alternative entities

TRANSCRIPT

DECEMBER 9, 2014

ALTERNATIVE ENTITIES

Presented by: Tamara Kling

KNOWLEDGE SHARE

NAVIGATING NEW CHOICES FOR

BUSINESS FORMATIONS

OVERVIEW

•Why are there so many statutory business entities these days?

•Series LLC

•Social Enterprise Entities

– Benefit Corporation

– Low-Profit LLC

– Others

•Miscellaneous entities of interest

– Master LP

– “Shareholder friendly” publicly traded corporation act

2

WHY IS IT IMPORTANT TO KNOW ABOUT ALTERNATIVE ENTITIES?

•Choice of entity depends upon many factors

– Type of business

– Business purpose

– Taxation

– Who are the owners

– Who will manage

– Length of venture

– Many more

•Hard to find a business entity that meets all of the business owners’

and investors’ needs

•The more entities, the better the chance of finding a good fit

•But it can be hard to keep up with, and obtain expertise on the

features of all the new entities

3

WHY DO STATES AUTHORIZE DIFFERENT FORMS OF BUSINESS ENTITIES?

•Provide economic benefits for their citizens

•Benefit people who want to start new businesses

•Encourage people to invest

•Create employment

•Create revenue through filings and taxes

4

POLLING QUESTION NO. 1

Why are you with us today?

A. I have a lot of knowledge about the topic and wish to learn more

B. I know very little about the topic and am excited to learn about it

C. This is not my field of law exactly but I need the information to be

an informed legal professional.

A BRIEF HISTORY OF STATUTORY ENTITY CREATION IN AMERICA

•Until the mid to late 1800’s business conducted as individuals

•The problem?

– Unlimited liability for the business’ debts

– Only the rich (or those who didn’t mind losing what they owned) could

start businesses

– Hard to find investors to help expand

– Not too many risky ventures

•The solution

– The Corporation

• Business owners and investors had limited liability

• Corporation had own identity; liable for own debts

• More businesses were started, economy grew

6

A BRIEF HISTORY OF STATUTORY ENTITY CREATION IN AMERICA

•Corporation did not meet all business needs

•The problem?

– Double taxation

– Burdensome management rules

– Shareholder’s creditors could attach stock

•The solution

– The limited partnership

• Met various needs of business

– Limited liability for passive investors

– Single level of taxation

– Management flexibility

– Charging order

7

A BRIEF HISTORY OF STATUTORY ENTITY CREATION IN AMERICA

•Some other entities created to meet needs not met by corp/LP

– Statutory Close Corporation

• Met needs of business owners who want to manage and limit liability

– Professional Corporation

• Met needs of professionals who want limited liability and right to deduct

fringe benefits

– S Corporation

• Created by Congress

• Met needs of small businesses that wanted limited liability and single

taxation

A BRIEF HISTORY OF STATUTORY ENTITY CREATION IN AMERICA

•Many business owners wanted an entity that provided single taxation,

limited liability, management flexibility

•The problem? – It didn’t exist

•The solution – The limited liability company

• Option of single taxation

• Limited liability

• Owners can manage or not

• Charging order protection

• Management and financial flexibility

•The problem? – Some people preferred the partnership form but wanted limited liability

•The solution – LLPs and LLLPs

SOME OF THE “NEW” ALTERNATIVE ENTITIES

•Series LLCs

•Benefit Corporations

•L3C

•Unincorporated nonprofit associations

•Limited cooperative associations

10

SERIES LLC

SERIES LLC

•What is a Series LLC?

– A limited liability company

– Formed under the laws of a state that authorizes Series LLCs

– That consists of series that function like a separate LLC

•What is a series?

– Part of a Series LLC that can have its own: • Assets

• Liabilities

• Business purpose

• Members

• Managers

12

WHAT PROBLEM DOES SLLC SOLVE?

•Many corporations, LLCs and other entities own more than one business or property

•Debts and liabilities associated with any business or property may be satisfied out of assets associated with any other business or property

•Entity may place each business or property in a separate subsidiary to shield each from liabilities of others

•Can be very expensive

– Formation and other filing fees

– Annual report and other maintenance fees

•Series LLC laws provide that in a properly formed and maintained Series LLC, each business or property may be contained in a separate series and each separate series has its own assets and own liabilities

13

SAVINGS ON ORGANIZATIONAL COSTS – AN EXAMPLE

•ABC Oil & Gas LLC – a Texas LLC owns and operates 5 oil fields

•ABC wants to separate the liabilities of each oil field

•ABC can form 5 separate LLCs with each LLC owning 1 oil field

– Total org cost = $1,500 ($300 fee for filing certificate of formation)

•ABC can form 1 Series LLC, establish 5 series with each series owning

an oil field

– Total org cost = $300 fee for filing certificate of formation

SOME TERMINOLOGY YOU MAY SEE

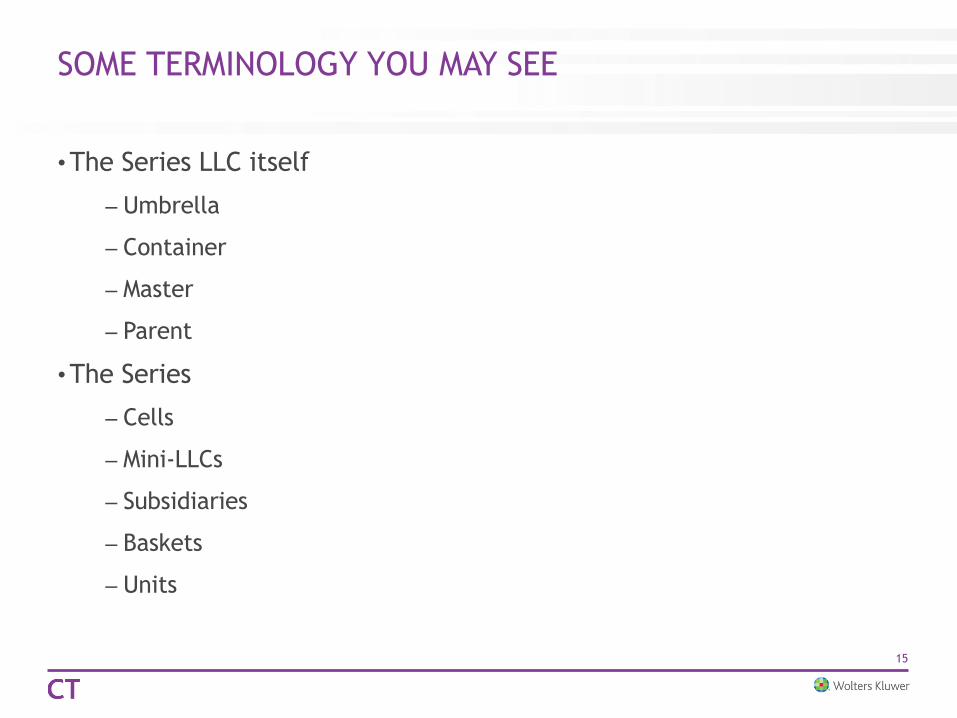

•The Series LLC itself

– Umbrella

– Container

– Master

– Parent

•The Series

– Cells

– Mini-LLCs

– Subsidiaries

– Baskets

– Units

15

SOME TERMINOLOGY YOU MAY SEE

•A separation of assets, liabilities, owners, and managers in a single

entity

– Concept sometimes referred to as “segregation”, “partitioning”, or

“compartmentalization”

•Be careful of some statutes that use the term “series” in a similar way

“series” is used in corporation statutes

– Authorizes creation of series of interests within classes which have

different rights to distributions, voting rights, etc.

– Do not have liability shield like in a SLLC law

SOME POSSIBLE USES FOR A SERIES LLC

•Owning real estate

– Owners of real estate are often advised to hold each piece in a separate entity

– Each piece of real estate can be placed in a separate series

– Each piece would, theoretically, be protected from liabilities of other piece with less expense than forming separate entities

•Ownership of personal property

– Business property – i.e. machinery, equipment

– Personal property like airplanes, boats

17

POLLING QUESTION NO. 2

Which applies to you?

A. I frequently use the SLLC in my practice

B. I rarely/never use the SLLC in my practice

SOME POSSIBLE USES FOR A SERIES LLC

•Separating business venture from business assets

– Example: client owns a bakery, property where bakery is located, ovens and other baking equipment. Form Series LLC and place bakery, property and equipment in separate series

•Ownership of multiple business ventures

– Example: client owns three bakeries. Form a Series LLC with each store assigned to a separate series

•Holding securities

– Series LLC concept originated from mutual fund/investment company concept where there is a master trust and several series, each with its own investment objective, portfolio of securities, managers, owners

– Example: Venture capitalist invests in four tech start-ups. Assigns shares to four different series

19

WHAT STATES AUTHORIZE SERIES LLCS?

•Alabama (Eff. 1/1/15)

•Delaware

•District of Columbia

• Illinois

• Iowa

•Kansas

•Missouri

•Montana

•Nevada

•Oklahoma

•Tennessee

•Texas

•Utah

THE DELAWARE SERIES LLC LAW

• Important Series LLC jurisdiction

•Many Series LLCs are Delaware Series LLCs

•As of end of 2013

– Approximately 7,500 total Series LLCs

– 1,100 formed in 2013

•Series concept adapted from DE Business Trust Act (now known as DE

Statutory Trust Act)

– Used in transactions involving mutual funds and highly financed asset

securitizations

• $ Savings for mutual fund – only Master trust has to file SEC registration rather

than each fund

21

FORMING A DELAWARE SERIES LLC

•File Certificate of Formation

•Contents

– Name

– Registered office and registered agent

– Notice of limitations on the liabilities of series

– Any other information members choose

•Filed certificate of formation is constructive notice of limitation of

liability of series

•Filing fee = $90

•One copy delivered to Division of Corporations

•Formation effective upon filing or delayed effective date up to 90 days

later

22

FORMING A DELAWARE SERIES LLC

•DE SLLC subject to same name, purpose, registered agent, annual

franchise tax provisions as regular DE LLC

•General LLC name requirements

– Contain “limited liability company”, “L.L.C.”, “LLC”

– Distinguishable on records from name of other corporation, partnership, LP,

ST, LLC

•SLLC may be formed to carry on any lawful business, purpose, activity -

profit or NP- except banking

•Required to file annual franchise report and pay annual fee

– Annual fee increased from $250 to $300 in 2014

•SLLC must appoint and maintain registered agent

•No statutory provisions re name, purpose, registered agent, franchise tax

applicable to each individual series

23

LLC AGREEMENT

•Main governing document of Series LLC

•Member agreement as to affairs of LLC and conduct of business

•Series are established within

•Rights of members of series provided for

•Management of series provided for

•Classes or groups established

•Termination of series provided for

24

CREATING A SERIES IN A DE SLLC

•Title 6, Sec. 18-215 Del Code

– LLC agreement may establish, or provide for establishment of 1 or more

series of members, managers, LLC interests or assets

– Having separate rights, powers or duties with respect to specified

property or obligations of LLC or profits and losses associated with

specified property or obligations

– May have a separate business purpose

– May have a separate investment objective

•Each series may sue or be sued, contract, hold title to assets, grant

liens and security interests and conduct business in its own name

– Not in original version of 18-215; added later to address confusion as to a

series’ powers

•Statute does not provide that a series is a separate entity under state

law

25

LIMITATION OF LIABILITY UNDER DE LAW

•Debts, liabilities, obligations incurred, contracted or existing with

respect to particular series are enforceable against assets of that

series and not assets of LLC or different series if:

– Notice of limitation of liability is set forth in certificate of formation

– LLC agreement created one or more series

– Separate and distinct records are maintained for each series

– Assets associated with each series are held in distinct and separate

records and accounted for in such records separately from assets of LLC

or other series

26

MEMBERS OF DE SERIES

•Have contractual freedom to decide their financial and management

rights and duties

•May agree to be personally liable for series’ debts

•Classes or groups of members with different rights, powers, duties

allowed

•Voting rights may be on per capita, number, financial interest or any

other basis or denied

27

MANAGEMENT OF DE SERIES

•Vested in members of series by DE LLC Act

•Decisions of members owning more than 50% interest control

– LLC agreement may provide otherwise

•LLC agreement may provide for managers of series

•Managers are elected, have duties and liabilities as provided in LLC

agreement

28

MORE ON MEMBERS AND MANAGERS

•Distributions may be made unless they will make series’ liabilities

exceed fair value of assets

•Event causing member or manager to cease association with one series

does not cause dissociation with any other series

29

TERMINATION OF DE SERIES

•Series may be terminated without causing dissolution of master Series LLC

• If master Series LLC is dissolved, each series must be terminated and its affairs wound up

• If LLC is dissolved, series must be terminated and wound up

•Series terminated upon first to occur of

– Time specified in LLC agreement

– Event specified in LLC agreement

– Consent of members owning more than two-thirds of interest in profits (unless otherwise provided)

– Time there are no members (and personal rep of last member does not consent to continue)

30

CHANGING FROM DE LLC TO DE SERIES LLC

•Amend certificate of formation to include notification of limitation of

liability of series

•File certificate of amendment

•Filing fee - $100

•Amend LLC agreement to establish series

– Procedure set forth in LLC agreement

31

THE SERIES LLC LAWS OF OTHER STATES

•Most SLLC laws based on Delaware law

•SLLC formed in same manner as regular LLC

– File articles of organization with SOS

– Financial rights, management provisions, etc. set forth in Op Ag

•SLLC subject to same compliance requirements as regular LLC

– Appoint registered agent, file annual report

•Series established in Op Ag

•Series added or dissolved by amending Op Ag

32

THE SERIES LLC LAWS OF OTHER STATES

•Debts, liabilities, obligations of series are enforceable against assets of

that series if:

– Notice of limitation of liability is set forth in articles of organization

– Operating agreement establishes 1 or more series having separate

liabilities

– Separate and distinct records are maintained for each series

– Assets associated with each series are held and accounted for separately

from assets of LLC or other series

THE SERIES LLC LAWS OF OTHER STATES – SOME INCONSISTENCIES

•A few states provide that a series may be considered a separate entity

– TX- specifically provides that series is not a separate entity

•Some (not all) states specifically provide that a series may sue and be

sued, hold assets, enter into contracts in its own name

•Some require public filing with SOS to establish series

•Some require name of each series to include name of master LLC and

be distinguishable from each other

ILLINOIS SERIES LLC LAW

•Some differences from Delaware law

– A few states adopted IL approach rather than DE

•Name of series

– Must contain entire name of LLC

– Must be distinguishable from name of other series

•File Certificate of Designation with SOS to form and terminate a series

– Contains series name

– Name of managers

– Whether member or manager managed

– Filed by LLC or any manager or designee

35

ILLINOIS SERIES LLC LAW

•May be treated as a separate entity to the extent set forth in the

articles of organization

•LLC and any of its series may

– Consolidate operations as a single taxpayer

– Work cooperatively

– Contract jointly

– Elect to be treated as a single business in order to qualify in IL or any

other state

QUALIFICATION OF SERIES LLC DOING BUSINESS IN FOREIGN STATES

•SLLC laws generally provide that a SLLC formed in another state that is

registering to do business as a foreign LLC must state in its certificate

of authority that it is a SLLC

•Some states require statement that the debts and liabilities of a series

may only be enforced against assets of that series

•Statutes do not provide whether individual series must (or may)

register

•Most LLC laws that do not authorize formation of SLLCs do not have

provisions dealing with qualification of foreign SLLC

TAXATION OF SERIES LLC

•Federal income taxation

– Proposed Reg. Sec. 30.7701-1, 75 Fed. Reg. 55,699 (2010)

– Treats each series as a separate entity

– Each series taxed pursuant to check-the-box rule

• Classified by default as partnership or disregarded entity

– Although only proposed, regulations are “substantial authority”

•State income taxation

– Only a few states have issued rulings or guidance

• CA – does not authorize domestic SLLCs but will treat each series of foreign

SLLC registering to do business as a separate LLC, subject to the minimum

annual franchise tax

• TX – will treat all series as a single taxable entity for margin tax purposes

• TN – held that a TN SLLC had to file separate franchise and excise tax returns

for each series

A WARNING TO BUSINESS OWNERS & INVESTORS

•Courts have not interpreted Series LLC laws yet

•State legislatures still need to clarify or change laws

•Federal and state agencies have not ruled on application of laws to Series LLCs

•Due to lack of court, legislative, and administrative guidance, there are uncertainties involved in doing business as a Series LLC

39

SOME OF THE UNANSWERED QUESTIONS

•Taxation

– Federal rules are not final

– Taxation other than income tax unclear

– Proposed regs do not address treatment of series for federal employment

taxes

– Proposed regs do not address ability of series to maintain an employee

benefit plan

– State taxation not clear

• Will states follow federal treatment?

• If one series establishes tax nexus will master Series LLC and other series be

subject to tax?

•Does the doctrine of veil piercing apply?

– If so, a creditor of one series might be able to reach the assets of another

series

– If it applies, under what circumstances would a court pierce a series’ veil?

40

SOME MORE UNANSWERED QUESTIONS

•Will a state that does not authorize formation of a Series LLC recognize

the internal liability shield granted by a foreign state’s law?

•Will determination of whether a Series LLC is doing business in a

foreign state differ from determination of regular LLC?

– What if only 1 series of multi-series LLC is doing business in state? Will

LLC have to register? Or will that be just one factor in determining

whether LLC as a whole is doing business?

•May an insolvent series file a bankruptcy petition separate and apart

from the master Series LLC?

– Issue – is a series a “person” under bankruptcy law

– If series can file, only its assets become part of bankruptcy estate

• If a series sells interests to the public is it subject to federal or state

securities laws?

•May a series make a filing under UCC article 9?

41

SERIES LLCS IN THE COURTS

•Alphonse v. Arch Bay Holdings, LLC, 2013 US App LEXIS 24665

•GxG Management, LLC v. Young Bros. & Co., Inc., 2007 U.D. LEXIS

43462

•Two decisions dealing with the capacity of a series to sue or be sued

•Neither court came to a conclusion

•But good illustrations of some of the issues to be decided

ALPHONSE V. ARCH BAY HOLDINGS, LLC

•DE SLLC (Master LLC) assigned a mortgage note to a series

•Default occurs

•Series files a petition to enforce the mortgage and forecloses on

mortgagor’s home

•Mortgagor files action against Master LLC under unfair debt collection

law

•District court dismisses action

– Held that claim against Master LLC was barred by the res judicata effect

of the series’ foreclosure action

– Held that Delaware law governed based on conflicts rule providing that

laws of formation state govern issues involving internal affairs

ALPHONSE V. ARCH BAY HOLDINGS, LLC

•Court of Appeals reverses

– For res judicata to bar claim, court must determine that there is a

sufficient identity of interest between the Master LLC and series

– This is a fact based determination that should not have been decided on a

motion to dismiss

– Delaware law did not necessarily govern as it is not clear if the issue of

whether an LLC or a series is liable to third parties is an issue of internal

or external affairs

– Remanded back to district court to determine if DE law governed and if

there was a sufficient identity of interest

GXG MANAGEMENT, LLC V. YOUNG BROS. & CO.

•DE Series LLC (Master LLC) bought a boat and formed a series to hold

title to and operate the boat

•Master LLC filed suit alleging poor workmanship and misrepresentation

•Master LLC moved to amend its complaint to add the series as a

plaintiff

•District court denied the motion, holding that the Master LLC could

maintain the action even though title was held by the series

GXG MANAGEMENT, LLC V. YOUNG BROS. & CO.

•District court later amended its findings of fact and conclusions of law

•Court clarified that it was not holding that the Master LLC could sue on

behalf of the series

•Court clarified that it was not holding that the Master LLC and series

were separate entities

•Court was holding that regardless of those issues the Master LLC had

suffered harm and could sue to recover for that harm

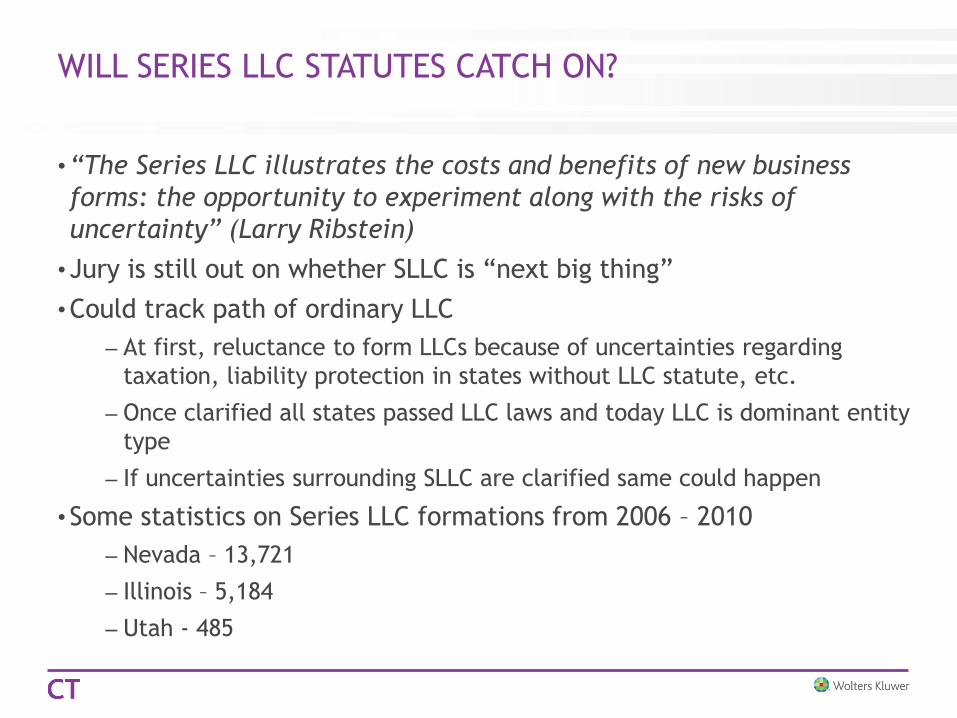

WILL SERIES LLC STATUTES CATCH ON?

•“The Series LLC illustrates the costs and benefits of new business

forms: the opportunity to experiment along with the risks of

uncertainty” (Larry Ribstein)

•Jury is still out on whether SLLC is “next big thing”

•Could track path of ordinary LLC

– At first, reluctance to form LLCs because of uncertainties regarding

taxation, liability protection in states without LLC statute, etc.

– Once clarified all states passed LLC laws and today LLC is dominant entity

type

– If uncertainties surrounding SLLC are clarified same could happen

•Some statistics on Series LLC formations from 2006 – 2010

– Nevada – 13,721

– Illinois – 5,184

– Utah - 485

WILL SERIES LLC STATUTES CATCH ON?

•Some indications it may not catch on

– NJ, CA, FL, MN recently enacted new LLC laws and did not include series

LLC provision

•Some indications it may catch on

– AL recently enacted a new LLC law and did include SLLC

– NCCUSL currently drafting uniform law which authorizes SLLCs

• when drafting RULLCA a few years ago NCCUSL criticized concept

– ABA Revised Prototype LLC Act includes SLLCs (original prototype did not)

•But will it catch on with legal professionals?

WHAT MOST CONCERNS YOU ABOUT USING THE SLLC?

•Uncertain how it will be treated in other states

•Uncertain about taxation

•Hasn’t been in use long enough, little case law

•All of the above

•None of the above, I frequently use the SLLC

SOCIAL ENTERPRISE ENTITIES

SOCIAL ENTERPRISE ENTITIES

•Hybrid statutory entities – part for-profit and part non-profit

•Blended mission – earn profits for owners; promote social good

• Incorporated social enterprise entities

– Benefit corporations

– Flexible purpose corporations

– Social purpose corporations

•Unincorporated social enterprise entities

– Low profit limited liability company

– Benefit LLC

•More than half the states have enacted laws authorizing one or more

social enterprise entities

INCORPORATED SOCIAL ENTERPRISE ENTITIES

•Some people start a business to earn a profit for themselves and their investors

– For profit corporation appropriate vehicle

•Some people start a business for charitable or other purpose designed to benefit society

– Nonprofit corporation appropriate vehicle

•Social entrepreneur

– Wants to earn a profit and benefit society

– For profit corporation not appropriate because directors are thought to have duty to maximize shareholder value and fear liability for decisions favoring interests of non-shareholders

– Nonprofit corporation not appropriate because it cannot distribute income to shareholders

WHAT IS A BENEFIT CORPORATION?

•An incorporated entity that can earn and distribute profits like a for

profit corporation and have a charitable or socially beneficial purpose

like a nonprofit corporation

•Addresses needs of social entrepreneur

•Estimated to be about 350 formed nationwide

– CA estimated to have most

•Should not be confused with “Certified B Corporation”

– Any entity type may apply for certification

• B Lab – nonprofit that provides third party certification; most commonly used

– Entity completes assessment survey, answering between 150 to 200

questions measuring its social and environmental impact

– If it scores high enough it can receive certification that it meets the

standard of social and environmental performance and advertise that fact

– Must amend its governing documents to state that it considers interests

other than financial interests of owners

THE BENEFIT CORPORATION STATUTES

•Maryland was first state to enact Benefit Corporation law (2010)

•About 20 states have done so since then

•Most statutes are based on a Model Benefit Corporation Act

– Drafted by B Lab

•Delaware enacted Public Benefit Corporation Law that differs in several ways from Model Act

•Some other states have enacted social enterprise corporation statutes that differ from Model Act

– Include CA, WA, MN

•Some states have enacted more than one type of social enterprise corporation statute

– CA, FL

FORMING A NEW BENEFIT CORPORATION (MODEL ACT)

•Benefit corporation is incorporated in same manner as a traditional for

profit corporation

•Subject to compliance requirements of general corporation law except

where statute expressly provides otherwise

– Must appoint and maintain a registered agent and office

• Company or person located in state authorized to receive and forward SOP and

official documents of corporation’s behalf

– Name must be distinguishable

– Must file documents to effect mergers, change of name, dissolution, etc.

•Articles of incorporation must state that it is a benefit corporation

BECOMING A BENEFIT CORPORATION (MODEL ACT)

•Existing corporation may become benefit corporation by amending its

articles of incorporation to add statement that it is a benefit

corporation

•Or existing corporation may merge into a benefit corporation

•Shareholders must approve amendment or merger by a two-thirds vote

– Supermajority intended to ensure broad shareholder support for decision

THIRD PARTY STANDARD (MODEL ACT)

•Some think it is the “signature” innovation of benefit corporation

•Generally defined as a standard for defining, reporting and assessing a benefit corporation’s social and environmental performance that is

– Comprehensive

– Independent

– Credible

– Transparent

•Standard must be developed by independent entities, not Benefit Corporation

•Factors considered in measuring performance, weighing of factors, identity of those developing and applying the standards must be available to the public

BENEFIT CORPORATION VS. TRADITIONAL FOR PROFIT CORPORATION

•Benefit corporation differs from a traditional for profit in three main

areas

– Corporate purposes

– Director duties

– Annual reporting

CORPORATE PURPOSES (MODEL ACT)

•Every benefit corporation has a purpose of creating a general public benefit

•General public benefit is defined by Model Act as a “material positive impact on society and the environment, taken as a whole, assessed against a third party standard, from the business and operations of the benefit corporation”

•May also have one or more specific public benefits

– Must be set forth in articles of incorporation

• Providing beneficial products or services to low-income or underserved individuals or communities

• Improving human health

• Promoting the arts, sciences or advancement of knowledge

•May have any other lawful purpose a traditional corporation can have

DIRECTORS’ DUTIES (MODEL ACT)

•Directors, in discharging their duties, must consider the effects of any

action or inaction upon

– Shareholders

– Employees

– Customers

– Community and societal factors

– Local and global environmental interests

– Corporation’s short and long term interests

– Corporation’s ability to accomplish its general and specific benefits

•Directors may consider other factors or the interests of other groups

that they consider appropriate

DIRECTORS’ DUTIES (MODEL ACT)

•Directors need not give priority to any particular factor or interest

unless articles of incorporation provide otherwise

•Directors are not personally liable for money damages for a failure by

benefit corporation to pursue or create general or specific public

benefit unless articles of incorporation provide otherwise

BENEFIT DIRECTOR (MODEL ACT)

•Required by most Model Act states to be designated by publicly traded

benefit corporation

•Permitted to be designated by private benefit corporation

•Some Model Act states require all benefit corporations to designate

benefit director

•Benefit director must prepare a statement that will be included in

annual report to shareholders

– Gives director’s opinion as to whether corporation has acted in

accordance with its public benefit purposes

– Gives director’s opinion as to whether directors and officers have

complied with their duties

BENEFIT ENFORCEMENT PROCEEDING (MODEL ACT)

•Model Act states provide that a person may not bring an action against

the benefit corporation or its directors and officers for a failure to

pursue or create a public benefit or for a violation of a duty, obligation

or standard of conduct except in a benefit enforcement proceeding

•Benefit enforcement proceeding may be brought by

– The corporation directly

– Derivatively by a shareholder holding a certain percentage of shares

– A director

– Other persons specified in articles of incorporation or bylaws

ANNUAL BENEFIT REPORT (MODEL ACT)

•Benefit corporation must prepare annual benefit report including:

– Description of ways corporation pursued a general public benefit and any

specific public benefit

– Extent to which benefits were created

– Circumstances hindering creation

– Process and rationale for selecting third party standard

– Assessment of its overall social and environmental performance measured

against a third party standard

– If there is a benefit director, his or her name and contact information and

a compliance statement

– Compensation paid to each director

– Statement of any connection between organization that established third

party standard and the benefit corporation

ANNUAL BENEFIT REPORT (MODEL ACT)

•Purpose of report

– Provide shareholders with information so they can evaluate benefit

corporation’s performance in creating a public benefit and judge whether

directors have discharged their responsibilities

– Reduce “green washing” – phenomenon where company falsely claims to

be environmentally and socially responsible

•Report must be sent to each shareholder within 120 days after end of

fiscal year or at time benefit corporation delivers any other annual

reports to shareholders

•Benefit corporation must post report on public portion of website

•Some states also require delivery to SOS

DELAWARE’S PUBLIC BENEFIT CORPORATION LAW

•Effective August 1, 2013

•Sec. 361 et seq of GCL

•Differs from Model Act’s benefit corporation in several respects

– At least 90% of existing DE corp’s shareholders must approve transition to PBC

status by amendment or merger

– Name must contain “Public Benefit Corporation”, “P.B.C.”, or “PBC”

– Required to identify specific public benefit in certificate of incorporation

– Directors required to balance certain interests

– Benefit report

• Only required every other year

• Does not have to be made public

• Third party standard for measuring performance not required

•158 formed in first year

DELAWARE PUBLIC BENEFIT CORPORATION

•Definition

– A for-profit corporation

– Intended to produce a public benefit

– And operate in a responsible and sustainable manner

•Public benefit defined as positive effect or reduction of negative effect

on 1 or more categories of persons, entities, communities or interests

– Includes effects of an artistic, charitable, cultural, economic, educational,

environmental, literary, medical, religious, scientific or technological

nature

DELAWARE PBC

•Subject to GCL except to extent PBC subchapter imposes different or

additional requirements

•New PBC formed by filing certificate of incorporation with SOS

– Must identify within its statement of business purposes one or more

specific public benefits to be promoted

– Must state within its heading that it is a PBC

– Required to appoint and maintain registered agent

•Corporation that is not a PBC may become PBC if

– 90% of outstanding shares of each class vote to amend the certificate of

incorporation to include provisions required of PBC

– 90% of outstanding shares vote to merge or consolidate with survivor being

a PBC

– Stockholder not voting for amendment, merger or consolidation is entitled

to appraisal rights

CERTIFICATE OF INCORPORATION OF DE PBC

•Minimum contents

– Corporation’s name

• Must include Benefit Corporation indicator

• Must be distinguishable upon the record from other entities on record

• May be reserved

– Registered office & agent

•Registered office may, but need not be a place of business

•Registered agent receives service of process and other official documents

•May be the corporation, individual, domestic or foreign corporation, LLC, LP or

ST

– Purposes

• One of which must be one or more specific benefit purposes

– Capital

• Authorized shares, par value or no par

– Incorporators

INCORPORATION FEES

• Incorporation fees consist of:

– Filing fee - based on authorized shares (minimum - $15, no maximum

limit)

– $25 receiving & indexing fee

– $5 fee for entering into database

– $20 municipality fee

– County assessment - $6 plus $9 per page

• Certification page counts as one page

DELAWARE PBC

•Stock certificates and notices of meetings must state that corporation is a PBC

•PBC may become traditional for-profit corporation upon amendment or merger or consolidation with approval of 2/3 of outstanding shares

•Board of directors shall manage PBC in a manner that balances

– Stockholders’ pecuniary interests

– Best interests of those materially affected by PBC’s conduct

– The public benefit identified in its certificate of incorporation

•Stockholders may bring derivative suit to enforce directors’ duty to balance interests

– Must own at least 2% of outstanding shares or if publicly traded, at least 2% or own shares with market value of at least $ 2 million

DELAWARE PBC – REPORTING OBLIGATION

•PBC must provide stockholders with a statement as to its promotion of

the public interests identified in certificate of incorporation and of the

best interests of those materially affected by its conduct

•Must be provided no less than biennially

•Certificate of incorporation or bylaws may require statement provided

more frequently

•Certificate of incorporation or bylaws may require that statement be

made available to public

•Certificate of incorporation or bylaws may require use of third party

standard

OTHER SOCIAL ENTERPRISE CORPORATE ENTITIES

• Flexible Purpose Corporation

– California Corporate Flexibility Act (2012)

– FPC formed under CA corporations code

– Differs from Benefit Corporation in some ways

• Must have “Flexible Purpose Corporation” or abbreviation in name

• Must identify particular special purpose in articles of incorporation

• Directors permitted (not required) to consider and weigh factors other than maximizing shareholder value

• Non-shareholder factors limited to those related to special purpose

• In addition to annual benefit report, “special purpose current reports” must be prepared after certain events (such as expenditures made having adverse impact, special purpose being satisfied or abandoned)

• Annual report to shareholders must include management discussion and analysis concerning special purposes

• Third party standard not required

– Senate Bill 1301, effective 1/1/2015

• Renames Corporate Flexibility Act as the Social Purpose Corporations Act

• Renames FPC as social purpose corporations (SPCs)

• Authorizes FPC to convert to SPC

• Requires directors to consider factors deemed relevant

OTHER SOCIAL ENTERPRISE CORPORATE ENTITIES

•Social Purpose Corporation

– In Washington Business Corporation Act (2012)

– Organized to carry out its business purposes in a manner intended to

promote positive short or long term effects of or minimize adverse effects

of its activities on any or all of its employees, suppliers or customers;

local, state or world communities; or environment

– May have specific purposes

– Articles of incorporation must include provision stating that its mission

may not be compatible with or may be contrary to maximizing

shareholder profit

– Directors may consider and weigh social purposes in discharging duties

– Articles of incorporation may require directors to consider and weigh

social purposes

– Annual social purpose report must be made available on website

OTHER SOCIAL ENTERPRISE CORPORATE ENTITIES

•Minnesota Public Benefit Corporation Act (eff. 1/1/15) – Corporation may be a “General Benefit Corporation” or a “Specific Benefit

Corporation”

– GBC – purpose is to pursue general benefit, which is a positive impact on

society, the environment and the well-being of present and future

generations; may state specific public benefit purposes in articles

– SBC – purpose is to pursue positive impact or reduction of negative impact on

specified categories of natural persons, entities, communities or interests,

other than shareholders; required to set forth specific public benefit purposes

in articles

– Name must contain words “General Benefit Corporation” or “Specific Benefit

Corporation” or abbreviation “GBC” or “SBC”

– Articles must state that it is either a GBC or SBC

– Directors required to consider effects of conduct on ability to pursue general

and or specific public benefit purposes

– Annual benefit report is filed with SOS • Annual benefit report of GBC must use third party standard to describe how corporation has

pursued general public benefit

LOW PROFIT LIMITED LIABILITY COMPANY (L3C)

•Hybrid of non profit organization and for profit organization

•Can earn modest profits but earning profits not main goal

•Main goal is to achieve a charitable or socially beneficial mission

•Formed under LLC act like any other LLC

– File articles of organization with SOS

– Registered agent and office required

– Members enter into operating agreement

•L3C designation must be indicated on articles of organization

•Name must include “Low Profit Limited Liability Company” or

abbreviation

L3C

•Vermont first state to authorize L3C (in 2008)

•Also authorized in IL, LA, MI, ME, RI, UT, WY

•NC enacted and later repealed

L3C – 3 REQUIREMENTS

• Its purpose is to significantly further the accomplishment of one or

more charitable or educational purposes within the meaning of Sec.

170(c)(2)(b) of IRC and it would not have been formed but for the

LLC’s relationship to the accomplishment of those purposes

• It does not have as a significant purpose the production of income or

the appreciation of property

• It does not have as a purpose the accomplishment of one or more

political or legislative purposes

L3C – WHAT PROBLEM DOES IT ADDRESS?

•Created to encourage charitable foundations to make more Program

Related Investments (PRI)

•PRI – one way foundation may meet IRS requirement to pay out at least

5% of its funds towards its mission

•Few foundations make PRIs

– Generally requires a Private Letter Ruling from IRS to determine whether

investment qualifies

• Expensive and time consuming process

– Difficult to locate entities involved in qualifying projects

•L3C intended to eliminate need for PLR by making statutory

requirement for being an L3C match IRS requirements

•Requirements that L3C status be set forth in articles of organization and

name intended to make it easier to find companies involved in

qualifying projects

L3C VS. BENEFIT CORPORATION - SOME MORE DIFFERENCES

•Same basic differences between corporation and LLC

– Management by board of directors vs. member/manager

– LLC’s financial flexibility re profits, losses, distributions

•L3C statutes do not impose disclosure obligations

•L3C statutes do not modify fiduciary duty standards

•L3C statutes do not rely upon third party standard to evaluate

achievements

L3C – IS IT THE NEXT BIG THING?

•Probably Not

•Commentators believe LLC is flexible enough entity that regular LLC

can accomplish same goals as L3C

•Critics question whether IRS will approve PRIs in L3C

•Critics believe foundations will still want legal opinion and IRS PLR

before making PRI in L3C

OTHER SOCIAL ENTERPRISE ENTITIES

•Benefit LLCs

– Maryland Benefit LLC Law (eff. 2011)

– Oregon Benefit Company Law (eff. 2014)

– LLC may be formed as or elect to be a Benefit LLC

– Articles of organization must identify it as such

– Has purpose of creating a general public benefit

– Articles of organization or operating agreement may identify specific

public benefit

– Persons managing must consider impact of decisions on members,

employees, customers, community, society, environment, etc.

– Must deliver annual benefit report to members

– Most useful for states whose LLC act does not state that LLC may be

formed for non profit purpose

POLLING QUESTION NO. 3

Have you formed, or have any of your clients expressed interest in

forming a social benefit entity?

A. Yes, but just a few

B. None

C. I do not think many clients are aware of such developments

MASTER LIMITED PARTNERSHIP

SOME OTHER ALTERNATIVE ENTITIES

•Master Limited Partnership (MLP)

– Not really new but good to know about

– First MLP formed in 1981 (Apache Corp)

– Early MLPs operated in a variety of industries (hotels, casinos, sports

teams, including the Boston Celtics)

– 1987 – tax law changed to restrict use of MLPs to natural resource based

activities

– Currently there are about 100 MLPs with a market capitalization of

approx. $400 billion

•Advantage of MLP – provides tax advantages of a partnership with

liquidity of a publicly traded corporation

MASTER LIMITED PARTNERSHIP – WHAT IS IT?

•Limited partnership formed under a state LP law

– Formed by filing certificate of limited partnership

– Subject to same compliance requirements as any other LP (filing

requirements, registered agent, foreign qualification, Annual Report etc.)

– Management and financial provisions set forth in LP agreement

– Most MLPs are formed under Delaware’s LP law

•Publicly traded

•Listed on a major stock exchange

– About two-thirds trade on NYSE, rest on NASDAQ

•Not subject to corporate taxation

•Engaged in the transportation, storage, processing of minerals and

natural resources

•To qualify as a MLP and not pay corporate income tax, LP must receive

at least 90% of its income from natural resource based activities

“SHAREHOLDER FRIENDLY” CORPORATION LAWS

•North Dakota’s Publicly Traded Corporation Act (2007)

– Referred to as US’ first “shareholder friendly” corporation act

– Ch. 10-35 of North Dakota Code

•Problem it addressed: lack of influence shareholders have over

corporate governance

– Enacted in reaction to governance & financial scandals

– Intended to allow shareholders to better monitor director performance

– Carl Icahn was major proponent

POLLING QUESTION NO. 4

What is your opinion of the MLP?

A. Interesting in theory but probably wont use for my clients.

B. I would like to use it but my clients do not need one.

C. My clients are big investors and are beginning to ask about setting

one up.

NORTH DAKOTA’S PUBLICLY TRADED CORPORATIONS ACT

•Shareholder friendly provisions

– Requires majority vote to elect directors

– Requires corporation to include in its proxy statement director candidates

nominated by shareholders owning at least 5% of shares

– Requires corporation to reimburse shareholder’s proxy solicitation costs

– Prohibits supermajority voting or quorum

– Directors’ terms may not be longer than 1 year or staggered

– 10% shareholder has right to call special meeting

– Restricts poison pills

– Permits any shareholder to propose the adoption, amendment or repeal of a

bylaw

– Prohibits chairperson of board from serving as executive officer

•Proponents hoped publicly traded corporations would reincorporate in

ND or DE would adopt these provisions

– Neither has happened

REVIEW

REVIEW

•Why there are so many statutory business entities

•Series LLC

•Social Enterprise Entities

– Benefit Corporation

– Low-Profit LLC

– Others

•Miscellaneous entities of interest

– Master LP

– “Shareholder friendly” publicly traded corporation act

SUMMARY

•Several new statutory entities have become available in 21st century

• Intended to solve certain problems identified by their proponents

•Options lawyers may consider when deciding what entity type best fits

clients’ needs

• Include the following

– Series LLCs

– Benefit corporations and other social enterprise entities

– UNPA, LCA

•Formed by filing documents with state business entity filing office

•Required to comply with state business entity laws to maintain status

ALTERNATIVE ENTITIES NAVIGATING NEW CHOICES FOR BUSINESS FORMATIONS

THANK YOU FOR ATTENDING