altiero spinelli building, brussels 9.00-11.40 room: asp ......by kalin a. anev, secretary general,...

TRANSCRIPT

European Stability Mechanism

European Financial Stability Facility

European Financial Stabilisation Mechanism

Budgetary control ofefSf/efSM/eSM

Chairman: Michael TheurerRapporteur: Iliana Ivanova

Designed by CLIENTS AND PROJECTS OFFICE, Intranet Services Unit | Printed by Printing Unit | DG ITEC, EDIT Directorate IPOL/30466

Public HearingCOMMITTEE ON BUDGETARY CONTROL

Tuesday 24.4.2012alTiero spinelli BuildinG, Brussels9.00-11.40 rooM: aSP 3g2

DV\897514EN.doc PE486.142v01-00

EN EN

EUROPEAN PARLIAMENT 2009 - 2014

Committee on Budgetary Control

PROGRAMME

Hearing on

"Budgetary control of the European Financial Stability Facility (EFSF), the European Financial Stabilisation Mechanism (EFSM) and the European

Stability Mechanism (ESM)"

Rapporteur: Iliana Ivanova (EPP)

Tuesday 24 April 2012, from 9.00 to 11.40

Brussels

Room: Altiero Spinelli (3G-2)

9.00 - 9.055 min

Opening remarks

by the Chairman

9.05 - 9.105 min

Introduction

by Iliana Ivanova, rapporteur

9.10 - 9.2010 min

Presentation of the study"The liability of the EU Budget concerning the EFSM and the ESM and interference on budget control by the European Parliament"

by Roland Jeanquart, Partner PwC Belgium

9.20 - 9.4020 min Questions, replies, debate

PE486.142v01-00 2/2 DV\897514EN.doc

EN

9.40 - 9.5010 min

Public accountability and control of the EFSF and the ESM- the role of the manager

- Accountability and transparency arrangements- Financial control arrangements- Internal audit arrangements

by Kalin A. Anev, Secretary General, European Financial Stability Facility

9.50 - 10.0010 min

Public accountability and control of the EFSF, the EFSM and the ESM - the role of the European Commission

- Accountability and transparency arrangements- Measures in place to safeguard the EU Budget

by Marco Buti, Director-General of Directorate General Economic and Financial Affairs

10.00 - 10.3030 min Questions, replies, debate

10.30 - 10.4010 min

External audit of the mechanisms - a European perspective

- Audit opportunities and challenges from a European perspective

by Vítor Manuel da Silva Caldeira, President of the European Court of Auditors

10.40 - 10.5010 min

External audit of the mechanisms - a national perspective

- Audit opportunities and challenges from a German perspective

by Horst Erb, Senior Audit Director and Member of the Bundesrechnungshof, Head of Division for liaison with the national Parliament's Public Accounts Committee, acting for the President of the Bundesrechnungshof, Prof. Dr. Dieter Engels

10.50 - 11.0010 min

External audit of the mechanisms - a national perspective

- Audit opportunities and challenges from a Dutch perspective

by Kees Vendrik, Vice-President of the Dutch Court of Audit

11.00 - 11.3030 min Questions, replies, debate

11.30 - 11.4010 min

Closing remarks and possible next step

by Iliana Ivanova, rapporteur

1. Introduction by Iliana Ivanova - Rapporteur

Hearing on Budgetary Control on the EFSF, the EFSM and the ESM - 24 April 2012 Committee on Budgetary Control

DT\897399EN.doc PE486.113v01-00

EN United in diversity EN

EUROPEAN PARLIAMENT 2009 - 2014

Committee on Budgetary Control

27.3.2012

WORKING DOCUMENTfor the hearing of 24 April 2012 on "Budgetary control of EFSF, EFSM andESM"

Committee on Budgetary Control

Rapporteur: Iliana Ivanova

PE486.113v01-00 2/4 DT\897399EN.doc

EN

This Working Document sets out the considerations of the Rapporteur in view of the hearing that will take place on 24 April 2012 on the "Budgetary control of EFSF, EFSM and ESM".

Background

In May 2010 the European Council decided to establish, based on Art. 122 of the TFEU, two temporary instruments for financial assistance to Member States experiencing financial difficulties - the European Financial Stabilisation Mechanism (EFSM) and the European Financial Stability Facility (EFSF). These two temporary mechanisms will be replaced by a permanent mechanism (European Stability Mechanism (ESM)) which will become operational in July 2012.

Budgetary control - state of play

EFSM & EFSF

The EFSM was created by Council Regulation 407/2010 which grants the Commission the right to borrow up to a total of EUR 60 bn at the capital markets and to lend them to a Member State of the euro zone experiencing difficulties. As the loans under the EFSM are backed up by the EU budget, the European Parliament scrutinises the Commission's actions with regards to the EFSM. Furthermore, the European Parliament could exercise control overthe Commission's operations in the context of the budget and the discharge procedures. However, the European Parliament is not accorded with any direct decision power for granting assistance under this mechanism. As far as the external audit is concerned the European Court of Auditors could perform financial and performance audits to all borrowing and lending activities of the Commission as regards the EFSM.

The EFSF was created as a Special Purpose Vehicle which is backed up by guarantee commitments from the euro zone Member States for a total of EUR 780 bn and has a lending capacity of EUR 440 bn. The democratic control of national governments' actions with regard to the EFSF is ensured by the National parliaments. Thus the European Parliament is not at all involved in this process. Furthermore the EFSF does not include any audit rights for the Supreme Audit Institutions (SAIs) at all and lacks of provisions on external public audit.

ESM

The ESM will be an international financial institution established by European treaty1. It will be financed through paid-in capital of EUR 80 bn and callable capital of EUR 620 bn. There are on-going discussions about granting the ESM with a banking licence which would allow it to be funded by the European Central Bank but also to fall under the banking regulatory supervision.The European Parliament pointed out in its resolution of 23 March 20112 that the establishment of the ESM outside the Union's institutional framework could create problems related to the control mechanism of the Union's institutions. Furthermore concerns were 1 See Treaty establishing the European Stability Mechanism http://www.europeancouncil.europa.eu/media/582311/05-tesm2.en12.pdf2 See European Parliament resolution of 23 March 2011 on the draft European Council decision amending Article 136 of the Treaty on the Functioning of the European Union with regard to a stability mechanism for Member States whose currency is the euro (P7_TA(2011)0103)

DT\897399EN.doc 3/4 PE486.113v01-00

EN

expressed by some of the SAIs that the Treaty lacks sufficient provisions for ensuring effective external audit. According to the last version of the Treaty establishing the ESM, the external public audit of the mechanism will be carried out by a Board of Auditors1. The ECA will be a permanent Member of this board alongside with two other SAIs appointed on a rotational basis and two further Members without specifying their background2. But even if the ECA is involved on a permanent basis in the external auditing process, the annual audit report of the Board of Auditors will only be reported to the Board of Governors of the ESM. Moreover the Board of Governors will then send this report to National parliaments and the SAIs only3. Neither the European Parliament nor the general public are envisaged as addressees.

Conclusions

The Declaration of the Rights of Man and of the Citizen of 1789 states in its Article 15 that "The society has the right to require of every public agent an account of his administration"4. Transposed into current times, this could be understood that all taxpayers' money should be subject to adequate public audit and adequate parliamentary scrutiny. Moreover According to the Lima Declaration5, “All public financial operations, regardless of whether and how they are reflected in the national budget, shall be subject to audit by Supreme Audit Institutions. Excluding parts of financial management from the national budget shall not result in these parts being exempted from audit by the Supreme Audit Institution. “

For all three instruments there is currently a lack of sufficient coordination of responsibilities, both in terms of democratic scrutiny and also in terms of audit rights of Supreme Audit Institutions (SAIs).

Points for further considerations

The Rapporteur would like to emphasise on the following questions:

1. The Rapporteur is of the opinion that Art. 30 of the ESM Treaty presents serious weaknesses related to the adequacy of the external audit which have been identified in the following documents:

- Resolution of the Contact committee of the SAIs of the EU dated 14 October 2011 on the Statement of SAIs of the euro area on the external audit of the ESM6

- Letter from the President of the Netherlands Court of Audit on issues to be addressed in the by-laws of the ESM with regard to Article 30 of the ESM Treaty7

1 See Art. 29 of the Revised ESM Treaty, 2 February 20122 See Art.30 (1) of the Revised ESM Treaty, 2 February 20123 See Art. 30 (5) of the Revised ESM Treaty, 2 Febraury 2012 4 See Art. 15 "La société a le droit de demander compte à tout agent public de son administration"5 See The Lima Declaration, http://www.issai.org/media%28622,1033%29/ISSAI_1_E.pdf6 See http://eca.europa.eu/portal/pls/portal/docs/1/9406723.PDF7http://www.courtofaudit.com/english/News/2012/02/Letter_of_president_Netherlands_Court_of_Audit_on_ESM_Board_of_Auditors

PE486.113v01-00 4/4 DT\897399EN.doc

EN

The by-laws of the ESM are still under negotiation and therefore the Member States and the Council should use them in order to fix these shortcomings and to elaborate appropriate arrangements for public external audit of legality, regularity as well as performance.

2. According to the last version of the ESM Treaty, signed on 2 February 2012, the Commission and the ECB will carry out important tasks such as "monitoring compliance with the conditionality attached to the financial assistance facility"1. These activities could be subject to an audit of the ECA in line with the ECA's audit rights as laid down in Articles 285-287 of the TFEU. This could create an opportunity to scrutinize this part of ESM-related work by the European Parliament.

3. The "Governance package" adopted in 2011 stipulates that in case of interests and fines collected from Member States whose currency is the euro they should be channelled through the EU budget to the ESM2. The transferred funds could also be subject to a possible audit of the ECA.

4. In case of granting a banking licence to the ESM, the ESM should become subject to banking regulatory supervision

5. In view of the political scrutiny that the European Parliament will exercise in the ESM it should be granted the same level of access to information as the National Parliaments.

1 Art. 13 (7) of the Revised ESM Treaty, 02 February 20122 See, for example, Art. 10 of Regulation No. 1173/2011 on the effective enforcement of budgetary surveillance in the euro area

2. Presentation of the study:

"The liability of the EU Budget concerning the EFSM and the ESM and interference on budget control by the European Parliament"

by Roland Jeanquart, Partner PwC Belgium

Hearing on Budgetary Control on the EFSF, the EFSM and the ESM- 24 April 2012 Committee on Budgetary Control

3. Public accountability and control of the EFSF and

the ESM - the role of the manager by Kalin A. Anev, Secretary General, European

Financial Stability Facility

Hearing on Budgetary Control on the EFSF, the EFSM and the ESM - 24 April 2012 Committee on Budgetary Control

“Accountability and control of the EFSF and ESM’’

European Parliament Committee on Budgetary Control

Kalin Anev, Secretary General of EFSF

Brussels, 24 April 2012

1

EFSF 1: The establishment of a crisis resolution mechanism in May 2010

European Financial Stabilisation Mechanism

“EFSM”

€60 bn

Available to all 27 EU member states

€750bn Financial Stability Package

European Financial Stability Facility

“EFSF”

€440 bn (lending capacity)

For euro area Member States

International Monetary Fund

€250 bn max

Up to half the amount drawn from EFSF and EFSM

2

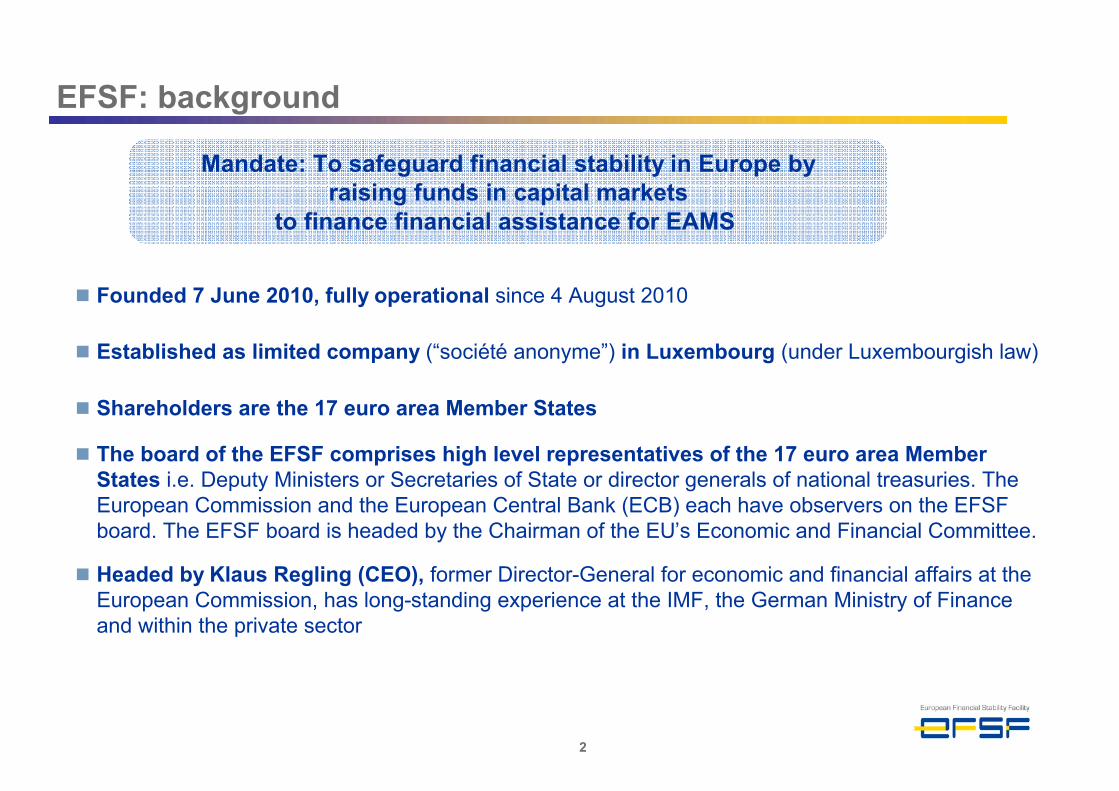

EFSF: background

Founded 7 June 2010, fully operational since 4 August 2010

Established as limited company (“société anonyme”) in Luxembourg (under Luxembourgish law)

Shareholders are the 17 euro area Member States

The board of the EFSF comprises high level representatives of the 17 euro area Member States i.e. Deputy Ministers or Secretaries of State or director generals of national treasuries. The European Commission and the European Central Bank (ECB) each have observers on the EFSF board. The EFSF board is headed by the Chairman of the EU’s Economic and Financial Committee.

Headed by Klaus Regling (CEO), former Director-General for economic and financial affairs at the European Commission, has long-standing experience at the IMF, the German Ministry of Finance and within the private sector

Mandate: To safeguard financial stability in Europe byraising funds in capital markets

to finance financial assistance for EAMS

3

Member States Credit rating (S&P/Moodys/Fitch)

New EFSF maximum guarantee

Commitments (€m)

New EFSF contribution

key (%)

New EFSF maximum guarantee

commitments (PT, GR, IE stepped out)

New EFSF contribution key in % (PT, GR, IE

stepped out)Austria (AA+/Aaa/AAA) 21,639.19 2.78 21,639.19 2.99Belgium (AA/Aa3/AA) 27,031.99 3.47 27,031.99 3.72Cyprus (BB+/Ba1/BBB-) 1,525.68 0.20 1,525.68 0.21Estonia (AA-/A1/A+) 1,994.86 0.26 1,994.86 0.27Finland (AAA/Aaa/AAA) 13,974.03 1.79 13,974.03 1.92France (AA+/Aaa/AAA) 158,487.53 20.31 158,487.53 21.83

Germany (AAA/Aaa/AAA 211,045.90 27.06 211,045.90 29.07Greece (SD/C/B-) 21,897.74 2.81 0.00 0.00Ireland (BBB+/Ba1/BBB+) 12,378.15 1.59 0.00 0.00Italy (BBB+/A3/A-) 139,267.81 17.86 139,267.81 19.18Luxembourg (AAA/Aaa/AAA) 1,946.94 0.25 1,946.94 0.27

Malta (A-/A3/A+) 704.33 0.09 704.33 0.10

Netherlands (AAA/Aaa/AAA) 44,446.32 5.70 44,446.32 6.12Portugal (BB/Ba3/BB+) 19,507.26 2.50 0.00 0.00Slovakia (A/A2/A+) 7,727.57 0.99 7,727.57 1.06

Slovenia (A+/A2/A) 3,664.30 0.47 3,664.30 0.51Spain (A/A3/A) 92,543.56 11.87 92,543.56 12.75Total 779,783.14 100 726,000.01 100

In case a country steps out, contribution keys would be readjusted among remaining guarantors and the guarantee committee amount would decrease accordingly.

EFSF shareholder contribution

4

EFSF 2: mission and scope of activity

Scope of activity, linked to appropriate conditionality

Provide loans to euro area Member States in financial difficulties

Intervene in the debt primary market

Intervene in the secondary bond markets

Act on the basis of a precautionary programme

Finance recapitalisation of financial institutions through loans to governments including in non programme countries

To fulfil its mission, EFSF issues bonds or other debt instruments on the capital markets

Mission : to safeguard financial stability in Europe by providing financial assistance to euro area Member States

5

2

EFSF: Budget, reporting and internal audit

6

EFSF: Budgetary procedure

Annual financial forecast and budget are presented for approval by Chief Executive Officer to the Board of Directors at the end of the preceding year (Budget 2012 was approved 17 November 2011)

The approved budget is monitored and discussed on a monthly basis by the Financial Committee (Chief Financial Officer, Secretary General, Director of Research and Institutional Relations, Chief Risk Officer and Head of Audit), the report, analysis and variances are reported to the Chief Executive Officer.

The financial activities are monitored and reported on a daily basis (daily P&L, investments P&L, accounting, ALM and Risk management)

Board of Directors are regularly updated on the state of the budget (actual figures versus approved budget ) and in case of potential deviation or new strategic development (e.g. new long term investments) the Board of Directors are consulted

7

EFSF: External Audit EFSF falls under the Law of 10th August, 1915 on commercial companies, companies

incorporated under Luxembourg Law must have their annual accounts audited by one or more external auditor.

Accounting standards: EFSF is fully IFRS compliant

The EFSF annual accounts and the financial statement are audited by PwC, an independent external audit firm. External auditors provide assurance on the truth and fairness of financial information. The audit scope principally covers:

testing on evidence of amounts and disclosures presented on the annual accounts,

review of complex transaction processing,

review of controls and policies,

confirmation of accounting treatments

External Auditor’s report is part of the year-end Financial Statement submitted to the Board of Directors and approved by Annual General Meeting. The Annual Report is then deposited in the commercial register and publically accessible

On a voluntary basis, EFSF has also requested PwC to perform semi-annual account reviews

8

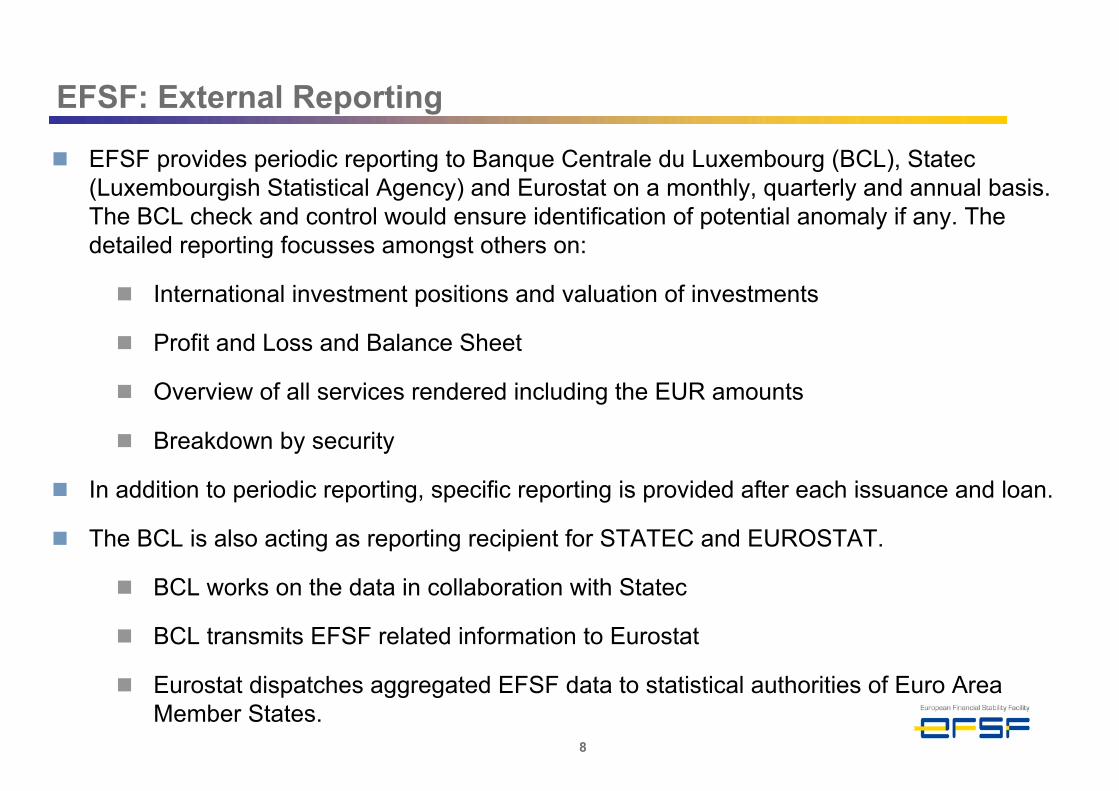

EFSF: External Reporting

EFSF provides periodic reporting to Banque Centrale du Luxembourg (BCL), Statec (Luxembourgish Statistical Agency) and Eurostat on a monthly, quarterly and annual basis. The BCL check and control would ensure identification of potential anomaly if any. The detailed reporting focusses amongst others on:

International investment positions and valuation of investments

Profit and Loss and Balance Sheet

Overview of all services rendered including the EUR amounts

Breakdown by security

In addition to periodic reporting, specific reporting is provided after each issuance and loan.

The BCL is also acting as reporting recipient for STATEC and EUROSTAT.

BCL works on the data in collaboration with Statec

BCL transmits EFSF related information to Eurostat

Eurostat dispatches aggregated EFSF data to statistical authorities of Euro Area Member States.

9

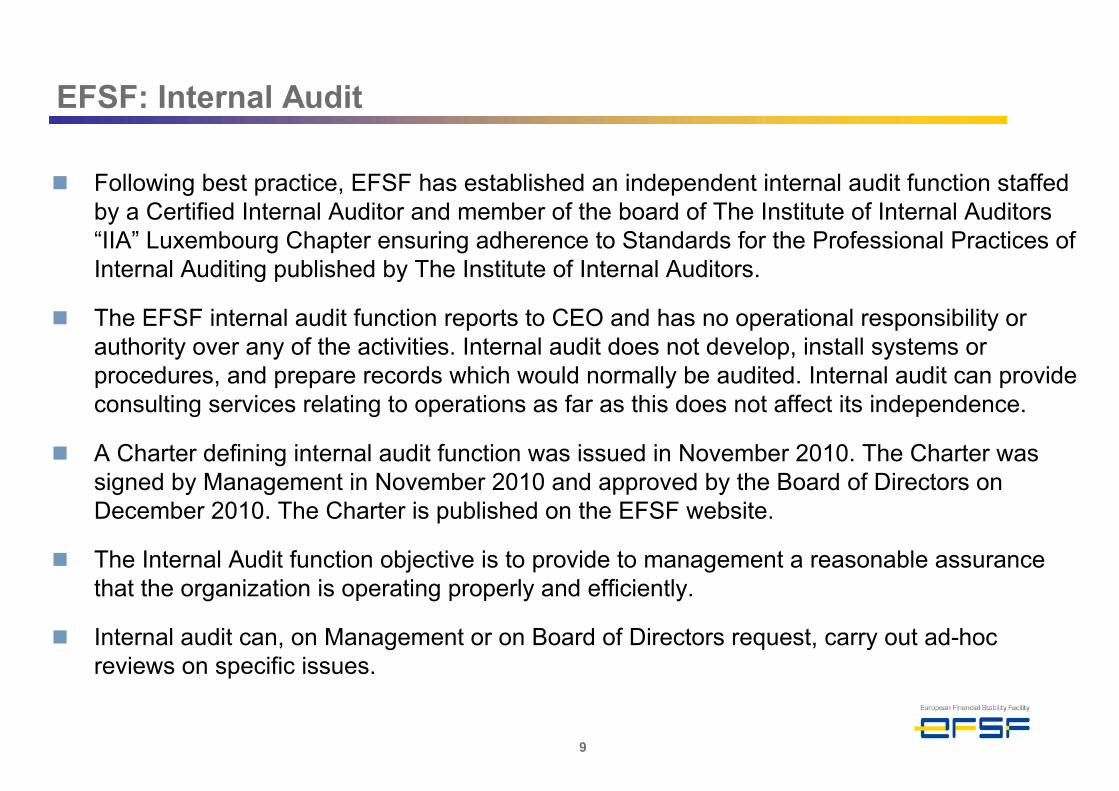

EFSF: Internal Audit

Following best practice, EFSF has established an independent internal audit function staffed by a Certified Internal Auditor and member of the board of The Institute of Internal Auditors “IIA” Luxembourg Chapter ensuring adherence to Standards for the Professional Practices of Internal Auditing published by The Institute of Internal Auditors.

The EFSF internal audit function reports to CEO and has no operational responsibility or authority over any of the activities. Internal audit does not develop, install systems or procedures, and prepare records which would normally be audited. Internal audit can provide consulting services relating to operations as far as this does not affect its independence.

A Charter defining internal audit function was issued in November 2010. The Charter was signed by Management in November 2010 and approved by the Board of Directors on December 2010. The Charter is published on the EFSF website.

The Internal Audit function objective is to provide to management a reasonable assurance that the organization is operating properly and efficiently.

Internal audit can, on Management or on Board of Directors request, carry out ad-hoc reviews on specific issues.

10

EFSF: Functions and responsibilities of Internal Audit Provide assistance in defining control during the initial setup of internal procedures of lending &

funding activities

Provide assistance to business on control assessment during operational transaction testing exercise

Assist Management in developing and the implementing signatory limit policy

Liaise with Corporate Governance officer on internal rules and procedure implementation

Liaise with Finance & Budget officer and accounting external provider to control accuracy and reliability of data generated

Advice and support Finance & Budget, Risk Management, accounting external provider and external auditor during financial statement semi-annual and year end audit

Perform regular control of regulatory reporting and liaise with Finance & Budget officer, external provider and Luxembourg Central Bank

Coordinate Business Continuity Planning aspect with external provider including IT and security aspect

Draft the audit plan for EFSF. The internal audit adopts a risk-based approach to prioritizing activities/processes within the organization for purposes of allocating audit resources.

11

2

European Stability Mechanism (ESM)

12

Creation of a permanent crisis resolution mechanism

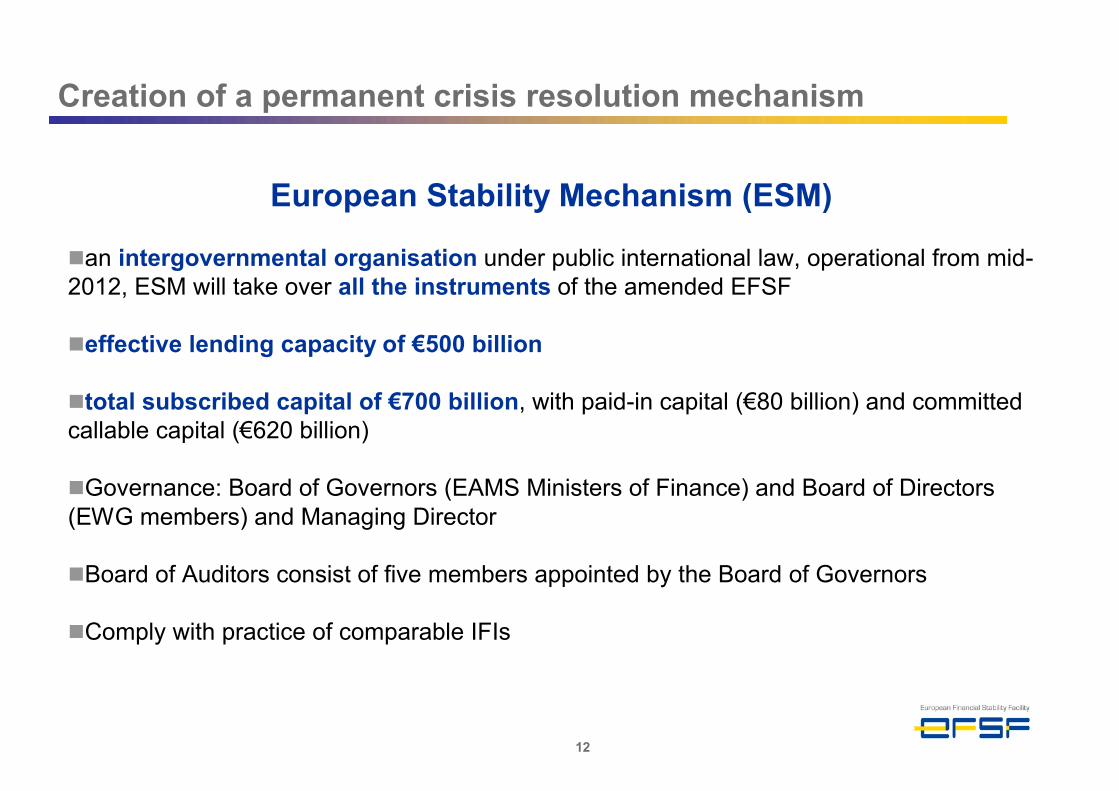

European Stability Mechanism (ESM)

an intergovernmental organisation under public international law, operational from mid-2012, ESM will take over all the instruments of the amended EFSF

effective lending capacity of €500 billion

total subscribed capital of €700 billion, with paid-in capital (€80 billion) and committed callable capital (€620 billion)

Governance: Board of Governors (EAMS Ministers of Finance) and Board of Directors (EWG members) and Managing Director

Board of Auditors consist of five members appointed by the Board of Governors

Comply with practice of comparable IFIs

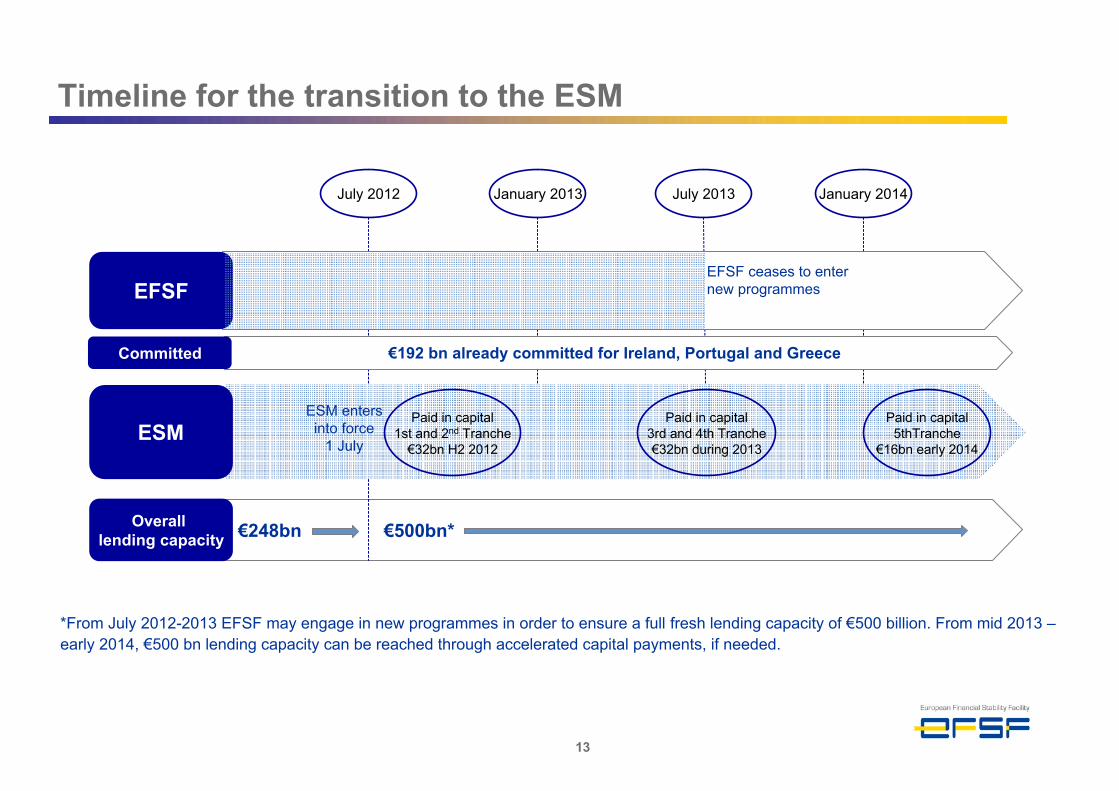

€192 bn already committed for Ireland, Portugal and Greece

13

Timeline for the transition to the ESM

*From July 2012-2013 EFSF may engage in new programmes in order to ensure a full fresh lending capacity of €500 billion. From mid 2013 –early 2014, €500 bn lending capacity can be reached through accelerated capital payments, if needed.

ESM enters into force

1 July

Paid in capital1st and 2nd Tranche

€32bn H2 2012

July 2012 January 2013

Paid in capital3rd and 4th Tranche€32bn during 2013

July 2013

EFSF ceases to enter new programmes

January 2014

Paid in capital5thTranche

€16bn early 2014

€248bn €500bn*

EFSF

Overall lending capacity

ESM

Committed

14

Article 26 Budget: The Board of Directors shall approve the ESM budget annually.

Article 27 Annual accounts:

1. The Board of Governors shall approve the annual accounts of the ESM.

2. The ESM shall publish an annual report containing an audited statement of its accounts and shall circulate to ESM Members a quarterly summary statement of its financial position and a profit and loss statement showing the results of its operations.

Article 28 Internal Audit: An internal audit function shall be established according to international standards.

Article 29 External audit: The accounts of the ESM shall be audited by independent external auditors approved by the Board of Governors and responsible for certifying the annual financial statements. The external auditors shall have full power to examine all books and accounts of the ESM and obtain full information about its transactions

Key articles in the ESM Treaty (1/2)

15

Article 30 Board of Auditors:

1. The Board of Auditors shall consist of five members appointed by the Board of Governors for their competence in auditing and financial matters and shall include two members from the supreme audit institutions of the ESM Members - with a rotation between the latter - and one from the European Court of Auditors.

2. The members of the Board of Auditors shall be independent. They shall neither seek nor take instructions from the ESM governing bodies, the ESM Members or any other public or private body.

3. The Board of Auditors shall draw up independent audits. It shall inspect the ESM accounts and verify that the operational accounts and balance sheet are in order. It shall have full access to any document of the ESM needed for the implementation of its tasks.

4. The Board of Auditors may inform the Board of Directors at any time of its findings. It shall, on an annual basis, draw up a report to be submitted to the Board of Governors.

5. The Board of Governors shall make the annual report accessible to the national parliaments and supreme audit institutions of the ESM Members and to the European Court of Auditors.

6. Any matter relating to this Article shall be detailed in the by-laws of the ESM.

Key articles in the ESM Treaty (2/2)

16

ESM Bylaws

Further detail is currently under discussion with Euro Area Member States in the context of the bylaws of the European Stability Mechanism (ESM), eg.

Composition, rotation, appointment and decision making of the Board of Auditors

Audit scope (audit regularity, compliance, performance, risk management and monitoring internal and external audit processes)

Reporting to the Board of Governors

Conflict of interest members of Board of Auditors

Bylaws are to be adopted during the inaugural meeting of the European Stability Mechanism (ESM) before July 2012

17

Conclusion

EFSF established ‘’best practice’’

– Full compliance with national requirements

– Adoption of IFRS

– Voluntarily and best practice set up of Internal Audit

– Voluntarily external reporting

ESM should be another exemplary institution

– Treaty established Board of Auditors

– Draft By laws are currently discussed by Member States and could be exemplary to other institutions

Hearing on Budgetary Control on the EFSF, the EFSM and the ESM - 24 April 2012 Committee on Budgetary Control

4. Public accountability and control of the EFSF, the

EFSM and the ESM - the role of the European Commission

by Marco Buti, Director-General of Directorate

General Economic and Financial Affairs

Hearing on Budgetary control of the European Financial Stability

Facility (EFSF), the European Financial Stabilisation

Mechanism (EFSM) and the European Stability Mechanism

(ESM)Brussels, 24 April 2012

EFSM – ESM – EFSF CONT hearing

STATEMENT

Version 0

EFSM

EFSM - Introduction

The EFSM was created by Council Regulation 407/2010 which

grants the Commission the right to borrow on the capital

markets and to lend those amounts to a Member State of the

euro zone experiencing difficulties.

As the borrowings under the EFSM are backed by the EU

budget, the European Parliament scrutinises the

Commission's actions with regards to the EFSM. Furthermore,

the European Parliament can exercise control over the

Commission's operations in the context of the budget and the discharge procedures.

The European Court of Auditors has full audit rights for the

programme as well as all borrowing and lending activities of the

Commission including the EFSM.

The overall conclusion is that EFSM is subject to adequatepublic audit and parliamentary scrutiny.

EFSM Accountability and transparency arrangements

The EFSM is a Union instrument which therefore is subject to

the general EU Treaty framework where the Commission is

always accountable to the European Parliament.

Similarly to the BoP and MFA, the ECA has full audit access

rights for EFSM .

Furthermore, as regards the EFSM, a specific role is outlined in

article 3.5 of the EFSM regulation: "The Commission shall

communicate the Memorandum of Understanding to the European Parliament and the Council".

For each country receiving a loan under BOP or EFSM, a

quarterly assessment on the fulfilment of the policy conditionality is carried out before a further instalment is

disbursed. These reports are published. The MoUs signed with

these countries are transmitted to the EP.

Furthermore there are regular reports to the EP and Council on the borrowing and lending activity of the EU as well as on

the guarantees covered by the budget. Therefore, the

Commission already provides a substantive amount of

information on the programme work and its borrowing and

lending activities.

The borrowings and loans are also accounted for in the annual financial statements of the EU and therefore subject

to political control by means of the budgetary adoption (BUDG

Committee) and discharge (CONT) procedures.

Globally the Commission believes that the procedural framework of the EFSM and the assignment of roles and responsibilities between the Institutions involved are appropriate.

EFSM - Measures in place to safeguard the EU budget

There are substantial measures in place to safeguard the EU

budget and the bonds issued by the EU finance, in principle, the

loans are "back-to-back" in € currency; thus they do not

generate open interest rate or currency positions for the EU.

Under normal circumstances the repayments by the borrowing country provide for the repayment of the bonds

issued by the EU.

In the unlikely event of a default, the cash management of the

Commission and its right to draw on Member States for contributions ensures timely payment of a l l obligatory

expenditures, including debt service for the bonds issued by the

EU. In such an instance, the Commission would submit a

proposal for an amending budget in order to account for these

amounts on the p.m. budget line established for the EFSM.

EFSF and ESM

EFSF and ESM - Introduction

The EFSF and the ESM are two financial assistance

mechanisms established as independent entities via agreement

or international Treaty among the euro-area Member States and

are, as such, outside of the EU Treaty framework. Their lending

activities are fully backed by the participating Member States

and, as such, do not have a direct impact on the EU budget.

The Commission, however, will have a critical role, which has

been enshrined in the EFSF Framework Agreement and the

ESM Treaty: it is responsible for negotiating the policy

conditionality attached to financial assistance and the

monitoring of compliance with said conditionality.

This role falls under the regular EP scrutiny established by the

Treaty and thus allows maintaining the normal checks and

balances of the Commission’s responsibilities.

Transparency of the EFSF and ESM

Similarly to the BOP or EFSM, each country receiving financial assistance from either the EFSF or the ESM will be subject to regular assessments on the fulfilment of the policy conditionality. In the case of loans, such assessments

are carried out on a quarterly basis and must be completed

before a further instalment is disbursed. These reports are published. The MoUs signed with these countries will continue

to be transmitted to the EP, as has been the status quo of

financial assistance provided under the EFSF.

Furthermore, the Commission has proposed a new regulation

(COM (2011) 819) that aims to ensure consistency between the

processes established under the EFSF Framework Agreement

and ESM Treaty and the EU’s multilateral surveillance

framework. This will serve to avoid inefficiencies while also

removing the burden of duplicating complex work.

Accountability of the EFSF and ESM

A substantial amount of work has been done to ensure not only

transparency but also accountability for the EFSF and ESM,

despite their existence outside the Treaty framework.

First, the EFSF has a number of arrangements to ensure public

(external) audit. As a company incorporated in Luxembourg, it is

submitted to the Luxembourgish legal provisions on auditing. Its

articles of incorporation also state that one or more statutory

auditors appointed by vote of the shareholders' meeting for a

maximum duration of six years. These statutory auditors are

independent external auditors (currently PWC). In addition, the

EFSF has also established an internal auditing process in view

of checking internal finances and processes.

Because the ESM is a permanent mechanism with a significant

paid-in capital base, work has been conducted directly with the

supreme audit institutions to develop an audit process

enshrined in international standards and best practices. And the

provisions on auditing and financial control in the ESM Treaty

are consistent with the characteristics of control mechanisms

deployed by similar public financial assistance providers.

The ESM will contain 3 levels of auditing: 1) an internal audit, 2)

an external independent audit, 3) an independent board of

auditors. The Board of Auditors will also have the right of

initiative to conduct independent audits on specific topics that it

deems necessary; the annual report shall be made accessible

to the national parliaments and supreme audit institutions of the

ESM Members and the European Court of Auditors, as well as

the European parliament. This will substantially enhance

transparency. Moreover, the by-laws of the ESM on auditing

have been prepared taking into full account the opinion

released by the European Supreme Audit Institutions and have

recently been endorsed by the European Court of Auditors.

Hearing on Budgetary Control on the EFSF, the EFSM and the ESM - 24 April 2012 Committee on Budgetary Control

5. External audit of the mechanisms - a European

perspective

by Vitor Caldeira, President of the European

Court of Auditors

Page 1 of 5 EN

EUROPEAN COURT OF AUDITORS

12, rue Alcide De Gasperi - L - 1615 Luxembourg

Tel.: (+352) 4398 45410 - Fax: (+352) 4398 46410

e-mail: [email protected]

EUROPEAN COURT OF AUDITORS SPEECH

Brussels, 24 April 2012 ECA/12/12

Speech by Vítor Caldeira, President of the European Court of Auditors

Budgetary control of the European Financial Stability Facility (EFSF), the European Financial Stabilisation Mechanism (EFSM)

and the European Stability Mechanism (ESM)

Hearing of the Committee on Budgetary Control of the European Parliament

24 April 2012

Check against delivery. The spoken version shall take precedence.

Page 2 of 5 EN

EUROPEAN COURT OF AUDITORS

12, rue Alcide De Gasperi - L - 1615 Luxembourg

Tel.: (+352) 4398 45410 - Fax: (+352) 4398 46410

e-mail: [email protected]

Mr Chairman,

Members of the Committee,

Distinguished guest speakers

I would like to thank the Committee, and in particular the rapporteur Mrs Iliana Ivanova, for arranging

this important hearing and for giving me the opportunity to contribute.

The initiative of the Committee to hold this hearing on the objectives, operation and oversight of the

financial assistance mechanisms created as a response to the ongoing economic and financial crisis, is

very much welcomed by the European Court of Auditors. It provides a valuable opportunity to raise

awareness of the issues involved, to benefit from each others’ experience and to deepen our

understanding.

Since the start of the current crisis - and particularly in relation to the creation of the response

mechanisms - the European Court of Auditors has repeatedly raised attention to the key principles to be

respected whenever public funds are at stake. This started with a letter to Mr Van Rompuy in November

2010 and continued with a Position Paper of the European Court of Auditors in May 2011. In October of

the same year, the Supreme Audit Institutions of the Member States alongside the ECA, jointly

reiterated and further developed these principles in a Contact Committee Statement.

I think it is worth briefly recalling these three key principles. They are:

• Transparency, in the form of reliable and timely information on actual or intended use of public

funds, and the risks to which they are exposed;

• Accountability, meaning the public scrutiny of the operations and holding to account decision-

makers and those responsible for managing the processes; and

• Public audit, to provide assurance and information on the use of public funds and the risks to

which they are exposed.

We at the European Court of Auditors are ready to play our part in achieving these principles in the

context of the mechanisms that are the subject of today’s hearing.

Page 3 of 5 EN

EUROPEAN COURT OF AUDITORS

12, rue Alcide De Gasperi - L - 1615 Luxembourg

Tel.: (+352) 4398 45410 - Fax: (+352) 4398 46410

e-mail: [email protected]

From the perspective of the ECA’s audit rights and obligations, we can distinguish three different types

of instrument. They have common elements, as well as some significant differences.

I will start with the EFSM and the Balance of Payment assistance, both of which operate under the

umbrella of the EU Treaty. These instruments are managed and administered by the European

Commission and guaranteed by the European Union. The financial flows move through the EU budget

and the operations, assets and liabilities are disclosed in the EU’s financial statements. The European

Court of Auditors has full audit rights, as well as the obligation for financial audit of these operations

within the annual statement of assurance exercise. This has been the case since 2008 when the

Balance of Payments assistance was first used. As the first EFSM support was disbursed in 2011, it will

be covered by the statement of assurance exercise we are currently working on.

The annual financial audit responsibility is supplemented by the right to do selected compliance and

performance audits on the quality of financial management, made public in the form of special reports.

As you can see from our work programme for 2012, we intend to start work on an audit of the Balance

of Payments assistance and the EFSM.

The second type of instrument from an ECA audit rights perspective consists of the Greek Loan

Facility and the EFSF. Here, the ECA’s audit rights do not derive from the EU Treaty – at least not

directly – and neither do these instruments implicate the EU budget. In practice they are arrangements

between euro-area countries and put at risk national funds. However, the European Commission and

the European Central Bank EU have key roles in operating these instruments, such as setting lending

conditions and monitoring compliance.

As the European Court of Auditors has the responsibility to audit the use of administrative spending of

the EU institutions (as well as the operational efficiency of the ECB) we have the possibility to audit the

management of these instruments by these Institutions. I of course do not need to remind this

Committee that our resources are limited, and we therefore need to select between different audit

priorities over the European Union budget and the European Development Funds. This prioritisation is

based on risk, financial importance, political and public interest and other factors helping us to maximise

the impact of our resources.

Page 4 of 5 EN

EUROPEAN COURT OF AUDITORS

12, rue Alcide De Gasperi - L - 1615 Luxembourg

Tel.: (+352) 4398 45410 - Fax: (+352) 4398 46410

e-mail: [email protected]

Finally, there is the ESM – the newest of the mechanisms, and intended as a permanent successor to

the temporary EFSM and EFSF arrangements (although if, and how, any takeover will take place has

not yet been made clear). We will hear more about the audit arrangements for the ESM in a moment

from my colleague from the German Bundesrechnungshof.

From the perspective of the European Court of Auditors I would like to emphasise that we do not have

the right to audit the ESM as an institution. However, I am pleased to say that the ECA will have the

right to nominate one of the five members of the Board of Auditors, an important addition to the ESM’s

accountability arrangements introduced in the revised ESM Treaty. Alongside will be two members to be

nominated by the SAIs of ESM countries on a rotational basis. Each member of the Board of Auditors

will act independently in his or her personal capacity and not as a representative of the institutions

nominating them.

Also, and similar to the EFSF, the European Commission will be playing a key role in preparing and

operating the economic adjustment programmes. This will include making a preliminary risk

assessment, negotiating conditionality and monitoring compliance. And again, the ECA will consider

auditing the Commission’s role as appropriate and useful.

When looking at the overall challenges of the economic and financial crisis, we should not forget that the

mechanisms we are discussing today are part of a broader policy response. I would like to

emphasise the collection of measures put in place, or currently being finalised, in order to improve EU

economic governance. This includes the European Semester, on which we held an important debate at

last year’s Contact Committee meeting, the six-pack of regulations and more recently the fiscal

compact. There is also the reform of the financial market regulation and supervision which has led to the

creation of three new supervisory agencies that the ECA has the responsibility to audit. Since for all

these measures the quality of statistics is of great importance, the Court is currently in the final stages of

completing an audit of the effectiveness of Eurostat in improving the process for producing reliable and

credible European statistics.

Page 5 of 5 EN

EUROPEAN COURT OF AUDITORS

12, rue Alcide De Gasperi - L - 1615 Luxembourg

Tel.: (+352) 4398 45410 - Fax: (+352) 4398 46410

e-mail: [email protected]

In a wider sense and beyond its explicit audit rights and obligations, the ECA as an EU institution

has a general responsibility to use its unique position and perspective to contribute to ensuring effective

public accountability, transparency and audit of the public funds put at stake to meet the EU’s

objectives. Therefore, we will continue to monitor the developments and contribute as necessary. We

will do so not only in the field of the EU response to the economic and financial crisis, but also by

assessing the entire landscape of EU policy developments in terms of the transparency, accountability

and audit implications.

To come back to the ESM, in my view, the emerging public external audit arrangements of the ESM are

largely promising, given the intergovernmental nature of the mechanism and particularly as compared to

its main predecessor, the EFSF. The raison d’être of the ESM is to protect the integrity of the Euro area

and with it, one of the pillars of economic and monetary union - a core EU policy.

Before finishing, I would like to take this opportunity to highlight the success of the recent co-operation

between national state audit institutions and the European Court of Auditors, both in the context

of the Contact Committee and between the euro-area countries. Working together we have been able to

prepare common positions which have had a significant impact on the revised ESM Treaty, and just

recently on the draft by-laws. I would particularly like to thank my German colleagues for their leadership

in this respect. The resulting positive outcome has demonstrated the effectiveness of close co-operation

for the common purpose of promoting adequate levels of public scrutiny and accountability, which this

Committee rightly considers as a key priority and is the driver behind today’s hearing.

On behalf of the European Court of Auditors, allow me to assure you, Mr Chairman and the members of

the Committee, that we are committed to assisting this Committee in furthering transparency,

accountability and public audit whenever public funds are put at stake to reach EU policy objectives.

Thank you for your kind attention.

6. External audit of the mechanisms - a national

perspective

by Horst Erb, Senior Audit Director and Member

of the Bundesrechnungshof

Hearing on Budgetary Control on the EFSF, the EFSM and the ESM - 24 April 2012 Committee on Budgetary Control

1

Public hearingby the European Parliament, Committee on Budgetary Control on

„Budgetary control of the European Financial Stability Facility (EFSF), the European Financial Stabilisation Mechanism (EFSM) and the European Stability

Mechanism (ESM)

Statement by Horst Erb

- Senior Audit Director and Member of the Bundesrechnungshof,

acting for the President of the Bundesrechnungshof, Prof. Dr. Dieter Engels -

“External audit of the mechanisms – a national perspective –

Audit opportunities and challenges from a German perspective”

A joint approach of the euro area SAIs …

(1) The heads of states and governments of the euro area decided to restructure

the temporary arrangements for safeguarding financial stability and to establish a

permanent European Stabilisation Mechanism (ESM). This will have a direct bearing

on the core duties of the euro area supreme audit institutions (euro area SAIs) since

the ESM is guaranteed by national governments and financed from national budgets.

Therefore, it is indispensable to subject the ESM to a comprehensive external audit

according to international standards.

(2) With concern, we had found that no arrangements for any external audit involving

SAIs had been made for the ESM in the Treaty in the version of 11 July 2011. It only

provided for an Internal Auditing Board (art. 24 ESM Treaty) and an audit to be

carried out by external auditors (art. 25 ESM Treaty). Thus, that version did not

comply with the International Standards of Supreme Audit Institutions (ISSAI).

2

(3) The ESM is an international institution governed by an international treaty.

Pursuant to ISSAI 5000, all international institutions financed with or supported by

public money are to be subject to an audit performed by SAI representatives,

including regularity and performance audit.

…resulted in a statement of the euro area SAIs (5 October 2011).(4) Recognising this, the euro area SAIs and the European Court of Auditors

(ECA) met on 27 September 2011 in Bonn to discuss questions concerning the

external audit of the ESM. Their aim was to incorporate in the Treaty an external

audit to be carried out by SAIs. In the “Statement of SAIs of the euro area on the

external audit of the ESM“, euro area SAIs and the ECA agreed on the key features

of such external audit:

An audit body consisting of up to five members of euro area member states’

SAIs is to be created.

The audit body is to examine the activities of the Internal Auditing Board of the

ESM and the external auditors’ audit opinion.

In particular, the audit body is to examine the financial management, risk

management and programme management of the ESM.

The audit body is to report on its findings to the Board of Governors and to

inform the national parliaments.

(5) On 14 October 2011, the Contact Committee of the Supreme Audit Institutions

of the European Union (Contact Committee), on which all 27 SAIs of the EU member

states as well as the ECA are represented, adopted a resolution supporting this

statement. Moreover, the Contact Committee’s chair submitted a draft of the euro

area SAIs aiming at the modification of the ESM’s internal and external audit

structures along with the resolution addressed to the national and European

stakeholders: parliaments, ministers of finance and heads of states and

governments, as well as to the European Parliament, European Council and

European Commission. The euro area SAIs also submitted the draft to their relevant

national contacts.

3

The draft by-laws for Art. 30 ESM Treaty …

(6) The joint initiative contributed to incorporating a Board of Auditors (BoA) in

art. 30 ESM Treaty. It shall be made up of five members which are to be designated

ad personam by the Board of Governors based on their qualifications in the field of

financial and audit matters. Two members shall be appointed by the euro area SAIs

and be subject to a principle of rotation, one member shall be appointed by the ECA.

Under these arrangements, the ESM is not subject to any audit by national SAIs.

Rather than that, the BoA members’ mission is to carry out an independent audit

according to international standards. The members represent neither the institutions

from which they come nor any national interests.

(7) The BoA shall audit the ESM at its own discretion. It shall inspect the ESM

accounts and verify that the operational accounts and balance sheet are in order. For

this purpose, it shall be granted full access to all ESM documents it deems necessary

for performing its mission. The BoA shall submit its annual report to the Board of

Governors; the latter shall make such report accessible to the ESM members’

national parliaments and supreme audit institutions and to the ECA.

…make detailed provisions governing the future external audit of the ESM.

(8) On 14 March 2012, representatives of the euro area SAIs and the ECA met

again in Bonn to specify the general provisions of art. 30 ESM Treaty by means of

the draft by-laws as follows:

The BoA members shall be appointed ad personam for a three-year term of

office;

Conflicts of interest of the members need to be precluded;

A rotation arrangement shall apply to the two members designated by the

national SAIs to ensure that both the SAIs of member states holding a larger

and those holding a smaller capital share in the ESM are represented;

The BoA shall independently examine the regularity, compliance and

performance and risk management of the ESM in accordance with

international standards;

4

The BoA may rely on subject-matter experts;

The BoA shall submit an annual report comprising its conclusions and

recommendations to the Board of Governors;

The ESM shall support the work of the BoA and pay travel and subsistence

allowances for the members and the experts.

(9) As to the future impact of the ESM on EU institutions and bodies, EU Member

States, and the importance of the single currency as a substantial element of EU

policy, the SAIs welcome the arrangements made and call on the ministers of finance

and heads of states and governments to proceed in this spirit to adopt the by-laws.

The citizens and the parliaments representing them are entitled to have all

international institutions financed with or supported by public funds audited by SAIs

to ensure a regular, efficient and cost-effective performance of the missions of these

international institutions and to promote transparency and accountability.

External Audit of the European Stability Mechanism

Horst Erb, Senior Audit DirectorMember of the Bundesrechnungshof 1

“External audit of the mechanisms

– a national perspective –

Audit opportunities and challenges

from a German perspective”Public hearing by the European Parliament

External Audit of the European Stability Mechanism

Horst Erb, Senior Audit DirectorMember of the Bundesrechnungshof

ISSAI 5000 states:

• “All international institutions financed with or supported by public money should be subject to audit by Supreme Audit Institutions to promote better governance, transparency and accountability”

• “The audit mandate should include regularity audit as well as performance audit.”

2

External Audit of the European Stability Mechanism

Horst Erb, Senior Audit DirectorMember of the Bundesrechnungshof 3

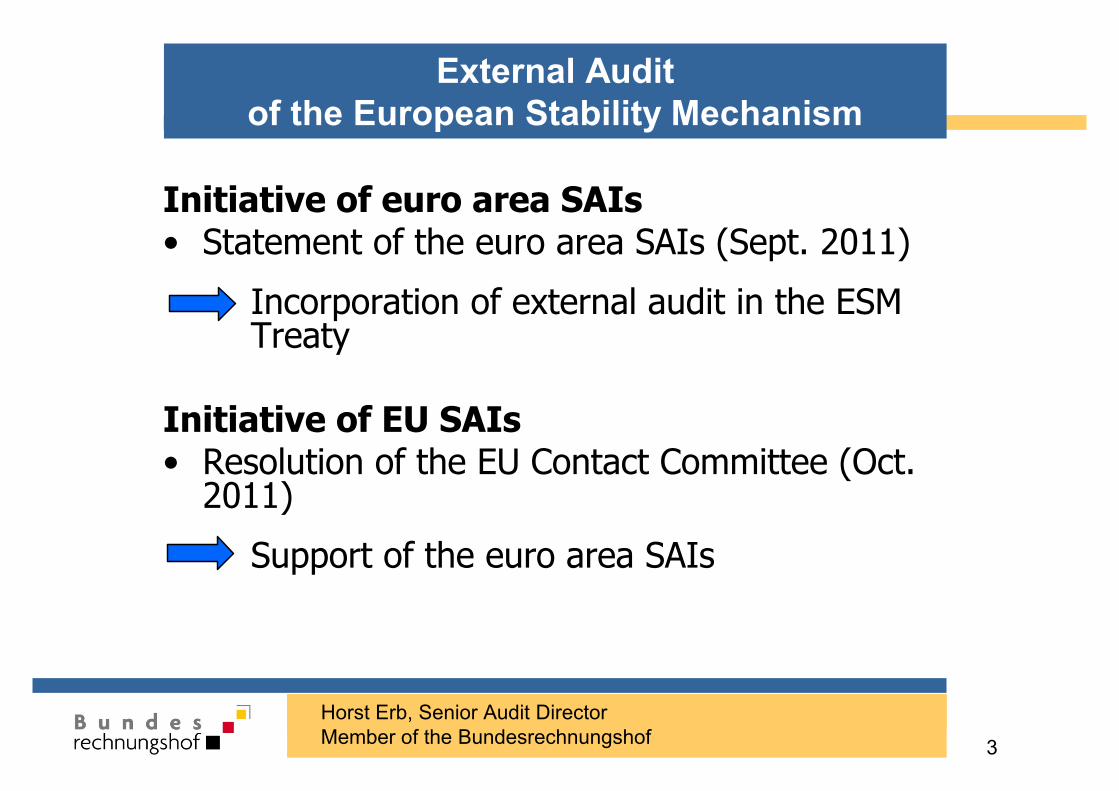

Initiative of euro area SAIs• Statement of the euro area SAIs (Sept. 2011)

Incorporation of external audit in the ESM Treaty

Initiative of EU SAIs• Resolution of the EU Contact Committee (Oct.

2011)

Support of the euro area SAIs

External Audit of the European Stability Mechanism

Horst Erb, Senior Audit DirectorMember of the Bundesrechnungshof 4

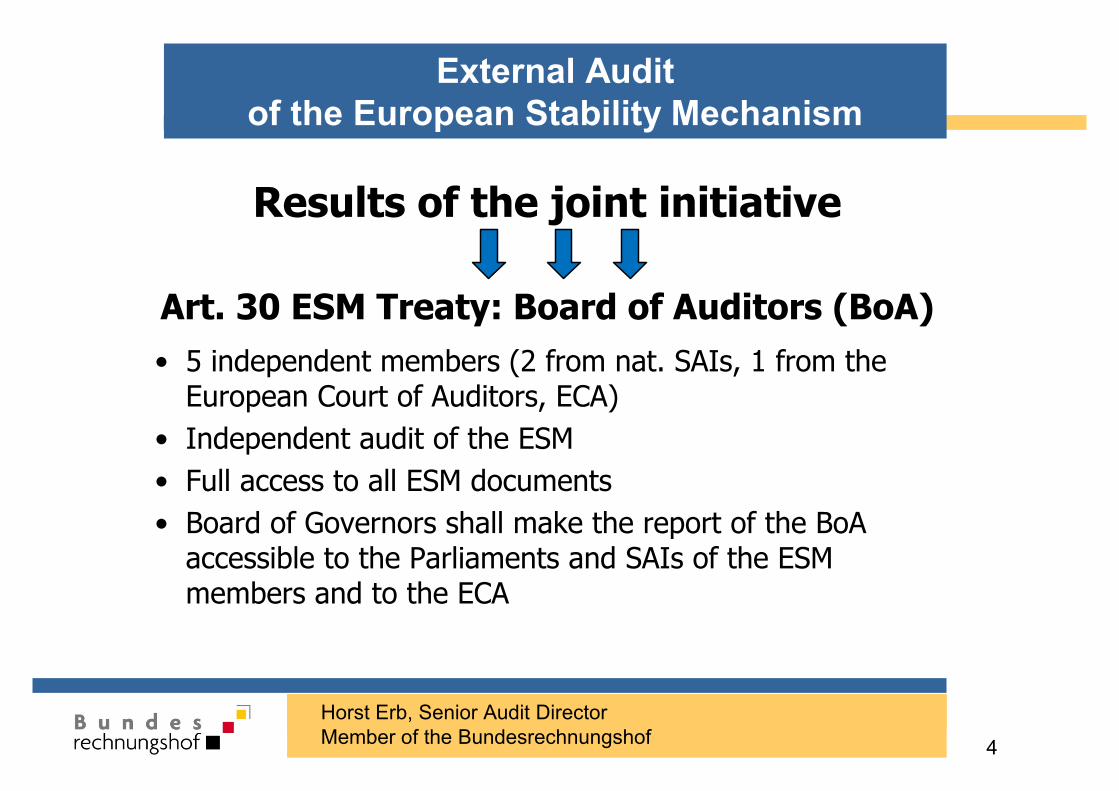

Results of the joint initiative

Art. 30 ESM Treaty: Board of Auditors (BoA)• 5 independent members (2 from nat. SAIs, 1 from the

European Court of Auditors, ECA)• Independent audit of the ESM• Full access to all ESM documents• Board of Governors shall make the report of the BoA

accessible to the Parliaments and SAIs of the ESM members and to the ECA

External Audit of the European Stability Mechanism

Horst Erb, Senior Audit DirectorMember of the Bundesrechnungshof 5

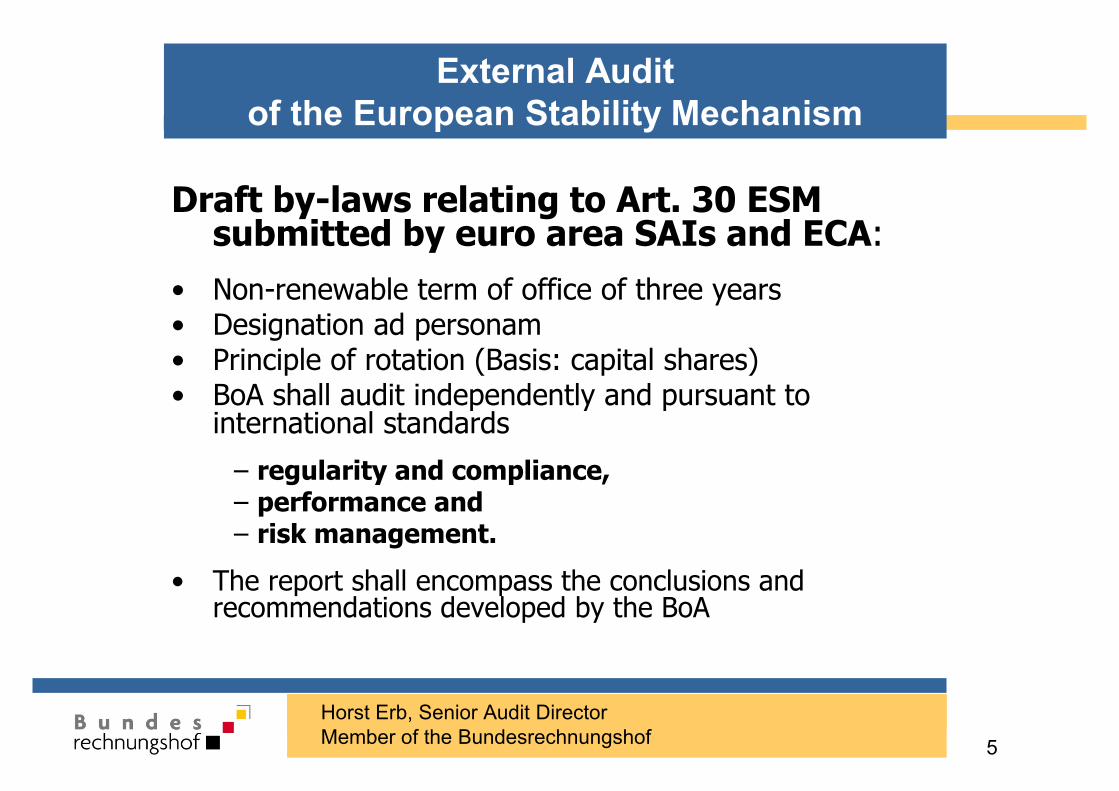

Draft by-laws relating to Art. 30 ESM submitted by euro area SAIs and ECA:

• Non-renewable term of office of three years• Designation ad personam• Principle of rotation (Basis: capital shares)• BoA shall audit independently and pursuant to

international standards

– regularity and compliance,– performance and – risk management.

• The report shall encompass the conclusions and recommendations developed by the BoA

External Audit of the European Stability Mechanism

Horst Erb, Senior Audit DirectorMember of the Bundesrechnungshof 6

Thank you very much for your interest and attention!

7. External audit of the mechanisms - a national

perspective

by Kees Vendrik, Vice-President of the Dutch

Court of Audit

Hearing on Budgetary Control on the EFSF, the EFSM and the ESM - 24 April 2012 Committee on Budgetary Control

1

Public hearing on “Budgetary control of the European Financial Stability Facility (EFSF), the European Financial Stabilisation Mechanism (EFSM) and the European Stability Mechanism (ESM)”

European Parliament

24 April 2012 in Brussels

The governance arrangements within the European Stability Mechanism from a Dutch perspective

Address to the Committee on Budgetary Control by Kees Vendrik, vice-president of the Netherlands Court of Audit

Check against deliverySeul le texte prononcé fait foiEs gilt das gesprochene Wort

Supreme audit institutions (SAIs) have a responsibility to promote accountability and

transparency in public activities where public funds are at stake. This is not only the view

of my institution, the Netherlands Court of Audit, but is also the opinion of all EU SAIs

and our concern for these matters has been expressed in recent statements and

resolutions of the Contact Committee of EU SAIs regarding the financial and sovereign

debt crisis. In the case of the European Stability Mechanism (ESM) and the other

financial stability instruments that have been set up, European leaders are taking

decisions on unprecedented amounts of public funds coming not only from Eurozone

member states but also from the European Union itself and international financial

institutions. In order to get and maintain adequate public backing for these instruments,

transparent reporting on what is being undertaken, holding to account those dealing with

the operations and a good independent public audit of the use and effect of the funds are

necessary. According to the Netherlands Court of Audit, the financial stability instruments

that have been developed do not take these principles enough into account. Compliance

with them should be strengthened in the permanent mechanism now being set up.

To be more precise SAIs are of the opinion (Contact Committee statement 2011) that in

the governance arrangements of the stability instruments three things are required:

(1) sufficient transparency, in the form of reliable and timely information (including

national statistics) on actual or intended use of public funds, and the risk to which

they are exposed;

2

(2) appropriate accountability, involving public scrutiny of the operations and holding

to account decision-makers and those responsible for managing the processes;

and

(3) adequate public audit, to provide assurance and information on the use of public

funds and the risks to which they are exposed, thereby contributing to

transparency and providing a basis for accountability.

Let us now take a closer look at the ESM. This financial stability instrument is being set

up on the basis of an intergovernmental treaty signed by the seventeen member states

of the Eurozone. It will be an international organisation with legal personality under

international public law. As described in the study carried out for the Committee on

Budgetary Control, the roles and arrangements of the governing bodies of the ESM are

clearly defined and aligned with the common practice implemented by international

financial assistance providers (i.e. IMF, EIB, World Bank, etc.). The ESM however does

not fit within the legal order and institutional framework of the EU – even though a

modification of the Treaty on the Functioning of the EU (TFEU) was necessary to enable it

– and some (like the Dutch Council of State in its opinions on the bills ratifying the ESM

Treaty and the modification of article 136 TFEU ) argue that this has been a deliberate

choice. The roles and competences of the European Commission, European Parliament,

European Court of Auditors and the Court of Justice of the EU with regard to the ESM are

limited and important provisions with regard to democratic and judicial control have not

been included in the ESM Treaty.

While the role the European Commission (together with the ECB) will play in the ESM is a

crucial one (see article 13) – analysing the severity of the risk to the financial stability of

the euro, negotiating the MoU with the ESM member requesting stability support,

detailing the conditionality attached to the financial assistance facility, monitoring the

compliance with the conditionality in practice – sufficient provisions for the democratic

control and effective external audit of the tasks of the European Commission are lacking

in the ESM Treaty. The only other explicit reference made in the ESM Treaty to these

tasks can be found in the preambule, where it is stated that post-programme surveillance

will be carried out by the Commission and the Council within the EU framework laid down

in articles 121 and 136 TFEU.

But who will be responsible for checking that the Commission has carried out its ESM

tasks properly? The Board of Governors? The Board of Auditors? The Treaty grants the

Board of Auditors (article 30) an explicit audit task only with regard to the inspection of

the ESM accounts and the verification of the operational accounts and balance sheet. The

Board of Auditors can undertake independent audits and has full access to any ESM

document needed for the implementation of its tasks. According to Dutch government

3

these are only the basic provisions and they can be expanded in the by-laws that are at

present being drafted (see Tweede Kamer documents 33221 nr. 3). The Second Chamber

of Dutch parliament recently adopted two motions on this subject and Dutch government

has promised that it will exert itself to the maximum to achieve a full-fledged public

external audit and anchor firmly the transparency and accountability of the spending of

ESM funds. As our German colleagues have just explained, the EU SAIs would like to see

that the Board of Auditors can audit regularity, compliance, performance and risk

management of the ESM more generally. At present the discussions are taking place on

the by-laws that need to be in place when ESM starts operations and we as SAIs have

made our wishes known. With the help of our governments these wishes will hopefully be

adopted.

If this however is not the case, then perhaps the only audit of the effects and results of

the ESM operations possible will be special audits by ECA of the activities carried out by

the European Commission within the 121 and 136 TFEU framework. Individual SAIs of

the Eurozone member states have no right of their own to audit an international

organisation. Their primary task is to audit their national government and its spending of

public money. This makes it difficult for EU SAIs to do more than what we at present are

doing with our website www.rekenkamer.nl/eu-governance-en, which gives insight into

the quickly changing developments in the field thereby helping create transparency for

national parliament and the general public. For the ECA audits of the effects and results

of the ESM operations are relatively new as their audit task (examining the revenue and

expenditure of the Union) has traditionally been restrictively interpreted. Such audits

moreover would take place outside the ESM-framework and only form an indirect check

of ESM operations. From the perspective of the ESM itself they alone can hardly be seen

as adequate public audit of the ESM.

Let us now briefly reflect on the other two aspects of ESM governance mentioned:

transparency and accountability. While initiatives are being undertaken to strengthen

ESM governance with regard to public audit, the arrangements formulated in the ESM

Treaty for transparency and accountability are weak and as far as we know nothing

concrete – aside from the hearing being held today – is being done to alter this.

According to the Treaty the ESM shall publish an annual report containing an audited

statement of its accounts and shall circulate to ESM members a quarterly summary

statement of its financial position and a profit and loss statement of its operations (article

27). The Board of Auditors too shall draw up an annual report and submit this to the

Board of Governors. It shall be made accessible to national parliaments, the SAIs of the

ESM members and the ECA. While the limited extent of the accountability reporting that

will be generated by the ESM is in itself concerning, the Netherlands Court of Audit

4

considers the fact that almost nothing will be made publicly available more disturbing.

Without information sharing and public scrutiny how will it become possible to acquire

and maintain the backing of the European citizens? We would like to see for instance that

the results of the audits carried out by the Board of Auditors are placed on internet.

In its opinion on the ESM Treaty the Dutch Council of State stresses that an important

consequence of the chosen intergovernmental structure is that the ESM bodies cannot be

held to account in the EU institutional framework. Furthermore it points out that the ESM

has judicial immunity, European Parliament plays no role, ECA has no audit right of its

own and the Court of Justice can only deal with disputes that are brought to it by an ESM

member. Democratic control and public scrutiny only exist to the limited extent that

ministers of Finance can be held to account by their national parliament for their

individual share in the functioning of the ESM and not for the functioning of the ESM

bodies or the organisation as such. The Dutch Council of State considers the deficient

democratic control problematic and even more so given the permanent character of the

stability mechanism and its potential financial volume. In its opinion the present

intergovernmental form cannot be the final outcome of the continuing process of the

structuring of ‘economic governance’ , but just an intermediate outcome. Dutch

government however disagrees. The accountability that it gives to national parliament for

the ESM exceeds that given for other international financial institutions like the IMF.

According to Dutch government this in combination with the involvement of EU SAIs and

ECA in the ESM Treaty has laid an adequate basis for ensuring the public and democratic

control of the ESM.

While the Netherlands Court of Audit is flattered by the democratic influence Dutch

government accredits it with, we share the concerns our Council of State has voiced in its

opinion on the bill ratifying the ESM Treaty. The limitations placed on transparency and

accountability are great. These together with the concerns mentioned earlier regarding

the adequacy of the public audit arrangement and the transparency of the results thereof

form in our opinion a serious threat to the support of the general public for ESM

operations and should be altered where possible.

Finally I would like to point to another area where we see similar problems regarding

transparency, accountability and public audit: namely the expenditure of EU funds in the

member states. For seventeen consecutive years the ECA has not been able to give an

unqualified opinion on the regularity of the spending of EU funds. ECA’s audit however

does not show exactly where the problems occur and what improvements are needed to

tackle them. Against this background Dutch government decided a number of years ago

to give account of how EU funds are spent in the Netherlands in an annual EU member

state declaration. Our SAI was asked to give extra assurance to the declaration in the

5

form of an independent opinion and we are doing so now for the sixth time. So far only

three other EU member states do the same: Denmark, Sweden and the United Kingdom.

In the negotiations that are at present taking place between the European Commission,

the Council and European Parliament on the new Financial Regulation this subject has

once again become contentious. Council has up to now refused to accept the proposal of

European Parliament to include an obligatory member state declaration in the Financial

Regulation. And to make things even worse, Council is maintaining in its resistance to

make public any form of accountability reporting that can be traced back to individual

member states. If these developments in the discussion of the new Financial Regulation

are accepted in the end, this would in my opinion turn back the clock on the reform of EU

financial management a number of years and deliver the cause of transparency,

accountability and good public audit an unexpected blow. A cause that we at the

Netherlands Court of Audit and you and your committee have always actively promoted.

I believe that in the coming years the challenge will lie in finding ways to promote strong

governance arrangements - both with regard to the financial stability instruments and

the implementation of the EU budget. From the perspective of the external auditor the

best way to contribute to this is through coordinated action from two levels – the EU and

the member state level. Only through the coordination of the interacting and mutually

reinforcing chains of accountability and control at the EU and member state level will it

become possible to enhance transparency and reconnect with the public. For the ESM

possibilities for coordinated action already embryonically exist in the set-up of the Board

of Auditors, for the implementation of the EU budget more change will be required. And

that is where you come in.