an introduction to financial management and credit...

TRANSCRIPT

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

1Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Trainer’s IntroductionYour trainers are: _______________________________________

The South African Cities Network (SACN) was created in 2002, as a

programme to improve understanding of trends in urban development, under the joint auspices of the then Department of Provincial and Local Government (now Department of Cooperative Governance and Traditional Affairs (COGTA)), and the nine largest cities in South Africa

(Johannesburg, Ekurhuleni, Tshwane, eThekwini, uMsunduzi, Nelson Mandela Bay, Cape Town, Mangaung and Buffalo City). It operates in association with the South Africa Local Government Association (SALGA).The SACN has an established track record in generating information and knowledge to improve understanding of recent urban development trends inside and outside South Africa. Many specific knowledge-sharing products have been produced, notably the State of the Cities Report (2004, 2006, and 2010 (forthcoming); and thematic reports on poverty, infrastructure, environment, and finances (further details can be obtained at the web-site www.sacities.net).

Hunter van Ryneveld (Pty) Ltd are specialists in public finance and management. The partners have substantial public finance management experience in South Africa, other parts of Southern Africa, and in South Asia. The company seeks to contribute to the sound financing and management of built environment services through its work on city and provincial government finances; inter-governmental

fiscal relations; the financing of public transport services; public sector financial strategy and budgeting; city tax and revenue policy and administration; city expenditure administration and audit; sub-national cash and debt management; financial capacity and credit assessment; and financial management and credit improvement.

Afcap Consulting specialises in financial advisory and consulting services to both public and private sector clients and the financial institutional sector in Southern Africa and the rest of the continent, Focus areas include the origination, structuring and placement of debt and equity capital (including bonds); strategic corporate finance advisory services; credit assessments of sub-national entities, especially water utilities and municipalities; structuring of credit enhancement measures, and public-private partnerships. The founding directors of the

company collectively have over 30 years in the financial sector and especially in the raising of finance and grants from the Developmental Financial Institutional (DFI) community.

The Resolve Group is a collection of specialist consulting companies bound by a common vision and driven by common values. We have been making a difference since 1997 and are experts in people, performance and change.

Our diverse teams of professionals bring to bear a unique blend of knowledge, experience, imagination and cultural capital to solve problems and craft sustainable results. They are people who believe in the importance of people and know that extraordinary performance is a consequence of hard teamwork and total involvement.

We are a born and bred South African company. We are majority black-owned. We have built ourselves to last and are intensely proud of our people, our growth and what we’ve achieved for our clients.

Unless otherwise indicated, copyright of this material vests in SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group. No part of this material may be reproduced, modified or adapted in any

form or by any means without their written permission

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

2Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Section 1

Introduction

The purpose of this section is to:

Introduce the trainer and participants Advise you of housekeeping details Provide an overview of the module Identify your own learning objectives for the module

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

3Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Housekeeping

Notes

Starting times and ending times

Tea and lunch breaks

Toilets

Speaking rules and group work

Language

Use of cellular phones

Smoking

File and materials

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

4Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Module ObjectivesAs a result of this training, you will be able to:

Explain what credit worthiness is

Explain the relationship between good financial management, credit worthiness and a clean audit

Describe some common challenges currently facing local governments

Describe what good financial management is at a local government level

Describe the key dimensions of good financial management

Identify some ways of improving financial management

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

5Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Participant’s Introduction & Objectives

On your own consider what YOU would like to get out of this module and why it is important to you. Write your answer in the space provided below.

Name:

Position:

Objectives:

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

6Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

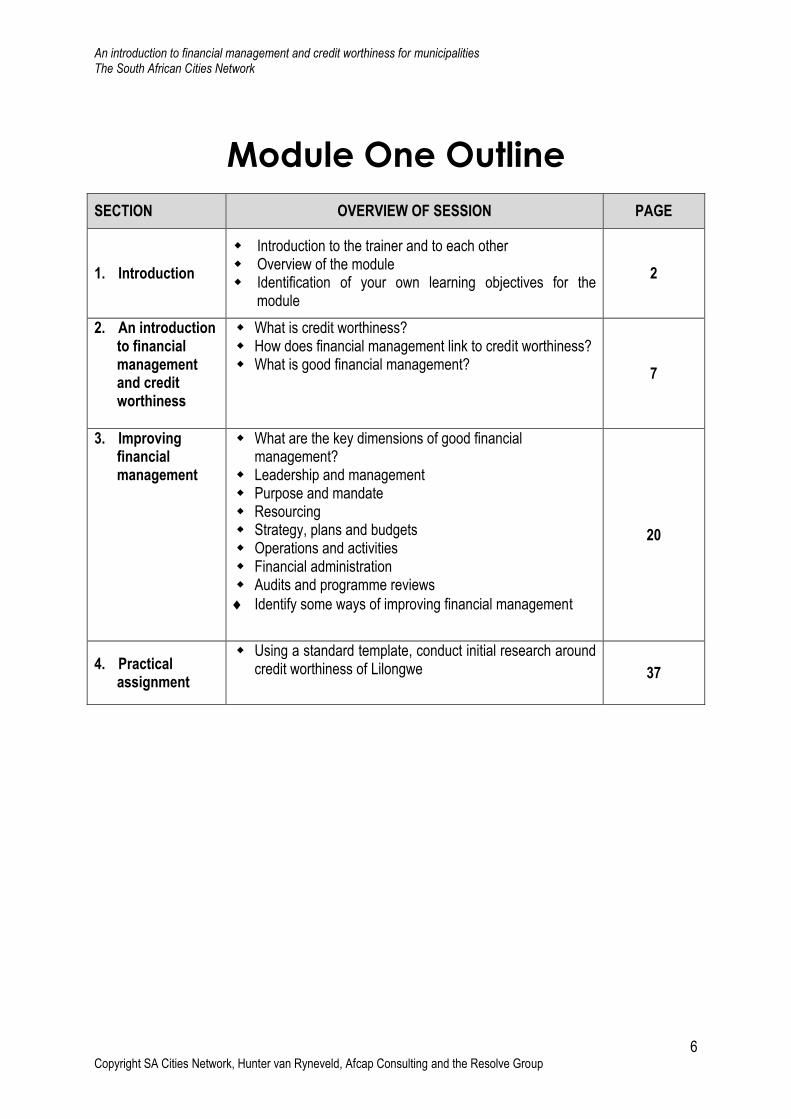

Module One OutlineSECTION OVERVIEW OF SESSION PAGE

1. Introduction

Introduction to the trainer and to each other Overview of the module Identification of your own learning objectives for the

module

2

2. An introduction to financial management and credit worthiness

What is credit worthiness? How does financial management link to credit worthiness? What is good financial management? 7

3. Improving financial management

What are the key dimensions of good financial management?

Leadership and management Purpose and mandate Resourcing Strategy, plans and budgets Operations and activities Financial administration Audits and programme reviews Identify some ways of improving financial management

20

4. Practical assignment

Using a standard template, conduct initial research around credit worthiness of Lilongwe 37

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

7Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Section 2

An Introduction to financial management and credit worthiness

At the end of this section you will be able to:

Explain what credit worthiness is Explain the relationship between good financial management, credit worthiness and a

clean audit

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

8Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Exploring credit worthiness and the link to good financial management

The following case studies describe different municipalities and illustrate various aspects of credit worthiness and good financial management. Read each case study and then record your responses to the questions that follow. Then discuss your responses with your neighbour.

1. EZULWINI TOWN BOARD, SWAZILAND (2004 – 2008)

Ezulwini, the ‘Valley of Heaven’, is Swaziland’s most prominent tourism node, and is located in the heart of the country. The valley houses several hotels of international standard, as well as a casino, a golf course, numerous restaurants, handicraft centres, a nature reserve, and the National Stadium. The Ezulwini Town Board (ETB), which was established in 1995, has a relatively large jurisdiction (1,719hectares, of which only approximately 1,120 hectares are ‘developable’), within which live approximately 6,000 people. There are only 445 households in formal areas.

The main service responsibilities of the ETB are the maintenance of roads and the collection and disposal of solid waste. The Swaziland Water Supply Corporation is responsible for water supply and sanitation, and the Swaziland Electricity Corporation for electricity distribution.

The Town Board consists of four persons, and the management team consists of the Town Clerk, the Town Treasurer, and the Inspector of Works. Key revenue and expenditure information for the Board between 2004 and 2008 is set out below.

EZULWINI TOWN BOARD 2004 2005 2006 2007 2008Revenue (Emalangeni)

Property tax - 1,756,878 1,794,896 3,606,266 1,959,301 Government subvention 500,000 450,000 950,000 950,000 950,000 Government capital grant - - - - 1,375,000 Interest income - - - - 360,913 Other 82,852 48,421 142,864 113,436 67,808 Total revenue 582,852 2,255,299 2,887,760 4,669,702 4,713,022

Expenditure (Emalangeni)Salaries and wages 54,972 185,018 276,885 315,421 371,932 Repairs and maintenance 2,754 254,035 40,617 63,691 74,094 Debt service costs - - - - - Other 442,205 588,911 701,511 628,419 967,126 Total expenditure 499,931 1,027,964 1,019,013 1,007,531 1,413,152

Surplus (Emalangeni) 82,921 1,227,335 1,868,747 3,662,171 3,299,870

The ETB has a historical pattern of operating surpluses arising from a relatively strong tax base and limited service operations. It has therefore been building up cash reserves because it was inadequately fulfilling its mandate to deliver services. The total accumulated surplus at the end of the 2007/8 financial year was E8.8 million excluding unspent capital grant funds. It is estimated that the opening cash balance at the start of the 2009/10 financial year was approximately E9.0 million.

Worksheet 1

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

9Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

The ETB has published audited financial statements since 2004. The auditors are an independent private firm, and have each year confirmed that ‘the financial statements fairly represent the financial position of the Board and the results of its operations’ at the end of each financial year. The municipality has therefore obtained a ‘clean’ audit for each year since 2004.

Global Credit Ratings (GCR), a credit rating agency, in October 2008 awarded the ETB a credit rating of BB+, which is one notch below investment grade. GCR describes ETB as having a strong net cash position, as well as having staff costs which are well contained when compared against income. But a non-investment grade rating is nevertheless given because of: a strong liquidity position as a result of low capital spending; a poor debtors collection profile; rising staff costs, despite being ‘well contained’; a ‘small and undiversified’ tax base

While the ETB is possibly over-dependent on the tourism industry, the other points can be disputed. Firstly, unspent capital grant funds account for only approximately E1.3 million of total cash balances of E9.0 million: and the balance consists of accumulated operational surpluses. Secondly, the debtors position (often government debtors) is admittedly poor, this does not imply weak future cashflows: on the contrary the ETB is well able to service debt (GCR agrees that capacity for timely repayment exists at the ETB). Thirdly, while staff costs are rising, this is a positive feature given the work that is required (GCR does acknowledge that staff costs are ‘well contained’ when compared to income); and finally, due recognition may not have been given to the strategic position and role of Ezulwini in the economy of Swaziland; and to the potential developments in Ezulwini which will expand the tax base.

? Questions?

1. In your view, did the ETB practice good financial management? Why do you say so?

2. In your view, is the ETB credit worthy? Why do you say so?

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

10Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

2. LAVUMISA TOWN BOARD, SWAZILAND (2006 - 2008)

The Lavumisa Town Board (LTB) is a tiny local authority in the south of Swaziland. It had a staff complement of five in 2007, and budgeted annual expenditure of just over E1.0 m in 2008. It provides refuse collection services (making use of a government tractor), maintains the roads and provides street lights. No property taxes are collected, and the municipality is chronically dependent upon central government grants. The municipality owns a Nissan TwinCab, and all the basic office infrastructure is in place.

The Town Clerk is a seconded part time official who is often away. The administrative heart of the municipality is the Accountant, who handles all financial and administrative arrangements for the municipality, including managing the three labourers (collect refuse today, fill potholes tomorrow). The financial statements are given a clean bill of health by an independent auditor each year.

The amount of the government grant is fixed but the timing is unreliable. Accordingly the municipality maintains a cash buffer of one-third to one-half of the annual budget. Nevertheless Lavumisa has been finishing each year with an operating deficit, and its position is increasingly precarious.

LAVUMISA TOWN BOARD 2006 2007 2008Revenues (Emalangeni)

Property tax 0 0 0Government subvention 565,000 565,000 565,000Government capital grant

0 0 425,000

Interest income 0 0 0Other 15,367 16,229 29,672Total revenue 580,229 581,229 1,019,672

Expenditure (Emalangeni)Salaries and wages 100,702 129,568 125,978Repairs and maintenance

146,628 49,544 61,753

Depreciation 30 115 23 377 15 747 Other 460 758 528 760 617 814 Total expenditure 738 203 731 249 821 292

Overall deficit (Emalangeni) -157,836 -150,020 198,320

Operating deficit -127,721 -126,643 -210,873Cash balance at year-end 386,626 222,222 387,163

This is a municipality which provides not much more than token (though necessary) services to its residents. There is no technical services manager, no planner, and no capacity to develop and implement a strategic plan to address service delivery deficiencies. There is anyway no tax base to support such a plan.

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

11Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

? Questions?

3. In your view, did Lavumisa practice good financial management? Why do you say so?

4. In your view, is Lavumisa credit worthy? Why do you say so?

3. CITY OF JOHANNESBURG, SOUTH AFRICA (1994 – 2004)

The City of Johannesburg provides comprehensive built-environment related services to some 3.5 million residents in its jurisdiction. Starting in 1993 from the eleven racially separated administrations which were its apartheid local government legacy, the current organizational and service delivery arrangements of the City were created in a transition process which lasted nearly a decade. There were two administrative transitions: firstly, to an interim arrangement (a two-tier government structure involving five authorities), which applied between 1995 and 2000, and then to final single-city governance structure, characterised by 11 single-function city-wide municipal entities, and a core administration arranged into 11 regions. The total staff complement of the city declined during this period from around 28,000, to below 25,000, before increasing slowly again.

By 2002 the City had successfully completed its long process of administrative transformation. It had also recovered from its financial crisis of five years previously, and its financial indicators were improving each year. But a consequence of the long drawn-out processes of substantial administrative change (coupled with financial crisis, declining staff numbers, and the loss of institutional memory and specific technical skill categories), was that financial accounting, control and reporting procedures either deteriorated, or did not improve from the inadequate legacy standards. The financial statements of the various components of the City of Johannesburg, as well as those for the City as a whole, were ‘disclaimed’ for more than a decade. It took a sustained and co-ordinated effort over five years, by all the different components of the City, before the Auditor General was prepared to grant that the 2007 financial statements of City truly reflected its real financial position.

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

12Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

City of Johannesburg (Rm) 2003 2004 2005 2006 2007 2008Revenues

Property rates 2 212 2 417 2 684 2 919 3 094 3 326RSC levies 1 261 1 322 1 551 1 937 0 0Electricity charges 2 490 2 852 3 256 3 382 3 810 4 133Water & sanitation charges 2 037 2 353 2 615 2 835 3 221 3 317Other service charges 639 526 404 383 377 540Interest earned 153 368 410 557 664 728Government grants and subsidies

217 566 1 050 1 295 3 138 4 446

Fines, public contributions, other

323 920 1 536 1 744 1 581 1 470

TOTAL 9 333 11 322 13 506 15 052 15 884 17 960Expenditures

Employee related costs 2 631 3 133 3 058 3 505 3 889 4 319Remuneration of Councilors 39 43 45 50 58 62Bad debts 862 691 980 855 638 739Depreciation 350 791 872 629 881 806Repairs and maintenance 150 152 206 240 257 399Interest 639 522 671 787 837 971Bulk purchases 2 656 3 117 3 243 3 517 3 956 4 324Other 2 471 2 627 2 973 3 797 4 028 5 622Total 9 798 11 076 12 048 13 379 14 545 17 243

Overall surplus(deficit) -465 246 1 458 1 673 1 339 716

Another consequence of the deterioration of systems and procedures associated with the major administrative changes was ‘billing crisis’. The number of unresolved billing queries has been increasing steadily for several years, but by May 2004, there were sufficient unresolved errors to cause as many as 8% of the city’s customers to raise account queries in that one month. Although this problem was brought under control over the following year, it again reflected inadequate financial management in the sphere of city revenue.

Despite these aspects of the financial management of the City evidently being inadequate, however, other dimensions were considerably stronger. The city did have strong strategic and budgeting capabilities, and had spent the previous few years developing a reliable medium-term budget framework to match its integrated development plan. The city also had a clear capital development programme, and urgently needed to sustain a higher level of capital expenditure than previously achieved. The City had also developed a new treasury capacity.

Furthermore, the city was creditworthy throughout this period. It had obtained its first credit rating in 2000, in the depths of its financial crisis, and the rating had been BBB+ (i.e. only just investment grade). Johannesburg commissions annual credit ratings by two separate rating agencies as a matter of course. It was 2003 before there was any improvement in the rating (to A-), and another three years before the rating improved again (to A in 2006).

Although the City had previously obtained bank loans for infrastructure funding, it took a further step in 2004 when it issued two R1 billion bonds to domestic investors. The successful raising of private

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

13Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

finance for infrastructure development was possible because of the inherent credit-worthiness of the city, despite its financial management deficiencies (poor audits, billing crisis).

But the City did pay a price for these deficiencies. Although the capital finance was successfully raised, the price of the borrowed money (i.e. the interest rate) was certainly higher it would have been had the city had better financial management.

? Questions?

5. In your view, did Johannesburg practice good financial management? Why do you say so?

6. In your view, was Johannesburg credit worthy in 2004? Why do you say so?

4. WELKOM, SOUTH AFRICA (1994 - 1996)

Gold was discovered in 1938 and Welkom was proclaimed a town in 1948 and a municipality in 1961 with city status being granted in 1961. The current municipal area is 5000 sq km and the current population is approximately 400000. The bulk of the initial infrastructure was planned and funded by the mining companies (Anglo American) and even today the traffic is so well planned that Welkom has no traffic lights. Welkom entered the 1990s with excellent infrastructure and a healthy economy underpinned by the gold mining industry which attracted a substantial amount of employment seekers. The municipality, today called Mathjabeng is responsible for all municipal services including trade services like water and sewage, electricity, refuse removal as well as social services like community halls, parks cemeteries etc.

In the years preceding 1994 the town had borrowed approximately R182 Million from various pension funds and had no problems services these loans. However the first problems should have been visible even in the good times as the maturity concentration of the loans mostly of a bullet nature was not well structured with close to 65% maturing in two consecutive years (normally 10 to 15% would be regarded as an absolute maximum if no ring fenced sinking fund is has been funded by cash).

A number of events occurred that made Welkom default on all its loans in 1996:

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

14Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

The new municipal political leadership, eager to deliver the fruits of democracy used all the built up reserves in the sinking funds to provide unaffordable services (irresponsible financial policy).

They were deliberately given a more rosy picture of the town’s financial position by the white financial manager who after 1994 had to report to a new but incompetent black financial director, which he resented and the new financial director did not have the skills or experience to realise that he was being “bullshitted”. The motive apparently was to show up the new director and in so doing regain the top dog position. This resulted in the political council not realising the seriousness of their situation before defaults and possession of municipal assets started. He was partially supported by some of the old councillors attempting to gain political advantage.

In addition the financial manger, albeit in difficult circumstances of conflict and loss of control and discipline, could not control operational expenses. As an example in a six month period R250 000 was paid to the fire department in overtime (for ten people) despite the fact that there was not a single fire incident recorded!

The gold price went through a serious slump, resulting in mine closures and also consequential business closures. This led to large scale layoffs (it is estimated that more than 25 000 mine workers were retrenched and became unemployed with no means to sustain themselves) and this lead to further business closure and erosion of the tax base.

The council, not realising the serious impact on the town, thought that not raising tariffs for three years would ease the hardship of the residents.

In summary the combined effect of the erosion of the tax base, the non cost recovery tax base and the maturity concentration and the unawareness of the political leadership of the deteriorating circumstances unavoidably led to a default on external loans and a general inability to meet obligations.

This combination of bad and irresponsible management and the collapse of the economic base moved resulted in Welkom moving from a creditworthy entity to a defaulting entity in less than a year and serves as a example of how quickly bad management can erode creditworthiness.

Corrective action The lenders got together and with the support of the Free State MEC for local government effectively suspended the Council, appointed a small committee under the Mayor’s chairmanship, dismissed both the financial manager and the director finance and appointed one of the lenders (Inca) as financial manager reporting directly to the Committee.

The financial manager appointed by the lenders took relatively drastic action: A programme of phasing in tariff increases was adopted with special sanction of the MEC The creditors financial manger had to authorise all expenditure by the municipality Fraud charges were laid in all cases where investigations showed misuse of Council Funds

(including the fire Department) In negotiations with the creditors all debt was rescheduled to stagger the maturities and a

period of capitalisation was agreed A small short term bridging loan was provided by one of the creditors to fund the municipality

during the adjustment period

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

15Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

All expenditure was reassessed by the external financial manger while training a new financial director

All capital expenditure was suspended The outcome of these drastic measures was that partial loan repayment recommenced after approximately 10 months and the creditor’s manager withdrawn. After two years normal capital expenditure was resumed although it was impossible to obtain new loans from the private sector illustrating that sound financial management does not necessarily lead to creditworthiness.

? Questions?

7. In your view, prior to these drastic measures, did Welkom practice good financial management? Why do you say so?

8. In your view, prior to these drastic measures, was Welkom credit worthy? Why do you say so?

9. Based on these case studies and your own experience, what is credit worthiness?

10. Based on these case studies, what is the relationship between good financial managementand credit worthiness, if there is one? Why do you say so?

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

16Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Responses to the case studies

The case of the Ezulwini Town Board (ETB)

1. ETB did practice good financial management because: Expenditure did not exceed revenue, It had a strong net cash position, Staff costs were contained and The municipality was given a “clean audit” for many years in a row.

However, it could be criticized for being too conservative by not delivering as full a level of service and building up cash reserves.

2. Although ETB was not deemed credit worthy by a global agency, it is likely that it would be able to raise loans locally and in that sense it is credit worthy.

The case of the Lavumisa Town Board (LTB)

3. The LTB did practice good financial management in that: the auditor was satisfied with the way the books were keptHowever, leadership appears to be absent and there is no capacity for strategic budgeting.

4. LTB is not credit worthy because it has no stable, independent revenue base (i.e. it is totally dependent on government grants which are unpredictably-timed) and it starts each year on an operating deficit.

The case of Johannesburg

5. Johannesburg at that time did not practice good financial management because: It received disclaimed audits Its financial accounting, control and reporting procedures were weak, and It had a billing crisis.

6. Notwithstanding this poor financial management, Johannesburg was deemed credit worthy during this time although the cost of credit was increased as a result of the poor financial management. It was probably deemed credit worthy because of its size and strategic importance in the country (and continent’s) economy, and its large tax base and there was by then an established pattern of financial management improvement. Johannesburg was “too big to fail.”.

The case of Welkom

7. Welkom at that time did not practice good financial management in that: It had not scheduled its loan maturity dates carefully so most of them matured simultaneously,

placing enormous pressure on the municipal fiscus. Reserves were used up providing new unaffordable services. The municipal management team was divided and operating on political agendas to the

detriment of the municipality. This included providing inaccurate information to the politicians with an oversight role.

Handout 1

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

17Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Operational expenses were not controlled. When the tax base was eroded by circumstances beyond the municipality’s control, it

nevertheless chose not to increase tariffs for three years in a row.

8. Welkom was not credit worthy for all of these reasons.

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

18Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Credit worthiness and good financial management

9. Credit worthiness means what it says: worthy of receiving credit. Essentially it is an opinion by third parties, mainly lenders, on whether debt service payments will be made fully and on time. A lender which has confidence in the long-term financial strength of the borrower, and in the ability and willingness of the municipality to pay its obligations in full and on time, will regard that municipality as creditworthy.

Clearly not all institutions or municipalities are equally creditworthy. Lenders and investors therefore need a way of assessing how risky their loan might be, and a simple scale has been developed to indicate the relative creditworthiness of potential borrowers in the form of a symbol. These symbols are credit ratings, and they are assigned to potential borrowers by independent credit rating agencies. A credit rating is a formal opinion by an independent specialised agency (the credit rating agency) on the long term ability, capacity and willingness to repay commercial debt at the specified times.

Credit ratings are widely used in the financial and banking sectors as an independent view of the creditworthiness or risk associated with the institutions being rated. They have also become important as a continuous monitoring mechanism, and as a tool for institutional investors who seek to balance their portfolios with appropriate amounts of financial assets in different risk classes.

While different credit rating agencies use different symbols, the basic concept is identical across all agencies, in that the symbol reflects the probability of default by the rated entity.

Experience has shown that there is a close relationship between credit ratings assigned, the probability of default and the loss severity; and also between the credit ratings assigned and the cost of borrowing. For example, the actual rate of default on loans taken by borrowers rated BBB+ may be around 6%, compared to less than 1% for borrower rated AAA. Accordingly, BBB+ borrowers can pay up to 200 basis points (i.e. 2%) more for an equivalent loan than a borrower rated AAA. The higher interest rate charged reflects the relatively higher risk of default associated with the BBB+ borrower.

Credit worthiness therefore matters most of all because investment grade municipalities are able to obtain commercial loans at a better rate than their sub-investment grade peers.

Handout 2

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

19Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

10. The relationship between good financial management and credit worthiness

Usually good financial management is a pre-requisite (but not a guarantee), of credit worthiness. In other words, if a municipality has good financial management, it is more likely to be deemed credit worthy, than a municipality which does not have good financial management. However, this is not always the case, as the case studies illustrate:

Good financial management

Credit worthiness

Implications

Ezulwini Town Board

Good financial management and favourable structural factors (i.e. strong tax base), rendered this municipality credit worthy to domestic investors.

Lavumisa Town Board

X Despite having good financial management in a basic sense, the “structural” challenges faced by this municipality (i.e. its lack of independent tax base and complete reliance on government’s unpredictably-timed grants), rendered it un-creditworthy.

Johannesburg

X Despite having poor financial management at the time, Johannesburg was nevertheless deemed credit worthy probably because of its size and strategic importance in the country (and continent’s) economy, and its large tax base.

Welkom X X Bad financial management can destroy credit worthiness in a very short space of time.

Standards should be appropriate to the level of affordability of those receiving the services.

Although sound financial management can be reinstituted in a relatively short period (if the political will is present), re-establishing credit-worthiness will take a long time to re-establish.

Financial management should have the necessary checks and balance to ensure that decision makers have the right information.

If there are problems the willingness to act on them and play open cards with the private sector to jointly address problems and financial distress is important. The private sector would rather restructure than write off but once a default has occurred it reflects as such in their portfolios.

One conclusion to reach from this is that good financial management is a worthy goal in and of itself. It may, or may not lead to credit worthiness as there may be external/structural factors beyond the control of the municipality, which affect credit worthiness. Good financial management however, remains largely within the control of the municipality.

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

20Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Section 3

Improving financial management

At the end of this section you will be able to:

Describe some common challenges currently facing local governments Describe what good financial management is at a local government level Describe the key dimensions of good financial management Identify some ways of improving financial management

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

21Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Identifying good financial management

Read the following extracts and then record your responses to the questions that follow. Then discuss your responses with your neighbour.

“Urban public authorities in developing countries have come under increasing financial pressures during the last decade. They now face a rapidly growing demand for urban services as a result of continuing rapid urban population growth; however, their capacity to supply urban services as well as to undertake the necessary infrastructure development, is severely constrained by a shortage of fiscal resources. This situation is a result of a combination of factors – including reductions in intergovernmental transfers, increased cost of debt servicing as well as the cost of borrowing due to higher interest rates, and higher unit costs of providing services – which have restricted revenue growth. To compound the problem, many cities not only have a massive backlog of new infrastructure requirements but also need to allocate substantially more resources to maintenance, renovation, and replacement of older, deteriorating equipment.

In this environment, urban government agencies can respond to fiscal stress by employing three broad strategies:

- First, they can seek to raise additional revenue through a variety of means such as increasing their user fees and charges, raising local taxes, introducing new taxes and charges, and selling off assets such as unused land.

- Second, they can seek to improve their efficiency and effectiveness of their operations through productivity improvement programs, more efficient programming, planning and budgeting; cutting back some programs; using low-cost approaches; or achieving cost savings through the use of private contractors.

- Third, they can reduce the scope of their activities by greater use of private participation in the provision of urban services under self-help activity systems and through mobilization of nongovernmental resources. Further, in situations where urban authorities are providing purely private goods such as car parking facilities and recreation facilities, they could withdraw and allow the private sector to finance such facilities.”

- From “Urban Financial Management A Training Manual” by James McMaster, published by the Economic Development Institute of the World Bank

“Cities are the engines that drive national economic growth. By clustering complementary economic activities, intellectual and financial capital, and entrepreneurial energy, they raise labour productivity and create the potential for sustainable growth through urbanization as low-productivity rural labourers move to the cities. The backbone of a well-functioning city is its urban infrastructure - the network of roads, distribution of electricity, water supply and waste removal – which allows residents and firms to work productively under high-density conditions….

…large sums will be required in all countries to invest adequately in urban infrastructure and to operate and maintain systems once they are built…what are needed are reliable revenue streams that can be dedicated to infrastructure support….

More than a revenue challenge alone, urban infrastructure is a challenge in terms of infrastructure is a

Worksheet 2

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

22Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

challenge in terms of institutional arrangements and management authorities….Accountability for results is perhaps the most essential element in an intergovernmental framework….

If institutional arrangements are clear, with transparent rules for accountabilities, and authorities are fiscally responsible, capital markets will provide adequate resources for overcoming the infrastructure deficit of the urban economy.”

- From pages 18-20 “Financing Cities” edited by George E Peterson and Patricia Clarke Annez and published by the World Bank

? Questions?

1. In your view, what are some common challenges facing local governments today?

2. Based on the extract, list three strategies local government could employ to cope with fiscal stress

3. In your view, what are the key dimensions of good financial management at local government level?

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

23Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Challenges and good financial management

Some common challenges facing local governments today: Rapidly growing demand for urban services due to rapid urban growth Shortage of fiscal resources due to reductions in intergovernmental transfers, increased cost of

debt servicing as well as the cost of borrowing due to higher interest rates, and higher unit costs of providing services

Massive backlog of new infrastructure requirements Need to allocate substantially more resources to maintenance, renovation, and replacement of

older, deteriorating equipment Challenges relating to institutional arrangements Challenges relating to management authority Challenges relating to accountability

Three strategies local government could employ to cope with fiscal stress: Raise additional revenue Improve efficiency and effectiveness of operations Reduce the scope of activities

Key dimensions of good financial management at local government level:

1 Purpose and mandate

The local government and other agencies operating within its jurisdiction: have clear and un-conflicted purposes and mandates, expressed

in law (effective city management requires integrated city-wide governance of at least the built environment-related functions).

share priorities on municipal built-environment services (priorities, trade-offs and ultimately service delivery strategies are aligned around city-specific built-environment requirements.

2 Leadership and management

The political and administrative leadership of the municipality: work together as a team (across functions and across the political-

administrative divide) work to a plan (they have vision & mission; and strategies & plans,

see below) make decisions based on information (they use a management

information system) have energy and insistence that financial and service delivery

targets will in fact be improved work to strengthen public service work culture & ethics (honesty,

transparency, measured effectiveness, accountability for performance, common goal-orientation, good-faith supportiveness and trust, etc) among senior and middle management and more generally

Handout 3

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

24Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

3 Resourcing The municipality has adequate revenue potential It has legal revenue sources (own sources and reliable inter-

governmental grants) commensurate with its expenditure responsibilities, both operating & capital

The municipality shows good revenue effort and achievement billing is complete and accurate (all those who should be billed

(invoiced) for taxes and service charges, are accurately billed (invoiced)

there are easy means of payment, visible campaigns to pay, incentives to pay early, effective credit control policies for those who do not pay, etc. so that collection rates are high (amounts billed are collected)

there is a carefully-managed programme to restructure tariffs (to better reflect actual consumption and costs, at least on a city-wide basis); and taxes (for greater equity), with due consideration for affordability and safety nets for the poor.

4 Strategy, plans & budgets

The municipal leadership understands and has quantified its service responsibilities, and

has developed an approach to fulfilling those responsibilities has clear, and well-conceived strategies from which multi-year

plans and budgets can be derived has developed an affordable plan with realistic service delivery

targets has developed medium-term plans & budgets to give effect to the

strategy5 Operations

and activities

The municipality has managers and professional, technical & other staff who: are adequately skilled have the equipment they require are performance-managed.

The municipality’s organizational structure facilitates effectivemanagement accountability, appropriate delegations, and teamwork

The municipality monitors and measures service delivery and asset maintenance during the year

Municipal expenditure is effective, efficient and economical6 Financial

administration

Financial accounting The structure of the accounting system parallels the organizational

structure (so that line managers can be held financially accountable).

Line managers receive written financial and operational delegations

Financial transactions are correctly authorized according to regulations, and are correctly recorded.

Financial controls should be effective without unduly inhibiting operations

There are effective systems for payments to suppliers and to staff

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

25Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Cash and treasury management Municipal bank accounts are managed so that they are not unduly

in deficit Any borrowing is managed to minimise long term Interest and

banking costs Procurement and asset management

Procurement procedures are fast, effective and clean (ie they quickly result in the best purchase decision)

Assets such as roads, municipal buildings, pipes, vehicles etc are maintained according to a regular schedule base, to minimize costs and ensure full value.

Financial reporting There is an in-year financial reporting regime involving quarterly,

monthly, weekly and daily financial management reports on different aspects of financial management

Financial management reports are read, discussed among top managers, and acted upon

Year-end financial statements are produced rapidly7 Audits and

programme reviews

There is Independent auditing of the annual financial statements and annual reports, within statutory time limits

Financial and service delivery outcomes are evaluated each year, and steps taken to improve performance

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

26Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

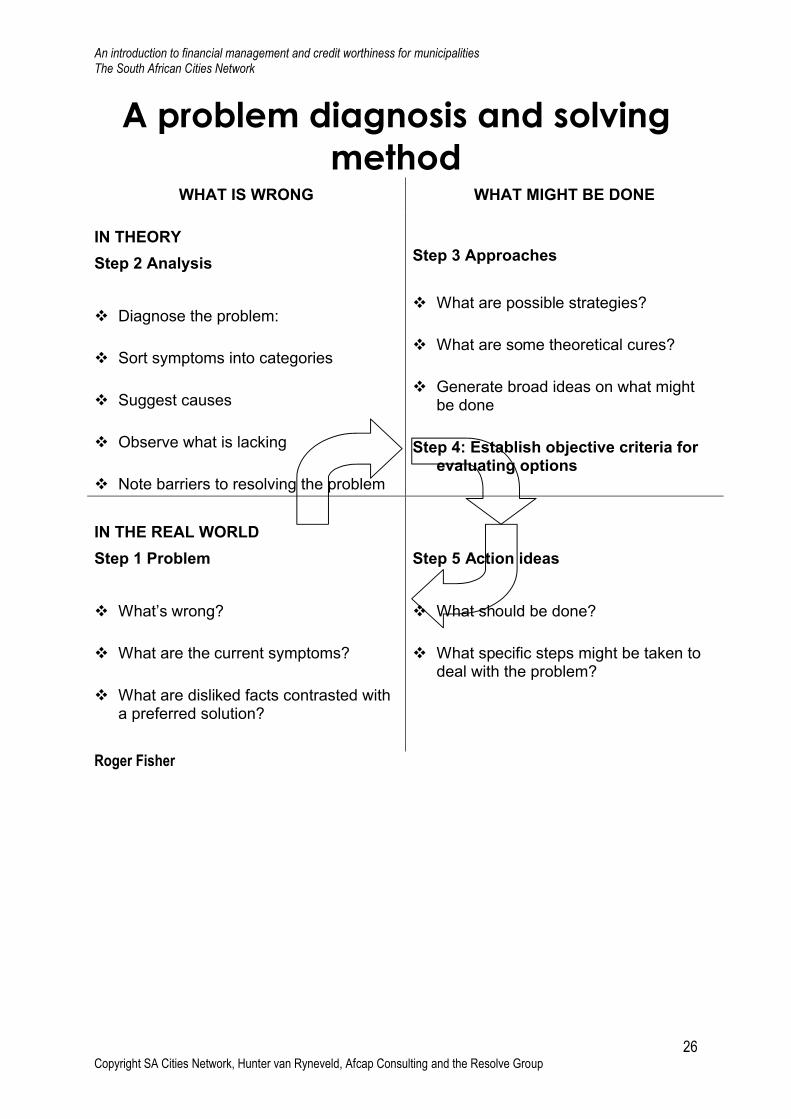

A problem diagnosis and solving method

WHAT IS WRONG WHAT MIGHT BE DONE

IN THEORY

Step 2 Analysis

Diagnose the problem:

Sort symptoms into categories

Suggest causes

Observe what is lacking

Note barriers to resolving the problem

Step 3 Approaches

What are possible strategies?

What are some theoretical cures?

Generate broad ideas on what might be done

Step 4: Establish objective criteria for evaluating options

IN THE REAL WORLD

Step 1 Problem

What’s wrong?

What are the current symptoms?

What are disliked facts contrasted with a preferred solution?

Step 5 Action ideas

What should be done?

What specific steps might be taken to deal with the problem?

Roger Fisher

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

27Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Financial management improvement plans

The cards given to you by the facilitator describe different municipalities in need of improvement in their financial management. Each card explores a different aspect of financial management that is in need of improvement. In pairs, read the front of the card and with your partner discuss your responses to the questions on the card. Then turn the card over and compare your answer with the answers on the back. Resist the temptation to turn the card over until you have discussed your responses to the question on the front of the card! Then move on to the next card until you have completed the pack.

Worksheet 3

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

28Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Ways of improving financial managementChallenge Suggested responses

1.A municipality that has no legal mandate to provide water services knows that the key service priority for its city is water and sanitation infrastructure. Furthermore a large property development, likely to yield substantial new property tax income, will take place only if the investor is guaranteed security of water services. The bulk infrastructure required for the property development could also become the backbone of new water services to many households in an entire section of the city.

Meanwhile the national water services utility, which does have the legal mandate to supply water services in the city jurisdiction, is currently over-borrowed due to water infrastructure investments in other parts of the country. Although the planned property development does offer the prospect of higher water sales, this would not on its own justify the investment by the water utility in the new infrastructure required.

The water utility therefore declines to provide the guarantee the investor is seeking, and the municipality has no legal power to do so. The property development does not proceed, no new property tax revenues are paid to the municipality and no new water services infrastructure is installed.

Which dimension of the city’s financial management does this problem relate to?What are the possible causes of the problem?What are possible solutions to the problem?

This problem relates to the purpose and mandate dimension of thecity’s financial management.

Possible causes are: The way that legal mandates are assigned is inappropriate Different agencies have different priorities There are no effective ways of co-ordinating activities and priorities The water infrastructure investment is not financially feasible Failure of the municipality to recognise that decisions of the

national water utility are based on national priorities

Possible solutions are: Seek to change legal mandates so that cities are responsible for all

built-environment services Establish city-wide strategic co-ordination mechanisms Establish special vehicles to combines revenue streams in the The municipality must stop dreaming and keep to its legal mandate

Handout 4

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

29Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

2. The municipality is planning a project to re-house an informal settlement, and Councillors expect high standards of housing and services, saying that this what the people require. Managers point out that more households could be re-housed if lower standards were accepted. The finance director is concerned that as the households concerned are poor, very little of the cost of the development will be recovered, and furthermore Council will incur substantial long-term costs delivering services that will not be paid for, but the technical services director wants to avoid the lowest standards because they imply higher operational and maintenance costs.

Which dimension of the city’s financial management does this problem relate to?What are the possible causes of the problem?What are possible solutions to the problem?

This problem relates to the leadership and management dimension of the city’s financial management.

Possible causes: Politicians do not understand the implications of their public

promises Managers do not understand the pressures facing politicians Political office bearers and managers do not share a vision and

mission for the city There is no agreed city strategy

Possible solutions: Leadership must lead! Build good political and management leadership teams Develop city vision and mission Develop realistic service delivery strategies

3. The current revenues collected are hopelessly inadequate to cater for planned expenditure.

Which dimension of the city’s financial management does this problem relate to?What are the possible causes of the problem?What are possible solutions to the problem?

This problem relates to the resourcing dimension of the city’s financial management.

Possible causes: Tariffs are too low Collection is inefficient Not all potential income sources are exploited Service standards are too high Planned expenditure is too high

Possible solutions: Increase tariffs Improve collection Develop new sources of income

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

30Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Reduce expenditure Reduce service standards Combination of above

4. In-fighting between the City’s Financial Director and the City’s Planning Director has led to them refusing to share information with each other and only communicating by e-mail.

Which dimension of the city’s financial management does this problem relate to?What are the possible causes of the problem?What are possible solutions to the problem?

This problem relates to the leadership and management dimension of the city’s financial management.

Possible causes: The managers do not share any common goals The managers do not trust each other There is no shared and common source of key management

information

Possible solutions: CEO to discipline both managers Engage in team building exercises Establish a management information system (MIS) to share

management information

5. The city roads department complains that the national water utility, the national electricity utility and national telecommunications utility are always digging up the city’s streets, and failing to adequately restored them to their original condition as the law requires. The roads department must then repair the roads at its own cost. But as soon as it has done this, another utility digs up the road again.

Which dimension of the city’s financial management does this problem relate to?What are the possible causes of the problem?What are possible solutions to the problem?

This problem relates to the purpose and mandate dimension of the city’s financial management.

Possible causes: National utilities are able to ignore legitimate municipal demands No common planning among agencies operating in the city No operational co-ordination among agencies operating in the city. City roads department fails to recognise that national utilities take

priority

Possible solutions: Build better relations among agency heads

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

31Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Establish a joint planning process among agency technical heads Establish a joint operations committee for operational co-ordination

6. Everyone knows that many businesses and households evading charges, apparently without consequences, so even fewer are willing to pay, why should I pay when my neighbour does not? Very low collections are stifling service delivery, and poor service delivery is again used to justify non-payment.

Which dimension of the city’s financial management does this problem relate to?What are the possible causes of the problem?What are possible solutions to the problem?

This problem relates to the resourcing dimension of the city’s financial management.

Possible causes: Administrative systems are weak and can be corrupted Credit policies are not applied evenly or fairly

Possible solutions: Manage overall step-change in revenue effort & achievement Comprehensive, target-driven, medium-term, politically & socially

sophisticated Easy means of payment, effective credit control, visible campaigns

and incentives to pay early, etc. Also visibly improve services!

7. The City Engineer is ambitious about service delivery, and overspends his budget three years in a row, arguing that the people need services; the roads, vehicles and equipment need to be maintained; and the role of the City Treasurer is to obtain the necessary funds. By the third year the City Treasurer is frantic, as she can see no way of raising income or limiting expenditure and the bank manager is complaining that City has exceeded its overdraft limit. She insists that the City Engineer curtail or at least delay his spending.

Which dimension of the city’s financial management does this problem relate to?What are the possible causes of the problem?What are possible solutions to the problem?

This problem relates to the strategy, plans and budgets dimension of the city’s financial management.

Possible causes: There is no agreed city strategy, plan and budget The managers do not share responsibilities for financial health and

service delivery Authority to spend is not matched by accountability for expenditure

incurred Financial controls are inadequate

Possible solutions: Build budget & planning capacity

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

32Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Develop realistic service delivery strategies & targets, with budgets that support them

Structure the accounting system to parallel the organizational structure, so that line managers can be held financially accountable.

Line managers should receive written financial and operationaldelegations

Enforce financial management discipline

8. A municipality seeks to substantially upgrade its services and so establishes a new technical services department, appoints an engineer to head it, and requires the director to establish the capacity needed to deliver the planned capital infrastructure. In the meantime the finance director obtains loan finance for the planned capital programme.

But as time passes many problems emerge. Staff are appointed for reasons other than their capacity to deliver the services required. The work programme fails to excite the department, which does not develop a sense of urgency. The programme runs slowly, and the finance director finds that loan funds that have been drawn down are being spent slowly, implying unnecessary interest costs incurred.

Which dimension of the city’s financial management does this problem relate to?What are the possible causes of the problem?What are possible solutions to the problem?

This problem relates to the operations and activities dimension of the city’s financial management.

Possible causes: Staff skills and capacity was inadequate Staff was not performance managed There were no consequences for the technical services director for

failing to deliver on time The finance director drew down the loan finance too early Departments were working in silos and not co-operating This should have been a city-wide project, and not just left to the

technical services department

Possible solutions: Managers and professional, technical & other staff should be

adequately skilled and equipped, and should be performance-managed.

Organizational structure should be facilitate effective management accountability and teamwork

In-year measurement and monitoring of service delivery, asset

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

33Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

maintenance Build on strengths, take action on deficiencies

9. To ensure tight control of spending, the municipal manager allows only two officials to authorise financial transactions of over a given figure.

The municipality was servicing a loan and every three months the finance department accountant prepared an authority to make the payment, to be signed by the two signatories.

On one occasion, one of the signatories had taken leave, the documents requiring his signature piled up in his office. His signature was finally obtained just before the date on which the payment was required. By then the other signatory had been called away to the capital to consult the national Department.

The debt service payment was not made on time, so the municipality had defaulted on the loan. In terms of the loan agreement a 2% penalty clause was then applied, so the municipality ended up incurring unnecessary and wasteful expenditure.

Which dimension of the city’s financial management does this problem relate to?What are the possible causes of the problem?What are possible solutions to the problem?

This problem relates to the financial administration dimension of the city’s financial management.

Possible causes: Managers and the Finance department failed to plan ahead There are too few signatories, so the financial controls are inhibiting

effective municipal administration

Possible solutions: Managers must take steps to ensure that their responsibilities are

covered when they are away Establish more signatories and or alternate signatories Financial controls should be effective without unduly inhibiting

operations

10. A municipality produces a glossy budget document at the start of each year, but it is very difficult for anyone outside of the finance department to understand. Financial statements are produced up to a year after financial year end, and seem to bear no relation to the original budget

Opposition politicians in the media claim that the financial statements of

This problem relates to the audits and programme reviewsdimension of the city’s financial management.

Possible causes: Inadequate financial management capacity No project management of year-end closure procedures

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

34Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

the municipality lack credibility, and that public resources are being wasted or being used corruptly. Bankers are similarly concerned and demand to see credible financial information.

Which dimension of the city’s financial management does this problem relate to?What are the possible causes of the problem?What are possible solutions to the problem?

No independent auditor

Possible solutions: Appoint an independent auditor Establish and enforce an annual reporting and auditing cycle Establish periodic reviews of performance and outcomes Take steps to address any deficiencies in resourcing or strategy, to

improve performance and to reduce risk.

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

35Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Financial Management Improvement Plans

Municipalities seeking to improve their financial management performance will need to implement a financial management improvement plan (FMIP). This should clearly be designed to be appropriate for the particular circumstances, characteristics and capabilities of that municipality. However in general terms municipalities will need to take actions and initiate programmes in the six dimensions indicated above. Less creditworthy municipalities will need more comprehensive FMIPs than those which have achieved a higher credit rating.

The more comprehensive the FMIP required, the more important it becomes to programme-manage it effectively, and with an appropriate change management strategy. A comprehensive FMIP in fact amounts to comprehensive organizational renewal, and therefore absolutely requires the correct management, leadership and political backing.

In cases where a less comprehensive or more targeted FMIP is required, it should be possible to incorporate the FMIP into existing improvement programmes without necessarily needing to address deficiencies across all fronts at once.

In some cases FMIPs may also need to include efforts to strengthen public service work culture and ethics (such as honesty, transparency, measured effectiveness, accountability for performance, common goal-orientation, good-faith supportiveness and trust, etc) among senior and middle management, as well as more generally. Leadership energy and insistence that the financial targets and service delivery will in fact be improved can have the effect of sharpening performance and of testing boundaries previously deemed out of bounds.

Component Municipal actions to improve deficiencies1 Leadership and

teamwork Political and functional agendas should be aligned Goals should be agreed and be transparent

2 Purpose and mandate

Seek establishment of city-wide strategic co-ordination mechanisms Seek to clarify boundaries and responsibilities

3 Resourcing Manage overall step-change in revenue effort and achievement Comprehensive, target-driven, medium-term, and politically/socially

sophisticated programme to ensure full tax coverage and billing and collection of revenues due.

Easy means of payment, visible campaigns to pay, incentives to pay early, effective credit control, etc.

In due course, carefully-managed programme to restructure tariffs (to better reflect actual consumption and costs); and taxes (for greater equity), with due consideration for affordability and safety nets for the poor.

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

36Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Component Municipal actions to improve deficiencies4 Strategy, plans &

budgets Ensure correct leadership and top management Develop realistic service delivery strategies Establish CFO as a strategic financial management position Build budget & planning capacity Develop medium-term plans & budgets to give effect to the strategy

5 Operations and activities

Managers and professional, technical & other staff should be adequately skilled and equipped, and should be performance-managed.

Organizational structure should be facilitate effective management accountability and teamwork

In-year measurement and monitoring of service delivery, asset maintenance,

Build on strengths, take action on deficiencies6 Financial

administration Structure of the accounting system should parallel the organizational

structure, so that line managers can be held financially accountable. Line managers should receive written financial and operational

delegations Effective systems for payments to suppliers and staff Financial controls should be effective without unduly inhibiting

operations Monthly and quarterly financial reporting regime, discussed and acted

upon Capacity and systems for effective cash, debt and asset management Fast, effective and clean procurement procedures

7 Audits and programme reviews

Obtain an independent auditor Establish and enforce an annual reporting and auditing cycle Establish periodic reviews of performance and outcomes Take steps to address any deficiencies in resourcing or strategy, to

improve performance and to reduce risk.

Most municipalities, even those that are creditworthy, will need to confront the fact that poor revenue effort and achievement (low tax coverage, under-assessment of values, tariffs which amount to undercharging; under-billing, and finally poor collection of amounts billed) adds up to very poor tapping of existing revenue potential. Accordingly every FMIP should have a revenue programme.

Many municipalities, again even those that are creditworthy, appear to need to make improvements to their organizational and management structure to ensure good financial management. There should be a post of Chief Finance Officer (with a strategic financial leadership role, to which a Chief Accountant should report). Municipalities should develop the administrative capacity to plan and budget reliably over the medium-term (budget office). They should also ensure that they have the capacity to manage cash, debt and assets (treasury). Almost all municipalities would greatly enhance their overall performance if procurement procedures could be improved.

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

37Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Section 4

Practical assignment

Using a standard template, conduct initial research around credit worthiness of Lilongwe

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

38Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

MUNICIPAL CREDIT ASSESSMENT TOOL

Question Definition Response

Internal criteria

Financial and Credit Management1. Accuracy of the billing system o Totally inaccurate

o 70% accurateo 80% accurateo 90% accurateo 95% accurate

2. Effectiveness of account delivery o Pooro Unsatisfactoryo Satisfactoryo Goodo Excellent

3. Application of a consumer credit policy o Pooro Unsatisfactoryo Satisfactoryo Goodo Excellent

Management Quality and capacity4. Management experience and commitment Supply interviewer impression o Poor

o Unsatisfactoryo Satisfactoryo Goodo Excellent

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

39Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

5. Collection efficiency Annual billed amounts/annual cash received

o Less than 85%o 85-89%o 90%-92%o 93%-94%o 95% and above

6. Effectiveness of performance management system

o Pooro Unsatisfactoryo Satisfactoryo Goodo Excellent

7. Vision and mission and mandate clearly defined o No written document existso Written document exists as a tokeno Document exists and is clearly

articulated but not acceptedo Clearly articulated document exists

and executive managemento Clearly articulated document exists

and all staff identify with it

8. Ability and willingness to carry out internal efficiency reform

o Resists all changeso Will accept changes under duresso Neutralo Will apply obvious improvementso Continuously searching to improve

efficiency

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

40Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

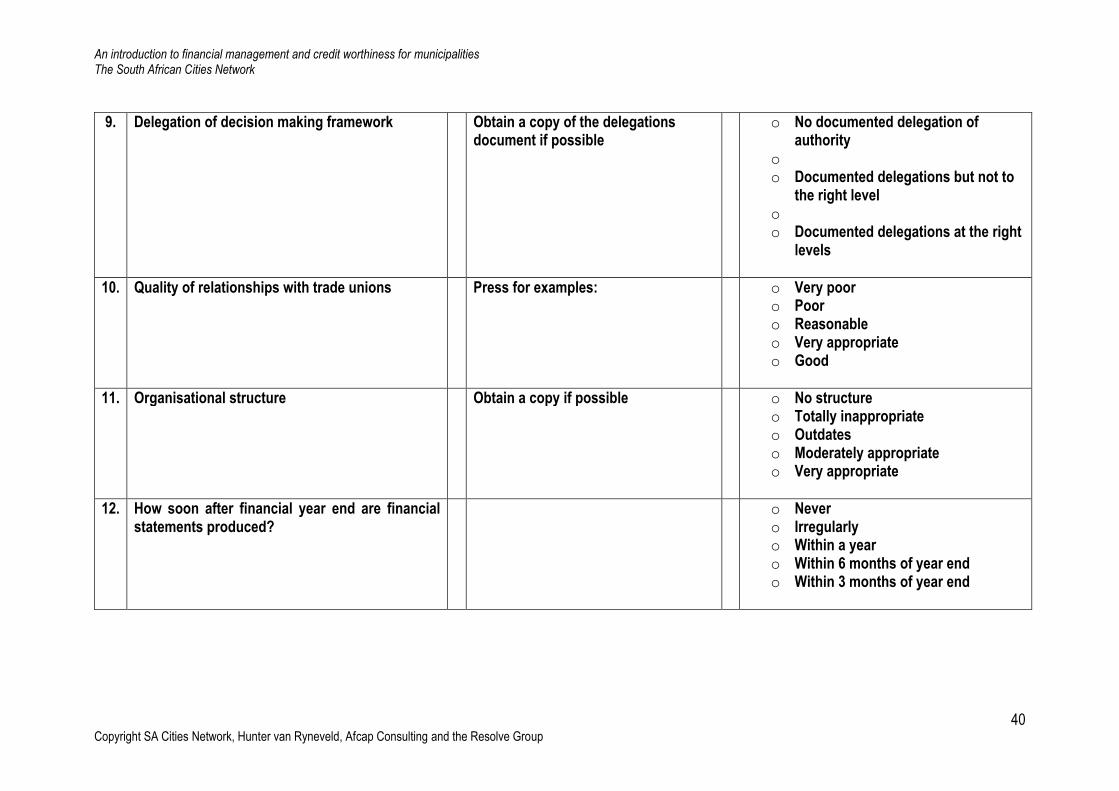

9. Delegation of decision making framework Obtain a copy of the delegations document if possible

o No documented delegation of authority

oo Documented delegations but not to

the right leveloo Documented delegations at the right

levels

10. Quality of relationships with trade unions Press for examples: o Very pooro Pooro Reasonableo Very appropriateo Good

11. Organisational structure Obtain a copy if possible o No structureo Totally inappropriateo Outdateso Moderately appropriateo Very appropriate

12. How soon after financial year end are financial statements produced?

o Nevero Irregularlyo Within a yearo Within 6 months of year endo Within 3 months of year end

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

41Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

13. Does political and executive leadership work together as a unified team?

o Nevero By exceptiono Seldomo Sometimeso Always

Strategic planning and internal transformation14. Formal, long-term strategic plan supported by all

stakeholderso No planningo Planning done but not appliedo 5 year planning appliedo 10 year planning appliedo 15 year plannikng applied

15. Are multi-year budgets prepared? o Not preparedo Prepared but not appliedo 1 year budgeto 2 year rolling budgeto 3 year rolling budget

16. Existence and quality of integrated management systems

Obtain examples of reports (HR? Financial? Billing?)

o No systemso Some departments have systemso All departments have their own

systemso Support systems integrated but

separate operational systemso Fully integrated MIS

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

42Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

17. What is the basis for maintenance expenditure planning?

o No planning and no maintenanceo Purely reactiveo For electromechanical equipment

onlyo For electromechanical equipment

and buildings onlyo For all moveable and immoveable

assets

Human resources and utilisation of private sector18. Meritocracy regime with length of services or

integrated with national government for staff promotions

o Promotion based on networkso Promotion based on length of

service and partially on networkso Promotion based on length of

serviceo Promotion based on merit and

length of serviceo Promotion based purely on merit

19. Training occurrence o No training programmeso Ad hoc trainingo Structured training once a year for

selected staff memberso Structured training at least once a

year for all staff memberso Regularly for all staff and

recognition given for all external qualifications

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

43Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

20. Appropriateness of staff qualifications in relation to tasks to be done

o Not matched at allo Shortage of qualified staffo Poor matcho Good matcho Total match

21. Use of private sector through outsourcing of non-core functions, management contracts, PPPs (public private partnerships)

o Against policyo Nevero Seldomo Selectivelyo Frequently

Customer relations22. Existence of customer service charter o None

o Yes but not appliedo Yes good but not appliedo Yes and applied but flawedo Yes good and applied

23. Regular proactive customer surveys? o Nevero Ad hoco At election timeo Every two yearso Annually

24. Integration of results of customer surveys in planning

o Nooo Partiallyoo Yes

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

44Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

25. Accessibility of pay points o More than 8 kmo Within 8 kmo Within 6 kmo Within 4 kmo Within 2 km

26. Availibility of call centres o Niloo Working hours onlyo .o 24 hours a day

27. Responsiveness to customer complaints of supply interruptions

Average time taken to adress customer complaints of supply interruptions

o Longer than 48 hourso Within 48 hourso Within 24 hourso Within 12 hourso Within 2 hours

28. What financial options are there to assist the poor?

o No assistanceo Interest-bearing loano Interest-free or subsidised loano Incorporated into the tariffo Free water

29. Communication with consumers o Noneo At the counter onlyo Only in times of crisiso Regular newsletters and leafletso Comprehensive use of radio,

newletters, leaflets, counters etc.

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

45Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

External CriteriaSupport from government30. Predictability of transfers from government Predictability of annual transfer

amountso No predictability at allo Nothing official but based on past

experienceo Able to budget reliably 1 year in

advanceo Able to budget reliably 2 years in

advanceo Able to budget reliably 3 years in

advance

31. Reliability of transfer payment dates Reliability of transfer payment dates (in terms of time)

o No due dates agreedo Usually within 6 months of due dateo Usually wihtin 3 months of due dateo Usually wihtin 1 month of due dateo Always on due date

32. Does government department pay their bills due to municipality?

Does government pay for services and taxes (use worst case)

o Nevero Longer than 12 monthso Within 6 monthso Within 3 monthso Within credit period

33. Probability of government support or intervention if serious financial problems develop

If unable to meet financial commitments (e.g. loan default or unable to pay staff), or serious management problems emerge (chronic service delivery breakdowns), what is the probability of government financial support?

o Highly unlikelyo Unlikelyo Possibleo Highly possibleo Certain

An introduction to financial management and credit worthiness for municipalitiesThe South African Cities Network

46Copyright SA Cities Network, Hunter van Ryneveld, Afcap Consulting and the Resolve Group

Autonomy and accountaibility34. Independence in setting key executive salaries How are salaries determined? o By government regulation

o By responsible Ministry/common scale

o By council wihtin government prescribed scales

o By council wtihin general pay scale structure