african trade report 2017 - african export–import bank · 4 afreximbank african trade report 2017...

TRANSCRIPT

African Trade Report2017

African Export-Import BankBanque Africaine D’Import-Export

Transforming Africa’s Trade

Bridging Africa’s Trade Finance Gap through Domestic Resource Mobilization

Bridging Africa’s Trade Finance Gap through Domestic Resource Mobilization

© Copyright Afreximbank, Cairo 2017. All rights reserved

No part of this publication may be reproduced or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise or stored in any retrieval system of any nature without the prior, written permission of the African Export-Import Bank, application for which shall be made to the Bank.

ISBN 978-92-95097-39-1

HEAD OFFICE African Export-Import Bank 72(B) El Maahad El Eshteraky Street Heliopolis, Cairo 11341 P O Box 613 Heliopolis Cairo 11757, Egypt Tel: +202 24564100/1/2/3 Email. [email protected] Website: www.afreximbank.com

AFRICAN TRADE REPORT 2017

4 AFREXIMBANK AFRICAN TRADE REPORT 2017

ForewordThe global economy appears to be gradually recovering after two years of tepid growth. The macroeconomic environment has been challenging despite concerted efforts at policy levels to counter major dislocations in several markets. In the midst of that challenging global economic and financial environment, some salient points stood out. First, for the first time in 15 years, the ratio of trade growth to world GDP growth fell below 1:1, signaling a weakening of the long-established relationship between the two indicators. Second, the sustained deterioration in commodity terms of trade led to renewed external imbalances, which heightened uncertainty and macroeconomic volatility, especially in natural resource–dependent economies in the developing world. Already widening trade deficits in Africa were aggravated by declining trade finance in a global context of increasing aversion to risk and a stringent international compliance environment. Finally, the large-scale withdrawal of international banks and financial institutions from developing countries, including those in Africa, and massive capital outflows were exacerbated by diverging monetary policy and increased uncertainty associated with macroeconomic management challenges, most notably currency gyrations and shortages of foreign reserves. In Africa, where financing gaps have been consistently singled out as major constraints to investment and economic growth, the implications were significant and evident in observed declines in Foreign Direct Investment (FDI) flows and increased recourse to domestic resource mobilization.

The 2017 edition of the African Export-Import Bank’s annual flagship report—African Trade Report—appropriately titled “Bridging Africa’s Trade Finance Gap Through Domestic Resource Mobilization”—provides important insights on the critical role of inward resource mobilization in growth and economic transition. In particular, it stresses the complementarity between domestic resource mobilization and foreign direct investment in structural transformation. By crowding in foreign direct investment, domestic resource mobilization creates the conditions for expanding investments while enhancing the transfer of technology needed for industrial upgrading and structural transformation.

As I write, the drive for domestic resource mobilization is taking hold across the continent, and recent developments and initiatives by both the public and private sectors have been very encouraging. Average tax revenue as a percentage of GDP has increased since the 1990s. In addition to traditional approaches—which have primarily involved expanding fiscal space—innovative market solutions are increasingly being considered to raise domestic resources in support of trade and investment. These have involved local currency financing through issuance of bonds by African sovereign and corporate entities and other options contemplated by banks and financial institutions to leverage African resources to support intra-African trade.

The 2017 edition of the African Trade Report also provides a comprehensive analysis of the state of global and African trade in 2015–16. It is published at a time when the institution is rebranding, with implications for all Bank publications. This combined issue, which ensures continuity in the coverage

AFREXIMBANK AFRICAN TRADE REPORT 2017 5

and publication of the Bank’s flagship report, is an exceptional measure, and subsequent issues will revert to an annual review covering developments in global and African trade.

While overall trade contracted in 2015–16, stemming the incremental growth in African trade of prior years, intra-African trade was more resilient, essentially absorbing global shocks. The Report reviews the progress related to ongoing efforts to boost intra-African trade by further mitigating the region’s exposure to global volatility and by deepening economic integration within the continent. The signing of the Tripartite Framework Agreement in 2015 and progress towards establishing the Continental Free Trade Area were particularly important.

Other initiatives undertaken to boost African trade in 2015–16 include measures to improve the trade-enabling environment and African trade–facilitating initiatives to expedite the movement, release and clearance of goods. Despite the challenging global and African economic context, a growing number of African countries improved their trade-enabling environment, recording significant improvement in trade facilitation metrics between 2014 and 2016. At the global level the most important development in the context of rising anti-trade rhetoric was the ability of the international development community to sustain the momentum towards adoption of the Trade Facilitation Agreement by members of the World Trade Organization.

Looking ahead to the near term, Africa is expected to enjoy stronger economic growth and trade in 2017 and beyond, riding on the momentum of the global economy, although weak investment in the face of low commodity prices and productivity growth will continue to weigh on the medium-term outlook. Growth prospects are also likely to be affected by downside risks associated with ongoing rebalancing in China—Africa’s main trade partner. To mitigate against these risks and set the region on a sustainable growth path, the Report argues for expanding intra-African trade to achieve economies of scale and for pursuing structural transformation to increase productivity and diversify the sources of Africa’s growth and exports. These two priorities form the bedrock of the Bank’s Fifth Strategic Plan covering 2017-2021. The Plan, dubbed Impact 2021—Africa Transformed will inform the Bank’s intervention in member countries over the next five years.

Dr. Benedict O. Oramah President and Chairman of the Board of Directors The African Export-Import Bank Cairo, Egypt June 2017

Table of Contents8 Introduction and Executive Summary

10 Domestic Resource Mobilization and Structural Transformation10 Global and Regional Output in 2015–1611 Merchandise Trade12 Prospects12 Structure of the Report

14 Bridging Africa’s Trade Finance Gap Through Domestic Resource Mobilization16 Domestic Resource Mobilization and Structural Transformation in Africa17 Successes and Failures in Domestic Resource Mobilization and Structural

Transformation19 Approaches to Mobilizing and Deploying Domestic Resources23 Policy Lessons for Africa

26 Economic environment26 Output and Price Developments36 International Financial Markets and Financing Conditions

40 Trade and the Trading Environment40 Global Trade42 Global Trading Environment45 Africa’s External Reserves and Exchange Rates

58 Commodity Prices

72 Rising Protectionism in Global Trade75 Protectionist Measures by Type75 State Aid75 Trade Defence Measures79 ImportTariffMeasures80 Standards and Technical Barriers to Trade80 Trade Finance Measures81 Other Protectionist Measures81 Trade Disputes

86 Trade facilitation88 The World Trade Organization Trade Facilitation Agreement90 Africa’s Trade-Enabling Environment93 Africa’s Trade Facilitation Initiatives

98 Intra-African Trade101 Intra-African Trade Champions105 Intra-African trade developments for selected countries108 Trade within regional economic communities

110 Prospects

113 References

1Chapter One

AFREXIMBANK AFRICAN TRADE REPORT 2017 9

Introduction and Executive Summary

As the global economic recovery continues to struggle against economic headwinds, this report—with the theme “Bridging Africa’s Trade Finance Gap Through Domestic Resource Mobilization”—reviews major developments in the global and African macroeconomic and trade environment in 2015–16. Continued weakness in the global economy characterized by synchronous growth decelerations in most developing economies, including China; by lingering effects of the fiscal and sovereign debt crisis in the Eurozone; and by financial market volatility—all of which contributed to dampening global demand at a time of creeping protectionism and sustained deterioration in commodity terms of trade—had adverse implications for liquidity, especially trade and development finance for Africa. These patterns exacerbated challenges related to macroeconomic management—that is, management of fiscal, monetary, real and external sectors—faced by African countries over the past two years, hindering Africa’s trade and economic growth.

In 2015–16, the global economic environment was affected by the divergence of monetary policy, with the US Federal Reserve committing to a gradual tightening of interest rates. It raised the federal funds rate in December 2015, from the zero lower bound, and in December 2016. Monetary policy remained highly accommodative

in Japan and the Eurozone, reflecting continued risk of stagnation or deflation. Episodes of volatility and the US Federal Reserve’s rate hikes affected global financial markets through tighter external financial flows, declining capital flows, and currency depreciations. Developing economies, which faced structural imbalances, slower growth and lower commodity prices, were the most affected by global liquidity constraints in 2016.

In a region where infrastructure and trade finance gaps are wide, the increasingly tightening financing conditions at the global level and the large-scale withdrawal of international banks from the region and particularly from correspondent banking relationships have heightened the urgency for Africa to pay more attention to domestic resource mobilization in order to ensure that financing to boost trade and infrastructure development in support of growth and structural transformation is sustained.1

1 The annual global infrastructure financing gap is

estimated at US$3–4 trillion and at US$93 billion

for Africa, mainly covering basic infrastructure,

housing, health and education (World Economic

Forum (2014); Foster and Briceno (2009)). The

region’s trade financing gap is conservatively

estimated at around US$120 billion a year

(African Development Bank, 2014).

10 CHAPTER ONE AFRICAN TRADE REPORT 2017

1.1 Domestic Resource Mobilization and Structural Transformation

For this report the African Export–Import Bank undertook a study to explore options for drawing on domestic resources to “bridge Africa’s trade finance gap”. It found that the shortage of hard currency across the region has been exacerbated by capital outflows that have seen capital-starved economies become net exporters of financial resources (see chapter 2). The counter-intuitive direction of financial flows from Africa is at odds with other regions of the world where domestic resource mobilization has played a key role in financing economic development and trade.

The findings of the study—which was motivated by efforts to draw on global best practices to increase domestic resource management to support growth and economic development—highlight a contrast in development strategy and outcomes, most notably between Africa and other developing regions. While foreign direct investment has played a key role in growth and structural transformation of local economies in Asia over the last few decades, investment has been financed primarily by surplus savings that ultimately crowded in foreign investment. In Africa, by contrast, structurally low domestic savings constrains the growth of physical capital, even though high marginal product and subsequent attraction of capital should have been expected, especially given the region’s excess natural resource endowment and growing population.

1.2 Global and Regional Output in 2015–16

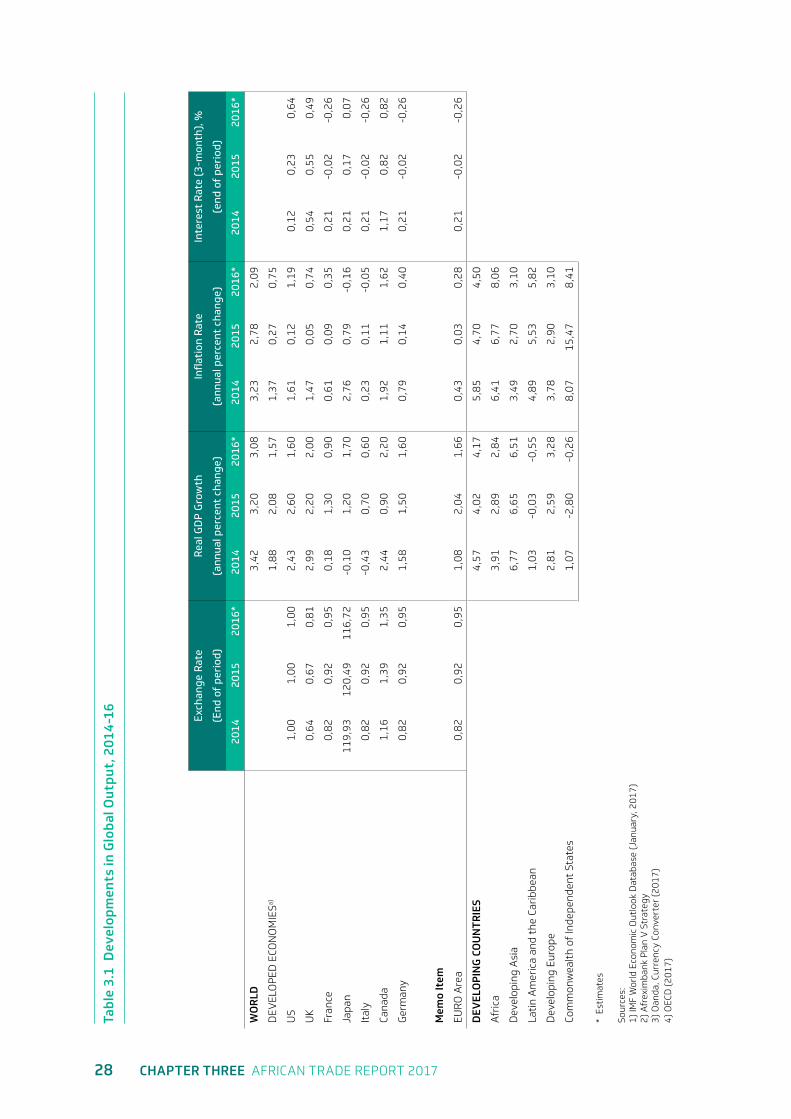

Growth in global output decelerated marginally, from 3.4 percent in 2014 to 3.2 percent in 2015 and 3.1 percent in 2016, largely mirroring the growth decelerations

that characterized developing economies, especially those in the Commonwealth of Independent States, Latin America and the Caribbean, and Developing Asia. Developing Asia was the leading driver of global growth and trade, and the deceleration of its output growth more than outweighed the modest recovery in Group of Seven countries.

African economies showed resilience in 2015–16 despite the challenging global environment. The difficulties posed by falling global demand and counter-shocks in commodity markets with the plunge in prices for commodities of export interest to Africa—particularly oil—emerged as major downside risks to growth and trade in a region where oil-exporting countries account for more than half of gross domestic product (GDP) and over 55 percent of exports. These risks were compounded by difficult domestic conditions such as heightened security concerns. Aggregate output in Africa expanded at a moderate rate, with average GDP decelerating slightly, from 3.9 percent in 2014 to 2.9 percent in 2015 to around 2.8 percent in 2016.

In tandem, global financial markets experienced phases of turbulence and volatility in 2015–16, leading to massive capital outflows, especially where foreign direct investment was dominated by portfolio flows, with adverse implications for macroeconomic management. These moves in financial markets were driven primarily by continued global uncertainties and uninspiring growth in developed economies; increasing macroeconomic management challenges in developing economies; divergent monetary policies between the US Federal Reserve and other major central banks, leading to volatility in capital markets; slowdown in growth and uncertainty over the rebalancing of the Chinese economy; weaker global commodity prices; and increasing protectionism.

AFREXIMBANK AFRICAN TRADE REPORT 2017 11

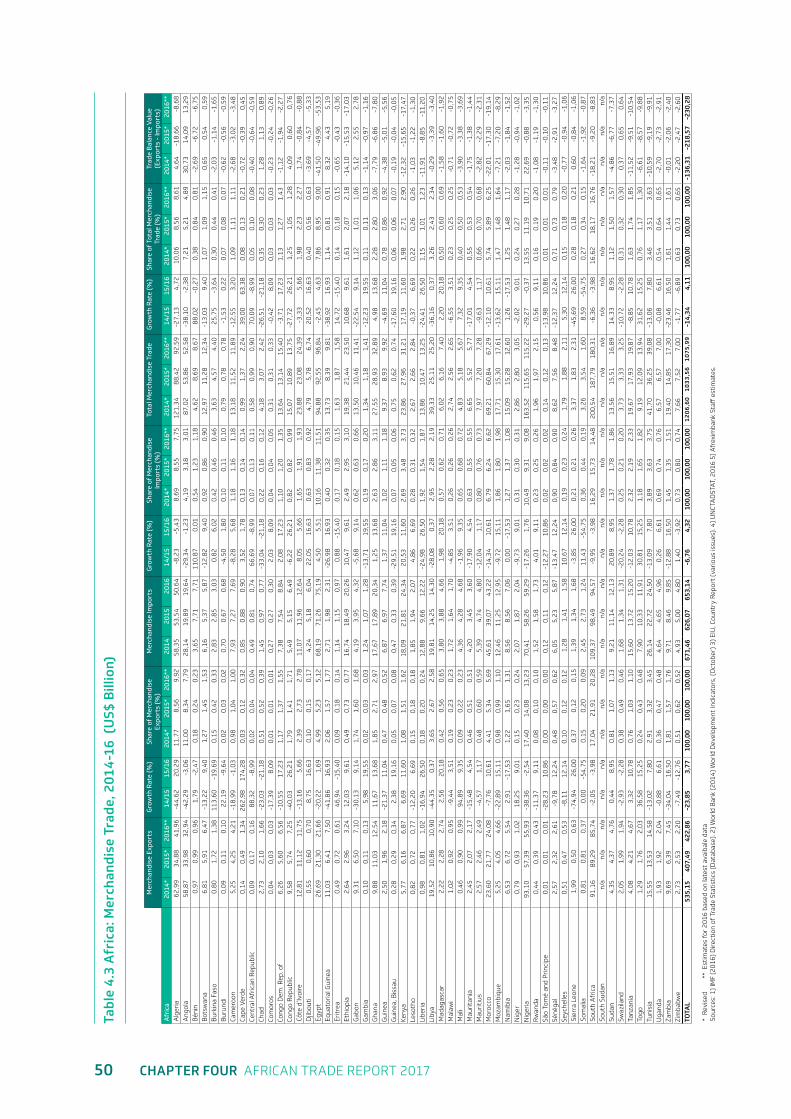

1.3 Merchandise Trade

Growth in the volume of world merchandise trade became increasingly lethargic in 2015–16, declining from 2.8 percent in 2014 to 2.7 percent in 2015 to 1.3 percent in 2016. Volatility in exchange rates and persistent weaknesses in global commodity prices, particularly for oil, which are priced in US dollars, resulted in a divergence between world merchandise trade figures in 2015–16 by volume and by value. Volume remained flat in 2015, but the value showed a sharp decline, with world merchandise exports falling 14 percent from 2014 (US$19 trillion) to 2015 (US$16 trillion) and 3.3 percent from 2015 to 2016 (US$15.46 trillion).

North American exports grew marginally, at 0.5 percent in 2016, down from 0.8 percent growth in 2015 and 4.1 percent in 2014. This sluggishness largely reflected weaknesses in the merchandise exports of the United States, the largest economy in the region. In Asia growth in merchandise exports rebounded slightly, to 1.8 percent in 2016 from a slump of 1.1 percent in 2015, but remained far below the 4.3 percent in 2014. The deceleration of merchandise exports in the region was due largely to weak performances in China and India, the two largest economies in the region. In Brazil and other developing economies, growth in exports remained weak in 2015–16 due to low prices of oil and other primary commodities and to higher exchange rate volatility. Brazil was hit by a wave of political scandals, a deep recession, a fiscal crisis and falling export prices, which undermined the performance of South and Central America, whose merchandise exports grew 1.3 percent in 2016.

Africa’s total merchandise trade fell 14.3 percent from 2014 (US$1.21 trillion) to 2015 (US$1.03 trillion) but rebounded 4.1 percent in 2016 (to US$1.08 trillion). The contraction in 2015 was due largely to slow growth in many developed and developing economies,

weak global demand for commodities and a challenging global environment, including the sharp decline in global commodity prices and the slowdown of the Chinese economy. However, China is still Africa’s largest country trade partner—accounting for 16.3 percent of Africa’s total trade in 2015 and 11.9 percent in 2016—followed by France—which accounted for 6 percent of Africa’s total trade in 2015 and 4.8 percent in 2016. The European Union remained Africa’s largest trade partner—accounting for 43.2 percent of Africa’s total trade in 2015 and 38.9 percent in 2016, though its share has been steadily declining over the last few years (after a peak of 45.1 percent in 2013).

Following growth of 8.6 percent in 2015, intra-African trade grew marginally by 0.6 percent in 2016, to US$156.94 billion. While still below the peak of US$174.9 billion in 2013, this growth was driven by a modest recovery in commodity prices, particularly in energy markets; improved regional trade across regional economic communities; and some countries’ increased focus on promoting intra-African trade. Trade within regional economic communities remained buoyant, aided by market access preferences and continued efforts to develop trade and transport corridors for intra-African trade.

At the regional level the Southern African Development Community (SADC) remained the most vibrant trading bloc on the continent, underpinned by strong demand for South African exports from other SADC countries, despite the dampening effect of the decline in energy prices. South Africa (23.3 percent), Nigeria (8.5 percent) and Namibia (8.1 percent) were the drivers of intra-African trade. Still, at about 15 percent of the continent’s total merchandise trade, the share of intra-African trade compares unfavourably with intra-regional trade in other regions—Europe (67 percent), Asia (58 percent), North America (48 percent) and Latin America and the Caribbean (20 percent).

12 CHAPTER ONE AFRICAN TRADE REPORT 2017

1.4 Prospects

Global growth is projected to rise to 3.5 percent in 2017, from 3.1 percent in 2016, as global economic activity continues its gradual improvement, supported by rising investment and manufacturing output coupled with an expected pick-up in global demand. Underpinned by accommodative policies, cyclical recovery, rising global manufacturing and improving market confidence, the gradual pick-up in economic activity among developed economies is expected to be sustained. The US economy is projected to strengthen, driven by growing public spending, especially on infrastructure; increasing manufacturing output; and rising consumer spending on the back of falling unemployment. In the Eurozone, the combined effects of cyclical recovery from the global financial crisis, abatement of the impact of the sovereign debt crisis, and accommodative monetary policy are expected to sustain the pace of 2016’s growth at 1.7 percent in 2017.

Growth in developing economies is projected to strengthen slightly, on the back of strong activity in India and expected recovery in Brazil. However, major downside risks include sustained growth deceleration in China as the country rebalances, with consequent dampening effects on commodity prices and revenues in commodity-dependent countries; tighter external financing conditions; and pronounced reversal of capital flows to the United States owing to gradual increases in interest rates by the US Federal Reserve, which are likely to strengthen the US dollar.

African economies are projected to strengthen, with growth quickening to about 3.4 percent in 2017, up from 2.8 percent in 2016, largely reflecting the gradual recovery in developed economies and knock-on effect on global demand, which will help sustain the upward momentum of most commodity prices and lift the growth of Africa’s merchandise trade. The projected recovery

of the largest economies in Africa, notably Nigeria on account of higher oil prices and growing public investment as well as South Africa and Angola, is also expected to pull up GDP growth on the continent.

Growth in the volume of global merchandise trade is projected to strengthen to 2.4 percent in 2017, from 1.3 percent in 2016, mirroring improvements in the global economy, led by a synchronized modest expansion in developed economies, notably the United States, Canada, and France, and a slight pick-up in developing economies, driven by strong performance in India and recovery in Russia and Brazil. Potential downside risks include sustained growth deceleration in China. Also, uncertainty associated with trade arrangements between the United Kingdom and the European Union after the vote on Brexit and the spectre of rising protectionism could limit the global recovery.

Still, intra-African trade is projected to improve as countries in the region continue to undertake measures and initiatives at the national and regional levels to boost intra-regional trade with a view to insulate themselves from global shocks. Efforts across the continent to deepen regional integration are expected to build a solid foundation for dynamic intra-African trade in the medium to long term, especially the Tripartite Free Trade Area aimed at deepening and strengthening economic integration in Southern and Eastern Africa; the Common External Tariff of the Economic Community of West African States to promote investment and industrialization and facilitate exports of processed goods; and the Continental Free Trade Area.

1.5 Structure of the Report

The report is organized in nine chapters. Chapter 2 presents thematic research on domestic resource mobilization. Chapter 3 reviews global macroeconomic and financial

developments, including Africa’s, while Chapter 4 discusses the global trade and trading environment. Chapter 5 looks at the dynamics of commodities, with an emphasis on commodities of trade interest to Africa. Chapter 6 examines the re-emergence of protectionism and its implications

for global and African trade. Chapter 7 discusses trade facilitation, highlighting Africa’s particularities while reviewing the role of such facilitation in promoting trade and economic growth. Chapter 8 focuses on intra-African trade. Chapter 9 reviews growth, development and trade prospects.

AFREXIMBANK AFRICAN TRADE REPORT 2017 13

2Chapter Two

AFREXIMBANK AFRICAN TRADE REPORT 2017 15

Bridging Africa’s Trade Finance Gap Through Domestic Resource Mobilization

Capital is essential for industrial upgrading, sectoral diversification, trade and infrastructure development, and many successful developing economies rely on domestic capital mobilization for investment and growth. High saving and investment rates have helped the economies that have consistently achieved robust economic growth rates over the last 25 years, setting them on a path to substantial capital accumulation. For instance, in China, Japan and the Republic of Korea foreign direct investment played only a small role in industrial investment. Instead, domestic resources were crucial for upgrading and capacity growth.

In contrast to the Asian development model, decades of insufficient foreign direct investment and of capital flight have left African economies severely undercapitalized, compromising total factor productivity and prolonging disinvestment by limiting returns to capital and ultimately undermining the diversification of Africa’s trade and its integration into the global economy. Ndikumana (2015,) argues that “by draining domestic resources, capital flight perpetuates dependence on external aid even as it undermines aid effectiveness”.

Furthermore, capital account liberalization, supported by Washington Consensus reform prescriptions, induced capital flight and may have constrained accumulation (Hermes and Lensink 2014). In seeking to stimulate industrial growth in sectors consistent with comparative advantages, developing countries often require immediate capital injections. Given the continuing frictions in international capital flows, sources of rapid capitalization exist more among domestic investors than among foreign investors. Domestic resource mobilization is thus crucial to economic transformation and must be understood from both a historical and cross-sectional perspective. It may even be more important now that there is a concerted effort to accelerate industrialization of African economies, as illustrated by the selection of industrialization and export development as the second pillar of the African Export–Import Bank’s Fifth Strategic Plan.

The Monterrey Consensus, which emerged from the United Nations International Conference on Financing for Development in 2002, emphasized the role of domestic resource mobilization in achieving the Millennium Development Goals. The

16 CHAPTER TWO AFRICAN TRADE REPORT 2017

2005 UN Millennium Project included domestic resource mobilization in a suite of initiatives alongside capacity building, public investment and official development assistance. According to USAID (2016), domestic resource mobilization programmes generate US$20 in increased revenue for every US$1 of related assistance. In 2014 the United States announced a US$63 million programme to assist countries in mobilizing domestic resources for public health initiatives. The variety, scope and depth of challenges facing developing countries—public health, education, infrastructure (including trade-supporting infrastructure), to name just a few—require more resources than what foreign aid can provide. This partly explains the rising interest in domestic resource mobilization from both academia and practitioners.

This chapter examines the importance of domestic resource mobilization for growth, trade and economic development and structural transformation in Africa, highlighting key persistent challenges. It discusses various successes and failures in raising domestic resources in support of investment and growth from around the globe. And it concludes with lessons for domestic resource mobilization and structural transformation as well as policy lessons for Africa.

2.1 Domestic Resource Mobilization and Structural Transformation in Africa

In an early study of Asian developing countries, Dowling and Hiemenz (1983) operationalized governments’ role in domestic resource mobilization as a ratio of tax revenue to gross domestic product (GDP), finding that government contributions to domestic resource mobilization have a significant positive effect on GDP growth despite the diminishing effect of higher taxes on private capital formation. Vos et al. (2007) took a

less sanguine view, arguing that financing Millennium Development Goal initiatives from taxes and domestic borrowing has negative macroeconomic impacts, including “Dutch Disease” (rising real exchange rates due to rapid capital inflows), the crowding-out of private investment and less disposable income. They argued that domestic resource mobilization strategies can also have unexpectedly delayed effects.

Scholarship has also explored different types of domestic resource mobilization. Binagwaho and Sachs (2005) argued that value-added taxes are an example of broad-based revenue initiatives needed to expand the fiscal space for increased resource mobilization. They recommended “rechanneling current low-priority spending into higher priority MDG investments” (p. 55).

Chong-Hyun and Chang-Jin (2000) found that the Republic of Korea’s corporate sector accounts for a large percentage of national savings and was crucial in mobilizing domestic resources in the country’s rapid development in the 1960s and 1970s. Extending the focus on the private sector, Fofack and Ndikumana (2009) argued that a potential source of domestic resources for Africa lies in repatriation of a vast store of capital that fled the continent for foreign banks. For example: the depletion of domestic resources in Nigeria throughout the 1970s and 1980s, when capital outflows exceeded foreign debt accumulation (Ajayi 1995). Weisskopf’s (1973) study of post-colonial India argued that the government’s failure to limit demand for foreign goods and services (particularly among wealthy consumers) constrained the growth of domestic capital.

While domestic capital markets are a potentially valuable source of domestic resource mobilization, many African countries’ under-developed or under-diversified industrial structures reduce their ability to channel surplus savings

AFREXIMBANK AFRICAN TRADE REPORT 2017 17

to productive investments. Options for drawing on external financing in the form of portfolio investments to the region are constrained because most African countries are not connected to the global financial architecture and because their financial infrastructure deficits of the last few years have further increased their dependency on foreign aid.

Tax reform, although it has been shown to hamper domestic consumption and raise producer costs, is an opportunity for governments to improve domestic resource mobilization (Ndikumana et al. 2015). Nevertheless, Africa continues to suffer from constraints to domestic resource mobilization.

Understanding the role of industrial policy and institutions in the growth patterns of resource-rich developing countries requires understanding the links among domestic resource mobilization, capital inflows and outflows, and economic transformation. Africa suffers from low physical capital despite having abundant natural resources and a large population. These conditions suggest the potential for high marginal product and subsequent attraction of capital—but they have not materialized.

The two channels of capital inflows for upgrading—government and the private sector—are both subject to perceptions of sovereign risk. Domestic and foreign investors must be assured that returns are lucrative and that loan repayments are guaranteed; financial intermediation is one method of addressing these concerns. According to Ndikumana and Blankson (2015, p. 24), “efficient financial intermediation…helps to channel resources into the most productive investments”. However, Africa’s weak financial intermediation constrains the flow of capital from private creditors to private borrowers. Costs associated with financial intermediary activity are numerous, and transaction costs are higher than those in

developed countries, limiting capital flows where government institutions are weak, loan markets thin, lending capacities low and trust among contracting parties lacking. The financial intermediary industry is designed to address such lending risks, but in Africa its underdevelopment has been a substantial deterrent to foreign direct investment.

Other risks that hamper capital inflows and raise Africa’s external finance premium include the threat of domestic and international banking crises, which reduces available risk capital; erroneous perceptions of high risk associated with investing in Africa; and weak or missing financial markets. These factors illustrate the challenges of mobilizing external resources for Africa and the need to explore the prospects for domestic resource mobilization.

2.2 Successes and Failures in Domestic Resource Mobilization and Structural Transformation

Many African countries still face the challenging growth conditions once endured by many developing countries in the post–World War II era: poor infrastructure, low educational attainment, high death rates with high population growth, and dependence on extractive industries and manufactured imports. Many developing post-war economies adopted an industrialization strategy centred on capital-intensive manufacturing, seeking to replicate the success of such industries in developed countries. However, this abrupt strategic shift was incompatible with the factor endowments of these largely agrarian economies. Further, it allocated aid capital and already scarce domestic capital to comparative advantage–defying industries (industries that are non-viable in competitive markets and require government policy support for their initial investment and continuous operations). Consequently, modern industries in

18 CHAPTER TWO AFRICAN TRADE REPORT 2017

developing countries, including Africa, failed to achieve the success of those in developed countries and remain uncompetitive and unprofitable.

To account for the costly and disruptive mismatch between industrial structure and factor endowments, most governments in Africa and other developing countries embraced interventionist policies, moving away from strict laissez-faire policies to protecting failing industries. However, this artificial support generated opportunities for rent-seeking behaviour, corruption and embezzlement (Kornai 1986; Schaffer 1998; Kornai et al. 2003). A perverse symbiosis emerged whereby firms relied on government subsidies and intervention despite the distortionary nature of such policies, and government relied on the survival of firms to maintain output, employment and social stability.

The reforms prescribed by post-war development institutions and governments embracing neoliberal ideology falsely

attributed stagnation to government failures, calling for the immediate and comprehensive removal of distortions and envisioning a single massive leap from central planning to market-based resource allocation. However, these recommendations were founded on an incomplete understanding of the interdependencies between governments and uncompetitive industries, which over time had ossified into an endogenous, albeit unproductive, equilibrium based on the misguided strategy of import substitution. Lacking any economic protection, these industries quickly failed and sent tenuously stable developing economies plummeting, in an era in Africa known as the lost decades (Artadi and Sala-i-Martin 2003; Fofack 2014). Countries that continued with market-distorting policies “under the radar” likewise suffered—first because new supportive policies were less efficient than the ones they replaced and second because developed countries with competitive industries commanded an increasing share of global trade and crowded out firms from developing countries.

AFREXIMBANK AFRICAN TRADE REPORT 2017 19

Notable counter-examples include the rapidly developing post-war economies of East Asia and Southeast Asia, as well as China. These newly industrializing economies eschewed the structuralist model of import substitution that focused on comparative advantage–defying and capital-intensive heavy industries and instead adopted a dual-track approach that maintained support for unviable industries while opening the production market to private firms. They also acquired foreign technologies to achieve structural change oriented towards comparative advantages. The resulting growth of labour-intensive industries initially generated rapid growth and attracted industries from countries with increasingly high labour-cost structures.

Over time, economic prosperity enabled these economies to invest public and private surpluses to improve factor endowments, including in infrastructure, technology-based industrial upgrading and workforce education. As they advanced rapidly through development stages, their constantly evolving factor endowment structures enabled them to become globally competitive in higher value-added production, particularly leading-edge technology. Examples are the Republic of Korea’s automobile industry; Taiwan, China’s semiconductor industry; and Singapore’s petrochemicals industry, all of which leveraged national comparative advantages such as labour productivity and innovative capacity.

Africa seems to have followed a different, if not the opposite, path. Despite evidence that comparative advantage is the basis of an effective growth strategy, many African countries failed to identify priority industries, while industrial policies have generally been ineffective. This failure has led to the allocation of resources either to existing low-growth industries or to advanced, overly ambitious, comparative advantage–defying industries. This strategic failure has perpetuated economic stagnation

and unemployment and kept several countries in a low-income trap.

The inherent strategic flaw is that governments targeted industries that did not take into account comparative advantages, forcing firms into competitively untenable positions where they were compromised either by low product quality or by high factor prices. In the absence of market distortions these firms were non-viable in globally competitive markets, and globalization only magnified growing gaps in competitiveness. Exploiting the weaknesses of economic planning elsewhere, firms in the newly industrializing economies entered markets with lower barriers to trade and outperformed the beneficiaries of legacy industrial policies in less successful countries.

To support initial investments and ensure favoured firms’ continued operations, African governments “doubled down” on their bad bets by channelling more resources into non-viable firms and sectors and by adopting numerous protectionist measures such as subsidies and tariffs. This misallocation led ultimately to rent-seeking by beneficiary industries but did nothing to improve long-term development. A fatal knock-on effect of this strategy was the suppression of investment returns, prompting capital flight and inhibiting foreign direct investment in most industries, natural resources aside. Under these conditions the Lucas Paradox arose (capital-starved economies became net exporters of financial resources), reflecting low domestic returns to capital and lost confidence among investors, foreign and domestic (the latter, owners of wealth often derived from rents and rent-seeking).

2.3 Approaches to Mobilizing and Deploying Domestic Resources

Almost all developing countries began their transition to the market system in

20 CHAPTER TWO AFRICAN TRADE REPORT 2017

the 1980s, out of pressure to improve development performance that had lagged under economic planning. Most countries in Africa and Latin America followed the Washington Consensus but were caught in the lost decades of the 1980s and 1990s. By contrast, several economies in East Asia adopted a gradual approach to development that avoided an immediate and full-scale embrace of free markets. This strategy proved highly successful, with these countries achieving macroeconomic stability and sustaining dynamic growth. A comparison of these case types offers lessons for transition strategies.

Before the advent of the 20th century’s rapid and unprecedented industrial restructuring, growth in developing countries was constrained by non-viable firms in legacy sectors. Transition strategies recommended by development advisors and aid organizations encouraged African governments to immediately eliminate all distortions, precipitating sectoral collapse and leading to deindustrialization, unemployment and strains on social support efforts. This fallout was particularly challenging at a time when government budgets were constrained by falling revenues. Washington Consensus–based reform prescriptions also discouraged governments from facilitating firms’ entry into sectors consistent with comparative advantages. So capital returns stayed low and capital flight endured.

By contrast, successful transition economies illustrate how a pragmatic and gradual approach enabled a smoother industrial restructuring without the economic and social disruptions accompanying free market “shock therapy”. The dynamic transition economies of China, Vietnam, Mauritius and Cambodia adopted this approach using a dual-track strategy. First, governments continued to provide transitional support to non-viable firms in legacy sectors and removed distortions only when those firms became viable or their sectors contracted.

Second, governments facilitated private firms’ entry into sectors that were consistent with national comparative advantages latent before transition. This dual strategy ensured stability while stimulating dynamic growth. It was also favourable to domestic resource mobilization and foreign direct investment.

According to Lin and Monga (2010, p. 18), “Policymakers around the world, especially in developing countries, still face difficulty in identifying actionable specific policy levers that can help ignite and sustain the type of dynamic growth rates that are necessary to reduce poverty”. There are numerous cases of successful economic transformation that can serve as examples for aspiring countries, but few are as dramatic and instructive as China’s, especially for growth, trade performance and poverty reduction.1 Deng Xiaoping’s reforms and “open door policy”, while appearing to outsiders to be an embrace of neoliberal market reforms, in reality represented a nuanced approach to development that simultaneously supported legacy industries by retaining some market distortions while liberalizing factor markets and enabling private sector growth to pursue comparative advantage–following industries.

This gradual and hybrid strategy helped China avoid the negative economic and social impacts endured by countries that chose, or were coerced into, shock therapy liberalization. With stable and shock-free economic growth, China’s household consumption fell as a percentage of GDP, while fixed asset formation and net exports rose. Growing savings provided a financial asset base to support industrial upgrading. Although China must eventually address growing income inequality, unsustainable

1 In its transition to a fully developed economy,

China achieved sustained and rapid economic

growth while reducing its poverty rate from 85

percent in 1981 to 24 percent in 2004, lifting 600

million people out of poverty (World Bank 2010).

AFREXIMBANK AFRICAN TRADE REPORT 2017 21

pension systems and lingering distortions in finance, natural resources and services, the success of its dual-track model is evidence of its validity. According to Lin (2013, p. 265), “No country in human history has ever grown so fast for so long as China did in the past three decades”.

Comparative advantage–based industrial policies have mitigated the risks of the Lucas Paradox in developing economies, and the results provide insights for governments and development finance institutions. In designing transition strategies and performance, countries must first identify an optimal economic governance framework that turns latent comparative advantages into “quick-win activities” that can be scaled up in support of structural transformation. To achieve this goal, countries must

reinterpret legacy economic planning as an industrial policy that emphasizes a facilitating but non-interventionist state. This type of industrial policy casts government not as an arbiter of sectoral determinism and favouritism, but as a provider of infrastructure and coordination that help industries attract capital and grow endogenously around factor endowments and comparative advantages. While government tasks may vary across countries depending on development conditions and the needs of industries and firms, industrial policy must be applied tactically, given the limited resources and capacity of the public sector.

The opportunities for domestic resource mobilization are promising, but the challenges are equally formidable. A

22 CHAPTER TWO AFRICAN TRADE REPORT 2017

development approach that avoids the interventionist determinism of traditional structural economics on the one hand, while shunning the anti-government ideology of neoliberalism on the other, implies that governments are responsible for conditions that attract foreign direct investment in sectors aligned with comparative advantages.

A new generation of economic governance reflects this approach to balanced and pragmatic economic stewardship and regards governments as facilitators of growth, creators of markets, enforcers of institutional norms and providers of enabling infrastructure. Further, these tasks must occur within the context of aligning industrial structure with factor endowments. In soliciting investment amid an increasingly competitive and financially constrained aid environment, countries must consider stores of capital held domestically. Encouraging domestic investors to commit their money to domestic firms and industries partly involves effective “branding”: a commitment to good governance and prudent industrial policy should be as reassuring to domestic investors as it is to foreign investors.

Lin (2012, p. 5) states that “Economic development is a process of structural change with continuous technological innovations, industrial upgrading, and improvement in infrastructure and institutions”. To this end, modern economic development is a process of continuous growth identification and facilitation: technological innovation and industrial upgrading that requires consistency in capital flows. Under the right conditions developing countries can achieve middle- or even high-income status after several decades of dynamic growth, but only if they exploit comparative and latecomer advantages. Poor development performance in Africa is the result of inadequate ideas that have wrongly shaped government policies for economic transition. Indeed, policy credibility requires availability of funds

to propel the continent towards accelerated growth and structural transformation. The right ideas, in combination with a new regime of cooperation among developing countries, can help African countries transform natural endowments into productive assets and grow as dynamically as the world’s most successful economies.

In this context, and given declining external capital flows, mobilization of domestic resources has gained traction among African governments, policy makers and academics. As available data on foreign reserves suggests, the challenge has not been lack of resources but the ability to effectively harness existing financial resources. Foreign reserves held by African central banks on behalf of their countries grew rapidly over the last 20 years (Figure 2.1), fuelled by the commodity super-cycle and debt relief under the World Bank’s Heavily Indebted Poor Countries (HIPC) Initiative, which enabled countries to grow their reserves. External reserve holdings of African countries rose from US$42 billion in 1995 to US$550 billion in 2013 before declining because of the end of the commodity super-cycle. Despite this wealth of liquidity, Africa’s reserves are either largely domiciled offshore or invested in foreign securities, which consequently restricts their use in funding viable trade, project and developmental needs of the continent.

A number of African countries are now making concerted efforts to mobilize domestic resources in support of long-term investment and economic growth by improving tax collection, broadening the tax base, reducing capital flight and increasing financial resource mobilization. The African Capacity Building Foundation (ACBF) (2015) notes that African countries have sought to improve fiscal revenues through reforms to boost domestic resource mobilization. These reforms include measures to modernize revenue management administration, expand the tax base, combat illicit financial flows and leverage financial resources. Tax

AFREXIMBANK AFRICAN TRADE REPORT 2017 23

revenue performance in African countries shows a positive trend, with average tax revenue as a share of GDP rising from 22 percent in 1990 to 27 percent in 2000, and reforming and widening the tax net of the continent will help address loopholes in existing tax structures.

African sovereigns, multilateral financial institutions and, to a smaller extent, corporations are also increasingly tapping into domestic currency markets to finance large-scale infrastructure development projects or investments, drawing on excess liquidity in the domestic banking system coupled with low yields while mitigating currency risks. For instance, the government of Côte d’Ivoire has successfully mobilized funds from within the West African Economic and Monetary Union and manages a local currency bond portfolio of around US$4.6 billion. Ethiopia introduced a housing savings programme; introduced pension programmes for government, nongovernmental organizations and the private sector; and issued diaspora bonds to finance large projects such as the Grand Renaissance Dam (ACBF 2015). Egypt issued domestic bonds to leverage finance for the expansion of the Suez Canal, a main artery for global

trade and significant foreign exchange earner for the country.

Similarly, several African countries used domestic bond issuances to raise resources in support of investment projects. The African Development Bank’s African Financial Markets Initiative Bloomberg African Bond Index, which assesses and tracks the market value of Africa’s most liquid local currency sovereign bond issuances, had a market capitalization of US$160 billion at the end of 2016, up from US$146 billion at the end of 2013, as Nigeria, South Africa, Ghana and Namibia reverted to domestic resources to champion national development efforts. The African Export-Import Bank, through its Central Bank Deposit Programme, is also supporting mobilization of domestic resources that can be deployed to galvanize intra-Africa trade and boost the continent’s structural transformation.

2.4 Policy Lessons for Africa

The efforts by African countries to mobilise and deploy domestic resources is commendable and should be done in the context of a robust industrial strategy. An overview of the history of economic

Figure 2.1: Africa’s reserve position, 1995–2016 (US$ billions)

Source: World Bank World Development Indicators Database, Afreximbank Annual Reports (2010-2016)

500 -

600 -

0 -

100 -

200 -

200 -

300 -

400 -

1995

20

03

201

1

199

9

20

07

201

5

1997

20

05

201

3

20

01

20

09

199

6

20

04

201

2

20

00

20

08

201

6

199

8

20

06

201

4

20

02

201

0

24 CHAPTER TWO AFRICAN TRADE REPORT 2017

development suggests that a winning strategy is one where developing countries look at what they can do well, based on what they have, and then create the conditions to scale up what they can do well (Lin 2012). The case of successful developing economies is used to provide the following five policy lessons for African countries.

First, countries must base their industrial promotion strategies on their current stage of development. This requires a diligent and honest accounting of factor endowments, a robust strategy to facilitate their contribution to the development of targeted growth industries and a robust understanding of how the country’s tradable goods industries can become globally competitive or how to enhance the global competitiveness of that country’s growth industries. Further, countries must embrace rather than deny their backward status in technological innovation, upgrading existing technologies and committing resources to acquiring and integrating new technologies for upgrading efforts. This process must be repeated for each development stage when it is reached, as factor endowment structures will evolve and new opportunities for comparative advantage will emerge.

Second, efficient and reliable institutions are essential for loosening production

bottlenecks that discourage investment, particularly for hard infrastructure, logistics, information sharing, financial capital, bureaucratic red tape, legal systems, workforce development and all other transaction costs. This requires stability and consistency across multiple policy arenas and, depending on a country’s bureaucratic capacities, may also require deep administrative reforms and restructuring. Two examples are special economic zones and financial institutions.

For countries struggling to address these constraints through comprehensive national policy and administrative reforms, special economic zones provide a small-scale policy laboratory for testing experimental initiatives in a controlled environment. Special economic zones also facilitate the development of highly specialized infrastructure and generate economies of scale (multiple users sharing the same facilities) and economies of scope (facilities for one purpose can be used for other purposes). This approach, which includes industrial parks, export processing zones and other forms of concentrated economic activity, has been used to productive effect in China and Southeast Asia. For example: Chinese government’s 1979 special economic zone initiatives in Shenzhen, which precipitated one of history’s most dynamic

AFREXIMBANK AFRICAN TRADE REPORT 2017 25

urban growth stories, transforming a fishing village of fewer than 100,000 people into a modern metropolis of 19 million that serves as an anchor for the Pearl River Delta, home to 45 million. The region’s transformative economic progress is evidence in part of the effectiveness of the special economic zone approach, and lessons from Shenzhen ultimately informed similar initiatives across China.

Further reforms should target financial institutions, which should be tailored to meet the needs of labour-intensive firms in the emerging industries of developing countries (Lin et al. 2013). Many developing countries have adopted, by choice or coercion, the types of domestic financial systems that serve the economic structures and interests of developed countries. Developing countries need smaller scale financial institutions that cater to the types of firms, often at the household level, that supply factors of production to larger firms. As these countries progress through development stages, financial institutions can be redesigned to serve the increasingly sophisticated needs of larger domestic producers.

Third, an efficient market is an important institutional mechanism for signalling the relative prices of production factors—not only to global investors but also to firms in growth industries that might relocate from developed countries. These markets help the private sector identify a country’s cost-based comparative advantages by reflecting the scarcity of production factors within the country’s endowment mix, thereby mobilizing capital towards productive uses. The collective strategic decisions of profit-maximizing entrepreneurs, who are driven to substitute low-cost factors of production for high-cost factors, are generated naturally and without market incentives in an industrial structure that efficiently aligns itself with a country’s factor endowments. Here, markets play an essential role in facilitating the endogenous

growth of comparative advantage–following industries, free from the risks and distortions of direct government intervention.

Fourth, countries must work to increase capital abundance in their factor endowment structures, enabling the intermediate upgrading of existing industries and the longer term structural transformation away from labour-intensive industries and towards capital-intensive industries. From a policy perspective rapid capitalization is possible through budgetary and fiscal prudence, including revenue collection, and through industrial profitability, including support of industries that are aligned with their comparative advantages. As a country’s industries achieve efficiency, profitability and global competitiveness, theory holds that capital inflows will accelerate through international financial markets. Additionally, investments will become more attractive to domestic entrepreneurs.

Finally, governments must monitor trends in shifting factor endowments, identifying and supporting firms in growth industries and in industries with latent comparative advantages. One important lesson is that “government should know which new industries are consistent with the country’s changing endowment structure, and which infrastructure and institutions require improvements to enable those new industries to thrive” (Lin 2012, p. 6). With this industrial monitoring also comes the need for governments to adopt a counter-cyclical policy in economic shocks; for example, in periods of recession, governments should invest in infrastructure to take advantage of low costs of capital and to stimulate the macroeconomic environment through investment and employment. Government investments in hard and soft infrastructure, along with institutional improvement, facilitate the type of dynamic structural change that keeps national development on pace.

3Chapter Three

AFREXIMBANK AFRICAN TRADE REPORT 2017 27

Economic Environment

3.1 Output and Price Developments

The Global and African economic environment remained challenging during 2015-2016. The sluggish recovery of developed economies and the slowdown in developing countries, mainly China, were key factors dragging down global growth. This chapter reports on the global and African economic environment with a focus on output and price developments and financial market developments and financing conditions.

3.1.1 Global

Global economic activity remained subdued in 2015–16 after a marginal pick-up in 2014. From 3.4 percent in 2014, growth in global

output declined to 3.2 percent in 2015 and further to 3.1 percent in 2016 (Table 3.1 and Figure 3.1). The outturn in 2015 was driven by growth decelerations in developing economies, especially those in the Commonwealth of Independent States, Latin America and the Caribbean, and Developing Asia, whose rate of decline outweighed the modest recovery made by Group of Seven countries, especially Canada, Germany and Japan. However, hampered by unfinished post-crisis adjustments, especially within the Eurozone, performance in 2016 largely mirrored the sluggish recovery in developed economies after the 2008/09 global financial crisis. It was also affected by the adverse impact of growth decelerations in developing market economies, especially in a context of sustained declines in commodity terms of trade.

Figure 3.1. Global Output and Inflation (Percent)

4.5 - 9 -

2.5 - 5 -

3.5 - 7 -

1.5 - 3 -

0.5 - 1 -

4 - 8 -

2 - 4 -

3 - 6 -

1 - 2 -

0 - 0 -Developed Economies

Developed Economies

World WorldAfrica AfricaDeveloping Countries

Developing Countries

Real GDP (%) Inflation (%)

2015 2016

28 CHAPTER THREE AFRICAN TRADE REPORT 2017

Tabl

e 3.

1 D

evel

opm

ents

in G

loba

l Out

put,

201

4-16 Ex

chan

ge R

ate

Real

GD

P G

row

thInflationRate

Inte

rest

Rat

e (3

-mon

th),

%

(End

of

peri

od)

(ann

ual p

erce

nt c

hang

e)(a

nnua

l per

cent

cha

nge)

(end

of

peri

od)

2014

2015

2016

*20

1420

1520

16*

2014

2015

2016

*20

1420

1520

16*

WO

RLD

3,42

3,20

3,08

3,23

2,78

2,09

DEV

ELO

PED

ECO

NO

MIE

Sa)1,

882,

081,

571,

370,

270,

75

US

1,0

0 1

,00

1,0

0 2,

432,

601,

601,

610,

121,

190,

120,

230,

64

UK

0,6

4 0

,67

0,8

1 2,

992,

202,

001,

470,

050,

740,

540,

550,

49

Fran

ce 0

,82

0,9

2 0

,95

0,18

1,30

0,90

0,61

0,09

0,35

0,21

-0,0

2-0

,26

Japa

n 1

19,9

3 1

20,4

9 1

16,7

2 -0

,10

1,20

1,70

2,76

0,79

-0,1

60,

210,

170,

07

Ital

y 0

,82

0,9

2 0

,95

-0,4

30,

700,

600,

230,

11-0

,05

0,21

-0,0

2-0

,26

Cana

da 1

,16

1,3

9 1

,35

2,44

0,90

2,20

1,92

1,11

1,62

1,17

0,82

0,82

Ger

man

y 0

,82

0,9

2 0

,95

1,58

1,50

1,60

0,79

0,14

0,40

0,21

-0,0

2-0

,26

Mem

o It

em

EUR

O A

rea

0,8

2 0

,92

0,9

5 1,

082,

041,

660,

430,

030,

280,

21-0

,02

-0,2

6

DEV

ELO

PIN

G C

OU

NTR

IES

4,57

4,02

4,1

7 5

,85

4,7

0 4

,50

Afr

ica

3,91

2,89

2,84

6,41

6,77

8,06

Dev

elop

ing

Asi

a6,

776,

656,

513,

492,

703,

10

Lati

n A

mer

ica

and

the

Cari

bbea

n1,

03-0

,03

-0,5

54,

895,

535,

82

Dev

elop

ing

Euro

pe

2,81

2,59

3,28

3,78

2,90

3,10

Com

mon

wea

lth

of In

depe

nden

t St

ates

1,

07-2

,80

-0,2

68,

0715

,47

8,41

* E

stim

ates

Sour

ces:

1)

IMF

Wor

ld E

cono

mic

Out

look

Dat

abas

e (J

anua

ry, 2

017)

2)

Afr

exim

bank

Pla

n V

Str

ateg

y 3)

Oan

da, C

urre

ncy

Conv

erte

r (2

017)

4) O

ECD

(20

17)

AFREXIMBANK AFRICAN TRADE REPORT 2017 29

Global activity in 2015–16 was also influenced by a gradual slowdown and rebalancing of economic activity in China—the lead driver of global trade and growth—away from investment and manufacturing towards domestic consumption and services, which continued to adversely impact global demand and commodity prices. In addition, lower commodity prices, persistent volatility in financial markets, subdued investment, less accommodating financing conditions, gradual tightening in US monetary policy and uncertainty over creeping protectionism and greater use of anti-trade rhetoric also dampened global activity.

After a modest recovery in 2015, when output in developed economies grew 2.1 percent—up from 1.9 percent in 2014—output growth decelerated to 1.6 percent in 2016, due largely to deflationary threats and rising uncertainty. Growth in the United States, which strengthened from 2.4 percent in 2014 to 2.6 percent in 2015, decelerated to 1.6 percent in 2016. Output in the United Kingdom followed a similar trend of slowing for two consecutive years, with growth of 2.2 percent in 2015 and 2 percent in 2016, down from 2.9 percent in 2014. While weakening growth in the United States was attributed partly to global uncertainty, low investment (especially in energy) and low labour productivity (due to a deceleration in the capital-intensive manufacturing and energy-producing industries), economic activity in the United Kingdom, especially in 2016, was hit by uncertainty over the Brexit vote and the future trade arrangements between the United Kingdom and the European Union in the post-Brexit era.

The Japanese economy continued on its recovery path with sustained growth expansion over the past two years, after contraction in 2014. The Canadian economy recovered from a blip in 2015, when growth was 0.9 percent, posting growth of 2.2 percent in 2016 on the back of increased household consumption and a strong

financial services sector, but expansion remained below the 2.4 percent in 2014.

Recovery in the Eurozone remained lacklustre. After a sharp rise, from 1.1 percent in 2014 to 2 percent in 2015, real GDP growth decelerated to 1.7 percent in 2016. Output expansion in the bloc was supported by firm domestic demand and some growth in investment, though recovery remained slow, with investment on the downside in many economies in the zone. Although financial markets remained resilient, the legacy of the crisis, including inadequate demand, high debt and elevated unemployment, continued to pose challenges to robust growth. Germany, the bloc’s largest economy (accounting for about 30 percent of its GDP), showed growth of 1.8 percent in 2016, a slight recovery from the 1.5 percent in 2015 and 1.6 percent in 2014. The improvement derived from solid domestic demand driven by increased consumption and from strong export performance.

Economic activity across developing countries picked up slightly, to 4.2 percent in 2016, after a decline to 4 percent in 2015 from 4.6 percent in 2014. While 2015’s slow growth was due primarily to the slump in commodity prices, deceleration in developing economies (especially China), heightened uncertainty and global financial market volatility, the marginal improvement in 2016 was driven by the gradual pick-up in commodity prices in the second half of the year and by countries’ policy responses to mitigate the impact of the lingering effects of the global economic crisis. Growth in developing economies in 2015–16 was driven largely by Developing Asia, despite the sustained growth deceleration in China, with Africa stagnating at about 2.9 percent (see Table 3.1 and Figure 3.1).

The Middle East showed mixed results in 2015–16. Growth contracted 0.5 percent in 2015, from 2.5 percent in 2014, owing to plummeting oil prices, but improved

30 CHAPTER THREE AFRICAN TRADE REPORT 2017

markedly in 2016, to 2.5 percent, thanks to expanded output in Gulf Cooperation Council countries and a modest improvement in oil prices, increased government spending and solid domestic investment. However, activity in the region’s oil-importing countries remained insipid on the back of deep-rooted inefficiencies in economic structures, conflicts, persistent political instability and geopolitical tensions in several countries.

Output in Latin America and the Caribbean contracted in both 2015 and 2016. From anaemic growth of 1 percent in 2014, output contracted 0.03 percent in 2015 and 0.6 percent in 2016. Exports fell short of expectations in both years, and the terms of trade deteriorated in some countries. Domestic factors were also important as Brazil, the region’s largest economy, slipped into recession during the period.

After a moderate pick-up in 2014, growth in Central and Eastern Europe blipped in 2015 but recovered to 3.3 percent in 2016. While the deceleration in 2015 was due to weaknesses in some countries, especially amid political tensions and timid private investment, the improvement in 2016 was stimulated by strong net exports and accelerated activity reflecting a pick-up in investment, falling unemployment and higher public spending in some countries, especially Hungary. After posting growth of 1.1 percent in 2014, the Commonwealth of Independent States saw contractions in 2015–16. A drop in investment in Russia and Ukraine, because of geopolitical tensions, and lower oil prices weighed on the region’s performance.

Global inflationary pressures continued to ease in 2015–16, owing to declining headline inflation on falling commodity prices. Core inflation remained relatively stable but was generally below most central bank inflation objectives. Global inflation eased from 3.2 percent in 2014 to 2.8 percent in 2015 and dipped further, to 2.1 percent, in 2016 (see Table 3.1 and Figure 3.1).

Inflation in developed economies slowed to 0.3 percent in 2015, from 1.4 percent in 2014, owing to weaker commodity prices, declining global demand and general decelerations in economic activity globally. However, the gradual pick-up in commodity prices in 2016 contributed to renewed inflation, which inched up to 0.8 percent.

Inflation in the United States eased in 2015, from 1.6 percent in 2014 to 0.1 percent, but inched higher in 2016, to 1.2 percent. The US Federal Reserve raised interest rates for the first time in almost a decade in the last quarter of 2015. The movement in the general price level in 2015 was anchored on a tight monetary policy stance of the Federal Reserve, while increased inflation in 2016 was driven by market reaction to the incoming Trump Administration’s promise of expansionary policies.

Inflation in the United Kingdom slowed from 1.5 percent in 2014 to 0.1 percent in 2015, owing to fiscal tightening and to lower food, energy and fuel prices. However, the Bank of England’s loose monetary policy, intended to boost growth after the Brexit referendum in June 2016, put upward pressure on prices, with inflation rising to 1.2 percent that year, driven largely by prices of key non-food items such as fuel and clothing.

After years of deflation, the inflationary gains achieved in Japan during 2014 appeared to have been mitigated in 2015–16, as the change in prices levels declined from 2.8 percent in 2014 to 0.7 percent in 2015 to 0.2 percent in 2016, influenced largely by global trends.

In the Eurozone, inflation declined from 2014 to 2015 on the back of fragile domestic demand and lower energy, oil and food prices, though average price increases climbed to 0.3 percent in 2016, from 0.03 percent in 2015, partly because of quantitative easing by the European Central Bank, but remained below the 0.4 percent in 2014.

AFREXIMBANK AFRICAN TRADE REPORT 2017 31

For developing countries generally, inflationary pressures eased with the end of commodity super-cycle. Inflation declined from 5.9 percent in 2014 to 4.7 percent in 2015 and to 4.5 percent in 2016.

In contrast to global and regional trends, Africa recorded a modest increase in inflation, from 6.4 percent in 2014 to 6.8 percent in 2015 to 8.1 percent in 2016. Currency depreciation in oil-exporting countries raised the price of imported goods and exerted upward pressure on prices. Similarly, the CFA franc, which is the currency of most oil-exporters in the Central African Economic and Monetary Community (including Cameroon, Chad, Republic of Congo, Equatorial Guinea and Gabon) and which is pegged to the euro, depreciated against the US dollar in line with the euro, stoking inflationary pressures. But the global oil price slump provided support to real incomes in most oil-importing countries and contributed to lowering inflationary pressures.

3.1.2 Africa

Growth in Africa’s aggregate output slowed from 3.9 percent in 2014 to 2.9 percent in 2015 to 2.8 percent in 2016 (see Table 3.1 and Figure 3.1). After 2014, falling global demand and plunging prices for commodities created challenges for the continent that required fiscal adjustments. Matters were exacerbated by difficult domestic conditions such as heightened terrorist activities and the prolonged effects of the Ebola outbreak in West Africa.

The overall deceleration in 2016 stemmed from macroeconomic management challenges relating to the end of the commodity super-cycle, the continued slowdown in China, pockets of socio-political instability in some parts of North and West Africa, sluggish growth in the Eurozone (still one of Africa’s largest trade partners), and a weak pickup in economic activity in other developed economies. Needless to

say, growth in output varied across the continent.

In 2015–16 oil-exporting countries in Africa saw growth decelerate, from 2.8 percent in 2014 to 2.4 percent in 2015 to 0.3 percent 2016 (Figure 3.2 and Table 3.2). The trend reflected continued weakness in oil prices owing to subdued demand, driven largely by the slowing Chinese economy, and a global supply glut, led by high production in members of the Organization of the Petroleum Exporting Countries and by increased oil production in the United States and Canada. These patterns exerted pressure on export receipts of African oil exporters, depressing their reserves and leading to sharp fiscal adjustments in some countries, particularly the largest oil producers, Nigeria and Angola. The difficulties of this group were compounded by lingering socio-political unrest in parts of North Africa, particularly Libya, Sudan and South Sudan, which disrupted oil production and overall economic activity.

Although GDP growth in oil-importing countries declined marginally in 2015, to 3.2 percent from 3.4 percent in 2014, on

Figure 3.2. Average Real GDP Growth of African Net Oil Exporters and Importers, 2015-16 (Percent)

2015 2016

Real GDP (%)4.5 -

2.5 -

3.5 -

1.5 -

0.5 -

4 -

2 -

3 -

1 -

0 -

Oil Exporters Oil Importers

32 CHAPTER THREE AFRICAN TRADE REPORT 2017

Table 3.2 Africa: Real GDP Growth, 2014 - 16 (annual percent change)

Country Name 2014* 2015* 2016**Algeria 3,80 3,90 3,57Angola 4,80 3,01 0,00Benin 6,54 4,96 4,60Botswana 3,21 -0,26 3,11Burkina Faso 4,01 4,03 5,20Burundi 4,49 -3,96 -0,51Cameroon 5,93 5,80 4,80Cape Verde 1,87 1,45 3,63Central African Republic 1,04 4,80 5,19Chad 6,89 1,77 -1,11Comoros 1,95 1,03 2,16Congo, Dem. Rep. of 7,92 6,92 3,94Congo, Rep. of 9,47 2,32 1,75Côte d’Ivoire 6,85 8,54 7,98Djibouti 6,00 6,50 6,50Egypt 2,24 4,20 3,83Equatorial Guinea -0,50 -7,44 -9,87Eritrea 4,99 4,78 3,67Ethiopia 10,32 10,20 6,49Gabon 4,32 4,01 3,18Gambia -0,22 4,38 2,31Ghana 3,99 3,88 3,34Guinea 1,11 0,14 3,85Guinea-Bissau 2,54 4,80 4,80Kenya 5,33 5,65 5,99Lesotho 3,45 2,83 2,39Liberia 0,69 0,02 1,96Libya -24,03 -6,38 -3,32Madagascar 3,32 3,12 4,14Malawi 5,70 2,95 2,70Mali 7,04 5,96 5,31Mauritania 5,35 1,24 3,22Mauritius 3,62 3,50 3,52Morocco 2,55 4,51 1,85Mozambique 7,44 6,61 4,50Namibia 6,46 5,30 4,24Niger 7,05 3,55 5,23Nigeria 6,31 2,65 -1,75Rwanda 6,96 6,91 6,00Sao Tome and Principe 4,50 4,00 4,00Senegal 4,34 6,49 6,64Seychelles 6,21 5,74 4,88Sierra Leone 4,56 -21,08 4,29Somalia n/a n/a n/aSouth Africa 1,63 1,27 0,12South Sudan 2,92 -0,17 -13,12Sudan 1,61 4,88 3,05Swaziland 2,45 1,66 0,47Tanzania 6,97 6,96 7,17Togo 5,40 5,40 5,30Tunisia 2,26 0,80 1,50Uganda 4,93 4,81 4,94Zambia 5,03 3,00 3,01Zimbabwe 3,85 1,06 -0,29

* Revised** Estimatesn/a not availableSources: IMF (2016) World Economic Outlook Database (October)

AFREXIMBANK AFRICAN TRADE REPORT 2017 33

the rippling effect of the general economic downtown, the net benefit accruing from the commodity price shock to this group saw their output increase 3.9 percent in 2016. The pick-up was driven largely by a dynamic services sector led by telecommunications, banking, a growing construction industry and higher consumer spending, as well as infrastructure investment.

Regional variations

Except for North Africa, which experienced a contraction, other regions saw growth decelerate. The weakest performer was Central Africa. On inflation, North Africa was by far the poorest performer, as inflation there shot up, while in Eastern and Central Africa it abated.

North Africa saw GDP grow 2.2 percent in 2014 and 1.7 percent in 2015 but contract 0.4 percent in 2016 (Figure 3.3 and Table 3.2). For most countries in the region the deceleration and subsequent contraction in the face of rising macroeconomic management challenges was driven by loss of revenue from declining commodity prices, exacerbated by socio-political instability in Libya. The tourism sector in Egypt and Tunisia was hit by security concerns.

Inflationary pressures in North Africa increased in 2015–16, with inflation surging to 80.2 percent in 2016, from 4.3 percent in 2014 and 15.1 percent in 2015 (Figure 3.4 and Table 3.3). Currency depreciations pushed up import costs, particularly in Algeria and Egypt. Reductions in subsidies and rising domestic demand also raised prices, particularly in Algeria, Egypt and Morocco.

Figure 3.3. Africa: Output by Region, 2015–16 (Percent)

Figure 3.4. Africa: Inflation by Region, 2015–16 (Percent)

Although economies in Southern Africa witnessed a moderate increase in output growth in 2015, they lost steam in 2016. GDP growth was up from 2.4 percent in 2014, to 2.7 percent in 2015, but decelerated to 2 percent in 2016 due to challenges facing the South African economy, the largest in the region. That country’s economy remained weak, growing only 0.1 percent in 2016, down sharply from 1.3 percent in 2015. The economy was choked by recurrent power shortages and their adverse effects on manufacturing, coupled with dwindling global demand for the country’s major natural resources. The poor performance of other economies, notably Lesotho, Swaziland and Zimbabwe, caused by weaknesses in commodity markets and a major drought, also undermined growth.

North WestSouth East Central

7 -

3 -

5 -

1 -

-1 -

6 -

2 -

4 -

0 -

2015 2016

North WestSouth East Central

90 -

50 -

70 -

30 -

10 -

80 -

40 -

20 -

60 -

0 -

2015 2016