akg financial strength assessment report - liverpool … · · 2017-12-19about this financial...

TRANSCRIPT

ISSUED 15 DECEMBER 2017

PROVIDER SECTOR LV=

FINANCIAL

STRENGTH

ASSESSMENT

LV= P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 2 15 December 2017

Com

pan

y A

nal

ysis

Guid

e

ABOUT THIS FINANCIAL STRENGTH ASSESSMENT

This AKG report and the analysis and ratings contained within it provide assessment of financial strength and associated

considerations. Financial Strength is focused on the ability of a company to deliver ongoing operational capability in the

interest of its customers and in line with their fairly held expectations. AKG’s perspective in the assessment of financial

strength is wholly that of a customer of a product or service. From that foundation, this analysis is specifically designed to

inform financial advisers and assist in their required understanding of a company’s operational financial strength.

Given the underlying customer perspective, the financial strength of companies needs to be focused at an operational

level (i.e. the elements and functions of an organisation which operate to specifically deliver and manage a proposition or

service to the customer), specifically on the company that is effecting the product or service that a customer is selecting.

This is important, because from the customer’s perspective it is that company that needs to survive in a form that maintains

the requisite operational characteristics to meet their fairly held requirements. And it is thus at this level that the selection

needs of the customers’ advisers must be met. This contrasts to credit rating, which will be undertaken at group or parent

company level where investment or debt placement etc. is made.

Further details on how analysis is undertaken is provided at the end of this report and may also be obtained from AKG.

TABLE OF CONTENTS

Rating & Assessment Commentary ........................................................................................................................................................................... 3

Ratings ................................................................................................................................................................................................................................................... 3

Summary .............................................................................................................................................................................................................................................. 3

Commentary ..................................................................................................................................................................................................................................... 3

Group & Parental Context ............................................................................................................................................................................................ 6

Background ......................................................................................................................................................................................................................................... 6

Group Structure (simplified) ..................................................................................................................................................................................................... 7

Company Analysis: Liverpool Victoria Friendly Society Ltd............................................................................................................................. 8

Basic Information ............................................................................................................................................................................................................................. 8

Operations ......................................................................................................................................................................................................................................... 9

Strategy .............................................................................................................................................................................................................................................. 11

Key Company Financial Data ................................................................................................................................................................................................. 13

Company Analysis: Liverpool Victoria Life Company Ltd ............................................................................................................................. 17

Basic Information .......................................................................................................................................................................................................................... 17

Operations ...................................................................................................................................................................................................................................... 18

Strategy .............................................................................................................................................................................................................................................. 18

Key Company Financial Data ................................................................................................................................................................................................. 19

Guide ................................................................................................................................................................................................................................... 22

Introduction .................................................................................................................................................................................................................................... 22

Rating Definitions ......................................................................................................................................................................................................................... 22

About AKG ..................................................................................................................................................................................................................................... 25

CONTACT INFORMATION

AKG Financial Analytics Ltd, Anderton House, 92 South Street, Dorking, Surrey, RH4 2EW Tel: +44 (0) 1306 876439 Email: [email protected] Web: www.akg.co.uk

LV= P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 3 15 December 2017

Rat

ing

& A

sses

smen

t C

om

men

tary

G

roup &

Par

enta

l Conte

xt

Com

pan

y A

nal

ysis

Guid

e

Rating & Assessment Commentary

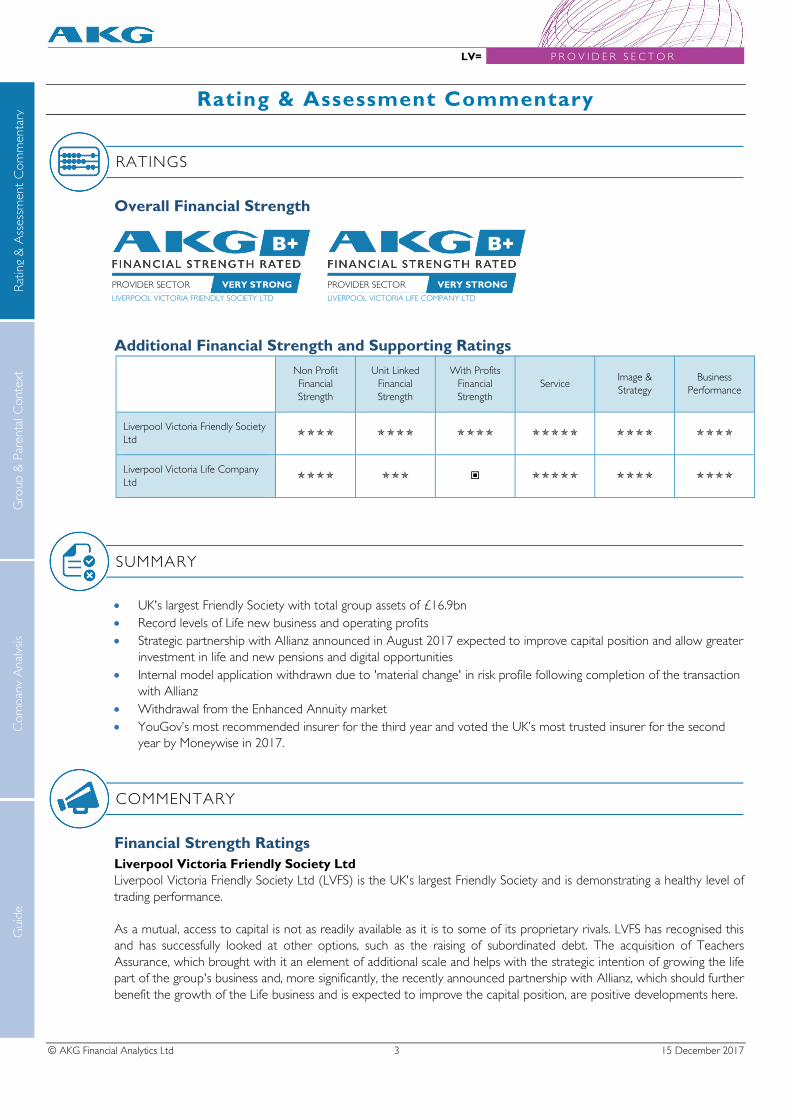

RATINGS

Overall Financial Strength

B+

PROVIDER SECTOR VERY STRONG

LIVERPOOL VICTORIA FRIENDLY SOCIETY LTD

B+

PROVIDER SECTOR VERY STRONG

LIVERPOOL VICTORIA LIFE COMPANY LTD

Additional Financial Strength and Supporting Ratings

Non Profit

Financial

Strength

Unit Linked

Financial

Strength

With Profits

Financial

Strength

Service Image &

Strategy

Business

Performance

Liverpool Victoria Friendly Society

Ltd ���� ���� ���� ����� ���� ����

Liverpool Victoria Life Company

Ltd ���� ��� � ����� ���� ����

SUMMARY

• UK's largest Friendly Society with total group assets of £16.9bn

• Record levels of Life new business and operating profits

• Strategic partnership with Allianz announced in August 2017 expected to improve capital position and allow greater

investment in life and new pensions and digital opportunities

• Internal model application withdrawn due to 'material change' in risk profile following completion of the transaction

with Allianz

• Withdrawal from the Enhanced Annuity market

• YouGov’s most recommended insurer for the third year and voted the UK’s most trusted insurer for the second

year by Moneywise in 2017.

COMMENTARY

Financial Strength Ratings

Liverpool Victoria Friendly Society Ltd

Liverpool Victoria Friendly Society Ltd (LVFS) is the UK's largest Friendly Society and is demonstrating a healthy level of

trading performance.

As a mutual, access to capital is not as readily available as it is to some of its proprietary rivals. LVFS has recognised this

and has successfully looked at other options, such as the raising of subordinated debt. The acquisition of Teachers

Assurance, which brought with it an element of additional scale and helps with the strategic intention of growing the life

part of the group's business and, more significantly, the recently announced partnership with Allianz, which should further

benefit the growth of the Life business and is expected to improve the capital position, are positive developments here.

LV= P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 4 15 December 2017

Rat

ing

& A

sses

smen

t C

om

men

tary

G

roup &

Par

enta

l Conte

xt

Com

pan

y A

nal

ysis

Guid

e

The group's capital position has also improved, to 153% as at 30 June 2017, with surplus capital increasing from £367m

at 31 December 2016 to £470m and getting closer to the group's risk appetite buffer of £550m.

The recent strategic refresh, which includes a cost reduction programme, bringing with it a clear focus on cost and

underwriting discipline, also provides comfort.

Non profit business in the Society is secure, given its heightened focus and the level of with profits business alongside it.

Similarly, the small amount of non profit business retained in Liverpool Victoria Life Company Ltd (LVLC) is secure and

enjoys the support of the parent.

Unit linked business is now key to the overall proposition and AKG expects appropriate support and attention to be

given. This line enjoys the comfort and support that the Society and its level of free assets brings.

In recent years, the Society has generally shown good with profits performance, and it maintains a reasonable equity

backing ratio. Whilst the largest of the Friendly Societies, it remains a relatively small fund when compared with the larger

life companies. Although other business lines now dominate marketing activities, with profits business remains important.

The transfer of Teachers Provident to LVFS and sale of goodwill, subsidiaries and non profit business has improved the

financial position of the Teachers Assurance Fund, although in part offset by the payment of £250 to each qualifying

member for loss of membership rights and a similar rating for with profits business applies for this fund.

The with profits rating shown does not apply to the smaller RNPFN fund, which is not as financially strong and has a rating

of 3 stars.

Liverpool Victoria Life Company Ltd

LVLC is a small declining company. The solvency coverage is reasonable, with the minimum capital requirement biting, in

the context of the run off of the small block of remaining UIA business. The company also benefits from its presence

within the LV= Group.

Service Rating LV= states that one of its core aims is to deliver a strong and reliable service proposition to clients and advisers. The

appointment of a Chief Customer Officer in 2016, with responsibility for delivering LV=’s strategic objective of being a

truly customer centric organisation is a demonstration of this and LV= remains highly regarded both by intermediaries and

consumers.

LV=’s Fastway quote and apply technology is enabling a swifter Protection service experience for advisers.

LV=’s adviser toolkit for Protection and Retirement is comprehensive and designed to provide advisers with value added

planning support.

Image & Strategy Rating LV= offers a comprehensive Protection and Retirement proposition for advisers.

LV=’s focus on the development of digital functionality and services is seeing it involved in innovative areas such as online

advice.

LV= has responded well to the pension freedoms changes. With drawdown already in place within its range, LV= has

sought to provide advisers with a retirement toolkit and resources to support the retirement planning process.

In brand terms LV= has seen significant growth in the last decade, establishing it from a relatively modest position, to be

one of the UK's leading financial services brands, both from general recognition and positive perception perspectives. This

is now a significant strength, enabling development of adjacent product offerings and distribution approaches.

Following the transaction with Allianz, the Society will continue to benefit from a presence in the general insurance market,

while being better placed to invest in its core life and pensions business and pursue new digital opportunities.

LV= P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 5 15 December 2017

Rat

ing

& A

sses

smen

t C

om

men

tary

G

roup &

Par

enta

l Conte

xt

Com

pan

y A

nal

ysis

Guid

e

Business Performance Rating 2016 saw Liverpool Victoria report record Life operating profits and new business levels. However, the group reported

an overall pre-tax loss, due to the significant impact of the Ogden rate change for general insurance business, model and

basis changes in its legacy business and a number of one off costs, mostly relating to the introduction of Solvency II.

The group undertook a range of actions to improve its capital position, which have continued into 2017. There is also a

continued emphasis on costs.

LV= remained highly regarded both for its service and its overall proposition.

LV= P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 6 15 December 2017

Com

pan

y A

nal

ysis

Guid

e R

atin

g &

Ass

essm

ent

Com

men

tary

G

roup &

Par

enta

l Conte

xt

Group & Parental Context

BACKGROUND

Established in 1843, Liverpool Victoria Friendly Society Ltd (LVFS) has grown to become the UK's largest Friendly Society,

with group assets of £16.9bn and a group Solvency II coverage ratio of 140% as at 31 December 2016. The Society had

widened its operations substantially via new activities and acquisition. Acquiring Frizzells in 1996 and Landmark in 1997

broadened its scope to include general insurance, banking and the provision of independent financial advice. In February

2001, the group acquired Permanent Insurance Company Ltd from Equitable, renamed it Liverpool Victoria Life Company

Ltd (LVLC) and in December 2001 used this structure to acquire the Royal National Pension Fund for Nurses (RNPFN).

In 2002, Bishopscourt, an IFA group specialising in affinity services, was acquired. In November 2005, LVLC acquired a

small portfolio of business from UIA Insurance (UK) Ltd. January 2007 saw the Group acquire Britannia Road Rescue

Services and in December 2007 the Group acquired the new business operations of Tomorrow (previously GE Life) from

Swiss Re and entered the unit linked pensions market. In October 2008, LV= acquired the Highway Insurance Group, an

organisation complementary to its existing general insurance operations. The group transferred much of the life business

of LVLC to LVFS in two tranches, December 2008 and December 2011.

In recent years, the group has tightened its focus on core businesses and currently operates through two Strategic Business

Units (SBUs): Life, which now includes Heritage, and General Insurance. The Partnership SBU was dissolved in 2010 and

the Banking operation has also been disposed of, apart from remaining obligations and liabilities of around £25m which

have been transferred to LVFS. In 2011, the asset management arm, Liverpool Victoria Asset Management Ltd (LVAM),

was sold to Threadneedle Investments (now Columbia Threadneedle Investments) to whom it now outsources its asset

management, enabling the Society to focus on general insurance, protection and retirement solutions. All life and pensions

business is now written directly into the Society. Equity release is written by LV Equity Release Ltd. The group also transacts

motor, home and travel insurance through Liverpool Victoria Insurance Company Ltd. General Insurance is also written

through 3 other subsidiaries, LV Protection Ltd, Highway Insurance Company Ltd and Teachers Assurance Company Ltd.

The group disposed of its Whole of Market advice business in 2007. 2007 also saw the group carry out a major rebranding

exercise, introducing the brand LV= and reconfirming its commitment to mutuality. In May 2013, the Society issued £350m

of subordinated debt, enabling it to improve capital efficiency and support growth ambitions. LV= acquired a majority

stake in Wealth Wizards Ltd in August 2015. The group acquired most of the business of Teachers Assurance in June

2016.

Richard Rowney, previously managing director of the group's life and pensions business, replaced Mike Rogers as Chief

Executive in July 2016. Similarly Steve Treloar was appointed as managing director of general insurance in May 2016,

joining the board from Aviva as successor to John O’Roarke. Recognising the importance of customers and members to

the long-term success of the Society, Katie Wadey was appointed to the new role of customer and member director in

January 2016. Alan Cook also replaced Mark Austen as chairman in January 2017.

In August 2017, LV= announced a strategic partnership with Allianz, subject to regulatory approval, with a target date of

31 December 2017. The transaction is structured in two phases. Allianz will pay LV= an initial £500m in exchange for a

49% stake in LV=’s General Insurance businesses. LV= will acquire Allianz’s personal home and motor insurer’s renewal

rights, while Allianz will obtain LV=’s commercial insurer’s renewal rights. In 2019 Allianz will pay £213m for a further

20.9% stake in the general insurance business, taking Allianz's holding to 69.9%.

LV= P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 7 15 December 2017

Com

pan

y A

nal

ysis

Guid

e R

atin

g &

Ass

essm

ent

Com

men

tary

G

roup &

Par

enta

l Conte

xt

GROUP STRUCTURE (SIMPLIF IED)

Liverpool Victoria Friendly Society Ltd P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 8 15 December 2017

Com

pan

y A

nal

ysis

Guid

e R

atin

g &

Ass

essm

ent

Com

men

tary

G

roup &

Par

enta

l Conte

xt

Company Analysis: Liverpool Victoria Friendly Society Ltd

BASIC INFORMATION

Company Type

Life Friendly Society

Ownership & Control

Mutual

Year Established

1843

Country of Registration

UK

Head Office

County Gates, Bournemouth, BH1 2NF

Contact

Tel: 01202 292333 Email: [email protected] Web: www.lv.com

Key Personnel

Role Name

Chairman A R Cook

Group Chief Executive R A Rowney

Group Finance Director A M Parsons

Group Actuarial Services Director J M Laidlaw

Managing Director, Life & Pensions J T Perks

Life Commercial Director N Austin

Chief Risk Officer S R Haynes

Chief Operating Officer, Life S Knight

Chief Information Officer R A Warner

Chief Customer Officer K Wadey

Life Chief Actuary P M Downey

With Profits Actuary A R Walton

Company Background

Established in 1843, the Society is the UK's largest friendly society. Operating for many years as a traditional home service

insurance company, writing both Ordinary and Industrial Branch business, it had re-positioned itself with a much broader

range of activities, via a number of different subsidiaries. Some of these have since been exited as part of a more tightened

focus. It stopped writing industrial business in 1999 and entered the IFA market in 2000. The acquisition of the new

business operations of Tomorrow, late in 2007, and the transfers-in of the business from LVLC in 2008 and 2011 changed

the profile of the Society, having previously almost exclusively written with profits business. The business of Teachers

Provident Society Ltd was transferred into the Society, as part of the Heritage business, in June 2016, amounting to assets

of around £750m.

Liverpool Victoria Friendly Society Ltd P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 9 15 December 2017

Com

pan

y A

nal

ysis

Guid

e R

atin

g &

Ass

essm

ent

Com

men

tary

G

roup &

Par

enta

l Conte

xt

OPERATIONS

Governance System and Structure

The Group’s Board has adopted a governance structure based on the principles and provisions of the Financial Reporting

Council’s UK Corporate Governance Code (the ‘Code’). The Board has chosen to adopt early the April 2016 amendments

to the Code. As a Friendly Society, it has voluntarily complied with the Code and its principle of comply or explain. The

Board has confirmed its compliance with the Code, with the exception of two decisions approved by the Board; to allow

the Chairman to be a member of the Audit Committee; and for only the Chairman to stand for annual re-election at the

Annual General Meeting. The Board believes that its practices are consistent with the principles of the Code and are

appropriate and suitable for the Society and its members.

Within its Systems of Governance, the key functions are Risk, Compliance, Actuarial and Internal Audit. In setting up these

functions, the Board has 'ensured that:

• they are free from influences that may compromise their ability to undertake duties in an objective, fair and

independent manner

• each function operates under the ultimate responsibility of, and reporting to the Board

• they have the necessary authority, resources and expertise, as well as unrestricted access to all relevant information

necessary to carry out their responsibilities'.

Each of these key functions has a Board approved Terms of Reference (ToR), setting out their scope, authority and an

overview of objectives. The ToR also confirms 'how each function achieves independence, and how potential conflicts of

interest are managed'.

The LV= Member Panel is a group of around 40 members who represent a cross-section of membership and challenge

the group's performance. They meet with the board, executives and senior leaders twice a year. The Member Panel Hub

was established in 2016 so that the panel can stay in touch with news throughout the year and comment on developments

and changes via posts and online forum.

Risk Management

The LVFS Board bears ultimate responsibility for management of all risk across the Group and has established a consistent

approach to be followed across all Group entities. In particular, the Board takes responsibility for:

• approving the Group risk strategy and associated risk appetite statements;

• setting out a ‘three lines of defence’ model to be followed for risk management;

• monitoring the overall Group risk profile on a regular basis; and

• reviewing and approving the Group ORSA report.

This 'ensures that a robust and effective risk management framework is applied consistently, aligned with recognised good

practice and with the nature and sophistication of the risks involved. Active monitoring and control is exercised across

risks of all types, whilst maintaining compliance with all policies, appetite statements and regulations'. The LVFS Board

delegates authority for oversight of risk management to the Risk Committee, who review regular reports on the

effectiveness of risk management across the Group. In 2016, the Risk Committee commissioned an external review to

provide additional insight, and initiated a Risk Development Programme to support the ongoing development of risk

capability through 2017 and 2018.

The Group operates an Enterprise Risk Management Framework (ERMF), which brings together risk management

strategies, objectives, processes, and reporting procedures. The ERMF has been developed by Group Risk Management.

It is reviewed at least annually, with changes approved by the Chief Risk Officer and the Risk Committee. The framework

is centred on the traditional risk management processes of Identification, Assessment and Management.

Liverpool Victoria Friendly Society Ltd P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 10 15 December 2017

Com

pan

y A

nal

ysis

Guid

e R

atin

g &

Ass

essm

ent

Com

men

tary

G

roup &

Par

enta

l Conte

xt

Administration

From a structural perspective, LV= stated that the June 2017 move to bring its Protection, Retirement Solutions and

Heritage businesses under one management would allow for greater operational efficiencies.

LV= states that over £80m has been invested on the development of digital propositions since June 2015 with a specific

requirement to improve core operating systems within the GI and Protection businesses as well as a current focus within

Retirement Solutions on systems and digital propositions.

As a key component of this work, LV= has now completed the roll out of its new quote and apply technology, Fastway,

to financial advisers, offering a faster way for advisers to protect clients. This technology can be used for LV=’s ‘personal’

Life Insurance, Life with Critical illness, Income Protection and Personal Sick Pay (PSP) product lines.

A new pre-underwriting tool is available online, 24/7, which enables advisers to submit business outside of regular working

hours and receive instant decisions without having to call an underwriter. The tool can provide an indication of the final

underwriting outcome, and can also be used for multiple conditions and confirming any necessary medical evidence. LV=

operates a tele-interview booking system which enables customers to book an appointment online as part of the

application process for the Flexible Protection Plan.

Recent service-based recruitment has included the appointment of a Technical Claims Manager, Protection, with specific

focus on customer outcomes and consistent claims processes, and a Rehabilitation Manager to focus on helping individuals

suffering from illness or injury with their recovery.

LV= operates with a large case team, to support the management of protection servicing for adviser’s high value clients,

and has a Business Protection Specialist team, to help advisers with underwriting and application processes.

Benchmarks

LV= states that its Fastway quote and apply technology can give advisers an immediate underwriting decision for over

75% of LV= Life and Life with Critical illness customers, and almost 70% of LV= Income Protection and Personal Sick Pay

customers.

LV= publishes claims performance data on its Adviser Centre. In 2016, LV= stated that it had paid out 94% of all new

individual protection claims, totalling close to £77m over the year, and that it had paid 100% of 50 Plus claims, 98% of life

insurance claims, 92% of critical illness claims and 90% of income protection claims. In total, LV= paid out almost 7,000

claims over the year.

LV= was named Insurance Provider of the Year at the Which Awards 2017, remained YouGov’s most recommended

insurer for the third year and was voted Most Trusted Insurer for the second year at the Moneywise Awards.

The LV= Protection and Retirement Solutions businesses continue to win awards and recognition for quality of products

and proposition. These include Gold Standard Awards in 2014, 2015 and 2016 for Protection, Retirement and Individual

Pensions and ILP Moneyfacts Awards for Income Protection, SIPP and Equity Release.

LV= was awarded five stars in the Life & Pensions and Investments categories at the Financial Adviser Service Awards in

2016 and 2017. LV= was awarded four stars in the Life & Pensions category and three stars in the Mortgages category at

the FTAdviser Online Innovation and Service Awards 2017.

Outsourcing

To ensure a consistent approach across the Group, the Group maintains an Outsourcing and Sourcing Policy. This policy

is reviewed on an annual basis and sets out detailed requirements on areas including:

• overall sourcing strategy

• supplier assessment criteria

• principles for identifying Critical and Important relationships, and

• contractual and operational requirements and ongoing supplier relationship management.

In January 2004, the Society concluded a long term contract with EDS Ltd to outsource the administration of its life

business, whilst retaining all customer contact. This business was brought back in-house in 2007/8 in line with the Society's

Liverpool Victoria Friendly Society Ltd P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 11 15 December 2017

Com

pan

y A

nal

ysis

Guid

e R

atin

g &

Ass

essm

ent

Com

men

tary

G

roup &

Par

enta

l Conte

xt

views on service. Some administration of investment products is outsourced to Outsourced Professional Administration

Ltd (OPAL).

A fundamental reappraisal of the group's strategy saw it outsource the investment management function in 2011. The

mandate was awarded to Columbia Threadneedle Investments, with the transfer of fund management completed during

the final quarter of 2011. LV= has governance processes in place to oversee the arrangement, including designing and

implementing asset allocations to reflect the risk tolerances with the strategic business units, setting benchmarks and

monitoring performance. SLAs have been established and are reviewed at the monthly Client Relationship Meeting.

A number of other functions are also outsourced, including infrastructure management & systems development, desktop

services & telephony and outbound printing & inbound scanning services,

STRATEGY

Market Positioning

In 2017, LV= launched a refreshed strategy, which included a cost reduction programme, targeting £40m of savings in

group costs by 2018.

To help deliver on its ambition to become the 'challenger brand' in the financial services industry, LV= has recently

launched a clear and simple blueprint for its future. Its strategic priorities focus on three themes: eradicating waste and

building stronger financial foundations; harnessing the power of the latest digital technologies and creating solutions for

customers that leave them feeling more confident about life and more confident in LV=.

LV= has a proposition which stretches across the Retirement and Protection markets. LV= also remains committed to its

with profits proposition and has experienced an increase in interest for this, primarily through its investment bond. LV=

has an equity release proposition within its product portfolio, provided by LV Equity Release Ltd, meaning that it can also

target the use of housing equity in retirement.

On the Life side, distribution is primarily through intermediaries (96% of sales), with 2% direct and 2% through tied advisers.

On the General side, the spilt is 40% brokers/60% direct. In aggregate this equates to 71% intermediary/broker, 28% direct

and 1% tied. LV= has a small team of 40, which includes 20 financial advisers (tied agents). operating in its in-house advise

service. LV= closed its Protection Advise Service, which operated in the term assurance market, because its offering is not

aimed at this market, which is more suited to commoditised, price driven products.

As part of a focus on its digital presence, LV= has invested in the development of an online retirement income advice

service in conjunction with Wealth Wizards. LV= Retirement Wizard (on-line regulated advice) was launched in July 2015,

opening up the online distribution channel as another option. The business has been actively developing a range of

corporate partners for its digital and adjacent retirement solutions. The partners for these are notable in their mix, including

financial services providers in other sectors, such as The People's Pension (B&CE), but also advisory businesses, 'end'

employers and other third parties.

LV= has subsequently appointed a new head of its Corporate Solutions business, which works with organisations to

provide specialist retirement advice and tools to pension scheme members. This role will form part of LV=’s commitment

to deliver engaging, accessible and affordable retirement solutions that support members of both Defined Benefit and

Defined Contribution pension schemes.

LV= has responded to a range of industry consultations in recent times, including the government’s consultation on a new

public financial guidance body. LV= has signed up and committed its support to the Treasury’s Cross-Industry Project

Group to build a Pensions Dashboard Prototype.

In December 2016, LV= announced the removal of all pension wrapper exit charges, allowing customers the freedom to

switch to another product or provider if they wish without incurring a charge. This move came as part of LV=’s

commitment to 'ensuring all customers are able to get the best possible outcome in retirement'.

Liverpool Victoria Friendly Society Ltd P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 12 15 December 2017

Com

pan

y A

nal

ysis

Guid

e R

atin

g &

Ass

essm

ent

Com

men

tary

G

roup &

Par

enta

l Conte

xt

Proposition

In November 2016, LV= announced that it was consulting with its employees on proposals to stop selling enhanced

annuities in order to increase its focus on secure drawdown options and its wider Retirement Solutions business. LV=

subsequently withdrew from the enhanced annuity market.

LV= operates with a Flexible Transitions Account, a Self-Invested Personal Pension, which can serve as a Personal Pension

or Drawdown Pension solution for customers, offering a wide range of investment options including access to DFMs.

LV=’s Protected Retirement Plan is a fixed term annuity, which aims to provide a secure income over a set term, with a

guaranteed value at maturity.

Development activities have subsequently focused on enabling advisers to recommend and blend a combination of LV=

product solutions through one overarching account, the LV= Retirement Account.

Investment options within the LV= Pension are categorised as LV= Value, LV= Secure, LV= Choice and LV= Wealth.

Under LV= Choice, LV= states that it is working with advisers to develop a new Model Portfolio Service.

LV= has designed a set of three funds to offer the potential for capital growth over the longer term with ongoing flexibility

and guarantee options. The LV= Flexible Guarantee Bond (FGB) has a structure and features which aim to provide an

element of protection and investment security for customers’ investments, while the funds are actively managed on LV=’s

behalf by Columbia Threadneedle Investments. The Flexible Guaranteed Funds are also available as fund options within

the SIPP wrapper.

LV= offers a comprehensive range of Personal and Business Protection lines. The Personal Protection range includes

Income Protection, Life Insurance, Life and Critical Illness, Flexible Protection Plan (a menu plan), Personal Sick Pay,

Inheritance Tax Protection, Family Income Assurance and Gift Inter Vivos. The Business Protection range includes Key

Person Cover, Share & Partnership Protection and Relevant Life Cover.

LV= offers Flexible Lifetime Mortgage and Lifetime Mortgage - Lump Sum+ product lines in the equity release market.

LV= is a member of the Equity Release Council and, in adherence with the Safe Home Income Plans (SHIP) standards,

therefore offers additional features and safeguards to LV=’s lifetime mortgage products. This includes offering a 'No

Negative Equity Guarantee' and a guarantee that the customer is safe to stay in their home for as long as they wish,

provided all terms and conditions of the mortgage are met.

LV= continues to work on integration of its products from a quote, apply and valuation perspective with back office

systems providers and quotation portals. It has back office systems links in place with suppliers including IRESS Adviser

Office, Best Practice, Intelliflo, Plum Software and True Potential, and portal links in place with suppliers including iPipeline,

Lifequote, Webline, Hub Financial Solutions (previously TOMAS) and Annuity Exchange.

Investment management of the various funds is completely outsourced to specialist investment managers. The asset

management undertaken by LV= Asset Management was transferred to Columbia Threadneedle Investments in 2011,

who are given specific objectives and benchmarks on how to run the funds. These funds include tracker funds and actively

managed equity funds covering the world's major markets. Fund managers include: 7IM, Artemis, BlackRock, Fidelity,

Invesco Perpetual, Investec, JPMorgan, Jupiter, Liontrust, M&G, Newton, Old Mutual and Schroder as well as Columbia

Threadneedle Investments.

LV='s flagship SIPP, the Flexible Transitions Account, also offers: Discretionary Management (through Brewin Dolphin,

Cazenove Capital Management, Charles Stanley, Investec Wealth & Investment, Quilter and Rathbones); access to

Cofunds, FundsNetwork and a Self Investment option.

The return on the main with-profits fund in 2016 was 14.5%, which is a significant increase on the 2015 performance of

3.8%. The with-profits fund performance was 1% below benchmark, driven by underperformance in equities, partially

offset by over performance in gilts and bonds.

Liverpool Victoria Friendly Society Ltd P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 13 15 December 2017

Com

pan

y A

nal

ysis

Guid

e R

atin

g &

Ass

essm

ent

Com

men

tary

G

roup &

Par

enta

l Conte

xt

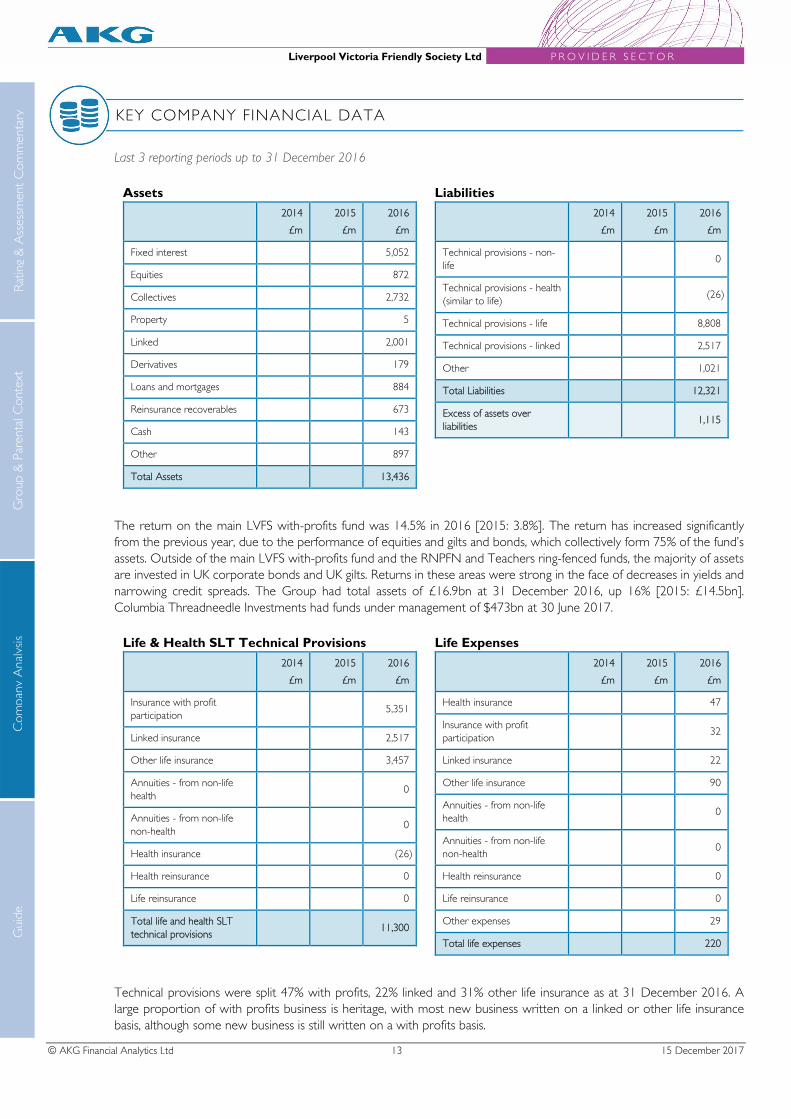

KEY COMPANY FINANCIAL DATA

Last 3 reporting periods up to 31 December 2016

Assets

2014

£m

2015

£m

2016

£m

Fixed interest 5,052

Equities 872

Collectives 2,732

Property 5

Linked 2,001

Derivatives 179

Loans and mortgages 884

Reinsurance recoverables 673

Cash 143

Other 897

Total Assets 13,436

Liabilities

2014

£m

2015

£m

2016

£m

Technical provisions - non-

life 0

Technical provisions - health

(similar to life) (26)

Technical provisions - life 8,808

Technical provisions - linked 2,517

Other 1,021

Total Liabilities 12,321

Excess of assets over

liabilities 1,115

The return on the main LVFS with-profits fund was 14.5% in 2016 [2015: 3.8%]. The return has increased significantly

from the previous year, due to the performance of equities and gilts and bonds, which collectively form 75% of the fund’s

assets. Outside of the main LVFS with-profits fund and the RNPFN and Teachers ring-fenced funds, the majority of assets

are invested in UK corporate bonds and UK gilts. Returns in these areas were strong in the face of decreases in yields and

narrowing credit spreads. The Group had total assets of £16.9bn at 31 December 2016, up 16% [2015: £14.5bn].

Columbia Threadneedle Investments had funds under management of $473bn at 30 June 2017.

Life & Health SLT Technical Provisions

2014

£m

2015

£m

2016

£m

Insurance with profit

participation 5,351

Linked insurance 2,517

Other life insurance 3,457

Annuities - from non-life

health 0

Annuities - from non-life

non-health 0

Health insurance (26)

Health reinsurance 0

Life reinsurance 0

Total life and health SLT

technical provisions 11,300

Life Expenses

2014

£m

2015

£m

2016

£m

Health insurance 47

Insurance with profit

participation 32

Linked insurance 22

Other life insurance 90

Annuities - from non-life

health 0

Annuities - from non-life

non-health 0

Health reinsurance 0

Life reinsurance 0

Other expenses 29

Total life expenses 220

Technical provisions were split 47% with profits, 22% linked and 31% other life insurance as at 31 December 2016. A

large proportion of with profits business is heritage, with most new business written on a linked or other life insurance

basis, although some new business is still written on a with profits basis.

Liverpool Victoria Friendly Society Ltd P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 14 15 December 2017

Com

pan

y A

nal

ysis

Guid

e R

atin

g &

Ass

essm

ent

Com

men

tary

G

roup &

Par

enta

l Conte

xt

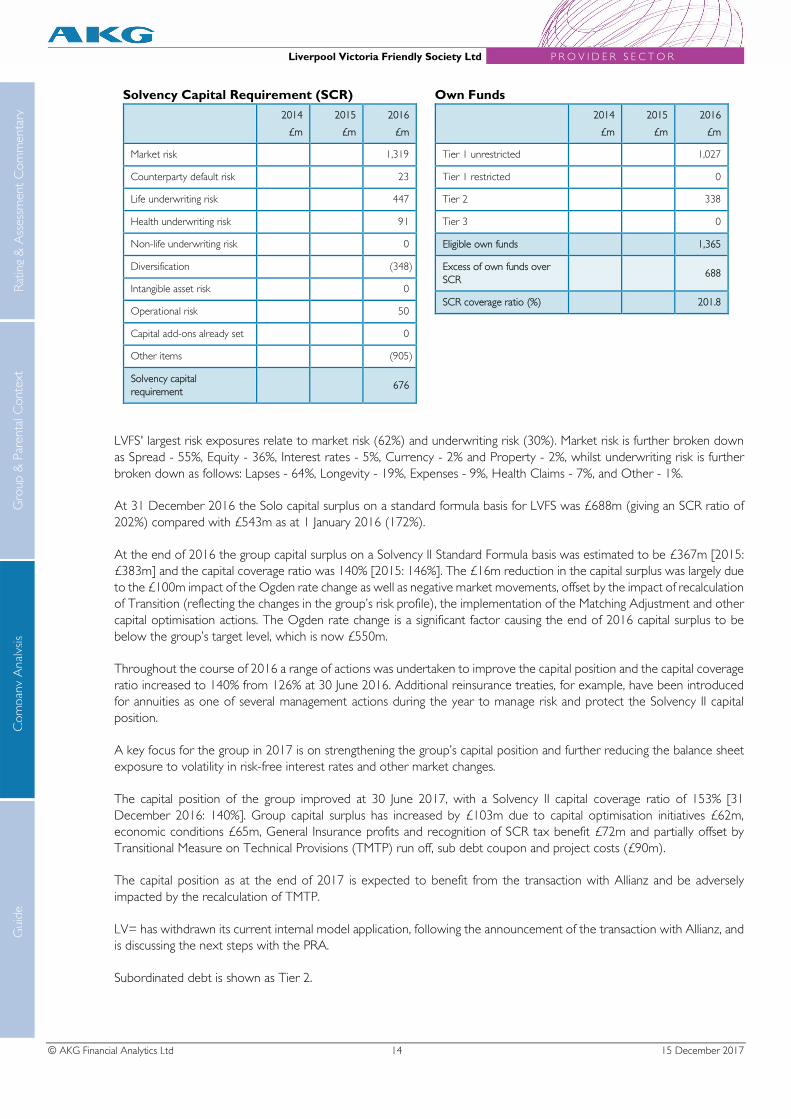

Solvency Capital Requirement (SCR)

2014

£m

2015

£m

2016

£m

Market risk 1,319

Counterparty default risk 23

Life underwriting risk 447

Health underwriting risk 91

Non-life underwriting risk 0

Diversification (348)

Intangible asset risk 0

Operational risk 50

Capital add-ons already set 0

Other items (905)

Solvency capital

requirement 676

Own Funds

2014

£m

2015

£m

2016

£m

Tier 1 unrestricted 1,027

Tier 1 restricted 0

Tier 2 338

Tier 3 0

Eligible own funds 1,365

Excess of own funds over

SCR 688

SCR coverage ratio (%) 201.8

LVFS' largest risk exposures relate to market risk (62%) and underwriting risk (30%). Market risk is further broken down

as Spread - 55%, Equity - 36%, Interest rates - 5%, Currency - 2% and Property - 2%, whilst underwriting risk is further

broken down as follows: Lapses - 64%, Longevity - 19%, Expenses - 9%, Health Claims - 7%, and Other - 1%.

At 31 December 2016 the Solo capital surplus on a standard formula basis for LVFS was £688m (giving an SCR ratio of

202%) compared with £543m as at 1 January 2016 (172%).

At the end of 2016 the group capital surplus on a Solvency II Standard Formula basis was estimated to be £367m [2015:

£383m] and the capital coverage ratio was 140% [2015: 146%]. The £16m reduction in the capital surplus was largely due

to the £100m impact of the Ogden rate change as well as negative market movements, offset by the impact of recalculation

of Transition (reflecting the changes in the group’s risk profile), the implementation of the Matching Adjustment and other

capital optimisation actions. The Ogden rate change is a significant factor causing the end of 2016 capital surplus to be

below the group’s target level, which is now £550m.

Throughout the course of 2016 a range of actions was undertaken to improve the capital position and the capital coverage

ratio increased to 140% from 126% at 30 June 2016. Additional reinsurance treaties, for example, have been introduced

for annuities as one of several management actions during the year to manage risk and protect the Solvency II capital

position.

A key focus for the group in 2017 is on strengthening the group’s capital position and further reducing the balance sheet

exposure to volatility in risk-free interest rates and other market changes.

The capital position of the group improved at 30 June 2017, with a Solvency II capital coverage ratio of 153% [31

December 2016: 140%]. Group capital surplus has increased by £103m due to capital optimisation initiatives £62m,

economic conditions £65m, General Insurance profits and recognition of SCR tax benefit £72m and partially offset by

Transitional Measure on Technical Provisions (TMTP) run off, sub debt coupon and project costs (£90m).

The capital position as at the end of 2017 is expected to benefit from the transaction with Allianz and be adversely

impacted by the recalculation of TMTP.

LV= has withdrawn its current internal model application, following the announcement of the transaction with Allianz, and

is discussing the next steps with the PRA.

Subordinated debt is shown as Tier 2.

Liverpool Victoria Friendly Society Ltd P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 15 15 December 2017

Com

pan

y A

nal

ysis

Guid

e R

atin

g &

Ass

essm

ent

Com

men

tary

G

roup &

Par

enta

l Conte

xt

Gross Life Premiums Written By Line of

Business

2014

£m

2015

£m

2016

£m

Health insurance 81

Insurance with profit

participation 609

Linked insurance 0

Other life insurance 538

Annuities - from non-life

health 0

Annuities - from non-life

non-health 0

Health reinsurance 0

Life reinsurance 0

Total gross life premiums

written 1,228

Gross Life Premiums Written By Country

2014

£m

2015

£m

2016

£m

Home country 1,228

Country 1 0

Country 2 0

Country 3 0

Country 4 0

Country 5 0

Other countries 0

Total gross life premiums

written 1,228

All business is written in the UK. Almost half of gross written premiums were on a with profits basis, recognising the

relative size of the heritage business and also investment into the Flexible Guaranteed Bond.

From a new business perspective results were good, APE written into LVFS increased by 5% from £189m to £198m.

New single premiums increased by 3.8% to £1.4bn, with pension business steady at £894m [2015: £893m], fixed term

annuities up to £239m [2015: £193m] and flexible guarantee bonds up to £217m [2015: £194m]. Sales of enhanced

annuities reduced from £116m to £99m, impacted by the decision to exit this market.

New regular premiums increased slightly from £49m to £53m, with pension sales up from £14m to £16m and protection

sales up from £35m to £37m.

Elsewhere in the group, equity release sales increased from £63m to £102m, benefiting from the new funding agreement

signed in 2016 and growing its market share from 4% to 7%.

Liverpool Victoria Friendly Society Ltd P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 16 15 December 2017

Com

pan

y A

nal

ysis

Guid

e R

atin

g &

Ass

essm

ent

Com

men

tary

G

roup &

Par

enta

l Conte

xt

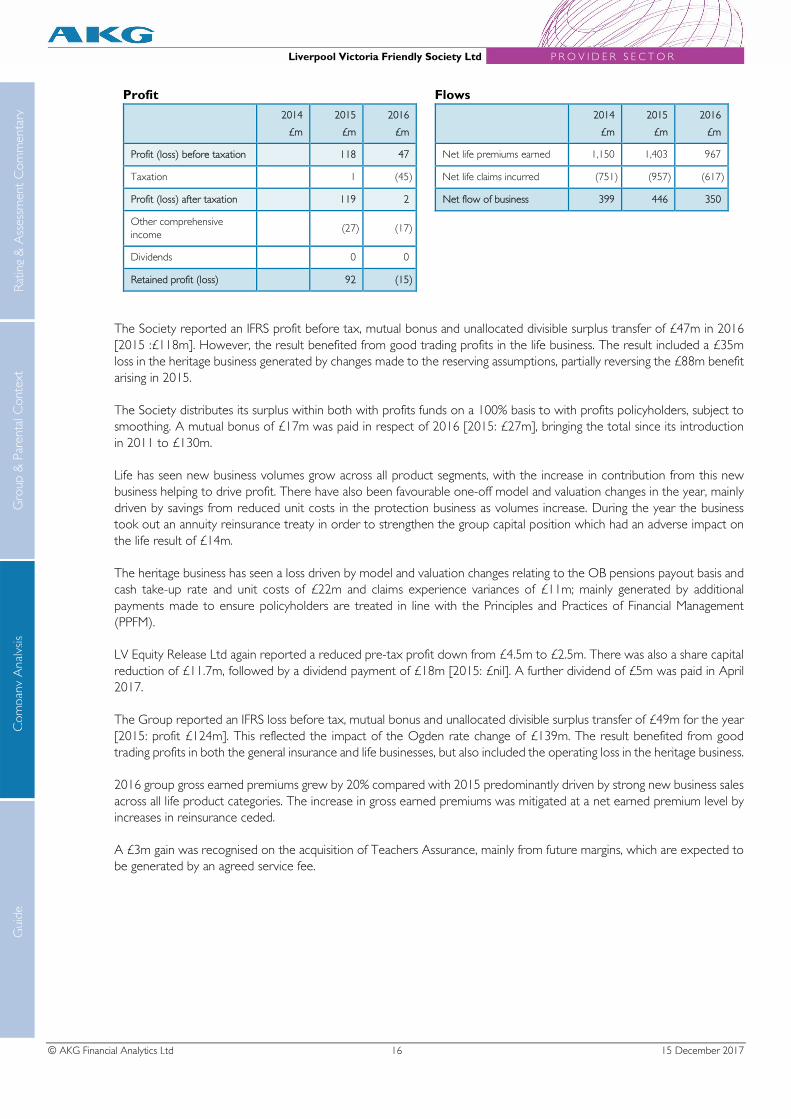

Profit

2014

£m

2015

£m

2016

£m

Profit (loss) before taxation 118 47

Taxation 1 (45)

Profit (loss) after taxation 119 2

Other comprehensive

income (27) (17)

Dividends 0 0

Retained profit (loss) 92 (15)

Flows

2014

£m

2015

£m

2016

£m

Net life premiums earned 1,150 1,403 967

Net life claims incurred (751) (957) (617)

Net flow of business 399 446 350

The Society reported an IFRS profit before tax, mutual bonus and unallocated divisible surplus transfer of £47m in 2016

[2015 :£118m]. However, the result benefited from good trading profits in the life business. The result included a £35m

loss in the heritage business generated by changes made to the reserving assumptions, partially reversing the £88m benefit

arising in 2015.

The Society distributes its surplus within both with profits funds on a 100% basis to with profits policyholders, subject to

smoothing. A mutual bonus of £17m was paid in respect of 2016 [2015: £27m], bringing the total since its introduction

in 2011 to £130m.

Life has seen new business volumes grow across all product segments, with the increase in contribution from this new

business helping to drive profit. There have also been favourable one-off model and valuation changes in the year, mainly

driven by savings from reduced unit costs in the protection business as volumes increase. During the year the business

took out an annuity reinsurance treaty in order to strengthen the group capital position which had an adverse impact on

the life result of £14m.

The heritage business has seen a loss driven by model and valuation changes relating to the OB pensions payout basis and

cash take-up rate and unit costs of £22m and claims experience variances of £11m; mainly generated by additional

payments made to ensure policyholders are treated in line with the Principles and Practices of Financial Management

(PPFM).

LV Equity Release Ltd again reported a reduced pre-tax profit down from £4.5m to £2.5m. There was also a share capital

reduction of £11.7m, followed by a dividend payment of £18m [2015: £nil]. A further dividend of £5m was paid in April

2017.

The Group reported an IFRS loss before tax, mutual bonus and unallocated divisible surplus transfer of £49m for the year

[2015: profit £124m]. This reflected the impact of the Ogden rate change of £139m. The result benefited from good

trading profits in both the general insurance and life businesses, but also included the operating loss in the heritage business.

2016 group gross earned premiums grew by 20% compared with 2015 predominantly driven by strong new business sales

across all life product categories. The increase in gross earned premiums was mitigated at a net earned premium level by

increases in reinsurance ceded.

A £3m gain was recognised on the acquisition of Teachers Assurance, mainly from future margins, which are expected to

be generated by an agreed service fee.

Liverpool Victoria Life Company Ltd P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 17 15 December 2017

Com

pan

y A

nal

ysis

Guid

e R

atin

g &

Ass

essm

ent

Com

men

tary

G

roup &

Par

enta

l Conte

xt

Company Analysis: Liverpool Victoria Life Company Ltd

BASIC INFORMATION

Company Type

Life Insurer

Ownership & Control

Liverpool Victoria Friendly Society Ltd

Year Established

1958

Country of Registration

UK

Head Office

County Gates, Bournemouth, BH1 2NF

Contact

Tel: 01202 292333 Email: [email protected] Web: www.lv.com

Key Personnel

Role Name

See Liverpool Victoria Friendly Society Ltd

Company Background

Established as Medical Sickness & Life Assurance Society Ltd to operate in the intermediary market, the company was

renamed Permanent Insurance Company Ltd in 1982 when it acquired the business of the Contingency Insurance

Company Ltd and Minster Insurance Company Ltd. Equitable Life bought a controlling interest in 1995 (100% ownership

in 1997), selling the company to LVFS in February 2001, when it was renamed Liverpool Victoria Life Company Ltd

(LVLC). Until the business transfer in 2008, LVLC was the protection specialist within the Liverpool Victoria group,

operating from its own offices in Exeter.

In December 2001, the company acquired the business of the Royal National Pension Fund for Nurses (RNPFN). At the

same time, it accepted reinsurance of around £300m of with profits bonds from LVFS. It also exited the Group PHI

market, reinsuring this business, other than claims in payment, to Unum. In November 2005, the company acquired a small

portfolio of business from UIA Insurance (UK) Ltd, as a result of the group’s relationship with Unison, a key affinity partner.

The majority of the business of LVLC, including the ring fenced RNPFN fund, was transferred into LVFS in December

2008, followed in December 2011, by the remainder of the business, excluding the UIA business, which remains in LVLC.

LVLC is now closed to all new business and all reinsurance treaties with LVFS have been cancelled. Its main purpose is to

manage the run-off of the UIA business; 1,288 policies in force at 31 December 2016 [2015: 1,683].

In November 2009 the company sold all of its subsidiaries to LVFS to simplify the group's legal structure and corporate

governance. LVLC's substantial reduction in size led to a capital reduction in December 2010 of £530m, together with

settlement of £82m of subordinated loan debt and a transfer of investments and cash totalling £164m. In November

2012, the company further reduced its share capital by £9.9m, £5m of which was paid as a dividend.

Liverpool Victoria Life Company Ltd P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 18 15 December 2017

Com

pan

y A

nal

ysis

Guid

e R

atin

g &

Ass

essm

ent

Com

men

tary

G

roup &

Par

enta

l Conte

xt

OPERATIONS

Governance System and Structure

See LVFS

Risk Management

See LVFS

Administration

See LVFS

Benchmarks

See LVFS

Outsourcing

See LVFS

STRATEGY

Market Positioning

LVLC’s main purpose during the year was to manage the run-off of the UIA (Insurance) Limited business acquired in 2005

which relates to 98% of the insurance contract liabilities reported. LVLC is also the reinsurer of Protection contracts

consisting of term assurances and critical illness policies for which it receives premium income.

Proposition

The product range in LVLC principally covers a mixture of whole of life assurances, endowment assurances and term

assurances acquired from UIA Ltd in 2005, in addition to accepting a small volume of reinsurance business from external

organisations. The company does not cede any reinsurance to other parties and all lines are closed to new business.

Liverpool Victoria Life Company Ltd P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 19 15 December 2017

Com

pan

y A

nal

ysis

Guid

e R

atin

g &

Ass

essm

ent

Com

men

tary

G

roup &

Par

enta

l Conte

xt

KEY COMPANY FINANCIAL DATA

Last 3 reporting periods up to 31 December 2016

Assets

2014

£m

2015

£m

2016

£m

Fixed interest 16.6

Equities 0.0

Collectives 1.4

Property 0.0

Linked 0.0

Derivatives 0.0

Loans and mortgages 0.0

Reinsurance recoverables 0.0

Cash 1.9

Other 1.1

Total Assets 21.0

Liabilities

2014

£m

2015

£m

2016

£m

Technical provisions - non-

life 0.0

Technical provisions - health

(similar to life) 0.0

Technical provisions - life 15.4

Technical provisions - linked 0.0

Other 0.4

Total Liabilities 15.9

Excess of assets over

liabilities 5.1

Assets are predominantly fixed interest in nature, 79% as at 31 December 2016.

97% of total liabilities related to life business.

Life & Health SLT Technical Provisions

2014

£m

2015

£m

2016

£m

Insurance with profit

participation 0.0

Linked insurance 0.0

Other life insurance 15.2

Annuities - from non-life

health 0.0

Annuities - from non-life

non-health 0.0

Health insurance 0.0

Health reinsurance 0.0

Life reinsurance 0.2

Total life and health SLT

technical provisions 15.4

Life Expenses

2014

£m

2015

£m

2016

£m

Health insurance 0.0

Insurance with profit

participation 0.0

Linked insurance 0.0

Other life insurance 0.1

Annuities - from non-life

health 0.0

Annuities - from non-life

non-health 0.0

Health reinsurance 0.0

Life reinsurance 0.0

Other expenses 0.0

Total life expenses 0.1

99% of technical provisions related to Other life insurance as at 31 December 2016, with the balance being reinsurance

accepted.

Liverpool Victoria Life Company Ltd P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 20 15 December 2017

Com

pan

y A

nal

ysis

Guid

e R

atin

g &

Ass

essm

ent

Com

men

tary

G

roup &

Par

enta

l Conte

xt

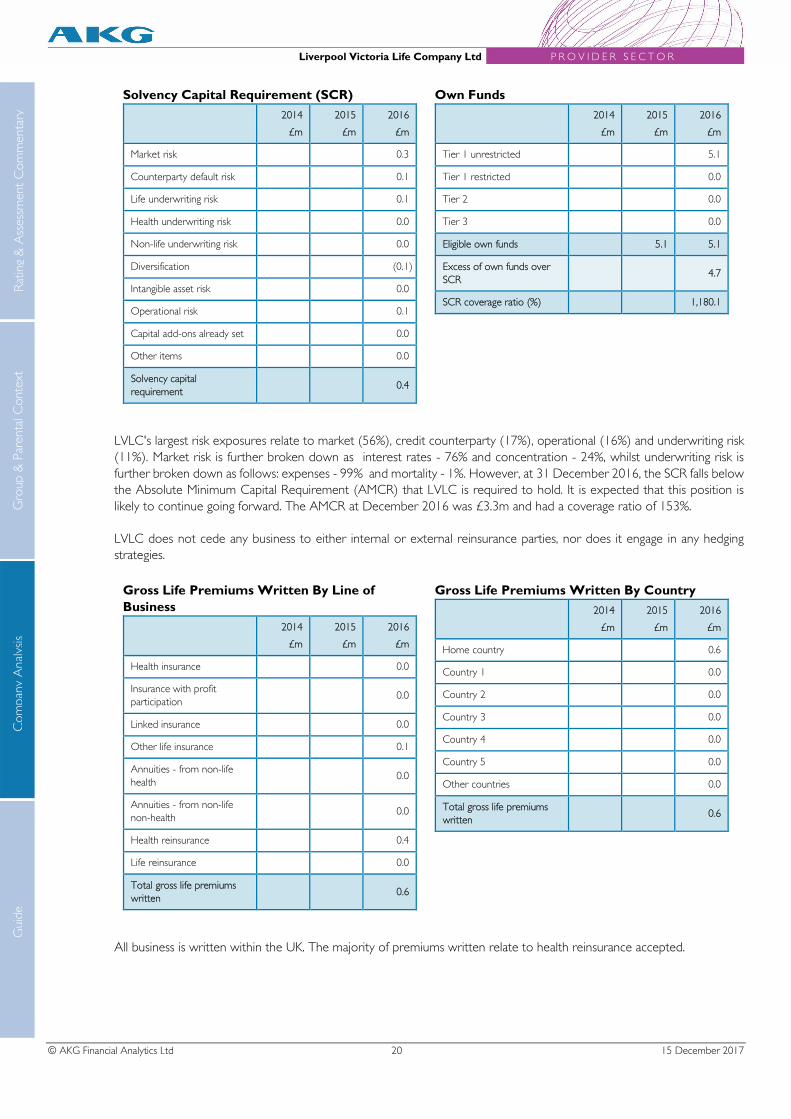

Solvency Capital Requirement (SCR)

2014

£m

2015

£m

2016

£m

Market risk 0.3

Counterparty default risk 0.1

Life underwriting risk 0.1

Health underwriting risk 0.0

Non-life underwriting risk 0.0

Diversification (0.1)

Intangible asset risk 0.0

Operational risk 0.1

Capital add-ons already set 0.0

Other items 0.0

Solvency capital

requirement 0.4

Own Funds

2014

£m

2015

£m

2016

£m

Tier 1 unrestricted 5.1

Tier 1 restricted 0.0

Tier 2 0.0

Tier 3 0.0

Eligible own funds 5.1 5.1

Excess of own funds over

SCR 4.7

SCR coverage ratio (%) 1,180.1

LVLC's largest risk exposures relate to market (56%), credit counterparty (17%), operational (16%) and underwriting risk

(11%). Market risk is further broken down as interest rates - 76% and concentration - 24%, whilst underwriting risk is

further broken down as follows: expenses - 99% and mortality - 1%. However, at 31 December 2016, the SCR falls below

the Absolute Minimum Capital Requirement (AMCR) that LVLC is required to hold. It is expected that this position is

likely to continue going forward. The AMCR at December 2016 was £3.3m and had a coverage ratio of 153%.

LVLC does not cede any business to either internal or external reinsurance parties, nor does it engage in any hedging

strategies.

Gross Life Premiums Written By Line of

Business

2014

£m

2015

£m

2016

£m

Health insurance 0.0

Insurance with profit

participation 0.0

Linked insurance 0.0

Other life insurance 0.1

Annuities - from non-life

health 0.0

Annuities - from non-life

non-health 0.0

Health reinsurance 0.4

Life reinsurance 0.0

Total gross life premiums

written 0.6

Gross Life Premiums Written By Country

2014

£m

2015

£m

2016

£m

Home country 0.6

Country 1 0.0

Country 2 0.0

Country 3 0.0

Country 4 0.0

Country 5 0.0

Other countries 0.0

Total gross life premiums

written 0.6

All business is written within the UK. The majority of premiums written relate to health reinsurance accepted.

Liverpool Victoria Life Company Ltd P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 21 15 December 2017

Com

pan

y A

nal

ysis

Guid

e R

atin

g &

Ass

essm

ent

Com

men

tary

G

roup &

Par

enta

l Conte

xt

Profit

2014

£m

2015

£m

2016

£m

Profit (loss) before taxation 0.1 0.7

Taxation 0.0 (0.4)

Profit (loss) after taxation 0.1 0.3

Other comprehensive

income 0.0 0.0

Dividends (10.0) 0.0

Retained profit (loss) (9.9) 0.3

Flows

2014

£m

2015

£m

2016

£m

Net life premiums earned 0.6 0.6 0.6

Net life claims incurred (2.0) (3.0) (1.5)

Net flow of business (1.3) (2.4) (0.9)

The company reported an increased Profit Before Tax of £713k in 2016 [2015: £102k]. No dividend was paid [2015:

£10m].

Net premiums reduced by 5% from £595k to £564k. The majority of this, 78% [2015: 72%] related to reinsurance

accepted. With net claims reducing from £3,019k to £1,454k, there was a reduced net outflow of £890k [2015: £2,424k].

LV= P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 22 15 December 2017

Com

pan

y A

nal

ysis

Guid

e R

atin

g &

Ass

essm

ent

Com

men

tary

G

roup &

Par

enta

l Conte

xt

Guide

INTRODUCTION

For over 20 years AKG has particularly focused on the financial strength requirements of financial advisers, who when

acting on behalf of their clients, need to ascertain a company's ability to deliver sustained provision.

From this customer perspective, the financial strength of companies needs to be focused at an operational level, specifically

on the company that is effecting the product or service that a customer is selecting. This is important, because from the

customer’s perspective it is that company (not some higher corporate entity) that needs to survive in a form that maintains

the requisite operational characteristics to meet their fairly held requirements. And it is thus at this level that the selection

needs of the customers’ advisers must be met.

It is also important to understand the sector approach (comparative peer groups) that is adopted in financial strength

assessment and rating process.

At AKG, this is again driven by the end customer perspective and the fact that assessment is designed solely for this

purpose, i.e. as a component in helping customers’ advisers to select between comparable companies competing to deliver

relevant products or services.

AKG’s focus and approach has remained consistent over the years since it commenced assessment and rating support for

the market. However, coverage, format and presentation has rightly evolved over this period, in line with the needs and

expectations of assessment and rating users in the market. And AKG considers further changes on a continual basis.

Further details including an explanation of what is included in the assessment reports and coverage can be found online

at http://www.akg.co.uk/information/reports/company-profiles.

AKG’s process for assessment and rating is to use a balanced scorecard of measures and comparative information, relevant

to the companies contained within each peer group. This is gathered via Public Information only for non-participatory

assessments and public information plus company interactions with companies for participatory assessments. Further

details on AKG’s process can be found at http://www.akg.co.uk/information/reports.

This includes further information on the different participatory and non-participatory basis and for companies wishing to

learn more about participatory assessment AKG is pleased to outline this and welcomes contact.

This is a participatory assessment.

RATING DEFINITIONS

Overall Financial Strength Rating

The objective is to provide a simple indication of the general financial strength of a company from the perspective of those

of financial advisers who when acting on behalf of their clients need to ascertain a company's ability to deliver sustained

operational provision of products or services.

The overall rating inherently reflects the mix of business within the company, since different types of customer or

policyholder have different requirements and expectations, and the company may have particular strengths and

weaknesses in respect of its key product or service areas. However, it also takes account of comparison across the sector

in which it is assessed.

The rating takes into account those of the following criteria which are relevant (depending upon the company's mix of

business in-force): capital and asset position, expense position and profitability, any specifically onerous elements such as

guarantees, structure (and size) of funds within the company, parental strength (and likely attitude towards supporting the

company), operational capability, management strength and capability, strategic position and rationale, brand and image,

LV= P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 23 15 December 2017

Com

pan

y A

nal

ysis

Guid

e R

atin

g &

Ass

essm

ent

Com

men

tary

G

roup &

Par

enta

l Conte

xt

typical fund performance achievements or product / service features, its operating environment and ability to withstand

external forces.

Rating Scale A B+ B B- C D �

Superior Very Strong Strong Satisfactory Weak Very Weak Not applicable

With Profits Financial Strength Rating

The objective is to assess the overall strength of the company’s with profits funds. The initial concern is the company's

ability to meet its ongoing guaranteed, or promised, commitments to customers, i.e. existing sum assured and bonuses.

However, the company's ability to continue to compete successfully in the with profits market is also particularly relevant,

given that closed funds are sometimes bad news for policyholders. In such situations, overall expenses tend to increase as

a proportion of the fund and investment performance may well deteriorate. These, together with other factors, may make

it difficult for companies in such situations to maintain competitive bonus rates at future declarations, although existing

declared bonuses are not affected (other than possibly by MVRs).

This is from the perspective of those of financial advisers who when acting on behalf of their clients, for this product type,

need to ascertain a company's ability to deliver sustained operational provision of with profits funds, products or

propositions. Its comparison is with other companies within the assessment sector that offer or have with profits business.

The main criteria taken into account are: capital and asset position, expense position and profitability, the amount of with

profits business in-force, parental strength (and likely attitude towards supporting the company), and image and strategy.

NOTE: More detailed analysis of with profits companies is included in AKG’s UK Life Office With Profits Reports.

Rating Scale ����� ���� ��� �� � �

Excellent Very Good Good Adequate Poor Not Rated

Unit Linked Financial Strength Rating

The objective is to provide a simple indication of the unit linked financial strength of a company, where it currently offers

unit linked business or has existing unit linked business within it. This is from the perspective of those of financial advisers

who when acting on behalf of their clients, for this product type, need to ascertain a company's ability to deliver sustained

operational provision of unit linked products or propositions. Its comparison is with other companies within the assessment

sector that offer or have unit linked business.

The main criteria taken into account are: capital and asset position, expense position and profitability, structure (and size)

of funds within the company, parental strength (and likely attitude towards supporting the company), operational capability,

management strength and capability, strategic position and rationale, brand and image, typical fund performance

achievements or product / service features, its operating environment and ability to withstand external forces.

Rating Scale ����� ���� ��� �� � �

Excellent Very Good Good Adequate Poor Not Rated

Non Profit Financial Strength Rating

The objective is to provide a simple indication of the non profit financial strength of a company, where it currently offers

or has existing products and propositions such as term assurance and annuities. This includes the company’s ability to

meet all guaranteed payments arising from such products, but also the company’s wider ability to deliver sustained

operational provision of such non profit products or propositions. Its comparison is with other companies within the

assessment sector that offer or have non profit business.

LV= P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 24 15 December 2017

Com

pan

y A

nal

ysis

Guid

e R

atin

g &

Ass

essm

ent

Com

men

tary

G

roup &

Par

enta

l Conte

xt

The main criteria taken into account are: capital and asset position, expense position and profitability, structure (and size)

of funds within the company, parental strength (and likely attitude towards supporting the company), operational capability,

management strength and capability, strategic position and rationale, brand and image, product / service features, its

operating environment and ability to withstand external forces.

Rating Scale ����� ���� ��� �� � �

Excellent Very Good Good Adequate Poor Not Rated

Service Rating

The objective is to assess the quality of the organisation's service to the intermediary market in respect of the brand

concerned.

Criteria taken into account include: performance in surveys, awards and benchmarking exercises (external and internal),

the organisation's philosophy, service charters, the extent of investments designed to improve service, and feedback from

intermediaries.

Rating Scale ����� ���� ��� �� � �

Excellent Very Good Good Adequate Poor Not Rated

Image & Strategy Rating

The objective is to assess the effectiveness of the means by which the organisation currently positions itself to distribute

its products for the brand concerned and the plans it has to maintain and/or develop its position.

Criteria taken into account include: overall trends in the company’s market share position, brand visibility and reputation,

feedback from intermediaries and industry commentators, and AKG’s view of the company’s general strategy.

Rating Scale ����� ���� ��� �� � �

Excellent Very Good Good Adequate Poor Not Rated

Business Performance Rating

This review is an assessment of how the company and the brand has fared against its peers, and how it is perceived

externally. Effectively this is how it has performed recently in the market. Whilst it will include performance indicators

from the most recent available statutory reporting (report and accounts and SFCRs in the case of insurance companies,

for example) it will also draw on other recent key performance elements before and after such disclosure, up to the point

at which the assessment is undertaken.

Criteria taken into account include: increase/decrease in market shares, expense containment, publicity good or bad, press

or market commentary, regulatory fines, and competitive position.

Rating Scale ����� ���� ��� �� � �

Excellent Very Good Good Adequate Poor Not Rated

LV= P R O V I D E R S E C T O R

© AKG Financial Analytics Ltd 25 15 December 2017

Com

pan

y A

nal

ysis

Guid

e R

atin

g &

Ass

essm

ent

Com

men

tary

G

roup &

Par

enta

l Conte

xt

ABOUT AKG

AKG is an independent organisation. Originally established as an actuarial consultancy AKG has, for over 20 years,

specialised in the provision of assessment, ratings, information and market assistance to the financial services industry.

As the market has evolved over this period, the range of entities considered by AKG has expanded. Consequently, AKG

has brought additional skill sets into its operations. This has meant the inclusion of accounting, corporate finance, IT and

market intelligence experience, alongside actuarial resources, to deliver an expanded professional capability.

Today AKG’s core purpose is in the provision of financial analysis and review services to support the wider financial services

sector and its customers.

© AKG Financial Analytics Ltd (AKG) 2017

This report is issued as at a certain date, and it remains AKG's current assessment with current ratings until it is superseded by a subsequently issued

report or subsequently issued ratings (at which point the newly issued report or ratings should be used), or until AKG ceases to make such a report

or ratings available.

The report contains assessment based on available information at the date as shown on the report’s cover and in its page footer. This includes prior

regulatory data which may have an earlier date associated with it, but the report also takes into account all relevant events and information, available

to and considered by AKG, which have occurred prior to this stated cover and footer date. Events and information subsequent to this date are not

covered within it, but AKG continually monitors and reviews such events and information and where individually or in aggregate such events or

information give rise to rating revision an updated report under an updated date is issued as soon as possible.

All rights reserved. This report is protected by copyright. This report and the data/information contained herein is provided on a single site multi

user basis. It may therefore be utilised by a number of individuals within a location. If provided in paper form this may be as part of a physical library

arrangement, but copying is prohibited under copyright. If provided in electronic form, this may be by means of a shared server environment, but

copying or installation onto more than one computer is prohibited under copyright. Printing from electronic form is permitted for own (single

location) use only and multiple printing for onward distribution is prohibited under copyright. Further distribution and uses of the report, either in its

entirety or part thereof, may be permitted by separate agreement, under licence. Please contact AKG in this regard or with any questions:

[email protected], Tel +44 (0) 1306 876439. AKG has made every effort to ensure the accuracy of the content of this report and to ensure that the

information contained is as current as possible at the date of issue, but AKG (inclusive of its directors, officers, staff and shareholders and any affiliated

third parties) cannot accept any liability to any party in respect of, or resulting from, errors or omissions. AKG information, comments and opinion,

as expressed in the form of its analysis and ratings, do not establish or seek to establish suitability in any individual regard and AKG does not provide,

explicitly or implicitly, through this report and its content, or any other assessment, rating or commentary, any form of investment advice or fiduciary

service.

AKG Financial Analytics Ltd Anderton House, 92 South Street, Dorking, Surrey RH4 2EW Tel: +44 (0) 1306 876439 Email: [email protected] Web: www.akg.co.uk © AKG Financial Analytics Ltd 2017