african mega trends: shaping and prolonging the future of lubricants

TRANSCRIPT

1

We Accelerate Growth

African Mega Trends: Shaping and

Prolonging the Future of LubricantsUnlocking Africa’s potential

“The 2nd ICIS African Base Oils & Lubricants Conference”

by Anthony Lawrence

2

Africa’s Mega Trends – The Future for Lubricants

Table of Contents

Why Frost & Sullivan

Mega Trends & Africa Perspective

What does this all mean for the Lubricants Market?

Snap shot into key African Markets

What does the future hold for the lubricants market?

3

Why Frost & Sullivan

Founded in 1961

• African office based in Cape Town• Staff compliment of 70 focussed on Africa

Clients worldwide, including emerging companies, the global 1000, and the investment community

Growth Partnership

ServicesGrowth

ConsultingEvents

Pioneered emerging market & technology research

Partnership relationship with clients, via consulting services and cross-industry events

Visionary innovation support via megatrends research, development of the GIL global community

4

Mining & Manufacturing

Industrial, Automation &

Process Control

Business, Financial Services

& Education

Environmental & Building

Technologies

Healthcare

Energy & Power

Systems

ICT Chemicals, Materials & Food

Aerospace & Defense Automotive & Transportation

A wide industry and technology breadth uncovering new creative markets and ideas

Global Industry Research Focus

5

How we align our research with your needs

Relevant Global/ African

Mega Trends

Selection of

relevant Mega

Trends in Africa

Design the

research for

most relevant

sectors

Frost & Sullivan’s Mega Trends / Theme based approach to designing a research strategy

Analyzing the key mega trends from the Global / African perspective – Key drivers of growth

Selecting the most relevant specific trends and identify themes / concepts for Africa - Identifying growth opportunities together

Africa Focus – Transportation Chemicals, Water Treatment & Sanitation, Agriculture, Oil & gas, mining, renewable energy, construction & infrastructure, manufacturing, consumer products & materials

MT MT MT MT MTMT

Aligning our research with your requirements and

needs

6

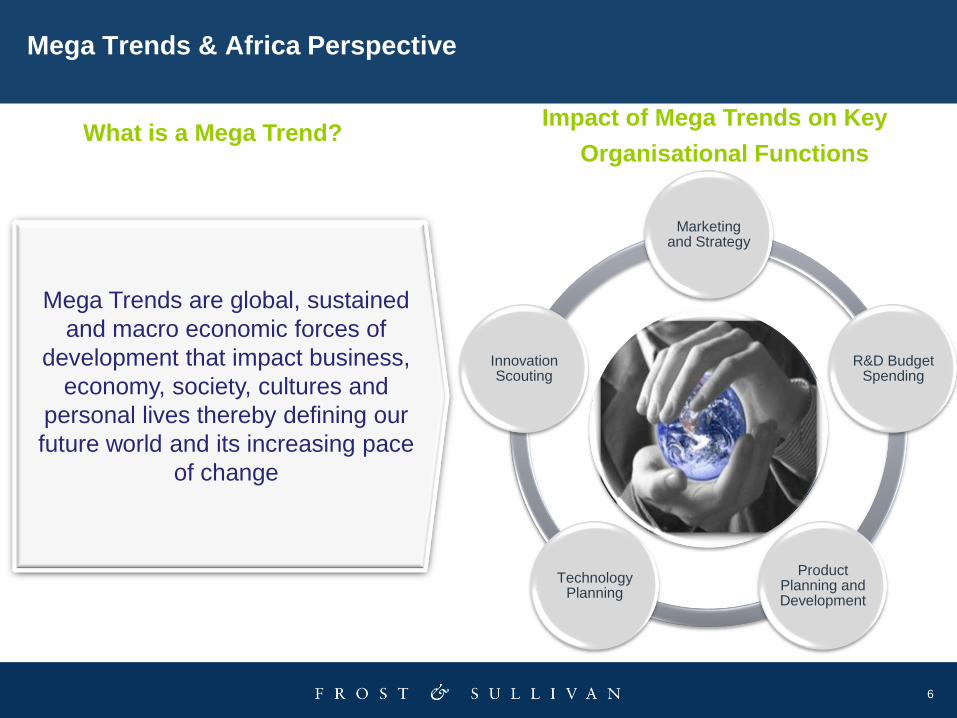

Mega Trends & Africa Perspective

What is a Mega Trend? Impact of Mega Trends on Key

Organisational Functions

Mega Trends are global, sustained

and macro economic forces of

development that impact business,

economy, society, cultures and

personal lives thereby defining our

future world and its increasing pace

of change

Marketing and Strategy

R&D Budget Spending

Product Planning and Development

TechnologyPlanning

InnovationScouting

7

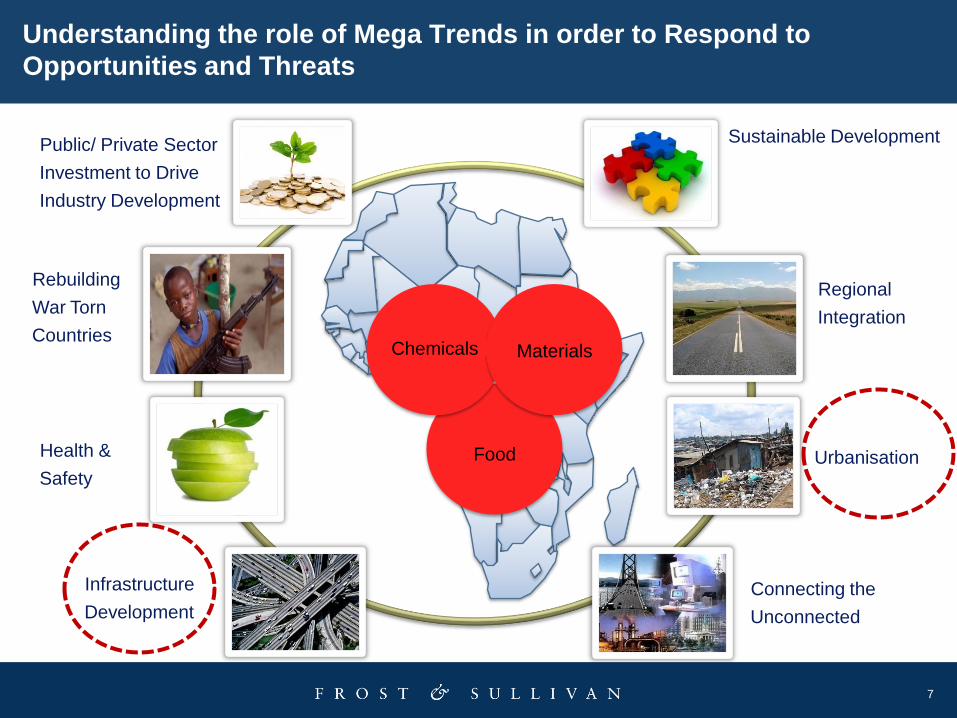

Regional

Integration

Public/ Private Sector

Investment to Drive

Industry Development

Infrastructure

Development

Sustainable Development

Connecting the

Unconnected

Urbanisation

Chemicals Materials

Food

Rebuilding

War Torn

Countries

Health &

Safety

Understanding the role of Mega Trends in order to Respond to

Opportunities and Threats

8

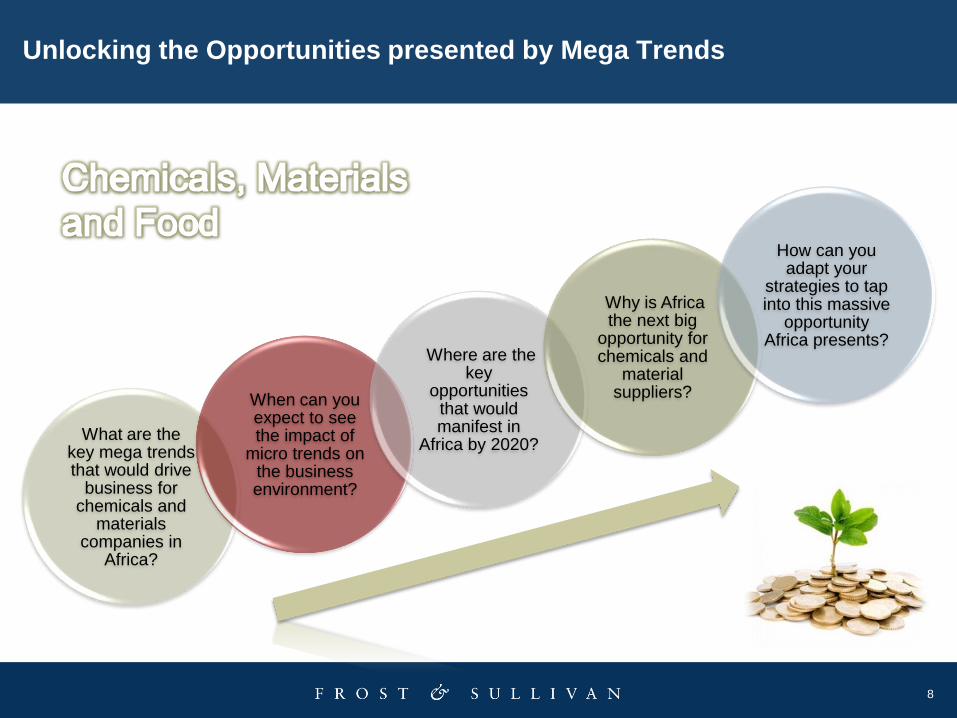

Unlocking the Opportunities presented by Mega Trends

What are the key mega trends that would drive

business for chemicals and

materials companies in

Africa?

When can you expect to see the impact of

micro trends on the business environment?

Where are the key

opportunities that would manifest in

Africa by 2020?

Why is Africa the next big

opportunity for chemicals and

material suppliers?

How can you adapt your

strategies to tap into this massive

opportunity Africa presents?

9

HOW DOES URBANISATION

INFLUENCE YOUR BUSINESS?

What does this mean for the Lubricants Market…

10

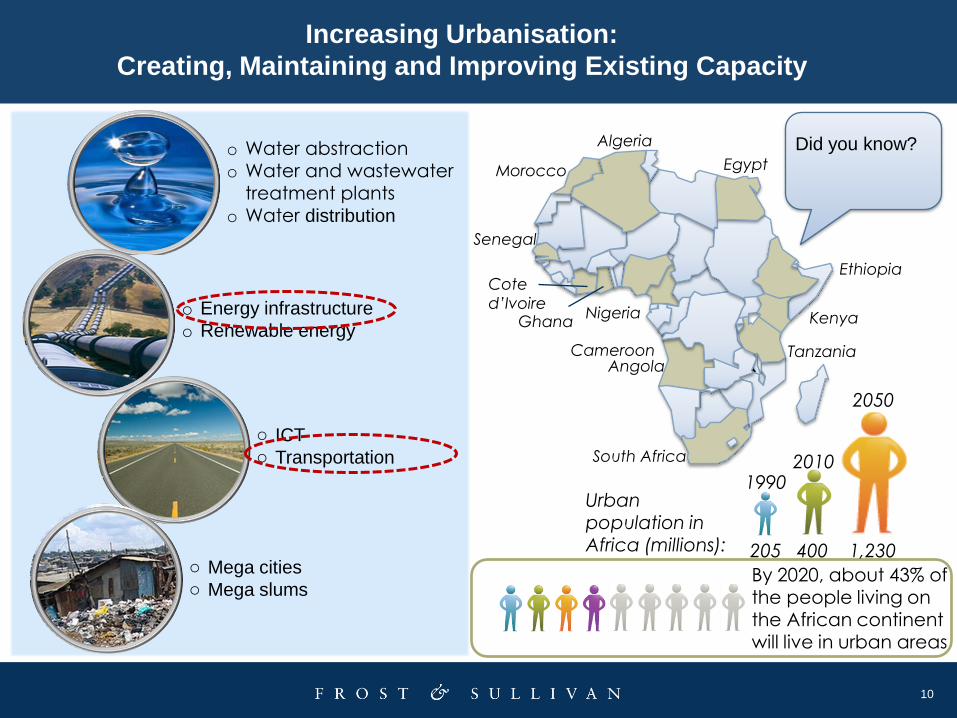

Increasing Urbanisation:

Creating, Maintaining and Improving Existing Capacity

o Water abstractiono Water and wastewater

treatment plantso Water distribution

o Energy infrastructure

o Renewable energy

o ICT o Transportation

o Mega citieso Mega slums

By 2020, about 43% of the people living on

the African continent will live in urban areas

Urban population in Africa (millions): 205

19902010

400

2050

1,230

`

South Africa

AngolaTanzania

Kenya

Ethiopia

Egypt

Algeria

Morocco

Cameroon

Nigeria

Cote

d’IvoireGhana

Senegal

Did you know?

11

HOW DOES INFRASTRUCTURE

INFLUENCE YOUR BUSINESS?

What does this mean for the Lubricants Market…

12

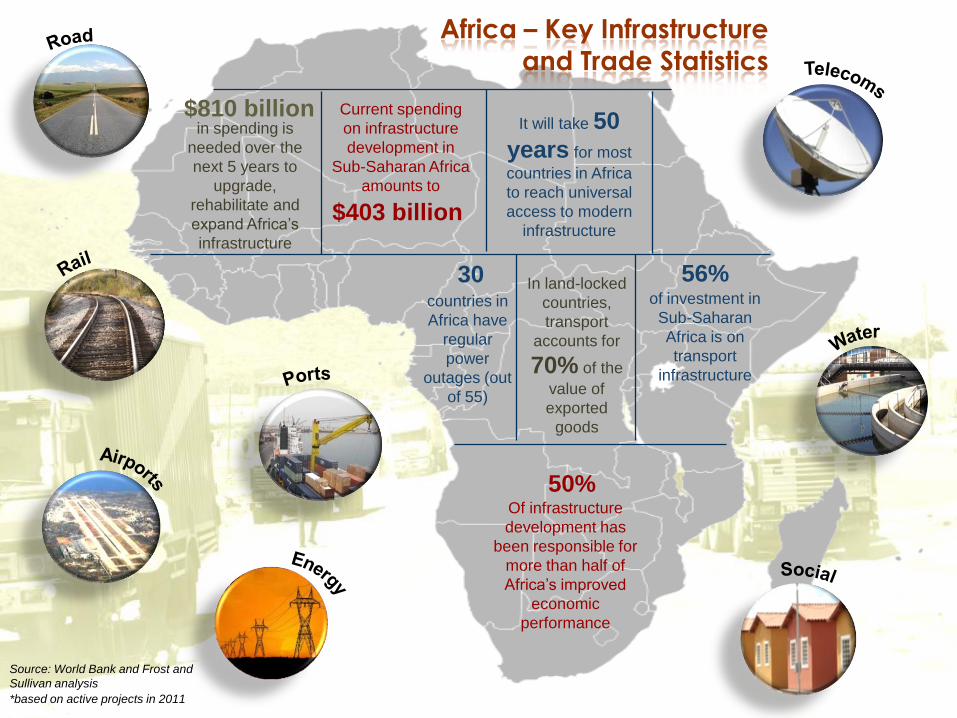

Africa – Key Infrastructure and Trade Statistics

$403 billion

Current spending

on infrastructure

development in

Sub-Saharan Africa

amounts to

of investment in

Sub-Saharan

Africa is on

transport

infrastructure

56%In land-locked

countries,

transport

accounts for

70% of the

value of

exported

goods

countries in

Africa have

regular

power

outages (out

of 55)

30

It will take 50

years for most

countries in Africa

to reach universal

access to modern

infrastructure

50%Of infrastructure

development has

been responsible for

more than half of

Africa’s improved

economic

performance

*based on active projects in 2011

Source: World Bank and Frost and

Sullivan analysis

$810 billionin spending is

needed over the

next 5 years to

upgrade,

rehabilitate and

expand Africa’s

infrastructure

13

A brief Snap Shot into Key African Markets for Automotive and Industrial

Lubricants

AFRICA:

5.3% Growth (2012)

5.6% Growth (2013)f

14

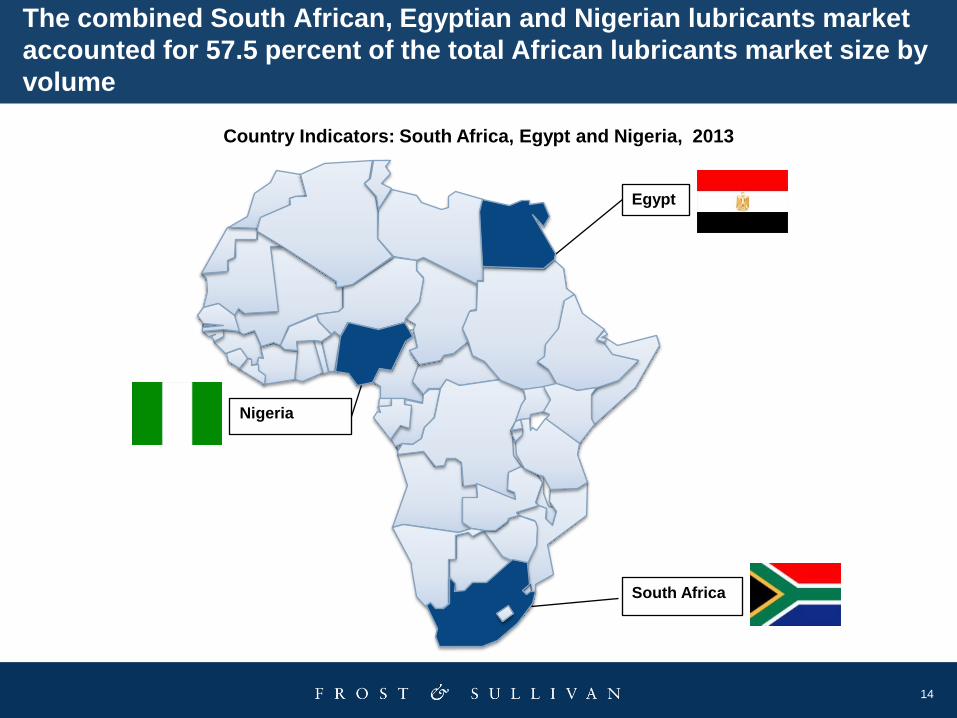

Country Indicators: South Africa, Egypt and Nigeria, 2013

Egypt

Nigeria

`

The combined South African, Egyptian and Nigerian lubricants market

accounted for 57.5 percent of the total African lubricants market size by

volume

South Africa

15

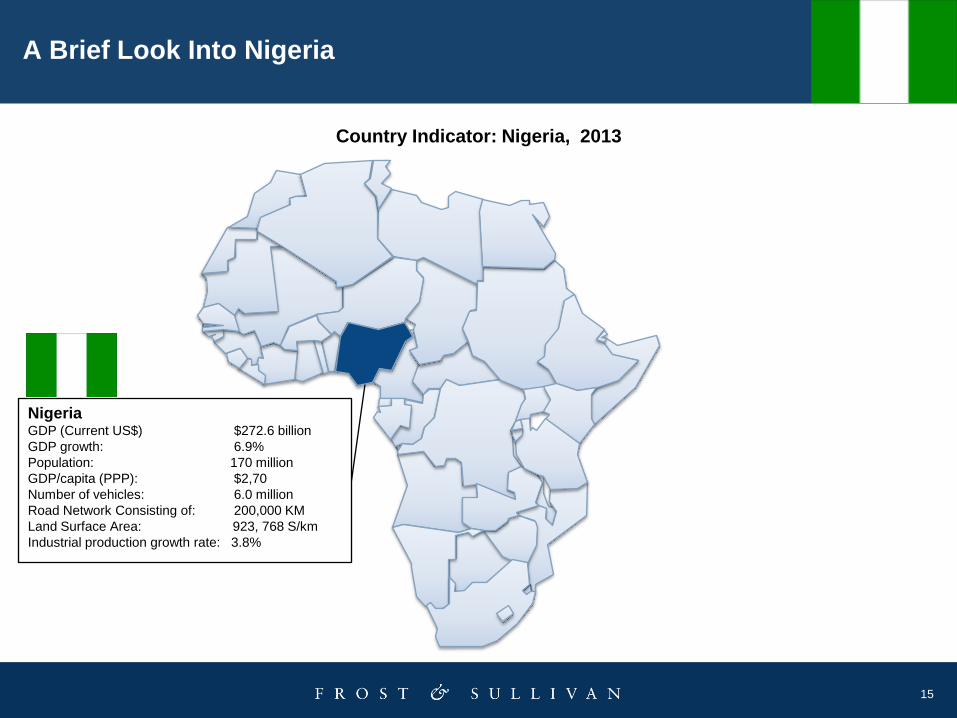

Country Indicator: Nigeria, 2013

NigeriaGDP (Current US$) $272.6 billion

GDP growth: 6.9%

Population: 170 million

GDP/capita (PPP): $2,70

Number of vehicles: 6.0 million

Road Network Consisting of: 200,000 KM

Land Surface Area: 923, 768 S/km

Industrial production growth rate: 3.8%

`

A Brief Look Into Nigeria

16

Note: All figures are rounded.

Source: Frost & Sullivan

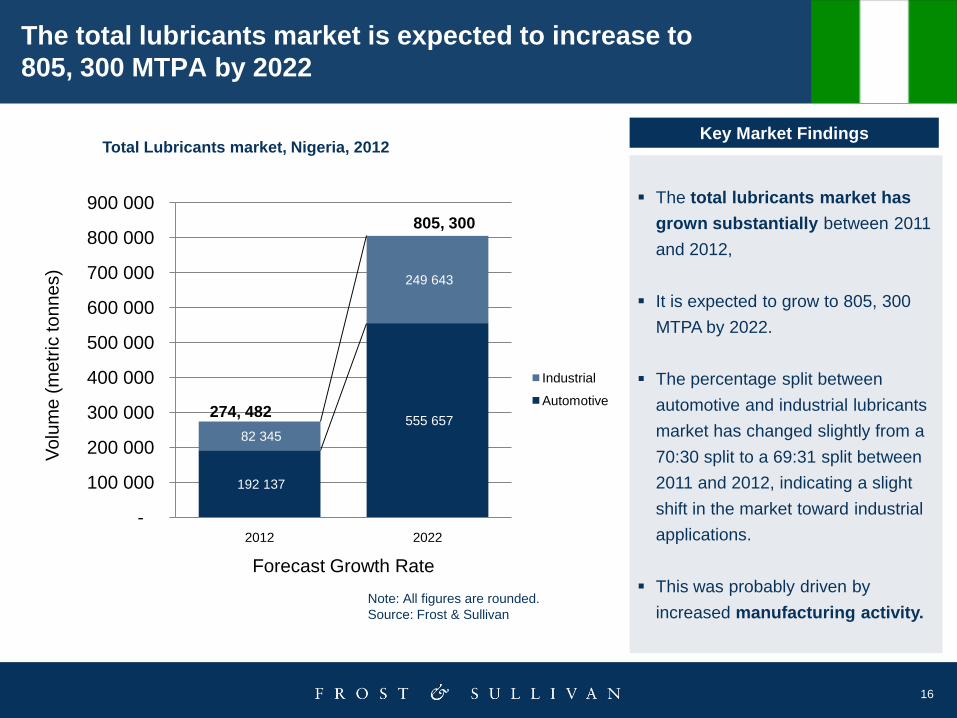

Total Lubricants market, Nigeria, 2012Key Market Findings

The total lubricants market has

grown substantially between 2011

and 2012,

It is expected to grow to 805, 300

MTPA by 2022.

The percentage split between

automotive and industrial lubricants

market has changed slightly from a

70:30 split to a 69:31 split between

2011 and 2012, indicating a slight

shift in the market toward industrial

applications.

This was probably driven by

increased manufacturing activity.

The total lubricants market is expected to increase to

805, 300 MTPA by 2022

192 137

555 657

82 345

249 643

-

100 000

200 000

300 000

400 000

500 000

600 000

700 000

800 000

900 000

2012 2022

Vo

lum

e (

me

tric

to

nn

es)

Forecast Growth Rate

Industrial

Automotive274, 482

805, 300

17

Note: All figures are

rounded Base year is 2012

Source: Frost & Sullivan

Key Market Findings

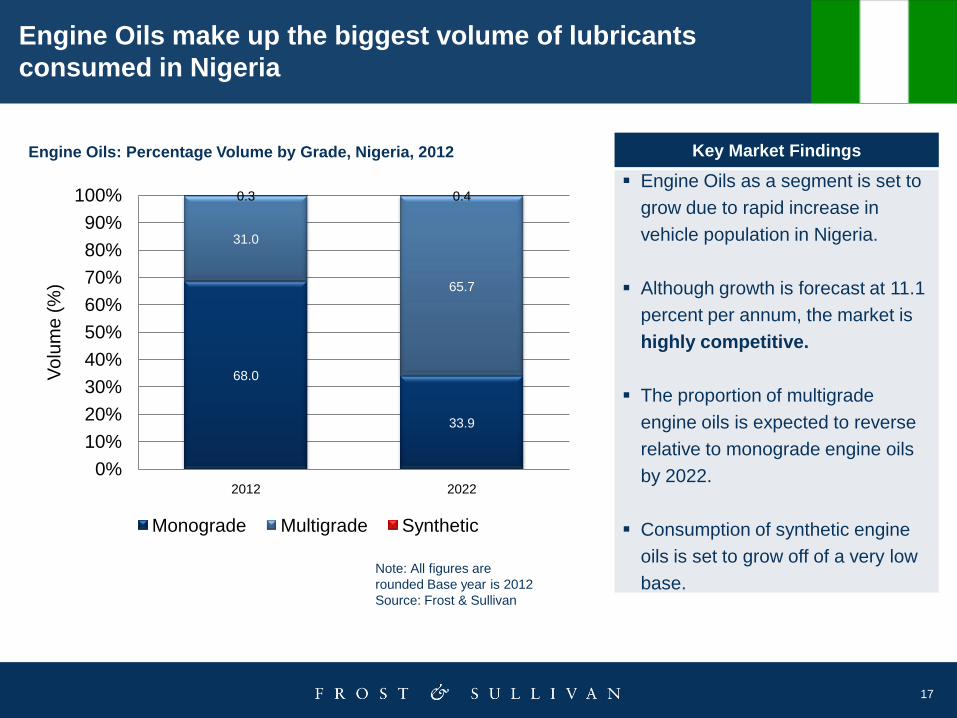

Engine Oils as a segment is set to

grow due to rapid increase in

vehicle population in Nigeria.

Although growth is forecast at 11.1

percent per annum, the market is

highly competitive.

The proportion of multigrade

engine oils is expected to reverse

relative to monograde engine oils

by 2022.

Consumption of synthetic engine

oils is set to grow off of a very low

base.

Engine Oils make up the biggest volume of lubricants

consumed in Nigeria

Engine Oils: Percentage Volume by Grade, Nigeria, 2012

68.0

33.9

31.0

65.7

0.3 0.4

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2022

Vo

lum

e (

%)

Monograde Multigrade Synthetic

18

Total Nigeria Plc hold the leading market share in terms

of the total market for lubricants in Nigeria

• Six tier one suppliers hold about just over 70

percent of the total lubricants market in

Nigeria.

• TOTAL Nigeria Plc is Nigeria’s lubricant

market leader in terms of the total market

share, followed by the leading indigenous

company, Conoil Plc.

• TOTAL was the only Tier 1 supplier that grew

its market share since 2011, as well as its

revenue from lubricants.

• The remaining Tier 1 suppliers lost market

share, predominantly to an increase in the

number of independent suppliers.

Analysis of the competitor market

19

Country Indicator: South Africa, 2013

` South AfricaGDP (Current US$): $384.3 billion

GDP growth: 3-4%

Population: 51.2 million

Road Network Consisting of: 750,000 KM

Land Surface Area: 1,219,090 S/km

A Brief Look Into Nigeria

20

Note: All figures are rounded.

Source: Frost & Sullivan

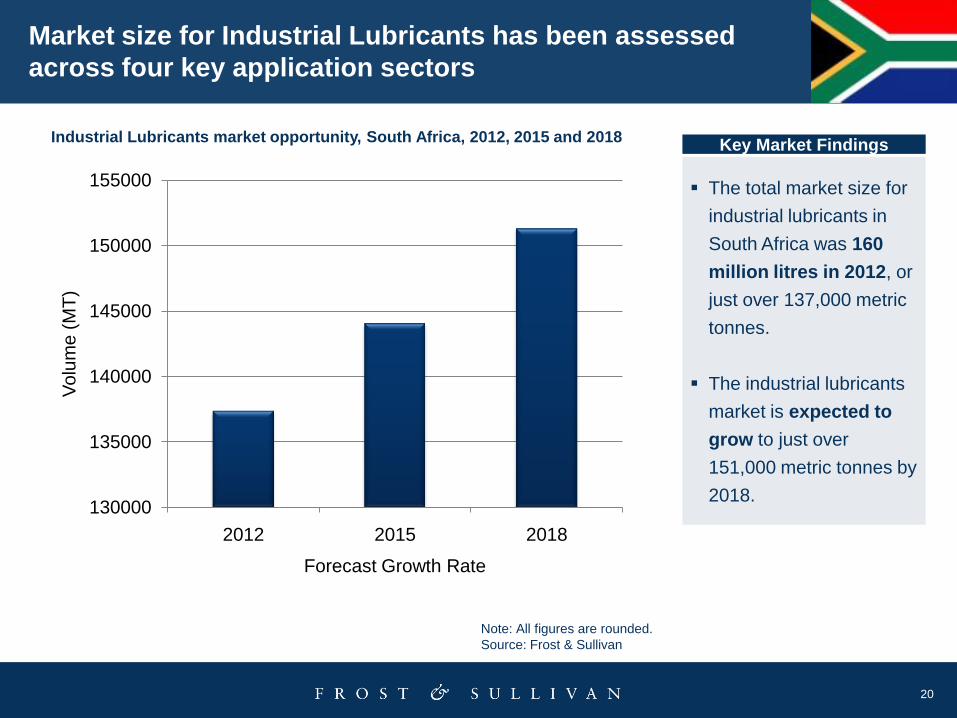

Industrial Lubricants market opportunity, South Africa, 2012, 2015 and 2018Key Market Findings

The total market size for

industrial lubricants in

South Africa was 160

million litres in 2012, or

just over 137,000 metric

tonnes.

The industrial lubricants

market is expected to

grow to just over

151,000 metric tonnes by

2018.

Market size for Industrial Lubricants has been assessed

across four key application sectors

130000

135000

140000

145000

150000

155000

2012 2015 2018

Vo

lum

e (

MT

)

Forecast Growth Rate

21

Note: All figures are rounded

Base year is 2012

Source: Frost & Sullivan

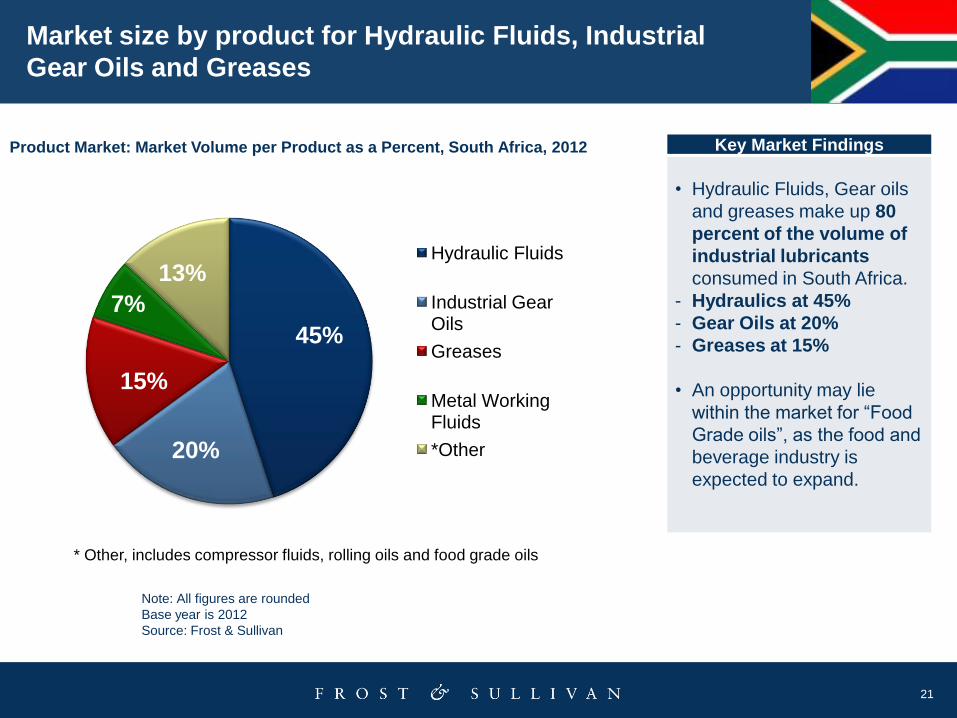

Key Market Findings

• Hydraulic Fluids, Gear oils

and greases make up 80

percent of the volume of

industrial lubricants

consumed in South Africa.

- Hydraulics at 45%

- Gear Oils at 20%

- Greases at 15%

• An opportunity may lie

within the market for “Food

Grade oils”, as the food and

beverage industry is

expected to expand.

Market size by product for Hydraulic Fluids, Industrial

Gear Oils and Greases

Product Market: Market Volume per Product as a Percent, South Africa, 2012

45%

20%

15%

7%

13%Hydraulic Fluids

Industrial Gear Oils

Greases

Metal Working Fluids

*Other

* Other, includes compressor fluids, rolling oils and food grade oils

22

Five of the major oil companies make up 80-90 percent of the

industrial lubricants market

• The major oil companies make up 80 - 90

percent of the industrial lubricants market.

• Shell and Chevron have the largest shares

of industrial lubricants.

• Engen, Castrol BP and TOTAL hold the

3rd, 4th and 5th position, respectively, in

terms of market share for industrial

lubricants in South Africa.

• The remainder of the market is split between

Fuchs, SASOL and a multitude of

independent blenders manufacturing a

wide range of products.

Analysis of the competitor market

23

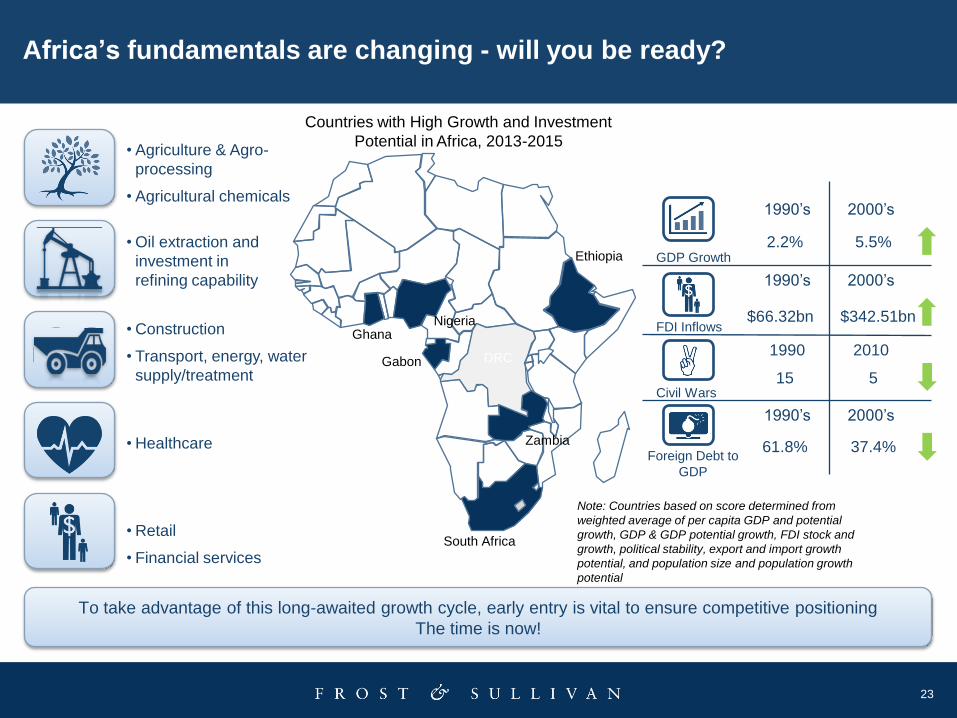

Africa’s fundamentals are changing - will you be ready?

To take advantage of this long-awaited growth cycle, early entry is vital to ensure competitive positioning

The time is now!

GDP Growth

1990’s 2000’s

FDI Inflows

Civil Wars

2.2% 5.5%

1990 2010

1990’s 2000’s

15 5

$66.32bn $342.51bn

Foreign Debt to

GDP

1990’s 2000’s

61.8% 37.4%

• Agriculture & Agro-

processing

• Agricultural chemicals

• Oil extraction and

investment in

refining capability

• Construction

• Transport, energy, water

supply/treatment

• Healthcare

Nigeria

Zambia

Ethiopia

DRC

Ghana

Note: Countries based on score determined from

weighted average of per capita GDP and potential

growth, GDP & GDP potential growth, FDI stock and

growth, political stability, export and import growth

potential, and population size and population growth

potential

Countries with High Growth and Investment

Potential in Africa, 2013-2015

• Retail

• Financial servicesSouth Africa

Gabon

24

How do I grow successfully in the Lubricants Market in Africa?

Risk / Challenge Identification

Identify Key Opportunities - fast emerging countries in SSA

Identify Market Opportunities - Product & customer Segments

Distribution / Supply Chain / Partners

Customer Preferences

Devise Growth Strategy

25

Frost & Sullivan’s Lubricants Multi Client Project in Sub-Saharan Africa

1. The emerging markets for lubricants.

2. Key end-user sectors (both within automotive and industrial lubricants).

3. Strategic insights into product technologies and customer trends, “voice

of customers”.

4. Identifying growth opportunities for lubricant suppliers.

Mani James Operations Director

Chemicals, Materials & Food

(0027) (0)21 680 3208

Kholofelo DzvukamanjaProgramme Manager

Chemicals, Materials & Food

(0027) (0)21 680 3261

The project will ultimately aim to provide an overall strategic market

analysis identifying emerging markets for lubricants in sub-Saharan

Africa, and their respective customer/product requirements

26

Thank You