an analysis of industrial infill development

TRANSCRIPT

An Analysis of Industrial Infill

Development

Marty Busekrus, HFF

Ed Harrington, CenterPoint Properties

Cathy Thuringer, Trammell Crow

Marty Busekrus

• Director with HFF focusing on the industrial

capital markets throughout the Southeastern

U.S.

• Responsible for sourcing industrial opportunities

by partnering owners with potential capital

sources for joint ventures, debt solutions and/or

buyers.

• Prior to joining HFF, Busekrus was a senior

associate in CBRE’s Private Capital Group and

focused on the dispositions of office and

industrial projects throughout Southeast Florida.

HFF

Give Us Your Feedback for this Session!

• Session evaluations are available on your chair. Please take a moment at the end of this session to provide your feedback on the content and speakers.

• Evaluations can be handed in to a NAIOP staff member at the back of the room.

Thank you!

An Analysis of Industrial Infill

Development

Marty Busekrus, HFF

Ed Harrington, CenterPoint Properties

Cathy Thuringer, Trammell Crow

Ed Harrington

• Joined CenterPoint Properties Trust in 1999 and currently oversees the development of logistically located facilities and industrial parks for CenterPoint Properties.

• Has overseen the development of new industrial business parks and manufacturing and distribution facilities. He has spent more than 18 years developing industrial commercial real estate.

• In addition, he worked for several years as a civil engineer with local Chicago engineering firms.

CenterPoint Properties

Cathy Thuringer

Trammell Crow

• Principal with Trammell Crow Company

• Has comprehensive management responsibility for development projects, commencing with initial site acquisition through ultimate project disposition.

• Oversees all aspects of industrial developments primarily in central and southern Arizona.

• Project profiles range from multi-phased business park infrastructure to single and multi-story speculative and build-to-suit office and industrial facilities.

DEFINING INFILL INDUSTRIAL

Industry veterans define it as…

• “Any area that has limited sites for new development without having to tear down existing

real estate.”

• “A mature industrial submarket with a total developable land inventory comprising less than

10-15% of the existing base, where land assemblages are a typical requirement and

redevelopment of existing buildings is common.”

• “Submarket representing an extremely dense collection of industrial buildings with very high

barriers to entry, while also characterized as being proximate to large population centers. “

• “Location that benefits from a dense surrounding population and is well positioned to major

thoroughfares.”

• “Potential development sites located within a heavily populated area that is fully built out with

different asset classes. Caused by restrictive zoning which pushes development out of

certain areas with more open land areas.”

Panelists collective definition

“Infill Industrial projects are new developments that are situated in

built-up, established, mature infrastructure areas constrained by

geographical or, political challenges whereby new supply can not be

added in a reasonable timeframe to meet increases in demand.

Tenants are largely focused on last mile delivery and driven by local

population or employment base vs. cost”

Examples of Infill & Greenfield Markets

• Northern New Jersey

• Los Angeles

• South Florida

• Chicago (O’Hare submarket)

• Atlanta (inner loop)

• Inland Empire

• Orlando

• Chicago (I-55 corridor)

• St. Louis

• Atlanta (outside of 285)

WHO ARE THE TENANTS?

• Types of users for infill space

• Locational drivers for infill tenants

• Buildout requirements for infill versus greenfield

MAXIMIZING COVERAGE

• Difference in FAR between infill and greenfield

• Considerations and challenges for maximizing coverage

• Potential for two-story industrial

CAPITAL MARKETS VIEW

• Differences in underwriting approach for infill versus greenfield• Rental rates / rental rate growth

• Downtime assumptions

• Cap rates / overall returns

• Portfolio diversification as it relates to:• Occupancy

• Rental rates

• Liquidity

• Competition

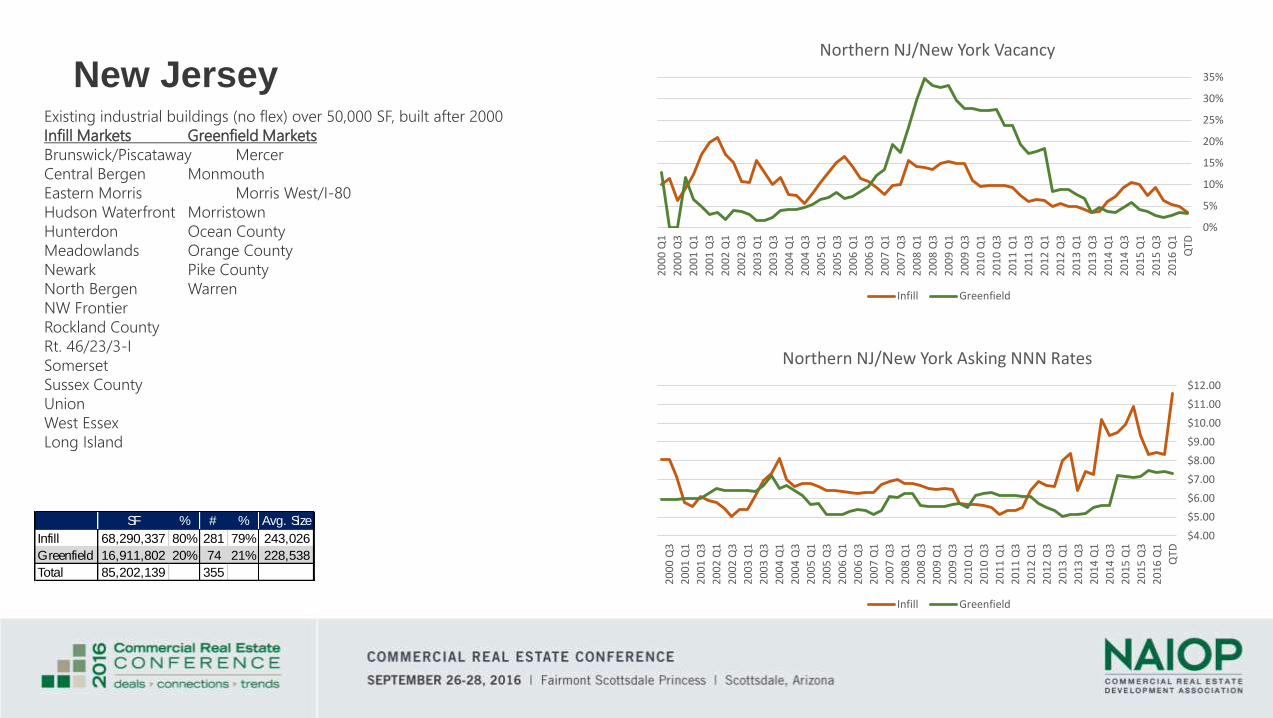

New Jersey

SF % # % Avg. Size

Infill 68,290,337 80% 281 79% 243,026

Greenfield 16,911,802 20% 74 21% 228,538

Total 85,202,139 355

Existing industrial buildings (no flex) over 50,000 SF, built after 2000

Infill Markets Greenfield Markets

Brunswick/Piscataway Mercer

Central Bergen Monmouth

Eastern Morris Morris West/I-80

Hudson Waterfront Morristown

Hunterdon Ocean County

Meadowlands Orange County

Newark Pike County

North Bergen Warren

NW Frontier

Rockland County

Rt. 46/23/3-I

Somerset

Sussex County

Union

West Essex

Long Island

0%

5%

10%

15%

20%

25%

30%

35%

QTD

20

16

Q1

20

15

Q3

20

15

Q1

20

14

Q3

20

14

Q1

20

13

Q3

20

13

Q1

20

12

Q3

20

12

Q1

20

11

Q3

20

11

Q1

20

10

Q3

20

10

Q1

20

09

Q3

20

09

Q1

20

08

Q3

20

08

Q1

20

07

Q3

20

07

Q1

20

06

Q3

20

06

Q1

20

05

Q3

20

05

Q1

20

04

Q3

20

04

Q1

20

03

Q3

20

03

Q1

20

02

Q3

20

02

Q1

20

01

Q3

20

01

Q1

20

00

Q3

20

00

Q1

Northern NJ/New York Vacancy

Infill Greenfield

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

$10.00

$11.00

$12.00

QTD

20

16

Q1

20

15

Q3

20

15

Q1

20

14

Q3

20

14

Q1

20

13

Q3

20

13

Q1

20

12

Q3

20

12

Q1

20

11

Q3

20

11

Q1

20

10

Q3

20

10

Q1

20

09

Q3

20

09

Q1

20

08

Q3

20

08

Q1

20

07

Q3

20

07

Q1

20

06

Q3

20

06

Q1

20

05

Q3

20

05

Q1

20

04

Q3

20

04

Q1

20

03

Q3

20

03

Q1

20

02

Q3

20

02

Q1

20

01

Q3

20

01

Q1

20

00

Q3

Northern NJ/New York Asking NNN Rates

Infill Greenfield

Chicago

Existing industrial buildings (no flex) over 50,000 SF, built after 2000

Infill Markets Greenfield Markets

North Chicago Indiana

North Cook Lake County

NW Cook Kenosha

O’Hare McHenry

South Chicago North Kane/I-90

Near SW Suburbs South Suburban

North I-55 Joliet

West Cook South I-55

North DuPage Central Kane/DuPage

West Suburbs I-88 West

SF % # % Avg. Size

Infill 40,441,386 21% 236 30% 171,362

Greenfield 150,354,411 79% 556 70% 270,422

Total 190,795,797 792 240,904

0%

5%

10%

15%

20%

25%

30%

QTD

20

16

Q1

20

15

Q3

20

15

Q1

20

14

Q3

20

14

Q1

20

13

Q3

20

13

Q1

20

12

Q3

20

12

Q1

20

11

Q3

20

11

Q1

20

10

Q3

20

10

Q1

20

09

Q3

20

09

Q1

20

08

Q3

20

08

Q1

20

07

Q3

20

07

Q1

20

06

Q3

20

06

Q1

20

05

Q3

20

05

Q1

20

04

Q3

20

04

Q1

20

03

Q3

20

03

Q1

20

02

Q3

20

02

Q1

20

01

Q3

20

01

Q1

20

00

Q3

20

00

Q1

Chicago Vacancy

Infill Greenfield

$3.00

$3.50

$4.00

$4.50

$5.00

$5.50

$6.00

$6.50

$7.00

QTD

20

16

Q1

20

15

Q3

20

15

Q1

20

14

Q3

20

14

Q1

20

13

Q3

20

13

Q1

20

12

Q3

20

12

Q1

20

11

Q3

20

11

Q1

20

10

Q3

20

10

Q1

20

09

Q3

20

09

Q1

20

08

Q3

20

08

Q1

20

07

Q3

20

07

Q1

20

06

Q3

20

06

Q1

20

05

Q3

20

05

Q1

20

04

Q3

20

04

Q1

20

03

Q3

20

03

Q1

20

02

Q3

20

02

Q1

20

01

Q3

20

01

Q1

20

00

Q3

20

00

Q1

Chicago Asking NNN Rates

Infill Greenfield

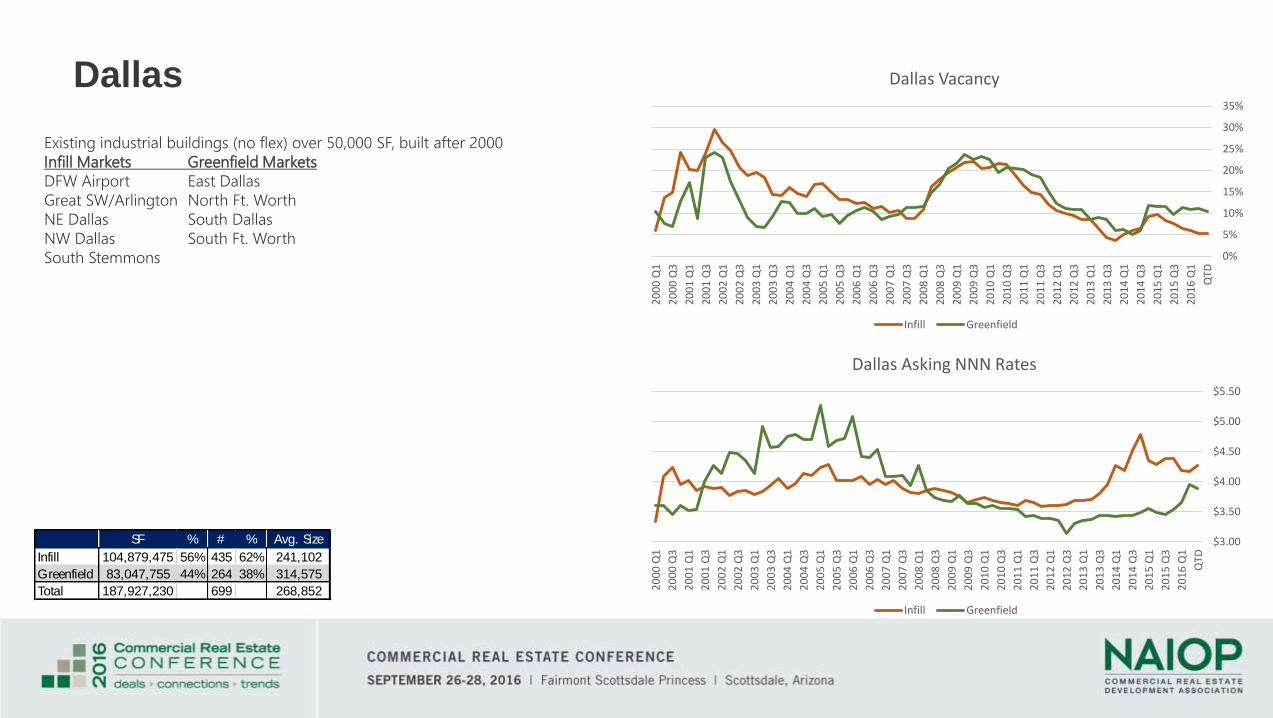

Dallas

SF % # % Avg. Size

Infill 104,879,475 56% 435 62% 241,102

Greenfield 83,047,755 44% 264 38% 314,575

Total 187,927,230 699 268,852

Existing industrial buildings (no flex) over 50,000 SF, built after 2000

Infill Markets Greenfield Markets

DFW Airport East Dallas

Great SW/Arlington North Ft. Worth

NE Dallas South Dallas

NW Dallas South Ft. Worth

South Stemmons 0%

5%

10%

15%

20%

25%

30%

35%

QTD

20

16

Q1

20

15

Q3

20

15

Q1

20

14

Q3

20

14

Q1

20

13

Q3

20

13

Q1

20

12

Q3

20

12

Q1

20

11

Q3

20

11

Q1

20

10

Q3

20

10

Q1

20

09

Q3

20

09

Q1

20

08

Q3

20

08

Q1

20

07

Q3

20

07

Q1

20

06

Q3

20

06

Q1

20

05

Q3

20

05

Q1

20

04

Q3

20

04

Q1

20

03

Q3

20

03

Q1

20

02

Q3

20

02

Q1

20

01

Q3

20

01

Q1

20

00

Q3

20

00

Q1

Dallas Vacancy

Infill Greenfield

$3.00

$3.50

$4.00

$4.50

$5.00

$5.50

QTD

20

16

Q1

20

15

Q3

20

15

Q1

20

14

Q3

20

14

Q1

20

13

Q3

20

13

Q1

20

12

Q3

20

12

Q1

20

11

Q3

20

11

Q1

20

10

Q3

20

10

Q1

20

09

Q3

20

09

Q1

20

08

Q3

20

08

Q1

20

07

Q3

20

07

Q1

20

06

Q3

20

06

Q1

20

05

Q3

20

05

Q1

20

04

Q3

20

04

Q1

20

03

Q3

20

03

Q1

20

02

Q3

20

02

Q1

20

01

Q3

20

01

Q1

20

00

Q3

20

00

Q1

Dallas Asking NNN Rates

Infill Greenfield

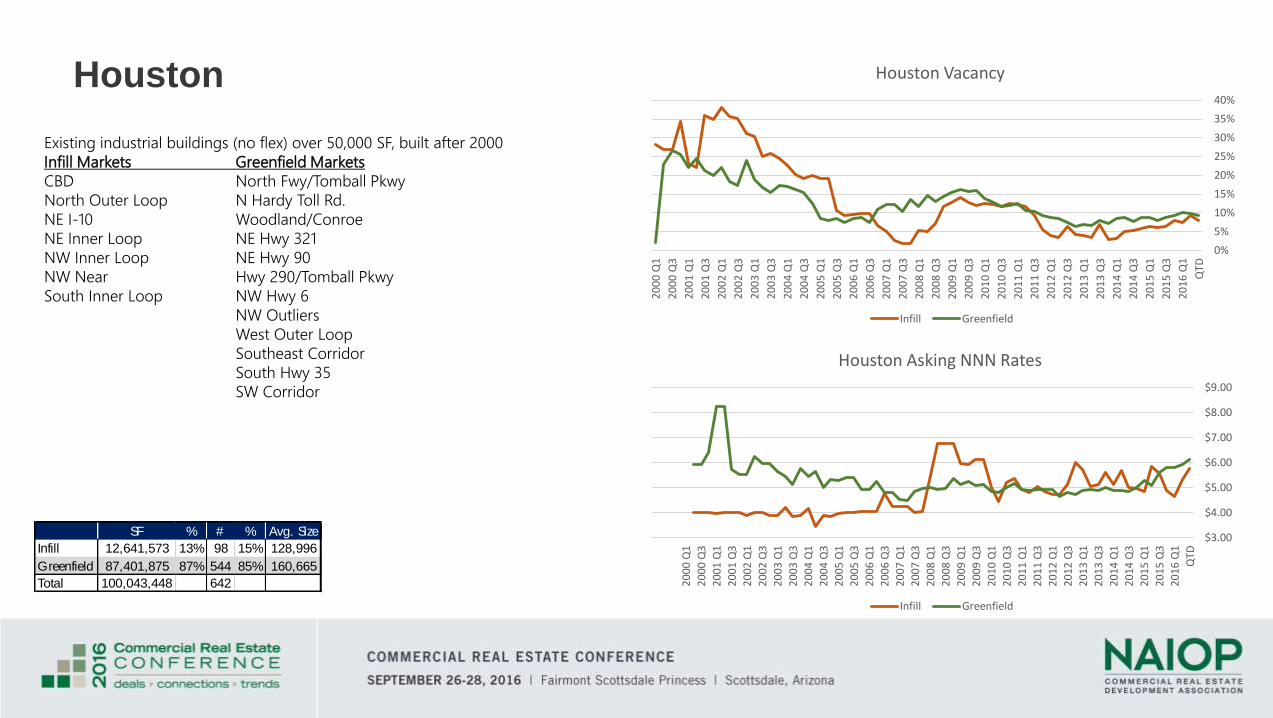

Houston

Existing industrial buildings (no flex) over 50,000 SF, built after 2000

Infill Markets Greenfield Markets

CBD North Fwy/Tomball Pkwy

North Outer Loop N Hardy Toll Rd.

NE I-10 Woodland/Conroe

NE Inner Loop NE Hwy 321

NW Inner Loop NE Hwy 90

NW Near Hwy 290/Tomball Pkwy

South Inner Loop NW Hwy 6

NW Outliers

West Outer Loop

Southeast Corridor

South Hwy 35

SW Corridor

SF % # % Avg. Size

Infill 12,641,573 13% 98 15% 128,996

Greenfield 87,401,875 87% 544 85% 160,665

Total 100,043,448 642

0%

5%

10%

15%

20%

25%

30%

35%

40%

QTD

20

16

Q1

20

15

Q3

20

15

Q1

20

14

Q3

20

14

Q1

20

13

Q3

20

13

Q1

20

12

Q3

20

12

Q1

20

11

Q3

20

11

Q1

20

10

Q3

20

10

Q1

20

09

Q3

20

09

Q1

20

08

Q3

20

08

Q1

20

07

Q3

20

07

Q1

20

06

Q3

20

06

Q1

20

05

Q3

20

05

Q1

20

04

Q3

20

04

Q1

20

03

Q3

20

03

Q1

20

02

Q3

20

02

Q1

20

01

Q3

20

01

Q1

20

00

Q3

20

00

Q1

Houston Vacancy

Infill Greenfield

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

QTD

20

16

Q1

20

15

Q3

20

15

Q1

20

14

Q3

20

14

Q1

20

13

Q3

20

13

Q1

20

12

Q3

20

12

Q1

20

11

Q3

20

11

Q1

20

10

Q3

20

10

Q1

20

09

Q3

20

09

Q1

20

08

Q3

20

08

Q1

20

07

Q3

20

07

Q1

20

06

Q3

20

06

Q1

20

05

Q3

20

05

Q1

20

04

Q3

20

04

Q1

20

03

Q3

20

03

Q1

20

02

Q3

20

02

Q1

20

01

Q3

20

01

Q1

20

00

Q3

20

00

Q1

Houston Asking NNN Rates

Infill Greenfield

Southern CA

Existing industrial buildings (no flex) over 50,000 SF, built after 2000

Infill Markets Greenfield Markets

Carson/Rancho Domingz Antelope Valley

Central LA Conejo Valley

Commerce Area SCV/Lancaster/Palmdale

Eastern SGV Inland Empire East

El Segundo

Gardena/110 Corridor

Long Beach

Lower SGV

Lynwoo/Paramount

Mid-Counties LA

Northwest SGV

SFV East

SFV West

Southwest SGV

Torrance

Upper SGV

Ventura County

Vernon

Inland Empire West

Orange County (all) $3.00$3.50

$4.00

$4.50

$5.00

$5.50

$6.00

$6.50

$7.00

$7.50

$8.00

QTD

20

16

Q1

20

15

Q3

20

15

Q1

20

14

Q3

20

14

Q1

20

13

Q3

20

13

Q1

20

12

Q3

20

12

Q1

20

11

Q3

20

11

Q1

20

10

Q3

20

10

Q1

20

09

Q3

20

09

Q1

20

08

Q3

20

08

Q1

20

07

Q3

20

07

Q1

20

06

Q3

20

06

Q1

20

05

Q3

20

05

Q1

20

04

Q3

20

04

Q1

20

03

Q3

20

03

Q1

20

02

Q3

20

02

Q1

20

01

Q3

20

01

Q1

20

00

Q3

20

00

Q1

Southern CA Asking NNN Rates

Infill Greenfield

0%

5%

10%

15%

20%

25%

30%

35%

QTD

20

16

Q1

20

15

Q3

20

15

Q1

20

14

Q3

20

14

Q1

20

13

Q3

20

13

Q1

20

12

Q3

20

12

Q1

20

11

Q3

20

11

Q1

20

10

Q3

20

10

Q1

20

09

Q3

20

09

Q1

20

08

Q3

20

08

Q1

20

07

Q3

20

07

Q1

20

06

Q3

20

06

Q1

20

05

Q3

20

05

Q1

20

04

Q3

20

04

Q1

20

03

Q3

20

03

Q1

20

02

Q3

20

02

Q1

20

01

Q3

20

01

Q1

20

00

Q3

20

00

Q1

Southern CA Vacancy

Infill Greenfield

SF % # % Avg. Size

Infill 184,914,784 56% 959 67% 192,820

Greenfield 143,118,898 44% 466 33% 307,122

Total 328,033,682 1,425 230,199

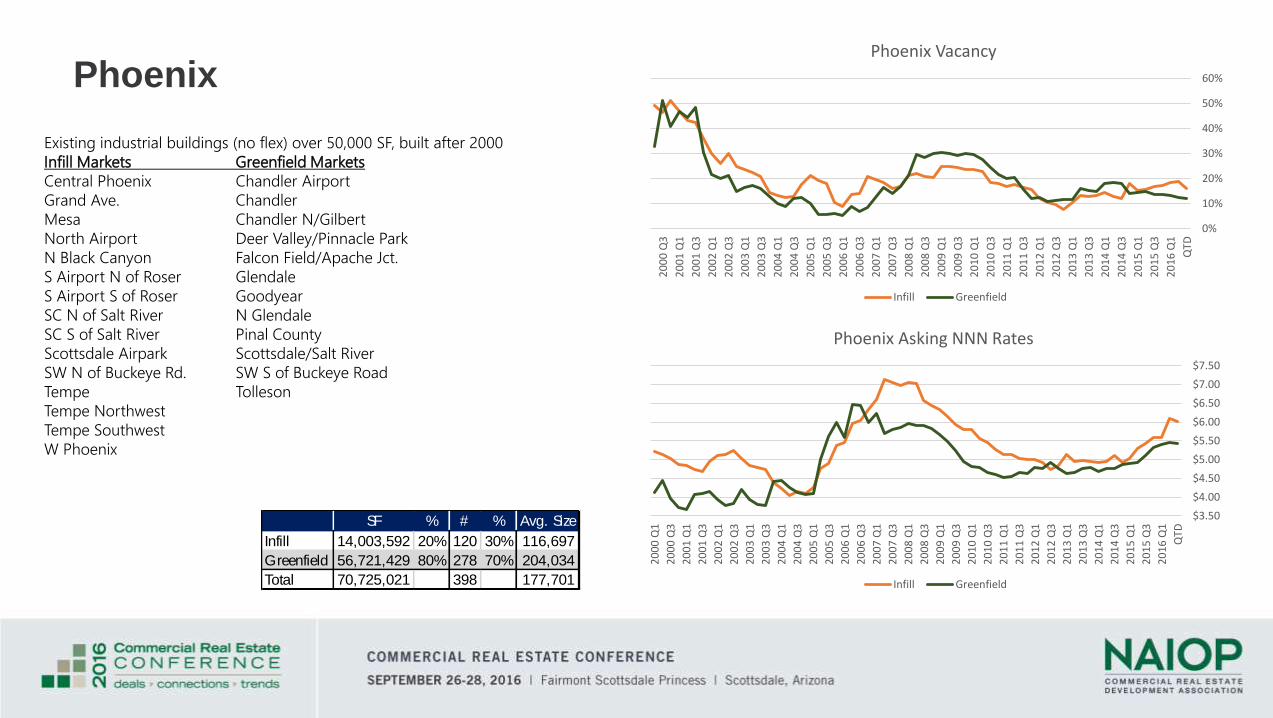

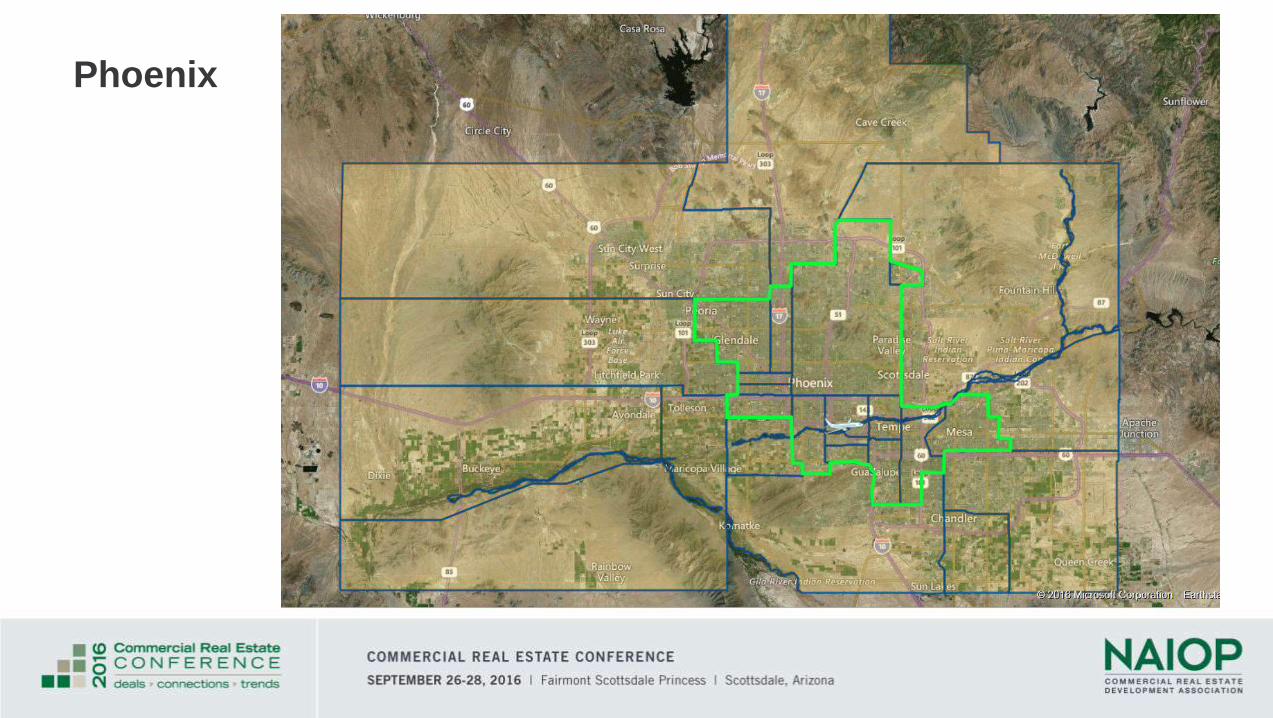

Phoenix

Existing industrial buildings (no flex) over 50,000 SF, built after 2000

Infill Markets Greenfield Markets

Central Phoenix Chandler Airport

Grand Ave. Chandler

Mesa Chandler N/Gilbert

North Airport Deer Valley/Pinnacle Park

N Black Canyon Falcon Field/Apache Jct.

S Airport N of Roser Glendale

S Airport S of Roser Goodyear

SC N of Salt River N Glendale

SC S of Salt River Pinal County

Scottsdale Airpark Scottsdale/Salt River

SW N of Buckeye Rd. SW S of Buckeye Road

Tempe Tolleson

Tempe Northwest

Tempe Southwest

W Phoenix

SF % # % Avg. Size

Infill 14,003,592 20% 120 30% 116,697

Greenfield 56,721,429 80% 278 70% 204,034

Total 70,725,021 398 177,701

0%

10%

20%

30%

40%

50%

60%

QTD

20

16

Q1

20

15

Q3

20

15

Q1

20

14

Q3

20

14

Q1

20

13

Q3

20

13

Q1

20

12

Q3

20

12

Q1

20

11

Q3

20

11

Q1

20

10

Q3

20

10

Q1

20

09

Q3

20

09

Q1

20

08

Q3

20

08

Q1

20

07

Q3

20

07

Q1

20

06

Q3

20

06

Q1

20

05

Q3

20

05

Q1

20

04

Q3

20

04

Q1

20

03

Q3

20

03

Q1

20

02

Q3

20

02

Q1

20

01

Q3

20

01

Q1

20

00

Q3

Phoenix Vacancy

Infill Greenfield

$3.50

$4.00

$4.50

$5.00

$5.50

$6.00

$6.50

$7.00

$7.50

QTD

20

16

Q1

20

15

Q3

20

15

Q1

20

14

Q3

20

14

Q1

20

13

Q3

20

13

Q1

20

12

Q3

20

12

Q1

20

11

Q3

20

11

Q1

20

10

Q3

20

10

Q1

20

09

Q3

20

09

Q1

20

08

Q3

20

08

Q1

20

07

Q3

20

07

Q1

20

06

Q3

20

06

Q1

20

05

Q3

20

05

Q1

20

04

Q3

20

04

Q1

20

03

Q3

20

03

Q1

20

02

Q3

20

02

Q1

20

01

Q3

20

01

Q1

20

00

Q3

20

00

Q1

Phoenix Asking NNN Rates

Infill Greenfield

Phoenix

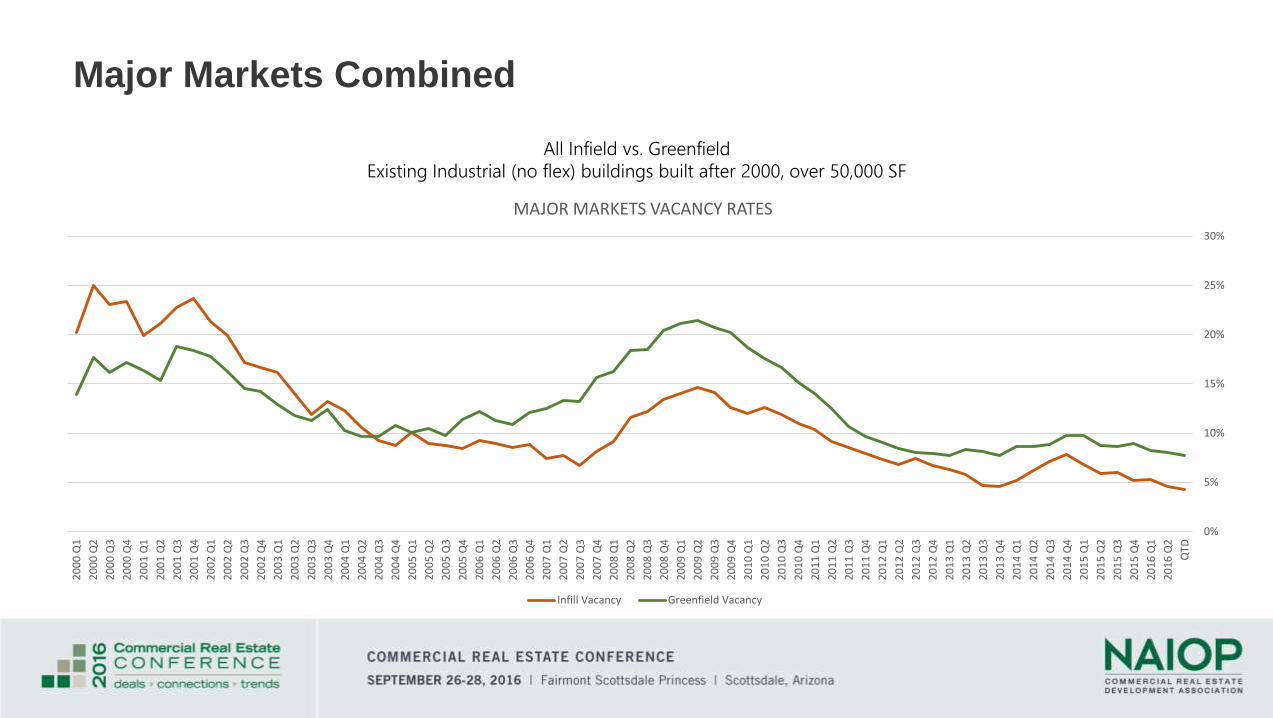

Major Markets Combined

All Infield vs. Greenfield

Existing Industrial (no flex) buildings built after 2000, over 50,000 SF

0%

5%

10%

15%

20%

25%

30%

QTD

20

16

Q2

20

16

Q1

20

15

Q4

20

15

Q3

20

15

Q2

20

15

Q1

20

14

Q4

20

14

Q3

20

14

Q2

20

14

Q1

20

13

Q4

20

13

Q3

20

13

Q2

20

13

Q1

20

12

Q4

20

12

Q3

20

12

Q2

20

12

Q1

20

11

Q4

20

11

Q3

20

11

Q2

20

11

Q1

20

10

Q4

20

10

Q3

20

10

Q2

20

10

Q1

20

09

Q4

20

09

Q3

20

09

Q2

20

09

Q1

20

08

Q4

20

08

Q3

20

08

Q2

20

08

Q1

20

07

Q4

20

07

Q3

20

07

Q2

20

07

Q1

20

06

Q4

20

06

Q3

20

06

Q2

20

06

Q1

20

05

Q4

20

05

Q3

20

05

Q2

20

05

Q1

20

04

Q4

20

04

Q3

20

04

Q2

20

04

Q1

20

03

Q4

20

03

Q3

20

03

Q2

20

03

Q1

20

02

Q4

20

02

Q3

20

02

Q2

20

02

Q1

20

01

Q4

20

01

Q3

20

01

Q2

20

01

Q1

20

00

Q4

20

00

Q3

20

00

Q2

20

00

Q1

MAJOR MARKETS VACANCY RATES

Infill Vacancy Greenfield Vacancy

QUESTIONS?

Give Us Your Feedback for this Session!

• Session evaluations are available on your chair. Please take a moment at the end of this session to provide your feedback on the content and speakers.

• Evaluations can be handed in to a NAIOP staff member at the back of the room.

Thank you!