alternative investments - lyxor asset management€¦ · · 2015-11-03july 2014 portfolio...

TRANSCRIPT

Alternativeinvestments

Investors want new and more flexible sources of return

In conversation:

Odi Lahav | Ben Shaw | Jean-Marc Stenger |

Emily Porter-Lynch | Simon Fox | Sebastian Cheek

J U LY 2 0 1 4 P O R T F O L I O P L AT F O R M

2 July 2014 portfolio platform: Alternative investments

Ben Shawpensions manager,

Telereal Trillium

Simon Foxprincipal,

Mercer

Odi LahavCEO,

Allenbridge Investment Solutions

July 2014 portfolio platform: Alternative investments 3

Jean-Marc StengerCIO for alternative investments,

Lyxor Asset Management

Emily Porter-Lynchdirector, investment advisory,

bfinance

Sebastian Cheekdeputy editor,

portfolio institutional

4 July 2014 portfolio platform: Alternative investments

New and more flexible sources of return

At the end of last year, f igures revealed global hedge fund assets stood at a record high of

$2.63trn; well above the pre-crisis peak of $1.87trn in 2007, while separate figures have found

28% of large institutional investors are likely to increase their allocation to hedge funds this

year.

With fixed income yields still low and equities looking expensive near all-time highs,

some commentators have touted this as the year alternative investments will step into the

mainstream. But, with investors still cautious about liquidity issues, poor performance and

scandal following the financial crisis, is this speculation too optimistic?

That all depends on whether investors are swayed by the merits of hedge funds and the

growing number of opportunities in other strategies, from alternative credit through to

infrastructure debt, which some might categorise as ‘alternative’ (although the precise

definiton of ‘alternative’ is hazy, as you will read).

In the case of hedge funds, advocates say by reconfiguring investments to spread exposure

across risk factors, institutional portfolios can benefit from better risk-adjusted returns,

greater diversif ication and lower correlation to markets – precisely what alternatives should

bring to a portfolio.

However, investors have to think carefully about how alternatives fit alongside traditional asset

classes in their portfolios. During the crisis, some alternatives became heavily correlated with

traditional assets and many defined benefit (DB) investors were left scarred as a result.

For defined contribution (DC) investors on the other hand, alternative assets have never

featured heavily in portfolios because of liquidity constraints and the need for daily pricing.

But, some believe there are ways to surmount these issues – through diversif ied growth

funds, for example – and as a result, DC could start to contribute meaningfully towards the

increasing inflows into alternatives.

For the most part however, alternatives remain the preserve of DB investors looking for added

sources of return and diversif ication. In this roundtable our panel of industry experts discuss

the changing world of alternatives from a DB and DC perspective, as well as the issues

involved in accessing them.

Sebastian Cheek

deputy editor, portfolio institutional

Sebastian Cheek

July 2014 portfolio platform: Alternative investments 5

At the end of 2013, global hedge fund assets stood at an all-time high of $2.63trn, well above

the pre-crisis peak of $1.87trn in 2007. Other data have shown 28% of large institutional

investors are looking to increase investments in hedge funds this year. With fixed income yields

still low and equities looking expensive, some commentators have touted 2014 as the year

alternative investments may step into the mainstream. So, let’s start by defining what we mean

by alternative assets.

Odi Lahav: Anything that isn’t mainstream is an alternative, with mainstream being standard equities,

bonds, some credit, and even real estate, which I don’t think is an alternative any more.

Jean-Marc Stenger: The old way to approach portfolio construction for institutional investors was to

split these portfolios in two: traditional assets on one side and alternative investments on the other, with

the traditional side holding the split between equity and bonds. Since the crisis, the trend has been to

construct broad portfolios in a different way, across investment styles. For instance, considering long/

short equities within the equity pocket.

Ben Shaw: Would you say long/short equity in a hedge fund construction is mainstream, or alternative?

Stenger: Today investors tend to mix all this within the same part of the broader portfolio.

Lahav: I’d agree with that, although there are still such things as alternative assets. Long/short equity is a

hedge fund. Hedge funds used to be called alternative. Is it still an alternative? Most investors today would

still define hedge funds as alternatives, and yet would think of long/short equity in portfolio construction

as part of the equity portfolio.

“Since the crisis, the trend has been to construct broad portfolios in a different

way, across investment styles. For instance, considering long/short equities

within the equity pocket.” Jean-Marc Stenger

Jean-Marc Stenger

6 July 2014 portfolio platform: Alternative investments

Shaw: It’s a real challenge, as different pension schemes or investors are going to define alternative

assets in different ways. I don’t think there’s a huge area of common ground for definition.

Simon Fox: People are thinking about it in terms of the drivers of returns. That will ultimately lead to peo-

ple thinking, not about having an alternative bucket, but how to diversify the portfolio. Some of those will

be traditional beta, some will be more exotic betas – credit such as high yield and and emerging market

debt (EMD). That continues through to the hedge funds base, and long/short equity is a good example.

Emily Porter-Lynch: It used to be very easy. You used to say it was high fees and a certain structure, but

now it’s a lot cheaper for everybody to access, which is very good.

Fox: The movement is coming in both ways: that traditional assets are becoming more alternative, and

alternatives are trying to become more traditional.

Stenger: Regulation will also bring these investment styles – hedge funds – into the broader asset mix of

our clients. Regulation of the alternative UCITS fund will allow more investors to consider these investment

styles, because it’s more regulated. It brings them some additional features which they are comfortable

with allocating to these assets for their broader portfolio.

Shaw: Would it make a clearer definition to say it’s investments that are not likely to be highly correlated

with the traditional asset classes of debt equity and arguably, real estate?

Porter-Lynch: Hedge funds are not purely alpha-driven strategies. Activists are often a long beta buy that

people pay high fees for as they think of them as hedge funds, and we still class them as alternatives, but

they have massive betas, don’t they?

Shaw: There is plenty of equity and debt/gilt exposure. We want things that are not correlated with those,

so you get a much smoother ride with investments. I would say long/

short hedge funds are likely to be highly correlated and therefore don’t

fall within an alternative bucket.

Stenger: The crisis taught investors that non-correlation is not true nec-

essarily every time. The point is it’s probably less correlated but you still

have some degree of correlation with traditional assets.

Fox: There’s also a risk you can become overly focused on correlation

as a metric. You can be very short-termist if you take that as your defin-

ing characteristic because some things will have spurious correlations at

periods of time, for instance with equity. Some strategies actually work

better with a degree of market risk embedded within them. You’re still

getting lots of differentiated returns, but you have to accept there’s going

to be some beta as part of it.

So is it about looking at it in terms of risk factors?

Lahav: That’s more an analysis that you do when you’re constructing a portfolio, as those things can be

misleading. It also depends a lot on manager style and you have to consider liquidity, which is not going

to be captured in a factor regression. This type of portfolio analysis was quite popular in the early 1990s

and resurged again over the last three or four years, but its popularity seems to be fading again.

Fox: There are soft and hard uses of it. The quantitative description Odi gave I’d put at the hard end,

where people are really trying to statistically drag out factors and build the portfolios. At the softer end, it’s

about what’s driving the performance, the strategy. Is it traditional beta, is it something else, and can you

differentiate what’s driving this investment versus another? Assigning risk factors in that sense, not neces-

sarily trying to be overly prescriptive in terms of what those factors are, but thinking about getting different

sources of return into the portfolio from a qualitative perspective has merit in a lot of cases.

I’d also argue the client base we work with is changing as well. The growth of defined contribution (DC) is

huge and it’s going to overtake defined benefit (DB) in very short order. What the alternatives are for DC,

and what is acceptable within the DC framework is very different from the DB perspective. That process

Odi Lahav

July 2014 portfolio platform: Alternative investments 7

is also introducing more of a continuum between those traditionally labelled as institutional investors and

the high net worth and family office side. The insurers are thinking about how they rebuild their portfolios

in light of regulatory changes.

Overall, the client base – and what they’re looking for from different investments – is evolving, and that has

an impact on how we define things.

Lahav: I believe that conceptually DB and DC should be managed in the same way, as the endgame of

pensions savings is the same, but unfortunately regulations don’t allow for anything that doesn’t have

pretty much daily liquidity in DC. People in DC schemes tend to lose out because they don’t have the

diversification of sources of return that you have within a DB scheme.

Shaw: From our experience, more than 90% of people opt for the default fund, and the default tends to be

suggested by the advisers – very cautious, safe – made up of equities, debt and probably no alternatives

in it. Hedge funds, even property, have very small allocations.

Lahav: DC funds need to offer certain levels of liquidity, which you can’t do if you, say, manage a

real estate fund.

Shaw: You can, by investing in REITs, or if large enough, by having the liquidity necessary. The reality,

though, is the consultants tend to play it safe and suggest something that doesn’t include alternatives or

a very small allocation to alternatives.

Fox: There are few schemes out there that can do the commingling in the way you describe to blend the

liquidity. Most are constrained by liquidity. The other thing is fees. That does affect a lot of DC investments.

“You’ve got all these – probably the most complex – funds that investors are

now going out to direct invest with. That’s a growing trend and I think it will

probably end in tears at some stage.” Emily Porter-Lynch

Emily Porter-Lynch and Ben Shaw

8 July 2014 portfolio platform: Alternative investments

Shaw: I don’t think the commingling is an issue because we do it through a large insurer, who provides

it for many, many other schemes other than ours. I imagine most small to medium-sized businesses do it

that way and therefore you do get the liquidity.

So what’s driving demand?

Stenger: There are two forces at work. The first is the need for more flexibility in the allocation which is

probably brought by hedge fund strategies. The other goes back to the point about regulation and the fact

that this industry is more mature today. A traditional hedge fund shop used to have one offshore vehicle;

nowadays they probably have two or three: one onshore, one UCITS, addressing different investor needs

with a different degree of flexibility in the way they manage the portfolio. There are different constraints in

terms of management, but at the end of the day more suitability for this type of investor.

Fox: For three years in the UK, the most popular manager search we’ve carried out has been for multi-

asset investing, for diversified growth funds (DGFs), which do embed alternatives.

There are merits for those from a DC context and they add value. We think they make sense, but they are

still only one step along that alternative spectrum and don’t provide exposure to the full range of return

sources you can get from alternatives.

Lahav: The main issue remains liquidity. You can’t put private equity fund investments, for example, into a

DGF if you’re going to be sensible and you need to match liquidity you offer on the other side to investors.

Simon Fox, Jean-Marc Stenger and Odi Lahav

“There are merits for [DGFs] from a DC context and they do add value. But

they are still only one step along that alternative spectrum and don’t provide

exposure to the full range of return sources from alternatives.” Simon Fox

July 2014 portfolio platform: Alternative investments 9

What have investors learnt from the financial crisis?

Shaw: We know that many hedge funds are correlated with traditional asset classes of equities or bonds,

depending on their strategies. The big mistake many people made is having an allocation to hedge funds

but not really understanding the different strategies that hedge funds followed and therefore the correla-

tions they had with the underlying assets.

People who are investing in hedge funds now have a much clearer idea of what that hedge fund is doing

and what it’s likely to be correlated with.

Lahav: People didn’t understand what they invested in, and to me that is absolutely the main lesson.

It’s caveat emptor. That, to me, is to understand all the facets of an investment and the market in which

it operates.

Fox: The flipside is people have learnt you need to build a growth portfolio that’s well diversified as a start-

ing point. That means hedge funds are part of that solution, and that if you try to get all your growth from

equities, you have got all your eggs in one basket, and you will be subject to big swings. There’s no silver

bullet with alternatives but the benefits of a balanced portfolio are clearly important.

Porter-Lynch: The rush into macro and CTA after the crisis just shows that people were wanting some

diversification. When I was with USS, we looked at the governance aspect, because while you might

know exactly what’s in the portfolio, if something happens within that fund and the directors act immorally,

perhaps, that’s pretty indefensible to your underlying investors, who you need to defend against that risk.

Investos are a lot more aware of the structures they’re investing in, not just ticking boxes.

Stenger: Prior to the crisis investors tended to see hedge funds as a homogenous space. They are now,

generally, more knowledgeable and able to be more granular in their understanding of them. Once you get

an exposure within your hedge fund portfolio to CTAs or global macro

strategies, you load in your own portfolio some exposures or perfor-

mance drivers which are clearly completely different.

Shaw: Some people were blinkered by a style manager who’d had great

performance and they trusted the manager, didn’t ask as many ques-

tions as they should have. Now we have consultants who are much

better at going in and deciphering what’s happening; what risk controls

are around, and a better framework for investing.

Are investors seeking greater liquidity?

Fox: There’s a distinct difference between the different layers of liquidity

across the hedge fund space. The challenge for many investors is to

understand how to get compensated for giving up a degree of illiquidity.

Shaw: Do you see a return premium for locking your money up for a

longer amount of time?

Stenger: The industry has evolved, and if investors sacrifice part of the

liquidity, they expect to be able to measure precisely the extra benefit

they will get from doing that. We have found managed accounts are a very efficient tool to align interests

between investors and hedge fund managers. For instance, to make sure the fee structure fits each other’s

interests perfectly or to align the effective liquidity of the portfolio to the terms of the fund, from weekly to

monthly to quarterly.

Lahav: The other thing to consider is that liquidity risk premium changes over time. So at the point where

everybody wants their money back and you have cash to make an investment, you would probably get a

better liquidity premium in that particular sector which maybe is out of favour. It’s not something you can

bank on. The only other objectively clear and quantifiable liquidity premium is if you get a fee reduction in

exchange for longer lockups.

Stenger: Our studies show that depending on the period of time, active portfolio management at funds

Ben Shaw

10 July 2014 portfolio platform: Alternative investments

of funds level brings an additional 1% to 5% net return per year to the investor on top of manager’s return.

It is about going from one hedge fund strategy to another at the right point in time as much as choosing

the right manager within each strategy.

On the liquidity side, figures are difficult to come by, but it could be as high as 10% or 15%, like 2009 or

almost zero. During those periods of time, you are clearly better off being in a liquid strategy – in 2011,

for instance. The key question is how to allocate and what type of performance drivers or allocation deci-

sions to take.

Fox: Looking at funds of hedge funds performance last year, there was clearly a kicker for those man-

agers that had more beta, more illiquidity, versus the ones that are more lowly correlated, less beta and

probably more liquid. There’s a danger as people look back on performance track records, they think they

would prefer the one that delivered 14%, not 6%, and you get back to a pre-2008 mindset where people

load up on illiquidity and beta, at precisely the wrong moment, forgetting the lessons of diversification.

What do hedge funds bring and how do they fit among traditional asset classes?

Porter-Lynch: There’s got to be a bit of an understanding that long-only haven’t tended to perform as

people hoped they would. A lot of the talent has gone to hedge funds and you can’t argue with the eco-

nomics – it attracts the best talent in the business. To access those potential returns, you have to pay

increased fees, and that’s the negative association with investing with these teams. Investors are realising

that the returns can be interesting and diversifying, that’s what makes it so attractive, and that if you want

“The default tends to be suggested by the advisers – very cautious, safe – made

up of equities, debt and probably no alternatives in it. Hedge funds, even

property, have very small allocations.” Ben Shaw

July 2014 portfolio platform: Alternative investments 11

to access those people then you need to pay high fees for it. Investors aren’t always so nervous about

fees.

Stenger: It seems to me the debate is actually not really about the absolute level of fees investors are

paying in that space. If you think in terms of value creation or capital appreciation, investors are very sensi-

tive if too large a chunk stays with the hedge fund manager. There should be an appropriate balance here

and that’s what pushes clients and providers like ourselves to basically have the fees reduced.

Porter-Lynch: They’ve got to pay the fees on the risk. I find it amazing that people still look at the

absolute level of fees versus the actual risk they are taking for a given level of fees. If somebody’s taking a

lot of risk for fairly high fees, compared to someone running a much lower risk portfolio for standard fees,

you’re not going to get the same upside potential from the lower fee manager despite the fee discount.

Do investors view fees in an absolute way?

Porter-Lynch: There are two types of multi-strategy manager. One who charges a fee up-front, and then

manages everything from there. Then there are the multi-strategists who pay a pass through. That cre-

ates a massive impact in your portfolio, and you think on the top line it’s a lot less fees, but you have to

understand what’s going on underneath because of hidden fees and netting between underlying funds.

Fox: Trustees aren’t arguing over the nuance of the fee arrangements. We do, and we make judgments

in terms of whether we think things will add value, net of fees. That said, there will be a few investors out

there who do take a slightly moral view in terms of whether it’s appropriate or not to be paying a manager

that much money, particularly when they have pensioners that are earning fractions of that every year,

having to work hard. We ultimately invest in hedge funds from a purely financial perspective, and the

industry’s in part addressed that, because fees have been coming down. Often there’s a justification for

higher fees, either because the manager’s closed, because they offer some sort of multi-strategy combi-

nation where there is netting risk and they have to capture it, or otherwise.

Lahav: At the risk of oversimplifying, I bifurcate our client base in terms of sophistication and a proxy of

12 July 2014 portfolio platform: Alternative investments

that is their size. The larger players with more sophisticated, potentially internal investment teams, and

maybe a handful of trustees that are well-versed in investments and understand, don’t mind paying the

high fees, and are more worried about what they’re getting for it than they are about the actual fee levels

in isolation. Then there are others, perhaps, who see the term ‘hedge fund’ and refuse to pay those fees.

They’re simply not interested in any discussion about what the net return is or the risk/return parameters.

Every investor is different, but how are investors looking to access hedge funds?

Stenger: We position ourselves more as a centre of expertise for hedge fund investments, rather than

as we used to be, a traditional funds of hedge funds manager. Depending on the needs of the investors,

we’ll aggregate all this expertise in a dedicated funds of funds format, and clients will leave us with the

discretionary portfolio management. Or we put our hedge fund selection team in front of the clients who

know where they want to go to advise them purely on manager selection. We need more flexibility and to

be more pragmatic in what investors are expecting from companies like ourselves.

The UK market is very consultant-driven, so is it rare for you to liaise directly with the client?

Stenger: There is no one single type of client, but obviously we need to fit into an approach the client

is considering, often with the help of a consultant. When we say we need to customise the hedge fund

solution to the need of the clients, that’s what it means. This could be a risk approach or ALM and you

need to be able to adjust your solution and the service you offer to your clients, to this new environment.

Lahav: Funds of funds were decimated post-crisis and in fairness many made a lot of mistakes. Many

schemes went direct but have realised they don’t have the governance structures for it, even with consult-

ants. So there’s been a resurgence as the funds of funds have looked for

ways to evolve their businesses. Other participants – including the big

consultants, who are arguably the largest funds of funds – have evolved

their businesses to offer bespoke services at a cheaper price than they

were offering pooled fund services.

Porter-Lynch: If you have a certain level of assets internally, you can

create bespoke mandates and control it. But you do need to be a certain

size, with the right skills and resources.

Stenger: All investors need advice from investment professionals. You

can go direct or you can go through a dedicated fund of funds, but you

still rely on advisers at some point in time.

Porter-Lynch: A lot of multi-strat funds are actually getting approaches

direct from pension schemes at the moment. That’s quite daunting as

looking at a multi-strategy fund is very difficult, because of all the differ-

ent levers that are working. Then somebody who doesn’t specialise tries

to figure out which is the best one to buy. If you look at the stats, multi-strats often have the worst issues

because they often add leverage and other strategies that perhaps are not with the best managers and

they just don’t understand. You’ve got all these – probably the most complex – funds that investors are

now going out to direct invest with. That’s a growing trend and I think it will probably end in tears at some

stage.

Stenger: The 50 largest multi-strat funds are not diversified. They have – all of them – a bias either to

equity strategies or macro. It’s different from a truly diversified portfolio. At the level of the investors’ port-

folios it creates a kind of index approach to our hedge fund strategies. If you look between a portfolio of

community strategy managers and HFR Index, you will find high correlation.

Fox: Manager selection is important and there are difficulties in selecting any type of hedge fund, but

multi-strats can be part of the solution. The important thing is to understand what you’re buying and

understand you’re going to have a tilt associated with it. That doesn’t invalidate it as part of a growth

Emily Porter-Lynch

July 2014 portfolio platform: Alternative investments 13

portfolio, but it does mean you’ve got to think about the concentration risk, what you’re missing and the

other drivers for return you can build in around it as well.

Lahav: I haven’t seen that trend in our business, but I agree with what Emily is saying and it is certainly a

cause for concern, as they’re going to end up being heavily focused on global macro or equities.

We’ve seen more investors moving to alternatives in the last year or so. Will that continue?

Fox: The growth of the hedge fund assets is not a surprise, but I don’t equate that with people thinking

hedge funds are the best thing since sliced bread. They are part of a properly diversified growth portfolio

and people need to add diversification to the exposures they already have. I think it will continue to grow.

Stenger: The search for more flexible investment solutions and new sources of return is for the long

run. The industry is maturing and there are new investment solutions, new ways to access these invest-

ment styles. So it’s probably a bit new for many investors but slowly investors will definitely increase their

allocations.

Lahav: I see money flowing into bank disintermediation. Direct lending to SMEs across Europe,

real estate-backed lending strategies, off-balance sheet CLO structuring, trade financing and private

equity structures rather than hedge funds. A move away from developed market equities to emerging

markets in a very specific and tactical way. People feel a little more comfortable with risk, so I see growth

in alternatives.

“I see a move away from developed to emerging markets in a very specific and

tactical way. People are feeling a little bit more comfortable with risk and I

think there’s going to be more moving in general into alternatives.” Odi Lahav

Jean-Marc Stenger and Odi Lahav

14 July 2014 portfolio platform: Alternative investments

Foreword

Total assets under management for the hedge fund industry reached an all-

time high of USD 2.6trn in 2013. With lower expectations for traditional assets,

many institutional investors, including pension funds and corporates, are

increasing their allocation to alternative assets to secure both performance

and resilience for their portfolios. As a result, hedge funds are now growing

faster than any other type of asset. They are expected to reach USD 3.3trn

by 2015 with a compound annual growth rate of around 15%.

This 11th white paper looks at hedge funds from a new perspective, in the context of Strategic Asset

Allocation (SAA). We see the growth of the assets managed the industry as an implicit consequence

of the different approach taken with regard to hedge fund investments.

Numerous studies using pre-2008 data have shown the benefits of adding hedge funds to SAA.

Hedge funds were previously considered to be a stand-alone asset which should account for a small

percentage of overall portfolios. Now, in the aftermath of the financial crisis, a new paradigm has

appeared: hedge funds are becoming mature investment styles exhibiting significant and persistent

performance divergence both with each other and when compared to traditional assets.

As such, hedge fund strategies should be disaggregated into sensible sub-categories which should

naturally migrate from a stand-alone asset into the broader equity and bond asset-mix. In this context,

we propose a reassessment of the relationship between hedge fund strategies and traditional markets

to introduce an updated SAA framework with hedge funds.

To highlight the above points, this paper addresses the following structural questions:

– What are the stylised facts of hedge fund performance in the post-2008 environment?

– How should we classify hedge funds in order to better reflect their true characteristics?

– What is the best way to integrate the new classification process into a SAA approach?

We hope you will find this article both interesting and useful in practice.

Alternative investments, including hedge funds, have

grown faster than non-alternatives and have now

surpassed their 2007 levels. Thus, many institutional

investors, including pension funds and corporate, are

lending increasing allocation to alternative assets,

especially hedge funds, to secure both performance and

resilience for their portfolios. Hedge funds have always

been considered as attractive investment tools driven

by appealing homogeneous historical performance

before 2008. However, the hedge fund industry has been profoundly revolutionised after 2008 and a

new paradigm appears. Hedge funds become more mature and granular. Investors have to study their

relationship with traditional assets in order to smartly introduce hedge funds in the Strategic Asset

Allocation (SAA) framework.

Lyxor’s new model for strategic asset allocation with hedge funds

By Jean-Marc Stenger, chief investment officer for alternative investment, Lyxor Asset Management

By Zélia Cazalet and Ban Zheng, research, Lyxor Asset Management

July 2014 portfolio platform: Alternative investments 15

Many academic studies show that hedge funds are generally more resilient than equities and bonds

in extreme periods. Before 2008, they also report homogeneous attractive performance for almost

all hedge fund strategies. This homogeneity allows investors to traditionally consider hedge funds

as a stand-alone asset class in strategic asset allocation. Nevertheless, hedge fund industry has

recently shown new characteristics. While hedge funds’ performances were quite similar in terms of

risk/return profile before 2008, more significant differences appeared during and after the crisis. For

example, in 2008, the Global Macro strategy delivered a promising positive performance whereas

other main strategies suffered significant losses. It seems that the tendency of SAA with hedge funds

is characterised by their migration from a stand-alone asset to the equity and bond portions. With this

new paradigm, the traditional approach is not adapted anymore. Considering hedge funds as a stand-

alone asset class has to give way to alternative approaches with more mature expectations. Hence

the relationship between hedge fund strategies and traditional assets must be reassessed in order to

introduce a more relevant SAA with hedge funds.

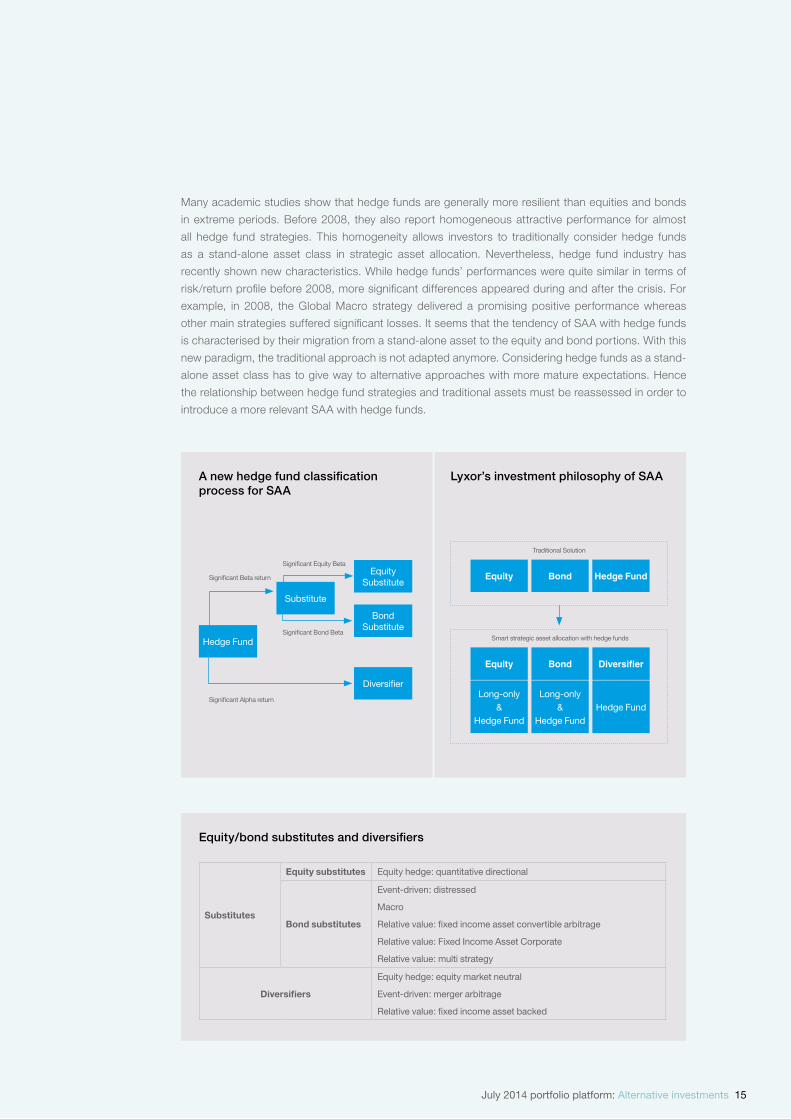

A new hedge fund classification process for SAA

Lyxor’s investment philosophy of SAA

Hedge Fund

Diversifier

BondSubstitute

Substitute

EquitySubstitute

Equity

Equity

Long-only&

Hedge Fund

Long-only&

Hedge FundHedge Fund

Bond

Bond

Hedge Fund

Diversifier

Significant Beta return

Significant Equity Beta

Significant Bond Beta

Significant Alpha return

Traditional Solution

Smart strategic asset allocation with hedge funds

Equity/bond substitutes and diversifiers

Substitutes

Equity substitutes Equity hedge: quantitative directional

Bond substitutes

Event-driven: distressed

Macro

Relative value: fixed income asset convertible arbitrage

Relative value: Fixed Income Asset Corporate

Relative value: multi strategy

Diversifiers

Equity hedge: equity market neutral

Event-driven: merger arbitrage

Relative value: fixed income asset backed

16 July 2014 portfolio platform: Alternative investments

Considering this new paradigm, hedge fund strategies may be grouped by their exposure to common

risk factors and their capacity of generating uncorrelated absolute return. The breakdown of hedge

fund returns into beta return and alpha return shows some hedge funds have more significant beta

return than alpha return and vice-versa. Lyxor therefore suggests a new hedge fund classification by

categorising some hedge funds as equity/bond substitutes (more significant beta return) or diversifiers

(more significant alpha return). Substitutes aim to replace equities and bonds in order to improve

portfolios’ risk/return profiles whereas diversifiers generate absolute performance and diversification.

This classification process with two families would allow investors to better diversify their portfolio risk

and generate alpha return in a granular hedge fund world. Thus, Lyxor introduces a smart strategic

asset allocation with hedge funds by integrating this new classification process.

Much research using hedge fund data from before 2008 uses a simple Markowitz mean-variance

framework to study the problem of allocating hedge funds in SAA. Nevertheless, due to the non-normal

distribution (asymmetric and/or fat-tailed) of hedge fund returns, a simple Markowitz mean-variance

framework will likely lead to an inefficient portfolio composition and also underestimate tail risk. One

solution consists in getting rid of the non normal distribution of hedge funds by considering a Markowitz

mean-variance framework with regime switching. Lyxor recommends the following allocation strategy

with hedge funds. In extreme market regimes, investors should replace a part of their long-only equities

with equity substitutes to improve more efficiently the risk/return profile of their portfolio. In normal

market regimes, investors should give priority to different families of hedge funds according to their

portfolio target volatility. If they aim for low, medium and high volatility, equity substitutes, diversifiers

and bond substitutes are respectively preferable.

Lyxor shows that the traditional approach is no longer adapted, as hedge funds cannot be considered

as a single asset class. It emphasises the necessity in SAA to analyse hedge funds by their styles to

better allocate into them. This approach is the unique way to help investors improve more efficiently

the risk/return profile in SAA and understand perfectly the real source of this improvement in terms of

risk diversification and absolute performance.

Allocation Strategy – Extreme Regime Allocation Strategy – Normal Regime

80 80

60 60

40 40

Low risk appetite Low risk appetite

Allo

catio

n (%

)

Allo

catio

n (%

)

Medium risk appetite Medium risk appetiteHigh risk appetite High risk appetite

20 20

0 0

EquityEquity SubstituteBondBond SubstituteDiversifier

EquityEquity SubstituteBondBond SubstituteDiversifier

July 2014 portfolio platform: Alternative investments 17

T H E P O W E R T O P E R F O R M I N A N Y M A R K E T

THE POWER TO PERFORM IN ANY MARKET

THE EXPERT IN ALL MODERN INVESTMENT TECHNIQUES

Lyxor Asset Management, a subsidiary of Societe Generale Group, was founded in 1998 and counts 600 professionals worldwide managing US$ 115.2 Bn * of assets.

Lyxor customizes active investment solutions as the expert in all modern investment techniques: ETFs & Indexing, Alternative, Structured, Active Quantitative & Specialized investments.

Supported by strong research teams and leading innovation capabilities, Lyxor’s investment specialists strive to optimize performance across all asset classes.

For more information visit www.lyxor.com

ETFs & INDEXING • ALTERNATIVE INVESTMENTS • STRUCTURED INVESTMENTS • ACTIVE QUANTITATIVE & SPECIALIZED INVESTMENTS

THIS COMMUNICATION IS FOR PROFESSIONAL CLIENTS AND SOPHISTICATED RETAIL CLIENTS IN THE UK. .* US$ 115.2 Bn, equivalent to EUR 83.5 bn – as of 31 March 2014

Not all advisory services and products are available in all jurisdictions due to regulatory restrictions. The advisory services and products described herein are suitable only for certain qualified and professional investors in accordance with applicable laws in the relevant jurisdiction. Interested Investors should first consult with their professional advisors in order to make an independent determination regarding such advisory services or products. This should not be construed as an offer to buy or a solicitation to sell any security or financial instrument, as such an offer or solicitation may only be done pursuant to an offering document. An investment in any security or financial instrument involves a high degree of risk, including potential loss of capital. Lyxor Asset Management (Lyxor AM), Simplified Private Limited Company having its registered office at Tours Société Générale, 17 cours Valmy, 92800 Puteaux (France), 418 862 215 RCS Nanterre, is authorized and regulated by the Autorité des marchés financiers (AMF). Lyxor AM is represented in the UK by Lyxor Asset Management UK LLP, which is authorized by the Financial Conduct Authority in the UK (FCA Registration Number 435658); and in the United States by Lyxor Asset Management Inc., which is a U.S. registered investment advisor.

C53629 LyxorCorporateTeam UKtemplate 297x210.indd 1 22/05/2014 12:48

18 July 2014 portfolio platform: Alternative investments

Editor: Chris Panteli

Deputy editor: Sebastian Cheek

Contributing editor: Pádraig Floyd

Publisher:

portfolio Verlag

Suite 1220 - 12th floor

Broadgate Tower

20 Primrose Street

London EC2A 2EW

This publication is a supplement to portfolio institutional and sponsored by:

Lyxor Asset Management

Contact:

Sidra Sammi

Phone: +44 (0)20 7596 2875

E-mail: [email protected]

Pictures:

Richie Hopson

Printed in Great Britain by Buxton Press

© Copyright portfolio Verlag. All rights reserved. No part of this publication may be reproduced in any

form without prior permission of the publisher. Although the publishers have made every effort to ensure

the accuracy of the information contained in this publication, neither portfolio Verlag nor any contributing

author can accept any legal responsibility whatsoever for any consequences that may arise from errors or

omissions contained in the publication.

ISSN: 2052-0409

Are you interested in participating in future roundtable discussions?

Investors and investment consultants are invited to share their opinion and can be

offered a complimentary place in future roundtable events. Asset managers interested

in joining the panel can secure one of the limited sponsorship packages.

Contact us to find out more:

Sidra Sammi

Phone: +44 (0)207 596 2875

E-mail: [email protected]

The next portfolio platform will be held on Friday 8 August

Commodities

Topics for upcoming roundtable discussions:

Exchange traded funds

Diversified growth funds

Emerging markets