ami market opportunities & challenges in asia pacific (2010 global electric power tech)

TRANSCRIPT

AMI Market Opportunities & Challenges in Asia Pacific

Presented atWorld Smart Grids Seminar 2010

Seoul, South Korea

19 May 2010

Presented bySubbu BettadapuraAssociate Director – Energy & PowerFrost & Sullivan

22

AMI Technology Trends & Evolution

Agenda

1

2

3

APAC Market Size and Cost breakdown

Key Industry Challenges4

5

AMI Benefits & Features

AMI Introduction and Value Chain

Key Growth Countries and Market Dynamics6

3

Utility Metering

Utility

Legacy System vs AMI Systems

Consumer

Electricity Meter

Cannot communicate

to/from consumer

One-way communication

Utility

AMI

RF MESHPLCBPL

RF MESHPLCBPL

MDMS

Utility MDMS WAN LAN MeteringConsumer

CDMAGSM

CDMAGSM

HAN

In home Display

Two-way communication

Smart Meter

4

AMI Value chain

MDMS

Process and store meter dataMajor PlayersItron, eMeter, SAP

Wide Area Network (WAN) Public/Private

Network

Local Area Network (LAN)

RF mesh, PLC, BPL, WiMax, GPRS

Home Area

Network (HAN) Zigbee, Home plug

WiFi, Z-Wave, Wavenis,

DigitalstromMajor Players

GridConnect, Freescale, MicroChip

Smart Meter

Data collection & storage

Major PlayersGE, Landis+Gyr, PRI,

Elster

System Integrators

Consultants

Installation Contractors

Source: Frost & Sullivan

Major PlayersItron, Elster, SSN, EKA

Systems, Trilliant

Meter Vendors Communication Vendors IT Vendors

5

AMI Technology UpdateIT systems

(GPRS, GSM, EDGE,RF,Power line)

NetworkCommunication

& application servers

Data Management Server( Outage,

Tariffs, Geography)

Meter Management Meter Data Management

Source: Frost & Sullivan

6

Advanced Metering Benefits

Reduced meter reading errors

Reduced billing errorsReduced meter reading costs

Prepayment option

Physical privacy for consumers

Half Hourly usage data

Reduced Energy bills

7

AMI Operational Benefits

Avoided meter reading costs and field services are the two main benefits of AMI

Source: Rochester Gas and Electric Corporation, New York State Electric and Gas Company

8

AMI Features

22

33

44

55

66

77

11

Remote reading and also ability to manually readRemote reading and also ability to manually read

Remote connection and disconnectionRemote connection and disconnection

Two-way communication and Communication path to in-home displayTwo-way communication and Communication path to in-home display

Visual display on meterVisual display on meter

Meter settings reconfiguration (remote)Meter settings reconfiguration (remote)

Tamper detectionTamper detection

Record at least Hourly Usage of dataRecord at least Hourly Usage of data

88

99

1010

1111

Outage notificationOutage notification

Prepayment optionPrepayment option

Time of useTime of use

Load ControlLoad Control

1212 Measurement of active/reactive energy flow (To allow for distributed

generation)

Measurement of active/reactive energy flow (To allow for distributed

generation)

9

2011 2012 20132010 2014

AMI Technology Evolution

2015 2016 2017 2018 2019 2020

Source: Frost & Sullivan.Source: Frost & Sullivan.

Remote Meter Configuration

In-Home Display

Time of use

Demand Response

Energy Management

Systems

Real time communication

Outage Notification

Remote Connect/ Disconnect

Remote meter reading

10

AMI – Communication Technology Options

Communication Options

Communication Options

GPRS, GSM, SMS, WIMAX, UMTS

GPRS, GSM, SMS, WIMAX, UMTS

RF Mesh NetworkRF Mesh Network WIFI, DSLWIFI, DSLPower Line

CarriersPower Line

Carriers

Communication is a vital factor for smart meters

Source: Frost & Sullivan

Wavenis Open

Source Alliance

11

Technology Trends – Communication Technology Penetration

AMI Technologies

AMI Technologies

WiMAXWiMAX

GPRSGPRS

RFRF

2010 2015 2020

PLCPLC

Low Medium High

Source: Frost & Sullivan

12

Lack of Standard Protocols and Interoperability

Initial upfront cost and cost recovery

Advanced Metering - Industry Challenges

Risk on information security clouding consumers judgment

Fear of losing power over load control by the utilities

Source: Frost & Sullivan

Issue of ”Stranded Assets” and evolving technology

13

AMI – Roll out Cost breakdown for Projects

Smart Meter and its installation form the majority of cost involved in AMI implementation

Source: Frost & Sullivan

14

Asia Pacific AMI Market Size

• Total APAC AMI market is expected to generate a cumulative demand of 41 million meter units by 2017

• The market is estimated to generate revenues of about US$12.5 billion from 2009 through 2017

• The market is estimated to have a CAGR of 69.32% for the period from 2009-2017

• The growth will be fuelled by AMI activity in Australia, New Zealand, South Korea, Japan and Taiwan

Source: Frost & Sullivan

Asia Pacific AMI Market size (USD million)

0.00

500.00

1000.00

1500.00

2000.00

2500.00

Year

US

D m

illi

on

0.00%100.00%200.00%300.00%400.00%500.00%600.00%700.00%

% g

row

th

Asia Pacif ic AMI Market Size (USD millions) % grow th

15

20102010 20152015 20202020

DriversDrivers

High Medium Low High Medium Low

ImpactImpact

Drivers and Restraints - Australia

Government Mandate

20102010 20152015 20202020

Rapidly changingtechnology

Restraints

Lack of standards

Rising cost to consumers

Enhanced Customer information

Operational Efficiency

Source: Frost & Sullivan.Source: Frost & Sullivan.

16

Australia

Victorian government is at the forefront of AMI roll out

First to mandate the rollout of smart meters across the state

Victoria and New South Wales are scheduled to complete the rollout by 2013

Source: Frost & Sullivan

Australia AMI market size - 32.6 million USD, 2009

13.04

3.26

Smart Meter Revenue Communication Network Revenue

17

20102010 20152015 20202020

DriversDrivers

High Medium Low High Medium Low

ImpactImpact

Drivers and Restraints – New Zealand

Demand side participation

20102010 20152015 20202020

Rapidly changingtechnology

Restraints

Lack of standards

Ageing workforce

Compliance deadline of 2015

Highly competitive &Deregulated market

Source: Frost & Sullivan.Source: Frost & Sullivan.

18

New Zealand

New Zealand AMI market size - 35 million USD, 2009

14

3.5

Smart Meter Revenue Communication Network Revenue

AMI rollout not regulated by the government

An aggressive market-led rollout

The main network technologies being deployed are RF mesh and GPRS

Source: Frost & Sullivan

19

20102010 20152015 20202020

DriversDrivers

High Medium Low High Medium Low

ImpactImpact

Drivers and Restraints – Taiwan

Reduced energy wastage

20102010 20152015 20202020

Regulation

Restraints

Lack of standards

Lack of funding

Reduction in peak load

Reduction in Green HouseGas emissions

Source: Frost & Sullivan.Source: Frost & Sullivan.

20

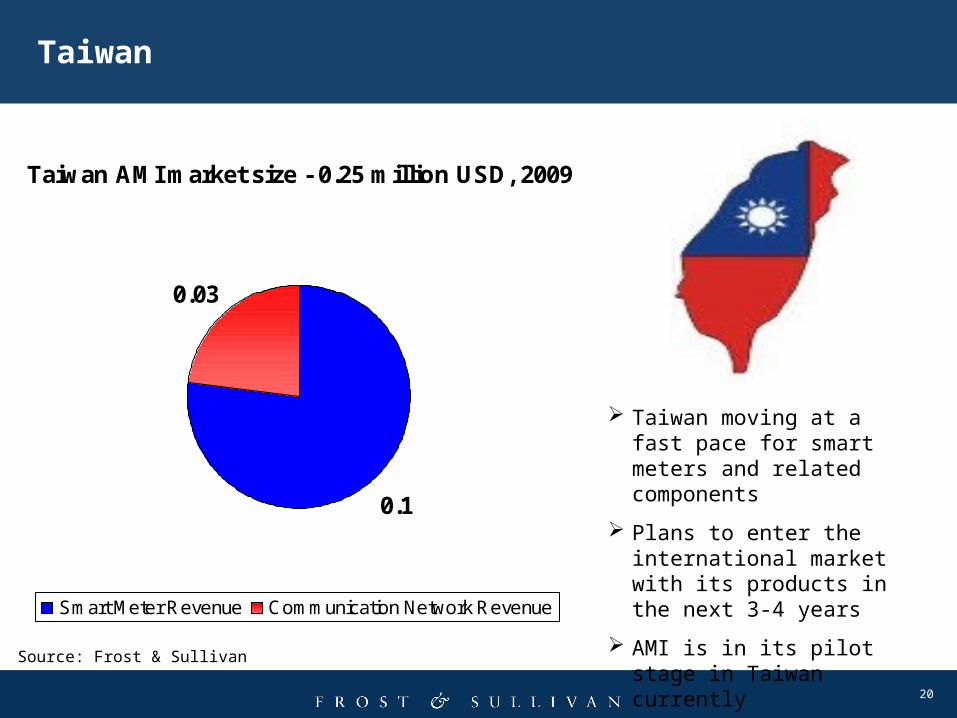

Taiwan

Taiwan moving at a fast pace for smart meters and related components

Plans to enter the international market with its products in the next 3-4 years

AMI is in its pilot stage in Taiwan currently

Taiwan AMI market size - 0.25 million USD, 2009

0.1

0.03

Smart Meter Revenue Communication Network Revenue

Source: Frost & Sullivan

21

20102010 20152015 20202020

DriversDrivers

High Medium Low High Medium Low

ImpactImpact

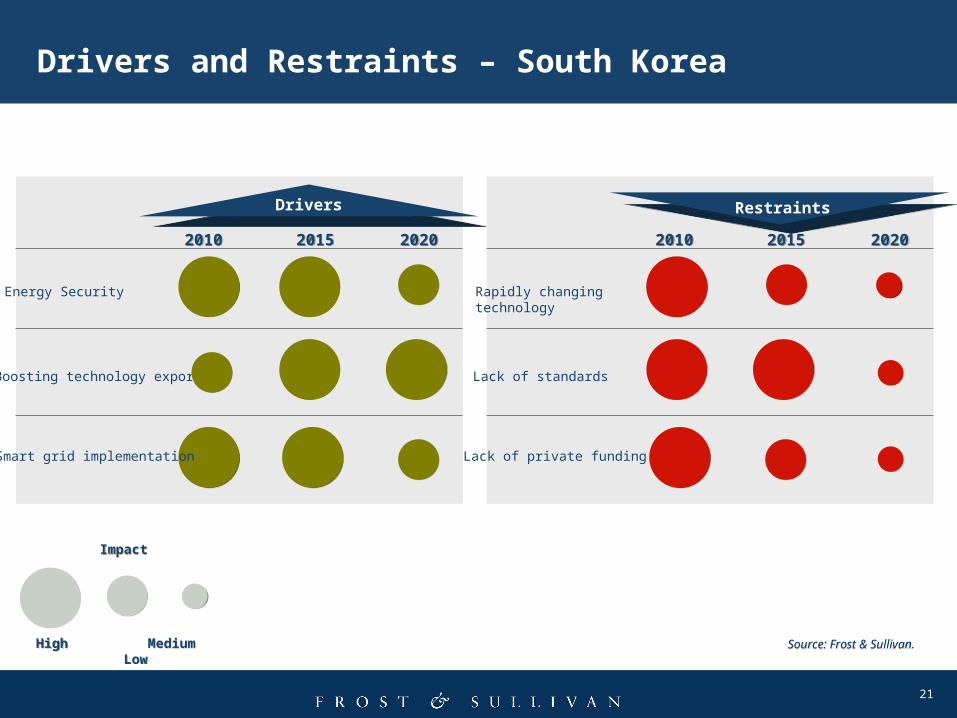

Drivers and Restraints – South Korea

Energy Security

20102010 20152015 20202020

Rapidly changingtechnology

Restraints

Lack of standards

Lack of private funding

Boosting technology export

Smart grid implementation

Source: Frost & Sullivan.Source: Frost & Sullivan.

22

South Korea

South Korea plans to start installing smart meters nationwide by 2012

Lagging behind other developed nations in smart meter deployment (only 4% penetration)

Power Line Carrier (PLC) is the main technology being deployed

South Korea AMI market size - 25 million, 2009

10

2.5

Smart Meter Revenue Communication Network Revenue

Source: Frost & Sullivan

23

20102010 20152015 20202020

DriversDrivers

High Medium Low High Medium Low

ImpactImpact

Drivers and Restraints – Japan

Infrastructure for EVs

20102010 20152015 20202020

No clarity on technology to deploy

Restraints

Efficient grid

Vertically integrated power suppliers

Developing new industries and enhanced services

Integration of renewable energy into grid

Source: Frost & Sullivan.Source: Frost & Sullivan.

24

Japan

AMI activity is just beginning in Japan

Kansai Electric has just started a planned 12 million smart meter rollout

Tokyo Electric is doing a pilot for 90,000 meters

Other utilities in the early stages of pilots/planning

Japan AMI market size 16 million USD , 2009

6.4

1.6

Smart Meter Revenue Communication Network Revenue

Source: Frost & Sullivan

25

Key Growth Markets – SEA/NA & Pacific

Australia

Market size of 4.02 billion USD over the next 9 years

CAGR of 70.45% from 2009-2017

New Zealand

Market size of 525 million USD over the next 9 years

CAGR of 35% from 2009-2017

South Korea

Market size of 3.15 billion USD over the next 9 years

CAGR of 71% from 2009-2017

Japan

Market size of 4.16 billion USD over the next 9 years

CAGR of 85% from 2009-2017

Taiwan

Market size of 600 million USD over the next 9 years

CAGR of 137% from 2009-2017

Source: Frost & Sullivan

26

Summary of Key Findings

The Asia Pacific advanced metering industry is in a nascent stage with rollouts expected to begin around 2011-2012The Asia Pacific advanced metering industry is in a nascent stage with rollouts expected to begin around 2011-2012

The Asia Pacific AMI market will be worth US$12.5 billion through 2017 and is likely to grow at at a CAGR of 69.3%

(2009-2017)The Asia Pacific AMI market will be worth US$12.5 billion through 2017 and is likely to grow at at a CAGR of 69.3%

(2009-2017)

Thailand , Malaysia and Philippines are currently focused only on automated meter reading capabilities for

commercial & industrial consumers. No plans yet for a large scale residential roll outThailand , Malaysia and Philippines are currently focused only on automated meter reading capabilities for

commercial & industrial consumers. No plans yet for a large scale residential roll out

Singapore is expected to begin rollout of AMI around 2015, with basic smart meter functionalitySingapore is expected to begin rollout of AMI around 2015, with basic smart meter functionality

Some of the key drivers for AMI in Asia Pacific include regulatory mandates, choice for customers, technology

upgrades, energy management and a move towards smart grids architectureSome of the key drivers for AMI in Asia Pacific include regulatory mandates, choice for customers, technology

upgrades, energy management and a move towards smart grids architecture

The growth in AMI is fuelled by Australia/New Zealand in the short term & Korea, Japan and Taiwan in the long termThe growth in AMI is fuelled by Australia/New Zealand in the short term & Korea, Japan and Taiwan in the long term

Major market restraints include financing issues, interoperability and lack of standards, limited experience &

reference instatallation s for the technology, and justifying the cost-benefit of AMI roll outMajor market restraints include financing issues, interoperability and lack of standards, limited experience &

reference instatallation s for the technology, and justifying the cost-benefit of AMI roll out

27

Thank YouQ&A