africa telecoms outlook 2014: maximizing digital service opportunities

TRANSCRIPT

This document is offered compliments of BSP Media Group. www.bspmediagroup.com

All rights reserved.

Africa Telecoms Outlook 2014:

Maximizing digital service opportunities

Nick Jotischky

Principal Analyst

November 12, 2013

The view from the industry: reasons to be cheerful – consumer appetite is driving growth of smartphone market and digital opportunities

A view of the industry: % of respondents who strongly agree with these statements

Source: Informa Telecoms & Media Africa Industry Survey, 2013 N: 347 respondents

www.informatandm.com

© Informa UK Limited 2013. All rights reserved

32%

25%

42%

19%

37%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

The Africantelecomsmarket ismaturing

I expect thereto be

consolidationamong Africanoperators over

the comingyears

I feel confidentabout the

prospects forthe Africantelecoms

industry overthe next few

years

The provision oftelecoms

services to ruralor remotemarkets inAfrica has

improved overthe past few

years

The provision oftelecoms

services to ruralmarkets in

Africa remainsinadequate

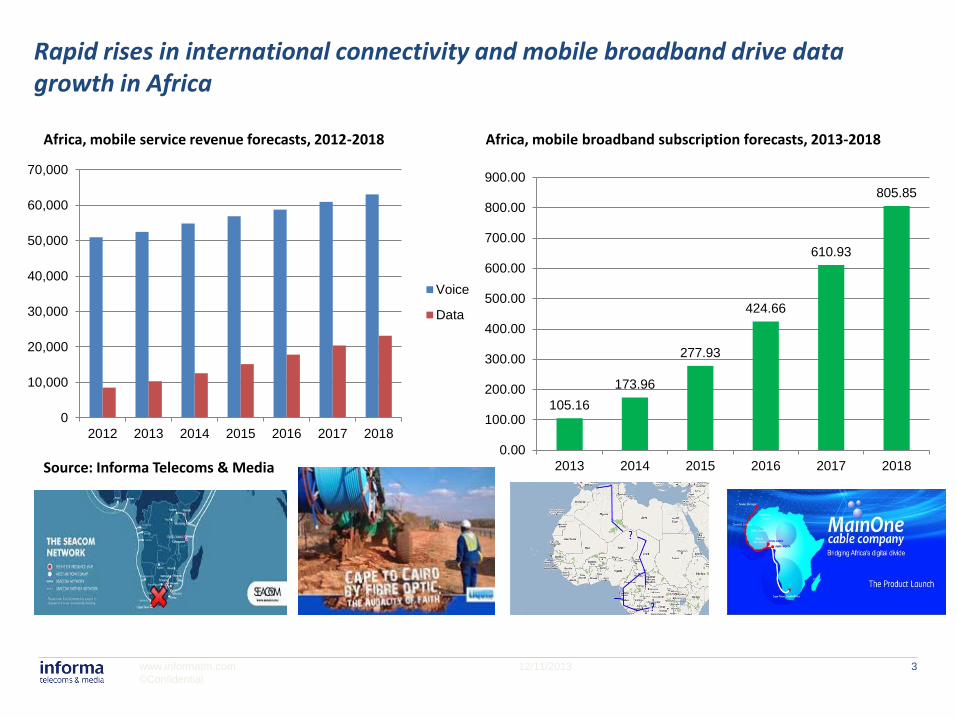

Rapid rises in international connectivity and mobile broadband drive data growth in Africa

12/11/2013 www.informatm.com

©Confidential

3

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2012 2013 2014 2015 2016 2017 2018

Voice

Data

105.16

173.96

277.93

424.66

610.93

805.85

0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00

800.00

900.00

2013 2014 2015 2016 2017 2018

Africa, mobile service revenue forecasts, 2012-2018 Africa, mobile broadband subscription forecasts, 2013-2018

Source: Informa Telecoms & Media

Low-cost smartphones have become a key enabler of mobile data access in Africa

12/11/2013 www.informatm.com

©Confidential

4

Africa, smartphone connection forecasts, 2012-2018

Source: Informa Telecoms & Media

0.00

200.00

400.00

600.00

800.00

1,000.00

1,200.00

1,400.00

2012 2013 2014 2015 2016 2017 2018

Smartphoneconnections

Mobile connections

0%

50%

100%

150%

200%

250%

US$100

US$150

US$250

Proportion of device costs to monthly income, selected markets

Source: Affordable Handsets Report, Informa Telecoms & Media

Increased data take-up powers demand for digital services in Africa

12/11/2013 www.informatm.com

©Confidential

5

Media Events per week

Mobile phone Tablet

Video streaming Hours 0.75 2.5

Video downloads Downloads 3 3

Music streaming Hours 0.75 2

Music downloads Downloads 3 4

App downloads Downloads 3 2.5

Games online Hours 1.5 2.5

Games downloads Downloads 2 2.5

Location-based services Hours 0.75 2.5

Browsing Hours 2.5 2.5

VoIP Hours 1.5 2.5

E-commerce Transactions 3 3

Instant messaging Messages 30 75

Social networking Hours 2.5 2.5

Email Messages 25 75

E-publications Downloads 2 2

Nigeria, mobile service usage, consumer survey 2013

Note: Figures are for median average, based on a survey of 619 smartphone users in Nigeria.

Media Events per week

Mobile phone Tablet

Video streaming Hours 0.75 1.5

Video downloads Downloads 2 3

Music streaming Hours 0.75 0.75

Music downloads Downloads 3 2

App downloads Downloads 2 2

Games online Hours 1.5 2.5

Games downloads Downloads 2 2

Location-based services Hours 0.25 0.25

Browsing Hours 1.5 2.5

VoIP Hours 0.75 1.5

E-commerce Transactions 3 3

Instant messaging Messages 150 30

Social networking Hours 2.5 1.5

Email Messages 25 75

E-publications Downloads 1 2

South Africa, mobile service usage, consumer survey 2013

Note: Figures are for median average, based on a survey of 511 smartphone users in South Africa.

The consumer wants greater access to data services - but is the telecoms industry doing all it can to satisfy this demand?

12/11/2013 www.informatm.com

©Confidential

6

44% 47%

11%

19%

36%

42%

34%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Datadevicesare too

expensive

The retailprices of

dataservicesare too

high

There is alack of

demandfrom

consumersfor dataservices

Operatorsare not

providingthe righttypes of

dataservices

Backhaulcapacity oravailability

isinsufficient

or tooexpensive

Theprovision

of servicesto rural or

remoteareas is

inadequate

Regulatoryaction orinaction

The most important barriers to the access to and take-up of data services in Africa

39.1%

27.7%

16.2%

9.2%

7.8% Significantlyincrease

Slightly increase

Remain the same

Slightly decrease

Significantlydecrease

Mobile phone planned expenditure over next 12 months, Nigeria

Note: Figures are based on a survey of 619 smartphone users in Nigeria

Source: Informa Africa Industry Survey, 2013

Consumers have insatiable appetite for data services and high expectations for the quality of the service • How does technology need to evolve to meet these expectations?

• Is the industry able to satisfy consumer demand and are operators set up to be service-centric rather than network-

centric?

• Do operators truly understand the behavior patterns of their customers?