ahmedabad - magicbricksproperty.magicbricks.com/microsite/buy/propindex... · ahmedabad vol3, issue...

TRANSCRIPT

AHMEDABAD

PropIndex has completed three years now. Over this period, we’ve accumulated a wealthof data/analytics on price/locality trends and market performance. As the Indianproperty buyer gets more focused on returns from investment, we hope the dataprovided here, helps you in making informed property decisions. Use d in tandem withthe host of advisory services available online at advice.magicbricks.com, the effort is tomake this a one-stop shop for all your property queries, requirements and information.

The year 2014 started with anticipation among real estate stakeholders concerning the16th general elections in the country. These Lok Sabha elections have kept the IndianReal Estate Market in the wait and watch mode. This is reflected in the NationalProperty Index with a mere 1 per cent change in the Jan-Mar 2014 quarter. City indexvalues too remained intact and ranged between minus 1 to plus 3 per cent.

The formation of new government is expected to infuse fresh life into the real estatemarket and improve home buyers sentiments. In the current quarter, property marketsremained sluggish. However, robust demand from end-users arrested any significantchange in property values. We have observed few finds from the current report:

Key Findings

lAcross the country, capital markets have remained passive while rental markets haveflourished.

lDemand patterns across cities remained more or less in line with the previous quarterwith the mid-budget range of Rs 30-50 lakh remained the most preferred category,especially in Bangalore and Pune. However high end properties remained more indemand in Gurgaon and Mumbai.

lPremium luxury properties remained oversupplied across cities despite a robustdemand of over 20%.

lMumbai topped the chart with maximum demand for properties worth Rs 1 crore andabove, followed by Delhi and Gurgaon.

lSlower demand for property forced sellers to negotiate between 5-15 per cent on theasking values.

In this issue we have incorporated Greater Noida as an independent city which hasrecorded growing demand for residential properties, offering huge options in theaffordable ranges.

Do write in at [email protected] and share your views on this report and howwe could make PropIndex even better.

FOREWORD

Sudhir PaiBusiness Head, Magicbricks.com

NATIONAL PROPERTY INDEX (NPI)

VOL 3, ISSUE 4; JAN-MAR, FY 2013-14 propindex.magicbricks.com

JAN-MAR 2014

With buyer sentiments down across the country and everyone awaitingthe general elections, the common consensus is against buying property.This has resulted in people opting for rental accommodation as opposed tobuying their own home. This is the prime reason that held the growth ofthe National Property Index (NPI). It rose by 1 per cent in the Jan-Mar 2014 quarter. NPI is a weighted average of supply and valuesacross 11 cities in India. During the Jan-Mar 2014 quarter the city indexvalue was found to be in the range of minus 1 to plus 3 per cent.

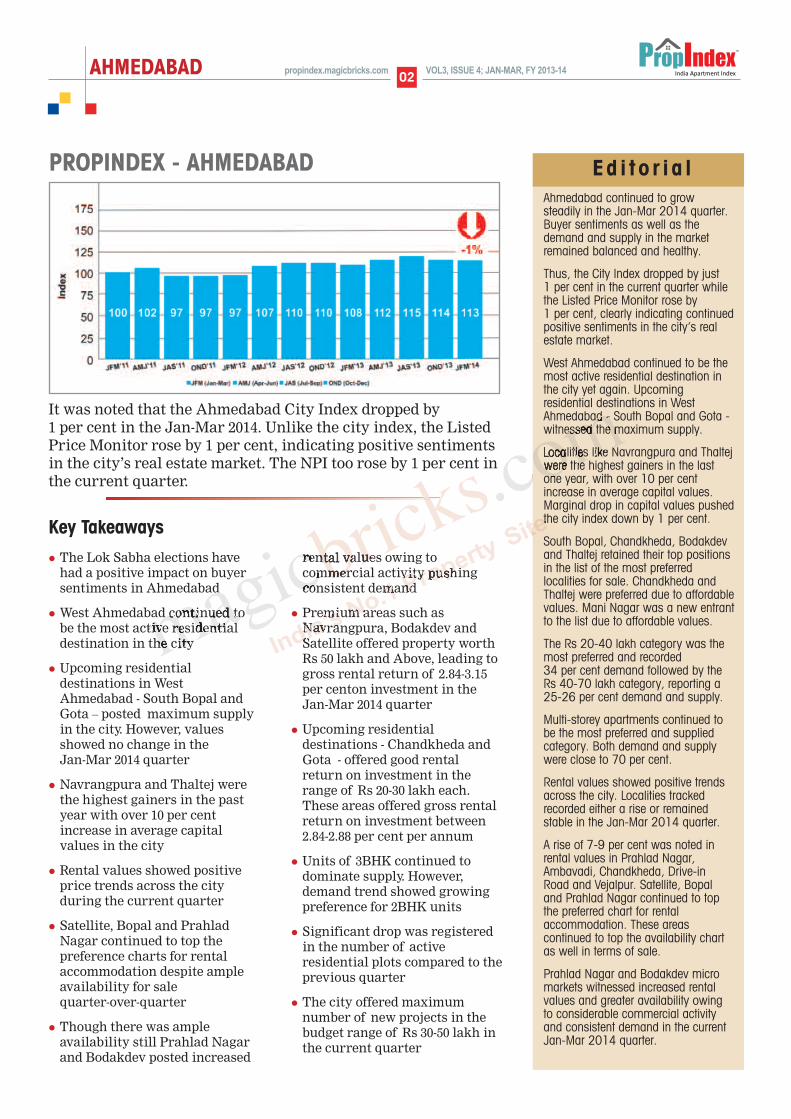

The Ahmedabad City Index droppedby 1 per cent in the Jan-Mar 2014quarter. Drop in values in over 35 per cent of the localities pusheddown the city index. The mostsupplied localities contributed to thisdrop. The Listed Price Monitor roseby 1 per cent. Marginal rise of 1-3 per cent in 35 per cent oflocalities held the Listed PriceMonitor.

n Capital markets across citieswere stable while rentalmarkets were active withconsiderable demand and risein values

n The preferred localities indifferent cities remainedunchanged since the Oct-Dec 2013 quarter

n Consumer demand slowly andsteadily moved towards themid-segment category. Demandinched up in the luxurycategory which remainedoversupplied.

JAN-MAR 2014

TOP YIELD GROSSERS

Gross yield is a ratio of average annualrental value to the average capital value ofthe property in the current quarter. Belowis the top yield-grossing locality in the city.

Locality Gross yield

Ahmedabad, Maninagar 4.22%

CAPITAL GAINS

It indicates the locality recorded maximumincrease in the capital value in the currentquarter.

Locality % Change

Ahmedabad, Navrangpura 3.64%

AHMEDABAD 02VOL3, ISSUE 4; JAN-MAR, FY 2013-14propindex.magicbricks.com

PROPINDEX - AHMEDABADAhmedabad continued to growsteadily in the Jan-Mar 2014 quarter.Buyer sentiments as well as thedemand and supply in the marketremained balanced and healthy.

Thus, the City Index dropped by just 1 per cent in the current quarter whilethe Listed Price Monitor rose by 1 per cent, clearly indicating continuedpositive sentiments in the city’s realestate market.

West Ahmedabad continued to be themost active residential destination inthe city yet again. Upcomingresidential destinations in WestAhmedabad - South Bopal and Gota -witnessed the maximum supply.

Localities like Navrangpura and Thaltejwere the highest gainers in the lastone year, with over 10 per centincrease in average capital values.Marginal drop in capital values pushedthe city index down by 1 per cent.

South Bopal, Chandkheda, Bodakdevand Thaltej retained their top positionsin the list of the most preferredlocalities for sale. Chandkheda andThaltej were preferred due to affordablevalues. Mani Nagar was a new entrantto the list due to affordable values.

The Rs 20-40 lakh category was themost preferred and recorded 34 per cent demand followed by theRs 40-70 lakh category, reporting a25-26 per cent demand and supply.

Multi-storey apartments continued tobe the most preferred and suppliedcategory. Both demand and supplywere close to 70 per cent.

Rental values showed positive trendsacross the city. Localities trackedrecorded either a rise or remainedstable in the Jan-Mar 2014 quarter.

A rise of 7-9 per cent was noted inrental values in Prahlad Nagar,Ambavadi, Chandkheda, Drive-inRoad and Vejalpur. Satellite, Bopaland Prahlad Nagar continued to topthe preferred chart for rentalaccommodation. These areascontinued to top the availability chartas well in terms of sale.

Prahlad Nagar and Bodakdev micromarkets witnessed increased rentalvalues and greater availability owingto considerable commercial activityand consistent demand in the currentJan-Mar 2014 quarter.

It was noted that the Ahmedabad City Index dropped by 1 per cent in the Jan-Mar 2014. Unlike the city index, the ListedPrice Monitor rose by 1 per cent, indicating positive sentimentsin the city’s real estate market. The NPI too rose by 1 per cent inthe current quarter.

l The Lok Sabha elections havehad a positive impact on buyersentiments in Ahmedabad

l West Ahmedabad continued tobe the most active residentialdestination in the city

l Upcoming residentialdestinations in WestAhmedabad - South Bopal andGota – posted maximum supplyin the city. However, valuesshowed no change in the Jan-Mar 2014 quarter

l Navrangpura and Thaltej werethe highest gainers in the pastyear with over 10 per centincrease in average capitalvalues in the city

l Rental values showed positiveprice trends across the cityduring the current quarter

l Satellite, Bopal and PrahladNagar continued to top thepreference charts for rentalaccommodation despite ampleavailability for sale quarter-over-quarter

l Though there was ampleavailability still Prahlad Nagarand Bodakdev posted increased

rental values owing tocommercial activity pushingconsistent demand

l Premium areas such asNavrangpura, Bodakdev andSatellite offered property worthRs 50 lakh and Above, leading togross rental return of 2.84-3.15per centon investment in theJan-Mar 2014 quarter

l Upcoming residentialdestinations - Chandkheda andGota - offered good rentalreturn on investment in therange of Rs 20-30 lakh each.These areas offered gross rentalreturn on investment between2.84-2.88 per cent per annum

l Units of 3BHK continued todominate supply. However,demand trend showed growingpreference for 2BHK units

l Significant drop was registeredin the number of activeresidential plots compared to theprevious quarter

l The city offered maximumnumber of new projects in thebudget range of Rs 30-50 lakh inthe current quarter

Key Takeaways

E d i t o r i a l

AHMEDABAD03VOL3, ISSUE 4; JAN-MAR, FY 2013-14 propindex.magicbricks.com

l Almost equal number of localities (approximately36%) witnessed a rise and drop in capital values inthe Jan-Mar 2014 quarter

l Drop of capital values in highly supplied localitiessuch as SG Highway pushed the city index down by 1 per cent

l SG Highway, SP Ring Road and Vaishno Devirecorded the highest drop of 4-5 per cent. In VaishnoDevi this may be attributed to a price correction inthe market as compared to the previous quarter.

l Navrangapura continued to do well. Capital valuesrose by almost 7 per cent in the locality in the pasttwo quarters

L I S T ED PR I CE MON I TOR

Locality Average Rental Average Capital Gross

Value (Rs/sqft/mth) Value (Rs/sqft) Yield

Motera 6.00 3,000 2.40%

Satellite 13.25 5,050 3.15%

Prahlad Nagar 14.50 4,875 3.57%

Vastrapur 12.75 4,525 3.38%

Bodakdev 13.75 5,325 3.10%

Vejalpur 11.00 3,200 4.13%

Maninagar 11.00 3,125 4.22%

Gurukul 12.25 4,500 3.27%

Bopal 8.50 3,250 3.14%

Thaltej 11.25 4,925 2.74%

Y I E L D M E T E R

l The Magicbricks yield meter clocked returns inthe range of 2.40-4.40 per cent during the Jan-Mar 2014 quarter, way ahead of the 2.48-3.78per cent recorded in the previous quarter

l Maninagar recorded the highest rental yield thisquarter, followed by Vejalpur at 4.13 per cent, thehighest grosser of the previous quarter

l A healthy rental return of 3.80-3.57 per cent wasregistered in localities such as Prahlad Nagar andVastrapur. These localities have been performingconsistently since the last few quarters, as far asrental yield is concerned

l Motera recorded the lowest yield at 2.40 during theJan-Mar 2014 quarter

RENT MON I TOR

l As opposed to the capital market, the rental marketwas more robust, with all tracked localitiesrecording either a rise or stable values in the Jan-Mar 2014 quarter

l A rise of 7-9 per cent was noted in rental values inPrahlad Nagar, Ambavadi, Chandkheda, Drive-inRoad and Vejalpur. Regularly rising capital valuesshifted the focus of buyers to rented properties

l SG Highway, Satellite and South Bopal alsorecorded a rise of 6 per cent each on the back ofavailable properties and affordable values

l Gota and Thaltej recorded stable rental valuesduring the current quarter

1%

AHMEDABAD 04VOL3, ISSUE 4; JAN-MAR, FY 2013-14propindex.magicbricks.com

Growth Number of Localities with Most ActiveCorridor Projects Maximum Property

Residential Projects Typology(Multi-storey)*

SG Highway 19 SG Highway, Gota, Prahlad 83%Nagar and Extension

SP Ring Road, West 10 Bopal and South Bopal Over 90%

SP Ring Road, North 6 Chandkheda, Tragad and Over 90%Vaishnu Devi

Central 3 CG Road and Navarangpura Over 90%

*Percentage of total supply

RENT

Locality Rental RankValues Q4 Q3

Satellite 12000 to15500 1 1

Bopal 7500 to 10000 2 2

Prahlad Nagar 13000 to17000 3 3

Bodakdev 12500 to 16000 4 4

Thaltej 10000 to13500 5 7

Vejalpur 10000 to 13000 6 8

Paldi 11000 to 14000 7 6

South Bopal 8000 to 11000 8 -

Vastrapur 11500 to 15000 9 5

Gurukul 11000 to 14000 10 -

Note: Q4 Jan-Mar 2014, Q3 Oct-Dec 2013

Locality Capital RankValues Q4 Q3

Bopal 2950 to 3750 1 2

Satellite 4600 to 5850 2 1

SG Highway 2950 to 3850 3 6

South Bopal 3050 to 3650 4 4

Prahlad Nagar 4300 to 5900 5 3

Gota 2600 to 3000 6 5

Bodakdev 4850 to 6150 7 7

Chandkheda 2300 to 2850 8 8

Thaltej 4500 to 5700 9 9

Mani Nagar 2900 to 3500 10 -

SALE

Note: Q4 Jan-Mar 2014, Q3 Oct-Dec 2013

PREFERRED LOCALITIES

l As compared to the previous quarter, there havebeen some significant changes in the top three spotsof the list of preferred locations for sale in the cityin the current quarter

l Affordability has pushed Bopal to the top of the listdisplacing Satellite, which was at number two

l SG Highway moved up three positions to settle atnumber three. Its popularity continued due to thecommercial set-ups and availability of both ready-to-move-in and under-construction properties ataffordable prices

l South Bopal, Chandkheda, Bodakdev and Thaltejretained their positions on the list of the preferredlocations for sale. Chandkheda and Thaltej werepreferred due to affordable values

l Mani Nagar was a new entrant in the list ofpreferred localities as compared to the previousquarter. Relatively affordable capital values may bethe reason for this preference in the current Jan-Mar 2014 quarter

l Top four positions remained unchanged in the list ofpreferred localities on rent

l Satellite, Bopal, Prahlad Nagar and Bodakdev werethe top four locations in that order

l While affordability pulled buyers towards Bopal,commercial set-ups in Prahlad Nagar ensuredcontinued rental demand

l Vejalpur moved up two positions to settle at thesixth position. The locality has been recordingrising rental values since the last two quarters.Proximity to the commercial hub of Prahlad Nagarand connectivity made it a preferred rental option

l South Bopal was a new entrant in the list thisquarter. Proximity to corporate offices and lowerrental values as compared to Satellite, PrahladNagar and Bodakdev made South Bopal popular

l Gurukul was the new entrant in the list of top tenlocalities for rent. The locality has several newprojects that have enhanced rental demand

Above 40% 30-40% 10-20% 5-10% Less than 5%

AHMEDABAD05VOL3, ISSUE 4; JAN-MAR, FY 2013-14 propindex.magicbricks.com

With major infrastructural development witnessed, Ahmedabad, the modern cityof the state of Gujarat, aims to provide housing for all segments of the society.Also, the Sabarmati River Front Development Project has pushed up theproperty values in many localities in the city.

How Sabarmati’s new avatar boosted realty valuesThe development of Ahmedabad’s Sabarmati River is a remarkable example of how ariver can be made pollution-free, re-developed, maintained and impact real estate. Sincethe inception of the project, an initiative by the AMC, values in localities facing theriver such as Paldi, Ellis Bridge and Ashram Road have appreciated by almost 30-40 percent within 3-4 years. The hike in the Floor Space Index (FSI) from 1.8 to 5.4 along the 10-km stretch of the river has attracted several developers to redevelop these locations.

n Magicbricks.com Bureau

No need to pay full stamp duty on jantri rates in AhmedabadIn an important judgment, Gujarat high court on March 3, held that registration ofproperty cannot be made mandatory on payment of stamp duty according to the jantrirates only. Thus, paying 5 per cent stamp duty of the market rates as prejudged by theready reckoner, will not be the deterrent in registration of property deals. Jantri is thegovernment document which specifies the market rates of the land and construction.Stamp Duty is payable at the time of transfer agreement according to the Jantri Rates.

n The Times of India, Ahmedabad

R E A L T Y N E W S

To read full story and more news go to www.content.magicbricks.com

Approximately 40,000 residential units areavailable in and around the city. This stock ismarginally over supplied. With increasingurbanization, migration from other states/cities and increasing conversion of jointfamilies to nuclear families will ensure theoversupply will be absorbed in no time.Buyers should leave the wait-and-watchapproach and buy, as there would not be anyrevision in values.

Nilay PatelDirectorDeep Builders

E X P E R T S P E A KDeveloper

The property market in Ahmedabad is amongthe most attractive. It is a major hub of IT/ITeSand retail. Growth in the manufacturing andcommercial business enhances the potentialof the market. The city has consistentlywitnessed a 10–15 per cent appreciation invalues. Prime residential opportunities are inShahibaug, Bodakev, Satellite, Prahlad Nagar,Vastrapur, Thaltej, Maninagar and areasaround Kankaria and Chandola Lake.

Neeraj BansalDirectorKPMG India

Consultant

Mukesh VasaniCEO, City Estate Management

Q&A

How will the elections impact andchange the dynamics of the city?

This year is crucial because of electionsand FDI Policy. Government hasliberalized the FDI policy to attractinternational investors. Although resaleand rental deals will get least affected, big deals should be closed.

Which localities are you active in?

Entire Ahmedabad.

Which of these localities see maximumpossessions this year?

Ahmedabad West and South.

Who is delivering?

What is the buyers profile?

Are you getting enquiries from buyers?

How many are getting converted toactual transactions?

Of the total transaction only 25 per centget converted.

Which BHK segment is popular?

Which budget category is popular?

What type of property is in demand?

Any infrastructure project expected toimpact the real estate market in 2014?

Established New developers If bothdevelopers

Active agegroup

ActiveProfession

Regular No queriesNot veryfrequent

1 BHK 2 BHK 3 BHK 4 BHK &Above

<Rs 25 lakh

Rs 25-50 lakh

Rs 75-1crore

Above1 crore

Rs 50-75 lakh

Builder floor units PlotsApartment

Metro Civicamenities

Socialinfrastructure

Roads/flyover

NRI/locals

Villas

AHMEDABAD 06VOL3, ISSUE 4; JAN-MAR, FY 2013-14propindex.magicbricks.com

BHK Configuration - City Level

60

50

40

30

20

10

0

11 10

5049

31 32

8 9

(Oct-Dec 2013)

(Jan-Mar 2014)

Fig

ures

in p

erce

ntag

e(%

)

1BHK 2BHK 3BHK 4BHK &above

DEMAND SUPPLY

60

50

40

30

20

10

0

4 5

33 33

40 39

23 23

(Oct-Dec 2013)

(Jan-Mar 2014)

Fig

ures

in p

erce

ntag

e(%

)

1BHK 2BHK 3BHK 4BHK &above

Property wise Analysis - City Level

80

60

40

20

0

7671

2 2

1114

7 7

(Oct-Dec 2013)

(Jan-Mar 2014)

Fig

ures

in p

erce

ntag

e(%

)

Multistorey Single Residential Residential Villaapartment floor house plot

DEMAND

4 6

80

60

40

20

0

6669

6 5

13 11

7 8

(Oct-Dec 2013)

(Jan-Mar 2014)

Fig

ures

in p

erce

ntag

e(%

)

Multistorey Single Residential Residential Villaapartment floor house plot

SUPPLY

8 7

40

30

20

10

0<20 20-40 40-70 70-100 100 &

above

11

Fig

ures

in p

erce

ntag

e(%

)

Figures in Rs lakh

10

32 3431

26

12 1214

18

(Oct-Dec 2013)

(Jan-Mar 2014)

Budget wise Analysis - City Level

DEMAND

40

30

20

10

0<20 20-40 40-70 70-100 100 &

above

8

Fig

ures

in p

erce

ntag

e(%

)

Figures in Rs lakh

7

2022

26 25

14 14

32 32

(Oct-Dec 2013)

(Jan-Mar 2014)

SUPPLY

Budget wise Analysis

l The Rs 20-40 lakh budget categorywas preferred and recorded 34 per cent demand. However, itssupply remained at 22 per cent, thesecond highest after the Rs 40-70lakh category. The latter recorded25-26 per cent demand and supply

l The budget range of Rs 100 lakhand Above noted a considerabledemand of 18 per cent, 4 per centhigher than the previous quarter.This category reported anoversupply by 14 per cent

DEMAND - S UPP LY ANALYS I SThere was an oversupply of luxury properties worth Rs 70-100 lakh and Above. There was a largegap between the demand and supply of properties priced at Rs 1 crore and Above. Supply leddemand by 14 per cent in this category. On the other hand, the Rs 20-40 lakh range wasundersupplied with demand leading supply by 12 per cent.

Even though supply of apartments in the market inched up by 3 per cent, it fell short of theexisting demand by 2 per cent. There was a significant lack of 16 per cent in the supply of 2BHKapartments, the most preferred category. Highest supply was noted for the 3BHK units, with anexcess of 7 per cent in the current quarter.

Property wise Analysis

l Multi-storey apartments continuedto be the preferred and suppliedcategory. Its demand dropped by 5 per cent and supply went up by 3 per cent in the Jan-Mar 2014quarter. Both demand and supplywere close to 70 per cent.

l Demand for independent houseswent up by 3 per cent and reached14 per cent in the current quarter.Its supply dropped by 2 per centand reached 11 per cent.

BHK wise Analysis - City Level

l While 2BHK units recorded thehighest demand by close to 50 per cent buyers, its supply fellshort by 16 per cent.

l Larger homes of 3 and 4BHK andAbove recorded a consolidateddemand of 41 per cent. There wasan oversupply of these units by 21 per cent. The mismatch wasmost visible in the 4BHK andAbove category with demand at 9 per cent and supply at 23 per cent.

CAPITAL VALUES – LOCALITY WISE

Average Listed Residential Apartment Prices

Ambavadi 4800 to 6000

Ambli 5050 to 6000

Anand Nagar 4050 to 5300

Bodakdev 4850 to 6150

Bopal 2950 to 3750

CG Road 5150 to 6100

Chandkheda 2300 to 2850

Chandlodia 2650 to 3150

Drive In road 4650 to 6050

Ghatlodia 3100 to 3800

Ghuma 2550 to 3000

Gota 2600 to 3000

Gurukul 4050 to 5300

Hathijan 1850 to 1850

Jivraj Park 2750 to 3500

Jodhpurgam 4850 to 6050

Jodhpur Village 4550 to 5750

Koteshwar 2850 to 3300

Makarba Road 3300 to 3750

Maninagar 2900 to 3500

Motera 2750 to 3450

Naranpura 4150 to 5350

Naroda 1700 to 1950

Narol 1650 to 1850

Navrangpura 5200 to 6600

Nehru Nagar 5200 to 5800

New CG Road 2600 to 3050

New Ranip 2350 to 2650

Nikol 1750 to 2050

Paldi 4600 to 5650

Prahlad Nagar 4300 to 5900

Prahlad Nagar Extension 3400 to 3850

Ramdev Nagar 4500 to 5500

SP Ring Road 2850 to 3400

Satellite 4600 to 5850

Sattadhar 3500 to 4250

Science City 3800 to 4500

SG Highway 2950 to 3850

Shilaj 2750 to 3400

Sola 3750 to 4400

South Bopal 3050 to 3650

Thaltej 4500 to 5700

Tragad 2200 to 2450

Vaishno Devi 2850 to 3300

Vasna 2800 to 3500

Vastrapur 4200 to 5150

Vastral 1600 to 2050

Vejalpur 2950 to 3600

Locality Capital Values (Rs/Sq feet)

Locality Capital Values (Rs/Sq feet)

AHMEDABAD

AHMEDABAD07VOL3, ISSUE 4; JAN-MAR, FY 2013-14 propindex.magicbricks.com

VOL3, ISSUE 4; JAN-MAR, FY 2013-14 propindex.magicbricks.com

D I S C L A I M E REvery effort has been made to make this Index as complete and as accurate as possible. MagicBricksaccepts no responsibility for inaccuracies in the information/data contained in this book. It shall haveneither liability nor responsibility to any person or entity with respect to any loss or damage caused, oralleged to have been caused, directly or indirectly, by the information contained in this book. Theinformation/data in this book is subject to change from time to time due to market condition.

CONTACT US

l Post your feedback to -

propindex @timesgroup.com

l Join our discussion forum at -

openhouse.magicbricks.com

l For business enquiries -

PROPINDEX TEAM

l Content & Research: E Jayashree Kurup,

Dipti Tandon, Subodh Kumar, Rishab Jain,

Kanchana Dwarkanath, Sruthi Kailas,

Shradha Goyal, Neha Nagpal, Bhawna Mongia,

Renu Arya, Aradhana Mozumdar, Girish Bindal,

Puneet Kukreja & Bikash Kumar.

l Layout Design: Harsha Khattar

l Cover Page Design: Raghav Krishnan &

Rahul Nair