agria investor presentation apr 2012 web final

TRANSCRIPT

Agria Corporation (NYSE:GRO)Investor presentation

April 2012

Agria is:

An International Agriculture Company.

Operating 3 Businesses: International Seeds China Seeds and Operating 3 Businesses: International Seeds, China Seeds and Agriservices.

Helping farmers increase productivity through innovativeHelping farmers increase productivity through innovative agricultural best practices and advanced technologies.

Exploiting international agricultural trade opportunities betweenExploiting international agricultural trade opportunities between China and global markets, including New Zealand, Australia and South America.

A publicly traded company listed on the New York Stock Exchange (NYSE) under ticker GRO.

Agria’s 3 Operating Business

China Seeds

• Edible corn seed, field corn seed and vegetable seeds

International Seeds

• Leading seeds supplier in the southern hemisphere

Agriservices

• New Zealand’s pre-eminent rural services business facilitating purchase of major inputs and sale of• Strong R&D capabilities including

partnership with China Academy of Agricultural Sciences (CAAS)

• Proprietary rights to market leading variety of ‘sticky’ edible corn seed

• New Zealand 60% forage seed market share

• Australia 40% forage seed market share

purchase of major inputs and sale of major outputs for NZ farmers

• Key inputs sold include agrichemicals, feed and seeds both through on-farm sales

i d i idvariety of sticky edible corn seed and best new variety of field corn seeds

• Sales to large scale farmers, food manufacturers and distributors in 30 provinces in China

• South America growing market share

• Portfolio of grasses, legumes, brassicas and herbs seeds

• Unique and defendable IP tailored

representatives and a nationwide chain of over 100 retail stores

• Leading livestock broker with national network of sales agents and yards for sheep, beef, dairy and deer provinces in China

• Production bases in Gansu and Xinjiang provinces

• Turnover RMB 61 million; operating profit RMB 20 million for six months

• Unique and defendable IP tailored to specific climates

• Globally leading R&D both in-house and through nine partnerships with research institutes in five countries

farmers, processors and importers/exporters

• Procurement, freight, sales and export of New Zealand Wool

Additi l i t fpended June 2011 • Also incorporates grain and animal

nutrition businesses

• Turnover NZD 420 million; operating profit NZD35 million for 12 months ended June 2011 (note 1)

• Additional services to farmers including irrigation and pumping solutions, real estate agents, agriculture training provision

• Turnover NZD 821 million; months ended June 2011 (note 1) operating profit NZD 26 million for 12 months ended June 2011 (note 1)

Note 1: Financials for international seeds and Agriservices sourced from PGW annual accounts. Agria only consolidated these businesses from 30 April 2011.

International Seeds – Financial Overview

Year ended 30 Jun 2010 Year ended 30 June 2011

NZD million USD million NZD million USD million

Revenue

- Seeds and grain 255 209 268 220

- Agrifeeds 44 36 56 46

- South America 85 70 96 79

- Total 385 316 420 344

EBITDAEBITDA

- Seeds and grain 32 26 28 23

- Agrifeeds 5 4 5 4

- South America 4 3 4 3

T t l 41 34 38 31- Total 41 34 38 31

Operating profits 38 31 35 29

Notes:1. The NZD results are extracted from PGG Wrightson’s filings.2. Agria started consolidating PGG Wrightson following completion of the partial offer in April 2011, therefore the results prior to that

date do not appear in Agria’s results3. USD figures are provided for reference only and are translated at exchange rate of NZD 1: USD 0.82

China Seeds – Financial Overview

Year ended 31 Dec 2010 (audited) 6 months ended 30 June 2011 ( )(unaudited)

RMB million USD million RMB million USD million

Revenue

- Edible corn seeds 29 4.4 27 4.1

- Field corn seeds - - 34 5.3

- Total 29 4.4 61 9.4

Gross profit

- Edible corn seeds 12 2 6 15 2 3Edible corn seeds 12 2.6 15 2.3

- Field corn seeds - - 12 2.9

- Total 12 2.6 27 4.2

Gross margin

Edibl d 40% 55%- Edible corn seeds 40% 55%

- Field corn seeds - 37%

- Total 40% 45%

Operating costs (note 3) (7) (1.1)

Operating profit 20 3.1

Notes:1. Agria changed its fiscal year end in 2011 in order to align year ends with its largest subsidiary, PGG Wrightson. 2. The next set of audited full year results will be for the year ended 30 June 20123. Prior to the 6 months period ended 30 June 2011, Agria did not separate operating costs between it’s China seeds division and

central overheads

Agriservices – Financial Overview

Year ended 30 Jun 2010 Year ended 30 June 2011

NZD million USD million NZD million USD million

Revenue

- Merchandising 542 444 566 464

- Livestock 87 71 140 115

- Other agriservices 66 54 115 94

- Total 695 570 821 673

EBITDAEBITDA

- Merchandising 22 18 24 20

- Livestock 13 11 16 13

- Other agriservices (8) (7) (10) (8)

T t l 27 22 30 25- Total 27 22 30 25

Operating profits 24 20 26 21

Notes:1. The NZD results are extracted from PGG Wrightson’s filings.2. Agria started consolidating PGG Wrightson following completion of the partial offer in April 2011, therefore the results prior to that

date do not appear in Agria’s results3. USD figures are provided for reference only and are translated at exchange rate of NZD 1: USD 0.824 Merchandising comprises rural supplies and fruitfed4. Merchandising comprises rural supplies and fruitfed5. Other agriservices comprises the business units detailed in this presentation and the regional overhead 6. There was a reclassification of certain costs during 2011 which transferred costs from Agriservices to Central costs

International Seeds Division

International Seeds Structure

Corporate

NZ Australia SouthAmerica International R & D Production

Turf

Contract growersJoint

ventures

Our International Seeds division also comprises grain and animal nutrition businesses and is part of PGG Wrightson, our New Zealand listed subsidiary

Market Leader in Temperate Forage SeedsMarket Leader in Temperate Forage Seeds

Key features Business unit revenue (FY10)

13% Leading seeds supplier in the Southern Hemisphere

Clear leadership in forage seeds across current focus markets:– New Zealand c.60% market share of forage seeds– Australia c.40% market share of forage seeds– South America growing market share

26%

32%

5%

South America growing market share

Unique and defendable IP tailors proprietary seed varieties to specific temperate climatic conditions

Commodity seeds also an important component, establishing customer relationships and preserving market position

Source: PGW

24%

NZ Forage AUSA TurfInternational

Approximately 400 staff, including 30 focused on R&D activities

Unit revenue split (NZ$m)

Source: PGW

World’s top 12 seed companies250250300

0 51.01.52.02.53.03.54.04.55.0

Sale

s U

S$bn

50

100

150

200

Reve

nue

(NZ$

m)

50

100

150

200

Reve

nue

(NZ$

m)

1.0

2.0

3.0

4.0

Sale

s US$

bn

0

50

100150

200

250

Source: PGWSource: ETC Group

0.00.5

Mon

sant

o

Dup

ont

Syng

enta

Limag

rain

LOL

KWS

Baye

r

Saka

ta

DLF

Taki

i

Bare

nbur

g

PGW

S

Seed Pasture and turf seed

2007 2008 2009NZ Forage Au ForageTurf InternationalOther

2008 2009 2010NZ Forage Au ForageTurf InternationalOther

0.0

Mon

sant

o

Dupo

nt

Syng

enta

Lim

agra

in

LOL

KWS

Baye

r

Delta

Saka

ta

DLF

Bare

nbur

g

PGW

Pasture and turf seed Seed

0FY08 FY09 FY10

NZ Forage AUSA TurfInternational

pNote:1 LOL is Land O’ Lakes

Extensive Product Portfolio Caters to a Range ofExtensive Product Portfolio Caters to a Range of Pastoral Requirements and Climatic Conditions

B d d t tf li t i d ithi t i Volume by product (NZ) Broad product portfolio across categories and within categories

Helps meet diverse customer requirements and account for specific geographic requirements

PGW Seeds strong in all forage product categories – c. 85% market share in NZ brassica market

Volume by product (NZ)

42%

14%

9%

6%

Seed coating and branded products create opportunities for additional margin

Developing food seed proposition (pea, beans)

12%15%

2%

9%

Key seed product overview

12%

Perennial Ryegrass Hybrid Ryegrass Italian RyegrassOther Grasses White Clover Other legumesBrassicas

Category Product Type s DescriptionForage grasses • Perennial ryegrass • Core to pastoral farming systemForage grasses • Perennial ryegrass

• Hybrid ryegrass• Italian ryegrass• Tall fescue

• Core to pastoral farming system• Grasslands Innovation is core development partner

Forage Legumes • Clovers• Lucerne

• Assists with p asture renewal• Grasslands Innovation is core development partner

• Lotus• Fulla

Forage Brassicas • Swede• Turnip• Rape• Kale

• Supplementary feed• Forage Innovation is core development partner

Forage Herbs • Chicory• Plantain

• Enhances forage nutritional quality• Various develop ment partners

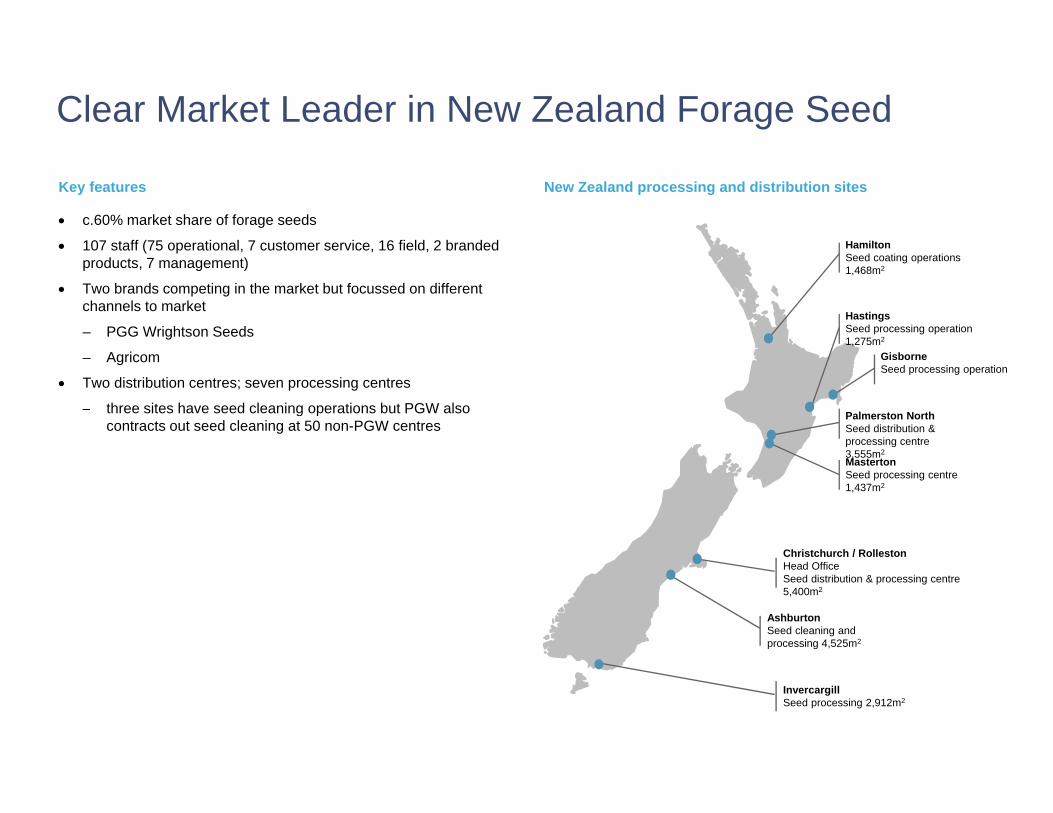

Cl M k t L d i N Z l d F S dClear Market Leader in New Zealand Forage Seed

Key features New Zealand processing and distribution sites

c.60% market share of forage seeds

107 staff (75 operational, 7 customer service, 16 field, 2 branded products, 7 management)

Two brands competing in the market but focussed on different channels to market

HamiltonSeed coating operations 1,468m2

channels to market

– PGG Wrightson Seeds

– Agricom

Two distribution centres; seven processing centres

three sites have seed cleaning operations but PGW also

HastingsSeed processing operation 1,275m2

GisborneSeed processing operation

– three sites have seed cleaning operations but PGW also contracts out seed cleaning at 50 non-PGW centres

Palmerston NorthSeed distribution & processing centre 3,555m2MastertonSeed processing centre 1,437m2

Christchurch / RollestonHead OfficeSeed distribution & processing centre 5,400m2

InvercargillSeed processing 2,912m2

AshburtonSeed cleaning and processing 4,525m2

#1 Market Position in Australian Forage Seeds#1 Market Position in Australian Forage Seeds

Key features

c 40% market share of forage seeds

Australian processing and distribution sites

c.40% market share of forage seeds

82 FTEs

Two proprietary brands:

– Wrightson Seeds Australia Keithprocessing, storage, distribution

– Agricom

Two seed distributors

– AusWest Seeds

– Stephens Pasture Seeds

Brisbane-AusWestdistribution

Armidale-AusWestdistribution

Expanding production capability with Keith Seeds acquisition

MelbourneHead Office, coating and mixing

Forbes/Orange-AusWestdistribution, coating, processing

distribution

Mt Gambier-SPSdistribution

Ballarat-SPSresearch, distribution, coating

Leading Provider of Turf Seeds to Stadia and Sports ClubsKey features

Supplies turf for stadia sports clubs and golf

Australasian Turf sites

Supplies turf for stadia, sports clubs and golf courses

Generally sell direct to consumer in New Zealand and through distributors in Australia

Strong synergies with Production, R&D and L i ti it i b dLogistics capacity in broader company

15 staff

AucklandOffice & Dispatch site

Mt Stewart Office & Dispatch site

ChristchurchOffice & Dispatch site

MelbourneOffice & Dispatch site

Office & Dispatch site

Expanding Presence in South AmericaExpanding Presence in South America

Key features South American sites

MontevideoWrightson PAS Head Office

Porto AlegreNZ Ruralco office

South America’s leading supplier of proprietary and commodity forage seed products with three key brands: Alfalfares in Argentina, and Wrightson PAS and Agrosan in Uruguay

all three businesses distribute to rural retailers and also sell direct to farmers

MontevideoAgrosan Head Office

OmbuesAgrosan Branch

#1 market position in Uruguay through Wrightson PAS and Agrosan with approximately 65% of the US$80m market

strong market position in Argentina through 51% ownership of Alfalfares and 50:50 ACA joint venture

67 staffMercedesAgrosan Branch

Buenos AiresAlfalfares Head Office

67 staff

PehuajoAlfalfares Branch

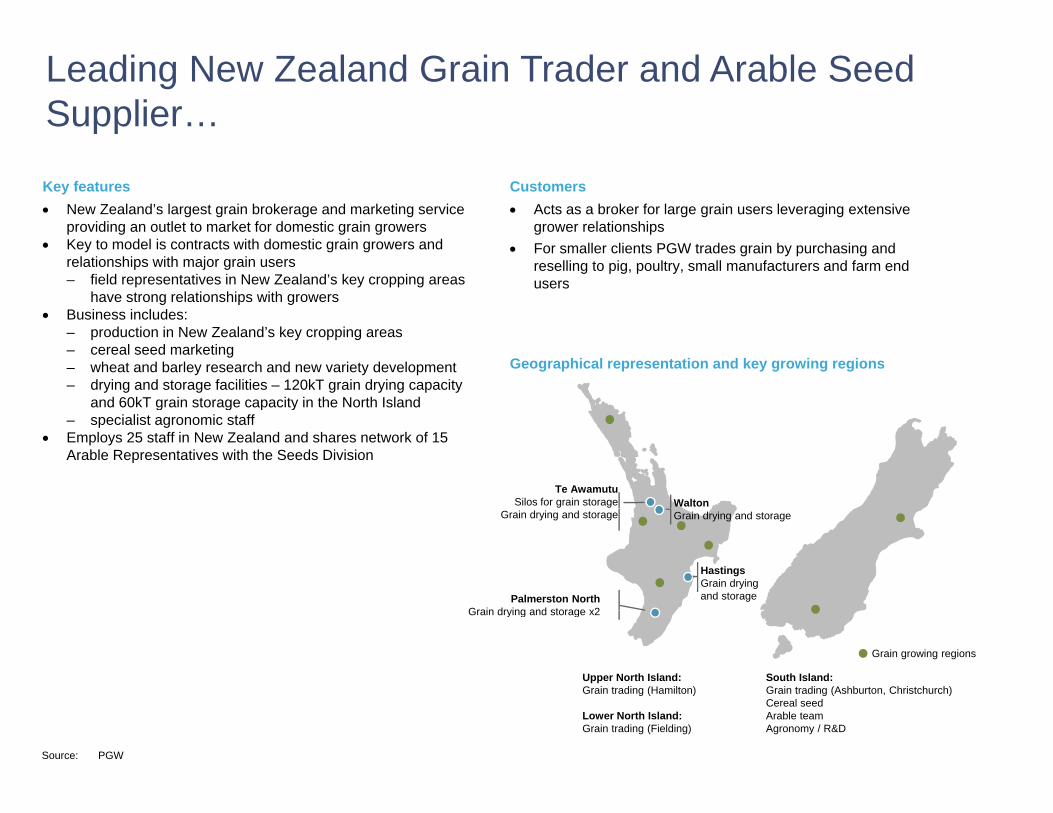

Leading New Zealand Grain Trader and Arable Seed S liSupplier…

Key features Customers New Zealand’s largest grain brokerage and marketing service

providing an outlet to market for domestic grain growers Key to model is contracts with domestic grain growers and

relationships with major grain users– field representatives in New Zealand’s key cropping areas

have strong relationships with growers

Acts as a broker for large grain users leveraging extensive grower relationships

For smaller clients PGW trades grain by purchasing and reselling to pig, poultry, small manufacturers and farm end users

Business includes:– production in New Zealand’s key cropping areas– cereal seed marketing– wheat and barley research and new variety development– drying and storage facilities – 120kT grain drying capacity

and 60kT grain storage capacity in the North Island

Geographical representation and key growing regions

and 60kT grain storage capacity in the North Island– specialist agronomic staff

Employs 25 staff in New Zealand and shares network of 15 Arable Representatives with the Seeds Division

Te AwamutuSilos for grain storage Walton

Palmerston NorthGrain drying and storage x2

Grain drying and storage

HastingsGrain drying and storage

Grain drying and storage

Grain drying and storage x2

Grain growing regions

Upper North Island:Grain trading (Hamilton)

L N th I l d

South Island:Grain trading (Ashburton, Christchurch)Cereal seedA bl t

Source: PGW

Lower North Island:Grain trading (Fielding)

Arable teamAgronomy / R&D

China Seeds Division

St t i R h & D l t P t hiStrategic Research & Development Partnerships• China National Academy of Agricultural Sciences

– Established in 1957 CNAAS is the largest agricultural research organization in ChinaEstablished in 1957, CNAAS is the largest agricultural research organization in China.

– Comprises 39 research institutes and employs over 5,000 scientists and research engineers

– Covers all major areas of the agricultural sector including advanced research in the development of both horticulture and livestock.

Through its network of research institutes CNAAS controls one of the largest seed banks in the world– Through its network of research institutes, CNAAS controls one of the largest seed banks in the world.

– In 2009 Agria entered into a strategic co-operation framework agreement with the China National Academy of Agricultural Sciences (“CNAAS”) providing for future co-operation across the spectrum of agricultural research.

– Agria has also entered into an investment agreement with CNAAS and its affiliates, under which Agria will invest RMB35 million into Zhongnong, a company previously wholly owned by CNAAS and its affiliates with priority rights toRMB35 million into Zhongnong, a company previously wholly owned by CNAAS and its affiliates with priority rights to accept the transfer of all existing and future cultivated seed varieties owned by CNAAS and its affiliates for the purposes of commercialization.

– Through this arrangement we have already secured the rights to Zhong Dan 909

Illustrative R&D pipeline

Selection

Approval

Breeding1-5 years

Commercialisation1-3 years

Testing2-3

years

Attractive Commercial Product PortfolioAttractive Commercial Product Portfolio

• Edible corn seeds - sticky

– North China market focusNorth China market focus

– Key product: JKN2000 – market leading position with 13% market share

– Pipeline products: Jin Tian Nuo2000B, Jin Ke Tian183 and Jin Ke Tian158

> Won three of top four positions at China’s 7th National Edible Corn Conference held in Beijing in 2011

> Competition comprised 160 edible corn seed varieties - group of leading corn seed experts from China’s research institutes and international companies evaluated edible corn seed varieties based on field performance and taste and awarded recommendations to the top four performing varieties entered

• Edible corn seeds - sweet

S th Chi k t f– South China market focus

– Under development

• Field corn seeds

– Key product Zhong Dan 909 – advanced attributes - high yield, antiviral, anti-insect, lodging resistance

– Launched in October 2011 following agreement with China National Academy of Agricultural Sciences (“CNAAS”) for the Agria to be licensed rights to its commercialization

– Zhong Dan 909 had recently been awarded nationally approved status by the Ministry of Agriculture in China. For the past two years it has been ranked as the number one field corn variety in national certification tests hosted by Ministry of Agricultureof Agriculture

– The qualities of Zhong Dan 909 make it suitable for sale in the central part of China which is one of the largest corn seed markets in China, representing approximately 40% of national yield for field corn

– Previously Agria’s field corn activities were focused around our 49% owned associate Ganxin in which we invested in 20102010

Strong Relationships with the Chinese GovernmentStrong Relationships with the Chinese Government

• Government grantGovernment grant

– In September 2011, we received first stage of a grant for RMB6 million

– Grant made by Science and Technology division of the Beijing Government one of the most prolific research funders in China

• Use of grant• Use of grant

– Funding of joint R&D into adaptation of six grass seed varieties that were originally developed in conjunction with our subsidiary PGG Wrightson in New Zealand with a view to the seed varieties’ application in China

– China has in total 390 million hectares of natural grassland (four times the area used for arable farming) but much of this is of very low productivity. y p y

– By working jointly with our and our partners’ scientists in China, those in New Zealand and our subsidiary PGG Wrightson, aim is to develop high technology content grasses to allow for the increase of productivity of this grass land.

– The R&D project also intends to develop GAP (Good Agricultural Practice) in the development of grass seed technology by following the high standards set in New Zealand

– Helps Agria to secure a pipeline of next generation seed technologies for future commercialization.

– It will also serve to strengthen the PGW brand in China

Agriservices division

Compelling Portfolio of Complimentary Businesses, Primarily Serving New Zealand Farmers

Rural Supplies 91 rural supply stores and on-farm technical advice

Fruitfed Supplies 18 retail stores and technical support for horticulture and viticulture

Livestock National agent platform buying and selling livestock for clients

Wool Procurement, logistics, sales and export of wool

Agr

Real Estate Specialty rural real estate agents in New Zealand

Irrigation & Pumping Design and installation for agriculture and horticulture

iservice

Insurance Marketing of insurance products brokered by Aon

Agriculture New Zealand Provider of agriculture training

es

South America Rural supplies business

Our Agriservices business is part of PGG Wrightson our New Zealand listed subsidiaryOur Agriservices business is part of PGG Wrightson, our New Zealand listed subsidiary

R l S liRural SuppliesKey features• Provider of goods and services to the rural sector • Approximately 40,000 customer accounts across New Zealand

Customers

– key product categories include agri-chemicals, stockfeed, seed and fencing

• On-farm technical sales representatives account for c.70% of revenue, providing advice and technical assistance together with supply orders

• Majority of revenue derived from sheep and beef (or mixed land use farms) and dairy

• Majority of customers are owner-operated farmers, but with share of corporate farmers (e.g. Landcorp) increasing

with supply orders

• Remaining 30% of revenue through a national network of 91 retail stores

• Approximately 350 employees with approximately c.70% in-store employees and the remainder technical sales representatives and support staff

Geographical representation

Upper South Island# Stores: 6

Northland# Stores: 10

South Auckland/Waikato# Stores: 12

Bay of Plenty / King Country# Stores: 6

Canterbury# Stores: 17

Otago# Stores: 12

S thl d

East Coast# Stores: 5

Southland# Stores: 10Taranaki/ Manawatu / Wairarapa

# Stores: 13

F itifi d S liFruitified SuppliesKey features Customers

• Leading horticulture service and supply business, providing grower clients with agronomic advice, technical expertise and an extensive product range

• Fruitified provides input materials for orchards including chemicals, fertilisers, pollination products and frost protection products

• Customers are primarily in:

– Viticulture

– Pipfruit

– Vegetables; andproducts

• 18 national retail outlets supported by 60 technical field staff that provide advice on soil, irrigation design, pest and disease identification, treatment plans and monitoring systems

– kiwifruit

Geographical representation

KerikeriMotueka

Blenheim

Christchurch

Katikati

Kumeu

Motueka

Pukekohe

Te Puke

Richmond Whangarei

Amberley

AlexandraCromwell

Gisborne

Hastings

Ohakune

Palmerston NorthLevin

LivestockLivestock

Key features Customers

• Sales agent for sheep, beef, dairy and deer farmers, meat processors and livestock importers and exporters

• Major service is trading livestock through auctions, private on farm sales, online or direct to meat processors

• Strong adviser relationship with agents offering genetics,

• Represent farmers trading stock to other farmers (“store”) or matching farmers to meat processors (“prime”), such as Silver Fern Farms, Alliance, Bernard Matthews, Affco, ANZO, etc

• Trading occurs between farmers before slaughter based on available pasture i.e. dry high country farms sell lambs to those with available grass for fatteningstocking, animal evaluation, valuation and strategic advice to

help facilitate a transaction through PGW

• PGW has 273 agents supported by 48, owned or co-owned sales yards and has just developed a web based platform in New Zealand

with available grass for fattening

• Sheep and beef are key markets with PGW’s market share, sold through saleyards, being 63% and 60% respectively

Geographical representation - stock yard infrastructure

Kaikohe

Coroglen

Dargiville

Frankton

a o e

Kauri

MorrinsvillePaeroa

RangiuruTe Awamutu Tirau

Tuakau

Wellsford

BlenheimBrightwater

Canterbury Park

CheviotCulverdenHawarden

Sheffield

Tinwald

Katikat

ReporoaMahoenui

Tekapo

Ross

Haast

Awakino

DannevirkeFeildingFordell Hunterville

Inglewood

Levin

M t t

Matawhero

RaetihiStortford Lodge

StratfordTaihape

Taumarunui Taupo

Te KuitiTirau

Allanton

BalcluthaCharlton

Invercargill

Milton

Owaka

Palmerston

Temuka

WaiarekaWaipiataWairoa

Tuatapere

Cromwell

Omarama

Tekapo

Hakataramea

Masterton

PGW 100% ownershipPGW investment (<100%) Non-PGW stock yards

Wairarapa

Large and Growing South American Presence

• PGW established a presence in the stock and station sector through the acquisition of a number of small retail operators, which followed the establishment of New Zealand Farming System Uruguay (NZFSU) in 2005.

Subsequent acquisitions have been successfully integrated and are

Irrigation

S

Business descriptionBusiness name

• Subsequent acquisitions have been successfully integrated and are well positioned to take advantage of improving market conditions. The group represent a significant participant in Uruguay’s agriculture sector, and also form an established platform for future growth into larger South American markets such as Argentina and Brazil.

Vet Supplies

Livestock, Real Estate, Wool

• These entities have mixed ownership structures ranging from complete ownership to minority shareholdings.

PGW Holding Structure and Results

Agria Asia and PGW - Structure

Agria Corporation Ngai TahuNew Hope

80.81% 11.95% 7.24%

Agria Asia

Agria Singapore

100%

NZ$34m Convertible

redeemable note

Acquisition debt (at acquisition):Bank debt NZ$53mLivestock Improvement Corporation NZ$10m

Agria Singapore

50.01%

(at acquisition)

Notes:CRN was redeemed for NZ$34m cash in December 2011

PGG Wrightson

AgriservicesInternational Seeds

Our Diverse Strategic Investment Partners Are Able to H l D i th S f PGG W i ht d E lHelp Drive the Success of PGG Wrightson and Explore Other Opportunities.

New Hope

• One of China’s first private companies established in 1982 and has grown to become one of China's largest

Ngai Tahu

• Investment company representing the largest group of indigenous iwi people in the South Island of New Zealand

LIC

• Livestock Improvement Corporation is a co-operative owned by individual dairy farmers of New Zealandbecome one of China s largest

agricultural and food corporations

• New Hope’s revenue for 2009 was approximately US$10 billion. The company employs more than 60,000 staff and continues to grow rapidly.

the South Island of New Zealand

• Founded by Government Act in 1996 for protecting and advancing the Ngai Tahu iwi’s collective interests and ensure that the benefits of the settlement are enjoyed by Ngāi Tahu Whānui now

farmers of New Zealand

• Farm improvement company providing a diverse range of products and services to the dairy, beef and deer industries both in New Zealand and around the world. g p y

• It is involved in

•agribusiness and food (accounting 85% of revenue)

•chemicals and resources

j y y gand in the future

• Significant business interests throughout New Zealand including:

• Substantial property and land investments

• Origins, which date back to the early 1900s, lie in animal performance management tailored to an innovative and wide range of products and services that deliver profit to a wide range of li k f• finance and investment

• real estate and infrastructure.

• The agribusiness and food sector of New Hope is the largest animal feed producer and one of the largest

investments

• Seafood operations

• Tourism attractions

livestock farmers

• Current operations include:

• Beef, deer and dairy animal recording,

• Dairy herd testing and milkproducer and one of the largest suppliers of meat, egg and dairy products in China.

•In addition, New Hope is the largest shareholder of MinSheng Bank (China’s seventh largest commercial bank)

• Dairy herd testing and milk analysis laboratories,

• Progeny testing for the dairy and deer industries,

• DNA analysis across species –b f d i t d ig ) beef, dairy, goats and pigs, artificial breeding for the beef, dairy and deer industries.

Collaborating to Further Enhance PerformanceCollaborating to Further Enhance Performance

• Representative office for PGG Wrightson

– PGW is in the process of establishing a representative office in Beijingp g p j g

• Live Export

– Strong demand from China dairy producers for high quality milking cows

– Under Chinese regulations, cows can only be imported from New Zealand, Australia or Uruguay

– Agria uniquely positioned to source livestock from these markets and arrange logistics for import to China and sale to major dairy– Agria uniquely positioned to source livestock from these markets and arrange logistics for import to China and sale to major dairy companies

• Sale of grass seeds

– Import of PGG Wrightson’s existing high quality grass seed for the China market

– Support from Beijing government through grant for research into adapting varieties to be more suitable for range of differentpp j g g g g p g gChinese climatic conditions

• China sourcing for merchandising

– Facilitation of sourcing of products from China for sale through agriservices division

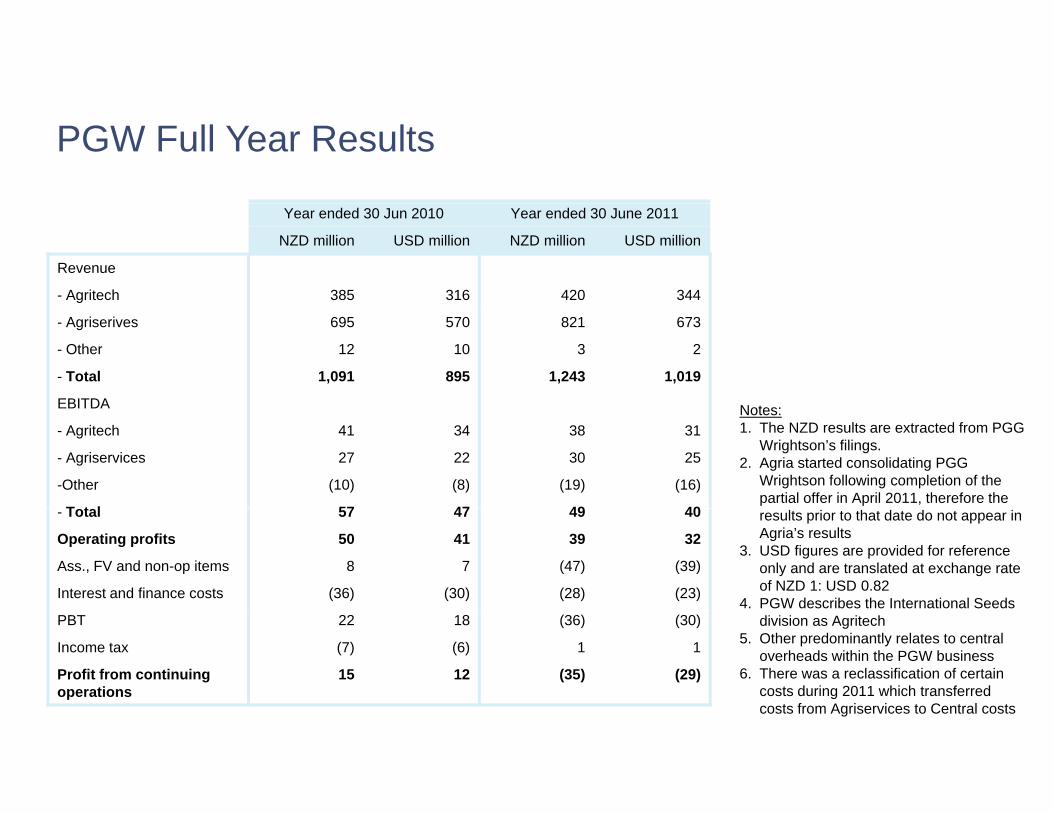

PGW Full Year Results

Year ended 30 Jun 2010 Year ended 30 June 2011

NZD million USD million NZD million USD million

Revenue

- Agritech 385 316 420 344

- Agriserives 695 570 821 673

- Other 12 10 3 2

- Total 1,091 895 1,243 1,019

EBITDA N tEBITDA

- Agritech 41 34 38 31

- Agriservices 27 22 30 25

-Other (10) (8) (19) (16)

T t l 57 47 49 40

Notes:1. The NZD results are extracted from PGG

Wrightson’s filings.2. Agria started consolidating PGG

Wrightson following completion of the partial offer in April 2011, therefore the

- Total 57 47 49 40

Operating profits 50 41 39 32

Ass., FV and non-op items 8 7 (47) (39)

Interest and finance costs (36) (30) (28) (23)

results prior to that date do not appear in Agria’s results

3. USD figures are provided for reference only and are translated at exchange rate of NZD 1: USD 0.82

4. PGW describes the International Seeds PBT 22 18 (36) (30)

Income tax (7) (6) 1 1

Profit from continuing operations

15 12 (35) (29)

division as Agritech 5. Other predominantly relates to central

overheads within the PGW business6. There was a reclassification of certain

costs during 2011 which transferred costs from Agriservices to Central costscosts from Agriservices to Central costs

PGW Interim Results

6 mths ended 31 Dec 2010 6 mths ended 31 Dec 2011 Change

NZD million USD million NZD million USD million %

Revenue

- Agritech 187 153 188 154

- Agriserives 426 349 503 412

- Other 4 3 3 2

- Total 617 506 694 569 + 12%

EBITDA N tEBITDA

- Agritech 13 11 12 10

- Agriservices 13 11 21 17

- Other (12) (10) (11) (9)

T t l 14 11 22 18 + 57%

Notes:1. The NZD results are extracted from PGG

Wrightson’s filings.2. Agria started consolidating PGG

Wrightson following completion of the partial offer in April 2011, therefore the

- Total 14 11 22 18 + 57%

Operating profits 10 8 18 15 + 80%

Ass., FV and non-op items (6) (5) (6) (5)

Interest and finance costs (11) (9) (9) (7)

results prior to that date do not appear in Agria’s results

3. USD figures are provided for reference only and are translated at exchange rate of NZD 1: USD 0.82

4. PGW describes the International Seeds PBT (7) (6) 3 2

Income tax - - - -

Profit from continuing operations

(7) (6) 3 2

division as Agritech 5. Other predominantly relates to central

overheads within the PGW business6. There was a reclassification of certain

costs during 2011 which transferred costs from Agriservices to Central costscosts from Agriservices to Central costs

Central Overhead and Balance Sheet Overview

Agria’s Central Costs• Six months to 30 June 2011

– As reported in the transition 20F for the 6 months period ended 30 June 2011 Agria’s central costs amounted toAs reported in the transition 20F for the 6 months period ended 30 June 2011, Agria s central costs amounted to RMB51 million (US$8 million)

– These costs included a portion of the costs incurred in relation to the partial takeover of PGG Wrightson which completed in April 2011

– Additionally these costs include non-cash amortisation of land use rights of RMB10 million (full year charge RMB20 y g ( y gmillion) in respect of leased land on which rents have already been paid in full for the life of the leases

– These costs also include non-cash share amortisation expenses in the period of RMB4 million

Balance Sheet Overview30 June 2011

RMB million USD million

Current assets

- Cash and equivalents 94 15Cash and equivalents 94 15

- Restricted cash 456 71

- AR, inventories and prepayments 2,680 415

- Assets held for sale 2,710 419

- Other current assets 141 22Other current assets 141 22

- Total 6,081 941

Non-current assets

- Property plant and equipment 511 79

- Intangible assets and goodwill 1,237 191Intangible assets and goodwill 1,237 191

- Other non-current assets 207 33

- Total 1,955 303

Current liabilities

- Short-term bank borrowings 486 75g

- Accounts payable and accrued expenses 1,259 195

- Liabilities held for sale 2,233 345

- Other current liabilities 28 5

- Total 4,006 620,

Non-current liabilities

- Long-term bank borrowings 1,229 190

- Other non-current liabilities 137 21

- Total 1,366 211,

Total Equity 2,665 412

Non-controlling interest 1,216 189

Total Company shareholder’s equity 1,449 224

Agria’s Mission Statement

“T b th t l i t ti l i lt“To be the truly international agriculture company based in China”

- Ability to take advantage of the best investment opportunities, irrespective of their geography and access the best teams to realise theirirrespective of their geography and access the best teams to realise their potentials

- Combine best international practice with local acumen to drive forward b i i Chi i ffi i t d li tcore businesses in China in efficient and compliant manner

- Be able to attract talent into senior management team with the rare combinations of international and China leadership abilities

- Exploit trade opportunities between China and investee markets (New Zealand, Australia, South America)

B d d i Chi d i it l k t th t th t t t- Be regarded in China and in capital markets as the team that can extract value from international investments

Agria Corporation (NYSE:GRO)Investor presentation

April 2012