alternative investments: risks & returns

TRANSCRIPT

29 South Pleasant St, Amherst, MA 01002Tel: 413-253-4601

Alternative Investments: Risks & Returns

Hossein Kazemi, PhD, CFAManaging Partner, AIAProfessor of Finance, Univ of [email protected]

THE FAMILY ALTERNATIVE INVESTMENT CONFERENCEFebruary 2007, Monaco

2

Outline

Alternative Investment Universe.Historical & Recent Performance.Risk-Return Characteristics of Hedge Funds.Alternative Investments in Diversified Portfolios.Performance under Various Conditions: Selected Review of 2006 & Preview of 2007.“Alternative Betas” and “Alternative Alphas”.Hedge Fund Managers: Persistence & Diversity.Funds of Funds and Investible Indices.Conclusion.

3

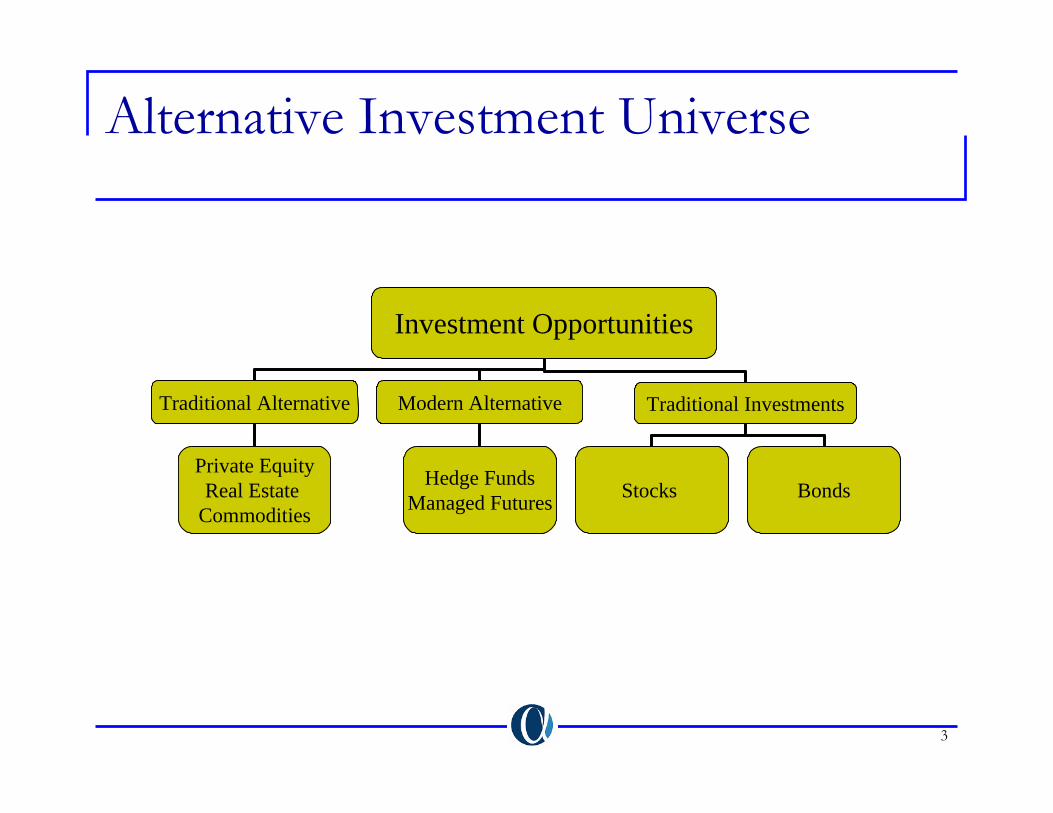

Alternative Investment Universe

Investment Opportunities

Traditional Alternative Modern Alternative Traditional Investments

Stocks BondsHedge FundsManaged Futures

Private EquityReal Estate

Commodities

Investment Opportunities

Traditional Alternative Modern Alternative Traditional Investments

Stocks BondsHedge FundsManaged Futures

Private EquityReal Estate

Commodities

4

Why Alternatives?

Alternative Sources of ReturnAccess to broader set of asset classes (e.g., private equity, real estate, commodities).Access to broader set of trading strategies (hedge funds, CTAs).

Diversifying risk of portfolios dominated by traditional assets.Enhancing the performance of portfolios dominated by traditional assets.

5

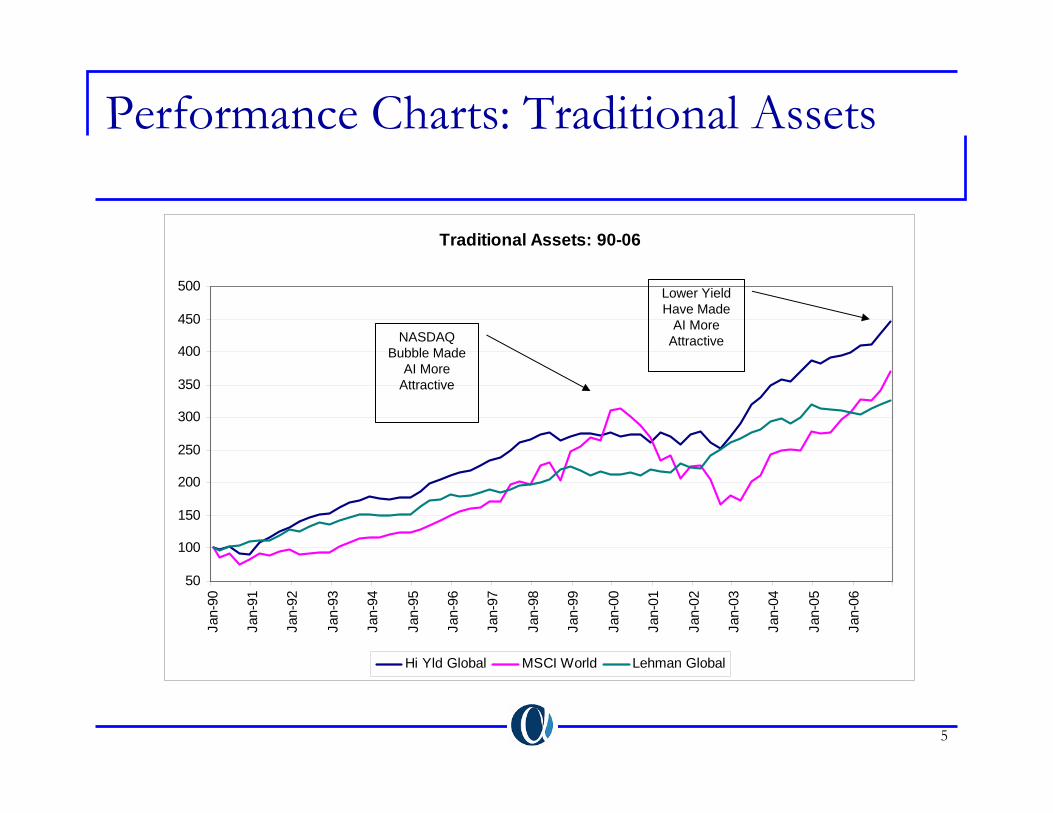

Traditional Assets: 90-06

50

100

150

200

250

300

350

400

450

500

Jan-

90

Jan-

91

Jan-

92

Jan-

93

Jan-

94

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Hi Yld Global MSCI World Lehman Global

Performance Charts: Traditional Assets

NASDAQ Bubble Made

AI More Attractive

Lower Yield Have Made

AI More Attractive

6

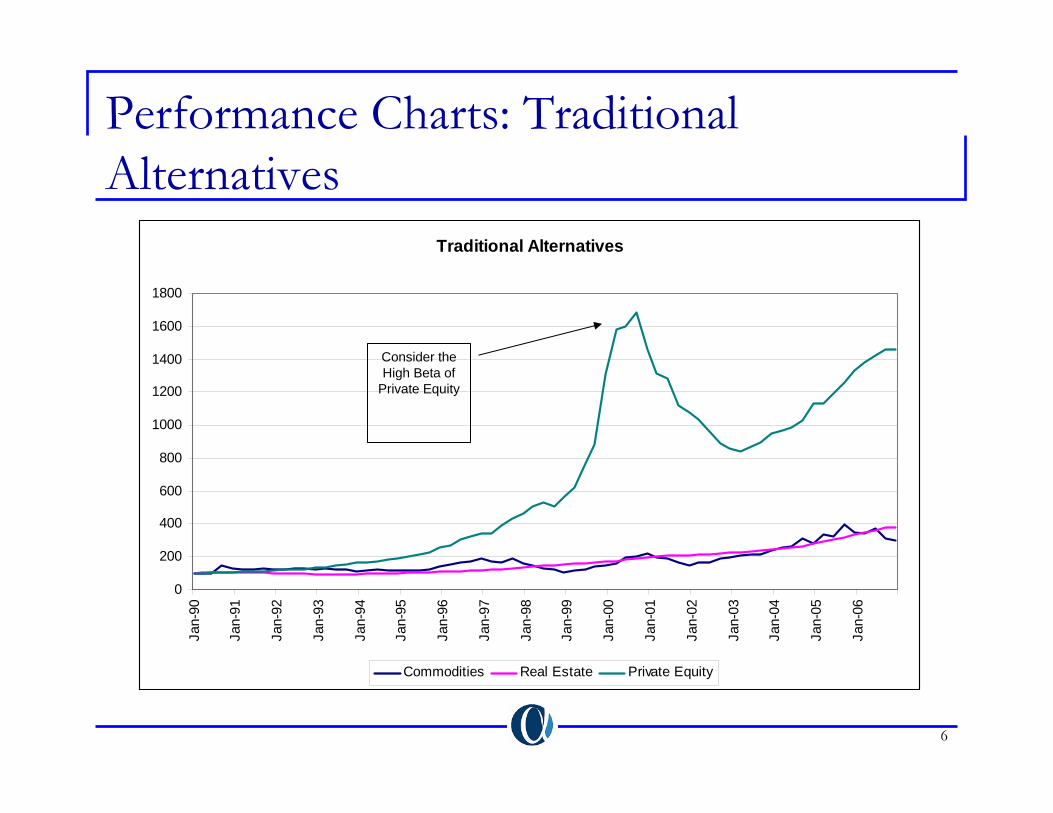

Performance Charts: Traditional Alternatives

Traditional Alternatives

0

200

400

600

800

1000

1200

1400

1600

1800

Jan-

90

Jan-

91

Jan-

92

Jan-

93

Jan-

94

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Commodities Real Estate Private Equity

Consider the High Beta of

Private Equity

7

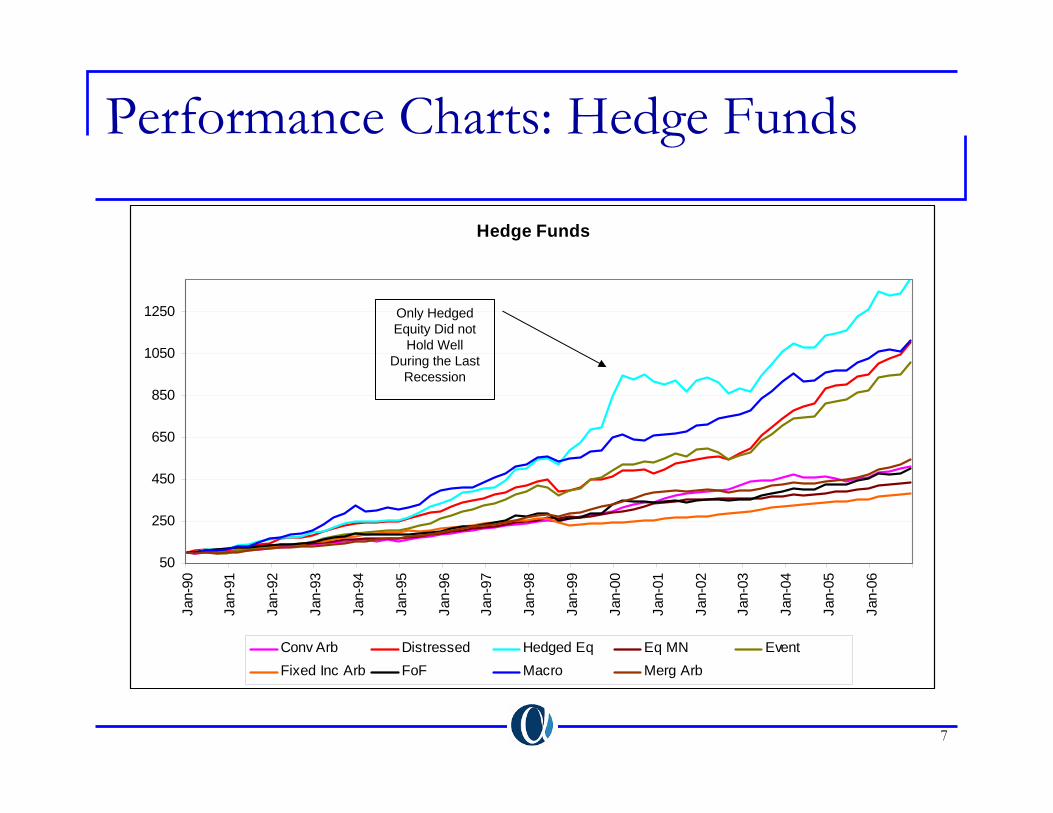

Performance Charts: Hedge Funds

Hedge Funds

50

250

450

650

850

1050

1250

Jan-

90

Jan-

91

Jan-

92

Jan-

93

Jan-

94

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Conv Arb Distressed Hedged Eq Eq MN EventFixed Inc Arb FoF Macro Merg Arb

Only Hedged Equity Did not

Hold Well During the Last

Recession

8

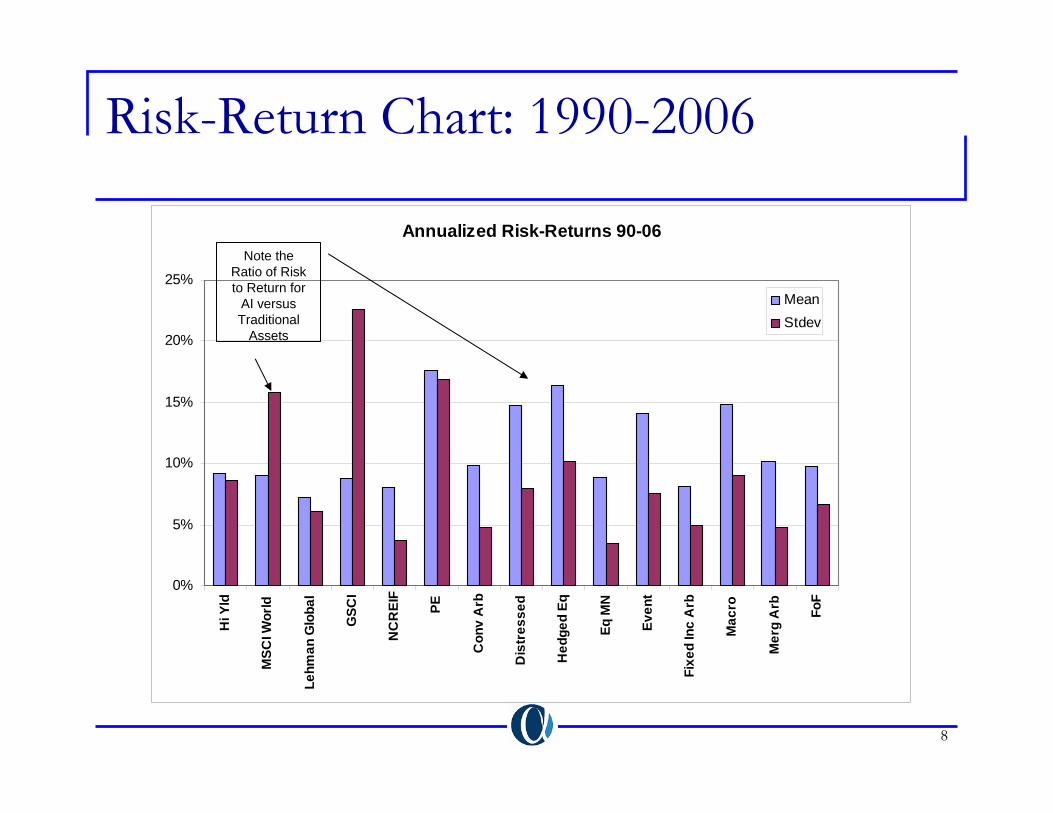

Risk-Return Chart: 1990-2006

Annualized Risk-Returns 90-06

0%

5%

10%

15%

20%

25%

Hi Y

ld

MSC

I Wor

ld

Lehm

an G

loba

l

GSC

I

NC

REI

F

PE

Con

v A

rb

Dis

tres

sed

Hed

ged

Eq

Eq M

N

Even

t

Fixe

d In

c A

rb

Mac

ro

Mer

g A

rb FoF

MeanStdev

Note the Ratio of Risk to Return for

AI versus Traditional

Assets

9

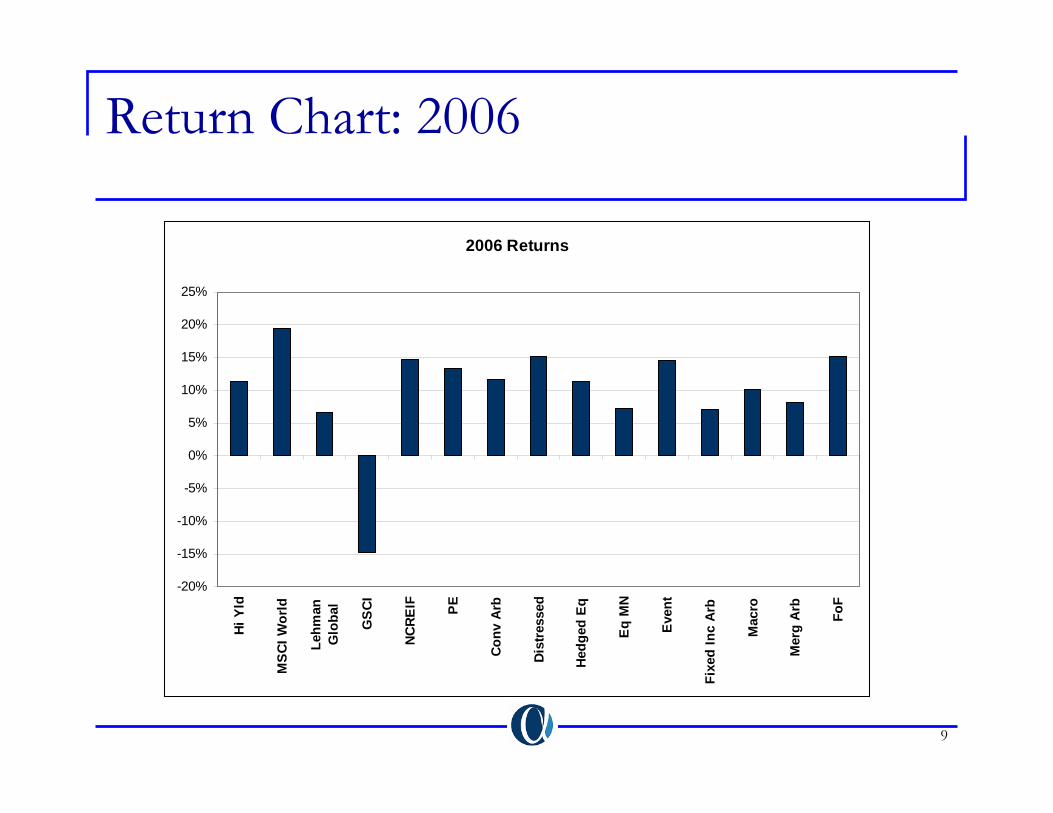

Return Chart: 2006

2006 Returns

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Hi Y

ld

MSC

I Wor

ld

Lehm

anG

loba

l

GS

CI

NCRE

IF PE

Conv

Arb

Dist

ress

ed

Hed

ged

Eq

Eq

MN

Even

t

Fixe

d In

c Ar

b

Mac

ro

Mer

g A

rb

FoF

10

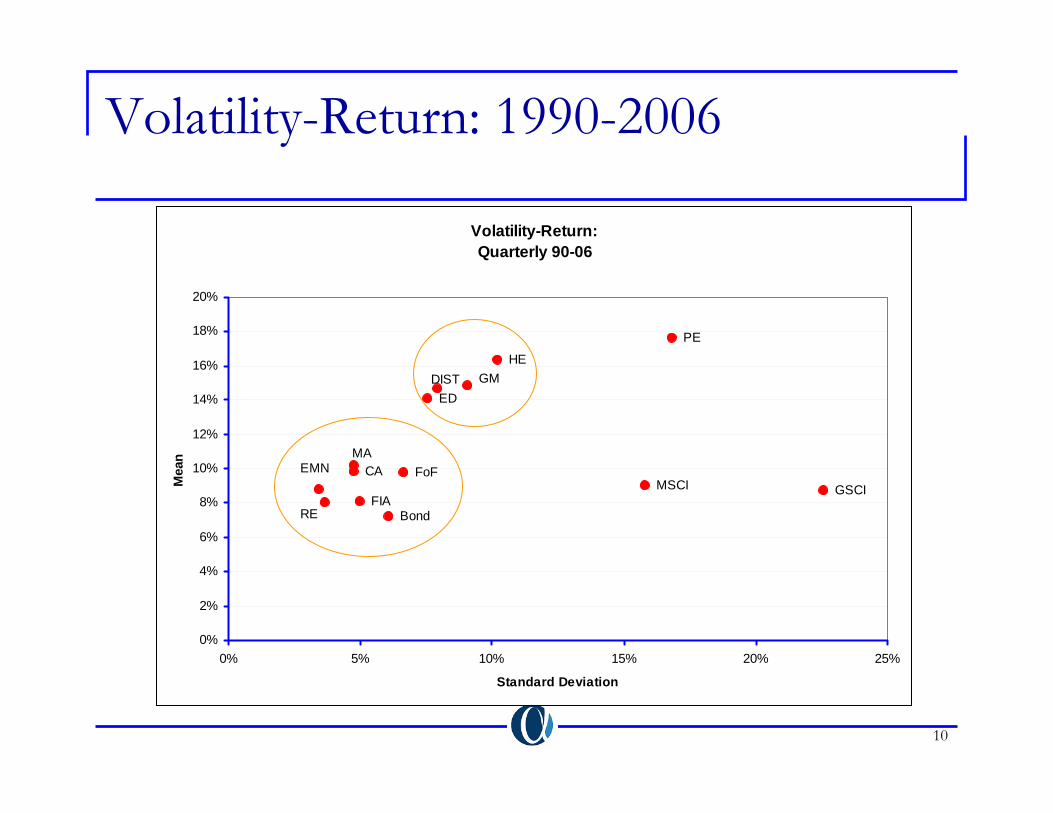

Volatility-Return: 1990-2006

Volatility-Return:Quarterly 90-06

GSCI

RE

PE

CA

DISTHE

EMN

ED

FIA

FoF

GM

MA

MSCI

Bond

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0% 5% 10% 15% 20% 25%

Standard Deviation

Mea

n

11

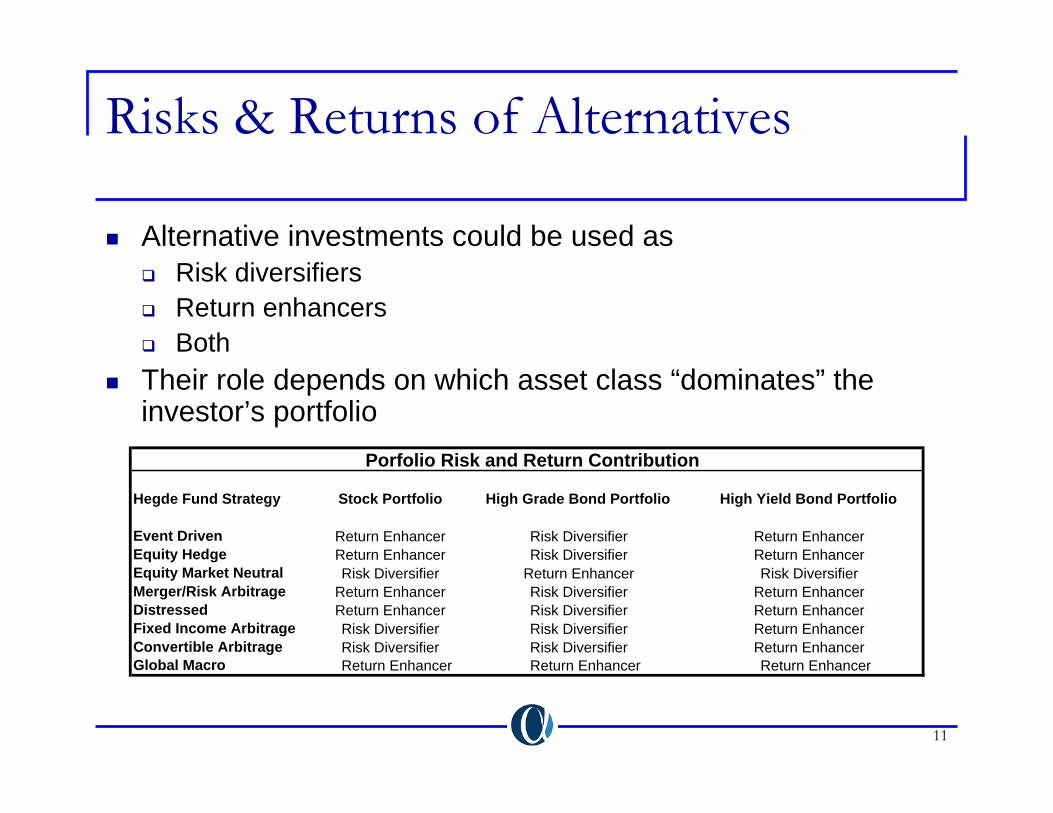

Risks & Returns of Alternatives

Alternative investments could be used asRisk diversifiersReturn enhancersBoth

Their role depends on which asset class “dominates” the investor’s portfolio

Hegde Fund Strategy Stock Portfolio High Grade Bond Portfolio High Yield Bond Portfolio

Event Driven Return Enhancer Risk Diversifier Return EnhancerEquity Hedge Return Enhancer Risk Diversifier Return EnhancerEquity Market Neutral Risk Diversifier Return Enhancer Risk DiversifierMerger/Risk Arbitrage Return Enhancer Risk Diversifier Return EnhancerDistressed Return Enhancer Risk Diversifier Return EnhancerFixed Income Arbitrage Risk Diversifier Risk Diversifier Return EnhancerConvertible Arbitrage Risk Diversifier Risk Diversifier Return EnhancerGlobal Macro Return Enhancer Return Enhancer Return Enhancer

Porfolio Risk and Return Contribution

12

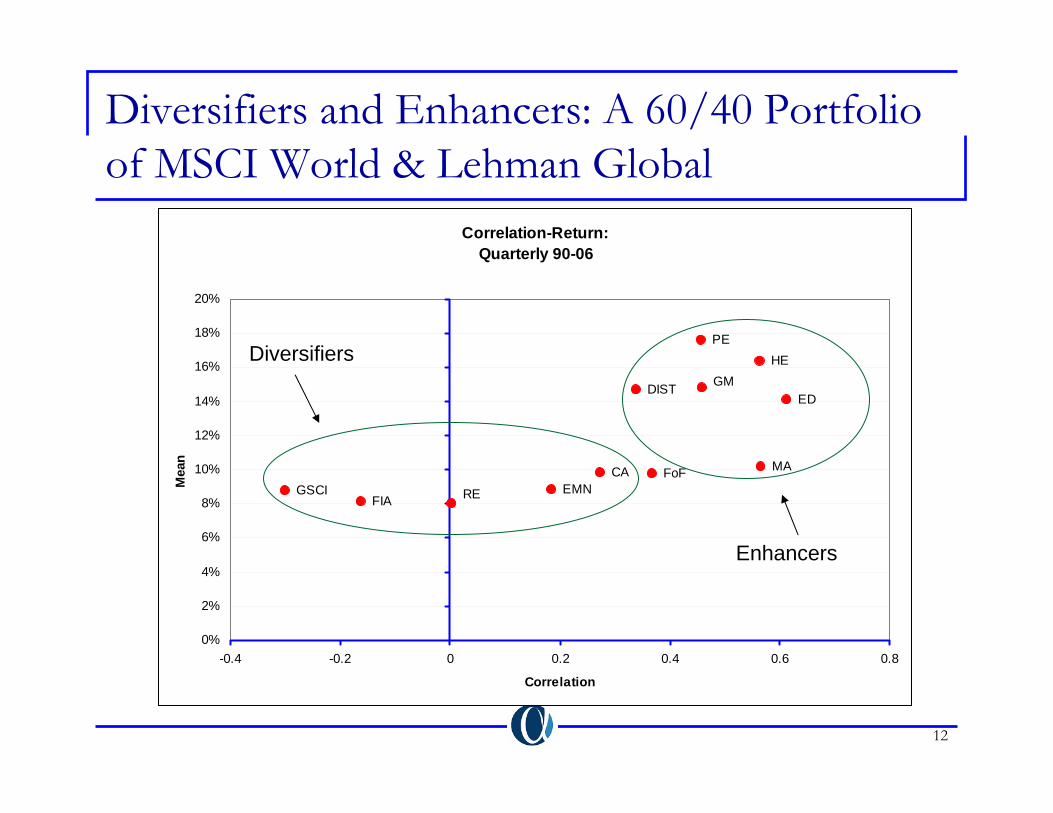

Diversifiers and Enhancers: A 60/40 Portfolio of MSCI World & Lehman Global

Correlation-Return:Quarterly 90-06

MA

GM

FoF

FIA

ED

EMN

HE

DIST

CA

PE

REGSCI

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

-0.4 -0.2 0 0.2 0.4 0.6 0.8

Correlation

Mea

n

Enhancers

Diversifiers

13

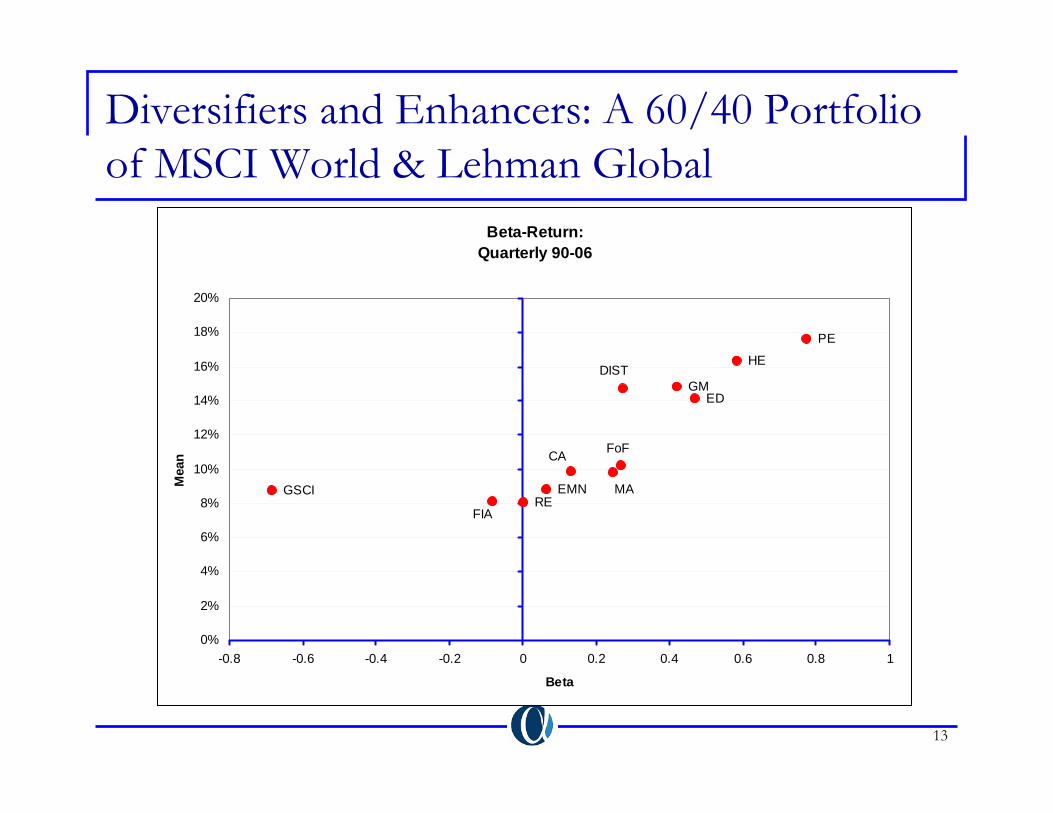

Diversifiers and Enhancers: A 60/40 Portfolio of MSCI World & Lehman Global

Beta-Return:Quarterly 90-06

MA

GM

FoF

FIA

ED

EMN

HEDIST

CA

PE

REGSCI

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

-0.8 -0.6 -0.4 -0.2 0 0.2 0.4 0.6 0.8 1

Beta

Mea

n

14

Model Portfolios

We examine several model portfolios.These highlight the benefits of alternative investmentsHow they fit into a diversified portfolio?

15

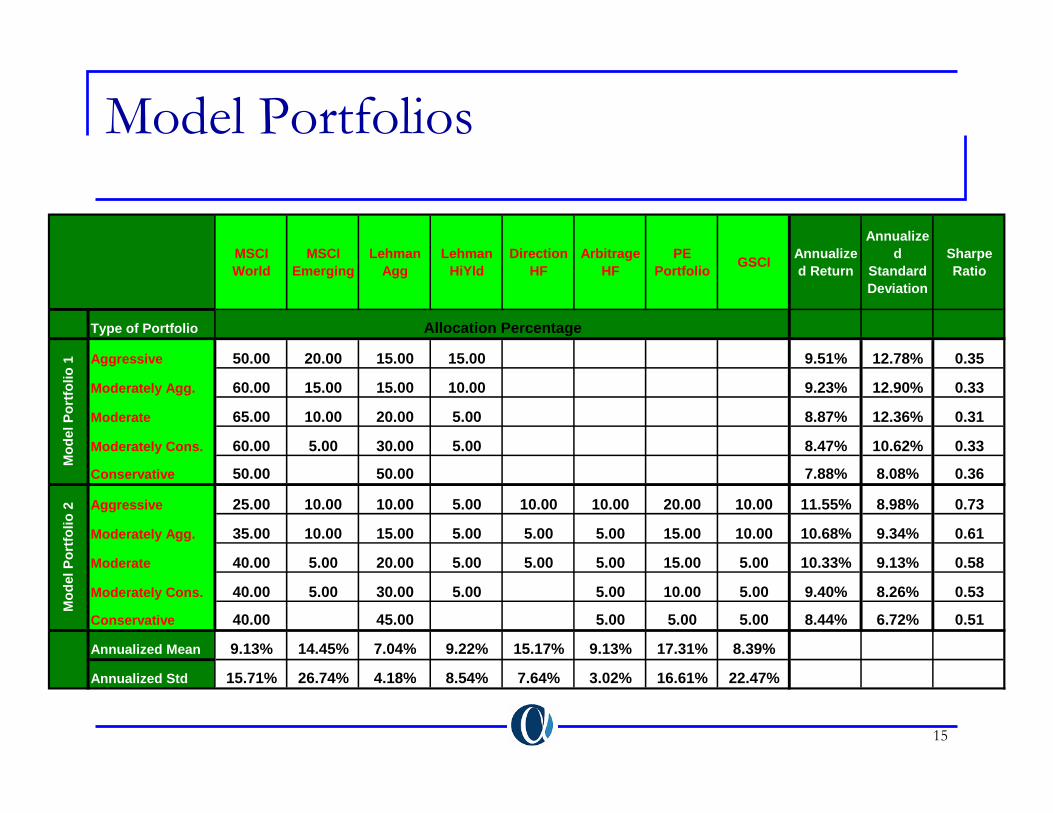

Model Portfolios

MSCI World

MSCI Emerging

Lehman Agg

Lehman HiYld

Direction HF

Arbitrage HF

PE Portfolio GSCI Annualize

d Return

Annualized

Standard Deviation

Sharpe Ratio

Type of Portfolio

Aggressive 50.00 20.00 15.00 15.00 0.00 0.00 0.00 0.00 9.51% 12.78% 0.35

Moderately Agg. 60.00 15.00 15.00 10.00 0.00 0.00 0.00 0.00 9.23% 12.90% 0.33

Moderate 65.00 10.00 20.00 5.00 0.00 0.00 0.00 0.00 8.87% 12.36% 0.31

Moderately Cons. 60.00 5.00 30.00 5.00 0.00 0.00 0.00 0.00 8.47% 10.62% 0.33

Conservative 50.00 0.00 50.00 0.00 0.00 0.00 0.00 0.00 7.88% 8.08% 0.36

Aggressive 25.00 10.00 10.00 5.00 10.00 10.00 20.00 10.00 11.55% 8.98% 0.73

Moderately Agg. 35.00 10.00 15.00 5.00 5.00 5.00 15.00 10.00 10.68% 9.34% 0.61

Moderate 40.00 5.00 20.00 5.00 5.00 5.00 15.00 5.00 10.33% 9.13% 0.58

Moderately Cons. 40.00 5.00 30.00 5.00 0.00 5.00 10.00 5.00 9.40% 8.26% 0.53

Conservative 40.00 0.00 45.00 0.00 0.00 5.00 5.00 5.00 8.44% 6.72% 0.51

Annualized Mean 9.13% 14.45% 7.04% 9.22% 15.17% 9.13% 17.31% 8.39%

Annualized Std 15.71% 26.74% 4.18% 8.54% 7.64% 3.02% 16.61% 22.47%

Allocation Percentage

Mod

el P

ortfo

lio 2

Mod

el P

ortfo

lio 1

16

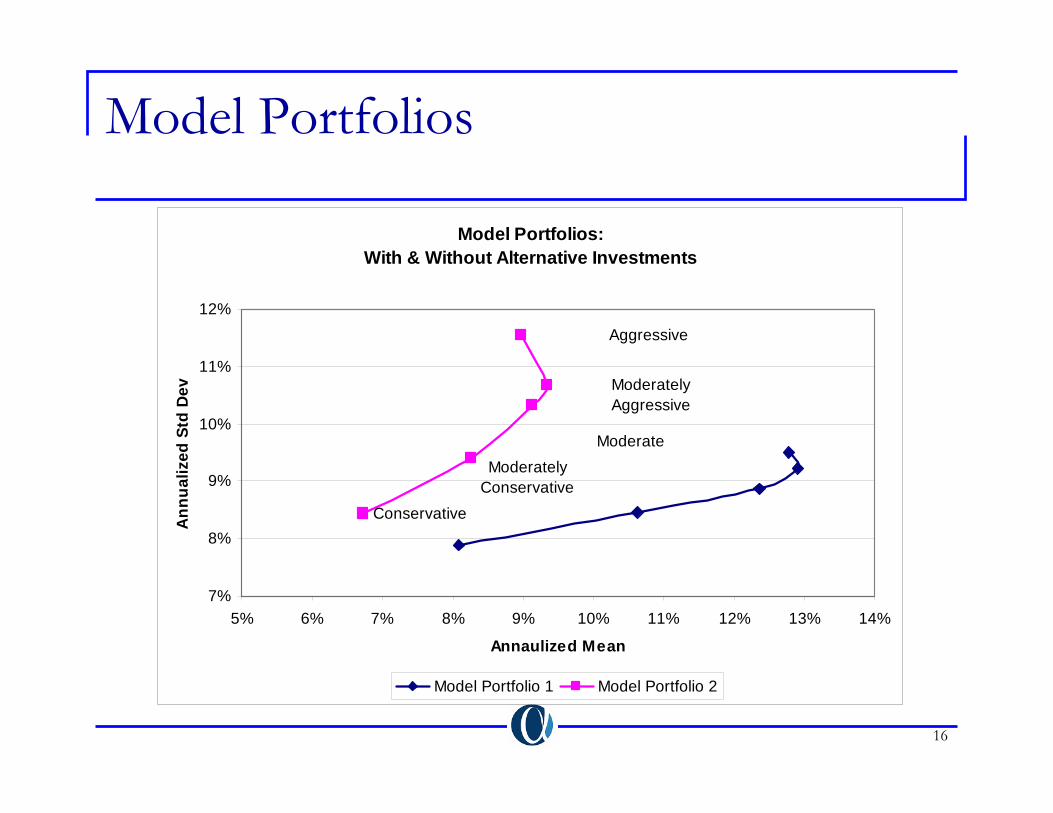

Model Portfolios

Model Portfolios: With & Without Alternative Investments

Conservative

Moderately Conservative

Moderate

Moderately Aggressive

Aggressive

7%

8%

9%

10%

11%

12%

5% 6% 7% 8% 9% 10% 11% 12% 13% 14%

Annaulized Mean

Ann

ualiz

ed S

td D

ev

Model Portfolio 1 Model Portfolio 2

17

AI and Economic Conditions

Here we look at performance of AI under various economic conditions. Economic conditions are “measured” by various indicators (yield curve, volatility, etc.)We look both at contemporaneous and leading indicators of AI performance.This leads us to have a selected review of 2006 and a preview of 2007.More charts are available upon request.

18

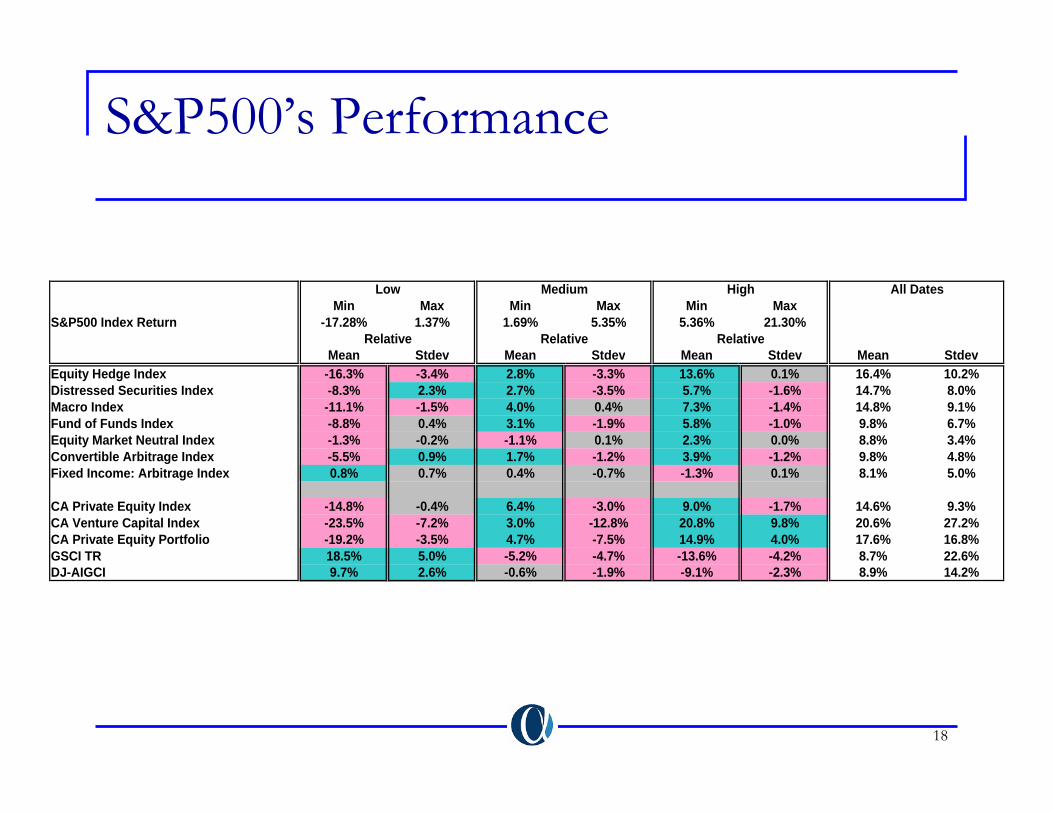

S&P500’s Performance

Min Max Min Max Min MaxS&P500 Index Return -17.28% 1.37% 1.69% 5.35% 5.36% 21.30%

Mean Stdev Mean Stdev Mean Stdev Mean StdevEquity Hedge Index -16.3% -3.4% 2.8% -3.3% 13.6% 0.1% 16.4% 10.2%Distressed Securities Index -8.3% 2.3% 2.7% -3.5% 5.7% -1.6% 14.7% 8.0%Macro Index -11.1% -1.5% 4.0% 0.4% 7.3% -1.4% 14.8% 9.1%Fund of Funds Index -8.8% 0.4% 3.1% -1.9% 5.8% -1.0% 9.8% 6.7%Equity Market Neutral Index -1.3% -0.2% -1.1% 0.1% 2.3% 0.0% 8.8% 3.4%Convertible Arbitrage Index -5.5% 0.9% 1.7% -1.2% 3.9% -1.2% 9.8% 4.8%Fixed Income: Arbitrage Index 0.8% 0.7% 0.4% -0.7% -1.3% 0.1% 8.1% 5.0%

CA Private Equity Index -14.8% -0.4% 6.4% -3.0% 9.0% -1.7% 14.6% 9.3%CA Venture Capital Index -23.5% -7.2% 3.0% -12.8% 20.8% 9.8% 20.6% 27.2%CA Private Equity Portfolio -19.2% -3.5% 4.7% -7.5% 14.9% 4.0% 17.6% 16.8%GSCI TR 18.5% 5.0% -5.2% -4.7% -13.6% -4.2% 8.7% 22.6%DJ-AIGCI 9.7% 2.6% -0.6% -1.9% -9.1% -2.3% 8.9% 14.2%

All Dates

Relative Relative Relative

Low Medium High

19

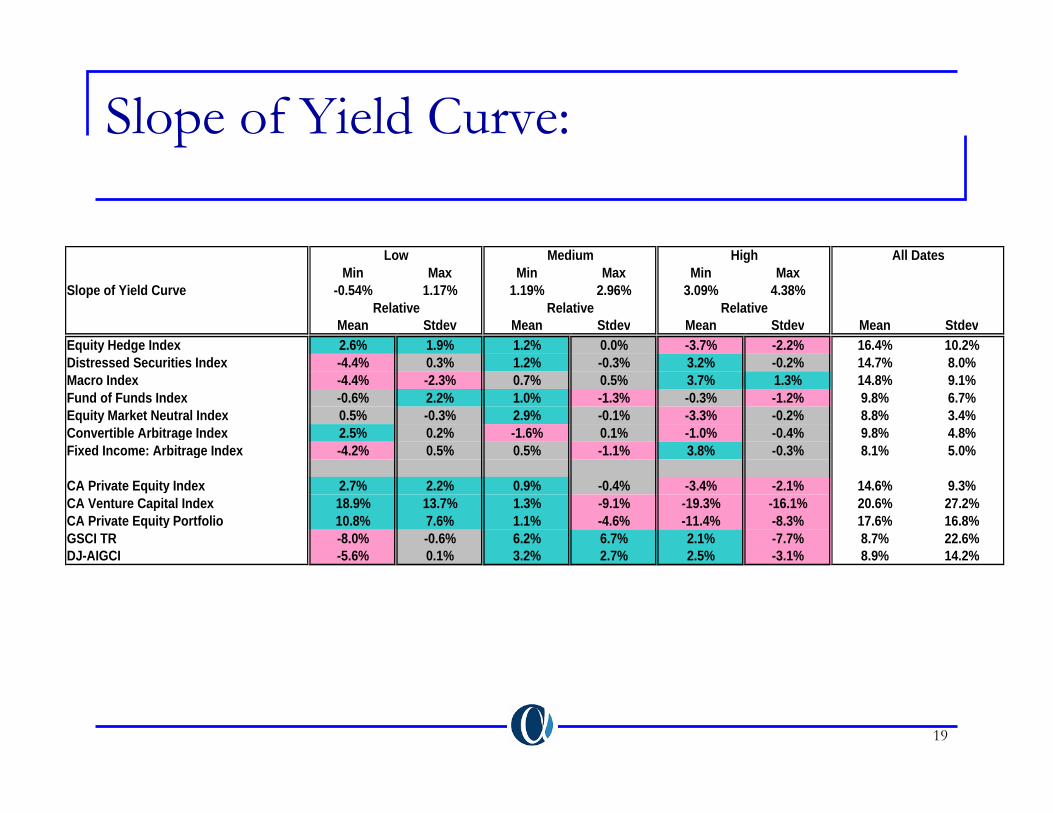

Slope of Yield Curve:

Min Max Min Max Min MaxSlope of Yield Curve -0.54% 1.17% 1.19% 2.96% 3.09% 4.38%

Mean Stdev Mean Stdev Mean Stdev Mean StdevEquity Hedge Index 2.6% 1.9% 1.2% 0.0% -3.7% -2.2% 16.4% 10.2%Distressed Securities Index -4.4% 0.3% 1.2% -0.3% 3.2% -0.2% 14.7% 8.0%Macro Index -4.4% -2.3% 0.7% 0.5% 3.7% 1.3% 14.8% 9.1%Fund of Funds Index -0.6% 2.2% 1.0% -1.3% -0.3% -1.2% 9.8% 6.7%Equity Market Neutral Index 0.5% -0.3% 2.9% -0.1% -3.3% -0.2% 8.8% 3.4%Convertible Arbitrage Index 2.5% 0.2% -1.6% 0.1% -1.0% -0.4% 9.8% 4.8%Fixed Income: Arbitrage Index -4.2% 0.5% 0.5% -1.1% 3.8% -0.3% 8.1% 5.0%

CA Private Equity Index 2.7% 2.2% 0.9% -0.4% -3.4% -2.1% 14.6% 9.3%CA Venture Capital Index 18.9% 13.7% 1.3% -9.1% -19.3% -16.1% 20.6% 27.2%CA Private Equity Portfolio 10.8% 7.6% 1.1% -4.6% -11.4% -8.3% 17.6% 16.8%GSCI TR -8.0% -0.6% 6.2% 6.7% 2.1% -7.7% 8.7% 22.6%DJ-AIGCI -5.6% 0.1% 3.2% 2.7% 2.5% -3.1% 8.9% 14.2%

All Dates

Relative Relative Relative

Low Medium High

20

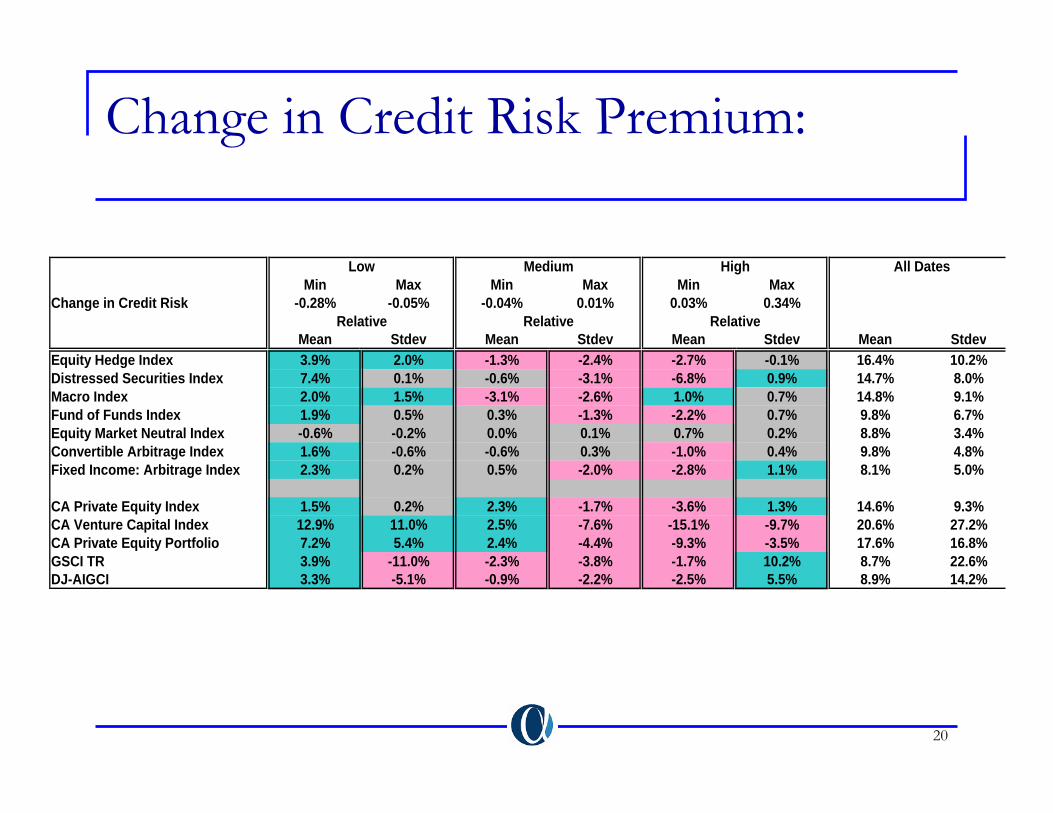

Change in Credit Risk Premium:

Min Max Min Max Min MaxChange in Credit Risk -0.28% -0.05% -0.04% 0.01% 0.03% 0.34%

Mean Stdev Mean Stdev Mean Stdev Mean StdevEquity Hedge Index 3.9% 2.0% -1.3% -2.4% -2.7% -0.1% 16.4% 10.2%Distressed Securities Index 7.4% 0.1% -0.6% -3.1% -6.8% 0.9% 14.7% 8.0%Macro Index 2.0% 1.5% -3.1% -2.6% 1.0% 0.7% 14.8% 9.1%Fund of Funds Index 1.9% 0.5% 0.3% -1.3% -2.2% 0.7% 9.8% 6.7%Equity Market Neutral Index -0.6% -0.2% 0.0% 0.1% 0.7% 0.2% 8.8% 3.4%Convertible Arbitrage Index 1.6% -0.6% -0.6% 0.3% -1.0% 0.4% 9.8% 4.8%Fixed Income: Arbitrage Index 2.3% 0.2% 0.5% -2.0% -2.8% 1.1% 8.1% 5.0%

CA Private Equity Index 1.5% 0.2% 2.3% -1.7% -3.6% 1.3% 14.6% 9.3%CA Venture Capital Index 12.9% 11.0% 2.5% -7.6% -15.1% -9.7% 20.6% 27.2%CA Private Equity Portfolio 7.2% 5.4% 2.4% -4.4% -9.3% -3.5% 17.6% 16.8%GSCI TR 3.9% -11.0% -2.3% -3.8% -1.7% 10.2% 8.7% 22.6%DJ-AIGCI 3.3% -5.1% -0.9% -2.2% -2.5% 5.5% 8.9% 14.2%

All Dates

Relative Relative Relative

Low Medium High

21

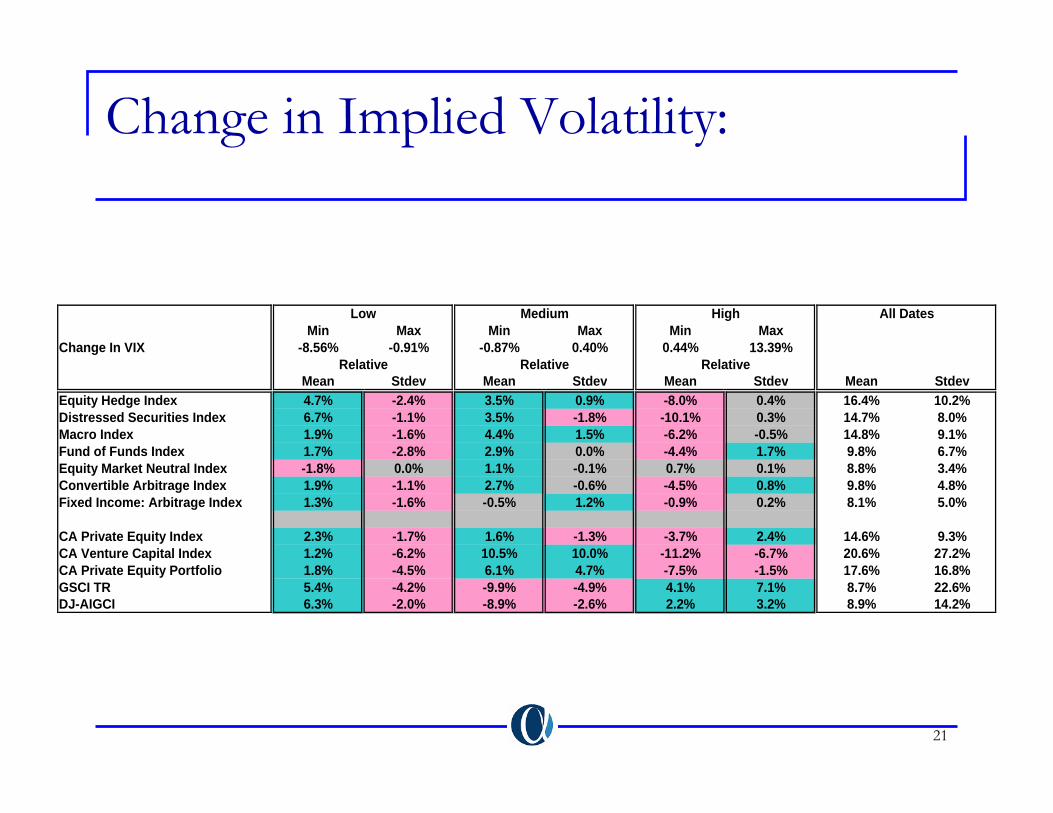

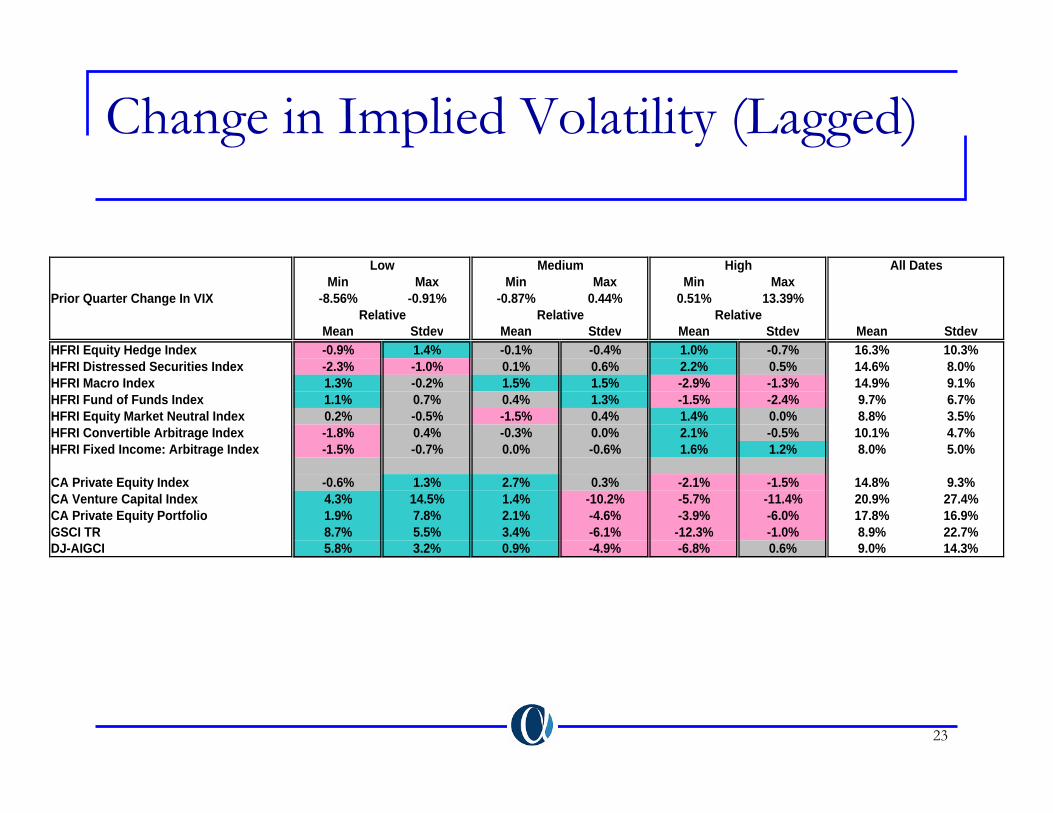

Change in Implied Volatility:

Min Max Min Max Min MaxChange In VIX -8.56% -0.91% -0.87% 0.40% 0.44% 13.39%

Mean Stdev Mean Stdev Mean Stdev Mean StdevEquity Hedge Index 4.7% -2.4% 3.5% 0.9% -8.0% 0.4% 16.4% 10.2%Distressed Securities Index 6.7% -1.1% 3.5% -1.8% -10.1% 0.3% 14.7% 8.0%Macro Index 1.9% -1.6% 4.4% 1.5% -6.2% -0.5% 14.8% 9.1%Fund of Funds Index 1.7% -2.8% 2.9% 0.0% -4.4% 1.7% 9.8% 6.7%Equity Market Neutral Index -1.8% 0.0% 1.1% -0.1% 0.7% 0.1% 8.8% 3.4%Convertible Arbitrage Index 1.9% -1.1% 2.7% -0.6% -4.5% 0.8% 9.8% 4.8%Fixed Income: Arbitrage Index 1.3% -1.6% -0.5% 1.2% -0.9% 0.2% 8.1% 5.0%

CA Private Equity Index 2.3% -1.7% 1.6% -1.3% -3.7% 2.4% 14.6% 9.3%CA Venture Capital Index 1.2% -6.2% 10.5% 10.0% -11.2% -6.7% 20.6% 27.2%CA Private Equity Portfolio 1.8% -4.5% 6.1% 4.7% -7.5% -1.5% 17.6% 16.8%GSCI TR 5.4% -4.2% -9.9% -4.9% 4.1% 7.1% 8.7% 22.6%DJ-AIGCI 6.3% -2.0% -8.9% -2.6% 2.2% 3.2% 8.9% 14.2%

All Dates

Relative Relative Relative

Low Medium High

22

Short-Term Rates

Min Max Min Max Min MaxT-Bill 0.93% 3.34% 3.48% 5.15% 5.16% 8.03%

Mean Stdev Mean Stdev Mean Stdev Mean StdevEquity Hedge Index -5.2% -1.5% -2.4% -2.0% 7.5% 2.2% 16.4% 10.2%Distressed Securities Index 1.7% -1.6% -2.1% 1.7% 0.3% -0.1% 14.7% 8.0%Macro Index 0.5% 1.0% -3.9% -2.6% 3.2% 1.1% 14.8% 9.1%Fund of Funds Index -1.3% -1.0% -1.7% 0.3% 2.9% 0.7% 9.8% 6.7%Equity Market Neutral Index -3.2% -0.4% -1.3% -0.1% 4.5% -0.7% 8.8% 3.4%Convertible Arbitrage Index -3.0% -0.2% 1.3% -0.2% 1.7% 0.2% 9.8% 4.8%Fixed Income: Arbitrage Index 1.6% -1.2% -2.5% 1.5% 0.8% -0.7% 8.1% 5.0%

CA Private Equity Index -2.2% 1.0% 1.1% -1.3% 1.2% 0.4% 14.6% 9.3%CA Venture Capital Index -23.0% -14.0% 5.8% -4.9% 17.7% 9.8% 20.6% 27.2%CA Private Equity Portfolio -12.6% -5.6% 3.5% -2.9% 9.4% 5.1% 17.6% 16.8%GSCI TR 0.4% -4.3% -9.0% -1.6% 8.3% 5.0% 8.7% 22.6%DJ-AIGCI -0.2% -2.1% -4.6% 1.1% 4.5% 1.1% 8.9% 14.2%

All Dates

Relative Relative Relative

Low Medium High

23

Change in Implied Volatility (Lagged)

Min Max Min Max Min MaxPrior Quarter Change In VIX -8.56% -0.91% -0.87% 0.44% 0.51% 13.39%

Mean Stdev Mean Stdev Mean Stdev Mean StdevHFRI Equity Hedge Index -0.9% 1.4% -0.1% -0.4% 1.0% -0.7% 16.3% 10.3%HFRI Distressed Securities Index -2.3% -1.0% 0.1% 0.6% 2.2% 0.5% 14.6% 8.0%HFRI Macro Index 1.3% -0.2% 1.5% 1.5% -2.9% -1.3% 14.9% 9.1%HFRI Fund of Funds Index 1.1% 0.7% 0.4% 1.3% -1.5% -2.4% 9.7% 6.7%HFRI Equity Market Neutral Index 0.2% -0.5% -1.5% 0.4% 1.4% 0.0% 8.8% 3.5%HFRI Convertible Arbitrage Index -1.8% 0.4% -0.3% 0.0% 2.1% -0.5% 10.1% 4.7%HFRI Fixed Income: Arbitrage Index -1.5% -0.7% 0.0% -0.6% 1.6% 1.2% 8.0% 5.0%

CA Private Equity Index -0.6% 1.3% 2.7% 0.3% -2.1% -1.5% 14.8% 9.3%CA Venture Capital Index 4.3% 14.5% 1.4% -10.2% -5.7% -11.4% 20.9% 27.4%CA Private Equity Portfolio 1.9% 7.8% 2.1% -4.6% -3.9% -6.0% 17.8% 16.9%GSCI TR 8.7% 5.5% 3.4% -6.1% -12.3% -1.0% 8.9% 22.7%DJ-AIGCI 5.8% 3.2% 0.9% -4.9% -6.8% 0.6% 9.0% 14.3%

All Dates

Relative Relative Relative

Low Medium High

24

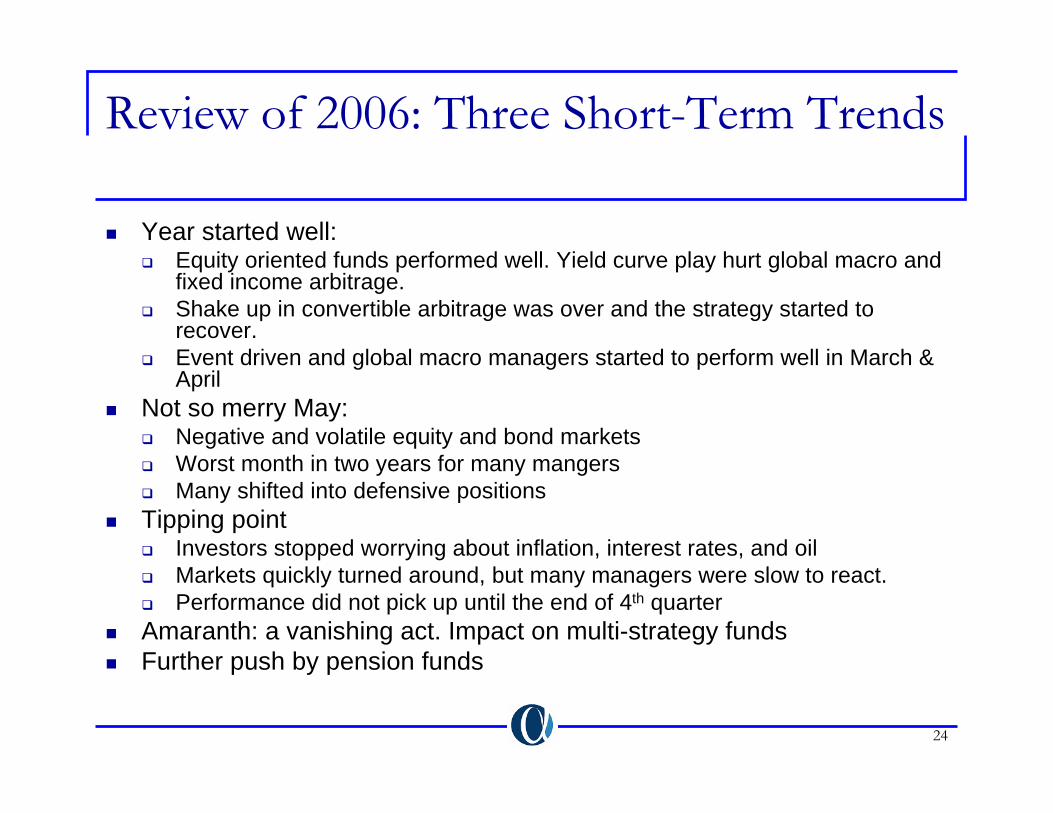

Review of 2006: Three Short-Term Trends

Year started well:Equity oriented funds performed well. Yield curve play hurt global macro and fixed income arbitrage.Shake up in convertible arbitrage was over and the strategy started to recover.Event driven and global macro managers started to perform well in March & April

Not so merry May:Negative and volatile equity and bond marketsWorst month in two years for many mangersMany shifted into defensive positions

Tipping pointInvestors stopped worrying about inflation, interest rates, and oilMarkets quickly turned around, but many managers were slow to react.Performance did not pick up until the end of 4th quarter

Amaranth: a vanishing act. Impact on multi-strategy fundsFurther push by pension funds

25

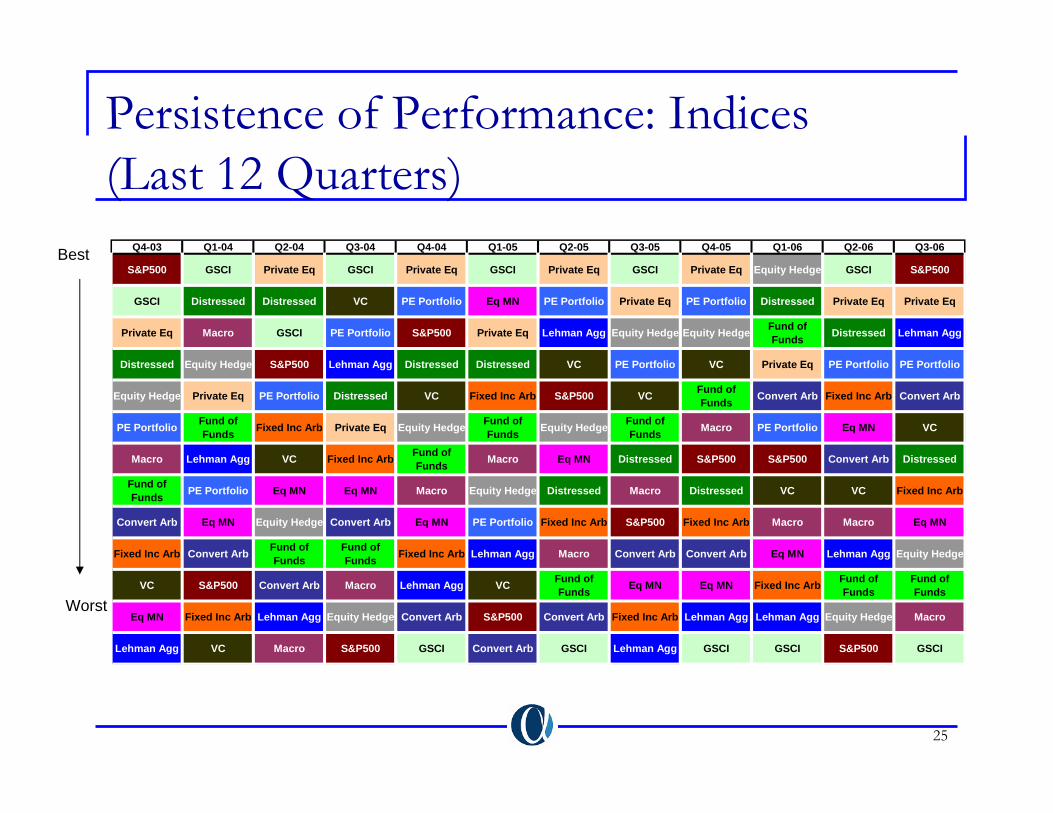

Persistence of Performance: Indices (Last 12 Quarters)

Best

Worst

Q4-03 Q1-04 Q2-04 Q3-04 Q4-04 Q1-05 Q2-05 Q3-05 Q4-05 Q1-06 Q2-06 Q3-06

S&P500 GSCI Private Eq GSCI Private Eq GSCI Private Eq GSCI Private Eq Equity Hedge GSCI S&P500

GSCI Distressed Distressed VC PE Portfolio Eq MN PE Portfolio Private Eq PE Portfolio Distressed Private Eq Private Eq

Private Eq Macro GSCI PE Portfolio S&P500 Private Eq Lehman Agg Equity Hedge Equity Hedge Fund of Funds Distressed Lehman Agg

Distressed Equity Hedge S&P500 Lehman Agg Distressed Distressed VC PE Portfolio VC Private Eq PE Portfolio PE Portfolio

Equity Hedge Private Eq PE Portfolio Distressed VC Fixed Inc Arb S&P500 VC Fund of Funds Convert Arb Fixed Inc Arb Convert Arb

PE Portfolio Fund of Funds Fixed Inc Arb Private Eq Equity Hedge Fund of

Funds Equity Hedge Fund of Funds Macro PE Portfolio Eq MN VC

Macro Lehman Agg VC Fixed Inc Arb Fund of Funds Macro Eq MN Distressed S&P500 S&P500 Convert Arb Distressed

Fund of Funds PE Portfolio Eq MN Eq MN Macro Equity Hedge Distressed Macro Distressed VC VC Fixed Inc Arb

Convert Arb Eq MN Equity Hedge Convert Arb Eq MN PE Portfolio Fixed Inc Arb S&P500 Fixed Inc Arb Macro Macro Eq MN

Fixed Inc Arb Convert Arb Fund of Funds

Fund of Funds Fixed Inc Arb Lehman Agg Macro Convert Arb Convert Arb Eq MN Lehman Agg Equity Hedge

VC S&P500 Convert Arb Macro Lehman Agg VC Fund of Funds Eq MN Eq MN Fixed Inc Arb Fund of

FundsFund of Funds

Eq MN Fixed Inc Arb Lehman Agg Equity Hedge Convert Arb S&P500 Convert Arb Fixed Inc Arb Lehman Agg Lehman Agg Equity Hedge Macro

Lehman Agg VC Macro S&P500 GSCI Convert Arb GSCI Lehman Agg GSCI GSCI S&P500 GSCI

26

Outlook 2007: What May Lie Ahead

Continued institutionalizations“Alternative Beta” products.

Further move toward permanent capital base.Can distressed securities strategy finally find the supply?Divergence of global monetary policies could benefit global macroM&A and other corporate events should continue to benefit event driven strategies.No sign of pick up in volatility means no relief for arbitrage strategies.

27

Alternative Betas & Alphas

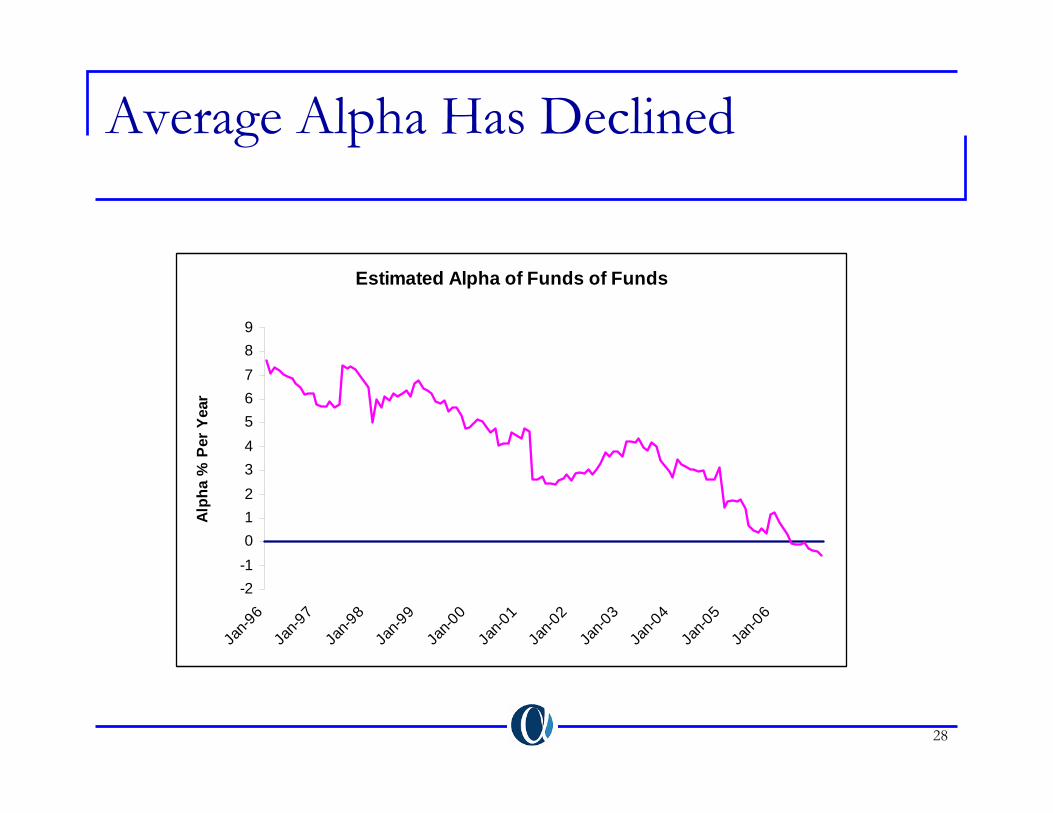

Using a single-factor benchmark (e.g., MSCI World), most hedge funds appear to have positive alpha.Using a multi-factor model, most hedge fund managers (about 75%) fail to deliver alpha on a consistent basis.Sources of returns for most hedge fund managers are from “alternative betas” (e.g., various types of credit, volatility, currency, commodity, illiquidity risks), rather than skill.A priori it is difficult to identify which managers will have positive alpha on a consistent basis.On average, hedge funds represent an expensive vehicle for accessing alternative sources of risk-return (betas).Using a multi-factor model we can see that average alpha of managers has been declining.Most top performing managers are closed or lack capacity

28

Average Alpha Has Declined

Estimated Alpha of Funds of Funds

-2-10123456789

Jan-9

6Ja

n-97

Jan-9

8Ja

n-99

Jan-0

0Ja

n-01

Jan-0

2Ja

n-03

Jan-0

4Ja

n-05

Jan-0

6

Alp

ha %

Per

Yea

r

29

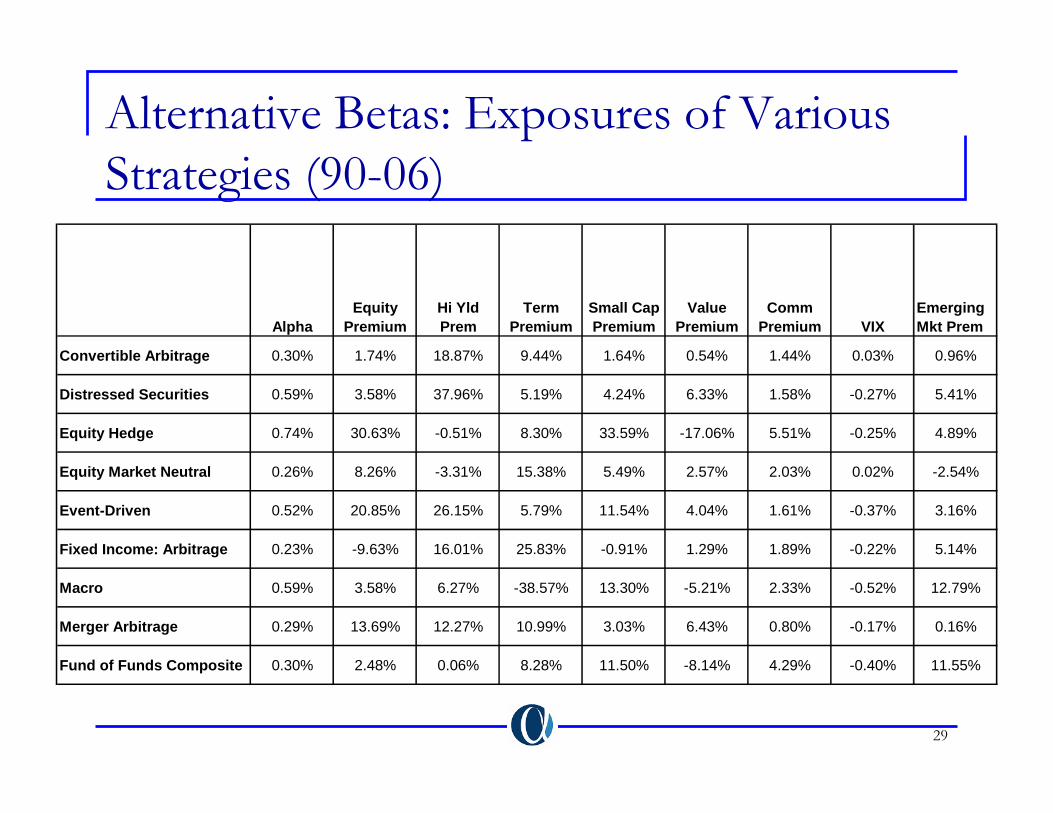

Alternative Betas: Exposures of Various Strategies (90-06)

AlphaEquity

PremiumHi Yld Prem

Term Premium

Small Cap Premium

Value Premium

Comm Premium VIX

Emerging Mkt Prem

Convertible Arbitrage 0.30% 1.74% 18.87% 9.44% 1.64% 0.54% 1.44% 0.03% 0.96%

Distressed Securities 0.59% 3.58% 37.96% 5.19% 4.24% 6.33% 1.58% -0.27% 5.41%

Equity Hedge 0.74% 30.63% -0.51% 8.30% 33.59% -17.06% 5.51% -0.25% 4.89%

Equity Market Neutral 0.26% 8.26% -3.31% 15.38% 5.49% 2.57% 2.03% 0.02% -2.54%

Event-Driven 0.52% 20.85% 26.15% 5.79% 11.54% 4.04% 1.61% -0.37% 3.16%

Fixed Income: Arbitrage 0.23% -9.63% 16.01% 25.83% -0.91% 1.29% 1.89% -0.22% 5.14%

Macro 0.59% 3.58% 6.27% -38.57% 13.30% -5.21% 2.33% -0.52% 12.79%

Merger Arbitrage 0.29% 13.69% 12.27% 10.99% 3.03% 6.43% 0.80% -0.17% 0.16%

Fund of Funds Composite 0.30% 2.48% 0.06% 8.28% 11.50% -8.14% 4.29% -0.40% 11.55%

30

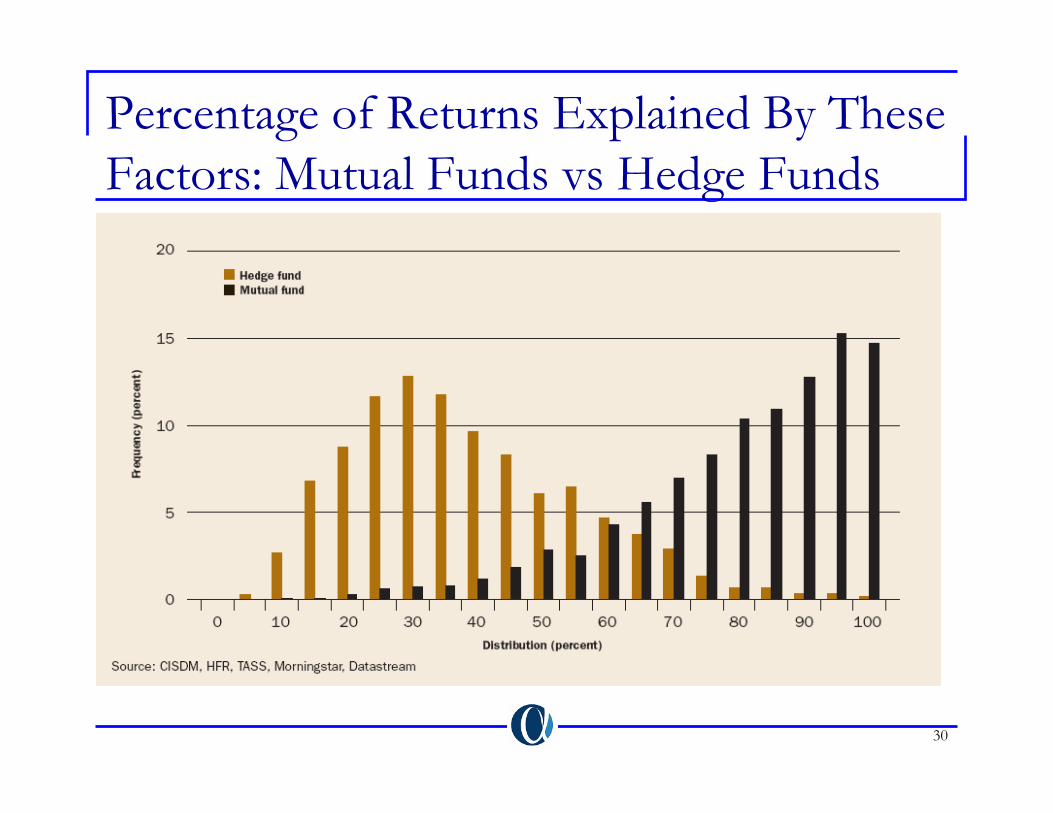

Percentage of Returns Explained By These Factors: Mutual Funds vs Hedge Funds

31

Why Replication Strategies?

Alphas for most hedge funds have been declining.More than 80% of the returns for most hedge funds comes from exposure to “alternative betas”.Hedge funds:

Lack transparency.Lack liquidity.Lack capacity (the good ones).Expose one to manager risk.Expose one to style drift.

Can go short replication strategies (Hedging hedge fund exposure!)Due diligence cost is very small.Investments do not have to be lumpy.Replication portfolios are typically well diversified.

32

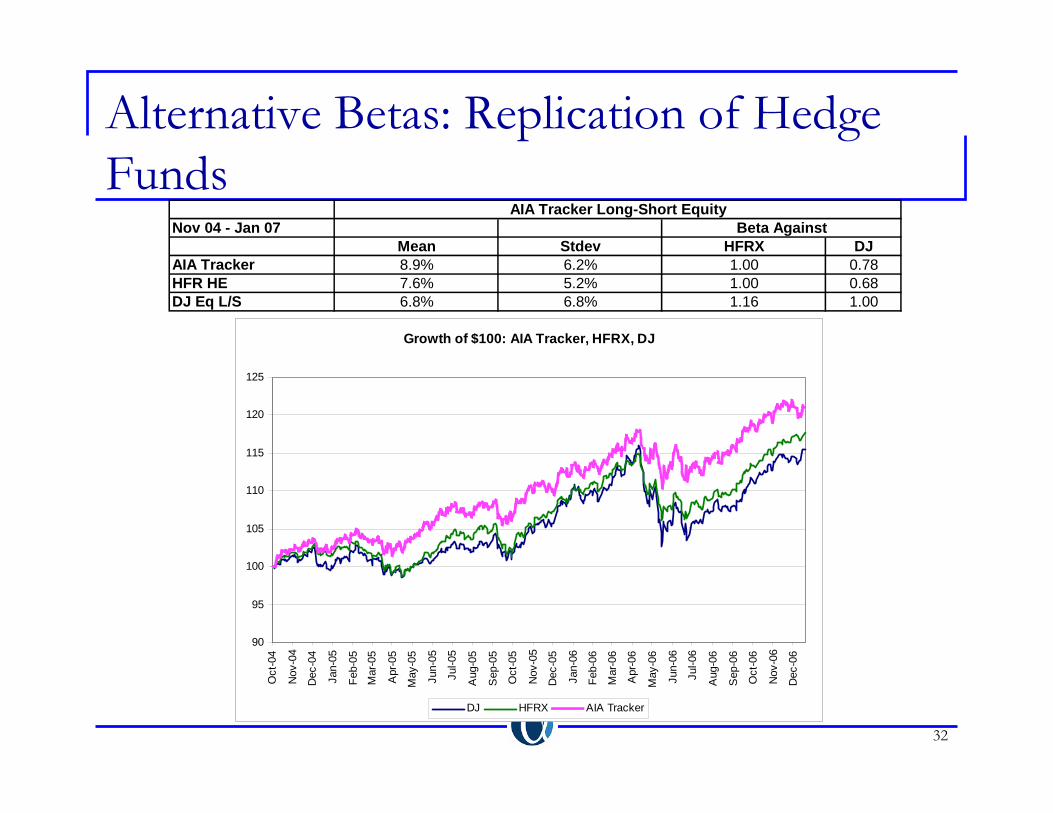

Alternative Betas: Replication of Hedge Funds

Nov 04 - Jan 07Mean Stdev HFRX DJ

AIA Tracker 8.9% 6.2% 1.00 0.78HFR HE 7.6% 5.2% 1.00 0.68DJ Eq L/S 6.8% 6.8% 1.16 1.00

Beta AgainstAIA Tracker Long-Short Equity

Growth of $100: AIA Tracker, HFRX, DJ

90

95

100

105

110

115

120

125

Oct

-04

Nov

-04

Dec

-04

Jan-

05

Feb-

05

Mar

-05

Apr

-05

May

-05

Jun-

05

Jul-0

5

Aug

-05

Sep

-05

Oct

-05

Nov

-05

Dec

-05

Jan-

06

Feb-

06

Mar

-06

Apr

-06

May

-06

Jun-

06

Jul-0

6

Aug

-06

Sep

-06

Oct

-06

Nov

-06

Dec

-06

DJ HFRX AIA Tracker

33

Replication Strategies: Multi-Factor Approach

The performance of a benchmark is tracked on monthly/daily basis through investment in a basket of liquid investments (small/large cap, value/growth, high/low quality bonds, vanillaoptions, etc). The objective to have a small tracking error on a monthly/daily basis.What happens if certain risk premiums disappear (value vsgrowth or small vs large)?What happens if a major source of return is not available through liquid traditional assets (e.g., illiquidity, certain credit risks)?Replication strategies buy what managers bought last period. Could lead to a situation where replication strategy is buying what managers are selling.Multi-factor approach is used by: Merrill Lynch, JP Morgan, Partners Group.Example: AIA Tracker

34

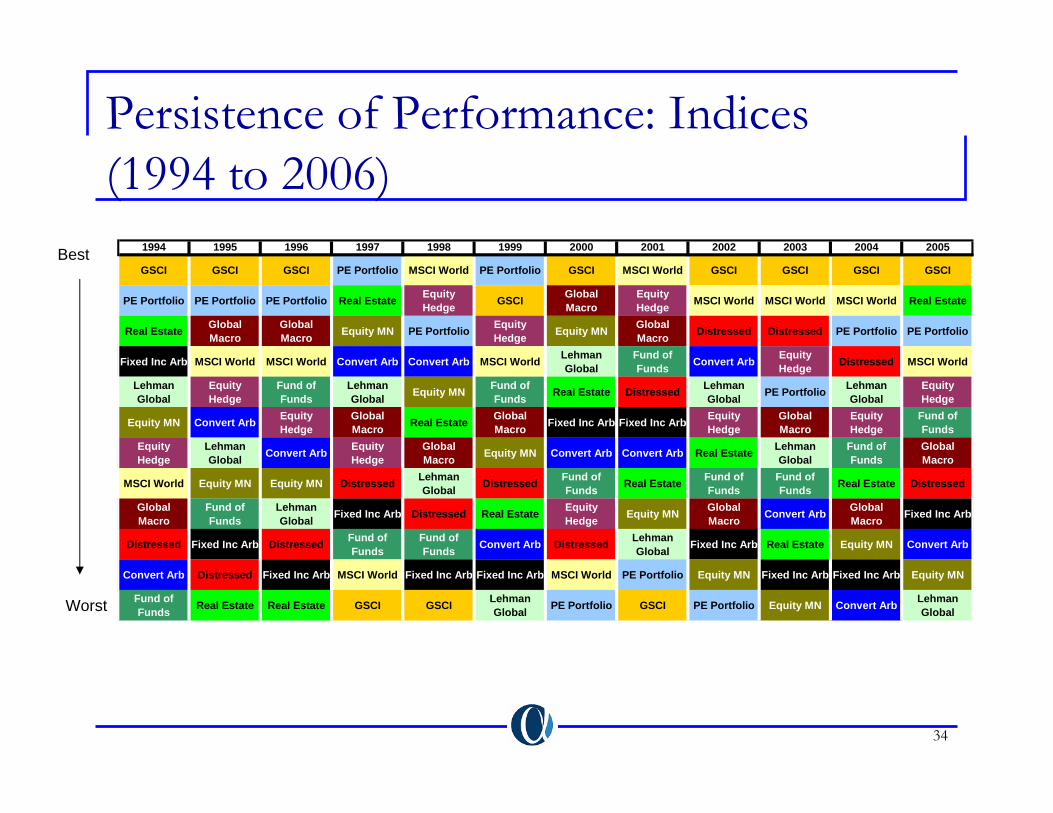

Persistence of Performance: Indices (1994 to 2006)

Best

Worst

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

GSCI GSCI GSCI PE Portfolio MSCI World PE Portfolio GSCI MSCI World GSCI GSCI GSCI GSCI

PE Portfolio PE Portfolio PE Portfolio Real Estate Equity Hedge GSCI Global

MacroEquity Hedge MSCI World MSCI World MSCI World Real Estate

Real Estate Global Macro

Global Macro Equity MN PE Portfolio Equity

Hedge Equity MN Global Macro Distressed Distressed PE Portfolio PE Portfolio

Fixed Inc Arb MSCI World MSCI World Convert Arb Convert Arb MSCI World Lehman Global

Fund of Funds Convert Arb Equity

Hedge Distressed MSCI World

Lehman Global

Equity Hedge

Fund of Funds

Lehman Global Equity MN Fund of

Funds Real Estate Distressed Lehman Global PE Portfolio Lehman

GlobalEquity Hedge

Equity MN Convert Arb Equity Hedge

Global Macro Real Estate Global

Macro Fixed Inc Arb Fixed Inc Arb Equity Hedge

Global Macro

Equity Hedge

Fund of Funds

Equity Hedge

Lehman Global Convert Arb Equity

HedgeGlobal Macro Equity MN Convert Arb Convert Arb Real Estate Lehman

GlobalFund of Funds

Global Macro

MSCI World Equity MN Equity MN Distressed Lehman Global Distressed Fund of

Funds Real Estate Fund of Funds

Fund of Funds Real Estate Distressed

Global Macro

Fund of Funds

Lehman Global Fixed Inc Arb Distressed Real Estate Equity

Hedge Equity MN Global Macro Convert Arb Global

Macro Fixed Inc Arb

Distressed Fixed Inc Arb Distressed Fund of Funds

Fund of Funds Convert Arb Distressed Lehman

Global Fixed Inc Arb Real Estate Equity MN Convert Arb

Convert Arb Distressed Fixed Inc Arb MSCI World Fixed Inc Arb Fixed Inc Arb MSCI World PE Portfolio Equity MN Fixed Inc Arb Fixed Inc Arb Equity MN

Fund of Funds Real Estate Real Estate GSCI GSCI Lehman

Global PE Portfolio GSCI PE Portfolio Equity MN Convert Arb Lehman Global

35

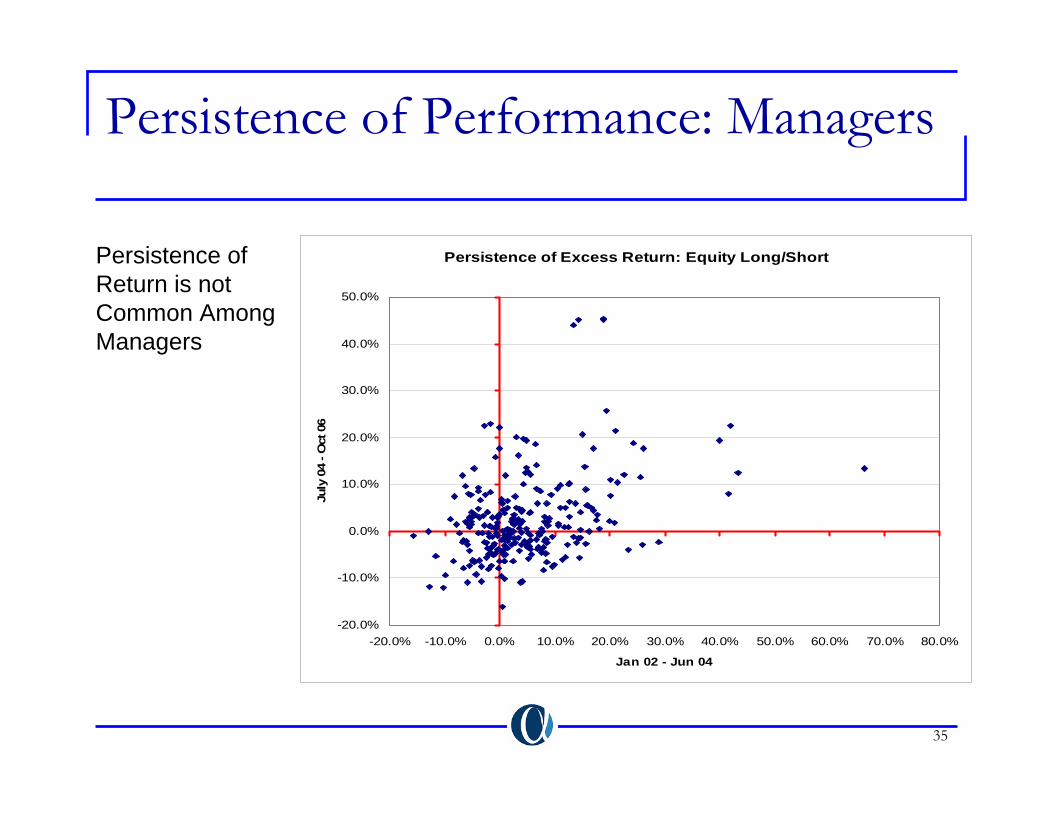

Persistence of Performance: Managers

Persistence of Excess Return: Equity Long/Short

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

-20.0% -10.0% 0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0% 80.0%

Jan 02 - Jun 04

July

04

- Oct

06

Persistence of Return is not Common Among Managers

36

Persistence of Performance: Managers

Persistence of Excess Volatility: Equity Long/Short

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0% 80.0% 90.0% 100.0%

Jan 02 - Jun 04

July

04

- Oct

06

Persistence of Risk or Exposure is more common

37

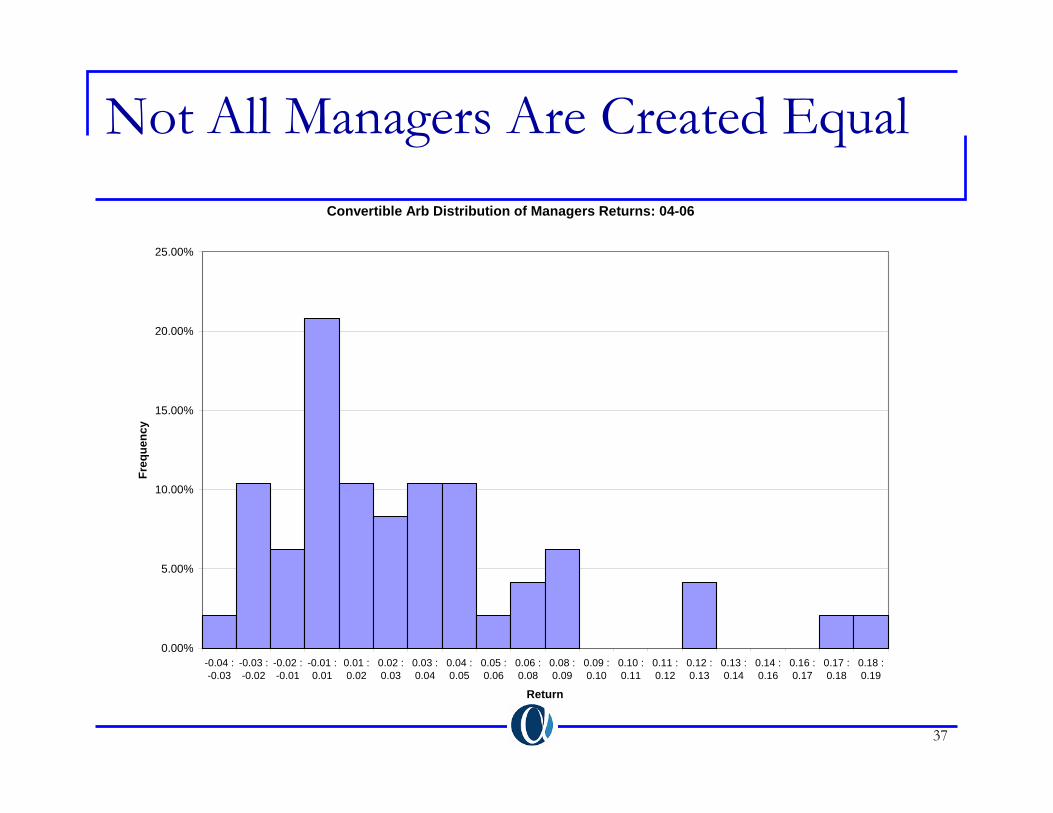

Not All Managers Are Created EqualConvertible Arb Distribution of Managers Returns: 04-06

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

-0.04 :-0.03

-0.03 :-0.02

-0.02 :-0.01

-0.01 :0.01

0.01 :0.02

0.02 :0.03

0.03 :0.04

0.04 :0.05

0.05 :0.06

0.06 :0.08

0.08 :0.09

0.09 :0.10

0.10 :0.11

0.11 :0.12

0.12 :0.13

0.13 :0.14

0.14 :0.16

0.16 :0.17

0.17 :0.18

0.18 :0.19

Return

Freq

uenc

y

38

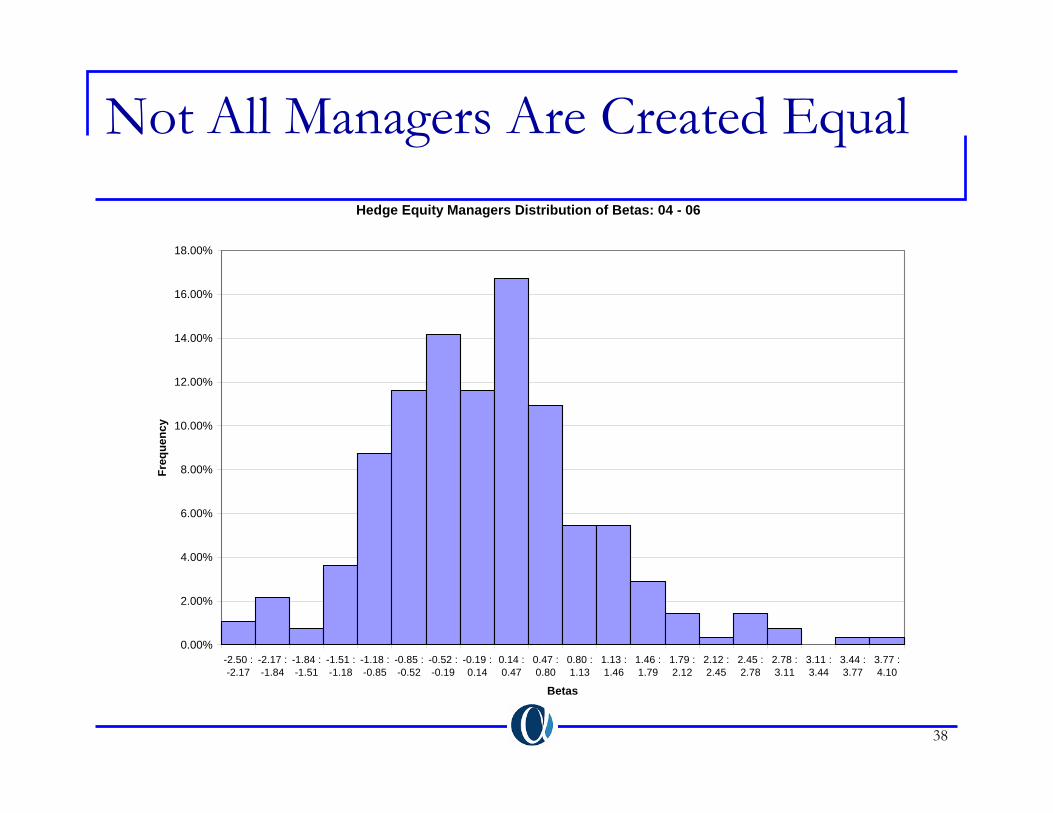

Not All Managers Are Created EqualHedge Equity Managers Distribution of Betas: 04 - 06

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

-2.50 :-2.17

-2.17 :-1.84

-1.84 :-1.51

-1.51 :-1.18

-1.18 :-0.85

-0.85 :-0.52

-0.52 :-0.19

-0.19 :0.14

0.14 :0.47

0.47 :0.80

0.80 :1.13

1.13 :1.46

1.46 :1.79

1.79 :2.12

2.12 :2.45

2.45 :2.78

2.78 :3.11

3.11 :3.44

3.44 :3.77

3.77 :4.10

Betas

Freq

uenc

y

39

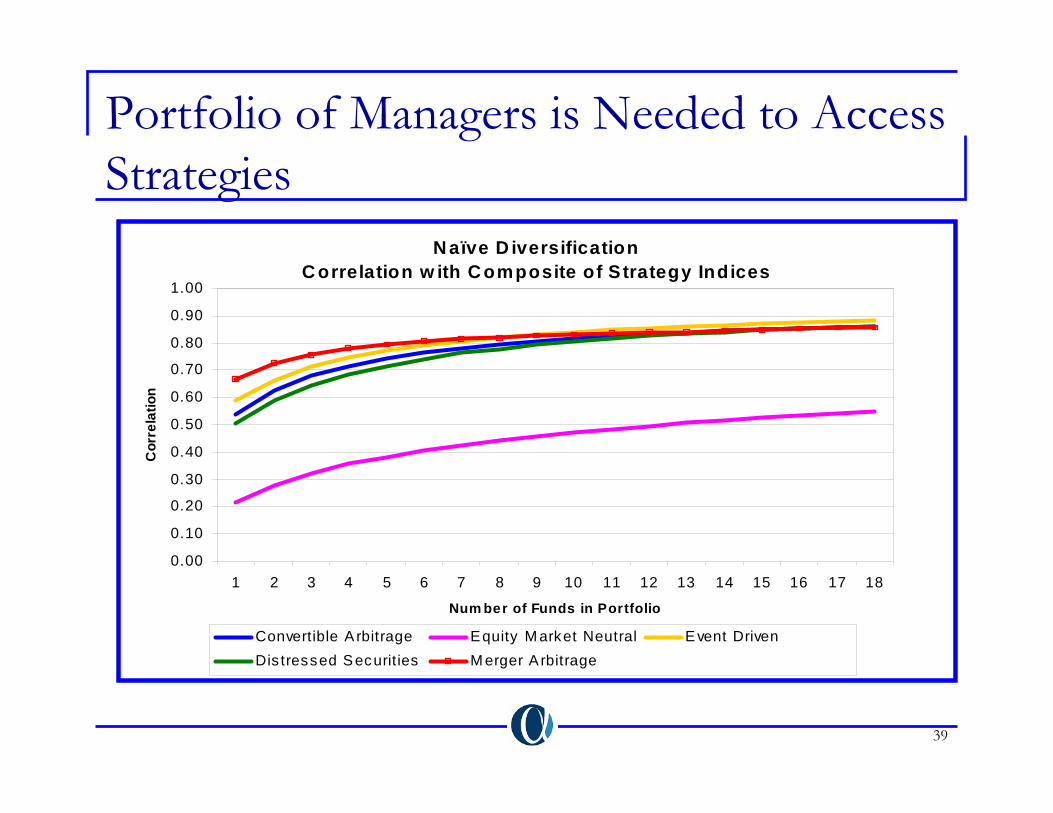

Portfolio of Managers is Needed to Access Strategies N aïve D iversification

C orrelation w ith C omposite of S trategy Indices

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

Num ber of Funds in Portfolio

Cor

rela

tion

Convertible A rbitrage Equity M arket Neutral Event DrivenDis tressed Securit ies M erger A rbitrage

40

Benefits of Funds of Funds

Reduced due diligence costs.Diversification by style: diversification across hedge fund strategies.Access to managers that are closed.May offer increased liquidity.Asset allocation: there is some evidence that hedge fund returns are predictable.Diversification by fund family and managers: reduced business risk and diversification of judgment.Investible Hedge Fund indices my serve as alternative.

41

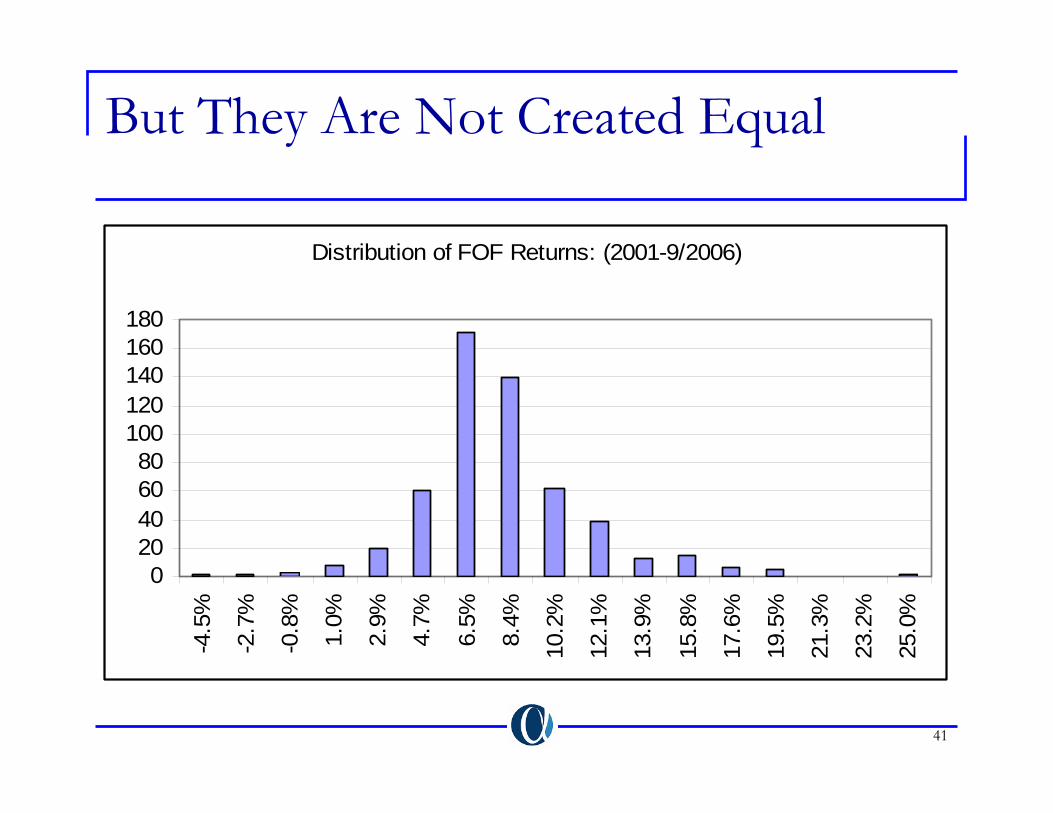

But They Are Not Created Equal

Distribution of FOF Returns: (2001-9/2006)

020406080

100120140160180

-4.5

%

-2.7

%

-0.8

%

1.0%

2.9%

4.7%

6.5%

8.4%

10.2

%

12.1

%

13.9

%

15.8

%

17.6

%

19.5

%

21.3

%

23.2

%

25.0

%

42

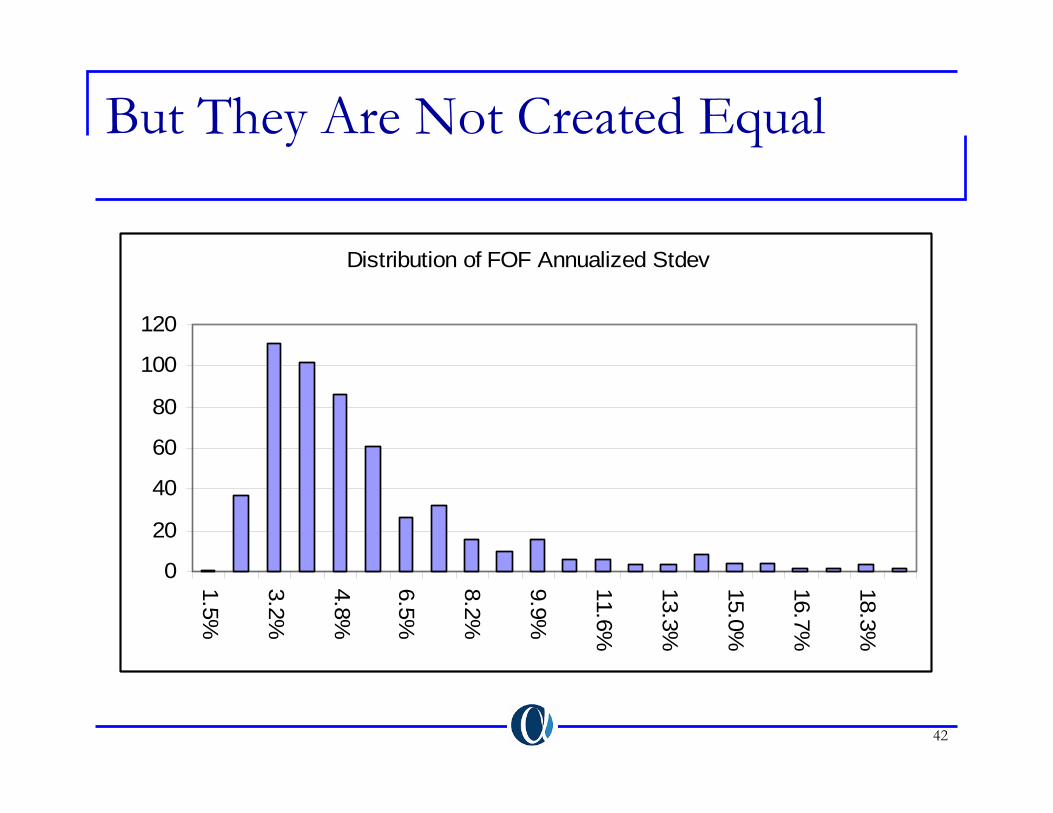

But They Are Not Created Equal

Distribution of FOF Annualized Stdev

0

20

40

60

80

100

120

1.5%

3.2%

4.8%

6.5%

8.2%

9.9%

11.6%

13.3%

15.0%

16.7%

18.3%

43

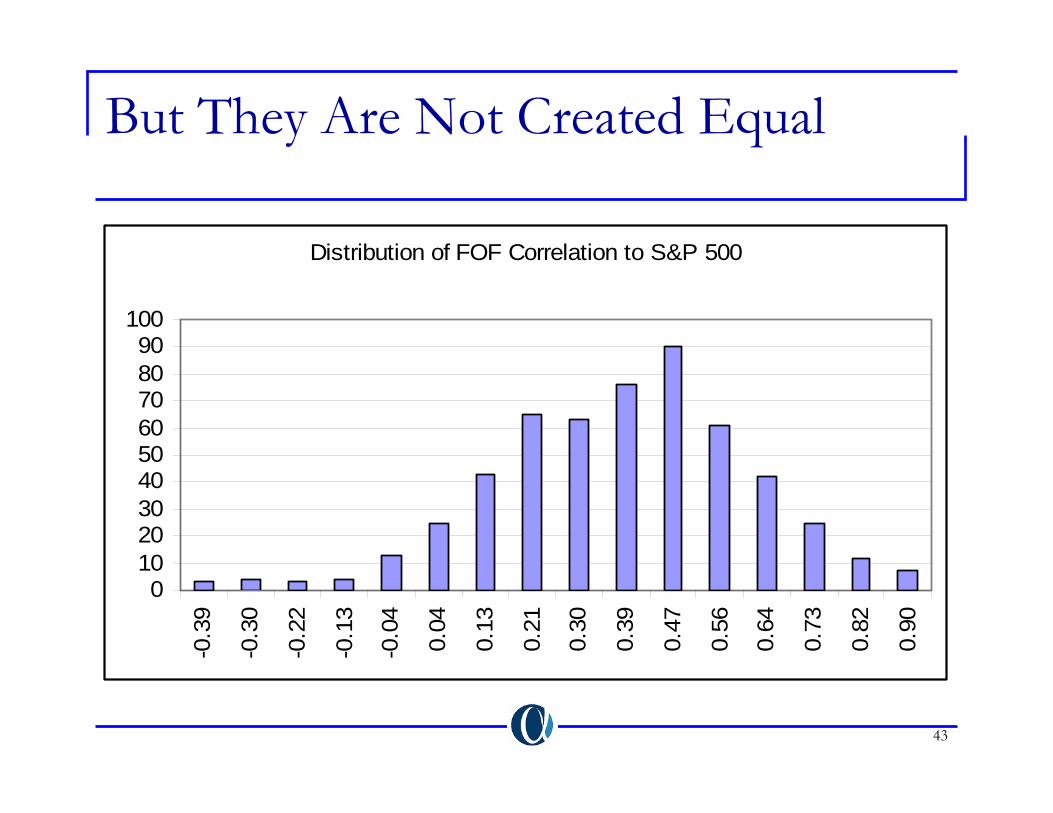

But They Are Not Created Equal

Distribution of FOF Correlation to S&P 500

0102030405060708090

100

-0.3

9

-0.3

0

-0.2

2

-0.1

3

-0.0

4

0.04

0.13

0.21

0.30

0.39

0.47

0.56

0.64

0.73

0.82

0.90

44

Conclusion: Alternatives, The Next Bubble?

Commodities (futures based): Investment has grown by 50% last year. Exceeding $100 billion. GSCI and DJ-AIG are major indices. Recent addition: Bach Commodity Index. Physical investment exceeds $2 trillion.Commercial Real Estate: Liquid investments (REITS) have doubled to $800 billion. Represents 5% of total global commercial real estate.Private Equity: Represented by limited partnerships. Total investment exceeds $1 trillion. Dominated by pension and endowments. Individuals hold about 15%.Hedge Funds: Steady growth reaching $1 trillion. Becoming increasingly institutionalized.Alternatives cover about 8% of the total investment universe (about $70 trillion)

45

Is There a Bubble?

Bubbles: Gains in asset prices far beyond their fundamental values.No known definite “test” to determine we are in a bubble.Typically, we find out about a bubble when the correction is already underway.What are the typical signals:

High recent returns (about 5 year).Expensive valuation metrics (yield below cost of carry).Speculative activity measured by volume and flows.Excessive leverage.

Each group of Alternatives may satisfy some of these tests. But none satisfies all of them. Oil represented the best case last year.

46

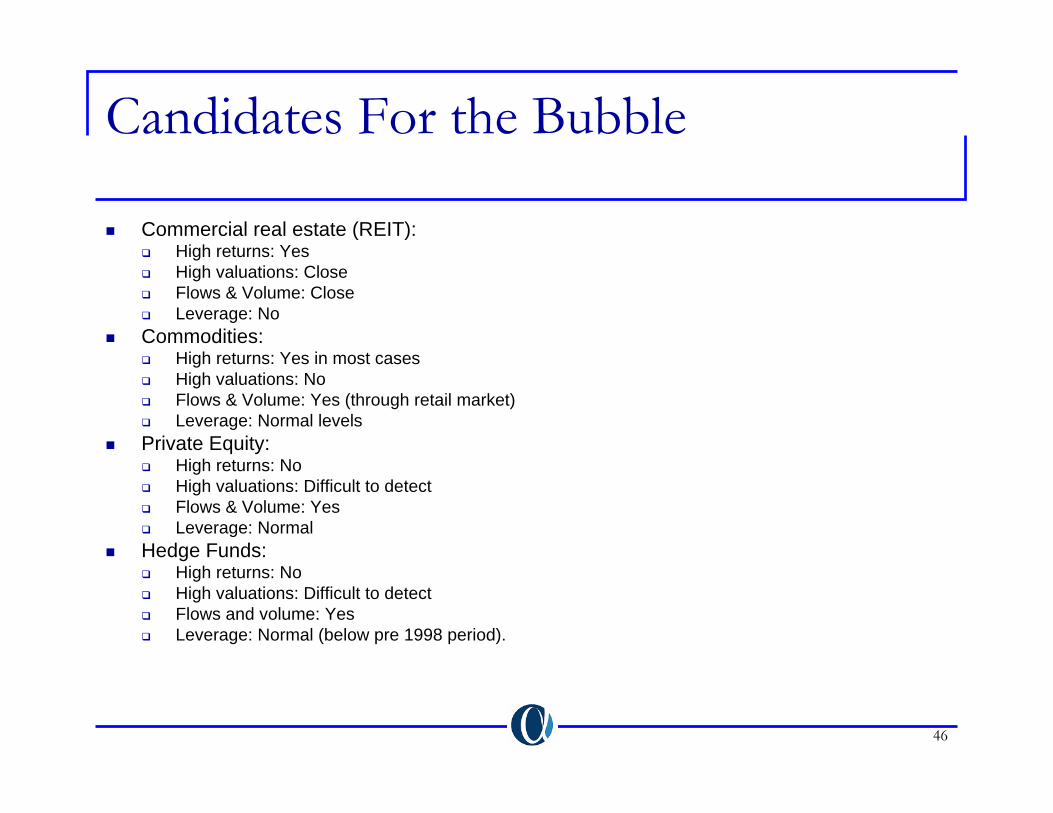

Candidates For the Bubble

Commercial real estate (REIT):High returns: YesHigh valuations: CloseFlows & Volume: CloseLeverage: No

Commodities:High returns: Yes in most casesHigh valuations: NoFlows & Volume: Yes (through retail market)Leverage: Normal levels

Private Equity:High returns: NoHigh valuations: Difficult to detectFlows & Volume: YesLeverage: Normal

Hedge Funds:High returns: NoHigh valuations: Difficult to detectFlows and volume: YesLeverage: Normal (below pre 1998 period).