

Another key motivation for retailer is to create competitive

advantage through store differentiation by offering products’ uniqueness to

the store. Store differentiation in turn is expected to increase store patronage

and to create store loyalty as described by Quelch and Harding (1996). By

introducing store brands, retailers strengthen their bargaining power with

manufacturers. Store brands are often designed to compete against branded

products, offering customers a cheaper alternative to national brands. Through

the actual or potential threat of store brands the retailers take share from

4

national brands, and so negotiate lower wholesale prices was found by

Narasimhan and Wilcox (1998).

Fernie et al. (2003) have identified various advantages to retailers

for the development of a store brand which includes, increased profitability

through cost saving and increased margins; increased store loyalty and

creation of a distinct corporate identity; opportunities to seize new market

ventures and increased bargaining leverage with suppliers.

The proliferation of store brands of grocery products reflects a

major shift in the product mix offered by retailers. Store brands provide

consumers with a competitive alternative to national brands. Store brands

offer lower prices owing to their lower manufacturing costs, inexpensive

packaging, minimal advertising and lower overhead costs. For retailers, store

brands offer an opportunity to increase store traffic and to build store loyalty.

Although store brands are generally priced lower than national brands, the

higher margins earned on the products enable retailers to expand into lower

volume categories for which success is greater per unit contribution margins.

More importantly, the availability of proprietary brands not sold elsewhere

encourage store loyalty and increase store traffic.

Store brands offer several benefits to both retailers and customers,

driving the segment's rising popularity. For retailers margins on store brand

goods are an average of 10% higher than those on similar branded products.

Customers benefit from store brands' lower prices, which are often

significantly lower than those of national brands. While both retailers and

consumers are benefited, substantial pressure is put on the manufacturers of

branded goods, who have to compete against their own customers, especially

the retailers, for market share. Though the public generally see them as low-

cost imitations of branded products, store brands have overcome this

5

disreputation and have achieved significant growth in recent years.

Department stores, electronics stores, and office supply retailers offer store

brand products or services.

1.3 RETAILING IN INDIA – AN OVERVIEW

India is one of the largest emerging markets, with a population of

over a billion. It is one of the largest economies in the world in terms of

purchasing power. Retailing in India is at a nascent stage of its evolution.

Within a short period of time certain trends are clearly emerging which are in

line with the global experiences. Organized retailing has become more

popular in big cities in India. Most of the metropolitan cities and other big

cities are flooded with modern organized retail stores. Many semirural areas

have also witnessed entry of such organized retail outlets.

India's retail sector is estimated to touch US$ 833 billion by 2013

and US$ 1.3 trillion by 2018, with a Compound Annual Growth Rate (CAGR)

of 10%, which is quite lucrative. Retailing as a whole contributes almost 10%

of India’s Gross Domestic Product (GDP), and employs almost 8% of India’s

employable population. The McKinsey’s report 'The rise of Indian Consumer

Market', estimates that the Indian consumer market is likely to grow four

times by 2025 as described in Tazyn Rahman (2012).

As an emerging market with high growth rates, consumers’

spending has risen sharply as the youth population, which is more than 33 %

of the country has seen a significant increase in its disposable income.

Consumer spending has risen up to 75% in the past four years. The organized

sector accounts for mere 5% indicating a huge potential market opportunity

and the purchasing power of Indian urban consumers is also growing.

Branded merchandise in categories like apparels, cosmetics, shoes, watches,

beverages, food and jewellery are slowly becoming lifestyle products that are

widely accepted by the urban Indian consumers.

6

In the past few years, retailing has emerged as one of the most

important sectors of the Indian economy in terms of its contribution to the

Gross Domestic Product (GDP) and employment creation. The lucrative

growth of the Indian retail has prompted many corporate giants such as

Reliance, ITC, Aditya Birla group to enter into the retail market in the last

few years. At present, many foreign players are also observing the Indian

retail arena keenly. This has further increased the competition in the retailing

sector. Although a major chunk of the Indian retail sector is accounted by the

unorganized market, a tremendous growth is witnessed in the organized retail

sector.

1.4 THE FACTORS DRIVING THE GROWTH OF RETAIL

SECTOR IN INDIA

Indian economy is growing at the rate of 8%, indicating a

prosperous future. The consistent economic growth has resulted in a decent

rise in the income level of the middle class. The wealth of the consumer has

resulted in a revolution of the retail industry. Many international brands have

entered the market. With the growth in organized retailing, unorganized

retailers have brought drastic changes in the business models. Many factors

which are responsible for the growth of retail sector are as follows:

1. Increasing disposable income: Rise in disposable incomes, in middle

class and lower middle class with increase in employment

opportunities for young adults in IT, and IT enabled sectors is the

major cause of retail growth in India.

2. Increasing number of dual income in nuclear families: In India, hefty

pay packets, nuclear family along with increasing working women

population and dual income family are the factors contributing to the

prosperous retail sector.

7

3. Changing lifestyle and consumer behavior: Due to increasing working

population comfortable life, travel and leisure are given importance.

These key factors are growth drivers of retail sector in India which

boast retailing in almost all the preferences of life such as apparel and

accessories, appliances, electronics, cosmetics and toiletries etc.

4. Experimentation with formats: Due to the competition in the market,

retailing is still evolving and the sector is witnessing a series of

experiments with new formats.

5. Store design: Shopping malls and super markets are growing at a very

faster rate. Improvements in infrastructure and enhanced availability of

retail space, store design are the factors that increase the share of the

organized retail and thereby contributing to the growth of Indian retail

sector.

1.5 ORGANISED AND UNORGANISED RETAIL IN INDIA

The Indian retail industry is the fifth largest in the world,

comprising of organized and unorganized sectors. It is one of the fastest

growing industries in India, especially over the last few years. Initially, the

retail industry in India was mostly unorganized. With the change of tastes and

preferences of the consumers, the industry is getting more popular these days

and is being well organized. With growing market demand, the industry is

expected to grow at a pace of 25-30% annually.

1.5 .1 Unorganised Retail Sector in India

India’s retail is dominated by a large number of small retailers

consisting of the local kirana shops, owner manned general stores, chemists,

footwear shops, apparel shops, paan and beedi shops, hand-cart hawkers,

pavement vendors etc. They together make up the so-called unorganized

retail. Vidushi Handa (2012) state that undeniably, around 96% of Indian

retail sector is unorganized and majority of sales take place through

8

unorganized stores popularly known as kirana or mom-and-pop stores. The

unorganized retail sector is expected to grow at about 10% per annum with

sales rising from 309 billion in 2006-07 to reach US $ 596 billion in 2011-13.

Despite the steady expansion of organized retailers, it is growing at a faster

rate. Unorganized sectors are still preferred by the customers as they are

more convenient and easy to approach. The kirana shop owner knows that the

buyer prefers place first and utility next. The total number of traditional

retailers is estimated to be 13 million by Technopak Advisers Pvt. Ltd.

1.5.2 Organized retail sector in India

Organized retail is reflected in sprawling shopping centers,

multiplex-malls and huge complexes which offer shopping, entertainment and

food under one roof. The last 3-4 years have witnessed the entry of a number

of organized retailers by opening stores in various modern formats in metros

and other important cities. Organized retailing has begun to capture the

enormous market but its share is small. A number of large business houses

have entered the retail business with ambitious expansion plan.

However, opinions are divided on the impact of the growth of

organized retail in the country. Concerns have been raised that growth of

organized retail will have an adverse impact on retailers in the unorganized

sector. It has also been that growth of organized retailing will yield

efficiencies in supply chain; enable better success to markets and to producers

including farmers and enable higher prices on the one hand and lower prices

to consumers, on the other. In India, organized retail contributed roughly 4%

of the total Indian retail from 2006 to 07, which is very small compared to

most of the emerging market economics. It has been projected to grow at a

compound rate of 40-45 % per annum and is estimated to contribute 16% to

the total Indian retail from 2011 to 12. According to the study conducted by

ICRIER (Indian Council for Research on International Economic Relations),

9

annually total retail business in India has grown at 13% , from US $322

billion in 2006-07 to US $590 billion in 2011-12 and in future it will increase

up to US $1 trillion by 2016-17. The regulatory controls on Foreign Direct

Investment (FDI) have been relaxed considerably in recent years. Currently

the government allows 51% FDI in single brand retailing and 100% in cash-n-

carry business. However, the government’s plan to further open up the retail

sector has hit the road block after facing strong political opposition and

nationwide protests by small traders against the proposal to allow FDI in

multiband retailing. The Government is also apprehensive about the uncertain

future of this sector considering the vote bank attached to retail. The political

environment is quite willing to take 100% risk FDI in retail. The major

challenge facing the organized sector is competition from unorganized sector.

The traditional retailing has been established in India for some centuries and it

is a low cost structure, mostly owner-operated, negligible real estate, labour

costs and payment of little or no taxes.

The Indian retail sector is highly fragmented, consisting

predominantly of small, independent, and owner managed shops. The

domestic organized retail industry is at a nascent stage. India has got started

with organized chain retailing just a few years ago. There are just very few

categories, the most prominent being apparel, where organized retail chains

have had a significant presence. Indian retailers have done very well

particularly after taking into account the various obstacles and hindrances like

real estate costs, lack of trained manpower etc. Growth of organized sector of

retailing will yield efficiencies in the supply chain, enabling better access to

markets, to producers and to customers. The strength of organized retail lies

in resource availability. It is translated into efficient supply chain

management, leading to faster inventory turnaround, resulting in improved

bottom lines. India’s organized sector is all set to explode, while the existing

players such as Future group, Bharti, Reliance Retail, Essar, Shopper’s Stop

10

and Aditya Birla group are endeavoring to consolidate their markets and

others such as Mahindra and Mahindra, Parsavnath and India bulls have

announced plans to enter the retail sector.

1.6 TRANSFORMATION OF RETAILERS IN THE STORE

BRAND

In the past, the retail companies were able to add only little value to

the customers. The retailers were simply seen as intermediaries who just

enabled the flow of goods and services between suppliers and consumers. At

the advent of modernization in retailing, which has been visible in developed

and emerging economies, the retailers become active agents with their own

rights within the value chain. The growth of larger firms and concentration of

retail ownership has led to the growth of buyers’ power, integration of supply

chain, consistent supply and availability of wider range of goods including

store brands. It has also led to the development of new retail formats in new

locations. From the marketer’s point of view it is observed that the retailers

are closer to the consumers than to suppliers. The significant flow of money,

people and goods through the retail supply chain has made the sector’s

businesses as the influential corporate players in the developed economics.

Store brand is a hot concept today and retailers are introducing

store brands to gain market share. For instance, Pantaloon's Food Bazaar has

introduced its store brand as Tasty treat, in the snacks category which has

gained a significant share in the market today. Retailers today have store

brands because of the following reasons:

• Manufacturing cost in the case of store brands is less because of the

elimination of the middlemen.

• The bargaining power of the retailer is enhanced.

• Since a large proportion of the store brands is mostly sold in the

retailer's own stores, it creates a sustainable competitive advantage for

the retailer and also helps to win customers’ loyalty.

11

• The pricing of the store brands is more competitive as compared to the

manufacturers’ brand.

• One of the main reasons for the wide introduction of the store brands is

the conflict between the retailers and the manufacturers. Many times,

manufacturers supply low quality products to the retailers in a bid to

earn extra profits. Azad (2010) has stated that, retailers prefer to have

their own in-store brands to ensure that the customers are satisfied and

are not supplied with low quality products.

Manufacturers and supermarkets have a long strong relationship as

member’s dependence. However, many situations have led supermarkets to

change the balance in the relationship with manufacturers and to re-design

their store brand programs. As reported by different authors, there are several

factors that motivated supermarkets to boost store brand and contribute to the

growth of organized retailing. The factors are as follows:

First, an excessive price increase by national brand manufacturers:

The 1980s was a decade that saw substantial increase in prices of the

suppliers as stated by Nandan and Dickinson (1994).

Second, the rising of retailing power: Wileman and Jary (1997)

state that the producer brands have dominated the consumer goods industry

for most of the last century. Nevertheless retailers have become large-scale,

concentrated, centralized, and sophisticated due to mergers and acquisitions

Thirdly, the smart consumers are mostly educated people who

tend to be among the most conscientious consumers: Nandan and Dickinson

(1994) have stated that the consumers have noticed the discrepancy in value

when price differences become very large. In general, consumers have

become more astute in the judgment of value and are less influenced by the

12

assumed social status of purchasing a certain brand and value-oriented

consumers demand value for money.

Fourth, the excess production capacity: Peles (1976) has reported

the excessive capacity production of manufacturers as a factor that facilitated

the store brand introduction. Consequently, Patty and Fisk (1982) have

reported that store brands have emerged as a key weapon and have started to

play an important role in the battle for control of the distribution channel and

consumer loyalty.

Mills (1995) indicates in the article that “The net effect of store

brand marketing is to improve the performance of supermarket distribution

channels.”(p.509) and also reported that store brands are the instruments that

retailers used to capture more profit out of the distribution channel.(p.513)

Supermarkets believe that manufacturers have a high profit margin and want

to increase the profit margin by considering distribution channel.

In addition supermarkets want to create consumers’ dependence on

them and reduce dependence on manufacturers of national brands. Lewison

and Balderson (1999) have identified that through a store brand program

supermarkets enhance store loyalty and brand loyalty. The majority of the

retailers focus on the store brand strategy especially on the price by

attention to low quality. However, retailers have recently started to pay more

attention to store brand’s quality.

1.7 THE IMPORTANCE OF STORE BRANDS IN THE

RETAILING INDUSTRY

Store brands are an important source of profits for retailers and are

formidable sources of competition for national brand manufacturers as stated

by Hoch and Banerji (1993). The success of store brands is seen as a

consequence of cleverly designed branding strategies employed by the

13

retailers described by Keller (1998). Dunne and Narasimhan (1999) have

stated that store brands have been claimed by the manufacturers as category

killers, which are cheap, me-too products taking profits out of a market by

making consumers more price-sensitive. Some marketing researchers like

Hoch (1996) and Verhoef et al. (2002) have investigated how branded

manufacturers respond effectively to the competition of store brand.

Ailawadi (2001) states that the importance of store brand success

for retailers has been evident in several ways. For instance, store brands bring

greater profits to retailers; increase retailers’ market power and bargaining

power; generate store loyalty and differentiate the retail outlets from other

chain stores

In addition, a successful store brand strengthens the negotiating

position of retailers in relation to national-brand manufacturers. Retailers have

the advantage of controlling shelf space which results in increased bargaining

power over manufacturers. This is particularly the case for those retailers who

have had some degree of market power. Mills (1995) states that store brands

are substitutes for popular national brands in an attempt to capture more

profits from the vertical structures to share with the manufacturers.

Narasimhan and Wilcox (1998) have shown that a credible store brand

competition allows the retailers to gain better terms of trade from the

manufacturers, such as higher margins on national brands.

Ailawadi (2001) and Steiner (2004) stated that high store brand

share enables retailers to obtain significantly higher profit margins on national

brands by negotiating with manufacturers for a lower price on the national

brands.. Furthermore some researchers like Dick et al. (1995), Miranda and

Joshi (2003), Steenkamp and Dekimpe (1997) also state that a successful

store brand potentially increases customers’ traffic, generates store loyalty

and even distinguishes the store from others by virtue of the fact that, such

14

products are unique to the sponsoring store but different from manufacturer

brands or other store brands.

Corstjens and Lal (2000) indicate that store brands of high quality

are instruments for retailers to generate store differentiation and store loyalty,

thus improving profitability. The empirical results also show that store loyalty

is positively related to store brand use. To summarize, store brands enable

retailers to gain higher margins, to improve their ability to negotiate with their

channel partners, to compete with other rival retailers, and to generate higher

store loyalty.

1.8 MODERN RETAIL FORMATS IN INDIA

The face of Indian retail sector is changing. New and innovative

business models are being adopted. The formats prevalent in retail sector are:-

1. Malls: Mall is the largest form of organized retailing today. Located

mainly in metro cities, in proximity to urban outskirts they range from

60,000 sq ft to 7,00,000 sq ft and above. They lend an ideal shopping

experience with an amalgamation of product, service and

entertainment, all under a common roof. Examples include Shoppers

Stop, Pyramid and Pantaloon.

2. Specialty stores: Focus on specific market segments and have

established themselves strongly in their sectors. Chains such as the

Bangalore based Kids Kemp, the Mumbai books retailer Crossword,

RPG's Music World and the Times Group's music chain Planet M are a

few examples.

3. Discount Stores: As the name suggests, discount stores or factory

outlets, offer discounts on the MSRP (Manufactured Suggested Retail

Price) through selling in bulk reaching economies of scale or excess

stock left over at the season. The product category ranges from a

15

variety of perishable/ non perishable goods. Discount Circuit is one

such example.

4. Department Stores: These are the large stores ranging from 20,000-

50,000 sq. ft, catering to a variety of consumer needs. Further they are

classified into localized departments such as clothing, toys, home,

groceries, etc.

5. Hyper marts/Supermarkets: Large self service outlets, catering to

varied shopper needs are termed as Supermarkets. These are located in

or near residential high streets. These stores today contribute to 30% of

all food and grocery organized retail sales. Super Markets are further

classified into mini supermarkets typically 1,000 sq ft to 2,000 sq ft

and large supermarkets ranging from of 3,500 sq ft to 5,000 sq ft.

having a strong focus on food and grocery and personal sales.

6. Convenience Stores: These are relatively small stores ranging from

400-2,000 sq. ft located near residential areas. They stock a limited

range of high-turnover convenience products and are usually open for

extended periods during the day as well as, seven days a week. The

prices are slightly higher due to the convenience premium.

7. MBO’s: Multi Brand outlets, also known as Category Killers, offer

several brands across a single product category. These usually do well

in busy market places and Metros.

8. E-trailers: These are the retailers providing online buying and selling

of products and services

1.9 PROFILE OF THE STUDY AREA

Madurai city is situated in south-west of Chennai at a distance of

498 kilometers Madurai city lies on the flat and fertile plain of the river

Vaigai which runs in the north-south direction through the city dividing it

almost into two equal halves. The 2011 census showed that the expanded city

corporation had a population of 25,78,201. In Madurai, males constitute

16

50.56% of the population and females 49.44%. The city has an average

literacy rate of 68%, which is higher than the national average of 64.5%. Male

literacy rate is 76%, and female literacy is 61%.

1.10 MAJOR RETAILERS IN MADURAI

1.10.1 Aditya Birla Retail Limited

Aditya Birla Retail Limited is the retail arm of Aditya Birla Group,

a USD 28 billion Corporation. The Company ventured into food and grocery

retail sector in 2007 with the acquisition of a south based supermarket chain

“Trinethra”. Subsequently Aditya Birla Retail Ltd. expanded its presence

across the country under the brand "MORE" with 2 formats: Supermarket and

Hypermarket.

Supermarket More for you - Conveniently located in

neighborhoods. More supermarkets cater to the daily, weekly and monthly

shopping needs of consumers. The product offerings include a wide range of

fresh fruits and vegetables, groceries, personal care, home care, general

merchandise and a basic range of apparels. Currently, there are over 640

MORE supermarkets across the country. The Hypermarket MORE

MEGASTORES, is one stop shopping destination for the entire family.

Besides a large range of products across fruits and vegetables, groceries and

FMCG (Fast Moving Consumer Goods) products, MORE MEGASTORE also

has a strong emphasis on general merchandise and apparels. Currently, eight

hypermarkets are operated under the brand MORE MEGASTORE in Mysore,

Vadodara, Aurangabad, Indore, Bengaluru, Mumbai, New Delhi and

Hyderabad. The Aditya Birla Retail Ltd provides customers a wide choice of

products under its own labels like Feasters, Kitchen's Promise, Enriche,

Germex and Best of India.

17

1.10.2 Reliance Retail Limited

Reliance Retail Limited (RRL), is a subsidiary of Reliance Limited.

Since its inception in 2006, RRL has grown into an organization that caters to

millions of customers, thousands of farmers and vendors. Based on its core

growth strategy of backward integration, RRL has made rapid progress

towards building an entire value chain starting from the farmers to the end

consumers. More than 3 years into operation, RRL has now expanded its

presence in more than 85 cities across 14 states in India. RRL has forged

ahead with its expansion plans and runs stores across the country. RRL’s

footprint now spans a network of more than 1,000 stores. RRL operates

several ‘Value’ and ‘Speciality’ formats. The ‘Value’ formats that RRL

operates are: ‘Reliance Fresh’, a neighborhood concept, ‘Reliance Mart’, an

all under one roof supermarket concept and ‘Reliance Super’, a mini-mart

concept. The ‘Value’ formats offer a wide range and assortment of products

required for daily household needs. The ‘Speciality’ formats are: ‘Reliance

Digital’, a consumer durables and information technology concept,‘ Reliance

Trends’, an apparel and accessories concept, ‘Reliance Wellness’, a health,

wellness and beauty concept, ‘iStore by Reliance Digital’, an exclusive

Apple products concept, ‘Reliance Footprint’, a footwear concept; ‘Reliance

Jewels’, a jewellery concept, ‘Reliance Time Out’, a books, music and

entertainment concept, ‘Reliance AutoZone’, an automotive products and

services concept and ‘Reliance Living’, a home ware, furniture, modular

kitchens and furnishings concept. RRL has rapidly expanded the stores

network and it operates through strategic partnerships with world-class

companies such as Marks and Spencer and Pearl Europe. RRL has also

entered into an exclusive distribution arrangement with Asics Corporation,

Japan, to market Asics brands of shoes and accessories in India. RRL has

recently opened its flagship store under its franchise agreement with Hamleys

18

and plans to expand the store network in the forthcoming years. RRL has also

expanded its presence in business-to business office supplies through its joint

venture with Office Depot. In Madurai it has established its retail outlet in

2005. It has expanded with 18 branches in various areas with an average of

150 customers visiting per day till now.

1.10.3 Spencer's Retail Limited

Spencer's Retail Limited is a Flagship Company of RPG

Enterprises. Spencer's Retail Limited is one of the largest and fastest growing

multi-format retailers in India with footage of approximately 1 million square

feet with, 220 stores, including 30 large format stores across 35 cities in India.

Spencer's focuses on verticals like fresh fruit and vegetables, food and

grocery, personal care, garments and fashion accessories, home and office

essentials, electrical and electronics items. Established in 1996, Spencer's has

become a popular destination for shoppers in India with hypermarkets and

convenient stores catering to various shopping needs of its large consumer

base. The Spencer's Hyper stores are destination stores, with more than

15,000 sq. ft. They offer everything under one roof. The merchandise ranges

includes fruits and vegetables, processed foods, groceries, meat, chicken, fish,

bakery, chilled and frozen foods, garments and fashion accessories, consumer

electronics and electrical products, home decor and needs, office stationeries

and soft toys. The Spencer's stores are neighborhood stores ranging from

1,500 sq. ft. to 15,000 sq. ft. These stores stock the necessary range and

assortment in fruit and vegetables, FMCG (Fast Moving Consumer Goods)

food and non-food, staples and frozen foods and cater to the daily and weekly

top-up shopping needs of the consumers. Music World is India's largest chain

of music stores retailing the widest range of music & home video products

both National and International. Music World's product portfolio comprises of

audio CDs, DVDs and VCDs, CD-ROMs, gaming consoles and software of

all the leading brands, and other music accessories. The company is an

19

important player in the home video market. Music World has successfully

forayed into high end 'personal audio' gadgets of several top brands. The

company also offers DVD players, home theatre systems, speakers and

headphones. In Madurai it has established its retail outlet in 2001. It has

expanded with 4 branches in various areas with an average of 200 customers

visiting per day till now.

1.10.4 Shri Kannan Departmental store

Shri Kannan Departmental store was started in 1985 as a

Departmental Store in Erode named as Sangeetha Shopping Centre. It was

encouraged by the response of the public a Mega Departmental Store was

started in the year 1999 under the name as "Shri Kannan Departmental Store

(P) Ltd.," as SKDS. And it has strong and committed human resource of

around 2500 employees. Shri T. Thanushgaran is Chairman cum Managing

Director of this Company. He actively engaged as a Executive Committee

Member in Tamilnadu Chamber of Commerce & Industry – Madurai and he

got vocational excellence award by Lions Club of Coimbatore. SKDS has

been selected as the best Departmental Store for the Region for the year 2010

by The Ministry of Food Processing Industries (MOFPI) jointly with the Food

Forum of India and will also strive to keep up the same momentum in the

years to come.

SKDS has many branches in all parts of Tamilnadu and presently

22 Departmental Stores were in various districts like Coimbatore, Erode,

Trichy, Salem, Nammakal and Palani. SKDS Group’s annual Turnover in the

last financial year is around Rs. 370 Cores. In Madurai its first branch was

started in the year 2008 which is located in K.Salaipudhur Bypass Road and

subsequently 2 more branches were started in Kamarajar salai

and Theppakulam in 2010 and 2012 respectively.

20

These are large stores ranging from 20000-50000 sq. ft, catering to

a variety of consumer needs. Further they are classified into localized

departments such as clothing, toys, home, groceries, etc. SKDS has stocks of

store brands in food categories including processed food, staples, sauces,

jams, pickles, tea, noodles and others. SKDS uses the name—Kannan—for its

store brand products. SKDS focuses on verticals like fresh fruit and

vegetables, food and grocery, personal care, garments and fashion accessories,

home and office essentials, electrical and electronics.

1.11 OPERATIONAL DEFINITIONS

1.11.1 Retail

The word ‘retail’ is derived from the French word ‘retailer’,

meaning ‘to cut a piece off’ or ‘to break bulk’. In simple terms, it implies a

first-hand transaction with the customer. Retail is the sale of goods and

services from individuals or businesses to the end-user. Retailers are part of

an integrated system called the supply chain. A retailer purchases goods or

products in large quantities from manufacturers directly or through a

wholesale, and then sells smaller quantities to the consumers for a profit.

1.11.2 Retailing

Retailing can be defined as an activity that ensures that customers

derive maximum value from the buying process. This includes the steps

needed to place the merchandise, made elsewhere into the hands of customers

or to provide services to the customers. Retailing is defined as the buying and

selling of goods and services. It is also defined as the timely delivery of goods

and services demanded by consumers at prices that are competitive and

affordable.

21

1.11.3 Organized Retailing

Organized retailing refers to trading activities undertaken by

licensed retailers, who have registered for sales tax, income tax, etc. It

includes the retail chains, corporate backed hyper markets and privately

owned large retail business. Organized retailing is comprised of shopping

malls and huge complexes that offer a large variety of products in terms of

quality and value for money and gives a shopping experience.

1.11.4 Unorganized Retailing

Unorganized retailing refers to the traditional formats of low-cost

retailing like the local kirana shops (mom-n-pop stores); owner manned

general stores; paan/beedi shops; convenience stores; hand cart and pavement

vendors’ etc. Unorganized retailing is defined as an outlet run locally by the

owner or caretaker of a shop that lacks technical and accounting

standardization. The supply chain and sourcing are also done locally to meet

the local needs. Its organized counterpart does not obtain its supplies from

local sources.

1.11.5 Brand

According to American Marketing Association (1996): “A Brand is

a distinguishing name and or symbol, such a logo, trademark or package

design, intended to identify the goods or services of either one seller or a

group of sellers and to differentiate these goods or services from competitors”

(p.536).

According to the Private Label Manufacturers’ Association

(PLMA): “Private label products encompass all merchandise sold under a

retailer’s brand” (p.206). That brand will be the retailer’s own name or a name

created exclusively by that retailer. In some cases, a retailer may belong to a

wholesale group that owns the brands that are available only to the members

22

of the group. In general, private labels are defined as those products owned,

controlled and sold exclusively by a retailer as stated by Raju et al. (1995a);

Mittelstaedt (1992). Dhar and Hoch (1997), Dekimpe (1997) have stated that

the retailer has to accept all responsibility of developing, sourcing,

warehousing and merchandising to marketing such as branding, packaging,

promoting and even advertising.

Fitzell (1992 and 1998) states that the distinction of ownership and

the exclusivity of distribution give the private label its identity. That identity

has been called by several different names in literature. Store products

meeting the definition of private labels are also called house brands; store

brands; private brands; retail brands; retail own brands; own labels or

controlled labels/ control brands; retailer-controlled brands; white labels; own

labels or own brands and premium labels.

1.11.6 Store Brands

Store brands are products that are owned and or licensed

exclusively by retailers, wholesalers, restaurant operators, foodservice

distributors, or suppliers for distribution in their respective segments of the

marketplace.

Retail Branding is a strategy based on the brand concept which

transfers it to a retail company. A retailer’s products are his or her stores that

are marketed in a way similar to branded goods. A retail brand is then a group

of the retailer’s outlets which carry a unique name, symbol, logo or

combination of words. The term ‘Retail Brand’ has to be distinguished from

the ‘Store Brand’. While retail brand refers to store, the term store brand

refers to the product label and is used synonymously with ‘Private Label’.

Often, the retail brand is also used to label the store brand, though it does not

have universal characteristics.

23

1.11.7 Perceived Risk

Perceived risk is most often defined as risk in terms of consumer

perceptions of the uncertainty and adverse consequences of buying a product

In other words, perceived risk is regarded as the “expected negative utility” or

the “expected penalty” associated with the purchase of a particular product or

brand. When purchasing a product a consumer feels that he/she is taking a

functional or psychosocial risk.

1.11.8 Quality Variable

Quality is defined as the totality of feature and characteristics of a

product or service that bears its ability to satisfy stated or implied needs.

1.11.9 Price Consciousness

It means the degree to which the consumer focuses exclusively on

paying lower prices.

1.11.10 Price-Quality Association

It is defined as the generalized belief across product categories that

the level of a price cue is related positively to the level of product quality.

1.11.11 Search Experience Attribute

The Search attributes refers to the tangible features that are verified

before purchase through direct inspection or through readily accessible

sources such as colour, look, packaging, or ingredient content, quality

standards, or other written description on product packaging. The experience

attributes refers to the untouchable, not-easily-described features that are

confirmed only by using the product, for instance, aroma, reliability, or

endurance.

24

1.11.12 Store Image

It means the ‘personality’ of a store or the way in which the store is

defined in the shopper's mind, partly by its functional qualities and partly by

an aura of psychological attributes.

1.11.13 Store Loyalty

It is as the behavioural response as a function of psychological

process. Store loyalty is the operational zed primary store where the consumer

does his or her daily shopping. It also refers to the tendency to repeat

purchase at the same store for similar or other products.

1.11.14 Brand Loyalty

In the branding literature, a consumer is said to be brand loyal,

when consumer consistently purchases a single brand. A consumer who is

loyal to a particular store brand, demonstrates a high level of brand recall. It

has been constructed both as related to store patronage dimension and repeat

purchase of the same brand over time which indicates loyalty and attitudes

resulting in purchase behavior.

1.11.15 Customer Satisfaction

Oliver (1980) defines customer satisfaction as “Customer

satisfaction is a summary of psychological state when emotions surrounding

disconfirmed expectations are coupled with the consumer’s prior feelings

about consumption experience” (p.62).

The following sections outline the background of the research,

research problem and objectives together with the major bodies of theory that

are reviewed. This is followed by a justification for the research and an

overview of the methodology used in the study. Subsequent sections provide

25

an outline of the research work, and prove the definitions adopted and the

final section provides a summary of the chapters.

1.12 BACKGROUND OF THE RESEARCH

Store Brand products have become a global phenomenon and are of

increasing interest to practitioners and academics alike. Ailawadi, Pauwels

and Steenkamp (2008) state that store brands have gained a sizeable share of

global grocery sales and further growth is predicted for the future. These

brands, owned and controlled by retailers, have become a significant threat to

national brand manufacturers as the quality gap between the two closes.

Quelch and Harding (1996) viewed as from the retailer‘s perspective, store

brands are seen as a strategy to improve profitability and store image. The

image of a store in turn is regarded as critical to retail success given the

impact on store patronage, loyalty and profitability is considered by Herstein

and Gamliel; Hansen and Solgaard (2004).

This research work examines the link between store brands and

store choice. Many considerable research works by Baltas and Argouslidis

(2007), Bellizzi and Krueckeberg , Hamilton and Martin (1981) Dick, Jain

and Richardson (1995) have been done to investigate consumers’ perceptions

of store brands as well as the correlation of store preference and loyalty.

Similarly in the research by Baker, Parasuraman, Grewal and Voss (2002),

Mazursky and Jacoby (1986), and Martineau (1958), store image has been the

subject of academic research for over fifty years. The relationship between

store image and attitudes to the brands carried by the store has also been

investigated. The relationship between store image and store brands has been

investigated by some researchers, but mainly in terms of the effect of store

brands on store choice; studies on the opposite causal relationship, the effect

of store image on store brands Collins-Dodd and Lindley (2003), Lee and

26

Hyman (2008), Semeijn, Van Riel and Ambrosini (2004), are common and

have provided varied evidences.

1.13 THE RESEARCH PROBLEM

In line with some researches indicated above, the research problem

addressed in this study is: How does a consumer factor influence a store brand

purchase and how consumer satisfaction leads to store loyalty. The research

work replicates and extends Collins-Dodd and Lindley‘s (2003) and Chen

(2005) study on the influence of store brand on store image and identifies the

impact of store image on overall satisfaction leading to store loyalty.

The research work proves that store choice attributes have effect on

store loyalty. It affects the attitudes to store brands, although the extent of the

effect depends on the satisfaction of store brands on the store image. The

research work further proves that the quality of the products carried by the

store is a key determinant of attitudes to specific store brands. There are some

supports for the original study conclusion that attitudes to store brands are

influenced by the unique positioning of stores. Thus store choice has link

between store image and brand image and more recent theoretical constructs

relevant to store image are also briefly covered.

1.14 OBJECTIVES OF THE RESEARCH

The objectives developed to investigate the research problem are:

• To understand the socio-demographic profile of the customers.

• To examine the factors to be considered to select a retail outlet.

• To identify the consumer attitude towards the importance of

purchase parameters of store brands.

• To examine the consumer factors influence towards store brands in

retail outlets.

27

• To identify the impact of store image on overall satisfaction which

leads to store loyalty.

• To find out the relationship among store brand factors, satisfaction

and store loyalty.

The purpose of this study is to ascertain the linkages between store

brand perception and customer satisfaction towards store loyalty especially in

Madurai city. It explores the relationship between store brand factors and

consumer satisfaction with store brand loyalty and store image attributes, as

well as the relationship between consumer satisfaction and store loyalty. It

identifies the factors that contribute to select particular retail to increase the

number of brand loyal customer. This study is justified by considering its

significance. It also has the potential to contribute the knowledge about store

brands that leads to understanding the consumers and retailers need, to adopt

strategies for creating loyal customers. The review of literature reveals that

there are very few studies addressing the problems related to store brand,

store loyalty and satisfaction. This research work focuses on the assessment of

consumer factors on store brand purchase and consumer satisfaction leading

to store loyalty. It determines the factors influencing the success of store

brands in the market.

. 1.15 JUSTIFICATION OF THE RESEARCH

In many countries, store brands have become a common brand

choice for shoppers; an important strategy for retailers and a significant

concern to national brand manufacturers. Historically, store brands have been

as low-priced and low-quality products. In recent years, however companies

have started using store brands to market higher quality items and many

believe that high-quality store brands will increase in the present scenario.

This has been a significant increase of store brands worldwide. In Europe,

store brand goods account for about 45% of products sold in supermarkets

28

compared to 25% in the USA. Wal-Mart for instance, has a 40% store brand

representation in the stores. The survey shows that 50 % of Indian retail will

be occupied by store brands within the next 10 to 15 years. The business

media predicts rapid growth for store brands in the future, as the world’s

major grocery retailers intensify the store brand penetration as stated by

Ailawadi et al. (2008).

First, there is a need to conduct more research on store brands in

India compared to other countries. There has been a smaller number of store

brand products in the Indian organized retail market, although store brands in

this country are growing in a slowly. The experience of other countries

suggests that retail consolidation is the key driver of store brand growth.

Morris (2002) states that although Indian retailers are consolidating, they are

still in the early stages of developing successful store brand programmes.

Another motivation for this thesis is that, there is a need to conduct

more category-level studies in store brand purchase. An interesting

phenomenon of store brand success is that its growth has been highly uneven

across different product categories as suggested by Batra and Sinha (2000).

For example, in India store brands value share is 46% in the category of fresh

milk and cream, whilst only 8% in the biscuit range as explored by

AC Nielsen (2003). Inter-category differences have been used as the most

important sources of variation in store brands share across markets, retailers

and categories.

Retailers motivations and strategies for store brands have been

developed over the years. Retailers initially viewed store brands as means to

improve profitability, through higher retail margins and increased bargaining

power with national brand manufacturers (Steiner 2004). While store brands

are generally positioned below national brands in terms of price and quality,

from the mid 1970s retailers have started to view them as means to achieve

29

retailer differentiation and have begun to upgrade the quality. By the mid

1990s, store brands in the food sector had been growing faster than national

brands and had become a significant threat to national brand manufacturers as

stated by Herstein and Gamliel (2004). The same time Laaksonen and

Reynolds (2002) also narrated that retailers had begun to view store brands as

one of the most dynamic forces in food retailing especially in developed

markets characterized by stagnant growth and intense competition.

The growth of store brands is seen by industry as the most

important indicator, as grocery retailers have moved away from the role of

merchants to become marketers (PLMA 2006). Now-a-days, retailers

continue to view store brands as critically important, ranking them sixth out

of the top ten critical issues declared by Baltas and Argouslidis (2007).

Reflecting this changing focus, Semeijn et al. (2004) says that store brands are

now regarded as brands in their own right, with similar characteristics and

advantages to brands in general. This is included as a base for brand

extension. Store brands are becoming major brands in own right with

identities and quality images.

Despite the increasing interest in store brands by academics, some