agrifin webinar date: july 15, 2015 · safl is currently offering 10 main products to the...

TRANSCRIPT

Sustainable Agro-commercial Finance Limited

AgriFin Webinar Date: July 15, 2015

Indian Agriculture Scenario

Population - 7% of the world ( growing at the rate of 2% per annum)

Land - 2.4% (with 43.0 % under cultivation and less than 21.0% under

irrigation )

Water Sources – Only 4% of the world (monsoon dependent).

Precipitation pattern - Uneven and Erratic.

70% of water is used in Irrigation (major water consuming sector)

Thus we need technological intervention to intervene into the

- water - food - energy security nexus….

• And Finance

2

Why Modern Irrigation Technologies?

The productivity of irrigated land is low compared to its potential.

The productivity per unit water is very low.

Water available for irrigation is becoming scarcer.

Micro Irrigation will increase the irrigation cover using the existingavailable water.

Micro-irrigation with fertigation will enhance production per unit inputin nutrient poor soils.

3

Challenge

Declining water resources and acute power shortage and Competitive

demand for land

Solutions

Precision farming with Micro Irrigation that conserves water and power

Result

Innovative crop cultivation packages ensuring high productivity per unit

input.

4

Payback period

CropsYield (MT/Ha)

Incremental QtyIncremental

income

Approx.

Cost of

DripConventional Drip

Sugarcane 128 170 42 84,000 1,00,000

Cotton 2.6 3.7 1.1 44,000 1,00,000

Grapes 26.4 32.5 6.1 91,500 1,00,000

Potato 23.6 34.4 10.85 86,800 1,00,000

Banana 57.5 87.5 30 3,00,000 87,000

Tomato 32 48 16 48,000 1,00,000

Sweet lime 100 150 50 3,00,000 55,000

Watermelon 24 45 21 2,10,000 87,000

Incremental income is sufficient for the farmer to repay a loan for installingdrip irrigation either after 1st harvest or at most 2 harvests.

5

• Jain Irrigation Systems Ltd. (JISL) has a multi productindustrial profile aimed at the Farmer communityspread largely in the rural and semi-urban areas inIndia.

• World number one in Drip Irrigation with PipeProduction

• World number one in Tissue culture Banana PlantProduction

• Engaged extensively in Tissue Culture, Hybrid &Grafted Plants

• Pioneer of Micro Irrigation Systems in India

• Globally second and the largest irrigation Companyin India.

• The largest manufacturer of PVC & PC sheets in Indiaand globally among the first 5 Companies

Jain Irrigation Systems Ltd

6

SAFL is a NBFC promoted by Jain Irrigation Systems Limited (JISL). IFC, Washington is the

first and anchor investor in the Company with 10% holding. Recently, Mandala Capital

Ltd an agri business focused private equity fund has invested in SAFL to the extent of

20% of the total equity holding of Rs.1200 million.(US $ 20 mn)

SAFL is exclusively focused on Farm & Farmer

SAFL is the first private sector NBFC in India providing only agri- loans with a wide and

diverse range of financing options for almost every need of agricultural activity.

About SAFL

7

• Farmer Empowerment

• Increased Agricultural Production

• Rural Prosperity & Inclusive Growth

Objectives of SAFL

8

Sustainable Agro-commercial Finance Ltd. (SAFL) has been accorded a Certificate ofRegistration by RBI to function as a Non Banking Finance Company (NBFC) in July2012.

SAFL currently has its Head Office in Mumbai, 4 Zonal Offices, 24 Branches & 19Satellite Offices in Maharashtra state.

In addition, SAFL is operating at 6 locations in Karnataka state and 1 location inTelangana state.

The distribution network thus comprises 54 offices excluding HO.

SAFL is currently offering 10 main products to the agriculture community

SAFL’s website is www.safl.in

An Overview

9

INDIA

10

Location of Branches in Maharashtra State

Branch /Zonal Offices - 28

Satellite Offices -19

• Total Offices (Excluding HO) - 47

• New Locations other than Maharashtra - 7

11

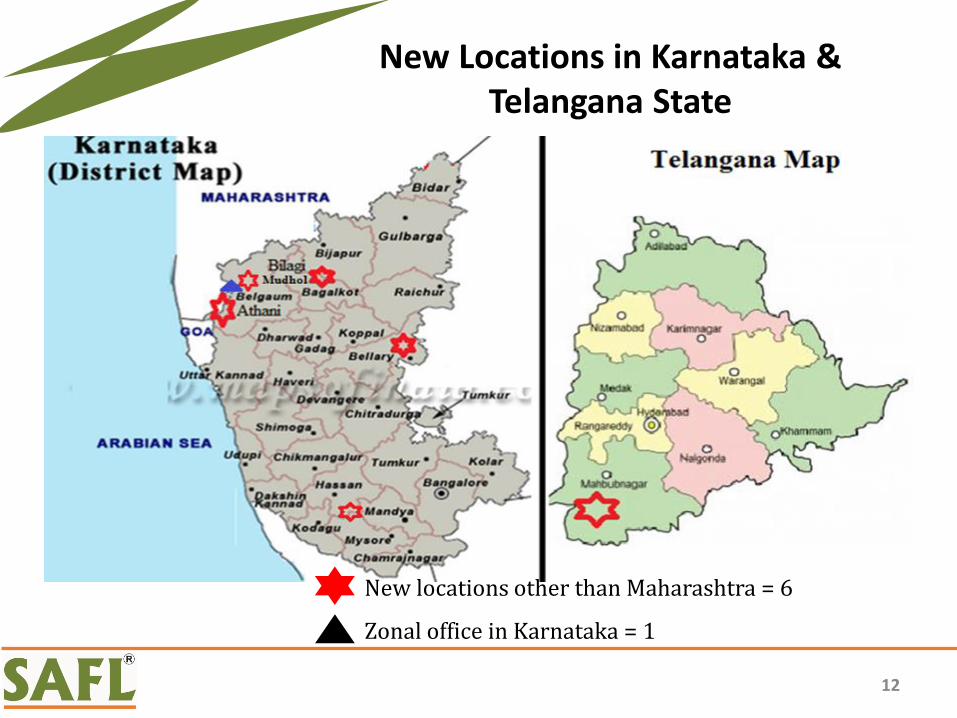

New Locations in Karnataka & Telangana State

New locations other than Maharashtra = 6

Zonal office in Karnataka = 1

12

SAFL has started business operations effectively in April 2013 and has begunits financing activity in the state of Maharashtra, to begin with as Phase I.

Phase II will expand operations of SAFL in the states of Karnataka, AndhraPradesh and Madhya Pradesh. It has started business operations in the stateof Karnataka, Andhra Pradesh & Telangana in current FY 2014-15

Phase III will further expand business operations in the states of Gujarat,Tamilnadu, Rajasthan and Haryana. This will occur in FY 2016-17

SAFL will have around 250 offices in India in 5 years’ time.

An Overview

13

• During FY 2014-15, SAFL has successfully raised funds of Rs 1120 million(approx. US $ 18.50 mn) by way of equity at premium and debt from anoverseas PE Investor by the name of Mandala Capital Ltd.(Mandala).

• Mandala has invested Rs 240 million (US $ 4 mn) in SAFL’s capital with a sharepremium of Rs 180 million (US $ 3 mn)

• In addition to the equity subscription mentioned above, Mandala hasextended an additional Rs 700 million (US $ 11.50 mn) to SAFL by way of Non-Convertible Debentures (NCD) without any security. These NCDs are for aperiod of 75 months to be repaid as a bullet payment after 75 months withhalf yearly interest payment at rate of 10% p.a.

• Paid up, Issued and Subscribed Capital: Rs. 1200 million (US $ 20 mn)

Raising of funds

14

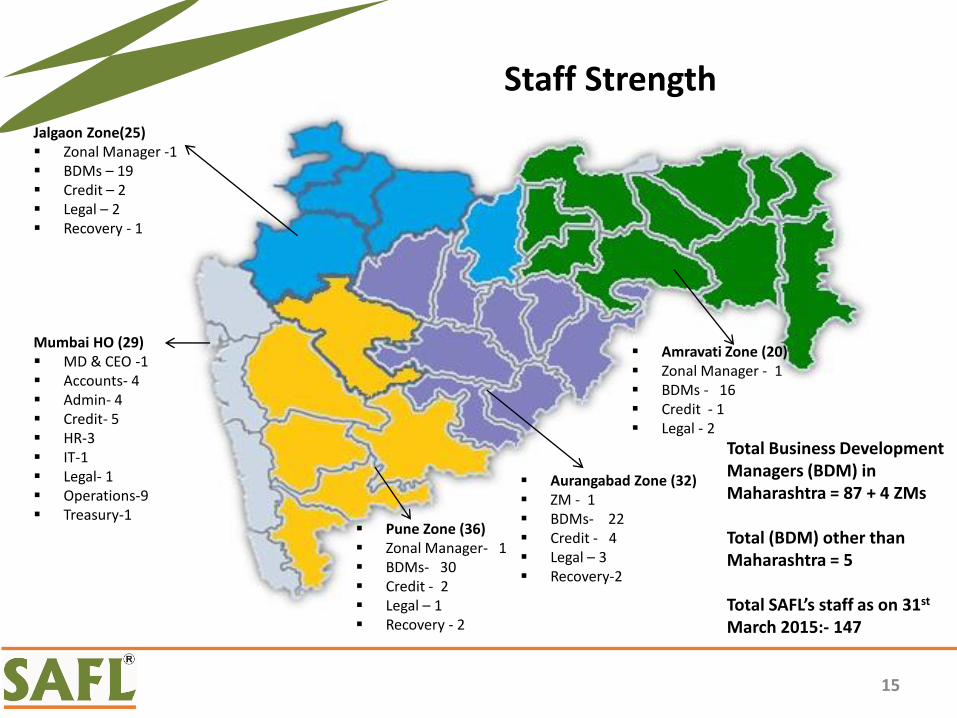

Pune Zone (36) Zonal Manager- 1 BDMs- 30 Credit - 2 Legal – 1 Recovery - 2

Aurangabad Zone (32) ZM - 1 BDMs- 22 Credit - 4 Legal – 3 Recovery-2

Jalgaon Zone(25) Zonal Manager -1 BDMs – 19 Credit – 2 Legal – 2 Recovery - 1

Amravati Zone (20) Zonal Manager - 1 BDMs - 16 Credit - 1 Legal - 2

Mumbai HO (29) MD & CEO -1 Accounts- 4 Admin- 4 Credit- 5 HR-3 IT-1 Legal- 1 Operations-9 Treasury-1

Total Business Development Managers (BDM) in Maharashtra = 87 + 4 ZMs

Total (BDM) other than Maharashtra = 5

Total SAFL’s staff as on 31st

March 2015:- 147

Staff Strength

15

1. Micro Irrigation System Financing

2. Farm equipment financing

3. Contract Farming Finance

4. Agri Projects Financing

5. Agri-business Financing

6. Financing Pipes & or motors / pumps for lift irrigation

7. Dairy Loan Cattle, Equipments & Sheds

8. Solar Module Financing

9. Financing Agro based Industry viz; Ginning mills, Jaggery Unit,

food processing unit like fruit juice, Tomato Sauce etc.

10. Short Term Crop Loan

Financing offered by SAFL

16

Financing offered by SAFL

• Micro Irrigation System Financing

• This product is offered to farmers who are in need offinancing for purchase / installation of MIS in their farms.The tenor applicable is usually 3 years but can go upto 5years depending upon crop harvesting period (e.g.pomegranate , mango plantations).

• Farm Equipment financing

• This product is offered to farmers who are desirous ofbuying farm equipment and require financing for thesame. These would include tillers, pneumatic ploughs, de-weeders, rotavators, harrows, threshers, harvesters etc.The tenure and other product features will vary on thebasis of crop; however maximum tenor for this productwill be 60 months.

17

Financing offered by SAFL

• Contract Farming Finance

• This product is offered to farmers who have tie-ups withthird party to sell their produce and they are in need ofCredit for installation of MIS. The third party willordinarily guarantee repayment of loan out of agricultureproduce supplied by the farmer to the third party.Acceptance of third party’s financial credentials will be inconformity with SAFL's pre-determined criteria.

• Agri Projects Financing

• Agriculture Project Loans are offered to farmers havingstrong credit record for a maximum period of 5 years tofinance expenses related to farm infra development.Activities that are covered under Agri Projectdevelopment include land development, farm ponds, PolyHouses / Green Houses, Nursery, Fruit Orchards and suchothers.

18

Financing offered by SAFL

• Agri-business Financing

• This product is offered to existing client / farmers /dealers to meet working capital requirements arising outof small and allied businesses. Generally, such type ofloan is provided for a maximum period of 3 years andrenewed annually on the basis of satisfactory conduct.

• Financing Pipes & or motors / pumps for lift irrigation

• This product is offered to farmers who have minimum of5 acres of land holding and are desirous of installingpipeline for lifting water for their farms and requirefinancing for the same. Components include motors,pumps, pipeline, excavation and installation costs. Thetenure is generally 5 years .

19

Financing offered by SAFL

• Dairy Loan Cattle, Equipments & Sheds

• A medium to long term loan facility to finance expensesrelated to setting up of dairy project which would includepurchase of buffalos / cows / chap cutter / milkingmachine / shed etc.

• Solar Module Financing

• This product is offered to clients for purchase of solarequipment. The objective of this product is to encouragefarmers / individuals to invest and utilize renewablesources of energy by providing credit facility in a hasslefree manner and at reasonable terms. The usual tenor is24 to 60 months depending upon the equipment that isfinanced. Products include solar pumps, solar waterheaters, solar lighting appliances.

20

Financing offered by SAFL

• Financing Agro based Industry

• This product is offered to businesses which requireMedium term loan for capital investment or for Shortterm working capital purpose. Tenure will range between1 years to 3 years. Businesses include cotton ginning mills,Jaggery units, fruit processing and such others.

• Short Term Crop Loan

• is offered as package bundled with other products suchas MIS / Lift Irrigation / Agri Project Finance for existingborrowers for meeting immediate needs for workingcapital of new crops.

21

Customer Profile

High End Farmers

Medium End Farmers

Small Farmers

Marginal Farmers

Leasehold Land Tillers

SAFL

22

Customer Profile

Social Status / Characteristics

Leasehold Land Tillers

Marginal Farmer

Small FarmerMedium EndFarmers

Higher End Farmers

Average LandHolding

1 acre to 5 acres

1 Acres to 2.5 Acres

2.5 Acres to 5 Acres

5 Acres to 10 Acres

> 10 Acres

Annual Family Income

< 1,00,000 < 1,50,000 < 3,00,000 < 6,00,000 > 6,00,000

Repayment Tenure

Linked to harvesting

cycle

Linked to Harvesting

Cycle

Linked to Harvesting

Cycle

Linked to Harvesting

Cycle

Linked to Harvesting

Cycle

SAFL’s customer segment are all individual farmers who are capital starved and need financialassistance for capital investment in their agriculture holding

23

Sourcing of business

• Jain Irrigation has more than 1500 Dealers across Maharashtra state and over 5000 dealers

pan India. SAFL also uses the same Dealer network to source clients for its loan products.

Thus, most loan proposals originate from Jain Irrigation dealers’ end. This piggy backing on

Jain Irrigation’s dealer network facilitates deep penetration minus the distribution cost to

SAFL

• Apart from the above, SAFL’s business development officers differentiate potential villages on

the basis of various parameters such as crops grown, track record of farmers, availability of

irrigation facility, land holding of the farmers and accordingly have been organizing farmer

meetings and informing them about various products offered by SAFL.

• SAFL also organizes camps during a local festival in the villages to impart information and

knowledge about the products offered by SAFL.

24

Typical Process Flow For Financing Drip Irrigation

1. Jain irrigation’s dealer finalises choice of drip irrigation system with farmerincluding design and components with farmer. He enquires if the farmer needsfinancing for the same. Most small and marginal farmers need financialassistance.

2. Competitors are banks, co-operative societies & money lenders. The dealerpoints to SAFL as a good, quick turnaround, hassle free and competitive pricingagency. The dealer offers all assistance to farmer to complete requirements ofSAFL.

3. The farmer submits the application form along with land holding documents andKYC documents. The application form provides for information about personaldetails, land details, family particulars, borrowings, assets, etc.

4. These are handed over by dealer to Business Development Manager (BDM) ofSAFL - i.e. the Relationship Manager.

25

Typical Process Flow For Financing Drip Irrigation

5. The BDM will carry out a field visit and validate KYC details. He will also verifyirrigation source, crop details, standard of living, repayment track record etc.

6. If the loan proposal meets with pre-determined eligibility criteria, only then willthe BDM submit above mentioned information and Field Inspection Report (FIR)along with documents to Credit Dept. at Zonal office along with hisrecommendations.

7. Credit verifies the information contained in the FIR and accompanyingdocuments. Credit also verifies CIBIL (credit information bureau) records to findout loan repayment record. Credit carries out detailed appraisal as per scoringmodel including rating of the customer, find income levels (pre loan and postloan) to find out capacity towards repayment etc.

26

Typical Process Flow For Financing Drip Irrigation

8. Credit either sanctions / rejects the proposal. If sanctioned, Credit issues a sanction letter. The sanction letter is mailed to the BDM who hands it over to the farmer. A copy of the sanction letter also goes to Legal Dept. in zonal office.

9. Legal Dept. prepares the legal documents by filling in all particulars and mails them to BDM to take a print out and execute the same.

10. After execution of legal documents, documents are sent to Legal Dept. for vetting.

11. After vetting legal documents by Legal Dept., and if all documents are in order, Operation department will disburse the loan.

12. In addition to the BDMs, collections and recoveries are carried out by a dedicated “Debt Collection ” team at select locations.

27

Process Flow – A Summary

Dealers provides application forms

and information of SAFL’s product to

the customers

Receipt of complete Application form

and other documents by

dealers / SAFL’s Branch staff

Verify whether it satisfy minimum

criteria

Verification by Branch staff with

the due diligence / Personal discussion

/ FIR

Appraisal / Sanction by Zonal Credit / appropriate

sanctioning authority.

Issuance of Legal documents on the basis of sanctioned

terms

Execution of Legal documents in line with

the sanctions

Process for disbursement and verification of Legal

documents as stipulated in sanction

Upon confirmation from Legal, Operations

disburses the loan amount and intimate

the customer

Compliance of Post disbursal documents

28

Approach to Credit Decision

Borrower Characteristics

Crop Characteristics

Credit Score Factor

Transactional & Financial

Characteristics

29

Credit Rating

• Credit rating model is designed on the basis of quantitative as well asqualitative parameters. Some of them are:-– Borrower Characteristics

• Age of the Applicant• Annual Family income• Year on year growth in income• Land holding• Farming practice• Total loan installment to total income

– Crop Characteristics• Type of Crop with appropriate region• Availability of Minimum support price• Cropping pattern• Potential increase in yield after using MIS

– Transaction and Financial Characteristics• Loan to Valuation of land• Tenure of loan• Guarantor type• CIBIL score

30

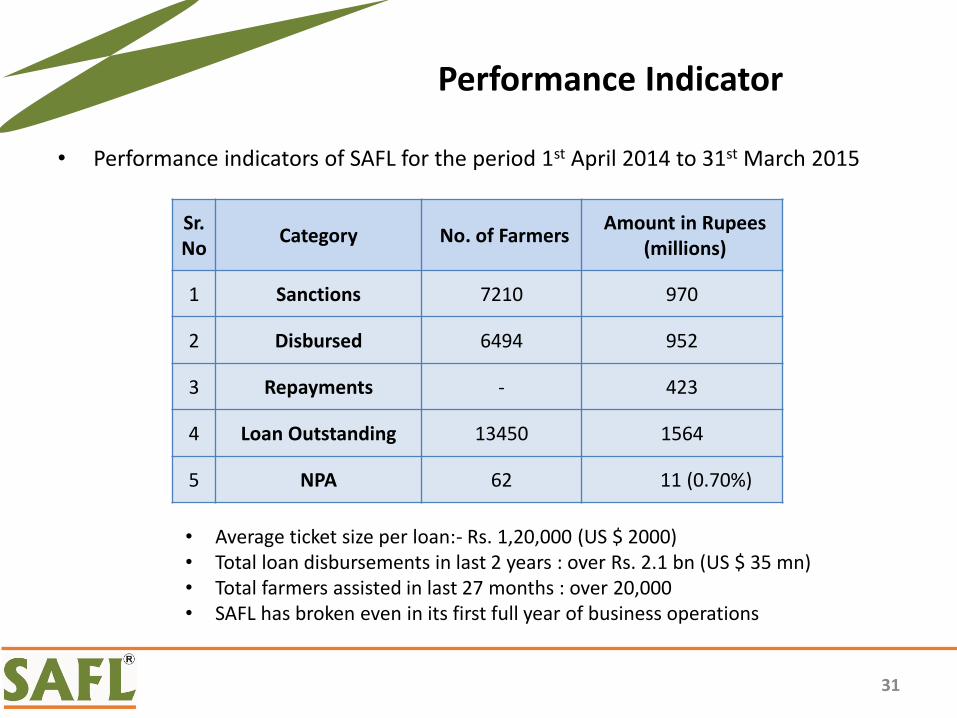

• Performance indicators of SAFL for the period 1st April 2014 to 31st March 2015

Performance Indicator

Sr. No

Category No. of FarmersAmount in Rupees

(millions)

1 Sanctions 7210 970

2 Disbursed 6494 952

3 Repayments - 423

4 Loan Outstanding 13450 1564

5 NPA 62 11 (0.70%)

31

• Average ticket size per loan:- Rs. 1,20,000 (US $ 2000)• Total loan disbursements in last 2 years : over Rs. 2.1 bn (US $ 35 mn)• Total farmers assisted in last 27 months : over 20,000• SAFL has broken even in its first full year of business operations

• SAFL operates on cost plus basis.

• SAFL follows hub & spoke model, where Satellite offices must breakeven in 1st year after achieving business of Rs. 30 Mn and areconverted into Branch office.

• Branch offices after achieving business of Rs. 100 Mn are convertedinto sub-zonal office.

Cost

32

►Strengths

– Easy & Fast appraisal and disbursement based on pre-determined parameters and

a credit scoring system. Usage of latest technologies for processing, sanctioning

and disbursing loans to farmers. Strong and stable dealer network of Jain Irrigation

Systems Ltd. (JISL) which has presence in remote topographies

– Offer end to end solution to farmers from sale of JISL’s product to offering of loans

under one roof.

►Weakness– Access to operating capital.

SWOT Analysis

33

►Opportunity

– Small and marginal farmers who constitute more than 80 per cent of total farmer

households in the country face exclusion from the formal financial channels.

– First entrant in the NBFC channel to provide gamut of agri finance.

►Threat

– Downturn in the economy due to low rain fall will have serious impact on thebusiness of SAFL.

– Competition from existing Banking / Rural banking channels providing loan at lowerinterest rate.

– Increase in defaults of agriculture loans in India.

SWOT Analysis

34

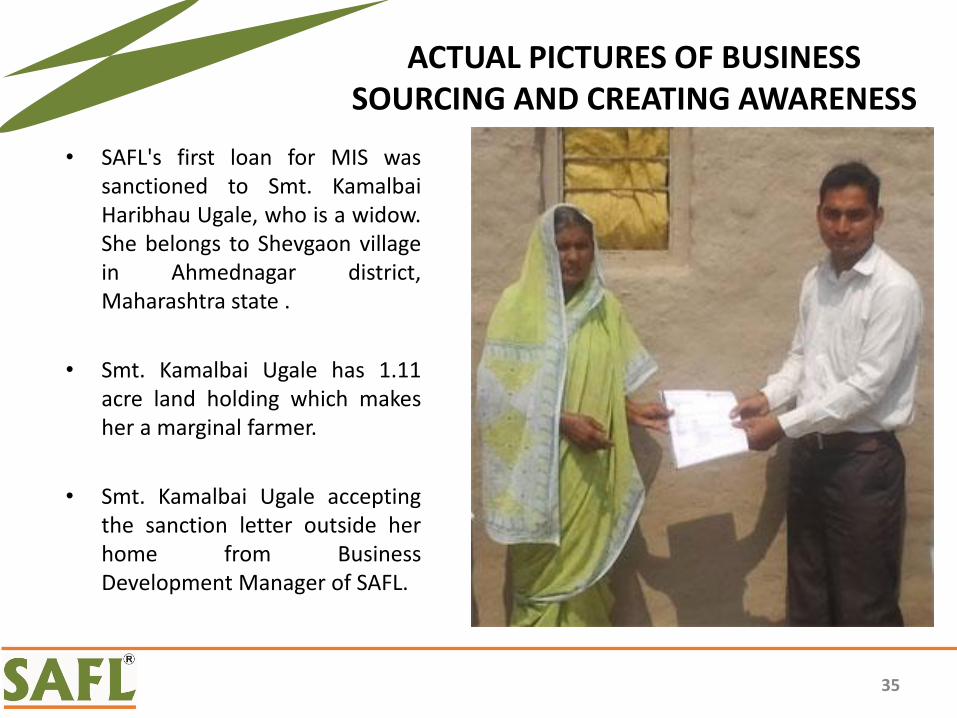

• SAFL's first loan for MIS wassanctioned to Smt. KamalbaiHaribhau Ugale, who is a widow.She belongs to Shevgaon villagein Ahmednagar district,Maharashtra state .

• Smt. Kamalbai Ugale has 1.11acre land holding which makesher a marginal farmer.

• Smt. Kamalbai Ugale acceptingthe sanction letter outside herhome from BusinessDevelopment Manager of SAFL.

ACTUAL PICTURES OF BUSINESS SOURCING AND CREATING AWARENESS

35

Farmer meetings are arrangedregularly across Maharashtra tocreate awareness about SAFL’sproducts and processes. JainIrrigation’s Dealers acts as First Pointof Contact for SAFL’s products.

Farmers are made aware of presanction and post sanctiondocuments that is required to besubmitted as well as regarding Rateof interest offered by SAFL fordifferent products.

Farmers are also informed about therepercussion of non payment of dues.

ACTUAL PICTURES OF BUSINESS SOURCING AND CREATING AWARENESS

36

Farmer meetings

37

SAFL Officers on field

38

SAFL Family

39

• TO GROW SAFL INTO A BANK WHICH WOULD BE ONE OF ITS KIND, CATERING TO THE FULL GAMUT OF BANKING SERVICES TO FARMERS ALL OVER INDIA

• - IN SUM- A UNIQUE INSTITUTION FOCUSSED ON FINANCING AGRICULTURE IN INDIA

THE FUTURE VISION

40