alternative service concepts, l.l.c. audits what you don’t do can be costly by: mark watkins vice...

TRANSCRIPT

Alternative Service Concepts, L.L.C.

AuditsWhat you don’t do can be costly

By: Mark WatkinsVice President

Alternative Service Concepts, L.L.C.1

AuditsWhat you don’t do can be costly

• Documented • Correctly Applied• Issues Addressed

Coverage

• Timely• Sufficient• StairsteppedReserves

• Initial Timely• Initial Adequate• Subsequent Timely/AdequateInvestigation

• Timely• AdequateDocumentation• Review/Analysis• Timely/Proper Referral• Not Abandoned• Client Apprised• Report/Bill

LitigationManagement

• Recognized• Timely• Proper Format

ExcessReporting

• CRLAuditCategor

ies

Alternative Service Concepts, L.L.C.2

Audits

• Costly Oversights• Not reporting excess reportable files to CRL.

Remember, when in doubt, report.

• Let’s identify excess reportable criteria …

What you don’t do can be costly

Alternative Service Concepts, L.L.C.3

Audits

• Excess Reportable Criteria Identified:

Claims with reserves that are higher than 50% of the retention

Spinal Cord Injuries – resulting in

paraplegia, quadriplegia Amputations Any severe head injury involving brain

damage affecting mentality or central nervous system- such as permanent disorientation, behavior disorder, personality change, seizures, motor deficit, inability to speak, unconsciousness (comatose)

Impairment of vision or hearing by 50% or more

Multiple fractures- involving more

than one member, non-union or significant shortening of the limbs

Nerve damage causing paralysis and loss of sensation in any body member

Massive internal injuries affecting body organ or organs

What you don’t do can be costly

Alternative Service Concepts, L.L.C.4

Audits

• Excess Reportable Criteria Identified continued…

Burns- involving over 10% of body with third degree or 30% with second degree

Injury to nerve at base of spinal canal or any other back injury resulting in incontinence of bowel and/or bladder

Fatalities

Occupational Disease- such as asbestosis, black lung disease or long term chemical exposure

Any claim or suit not specified above that presents an unusual exposure to the coverage. Examples include: sexual molestation, AIDS, rape, environmental exposure, class actions and bad faith allegations

Property claims (including multiple claims) arising out of an occurrence or accident that may require payment in excess of retention

Any other serious injury that may involve CRL’s liability

What you don’t do can be costly

Alternative Service Concepts, L.L.C.5

Audits

• Costly Oversights• Reservation of Rights (R&R) letters not being sent out addressing

coverage issues.

• Let’s identify coverage issues where R of R would normally apply if alleged or sought …

What you don’t do can be costly

Alternative Service Concepts, L.L.C.6

Audits

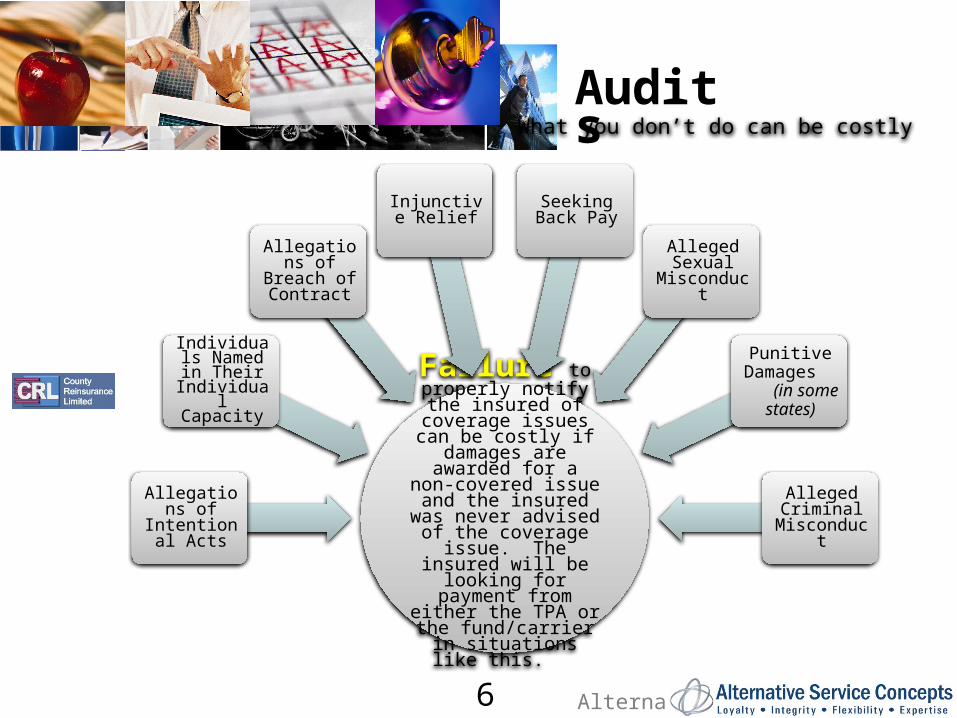

Failure to properly notify the insured of

coverage issues can be costly if damages are awarded for a non-

covered issue and the insured was never advised of the coverage issue. The insured will be looking for payment from either the TPA or the fund/carrier in

situations like this.

Allegations of Intentional

Acts

Individuals Named in

Their Individual Capacity

Allegations of Breach of Contract

Injunctive Relief

Seeking Back Pay

Alleged Sexual Misconduct

Punitive Damages

(in some states)

Alleged Criminal

Misconduct

What you don’t do can be costly

Alternative Service Concepts, L.L.C.7

Audits

• Costly Oversights• Excess ad damnum letters not being sent where damages

sought are not specified or capped.

• Let’s identify what happens when ad damnum letters are not sent …

What you don’t do can be costly

Alternative Service Concepts, L.L.C.8

Audits

Plaintiff seeks damages in a lawsuit but does not seek a specific dollar amount or the amount the plaintiff is asking for is for more than the applicable coverage limits.

A letter should be sent to the insured advising them that in the event of an excess judgment (over the limits) that it will be the responsibility of the defendants against whom it is awarded to pay the difference between the available limit of coverage and the amount of the judgment.

Example: Failure to advise the insured of this potential can be costly if damages are awarded above the applicable limits and the insured will be looking to the TPA or fund/carrier to cover the entire loss.

#1

#2

What you don’t do can be costly

Alternative Service Concepts, L.L.C.

Audits

Sample Ad Damnum

Letter

9

What you don’t do can be costly

Alternative Service Concepts, L.L.C.

Audits

10

What you don’t do can be costly

Alternative Service Concepts, L.L.C.

Audits

11

What you don’t do can be costly

Alternative Service Concepts, L.L.C.12

Audits

• Costly Oversights

Rese

rves Should be

established to reserve for realistic, practical, ultimate exposure taking into consideration the injury, damages, liability, jurisdiction and other influencing factors. Failure to establish proper reserves when there is a legitimate known exposure could potentially be considered bad faith.

Insu

ffici

ent R

eser

ves This can lead an

insured or fund/carrier to get a false sense of potential financial exposure they have if the reserves are not properly set.

Litig

ation

Bud

gets Should be

obtained in order to properly establish legal expense reserves.

Life

care

Pla

ns

What you don’t do can be costly

Should be obtained where applicable to help establish proper reserves on workers’ compensation claims that are expected to be open for a person’s lifetime.

Alternative Service Concepts, L.L.C.13

Audits

• Costly Oversights File Documentation is “key!”

File Documentation should be detailed to where anybody could review the claim and tell what the claim is about, what the real facts are, what has occurred since the claim was received and what the plan is to bring the claim to a resolution or closure. This would include things such as investigation details, summaries of medical and legal reports and any other correspondence. This should also include all demands, offers and negotiations as well as plans of actions and any other activity by the adjuster or supervisor.

Documentation should also indicate whether the file is one where there is exposure, potential exposure or compensability.

What you don’t do can be costly

Alternative Service Concepts, L.L.C.14

Audits

• Costly OversightsA lack of proper file documentation can be costly in a couple of ways:

If the file is not documented properly and the adjuster handling the file is no longer around or the parties involved from the insured standpoint are no longer around, then it could potentially cost the insured/carrier money because it could end up being the claimant’s or plaintiff’s word against nobody. This is not a scenario that any insured wants to be up against.

(Example: Adjuster handling file investigates the claim and knows all the facts but does not document this. Adjuster gets hit by a bus or wins multi-million progressive slot jackpot and quits job, two years later Mr./Ms. claimant decide to file suit and when the file is reviewed to determine what happened there is nothing documented as to the facts and investigation.) Chances are the cost of that claim just went up since Mr./Ms. claimant will paint a picture of gloom and doom and how the insured was negligent or responsible for their injuries and damages. It will make it a lot harder to defend due to the fact the file was not documented with detailed information as to what occurred, what the investigation turned up, etc.

What you don’t do can be costly

Alternative Service Concepts, L.L.C.15

Audits

• Costly OversightsA lack of proper file documentation can be costly in a couple of ways:

Lack of documenting an excess report and/or reservation of rights letter and excess ad damnum letter could be costly if there is no documentation to prove these things were done on applicable cases. *

(Example: A carrier disclaims coverage due to the fact that they say the claim was never reported. The adjuster claims that the file was reported but the file documentation does not support that and the hard copy of the report is nowhere to be found)

* GOOD LUCK with trying to explain this to the insured and see how happy they are to hear this news!

What you don’t do can be costly

Alternative Service Concepts, L.L.C.

Audits

Questions????

By: Mark WatkinsVice President

What you don’t do can be costly