a.f.ferguson & co. - pwc pakistan · pdf file · 2015-06-032 a. f. ferguson...

TRANSCRIPT

A.F.FERGUSON & CO.a member firm of the PwC network

Provincial Finance Acts, 2014

1

A. F. FERGUSON & CO. Provincial Finance Acts, 2014a member firm of the PwC network

A. F. FERGUSON & CO.

PROVINCIAL FINANCE ACTS, 2014SINDH, PUNJAB & KHYBER PAKHTUNKHWA

This Memorandum summarises salient features of the Provincial Finance Acts, 2014 passed byrespective Provincial Assemblies. Under the Constitution, Provinces can levy tax inter alia onrendering of services, disposal and use of immovable properties and agricultural income tax.

This Memorandum contains our views on the revised status of the respective fiscal statutes,after the enactment of Provincial Finance Acts. All changes made through the Provincial FinanceActs are effective July 1, 2014. For considering the precise effect of a particular change, it isadvised that reference should be made to the specific wordings in the relevant statute and theamendments made through the Provincial Finance Acts should be acted upon only afterobtaining appropriate advice.

This Memorandum can also be accessed on our website www.pwc.com/pk

© 2014 A. F. FERGUSON & CO., Chartered Accountants, a member firm of the PwC network. All rights reserved. PwC refers to the network ofmember firms of PricewaterhouseCoopers International Limited, each of which is a separate and independent legal entity.

September 25, 2014

2

A. F. FERGUSON & CO. Provincial Finance Acts, 2014a member firm of the PwC network

Page Number

Sindh Finance Act, 2014 3

Punjab Finance Act, 2014 11

Khyber Pakhtunkhwa Finance Act, 2014 15

CONTENTS

3

A. F. FERGUSON & CO. Provincial Finance Acts, 2014a member firm of the PwC network

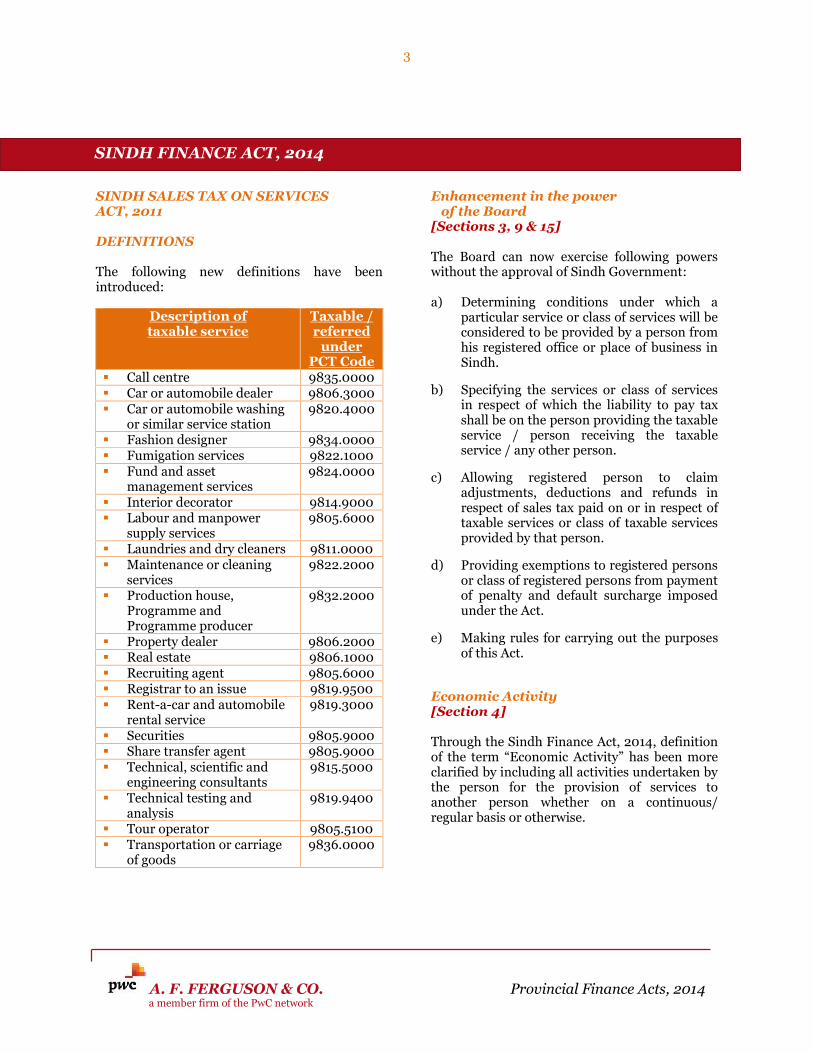

SINDH SALES TAX ON SERVICESACT, 2011

DEFINITIONS

The following new definitions have beenintroduced:

Description oftaxable service

Taxable /referred

underPCT Code

Call centre 9835.0000 Car or automobile dealer 9806.3000 Car or automobile washing

or similar service station9820.4000

Fashion designer 9834.0000 Fumigation services 9822.1000 Fund and asset

management services9824.0000

Interior decorator 9814.9000 Labour and manpower

supply services9805.6000

Laundries and dry cleaners 9811.0000 Maintenance or cleaning

services9822.2000

Production house,Programme andProgramme producer

9832.2000

Property dealer 9806.2000 Real estate 9806.1000 Recruiting agent 9805.6000 Registrar to an issue 9819.9500 Rent-a-car and automobile

rental service9819.3000

Securities 9805.9000 Share transfer agent 9805.9000 Technical, scientific and

engineering consultants9815.5000

Technical testing andanalysis

9819.9400

Tour operator 9805.5100 Transportation or carriage

of goods9836.0000

Enhancement in the powerof the Board

[Sections 3, 9 & 15]

The Board can now exercise following powerswithout the approval of Sindh Government:

a) Determining conditions under which aparticular service or class of services will beconsidered to be provided by a person fromhis registered office or place of business inSindh.

b) Specifying the services or class of servicesin respect of which the liability to pay taxshall be on the person providing the taxableservice / person receiving the taxableservice / any other person.

c) Allowing registered person to claimadjustments, deductions and refunds inrespect of sales tax paid on or in respect oftaxable services or class of taxable servicesprovided by that person.

d) Providing exemptions to registered personsor class of registered persons from paymentof penalty and default surcharge imposedunder the Act.

e) Making rules for carrying out the purposesof this Act.

Economic Activity[Section 4]

Through the Sindh Finance Act, 2014, definitionof the term “Economic Activity” has been moreclarified by including all activities undertaken bythe person for the provision of services toanother person whether on a continuous/regular basis or otherwise.

SINDH FINANCE ACT, 2014

4

A. F. FERGUSON & CO. Provincial Finance Acts, 2014a member firm of the PwC network

Time, manner and modeof payment

[Section 17]

Prior to the Sindh Finance Act, 2014, the SindhSales Tax on Services Act, 2011 prescribed thatthe sales tax was to be paid by the person at thetime of filing of return for the relevant taxperiod. However, the relevant rule required thatpayment of sales tax to be made by 15th day ofthe month next following the tax period to whichit relates, and the sales tax return was to be filedwithin 3 days of due date for the payment ofsales tax.

The Sindh Sales Tax on Services Act, 2011 hasnow been brought in line with relevant rule,whereby sales tax shall be paid by a person by15th day of the month next following the taxperiod to which it relates.

Records[Section 26]

Prior to the Sindh Finance Act, 2014, aregistered person was required to maintain andkeep records of taxable services provided by himor by his agent in English or Urdu languagesonly. As a result of amendment made throughthe Sindh Finance Act, 2014, records can also bemaintained in Sindhi language.

As a result of another change made through theSindh Finance Act, 2014, a registered personwhose accounts are subject to audit under anylaw including the Companies Ordinance, 1984has been required to submit a printed copy ofthe annual audited accounts to the AssistantCommissioner - SRB within 60 days from thedate of audit report of the auditors. Prior to theSindh Finance Act, 2014, the law merelyrequired submission of annual audited accountswith SRB, without specifying the time limit.

The issue of ‘certification’ by auditor of paymentof sales tax by registered person needs to beresolved. In this regard, generally acceptedauditing principles do not include ‘certification’of information like complete discharge of taxliability of any person.

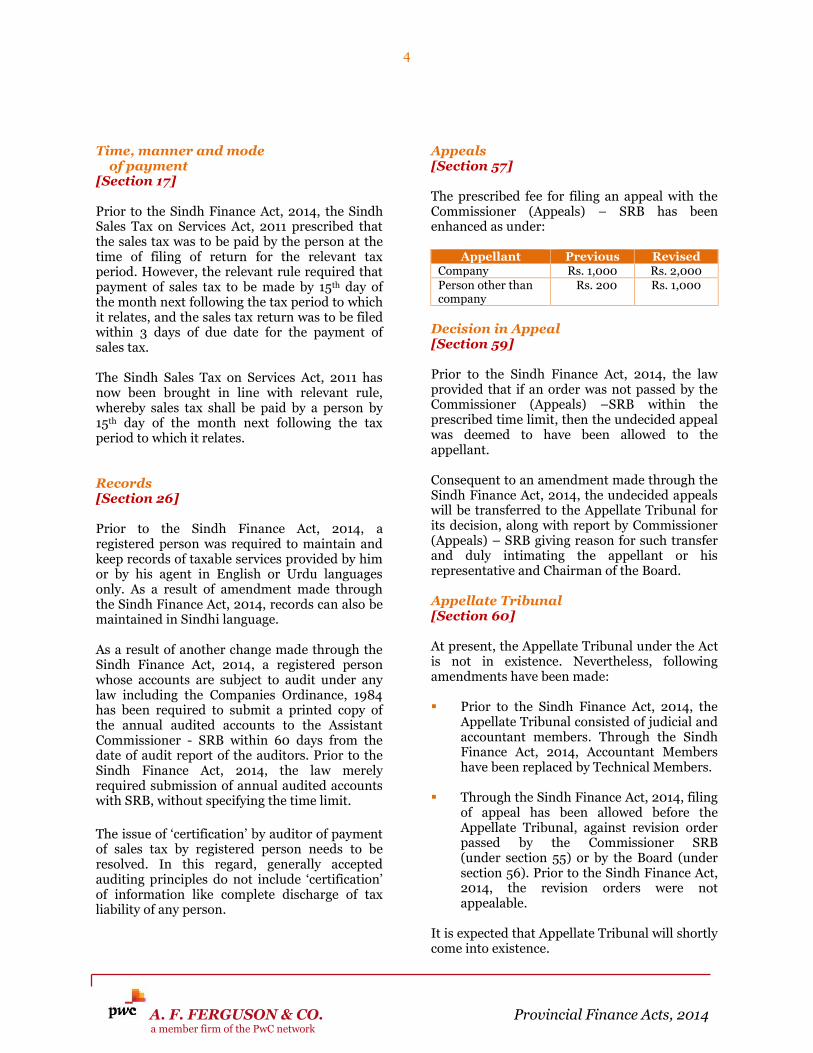

Appeals[Section 57]

The prescribed fee for filing an appeal with theCommissioner (Appeals) – SRB has beenenhanced as under:

Appellant Previous RevisedCompany Rs. 1,000 Rs. 2,000Person other thancompany

Rs. 200 Rs. 1,000

Decision in Appeal[Section 59]

Prior to the Sindh Finance Act, 2014, the lawprovided that if an order was not passed by theCommissioner (Appeals) –SRB within theprescribed time limit, then the undecided appealwas deemed to have been allowed to theappellant.

Consequent to an amendment made through theSindh Finance Act, 2014, the undecided appealswill be transferred to the Appellate Tribunal forits decision, along with report by Commissioner(Appeals) – SRB giving reason for such transferand duly intimating the appellant or hisrepresentative and Chairman of the Board.

Appellate Tribunal[Section 60]

At present, the Appellate Tribunal under the Actis not in existence. Nevertheless, followingamendments have been made:

Prior to the Sindh Finance Act, 2014, theAppellate Tribunal consisted of judicial andaccountant members. Through the SindhFinance Act, 2014, Accountant Membershave been replaced by Technical Members.

Through the Sindh Finance Act, 2014, filingof appeal has been allowed before theAppellate Tribunal, against revision orderpassed by the Commissioner SRB(under section 55) or by the Board (undersection 56). Prior to the Sindh Finance Act,2014, the revision orders were notappealable.

It is expected that Appellate Tribunal will shortlycome into existence.

5

A. F. FERGUSON & CO. Provincial Finance Acts, 2014a member firm of the PwC network

Reduction in General Sales Tax Rate[Second Schedule]

Through the Sindh Finance Act, 2014, thegeneral rate of 16% has been reduced to 15%for all taxable services, except for tele-communication services which will continue tobe chargeable to tax @ 19.5%.

Addition in Taxable Services[Second Schedule]

The following new services have been taxedthrough the Finance Act, 2014:

Services taxable @ 15%:

Recruitment agents

Share transfer agents

Services provided or rendered by laundriesand dry cleaners

Interior decorators

Technical testing and analysis service

Services provided or rendered by registrar toan issue

Workshops for electric or electronicequipments or appliances, etc., includingcomputer hardware

Car or automobile washing or similar servicestations

Services provided or rendered by call centres

Services taxable @ 10%:

Tour operators

Services provided or rendered in the matterof purchase or sale or hire of immovableproperty

Services provided or rendered by Propertydealers

Services provided or rendered by Car orautomobile dealers

Technical, scientific and engineeringconsultants

Rent a car and automobile rental service

Cable TV operators

Fumigation services

Maintenance or cleaning services

Janitorial services

Services provided or rendered byprogramme producers and productionhouses

Services provided or rendered by fashiondesigners

Services taxable @ 5%:

Services provided or rendered by corporatelaw consultants

Services provided or rendered by personsengaged in inter-city transportation orcarriage of goods by road or throughpipeline or conduit

Increase in reduced concessionary rates[Second Schedule]

Through SRB’s Notification no. 3-4/10/2014dated July 1, 2014, the reduced rate of SindhSales Tax @ 4% applicable on the followingsectors has been increased to 5%, with a view toreducing the gap between the standard rate andthe reduced rate:

Legal practitioners & consultants

Accountants & auditors;

Tax consultants; and

Constructors.

6

A. F. FERGUSON & CO. Provincial Finance Acts, 2014a member firm of the PwC network

Withdrawal of exemption[Notification dated July 1, 2014]

Through SRB’s Notification No. 3-4/11/2014dated July 1, 2014, following exemptions havebeen withdrawn by making amendmentsin earlier Notification No. 3-4/7/2013 datedJune 18, 2013:

(i) Group life insurance of individuals forinsurance policy coverage of more thanRs. 500,000.

(ii) Health insurance

(iii) Construction services related to projects ofdeveloping or promoting conversion of landinto residential or commercial plots orconstruction of residential or commercialbuildings, subject to payment of tax asproperty development or promoters.

Extension / Rationalization of exemption[Notification dated July 1, 2014]

Through SRB’s Notification No. 3-4/11/2014dated July 1, 2014, amendments have beenmade in earlier Notification No. 3-4/7/2013dated June 18, 2013, for extending theexemption to following:

Description Taxableunder

PCT Code Hajj and Umrah tour

operators9805.5100

Services of cable TVoperators in rural areasunder PEMRA’s license of‘R’ category

9819.9000

Public health fumigationservices provided orrendered by the Federal,Provincial or LocalGovernments andCantonment Boards

9822.1000

Agricultural fumigationservices

9822.1000

Furthermore, exemption available to thefollowing has been rationalized:

Description Taxableunder

PCT Code Beauty parlours / clinics

and slimming clinics9810.0000

Laundries and dry cleaners 9811.0000 Network services 98.12 Workshop for electric or

electronic equipments orappliances includingComputer Hardware

9820.3000

Car or automobile washingor similar service stations

9820.4000

Sindh Sales Tax Withholding Rules[Notification dated July 1, 2014]

Through SRB’s Notification No. 3-4/14/2014dated July 1, 2014, the Sindh Sales Tax SpecialProcedure (Withholding) Rules, 2011 have beenreplaced by Sindh Sales Tax Special Procedures(Withholding) Rules, 2014 with effect fromJuly 1, 2014. Following significant changes havebeen made in new withholding rules:

(i) Now every company is required to withholdSindh Sales Tax. Previously, onlycompanies falling under jurisdiction ofLarge Taxpayers Unit were required towithhold Sindh Sales Tax.

(ii) Withholding of Sindh Sales Tax is notrequired if the withholding agent is not aresident of Sindh and/or does not have aplace of business in Sindh.

(iii) Now, only SRB registered persons are liableto make 100% withholding while makingpayment to unregistered person providinga taxable service. Previously, allwithholding agents were required to make100% withholding while making paymentto unregistered persons. There is howeverno change in withholding from payment onaccount of advertisement services, whichshall be made at the rate of 100% of theapplicable rate of sales tax.

7

A. F. FERGUSON & CO. Provincial Finance Acts, 2014a member firm of the PwC network

(iv) Non-LTU registered persons providingtaxable supplies are now subject towithholding at 1/5th of the sales tax chargedon invoices. The general rate of withholdingfor registered persons providing taxableservices (other than advertisementservices) is also 1/5th of sales tax charged(previously, withholding of non-LTUregistered person was applicable at 1/16th ofsales tax charged).

Significant changes in Sindh Sales Taxon Services Rules, 2011 (SST Rules)[Notification dated July 1, 2014]

Through SRB’s Notification No. 3-4/13/2014dated July 1, 2014, following significant changeshave been made in the SST Rules:

(i) For insurance companies, ‘value of taxableservice’ is the gross amount of premiumcharged on risk covered in the insurance orreinsurance policy, which has now beenamended/extended to include grossamount of reinsurance premium, fee orcharges received by a reinsurance company.The amendment has apparently been madeto address the issue raised in the case ofinsurance companies, where there was aview that reinsurance premium charged byinsurance companies was not chargeable toSindh Sales Tax.

(ii) The due date for payment of monthly salestax by an advertising agent was previouslymentioned in Rule 33 as 15th day of themonth following the tax period to which itrelates. To provide relief, necessaryamendment has been made in Rule 33prescribing the due date for payment ofsales tax to be 15th day of the second monthfollowing the tax period.

Similarly, the due date for payment ofmonthly sales tax by persons providingservices of advertisement on television,radio, cable TV and CCTV was notprescribed in Rule 34, which has now beenprescribed to be 15th day of the secondmonth following the tax period.

(iii) Rule 40 deals with Port Operators andTerminal Operators. The Rule has beensubstituted to clarify various services whichare chargeable to Sindh Sales Tax. It hasalso been clarified that all services relatingto cargo imported into Pakistan or theimported cargo in transit or intransshipment through a port or terminalin Sindh, shall be chargeable to Sindh SalesTax.

(iv) By substituting Rule 41(3), the ‘value oftaxable service’ of Stockbrokers andCommodity brokers has been defined toinclude gross commission, fee,remuneration and charges received by astockbroker or commodity brokers inrespect of:

(a) sale or purchase or subscriptionof securities in an exchange orover-the-counter market/deal.

(b) advisory or consultancy services.(c) research services.(d) other such incidental or similar

services.

(v) Consequent to levy of Sindh Sales Tax oninter-city transfer of goods by road orthrough pipelines or conduit, specialprocedure rules have been introducedunder Rule 42G, salient features of whichare as under:

(a) every person or goods transportagency providing the service of inter-city transportation or carriage ofgoods by road or through pipeline orconduit, whether in Sindh or fromSindh, is liable to registration withSRB.

(b) The value of taxable services is definedto be the gross amount charged forservices, including the charges forservices of cargo handling like loading,unloading, packing, unpacking,stacking and storage of goods or cargo.

8

A. F. FERGUSON & CO. Provincial Finance Acts, 2014a member firm of the PwC network

(c) The amount of sales tax is to bedeposited with SRB:

- in case of prepaid transportationor carriage services, by 15th day ofthe month following the taxperiod; and

- in case of post-paid or ‘to pay atdestination’ transportation orcarriage of goods, by 15th day ofthe second month following thetax period.

NEGATIVE LIST

In the Salient Features issued by SindhGovernment, it has been announced that w.e.f.July 1, 2015, all services provided in or fromSindh will be taxable except for certain exemptservices for which negative list will be issued.As a result, existing tariff schedules (i.e.,First and Second Schedules to the Sindh SalesTax on Services Act, 2011) will be dispensedwith.

CAPITAL VALUE TAX ON IMMOVABLEPROPERTY

Section 4 of the Sindh Finance Act, 2010,introduced capital value tax on the capital valueof an immovable property payable by everyperson who acquires by purchase, gift, exchange,power of attorney (other than revocable andtime-bound), an immovable property or a rightto use thereof for more than 20 years, or renewalof the lease or any premium paid thereon.

The immovable properties for the purposes ofCapital Value Tax (CVT) are classified into twocategories:

a) Residential immovable property (recordedand unrecorded property value).

b) Commercial and Industrial immovableproperty situated in Sindh.

Prior to the Sindh Finance Act, 2014, immovableproperty, where the value thereof was recorded,was subject to CVT as prescribed percentage ofrecorded value; whereas CVT on immovableproperty, where the value was not recorded, wascharged on the basis of prescribed fixed rates persquare feet / yard.

Through the Sindh Finance Act, 2014, it hasbeen prescribed that the CVT on immovableproperty, where value is recorded, should becharged at the higher of:

a) recorded value of the property; or

b) value according to the Valuation Table.

In this perspective, Valuation Table means,“the Valuation Table notified under section 27-Aof the Stamp Act, 1899 (Act No.II of 1899).”

Real Estate Investment Trust

Through the Sindh Finance Act, 2014, CVT hasbeen levied @ 1% of the market value ontransfers of properties to the Real EstateInvestment Trust.

Moreover, Registration Fee for all properties tobe transferred in favour of Real EstateInvestment Trust has been prescribed @ 0.5% ofthe market value of the property. Prior to theSindh Finance Act, 2014, the transfer ofimmovable property in Sindh was liable toregistration fee @ 1% of the property value.

In this regard ‘market value’ has been defined tomean, “...the fair value of the property to bedetermined by the authority notified by theBoard of Revenue Sindh in consultation withFinance Department; provided that such marketvalue shall not be below the value specified inValuation Table”.

STAMP DUTY

The Stamp Act, 1899, is a federal legislation;however the rates of stamp duty are fixed by theProvincial Governments.

Through the Sindh Finance Act, 2014, the ratesof stamp duty on certain documents have beenincreased.

9

A. F. FERGUSON & CO. Provincial Finance Acts, 2014a member firm of the PwC network

Apart from increasing the rates of stamp duty,another significant amendment made throughthe Sindh Finance Act, 2014 is a considerablechange in the classes of documents which nowfall within the ambit of dutiable instruments.

Allotment Order or Transfer ofAllotment Order

Prior to the Sindh Finance Act, 2014, AllotmentOrder or Transfer of Allotment Order issued by adeveloper, builder, co-operative society, housingsociety or housing authority, or any other bodyor organization providing before lease, weredutiable only in respect of open plots.

Through the Sindh Finance Act, 2014, a newcategory has been introduced in Schedule I,Article 4, for Allotment Order or Transfer ofAllotment Order issued by aforesaid persons /entities in respect of built-up properties. In suchcase, the Allotment Order will now also be liableto stamp duty as follows:

Description Rate(i) Residential

houseTen rupees per Sq.ft.

(ii) Residential flat Five rupees per Sq.ft.(iii) Commercial

Offices /Premises

Fifteen rupees perSq.ft.

(iv) Industrial units/factories

Fifteen rupees perSq.ft.

Moreover, an increase has been made in therates at which stamp duty is chargeable onAllotment Order or Transfer of Allotment Orderin respect of open plots. A comparison ofprevious and revised rates is as under:

Description Previousrate

Revisedrate

(i) Residential Plots:

(a) up to 399Sq.yds

(b) 400 Sq.yds orabove

Rs. 10 perSq. yd.Rs. 20 perSq. yd.

Rs. 15 perSq. yd.Rs. 30 perSq. yd.

Description Previousrate

Revisedrate

(ii) Residential plots(termed ascommercial openplots in the existingSchedule)

Rs. 30per Sq.yd.

Rs. 40 perSq. yd.

(iii) Industrial plots Rs. 5 perSq. yd.

Rs. 20 perSq. yd.

Contract (Schedule I, Article 15)

Amendment has been made through the SindhFinance Act, 2014 to extend the scope ofdocuments that fall within the description of‘contract’ from contracts relating to ‘engineeringconsultancy’ to ‘any other services’ as wellchargeable to stamp duty @ 30 paisa for every100 rupees or part thereof of the amount ofcontract.

Instrument of Gift (Schedule I, Article 20)

Through the Sindh Finance Act, 2014,gift instruments of (not being settlement or willor transfer) executed between spouses, father,mother, son, daughter, grandparents, grandchildren, brother and sister, have been subjectedto stamp duty @ 1/5th of the duty leviable onConveyance [(No.16-A(iii) – which, prior to theSindh Finance Act, 2014, was 2% of the value inaccordance with the valuation table; whereassuch instrument, if executed between personsother than the above, has been subjected tostamp duty at the rate as applicable onConveyance [(No.16-A(iii)].

Prior to the Sindh Finance Act, 2014, an affidavit/ declaration in writing confirming an oral giftwas chargeable @ 1/10th of the duty leviable onConveyance (No.16-A(iii), if made in favour of alegal heir, and @ 3% if made in favour of anyperson other than a legal heir, of the value ofproperty determined in accordance with thevaluation table

Lease (Schedule I, Article 21)

In Schedule I, Article 21 (i) Open plots have beenincluded in the categories of propertiessubjected to stamp duty for which leaseinstument is to be drawn out. Moreover, it hasalso substituted the existing slab rates of stampduties with a flat rate of 1% as per valuationtable.

10

A. F. FERGUSON & CO. Provincial Finance Acts, 2014a member firm of the PwC network

Through an amendment made in Schedule I,Article 21 (ii), surrender of a lease, sub-lease andpre lease of open property in urban areas is nowalso chargeable to stamp duty in addition tobuilt-up properties.

A reduction in the rate of stamp duty has alsobeen made regarding instruments of surrenderof lease, as follows:

Previous rate Revised rate

3% of such valuedetermined inaccordance with thevaluation table.

2% of such valuedetermined inaccordance withthe valuation table

Settlement (Schedule I, Article 30)

Any Settlement instrument (including a deed ofdower), other than where the settlement is madefor charitable or religious purpose, shall now beliable to stamp duty either @ 2% of the valuein accordance the valuation table undersections 27-A and 27 B or 5% of the value ofmovable property settled.

11

A. F. FERGUSON & CO. Provincial Finance Acts, 2014a member firm of the PwC network

PUNJAB SALES TAX ON SERVICES ACT,2012

DEFINITIONS

Authority[Section 2(6)]

Definition of “Authority” has been redrafted tospecify that Punjab Revenue Authority isestablished under the Punjab Revenue AuthorityAct, 2012.

Association of Persons[Section 2(29)]

The definition of “Person” has been amended toinclude an “association of persons” to rectify anapparent omission in the present law, as a resultof which ‘association of persons’ was not earlierrequired to charge sales tax on taxable servicesprovided by them.

Services in relation to disposition ofgoods[Section 2(38)]

While defining the term ‘service’ or ‘services’, ithas been clarified that a service remain andcontinue to be treated as service regardless ofthe fact that rendering thereof involves any ‘use’,‘supply’ or ‘consumption’ of goods.

Through this amendment, ‘disposition of goods’has been added along with the word ‘supply’.

Tax Fraud[Section 2(43)(d)]

At present, any act done knowingly, dishonestlyor fraudulently and without having any lawfulexcuse by acting in contravention of the dutiesor obligations imposed under the Act or rules orinstructions issued there-under with theintention of ‘understating’ or ‘suppressing’ taxliability constitutes a ‘tax fraud’. Prior to theFinance Act, the law did not expressly treat ‘non-payment’ of sales tax as an act of ‘tax fraud’.

The expression ‘not paying’ has, therefore, beenadded to the definition of ‘tax fraud’.

This amendment needs to be examined inlegal sense. Non-payment unless coupled with‘mens rea’ cannot be considered as a ‘fraud’.

VALUE OF TAXABLE SERVICE[Section 7]

Prior to the Punjab Finance Act, 2014, ‘value oftaxable service’ was taken equivalent to theconsideration in money that a service providerreceives from the recipient of the service.This also included all duties and taxes (otherthan sales tax).

Through the Punjab Finance Act, 2014, the basishas been amended from mere ‘consideration’ to‘gross consideration’.

REGISTRATION[Section 25]

An ‘explanation’ has been inserted in provisionsrelating to ‘registration’ in order to clarify thatno person shall be absolved of any tax liabilityaccrued under the Act owing to mere non-registration with the Authority.

RESTORATION OF REGISTRATION[Section 29A]

A new section has been inserted empowering theAuthority to reactivate, revive, reinstate orrestore any registration which was deactivated,suspended or cancelled for any reason or underany circumstances. However, the Authority shallonly exercise such powers upon fulfillment of theprescribed conditions.

3%

PUNJAB FINANCE ACT, 2014

12

A. F. FERGUSON & CO. Provincial Finance Acts, 2014a member firm of the PwC network

RECORDS[Section 31]

Presently, every registered person providingtaxable services is required to maintain and keepspecified record of taxable services in theprescribed manner. Now, a person required topay tax under the Act or Rules is alsoresponsible to maintain and keep the relevantrecord like a registered person providing taxableservices.

OFFENCES AND PENALTIES[Section 48(2)]

Through the Punjab Finance Act, 2014,following amendments have been made in penalprovisions:

Penalty regarding failure to make anapplication for registration is enhanced fromRs 10,000 to Rs 50,000, or 5% of the taxinvolved (whichever is higher).

Recipient of services is also made liable topay penalty of Rs 25,000 or 100% of taxpayable in case of non-payment of due tax,being an act of obstruction in theperformance of duties by tax authorities.[This amendment seems inappropriate inthe contextual background].

RECOVERY OF TAX NOT LEVIED ORSHORT LEVIED[Section 52]

Previously, an officer of the Authority wasempowered to issue a show-cause notice to theperson liable to pay tax in respect of amount oftax not levied or short levied within three yearsof the relevant tax period. Through the PunjabFinance Act, 2014, this time limit of three yearshas been increased to five years.

RECOVERY OF ARREARS OF TAX[Section 70]

For the purposes of recovery of arrears of tax, anew sub section (3) has been inserted wherebyan officer of the Authority or the Authority isempowered to exercise powers of a Civil Courtunder the Code of Civil Procedure, 1908.

SCOPE OF TAXABLE SERVICESEXTENDED[Second Schedule]

Extension of kinds of services taxable under theexisting entries of the Second Schedule:

Description PCT Code Race clubs 9830.0000 Cargo services by road

passenger transportationbusiness and transportationthrough pipe line andconduit services

9804.9000

Cafes, food (including ice-cream) parlors, coffeehouses, coffee shops, deras,food huts, eateries, resortsand similar cooked,prepared or ready-to-eatfood service outlets etc.

9801.9000

Intellectual property rightsservices

9839.0000

Investment managementservices

9815.4000and

9826.0000 Technical inspection and

certification services,quality control (standards'certification), technicalanalysis and testing,erection, commissioningand installation services.

9815.5000and

9819.9400

Other consultants includingbut not limited to humanresource and personneldevelopment services,exhibition or conventionservices, event managementservices, valuation services(including competency andeligibility testing services),market research servicesand credit rating services.

9815.9000,9832.0000,9827.0000,9818.3000,9818.2000,9819.9300,9852.0000

and9859.0000

Travel agents including alltheir allied services orfacilities.

9805.5000and

9803.9000

Labour and manpowersupplies.

9805.6000

13

A. F. FERGUSON & CO. Provincial Finance Acts, 2014a member firm of the PwC network

Services provided by sharetransfer or depositoryagents including servicesprovided through manual orelectronic book-entrysystem used to record andmaintain securities and toregister the transfer ofshares, securities andderivatives.

Respectiveheadings

Services by Realtors 9844.0000

Services provided byfashion designers whetherrelating to textile, leather,jewellery or other productregimes including alliedservices such as cutting,stitching, printing,manufacturing, fabrication,assembly, embellishment,adornments, display(including marketing,packing and delivery etc.)

9819.6000

Services by automobiledealers

9845.0000

Industrial and commercialpackaging services andsimilar outsourcing ofindustrial or commercialprocesses

9841.0000and

9819.1400

All the above services are subject to sales tax at16%.

ADDITION IN TAXABLE SERVICES[Serial No 38 through 47 of the SecondSchedule]

The following new services have been taxedthrough the Punjab Finance Act, 2014:

Services taxable @ 19.5%:

Call centers

Services taxable @ 16%:

Services provided by specialized workshopsor undertakings (auto – workshops;workshops for industrial machinery,

construction and earth moving machinery orother special purpose machinery etc.;workshops for electric or electronicequipment or appliances etc. includingcomputer hardware; car washing or similarservice stations and other workshops)

Services provided for specified purposesincluding fumigation services, maintenanceand repair (including building andequipment maintenance and repairincluding after sale services) or cleaningservices, janitorial services, dredging ordesilting services and other similar servicesetc.

Brokerage (other than stock) and indentingservices including commission agents,underwriters and auctioneers

Services provided by laboratories other thanservices related to technological ordiagnostic services for patients

Services provided in specified fields such ashealthcare, gym, physical fitness, indoorsports, games and body or sauna massageetc.

Services provided by laundries and drycleaners

Services provided by cable TV operators

Services provided by TV or radio programproducers or production houses

Services taxable @ 5%:

Advertisements (including classified ads) innewspapers, magazines, journals andperiodicals

14

A. F. FERGUSON & CO. Provincial Finance Acts, 2014a member firm of the PwC network

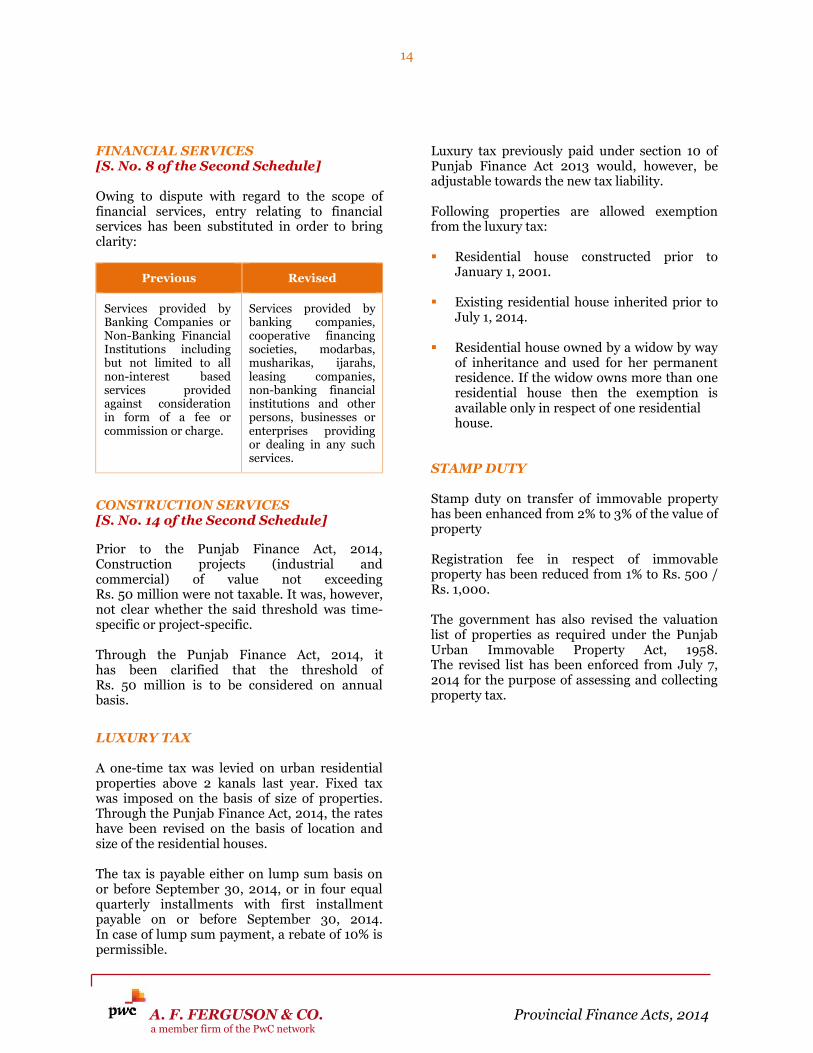

FINANCIAL SERVICES[S. No. 8 of the Second Schedule]

Owing to dispute with regard to the scope offinancial services, entry relating to financialservices has been substituted in order to bringclarity:

Previous Revised

Services provided byBanking Companies orNon-Banking FinancialInstitutions includingbut not limited to allnon-interest basedservices providedagainst considerationin form of a fee orcommission or charge.

Services provided bybanking companies,cooperative financingsocieties, modarbas,musharikas, ijarahs,leasing companies,non-banking financialinstitutions and otherpersons, businesses orenterprises providingor dealing in any suchservices.

CONSTRUCTION SERVICES[S. No. 14 of the Second Schedule]

Prior to the Punjab Finance Act, 2014,Construction projects (industrial andcommercial) of value not exceedingRs. 50 million were not taxable. It was, however,not clear whether the said threshold was time-specific or project-specific.

Through the Punjab Finance Act, 2014, ithas been clarified that the threshold ofRs. 50 million is to be considered on annualbasis.

LUXURY TAX

A one-time tax was levied on urban residentialproperties above 2 kanals last year. Fixed taxwas imposed on the basis of size of properties.Through the Punjab Finance Act, 2014, the rateshave been revised on the basis of location andsize of the residential houses.

The tax is payable either on lump sum basis onor before September 30, 2014, or in four equalquarterly installments with first installmentpayable on or before September 30, 2014.In case of lump sum payment, a rebate of 10% ispermissible.

Luxury tax previously paid under section 10 ofPunjab Finance Act 2013 would, however, beadjustable towards the new tax liability.

Following properties are allowed exemptionfrom the luxury tax:

Residential house constructed prior toJanuary 1, 2001.

Existing residential house inherited prior toJuly 1, 2014.

Residential house owned by a widow by wayof inheritance and used for her permanentresidence. If the widow owns more than oneresidential house then the exemption isavailable only in respect of one residentialhouse.

STAMP DUTY

Stamp duty on transfer of immovable propertyhas been enhanced from 2% to 3% of the value ofproperty

Registration fee in respect of immovableproperty has been reduced from 1% to Rs. 500 /Rs. 1,000.

The government has also revised the valuationlist of properties as required under the PunjabUrban Immovable Property Act, 1958.The revised list has been enforced from July 7,2014 for the purpose of assessing and collectingproperty tax.

15

A. F. FERGUSON & CO. Provincial Finance Acts, 2014a member firm of the PwC network

SALES TAX ON SERVICES

Reduction in General Sales Tax Rate[Second Schedule]

Through the KPK Finance Act, 2014, the generalrate of 16% has been reduced to 15% for alltaxable services, except for telecommunicationservices which will continue to be chargeable totax @ 19.5%.

Addition in Taxable Services[Second Schedule]

Through Notification dated August 4, 2014, thefollowing new services have been taxed by way ofaddition in the Second Schedule:

Services taxable @ 15%:

Services provided by shipping agents.

Services provided or rendered by freightforwarding agents.

Services provided by tour operators, otherthan Hajj and Umrah.

Manpower recruitment and labour supplyservices.

Services provided by advertising agents.

Services provided by share transfer agents.

Services provided by property dealers, realestate agents, real estate planners, bywhatever name called.

Services provided by car or automobiledealers, bargain centres, by whatever namecalled.

Services provided by car or automobiledealers, bargain centres, by whatever namecalled.

Rent-a-car services.

Services provided by workshops forindustrial construction and earth-moving orother special purpose machinery.

Services provided by persons engaged incontractual execution of work or furnishingsupplies.

Services provided by persons engaged incontractual execution of work or furnishingsupplies.

Services provided by architects, townplanners, property developers or promotersand interior decorators.

Management consultancy services includingfund and asset management service.

Services provided by technical, scientific &engineering consultants.

Airport services.

Contracting services rendered or providedby the contractors of buildings, electro-mechanical works, turn-key projects andsimilar other works, excluding constructionprojects having value not exceeding Rs. 50million, construction of industrial estatesand zones, consular buildings andconstruction works under internationaltenders based on foreign grants.

Port operating services.

Services provided in respect of mining ofminerals, exploration of oil & gas includingrelated surveys and allied activities

Sponsorship services

Event management, exhibition services,services by event photographers, video-grapher and other persons related to suchevents

KHYBER PAKHTUNKHWA FINANCE ACT, 2014

16

A. F. FERGUSON & CO. Provincial Finance Acts, 2014a member firm of the PwC network

Services provided or rendered by:- Professionals and consultants- Health care consultants- Legal practitioners or consultants- Management consultants- Software or IT based system developmentconsultants

- Accountants, auditors and tax consultants- Services provided by other consultants.

Public bonded warehouses

Container Terminal Services

Copy Right Services

Cosmetic & Plastic Surgery Services

Sale of Space for Advertisement Services

Video Tape & Production Services

Sound Record Services

TV, Radio & Production house Services

Services provided by clubs

Broadcasting services

Services taxable @ 10%:

Services provided or rendered by specializedagencies, Security agency, Market researchagency, other such agencies.

Services provided by business supportservices.

Franchise Services.

Services provided in respect ofmanufacturing or processing on toll basis.

Tracking services and security alarmservices.

Services provided by motor vehicleworkshops, mechanic shops, airconditioningfitting service and clearing centres

Services taxable at other rates:

Services provided by land and propertydevelopers or promoters for development ofland, purchased or leased, for conversioninto residential or commercial plots(taxable @Rs. 100/- per square yard for landdevelopment); and

Construction of residential or commercialunits, excluding residential commercialprojects where the covered area does notexceed 10,000 square feet for houses and20,000 square feet for apartments(taxable @ Rs. 50/- per square yard for landdevelopment).

SCOPE OF TAXABLE SERVICESEXTENDED / RATIONALISED[Second Schedule]

Through Notification dated August 4, 2014,services taxable under the existing entries of theSecond Schedule have been extended /rationalised by substituting the existing entriesas under:

Previous RevisedServices providedby hotels,marriage halls,lawns, clubs andcaterers andservices ancillarythereto.

Services provided or renderedby hotels, restaurants,marriage halls, pandals andshamiana services, lawns,caterers, motels, guest houses,by whatever name called,including any other servicesancillary thereto.

Services providedor rendered forpersonal care bybeauty parlours,beauty clinics,slimming clinics.

Services provided or renderedfor personal care by beautyparlours, beauty clinics, Healthcare centres, health clubs,gyms, physical fitness centres,body massage centres andpedicure centres.

Advertisementon close circuitTV or Cable TV

Advertisement on hoardingboards, pole signs and signboards and on close circuit TV,Cable TV, Websites or internet.

17

A. F. FERGUSON & CO. Provincial Finance Acts, 2014a member firm of the PwC network

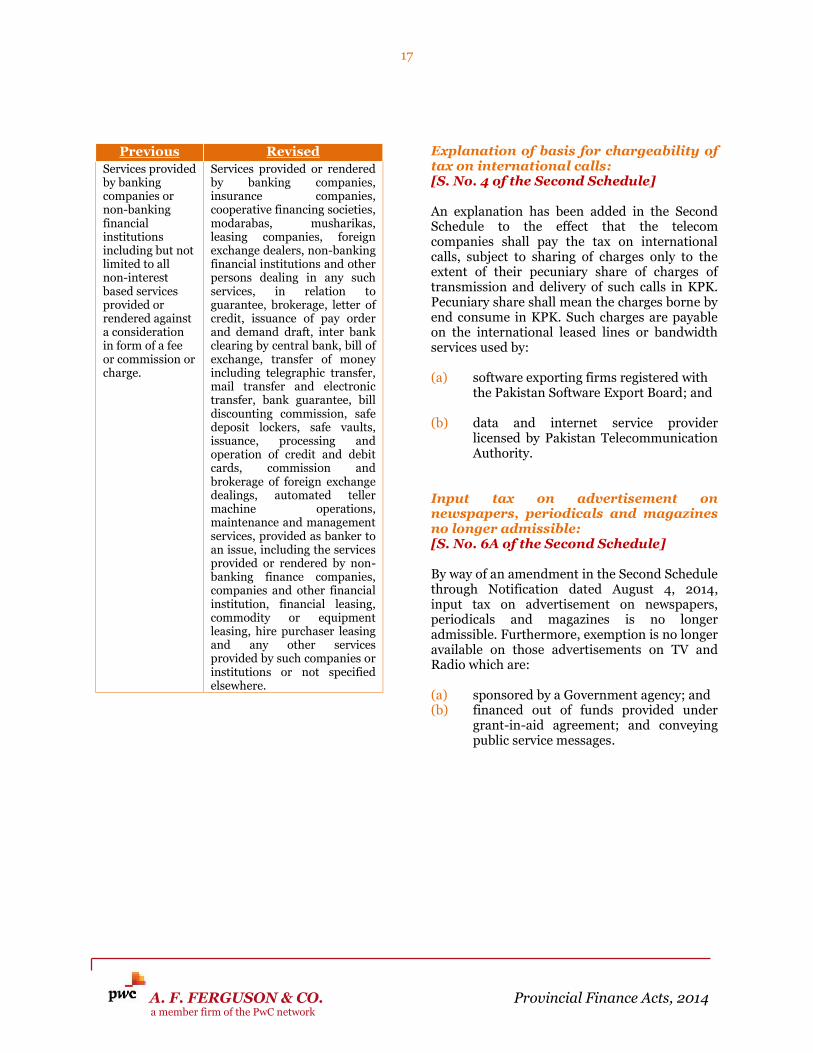

Previous RevisedServices providedby bankingcompanies ornon-bankingfinancialinstitutionsincluding but notlimited to allnon-interestbased servicesprovided orrendered againsta considerationin form of a feeor commission orcharge.

Services provided or renderedby banking companies,insurance companies,cooperative financing societies,modarabas, musharikas,leasing companies, foreignexchange dealers, non-bankingfinancial institutions and otherpersons dealing in any suchservices, in relation toguarantee, brokerage, letter ofcredit, issuance of pay orderand demand draft, inter bankclearing by central bank, bill ofexchange, transfer of moneyincluding telegraphic transfer,mail transfer and electronictransfer, bank guarantee, billdiscounting commission, safedeposit lockers, safe vaults,issuance, processing andoperation of credit and debitcards, commission andbrokerage of foreign exchangedealings, automated tellermachine operations,maintenance and managementservices, provided as banker toan issue, including the servicesprovided or rendered by non-banking finance companies,companies and other financialinstitution, financial leasing,commodity or equipmentleasing, hire purchaser leasingand any other servicesprovided by such companies orinstitutions or not specifiedelsewhere.

Explanation of basis for chargeability oftax on international calls:[S. No. 4 of the Second Schedule]

An explanation has been added in the SecondSchedule to the effect that the telecomcompanies shall pay the tax on internationalcalls, subject to sharing of charges only to theextent of their pecuniary share of charges oftransmission and delivery of such calls in KPK.Pecuniary share shall mean the charges borne byend consume in KPK. Such charges are payableon the international leased lines or bandwidthservices used by:

(a) software exporting firms registered withthe Pakistan Software Export Board; and

(b) data and internet service providerlicensed by Pakistan TelecommunicationAuthority.

Input tax on advertisement onnewspapers, periodicals and magazinesno longer admissible:[S. No. 6A of the Second Schedule]

By way of an amendment in the Second Schedulethrough Notification dated August 4, 2014,input tax on advertisement on newspapers,periodicals and magazines is no longeradmissible. Furthermore, exemption is no longeravailable on those advertisements on TV andRadio which are:

(a) sponsored by a Government agency; and(b) financed out of funds provided under

grant-in-aid agreement; and conveyingpublic service messages.

18

A. F. FERGUSON & CO. Provincial Finance Acts, 2014a member firm of the PwC network

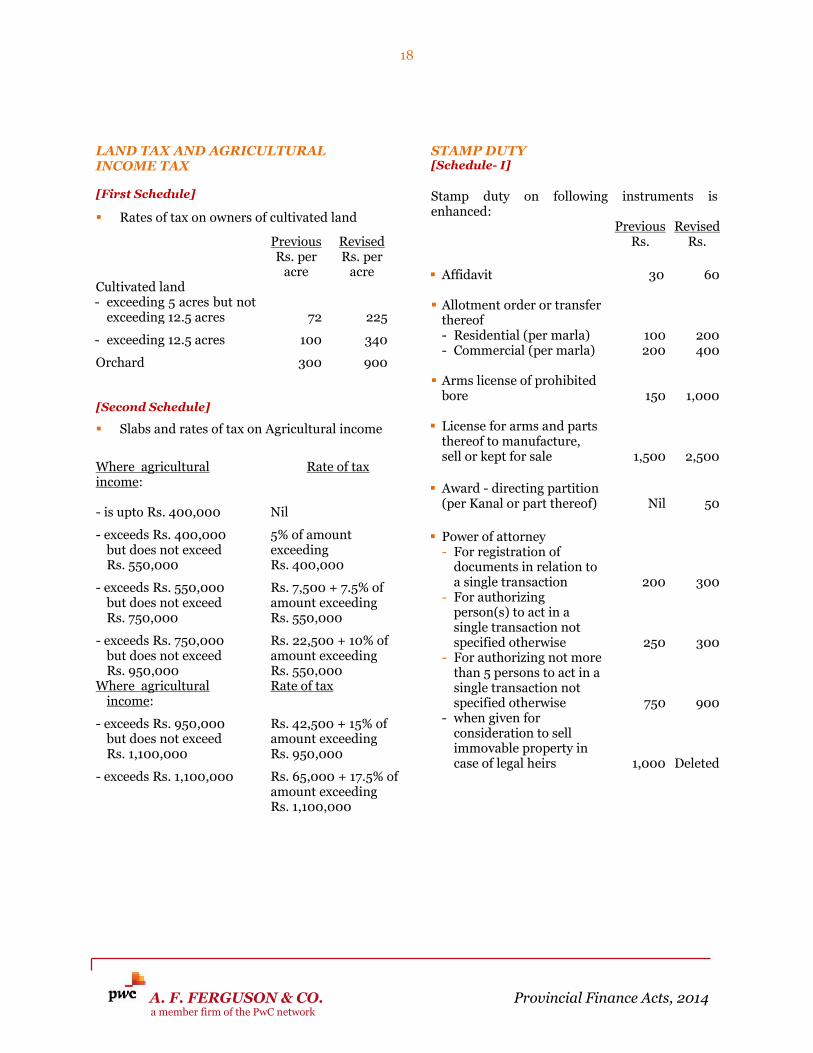

LAND TAX AND AGRICULTURALINCOME TAX

[First Schedule]

Rates of tax on owners of cultivated land

Previous RevisedRs. per

acreRs. per

acreCultivated land- exceeding 5 acres but not

exceeding 12.5 acres 72 225

- exceeding 12.5 acres 100 340

Orchard 300 900

[Second Schedule]

Slabs and rates of tax on Agricultural income

Where agriculturalincome:

Rate of tax

- is upto Rs. 400,000 Nil

- exceeds Rs. 400,000but does not exceedRs. 550,000

5% of amountexceedingRs. 400,000

- exceeds Rs. 550,000but does not exceedRs. 750,000

Rs. 7,500 + 7.5% ofamount exceedingRs. 550,000

- exceeds Rs. 750,000but does not exceedRs. 950,000

Rs. 22,500 + 10% ofamount exceedingRs. 550,000

Where agriculturalincome:

Rate of tax

- exceeds Rs. 950,000but does not exceedRs. 1,100,000

Rs. 42,500 + 15% ofamount exceedingRs. 950,000

- exceeds Rs. 1,100,000 Rs. 65,000 + 17.5% ofamount exceedingRs. 1,100,000

STAMP DUTY[Schedule- I]

Stamp duty on following instruments isenhanced:

Previous RevisedRs. Rs.

Affidavit 30 60

Allotment order or transferthereof- Residential (per marla) 100 200- Commercial (per marla) 200 400

Arms license of prohibitedbore 150 1,000

License for arms and partsthereof to manufacture,sell or kept for sale 1,500 2,500

Award - directing partition(per Kanal or part thereof) Nil 50

Power of attorney- For registration of

documents in relation toa single transaction 200 300

- For authorizingperson(s) to act in asingle transaction notspecified otherwise 250 300

- For authorizing not morethan 5 persons to act in asingle transaction notspecified otherwise 750 900

- when given forconsideration to sellimmovable property incase of legal heirs 1,000 Deleted

19

A. F. FERGUSON & CO. Provincial Finance Acts, 2014a member firm of the PwC network

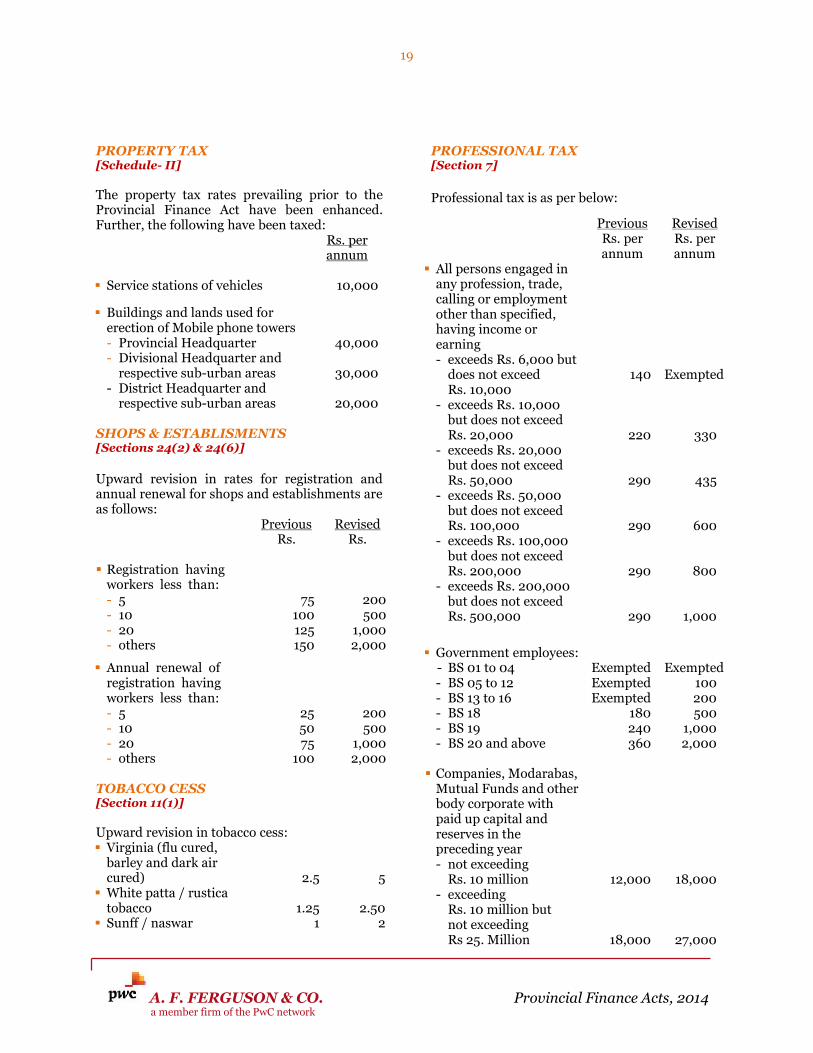

PROPERTY TAX[Schedule- II]

The property tax rates prevailing prior to theProvincial Finance Act have been enhanced.Further, the following have been taxed:

Rs. perannum

Service stations of vehicles 10,000

Buildings and lands used forerection of Mobile phone towers- Provincial Headquarter 40,000- Divisional Headquarter and

respective sub-urban areas 30,000- District Headquarter and

respective sub-urban areas 20,000

SHOPS & ESTABLISMENTS[Sections 24(2) & 24(6)]

Upward revision in rates for registration andannual renewal for shops and establishments areas follows:

Previous RevisedRs. Rs.

Registration havingworkers less than:- 5 75 200- 10 100 500- 20 125 1,000- others 150 2,000

Annual renewal ofregistration havingworkers less than:- 5 25 200- 10 50 500- 20 75 1,000- others 100 2,000

TOBACCO CESS[Section 11(1)]

Upward revision in tobacco cess: Virginia (flu cured,

barley and dark aircured) 2.5 5 White patta / rustica

tobacco 1.25 2.50 Sunff / naswar 1 2

PROFESSIONAL TAX[Section 7]

Professional tax is as per below:

PreviousRs. perannum

RevisedRs. perannum

All persons engaged inany profession, trade,calling or employmentother than specified,having income orearning- exceeds Rs. 6,000 but

does not exceedRs. 10,000

140 Exempted

- exceeds Rs. 10,000but does not exceedRs. 20,000 220 330

- exceeds Rs. 20,000but does not exceedRs. 50,000 290 435

- exceeds Rs. 50,000but does not exceedRs. 100,000 290 600

- exceeds Rs. 100,000but does not exceedRs. 200,000 290 800

- exceeds Rs. 200,000but does not exceedRs. 500,000 290 1,000

Government employees:- BS 01 to 04 Exempted Exempted- BS 05 to 12 Exempted 100- BS 13 to 16 Exempted 200- BS 18 180 500- BS 19 240 1,000- BS 20 and above 360 2,000

Companies, Modarabas,Mutual Funds and otherbody corporate withpaid up capital andreserves in thepreceding year- not exceeding

Rs. 10 million 12,000 18,000- exceeding

Rs. 10 million butnot exceedingRs 25. Million 18,000 27,000

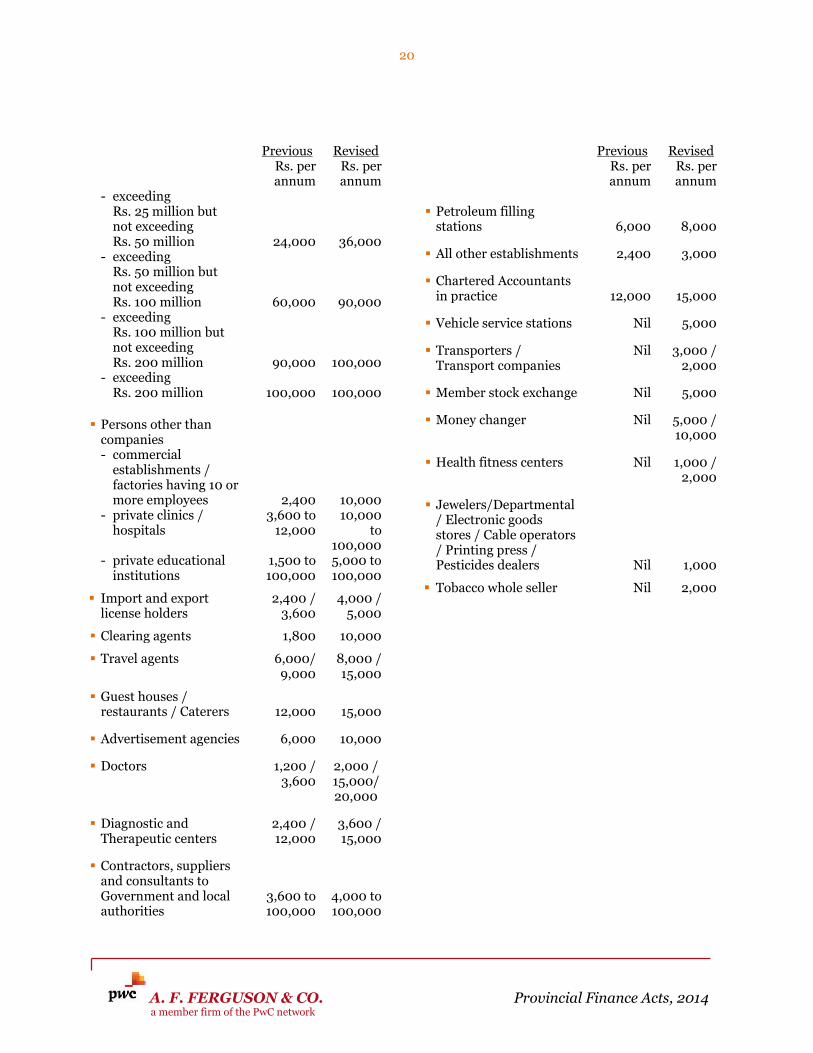

20

A. F. FERGUSON & CO. Provincial Finance Acts, 2014a member firm of the PwC network

PreviousRs. perannum

RevisedRs. perannum

- exceedingRs. 25 million butnot exceedingRs. 50 million 24,000 36,000

- exceedingRs. 50 million butnot exceedingRs. 100 million 60,000 90,000

- exceedingRs. 100 million butnot exceedingRs. 200 million 90,000 100,000

- exceedingRs. 200 million 100,000 100,000

Persons other thancompanies- commercial

establishments /factories having 10 ormore employees 2,400 10,000

- private clinics /hospitals

3,600 to12,000

10,000to

100,000- private educational

institutions1,500 to100,000

5,000 to100,000

Import and exportlicense holders

2,400 /3,600

4,000 /5,000

Clearing agents 1,800 10,000

Travel agents 6,000/9,000

8,000 /15,000

Guest houses /restaurants / Caterers 12,000 15,000

Advertisement agencies 6,000 10,000

Doctors 1,200 /3,600

2,000 /15,000/20,000

Diagnostic andTherapeutic centers

2,400 /12,000

3,600 /15,000

Contractors, suppliersand consultants toGovernment and localauthorities

3,600 to100,000

4,000 to100,000

PreviousRs. perannum

RevisedRs. perannum

Petroleum fillingstations 6,000 8,000

All other establishments 2,400 3,000

Chartered Accountantsin practice 12,000 15,000

Vehicle service stations Nil 5,000

Transporters /Transport companies

Nil 3,000 /2,000

Member stock exchange Nil 5,000

Money changer Nil 5,000 /10,000

Health fitness centers Nil 1,000 /2,000

Jewelers/Departmental/ Electronic goodsstores / Cable operators/ Printing press /Pesticides dealers Nil 1,000

Tobacco whole seller Nil 2,000

21

A. F. FERGUSON & CO. Provincial Finance Acts, 2014a member firm of the PwC network

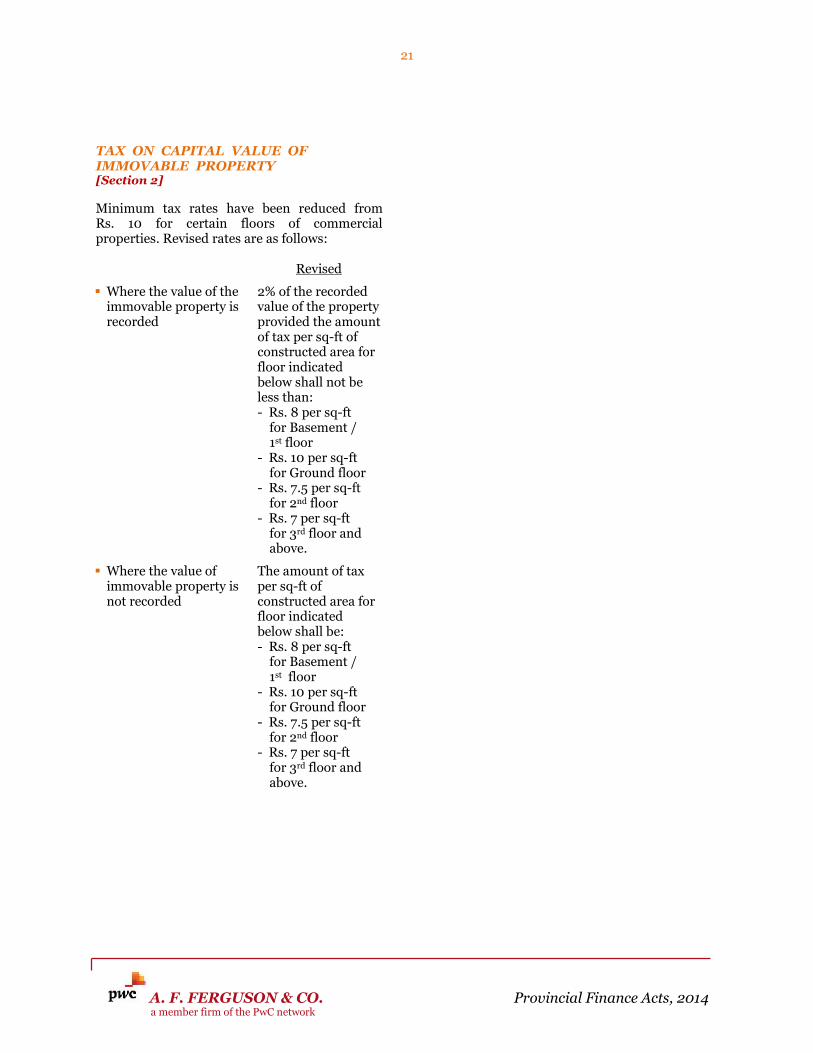

TAX ON CAPITAL VALUE OFIMMOVABLE PROPERTY[Section 2]

Minimum tax rates have been reduced fromRs. 10 for certain floors of commercialproperties. Revised rates are as follows:

Revised

Where the value of theimmovable property isrecorded

2% of the recordedvalue of the propertyprovided the amountof tax per sq-ft ofconstructed area forfloor indicatedbelow shall not beless than:- Rs. 8 per sq-ft

for Basement /1st floor

- Rs. 10 per sq-ftfor Ground floor

- Rs. 7.5 per sq-ftfor 2nd floor

- Rs. 7 per sq-ftfor 3rd floor andabove.

Where the value ofimmovable property isnot recorded

The amount of taxper sq-ft ofconstructed area forfloor indicatedbelow shall be:- Rs. 8 per sq-ft

for Basement /1st floor

- Rs. 10 per sq-ftfor Ground floor

- Rs. 7.5 per sq-ftfor 2nd floor

- Rs. 7 per sq-ftfor 3rd floor andabove.