agriculture and rural development discussion...

TRANSCRIPT

The World Bank

Agriculture and Rural Development Discussion Paper

The Challenge of Compliance with SPS and Other Standards Associated with the Export of Shrimp and Selected Fresh Produce Items to the United States Market

John E. Lamb Julian A. Velez Robert W. Barclay

2

First printing or web posting: 2005 © 2004 The International Bank for Reconstruction and Development/The World Bank 1818 H Street, NW Washington, DC 20433 Telephone 202-473-1000 Internet www.worldbank.org E-mail [email protected] All rights reserved. Agriculture and Rural Development Discussion Papers is an informal series produced by the Agriculture and Rural Development Department of the World Bank. These papers raise concepts and issues for discussion in the broader development community and describe ongoing research and/or implementation experiences from the Bank. The findings, interpretations, and conclusions expressed herein are those of the author(s) and do not necessarily reflect the views of the Board of Executive Directors of the World Bank, the governments they represent, or the organizations of contributing authors. The World Bank does not guarantee the accuracy of the data included in this work. Rights and Permissions The material in this work is copyrighted. Copying and/or transmitting portions or all of this work without permission may be a violation of applicable law. The World Bank encourages dissemination of its work and will normally grant permission promptly. For permission to photocopy or reprint any part of this work, please send a request with complete information to the Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers, MA 01923, USA, telephone 978-750-8400, fax 978-750-4470, www.copyright.com. All other queries on rights and licenses, including subsidiary rights, should be addressed to the Office of the Publisher, World Bank, 1818 H Street NW, Washington, DC 20433, USA, fax 202-522-2422, e-mail [email protected].

3

Contents

Foreword v Acronyms vi Introduction 1 1. Food Consumption and Import Trends 3 Per Capita Consumption for Selected Categories 3 Role of Imports in U.S. Food Supply 3 Seafood Imports: Spotlight on Shrimp 9 Fresh Produce Imports: Spotlight on Selected Fruits and Vegetables 11 2. Standards Applicable to Imported Food

18

Definitions 18 Purposes 18 Tangible vs. Intangible Standards 18 Degree of Voluntarism 18 Types of Standards 19 Areas of Application in Food and Agriculture 20 3. Coping with Shrimp Standards

24

Standards Applicable to Shrimp 24 Compliance Issues 28 Direct Cost Implications of Compliance Issues for Shrimp 31 4. Coping with Standards for Fresh Fruit and Vegetables

34

Standards Applicable to Fresh Produce 34 Compliance Issues for Selected Fresh Produce Categories 41 Direct Cost of Compliance Issues in Selected Produce Categories 47 5. Other Costs Associated with Compliance with Emerging Standards

50

Additional Costs of Noncompliance 50 Industry Perceptions Concerning Costs of Noncompliance 51 Strategies for Dealing with Risks Associated with Noncompliance 51 6. Conclusions

54

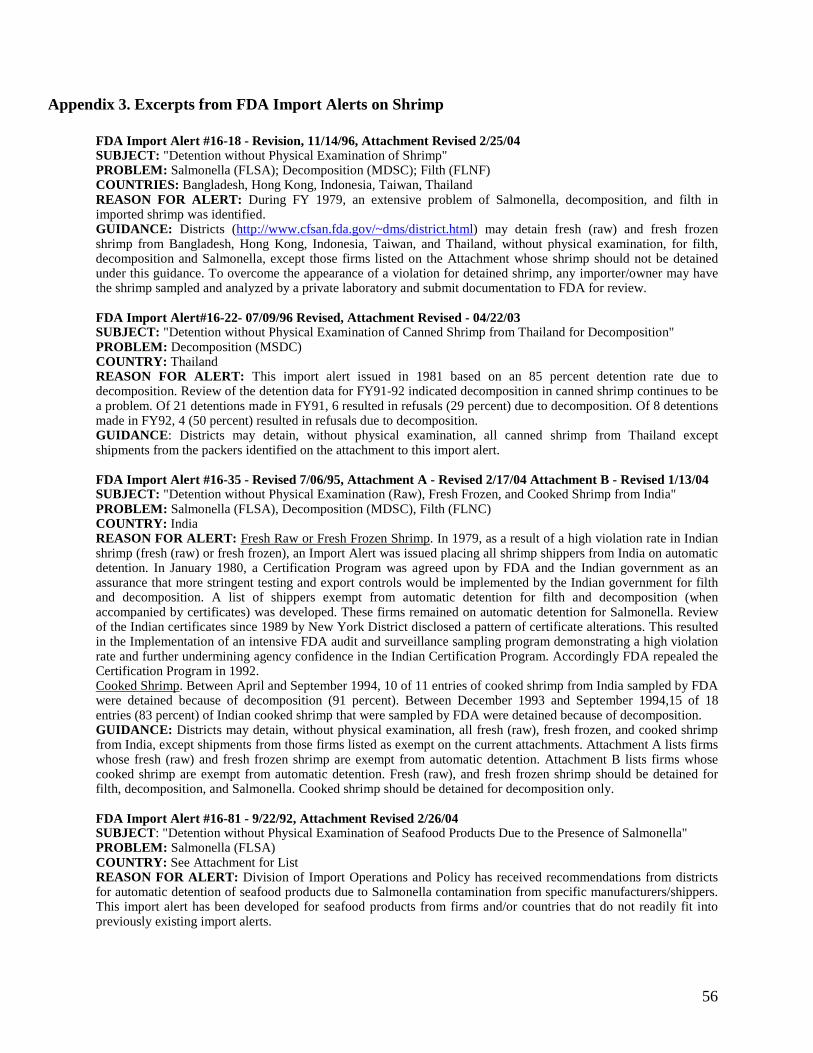

Findings 54 Recommendations 54 Appendixes 1. Value of U.S. Imports of Shrimp from All Countries, 1998–2003 56 2. Volume of U.S. Imports of Shrimp from All Countries, 1998–2003 3. Excerpts from FDA Import Alerts on Shrimp 4. Excerpts from FDA Import Alerts on Fruits and Vegetables

57 58 60

Bibliography 62 Figure

4

1 Causes for FDA refusal of entry for shrimp (all exporting countries and all ports of entry) June–October 2003

31

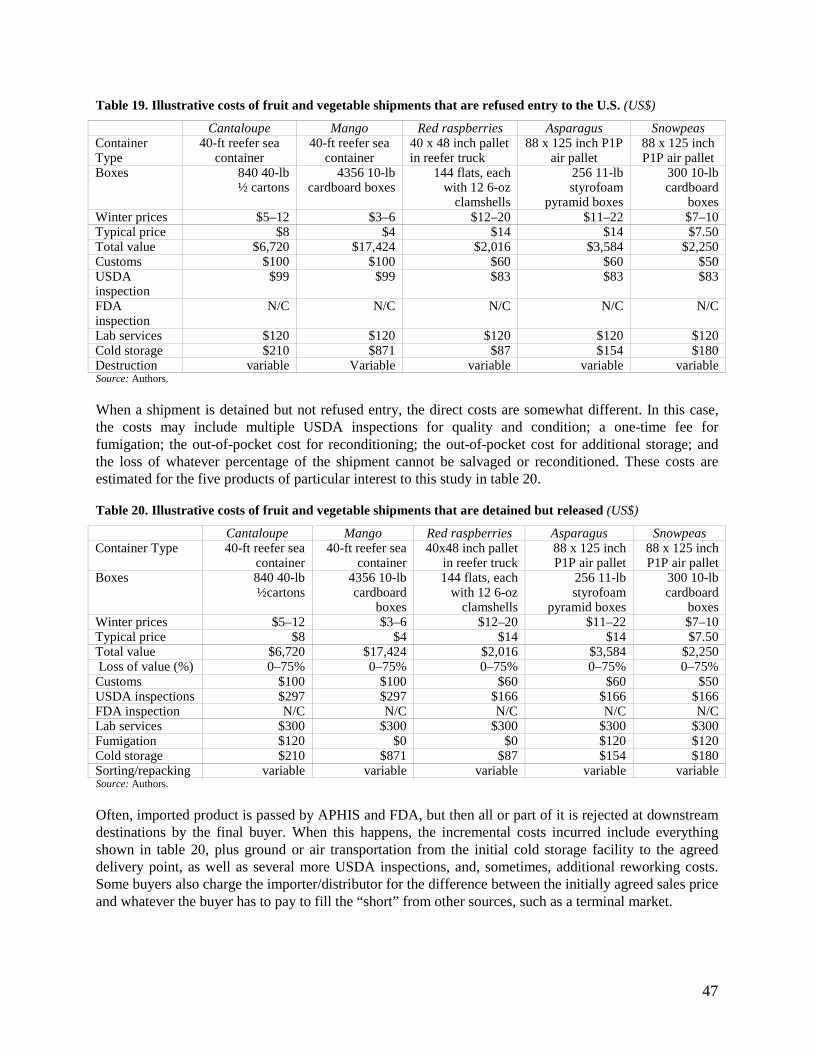

Tables 1 US per capita consumption of major food commodities 5 2 Import shares of United States food consumption for major categories by weight 6 3 Detailed import shares of United States food consumption by value, 1980–2001 (%) 7 4 US imports of fish products from all countries, 1999–2000 (US$) 9 5 Volume of US imports of fish products from all countries (MT) 10 6 Shrimp import share by form and presentation (US$) 12 7 US cantaloupes: Supply, use, and price, farm weight, 1978–2003 13 8 US imports of fresh cantaloupe by value 14 9 Fresh mangos: Supply and use, 1980 to date 15 10 US imports of fresh mangos by value, 1998–2002 15 11 US asparagus: Supply, use, and price, farm weight, 1978–2003 15 12 US imports of fresh asparagus by value, 1998–2003 16 13 US imports of fresh red raspberries by value, 1998–2003 17 14 US imports of fresh edible pea pods by value, 1998–2003 17 15 Matrix of standards applicable to shrimp 25 16 Direct costs associated with FDA hold/exam for a container of shrimp 32 17 Direct costs associated with FDA detention/refusal of a container of shrimp 33 18 Matrix of standards applicable to fresh produce 36 19 Illustrative costs of fruit and vegetable shipments that are refused entry to the US

(US$) 49

20 Illustrative costs of fruit and vegetable shipments that are detained but released (US$) 49

5

Foreword

Food and agricultural trade is the vital link in the mutual dependency of the global trade system and developing countries. Developing countries derive a substantial portion of their income from food and agricultural trade. The emergence of food safety and agricultural health issues and the related tightening of market requirements form challenges to further gains from trade due to the lack of technical and financial capacities of many developing economies.

As part of a joint program between the World Bank’s Agriculture and Rural Development Department (ARD) and International Trade Department (PRMTR), a survey on the Cost of Compliance of exporting developing countries was undertaken. The survey was focused on the supply chains of high-value food products (horticulture, fish, meat, spices, and nuts). The study quantified the costs incurred by both the public and private sectors; identified the coping strategies employed by the various stakeholders in the supply chains; determined the constraints that hinder compliance; examined the structural changes in the supply chain resulting from compliance with the safety standards; and evaluated the impact of these standards on small-scale enterprises and producers. The survey included Ethiopia (animal products), India (fish and spices), Jamaica (nontraditional agricultural exports), Kenya (fish and horticulture), Latin America Southern Cone (animal products), Morocco (fruits and vegetables), Nicaragua (shrimp), Senegal (fish and groundnuts), and Thailand (shrimp and horticulture).

A complementary perspective is provided by the companion series of buyer surveys involving representative importers, brokers, retailers, and distributors in the European Union, Japan, and the United States. This series, in turn, discusses the buyers’ perception of the strengths and weaknesses of their suppliers and describes the assistance and/or interventions offered by the buyers to their developing country suppliers.

This working paper is one of a series of such buyer surveys. These surveys examined the strategies of suppliers from the buyers’ perspective and the costs of intervention to assist the various developing country stakeholders to comply with international agro-food standards. This paper was prepared by John E. Lamb, Julian A. Velez, and Robert W. Barclay (all with Abt Associates, Inc.), with guidance from Steven Jaffee (PRMTR).

The findings and conclusions derived from these country studies are discussed in a synthesis report that seeks to identify possible points of intervention by the World Bank and other donor agencies and to determine the types of technical assistance that would be most efficient and appropriate. It is hoped that the experiences of these exporter and importer countries will provide useful insights to practitioners in the field, and to national and international policymakers in both the public and private sectors.

Kevin Cleaver Director, Agriculture and Rural Development Department

Uri Dadush Director, International Trade Department

6

Acronyms

ADI Acceptable Daily Intake AGEXPRONT Guild of Non-traditional Products Exporters (Guatemala) AMS Agricultural Marketing Service (USDA ) APHIS Animal and Plant Health Inspection Service (USDA) ASDA American Seafood Distributors Association BSE Bovine Spongiform Encephalopathy (mad cow disease) CBP Customs and Border Protection CDC Centers for Disease Control and Prevention (DHHS) CIF Cost, Insurance and Freight CFSAN Center for Food Safety and Applied Nutrition (FDA) CODEX Codex Alimentarius COMTRADE Commodity Trade Statistics Database (UNSTAT) COOL Country of Origin Labeling DEA Drug Enforcement Agency (US) DHHS United States Department of Health and Human Services DRC Dispute Resolution Corporation DWPE Detention without Physical Examination EBDC Ethylenebis dithiocarbamate EDB ethylene dibromide EDI Electronic data interchange EPA Environmental Protection Agency (U.S.) ERS Economic Research Service (USDA) ESSTO European Seafood Safety and Traceability Organisation EurepGAP European Retailers Programme for Good Agricultural Practices FAO United Nations Food and Agriculture Organization FDA United States Food and Drug Administration (DHHS) F&DC Food, Drug and Cosmetic Act FFDCA Federal Food, Drug and Cosmetic Act FIFRA Federal Insecticide, Fungicide, and Rodenticide Act FMI Food Marketing Institute (US) FOB free on board FQPA Food Quality Protection Act of 1996 FSIS United States Food Safety and Inspection Service (USDA) FTS Federal Technology Service (GSA) FY Fiscal Year GAA Global Aquaculture Alliance GAO Government Accountability Office GAP Good Agricultural Practices GMP Good Manufacturing Practices HACCP Hazard Analysis and Critical Control Points HHS U.S. Department of Health and Human Services HWT hot water treatment IAMA International Food and Agribusiness Management Association (US) IPM integrated pest management IR-4 Minor Use Pesticide Registration Program (EPA) ITC International Trade Commission LAC Latin America and the Caribbean

7

LACF Low Acid Canned Food MDR minimum daily requirement MOU Memorandum of Understanding MPE Model Plan of Excellence (Guatemala) MPF Merchandise processing fee MPN most probable number NMFS National Marine Fisheries Service (US NOAA) NOAA National Oceanic and Atmospheric Administration OIE World Organization for Animal Health OPPTS Office of Prevention, Pesticides, and Toxic Substances ORA Office of Regulatory Affairs OSHA Occupational Safety and Health Administration PACA Perishable Agricultural Commodities Act (USDA) PI preharvest interval PIP Pesticide Improvement Program (ACP/Cotonou) PIPAA Integrated Program for Agricultural and Environment Protection (Guatemala) P.L. Public Law (US) PLU Product Look-Up number POP Point of Purchase PPQ Plant Protection and Quarantine PRIA Pesticide Registration Improvement Act of 2003 PROEXAG/ Project for Support of Non-traditional Agricultural Exports/Export Import EXITOS Technology Support Project, for Central America (USAID) PROMPEX Program for the Promotion of Exports of Peru QAP quarantine action pest RFID Radio Frequency Identification Device SGS Société Générale de Surveillance (international) SPS Sanitary and Phytosanitary SQF Safe Quality Food (certification program of Food Marketing Institute in US) SSA Southern Shrimp Alliance SSOP Sanitation Standard Operating Procedures TBT Technical Barrier to Trade TED turtle excluder device UNEP United Nations Environment Programme UPC Universal Product Code UPOV International Union for the Protection of New Varieties of Plants USCS United States Customs Service USDA United States Department of Agriculture USG United States Government WHO World Health Organization WPS Worker Protection Standard (EPA) WTO World Trade Organization

1

Introduction

The World Bank commissioned this study to understand the challenges faced by United States receivers and buyers of offshore frozen shrimp and selected fresh fruits and vegetables. With this objective in mind, the report analyzes both statistical evidence from regulatory and other governmental agencies and the viewpoints of a sampling of importers, handlers, distributors, and chain buyers. The evidence was collected through a combination of literature review and direct interviews in person and by telephone. Besides discussing costs and difficulties with compliance, the report identifies coping strategies, equity impacts, and the resulting needs for capacity building.

As recent events clearly demonstrate, standards do matter greatly, not only to regulators but also to economic actors in the food industry and to consumers. Unfortunately, standards are most noteworthy in time of food or trade crisis–whether real, alleged or imagined. Coincidentally, several attention-getting crises relating to standards occurred in the United States while this report was being written. First, in 2003, several outbreaks of Hepatitis A occurred in four Eastern states associated with eating raw or undercooked green onions, apparently from Mexico. Next, bovine spongiform encephalopathy (BSE, or, more commonly, “Mad Cow Disease”) was presumptively identified in an adult Holstein cow in the State of Washington.1

The consequences of a food-related incident can be huge, whether justified by the findings or not. In the “Chilean Grape Scare” of 1989 (reports of cyanide injection in table grapes), although the evidence was very doubtful, the U.S. Food and Drug Administration (FDA) impounded 2 million boxes of grapes–an entire shipping season’s worth. An estimated $240 million was lost, and 20,000–50,000 workers reportedly lost their jobs.

In the case of BSE, the consequences have been much greater and will persist over time even if it is fully resolved. When the Washington State problem was first identified, the U.S. Department of Agriculture (USDA) immediately undertook aggressive remedial, trace-back, and media actions to contain the crisis. Despite the rapid response, market access for U.S. beef products was denied quickly in approximately 25 countries, including all major U.S. markets,2 potentially affecting an estimated 2.58 billion pounds of annual U.S. exports to the world, valued at $3.266 billion.3

These incidents show the tremendous challenges, particularly to developing country suppliers. Getting the right product to market on time, in good condition, and at competitive cost is no longer enough. Myriad public and private standards for sanitary and phytosanitary (SPS) matters, environmental protection, and treatment of labor both guide or constrain the production, logistics, marketing, and trade of food products, especially those destined for major markets such as the United States. The risks are enormous. Invasive species or exogenous pests or diseases can do great harm to U.S. agriculture. The U.S. General Accountability Office (GAO) estimates that there are 81 million cases of food-borne illness annually. FDA estimates that 300,000 hospitalizations and 5,000 deaths occur each year due to food-borne pathogens.4

1 http://www.usda.gov/news/releases/2003/12/0432.htm. 2 http://www.cbc.ca/stories/2003/12/28/bse031228. 3 http://www.ers.usda.gov/news/BSECoverage.htm. 4 Figures mentioned by the Director Designate of FDA’s Center for Food Safety and Applied Nutrition in keynote address at the Food Safety Summit held in Washington, D.C., March 2003.

2

Some observers argue that emerging standards have become de facto non-tariff trade barriers. Critics assert that stricter standards generally limit the success of developing countries at penetrating the main foreign markets, and raise costs and reduce net returns to upstream actors in the food chain. These standards may hamper food export development by less experienced and late-moving countries, and discourage participation by small farmers and their producer/exporter organizations.

Other observers argue that emerging standards actually stimulate food trade. Standards can facilitate arms-length transactions. Improvements in their application raise the confidence level of government, industry, and consumer alike in food in general and imported food in particular, and lower the incidence of market-depressing food scares. Standards-based improvements in the quality and condition of supply reduce product shrinkage and associated expenses all along the farm-to-market chain.

While this study was too limited in scope to resolve this important debate, the authors do hope that it will inform the discussion, at least for selected high-value products being exported to the U.S. market.

The study starts off with the consumption and production patterns for selected commodities (seafood, fruits, and vegetables), and, consequently, the significant role of imports. The different types of standards applicable to imported food are described in the next section. That section is followed by a discussion of how offshore suppliers of the pertinent commodities comply with these standards, including cost implications. The subsequent section deals with the much larger costs associated with loss of confidence, image, and market, and identifies the strategies for dealing with the risks associated with noncompliance. Finally, the authors present their main findings and recommend specific strategies for capacity building to the World Bank and other donor agencies.

3

1. Food Consumption and Import Trends

Per Capita Consumption for Selected Categories Annual per capita consumption of food in the United States reached more than 2,000 pounds in 2001,5 up from 1,800 pounds 2 decades ago. The fruit and vegetable category accounted for the largest share of per capita food consumption, but its total in terms of farm weight has risen very slowly and inconsistently (table 1).6 Fruit and vegetable consumption in 2001 amounted to 689 pounds per year, barely up from the 1992 figure of 677 pounds. Fruit consumption actually fell slightly during this period, from 282 pounds to 276. Meanwhile, per capita vegetable consumption rose gradually, from 395 pounds to 413 pounds. Despite the widespread perception that fish and shellfish are good for health, U.S. per capita consumption of fish and shellfish products has actually remained fairly low and flat for the last decade, oscillating between 14.6 and 15.2 pounds annually in terms of retail weight. Red meat consumption remains approximately 7 times as high as that of seafood, and poultry more than 4 times as great.

Role of Imports in U.S. Food Supply

Imports of food in 2003 amounted to more than 6 million shipments, and the number is rising rapidly.7 Food from abroad plays a key role in the United States food system. Between 1997 and 2001, imported fruits, vegetables, seafood, meat, and other foods provided 11.1 percent by weight of the food consumed by U.S. citizens, up from 8.2 percent in the early 1980s. Imports may supply products that cannot be grown within the country due to agroclimatic conditions. Imports fill windows that occur naturally each year because of the change in seasons, and also help fill shortfalls that occur unpredictably due to crop failures. Imports help ensure year-round supply of nearly all food products demanded in the marketplace. This near-certainty in turn helps ensure a strong and orderly market for domestic supplies of similar items during peak supply periods. Imports also provide greater diversity of products and varieties. Finally, by stimulating competition with domestic production where supply periods may overlap, imports help lower the overall cost of food to consumers. For example, in 2000, U.S. consumers devoted just 9.73 percent of their total expenditures to food, which is the lowest ratio in the world.8 The trend continues downward.

5 2001 is the latest year reported fully by USDA. 6 Agricultural Outlook Board, “Per Capita Consumption of Major Food Commodities,” AO Table 39, Economic

Research Service, USDA, May 2003. 7 http://www.fda.gov/bbs/topics/news/2004/NEW01057.html. 8 http://www.ers.usda.gov/publications/wrs011/wrs011.pdf.

4

Many different factors explain the growth in U.S. food imports. On the demand side, consumers increasingly want a greater variety of fresh and processed food items, and for the full 12 months of the year. Many consumers are willing to pay a premium for fresh fruits and vegetables during winter months. They expect to be able to purchase a wide range of ethnic items that match their heritage or to which they were exposed through travel and the media. Most want convenience in the form of different sizes, presentations, degree of processing, and consumer packaging. They also want the choice between conventionally and organically grown items. On the supply side, growers and shippers both have responded to and further stimulated the consumption of offshore and winter season supplies of different

5

varieties and products. Moreover, new technologies in production, post-harvest handling, storage, transport, and distribution have made it possible to lower costs, maintain condition, reduce transit time, ship longer distances, and extend shelf-life.

Imported crops and their derived products predominate over imported animal products. Over the last 20 years, plant products increased their share by 4.8 percentage points, as compared with just 0.7 percentage points for animal products (table 2). The main subcategories of interest in the present study fall within

Table 1

U.S. Per Capita Consumption of Major Food Commodities1

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Lbs.

Red meats2,3,4 113.4 111.2 113.5 113.6 111.0 109.0 113.2 115.1 113.7 111.3 Beef 62.4 61.0 62.9 63.5 64.0 62.6 63.6 64.3 64.5 63.1 Veal 0.8 0.8 0.8 0.8 1.0 0.8 0.7 0.6 0.5 0.5 Lamb & mutton 1.0 1.0 0.9 0.9 0.8 0.8 0.9 0.8 0.8 0.8 Pork 49.1 48.5 49.0 48.4 45.2 44.7 48.2 49.3 47.8 46.9Poultry2,3,4 60.4 62.0 62.6 62.1 63.1 63.1 63.7 66.7 66.9 66.2 Chicken 46.4 48.1 48.7 48.2 48.8 49.4 49.7 52.8 53.2 52.4 Turkey 14.0 13.9 13.9 13.9 14.3 13.6 13.9 13.8 13.7 13.8Fish and shellfish3 14.6 14.8 15.0 14.8 14.5 14.3 14.5 14.8 15.2 14.7

Eggs4 30.1 30.1 30.3 29.9 30.1 30.2 30.7 32.1 32.2 32.4Dairy products Cheese (excluding cottage)2,5 25.9 26.0 26.5 26.9 27.3 27.5 27.8 29.0 29.8 30.0 American 11.3 11.3 11.4 11.7 11.8 11.8 11.9 12.6 12.7 12.8 Italian 9.9 9.7 10.2 10.3 10.6 10.8 11.1 11.6 12.0 12.3 Other cheeses6 4.7 5.0 5.0 5.0 4.9 4.9 4.7 4.9 5.1 4.9 Cottage cheese 3.1 2.9 2.8 2.7 2.6 2.6 2.7 2.6 2.6 2.6

Beverage milks2 216.3 210.8 209.3 206.3 205.4 201.9 198.5 197.6 193.8 189.8 Fluid whole milk7 83.2 79.1 77.2 74.0 73.0 71.0 69.5 70.1 69.2 67.2 Fluid lower fat milk8 108.3 105.4 103.9 100.9 99.5 97.4 95.6 95.3 94.7 93.8 Fluid skim milk 24.8 26.3 28.2 31.4 32.9 33.5 33.4 32.2 29.9 28.8 Fluid cream products9 7.9 7.9 7.9 8.3 8.5 8.8 8.9 9.4 9.8 10.6 Yogurt (excluding frozen) 4.5 4.9 5.3 6.2 5.9 5.8 5.9 6.2 6.5 7.0 Ice cream 16.2 16.0 16.0 15.5 15.6 16.1 16.3 16.7 16.6 16.3 Lowfat ice cream10 7.0 6.9 7.5 7.4 7.5 7.8 8.1 7.5 7.3 7.3 Frozen yogurt 3.1 3.5 3.4 3.4 2.5 2.0 2.1 1.9 2.0 1.5 All dairy products, milk equivalent, milkfat basis11 562.6 569.3 579.7 576.2 566.2 567.2 572.4 584.6 592.8 587.2

Fats and oils--total fat content 66.4 69.1 67.3 65.4 64.2 63.7 64.3 67.0 74.5 -- Butter and margarine (product weight) 15.2 15.6 14.6 13.5 13.3 12.5 12.6 12.6 12.8 -- Shortening 22.3 24.9 23.9 22.2 21.9 20.5 20.5 21.1 23.1 -- Lard and edible tallow (direct use) 3.5 3.4 4.2 4.3 4.6 4.0 5.1 5.6 5.9 -- Salad and cooking oils 27.0 26.6 25.9 26.5 25.7 28.0 27.3 28.8 33.7 --

Fruits and vegetables12 676.8 687.8 691.2 690.6 700.5 708.4 696.7 698.3 705.4 688.7 Fruit 282.1 280.6 278.4 283.3 283.1 290.3 283.9 284.6 280.3 275.7 Fresh fruits 122.8 123.5 124.9 122.5 126.2 129.4 128.8 129.6 127.2 125.8 Canned fruit 22.8 20.5 20.7 17.3 18.5 20.1 17.0 19.2 17.5 17.7 Dried fruit 10.7 12.5 12.7 12.6 11.1 10.6 12.1 10.1 10.4 10.2 Frozen fruit 4.2 3.6 3.1 4.6 4.2 3.5 4.0 4.4 3.1 5.9 Selected fruit juices 121.1 120.1 116.6 126.0 123.0 126.1 121.6 120.8 121.6 115.8 Vegetables 394.6 407.2 412.8 407.2 417.4 418.0 412.9 413.7 425.1 412.9 Fresh 173.9 180.7 186.5 180.9 185.9 190.1 186.5 191.3 200.4 196.6 Canning 110.6 110.1 109.8 108.0 106.3 105.4 105.3 102.8 103.0 97.1 Freezing 70.5 75.3 77.5 78.8 83.3 81.5 80.4 80.9 79.6 78.2 Dehydrated and chips 31.4 33.4 30.7 30.9 33.9 32.7 32.5 30.6 33.8 33.3 Pulses 8.3 7.7 8.2 8.5 8.0 8.3 8.2 8.1 8.4 7.8Peanuts (shelled) 6.2 6.0 5.7 5.6 5.6 5.7 5.8 6.0 5.7 --Tree nuts (shelled) 2.2 2.3 2.3 1.9 1.9 2.1 2.2 2.5 2.5 2.2

Flour and cereal products13 184.6 189.1 191.8 190.2 196.2 197.3 194.2 195.5 199.8 195.7 Wheat flour 138.0 142.1 142.9 140.0 146.4 146.8 143.0 142.6 146.3 140.9 Rice (milled basis) 16.7 16.6 18.0 18.6 17.6 18.1 18.3 19.5 19.6 20.2Caloric sweeteners14 136.1 139.1 141.5 143.8 145.0 148.1 149.1 151.3 148.9 147.1Coffee (green bean equiv.) 10.0 9.0 8.1 7.9 8.7 9.1 9.3 9.8 10.3 9.4Cocoa (chocolate liquor equiv.) 4.5 4.3 3.8 3.6 4.2 4.0 4.3 4.5 4.7 4.5-- = Not available. 1. In pounds, retail weight unless otherwise stated. Consumption normally represents total supply minus exports, nonfood use, andending stocks. Calendar-year data, except fresh citrus fruits, peanuts, tree nuts, and rice, which are on crop-year basis. 2. Totals may not add due torounding. 3. Boneless, trimmed weight. 4. Excludes shipments to the U.S. territories. 5. Whole and part-skim milk cheese. Natural equivalent of cheese and cheese products. 6. Includes Swiss, Brick, Muenster, cream, Neufchatel, Blue, Gorgonzola, Edam, and Gouda. 7. Plain and flavored8. Plain and flavored, and buttermilk. 9. Heavy cream, light cream, half and half, eggnog, sour cream, and dip. 10. Formerly known as ice milk. 11. Includes condensed and evaporated milk and dry milk products. 12. Farm weight. 13. Includes rye, corn, oats, and barley products. Excludesquantities used in alcoholic beverages, corn sweeteners, and fuel. 14. Dry weight equivalent. Source: USDA, May 2003

6

three major categories—fish/shellfish, fruits/juices/nuts, vegetables—each of which shows a large and rapidly increasing share of total food imports, especially in value terms.

Table 2. Import shares of United States food consumption for major categories by weight1

Source: Jerardo 2003.

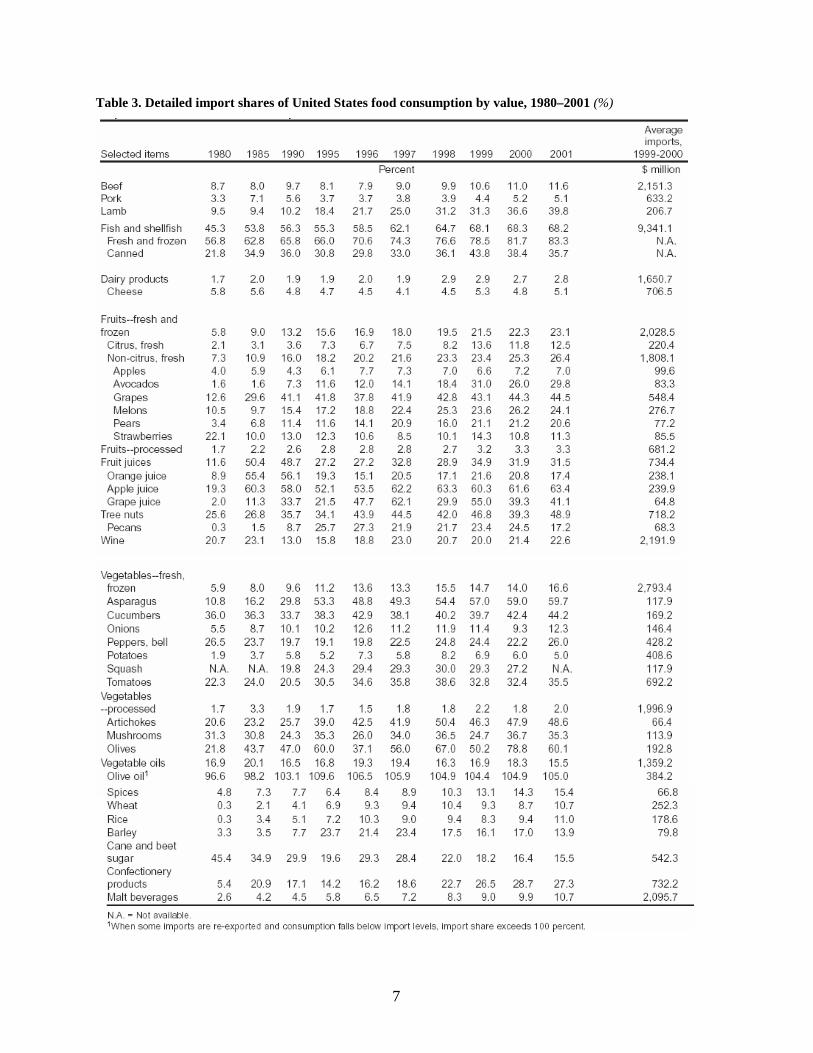

The value of imports of fish and shellfish in 1999–2000 averaged $9.3 billion (table 3). Between 1980 and 2000, the fish/shellfish share of food consumption value jumped more than 11 percentage points each decade, from 45.3 percent to 68.3 percent in 2001. Edible fish and seafood products have also had a large and gradually increasing share of all U.S. agricultural imports: 13.8 percent by value in 1998, 15.4 percent in 2000, and 14.7 percent in 2002.9 Most shrimp consumed in the United States falls within the “fresh and frozen” fish and shellfish category, for which the import share of food consumption value rose dramatically between 1980 and 2001, from 56.8 percent to 83.3 percent.

The import value of fresh and frozen fruits averaged $2 billion in 1999–2000. Of this total, $220 million represented citrus items and $1.8 billion represented non-citrus products. The import share for fresh citrus in food consumption value rose six-fold between 1980 and 2001, from 2.1 percent to 12.5 percent. Meanwhile the share for fresh non-citrus nearly quadrupled, from 7.3 percent to 26.4 percent. Table grapes and melons were the top performers by far, followed by apples, strawberries, avocadoes, and pears. Fruit juice imports also gained market share during these two decades, up from 11.6 percent to 31.5 percent, amounting to $734 million by 1999–2000. Other processed fruit rose as well, from 1.7 percent of all food consumption value to 3.3 percent.

9 See BICO report from Department of Commerce data for CY1998–2002, included as appendix 1.

7

Table 3. Detailed import shares of United States food consumption by value, 1980–2001 (%)

8

Import shares for most vegetables also increased dramatically between 1980 and 2001. For the fresh and frozen vegetable category as a whole, the share of food value nearly tripled, from 5.9 percent to 16.6 percent, culminating in $2.8 billion worth of imports in the years 1999 and 2000. Tomatoes were the leading performer. Bell peppers and potatoes formed a second tier, while cucumbers, onions, asparagus, and squash form a third tier. The processed vegetable category experienced slower growth, with an import share of 2.0 percent in 2001, as compared with 1.7 percent in 1980, but the absolute value of processed vegetable imports remained significant at $1.997 billion.

Actually, every product group listed in table 3 showed an increase in share of U.S. consumption, in some cases, as high as 500 percent over the 20-year period. Given these trends, observers generally agree that, despite a positive agricultural trade balance that stretches back more than 40 years, the United States is on the way to becoming a net agricultural importer. U.S. agricultural exports are expected to increase by approximately $500 million in the current fiscal year, to approximately $56.5 billion, while imports will grow as much as $3.5 billion to approximately $47.5 billion. "We can see this gap narrowing," Purdue University agricultural economist Phil Paarlberg said in a recent interview. "Where we were looking at an agricultural trade surplus five or six years ago of $15 billion to $20 billion, now it's under $10 billion." Although the trade gap was similar in the mid-1980s, the United States has not been a net agricultural importer since 1959. If the present trend continues, U.S. agricultural imports could overtake exports by 2007.10

Before focusing on the matter of standards, the authors set the stage by examining overall trends in origin, volume, value, and presentation for the selected product categories.

Seafood Imports: Spotlight on Shrimp

The authors selected shrimp for detailed consideration for various reasons. It is a major export product for many developing countries with which the World Bank works. Overall volume and value of U.S. imports are both increasing rapidly. Average unit value remains very high, although it has been declining over time as increasing supply drives down prices. Finally, shrimp presents significant challenges in terms of standards, especially with respect to production practices and sanitary compliance.

Table 4. US imports of fish products from all countries, 1999–2003 (US$000)

Product 1999 2000 2001 2002 2003 Fish and seafood products, edible

8,884,945 9,903,575 9,688,548 9,989,703* 10,892,941*

Shrimp 3,144,128 3,759,731 3,627,720 3,425,671 3,763,302*

Tuna 755,335 640,479 664,332 697,821 806,889*

Lobster 724,084 879,332 827,649 930,824* 742,521 Groundfish, fillet/steak 674,057 589,193 478,603 545,402 504,824 Salmon, whole or eviscerated 344,909* 333,161 323,726 343,176 323,914 Other edible fish and seafood 3,242,432 3,701,679 3,766,517 4,046,808 4,498,145*

Source: US Bureau of Census, Trade Data. Note: * = highest import levels since at least 1970. Shrimp has long been the leading contributor to U.S. seafood imports, boasting a 35.9 percent share of total seafood import value for the 5 years from 1999 to 2003 (table 4). The total value of shrimp imports has averaged $3.5 billion over the last 5 years, starting out at $3.1 billion and rising to a new record of $3.8 billion in 2003. Although the 5-year growth in value from 1998 to 2002 averaged approximately 7 percent, 2003 showed a surge of 11.2 percent. Import prices fell 29 percent between 2000 and 2002, and continued to fall throughout most of 2003, at which point wholesale prices fell to their lowest level in 40

10 “U.S. Heads toward Net Food Imports,” The Associated Press, September 26, 2003.

9

years.11 The sluggish economy and oversupply were the main reasons for the decline in average unit price.

The volume of U.S. shrimp imports rose steadily between 1999 and 2003, with a 52 percent overall growth that equates to an annual average increase of approximately 11 percent (table 5).12 Declining prices certainly stimulated more effective demand; yet industry insiders attribute the volume increase more to supply push. Throughout this period, the Thai shrimp export industry continued to grow; Chinese shippers responded to the 2001 EU import ban by turning more toward the United States market; shrimp farming continued to expand in Brazil; and shrimp aquaculture in Ecuador began to recover from virus problems.13

Table 5. Volume of US imports of fish products from all countries (MT)

1999 2000 2001 2002 2003 2002–03 % change

Other seafood 757,963 818,709 882,394 950,269 1,025,747 7.94 Shrimp 332,421 345,526 400,779 429,794 504,862 17.47 Tuna 308,808 269,753 231,974 246,821 297,750 20.63 Groundfish 185,980 178,193 140,578 157,822 150,552 -4.61 Salmon, whole 70,629 68,553 72,140 82,569 73,777 -10.65 Lobster 40,952 47,268 46,384 50,660 50,238 -0.83

Total 1,696,753 1,728,003 1,774,248 1,917,935 2,102,926 9.65 Source: USDA Trade Database, Bureau of Census data.

Perceiving these trends as a significant threat, in October 2002, prominent representatives and supporters of the Gulf and Atlantic Coast wild shrimp harvest, processing, and distributing industry from eight states formed the Southern Shrimp Alliance (SSA) to lobby for protection.14 Ironically, the prospect of a possible antidumping action by SSA caused foreign imports to accelerate in the third and then the fourth quarters of 2003 in anticipation of the possibility of retroactive penalties. The 17.5 percent growth in volume for 2003 led to a problem of oversupply and low prices.

At the very end of 2003, the SSA’s Shrimp Trade Action Committee actually filed the long-awaited antidumping petition with the Department of Commerce against Brazil, China, Ecuador, India, Thailand, and Vietnam.15 The petition alleges a dumping margin of between 27 percent and 267 percent on frozen and canned warm water shrimp (whether wild or farmed). The Commerce Department agreed on January 24, 2004 to investigate the allegations. On February 17, the US International Trade Commission (ITC) voted unanimously that there was a “reasonable indication that all six exporting countries had harmed or threatened local industry.” This vote meant that antidumping investigations would proceed, leading to a preliminary finding on June 8, 2004. If that were positive, a dumping margin would be determined Antidumping tariffs ranging from 58 percent for Thailand to 349 percent for Brazil could be imposed by mid-October 2004.16 Since some other major interest groups, such as the American Seafood Distributors Association (ASDA) and Global Aquaculture Alliance (GAA), opposed the petition, there was considerable uncertainty concerning what the U.S. Government ultimately would find and then do, as well as the final impact on industry and trade.

11 http://www.hotel-online.com/News/2003_Dec_31/p.403.1072895255.html. 12 NOAA, Imports and Exports of Fishery Products, Annual Summaries 1998 to 2002. Fisheries Economics and Statistics Division, National Marine Fisheries Service. 13 FAO, “China, Vietnam and Brazil Increase Share of US Shrimp Market,” Infopesca, August 2003. 14 http://www.shrimpalliance.com/about_us.htm. 15 http://www.olemiss.edu/orgs/SGLC/cnews.html#alliance. 16 http://www.accessnorthga.com/news/ap_newfullstory.asp?ID=29812.

10

Table 6. Shrimp import shares by form and presentation (US$)

Product name Imports

($) Exports

($) Re-exports

($) Balance of trade

($) Shrimp peeled frozen 1,123,280,867 19,355,730 16,162,502 -1,087,762,635 Shrimp frozen other preparations 663,860,778 0 0 -663,860,778 Shrimp shell-on frozen 31/40 311,370,229 3,704,441 4,878,866 -302,786,922 Shrimp shell-on frozen 15/20 283,456,742 2,141,644 1,650,567 -279,664,531 Shrimp shell-on frozen < 15 294,266,104 12,106,708 13,866,692 -268,292,704 Shrimp shell-on frozen 26/30 252,609,086 955,411 352,446 -251,301,229 Shrimp shell-on frozen 21/25 245,428,590 1,332,324 1,392,584 -242,703,682 Shrimp shell-on frozen 41/50 158,013,006 1,666,543 481,777 -155,864,686 Shrimp shell-on frozen 51/60 134,783,868 5,340,919 426,123 -129,016,826 Shrimp shell-on frozen 61/70 89,419,460 232,901 284,267 -88,902,292 Shrimp shell-on frozen > 70 82,709,076 5,752,328 228,648 -76,728,100 Shrimp breaded frozen 51,928,647 0 0 -51,928,647 Shrimp peeled fresh/dried/salted/brine 17,112,124 0 0 -17,112,124 Shrimp other preparations 30,807,545 12,692,551 1,236,582 -16,878,412 Shrimp frozen in ATC 11,316,219 1,332,006 137,182 -9,847,031 Shrimp shell-on fresh/dried/salted/brine 2,756,284 0 0 -2,756,284 Shrimp live/fresh/dried/salted/brine 0 5,454,739 757,698 6,212,437 Shrimp canned 7,330,554 19,435,699 479,307 12,584,452 Shrimp frozen 0 13,736,999 9,721,797 23,458,796 Totals 3,760,449,179 105,240,943 52,057,038 -3,603,151,198 Source: Foreign Trade Information, National Marine Fisheries Service, http://www.st.nmfs.gov/st1/trade/index.html.

U.S. shrimp imports actually originate in many different countries: 65 in total in 2003 (appendixes 1 and 2). Thailand stands far above the rest, with nearly a billion dollars in 2003 value and more than 133,000 MT in volume. China, India, and Vietnam form a second tier, each with $400–$600 million in value, and 40,000–80,000 MT in volume. Mexico, Ecuador, and Indonesia constitute a third tier, each with $150–200 million in export value and 20,000–35,000 MT in annual volume. In effect, the recent antidumping petition targeted the first and second tier, except for Mexico.

Shrimp imports take on various forms (table 6). The main presentation is frozen, shell-on shrimp of various sizes, amounting to 41 percent of value. Peeled and frozen shrimp is the next most important presentation, representing nearly 30 percent of value. “Other frozen preparations” follow, with approximately 18 percent of value. At the other extreme, canned shrimp accounted for just 0.19 percent of value.

Thailand predominates in many market segments: frozen, breaded shrimp; canned shrimp; shrimp frozen in ATC17; other frozen preparations; other preparations; peeled and frozen; and frozen shell-on of 26/30 and 31/40 size. As of 2002, China was the leader in shrimp that was fresh/dried/salted/brined, and in frozen shell-on 41/50 count shrimp. Mexico is the leading supplier of 21/25 frozen shrimp with shell, while Ecuador leads in 61/70 count shrimp, and Brazil in the very small 70+ count frozen shrimp with shell. Meanwhile, India has the lead in very large shrimp, that is, fewer than 15 counts.

Fresh Produce Imports: Spotlight on Selected Fruits and Vegetables

In addition to shrimp, this report will also consider certain horticultural exports: cantaloupe, mangos, red raspberries, asparagus, and snow peas. These particular crops were selected for close analysis for several

17 ATC is the enzyme, aspartate transcarbamylase.

11

reasons. They are all important export products for more than one of the developing countries with which the World Bank works. Overall volume and value of U.S. imports is increasing for each item. Although unit values are generally declining (as seasonal windows fill in), they still remain high. Most importantly, each one of these products presents significant challenges in terms of standards–especially sanitary or phytosanitary. To set the stage, we quickly review the supply and demand situation for each of the selected crops.

U.S. Supply, Demand, and Use of Cantaloupe

In the last 10 years, per capita use for cantaloupes in the United States rose 27 percent (approximately 2.5 percent per year), from 8.6 pounds to approximately 11 (table 7). Consumption has risen 70 percent over the past 20 years. Rising disposable income, ethnic diversity, and health consciousness all have played a role in this demand growth. From the supply side, varietal improvement, year-round availability, and promotion have been important factors. Domestic production rose 23 percent between 1993 and 2003, from 1.9 billion pounds to 2.3 billion. Yet, over the same period, import volume more than doubled from 498 million pounds to 1.1 billion, which meant a major increase in market share.

Varietal improvements, increased scale, investment in drip irrigation, more sophisticated post-harvest handling, and more efficient sea transport have all helped Central American growers, shippers, and exporters to effectively satisfy the winter window from November through early April. Until a salmonella ban (to be examined later) occurred in late October 2002, Mexico also continued to increase early season supplies, especially from March through May. The disparity between domestic and import growth rates caused the import share of available supply to rise from 19 percent to 33 percent in the last decade.

The value of cantaloupe imports rose steadily for most of the past two decades, but it peaked in 2001 at approximately $161 million, and then dropped back to $140 million in 2002 and to $116 million in 2003. The upward trend stalled in 2002 and 2003 due to Mexico’s SPS difficulties (table 8).

Table 7. US cantaloupes: supply, utilization, and price, farm weight, 1978-2003

Supply Utilization Per

Year Production Imports Total Exports Domestic capita 1/ 2/ 2/ use

-- Million pounds -- Pounds

1990 1,856.7 530.3 2,387.0 78.8 2,308.1 9.2 1991 1,664.0 602.5 2,266.5 75.7 2,190.8 8.6 1992 1,811.1 481.9 2,293.0 115.9 2,177.1 8.5 1993 1,898.7 458.1 2,356.8 116.2 2,240.7 8.6 1994 1,795.7 523.9 2,319.6 112.7 2,206.9 8.4 1995 1,896.2 613.1 2,509.3 118.1 2,391.3 9.0 1996 2,157.2 740.8 2,898.0 126.8 2,771.2 10.3 1997 2,084.0 921.6 3,005.6 134.4 2,871.2 10.5 1998 2,149.2 938.6 3,087.8 144.0 2,943.8 10.7 1999 2,257.7 1,108.1 3,365.8 153.9 3,211.9 11.5 2000 r 2,096.5 1,119.2 3,215.7 155.5 3,060.2 10.8 2001 r 2,271.8 1,070.1 3,341.9 146.0 3,195.9 11.2 2002 2,304.6 1,108.6 3,413.2 156.1 3,257.1 11.3 2003 f 2,230.0 1,090.0 3,320.0 155.0 3,165.0 10.9 -- = Not available. r= Revised. f = ERS forecast.

1/ Source: National Agricultural Statistics Service, USDA. 2/ Source: Bureau of the Census, U.S. Dept. of Commerce.

12

Mexico was the largest foreign source of cantaloupes until 2001. Mexican imports peaked in 1999 at $71.8 million, with a volume of 196,802 MT. Since then, however, its imports have fallen precipitously, to $17.5 million in value and 58,714 MT in volume in 2002, and then an additional drop of 85 percent in annual value and 89 percent in annual volume for 2003. The ongoing decline is attributable to the salmonella findings explained later.

As the problem began to emerge, Central America producers ramped up late-season production to fill the void left by Mexico. However, uncertainty concerning the rate of FDA re-approval of individual Mexican shippers together with the normal onset of the Central American rainy season in May appear to have prevented full recovery of past import volume and value. Yet, cantaloupes remain an important fruit product for the U.S. market, particularly among imports.

Table 8. U.S. Imports of fresh cantaloupe by value (US$ 000)

Countries of origin 1998 1999 2000 2001 2002 2003 Costa Rica 22,022 26,701 32,209 50,130 43,324 30,924 Dominican Republic 3,735 5,288 4,894 5,180 5,639 4,139 Guatemala 21,139 32,928 41,031 35,858 52,926 52,578 Honduras 19,260 16,988 18,434 22,941 20,079 24,784 Mexico 57,000 71,783 49,465 46,386 17,547 2,727 Others 800 605 1,140 454 470 881 Total 123,956 154,293 147,173 160,949 139,985 116,033

Source: USDA Foreign Agricultural Service.

U.S. Supply, Demand, and Use of Mangos Mango consumption has been increasing steadily for the past two decades (table 9). It doubled between 1980 and 1986, again between 1986 and 1994, and yet again between 1994 and 2002, when it reached 1.97 pounds per capita. Although the absolute number is still modest, such growth rates in fresh produce are very unusual.

As with cantaloupes, both demand and supply factors are at play. On the one hand, rapid growth in various ethnic segments (especially Latin, Asian and Caribbean) of the U.S. population has been accompanied by greater familiarity with and demand for mangos and other tropical fruits such as papaya. Other segments of the population have come to know and appreciate mangos through travel and the food media. On the supply side, growth in exportable volume from many different countries—but especially Brazil, Costa Rica, Ecuador, Guatemala, Haiti, Mexico, and Peru—has pushed product into the system and brought prices down even in past periods of scarcity, such as early September through Thanksgiving. A critical factor in this expansion from abroad was approval by USDA/APHIS of the hot water treatment as a plant quarantine treatment. to control fruit flies, especially the Mediterranean fruit fly.

U.S. domestic production of mangos, which had long been limited to Hawaii, Florida, and Puerto Rico, held its own until 1992, when Hurricane Andrew destroyed many trees in the Homestead area of South Florida. Since then the domestic industry has languished. It is not likely to recover because of land use pressure and the abundance of inexpensive fruit from Mexico and Puerto Rico during Florida’s summer production season.

13

Import volume tripled between 1980 and 1990, and tripled again by 2000, at which point it reached 518 million pounds. Mango imports continue to increase in volume at approximately 10 percent per year. Given demographic trends and changing consumer preferences, the future is bright for mango imports, as long as there are no major SPS issues that might constrain offshore supply. As will be explained later, fruit fly findings remain a serious threat.

During the 1998–2002 timeframe, volume increased 33 percent, from 197,393 MT to 263,348 MT (table 10). The value of mango imports reached $153 million in 2002, up 16 percent from the $132 million level 5 years earlier. Eleven-month figures for 2003 suggest a 5.4 percent rise in total annual value, coupled with a 6.1 percent increase in volume. The share of U.S. import value held by Mexico continues to be very large–53 percent in 2002–but has fallen from the 78 percent share 5 years back. Meanwhile, Mexico’s share of import volume has fallen from 81.8 percent to 62.3 percent. Increases in fall and winter season exports from South American countries are eroding Mexico’s share of market. Value is more affected than volume, because off-season imports from South America have average unit values 2 to 4 times higher than Mexico’s.

Table 9. Fresh mangos: supply and utilization, 1980 to date

Supply Utilization Year Consumption

Utilized production Import s 1/ Total supply Exports 2/ Total Per capita -- Million pounds -- Pounds

1990 19.3 130.5 149.7 15.8 133.9 0.54 1991 27.5 203.6 231.1 15.2 215.9 0.85 1992 22.0 167.9 189.9 17.1 172.8 0.67 1993 3/ 2.8 243.9 246.7 14.9 231.7 0.89 1994 5.5 271.4 276.9 21.7 255.1 0.97 1995 8.3 312.4 320.6 22.2 298.4 1.12 1996 5.5 378.3 383.8 22.9 360.9 1.34 1997 5.5 411.3 416.8 25.2 391.6 1.44 1998 N.A. 435.2 435.2 23.2 412.0 1.49 1999 N.A. 483.1 483.1 29.8 453.3 1.62 2000 N.A. 518.3 518.3 23.3 495.0 1.75 2001 N.A. 524.6 524.6 14.6 510.0 1.79 2002 4/ N.A. 580.7 580.7 11.8 568.9 1.97 N.A.= Not available. 1/ Imports 1989 - 92 include small amounts of fresh guava. 2/ Before 1981, mango, papaya, and kiwifruit exports were reported together; 1984 - 88 assume mangos 75 percent of "other fruit" exports; 1989 - 92 exports include mangosteens and guavas. 3/ Reflects tree losses due to Hurricane Andrew in August 1992. 4/ Preliminary. Source: Economic Research Service, USDA.

14

Table 10. U.S. imports of fresh mangos by value (US$ 000)

Countries of Origin 1998 1999 2000 2001 2002 2003 Brazil 7,013 11,666 13,622 21,355 28,693 27,897 Ecuador 4,056 6,709 9,911 8,571 10,333 8,151 Guatemala 4,485 4,250 4,257 4,068 4,788 3,644 Haiti 5,439 6,701 7,111 3,465 5,493 4,412 Mexico 103,236 98,429 88,702 100,194 81,215 90,433 Nicaragua 2,490 1,067 2,174 1,982 1,242 2,006 Peru 4,477 12,962 13,383 15,780 19,885 15,980 Others 1,007 1,204 1,592 1,269 1,356 1,269 Total 132,203 142,988 140,752 156,684 153,005 153,792

Source: Department of Commerce, US Census Bureau, Foreign Trade Statistics. Note: Data for 2003 is January to November.

U.S. Supply, Demand, and Use of Asparagus Per capita use of asparagus in all its forms rose 30 percent between 1987 and 2003, or from 1.0 to 1.3 pounds. However, during this 15-year period, the consumption of canned asparagus actually fell, and the consumption of frozen asparagus stagnated. Meanwhile, fresh use has increased rapidly, from 0.6 pounds per capita to 1.0 pounds.

Reliable supplies of good quality from offshore sources are the main explanation. Fresh asparagus is now available year-round, and retail prices have begun to fall even from August through December, when most product must be shipped from South America either by air or in controlled atmosphere sea containers.

Domestic production for fresh use began to stagnate in the late 1980s, and during the early 1990s actually fell for approximately 5 years (table 11). Starting around 1990, foreign imports began to rise, accelerating greatly during the latter 1990s and into the new millennium. Imports almost doubled in volume between 1990 and 1995, then again between 1995 and 2000. Meanwhile, U.S. export volume declined in the 1990s and beyond, largely because of the recession associated with the Asian financial crisis.

Table 11. US asparagus: supply, utilization, and price, farm weight, 1978-2003

Supply Utilization Year Per

Production Imports Total Exports Domestic capita 1/ 2/ 2/ use

-- Million pounds -- Pounds

1990 142.4 43.8 186.2 39.4 146.8 0.6 1991 137.0 52.4 189.4 37.2 152.2 0.6 1992 137.6 57.7 195.3 42.3 153.0 0.6 1993 125.2 69.3 194.5 46.9 147.6 0.6 1994 131.1 64.8 195.9 48.5 147.4 0.6 1995 110.0 79.1 189.1 40.7 148.4 0.6 1996 111.4 76.1 187.5 31.7 155.8 0.6 1997 124.8 88.6 213.4 33.6 179.8 0.7 1998 126.4 109.8 236.2 34.4 201.9 0.7 1999 145.5 142.3 287.8 38.1 249.7 0.9 2000 r 150.4 159.4 309.8 36.6 273.2 1.0 2001 r 137.2 157.0 294.2 31.6 262.6 0.9 2002 126.7 180.3 307.0 29.3 277.7 1.0 2003 f 115.0 195.0 310.0 31.0 279.0 1.0 -- = Not available. r = Revised. f = ERS forecast. 1/ Source: National Agricultural Statistics Service, USDA. 2/ Source: Bureau of the Census, U.S. Department of Commerce.

15

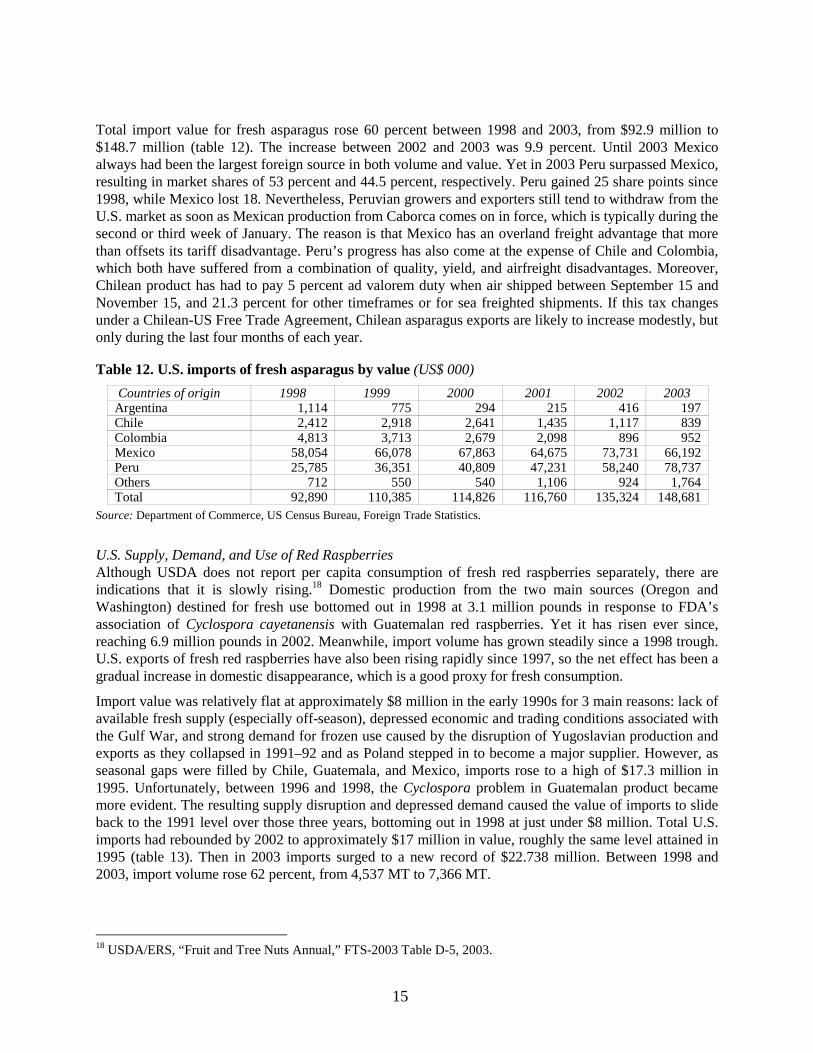

Total import value for fresh asparagus rose 60 percent between 1998 and 2003, from $92.9 million to $148.7 million (table 12). The increase between 2002 and 2003 was 9.9 percent. Until 2003 Mexico always had been the largest foreign source in both volume and value. Yet in 2003 Peru surpassed Mexico, resulting in market shares of 53 percent and 44.5 percent, respectively. Peru gained 25 share points since 1998, while Mexico lost 18. Nevertheless, Peruvian growers and exporters still tend to withdraw from the U.S. market as soon as Mexican production from Caborca comes on in force, which is typically during the second or third week of January. The reason is that Mexico has an overland freight advantage that more than offsets its tariff disadvantage. Peru’s progress has also come at the expense of Chile and Colombia, which both have suffered from a combination of quality, yield, and airfreight disadvantages. Moreover, Chilean product has had to pay 5 percent ad valorem duty when air shipped between September 15 and November 15, and 21.3 percent for other timeframes or for sea freighted shipments. If this tax changes under a Chilean-US Free Trade Agreement, Chilean asparagus exports are likely to increase modestly, but only during the last four months of each year.

Table 12. U.S. imports of fresh asparagus by value (US$ 000)

Countries of origin 1998 1999 2000 2001 2002 2003 Argentina 1,114 775 294 215 416 197 Chile 2,412 2,918 2,641 1,435 1,117 839 Colombia 4,813 3,713 2,679 2,098 896 952 Mexico 58,054 66,078 67,863 64,675 73,731 66,192 Peru 25,785 36,351 40,809 47,231 58,240 78,737 Others 712 550 540 1,106 924 1,764 Total 92,890 110,385 114,826 116,760 135,324 148,681

Source: Department of Commerce, US Census Bureau, Foreign Trade Statistics.

U.S. Supply, Demand, and Use of Red Raspberries Although USDA does not report per capita consumption of fresh red raspberries separately, there are indications that it is slowly rising.18 Domestic production from the two main sources (Oregon and Washington) destined for fresh use bottomed out in 1998 at 3.1 million pounds in response to FDA’s association of Cyclospora cayetanensis with Guatemalan red raspberries. Yet it has risen ever since, reaching 6.9 million pounds in 2002. Meanwhile, import volume has grown steadily since a 1998 trough. U.S. exports of fresh red raspberries have also been rising rapidly since 1997, so the net effect has been a gradual increase in domestic disappearance, which is a good proxy for fresh consumption.

Import value was relatively flat at approximately $8 million in the early 1990s for 3 main reasons: lack of available fresh supply (especially off-season), depressed economic and trading conditions associated with the Gulf War, and strong demand for frozen use caused by the disruption of Yugoslavian production and exports as they collapsed in 1991–92 and as Poland stepped in to become a major supplier. However, as seasonal gaps were filled by Chile, Guatemala, and Mexico, imports rose to a high of $17.3 million in 1995. Unfortunately, between 1996 and 1998, the Cyclospora problem in Guatemalan product became more evident. The resulting supply disruption and depressed demand caused the value of imports to slide back to the 1991 level over those three years, bottoming out in 1998 at just under $8 million. Total U.S. imports had rebounded by 2002 to approximately $17 million in value, roughly the same level attained in 1995 (table 13). Then in 2003 imports surged to a new record of $22.738 million. Between 1998 and 2003, import volume rose 62 percent, from 4,537 MT to 7,366 MT.

18 USDA/ERS, “Fruit and Tree Nuts Annual,” FTS-2003 Table D-5, 2003.

16

Table 13. U.S. imports of fresh red raspberries by value (US$ 000)

Countries of origin 1998 1999 2000 2001 2002 2003 Canada 3,315 7,102 3,473 5,131 3,115 4,088 Chile 1,485 1,568 1,046 2,321 4,720 4,766 Mexico 2,994 4,319 8,718 6,857 8,864 13,741 Others 167 308 278 191 640 143 Total 7,961 13,297 13,515 14,500 17,339 22,738

Source: Department of Commerce, US Census Bureau, Foreign Trade Statistics.

Import shares have changed considerably over time because of the changes just described. Mexico was number two in value until 2000, at which point it overtook Canada. Canada remains the volume leader, but not by much. In 2003 Mexico had a 60 percent share of import value, while Chile’s share was 25 percent and Canada’s was 17 percent. Mexico has been the industry leader, achieving a 43 percent jump in import value between 2003 and 2002. Meanwhile export value for Chile has remained flat. After Guatemala was subjected to an FDA ban in late 1997, its market share fell immediately to zero, bounced back slightly by 2002 to 3.7 percent, then fell again in 2003.

U.S. Supply, Demand, and Use of Snow Peas Snow peas, a flat edible pea pod containing immature seeds, are a specialty vegetable traditionally used in Chinese cuisine. However, they are increasingly sold in supermarkets in loose form or in consumer packs, and are now found in many frozen vegetable blends. USDA statistics combine snow peas with sugar snaps, which are sweeter and have more developed seeds that provide a robust rather than flat shape. Notwithstanding their perceived popularity, fresh consumption of snow peas and sugar snaps has actually stayed flat in the United States over the past decade or more, at just 0.15 pounds per capita. Whatever growth in total product consumption has occurred probably applies more to their use in frozen vegetable mixes than in fresh form.

While domestic production has varied between 24–30 million pounds for more than a decade, imports have long predominated. Imports have grown steadily in the past five years, from 14,125 MT in 2000 to 24,079 MT in 2003, which gives imports approximately a two-thirds market share of this commodity.

Import value in 1998 amounted to $18.1 million, while in 2003 it was $19.3 (table 14). Given the 63 percent increase in volume over that same period, it is evident that average unit values have fallen considerably, and are now in the $7.00/10-lb box (CIF) range.

Table 14. U.S. imports of fresh edible pea pods by value (US$ 000)

Countries of origin 1998 1999 2000 2001 2002 2003 Guatemala 5,117 3,804 4,271 5,644 5,930 7,834 Mexico 11,934 12,554 8,197 8,136 9,429 8,168 Peru 501 1,022 1,602 1,543 2,817 2,796 Others 515 210 130 244 129 453 Total 18,067 17,590 14,200 15,567 18,305 19,251

Source: Department of Commerce, US Census Bureau, Foreign Trade Statistics.

Guatemala has long been the volume leader among snow pea suppliers to the U.S. market, boasting almost 49 percent more exports than Mexico in 2002 and triple the volume in 2003. Mexico remains the leader in terms of value, but by 2003 both countries were converging on the $8 million level, with Guatemala’s value rising and Mexico’s falling. It is important to note as well that Peru has significantly increased its exports in recent years, from just 227 MT worth $500,000 in 1998, to 2,083 MT worth $2.8 million in 2003. Peru has some agro-climatic advantages over Guatemala and Mexico in the months of September and October.

17

2. Standards Applicable to Imported Food

Definitions The technical definitions of “standard” vary widely. Here are some examples:

International Organization for Standardization: “rules, guidelines, or characteristics for activities or their results, aimed at achievement of the optimum degree of order in a given context”

British Standards Institution: “published specifications that establish a common language, and contain a technical specification or other precise criteria and are designed to be used consistently, as a rule, a guideline, or a definition”

Codex Alimentarius: “requirements for food aimed at ensuring for the consumer a sound, wholesome food product free from adulteration, correctly labeled and presented.”

As will become clear from the discussion below, even the last definition is too narrow, given the way the food and agricultural industry is evolving worldwide. Consumers are not the only stakeholder group. Not only the product itself, but also the procedures used to produce, handle, transform, and market it, are of interest. The circumstances surrounding production and marketing are also of interest to some stakeholders. Pests or diseases that might accompany imported food are of great interest to farmers in target markets.

Purposes

Standards can provide benchmarks by which to measure attributes of interest. When used in this manner, typically, they either set minimal acceptable levels, or else aspirational targets. Quantitative measures are customarily used for most standards of this kind. Yet, increasingly, standards are also being used to ensure responsible practices, more broadly defined. In such situations, qualitative judgments by an independent, respected observer are usually the main means of measurement and verification.

Tangible vs. Intangible Standards

Standards may be either tangible or intangible, depending on whether the attributes in question can be measured by examining the product itself or not. For example, a pesticide residue standard is tangible, while a minimum preharvest interval (PI) for applying a given pesticide is not. Intangible standards are not evident to the buyer or consumer, who therefore suffers from imperfect information (not knowing whether he/she is getting what is expected). The marketability of “credence goods” may benefit from, or even require, independent certification. This service is typically provided by an objective, qualified third party who is viewed as credible by the stakeholders. The third party may be governmental or private.

Degree of Voluntarism

Standards may be compulsory, advisory, voluntary, or involuntary. Compulsory standards are most often set by public law, decree, or regulation; and they are also usually enforced by governmental agencies (or their contractors). Typically, they carry penalties for noncompliance. Examples include food labeling controlled by FDA for purposes of product identification, nutritional information, or country-of-origin; quality grades for certain agricultural products governed by USDA Agricultural Marketing Orders; and condition standards for fresh produce defined and administered under the United States’ Perishable Agricultural Commodities Act.

18

Advisory standards may be issued by government or private enterprise. When issued by a regulatory agency, they may indicate a desired direction, foreshadow a future mandatory standard, or simply reflect the reality that a definitive standard cannot be finalized at that time. A good example is the FDA’s “Guide to Minimize Microbial Food Safety Hazards for Fresh Fruits and Vegetables.”19 Via this document, FDA in effect recognized that there was an issue of great concern, but fell short of requiring formal application of HACCP, which the fresh produce industry did not consider feasible because of the diversity of products, forms, presentations, sources, and pest/disease/pathogen problems.

Voluntary standards are more often set and applied by suppliers, handlers, processors, marketers, or other actors in the farm-to-market chain. Such standards are generally established to limit risk or to add value through quality improvement, differentiation, or supply management. Examples in food products include designation as “pesticide-free”; use of quality seals; differentiation via branding; sorting by size; and classifications such as “premium,” “select,” “gourmet,” or “fancy.” Voluntary standards are usually self-enforced, whether by the producer, the middleman, or the marketer. However, the use of third-party private certification is increasing.

Involuntary standards fall between these two extremes. When a voluntary standard really gains traction in a given deal (product/market combination), it can become so compelling in terms of maintaining market access or competitive position in a given supply chain that industry actors must treat it as mandatory even though it is not. Examples include slotting allowances commonly paid to introduce new products into supermarkets, and the use of PLU (product look-up stickers) on individual pieces of fruit.

Types of Standards

While many discussions of standards draw a distinction only between product and process, the standards arena is actually much more complicated than that. For this analysis, the authors prefer to differentiate between four types rather than just two.

Outcome standards are concerned with the situation expected at a given stage in the supply chain.20 When a product has been recently harvested, it has certain quality attributes that can be used as standards. Depending on the product, these may include size, shape, deformity, style, pulp temperature, ripeness, maturity, color, sugar (Brix) level, organoleptic traits (taste, sight, and smell), chemical residues, or presence of pests or diseases. These same attributes may also be used at the packing shed or processing plant as standards for product quality, along with additional ones such as firmness, cosmetic appearance, filth, extraneous matter, decomposition, conformity to count, and gross and net weight. Outcome standards relating to markings (PLU sticker, UPC code, labeling), packaging (type, material, protection against bruising), packing (count per box, use of gel packs), and palletizing may be specified for all products that leave a facility. As the product moves into channels, defects of condition such as percentage of product broken, crushed, or decayed; absence of post-harvest disease; internal temperature; and integrity of the box become more important. At the point of final sale to the retail customer, some set of additional quality and condition standards will also apply, varying by circumstances.

Process standards concern how a given food or agricultural item is produced, harvested, cooled, washed, graded, sorted, handled, processed, packed, stored, transported, traded, distributed, or sold. Good agricultural practices (GAP) and good manufacturing practices (GMP) are sets of process standards that apply during the production, harvesting, and processing stages. For shrimp and other seafood, specific standards have been developed to ensure sustainable harvests, such as the use of turtle excluder devices (TEDs). In some situations, there are standards that govern transport method (air, land, or sea freight), conditions (temperature, ethylene level, venting), and transit time. At the point of retail sale or

19 http://vm.cfsan.fda.gov/~dms/prodguid.html. 20 Adapted from Reardon and others, “Strategic Roles of Food and Agricultural Standards,” MSU, 1999.

19

institutional use, any or all of the previous process standards may be applied, along with others such as shelf life or time held in storage. Variants such as EurepGAP (European Retailers’ Programme for Good Agricultural Practices) further define acceptable agricultural practices in a particular marketplace for selected product groups, initially just fresh produce and cut flowers. Organic standards define agricultural and manufacturing processes that will preserve certain measurable and immeasurable attributes in a product of interest. The HACCP (Hazard Analysis and Critical Control Points) approach further defines acceptable food, consumer, and environmental safety practices for meat, poultry, seafood, processed fruits and vegetables, and certain juices, with application in nearly all developed country markets. LACF (Low Acid Canned Food) regulations prescribe how to process products such as tomato paste or canned asparagus to avoid a particular problem, botulism.

Performance standards are concerned with how well a given product or entity achieves its intended purpose. In the past, such standards applied mainly to non-food agricultural items such as colorants, fragrances, and essential oils. In recent years, they have become relevant to edible agricultural products that serve as “functional foods,” for example, foods whose bioactive ingredients may lower cholesterol, prevent high blood pressure, reduce the risk of heart attacks, or improve the body’s resistance.

Impact standards are concerned with the consequences of consuming, utilizing, or handling a given item. Human safety is the prime example, but animal safety can be an impact concern for products such as ruminant proteins used for feed, while environmental safety can be an impact concern for products such as agricultural waste whose disposal could propagate pests or diseases.

Areas of Application in Food and Agriculture

Quality and condition: Quality standards refer to the desired attributes of a given food item at a particular point in its journey from farm to fork. Condition standards refer to the deterioration that may occur during that same journey, especially for perishable products. This may be due to biological processes such as maturation, ripening, or respiration; or to physical processes such as dehydration or bruising. Quality and condition standards may also apply to packaging, packing materials, or pallets.

Quality and condition standards serve mainly to facilitate arms-length trading, lower transaction costs, reduce rejections and shrinkage, lower commercial or user risk, and differentiate products or suppliers.

Traditionally, official quality standards issued by public agencies in source and destination countries governed most international trade in food and agricultural products. Yet, as trade has become more competitive and demand-driven, and as high-value products have gained market share, more stringent and varied buyer specifications have become more important. The same applies in domestic commerce, and increasingly in major cities, even in developing countries.

For private standards, especially for quality and condition, whoever dominates the supply chain tends to set the standards. For standards that apply only to a particular segment of the supply chain (for example, the production of seed cotton), entities that control a choke point (that is, the gin) may set the quality standards, at least on an interim basis, but always with the next buyer’s expectations in mind.

Most agricultural and food products exported from developing countries quickly enter importer or buyer-dominated supply chains, but there are a few in which growers or exporters have the greatest leverage in the supply chain. Mangos and shrimp are examples of the former, while bananas and rock lobster are examples of the latter.

Sanitary and phytosanitary: SPS standards generally refer to attributes and practices that may affect the life or health of humans, plants, or animals. Although food safety is arguably the most important sanitary issue as far as humans are concerned, worker health and safety are also significant SPS issues. In the phytosanitary field, the main issue is the threat of introducing pests or diseases that could harm potential

20

host plants in the destination market. Zoosanitary threats or risks concern mainly the introduction of animal pests or diseases that might harm the same or related animal hosts in the target market, but there are also zoonotic diseases, such as Avian flu, that can pass from animals to humans. The new field of biosecurity would logically fit under SPS as well, although it has not yet been codified in the 1994 WTO Agreement on the Application of SPS Measures, nor is it written into all of the major international trade or agricultural agreements that contain SPS chapters or provisions.

The main intent and function of SPS standards is to lower risks of unacceptable direct or indirect impacts on consumers, agricultural workers, and flora or fauna in the source and destination countries. However, the use of best practices in SPS has other benefits, in that it facilitates arms-length trading, reduces rejections and shrinkage, lowers commercial risk, and helps to differentiate products or economic actors in the food chain.

More than any other category of standards, SPS can have a dramatic effect on market access. In the United States, for example, inability to prove a level of risk acceptable to APHIS or FDA can: (1) entirely prevent entry of a certain commodity; (2) increase the rate of sampling at the border and subsequent laboratory analysis to levels that stifle trade and raise trading costs; and/or (3) require the use of an approved plant or animal quarantine treatment. And even if in the past a product has been deemed generally admissible from a given source area to certain ports of entry, continued interception of problem shipments can lead to gradual or sudden closing of the border to shipments emanating from specific companies or an entire country. For some SPS issues (such as pesticide residues), there may be a maximum limit, while for others (such as salmonella) there is zero tolerance.

Governments are the main source of SPS standards in the plant and animal health area, in which the potential harm generally takes the form of unacceptable externalities. By contrast, the private sector is playing an increasingly active role in specifying SPS standards for food safety, because the financial and other business costs of a product recall and/or liability suits are huge. While some suppliers still see higher standards as a burdensome problem, others are now using food safety standards, as well as the certification and audit processes that go along with them, as a competitive tool to differentiate their products or supply chains.

Social accountability: These standards generally refer to the conditions that surround the production, handling, processing, and distribution of a given food product. Use of child labor, especially in the fields, is one major concern. Another concern is gender sensitivity, which usually subsumes maternity and child care issues. A third concern is general working conditions, which include worker health and hygiene, hours worked, wage/pay structures, fringe benefits, and right to organize. A fourth is the use of forced, prison, or military labor.

Since labor standards have no tangible effect on product quality or appearance, the only way that they can be enforced is through certification or audit. Depending on whether they are imposed by government or required by buyers, the penalties for noncompliance may be fines or loss of market. Increasingly, labor standards are more imposed by buyers in destination markets than by governments in source countries.

Environment: Environmental standards generally cover risks of harm to water, soils, air, biodiversity, landscape, and cultural heritage. One major set of concerns in agriculture is pollution of underground or surface water through fertilizer and pesticide run-off or leaching, micro-bacteriological contamination from animals or workers, and effluent discharge from processing plants. In the case of soils, the main issues are pesticide residues and depletion of soil fertility. Risks to air quality can come from excessive formation of dust particles due to lack of soil cover and over-tillage; and from smoke, gases, or odors given off by processing plants. The main concerns with respect to biodiversity are uptake of agrochemicals by animals or plants, and the destruction of natural flora or fauna caused by loss of forests, marshlands, or other habitats of importance; and their replacement by monoculture or extensive livestock

21

grazing operations. With respect to cultural heritage, the main issues are typically loss of traditional rural ways of life such as pastoralism, and destruction of historical landmarks.

Again, because environmental standards affect the public welfare, they are promulgated mostly by government––often under pressure from particular environmental interest groups. However, private standards are emerging as well. For example, the “bird-friendly” designation is now being applied to some coffees that are grown without applying granulated agrochemicals.

Service: This last area of application for standards is much less documented and much less tangible than the previous four. Service is becoming crucial for offshore growers and shippers who want to consolidate a major position in major global supply networks. Several megatrends in the United States food system have caused service to assume greater importance as a competitive requirement (or tool, as the case may be). One trend has been the rapid expansion of food service, which was stimulated by growth in the hotel, restaurant, and institutional food retailing system as people began to eat away from home more frequently. Since food service purveyors handle some 4000 items, of necessity they need to rely on standards for both products and level of service. Another has been the emergence of alternative retailing channels for food and dry goods that compete with the traditional grocery store. These include supercenters (for example, Wal-Mart), warehouse clubs, other mass merchandisers, dollar stores, convenience/gas outlets, and even drug stores. Wal-Mart’s pioneering approach of relentlessly squeezing costs of supply chains and eliminating middlemen who do not add value has put a premium in service as well. A third major trend worth mentioning has been consolidation among the major retailing, distribution, manufacturing, processing, and importing companies. As buying offices have shrunk relative to the physical volume they have to manage, suppliers who can provide better service are strongly favored. A fourth big trend has been overhaul of procurement, distribution, and marketing practices. Again the use of technologies such as scanning and electronic data interchange, the application of new techniques such as “category management” and “efficient consumer response,” and growing reliance on preferred supplier arrangements and longer-term contracts all favor seamless integration and cooperative behavior within global supply networks.

It is difficult to generalize about service standards, because they can vary by stage in the supply chain (exporting vs. distribution), by product form (fresh vs. processed), by product type (raw vs. packaged), by source (domestic vs. foreign), and by enterprise. Moreover, they are evolving rapidly in response to changes in the structure and conduct of the food industry. Nevertheless, it is possible to identify the different aspects of service that foreign suppliers may have to address. These may include any or all of the following:

Product improvements: Custom packs (size, count, place-packed), consumer packs, high-graphics packaging, minimal processing, private label

Quality and safety assurance: Certification, audits, bar-coding, radio frequency identification device (RFID) applications, trace-forward and trace-back systems

Incentives: Slotting fees, failure fees, volume rebates, nonvolume rebates Promotional support: Allowances, ad slicks, brochures, press kits Merchandising support: Product look-up (PLU) stickers, point of purchase (POP) materials,

signage, in-store replenishment, cross-merchandising, in-store sampling Information management: Software upgrades, situation and outlook reporting Telecommunications: E-commerce, electronic data interchange (EDI) Capital investment: Food safety systems (such as ozone), dedicated or automated distribution

centers, regional fresh-cut processing facilities.

Service standards present a special challenge to international development programs because (1) they are not transparent; (2) they are not uniform; (3) they are sometimes proprietary; and (4) they may be applied

22

in a discriminatory manner. While some major food retailing chains promulgate and publicize specifications for product quality as well as company codes of practice that cover SPS (including traceability and certification), labor, and environmental matters, the other aspects of service that they expect often remain unwritten. Yet, at some point, best practices by leading firms tend to evolve into generally accepted private standards.