affordable care act update: has the dust settled yet?

TRANSCRIPT

Affordable Care Act Update: Has the Dust Settled Yet? MARCH 8

A CBIZ Benefits & Insurance Services Program

Today’s Speakers

2

KAREN R. MCLEESE, ESQ. VICE PRESIDENT - REGULATORY AFFAIRS

CBIZ BENEFITS & INSURANCE SERVICES, INC.

WILLIAM M. SMITH, ESQ. MANAGING DIRECTOR, NATIONAL TAX OFFICE

CBIZ MHM, LLC

ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

Today’s Agenda

3

Quick Review of New Laws and Regulatory Guidance

Focus on ACA Reporting – Forms 1094/1095

ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

QUICK REVIEW OF NEW LAWS AND REGULATORY GUIDANCE

4 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

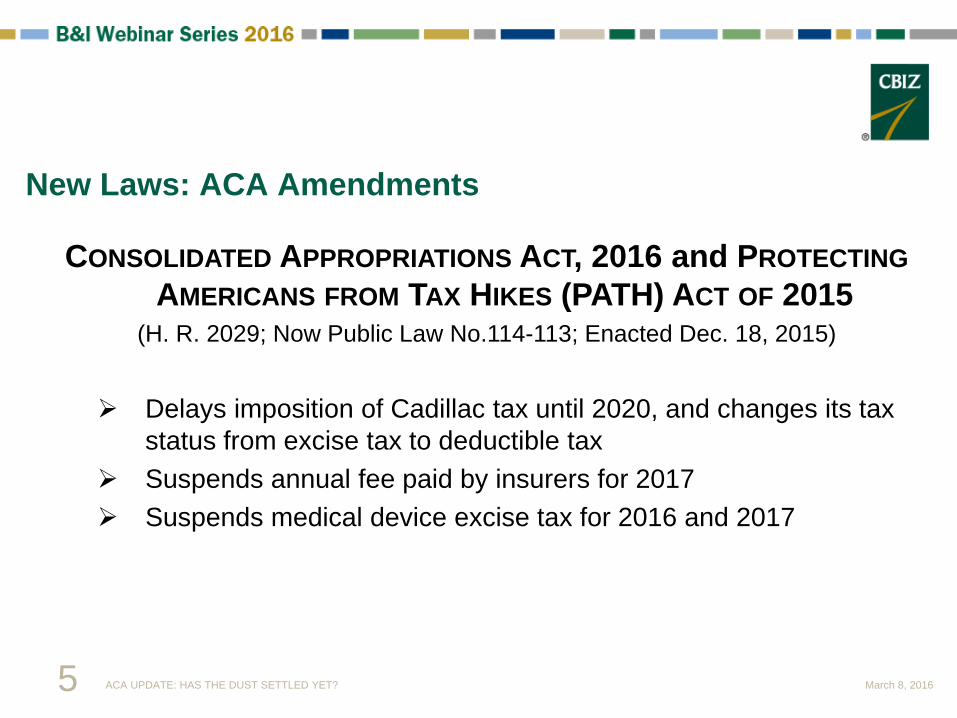

CONSOLIDATED APPROPRIATIONS ACT, 2016 and PROTECTING AMERICANS FROM TAX HIKES (PATH) ACT OF 2015

(H. R. 2029; Now Public Law No.114-113; Enacted Dec. 18, 2015) Delays imposition of Cadillac tax until 2020, and changes its tax

status from excise tax to deductible tax Suspends annual fee paid by insurers for 2017 Suspends medical device excise tax for 2016 and 2017

New Laws: ACA Amendments

5 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

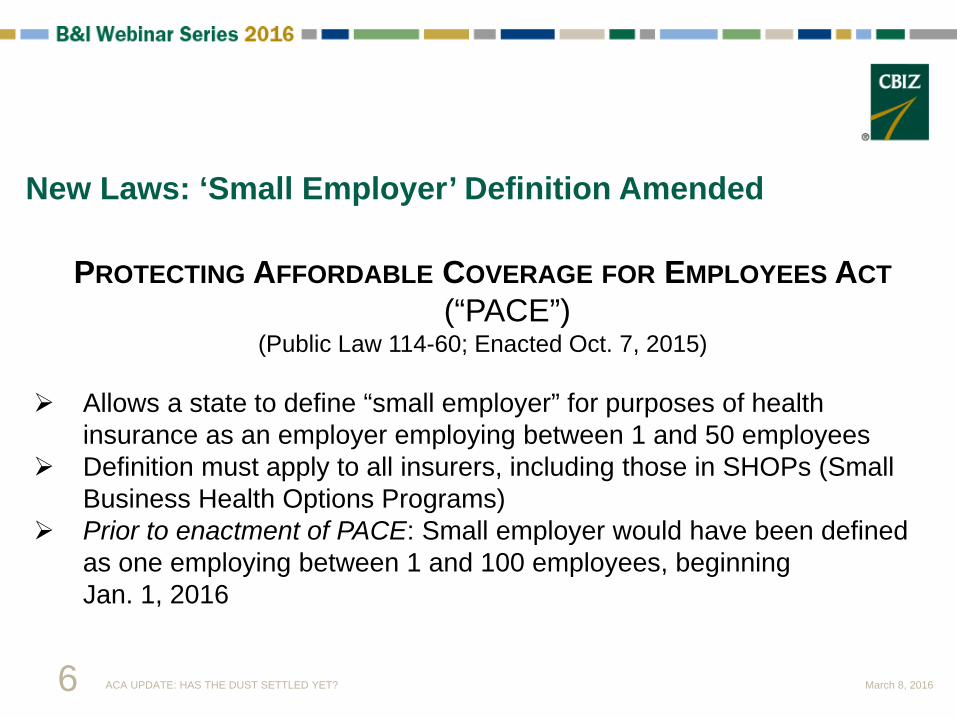

PROTECTING AFFORDABLE COVERAGE FOR EMPLOYEES ACT (“PACE”)

(Public Law 114-60; Enacted Oct. 7, 2015)

Allows a state to define “small employer” for purposes of health insurance as an employer employing between 1 and 50 employees

Definition must apply to all insurers, including those in SHOPs (Small Business Health Options Programs)

Prior to enactment of PACE: Small employer would have been defined as one employing between 1 and 100 employees, beginning Jan. 1, 2016

New Laws: ‘Small Employer’ Definition Amended

6 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

BIPARTISAN BUDGET ACT OF 2015 (Public Law 114-74; Enacted Nov. 2, 2015)

Repeals the ACA’s Automatic Enrollment Provision

This provision would have required employers with 200-plus employees to automatically enroll new full-time equivalents into qualifying health plan offered by

employer and automatically continue enrollment of current employees

New Laws: Automatic Enrollment Provision Repealed

7 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

Employee Affordability (the 9.5% safe harbor rule) for purposes of employer’s risk of excise tax is addressed Percentage amount now tied to inflation: 9.56% in 2015;

9.66% in 2016 Newly available health reimbursement arrangement (HRA)

funds Opt-out for other health or nonhealth benefits Cash-out option

In determining employee’s cost of coverage, as long as employment relationship exists: Third-party paid time (short- or long-term disability, etc.) is

counted in determining hours worked. State workers compensation or state temporary disability

amounts are not counted

Regulatory Updates – IRS Notice 2015-87

8 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

Individual Premium and Health Reimbursement Arrangements (HRAs) IRS guidance affirms prior guidance that employers cannot directly

or indirectly contribute to individual premium HRAs for active employees must be integrated with comprehensive

health coverage. If HRA covers dependents, they must be eligible for properly integrated health coverage.

An HRA covering retiree-only individuals need not be integrated with comprehensive plan

HRA funds can be used to pay excepted benefits (dental-only or vision-only plan) without violating the prohibition against premium payment plans

Regulatory Updates – IRS Notice 2015-87

9 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

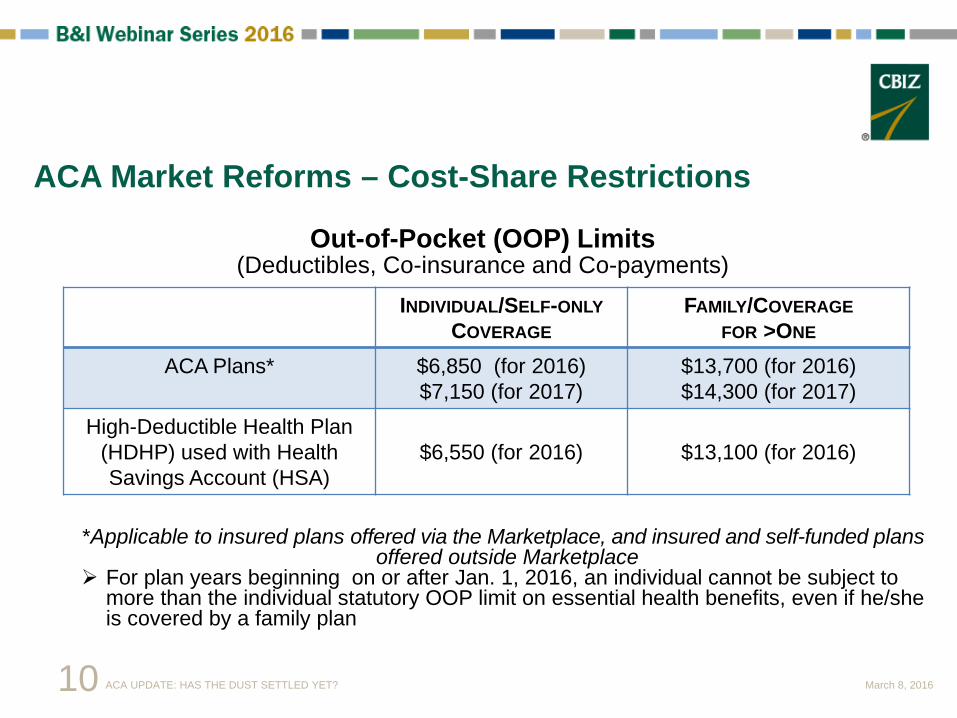

Out-of-Pocket (OOP) Limits (Deductibles, Co-insurance and Co-payments)

*Applicable to insured plans offered via the Marketplace, and insured and self-funded plans offered outside Marketplace

For plan years beginning on or after Jan. 1, 2016, an individual cannot be subject to more than the individual statutory OOP limit on essential health benefits, even if he/she is covered by a family plan

ACA Market Reforms – Cost-Share Restrictions

INDIVIDUAL/SELF-ONLY COVERAGE

FAMILY/COVERAGE FOR >ONE

ACA Plans* $6,850 (for 2016) $7,150 (for 2017)

$13,700 (for 2016) $14,300 (for 2017)

High-Deductible Health Plan (HDHP) used with Health Savings Account (HSA)

$6,550 (for 2016)

$13,100 (for 2016)

10 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

REVIEW OF ACA REPORTING

11 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

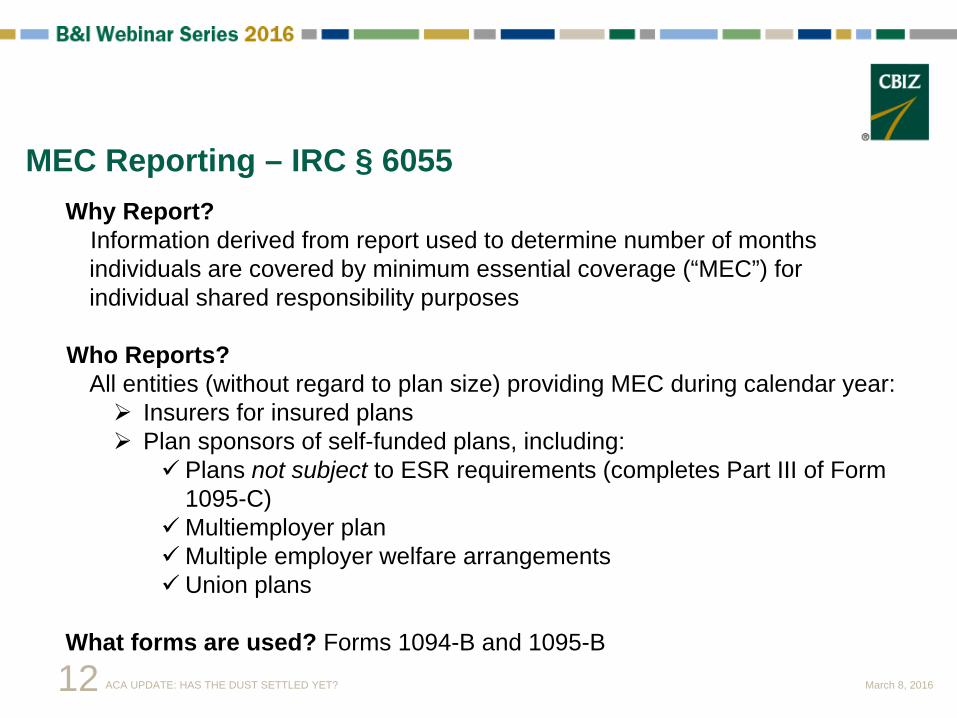

MEC Reporting – IRC § 6055 Why Report?

Information derived from report used to determine number of months individuals are covered by minimum essential coverage (“MEC”) for individual shared responsibility purposes

Who Reports?

All entities (without regard to plan size) providing MEC during calendar year: Insurers for insured plans Plan sponsors of self-funded plans, including:

Plans not subject to ESR requirements (completes Part III of Form 1095-C)

Multiemployer plan Multiple employer welfare arrangements Union plans

What forms are used? Forms 1094-B and 1095-B

12 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

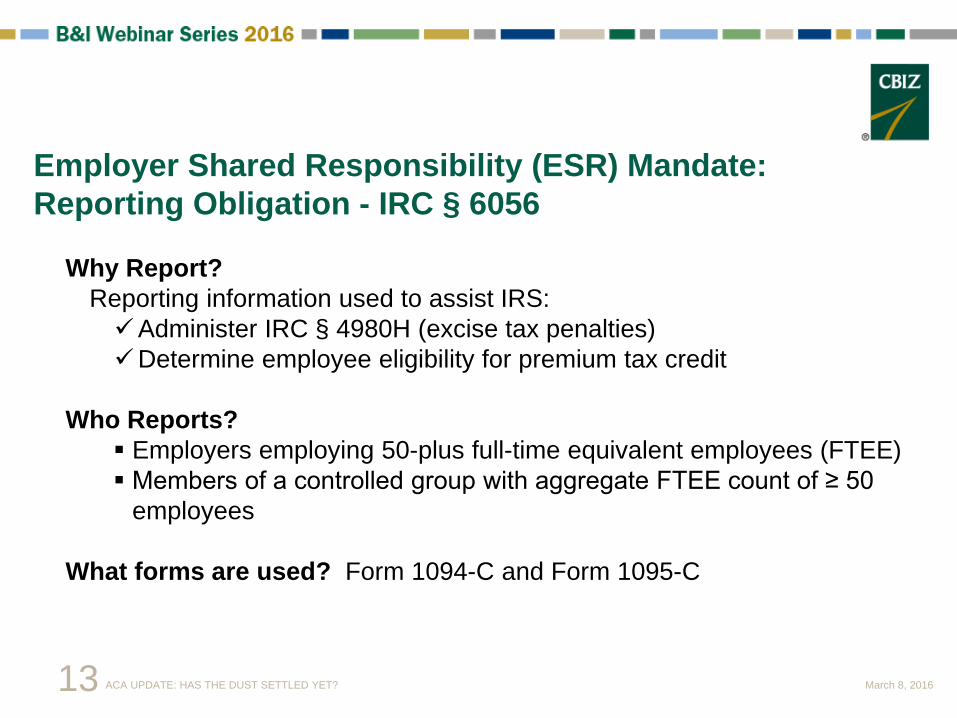

Why Report? Reporting information used to assist IRS: Administer IRC § 4980H (excise tax penalties) Determine employee eligibility for premium tax credit

Who Reports? Employers employing 50-plus full-time equivalent employees (FTEE) Members of a controlled group with aggregate FTEE count of ≥ 50

employees What forms are used? Form 1094-C and Form 1095-C

Employer Shared Responsibility (ESR) Mandate: Reporting Obligation - IRC § 6056

13 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

Determining ALE status: Average number of employees and their hours of service in preceding year determines ALE status for the current year

Employee defined as “common-law employee” Does not include leased employees, sole proprietor, partner in

partnership, 2% S-Corp shareholders, or real estate agents and direct sellers (“IRC Section 3508 employees”)

Full-time employee (FTE): One who works average of 30 hrs/week (130 hrs/calendar month = 30 hrs/week)

Employer Shared Responsibility Mandate: Reporting Obligation - IRC § 6056

14 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

Who Is Considered an Employee: Myth No. 1

There is a difference between an “independent contractor” and a “consultant”

Only two choices: – Employee or independent

contractor (“IC”) based on application of particular test at issue

– Labels do not matter – A valid business-to-business

relationship does not involve individuals and so is not at issue when making that determination A business itself, however, does

not resolve issue

15 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

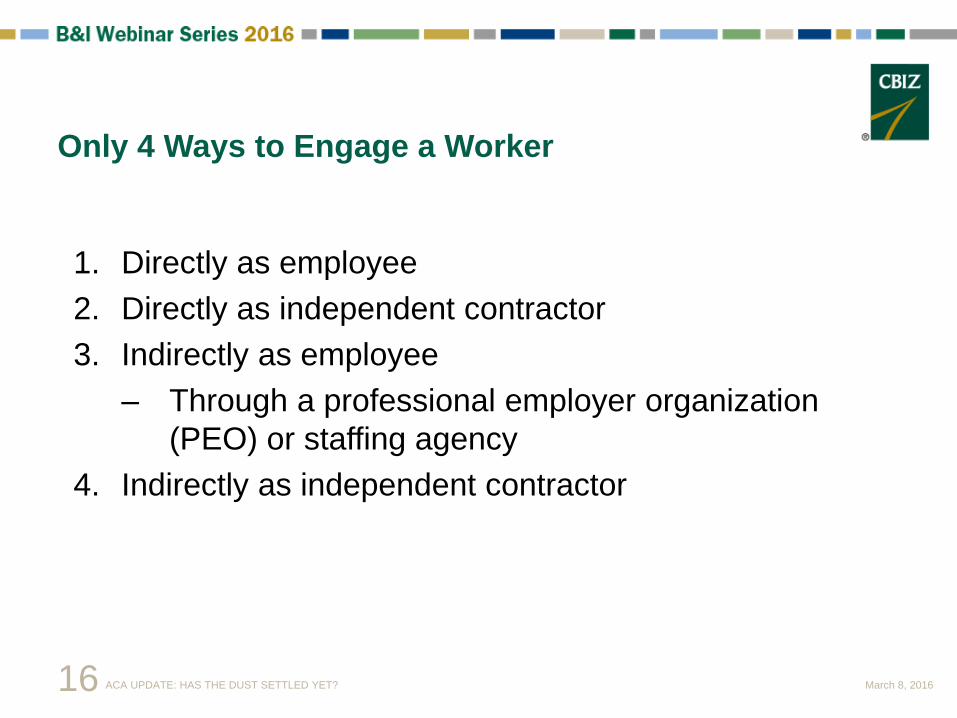

Only 4 Ways to Engage a Worker

1. Directly as employee 2. Directly as independent contractor 3. Indirectly as employee

– Through a professional employer organization (PEO) or staffing agency

4. Indirectly as independent contractor

16 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

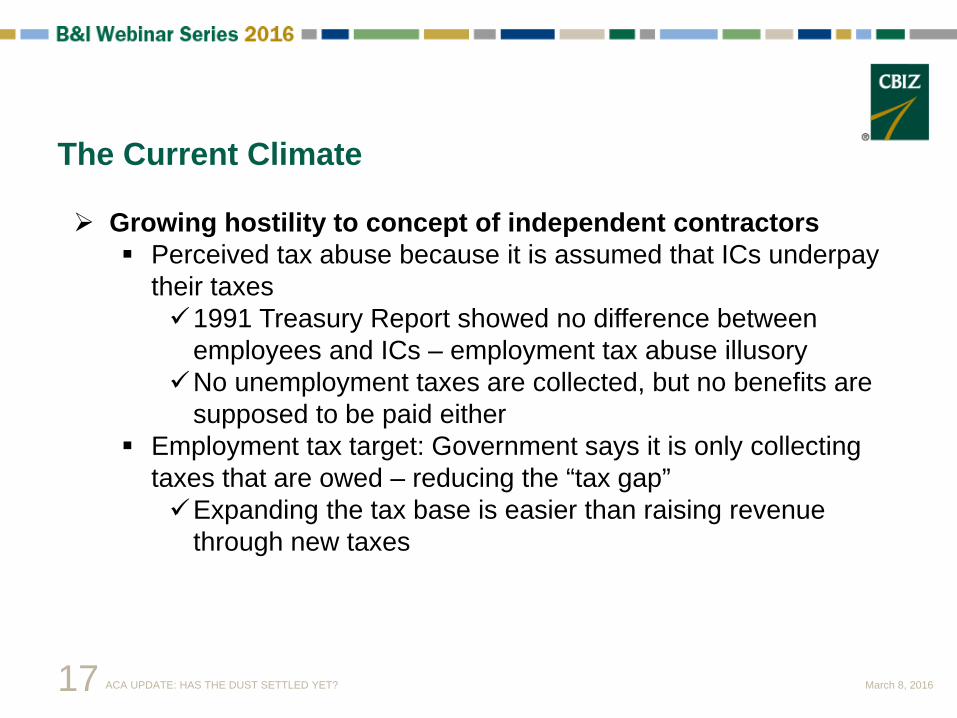

The Current Climate

Growing hostility to concept of independent contractors Perceived tax abuse because it is assumed that ICs underpay

their taxes 1991 Treasury Report showed no difference between

employees and ICs – employment tax abuse illusory No unemployment taxes are collected, but no benefits are

supposed to be paid either Employment tax target: Government says it is only collecting

taxes that are owed – reducing the “tax gap” Expanding the tax base is easier than raising revenue

through new taxes

17 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

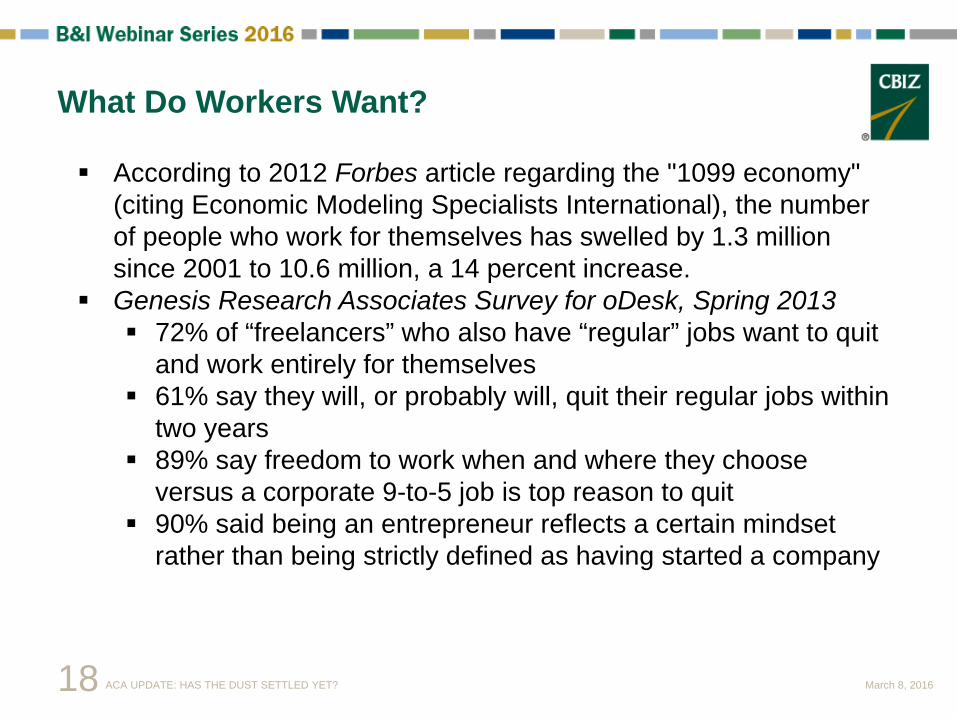

What Do Workers Want?

According to 2012 Forbes article regarding the "1099 economy" (citing Economic Modeling Specialists International), the number of people who work for themselves has swelled by 1.3 million since 2001 to 10.6 million, a 14 percent increase.

Genesis Research Associates Survey for oDesk, Spring 2013 72% of “freelancers” who also have “regular” jobs want to quit

and work entirely for themselves 61% say they will, or probably will, quit their regular jobs within

two years 89% say freedom to work when and where they choose

versus a corporate 9-to-5 job is top reason to quit 90% said being an entrepreneur reflects a certain mindset

rather than being strictly defined as having started a company

18 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

Which workers are most likely to see status questioned?

Highly skilled, highly paid workers Examples: computer programmers, doctors

Low-skilled, low-paid workers Little control often needed given the nature of the work, but is

there real entrepreneurism?

Small businesses or startups Lack the knowledge to properly apply the rules or just trying to

survive

19 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

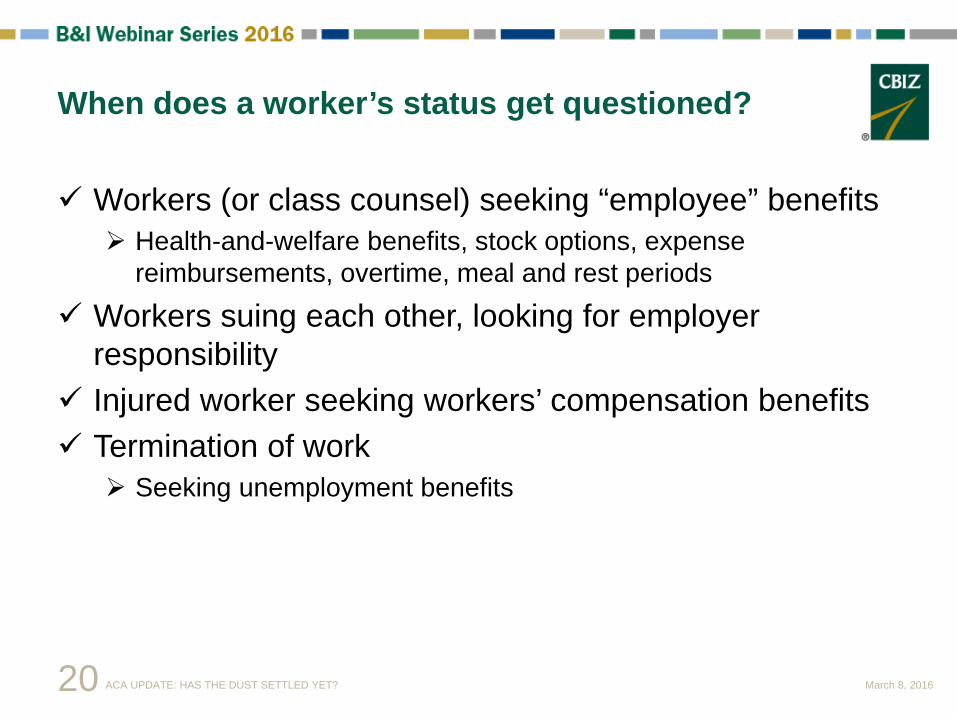

When does a worker’s status get questioned?

Workers (or class counsel) seeking “employee” benefits Health-and-welfare benefits, stock options, expense

reimbursements, overtime, meal and rest periods

Workers suing each other, looking for employer responsibility

Injured worker seeking workers’ compensation benefits Termination of work

Seeking unemployment benefits

20 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

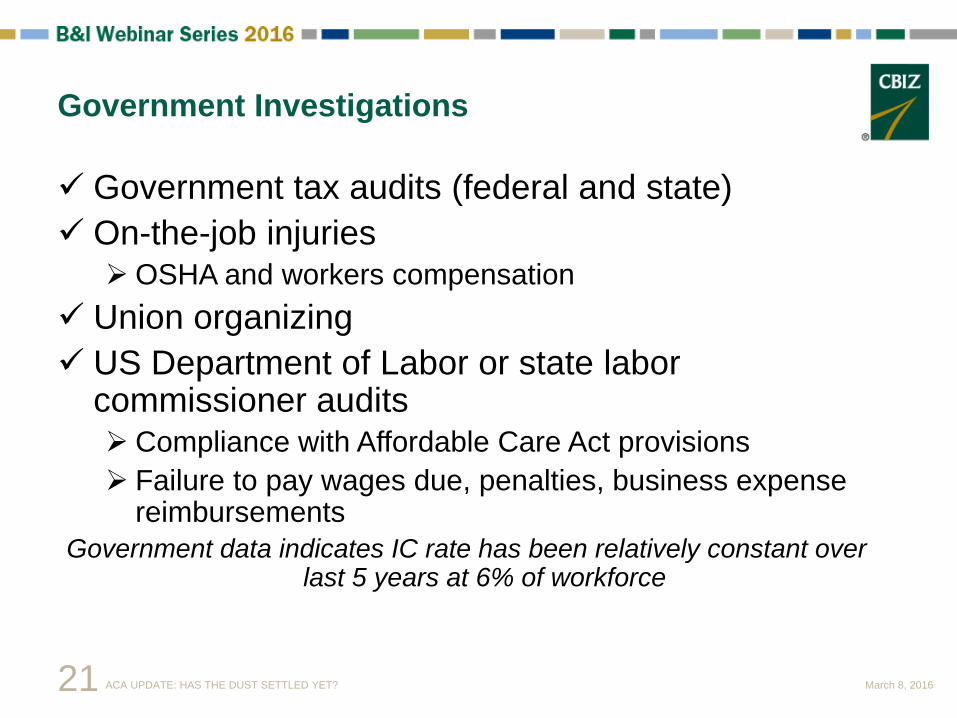

Government Investigations

Government tax audits (federal and state) On-the-job injuries OSHA and workers compensation

Union organizing US Department of Labor or state labor

commissioner audits Compliance with Affordable Care Act provisions Failure to pay wages due, penalties, business expense

reimbursements Government data indicates IC rate has been relatively constant over

last 5 years at 6% of workforce

21 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

Who Is an Independent Contractor for Tax Purposes?

Common-Law Rules

Does the principal have the right to control the manner and means by which services are performed in addition to the result to be achieved? Behavioral control

Does the company control or have the right to control what the worker does and how the worker does his or her job?

Financial control Are the business aspects of the worker’s job controlled by the payer?

Relationship of the parties Are there written contracts or employee-type benefits?

22 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

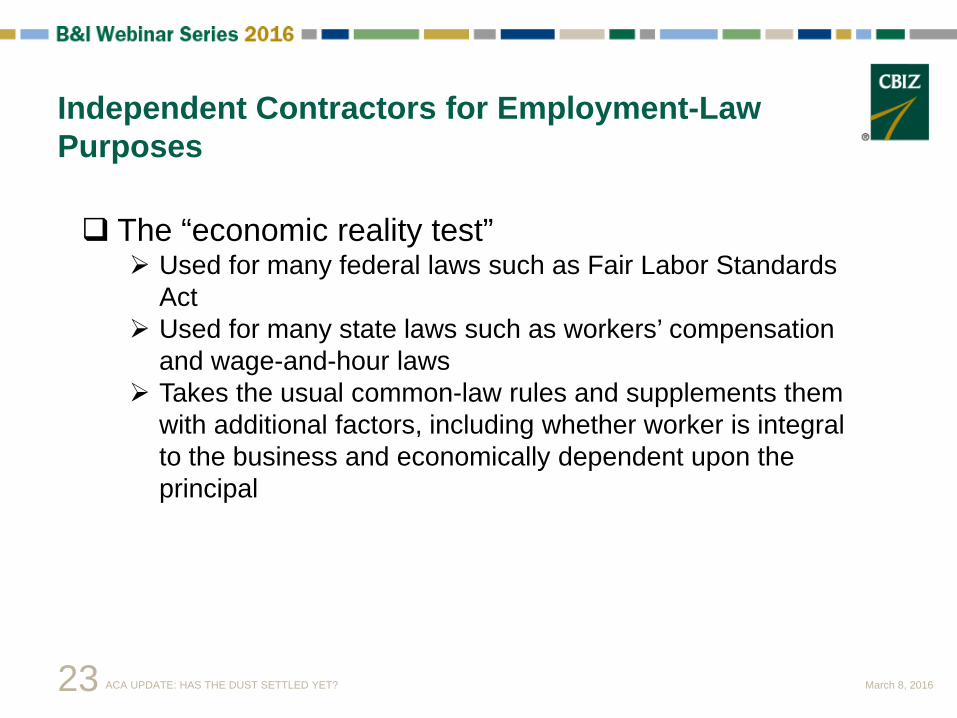

Independent Contractors for Employment-Law Purposes

The “economic reality test” Used for many federal laws such as Fair Labor Standards

Act Used for many state laws such as workers’ compensation

and wage-and-hour laws Takes the usual common-law rules and supplements them

with additional factors, including whether worker is integral to the business and economically dependent upon the principal

23 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

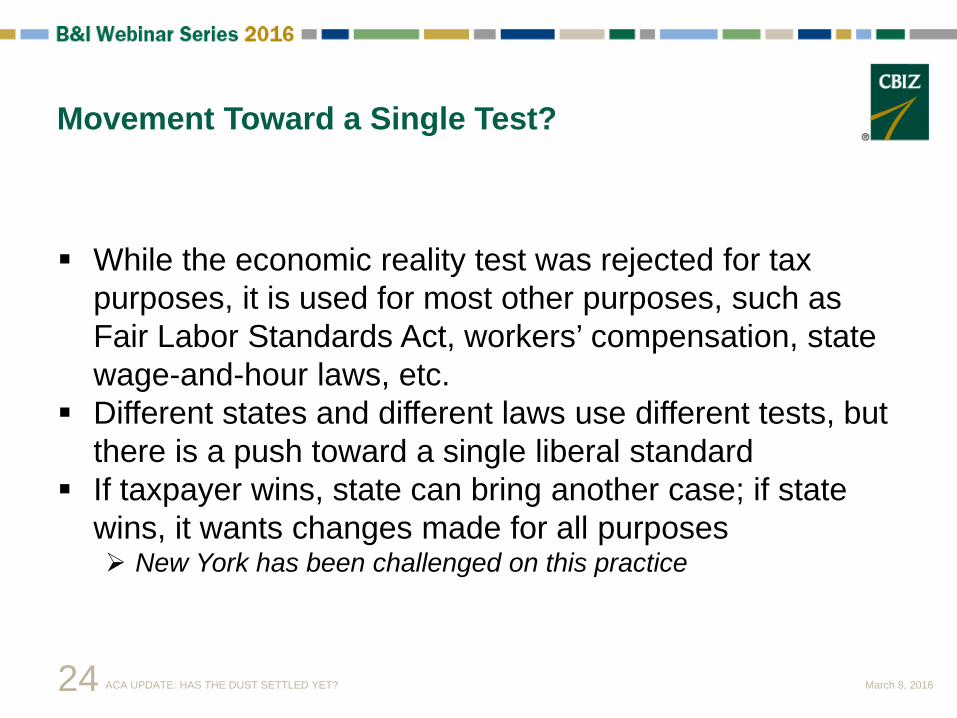

Movement Toward a Single Test?

While the economic reality test was rejected for tax purposes, it is used for most other purposes, such as Fair Labor Standards Act, workers’ compensation, state wage-and-hour laws, etc.

Different states and different laws use different tests, but there is a push toward a single liberal standard

If taxpayer wins, state can bring another case; if state wins, it wants changes made for all purposes New York has been challenged on this practice

24 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

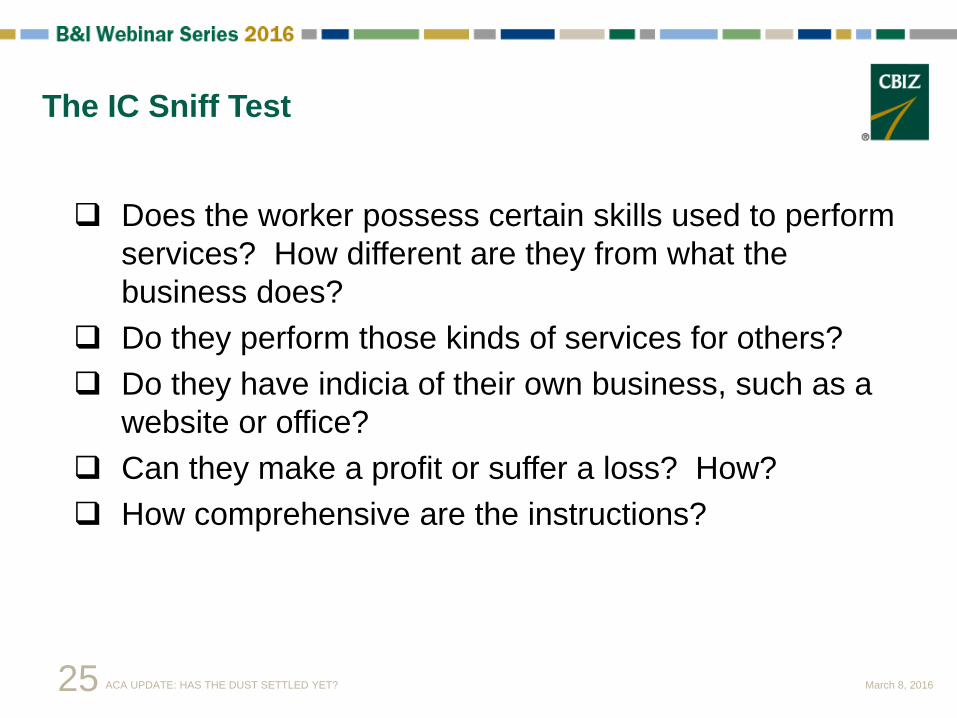

The IC Sniff Test

Does the worker possess certain skills used to perform services? How different are they from what the business does?

Do they perform those kinds of services for others? Do they have indicia of their own business, such as a

website or office? Can they make a profit or suffer a loss? How? How comprehensive are the instructions?

25 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

The Risks of Getting It Wrong

Tax issues Wage-and-hour issues Workers’ compensation issues Immigration issues Benefit issues Other employment-law issues

26 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

IRS Voluntary Classification Settlement Program (VCSP)

Who is it for? Available for taxpayers who want to voluntarily change the

prospective classification of their workers. The program applies to taxpayers who are currently treating their workers (or a class or group of workers) as independent contractors or other nonemployees and want to prospectively treat the workers as employees.

Eligibility Must be treating the workers to be reclassified as independent

contractors or other nonemployees Must have consistently treated the workers as nonemployees,

including having filed any required Forms 1099, consistent with the nonemployee treatment, for the previous three years with respect to the workers to be reclassified

Cannot be currently under employment tax audit by the IRS Cannot be under audit by the Department of Labor or any state

agency regarding the classification of workers

27 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

IRS Voluntary Classification Settlement Program (VCSP)

Benefits 1. Pay 10% of employment tax liability that would have been

due on compensation paid to the workers for the most recent tax year, determined under the reduced rates of IRC § 3509(a);

2. Avoid liability for any interest and penalties on the amount; and

3. Avoid being subjected to an employment tax audit with respect to the worker classification of the workers being reclassified under the VCSP for prior years.

28 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

ACA and Worker Status

Will ACA cause an increase in use of ICs? Many large businesses have medical insurance

Reduction in hours will not spur switch to ICs Businesses at or near 50 FTEs motivated to use ICs According to a June 2013 Gallup Poll, small business will

stop hiring or reduce head count to avoid triggering ACA penalties 41% of small businesses have frozen hiring 19% have reduced head count because of ACA 38% have scaled back growth plans

According to a March 2015 Brookings Institution study, it is difficult to tell the impact caused by ACA on employment because of the economic downturn

29 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

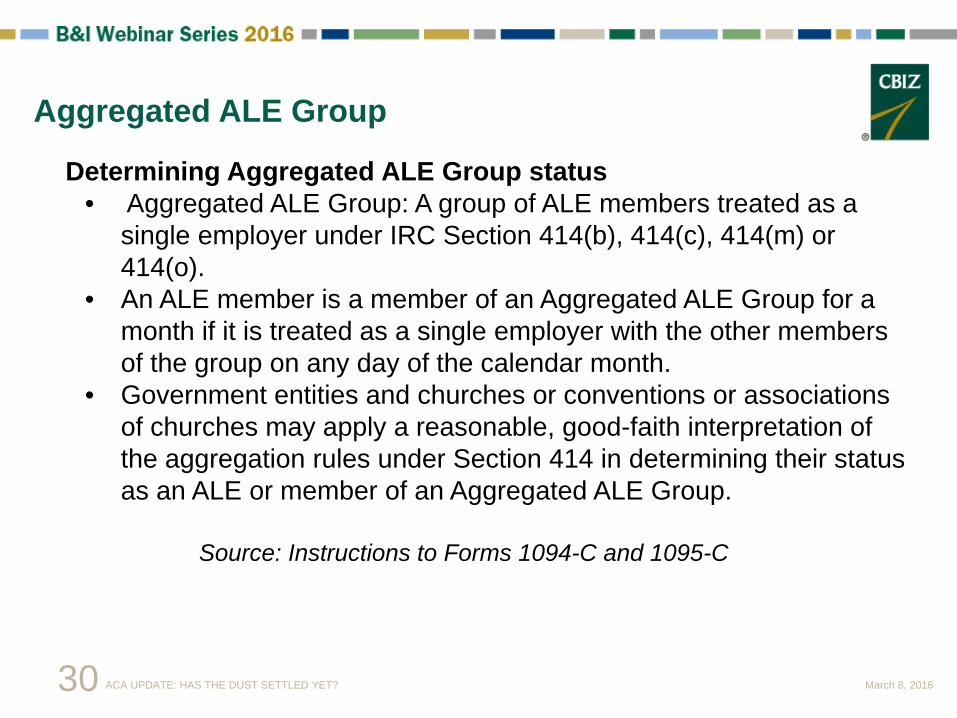

Determining Aggregated ALE Group status • Aggregated ALE Group: A group of ALE members treated as a

single employer under IRC Section 414(b), 414(c), 414(m) or 414(o).

• An ALE member is a member of an Aggregated ALE Group for a month if it is treated as a single employer with the other members of the group on any day of the calendar month.

• Government entities and churches or conventions or associations of churches may apply a reasonable, good-faith interpretation of the aggregation rules under Section 414 in determining their status as an ALE or member of an Aggregated ALE Group.

Source: Instructions to Forms 1094-C and 1095-C

Aggregated ALE Group

30 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

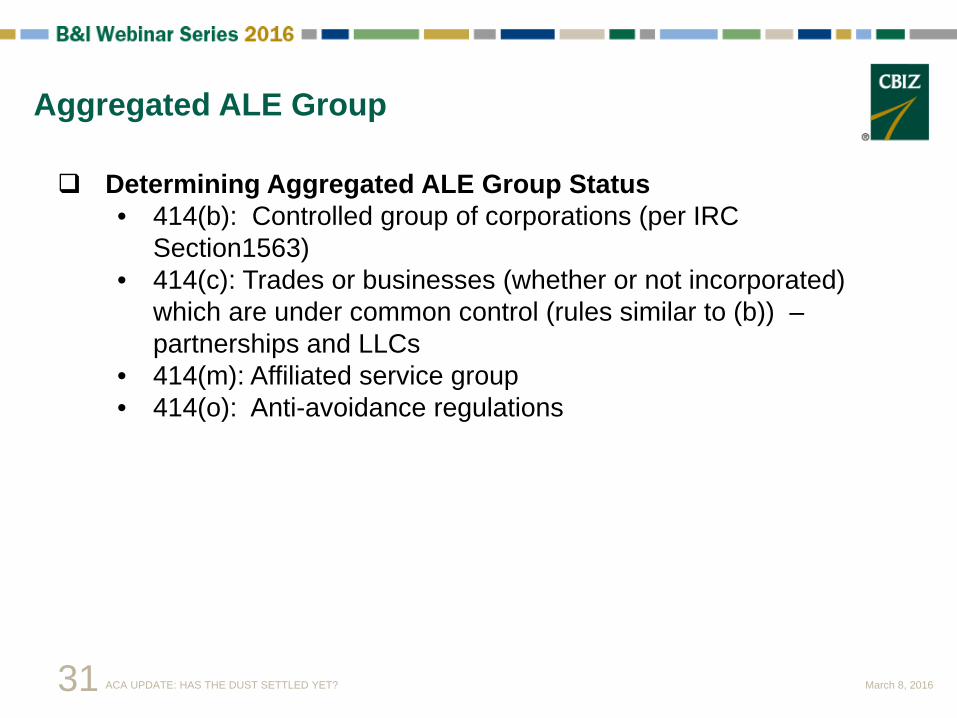

Determining Aggregated ALE Group Status • 414(b): Controlled group of corporations (per IRC

Section1563) • 414(c): Trades or businesses (whether or not incorporated)

which are under common control (rules similar to (b)) – partnerships and LLCs

• 414(m): Affiliated service group • 414(o): Anti-avoidance regulations

Aggregated ALE Group

31 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

Determining Aggregated ALE Group Status Section 1563 – Controlled Group of Corporations: Parent – Subsidiary (80% vote or value) Brother – Sister Controlling interest: At least 80% vote or value by 5 or fewer

individuals Effective control: >50% vote or value, but only to the extent

of identical ownership by the same 5 or fewer individuals Similar rules for partnerships Attribution applies (breaking up is hard to do)

Aggregated ALE Group

32 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

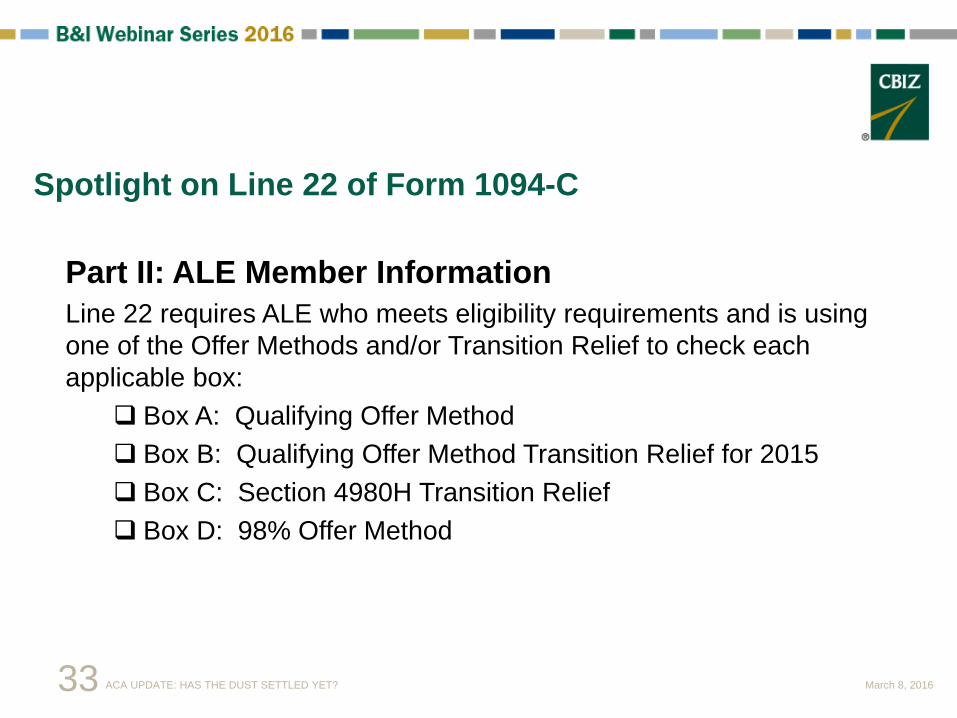

Part II: ALE Member Information Line 22 requires ALE who meets eligibility requirements and is using one of the Offer Methods and/or Transition Relief to check each applicable box:

Box A: Qualifying Offer Method Box B: Qualifying Offer Method Transition Relief for 2015 Box C: Section 4980H Transition Relief Box D: 98% Offer Method

Spotlight on Line 22 of Form 1094-C

33 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

Form 1094-C, Transmittal

Part II: ALE Member Information Enter ALE member info (designated ALE/aggregated ALE member), certifications of eligibility. Box A: Qualifying Offer Method. Box B: Qualifying Offer Method Transition Relief. Box C: Section 4980H Transition Relief. Box D: 98% Offer Method.

34 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

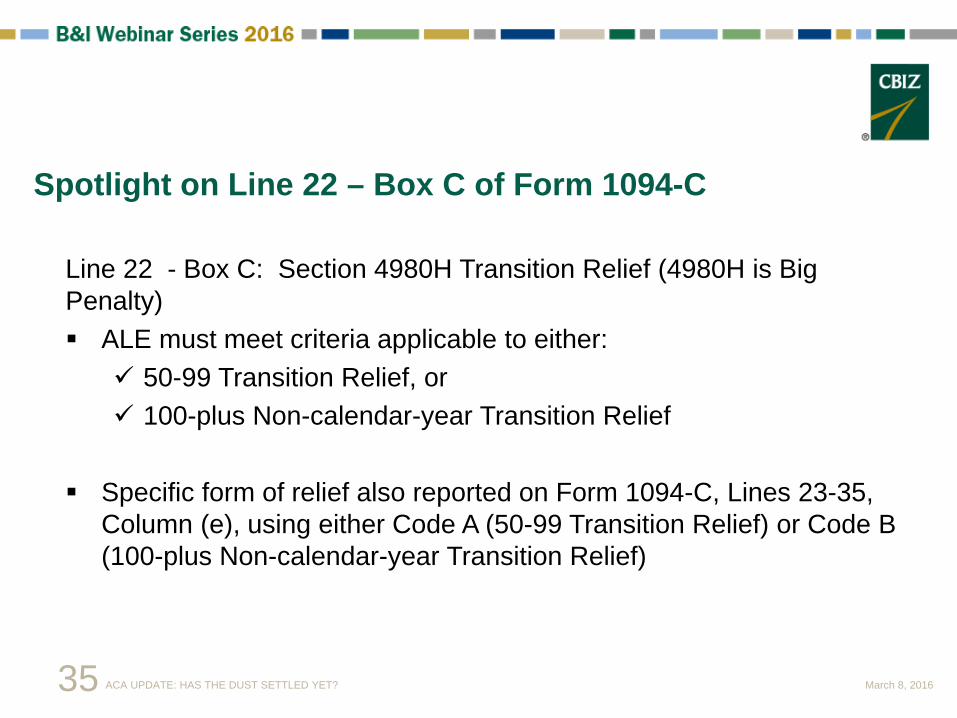

Line 22 - Box C: Section 4980H Transition Relief (4980H is Big Penalty) ALE must meet criteria applicable to either:

50-99 Transition Relief, or 100-plus Non-calendar-year Transition Relief

Specific form of relief also reported on Form 1094-C, Lines 23-35,

Column (e), using either Code A (50-99 Transition Relief) or Code B (100-plus Non-calendar-year Transition Relief)

Spotlight on Line 22 – Box C of Form 1094-C

35 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

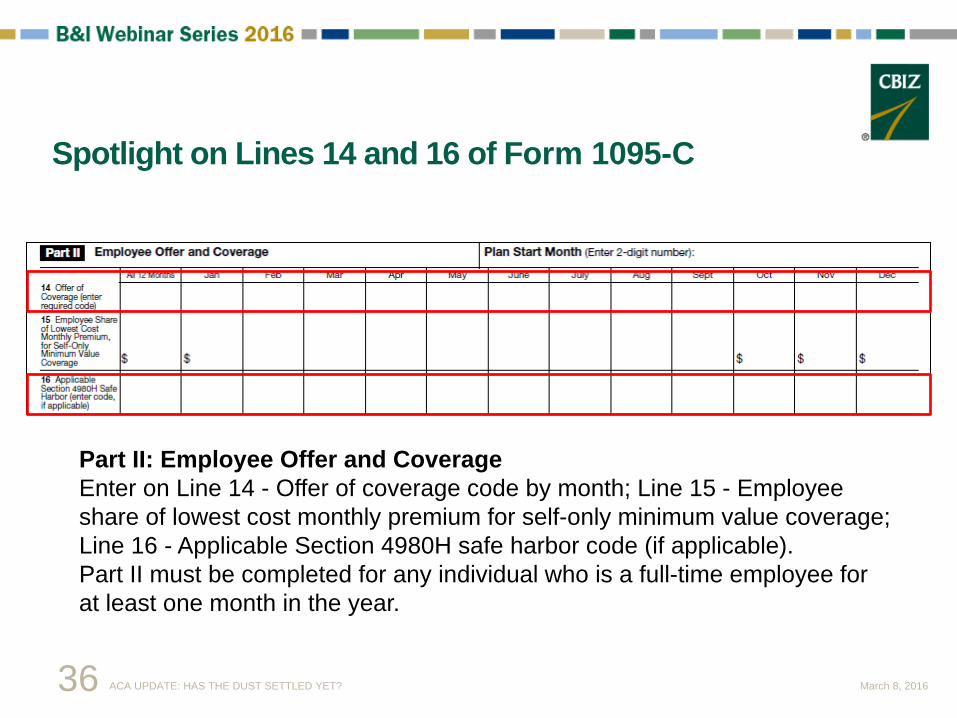

Spotlight on Lines 14 and 16 of Form 1095-C

Part II: Employee Offer and Coverage Enter on Line 14 - Offer of coverage code by month; Line 15 - Employee share of lowest cost monthly premium for self-only minimum value coverage; Line 16 - Applicable Section 4980H safe harbor code (if applicable). Part II must be completed for any individual who is a full-time employee for at least one month in the year.

36 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

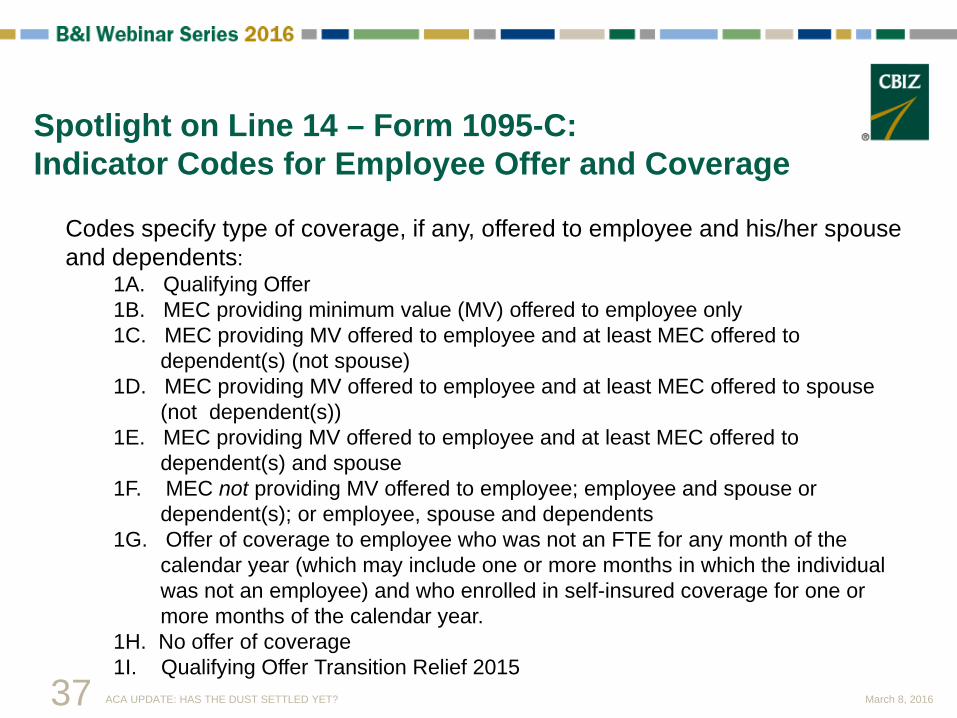

Codes specify type of coverage, if any, offered to employee and his/her spouse and dependents:

1A. Qualifying Offer 1B. MEC providing minimum value (MV) offered to employee only 1C. MEC providing MV offered to employee and at least MEC offered to

dependent(s) (not spouse) 1D. MEC providing MV offered to employee and at least MEC offered to spouse

(not dependent(s)) 1E. MEC providing MV offered to employee and at least MEC offered to

dependent(s) and spouse 1F. MEC not providing MV offered to employee; employee and spouse or

dependent(s); or employee, spouse and dependents 1G. Offer of coverage to employee who was not an FTE for any month of the

calendar year (which may include one or more months in which the individual was not an employee) and who enrolled in self-insured coverage for one or more months of the calendar year.

1H. No offer of coverage 1I. Qualifying Offer Transition Relief 2015

Spotlight on Line 14 – Form 1095-C: Indicator Codes for Employee Offer and Coverage

37 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

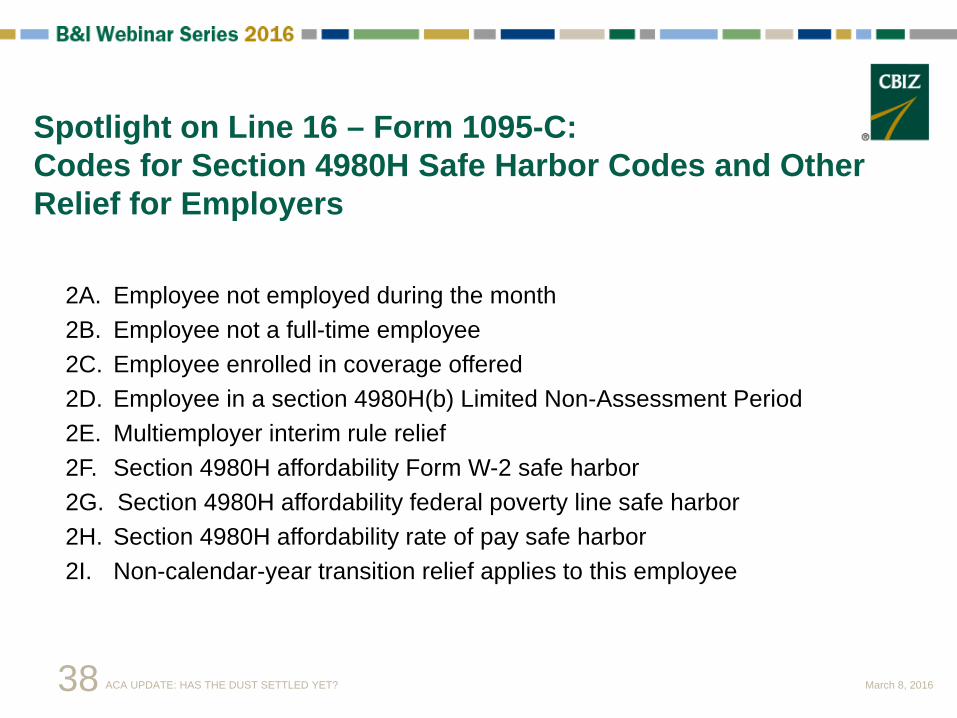

2A. Employee not employed during the month 2B. Employee not a full-time employee 2C. Employee enrolled in coverage offered 2D. Employee in a section 4980H(b) Limited Non-Assessment Period 2E. Multiemployer interim rule relief 2F. Section 4980H affordability Form W-2 safe harbor 2G. Section 4980H affordability federal poverty line safe harbor 2H. Section 4980H affordability rate of pay safe harbor 2I. Non-calendar-year transition relief applies to this employee

Spotlight on Line 16 – Form 1095-C: Codes for Section 4980H Safe Harbor Codes and Other Relief for Employers

38 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

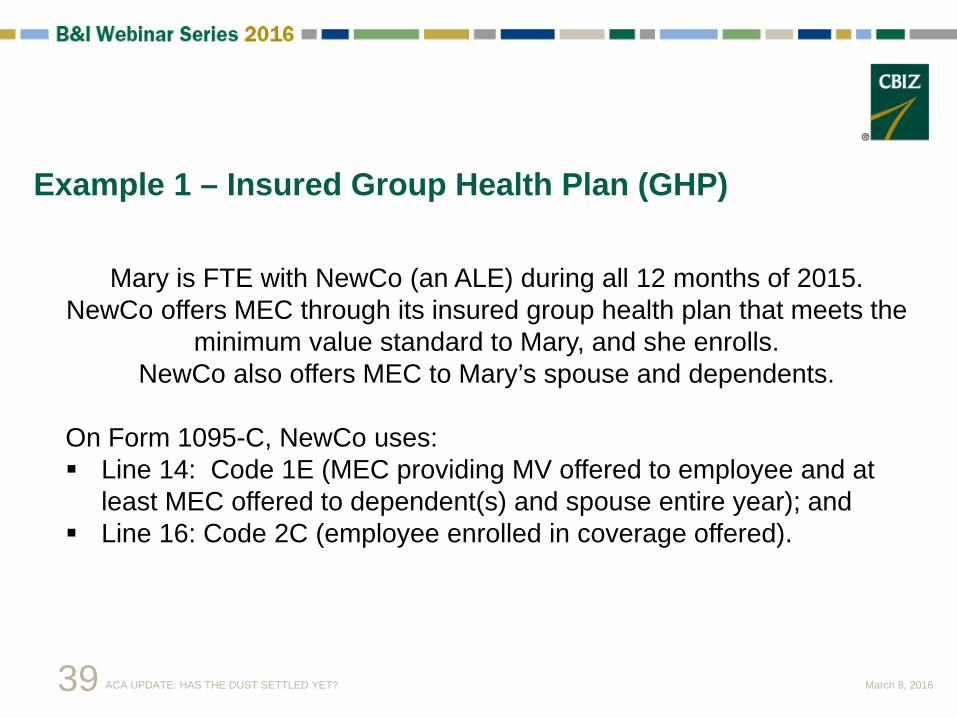

Mary is FTE with NewCo (an ALE) during all 12 months of 2015. NewCo offers MEC through its insured group health plan that meets the

minimum value standard to Mary, and she enrolls. NewCo also offers MEC to Mary’s spouse and dependents.

On Form 1095-C, NewCo uses: Line 14: Code 1E (MEC providing MV offered to employee and at

least MEC offered to dependent(s) and spouse entire year); and Line 16: Code 2C (employee enrolled in coverage offered).

Example 1 – Insured Group Health Plan (GHP)

39 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

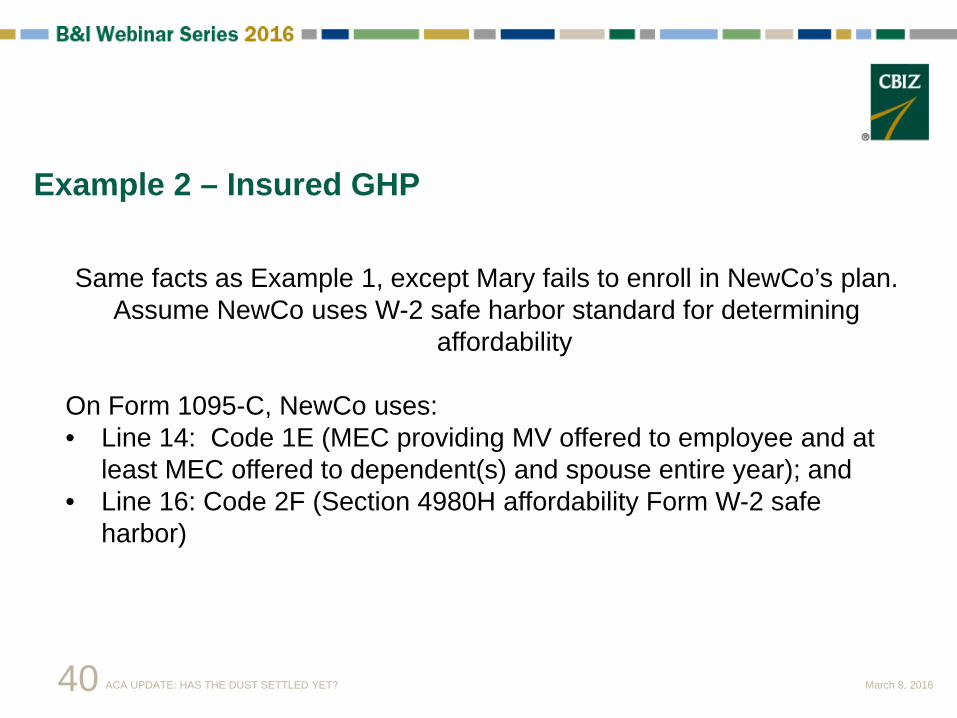

Same facts as Example 1, except Mary fails to enroll in NewCo’s plan. Assume NewCo uses W-2 safe harbor standard for determining

affordability On Form 1095-C, NewCo uses: • Line 14: Code 1E (MEC providing MV offered to employee and at

least MEC offered to dependent(s) and spouse entire year); and • Line 16: Code 2F (Section 4980H affordability Form W-2 safe

harbor)

Example 2 – Insured GHP

40 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

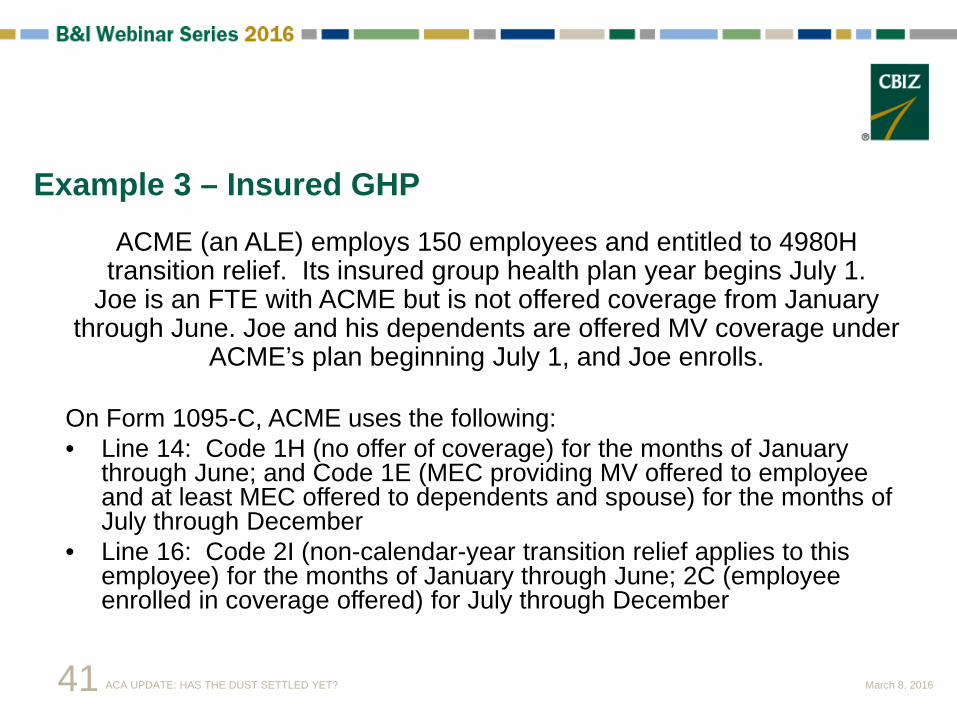

ACME (an ALE) employs 150 employees and entitled to 4980H transition relief. Its insured group health plan year begins July 1.

Joe is an FTE with ACME but is not offered coverage from January through June. Joe and his dependents are offered MV coverage under

ACME’s plan beginning July 1, and Joe enrolls.

On Form 1095-C, ACME uses the following: • Line 14: Code 1H (no offer of coverage) for the months of January

through June; and Code 1E (MEC providing MV offered to employee and at least MEC offered to dependents and spouse) for the months of July through December

• Line 16: Code 2I (non-calendar-year transition relief applies to this employee) for the months of January through June; 2C (employee enrolled in coverage offered) for July through December

Example 3 – Insured GHP

41 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

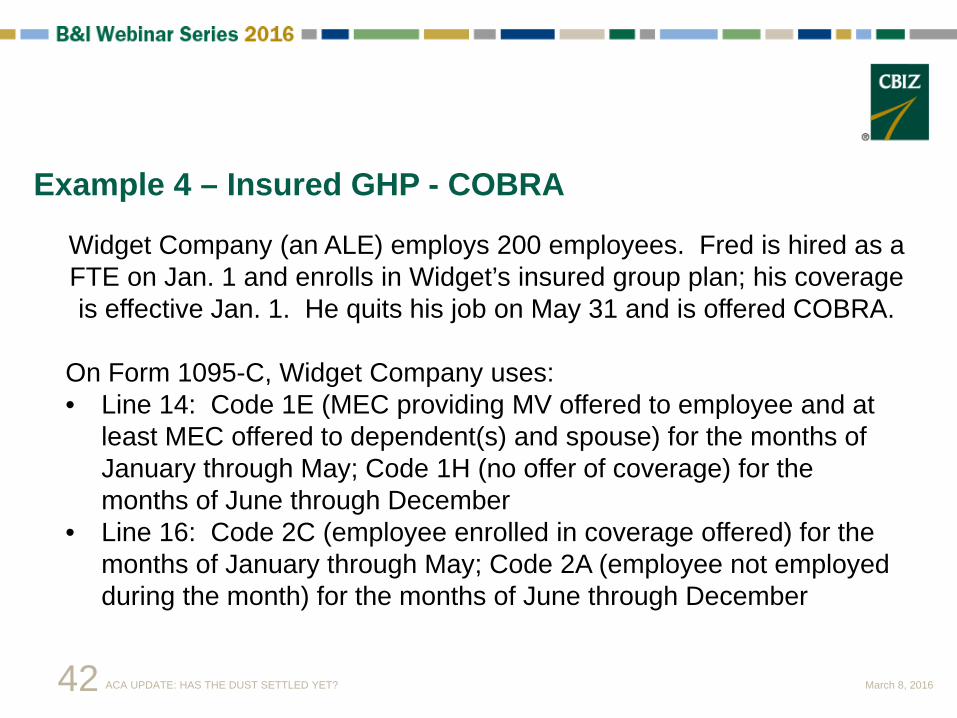

Widget Company (an ALE) employs 200 employees. Fred is hired as a FTE on Jan. 1 and enrolls in Widget’s insured group plan; his coverage is effective Jan. 1. He quits his job on May 31 and is offered COBRA.

On Form 1095-C, Widget Company uses: • Line 14: Code 1E (MEC providing MV offered to employee and at

least MEC offered to dependent(s) and spouse) for the months of January through May; Code 1H (no offer of coverage) for the months of June through December

• Line 16: Code 2C (employee enrolled in coverage offered) for the months of January through May; Code 2A (employee not employed during the month) for the months of June through December

Example 4 – Insured GHP - COBRA

42 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

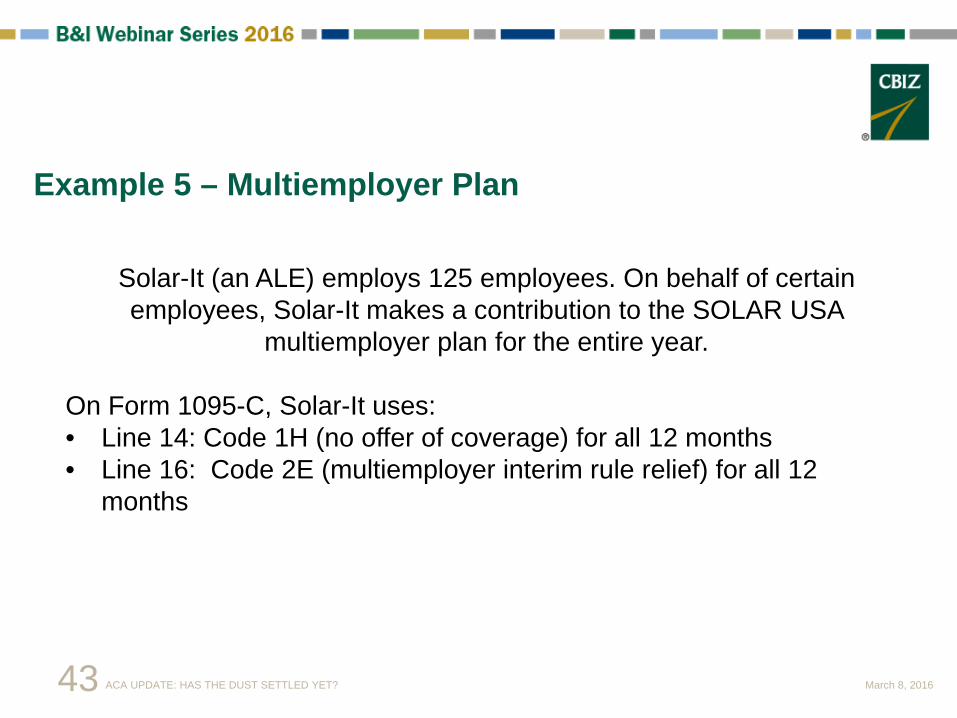

Solar-It (an ALE) employs 125 employees. On behalf of certain employees, Solar-It makes a contribution to the SOLAR USA

multiemployer plan for the entire year. On Form 1095-C, Solar-It uses: • Line 14: Code 1H (no offer of coverage) for all 12 months • Line 16: Code 2E (multiemployer interim rule relief) for all 12

months

Example 5 – Multiemployer Plan

43 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

Jane is an FTE employed by Old Company (an ALE). She and her spouse

and two children are offered MEC that meets the Form W-2 affordability standard. All four of them enroll in Old Company’s self-funded group

health plan. On Form 1095-C, Old Company uses:

• Line 14: Code 1E (MEC providing MV offered to employee and at least MEC offered to dependent(s) and spouse) for all 12 months

• Line 16: Code 2C (employee enrolled in coverage offered) for all 12 months

Example 6 – Self-Funded GHP

44 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

Then, in Part III of the Form 1095-C, Old Company completes columns (a) through (e) for Jane, her spouse and two children: Column (a): Name of each covered individual Column (b): Enter the nine-digit Social Security number (SSN) for each

covered individual, including the dashes Column (c): Enter date of birth (MM/DD/YYYY) for the covered individual

only if column (b) is blank Column (d): Check this box if the individual was covered for at least one day

per month for all 12 months of the calendar year Column (e): If the individual was not covered for all 12 months of the

calendar year, check the applicable box(es) for the months in which the individual was covered for at least one day in the month

Example 6, cont’d

45 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

Same facts as Example 6, except Jane terminates employment with Old Company on Sept. 30. She and her family elect COBRA continuation

coverage. On the 2015 Form 1095-C, Old Company uses: • Line 14: Code 1E (MEC providing MV offered to employee and at least MEC

offered to dependent(s) and spouse) for the months of January through September; Code 1H (no offer of coverage) for the months of October through December

• Line 16: Code 2C (employee enrolled in coverage offered) for the months of January through September; Code 2A (employee not employed during the month) for the months of October through December.

Example 7 – Self-Funded GHP - COBRA

46 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

Then, in Part III of the 2015 Form 1095-C, Old Company completes Columns (a) through (e) for Jane, her spouse and two children:

Column (a): Name of each covered individual Column (b): Enter the nine-digit SSN for each covered individual,

including the dashes Column (c): Enter a date of birth (MM/DD/YYYY) for the covered

individual only if column (b) is blank Column (d): Check this box if the individual was covered for at least one

day per month for all 12 months of the calendar year Column (e): If the individual was not covered for all 12 months of the

calendar year, check the applicable box(es) for the months in which the individual was covered for at least one day in the month

Example 7, cont’d

47 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

For the following year on the 2016 Form 1095-C, Jane, her spouse and dependents are still receiving COBRA coverage. Old Company would use:

Line 14: 1G (offer of coverage to employee who was not an FTE for any month of the calendar year, which may include one or more months in which the individual was not an employee, and who enrolled in self-insured coverage for one or more months of the calendar year)

Line 16: [leave blank] Then, in Part III of the Form 1095-C, Old Company completes Columns (a) through (e) for Jane, her spouse and two children who elected COBRA coverage.

Example 7, cont’d

48 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

ACA Information Center for Applicable Large Employers (ALEs)

http://www.irs.gov/Affordable-Care-Act/Employers/ACA-Information-Center-for-Applicable-Large-Employers-ALEs

Information Reporting by Providers of Minimum Essential Coverage

http://www.irs.gov/Affordable-Care-Act/Employers/Information-Reporting-by-Providers-of-Minimum-Essential-Coverage

Questions and Answers about Health Care Information Forms for

Individuals (Forms 1095-A, 1095-B, and 1095-C) http://www.irs.gov/Affordable-Care-Act/Questions-and-Answers-about-Health-Care-Information-

Forms-for-Individuals

IRS Resources, Forms, Publications, Q and A’s, Webinars, Tax Tips and Related Outreach Materials

49 ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

QUESTIONS?

The information contained herein is not intended to be legal, accounting, or other professional advice, nor are these comments directed to specific situations. The

information contained herein is provided as general guidance and may be affected by changes in law or regulation. The information contained herein is not intended to replace or substitute for accounting or other professional advice. Attorneys or tax advisors must

be consulted for assistance in specific situations. This information is provided as-is, with no warranties of any kind. CBIZ shall not be liable

for any damages whatsoever in connection with its use and assumes no obligation to inform the reader of any changes in laws or other factors that could affect the information

contained herein.

ACA UPDATE: HAS THE DUST SETTLED YET? March 8, 2016

50