an evaluation of the navy resale system's operating and financial ... · branchstorereports...

TRANSCRIPT

Calhoun: The NPS Institutional Archive

Theses and Dissertations Thesis Collection

1984-03

An evaluation of the Navy Resale System's

operating and financial statements

Barnett, Michael Stephen

Monterey, California. Naval Postgraduate School

http://hdl.handle.net/10945/19313

DUDLEY KNC"

naval por/

AVALAnn

Monterey, Caiifornia

THESISAN EVALUATION OF THE NAVY RESALE SYSTEM' S

OPERATING AND FINANCIAI

by

, STATEMENTS

Mich ael Stephen Eiarnett

March 19 84

K. EuskeThesis Advisors : J. F. Mullane, Jr.

Approved for public release; distributionunlimited

T21 f f

Unclassif ied

SECURITY CLASSIFICATION OF THIS PAGE (When Data Entered)

REPORT DOCUMENTATION PAGE READ INSTRUCTIONSBEFORE COMPLETING FORM

I. REPORT NUMBER 2. GOVT ACCESSION NO 3. RECIPIENT'S CATALOG NUMBER

4. TITLE (and Subtitle))

An Evaluation of the Navy Resale System'sOperating and Financial Statements

5. TYPE OF REPORT & PERIOD COVEREDMaster ' s Thes isMarch 19846. PERFORMING ORG. REPORT NUMBER

7. AUTHORS.)

Michael Stephen Barnett8. CONTRACT OR GRANT NUMBERS.)

9. PERFORMING ORGANIZATION NAME ANO ADDRESS

Naval Postgraduate SchoolMonterey, California 93943

10. PROGRAM ELEMENT. PROJECT, TASKAREA 4 WORK UNIT NUMBERS

II. CONTROLLING OFFICE NAME ANO AOORESS

Naval Postgraduate SchoolMonterey, California 93943

12. REPORT DATE

March 198413. NUMBER OF PAGES167

I* MONITORING AGENCY NAME 4 ADORESSf/f different from Controlling Office) IS. SECURITY CLASS, (of this report)

Unc lassifiedIS*. DECLASSIFICATION DOWNGRADING

SCHEDULE

l«. DISTRIBUTION STATEMENT (of thla Rupert)

Approved for public release; distribution unlimited

'7. DISTRIBUTION STATEMENT (of the ebatraet entered In Block 30. If different from Report)

IB. SUPPLEMENTARY NOTES

19. KEY WORDS (Continue on reverie eide II neeeeemry end Identify by block number)

Operating Statements Navy Resale and Services Support OfficeFinancial StatementsAccounting StatementsNavy Resale System

20. ABSTRACT (Continue on reveree aide If neceeeary and Identity by block number)

This thesis contains an evaluation of the Navy Resale Systemfinancial and operating statements used to manage the salesactivities from the headquarters, region, main, and branchlevels. Navy Resale System (NRS) statements are comparedto the National Retail Merchants Association's (NRMA)statements presented in the Retail Ac coun ting Manua

1

andto statements provided by major retailers.

do ,:FORMAN 73 1473 COITION OF 1 NOV 6S IS OBSOLETE

S/N 0102- LF- 014-6601Unclassified

SECURITY CLASSIFICATION OF THIS PAGE (When Dale Enter;

ULU-icissii xeuSECURITY CLASSIFICATION OF THIS PAGE (When Dmtm Enfrmd)

From the results of the evaluation a number of conclusionsare drawn. To summarize the Navy Resale System statementsare essentially sound. However, change is needed in expensestatement and leased sales presentation to communicate a

better picture of how the Navy Resale System compares to

other major retailers.

S N 0102- LF- 014- 6601

UnclassifiedSECURITY CLASSIFICATION OF THIS PAGE(T»7»»n Data Enfrod)

Approved for public release; distribution unlimited

An Evaluation of the Navy Resale System

Operating and Financial Statements

by

Michael Stephen BarnettLieutenant Commander, Supply Corps, United States Navy

B.S., University of Kansas, 1973

Submitted in partial fulfillment of therequirements for the degree of

MASTER OF SCIENCE IN MANAGEMENT

from the

NAVAL POSTGRADUATE SCHOOLMarch 1984

ABSTRACT

This thesis contains an evaluation of the Navy Resale

System financial and operating statements used to manage the

sales activities from the headquarters, region, main, and

branch levels. Navy Resale System (NRS) statements are

compared to the National Retail Merchants Association's

(NRMA) statements presented in the Retail Accounting Manual

and to statements provided by major retailers.

From the results of the evaluation a number of conclu-

sions are drawn. To summarize the Navy Resale System state-

ments are essentially sound. However, change is needed in

expense statement and leased sales presentation to

communicate a better picture of how the Navy Resale System

compares to other major retailers.

u<JOLEY KNOX LIPRARY

TABLE OF CONTENTS

I. INTRODUCTION 10

A. GENERAL INFORMATION 10

B. NEED FOR A STUDY OF THE NAVY RESALE SYSTEMFINANCIAL OPERATING STATEMENTS 10

C. OBJECTIVE AND SCOPE OF THE THESIS 11

D. METHOD OF RESEARCH 12

E. THESIS ORGANIZATION 13

II. RETAIL ACCOUNTING AND REPORTING 14

A. INTRODUCTION 14

B. MERCHANDISE ACCOUNTING 14

1. Departments Within Retail Stores 14

a. Retail Inventory Departments 15

b. Cost or Non-Retail SellingDepartments 15

c

.

Contract Departments 16

d. Leased or Licensed Departments 16

e. Workrooms 17

f. Miscellaneous Revenue Operations -- 17

2. Computation of Gross Margin 18

C. EXPENSE ACCOUNTING 18

1. Expense Centers 19

2. Natural Divisions 21

3. Expense Comparisons 22

5

Ill

D. MANAGEMENT REPORTING 23

1. Merchandise Department PerformanceStatistics 23

a. Merchandise Department Statistics - 23

b. Merchandise Department PerformanceReports 25

2. Cost or Non-Retail Operations Reports - 29

3. Summaries of Expense Data 32

4 . Branch Store Reporting 4 5

5. Executive Level Reporting 47

a. Planning and Budgeting 47

b. Suggested Reporting Formats 48

(1) Total Company Balance Sheet -- 49

(2) Condensed Income Statement 49

(3) Total Company Income andExpense Statement 53

E. EFFECTIVE FINANCIAL MANAGEMENT REPORTS 53

1. Improving the Effectiveness ofManagement Reports 55

a. Report Content 55

b. Timing of Reports 56

c. Recipient of Report 56

d. Presentation 56

2. Common Weaknesses of ManagementReports 57

INFORMATION PROVIDED IN GENERAL PRACTICE 59

A. INTRODUCTION 59

B.' RETAIL MERCHANDISE REPORTS 59

6

C. COST OR NON-RETAIL MERCHANDISE REPORTS 65

D. EXPENSE REPORTS 67

E. BRANCH STORE REPORTS 76

F. EXECUTIVE LEVEL REPORTS 90

IV. NAVY EXCHANGE FINANCIAL OPERATING STATEMENTS -- 101

A. INTRODUCTION 101

B. RETAIL MERCHANDISE REPORTS 102

C. COST OR NON-RETAIL MERCHANDISE REPORTS 104

1. Service Departmental OperationsReport 104

2. Service Department Employee Benefits andOther Direct Expense Report 108

D. EXPENSE REPORTS 108

E. BRANCH STORE REPORTS 109

1. Retail Operations 109

2. Service Operations 111

3. General Expense Payroll 113

4. General Expense 113

5. Operating Statement (Excluding RetailClothing Stores and Navy Lodges) 119

6. Retail Clothing Stores 119

7. Navy Lodges 122

F. EXECUTIVE LEVEL REPORTS 122

1. Regional Reports 122

2. Headquarters Reports 124

V. COMPARISONS, CONCLUSIONS, AND RECOMMENDATIONS - 125

A. INTRODUCTION 125

COMPARISONS 125

1

.

Retail Merchandise Reports 125

2. Expense Reports 126

a. Comparative Statement of OperatingExpenses by Expense Center andSubcenter 126

b. Comparative Statement of OperatingExpenses by Natural Division 127

c. Other Expense Reports 127

3. Cost or Non-Retail MerchandiseReports 128

4. Branch Store Reports 129

5. Executive Level Reports 130

a. Total Company Balance Sheet 130

b. Condensed Income Statement 130

c. Total Company Income and ExpenseStatement 131

CONCLUSIONS, DISCUSSION, AND RECOMMENDATIONS 131

1

.

Retail Merchandise Reports 131

a. Department Total CompanyContribution Report 131

b. Department Contribution by SellingLocation Report 132

2. Expense Reports 134

a. General 134

b. Comparative Statement of OperatingExpenses by Expense Center andSubcenter 136

c

.

Comparative Statement of OperatingExpenses by Natural Division 136

d . Other Expense Reports 137

3. Cost or Non-Retail MerchandiseReports 138

a. Service Department OperationsReport 138

b. Service Department Expense CenterReport 140

4. Branch Store Reports 140

a. Retail Operations 142

b. Services Operations 142

c. General Expense Payroll andGeneral Expense 145

d. Operating Statement (ExcludingRetail Clothing Stores and NavyLodges) 145

e. Retail Clothing Stores andNavy Lodges 145

5. Executive Level Reports 147

a. Total Company Balance Sheet 147

b. Condensed Income Statement 147

c. Total Company Income and ExpenseStatement 148

D. CLOSING REMARKS 149

APPENDIX A GROSS MARGIN COMPUTATION 150

APPENDIX B EXPENSE CENTER ACCOUNTING 152

APPENDIX C WORKROOM AND COST DEPARTMENT OPERATINGSTATEMENT— LINE ITEM EXPLANATIONS 162

LIST OF REFERENCES 166

INITIAL DISTRIBUTION LIST 167

I . INTRODUCTION

A. GENERAL INFORMATION

The military exchange system consists of retail store

operations located on bases throughout the world. This

organization of stores had sales revenues which exceeded 6.3

billion dollars in Fiscal Year (FY) 1982. In comparison to

the countries leading retailers, in 1982 the military

exchange system's total sales ranked in fifth position

behind Sears, K mart, J. C. Penny, and Federated Department

Stores. [Ref. 1: p. R121]

The Navy Resale System FY 1982 total sales exceeded 1.5

billion which equates to approximately twenty-three percent

of the total military exchange sales. These sales would

place the Navy Resale System in twenty-third position in

relation to the countries retailers. [Ref.l: p. R 1 2 1 ]

Generation of such revenues places the Navy Resale

System in the category of "big business." As such an opera-

tion, it should follow the precepts of sound management and

proper accounting.

B. NEED FOR A STUDY OF THE NAVY RESALE SYSTEM FINANCIAL

OPERATING STATEMENTS

For management and fiscal control information, the exec-

utives of the Navy Resale System rely on operating and

10

financial reports provided by the Navy Resale and Services

Support Office. These operating and financial reports must

contain data which is accurate, clear, and concise.

The Commander of the Navy Resale and Service Support

Office has expressed concern that there may be a lack of

properly presented financial management information

available to the Navy Resale System and has requested that

this study be undertaken. [Ref. 2]

C. OBJECTIVE AND SCOPE OF THE THESIS

The objective of this thesis is to determine what opera-

ting and financial information should be made available to

headquarters, region, main, and branch levels of the Navy

Resale System to properly manage the local sales activities.

The scope of this thesis is limited to a review of Navy

Resale System reports and to provide recommendations for

their improvement. It is beyond the scope of this thesis to

provide an economic analysis of such recommendations or

implementation procedures.

This thesis introduces general retail accounting and

reporting standards as provided in the National Retail

Merchants Association, Retail Accounting Manual . Based on

an analysis of current literature common weaknesses and ways

of improving the effectiveness of management reports are

described. This information is provided to not only make

improvements in what information should be provided but also

11

to explain how the information should be provided to

encourage its use. The thesis reviews current retail opera-

ting and financial reports provided by major companies

within the retailing industry to determine to what extent

the retailing industry follows the Retail Accounting Manual .

D. METHOD OF RESEARCH

A review of the literature that was available from the

following data bases was completed:

1 . Defense Logistics Studies Information Exchange, U . S.

Army Logistics Management Center, Fort Lee, Virginia.

2 . Defense Technical Information Center and DefenseDocumentation Center, Defense Logistics Agency,Cameron Station, Alexandria, Virginia.

3. The Naval Postgraduate School Thesis, TechnicalReports, and General Collections, Monterey, California

4. DIALOG Information Retrieval Service, Lockheed Missleand Space Co., Inc., Palo Alto, California.

Letters were sent to the top twenty retailers, in sales

volume, as listed by Standard and Poors, November 1981

edition of Industry Surveys and to the Army and Air Force

Exchange Service in an attempt to obtain operating and

financial reports representative of the major retailers.

Responses were received from nine of the retailers including

the Army and Air Force Exchange Service. Of those nine, six

retailers supplied various operating and financial

accounting reports.

Interviews were conducted with twelve executive level

personnel at the Navy Resale and Services Support Office and

12

seven executive level personnel at the region and exchange

level

.

E. THESIS ORGANIZATION

The first chapter briefly introduced the magnitude of

the Navy Exchange System and presented the impetus for the

research. It also delineated the author's objectives and

research methodology.

Chapter Two provides the reader with an introduction to

retail accounting and the reports currently suggested by the

National Retail Merchants Association. It also provides

techniques to improve the effectiveness of management

reports as well as common weaknesses of management reports.

Chapter Three provides a description and discussion of

operating and financial reports used by the private and

public sector.

Chapter Four provides a description and discussion of

operating and financial reports used by the Navy Resale

System .

Finally, in Chapter Five, the author makes comparisons

between the National Retail Merchants Association, private,

public, and Navy Resale System reports. Conclusions and

recommendations are then drawn based on the comparisons and

the retail accounting standards provided in the Retail

Accounting Manual .

13

II . RETAIL ACCOUNTING AND REPORTING

A. INTRODUCTION

This chapter describes the various aspects of retail

accounting in accordance with today's generally accepted

procedures and norms. The topics covered are merchandise

accounting, expense accounting, management reporting, and

the improvement of management reports. The Merchandise

Accounting section defines the various types of departments

in retail stores and the computation of gross margin for

these departments. The Expense Accounting section describes

the recommended method of segregating expenses for expense

control. The Management Reporting section provides the

rationale for various management reports and suggested

formats for each type report. In the section on improving

management reports, techniques for improving reports are

described and some of the major weaknesses in current

reports are delineated.

B. MERCHANDISE ACCOUNTING

1 . Departments Within Retail Stores

As defined by the National Retail Merchants

Association (NRMA) in their Retail Accounting Manual (RAM)

departmentalized stores are organized in a series of

departments "for the purpose of maximizing efficiency and

14

control in either selling merchandise or rendering serv-

ices." Departments differ in the nature of an item or

service sold, the method of inventory valuation, and their

relation to other departments. The NRMA has defined six

principal types of departments as follows:

a. Retail Inventory Departments

Retail inventory departments "sell merchandise

to the public, using the retail inventory method of account-

ing to determine departmental inventories at retail and at

cost, and to compute [owned retail] gross margin." (Owned

retail gross margin refers to the gross margin of depart-

ments which are owned by the store versus the gross margin

of leased or licensed departments.) Basic merchandise such

as hardware, fashion goods, linens, stationery, jewelry,

notions, housewares, and luggage, as well as other typical

department store merchandise are usually sold in retail

inventory departments.

b. Cost or Non-Retail Selling Departments

Cost or non-retail selling departments, other-

wise known as service departments, carry inventory on hand

at cost only, versus cost and retail. Typical cost selling

departments are beauty salons, flower shops, custom order

departments, gift wrapping, repair departments, restaurants,

and engraving. Inventory in these departments consists of

15

supplies necessary to perform the service involved; not

finished goods for resale.

c

.

Contract Departments

Contract departments sell merchandise at whole-

sale prices to business and institutional purchasers such as

hotels, restaurants, hospitals, and churches. The orders

placed by these businesses are normally very large, there-

fore, prices charged are considerably lower than the normal

retail prices charged for the same items to a store's

regular customers. Items normally sold in this manner are

furniture, linens and domestics, and china and glassware.

d. Leased or Licensed Departments

Leased Departments are merchandise or service

departments operated by independent companies under contract

or lease. Usually these departments are highly specialized

in nature or require a heavy investment in equipment which

the store does not desire to make. Examples of these

departments might be shoe or shoe repair, auto repair,

vending, beauty salons, photo studios, pharmacies, and opti-

cal shops. In return for the permission to operate such a

department the independent firm pays a fixed percentage of

their sales to the lessor store. Normally, a leased depart-

ment follows the store policies and procedures and is

presented to the patron as if it were just another part of

the store.

16

e

.

Workrooms

Workrooms are departments that ordinarily deal

with alterations and repair of merchandise sold in retail

departments. However, workrooms also set-up, assemble, and

finish merchandise before it is put on sale. Because there

is a similarity between workrooms and cost selling depart-

ments, guides were established by the NRMA as an aid to

proper classification. The NRMA guide states that:

A department should be considered a merchandise

service workroom if:

1. its operations and income are substantially involvedwith services performed for the principal retaildepartment(s)

;

2. its revenue is used only as an offset against theworkroom's cost, and is not included in the principalretail department's sales;

3. the amount charged for services performed is suffi-cient to enable the workroom to operate at or near thebreak-even point; and

4. it neither manufactures an item nor, in effect, con-verts merchandise into a finished product.

The more common types of workrooms are drapery,

engraving-glassware and stationery, furniture, men's and

boy's clothing alterations, and monogramming workrooms.

f. Miscellaneous Revenue Operations

Miscellaneous revenue operations consist of

various services which stores furnish at a nominal charge to

patrons. Some of these services are delivery and layaway

17

charges, check cashing, money order sales, pay toilets, and

scales. [Ref. 3: pp. VI - V 4

]

2 . Computa t ion o f Gross Margin

The NRMA has suggested that the various departments'

gross margin be split into three major groups, Owned Retail

Departments, Owned Cost Departments (including Contract),

and Leased and Licensed Departments instead of grouping them

into one total amount.

In general, gross margin for owned departments is

derived by subtracting from net sales the net cost of mer-

chandise sold, workroom loss or gain, and other costs of

sales. The detailed method for computation of gross margin

for owned retail and cost departments, as provided by the

RAM, are described in Appendix A.

Leased or licensed departments differ from an owned

department in that its merchandise does not, per se, have a

merchandise cost or a gross margin. Instead, reported gross

margin for these departments is the net sales less the gross

commission. The RAM states,

For development of departmental operating statements,leased department commissions are considered as part ofgross margin. In the development of financial statements,leased department sales and commissions are shown sepa-rately from owned departments. [Ref. 3: pp. V13-V15]

C. EXPENSE ACCOUNTING

Expense accounting improves profitability through the

control of operating expenses. This is done by accumulating

operating expenses into expense centers and then holding the

center's management responsible for controlling expenses by

comparing actual to budgeted and prior years' figures.

The NRMA's Retail Accounting Manual (RAM) describes in

detail how expenses should be recorded and reported. This

section discusses the basic concepts of expense recording

and reporting. A detailed presentation of expense recording

is provided in APPENDIX B.

1 . Expense Centers

For the RAM to serve the needs of not only large

store chains but also small, one man operations, 10 expense

summaries were created, with 44 expense centers and 22

subexpense centers. The smaller operations need only use

the 10 expense summaries that follow:

010 Property and equipment

100 Company management

200 Accounting and management information

300 Credit and accounts receivable

400 Sales promotion

500 Services and operations

600 Personnel

700 Merchandise

800 Selling and supporting services

900 Merchandising

A company may use as many of the 44 expense centers

as they. desire to provide needed expense breakdown. Some of

19

the largest companies may even find it preferable to add

more expense centers. An example of the breakdown possible

is shown below using expense center 800, selling and sup-

porting services:

800 Selling and Supporting Services

810 Selling Supervision

820 Direct Selling

830 Customer Services

840 Selling Support Services

860 Central Wrapping and Packing

880 Delivery

If all the expense centers are not used, the NRMA

has suggested the management expense centers ending with

"10" be used to accumulate items of expense for unused

expense centers. Using the expense summary above, a firm

might want to use the expense center 820-Direct Selling and

then accumulate all other expenses in expense center 810-

Selling Supervision.

An even more detailed breakdown can be made using

subexpense centers. The 820-Direct Selling expense center

can be divided into the following subexpense centers:

820 Direct Selling

821 Retail Selling Departments Salespeople

823 Interior Decorators

824 Cost Selling Departments Salespeople

20

826 Floor Cashiers and Wrappers

828 Forward Stock Maintenance

2 . Natural Divisions

The RAM classifies 17 types of expenses which they

identify as natural divisions besides accumulating the

expenses by areas of activity. Some of the largest firms

may desire to add more natural divisions, however the 17

natural divisions that follow should be sufficient for most

firms:

01 Payroll

03 Media Costs

04 Taxes

06 Supplies

07 Services purchased

08 Unclassified

09 Travel

10 Communications

11 Pensions

12 Insurance

13 Depreciation

14 Professional services

16 Bad debts

17 Equipment rentals

18 Outside maintenance and equipment service contracts

20 Real property rentals

92 Credits and outside revenues

21

Additionally, three transfer accounts are identified

by the RAM as an aid to transferring expenses between

expense centers:

02 Allocated fringe benefits

90 Expense transfers-in

91 Expense transfers-out [Ref. 3: pp. II 1 — 1 1 1 5]

The allocated fringe benefits transfer account ( A c c t # 02)

is used to redistribute actual expenses accumulated in

Expense Center 660- Medical and Other Employee Services and

Expense Center 670- Supplementary Benefits to all other

expense centers having a natural payroll division. The

remaining transfer accounts (Acct # 90 and 91) are needed

to effect a transfer from one expense center to another in

order to properly reflect the actual operating costs of the

expense centers; the amount to be transferred out of an

expense center is the composite of several natural

divisions .

3 . Expense Comparisons

Why is there a need for expense centers if all

expenses are also tracked by natural division? The National

Retail Merchants Association states,

Because of the increasingly diversified manner in whichstores are performing identical activities, comparisons by

natural divisions are becoming more meaningful as thevalid basis for such comparison. This comes about princi-pally because with mechanization and the use of moresophisticated equipment, the number of people and the

resulting payroll expense are reduced, while the amount of

depreciation and equipment rental cost is increased. In

22

other instances, greater reliance on outside servicebureaus and service agencies are similarly replacing pay-roll and supply expense in the expense center concerned.Therefore, comparability by natural division diminishes,although comparability by expense center remains signifi-cant and valid. [Ref. 3: p. 11-10]

D. MANAGEMENT REPORTING

This section describes management reports that are sug-

gested as necessary by the National Retail Merchants

Association (NRMA). Included are the various retail mer-

chandise departments reports, cost or non-retail operation

departments reports, expense reports, branch store reports,

and top executive level reports.

1 . Merchandise Department Performance Statistics

a. Merchandise Department Statistics

Merchandise department statistics are developed

on owned retail inventoried merchandise as a means to

measure a department buyer's performance. Through the review

of a merchandise department's total company performance and

other direct expenses over which a buyer has control manage-

ment may evaluate a buyer's performance.

The NRMA has stated,

Departmental expense distribution is a matter in

which considerable latitude must be allowed. Hard and fastrules cannot be applied. The distribution of expenses to

selling departments poses problems on which many differingviews are held.

In general there are two approaches to depart-

mental expense accounting; the Net Profit Plan and the

Contribution Plan.

23

The Net Profit approach is a full cost approach

which requires the allocation of indirect expenses in addi-

tion to direct expenses. The supporters of this method

believe that it produces a profit figure that can be used to

judge the operations of the department and that it develops

some degree of responsibility by the buyer for the depart-

ments profit performance. The Net Profit approach has cer-

tain disadvantages. First, the buyer is not in a position

to have any affect on the expenses pro-rated to his or her

department. Second, it is difficult to develop a reasonable

or meaningful basis for proration which usually leads to the

use of sales as the proration base and the subsequent con-

cealment of the department's true performance picture.

Third, the allocation of expenses can be both costly and

time-consuming. Finally, most expense control is the

responsibility of operating and sales supporting activities,

not the selling department.

The Contribution approach, on the other hand,

accommodates both the measurement of department results and

evaluation of a buyer's performance without the disadvan-

tages above. The contribution approach is based on the

concept that each selling department generates a gross mar-

gin on its sales as well as related direct expenses. The

difference between these direct expenses and the gross mar-

gin produces the contribution. The RAM states, that

24

expenses used in figuring contribution are different

depending on whether you are computing a selling locations

contribution or a total company contribution. This

difference is caused by the expansion from single store to

multi-store organizations. In the single store operation the

department buyer is responsible for all departmental

expenses including those related to acquisition, distribu-

tion, promotion, and selling of merchandise. In the multi-

store organizations the sales manager is responsible for

selling location expenses while buyers are held responsible

for acquisition, distribution, and promotion of merchandise

as well as other expenses that are performed on a central

basis and cannot be associated with a single selling loca-

tion. Expenses which cannot be associated with a single

selling location cause the difference between the summation

of all selling location contributions and the total

company's contribution.

b. Merchandise Department Performance Reports

Merchandise department reporting differs for

multi-store operations as compared to single store compa-

nies, since both the selling location and central organiza-

tion expenses are accounted for separately. This results in

the need for two merchandise department reports, one for the

total company and another for the selling locations. The

NRMA suggested reports may be seen in Exhibits 2-1 and 2-2.

Though these are only suggested formats, the information

25

o£

in ra

-l>-

E<

UJH<9 c

(0

51

3n

o

EC<ID>

£<

5?

•" Is

C m

E<

zoI-

m

zoo>z<0.

soo_l

<I-

oHI-zUJ

h-cc

<aUJ

o

3?

in co

E<

a5?

oDCUJCl-

cCTJ

a.

F<

5?

• Is

E<

C3 -

03 .ora °^1/3 m« 5

§1

|S«oaj a> EQ

a ow

^ CD 0J O u

2c/)z - z ^

i° s ° °; o ^ o

Cost-

ito

Nge-%

count °i ros?

«tf> c

B », « W(J O

E «

8<3

wm in r oSCO ca

5»00!5c a ^ £"Jo u f <5

fj ro O 3 ofj c3

2I^a 50

zO en— cu

0> 03ro •-

to o

1 2in

*-

oj O j5«" J.

Z EJ. w5- <nn" 0) O O-—_Z"5-rS 2 w *? >< .0 O ojrf„« °^ 2 Q-_

ra- vp 2 -^

-52 i°- =1 z «3"J£ 2'5£QOl-ZO

oo

J Dl

L0 <ro ift

0)

co

EC crVa

0) W(Jto c 10 -

5i

n C >

a>< ?

o c(/>

ro oto

o 0) OP55 a

zoHH»PQHPi

HZou!h

Z<

soo

<HOHHZWsHPi

<Ph

wQ

I

1-1

wXw

26

UJ

>mzor-

amtrh-Zooh-ZUJ

2r-or<o.UJ

o

Gross Margin%lo

Sales

s5

1<

Workroom

and

Other

Cost

ol

Sales

%to

Sales

J?

E<

StockShortage

%to

Sales

5?

<

c

«5

*

E<

Merchandise Cost

Incl.

disc

%to

Sales

s?

E<

S 5

1 1

g?

E<

Returns %lo

Gross Sales

3?

E<

11OB)

j?

E<

>- -i >t— 1 M5 1-0. -J

> -J >h-B. -i 1— Q. _J t-Q._l

r*--J>f- 1

> -l>-H- 1

>- _1>(-0.-J

> —1>1— Q. _l

</>i-0 r lu

zoHH<Coor-J

ozHhJwCO

><pa

zoI—

I

HpaH

HZooHZW

Hoi

<!Oh

WPCN

I

CM

HHpa

H33

W

27

zof-<uo-J

oz

UJ</>

>-

CD

zo

3CO

zoor-zUJ

rx<aUJa

ai

Gross Margin Dollars Per

Sq

Foot

E<

tn u.

S rr

w"5

E<

13O

Sales

%of

Common Base35

0.

Dept. Contnb. %to

Sales

s

E<

Other

Direct

&

AssignedExpenses

%to

Sales

S*

E<

Sales Promotion %to

Sales

^p

E<

DeptSupplies

%to

Sales

j?

E<

Salespeople

Payroll

%to

Sales

s?

E<

Department Supervision

%to

Sales

5? V

E<

c

E> -i>I-Q--I

> _l>1— 1 i— a i

>- -i >1-0.-1

> -i>I-Q.-J

> -1 >h-a._i

> -i>h-CL-J 1— Q 1

9a int-CDCClu

53oH

<iUO

o53HhJkJ

w

PQ

53oH

5=>

PQ

HPS

HOCJ

HWSH<PmwQCN

I

pa

HX!W

28

provided is considered the minimum necessary for proper

evaluation of a departments gross margin performance.

In producing a total company contribution figure

the Depar tment Total Company Con tribution report, Exhibit 2-

1 , uses only direct expense items which are easily

obtainable and relatively meaningful on a total company

basis: merchandising and buying costs, and advertising media

costs. Other costs, such as merchandise distribution

expense, can be added to the report if a company feels the

added costs of computations are worthwhile and necessary in

measuring company and buyer performance. The more expenses

allocated to a department, the closer the report approaches

the net profit or full cost approach.

The Department Con tribution By Selling Location

report, Exhibit 2-2, uses direct selling expenses that are

related to a selling location such as selling payroll and

supplies. In addition there are other valuable departmental

statistics which can be used in evaluating a department's

performance by selling location. Two of these, sales per

square foot and gross margin dollars per square foot are

shown on Exhibit 2-2. [Ref. 3: pp. VII 1-3]

2 . Cost or Non-Retail Operation Reports

In the previous section the discussion covered

merchandise departments that are controlled by the retail

inventory method. Departments that are normally considered

29

cost or non-retail departments are not suited to the use of

the retail inventory method, since they do not have invento-

ries or purchases at retail and are not concerned with

markons (markon is the increase in price between cost and

retail used to cover direct expenses, overhead, and generate

a profit) as an element of recordkeeping. In addition these

departments usually do not have problems of markdowns

(markdown is the reduction of a retail price to enhance

movement of an item) and shortages as separate elements in

the determination of gross margin. Though the derivation of

cost of sales for the various cost departments is similar

in principle to retail departments, the elements of cost are

usually very different.

For the above reasons, and because it would not be

appropriate to allocate expenses such as buying and mer-

chandise management, separate operating statements should be

prepared for cost or non-retail operations which are inde-

pendent of any other department. [Ref. 3: p. VI-1] However,

the NRMA has stated that, sales of cost selling departments

should be included in total store sales. The NRMA suggests

the use of Exhibit 2-3 for any of the cost departments or

workrooms normally operated in conjunction with retail

stores. A detailed explanation of the items in the operating

statement can be seen in Appendix C.

30

zUJ

<I-

oZr-<ccHIa.

OI-zUJ

5tr<Q.UJaI-C/5

ooaz<

oorx

en

O5

UJ

z

o_

S5

IS£°j

£ Q

|Ioui

g Bl

OdP <

isccr~

a

Net Department

ChargesS

I

CC

Om<-j

t-urx

ou.

o

UJ

DZ2X

zDXco5UJzO

53

§|OS—

STATISTICS

No

ot

Hours

Worked

Averaqe

No

of

Employees

Average

Floor

Space

in

Sq

Ft.

Average

Cost

per

Unit

Sales

to

Customers

01

IIto

Distribution

of

Production

CostS'itit/j —

II

c— B3|d

BD

<ot-

rx

Oa.

cc

az

<cc

a.

o

1

1

1 1

1.

Revenue

from

Sales

to

Customers

LABOR

AND

MATERIALS

2.

Inventory

of

Materials

and

Supplies—

Beginning

of

Period

3.

Purchases

of

Materials

and

Supplies

4.

Material

and

Labor

Services

Purchases

5

Total

6

Inventory

of

Malorlals

and

Supplies

—

End

ol

Period

7.

Materials

and

Supplies

Used

o

I

J —

>l

o o 10

Total

Labor

11

Work

In

Process

Ad|ustment

12

Total

Materials

and

Labor

OTHER

MANUFACTURING

CHARGES

13

Space

Charge

14

Supplies

IS.

Utilities

16

Use

ot

Cars

and

Trucks

17

Carfare

and

Travel

18

Services

Purchased

19

Repairs

lo

Equipment

20

Payroll

Taxes

and

Supplementary

Benefits

21

Insurance

22

Depreciation

23

Total

Other

Manufacturing

Charges

24.

TOTAL

COST

OF

PRODUCTION

25

Less

Credits

from

Transfers

26

Net

Cost

of

ProOuction

27.

PROFIT

OR

LOSS

(Indirect

Manufacturing

Departments

and

Merchandise

Service

Workroomsl

OPERATING

EXPENSES

(lor

Cost

Selling

Departments

only)

28

Operating

Expenses

(for

Cost

Selling

Departments

only)

26a

128b

I

Each

Store

to

Insert

appropriate

Expense

Cenler

28c

1

No

s

and

Titles

etc

)29

Total

Operating

Expenses

30

Operating

Profit

or

Loss

(Cost

Selling

Departments)

l s.

t o

T °

6 s

Is

5 Is t

I °E 5

I I

I 6

6 2

HBSWXwH<HCO

OHH<wPhoHWs

<P-WoHCO

OCJ

Qz<XooOS

PS

o

mi

CN

HMCQHBS

XW

31

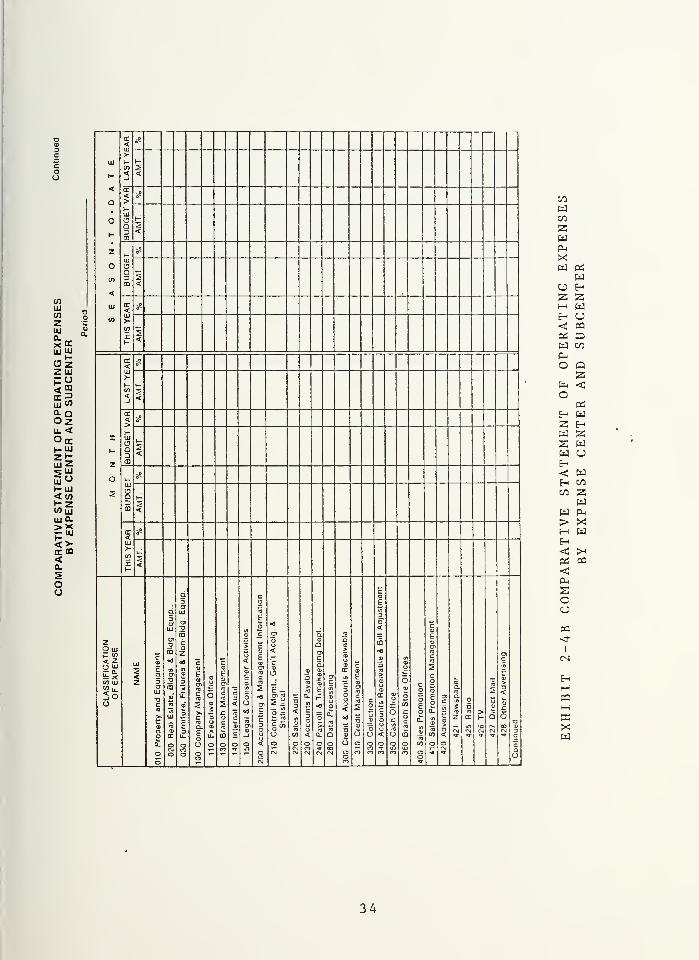

3 . Summar ies of Expense Data

To achieve the objective of improved profitability

as stated in the expense accounting section of this chapter,

management must be provided with reports concerning expenses

in the monthly financial statements. These reports can then

be used for comparison against the company's budget and to

expense percentages provided by the NRMA for retailers

similar in size, merchandise composition or geographic

section of the country. The Retail Accounting Manual

provides six different expense reports which are described

below.

The first expense report shown in the RAM displays

expenses by expense summary as compared to the current

budget and to last year's performance, and shows variances

from the budget. Amounts are shown both for the current

month and season-to-date. The report as presented in Exhibit

2-4A shows only the 10 expense summaries. However, companies

that use expense and subexpense centers may wish to display

them as in Exhibit 2-4B.

The second expense report shown is a statement of

operating expenses by natural division. This report is

similar in format to the first report and is presented in

Exhi bit 2-5 .

The third expense report is displayed in Exhibit 2-6

and is a report for individual expense centers. The format

for this report provides for variances from budgeted

32

05

z>->

'

CO111

co

zLUaxuj eg

LL

CEHI

OS"U.3 >qCO CD

. ui ai7« CO

Sis

was uj

UJ>i-<(X

<a5oo

coUJ

aaCO

IT<LU>

5

s8

<

UJ

<Q

O

a.

<>h-jj

aoCD

5°

2<

Zo

<UI

CO

cu3

Q

CO

,".

r—

<

DC<UJ>

Xl-

3*

5<

X

2o5

cr

<:jj

>

t/)

<J

*

<

<>

UJ

aa3CD

c»

i-

<

h-UJ

C3QCD

„»

i-

<

cr<LU

>(0

z

3!

<

zO uj

< z

CO UJ

3oo

LU

s<z

ca)

Ea

crLU

•ac<o

>.r»a.

at

cn>

S<u

O)CO

cCO

>.cCO

a.

E

O

dc

cCO

ECO

o>CO

cCO

5

cCO

o>c

c3

u<

C\J

OCO>

OCO

I(I)

c13

<0cCO

•5CD

6

c

E

li-

enCD

CO

CO

O

c

ra

CBa.

OocCO

CDU

z<a

CO

in

o>ccV)

CO

Q_

OOCO

. CO)

II= a° Tl.2 c"D a]

« ft•= S

1

O CO

oj

5 co

encCaQ.

CO

TJcCO t/»

°> 8c -L= ><jj CD

CO CO

ao

ctrt

0cCO

J=

5

s1

m

LUCOzLUQ-XLU

—1<h-O1-

on

Pd00

WPL,

XWoS3HHPS PS

wPm

opn

o

S3

WUj

2W W£ Ph

W XH W<OT PO

W>HH<CPS

<P-

£OO<i

CM

HHpa

Hsaxw

3 3

enUJenzUJ

£«UJUJ

OZZ uj

EC 3

Ozu.<Oct

£Suj Z5 uj

l-UJ< co

UJ Q.

> X

**£CC CD

<Q.

5OO

UJ

1-

<

O

o1-

z

o

<

UJ

trt

<UJ>t-

if"

<>

UJ

OQ3CD

2<

1-UJ

aaCO

i:

<

DC<>

r

°

<

I

i-

z

o

2

<

>

<

o'

5<

DC

<>1-UJ

<3aU

»°

2<

1-UJ

aQD

°°

1-

5<

OC

<UJ>•

to

I1-

i°

2

zO ai

< z(J UJ

y") uj

5oo

Ul

2<z

cCD

£a5CJUJ

DCo>•CCD

CLoCL

oo

a5CTUJ

m*3

CJ.

T3

CD

cd"

s

UJ

15

a:

orgO

dC7UJ

d»aCD

Co

71

D3

ii

a

c

5u.

ono

cIt

£0)

enac

S>c•n

a.EooQo

XI

u

5<t>

3u©u-

a

CD

EsCTa

a

Cuc

CD

a

3<

C

c

Q

-.1

>

<oc3CoOofl

<3aiQ-j

oa-)

co

E

ac

cai

ECD

O)ac

C>c

c

ou<aoCM

a»

ou<'cCD

O

E -

252 —

!«ooCM

63<

CO

aCMT\J

CD

aco

nj

a.

c3ouo<oCTCM

CD

Qo>caED

CDJC

E

a

DO

0.

o-T

atc

uU

u

aQOCDCM

5CO>s'J

D

c3Ou<*3

u

5o5en

c9ED0)nc<o

fi

aoc*i

c

u«oOooct

5oEEfl

^5

.aCO>s

CD

CE

C3Ou<oC-i

CDO

5JC

Ooilln

a

5

a

cunj

CO

o

cg3Eo

C/>

oo

c

ECD

o>(fl

c

co

oEoa.

a>

CO

E/3

o**

Olc

>•a

<oTJ

a.COaS

z

OJ

5cc

in

>KcOCM

u

d

CMT

a>c

1<

CD

oTJCMT

T3CD

C

COo

C/J

WC/j

WX!pa

CJ22HH<JOS

wHWa«

W cn

O QZ<c

Pi

WHW

w u< wH c/j

en Zw

W PU

> XH WHpi pa

<Ph

oCJ

P3<!

I

CN

Hi—

i

pqHaxw

34

LU

wzUJ

LU UJ

OzZUJ

<E°EC 3uj w

Ozu.<ObKUJ

Sz•>luUjOi-UJ< I/)HZ</>LULU CL>xpui

tr co

<a.

5oo

UJ

>-

<

o

o1-

z

o

<

UJ

in

<UJ>

'.1

5

°°

5

tr

<>

UJ

aari

m

X

_

5

~

UJ

aDCD

°°

-

<

rr<r

>-

c/)

I

°*

2

I

t-

z

o

2

tr

<LU>-

I-co

5

o*

s<

cr<>t-LU

co3a

°

s<

(

Oc3

*

2<

<Uj>

v-

*°

5<

zO UJ

P BI< zo uj

&SCO UJ<fl 11

5oo

2<z

5cUJ

ac

IfIT

JJ

u0.

'J)

4

cIf)

a

co

5Io

3Q_

1a

CO

(D

c-c

oa>

2

n

Dr:

UJ

acTj

CB>UJ

atfl -a

Q.

6oT

Co

5O5a

<a

a

6

aa

ccr

W«»

3

Co

a

"OcIS

s

s

coEaai

c

1co

BaOr>cAo

>

to

otf-j

5

•.o

oP3

CQ

E3E<E

o

qc-o

BCacau3

o5o

atc

aBa

DOXo

a.0)

ex

oc(0

«c

cB

c

2oX'

ucco

D

8

c

E9CTfl>

C

cco

CU

£o

c

E:>

a£UJ

oCM

=c

o'-O

>

CO

©a

EUJ

—

t:

'V

5•j

2a

cDCD

£

c

1Baa

O

so>

o07

cic>

* -9

il

s

S

©

o03

>o©cr

V

T3

o —

or*

o

C

2ac

C

iu

Btx

o

ac

QC

c

£OCM

c «

*!:

r0]

o

o

>C

c

aen

C

o5

a

>

OS

XoPI

go

c

Co'J

I

ct:

wwSSw.Oi

Xw &W

o H2 ZH uf- U< CQ

CKi 3w t/J

Pho Q2

u. <o

Ci

H W2 HPd z.

32 UJ

W uc^-

< wH Cfi

W z:

wW Pu> XM wH< PHCi =3

<p-

*c_.

OCJ>

pq<r

<>j

CO

M

35

(/>

LUIf)

ZUJ

OzZ LU

PSCC 3LU W

Ozu. <Ol(-UJ

UjZs wLu oi-iu< c/>

t-zwShi &>x

<a5OO

IU

1-

<

a

o

Z

oto

<

UJ

to

re

<>-

en<

."

H

<

<>HLU

'J

QDa

o?

<

oa3m

°°

5<

IT

<>(A

zt-

*

<

I

i-

z

o

2

<LU>

<_J

je

2<

<>

LU

ao3

*

2<

oQm

j5

<

DC

<LU>-

03

XH

o°

1

*

zO alc to<zo UJ

C/J UJ

o

UJ

S<z

E-p

Cfl

a>c

6aaa3en

ac

Kgo

co

>

a3(/]

C?C

i

o£1

c

S

6o

UCIaataB

(A

5aac

ai

CO

5X

CM

osa

9CC

gc

Bt

«aaex

up

a.aa01c

w

ou-r

oa

5

c

£

ucc

cfi

tc

oc

cuc

I

u.

CO

>

Eo

uoi

D

E

_n

aaa3

(/)

ac

a(0

o00

c

tti

a.

oc

ca,aca

5

c<o

Ua3

a

Qas

ncrBO

CL

x

303

ac

t

c

LL

PI

30.

CL

c

eu

a

UJ

gi

Lb

i£

CD

|6c

jZ

3J

oo9

cCD

ECD

ai

c

2oc

6c

jC

2

oen

ac53iD

aa

o

coU<X>

c

cen0>

UJCOzUJCLXUJ

<O

en

wC/3

WPhXmo5ZHEH<Pi

pet

WH5Swupa

W CO

p-l

o o

<Pi

wH

Cmo

Hz

S3

H< WH Wen 2W

W PU> XH W<PS

<Pi

Soo

i

CN

COMSBXIw

36

HI10za

z>-

<zceoUJ —

o>

*£

UJ <

toco

ui>t-<cc<a2oo

cr,0

1<

> 1

f~ H (05 > \

a <

BT<>

*

<

a C32

T;

<

zO

1-f.

u< DO 5

(1)

rr *<

>\-

i

rr.

>

tn s.j <

cr -«j

>

I c

m

2<

(

ZO ^S

QaCD 3<

c ,<

>

d ©3 3a- C

CO 111 >" —

z<yi « en CC O

CO

mat

c

u n> UJ

a 2_j << z

c£CD

to

10

nj

Caa:

cVEa

c

is5 c

is

ca>

cr

>•

5

3O

C3

CO

c3c

5C

0:

<Z

CD

X

3Q.

(A

a

•0©

to cp

uc3E

crt

cCD

Uc

cg

0)

"5

c (A

B

ca>a.

i

DC©IA

5

©

u

CD

C

CO(/J

cCO

T3 a ? > b 3 a 0 3 i2 > A a ac <u a ^ » CO X

0. & 1- to to 13 f- O Q_ — O £ CD UJ U co X O 1'

,_ en ^ <D r*. «_ cm en T X 1 r*. CO CM4.O O O O UJ

r

en

Wen

Zw

Xw

o

S3O<

CtC HW cn

P-, ho >

o

HW

Pi

H<2H

<lo pa

W>1-1

<OS

<P-.

ooun

I

CN

paH

x;w

37

»-cc

oaUJDC

CCUJr-zUJ

oUJto

zUJaXUJ

LUO *

oiri

Q Z<

~-~

Occ

Zcc 3UJa.

<> m to N >o en oO (D o CO CO <n r^ CO

O o ;**_,*-* ""^ ""* ^"" CO

5 C- c

LU

< <A wj

HQO

<Q

Ul

QCO

in CO o u-) m o ,_

6 in in CD en m O)

ccLU

in

CO

CO CM t r" r»co'

°- OCO o= o

CC<LU

<a w»

I - >t- •"

CO1-

z3 _l o CM ,_ CM T_ in N.

< CM CD CO f» CM

ID CO r- co * *~ CD o"1-O c»

t- s <— T3Z a3 5

£ 1co"CO

> <u LU tf~ CO

P E O ^< a.

z<cc 1-

< Z O oto

cd CD

j2CM m

CMo>CM> 3 COO

2 (A </»

Ol a <ca

oCC

NSE

CENTER

roll

&

Timekee

Department

LUD-

1- O CO o o o O tot- 111 in en o en tn Ul COH o CO CM *~ *™ CM *~

LUCCtr

QCO

cm"M co'

(A

3o

LU >•

£ o-

UJ_l o CO T CO CM CO in

<1-o

CO CO CO CO a> r-- COo CDCm"cy»

CM CM mco"

<

O cflto

v) a)

1 °CD

C C2 ~> CD aCL z CO CD to

o?x o

COUJ-11-

CD

o>c

CO

cu

£In

CO

<>Q

<

u.

aCD

COCD

50-

CO

oCD

to

CD

oXCD

CC

<

O><

^0

aQ.a.

CJ

>£3

ocCD

a.

o> CD to

0. <3CO

5CO

cCD

XLU

o CD

oO z

"co .^

cCO o

ob ,_ CM to h- co o

o z o O o o o en

HPSOOh

wOS

PiwHWUwen

S3wP*Xw

I

CM

4J

•H

•H,C

W

3"8

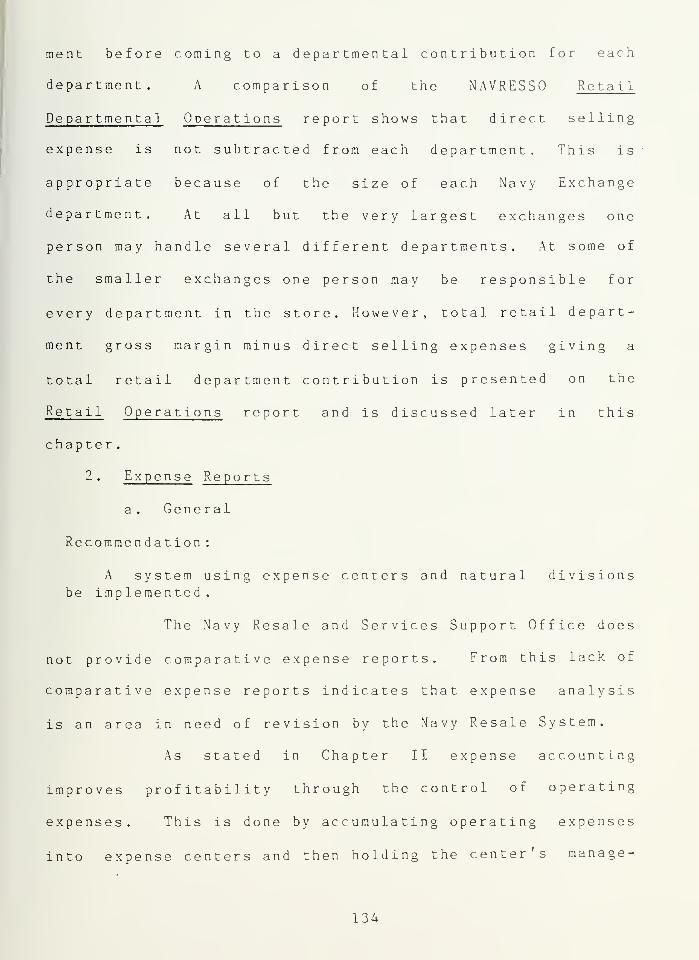

expenses and may be made for a single selling location or

aggregated for the firm as a whole.

The fourth expense report deals with expense center

productivity and is shown in Exhibit 2-7. This report

deals not only with expenses by natural division for an

expense center, but also with production measurement in the

form of productive hours consumed, average hourly production

pay rates, relative work loads, total dollars expended, and

other factors entering into the analysis of an expense

center. However, it must be understood that not all expense

centers can use productivity measurement techniques. For

example it would be difficult to establish a productivity

measurement for the Property and Equipment, the Company

Management , and the Sales Promotion expense centers, since

it would be difficult to define a transaction in relation to

these expense centers. However, it is easy to define trans-

actions in the Accounting and Management Information (bills

paid), Credit and Accounts Receivable (accounts collected),

and Personnel Expense Centers (personnel hired or trained).

The fifth expense report is used to establish a

flexible budget for an expense center and is illustrated in

Exhibit 2-8. As stated in the RAM, "The unit used to

measure the level of activity should be one which reflects

the work load of the expense center and which may be

measured relatively easily." The RAM goes on to stress the

39

I-cc

oQ.UJ

cc

>

OZ>Qoa.a.

0CUlI-zLU

oUJV)zUJaxUJ

acCOuto

P<j-

co»-to

O(J

PER UNITTRANS.

(16-4) 01 JUJ

ZUloUl(0Z

/oO COO UJO -Jp- <r*» o>

E u.

o £i

—

33 _)I /

a.Xui 6

z <o *

0-rX^h» j J

1 (

aoa

a.

UlLL

:W

2U.

zI

AS38§i5 <... a:

PX >LU CD

-1<O

m

"1

\* _\* ~7 /Ipj

-A (—o 1 z

3s Ar

. totr> i Q- LU3 1 D j

- j Y_.- i > -.o 1 < o

a. tt

o j /_

g^txSi ~

.]a /_\ \

a)

) V>

U(E

Q OoxITa.

tt lu nmSo -1tv J /

/ /-1 ,

o< 2 UJ

to 2- CO

<£>

]A /_UJ-j

6LU CE

c

_\ v^

is

,8 Ss « \\>Ea.

n§538

^ <

- / )

\ C-He!

<o §i

«•> \ \~) /^

-

<

>-

V)

5

z2a.

z<a.

3<

•t

3J<

LU

Oz<

<>

E<>

CO

2

z<EL

Z

Q.

<

<

U<

UJ

Oz<E<> \

DC<

(0

5

z<

Q.

z<

a< *

UJoz<X<>

QO£UJa.

-i

o o3

I

2

X

2

CO

o u-i-

Hp£

OPL,

WPi

fH

H

UP3OOPrf

Pu

P6j

WHZiwu

w

zwPL.

Xw

CM

HMPQHPC

Xw

40

cc

oEL

1.1

CC oK QUJ 3l- CD2UJ

HI1U m

111

COXin

ZL _j111 u.aXin

o o o iOCMr o CMm to

" to

o © o O oa o ^

CM^*

-UJa

-' (O

z <3 s> to

1-z>

OUJ

>oo oo

CD

oCO

1/1

(O

< <a "~ m"

o o o oo o CM CO ocj CO

u*>

oa o

oo o lO

atc

_• o ^"*~ *~

£X

a0) I

UJQ.

ILI

D > CC

z E c Y-o

UJ P| oO < Hinz Si

U_

Oooo Q

3

s oo o o

ijj

a.o a jj Jj

><UJ a.

> - UJCO2

o UJ

CM oo9)

a.X 8

CM 3 2m

aQa 8

CMo o

CMo

CO CO VUJ>

cc111

0-

ZO

D I<n

zoCO

X >5 CD

cs

E©CO

"co

co

ffl

UJ

z

<tr

<Z

CO

OU5

U

aCD

co

o

5VI

co

CDOc

Co

3<D

cCD

CI

c<D

E

dtr

O UJ-j cc c o s

CDXas1-

aa.DCO

U <a CD E «J CD CD D a<cc

z

oto

a:

O ma. 5 CO

c>(0

Eo c

CD

a.

3C

aOO a

3

UJ

UJ CO ^ 'O f- CD o> o CM n CO h-'J O o o o o o O o

HWoQPQ

WhJpa

HXWhJ

Pn

HpiOPhwPi

pi

wHzwcj

wCO

wX!wCO

I

CN

M«HPC

Xw

41

HCC

oEL l-UJ UJrx arr QIII 3r- 03

2 UJUJ -I

O CO

UJ XCO UJ7 _lUJ Li.

a.XUJ

o m IS) oo t

en co © i- og

Oo oo ooS o ai m CO< *~ *" CO *o"

oo in o in oz , P3 N.

-J<T> o

UJ«- co

Q i- o o O o<2

o a o o2 o so m CO< CO CO

CO

zUJ o o m in O n r*.

2 CJ OJ CO zCO (X> co co

t $z a3

r-*

1- o o o o5 o o o o5 so o CO

> < ri m*

>1- o d »_ CO COO o o o o z< d

COoen

coco

N." i-

2<

QO oo

Oo ooQ

o CO o CD

COO(X

dzoc

LUa ino m

CM

oo

•" en CO

Ccc

*" Ou,

ID-1 h- o o o o

Q. >2<

o o o o

B> LU

aD

<1-

UJ

o tN

cm"

E c Ouj _ E

<ogo

in O ma o

z - CM m

NSE

CENT

Payroll

ana

Depart

C llj

UJo

CMinen _j

UJ>LU—1

ZLU0.XUJ

in -i

orx

>-

2<

oooOoCM_

oocm"

oor*-

UJ i <X *r o o m in a. d

z»- CM Ml

UJ CM oen s CM

CMCMen

*n1-

2oo O

aOo

ooo o CM_

< *• " CM t"

o ._ CM *o o O o zoCO CO

OCM C\i

rx inO H o O o o(/> g o o oa u> 2 5 CM a CM

<0 I

< ^ -'cm' V

a>

Oz

- CM *r

3 cc

ZoGO

' atc —

o 3 «

CO>

"3

cC

3o

2qcxrx

o5o

Oo•D

ooin

u — <0 CD a> go < UJ ^X >

Q<rx

1-<Z

c cEB Oc O2 o

c

cc

ao

a

oocCO

CD

c c

Hi

<-JO.<CO

<

Kc-1

UJIT

zo

c y

- 9-— 33 CT

<D»C

CO

toJi

c

O1- z

Ocop o

5Q)

Q.o

CD

O

< O1- U 15

Uo a.

aa. oo > O

z co UJ O uj tx o < UJ UJ 3 a JZ "c

UI u. 3 u CO

u OD o • cm oCO GO 2 O

HWOQ&pa

wi-j

pai—

i

xw

HPi

OPi

wPi

Pi

wH2WCJ

WC/J

awPiXw

COI

pa

HS3Xw

42

importance of agreement on the budgeted level of productiv-

ity at each activity level between the individual setting

the budgeted amounts and the supervisor who must work within

those budgets.

The final expense report provided by the RAM, a

payroll and production summary, is depicted in Exhibit 2-9.

Payroll is normally the largest natural division expense in

every expense center and, therefore, deserves the extra

control. This report delves further into the area of pay-

roll than the expense center productivity report by dividing

the payroll into smaller periods of time, by delineating

planned requirements for executive, regular, and overtime

payroll and by giving statistics in the area of average wage

rates .

Besides the reports discussed above the RAM contends

that it is feasible to develop a supplemental system of

exception reports which will direct top management's atten-

tion directly to problem areas. As an example, a report

could be produced that lists those expense accounts that

have budget variances exceeding a certain percentage. [Ref.

3: pp. VIII 1-13] This could be problematic if the reports

are used as a means for evaluating a managers performance

[Ref. 4: pp. 109-113], If a manager's evaluation is based

strictly on his department's performance in regard to the

short term budget, he will tend to make sure his figures

look good in relation to the short term budget regardless of

43

>•

<

5(/>

Zo

OQoccQ.

QZ<-JJocc

<

. wr S

y] yi h- >-

sis o£ 1

.

t- O s s-J > y? 5 1

EE <« 1

>UJ

zu

aUJi-

<

>•CC

4 I"V) 5

z en

o eCO Is

Oz

"

a. o « t- >2 -i 5

a: S

5 H*Z

* *<0.

<3

u

J * o&5 f | >

6z

< o

a.IS c

! 5

,_

cc 6<> Uj

X UJCO

zo o

zcc s «

ccUJ Q.

CL""

2<

i3a

co

jj

ii cc UJ_j UJ

O UJ * o

z 5enUJ

o zUJ <

s 5OX9

3

•1 «€) «-1 > 3

<£

14.

2<z

Z3 Is

Z ^1- >

Q 3

§?a. x

< SI >

fc

3

U< o

£ >

, Q|*~ ,_

a S| c UJ

§*~

fc

O -< 2 Cfl

|o

3CCa.

23* cS SO 3

-I

<

3>

5UJzz

s

Sl O

<

oCC >

a. _l UJ-j

Oe

> Q. * Oo6

s U.

OUJ <

s5

><

Z £3

Ck<rt <a iu

.j z^tti Qg sUJa

UJ

2<zz a _,

ao I s

!s o!

<

-

02«:

aap

SBoHHaPpo05PL,

PSB<

-J

oOS

<u

o>I

og

HH«HPXw

44

the affect on long term profitability of the company. The

manager could do this either by manipulation of the records

or by making less cost effective decisions, such as putting

off needed repairs until money is available in the budget.

[Ref. 4: pp. 109-113]

4 . Branch Store Reporting

With the advent of multi-store operations many new

problems in retail accounting have become apparent when

attempting to evaluate the profitability of each store. The

proper charging of expenses is of major concern. In this

area it has become common to charge expenses directly incur-

red by a location to that location while all other expenses

are recorded initially as a central organization expense.

The central organization expenses are then assigned or allo-

cated to profit centers.

A sample branch store report can be seen in Exhibit

2-10. This report may be changed or altered slightly depend-

ing on management's information needs. However, it should

show the store's operating results for each month and year-

to-date. Besides those columns shown, many companies add a

column to show variances from the budget and last year.

Though comparisons to budget are usually considered realis-

tic and essential to the measurement of current performance

the same cannot be said for comparisons to last year. Allen

H. Seed III, in his article "Improving the Effectiveness of

45

HWSwH<HCO

Oss

5u

azt-<UJQ.

ozo

<oo-I

UJcr

oI-0)

_l<O>QZ

2 aE 2 a5 X a

' c o- c

<WP*o

oH

<CJ

o

wPi

oHCO

<!=

QH>Ho2

19 a>

a 5 c - a) 8

«i I 3a o o

2 - 3 8 0-

j. 2 * | Con o O n ^ i-o ioj a o

o oo o— IT)

en a.

o oo o

2*<" oto i-

= — 9

I

CM

H«H35

XW

46

Management Reports" [Ref. 5: p. 63], and Louis C.

Moscarello, in his book Retail Ac counting and Financial

Control [Ref. 6: p. 323], object to comparisons made to last

year. Each state that a comparison to previous years is

looking backward at times that may have been either excep-

tionally good or bad and is not consistent with the philoso-

phy of management by objectives.

5 . Executive Level Reporting

In the previous sections the discussion has been

concerned mainly with reports received by operating

managers. This section discusses senior executive level

reporting. As background to this discussion, the need for

planning on a seasonal, annual, and long-term basis is

emphasized .

a. Planning and Budgeting

Long-term goals, looking ahead three to five

years or more, should reflect where the firm is, where it

wants to go (its objectives), and what resources, including

funds, are needed to achieve the objectives. Seasonal and

annual plans must, in-turn, reflect the intent of the firm's

long-range objectives.

A prime objective for each firm is the profit

objective. Depending on the organization, this objective may

be simply to cover their cost of operation, such as for

nonprofit organizations similar to Goodwill Industries, or

to make. a profit which can be shared by the stockholders of

47

the company. To obtain this objective company- wide profit

plans must be established reflecting management's expecta-

tions for sales, gross margin, operating expenses, and other

income. From this company-wide profit plan detailed opera-

ting budgets must be prepared for each responsible location

whether it be a profit or expense center. Once the detailed

plans are established and agreement reached between senior

management and the levels of operating management (i.e.,

buyers, merchandise managers, and store managers), each

member of the management team then has a financial plan

which he or she is expected to follow. With the concept of

management by objectives and the above planning functions

installed as an integral part of a firm's method of opera-

tion, reports can be developed to provide top management

with the feedback necessary to perform their management

responsibilities. [Ref. 3: pp. X 1 - 2

]

b. Suggested Reporting Formats

The NRMA has suggested three reports for senior

executive level management though they stress that these

reports represent only one of several alternatives and that

the specific reports used will depend on management's speci-

fic needs and desires. The reports consist of a total

company balance sheet, a condensed income statement, and a

total company income and expense statement. The following

assumptions apply to each of the suggested reports:

48

1 . The firm has several selling locations.

2. The firm accounts for inventory investment by depart-ments so that gross merchandise margin can be deter-mined by department and by location.

3. The firm develops a written profit plan for eachfiscal period.

4. The firm is organized so that individual store mana-gers have responsibility for the direct and assignableoperating expenses of the store.

5. The firm uses the expense center summaries, expensecenters, and sub-expense centers as outlined in thismanual, providing sufficient expense center breakdownsto reflect executive responsibilities.

6. The firm uses flexible expense budgets.

(1) Total Company Balance Sheet . This report, as

shown in Exhibit 2-11, presents a summary of data with only

significant pieces of information or key figures that the

NRMA has considered to be necessary to management needs.

The information is compared with a plan and is shown in

trend format so that management can more easily spot prob-

lems. Finally all dollar amounts are rounded to the nearest

thousand dollars for easier reading with no degradation of

report quality.

(2) Condensed Income S tat emen t . The report

shown in Exhibit 2-12 presents a conventional company- wide

operating report prepared for management. It is an accumu-

lation of individual-selling- location income statements for

the current month and for the vear-to-date.

49

m <r i2 3

I-Ul111

Xto

111

o2<-I<CD

>z<a a5uO zU iii

J s< 2I- oc

O w

is

3

5

CO CN O CD

s ; s

3a.

o m to

» 5 ?momo o en•H- CO

<3 to

CO

03(0g cj> »-

0)

Qt.

<

U<

<s

5O 3

01 — COto to in

o o om (33 C33to m to

-l co co co CO CO CO

z

U<

Ifl-T <J3 —n a N

t- z°sa(J

z

5a.

O tn oi/3 lO CO

co in inin in m

<3

r-.

(09 03 K«i n nCM » *r

jj'j v m in m

Iaz

'/i

>z ?

at

g g m3 o cmCO CM in

O O U3co m cmO T to

in m m in in in

vi

z 3CO

— co egr-- *T CO•- V CM

c3'J

(J

X

uo<

o<

O O O —

5

«/3 m oS Ol OlO V oo m inCO CO COCO O) r-

a. O O — O O O

<3

01 N Oin »- -i-

CM CM CO

<— *" — —

X

5

5•n o oCM CM CO

to o O

E .2

5 o

c!a2C 3o 2

_ o- cc *3 »

HWWseCO

wa

<-J

<pa

<SoCJ

J<HOH

I

pai—

i

S3Xw

uj <u. 2

C3 Q. K £ u3 LU O O iu

< to O Z Q

50

E 2 < 2^> J1 -i

a a. i-3 <u o< (O O

coo

LUatxto

lil

(Jz<-J<

>2<a.

5Ou-I<I-

o

- O *- v m*"t T °>

1. 5en o ri pj

5°

isu

5 o» *- o> o to *-o w o> en cm en

a. C5 CM en en en

,

to m m cmto F<* »

uJ zQ ui

tO O* CM

J to" to' to' to'

3 s <o £2E2u > o m m O O in

o z O i- f- o f*- «r •

*°. °* *~- cm en mto. i to" to' N-* r-~ r--." n."

<3

ui m m m5<2 a|§5

|SSK w £

J <n"

K f«* f*t*> <*> <*>

m ci m m in mI

CO CO COu5 r*. — r*. h* r- h*Q a. ri *• en n rt rt

crt < o in <o(O N CO

_t — en CM 1— C3

< < •- *- *-" **

>-<a.

|

o cn m o in om en cm ^- r^ mO cm *-_ <n CD 91 O

X F- — »- "

j<

enin

cm in oto n co

X m r» coCO < <

H 2O

i ?a.

o o o in o mcm a> to en en cm

CD to r- co (O N CO

<

< to o> o inZ tf) 3 »- m w

Z U<

—

-

•- — en

E £CE

X

au3CC z o m in o m oU CM en CM m t cmO *- *- CM ^- m ^<

* i/> co r* oi>

to *f_ ^ m'i ri cj en en

a,

z

8 |q m oO r^ o O ^n mO CM o

J T *". *°. CM *- O< a en" en en

a B

a2

HWW3=en

Wu

<

<Ph

OCJ

<O

HI

«H

Xw

a 5 suj < a.u. 5 <

2 o

51

t-zIAJ

5UJt-<Hcfl

UJ

5OozQUJCOzLUQZoo

UJ

<Oo

X<>-

<_>1-

5111

OZ<K<>

C3Z>

'X<LU>r>

X

o3

UJQ.

X<

>

1LU

u<X<>

aa3X)

X<

:n

r

Total

Sales

Owned

Retail

Sales

Less,

Returns

&

Allowances

Net

Owned

Retail

Sales

Cost

of

Merchandise

Handled

Gross

Margin

•

Owned

Depts

Commissions

from

Leased

Depts.

Workroom

and

Other

Cost

of

Sales

Gross

Margin

Operating

Expenses

Operating

Income

(Loss)

Other

Income.

Net

Finance

Charge

Income

Sundry

Revenue

Interest

Income

Interest

Expense

Income

(Loss)

Belore

Taxes

Provisions

for

Taxes

Based

on

Income

Federal

Slate

and

Local

NET

INCOME

HZww

<Hen

w

oz

ow

zwGzoo

I

HHPQHSG

XW

52

(3) Total Compan y Income and Expense Stat ement .

Exhibit 2-13 illustrates several concepts of sound manage-

ment reporting. First, only significant elements of informa-

tion are presented to management for a quick, overall

picture of the operating results. Second, all amounts are

presented in trend format, as well as showing season-to-date

and year-to-date. Third, all amounts are compared to the

profit plan with variations to plan being highlighted.

Fourth, Return on Sales, Assets, and Equity are highlighted.

Finally, the five reasons for planned profits differing from

actual profits are highlighted. The reasons for differences

ar e :

1 . Volume Variance ((Actual Net Sales - Planned NetSales) X Planned Gross Margin Rate)

2. Rate Variance ((Actual G.M. - Planned G.M. Rate) X

Actual Net Sales)

3. Operating Expense Budget Adjustment (Total operatingexpense per profit plan minus total budgeted operatingexpense based on activity levels.)

4. Operating Expense Spending Variance (Total budgetedoperating expense based on actual activity levelsminus total actual operating expense.)

5. Net Other Income Variance (Variation between actualnet other income and planned net other income.) [Ref.3: pp. X6-7]

E. EFFECTIVE FINANCIAL MANAGEMENT REPORTS

As discussed in the introduction of this thesis the

following section will describe techniques for improving the

effectiveness of management accounting reports and

53

sis in ? 3*5 m h m iu m m

UJ

2UJt-<

UJ<f>

ZUJQ.XUJ

Qz<Ul

5OoZ>z<Q.

5Oo-I<I-o

i

ifa

S«!

1

1

2

s 5as

< 31 i3 i>

5^

*i

El

I?

??! fcfec

sis in

3SS jfc*

:ss a! =

315 SI!

?<« XXX

iJi 5**

K

5

J!

a

5

3

xX

8

3

s

§Sis

-5»

!'fell

Ifj

z • »si *

i<

1Hi

£

h • ••-

o!

IE <a

I^

ifi

-99

T. u

2S 1

1

Efi«

i 53i

aaa sis

I 3--.

<

a

i

I

5o

5*33; is;

C £= I§

Xo3

la99S kii

E| E 9

|li

"32 IIS

i

i!« €

f

3

3o

I!

>a; :~s

= Ra

I

3

i? 112 ssi?

Ssj

H "«S

lI!

S36 iii

iC

|« ss

5

9

s

s

5

I

i

j

If

!

HWswH<HWwwzwCMXwQZ<wgouzM

z<P-.

soo

<HOHenH

i

CN

E-H«H»XW

III 15* 3a§ is? |iilS iJS I5S Sal 1,

54

weaknesses which should be avoided in management accounting

reports:

1 . Improving the Effectiveness of Management Reports

Allen H. Seed III, in his article "Improving the

Effectiveness of Management Reports", presented the follow-

ing categories and techniques to improve the effectiveness

of management reports:

a. Report Content

Attention should be focused on key control-

lable items on which the concerned executive can affect

change .

"" Actual results should be compared with plan,

budget or standard to evaluate information in relation to

objectives .

":;" Significant ratios and unit costs should be

included on reports so that quantitative results may be

related to activity levels.

* Trends should be emphasized for planning

purposes in order that unfavorable trends may be controlled

and so that benefit may be gained from favorable trends.