alternative financing for renewable energy projects...

TRANSCRIPT

Alternative Financing for Renewable Energy

Projects: Evaluating Options, Structuring

the Deal

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 1.

THURSDAY, MAY 31, 2018

Presenting a live 90-minute webinar with interactive Q&A

Paul N. Belval, Partner, Day Pitney, Hartford, Conn.

Caileen Kateri (Kat) Gamache, Senior Counsel, Norton Rose Fulbright, Washington, D.C.

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-755-4350 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can address

the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 2.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Alternative Financing for

Renewable Energy

Projects

May 31, 2018

Presenters:

Paul N. Belval Caileen Kateri Gamache

Agenda

I. Financeability of Renewable Energy ProjectsA. Regulatory Issues & Options

B. Tax Considerations

C. Offtake & Revenue AgreementsA. Market Offtake Options

B. Traditional PPAs

C. Alternative Revenue Contracts

II. Financing StructuresA. Traditional Project Finance

B. Balance Sheet Financing

C. Tax Equity Financing

D. Partnership Flip Structure

E. Leveraged Leasing

F. Back Leverage

G. Tax-Exempt Financing

H. 144A Bond Offerings

III. Questions & Discussion

Financeability of Renewable

Energy Projects

Financeability – Regulatory &

Tax Considerations

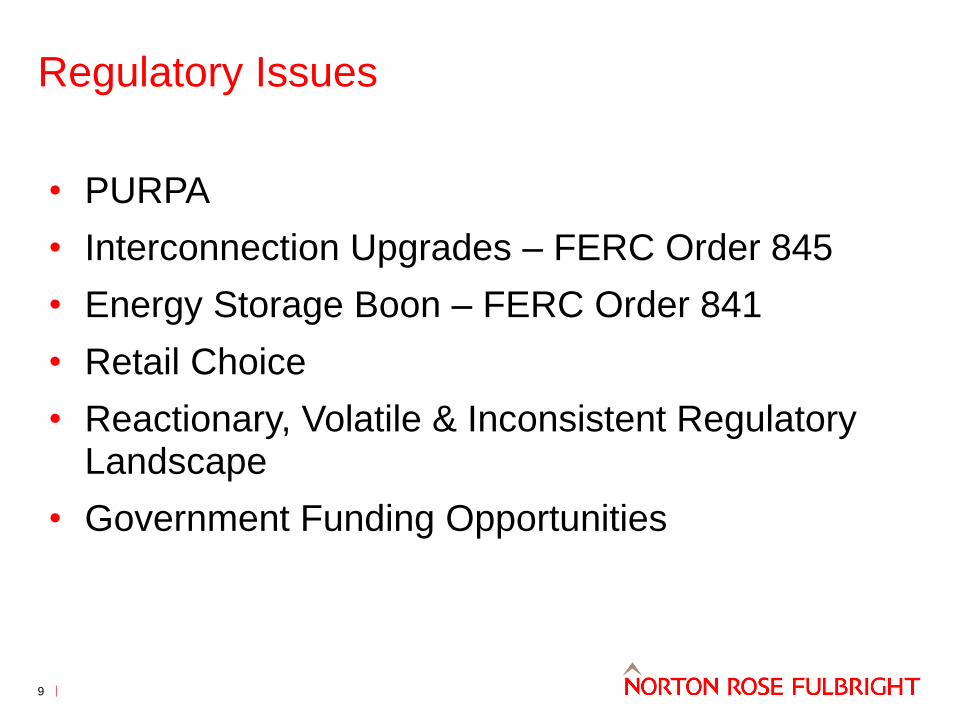

Regulatory Issues

9

• PURPA

• Interconnection Upgrades – FERC Order 845

• Energy Storage Boon – FERC Order 841

• Retail Choice

• Reactionary, Volatile & Inconsistent Regulatory Landscape

• Government Funding Opportunities

Regulatory Mitigants

10

• Declaratory Relief

• Diversify

• Portfolios

• Structure financing transactions consistent with FERC’s passive investment precedent

• Negotiate contractual protections

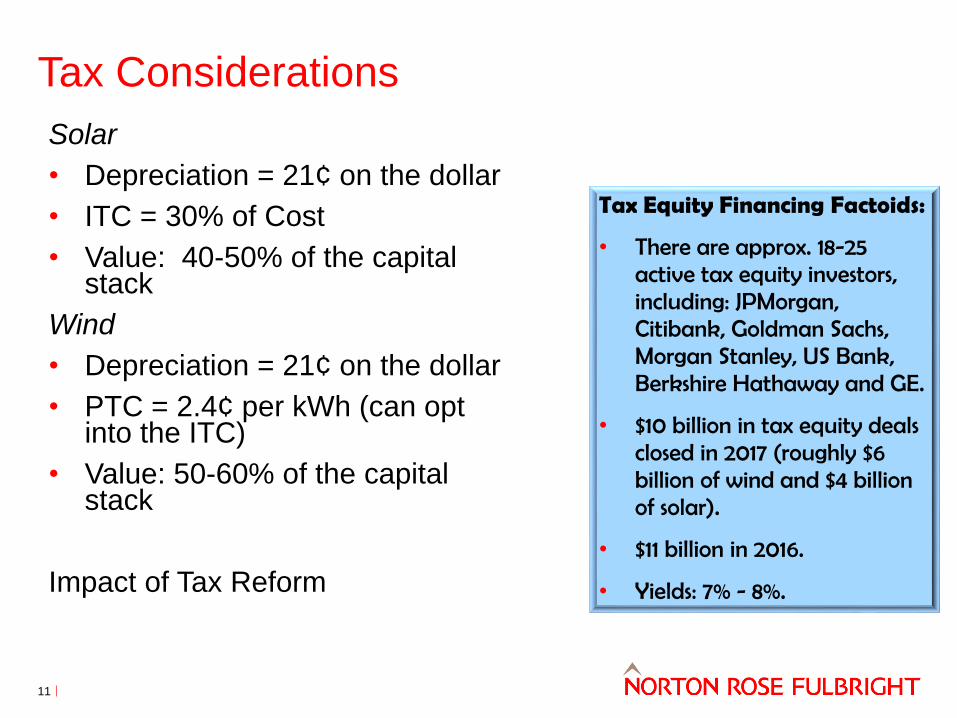

Tax Considerations

11

Solar

• Depreciation = 21¢ on the dollar

• ITC = 30% of Cost

• Value: 40-50% of the capital stack

Wind

• Depreciation = 21¢ on the dollar

• PTC = 2.4¢ per kWh (can opt into the ITC)

• Value: 50-60% of the capital stack

Impact of Tax Reform

Tax Equity Financing Factoids:

• There are approx. 18-25 active tax equity investors, including: JPMorgan, Citibank, Goldman Sachs, Morgan Stanley, US Bank, Berkshire Hathaway and GE.

• $10 billion in tax equity deals closed in 2017 (roughly $6 billion of wind and $4 billion of solar).

• $11 billion in 2016.

• Yields: 7% - 8%.

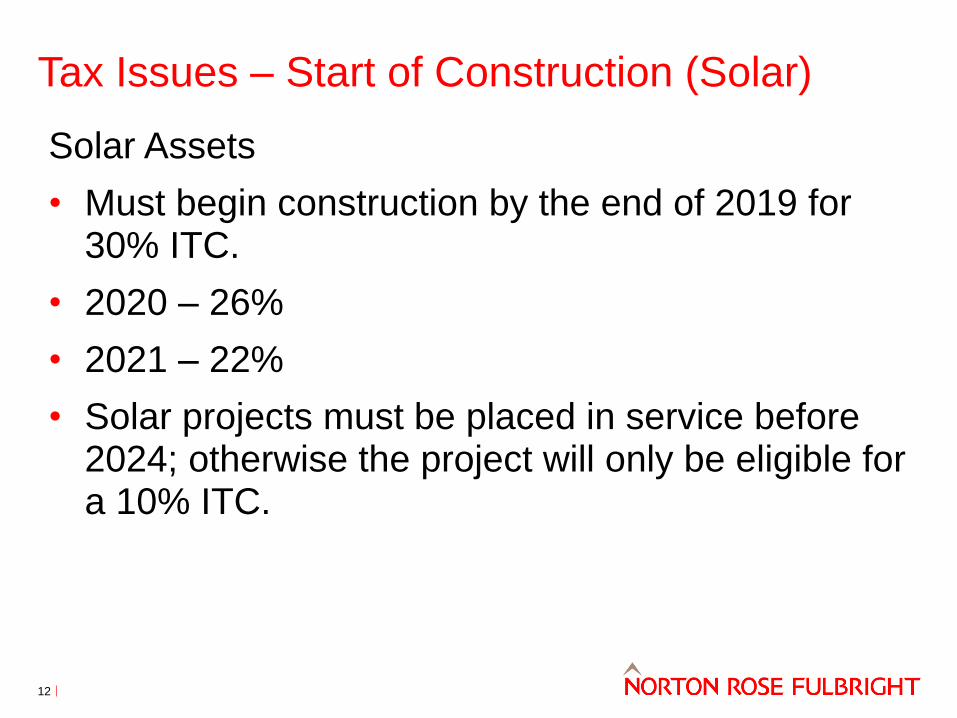

Tax Issues – Start of Construction (Solar)

12

Solar Assets

• Must begin construction by the end of 2019 for 30% ITC.

• 2020 – 26%

• 2021 – 22%

• Solar projects must be placed in service before 2024; otherwise the project will only be eligible for a 10% ITC.

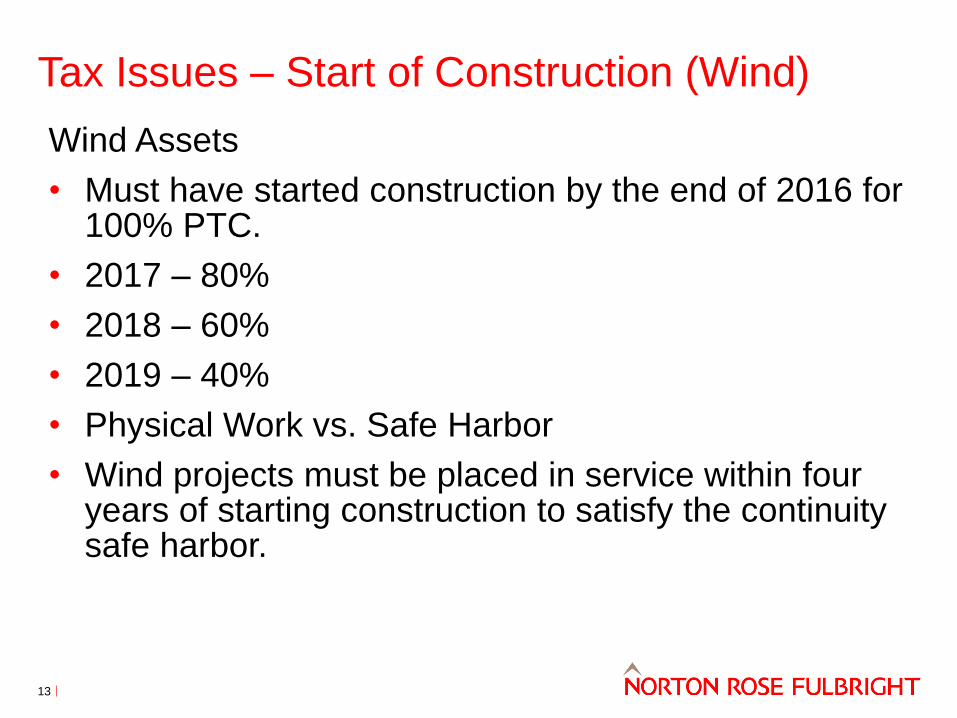

Tax Issues – Start of Construction (Wind)

13

Wind Assets

• Must have started construction by the end of 2016 for 100% PTC.

• 2017 – 80%

• 2018 – 60%

• 2019 – 40%

• Physical Work vs. Safe Harbor

• Wind projects must be placed in service within four years of starting construction to satisfy the continuity safe harbor.

Financeability – Offtake &

Revenue Contracts

Revenue & Offtake Opportunities

15

• Merchant (good luck…)

• Capacity, Resource Adequacy, Ancillary Services

• Revenue Stacking

• Renewable Energy Attributes

• Net Metering; Green Tariffs

• Offtake Agreements

• Traditional PPAs

• Trending: Alternative Offtake Structures‒ Bank Hedges

‒ Virtual PPAs (aka Corporate PPAs)

‒ Proxy Revenue Swaps

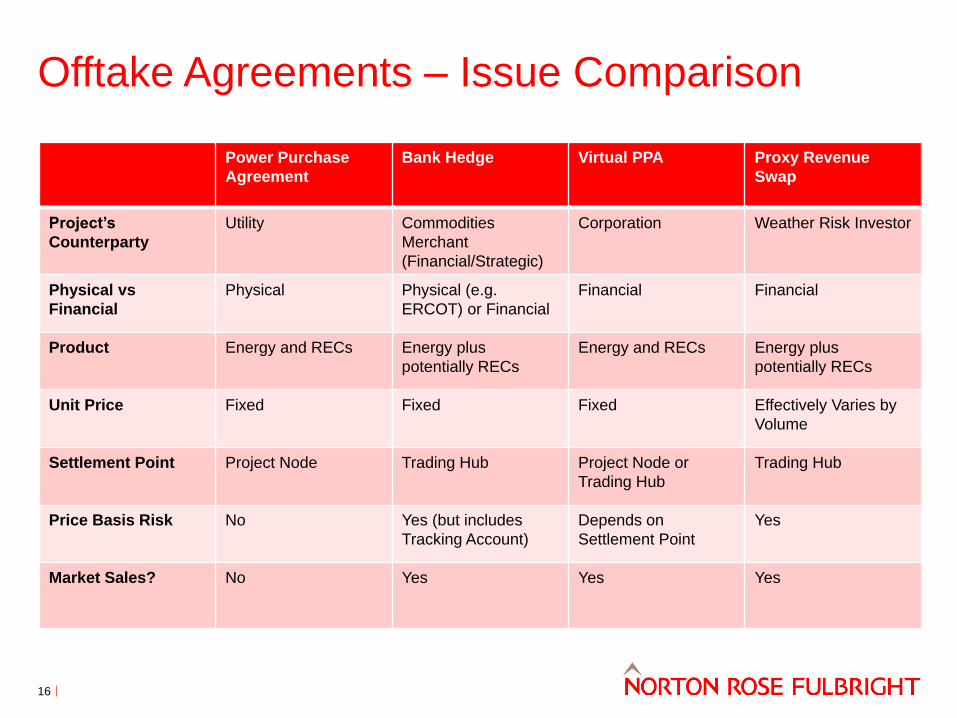

Offtake Agreements – Issue Comparison

16

Power Purchase

Agreement

Bank Hedge Virtual PPA Proxy Revenue

Swap

Project’s

Counterparty

Utility Commodities

Merchant

(Financial/Strategic)

Corporation Weather Risk Investor

Physical vs

Financial

Physical Physical (e.g.

ERCOT) or Financial

Financial Financial

Product Energy and RECs Energy plus

potentially RECs

Energy and RECs Energy plus

potentially RECs

Unit Price Fixed Fixed Fixed Effectively Varies by

Volume

Settlement Point Project Node Trading Hub Project Node or

Trading Hub

Trading Hub

Price Basis Risk No Yes (but includes

Tracking Account)

Depends on

Settlement Point

Yes

Market Sales? No Yes Yes Yes

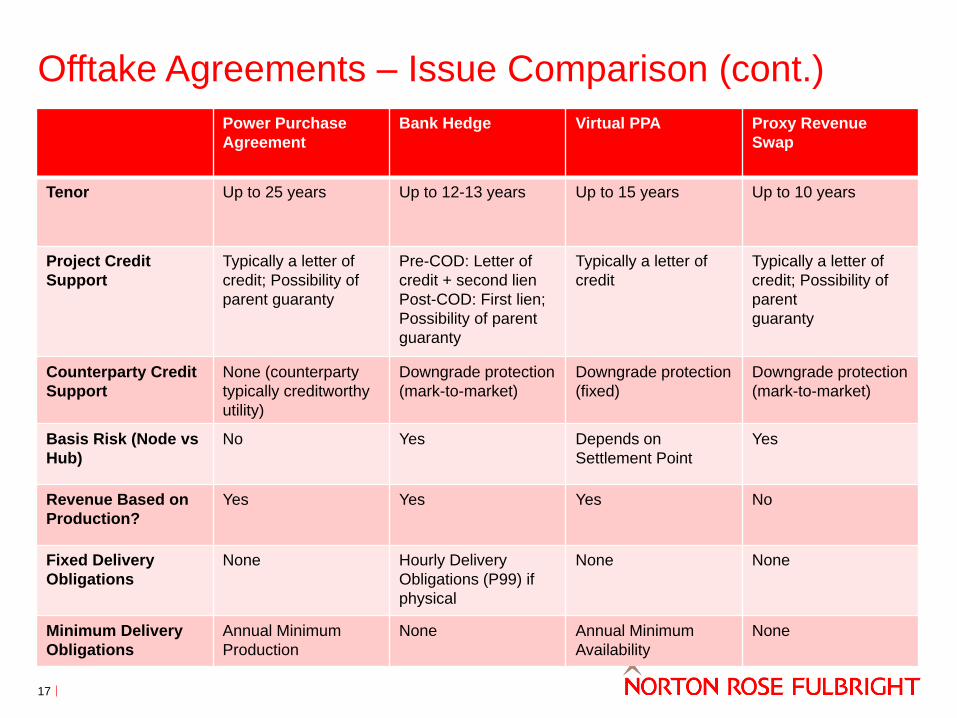

Offtake Agreements – Issue Comparison (cont.)

17

Power Purchase

Agreement

Bank Hedge Virtual PPA Proxy Revenue

Swap

Tenor Up to 25 years Up to 12-13 years Up to 15 years Up to 10 years

Project Credit

Support

Typically a letter of

credit; Possibility of

parent guaranty

Pre-COD: Letter of

credit + second lien

Post-COD: First lien;

Possibility of parent

guaranty

Typically a letter of

credit

Typically a letter of

credit; Possibility of

parent

guaranty

Counterparty Credit

Support

None (counterparty

typically creditworthy

utility)

Downgrade protection

(mark-to-market)

Downgrade protection

(fixed)

Downgrade protection

(mark-to-market)

Basis Risk (Node vs

Hub)

No Yes Depends on

Settlement Point

Yes

Revenue Based on

Production?

Yes Yes Yes No

Fixed Delivery

Obligations

None Hourly Delivery

Obligations (P99) if

physical

None None

Minimum Delivery

Obligations

Annual Minimum

Production

None Annual Minimum

Availability

None

Alternative Offtake - Bank Hedges

18

• A fixed volume price swap with a commodities merchant (either financial or strategic)

• Project receives fixed price

• Hedge provider receives market price

• Volumes typically set based

on P99 production

• Tracking Account

Wind

Project

Hedge

Provider

Market

Merchant

Revenue at

Node

Settlement Amount

Bank Hedges -- Financing Interfaces

Sponsors of U.S. renewables projectsface a complex set of interface pointsamong their contract counterpartieswhen they must rely on third partydebt for construction and operations,they cannot use the PTC or ITCefficiently, and (given the lack ofavailable power purchaseagreements) they seek to use bankhedges to fix project revenues.

For example:

• Construction lenders wantassurance that their loans will berepaid in full at project completion,while tax equity seeks an ability tore-size their investment based onas-built conditions and changes intax law.

• Back-leverage lenders wantassurance that distributable cashwill be available to service debt,while tax equity investors seek theright to divert sponsor cash tocover indemnity claims.

• Hedge providers seek to have theability to exercise remedies ontheir lien-based collateral, whiletax equity investors seek anopportunity to protect theirinvestment and avoid recapture ofpreviously-claimed tax credits.

.

19

Construction Debt Tax Equity Back-Leverage Debt

Tax Equity • Tax Equity Funding

Conditions

• Tax Equity Pre-

Funding Sizing

Adjustments

Back-Leverage Debt • Back-Leverage

Funding Conditions

• Back-Leverage

Sizing Adjustments

• Tax Equity Cash

Sweeps

• Tax Equity Post-

Funding Sizing

Adjustments

• Equity Transfer

Restrictions

Energy Hedge • 1st lien/2nd Lien

Collateral Structure

and Intercreditor

Arrangements

• Forbearance

Arrangements

• Mark-to-market

collateral posting

requirements

• Mark-to-market

collateral posting

requirements

Bank Hedges: Strategic Considerations for

Sponsors & Lenders

20

• When to execute relative to financial close?

• Should your hedge provider and other financing parties be affiliates?

• How many potential hedge providers should you negotiate with?

• Exclusivity?

• Hedge provider credit support?

• Critical for financing

Alternative Offtake – Virtual / Corporate PPAs

21

• Variety of forms‒ On-site, contract for differences, back-to-back

• Payment for Physical PPA: fixed price to Seller

• Payment for VPPA:1. Seller gets fixed price; Buyer gets floating price, either at node

or hub.

2. Floating Price: market price at time of delivery (locational marginal price or LMP).

3. Netting: If fixed price payments exceed floating price payments, Buyer pays Seller the difference. If fixed price payments are less than floating price payments, Seller pays Buyer the difference.

Corporate PPAs: Strategic Considerations for

Sponsors & Lenders

22

• Importance of the Settlement Point • What basis risk is palatable?

• Market disruption events

• Negative Price Risk• Should there be a floor price?

• What is the impact on PTC?

• Credit Support – Is the offtaker creditworthy? Should there be downgrade options?

Corporate PPAs: Strategic Considerations for

Sponsors & Lenders (cont.)

23

• Who owns the Environmental Attributes?

• Corporate offtakers often do not have RPS requirements, yet want to retire RECs).

• How about future attributes?

• Apportionment of capacity rights and participation costs and penalties?

• Risk of curtailment by market operator

• Impact on minimum performance requirement; payments for energy

• Development risks – delay damages and termination

• Minimum Performance requirement

• Availability vs. production & performance excuses

Examples of Corporate Renewable PPAs

24 Source: World Business Council for Sustainable Development, Corporate

Renewable Power Purchase Agreements (2016)

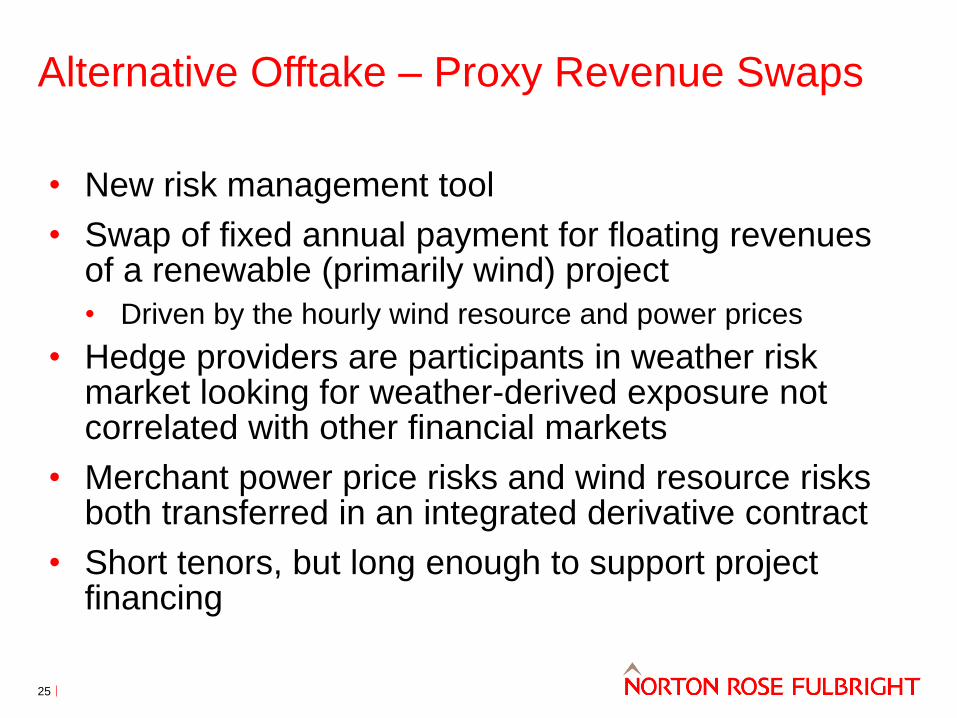

Alternative Offtake – Proxy Revenue Swaps

25

• New risk management tool

• Swap of fixed annual payment for floating revenues of a renewable (primarily wind) project

• Driven by the hourly wind resource and power prices

• Hedge providers are participants in weather risk market looking for weather-derived exposure not correlated with other financial markets

• Merchant power price risks and wind resource risks both transferred in an integrated derivative contract

• Short tenors, but long enough to support project financing

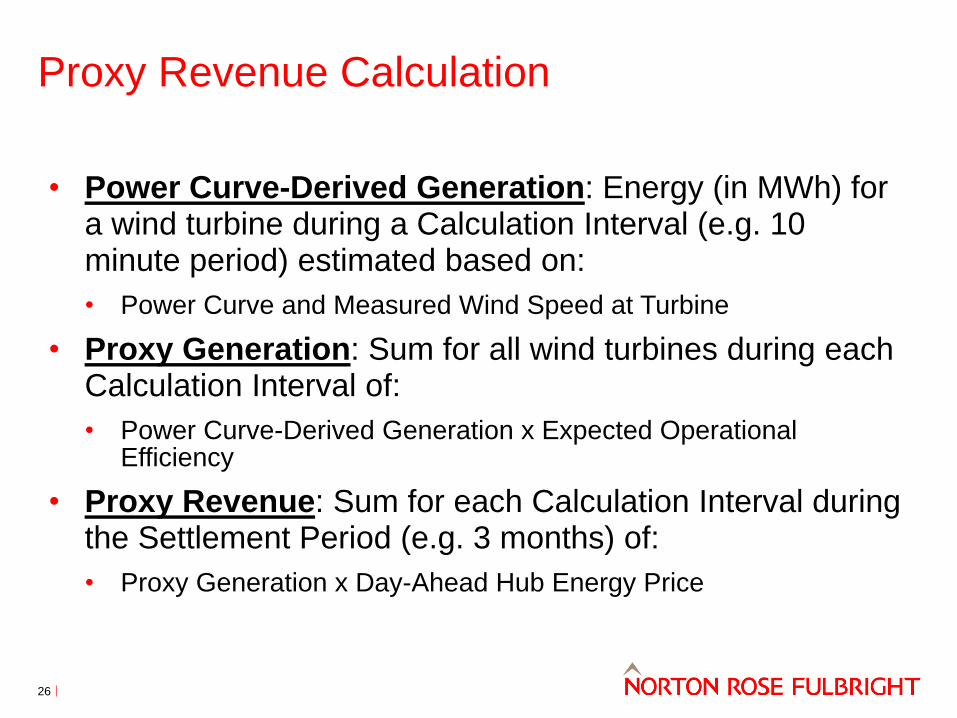

Proxy Revenue Calculation

26

• Power Curve-Derived Generation: Energy (in MWh) for a wind turbine during a Calculation Interval (e.g. 10 minute period) estimated based on:

• Power Curve and Measured Wind Speed at Turbine

• Proxy Generation: Sum for all wind turbines during each Calculation Interval of:

• Power Curve-Derived Generation x Expected Operational Efficiency

• Proxy Revenue: Sum for each Calculation Interval during the Settlement Period (e.g. 3 months) of:

• Proxy Generation x Day-Ahead Hub Energy Price

Two-Way Settlement

27

Wind

Project

Hedge

ProviderSettlement Amount

If Proxy Revenue >

Fixed Payment

High winds,

high prices, or a

combination during

settlement period

Wind

Project

Hedge

ProviderSettlement Amount

If Proxy Revenue <

Fixed Payment

Low winds,

low prices, or a

combination during

settlement period

Proxy Revenue Swap: Strategic

Considerations for Sponsors & Lenders

28

• Additional Fees

• Upfront Structuring Fee & Annual Fees to Hedge Provider

• Service Fees for Calculation Agent and Reporting Services

• Accurate Data Collection Critical

• Provisions for installation, operation and maintenance of anemometers, permanent met towers

• Wake Impacts of Neighboring Projects & Other Non-Weather Interferences

• As-Built Conditions – Consistent with Assumptions?

• Credit Support, Delay Risks, Dodd-Frank – Similar to Bank Hedge

Proxy Revenue Swaps Signed in 2016-17

29

Project Market Sponsor Lender Tax Equity Hedge

Provider

Back-to-

Back Price

Hedge

Provider

Calculation

Agent

Bloom

(KS)

SPP Capital

Power Corp.

N/A Goldman

Sachs

Allianz Risk

Transfer /

Nephila

Capital

Microsoft

Corporation

REsurety

Old Settler

(TX)

ERCOT Apex Clean

Energy

Deutsche

Bank

JPMorgan

(lead)

Allianz Risk

Transfer /

Nephila

Capital

Confidential REsurety

Confidential

(OK)

SPP Confidential N/A N/A Allianz Risk

Transfer /

Nephila

Capital

Confidential REsurety

Upstream

(NE)

SPP Invenergy Santander N/A Allianz Risk

Transfer /

Nephila

Capital

Confidential REsurety

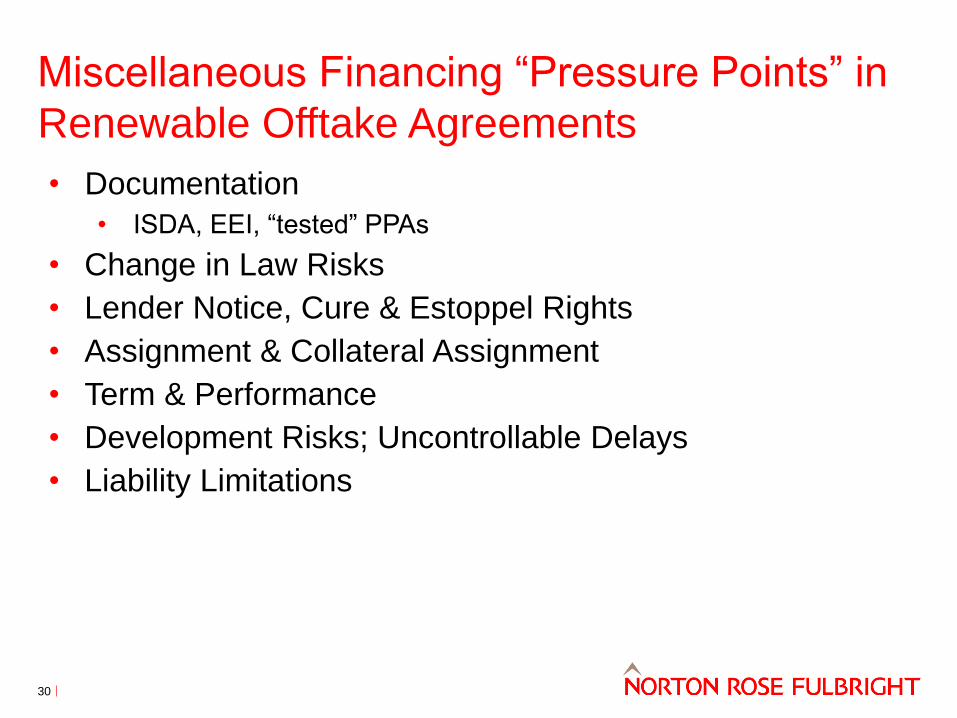

Miscellaneous Financing “Pressure Points” in

Renewable Offtake Agreements

30

• Documentation

• ISDA, EEI, “tested” PPAs

• Change in Law Risks

• Lender Notice, Cure & Estoppel Rights

• Assignment & Collateral Assignment

• Term & Performance

• Development Risks; Uncontrollable Delays

• Liability Limitations

Disclaimer

Norton Rose Fulbright US LLP, Norton Rose Fulbright LLP, Norton Rose Fulbright Australia, Norton Rose Fulbright Canada LLP and Norton Rose Fulbright South Africa Inc are separate legal entities and all of them are members of Norton Rose Fulbright Verein, a Swiss verein. Norton Rose Fulbright Verein helps coordinate the activities of the members but does not itself provide legal services to clients.

References to ‘Norton Rose Fulbright’, ‘the law firm’ and ‘legal practice’ are to one or more of the Norton Rose Fulbright members or to one of their respective affiliates (together ‘Norton Rose Fulbright entity/entities’). No individual who is a member, partner, shareholder, director, employee or consultant of, in or to any Norton Rose Fulbright entity (whether or not such individual is described as a ‘partner’) accepts or assumes responsibility, or has any liability, to any person in respect of this communication. Any reference to a partner or director is to a member, employee or consultant with equivalent standing and qualifications of the relevant Norton Rose Fulbright entity.

The purpose of this communication is to provide general information of a legal nature. It does not contain a full analysis of the law nor does it constitute an opinion of any Norton Rose Fulbright entity on the points of law discussed. You must take specific legal advice on any particular matter which concerns you. If you require any advice or further information, please speak to your usual contact at Norton Rose Fulbright.

31

Caileen Kateri Gamache (“Kat”) works

with project developers, investors,

utilities and financial marketers to find

solutions to complex energy regulatory

issues, develop ideas into operational

projects, draft and negotiate material

contracts and close deals.

Contact Information:

+1 202-974-5671

Thank you!

© 2018 Day Pitney LLP

Financing StructuresMay 31, 2018

33 | 5/31/2018

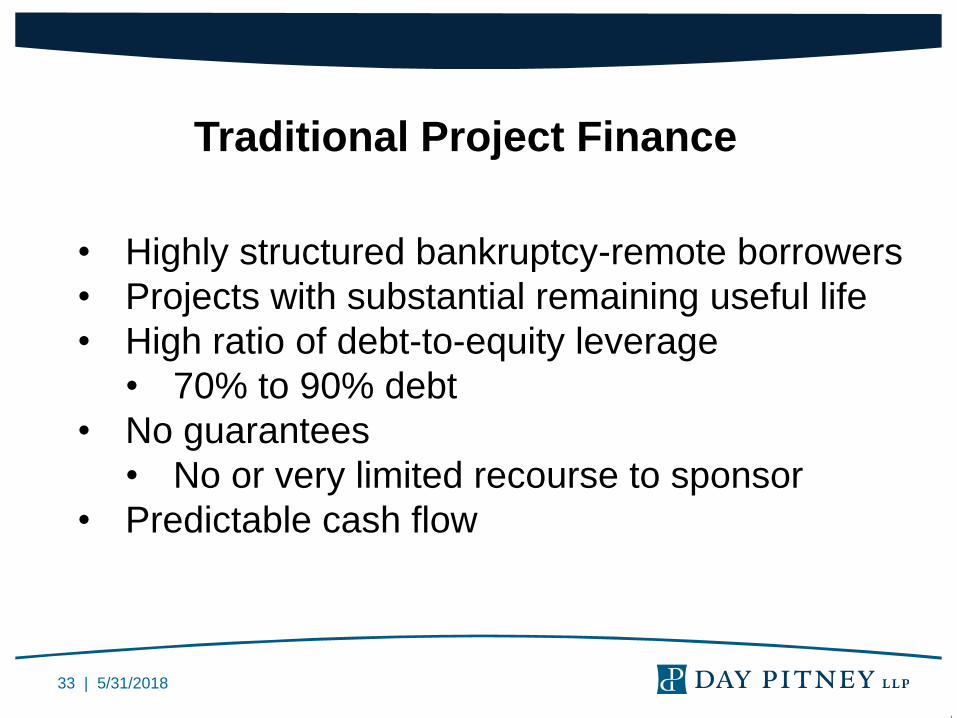

Traditional Project Finance

WHAT IS IT?

• Highly structured bankruptcy-remote borrowers

• Projects with substantial remaining useful life

• High ratio of debt-to-equity leverage

• 70% to 90% debt

• No guarantees

• No or very limited recourse to sponsor

• Predictable cash flow

34 | 5/31/2018

Elements of Traditional Project

Finance Model

• Lockbox for payments

• Waterfall payment structure

• Reserve accounts

• Lien on all project assets/all project equity

• Strong covenants (positive and negative)

• Strong lender consent rights

35 | 5/31/2018

Benefits of Traditional Project Finance

• High leverage

• Off-balance sheet financing

• Sponsor is often less than 50% of equity

• Preserve borrowing capacity

• Non-recourse debt not counted against

sponsor

• Risk limited to amount of equity invested

• Credit analysis based on off-taker

36 | 5/31/2018

Disadvantages of Traditional Project

Finance

•Increased lender risk (relative to return)

•Higher interest rates and fees

•High transaction costs (legal, consultants,

engineers, insurance)

•Intense lender oversight for borrower

•Expensive and time consuming due diligence

•Restrictive covenants

•Restrictions on distributions

37 | 5/31/2018

Balance Sheet Financing

• Large developers (often associated with utility)

have adequate capital to finance project

development with their own funds

• Will often move to project finance model post-

COD

• Lower cost of capital for project already in

operation

• More leverage in negotiations if already built

38 | 5/31/2018

Tax Equity Financing

• Benefit for equity investor is primarily through

tax credits and other incentives• PTC and ITC

• Accelerated Depreciation

• Pass-through entity (partnership or LLC)

• Needed to take advantage of tax benefit

• May include preferred return to attract investors

• Forbearance Agreement with lenders• Preserve tax credit during recapture period

39 | 5/31/2018

Advantages of Tax Equity Financing

• Creates another layer of financing

• Except for preferred return, share distributions

• Equity has greater risk tolerance than debt• Merchant risk - can tolerate some level of

uncontracted offtake sales

• Often lighter due diligence than debt, so time

saving

• Tax equity investors pay own expenses

(although cost factors into return)

• Use in portfolio transactions

40 | 5/31/2018

Disadvantages of Tax Equity Financing

• Must have, or find investor with, tax liability that

can use credit

• Still some control over project operation

• Transactions can be highly structured• Can impact ability to project finance later

• Disappearing tax credits• PTC – See above

• ITC - Declining to 10%/0% in 2022

• Base Erosion Anti-Abuse Tax • Foreign investors can generally take at least 80% of

credit through 2025

41 | 5/31/2018

Partnership Flip Structure

• Allocations of profit and loss between classes

of investors change over time• For ITC, flip after five-year recapture period

• For PTC, after end of credit availability• IRS safe harbor on percentages before and after flip

(99%/1% to 5%/95%)

• Can also flip based on returns

• Allows developer to retain residual value

• May result in Deficit Restoration Obligation if deficit at

time of liquidation of partnership

42 | 5/31/2018

Leveraged Leasing

• Sponsor sells project to a trust, then leases the

project back from the trust

• Sales proceeds finance project

• Equity investor is owner of trust and gets tax

benefits

• Trust issues notes or bonds to finance project

• Lease payments provide cash to repay

• Residual interest reverts to sponsor at expiration

of lease, before end of useful life

• Forbearance Agreement to protect ITC

43 | 5/31/2018

Back-Leverage

• Loan financing at Holdco/Sponsor level, not at

project company level

• May include limited recourse or limited sponsor

guarantee

• Secured by pledge of equity in project company

• Distributions into lockbox account

• Usually does not include project company-level

debt

• If so, sponsor level lender is structurally subordinated

• If not, negative pledge by project company with

respect to assets

44 | 5/31/2018

Back Leverage (cont.)

• More attractive to tax equity if no lien on project

• Avoids recapture issue

• Avoids need for project contract consents

• Reduced time and cost

• Useful in portfolio transactions

• Less secure than traditional project finance, so

higher cost of capital

• Still requires negotiation between debt and

equity regarding what happens post-default

45 | 5/31/2018

Tax-Exempt Financing

• Financing through a government entity that can

issue tax-exempt debt

• Typically an economic or industrial development

agency

• “Conduit” financing – project issues debt to

government agency, which then issues its bonds

secured by that debt

• Tax-exempt means lower cost of capital

• Restrictions on use of project under IRS rules

• Limitations under enabling legislation

46 | 5/31/2018

144A Bond Offerings

• Quasi-public offering of bonds to “qualified

institutional buyers” under Rule 144a

• Exempt from registration with SEC

• Underwritten by investment bank, which negotiates

documents before offering

• Offered on a “take it or leave it” basis

• Generally less bondholder oversight

• Need to know market well enough to know sorts of

covenants that will be expected