ambit rajan%27s performance aug 25

TRANSCRIPT

8/9/2019 Ambit Rajan%27s Performance Aug 25

http://slidepdf.com/reader/full/ambit-rajan27s-performance-aug-25 1/12

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capitalmay have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision.

Economy

THEMATIC August 25, 2014

Exhibit A: Inflationary expectationshave abated only marginally

Source: RBI, Ambit Capital research

Exhibit B: Rising stressed assets in theIndian banking system

Source: RBI, Ambit Capital research

Exhibit C: The RBI has beenpurchasing USDs since 3QFY15

Source: RBI, Ambit Capital research

Analyst details

Ritika Mankar Mukherjee, [email protected]+91 22 3043 3175

Pankaj Agarwal, [email protected]+91 22 3043 3206

Ravi [email protected]

+91 22 3043 3181

THIS NOTE HAS BEEN WRITTEN FOR AMBIT

CAPITAL’S CLIENTS. IT CANNOT BE REPRODUCED

IN THE MEDIA IN ANY SHAPE OR FORM.

11%

12%

13%

14%

Current 3 monthsahead

1 yr ahead

C P I e x p e c t a t i o n s

( Y o Y c h a n g e ,

i n % )

Sep-13 Dec-13

Mar-14

0

5

10

15

20

F Y 0 8

F Y 0 9

F Y 1 0

F Y 1 1

F Y 1 2

F Y 1 3

F Y 1 4

Std. retructured (%) Total stressed (%)

-20

-10

0

10

20

0 3 / 2 0 1 1

0 7 / 2 0 1 1

1 1 / 2 0 1 1

0 3 / 2 0 1 2

0 7 / 2 0 1 2

1 1 / 2 0 1 2

0 3 / 2 0 1 3

0 7 / 2 0 1 3

1 1 / 2 0 1 3

0 3 / 2 0 1 4

N e t U S D p u r c h a s e s

m a d e b y t h e R B I ( i n

U S D b n )

Dr Raghuram Rajan’s report card

Ahead of the RBI Governor, Dr Raghuram Rajan, completing his firstyear in office, we have rated his performance for the year that was.Contrary to popular perception, our assessment suggests that Dr.Rajan’s performance in office was ‘above average but could have beenbetter’. Whilst his macroeconomic management has been almostexemplary, the RBI’s regulation and supervision of the financial systemcontinues to be sub-par. In particular, in the last six months whilst theRBI has taken decisive steps to close the regulatory arbitrage betweenbanks and NBFCS, the RBI has also made a series of announcementswhich gives more room to banks to massage their asset quality.

Determining the parameters to rate a celebrity GovernorWith India’s most high-profile and arguably most-competent RBI Governor set

to complete a year in office on September 4, 2014, we take on the task ofcreating Raghuram Rajan’s report card for year 1 to objectively assess his

performance thus far. We rate the Governor on four parameters:

Parameter 1: Containing CPI inflation and inflation expectations,

Parameter 2: Regulating and supervising the financial system,

Parameter 3: Promoting inclusive development, and

Parameter 4: Hiring competent personnel and doing so transparently.

These parameters are primarily derived from the goal-setting exercise that theGovernor himself undertook on his first day in office through his first speech as

the 23rd

Governor of the RBI (available at: goo.gl/58dV6D).Contrary to popular perception, our assessment suggests that whilst Dr. Rajan’sperformance has been above average, it could have been better. Whilst theGovernor has been able to make important changes to India’s monetary policyframework (parameter 1), the Governor’s performance on the regulatory front(parameter 2) has been mixed. As regards parameters 3 and 4, hisperformance has been just above par.

Macroeconomic management is clearly Dr Rajan’s forte…Dr. Rajan has lived up to his reputation as a first rate macroeconomist by notonly calmly dealing with the sliding INR a year ago but also focusing the RBIfirmly on fighting inflation (that too measured by CPI, not WPI). By moving theRBI to an informal inflation-targeting regime and by hiking the repo rate by

75bps in 12 months, Dr Rajan has thankfully re-positioned the RBI as aguardian of the value of the INR. However, he has not done enough, which isapparent from the fact that inflation expectations are where they were when hetook charge a year ago (see Exhibit A). As the Fed pulls the US out of QE, theRBI’s resolve to protect the value of the INR looks likely to be tested in the

coming months.

…whilst banking regulation and supervision are more of a struggleWhilst under Dr. Rajan’s leadership, the RBI is sending out a clear message thatthe party is coming to an end for NBFCs that handsomely profit from regulatoryarbitrage, it is notable that over the past six months the RBI has issued a spateof circulars which give further room to banks to massage their asset quality.These circulars will only add to the woes of the Indian banks when they finally

come clean on the real value of their distressed infrastructure assets. With NPAsand restructured assets continuing to rise, Dr. Rajan will have to showconsiderable spine if he is to convince the Finance Ministry to come up with a

credible recap plan for PSU banks.

8/9/2019 Ambit Rajan%27s Performance Aug 25

http://slidepdf.com/reader/full/ambit-rajan27s-performance-aug-25 2/12

Economy

August 25, 2014 Ambit Capital Pvt. Ltd. Page 2

Dr. Rajan’s report card for year 1

Parameter 1: Containing CPI inflation and inflation expectations

Ambit’s rating: 4/5

The most important change that Rajan administered as the RBI’s governor was to

effect a swift transition from being a central bank that ‘loosely targeted both GDPgrowth and WPI inflation’ to one that is now ‘explicitly focussed on targeting CPInflation’. The exhibit below traces the swift changes engineered by Dr. Rajan over theast 12 months to catalyse this iconic change.

Evolution of performance parameter 1 i.e. targeting inflation and inflationExhibit 1:expectations

Source Details

Monetary policy reviewdated July 30, 2014 (i.e.ast policy reviewundertaken by Rajan’spredecessor D Subbarao)

“The objective is to contain headline WPI inflation at around 5.0% in theshort term, and 3.0% over the medium term, consistent with India’s broaderintegration into the global economy.”

RBI Act, 1934 The RBI was constituted to “regulate the issue of Bank notes and the keeping ofreserves with a view to securing monetary stability in India and generally tooperate the currency and credit system of the country to its advantage”.

Rajan’s speech on takingoffice on September 4,2013

“The primary role of the central bank, as the Act suggests, is monetary stability,that is, to sustain confidence in the value of the country’s money. Ultimately,this means low and stable expectations of inflation, whether thatinflation stems from domestic sources or from changes in the value ofthe currency, from supply constraints or demand pressures. I have askedDeputy Governor Urjit Patel, together with a panel he will constitute of outsideexperts and RBI staff, to come up with suggestions in three months on whatneeds to be done to revise and strengthen our monetary policy framework.”

Urjit Patel committeereport (submitted onanuary 21, 2014)

“The nominal anchor or the target for inflation should be set at 4% with a bandof +/- 2% around it…the transition path to the target zone should begraduated to bringing down inflation from the current level of 10% to8% over a period not exceeding the next 12 months and to 6% over a

period not exceeding the next 24 months.”

Monetary policy reviewdated January 28, 2014

“The Dr. Urjit Patel Committee has indicated a ‘glide path’ for disinflation thatsets an objective of below 8% CPI inflation by January 2015 and below 6%CPI inflation by January 2016... An increase in the policy rate will not only beconsistent with the guidance given in the Mid-Quarter Review but also will setthe economy securely on the recommended disinflationary path.”

Source: RBI, Ambit Capital research

The Urjit Patel committee (which was constituted by Dr. Rajan) report noted theoutright superiority of inflation measured through the CPI vs the WPI in its reportsaying that, “The true inflation that consumers face is in the retail market. Althoughprice indices that relate to consumer expenditures are at best imperfect, they are stillclose indicators of the cost of living… The widespread use of the CPI as the major pricendicator reflects its advantages – it is familiar to large segments of the population and

often used in both public and private sectors as a reference in the provision ofgovernment benefits or in wage contracts and negotiations.”

Following the publication of this report, the RBI formally adopted a CPI target onJanuary 28, 2014. Besides improving the monetary policy framework of the RBI, Dr.Rajan has administered repo rate hikes of 75bps over his 12-month tenure. This inturn was accompanied by CPI inflation cooling from 9.8% YoY in September 2013 to8.0% YoY in July 2014 (see the exhibit below).

The most important change thatDr. Rajan administered as theRBI’s governor was to effect a

swift transition from being acentral bank that ‘looselytargeted both GDP growth andWPI inflation’ to one that is now‘explicitly focussed on targetingCPI inflation’

8/9/2019 Ambit Rajan%27s Performance Aug 25

http://slidepdf.com/reader/full/ambit-rajan27s-performance-aug-25 3/12

8/9/2019 Ambit Rajan%27s Performance Aug 25

http://slidepdf.com/reader/full/ambit-rajan27s-performance-aug-25 4/12

Economy

August 25, 2014 Ambit Capital Pvt. Ltd. Page 4

Parameter 2: Regulating and supervising the financial system

Ambit’s rating: 2.5/5

Over the last 12 months, the RBI has been focused on three specific aspects: (1) Actively addressing asset quality challenges in the banking system, (2) Encouragingbetter corporate governance for PSU banks, and (3) Closing the regulatory advantagethat NBFCs have enjoyed, relative to banks, thus far. Whilst the RBI continues to move

at a fairly rapid pace on (3), progress on (1) and (2) has been relatively slow. For moredetails on the RBI’s rapid progress on (3), click here for our 8 August 2014 thematic,‘Closing the regulatory arbitrage’.

Unlike the decisiveness shown by the Governor, who is also a renowned Economist, indramatically altering India’s monetary policy framework, his conviction levels onexecuting (1) and (2) have been low.

Actively addressing asset quality challenges in the banking system

Under the leadership of Rajan, the RBI introduced in February 2014 a newframework for early recognition of stressed assets and the formation of JointLenders Forums (JLFs) to address stress in large-ticket corporate loans bymandating a joint approach by all lenders.

In February, the RBI also eased regulation for banks to facilitate sale of NPAs to Asset Reconstruction Companies (ARCs). However, when the RBI witnessed banksparking their NPAs at ARCs without significant risk transfer, the RBI closed theloopholes in the regulation by asking ARCs to have more skin in the game (15% vs5% earlier) in security receipts (S ` ) issued by them against the NPA they boughtfrom banks. This sort of proactive regulation of banks had rarely been seen in thepre-Rajan world.

The RBI has also closed some of the loopholes which potentially allowed banks to‘evergreen’ stressed loans. For instance, on April 22, 2014, the RBI barredcompanies from repaying domestic loans through funds raised from externalcommercial borrowings (ECBs) from foreign branches of Indian banks.

Furthermore, the RBI told banks to impose restrictions on banks’ foreign branchesin terms of giving guarantees to offshore joint ventures/subsidiaries of Indiancompanies to avail of foreign currency loans to repay rupee credit.

All of that being said, the RBI, has over the past six months, also announced aseries of measures which are intended to help banks manage their stressedexposure to infrastructure projects better. Whilst the RBI’s intentions seem noble,the distinct possibility of India banks abusing these measures to massage theirasset quality cannot be ruled out:

-

On 26 February 2014, the RBI said that “if they [banks] refinance any existinginfrastructure and other project loans by way of take-out financing, even without a pre-determined agreement with other banks/financial institutions,and fix a longer repayment period, the same would not be considered asrestructuring if the following conditions are satisfied: (a) Such loans should be‘standard’ in the books of the existing banks, and should have not beenrestructured in the past; (b) Such loans should be substantially takenover (more than 50% of the outstanding loan by value) from theexisting financing banks/financial institutions; and (c) The repaymentperiod should be fixed by taking into account the life cycle of the project andcash flows from the project.” (The emphasis in bold is ours.) (Source:

goo.gl/6A5wsg).

In a follow-up circular on 7 August 2014, the RBI reduced the minimumrequirement for take-out financing from 50% to 25%.

-

On 14 August 2014, the RBI announced that for project loans: (i) banks may

fund additional ‘Interest during Construction’, which may arise on account ofdelay in completion of a project; and (ii) banks may fund other cost overruns(excluding Interest During Construction) up to a maximum of 10% of the

original project cost (source: goo.gl/HC4kiQ).

Unlike the decisiveness shown bythe governor, who is also arenowned economist, indramatically altering India’smonetary policy framework, hisconviction levels on ‘Activelyaddressing asset qualitychallenges in the banking system’

and ‘Encouraging bettercorporate governance for PSUbanks’ have been low

8/9/2019 Ambit Rajan%27s Performance Aug 25

http://slidepdf.com/reader/full/ambit-rajan27s-performance-aug-25 5/12

Economy

August 25, 2014 Ambit Capital Pvt. Ltd. Page 5

Standing up to political pressure on loan waivers/restructuring

Winning elections by promising loan waivers for farmers is an old trick played byIndian politicians. However, this puts banks under severe risk as borrowers stoprepaying their loans to banks in the hope of getting a waiver. The current stategovernment of Andhra Pradesh also promised a similar waiver during its electioncampaign this year and is now trying to implement this scheme. However, the RBI

did not clear this loan waiver scheme despite immense political pressure. This isin contrast to 2008 when the RBI facilitated the UPA government’s nation-wideloan waiver scheme for farmers.

Encouraging better corporate governance of PSU banks

Raghuram Rajan began his tenure by setting up a committee ‘to review thegovernance of boards of banks in India’. This committee, under the leadership ofPJ Nayak, released a well thought out report on May 13, 2014 (available at:goo.gl/rY5ZRg).

The proposals mentioned in this report created an explicit reform agenda for PSUbanks, including: (a) separating the role of the Chairman from that of the MD; (b)giving guaranteed five-year tenures to the Chairman; (c) creating a PSU bankHoldco where all of the Government’s stakes is PSU banks can be housed; and (d)taking the Government’s stakes in PSU banks down to 40%.

Whilst Dr. Rajan has publicly lauded the report, the Finance Ministry has notuttered a word about the report and the RBI seems unable to implement any ofthe report’s recommendations.

This inertia shown by the RBI when it comes to day-to-day supervision of PSUbanks is also visible elsewhere. For example, neither under Dr. Rajan nor beforehim have we seen even a single instance of the RBI blocking the appointment ofany Board Director for an Indian bank in spite of the Indian press commenting onthe inadequacy of some of the people who are being inserted into the Boards ofPSU banks.

Meanwhile, the life for India’s smashed PSU banks continues as normal with theusual homilies from the Finance Ministry about the need to graduallyprofessionalise these banks.

Closing the regulatory advantage that NBFCs have enjoyed thus far

More than any other RBI Governor in recent history, Raghuram Rajan seems intentupon changing the fabric of financial regulation in India. Under Dr. Rajan’sleadership, the RBI is sending out a clear message that the party is coming to anend for NBFCs who compete head-on with banks and handsomely profit fromregulatory arbitrage.

There have been several regulatory announcements on this front over the last fourmonths: (i) In April 2014, the RBI stopped giving new NBFC licences until it

announces the new NBFC guidelines; (ii) The Finance Ministry removed theregulatory arbitrage between bank deposits and debt mutual funds in July2014; (iii) The RBI allowed banks to raise 7+ year maturity bonds to fundinfra/housing loans with an exemption on the CRR/SLR/PSL requirements in July2014; (iv) The RBI making rules tighter for NBFCs in ”loan against shares”segment in August, 2014.

These announcements seem to be part of a larger scheme of things, as the policyreports published by Dr Rajan (before he became an RBI Governor) and theNachiket Mor committee’s report on financial inclusion have extensively talkedabout closing the regulatory arbitrage between different types of financial

institutions (please click here for our detailed note dated August 8, 2014).

The current state government ofndhra Pradesh also promised a

similar waiver during its electioncampaign this year and is nowtrying to implement this scheme;however, the RBI did not clearthis loan waiver scheme despiteimmense political pressure

8/9/2019 Ambit Rajan%27s Performance Aug 25

http://slidepdf.com/reader/full/ambit-rajan27s-performance-aug-25 6/12

Economy

August 25, 2014 Ambit Capital Pvt. Ltd. Page 6

Parameter 3: Promoting inclusive development

Ambit’s rating: 3/5

Over the last 12 months, the RBI has been focused on three specific aspects in thisregard, namely: (1) Liberalising bank branch l icensing norms, (2) Granting new bankicences, and (3) Reducing regulatory costs for banks. Whilst the RBI has moved

quickly on (1), and (3), progress on (2) has been slow partially due to politicalconsiderations and partially due to resistance from New Delhi (see the exhibit belowfor details). That being said, it is hard to pin too much blame on Dr Rajan for (2) – bythe time he joined the RBI the die was more or less cast in terms of the process to befollowed for the bank licensing process.

The liberalised branch licensing announced in September 2013 has borne fruits andthe total number of branches opened by Indian banks in the Oct-Dec quarter of 2013was almost twice the number of branches opened in similar quarters in the previousthree years.

Performance on parameter 3 i.e. promoting inclusive development andExhibit 4:ncreasing competition in the banking sector

Sub-parameter Performance

Liberalising bank branchicensing norms

Decision: On September 19, 2014, the RBI decided to grant automaticpermission to banks to open branches in tier-1 centres subject to twoconditions: (a) At least 25% of branches opened during the financial year mustbe opened in unbanked rural (tier 5 and tier 6) centres, i.e. centres which donot have a brick-and-mortar structures of any bank for customer-basedbanking transactions and (b) The total number of branches opened in tier-1centres during the financial year cannot exceed the total number of branchesopened in tier 2-6 centres and all centres in the north eastern states andSikkim.

Area for improvement: Given that 65-75% of system deposits originate inurban and metro centres, the competition for low-cost deposits has intensifiedfollowing this move. However, conditions on opening a certain proportion ofnew branches in semi-urban and rural centres continue to apply for banks

which can be eliminated in a phased manner.

Granting new bankicences

Decision: On April 02, 2014 the RBI decided to grant bank licences to twoNBFCs: infra lender, IDFC, and unlisted microfinancelender, Bandhan Financial Services. Then on July 17, 2014, the RBI formallyintroduced the concept of differentiated banking licences in India for licensingof payment banks and small banks. The objective was to make depositsfinancing more competitive and extend the banking services in unbanked andunder-banked areas. Area for improvement: Whilst the RBI under the leadership of Dr Rajan hasbeen trying to increase competition in the banking system, the extent ofcompetition in the banking system remains low, with the largest bankaccounting for more than a fifth of the banking system’s deposits andadvances.The grant of ‘on-tap’ continuous licensing for universal banks as well as thegrant of more types of differentiated bank licenses (like wholesale banks, smallbanks and payment banks) is required to further this agenda moreaggressively.

Reducing regulatory costsor banks

Decision: The RBI under the leadership of Dr Rajan has reduced the SLR by100bps over one year which compares with the 200bps reduction in the SLRadministered by the previous RBI Governor (from the peak of 25%). On July 15,2014, the RBI decided to grant exemption from CRR/SLR requirements for banklending to the infrastructure sector (including affordable housing). Area for improvement: The RBI needs to undertake reforms in priority sectorlending through steps such as allowing an efficiently run rural bank to over-achieve its PSL obligation and sell the excess to other banks to let others focuson their core-competencies.

Source: RBI, Ambit Capital research

Whilst the RBI has moved quicklyon (1), and (3), progress on (2)has been slow partially due to

political considerations and partially due to resistance fromNew Delhi

8/9/2019 Ambit Rajan%27s Performance Aug 25

http://slidepdf.com/reader/full/ambit-rajan27s-performance-aug-25 7/12

Economy

August 25, 2014 Ambit Capital Pvt. Ltd. Page 7

Parameter 4: Hiring competent personnel and doing so transparently

Ambit’s rating: 3/5

Proposals initiated by the new Governor on the recruitment front that are noteworthynclude:

The move to allow lateral hiring from the private sector to expand the RBI’s talent

pool; and

A proposal to professionalise the Human Resource (HR) functions in the ReserveBank, including the creation of a more effective Performance ManagementSystem.

Whilst as yet neither of these steps has resulted in either noteworthy appointments ornoteworthy changes in the RBI, the fact that Dr. Rajan has taken on the vested

nterests inside the RBI and pushed these changes through is in itself laudable.

Less notably, whilst 2 of the 4 Deputy Governors remain the same (namely Urjit Pateland Harun Khan), the other two Deputy Governors – Anand Sinha and Dr KCChakrabarty - have retired:

Anand Sinha has been replaced by RR Gandhi; and

Dr KC Chakrabarty has been replaced by the former Chairman of Bank of Baroda,SS Mundra (see the exhibit below for details).

The RBI’s two new deputy GovernorsExhibit 5:

Critical portfolios held Before Today

Department of BankingOperations and Developmentand Non-BankingSupervision.

Term: Jan 2011-Jan 2014 Anand Sinha was an RBI insider and joined the RBI as a Grade-Bofficer (i.e. an entry-level position).He has a Master’s degree in Physics from IIT, Delhi. His initialtenure was extended by 11 months until January 2014 tosmoothen the process of issue of new bank licences.

RR Gandhi joined the RBI in 1980 and he is an RBIinsider as well.He has a Master’s degree in Economics from AnnamalaiUniversity. During his career at the RBI, Gandhi has builtexpertise in two critical fields namely the Governmentsecurities market and OTC derivatives market.

Department of Bankingsupervision, Currencymanagement, Financial

stability and HumanResources and security

Term: Jun 2009-Mar 2014KC Chakrabarty resigned in March 2014 and was a careerbanker.Before joining the RBI, Chakrabarty worked as the Chairman and

MD of Indian Bank and then Punjab National Bank. During hisfive-year stint as the deputy governor he was temporarily strippedof key portfolios for violating the RBI’s communication policy.

SS Mundra too is a career banker.Before joining the RBI, SS Mundra was the Chairmanand Managing Director of Bank of Baroda (BoB) for

more than a year. Prior to this role, he was the ExecutiveDirector of Union Bank of India. He joined BoB as aprobationary officer in 1977.

Source: RBI, Ambit Capital research

Both these roles require personnel to be recruited from a very limited pool ofcandidates:

The Deputy Governor in charge of the Department of Banking Operations has to

be selected from the pool of RBI executive directors; and

The Deputy Governor in charge of the Department of Banking supervision isrequired to be selected from the pool of serving PSU bank CMDs.

As a result, the choices can seldom reflect the hiring capabilities of the Governor. That

said, two future developments will play a critical role in determining the RBIGovernor’s ability to hire appropriate personnel through transparent procedures:

The RBI is likely to create an additional position of a Chief Operating Officer(COO). It is likely that this post will have the same rank as Deputy Governor.Several policy experts are of the view that this role has been created toaccommodate Nachiket Mor, once a prominent Indian banker who thendedicated himself to working in the area financial inclusion. Mr Mor alsohappens to be the current Governor’s batch mate from the Indian Institute ofManagement (Ahmedabad).

Whilst Mr. Mor may indeed be the ideal person for the role, it will beinteresting to see whether the hiring process for the role is undertakentransparently (i.e. the profile should be advertised in the financial press and

then a wide pool of applications should be solicited).

Dr. Urjit Patel’s term is set to expire on January 10, 2016. Once again, it willbe critical to note whether the hiring process is undertaken transparently.

That said, two future

developments will play a criticalrole in determining the RBIGovernor’s ability to hireappropriate personnel throughtransparent procedures

8/9/2019 Ambit Rajan%27s Performance Aug 25

http://slidepdf.com/reader/full/ambit-rajan27s-performance-aug-25 8/12

Economy

August 25, 2014 Ambit Capital Pvt. Ltd. Page 8

Year 2 is likely to be far more challengingWhilst the Governor has been able to engineer an iconic change in India’s monetarypolicy framework in his first year in office against the backdrop of reduced volatility onthe global macroeconomic front, year 2 in all likelihood will be far more challengingfor two sets of reasons namely, (1) with the Federal Reserve’s quantitative easing

programme likely to be unwound completely in 2HCY14 and the spectre of the Fedhiking interest rates, emerging markets like India could be once again exposed toncreased volatility; and (2) the smashed balance sheets of PSU banks will make life

difficult for the RBI.

Macro turbulence ahead as the Fed unwinds QE and contemplates rate hikes

n his first year in office, the Governor has been able to reform the RBI’smacroeconomic management with some degree of success. Furthermore, hisgovernorship has coincided with reduced volatility in foreign exchange markets (see

the exhibit below).

Rajan’s first year in office saw currency marketExhibit 6:volatility reduce substantially

Source: CEIC, Ambit Capital research

India’s FX reserves are 9x its CAD owing to aExhibit 7:contraction in India’s CAD and an expansion in FX reserves

Source: CEIC, Ambit Capital research

Also, India’s forex reserves now amount to US$315bn or 9x its current account deficitsee Exhibit 7 above). The health of this metric has been partially driven by the factthat India’s CAD has shrunk and also because the RBI has been a net buyer of USDssince 3QFY15 (see the exhibit below).

The RBI has been purchasing USDs since 3QFY15Exhibit 8:

Source: CEIC, Ambit Capital research

Rajan’s first year in office has beenExhibit 9:accompanied by the tailwind of relatively calm globalfinancial markets

Source: CEIC, Ambit Capital research

0%

1%

2%

3%

4%

5%

6%

Sep 2012- Aug 2013 Sep 2013- Aug 2014

C o e f f i c i e n t o f v a r i a t i o n o f

t h e I N R / U S D s p o t r a t e ( i n

% )

0123456789

10

0 3

/ 2 0 1 1

0 6

/ 2 0 1 1

0 9

/ 2 0 1 1

1 2

/ 2 0 1 1

0 3

/ 2 0 1 2

0 6

/ 2 0 1 2

0 9

/ 2 0 1 2

1 2

/ 2 0 1 2

0 3

/ 2 0 1 3

0 6

/ 2 0 1 3

0 9

/ 2 0 1 3

1 2

/ 2 0 1 3

0 3

/ 2 0 1 4

F X r e s e r v e s d i v i d e d b y 4

q u a r t e r m o v i n g s u m m a t i o n

o f C A D ( i n t i m e s )

-15

-10

-5

0

5

10

15

20

0 3

/ 2 0 1 1

0 6

/ 2 0 1 1

0 9

/ 2 0 1 1

1 2

/ 2 0 1 1

0 3

/ 2 0 1 2

0 6

/ 2 0 1 2

0 9

/ 2 0 1 2

1 2

/ 2 0 1 2

0 3

/ 2 0 1 3

0 6

/ 2 0 1 3

0 9

/ 2 0 1 3

1 2

/ 2 0 1 3

0 3

/ 2 0 1 4

N e t U S D p u r c h a s e s m a d e

b y t h e R B I ( i n U S D b n )

0

5

10

15

20

25

30

Subbarao's tenure Rajan's tenure (YTD)

A v e r a e m o n t h l y V I X

Subbarao's tenure Rajan's tenure (YTD)

8/9/2019 Ambit Rajan%27s Performance Aug 25

http://slidepdf.com/reader/full/ambit-rajan27s-performance-aug-25 9/12

Economy

August 25, 2014 Ambit Capital Pvt. Ltd. Page 9

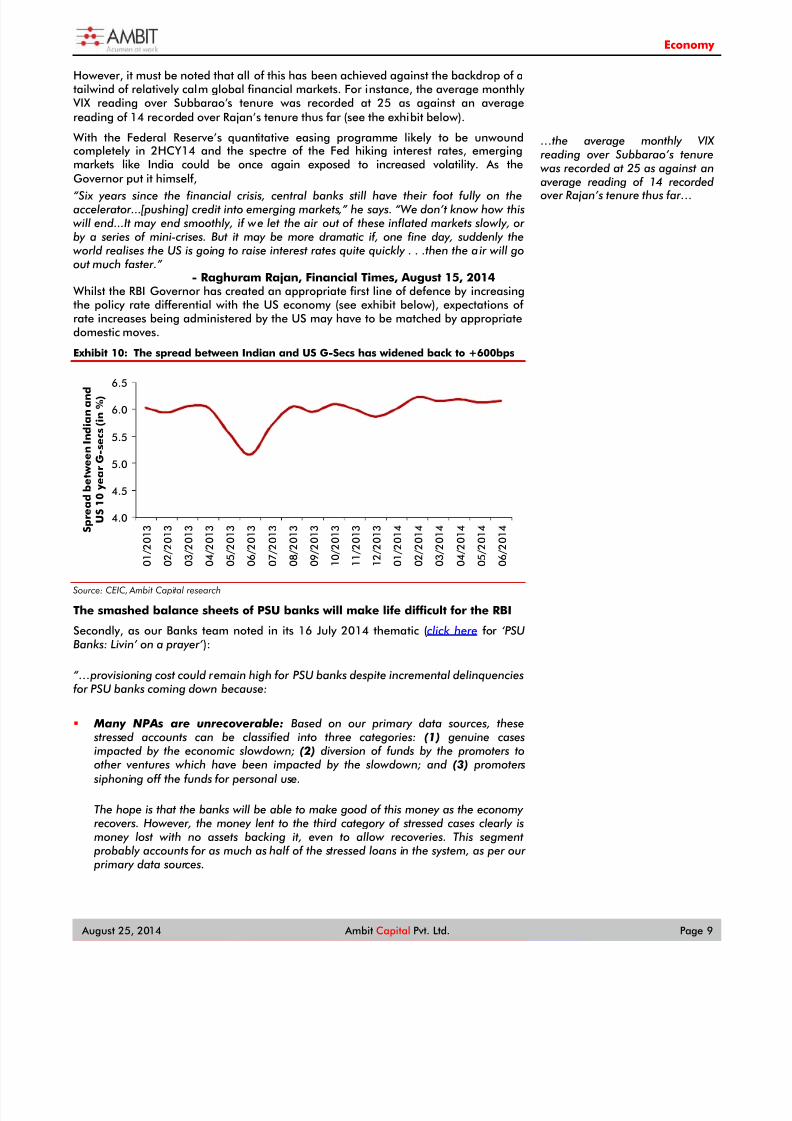

However, it must be noted that all of this has been achieved against the backdrop of atailwind of relatively calm global financial markets. For instance, the average monthlyVIX reading over Subbarao’s tenure was recorded at 25 as against an average

reading of 14 recorded over Rajan’s tenure thus far (see the exhibit below).

With the Federal Reserve’s quantitative easing programme likely to be unwoundcompletely in 2HCY14 and the spectre of the Fed hiking interest rates, emerging

markets like India could be once again exposed to increased volatility. As theGovernor put it himself,

“Six years since the financial crisis, central banks still have their foot fully on theaccelerator...[pushing] credit into emerging markets,” he says. “We don’t know how thiswill end...It may end smoothly, if we let the air out of these inflated markets slowly, orby a series of mini-crises. But it may be more dramatic if, one fine day, suddenly theworld realises the US is going to raise interest rates quite quickly . . .then the air will goout much faster.”

- Raghuram Rajan, Financial Times, August 15, 2014Whilst the RBI Governor has created an appropriate first line of defence by increasingthe policy rate differential with the US economy (see exhibit below), expectations ofrate increases being administered by the US may have to be matched by appropriatedomestic moves.

The spread between Indian and US G-Secs has widened back to +600bpsExhibit 10:

Source: CEIC, Ambit Capital research

The smashed balance sheets of PSU banks will make life difficult for the RBI

Secondly, as our Banks team noted in its 16 July 2014 thematic (click here for ‘PSUBanks: Livin’ on a prayer’):

“…provisioning cost could remain high for PSU banks despite incremental delinquenciesfor PSU banks coming down because:

Many NPAs are unrecoverable: Based on our primary data sources, these stressed accounts can be classified into three categories: (1) genuine casesimpacted by the economic slowdown; (2) diversion of funds by the promoters toother ventures which have been impacted by the slowdown; and (3) promoters

siphoning off the funds for personal use.

The hope is that the banks will be able to make good of this money as the economyrecovers. However, the money lent to the third category of stressed cases clearly ismoney lost with no assets backing it, even to allow recoveries. This segment

probably accounts for as much as half of the stressed loans in the system, as per our primary data sources.

4.0

4.5

5.0

5.5

6.0

6.5

0 1 / 2 0 1 3

0 2 / 2 0 1 3

0 3 / 2 0 1 3

0 4 / 2 0 1 3

0 5 / 2 0 1 3

0 6 / 2 0 1 3

0 7 / 2 0 1 3

0 8 / 2 0 1 3

0 9 / 2 0 1 3

1 0 / 2 0 1 3

1 1 / 2 0 1 3

1 2 / 2 0 1 3

0 1 / 2 0 1 4

0 2 / 2 0 1 4

0 3 / 2 0 1 4

0 4 / 2 0 1 4

0 5 / 2 0 1 4

0 6 / 2 0 1 4 S

p r e a d b e t w e e n I n d i a n a n d

U S 1 0 y e a r G - s e c s ( i n % )

…the average monthly VIXreading over Subbarao’s tenure

was recorded at 25 as against anaverage reading of 14 recordedover Rajan’s tenure thus far…

8/9/2019 Ambit Rajan%27s Performance Aug 25

http://slidepdf.com/reader/full/ambit-rajan27s-performance-aug-25 10/12

Economy

August 25, 2014 Ambit Capital Pvt. Ltd. Page 10

Provisioning cycle lags NPA accretion cycle: Moreover, the experience from thelast credit cycle (1998-2003) shows that though banks’ stressed assets had startedcoming off from 1998 onwards, credit costs kept on increasing until 2004, as bankshad to resort to aggressive write-offs during this period.

Exhibit 11: Credit cost and stressed assets ratio for the banking system

Source: RBI, Company, Ambit Capital research

Even in the last cycle, the stressed sectors (such as iron & steel, construction and textiles)were similar to the currently stressed sectors, with the infra sector being a new stressedsector. Hence, we believe that provisioning costs would remain high for PSU banks overthe next 2-3 years.

Taking account of these elevated levels of stress, the total tier-1 capital requirement forall the PSU banks combined could be anywhere between US$40bn-50bn (excludingretained earnings) over the next five years.”

Given that this amount of around US$45bn forms around 85% of the PSU banks’current market cap (and as high as 300% of the market cap for the more beleagueredPSU banks), Dr. Rajan will have to show considerable spine if he is to convince the

Finance Ministry to come up with a credible recap plan for PSU banks. Without such arecap plan it is hard to understand how, even in FY16, Indian credit growth can movetowards the 20% per annum region (vs 13% currently), thus lifting GDP growth northof 6%.

0%

2%

4%

6%

8%

10%

12%

14%16%

0.0%

0.5%

1.0%

1.5%

2.0%

F Y 9 8

F Y 9 9

F Y 0 0

F Y 0 1

F Y 0 2

F Y 0 3

F Y 0 4

F Y 0 5

F Y 0 6

F Y 0 7

F Y 0 8

F Y 0 9

F Y 1 0

F Y 1 1

F Y 1 2

F Y 1 3

F Y 1 4

Credit cost (LHS) Gross NPLs + restructured (RHS)

Given that around US$45bnforms around 85% of the PSUbanks’ current market cap (and

as high as 300% of market capfor the more beleaguered PSUbanks), Dr. Rajan will have to

show considerable spine if he isto convince the Finance Ministryto come up with a credible recap

plan for PSU banks

8/9/2019 Ambit Rajan%27s Performance Aug 25

http://slidepdf.com/reader/full/ambit-rajan27s-performance-aug-25 11/12

Economy

August 25, 2014 Ambit Capital Pvt. Ltd. Page 11

Institutional Equities Team

Saurabh Mukherjea, CFA CEO, Institutional Equities (022) 30433174 [email protected]

Research

Analysts Industry Sectors Desk-Phone E-mail

Nitin Bhasin - Head of Research E&C / Infrastructure / Cement (022) 30433241 [email protected]

Aadesh Mehta Banking / Financial Services (022) 30433239 [email protected]

Achint Bhagat Cement / Infrastructure (022) 30433178 [email protected]

Aditya Khemka Healthcare (022) 30433272 [email protected]

Akshay Wadhwa Banking & Financial Services (022) 30433005 [email protected]

Ashvin Shetty, CFA Automobile (022) 30433285 [email protected]

Bhargav Buddhadev Power / Capital Goods (022) 30433252 [email protected]

Dayanand Mittal, CFA Oil & Gas / Metals & Mining (022) 30433202 [email protected]

Deepesh Agarwal Power / Capital Goods (022) 30433275 [email protected]

Gaurav Mehta, CFA Strategy / Derivatives Research (022) 30433255 [email protected]

Karan Khanna Strategy (022) 30433251 [email protected]

Krishnan ASV Real Estate (022) 30433205 [email protected]

Pankaj Agarwal, CFA Banking / Financial Services (022) 30433206 [email protected]

Paresh Dave Healthcare (022) 30433212 [email protected]

Parita Ashar Metals & Mining / Oil & Gas (022) 30433223 [email protected]

Pratik Singhania Retail (022) 30433264 [email protected]

Rakshit Ranjan, CFA Consumer / Retail (022) 30433201 [email protected]

Ravi Singh Banking / Financial Services (022) 30433181 [email protected]

Ritesh Vaidya Consumer (022) 30433246 [email protected]

Ritika Mankar Mukherjee, CFA Economy / Strategy (022) 30433175 [email protected]

Ritu Modi Automobile (022) 30433292 [email protected]

Sagar Rastogi Technology (022) 30433291 [email protected]

Sumit Shekhar Economy / Strategy (022) 30433229 [email protected]

Tanuj Mukhija, CFA E&C / Infrastructure (022) 30433203 [email protected]

Utsav Mehta Technology (022) 30433209 [email protected]

Sales

Name Regions Desk-Phone E-mail

Sarojini Ramachandran - Head of Sales UK +44 (0) 20 7614 8374 [email protected]

Deepak Sawhney India / Asia (022) 30433295 [email protected]

Dharmen Shah India / Asia (022) 30433289 [email protected]

Dipti Mehta India / USA (022) 30433053 [email protected]

Nityam Shah, CFA USA / Europe (022) 30433259 [email protected]

Parees Purohit, CFA UK / USA (022) 30433169 [email protected]

Praveena Pattabiraman India / Asia (022) 30433268 [email protected]

Production

Sajid Merchant Production (022) 30433247 [email protected]

Sharoz G Hussain Production (022) 30433183 [email protected]

Joel Pereira Editor (022) 30433284 [email protected]

Nikhil Pillai Database (022) 30433265 [email protected]

E&C = Engineering & Construction

8/9/2019 Ambit Rajan%27s Performance Aug 25

http://slidepdf.com/reader/full/ambit-rajan27s-performance-aug-25 12/12