an analysis of basic investment strategies: buy-and-hold

TRANSCRIPT

University of Central Florida University of Central Florida

STARS STARS

Retrospective Theses and Dissertations

Summer 1982

An Analysis of Basic Investment Strategies: Buy-And-Hold and An Analysis of Basic Investment Strategies: Buy-And-Hold and

Market Timing Market Timing

David L. Hansen University of Central Florida

Part of the Business Commons

Find similar works at: https://stars.library.ucf.edu/rtd

University of Central Florida Libraries http://library.ucf.edu

This Masters Thesis (Open Access) is brought to you for free and open access by STARS. It has been accepted for

inclusion in Retrospective Theses and Dissertations by an authorized administrator of STARS. For more information,

please contact [email protected].

STARS Citation STARS Citation Hansen, David L., "An Analysis of Basic Investment Strategies: Buy-And-Hold and Market Timing" (1982). Retrospective Theses and Dissertations. 630. https://stars.library.ucf.edu/rtd/630

AN ANALYSIS OF BASIC INVESTMENT STRATEGIES: BUY-AND-HOLD AND MARKET TIMING

BY

DAVID LUDWIG HANSEN B.A., Yale University, 1961

MB.A., Harvard University, 1966

THESIS

Subffiitted in partial fulfillment of the requirements for the Master of Arts degree in Applied Economics

in the Graduate Studies Program of the College of Business Administration

University of Central Florida Orlando, Florida

Summer Term 1982

TABLE OF CONTENTS

Chapter I. DEVELOPMENT OF THE STUDY . . . . . 1

II. METHODOLOGY . . . . . . . . . . . . • • 12

III. FINDINGS • • • . . • 16

IV. CONCLUSIONS . . .. . • 37

SELECTED BIBLIOGRAPHY • 39

LIST OF TABLES

1. Results of a Buy-and-Hold Strategy, Initial Investment of $10,000 . . . . . . . . . . . 18

2. Results of Market Timing Strategy #1, Initial Investment of $10,000, Base Period • . . . . . 19

3. Results of Market Timing Strategy #1, Initial Investment of $10,000, Test Period . . . . . . 20

4. Results of Market Timing Strategy #2, Initial Investment of $10,000 ••••.•.•.•..• 21

5. Results of a Buy-and-Hold Strategy, Monthly Investment of $100 • • • . • . • • . . • . 22

6. Results of Market Timing Strategy #1, Monthly Investment of $100, Base Period •••••• 23

7. Results of Market Timing Strategy #1, Monthly Investment of $100, Test Period •••.•••. 24

-

8. Results of Market Timing Strategy #2, Monthly Investment of $100 • . . . . . . • .

9. Analysis of Market Timing Strategy #l . 10. Analysis of Market Timing Strategy #2 • . . 11. Results of Combined Buy-and-Hold and Market

Timing Strategy #1, Initial Investment of

. 25

. 27

. . . 28

$10,000 •••••••••••••••.•••. 30

12. Results of Combined Buy-and-Hold and Market Timing Strategy #1, Monthly Investment of $100 • • • • • • • • • • • • • • • • • • . • • 31

13. Results of Combined Buy-and-Hold and Market Timing Strategy #2, Initial Investment of $10,000 •••••••••••••••••••• 33

14. Results of Combined Buy-and-Hold and Market Timing Strategy #2, Monthly Investment of $100 • • • • • • • • • • • • • • • • • • • 34

15. Analysis of Risk and Return •••••• • • • 36

CHAPTER I

DEVELOPMENT OF THE STUDY

There are probably as many investment strategies as

there are investors. The one thread common to most of them

is that they do not work. Numerous studies have shown that,

on average, professional investment managers cannot out

perform the market (Rolo 1982). When fees are taken into

consideration, these professionals underperform the market.

The results of the majority of professional

investment managers are part of the public record and lend

themselves to objective analysis. No such accumulation of

data is available to measure the success or failure of the

amateur investor. Yet, few have even advanced the theory

that the amateur can do as well as the professional.

The random walk hypothesis provides a partial

explantion of the above observations. It holds that

movements of stock prices are not predictable, as they are

independent of previous changes. These early studies tend

to destroy the technical theory approach, as it is based

on the exact opposite hypothesis - that stock and

commodity prices are predictable on the basis of past

experience.

2

The narrow form of the random walk hypothesis has

been stated as follows (Malkiel 1973):

The history of stock-price movements contains no useful information that will enable an investor consistently to outperform a buy-and-hold strategy in managing a portfolio.

The broad form of the random walk hypothesis has

been summarized by Professor Samuelson (Malkiel 1973):

If intelligent people are constantly shopping around for good value, selling those stocks they think will turn out to be overvalued and buying those they expect are now undervalued, the result of this action by intelligent investors will be to have existing stock prices already have discounted in them an allowance for their future prospects. Hence, to the passive investor, who does not himself search out for under- and overvalued situations, there will be presented a pattern of stock prices that makes one stock about as good or bad a buy as another. To that passive investor, chance alone would be as good a method of selection as anything else.

-The broad form of the random walk hypothesis is

similiar to the efficient capital market theory.

Efficient capital market theory builds on the random walk

hypothesis and labels all security analysis as useless in

predicting future stock prices. It maintains that all

information is known to the investing public so that

existing prices relect everything that is predictable or

anticipated. If the market has already discounted the

future, there is not much room for even the superior

analyst to beat the market. Thus, fundamental analysis

is no more helpful than technical analysis in an

investment strategy.

3

The efficient capital markets theory is based on

several important premises (Reilly 1979):

An initial, and very important, premise of an efficient market is that there are a large number of profit maximizing participants concerned with . the analysis and valuation of securities and operating independently of each other. A second assumption is that new information regarding securities comes to the market in a random fashion and the announcements over time are generally independent from one another. The third assumption of an efficient market is especially crucial. Investors adjust security prices rapidly to reflect the effect of new information. While the price adjustment is not always perfect, it is unbiased • • • the combined effect of (1) information coming in a random, independent fashion, and (2) numerous investors who adjust stock prices rapidly to reflect this new information is that price changes are independent and random.

Finally, because security prices adjust to all new information and, therefore, supposedly reflect all public information at any point in time, the security prices that prevail at any point in time should be an unbiased reflection of all currently available information. Based upon the foregoing discussion, an efficient market is one in which security prices fully reflect all available information including the risk involved. Therefore, the returns implicit in the price reflect the risk involved, so the expected return is consistent with risk.

A strategy of investing in an index fund that

reflects the Standard & Poor's 500 is supported by the

efficient capital market hypothesis. A simple buy-and-

hold policy is dictated since market movement is not

considered predictable.

Modern portfolio theory is a further refinement

of the efficient capital market hypothesis. It relies

on two basic assumptions: 1) that any investor wishes

4

to maximize the returns from his investment; and 2) that

investors are basically risk averse, which means simply

that, given a choice between two assets with equal rates

of return, an investor will select the asset with the

lower level of risk (Reilly 1979).

The portfolio model requires i .nvestors to

quantify their risk variable. The purpose of the model

is to derive the expected rate of return and an expected

risk measure for a portfolio. The variance of the rate

of return is a meaningful measure of risk. The variance

or standard deviation of expected returns is a statistical

measure of the dispersion of .returns around the expected

value. The greater the dispersion, the gr~ater the degree

of uncertainty surrounding future r~turns (Markowitz 1952).

Markowitz showed the importance of diversification

for reducing risk by relating expected return for an

individual asset to expected return for a portfolio of

assets. He went on to develop the efficient frontier

concept which relates risk to return for a number of

alternative portfolios. Those portfolios that show the

gr~atest return for each alternative level of risk appear

on the efficient frontier. The investor can select the

optimum portfolio consistent with his individual risk

preference.

Given the efficient market hypothesis, the

5

investor must wonder if there is an investment strategy

that, adusted for . risk, consistently outperforms the

market. The majority of investors must believe that there

is .or they would not bother to pour time and money into

research. Ironically, if investors stopped trying to beat

the market and research was discontinued, the market would

no longer be efficient.

Four basic approaches have been cited as working

effectively for some investors over an extended period of

time. These investors have apparently indentified and

capitalized on an inefficient sector of the market.

The first of these is the bargain hunting strategy.

This was formalized and followed successfully by Benjamin

Graham, the father of fundamental security analysis.

Graham made a fortune by applying rigorous standards and

buying sharply undervalued stocks (Train 1980).

The second strategy involves growth investing,

locating small high-growth companies before they have been

discovered by the market. T. Rowe Price with his Growth

Stock Fund and Warren Buffett are prime examples of the

successful application of this approach. The Templeton

Growth Fund capitalized on a combination of growth

investing and bargain hunting to earn a phenomenal return

(Train 1980).

The contrarian investment strategy involves

6

bargain hunting of a sort. Its main advocate, David

Dreman .(.1979), achieved notable success through the

purchase .of out-of-favor stocks with very low price/

earnings ratios. His work shows that the stocks with

the lowes~ P/E ratios consistently outperform the stocks

with the highest P/E ratios.

These first three investment strategies involve

the selection of individual stocks and their application

requires extensive research on the part of the investor

or his advisor. The successful practitioners tend to

have fairly large staffs to conduct their research. This

is obviously not practical for the average investor.

The market timing approach is the forth basic

strategy. This approach does not depend on the selection

of individual stocks as do the three other strategies.

One can invest in an index fund and follow this game plan.

It is possible and probably advisable to pursue this

strategy while following any of the other three. If a

stock represents a bargain at the market peak, it must b e

an even better bargain at the market trough - all other

things being equal. The investor would stand to benefit

from the recovery of the market in addition to market

recognition of the individual stock.

A definitive study of market timing was performed

by William F. Sharpe (1975). He points out that:

7

The investment manager who hopes to outperform his competitors . usually expects to do so either by the selection of securities within a given class or by the allocation of assets to specific classes of securities. Potentially, one of the most productive forms of the latter strategy is to hold common. stocks during bull markets and cash equivalents during bear markets (market timing) •

In a perfectly efficient market, any attempt to obtain performance superior to that of the overall "market portfolio" (taking into account both risk and return) by picking and choosing among securities would fail. Although few investment managers are ready to admit that U. S. security markets are completely efficient, there is a growing awareness that inefficiencies are .few: any divergence between the price of a security and the "intrinsic value" that would be assigned to it by well informed and highly skilled analysts is likely to be small, temporary and difficult to identify in advance. Empirical studies of the performance of professionally managed . portfolios yield results consistent with this view: few, if any, provide better-than-average r~turn relative to risk year in and year out.

Some have argued that abnormal gains from selection of individual stocks or even industry groups are likely to be too small to justify the costs associated with attempts to identify and take advantage of apparent inefficiencies. Instead, it is said, the big gains are to be made by successful market timing.

Sharpe goes on to compare a buy-and-hold strategy

with perfect timing over several time periods. The perfect

timing is achieved only with hindsight. It is presented

only for comparison and to provide an upper limit for

application of this strategy. The results for the periods

analyzed were as follows (Sharpe 1975):

•

From To

1929 1972 1934 1972 1946 1972

8

Equivalent Annual Rate of Capital Growth

Buy-and-hold Timing Strategy Strategy

3.8%/year 19.9%/year 6.6 17.3 7.1 15.7

The balance of Sharpe's study is devoted to market

timing strategies involving scheduled annual reviews. The

senario assumes that the investment manager assesses the

market outlook at the start of the year and commits all

assets to either stocks (as represented by the Standard &

Poor's 500) or short-term money market instruments

(Treasury bills) for the year. The overall performance of

cash equivalents, stocks, and a policy with perfect

timing, is as follows (Sharpe 1975)_:

Overall Performance: Cash Equivalents, Stocks, and a Policy with Perfect Timing

1929-1972

Average Return Standard Deviation of Annual Returns

1934-1972

Average Return Standard Deviation of Annual Returns

1946-1972

Average Return Standard Deviation of Annual Returns

Cash Equivalents

2.38%

1.96

2 .• 40%

2.00

3.27%

1.83

Stocks

10.64%

21.06

12.76%

18.17

12.79%

15.64

Perfect Timing

14.86%

14.56

15.25%

13.75

14.63%

12.46

Sharpe found that an investment manager must be

9

correct in his market assessment of . the corning year at

least 70% of the time to outperform a buy-and-hold

strategy. His obvious conclusion is that market timing

is not a viable strategy for any but the superior manager.

The Sharpe study did not attempt to establish

decision rules that would trigger moves into and out of

the stock market. Rather, he attempted to quantify the

manager's predictive ability. Perhaps there are objective

rules that can be established to call for changes in the

investment portfolio.

Michael S. Rozeff (1975) challenged the

relationship of the money supply to changes in stock

market prices. He states:

While few propositions about. the stock market are universally accepted, most members of the financial community probably agree that changes in Federal Reserve Board monetary policy strongly influence changes in stock prices ••• with the expectation that a tighter monetary policy will be associated with falling stock prices and an easier monetary policy with rising stoc~ p~ices.

Rozeff found that current stock price changes are

virtually unrelated to prior money supply changes and

cannot be predicted profitably by trading rules using past

monetary data. His work supports the efficient capital

market hypothesis as he found that stock price movements

anticipate future mone~~ry growth.

Bryan Heathcotte and Vincent P. Apilado (1974)

looked at the predictive content of some leading economic

10

indicators for future stock prices.

The authors worked with diffusion indexes and

established filter rules to test the hypothesis that

movements in the economic indicators contain useful

information concerning subsequent movements in stock

prices. The looked at the period from November, 1959

to November, 1971:

The authors admit to mild surprise that the described policy produced results as profitable as those observed. The voluminous evidence cited in the academic literature in support of the efficiency of the organize~ security exchanges would lead one to expect a large, persistent profit advantage to the buy-and-hold policy. The latest values of the "predicting" series are, after all, swiftly and costlessly available to any investor who reads the financial press, and their publication is usually accompanied by helpful interpretive conunent. This is precisely the kind of information generally assumed to be rapidly discounted by the organized _securities markets. Further, the described policy results in the payment of trading commissions and in the payment of dividends while in short positions, actions which are ordinarily viewed as prohibitively costly to trading schemes.

While this study did not define an objective

strategy that would outperform a buy-and-hold approach, it

at least did as well. The authors felt that further

refinement of the diffusion indices and more timely

reporting of corporate profits would result in superior

performance.

A search of the literature does not reveal the

basis for a market timing approach that will outperform a

buy-and-hold strategy. This study will attempt to

11

establish decis~on rules for a profitable market timing

strategy. It will also attempt to establish decision

rules for effecting a change in strategy that will improve

results. This would involve a move from market timing to

buy-and-hold or vice versa.

CHAPTER II

METHODOLOGY

The fifteen year period from 1962 through 1976 was

selected for observation. The monthly average of the

Standard & Poor's 500 was used as a proxy for the market

portfolio. The short-term U. S. Treasury bill rate was

used to determine the return on funds not invested in the

stock market.

An element of risk is introduced by utilizing the

91-day Treasury bill discount rate. A capital gain or

loss could result from a change in the market rate during

the holding period. However, the Treasury bill rate is a

readily available indicator of relative money market rates

and. can serve as a proxy for shorter term instruments.

A buy-and-hold policy with all funds invested in

stocks was employed as the first strategy in the study.

This is the standard against which the market timing

approach was measured. The first senario calls for a

one-time investment of $10,000 at the start of the period.

The second situation involves the investment of $100 each

month for a total investment of $18,000 over the fifteen

year period.

13

The market timing strategy was first keyed to the

composite index of the twelve leading indicators. The

survey of th~ literature suggests that the leading

indicators hold the most promise for successfully

predicting market turns.

It must be pointed out that the Standard & Poor's

500 undex is itself one of the twelve leading indicators.

It is, in fact, the indicator that is given the most

weight in the composite index. This factor introduces a

bias, but not a damaging one. One goal of the study is to

find a useful indicator for predicting movement in the

stock market. An index of the stock market itself

qualifies under this criteria. The technical theory

approach uses historical market data; The thrust of this

research was to identify readily obtainable and easily

understood indicators to improve performance over the buy

and-hold strategy.

Risk must be recognized as a factor in evaluating

the returns from the various strategies. The returns from

all strategies were reduced to a monthly average figure.

The standard deviation and coefficient of variation were

calculated to attempt to measure the risk involved.

Transaction costs of two percent of the value of

the assets were assessed upon the purchase or sale of

stocks. A lag of one month was assumed before data became

14

available. To compensate for this lag, the purchase or

sale price used was for the month following the purchase

or sale signal.

Dividends on stocks and interest on Treasury bills

were considered to roughly offset during rnost · of the

period and were not included in the calculations. An

adjustment was made for the period from 1969 to 1981,

when interest rates moved into the double-digit range.

Actually, rates on Treasury bills tended to far exceed

dividends on common stocks and would result in more

favorable results for the market timing strategies if

considered. The average dividend rates on the Standard &

Poor's 500 and the average discount rate on Treasury bills

were as follows:

Dividend Treasury Period Rates Bill Rates

1961-1963 2.14% 2.77% 1968-1970 3.13 6.16 1980-1981 5.77 12.85

The effect of taxes was not considered in the

study. The tax effect would be rather small for the

average investor. It can easily be added to the

calculations for the investor in a high tax bracket.

Conclusions were drawn from the fifteen-year base

period and applied to a five-year test period from 1977 to

1981. Again, a one-time investment of $10,000 and a

monthly investment of $100 were used to test the two

15

approaches.

The data was analyzed to determine whether or not

a shift between strategies would produce .better results

than pursuing a single approach for the whole period. An

attempt was then made to identify factors that would

correctly key such a change.

CHAPTER III

FINDINGS

Two decision rules were developed for a market

timing strategy that significantly outperformed the

buy-and-hold approach. Both of these decision rules

involve using the composite index of twelve leading

indicators.

The first and simplest of the successful

strategies calls for a purchase after two successive

monthly increases in the composite .index of twelve leading

indicators. Conversely, it calls for a sale after two

successive monthly decreases in the index. This ~ery

simple approach resulted in eight moves in and out of the

market, half of which were counter productive.

Nevertheless, . it was significantly better than merely

buying and holding stocks for the fifteen-year period.

A refinement of the first strategy provided for

significantly improved results. This approach called for

purchases or sales after two consecutive monthly positive

or negative changes in the composite index of twelve

leading indicators over three month spans. The smoothing

effect of this indicator resulted in fewer trades, five,

17

of which only one produced .unfavorable results.

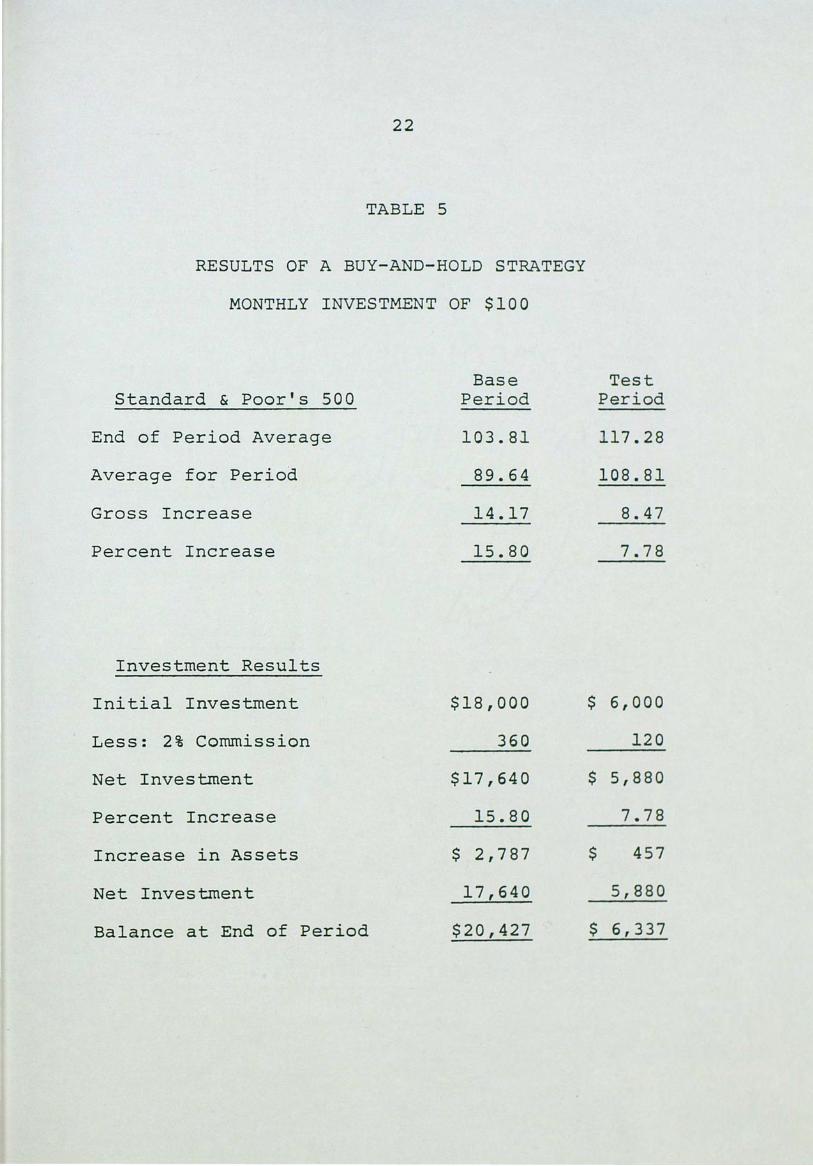

The buy-and-hold strategy provided an increase of

$4,729 on the .original $10,000 investment • . Table 1 shows

the calculation . . This compares to an increase of $9,227

with the first market timing approach and $11,466 with the

second. These calculations are shown ~n Tables 2 and 4,

respectively. Neither .of these last two figures include

earnings in the money market while funds were held out of

the stock market.

A second comparison was made of the various

strategies. This study involved an investment of $100

per month for the same fifteen-year . period. The total

investment of $18,000 resulted in a balance of $20,427

at the end of the period for the buy-and-hold alternative.

The increase was $2,427 as is shown in Table 5.

Both of the market timing strategies produced a

greater gain from stock market transactions than the buy

and-hold approach. The first of these strategies resulted

in an increase of $5,541, while the second yielded $6,245.

Tables 6 and 8 show these results. Thus, the overall

results of market timing are superior to the buy-and-hold

program.

The decision rules developed above were applied to

the test period. of 1977 through 1981. The results obtained

on stock market investments were not in keeping with the

18

TABLE 1

RESULTS OF A BUY-AND-HOLD STRATEGY

INITIAL INVESTMENT OF $10,000

Standard & Poor's 500

End of Period Average

Start of Period Average

Gross Increase

Percent Increase

Investment Results

Initial Investment

Less: 2% Commission

Net Investment

Percent Increase

Increase in Assets

Net Investment

Balance at End of Period

Base Period

103.81

69.07

34.74

50.30

$10,900

200

$ 9,800

50.30

$ 4,929

9,800

$14,729

Test Period

117.28

103.81

13.47

12.98

$10,000

200

$ 9,800

12.98

$ 1,272

9,800

$11,072

TA

BL

E

2

RE

SUL

TS

OF

MA

RK

ET

TIM

ING

ST

RA

TE

GY

#

1

INIT

IAL

IN

VE

STM

EN

T

OF

$1

0,0

00

BA

SE

PE

RIO

D

Buy

S&

P C

ash

2%

N

et

Sell

S&

P G

ain

S

ale

2%

D

ate

5

00

A

vail

ab

le

Fee

Inv

este

d

Date

5

00

(L

oss

) P

roceed

s F

ee

Sep

/62

:5

8.0

0

$1

0,0

00

$

20

0

$ 9

,80

0

Au

g/6

3

70

.98

2

2.3

7%

$

11

,99

2

$2

40

Oct/

62

7

3.0

3

11

,75

2

23

5

11

,51

7

Jun

/66

8

6.0

6

17

.84

1

3,5

72

2

71

~

\0

Mar

/67

8

9.4

2

13

,30

1

26

6

13

,03

5

Ap

r/6

9

10

1.2

6

13

.24

1

4,7

61

2

95

Jun

/70

7

5.5

9

14

,46

6

28

9

14

,17

7

Au

g/7

0

77

.92

3

.08

1

4,6

14

2

92

Oct/

70

8

4.3

7

14

,32

2

28

6

14

,03

6

Sep

/71

9

9.4

0

17

.81

1

6,5

36

3

31

No

v/7

1

92

.78

1

6,2

05

3

24

1

5,8

81

M

ay/7

3

10

7.2

2

15

.56

1

8,3

52

3

67

Dec

/73

9

4.7

8

17

,98

5

36

0.

17

,62

5

Feb

/74

9

3.4

5

(1.4

0)

17

,37

8

34

8

May

/75

9

0.1

0

17

,03

0

34

1

16

,68

9

Jan

/77

1

03

.81

1

5.2

1

19

,22

7

TA

BL

E

3

RE

SUL

TS

OF

MA

RK

ET

TIM

ING

ST

RA

TE

GY

#

1

INIT

IAL

IN

VE

STM

EN

T

OF

$1

0,0

00

TE

ST

P

ER

IOD

Buy

S&

P C

ash

2%

N

et

Sell

S&

P G

ain

S

ale

2%

D

ate

5

00

A

vail

ab

le

Fee

Inv

este

d

Date

5

00

(L

oss

) P

roceed

s F

ee

--

Sep

/77

9

6.2

3

$1

0,0

00

$

20

0

$ 9

,80

0

Mar/

79

1

00

.11

4

.03

%

$1

0,1

95

$

20

4

tv

Ju1

/79

1

02

.71

9

,99

1

20

0

9,7

91

S

ep

/79

1

08

.60

5

.73

1

0,3

52

2

07

0

Au

g/8

0

12

3.5

0

10

,14

5

20

3

9,9

42

F

eb

/81

1

28

.40

3

.97

1

0,3

37

2

07

May

/81

1

31

.73

1

0,1

30

2

03

9

,92

7

Ju1

/81

1

29

.13

{

1.9

7)

9,7

31

1

95

9,5

36

TA

BL

E

4

RE

SUL

TS

OF

MA

RK

ET

TIM

ING

ST

RA

TE

GY

#2

INIT

IAL

IN

VE

STM

EN

T

OF

$1

0,0

00

Bu

y

S&P

Cash

2%

N

et

Sell

S&

P G

ain

S

ale

2%

D

ate

5

00

A

vail

ab

le

Fee

Inv

este

d

Date

5

00

{

Lo

ss)

Pro

ceed

s F

ee

Base

P

eri

od

Sep

/62

5

8.0

0

$1

0,0

00

$

20

0

$ 9

,80

0

Jun

/66

8

6.0

6

48

.37

%

$1

4,5

40

$

29

1

Feb

/67

8

9.4

2

14

,24

9

28

5

13

,96

4

Ap

r/6

9

10

1.2

6

13

.24

1

5,8

13

3

16

N

.._,

Oct/

70

8

4.3

7

15

,49

7

31

0

15

,18

7

Sep

/71

9

9.4

0

17

.81

1

7,8

92

3

58

No

v/7

1

92

.78

1

7,5

34

3

51

1

7,1

83

Ju

n/7

3

10

4.7

5

12

.90

1

9,4

00

3

88

May

/75

9

0.1

0

19

,01

2

38

0

18

,63

2

Jan

/77

1

03

.81

1

5.2

1

21

,46

6

Test

Peri

od

Sep

/77

9

6.2

3

$1

0,0

00

$

20

0

$ 9

,80

0

Feb

/79

9

8.2

3

2.0

9%

$

10

,00

5

$2

00

Aug

-SO

1

23

.50

9

,80

5

19

6

9,6

09

Ju

1/8

1

12

9.1

3

4.5

5

10

,04

6

20

1

9,8

45

22

TABLE 5

RESULTS OF A BUY-AND-HOLD STRATEGY

MONTHLY INVESTMENT OF $100

Base Test Standard & Poor's 500 Period Period

End of Period Average 103.81 117.28

Average for Period 89.64 108.81

Gross Increase 14.17 8.47

Percent Increase 15.80 7.78

Investment Results

Initial Investment $18,000 $ 6,000

Less: 2% Corrunission 360 120

Net Investment $17,640 $ 5,880

Percent Increase 15.80 7.78

Increase in Assets $ 2,787 $ 457

Net Investment 17,640 5,880

Balance at End of Period $20,427 $ 6,337

TA

BL

E

6

RE

SUL

TS

OF

MA

RK

ET

TIM

ING

ST

RA

TE

GY

il

MO

NTH

LY

INV

EST

ME

NT

O

F $

10

0

BA

SE

PE

RIO

D

Buy

S&

P C

ash

2%

N

et

Sell

S&

P G

ain

S

ale

2%

C

ash

D

ate

5

00

A

vail

ab

le

Fee

Inv

este

d

Date

5

00

(L

oss

) P

roceed

s F

ee

Ad

ded

N

Sep

/62

5

8.0

0

$ 9

00

$

18

$

88

2

Au

g/6

3

70

.98

2

2.3

7%

$

1,0

79

$

22

$1

,30

0

w

Oct/

63

7

3.0

3

2,3

57

47

2

,31

0

Jun

/66

8

6.0

6

17

.84

2

,72

2

54

4,1

00

Mar/

67

8

9.4

2

6,7

68

1

35

,6

,63

3

Ap

r/6

9

10

1.2

6

13

.24

7

,51

1

15

0

3,9

00

Jun

/70

1

12

.61

1

1,2

61

2

25

1

1,0

36

A

ug

/70

7

7.9

2

3.0

8

11

,37

6

22

8

40

0

Oct/

70

8

4.3

7

11

,54

8

23

1

11

,31

7

Sep

/71

9

9.4

0

17

.81

1

3,3

33

2

67

1

,30

0

No

v/7

1

92

.78

1

4,3

66

2

87

1

4,0

79

M

ay/7

3

10

7.2

2

15

.56

1

6,2

70

3

25

2

,50

0

Dec/7

3

94

.78

1

8,4

45

3

69

1

8,0

76

F

eb

/74

9

3.4

5

(1.4

0)

17

,82

3

35

6

1,7

00

May

/75

9

0.1

0

19

,16

7

38

3

18

,78

4

Jan

/77

1

03

.81

1

5.2

1

21

,64

1

-1

,90

0

23

,54

1

TA

BL

E

7

RE

SUL

TS

OF

MA

RK

ET

TIM

ING

ST

RA

TE

GY

#

1

MO

NTH

LY

INV

EST

ME

NT

O

F $

10

0

TE

ST

P

ER

IOD

Buy

S&

P C

ash

2%

N

et

Sell

S&

P G

ain

S

ale

2%

C

ash

D

ate

5

00

A

vail

ab

le

Fee

Inv

este

d

Date

5

00

(L

oss

) P

roceed

s F

ee

Ad

ded

N

Sep

/77

9

6.2

3

$ 9

00

$

18

$

88

2

Mar/

79

1

00

.11

4

.03

%

$ 9

18

~

$ 1

8

$2

,20

0

Ju

l/7

9

10

2.7

1

3,1

00

6

2

3,0

38

S

ep

/79

1

08

.60

5

.73

3

,21

2

64

1

,30

0

Au

g/8

0

12

3.5

0

4,4

48

89

4

,35

9

Feb

/81

1

28

.40

3

.97

4

,53

2

91

9

00

May

/81

1

31

.73

5

,34

1

10

7

5,2

34

Ju

l/8

1

12

9.1

3

(1.9

7)

5,1

31

1

03

7

00

5,7

28

\

TA

BL

E

8

RE

SUL

TS

OF

MA

RK

ET

TIM

ING

ST

RA

TE

GY

#

2

MO

NTH

LY

INV

EST

ME

NT

O

F $

10

0

Buy

S&

P C

ash

2%

N

et

Sell

S&

P G

ain

S

ale

2%

C

ash

D

ate

5

00

A

vail

ab

le

Fee

Inv

este

d

Date

5

00

(L

oss

) P

roceed

s F

ee

Ad

ded

Bas

e P

eri

od

t\

..)

Sep

/62

5

8.0

0

$ 9

00

$

18

$

88

2

Jun

/66

8

6.0

6

48

.37

%

$ 1

,30

9

$ 2

6

$5

,30

0

Ul

Feb

/67

8

9.4

2

6,5

83

1

32

6

,45

1

Ap

r/6

9

10

1.2

6

13

.24

7

,30

5

14

6

4,4

00

Oct/

70

8

4.3

7

11

,55

9

23

1

.1,1

,328

S

ep

/71

9

9.4

0

17

.81

1

3,3

46

2

67

1

,30

0

No

v/7

1

92

.78

1

4,3

79

2

88

1

4,0

91

Ju

n/7

3

10

4.7

5

12

.90

1

5,9

09

3

18

4

,20

0

May

/75

9

0.1

0

19

,79

1

39

6

19

,39

5

Jan

/77

1

03

.81

1

5.2

1

22

,34

5

-1

,90

0

24

,24

5

Test

Peri

od

Sep

/77

9

6.2

3

$ 9

00

$

18

$

88

2

Feb

/79

9

8.2

3

2.0

9

$ 9

00

$

18

$

3,5

00

Au

g/8

0

12

3.5

0

4,3

82

8

8

4,2

94

Ju

1/8

1

12

9.1

3

4.5

5

4,4

89

89

1

,60

0

6,0

00

26

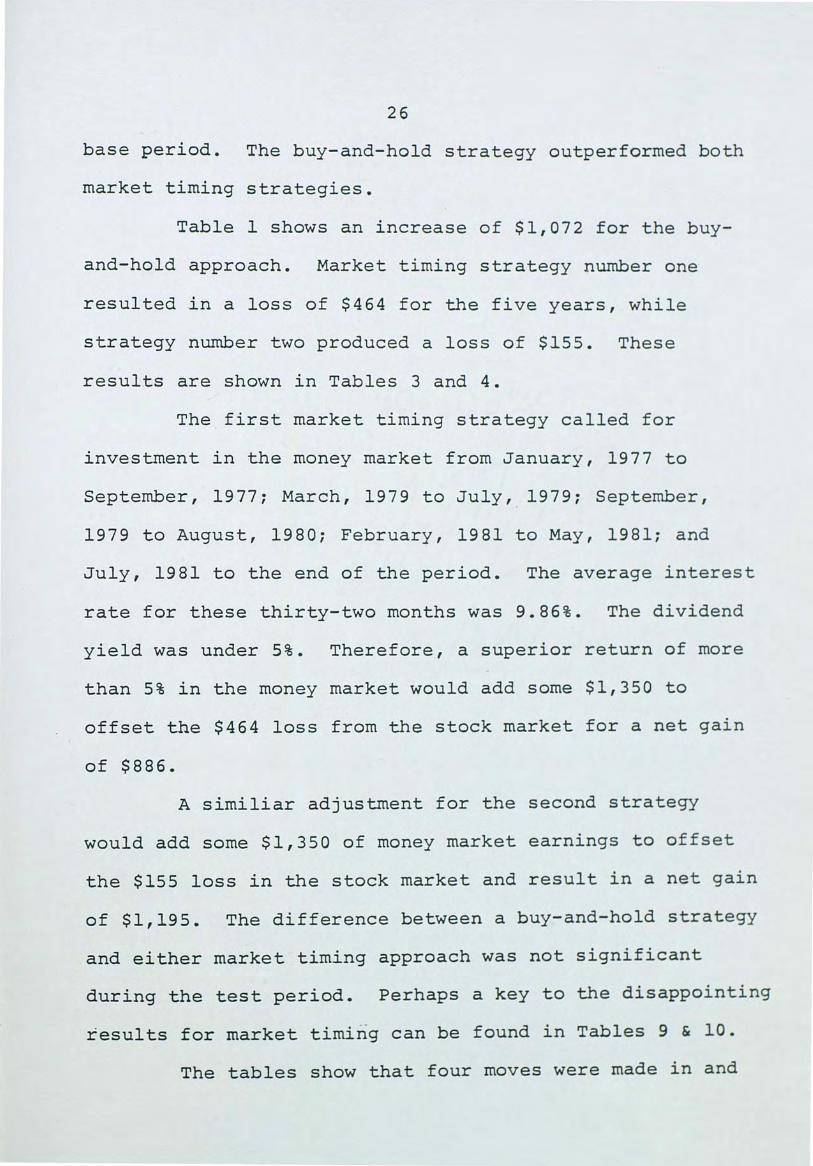

base period. The buy-and-hold strategy outperformed both

market timing strategies.

Table 1 shows an increase of $1,072 for the buy

and-hold approach. Market timing strategy number one

resulted .in a loss of $464 for the five years, while

strategy number two produced a loss of $155. These

results are shown in Tables 3 and 4.

The first market timing strategy called for

investment in the money market from January, 1977 to

September, 1977; March, 1979 to July, _ 1979; September,

1979 to August, 1980; February, 1981 to May, 1981; and

July, 1981 to the end of the period. The average interest

rate for these thirty-two months was 9.86%. The dividend

yield was under 5%. Therefore, a superior return of more

than 5% in the money market would add some $1,350 to

offset the $464 loss from the stock market for a net ga1n

of $886.

A similiar adjustment for the second strategy

would add some $1,350 of money market earnings to offset

the $155 loss in the stock market and result in a net gain

of $1,195. The difference between a buy-and-hold strategy

and either market timing approach was not significant

during the test period. Perhaps a key to the disappointing

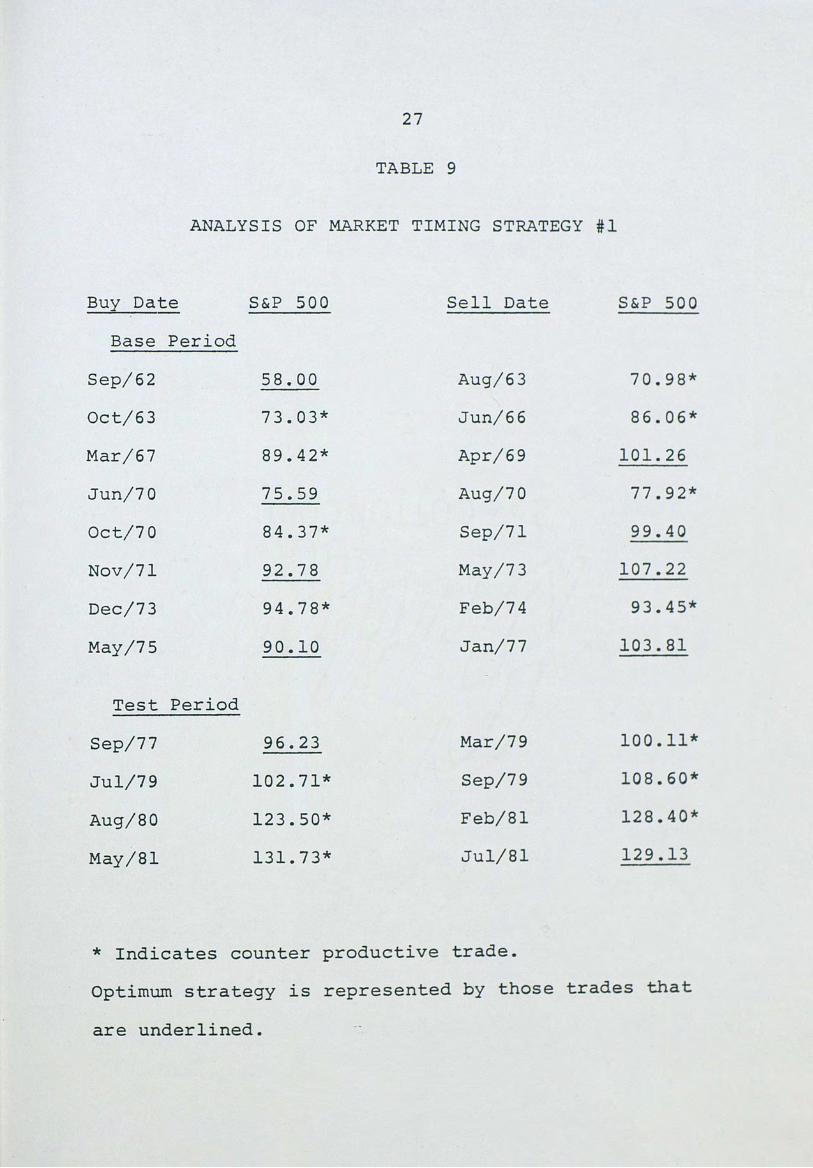

results for market timing can be found 1n Tables 9 & 10.

The tables show that four moves were made in and

27

TABLE 9

ANALYSIS OF MARKET TIMING STRATEGY #1

Buy Date S&P 500 Sell Date S&P 500

Base Period

Sep/62 58.00 Aug/63 70.98*

Oct/63 73.03* Jun/66 86.06*

Mar/67 89.42* Apr/69 101.26

Jun/70 75.59 Aug/70 77.92*

Oct/70 84.37* Sep/71 99.40

Nov/71 92.78 May/73 107.22

Dec/73 94.78* Feb/74 93.45*

May/75 90.10 Jan/77 103.81

Test Period

Sep/77 96.23 Mar/79 100.11*

Ju1/79 102.71* Sep/79 108.60*

Aug/80 123.50* Feb/81 128.40*

May /81 131.73* Ju1/81 129.13

* Indicates counter productive trade.

Optimum strategy is represented by those trades that

are underlined.

28

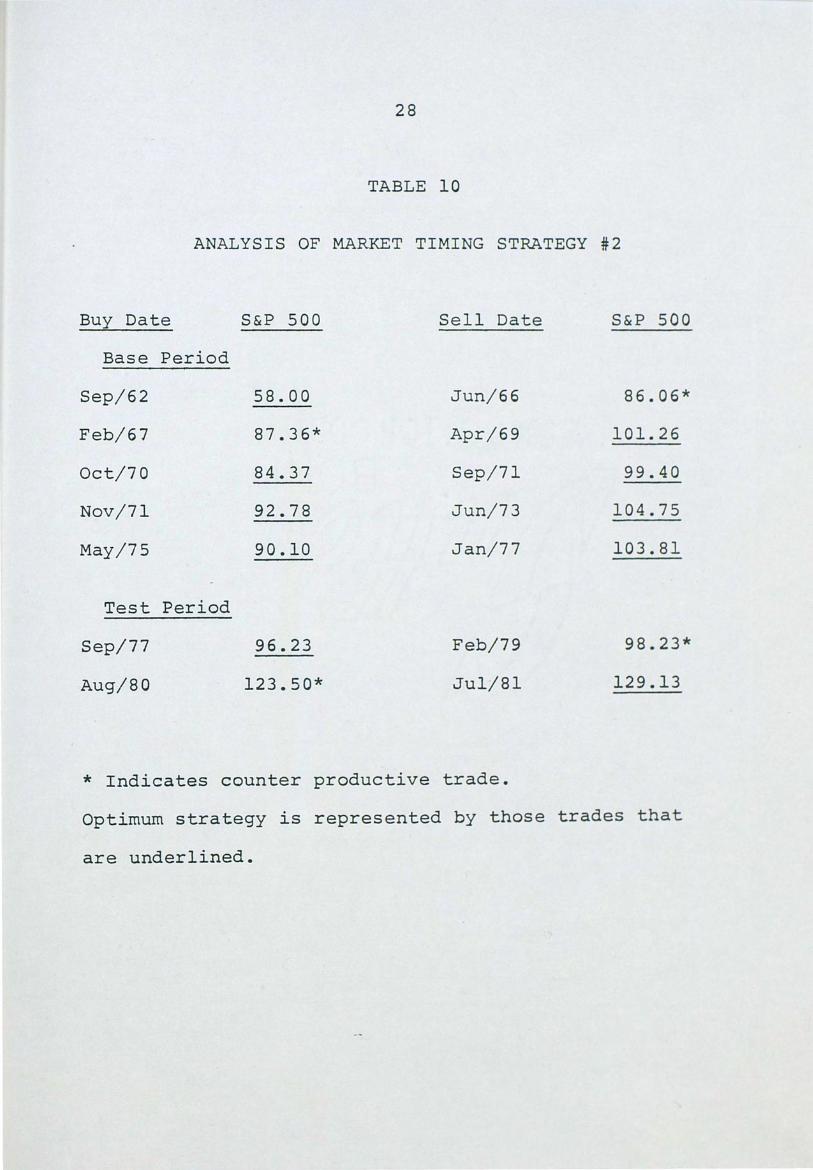

TABLE 10

ANALYSIS OF MARKET TIMING STRATEGY #2

Buy Date

Base Period

Sep/62

Feb/67

Oct/70

Nov/71

May/75

Test Period

Sep/77

Aug/80

S&P 500

58.00

87.36*

84.37

92.78

90.10

96.23

123.50*

Sell Date

Jun/66

Apr/69

Sep/71

Jun/73

Jan/77

Feb/79

Jul/81

* Indicates counter productive trade.

S&P 500

86.06*

101.26

99.40

104.75

103.81

98.23*

129.13

Optimum strategy is represented by those trades that

are underlined.

29

out of the stock market during the test period under the

first market timing strategy. Three of these moves, or

75% of the total, were counter productive. One of the two

moves called for under the second market timing strategy

was counter productive, a 50% failure rate. If some or all

of these transactions could be eliminated by keying a

change in strategy at the appropriate time, the results

should be substantially improved.

Looking at the entire twenty-year span that

encompasses both the base and test periods, the buy-and

hold strategy prod.uced the best results through April,

1979. The market timing strategies were vastly superior

from April, 1969 to September, 1977. The period from

September, 1977 to July, 1981 again called for the buy

and-hold alternative. Finally, one would be well advised

to switch to the market timing approach at July, 1981.

These few adjustments make for dramatic improvements in

performance.

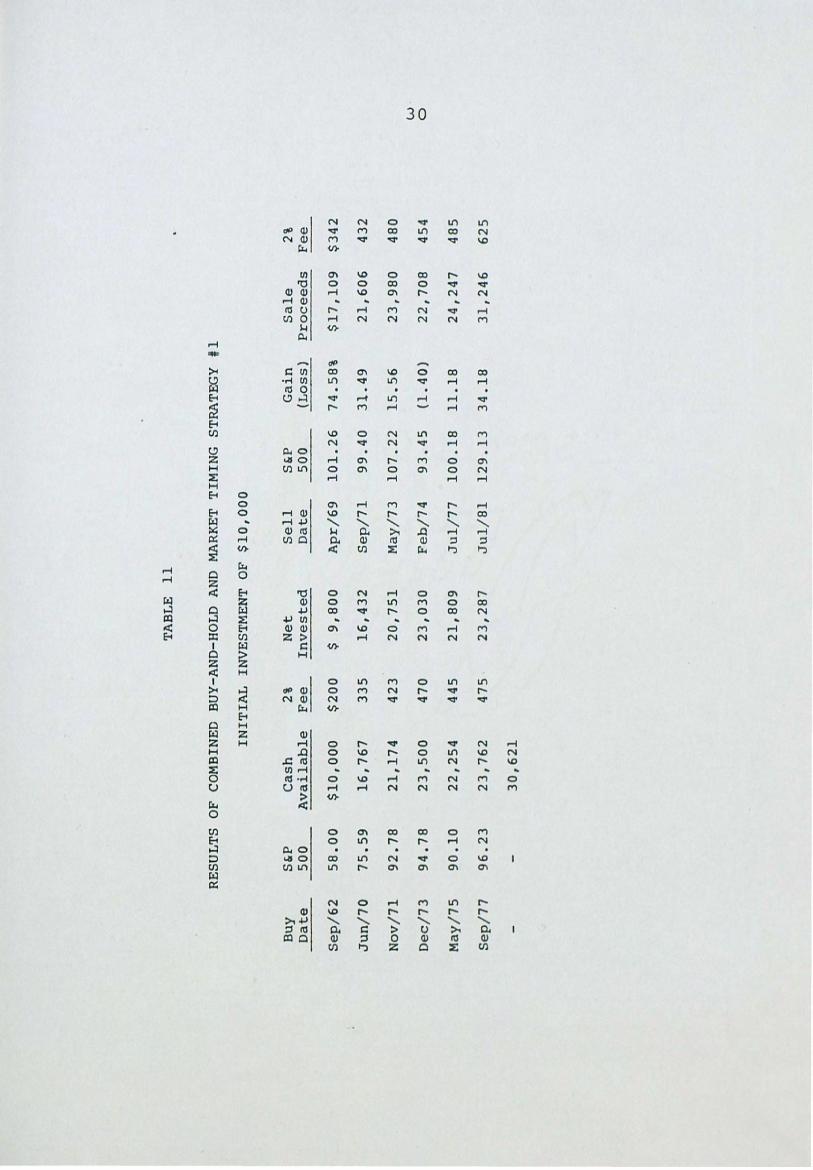

The combination of buy-and-hold with the first

market timing strategy resulted in a return of $20,621 on

the initial $10,000 investment. The same approach returns

$12,505 on a $100 per month investment over the twenty-year

period. Tables 11 and 12 show these results.

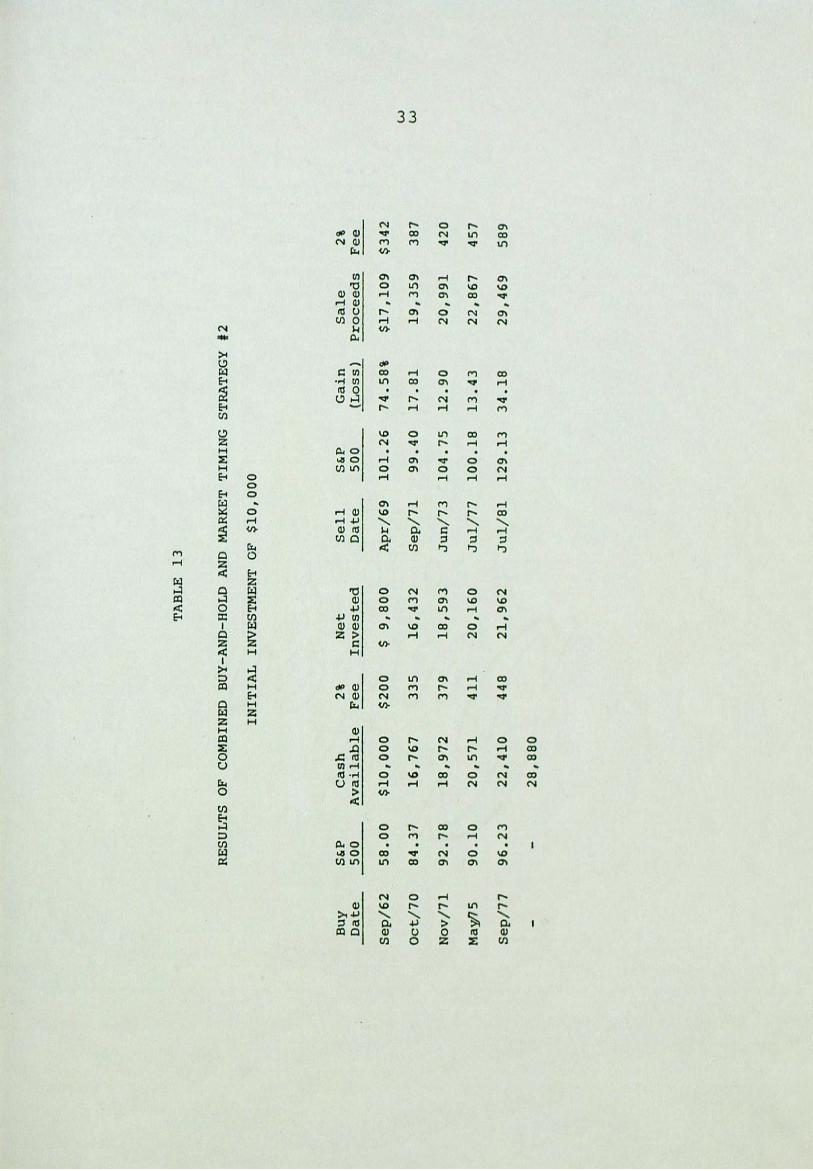

The second market timing strategy, when alternated

with buy-and-hold, returned $18,880 on the original

TA

BL

E

11

RE

SUL

TS

OF

CO

MB

INE

D

BU

Y-A

ND

-HO

LD

A

ND

M

AR

KET

T

IMIN

G

STR

AT

EG

Y

#1

INIT

IAL

IN

VE

STM

EN

T

OF

$1

0,0

00

Buy

S&

P C

ash

2%

N

et

Sell

S&

P G

ain

S

ale

2%

D

ate

5

00

A

vail

ab

le

Fee

Inv

este

d

Date

5

00

(L

oss

) P

roceed

s F

ee

-

Sep

/62

5

8.0

0

$1

0,0

00

$

20

0

$ 9

,80

0

Ap

r/6

9

10

1.2

6

74

.58

%

$1

7,1

09

$

34

2

Ju

n/7

0

75

.59

1

6,7

67

3

35

1

6,4

32

S

ep

/71

9

9.4

0

31

.49

2

1,6

06

4

32

No

v/7

1

92

.78

2

1,1

74

4

23

2

0,7

51

M

ay/7

3

10

7.2

2

15

.56

2

3,9

80

4

80

W

· D

ec/7

3

94

.78

2

3,5

00

4

70

2

3,0

30

F

eb

/74

9

3.4

5

(1.

40

) 2

2,7

08

4

54

0

May

/75

9

0.1

0

22

,25

4

44

5

21

,80

9

Ju

l/7

7

10

0.1

8

11

.18

2

4,2

47

4

85

Sep

/77

9

6.2

3

23

,76

2

47

5·

23

,28

7

Ju

l/8

1

12

9.1

3

34

.18

3

1,2

46

6

25

30

,62

1

TA

BL

E

12

RE

SUL

TS

OF

CO

MB

INED

B

UY

-AN

D-H

OL

D

AN

D

MA

RK

ET

TIM

ING

ST

RA

TE

GY

#

1

MO

NTH

LY

INV

EST

ME

NT

O

F $

10

0

Buy

S&

P C

ash

2%

N

et

Sell

S&

P G

ain

S

ale

2%

C

ash

D

ate

5

00

A

vail

ab

le

Fee

Inv

este

d

Date

5

00

(L

oss

) P

roceed

s F

ee

Ad

ded

--

Sep

/62

5

8.0

0

$ 9

00

$

18

$

88

2

Ap

r/6

9

10

1.2

6

74

.58

%

$ 1

,54

0

$ 3

1

$9

,30

0

Jun

/70

7

5.5

9

10

,80

9

21

6

10

,59

3

Sep

/71

9

9.4

0

31

.49

1

3,9

29

2

79

1

,70

0

No

v/7

1

92

.78

1

5,3

50

3

07

1

5,0

43

M

ay/7

3

10

7.2

2

15

.56

1

7,3

84

3

48

2

,50

0

w ~

Dec/7

3

94

.78

1

9,5

36

3

91

1

9,1

45

F

eb

/74

9

3.4

5

(1.4

0)

18

,87

7

37

6

1,7

00

May

/75

9

0.1

0

20

,20

1

40

4

19

,79

7

Ju1

/77

1

00

.18

1

1.1

8

22

,01

0

44

0

2,8

00

Sep

/77

9

6.2

3

24

,37

0

48

7

23',

88

3

Ju

l/8

1

12

9.1

3

34

.18

3

2,0

46

6

41

5

,10

0

36

,50

5

32

investment of $10,000. The monthly investment of $100

returned $11,889 at the end of twenty years. These

figures are shown in Tables 13 and 14. Approximately

$1,000 in money market earnings can be added to all four

of the returns shown above for comparison with the

previous market timing results.

These combined strategies must be compared with

the entire twenty-year period under examination, which is

composed of the base period and the test period. The

buy-and-hold strategy would show a return of $6,640 on

the $10,000 investment and $5,207 on the $100 per month

investment. The first market timing strategy returned

$9,343 on $10,000 and $6,056 on the ~onthly investment

program. The figures for the second market timing

strategy were $12~790 and $8,097, respectively. Thus,

trerewards are great for a timely changing of strategy.

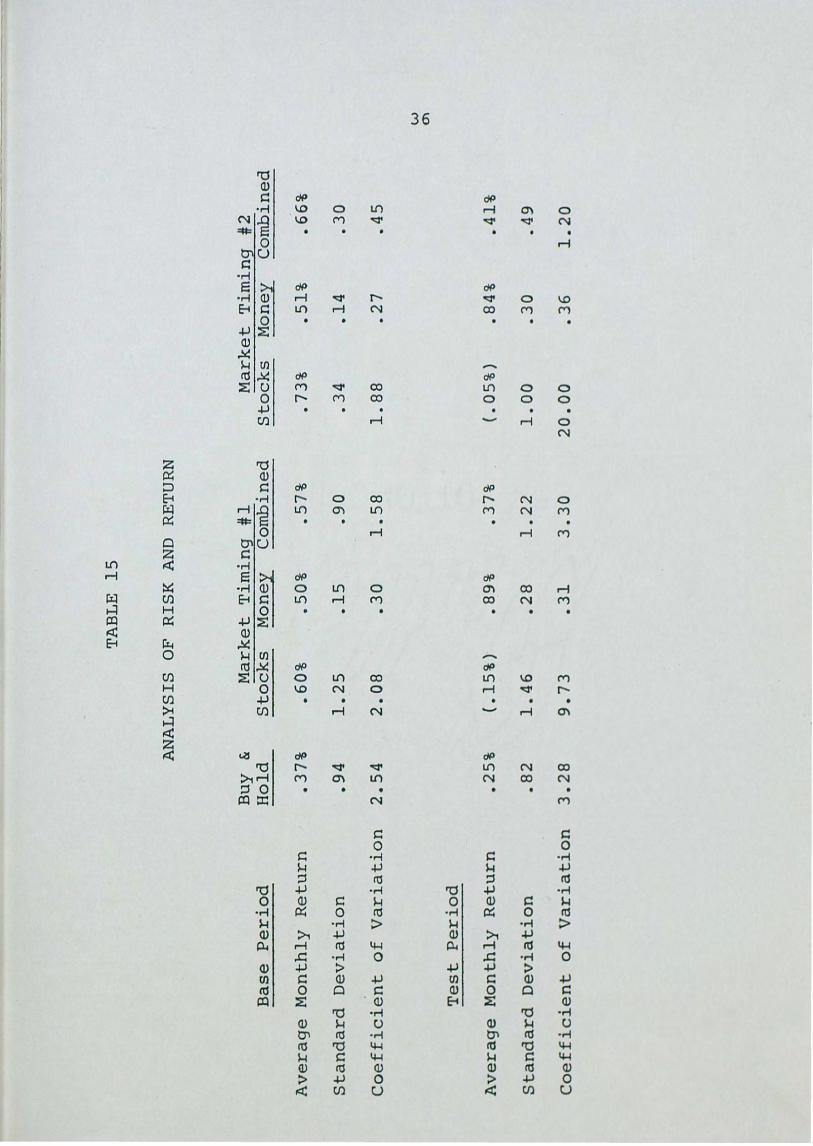

The introduction of risk into the study was

accomplished by calculating the standard deviation for

each of the basic strategies, both during the base period

and the test period. The calculations were made only for

the $10,000 investment program. The results were rather

surprising.

The first market timing strategy shows a greater

return, adjusted for transaction costs, than the buy-and

hold strategy. It shows comparable risk during the base

Buy

D

ate

Sep

/62

Oct/

70

No

v/7

1

Ma~5

Sep

/77

TA

BL

E

13

RE

SUL

TS

OF

CO

MB

INED

B

UY

-AN

D-H

OL

D

AN

D

MA

RK

ET

TIM

ING

ST

RA

TE

GY

#2

INIT

IAL

IN

VE

STM

EN

T

OF

$1

0,0

00

S&P

Cash

2%

N

et

Sell

S&

P G

ain

S

ale

5

00

A

vail

ab

le

Fee

Inv

este

d

Date

5

00

(L

oss

) P

roceed

s --

58

.00

$

10

,00

0

$2

00

$

9,8

00

A

pr/

69

1

01

.26

7

4.5

8%

$

17

,10

9

84

.37

1

6,7

67

3

35

1

6,4

32

S

ep

/71

9

9.4

0

17

.81

1

9,3

59

92

.78

1

8,9

72

3

79

1

8,5

93

Ju

n/7

3

10

4.7

5

12

.90

2

0,9

91

90

.10

2

0,5

71

4

11

2

0,1

60

Ju

1/7

7

10

0.1

8

13

.43

2

2,8

67

96

.23

2

2,4

10

4

48

2

1,9

62

Ju

1/8

1

12

9.1

3

34

.18

2

9,4

69

28

,88

0

2%

Fee

$3

42

w

3

87

w

42

0

45

7

58

9

TA

BL

E

14

RE

SUL

TS

OF

CO

MB

INED

B

UY

-AN

D-H

OL

D

AN

D

MA

RK

ET

TIM

ING

ST

RA

TE

GY

#2

MO

NTH

LY

INV

EST

ME

NT

O

F $

10

0

Buy

S&

P C

ash

2%

N

et

Sell

S&

P G

ain

S

ale

2%

C

ash

D

ate

5

00

A

vail

ab

le

Fee

Inv

este

d

Date

5

00

~oss)

Pro

ceed

s F

ee

Ad

ded

Sep

/62

5

8.0

0

$ 9

00

$

18

$

88

2

Ap

r/6

9

10

1.2

6

74

.58

%

$ 1

,54

0

$ 3

1

$9

,70

0

Oct/

70

8

4.3

7

11

,20

9

22

4

10

,98

5

Sep

/71

9

9.4

0

17

.81

1

2,9

41

2

59

1

,30

0

No

v/7

1

92

.78

1

3,9

82

2

80

1

3,7

02

Ju

n/7

3

10

4.7

5

12

.90

1

5,4

70

3

09

4

,20

0

w ~

May

/75

9

0.1

0

19

,36

1

38

7

18

,97

4

Ju1

/77

1

00

.18

1

3.4

3

21

,52

2

43

0

2,8

00

Sep

/77

9

6.2

3

23

,89

2

47

8

23

,41

4

Ju1

/81

1

29

.13

3

4.1

8

31

,41

7

62

8

5,1

00

35

,88

9

35

period and higher risk during the test period. The return

relative to risk is much greater for the market timing

strategy during the base period and roughly equivalent

during the test period. Table 15 shows the results.

The second market timing strategy shows a greater

return and a lower risk than the buy-and-hold approach.

This is the case during the base period and the test

period. If one must choose a single strategy and hold to

it, the second market timing strategy is clearly the one.

The first market timing strategy is slightly superior if

one can move between basic strategies on a timely basis.

It does involve significantly greater risk than is

justified by the return.

The results shown in Table 15 are felt to be

reliable on the basis of their t ratios. The t ratios

were as follows:

Buy-and-Hold/ Market Timing #1

Market Timing #1/ Market Timing #2

Buy-and-Hold/ Market Timing #2

Base Period

.58

.37

1.16

Test Period

.21

.08

.35

TA

BL

E

15

AN

AL

YSI

S O

F R

ISK

A

ND

R

ETU

RN

Buy

&

M

ark

et

Tim

ing

#l

. M

ark

et

Tim

in9

: #2

B

ase

P

eri

od

H

old

S

tock

s M

on

ey

Co

mb

ined

S

tock

s M

oney

C

om

bin

ed

--

Av

era

ge

Mo

nth

ly

Retu

rn

.37

%

.60%

.5

0%

.5

7%

.7

3%

.51%

.6

6%

Sta

nd

ard

D

ev

iati

on

.9

4

1.2

5

.15

.9

0

.34

.1

4

.30

Co

eff

icie

nt

of

Vari

ati

on

2

.54

2

.08

.3

0

1.5

8

1.8

8

.27

.4

5

w

0)

Test

Peri

od

Av

era

ge

Mo

nth

ly

Retu

rn

.25%

( .

15%

)'

.89%

.3

7%

(.0

5%

) .8

4%

.41%

Sta

nd

ard

D

ev

iati

on

.8

2

1.4

6

.28

1

.22

1

.00

.3

0

.49

Co

eff

icie

nt

of

Vari

ati

on

3

.28

9

.73

.3

1

3.3

0

20

.00

.3

6

1.2

0

CHAPTER IV

CONCLUSIONS

The returns to be obtained from an investment

program that moves back and forth between two different

strategies at the appropriate time are quite impressive.

Two easily applied decision rules have been established

for the market timing phase of the program. These rules

do not pretend to signal market peaks or troughs. They

did supply results superior to the basic buy-and-hold

strategy. They are objective rules that require no

judgement call on the part of the investor.

The problem then becomes one of determining in

advance when to switch basic strategies. Changes in

strategy were called for in 1969, 1977 and 1981. It had

been suggested that changes in the political scene might

call for changes in investment strategy. This lead to the

observation that 1969 was the first year in office of a

Republican President, 1977 was the first year in office of

a Democrat President, . and 1981 was the first year in office

of a Republican President. Thus, a change in investment

strategy is apparently called for whenever there is a

change in political parties in the White House.

The appropriate investment strategy under the

38

Democrats (1962-1968 and 1977-1980) is to buy-and-hold.

The appropriate investment strategy under the Republicans

(1969-1976 and 1981 to the present) is market timing.

A possible explanation for this observation is

that the investing public perceives the Democrat

administrations as inflationary in nature. Presidents

Johnson (guns and butter) and Carter (double-digit

inflation) did nothing to dispell this notion. The

investing public perceives the Republican administrations

as anti-inflationary in nature. Presidents Nixon (wage

and price controls), Ford (Whip Inflation Now), and

Reagan (single-digit inflation) have done nothing to

dispell this notion. This perception alone seems enough

to trigger a change in investment philosophy.

If the investing public anticipates continued

inflation, it remains fully invested in stocks. If it does

not anticipate continued inflation, it is indecisive in its

investment strategy. The stock market will therefore be

more volatile and a strategy of market timing will be more

appropriate. While these may be subjective conclusions,

they are supported by the results of this study. It will

be interesting to see if they hold true in the future. At

the time of this writing, a market timing strategy is

called for and the leading indicators are signaling for

a move into the stock market.

39

SELECTED BIBLIOGRAPHY

Dreman, David. Contrarian Investment Strategy. New York: Random House, 1979.

Heathcotte, . Bryan, and Apilado, Vincent P. "The Predictive Content of Some Leading Economic Indicators for Future Stock Prices," Journal of Financial and Quantitative Analysis 9 (March, 1974): 247-258.

Malkiel, Burton G. A Random Walk Down Wall Street. New York: W. W. Norton & Co., 1973.

Markowitz, Harry. "Portfolio Selection," Journal of Finance 7 (March, 1952): 77-91.

Reilly, Frank K. Investment Analysis and Portfolio Management. Hinsdale IL: Dryden Press, 1979.

Rolo, Charles J. Gaining on the Market. Boston: Little, Brown and Company, 1982.

Rozeff, M. s. "The Money Supply and the Stock Market," Financial Analysts Journal 31 (September-October, 1975): 18-26.

Sharpe, William F. Portfolio Theory and Capital Markets. New York: McGraw-Hill, Inc., 1970 •

• "Likely Gains from Market Timing," Financial ---~-Analysts Journal 31 (March-April, 1975): 60-69.

Train, John. The Money Masters. New York: Harper & Row, 1980.