agility of the swiss banking - deloitte · outsource 15 per cent of their activities mostly ... in...

TRANSCRIPT

Industrialisation Unlocking the efficiency and agility of the Swiss banking industry

August 2016

Contents

1. Introduction and key findings 01

2. Swiss banking: pressures continue 03

3. Industrialisation as response 06

4. Banks’ industrialisation plans 10

5. Our perspective: A call for action 22

Bibliography 29

Appendix 30

Authors & contributors 31

Acknowledgment We would like to thank all participating executives for their support in completing the survey and sharing their expertise in the interviews with us.

1. Introduction and key findings

Since the financial crisis the Swiss Banking industry has been under tremendous pressure. An unfavourable economic climate, rising expectations of empowered customers, increased regulatory focus and intense on- and offshore competition have reduced the revenue margins as a percentage of assets under management of Swiss banks by 21 per cent between 2010 and 2015. Combined with the emergence of FinTech entrants and disruptive technologies, these trends are creating an urgent need for innovation, and also to cut costs and improve agility in order to fund and execute new business models. In recent years many banks have limited themselves to taking only tactical cost reduction measures. We believe it is now time to improve agility and efficiency by industrialising how banks operate. The objective of industrialisation is to eliminate redundancies, re-engineer the value chain, automate and standardise processes wherever possible, while providing transparency about the profit of activities.

In collaboration with the Hochschule Luzern, Institut für Finanzdienstleistungen (IFZ), we have conducted an online survey and personal interviews with executives from Swiss banks on their current levels of industrialisation and their industrialisation strategies for the next five years. With this survey, we aim to contribute to a discussion about how Swiss banks can boost their efficiency and agility, and lead the way in the ongoing transformation within the industry. Over the following sections we will discuss survey findings covering major players in the Swiss banking landscape, the trends affecting Swiss banking, and the ways in which the industry is currently responding to them.

The concept of industrialisation in banking is explained, and the report will suggest, based on our experience working with many of the key players in the industry, how an industrialisation strategy can be used by banks to increase efficiency and agility. We conclude with a view on anticipated efficiency gains and on the potential future business and operating models for the industry to consider when developing an industrialisation strategy.

We believe it is now time to improve agility and efficiency by industrialising how banks operate. The objective of industrialisation is to eliminate redundancies, re-engineer the value chain, automate and standardise processes wherever possible, while providing transparency about the profit of activities.

1

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

88%say that industrialisation will reduce their costs

1. Industrialisation as a cureIn order to prepare for the new environment, banks must reduce cost. 88 per cent of banks regard industrialisation as a suitable way to reduce costs and increase scalability.

69%believe that industrialisation will speed up innovation

2. Boosted innovationFocussed efforts on industrialisation will improve the agility of banks and free up valuable resources that can be channelled into the development of other value-adding activities, such as freeing up management time for client-facing activities and innovative offerings.

50%of activities to be mostly or fully industrialised by 2021

3. High industrialisation ambitions of Swiss banksSwiss banks want to pursue industrialisation efforts energetically over the coming five years, during which they expect to industrialise 50 per cent of activities, covering key areas such as IT and operations, risk control and compliance as well as advisory and portfolio management.

100%of banks see resistance to change as a major challenge

4. Resistance to change as main challengeCultural resistance was found to be the main challenge for further progress in industrialisation. Successful industrialisation requires a clear mandate from the top of the organisation, but must also be embraced by all areas within the organisation. This requires investment in change management.

80%have at least partially standardised their processes across departments/countries

5. Process Excellence and Organisational Efficiency as a starting point for industrialisationBanks show the highest maturity in industrialisation in the areas of Process Excellence and Organisational Efficiency. The measurement of process performance through the use of KPIs is still fairly uncommon.

15%of activities are mostly or fully outsourced in 5 years

6. Outsourcing still developing todaySwiss banks are still somewhat hesitant about outsourcing, and only six per cent of activities are mostly or fully outsourced. However by 2021 banks aim to outsource 15 per cent of their activities mostly or fully. A notable example is IT which a large number of banks aim to have at least partially outsourced in the near future.

88%see data confidentiality as a major risk of outsourcing

7. The perceived risks of outsourcing are still largeMost bank executives are concerned about data security, overly-optimistic business cases and an erosion of service levels with outsourcing. However, they expect that by 2021 these risks will better mitigated, as the industry gains further experience in managing outsourcing arrangements.

62%operate nearshore, offshore and onshore low-cost locations

8. Talent considerations limit the possibilities of Location OptimisationWhile banks do utilise low cost locations currently, they do not aspire to increase the use of relocation of support services to low cost centres in Switzerland or abroad over the next five years. The main driver behind this is the lack of appropriate talent at alternative locations and management complexity.

48%apply Economic Value Management mostly or fully for clients and relationship managers

9. Economic Value Management still relatively rareMost banks mainly use Economic Value Management (EVM) to measure the profit contribution of clients and relationship managers. In future, banks will extend the use of EVM measurements to countries and products, in order to make decisions about where to channel scarce resources most effectively.

20%-30%

cost savings can be achieved by fully industrialising a bank

10. Industrialisation will drive down costsOur experience with clients, combined with the findings from the survey, suggests that the targeted industrialisation levels of Swiss banks should drive cost savings of 10-15 per cent, but banks could potentially save 20-30 percent of operating expenditures by fully implementing a rigorous industrialisation strategy. This would also drive a reduction in full time employee (FTE) numbers by 30-40 per cent including shifts to 3rd parties.

2

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

2. Swiss banking: pressures continue

2.1 Swiss banks under pressureThe Swiss banking industry has been under pressure in a number of ways in the aftermath of the financial crisis. An uncertain economic climate, ever-increasing customer expectations, and a restrictive regulatory landscape, together with disruptive new technologies, are increasing pressure on cost and profitability to such an extent that most banks need to review their business models and operational configurations.

The growing preference among clients for onshore banking, combined with stronger competition both on- and offshore, weakens margins1, while regulatory developments in Switzerland and elsewhere are putting ever-increasing pressures on the banking industry.2,3 Additional regulations require the establishment of new controls, processes and reporting requirements, which often offset any operational efficiencies achieved. Substantially increased capital and liquidity requirements force banks to decide whether certain business lines, markets and products should be continued or abandoned.4

In the current climate of economic uncertainty5, record-low interest rates and slow economic growth in developed economies reduce profit margins and limit opportunities to grow the client asset base. At the same time, non-banking players such as Google, Apple, and Facebook6 have both a commercial interest and the required global reach to disrupt the industry with technological innovations.7 Technological innovations are also being developed by a large number of start-ups in financial technology (FinTechs), challenging the way banks have traditionally served their clients.8 Above developments9 indicate that the banking industry needs to find new ways to service customers to remain competitive.

Figure 1. Key industry trends

On- and offshore competition

Increasing client expectations

Disruptive non-banking entrants

Technological innovation

Economic uncertainty

Cost focus to compensate for

declining revenue

Capital and liquidity

requirements

Regulatory change

Banks under pressure

3

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

2.2 Performance of Swiss banks in recent years The financial results of Swiss banks in recent years reflect some of these trends and shed light on the actions taken by banks so far; but they also show clearly that further transformational changes are required.

Revenue margins declined significantly over the past few yearsThe revenues of Swiss banks deteriorated substantially over the years following the financial crisis. The average revenue margin as a share of assets under management (a KPI for private banks but a measure also used frequently by other banks) fell by 21 per cent from 134bps in 2010 to 106bps in 2015 (-21%). This trend can be observed across all categories of banks in Switzerland. Looking at the net interest margin the picture is very similar, it fell by 19% from 2010 to 2015.

Banks have reduced costs mainly by cutting personnel costsSwiss banks have made efforts to reduce their operating costs, to counteract the decline in revenue margins. They have done so in recent years mainly by reducing their staff numbers (by six per cent) and average compensation (by five per cent). Over the same period, general and administrative expenses have risen significantly. One of the reasons for this rise in non-personnel expenses is the increasing use of outsourcing by banks as a means of cost reduction. An example of this trend is Deutsche Bank (Schweiz) AG, which outsourced its core banking technology and back office to Avaloq Sourcing in 2014, in order to focus on their core business activities.10

Figure 2. Revenue margins of Swiss banks*(as share of AuM)

bps

8090

100110120130140

201520142013201220112010

-21%

Source: Deloitte Banking Database

Figure 3. Net interest margins of Swiss banks*(as share of total balance sheet)

*excluding the two big banks

bps

90

100

110

120

201520142013201220112010

-19%

Figure 4. Personnel expenses, other operating expenses and number of employees in the Swiss banking industry

In b

n CH

F

0

10

20

30

201520142013201220112010

+29%

-13%

Source: Swiss National Bank, Deloitte calculations

132 133 129 127 124125

Personnel expenses Non-personnel expenses Number of employees (000s)

4

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

Swiss banks have kept their cost-to-income ratio stableWith these measures, Swiss banks have managed to keep their cost-to-income ratio more or less stable during the past few years. However operating return on equity has deteriorated, and pressure on the top line and the need to innovate remain.

Figure 5. Cost-income ratio of Swiss banks*

50%

55%

60%

65%

70%

201520142013201220112010

+0.5%

Source: Deloitte Banking Database

Figure 6. Operating return on equity of Swiss banks*

6%

8%

10%

201520142013201220112010

-16%

* excluding the two big banks

Economies of scale influence cost margins Some banks are more successful than others in managing their costs and profitability. Across levels of assets under management (AuM), and also within categories of banks, cost levels differ significantly between individual banks. The degree of correlation between a bank’s costs (measured as bps of AuM) and its size (measured by AuM) indicates the extent of economies of scale within the industry and the potential benefits of ongoing consolidation and measures for re-engineering the value chain.

Considering the revenues under pressure, banks will only be able to generate funds to innovate and adapt to ongoing disruptive changes in the industry by fundamentally increasing efficiency and cutting costs. With some of the ‘quick wins’ to reduce cost already utilised, there is a requirement for more comprehensive measures and a fundamental change in the banks’ business and operating models to realise sustainable efficiency gains.

R² = 0.1836

Cost

mar

gin

in b

ps o

f AuM

0

50

100

150

200

250

100 1,000 10,000 100,000 1,000,000

Figure 7. Size-cost relationship of Swiss banks in 2015*

Source: Deloitte Banking Database

AUM in CHFm

*excluding the two big banks

5

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

Having highlighted the challenges the Swiss banking industry is facing we propose industrialisation as a tool in response to cost and innovation pressures. In this chapter we introduce the concept and provide further details on the framework applied throughout our survey.

3.1 The concept of industrialisation The aim of industrialisation is to eliminate redundancies, source smartly, automate and standardise processes wherever possible. In the past the concept has been applied successfully in other industries in response to difficult market situations, by reducing the cost base and re-thinking the value creation process.

The crisis in the Swiss watch industry in the 1980s is an example, when the share of the Swiss watch manufacturers in the global market shrank dramatically following the introduction of a disruptive technology, the quartz watch (and the industry is again challenged today with the emergence of smart watches). A turnaround was achieved only after an impressive standardisation and automation process, led by Nicolas G. Hayek’s Swatch Group.11 This industrialisation effort involved a complete re-design of the clockwork, a drastic reduction in the number of parts used to build a watch, and a revolution in the manufacturing process, cutting the total labour costs significantly.

Another feature of this industrialisation process was the high level of innovation in materials, process and design. For example, traditional watch cases were built around the watch after the movement had been assembled; but using new materials and process innovation engineers were able to mount movements directly into the watch case. This re-design also made use of ultrasonic welding, eliminating the need for screws that were traditionally used to seal watches. Welding had a further positive impact on product quality, and the reduced number of parts made quality control much easier.12

The two industries share some characteristics. Both were global leaders for decades based on historical advantages (superior technological know-how in the case of watches, and favourable regulatory regimes and political stability for banking) until the emergence of disruptive technologies and structural change, such as the end of banking secrecy in Switzerland, challenged their competitive advantage. A reason why the watch industry slid into such a severe crisis was that it was unable to carry out the necessary changes quickly enough: this is a danger that Swiss banks need to avoid by taking measures towards industrialisation.

3. Industrialisation as response

6

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

Front-to-back service alignment

• Coordinate services along the value chain in order to maximise client- and service-orientation

• Focus on improving availability, service quality and processing improvements

Distinct process orientation

• Build banks’ operating models around processes • Steadily and consistently improve productivity of all processes

Cultural shift • Instil a distinct mind-set among staff to value efficiency and evolution • Reward employees for suggesting improvements and involve staff early in the change process

Resource optimisation • Introduce a meaningful performance measurement system aiming at optimising resource allocation

• “You can’t manage if you don’t measure”

Value chain decomposition

• Re-think your value chain regularly and source smartly • Be aware of core competencies and differentiating activities

Figure 8. Five principles of banking industrialisation

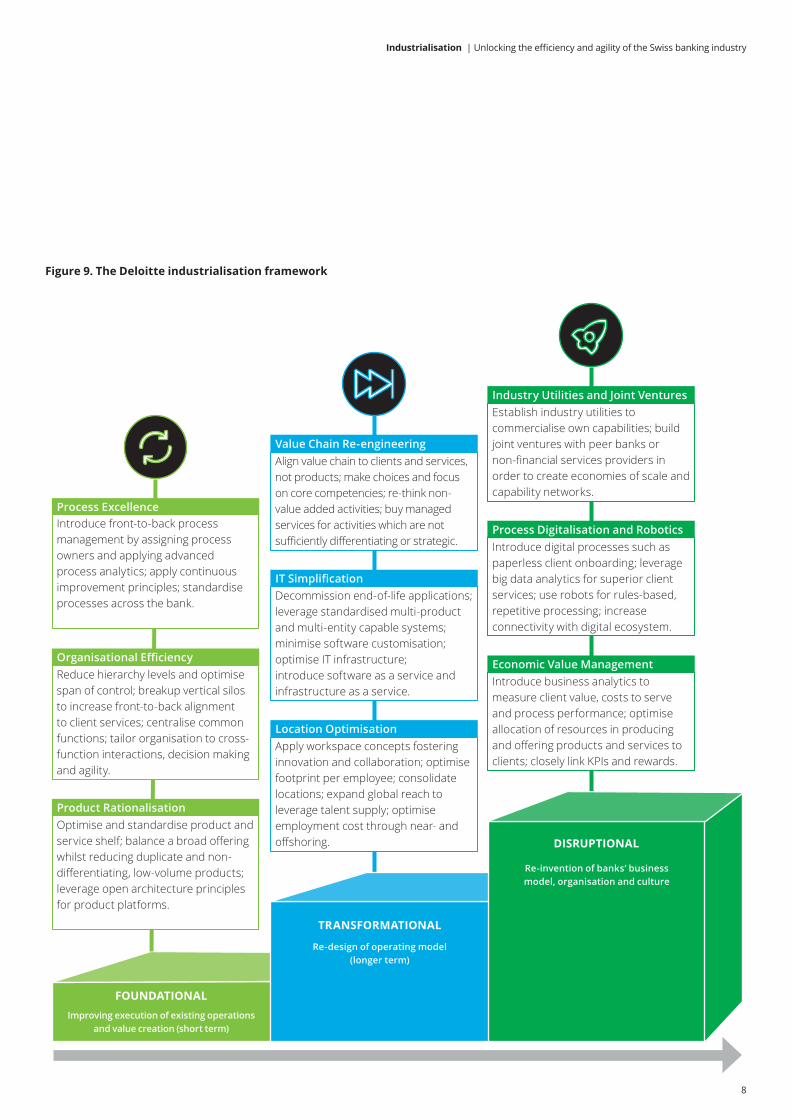

To apply these principles in practice, actionable levers must be defined. These ‘industrialisation levers’ are defined and explained below.

3.3 The Deloitte industrialisation frameworkWe have identified nine industrialisation levers that can be used by banks to apply the industrialisation principles in practice. Each lever addresses one or more of the underlying five principles of banking industrialisation. The nine levers are divided into three main categories:

• Foundational levers, which aim at improving the execution of existing operations in the shorter term

• Transformational levers, which target the re-design of the operating model in the long run

• Disruptional levers, which can be utilised to re-invent a bank’s business model, organisation and culture

While each lever can be applied in isolation, the full benefits of the industrialisation framework will only be achieved by taking a holistic view, based on the five principles, and coordinating change across the entire organisation.

3.2 Five principles of banking industrialisationBuilding upon industrialisation principles in other industries, principles for industrialisation in banking can be derived, taking into account the service nature of banking. The following five principles are aimed at increased productivity, economies of scale and reduced error rates.

7

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

Align value chain to clients and services, not products; make choices and focus on core competencies; re-think non-value added activities; buy managed services for activities which are not sufficiently differentiating or strategic.

Value Chain Re-engineering

Decommission end-of-life applications; leverage standardised multi-product and multi-entity capable systems; minimise software customisation; optimise IT infrastructure; introduce software as a service and infrastructure as a service.

IT Simplification

Apply workspace concepts fostering innovation and collaboration; optimise footprint per employee; consolidate locations; expand global reach to leverage talent supply; optimise employment cost through near- and offshoring.

Location Optimisation

Establish industry utilities to commercialise own capabilities; build joint ventures with peer banks or non-financial services providers in order to create economies of scale and capability networks.

Industry Utilities and Joint Ventures

Introduce digital processes such as paperless client onboarding; leverage big data analytics for superior client services; use robots for rules-based, repetitive processing; increase connectivity with digital ecosystem.

Process Digitalisation and Robotics

Introduce business analytics to measure client value, costs to serve and process performance; optimise allocation of resources in producing and offering products and services to clients; closely link KPIs and rewards.

Economic Value Management

Figure 9. The Deloitte industrialisation framework

Improving execution of existing operations and value creation (short term)

FOUNDATIONAL

DISRUPTIONAL

Re-design of operating model (longer term)

TRANSFORMATIONAL

Re-invention of banks’ business model, organisation and culture

DISRUPTIONAL

Reduce hierarchy levels and optimise span of control; breakup vertical silos to increase front-to-back alignment to client services; centralise common functions; tailor organisation to cross-function interactions, decision making and agility.

Organisational Efficiency

Optimise and standardise product and service shelf; balance a broad offering whilst reducing duplicate and non-differentiating, low-volume products; leverage open architecture principles for product platforms.

Product Rationalisation

Introduce front-to-back process management by assigning process owners and applying advanced process analytics; apply continuous improvement principles; standardise processes across the bank.

Process Excellence

8

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

3.4 Innovation versus industrialisationBanking executives and other industry experts often express a concern that industrialisation limits innovation. In our view innovation and industrialisation are not incompatible, but rather complement each other.

First, a stricter focus on core competencies inherent in industrialisation will free up resources otherwise trapped in activities with limited value. These resources (financial, technological and labour) can then be employed for innovating in key differentiating areas. A recent study found that banks intend to redeploy savings mainly into client-facing technology (such as mobile apps), enhanced technology for advisors and the development of new solutions.13

Secondly, while not every aspect of industrialisation effort is innovative, challenging the status quo resembles closely an innovation approach. This could include the decomposing of the value chain or rethinking front-to-back processes from a client service perspective. The accumulation of knowledge and insights through the application of industrialisation principles may enable banks to come up with and implement fundamentally different ways of doing things, leapfrogging over existing solutions and creating a sustainable competitive advantage.

For example, Process Excellence can lead banks into developing innovative and efficient methods for delivering products and services, by applying continuous improvement principles and by standardising and automating processes. This allows banks to position themselves as a distinctive and reliable provider, delivering high-quality services with superior customer experience, whilst pricing services competitively.

If industrialisation is applied well, it has the potential to create a more competitive cost base and enable the business to drive innovation in a more agile way.

9

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

4. Banks’ industrialisation plans

4.1 Survey methodologyIn order to assess the current state of the Swiss banking industry and the levels of industrialisation among Swiss banks (excluding the two big banks) we conducted a web-based survey between December 2015 and April 2016 (using 20 quantitative and qualitative questions and over 150 metrics). In addition we conducted face-to-face interviews in May and June 2016 with a number of Swiss bank executives. In total 36 bank executives participated from banks of various sizes and with a different mix of business activities (see Appendix for details).

4.2 Benefits and challenges of industrialisationSwiss banks see various benefits arising from an increased level of industrialisation. 92 per cent of the responding banks expect that industrialisation will enable them to scale their operations more easily and, not surprisingly, 88 per cent see industrialisation as a tool for reducing costs. Dr. Michael Eisenrauch, Head Competence Centre Services of Basler Kantonalbank, commented: “Without industrialisation the cost pressure will be too high to manage going forward”. Another benefit cited by about three-quarters of respondents was more time for the client being made available due to greater automation and leaner processes.

Industrialisation is also seen by about two-thirds of our respondents as an accelerator for innovation and an enabler of greater agility. One executive of a smaller bank explained that smaller banks would often be unable to offer innovative solutions if they could not rely on their sourcing partners. Dr. Christian Poerschke, COO Raiffeisen Switzerland, stressed the need for increased industrialisation to cope with disruptional innovation: “We need to be fit in both processes and philosophy today in order to react quickly in response to disruptional changes in the future.” The need for preparation was also emphasised by Stefan Gempeler, Head Products and Operations, Valiant, “It’s not necessary to be the overall trendsetter for innovation but it is important to attain a level of readiness so a quick reaction is possible in the event of a particularly disruptive trend catching on.”

While not as important as the other factors, more than half of the participating banks see improved compliance and reduced risk as further benefits from industrialisation.

Figure 10. Key benefits and challenges identified by the banks

Improved compliance and reduced risk

Increased agility

Accelerated innovation

More time for client relationship

Reduced costs

Enhanced scalability

Increased risks

Other measures are more suited

Not compatible with indiv. client service

Insufficient knowledge of tools and methods

Too costly

Resistance to change and culture

Benefits Challenges

58%

65%

69%

77%

88%

92%

8%

16%

40%

68%

80%

100%

While most banks recognise the benefits and necessity of industrialisation for the future, many are hesitant about putting it into practice, in view of the relatively high investment required for industrialisation programmes. Four in five of our respondents agreed that industrialisation is expensive.

10

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

The main obstacle to further progress in industrialisation, however, is cultural resistance. This is understandable given the fact that very often initiatives will result in a reduction in staff numbers or in outsourcing of activities. In the view of Dr. Eisenrauch: “Industrialisation cannot be imposed from the outside but needs to come from within the organisation.” As a result it is usually a lengthy process for most banks, but he emphasised: “The sustainability of industrialisation is more important than the length of time required to implement it”. From our own experience, we believe that the sustainability of efforts is largely a function of time and buy-in from bank staff at all levels, as well as a clear commitment and drive from the very top of the organisation. Stefan Gempeler, Valiant, agrees: “The top management needs to have a clear vision and be able to communicate the need for change and demand the implementation. Furthermore, implementation needs to be driven and embraced by own working groups so that the change will be accepted in the organisation from the beginning.” As the banks move increasingly towards industrialisation of most critical functions, they will see tangible rewards from their efforts, receive and build on positive client feedback and, of course, cut costs and incorporate best practices.

About two-thirds of our respondents reported insufficient knowledge of the tools and methods required for a successful industrialisation. While the required knowledge can certainly be sourced externally, all banks need to build this internally over time.

If banks choose the areas for industrialisation wisely, client experience should not be impacted. Only 40 per cent of our participants see industrialisation affecting individual customer service. In fact, contrary to usual preconceptions, industrialisation might actually improve client service. Dr. Poerschke commented: “Standardisation improves data availability and client knowledge, and therefore allows for a faster and more individual client service.”

4.3 Industrialisation maturity Our survey found that banks already show a high level of maturity in implementing foundational levers such as Process Excellence and Organisational Efficiency. This limits the potential for further efficiency gains in these areas in the future. We believe that banks must take more radical measures in order to exploit the full potential of industrialisation.

Whereas Swiss banks intend to give much greater consideration to the three transformational levers, their attitude to disruptional levers over the next five years is less clear. 67 per cent of the participating banks indicated that they want to exploit Process Digitalisation and Robotics, and only one in five want to do so for Industry Utilities and Joint Ventures (which is not surprising, considering the complexity of such constructs). The biggest gap between industrialisation models today and in the future lies in Product Rationalisation and Process Digitalisation. As an example, none of the surveyed banks currently has fully digitalised processes, but in the next five years, two-thirds of banks in our survey are looking to achieve near-complete digitalisation.

Looking to the next five years, banks have enormous potential for improvement, applying each of the nine industrialisation levers.

11

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

The results of our survey show that, whilst all bank types are at similar levels today, private banks aim to exploit more of the industrialisation levers than retail banks over the next five years. Our survey responses also show that small banks usually do not have the same capacity or knowledge for industrialisation efforts as mid-size banks, partly because of low volumes. Large banks face different challenges and due to their complexity find it difficult to utilise some industrialisation levers. However, looking at their industrialisation intentions over the next five years, we observe that overall large banks aim to be more ‘mature’ than smaller banks.

Figure 12. % of levers that are mostly or fully industrialised

% of levers that are mostly or fully industrialised

% of levers that are mostly or fully industrialisedToday

Private andforeign banks

Retail, savings andcantonal banks

In 5 years In 5 yearsToday

< CHF 10bnAUM

CHF 10-50bnAUM

> CHF 50bnAUM

8% 9%67% 49%

11% 57%

6% 67%

11% 49%

Figure 11. Exploited industrialisation potential per lever

Organisational Efficiency

Product Rationalisation

Value Chain Re-engineering

IT SimplificationLocal Optimisation

Industry Utilities and Joint Ventures

Process Digitilisation and Robotics

Economic Value Management

Process Excellence

Today In 5 years

12

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

Focus shift from IT and operations towards a broader set of functionsWe have observed that industrialisation efforts have so far been focused mainly on operations and IT. Over the next five years these efforts are expected to extend to other functions, including core business activities such as advisory and product development and management. Survey participants commented that the challenge will be to maximise customisation from a client perspective while standardising processes as much as possible. There is a notable increase in the expected level of industrialisation efforts in the area of compliance, which can be explained by the increase in both the cost and the complexity of the compliance function in recent years.

0% 20% 40% 60% 80%

Tax

Product development and management

Legal and regulatory

Other

Finance

Advisory and portfolio management

Risk control and compliance

IT

Operations

Today In 5 years

Figure 13. Explored industrialisation potential per function

Rising levels of customer expectations, combined with the insight that automated advisory engines may achieve solid investment performance, explains a similar increase in the area of advisory and portfolio management.

Surprisingly, even in five years’ time, the potential for industrialisation across many functions is expected to have been exploited only partially, indicating that there will still remain room for further improvements.

However considering current industry dynamics, we believe that industrialisation endeavours can and must be expedited across all functions in order to fully leverage their potential.

13

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

4.4 Deep dive into foundational leversProcess ExcellenceOur survey findings reveal that half the banks already fully document their processes. However only 12% have fully integrated their processes into system-supported workflows and only 20% have ‘mostly or fully’ standardised processes across different departments and countries. Additionally over one-third of banks do not monitor their processes systematically with KPIs and do not follow continuous improvement principles. As Dr. Eisenrauch observed: “Monitoring processes does not suffice, but to find the right KPIs is challenging. Nevertheless, banks need to monitor the processes in the first place in order to improve them eventually.” Over the next five years most banks want to improve their practices substantially in these areas. In our opinion this development is required urgently because Process Excellence not only helps to generate savings, it also contributes to superior customer experience and proactive management of risks.

Figure 14. Survey results for Process Excellence. Processes are…

0% 20% 40% 60% 80% 100%

Bank follows continuousimprovement principles

...are monitored through KPIsand governed by SLAs

...standardised across differentdepartments or countries

...integrated into systemsupported workflows

...documented

Not at all/Limited

Today

In 5 years

Partially Mostly or fully

4%

4%

4%

48% 48%

12% 88%

28% 60% 12%

24% 72%

20% 60% 20%

28% 72%

44% 52% 4%

56% 44%

36% 44% 20%

40% 56%

Organisational EfficiencyWithin Organisational Efficiency, the greatest potential for improvements lies in the optimisation of hierarchy levels and spans of control. While today only one in six banks applies these principles extensively, almost half aim to do so within the next five years. Similarly, most banks hope to exploit centralisation to a greater degree over the same period. This suggests that banks are still able to exploit significant potential for improvements in this area, despite already having reduced full time equivalents by over five per cent in the last four or five years. In our experience an efficient organisation will also often increase the speed and the agility of decision-making and thus positively impact the ability to innovate resulting in additional benefits to customers.

14

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

Figure 15. Survey results for Organisational Efficiency

0% 20% 40% 60% 80% 100%

Centralisation potentialis continuously exploited

Hierarchy levels and spans ofcontrol are regularly optimised

Not at all/Limited

Today

In 5 years

Partially Mostly or fully

32%

8%

52% 16%

48% 44%

16% 52% 32%

32% 68%

Product RationalisationOur survey shows a similar picture for Product Rationalisation: the levers of industrialisation are applied only partially. For example only 13% of respondents stated that product lifecycle management is fully aligned with business strategy. And while 40% apply a standardised and bank-wide catalogue, hardly any bank evaluates products coherently using KPIs. However, within the next five years nearly half the banks want to use KPIs fully in the evaluation process. Our own experience confirms that most banks often do not look at the complete product management lifecycle in a holistic way and are hesitant about decommissioning old products, often keeping products with low volumes on the shelf for too long. This is an area where stringent process standardisation would allow banks to become more efficient, reduce their complexity, but also increase their agility in implementing change – a leaner product shelf makes technology upgrades and innovation simpler. Targeted rationalisation of products also provides an opportunity to review the existing portfolio with discrete client segments in mind, and adopt a product suite that is closely aligned to them – and in doing so ultimately establish a leaner and more efficient product portfolio.

Figure 16. Survey results for Product Rationalisation

0% 20% 40% 60% 80% 100%

KPIs used to evaluate products

Standardised bank-wide andup-to-date product catalogue

Aligned product lifecyclemanagement process in place

Today

In 5 years

Not at all/Limited Partially Mostly or fully

46%

8%

20%

42% 12%

46% 46%

40% 40%

24% 76%

28% 68% 4%

4% 52% 44%

15

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

In conclusion, there is still much potential benefit from the three foundational levers although they are currently used more extensively than the transformational and disruptive levers. Within the next five years, all banks aim to exploit the benefits of industrialisation, mostly or fully, in at least one of the three foundational levers.

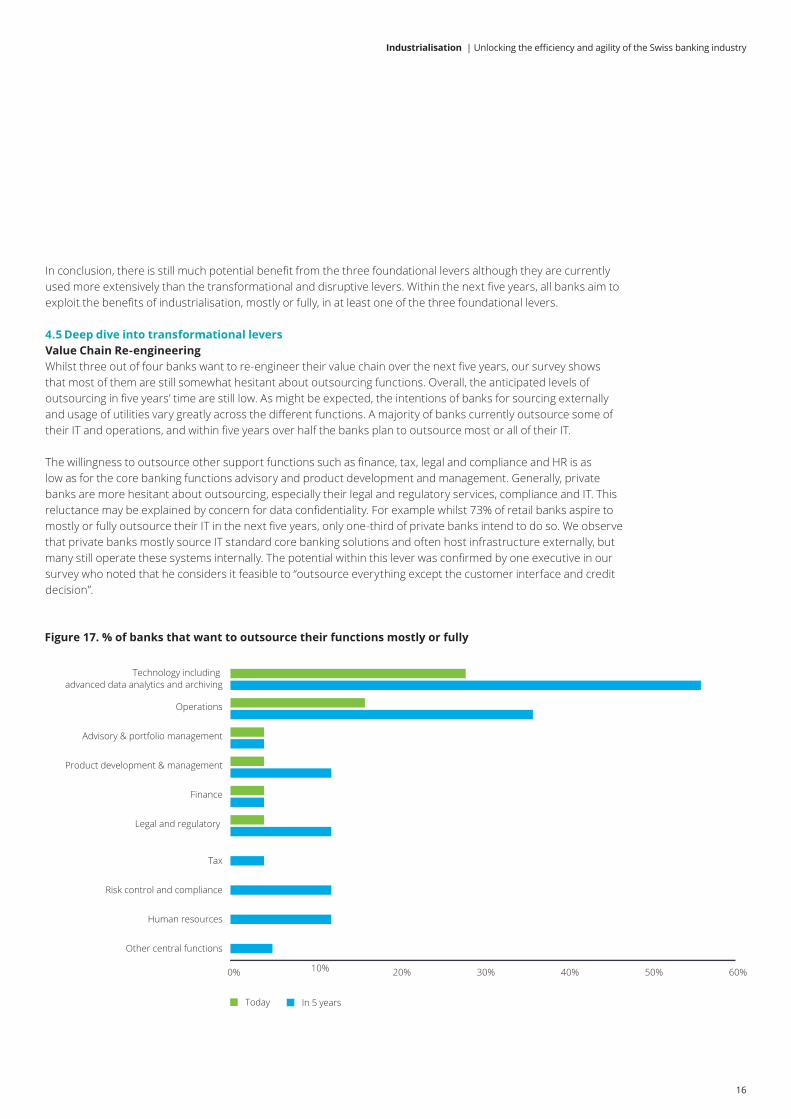

4.5 Deep dive into transformational leversValue Chain Re-engineering Whilst three out of four banks want to re-engineer their value chain over the next five years, our survey shows that most of them are still somewhat hesitant about outsourcing functions. Overall, the anticipated levels of outsourcing in five years’ time are still low. As might be expected, the intentions of banks for sourcing externally and usage of utilities vary greatly across the different functions. A majority of banks currently outsource some of their IT and operations, and within five years over half the banks plan to outsource most or all of their IT.

The willingness to outsource other support functions such as finance, tax, legal and compliance and HR is as low as for the core banking functions advisory and product development and management. Generally, private banks are more hesitant about outsourcing, especially their legal and regulatory services, compliance and IT. This reluctance may be explained by concern for data confidentiality. For example whilst 73% of retail banks aspire to mostly or fully outsource their IT in the next five years, only one-third of private banks intend to do so. We observe that private banks mostly source IT standard core banking solutions and often host infrastructure externally, but many still operate these systems internally. The potential within this lever was confirmed by one executive in our survey who noted that he considers it feasible to “outsource everything except the customer interface and credit decision”.

Figure 17. % of banks that want to outsource their functions mostly or fully

0% 10% 20% 30% 40% 50% 60%

Other central functions

Human resources

Risk control and compliance

Tax

Legal and regulatory

Finance

Product development & management

Advisory & portfolio management

Operations

Technology including advanced data analytics and archiving

Today In 5 years

16

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

The major risks identified by survey respondents are data confidentiality, overly-optimistic business cases, erosion of service levels and the limited capacity of their joint venture partners and third party providers. For larger banks the perceived issues are centred more around lack of control and the erosion of service levels. Interestingly these problems are expected to slightly diminish over the next five years, due to the anticipated greater maturity of vendor solutions and accumulation of experience of banks in using outsourcing services. Outsourcing may also be seen as a means of improving security. The CEO of a small bank commented: “Large banks normally have much better processes in place to ensure data confidentiality, and there would be no reason for small banks not to outsource to large banks.”

In order to make well-informed decisions about whether a bank should continue to deliver services in-house or source externally, it is important to understand the true costs of banks’ internal processes and functions. As Werner Kriech from Incore Bank, a provider of sourcing services, explains: “Many banks still do not entirely understand full cost accounting and transaction cost calculations when considering sourcing services as an alternative to their in-house activities.”

It is useful to understand the cost constraints against which banks may consider outsourcing. Dr. Eisenrauch commented: “For outsourcing to be profitable within three to four years the cost advantage should be between 25-30 per cent, as otherwise the required effort would be too great.” He added that in his view, banks should first optimise their processes before outsourcing them. While we believe this holds true for mid-size and larger banks, our project experience shows that small banks may also consider outsourcing their functions without standardising them beforehand: this gives them an opportunity to leverage directly best practice processes and systems from their providers.

A further point discussed with several executives during interviews was that innovation requires significant investment, and one that is only worth making if the banks have large enough volumes and revenues after implementation. Usually banks get around this issue by outsourcing. As Werner Kriech, from Incore Bank explained: “Digitalisation requires outsourcing for smaller banks. It will be too expensive for them to buy solutions in the market and implement them internally, let alone develop solutions internally on their own. This is what will drive structural change in the market.” This is especially relevant for very small banks who may find it difficult in the future to access the necessary platforms and innovation ecosystems.

Figure 18. Risks associated by banks with outsourcing

Today In 5 years

Loss of customer access

Average: 68%

Average: 64%

Capacity of the partner

Lack of control

Erosion of service level

Too optimistic business case

Data confidentiality

42%

58%

67%

71%

83%

88%

38%

58%

61%

63%

79%

83%

17

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

IT SimplificationThis transformational lever is concerned with the impact of IT complexity and how banks can deal with it. Besides the impact of IT complexity on costs, operational risks, compliance and security, 70 per cent of banks fear that it also impacts their market agility and damages client satisfaction, as it may lead to operational issues such as outages, reporting problems and incorrect data.

Half the participating banks in our survey try to reduce this complexity through continuous improvement programmes. One-fifth are currently addressing the issue with targeted programmes and one in five banks plan to run a targeted programme in the next three years.

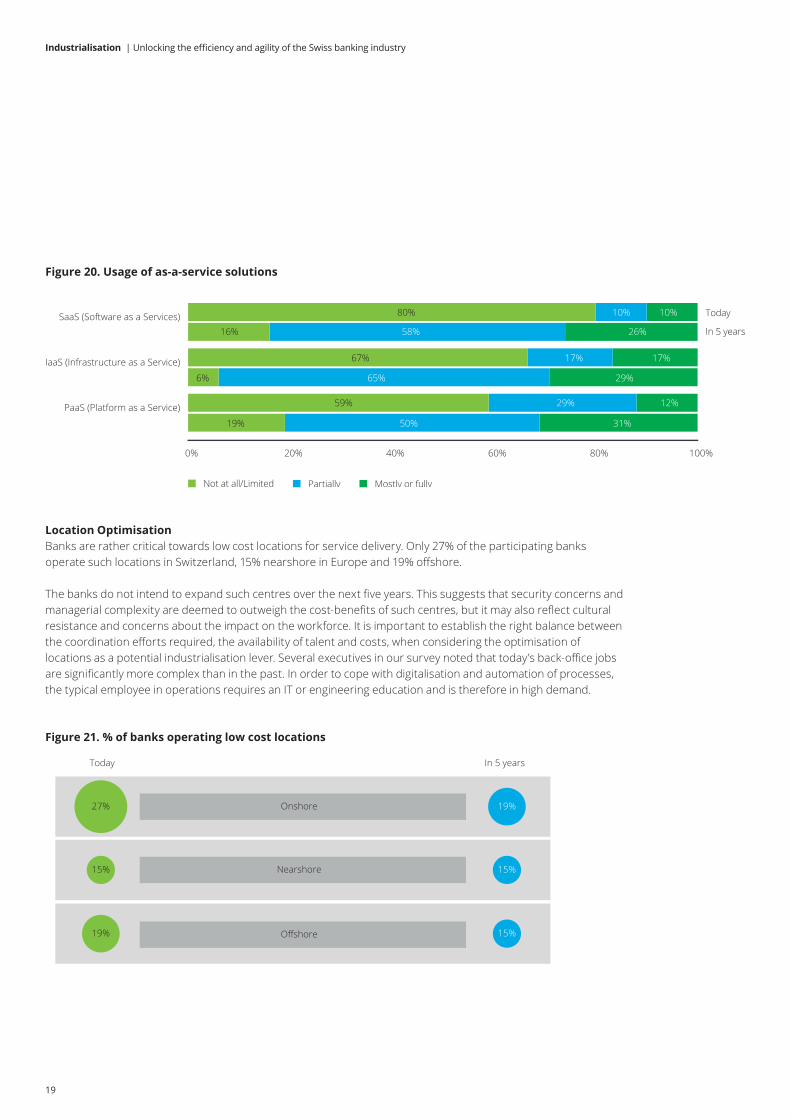

Banks reported a clear, but still somewhat hesitant trend towards ‘as-a-service’ solutions. These solutions allow for an accelerated implementation of new and improved capabilities and simplify the underlying IT architecture. Prominent examples are in CRM and the learning and HR space, which have already achieved a high level of penetration in banks outside Switzerland. While today most of the surveyed banks use such services in only a limited way, by 2021 most of them expect to employ them. The proliferation of ‘cloud solutions’ for SaaS, IaaS and PaaS offerings, which are often hosted outside Switzerland, is still held back by the banking secrecy laws. We anticipate however that the current restrictive regulatory landscape may change and technical solutions will be accepted more widely, increasing the attractiveness of as-a-service solutions. We also predict that the emergence of local, Swiss-based cloud solutions will accelerate. These trends have the potential to streamline further the overall IT landscape.

Continous programme Targeted programme in the last 3 years

Targeted programme in the next 3 years

54%

21%

21%

4%

No targeted investment planned

Figure 19. IT programmes

18

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

Location OptimisationBanks are rather critical towards low cost locations for service delivery. Only 27% of the participating banks operate such locations in Switzerland, 15% nearshore in Europe and 19% offshore.

The banks do not intend to expand such centres over the next five years. This suggests that security concerns and managerial complexity are deemed to outweigh the cost-benefits of such centres, but it may also reflect cultural resistance and concerns about the impact on the workforce. It is important to establish the right balance between the coordination efforts required, the availability of talent and costs, when considering the optimisation of locations as a potential industrialisation lever. Several executives in our survey noted that today’s back-office jobs are significantly more complex than in the past. In order to cope with digitalisation and automation of processes, the typical employee in operations requires an IT or engineering education and is therefore in high demand.

Figure 21. % of banks operating low cost locations

Today In 5 years

Onshore

Nearshore

Offshore

19%

19%

27%

15%15%

15%

Figure 20. Usage of as-a-service solutions

0% 20% 40% 60% 80% 100%

PaaS (Platform as a Service)

IaaS (Infrastructure as a Service)

SaaS (Software as a Services) Today

In 5 years

80%

16%

67%

6%

10% 10%

58% 26%

17% 17%

65% 29%

59% 29% 12%

19% 50% 31%

Not at all/Limited Partially Mostly or fully

19

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

4.6 Deep dive into disruptional leversIndustry Utilities and Joint Ventures (JVs)Many banks are still hesitant about breaking up their traditional value chains. Even greater is their resistance to Industry Utilities and Joint Ventures. Only one in eight banks specifically wants to pursue this industrialisation lever in the next five years. A difference from traditional outsourcing is the increased complexity of managing such a venture; however banks have more influence in designing the solution and maintain direct control. A notable development is Arizon, a JV between Avaloq and Raiffeisen, to which the bank is outsourcing back office administration processes and technology, such as payments, securities, central bank functions and trust administration.14 This example may suggest that banks willing to drive such constructs must be of a certain minimum size, as a high level of management input is required. The COO of a small private bank commented to us: “The industry has been evolving gradually and cautiously, at different paces in different geographies. It is now at an inflexion point, where some emerging genuine utilities are proving to the market that actually, it can be done.”

Process Digitalisation and RoboticsTraditionally only transaction-oriented tasks such as payments and trade settlement were mostly automated, whereas client-facing activities exhibited low degrees of digitalisation. Our survey suggests that this situation is about to change very soon. Not only will the digitalisation of the mature functions be extended further in the next five years, but 80 per cent of all processes will be mostly or fully digitalised. The sharpest rise will be seen in activities such as account opening, advisory, product suitability assessments and loan applications, which have not traditionally been a focus for digitalisation.

Figure 22. % of banks that mostly or fully exploit Process Digitalisation in a function

Today In 5 years Today In 5 years Today In 5 years

Trade processing

Mature

Payments

Documentmanagement

Developing

OthersRisk controlAccounting & reporting

Product suitability

Rising

Loans

AdvisoryAccount opening

20%

40%

60%

80%

20%

40%

60%

80%

20%

40%

60%

80%

A risk seen by many executives in adopting digitalisation without giving due consideration to all the issues is forgetting the business case and shaping their own strategies for addressing the demands of their chosen customer segments. Some may prefer 100 per cent automation of even client-facing activities whilst others may want to retain the traditional roles of the RMs. In our opinion, banks need to consider a variety of factors in conjunction with their own priorities before investing into Process Digitalisation and Robotics. For example, if a bank only has a small number of new clients each month, digitalisation of on-boarding may be too expensive or only viable via a third party offering. Another bank executive supported this view, saying: “As long as the business case has been thought through in the right way, you will make the decisions that are right for your organisation; and the more you put in, the more you get out.”

20

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

A bank’s broader strategy for automation and digitalisation must therefore be closely linked to its business strategy in order to maximise the overall return on investments. Mr Mark Dambacher, CEO of Incore Bank explains: “When investing in digital offerings, business plans should not be forgotten. Who will use the new digital products? How will we earn money with it? Digitalisation requires a significant investment and banks should have a plan how to recover their investment costs and generate additional revenues.” Automation and digitalisation therefore need to come with a clear intent, and should not be a tactical move that may be risky and ultimately costly.

Economic Value ManagementEconomic Value Management (EVM) is a method of creating transparency about profits of services, taking full costs into consideration including cost of capital. In the simplest of terms, it is a measure of profit, and it attempts to identify the true profit-generating activities of a company. Our survey confirms our own experience that adoption levels of EVM in banking are low, and when it is used, it is applied mainly to clients and relationship managers. However most banks in our survey aspire to use EVM for clients and relationship managers within the next five years, one-third aim to extend its use to processes, channels, products and markets. A survey participant commented: “Strong competitive pressures hinder the implementation of the insights gained from EVM, as key products need to be offered at competitive prices in order to retain customer relationships. Economic Value Management may however help relationship managers to understand the consequences of their decisions and concessions”.

Figure 23. % of banks which mostly or fully apply Economic Value Management

Today In 5 years

Countries/marketsProductsChannelsProcesses RMs Clients

100%

80%

60%

40%

20%

0%

One banking executive expressed the view that as the next generation of bank managers comes into positions of authority, EVM concepts will be used more extensively. The first banks to do so will have a powerful tool for making strategic decisions based on insights into profitability – where to retreat, where to focus, where to reduce service levels, which customers to target even further, and so on. However execution will require some tough decisions and a shift away from pure top-line thinking.

21

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

5. Our perspective: A call for action

5.1 Need to establish a bold industrialisation strategyOur survey results indicate that banks have ambitions about how they aim to industrialise their businesses substantially, and so the way in which they operate, over the next five years. Whilst these ambitions are commendable and may even be sufficient, we would argue that banks could choose to take even bolder measures within an industrialisation framework to realise the vision to become a fully-industrialised bank.

In view of the disruptive forces that are expected to come into play, and their potentially huge impact on the top line, there will be a need for banks to make significant investment in their business. We also believe that Swiss banks should now work decisively towards overcoming the barriers of industrialisation, which are mostly internal and cultural. Unless they make bold and decisive moves, we believe that banks may find themselves with an outdated business model and unable to invest in innovation. Banks that act rapidly now towards industrialisation will reap the biggest benefits and acquire strategic flexibility to respond successfully to disruptive forces in the market.

In order to understand what being fully industrialised means, we have developed an industrialisation maturity framework. This describes five maturity levels. The lowest and highest levels (1 and 5) are described briefly in Figure 24. As we have seen, banks will have varying levels of maturity across the different industrialisation levers and this can provide an indication for where the greatest potential for improvement remains.

An industrialisation strategy, to be truly effective, would need to be aligned with overall business goals. In addition, due to resource constraints, all planned initiatives cannot be implemented simultaneously and banks will therefore need to define a holistic and coordinated approach to industrialisation. The business goal of a bank (for example, positioning as a trusted advisor, or transaction champion) will drive significant decisions and prioritisation choices across many of the industrialisation levers, most notably around how to re-configure the value chain.

Swiss banks should now work decisively towards overcoming the barriers of industrialisation, which are mostly internal and cultural.

22

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

Figure 24. Industrialisation levers maturity model (excerpt only)

Not industrialised Fully industrialised

• Lack of process standardisation and ad-hoc documentation of processes

• Ambiguous process governance • No process analytics

• Bank-wide process methodology and accessible process documentation

• Frequent reviews of process governance • Consistent performance measurement

• Organisation structure around positions not other way round

• Top-down decision making and no decision criteria

• Duplication of activities

• Periodical reporting of KPIs on organisation structure

• Unambiguous decision authorities and decentralised decision-making

• Central shared functions

• Legacy product portfolio • No review of product profitability, growth potential

and compliance requirements • Abundance of low-volume, low-differentiating

products

• Product portfolio in accordance with bank strategy and client segmentation

• Constant monitoring of product profitability and volumes

• Active management of product lifecycle

• No consistent guidelines on sourcing decisions in place

• No periodic benchmarking of service provisioning

• Bank-wide sourcing framework and governance • Detailed service level agreements incl. key KPIs • Regular benchmarking of (in-house and

outsourced) service provisioning

Process Excellence

Organisational Efficiency

Product Rationalisation

Value Chain Re-Engineering

IT Simplification

Location Optimisation

Industry Utilities and

Joint Ventures

Process Digitalisation and Robotics

Economic Value

Management

• Historically grown and complex IT system landscape

• Proprietary IT solutions for non-differentiating applications

• Highly customised IT solutions

• Standardised vendor solutions as core IT systems • Majority of IT landscape on ‘as-a-service’ model • Customisation only for truly differentiating

applications

• No standardisation of workspace fittings • No benchmarking of occupancy costs • No leverage of lower cost locations

• High standardisation of workspaces • Regular review of occupancy costs • Systematic use of lower cost locations

• No use of industry utilities • Ad-hoc partnership agreements • No identification of commercialisation potential

• Systematic use of industry utilities for non-differentiating services

• Framework for management of partnerships • Regular review of commercialisation opportunities

• Only limited digitalisation of processes • Disrupted system interfaces with manual

processing • Data largely unstructured and not digitalised

• Front-to-back digitalisation of all standard processes

• Systematic use of robots to overcome disrupted system interfaces and to automate processes

• Full digitalisation for data processing

• No systematic business analytics • No profitability measurement on client, RM,

product and channel level • Performance management solely based on

volume not profit contribution

• Fully embedded business analytics • Application of full cost or activity based accounting

principles • Performance management based on economic

principles

Foun

dati

onal

leve

rsTr

ansf

orm

atio

nal l

ever

sD

isru

ptio

nal l

ever

s

1 52 3 4

23

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

5.2 Selecting the future business model and value chain configurationThe anticipated level of industrialisation and value chain configuration, and thus the target operating model, will depend not only on the size of the bank but also on its chosen business strategy. Unlike today, when most banks conduct activities along the whole value chain, in the future we can expect banks to focus on specific parts of the banking value chain. In a Deloitte study on future business models for Swiss banks, five business models have been identified that are likely to emerge, where each model is geared towards a specific part of the value chain.15

Figure 25. Future business models of Swiss banks

Business models

Banking value chain

Client assessment

Financial advisory

Product development

Operations & transactions

Support functions

Trusted advisorTA

Universal bankUB

Product leaderPL

Transaction championTC

Managed solutionsMS

TABanks becoming a ‘trusted advisor’ will focus on exploiting economies of scope through gaining a high share of their client’s wallet.

PLBanks choosing to become a ‘product leader’ will focus on developing innovative products to gain market share quickly at premium prices.

TCBanks selecting the business model ‘transaction champion’ will focus on exploiting economies of scale through partnering with other providers and acting as transactions consolidator.

MSBanks (or non-banks) becoming a ‘managed solution provider’ will focus on building economies of scale through providing specific banking solutions to other providers.

UBBanks choosing to become a ‘universal bank’ will focus on exploiting economies of scope through offering a wide range of services, but must achieve scale in all their business lines to achieve low cost levels and overall efficiency.

We suggest that truly industrialised banks should choose their preferred business model first and then rigorously adjust their configurations accordingly. We anticipate that this will result in the following types of value chain models.

24

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

Figure 26. Model bank of the future

Trus

ted

advi

sor Client

assessmentFinancial advisory

Product development

Operations & Transactions

Risk control & Compl.

Legal & regulatory

Finance

Tax

HR

IT

• Focus on trust-based holistic advisory services for end-clients

• Product portfolio based on an open architecture, with products sourced internally and externally

• All transactions and support services outsourcedTAPr

oduc

t le

ader

PL

Client assessment

Financial advisory

Product development

Operations & Transactions

Risk control & Compl.

Legal & regulatory

Finance

Tax

HR

IT

• Focus on developing innovative products for third party financial services providers

• Customise IT systems allowing the bank to develop and manage their products efficiently

• Outsource all transactions and support services

Tran

sact

ion

cham

pion

TC

Client assessment

Financial advisory

Product development

Operations & Transactions

Risk control & Compl.

Legal & regulatory

Finance

Tax

HR

IT

• Focus on operations and transactions offering at low cost for end-clients and third party banks and non-banks

• Products sourced externally, advisory and portfolio management in-house and with partners

• Transaction-related IT partly in-house, all other support functions fully outsourced

Man

aged

so

luti

ons

MS

Client assessment

Financial advisory

Product development

Operations & Transactions

Risk control & Compl.

Legal & regulatory

Finance

Tax

HR

IT

• Specialist offering to banks and non-bank providers allowing them to break up their internal value chain

• Solutions can range from regulatory insights, KYC, tax, payment and other support functions

• No end-clients or product development

Uni

vers

al

bank

UB

Client assessment

Financial advisory

Product development

Operations & Transactions

Risk control & Compl.

Legal & regulatory

Finance

Tax

HR

IT

• Full product offering across several industry sectors with seamless control over front-to-back processes

• Outsource some transactions and support services

• Only feasible for very large banks

Outsourced functions

Partially outsourced functions

Core competenciesLegend

25

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

Figure 27. Impact of industrialisation levers on revenues and costs of banks

Revenue growth Cost reduction FTE reduction

Process Excellence

Organisational Efficiency

Product Rationalisation

Value Chain Decomposition

IT Simplification

Location Optimisation

Joint Ventures and Industry Utilities

Process Digitalisation and Robotics

Economic Value Management

0% 0-5% 5-10% 10-20% >20%Increase in revenues/decrease in costs

Applying these impacts to a model bank, and taking into account current maturity levels of industrialisation, we have assessed the effect on cost reduction and full-time employee numbers in two different scenarios. (The revenue impact was not the focus of this study and has therefore not been quantified in this assessment.)

The first scenario assumes that Swiss banks achieve their intended level of industrialisation maturity over the next five years, as reported in our survey. This would enable them to reduce costs by 10-15 per cent and reduce FTE numbers by 12-18 per cent.

The second scenario assumes that a bank will be fully-industrialised, exploiting all the industrialisation levers across all functions: This would deliver a reduction in costs of 20-30 per cent from today’s cost base and a fall in FTE numbers of 30-40 per cent (including shifts in staff to third parties).

Figure 28. Anticipated savings in two industrialisation scenarios

Bank average target 2021 Fully industrialised vision

Costs savings 10-15% 20-30%

FTE reduction/shift 12-18% 30-40%

5.3 Understanding the financial impactBefore reaching a conclusion about how banks may take action, the potential financial impact of industrialisation on banking operations should be considered. Based on our experience with industrialisation, we have developed a model that quantifies the potential benefits from increased industrialisation. The following graph exhibits the impact of each of the nine industrialisation levers on the revenues and the costs of the banks.

26

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

Our model assumes that previously estimated savings from each industrialisation lever can be achieved across different functions. For modelling purposes we used the ‘trusted advisor’ configuration as one of the example configurations. In addition we assume that marginal savings decrease with increasing maturity. This means that a bank with a low level of industrialisation maturity can achieve higher savings with the same investments than a mature bank. The savings per function are impacted by the different levers and the current and the future maturity of the function. The percentage reduction in FTE numbers is greater than the percentage cost reduction, as banks will outsource functions and own a smaller part of the value chain: outsourced jobs will not all be lost, but may transfer to other non-banking providers.

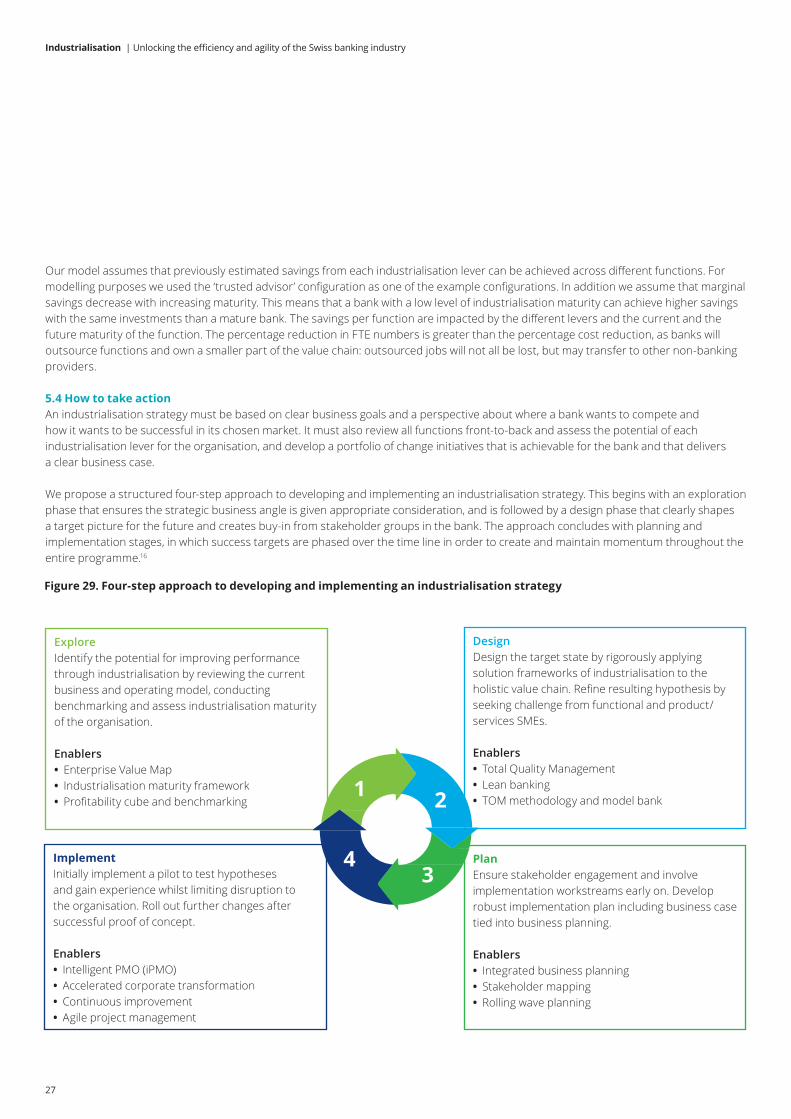

5.4 How to take actionAn industrialisation strategy must be based on clear business goals and a perspective about where a bank wants to compete and how it wants to be successful in its chosen market. It must also review all functions front-to-back and assess the potential of each industrialisation lever for the organisation, and develop a portfolio of change initiatives that is achievable for the bank and that delivers a clear business case.

We propose a structured four-step approach to developing and implementing an industrialisation strategy. This begins with an exploration phase that ensures the strategic business angle is given appropriate consideration, and is followed by a design phase that clearly shapes a target picture for the future and creates buy-in from stakeholder groups in the bank. The approach concludes with planning and implementation stages, in which success targets are phased over the time line in order to create and maintain momentum throughout the entire programme.16

ExploreIdentify the potential for improving performance through industrialisation by reviewing the current business and operating model, conducting benchmarking and assess industrialisation maturity of the organisation.

Enablers • Enterprise Value Map • Industrialisation maturity framework • Profitability cube and benchmarking

ImplementInitially implement a pilot to test hypotheses and gain experience whilst limiting disruption to the organisation. Roll out further changes after successful proof of concept.

Enablers • Intelligent PMO (iPMO) • Accelerated corporate transformation • Continuous improvement • Agile project management

PlanEnsure stakeholder engagement and involve implementation workstreams early on. Develop robust implementation plan including business case tied into business planning.

Enablers • Integrated business planning • Stakeholder mapping • Rolling wave planning

DesignDesign the target state by rigorously applying solution frameworks of industrialisation to the holistic value chain. Refine resulting hypothesis by seeking challenge from functional and product/services SMEs.

Enablers • Total Quality Management • Lean banking • TOM methodology and model bank

1 2

34

Figure 29. Four-step approach to developing and implementing an industrialisation strategy

27

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

Figure 30. Key success factors to realise the full potential of an industrialisation strategy

To realise the full potential of an industrialisation strategy, senior management should pay close attention to seven key success factors that we have identified in various client engagements.

We believe, and the banks in our survey confirm, that industrialisation implemented in a considered way will provide the banks with a robust and comprehensive toolkit that will help them to respond to the challenges of difficult market conditions, demanding customers and an ever-changing technological landscape.

Ensure stakeholder buy-in across the bank from day one whilst initiative is being driven from the top1

Prioritise change areas to focus momentum2

Apply systematic hypothesis generation3

Balance green-field approach versus continuous improvement4

Apply agile development and involve implementation workstreams in solution design early on5

Develop solutions around the complete front-to-back value chain6

Communicate successes and milestones to the whole organisation to foster cultural change7

28

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

Bibliography

1 Deloitte, “Deloitte International Wealth Management Centre Ranking 2015,” [Online]. Available: http://www2.deloitte.com/ch/de/pages/financial-services/articles/wealth-management-centre-ranking-2015.html.

2 Deloitte, “Third country rules under the new Swiss Financial Services Act (“FIDLEG”) 2014,” [Online]. Available: http://www2.deloitte.com/content/dam/Deloitte/uk/Documents/financial-services/deloitte-uk-fs-structural-reform-eu-banking-april-14.pdf.

3 Deloitte, “Structural reform of EU banking 2014,” [Online]. Available: http://www2.deloitte.com/ch/en/pages/financial-services/articles/third-country-rulesunder-the-new-swiss-financial-services-act-fidleg.html.

4 Swiss Banking Institute, “The extra cost of Swiss banking regulation 2014,” [Online]. Available: http://www.swissfinanceinstitute.ch/the_extra_cost_cost_of__swiss_banking_regulation.pdf.

5 Seco, “Konjunkturtendenz Frühjahr 2016,” [Online]. Available: https://www.seco.admin.ch/seco/de/home/Publikationen_Dienstleistungen/Publikationen_und_Formulare/konjunktur/konjunkturtendenzen-fruehjahr-2016.html.

6 Finews, “Apple Pay steht in der Schweiz in den Startlöchern,” [Online]. Available: http://www.finews.ch/news/banken/22323-apple-pay-ist-in-der-schweiz-in-den-startl%C3%B6chern.

7 Deloitte, “Banking disrupted 2014,” [Online]. Available: http://www2.deloitte.com/ch/de/pages/financial-services/articles/banking-disrupted.html.

8 Deloitte, “Die Schweizer FinTech-Landschaft im europäischen Vergleich 2016,” [Online]. Available: http://blogs.deloitte.ch/banking/2016/03/die-schweizer-fintech-landschaft-im-europaeischen-vergleich.html.

9 Deloitte, “10 disruptive trends in wealth management 2015,” [Online]. Available: http://www2.deloitte.com/content/dam/Deloitte/us/Documents/strategy/us-cons-disruptors-in-wealth-mgmt-final.pdf.

10 Avaloq 2014, [Online]. Available: https://www.avaloq.com/de/ueber-uns/news/article/news/show/2014/b-source-migrates-deutsche-bank-switzerland-ltd-core-banking-platform-to-avaloq-banking-suite-2554/.

11 Harvard Business Review, “Rebirth of the Swiss Watch Industry 2000,” [Online].

12 Harvard Buisness Review 1994, “Nicolas G. Hayek,” [Online].

13 Wealth briefing, “Evolving operating models in wealth management 2016,” [Online].

14 Arizon 2016, [Online]. Available: https://arizon.ch/.

15 Deloitte, “Swiss banking business models of the future 2015,” [Online]. Available: https://www2.deloitte.com/content/dam/Deloitte/ch/Documents/financial-services/ch-en-fs-bank-of-tomorrow.pdf.

16 Deloitte “Industrialisation reconfigured,” [Online]. Available: http://www2.deloitte.com/ch/de/pages/financial-services/solutions/industrialisation-re-configured.html.

29

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

Appendix

Survey methodologyThe results of this report are based on an online survey (that included 20 qualitative and quantitative questions and analysed over 150 key metrics) and on discussions with Swiss bank executives during the first half of 2016. A total of 36 bank executives, covering a broad range of business activities and diversity in size of assets under management, participated in the survey and the discussions.

Private banking78%

59%

56%

38%

19%

3%

Corporate banking

Retail banking

Asset management

Bank for bank services

Investment banking

14%

29%39%

18% <2bn2-10bn

10-50bn>50bn

CHF Assets under management

*Participants could choose several fields of operations

Broad range of participants covered

Diversity in terms of size

43% of the banks have an international footprint

Business activities of participants*

30

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

Authors & contributors

Patrik SpillerPartner Head of Monitor Deloitte Financial Services Strategy Consulting+41 58 279 6805 [email protected]

Dr. Thomas AnkenbrandHochschule Luzern, Institut für Finanzdienstleistungen Zug (IFZ)+41 41 757 67 23 [email protected]

Dr. Stefan Bucherer Senior ManagerBanking Strategy ConsultingMonitor Deloitte+41 58 279 6774 [email protected]

Anupriya DwivediSenior Manager Banking Strategy Consulting Monitor Deloitte+41 58 279 6576 [email protected]

Dennis BrandesManagerResearch Banking Deloitte+41 58 279 6537 [email protected]

Special thanks to: Lennart Wurm, Marc Fröhlich and Sara Banelli

Christoph BühlerTraineeBanking Strategy Consulting Monitor Deloitte+41 58 279 6436 [email protected]

31

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

Contacts

Sven ProbstPartnerHead of Financial Services Industry+41 58 279 6401 [email protected]

Jürg FrickPartnerSenior Advisor+41 58 279 6820 [email protected]

Dr. Daniel KoblerPartnerHead of Banking Innovation+41 58 279 6849 [email protected]

Micha BitterliPartnerHead of Managed Services+41 58 279 7310 [email protected]

Alexandre BugaPartnerHead of Retail Banking +41 58 279 8049 [email protected]

Adam StanfordPartnerHead of Strategy & Operations +41 58 279 6782 [email protected]

32

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

Notes

33

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

Notes

34

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

Notes

35

Industrialisation | Unlocking the efficiency and agility of the Swiss banking industry

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/ch/about for a detailed description of the legal structure of DTTL and its member firms.

Monitor Deloitte is the tradename of Monitor Company GmbH, which is a subsidiary of Deloitte LLP, the United Kingdom member firm of DTTL.

This publication has been written in general terms and therefore cannot be relied on to cover specific situations; application of the principles set out will depend upon the particular circumstances involved and we recommend that you obtain professional advice before acting or refraining from acting on any of the contents of this publication. Monitor Company GmbH would be pleased to advise readers on how to apply the principles set out in this publication to their specific circumstances. Monitor Company GmbH accepts no duty of care or liability for any loss occasioned to any person acting or refraining from action as a result of any material in this publication.

© 2016 Monitor Company GmbH. All rights reserved.

Designed and produced by The Creative Studio at Deloitte, Zurich. J8248