aedes siiq final · the reproduction of the information, recommendations and research produced by...

TRANSCRIPT

Intermonte SIM S.p.A. Milan 20122 (Italy) – Galleria de Cristoforis, 7/8 - phone: +39-02-77115.1 fax: +39-02-77115.300 New York - (USA) - Sales contacts: JPP Eurosecurities, 595 Madison Avenue, 10022 - phone: +1 (212) 521 6718

Italian Research New Coverage Milan, May 24, 2016

AEDES SIIQ Price (Eu):

Target Price (Eu):

OUTPERFORM0.39

0.60

SECTOR: Real Estate

Federico Pezzetti +39-02-77115.268e-mail: [email protected]

Simpler, Healthier, And Ready to Grow A “Historic” real estate company with a revamped look. Aedes was founded in 1905 and

became the first real estate company to float on the Milan Stock Exchange in 1924. In 2008, when the real estate market was hit by the economic crisis, the company found itself in increasing financial difficulties and was forced to take extraordinary measures, including several operations to raise new capital in 2014-2015. The group is now run by a completely new board representing a mostly new controlling shareholders and is pursuing a simpler investment strategy than in the past.

Moving towards a simpler “REIT” business model. Thanks in part to its new status as a SIIQ (the Italian version of REIT), Aedes’s strategy is now focused on the creation and medium to long term retention of an income-bearing portfolio of commercial property, predominantly in the retail arena. The group is building for the future by investing in two portfolios, one income-bearing and the other a development portfolio which it already owns.

Development portfolio: the key source of organic growth. The development property portfolio is composed chiefly of projects for commercial use and the company expects some of these initiatives to turn into income-generating assets. Some initiatives centre around the Serravalle Scrivia “Designer Outlet”, although the key one is represented by a Eu300mn capex retail and entertainment project in Caselle (Turin).

Real estate funds: a market for opportunistic acquisitions. Another pillar of the group’s strategy is the intention to look for acquisition opportunities among real estate funds, (usually trading at a deep discount to face values) with the subsequent goal of assimilating them into the group’s real estate portfolio (a clear example of this strategy is the recent acquisition of the Redwood fund). This also comes on the back of some new options introduced by the Renzi government with the “Unblock Italy” decree.

Knowledgeable management boasting a major success story in retail real estate. CEO Giuseppe Roveda, through the Praga group, was responsible for the development of the Serravalle Designer Outlet in the early 2000’s. This innovative intervention involved the construction of the biggest outlet centre in Europe, and was a major success that radically enhanced the local area’s profile and economic status.

We initiate with an Outperform recommendation and a Eu0.60 target price. Despite the huge progress made over the last couple of years, Aedes SIIQ remains a “work-in-progress” with still a number of weaknesses/risks including low cashflow generation, sub-par dividend distribution and uncertainty around the Caselle development project. Still, we believe that a committed management, an opportunistic approach on income bearing assets, and interesting development opportunities represent an appealing mix at current valuations. The stock is currently trading at a 60% discount to 2016E NAV which represents a significant gap vs the 30% average discount at which trade its main Italian peers Beni Stabili and IGD.

AEDES SIIQ - 12m Performance

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

m-15 l-15 s-15 n-15 g-16 m-16

AEDES SIIQ

AEDES SIIQ Rel. to BCI Index (Reb.)

RATING: New Coverage

TARGET PRICE (Eu): New Coverage Change in EPS est: 2016E 2017E

STOCK DATAReuters code: AEDI.MIBloomberg code: AE IM

Performance 1m 3m 12m Absolute -8.4% 4.0% -49.5% Relative -3.1% 2.6% -28.3%12 months H/L: 1.03/0.32

SHAREHOLDER DATANo. of Ord. shares (mn): 320Total No. of shares (mn): 320Mkt Cap Ord (Eu mn): 126Total Mkt Cap (Eu mn): 126Mkt Float - ord (Eu mn): 46Mkt Float (in %): 36.2%

Main shareholder: Augusto 51.2%

BALANCE SHEET DATA 2016Book value (Eu mn): 286BVPS (Eu): 0.89P/BV: 0.4Net Debt (#BadKeyword mn): -161NAV (Eu mn) 313

The reproduction of the information, recommendations and research produced by Intermonte SIM contained herein, and of any of its parts, is strictly prohibited. None of the contents of this document may be shared with third parties without Company authorization.

Key Figures 2014A 2015A 2016E 2017E 2018EEBIT (Eu mn) (4) 8 23 7 26Net profit (Eu mn) -6 0 17 2 19EPS - New (Eu) -0.042 -0.044 -0.016 -0.014 -0.010EPS - Old (Eu)DPS (Eu) 0.000 0.000 0.000 0.000 0.009NAVPS (Eu) 1.010 0.872 0.979 0.983 1.031

Ratios & Multiples 2014A 2015A 2016E 2017E 2018EP/E nm nm nm nm nmDiv. Yield 0.0% 0.0% 0.0% 0.0% 2.4%P/NAVPS 0.4 0.5 0.4 0.4 0.4ROCE -1.6% 3.0% 6.7% 1.5% 4.6%

Please see important disclaimer

on the last page of this report

2

AEDES SIIQ - KEY FIGURES 2014A 2015A 2016E 2017E 2018E

Fiscal year end 31/12/2014 31/12/2015 31/12/2016 31/12/2017 31/12/2018

PROFIT & LOSS (Eu mn) Sales 22 32 39 22 25EBITDA (1) 6 17 2 6EBIT (4) 8 23 7 26Financial income (charges) (5) (4) (5) (7) (10)Associates & Others (2) (1) (1) 1 1Pre-tax profit (loss) (13) 2 17 2 19Taxes 6 (1) (0) (0) (0)Tax rate (%) 32.0% 32.0% 32.0% 32.0% 32.0%Minorities & discontinue activities (1) 1 1 1 1Net profit -6 0 17 2 19Total extraordinary items 0 0 0 0 0Ebitda excl. extraordinary items (1) 6 17 2 6Ebit excl. extraordinary items (4) 8 23 7 26Net profit restated (10) (14) (5) (4) (3)

PER SHARE DATA (Eu) Total shares out (mn) - average fd 233 320 320 320 320EPS stated fd 0.217 0.019 0.053 0.002 0.055EPS restated fd -0.042 -0.044 -0.016 -0.014 -0.010BVPS fd 0.000 0.841 0.893 0.898 0.947NAVPS fd 1.010 0.872 0.979 0.983 1.031Dividend per share (ord) 0.000 0.000 0.000 0.000 0.009Dividend pay out ratio (%) 0.0% 0.0% 0.0% 0.0% 16.1%

CASH FLOW (Eu mn) Change in NWC 0 160 0 0 0Capital expenditure 2 2 8 97 96Other cash items 0 0 0 0 0Free cash flow (FCF) (17) (10) (11) (99) (97)Acquisitions, divestments & other 17 38 (54) (15) (10)Dividend 0.0 0.0 0.0 0.0 -3.0Change in Net Financial Position 0 28 (65) (114) (110)

BALANCE SHEET (Eu mn) Total fixed assets 165 325 444 559 683Net working capital 215 56 56 56 56Long term liabilities (110) (95) (96) (97) (98)Net capital employed 270 286 403 517 641Net financial position (124) (96) (161) (275) (385)Group equity 239 275 291 292 307Minorities 5 6 6 5 5Net equity 234 269 286 287 303

NAV DATA (Eu mn) Properties and other assets - Book value 298 321 419 534 658Properties and other assets - Market value 298 321 419 534 658NAV 235 279 313 314 330

RATIOS(%) EBITDA margin* nm 19.9% 44.5% 9.4% 23.3%EBIT margin* nm 26.1% 59.5% 31.7% 106.4%Gearing - Debt/equity 52.0% 34.8% 55.2% 94.0% 125.3%Interest cover on EBIT nm 2.0 4.9 1.0 2.8Debt/Ebitda nm 15.00 9.36 134.10 66.58Capex as % sales 7.8% 5.6% 19.4% 444.5% 386.0%ROCE* -1.6% 3.0% 6.7% 1.5% 4.6%ROE* -5.4% 0.0% 6.0% 0.5% 6.3%

GROWTH RATES (%) Sales nm 44.2% 20.1% -43.6% 14.3%EBITDA* nm nm 168.6% -88.1% 182.2%EBIT* nm nm 174.1% -70.0% 283.8%Net profit nm nm 57419.4% -90.8% 1127.0%EPS restated nm nm nm nm nm

* Excluding extraordinary items

Source: Intermonte SIM estimates

3

Index

Executive Summary page 4

Company Overview page 6

Portfolio Description and Statistics page 12

Italian Market Fundamentals page 19

Group Financials & Estimates page 23

Valuation page 29

Appendix I page 32

Appendix II page 33

Appendix III page 35

4

Executive Summary A “Historic” real estate company with a revamped look. Aedes was founded in 1905 and became the first real estate company to float on the Milan Stock Exchange in 1924. In 2008, when the real estate market was hit by the economic crisis, the company found itself in increasing financial difficulties and was forced to take extraordinary measures, including several operations to raise new capital in 2014-2015. The group is now run by a completely new board representing a mostly new controlling shareholders and is pursuing a simpler investment strategy than in the past. Moving towards a simpler “REIT” business model. Thanks in part to its new status as a SIIQ (the Italian version of REIT), Aedes’s strategy is now focused on the creation and medium to long term retention of an income-bearing portfolio of commercial property, predominantly in the retail arena. The group is building for the future by investing in two portfolios, one income-bearing and the other a development portfolio which it already owns. On the one hand it will purchase new rented properties to compete with the performance of European REITs, while on the other it will develop a new generation of shopping and leisure centres through a development pipeline, with the aim of eventually transferring them to the income-bearing portfolio controlled by Aedes SIIQ. A real estate portfolio focused on retail properties... At the end of 2015 Aedes SIIQ had a real estate portfolio with a “pro-quota” GAV (i.e. including its stakes in real estate funds and joint ventures) of Eu412mn. Around 47% of this was represented by the rented portfolio with another 30% coming from development assets (the “develop to be rented” part of the portfolio) and the remaining 23% being represented by the trading portfolio. Retail represents the largest category, accounting for some 50% of the total, while office properties represent some 24% of the total “pro-quota” portfolio. … and concentrated in northern Italy. From a geographical standpoint the portfolio is heavily concentrated in the richest regions of northern Italy. In particular, Piedmont and Lombardy are the two key regions where over 80% of Aedes’s total pro-forma assets are located. The city that stands out most in the company’s portfolio is Milan, where almost 30% of the total asset value is concentrated. Other key locations are Serravalle and Caselle (near Turin), both in the north-west region of Piedmont. Income-bearing portfolio: room to work on vacancy rates but limited reversionary potential. Within the rented portfolio there is potential to improve vacancy rates, which currently stand at 13% for the fully consolidated portfolio. On the other hand reversionary potential is limited: when looking at the entire pro-quota portfolio the market yield of 7.7% compares to a passing yield at full occupancy of 7.3%, suggesting 5% reversionary potential on average. Development portfolio: the key source of organic growth. The development property portfolio is composed chiefly of projects for commercial use. The company expects some of these initiatives to turn into income-generating assets and financial leverage is on the whole much lower than in the rest of the portfolio, at 20%. A number of the development initiatives centre around the Serravalle Scrivia “Designer Outlet”, although the key initiative is represented by a Eu300mn capex retail and entertainment project in Caselle (next to Turin airport). Real estate funds: a market for opportunistic acquisitions. Another pillar of the group’s strategy is the intention to look for acquisition opportunities among real estate funds (usually trading at a deep discount to face values) with the subsequent goal of assimilating them into the group’s real estate portfolio (a clear example of this strategy is the recent acquisition of the Redwood fund). This also comes on the back of some new options introduced by the Renzi government with the “Unblock Italy” decree, which addressed the situation of numerous real estate funds approaching maturity by trying to create new exit strategies for funds’ shareholders. Knowledgeable management boasting a major success story in retail real estate. CEO Giuseppe Roveda, through the Praga group, was responsible for the development of the Serravalle Designer Outlet in the early 2000’s. This innovative intervention involved the construction of the biggest outlet centre in Europe, and was a major success that radically enhanced the local area’s profile and economic status. Valuation at deep discount to Net Asset Value. Aedes SIIQ stock is currently trading at a 60% discount to 2016E NAV. Despite part of this discount could be related to the uncertainties over the group’s development projects (particularly the one in Caselle which is at a much earlier stage) as well as its sub-optimal cost base (which can be leveraged with a much larger portfolio), this still represents a significant gap vs the 30% average discount at which its main Italian peers Beni Stabili and IGD are trading, especially considering the lower LTV of Aedes SIIQ.

5

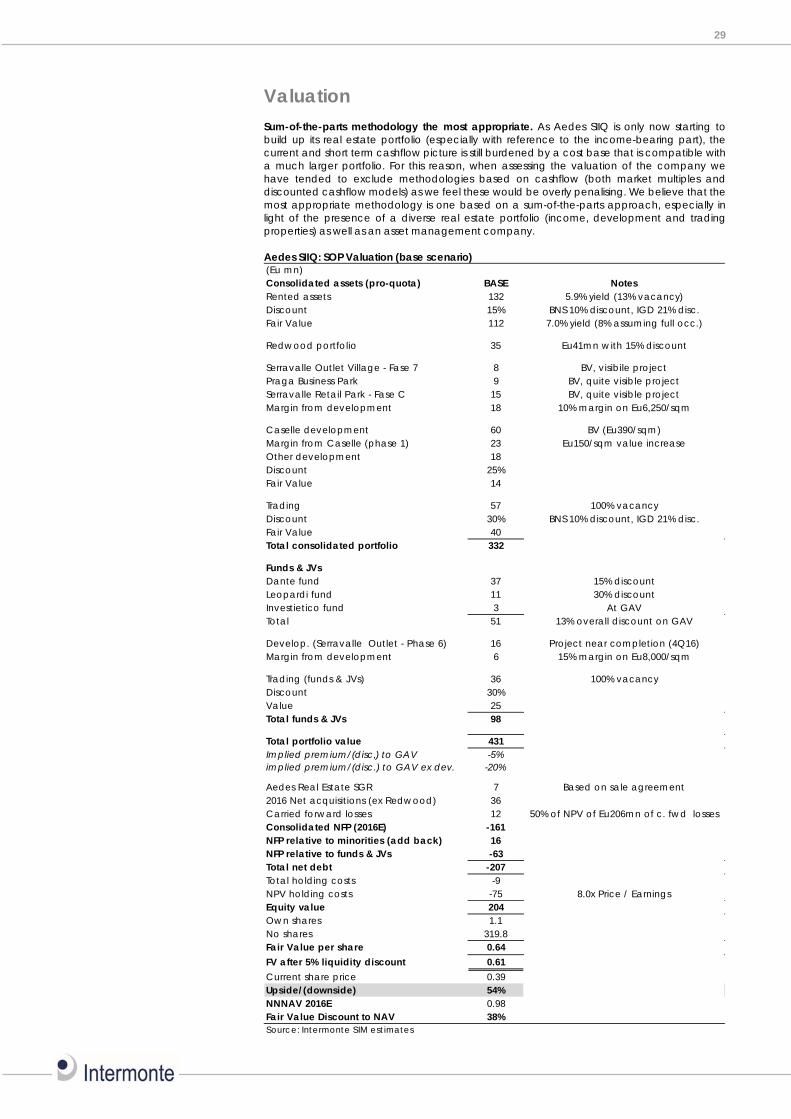

We initiate coverage with an Outperform recommendation and set a target price of Eu0.60ps (52% upside to current prices). As Aedes SIIQ is only now starting to build up its real estate portfolio (especially with reference to the income-bearing part), the current and short term cashflow picture is still burdened by a cost base that is compatible with a much larger portfolio. For this reason, when assessing the valuation of the company we have tended to exclude methodologies based on cashflow as we feel these would be overly penalising. We believe that the most appropriate methodology is one based on a sum-of-the-parts approach and we set a target price of Eu0.60 while also running a bear and a bull case scenario (with fair values, respectively, of Eu0.41 and Eu0.85). We start our coverage with an Outperform recommendation on the stock. Main weaknesses/risks. Despite the huge progress made by the company over the last couple of years, we highlight a number of key weaknesses and risks: Low WALT of the portfolio. The rented portfolio (included Redwood) has a weighted

average lease term (WALT) of just 2.6 years exposing it to potential further vacancy; Trading portfolio mostly vacant. Around 20% of GAV is represented by the trading

portfolio, a fairly diverse mix of mostly vacant assets which might be difficult to sell on the market;

Low cashflow generation. Due to the fact that the rented portfolio represents less

than 50% of total pro-quota GAV and that the cost base is consistent with that of a much larger asset base, cashflow generation currently remains negative, and will only show significant improvements in the next few years.

The Caselle project is not without risks: while there is very high visibility on execution

of the company’s development projects around the Serravalle Designer Outlet, the Caselle project represents a more uncertain bet, with a much higher risk/reward profile;

Sub-par dividend distribution: the low cashflow generation means that the group is

not currently distributing any dividends; it will probably take a few years for dividend yields to come close to sector averages;

Capital structure: despite the low initial LTV at the group level (35% at the pro-quota

level in 2015), the development of even the first phase of a large project such as Caselle might force the company to raise fresh resources.

6

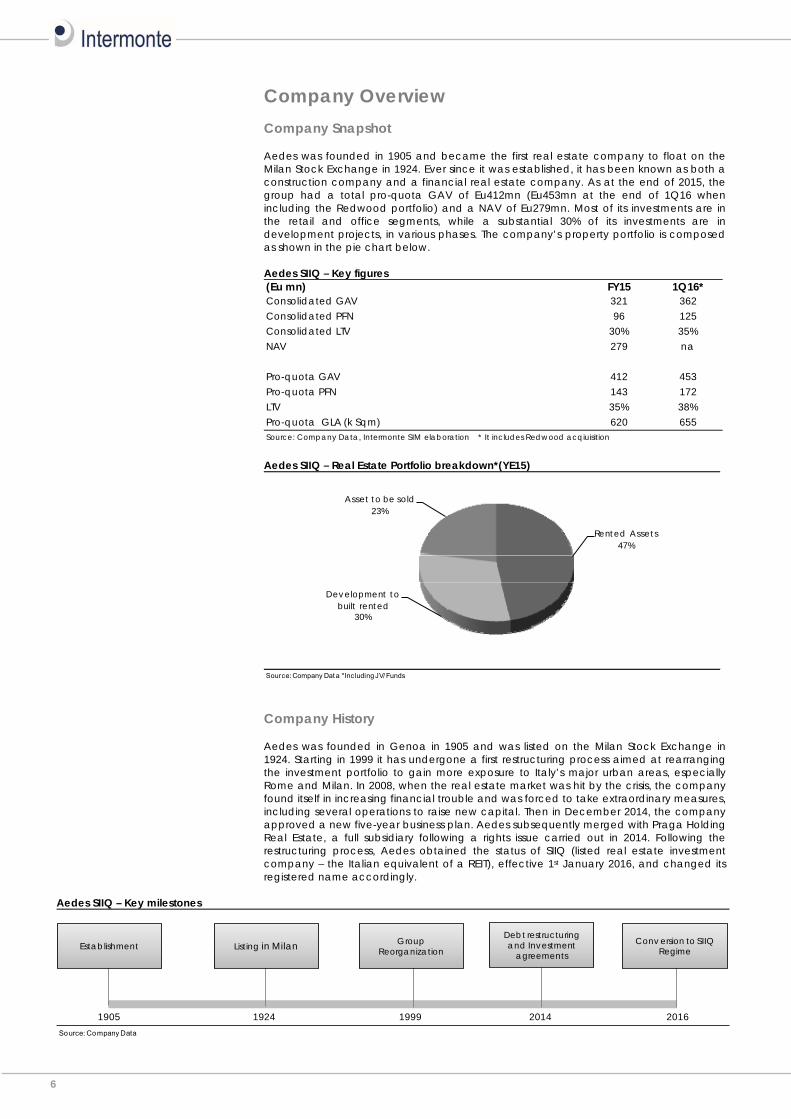

Company Overview Company Snapshot Aedes was founded in 1905 and became the first real estate company to float on the Milan Stock Exchange in 1924. Ever since it was established, it has been known as both a construction company and a financial real estate company. As at the end of 2015, the group had a total pro-quota GAV of Eu412mn (Eu453mn at the end of 1Q16 when including the Redwood portfolio) and a NAV of Eu279mn. Most of its investments are in the retail and office segments, while a substantial 30% of its investments are in development projects, in various phases. The company’s property portfolio is composed as shown in the pie chart below. Aedes SIIQ – Key figures (Eu mn) FY15 1Q16*Consolidated GAV 321 362Consolidated PFN 96 125Consolidated LTV 30% 35%NAV 279 na

Pro-quota GAV 412 453Pro-quota PFN 143 172LTV 35% 38%Pro-quota GLA (k Sqm) 620 655Source: Company Data, Intermonte SIM elaboration * It includes Redwood acqiuisition Aedes SIIQ – Real Estate Portfolio breakdown*(YE15)

Source: Company Dat a *Including JV/ Funds

Rented Assets47%

Development to built rented

30%

Asset to be sold23%

Company History Aedes was founded in Genoa in 1905 and was listed on the Milan Stock Exchange in 1924. Starting in 1999 it has undergone a first restructuring process aimed at rearranging the investment portfolio to gain more exposure to Italy’s major urban areas, especially Rome and Milan. In 2008, when the real estate market was hit by the crisis, the company found itself in increasing financial trouble and was forced to take extraordinary measures, including several operations to raise new capital. Then in December 2014, the company approved a new five-year business plan. Aedes subsequently merged with Praga Holding Real Estate, a full subsidiary following a rights issue carried out in 2014. Following the restructuring process, Aedes obtained the status of SIIQ (listed real estate investment company – the Italian equivalent of a REIT), effective 1st January 2016, and changed its registered name accordingly.

Aedes SIIQ – Key milestones

Source: Company Data

sssssssss2014 20161905 1924 eeeee 1999

Establishment Listing in Milan GroupReorganization

Debt restructuringand Investment

agreementsConv ersion to SIIQ

Regime

7

The 2014-2015 restructuring process… In 2013, in the wake of the financial crisis, Aedes found itself in an extremely critical financial condition, with equity of just Eu28mn against a net debt of Eu430mn. In the 2014-2015 the group embarked upon a long, in-depth restructuring process involving an investment agreement that encompassed various share issues and a debt restructuring agreement. Below is a brief summary of this process, which led to the creation of the current capital and corporate governance structures. Debt restructuring agreement. Aedes signed an agreement that restructured its debt exposure to creditor banks. Specifically, the agreement stipulated. 1. The sale of property and investments in companies owning property to one of the

creditor banks in exchange for a Eu167mn reduction in the bank debt. 2. Assumption by Aedes of all of the group’s unsecured credit, comprised of two

mortgages and Eu92mn of debt relating to group companies. 3. Transfer to a real estate fund (fondo Leopardi), managed by Aedes SGR, of property

and stakes in real estate companies that do not fit in with the new real estate strategy. The assets transferred have a NAV of Eu54.6mn. The majority of the stakes in these property funds were transferred to creditor banks, in exchange for the cancellation of Eu41mn in debt.

4. Eu47.5mn cash rights issue, without option rights, reserved for Aedes’s creditor banks to be paid through the conversion of the outstanding loans receivable from the group.

5. Aedes released from the guarantees it provided. Investment agreement. In conjunction with the restructuring agreement, Aedes signed a further agreement in order to grant the group the necessary resources to complete its restructuring. Specifically, this agreement involved: 1. Eu40mn share issue (at Eu0.46ps), without option rights, reserved for a NewCo

(Augusto SpA) owned by Tiepolo, Prarosa, Agarpa and SATOR. Augusto subscribed to this rights issue using the proceeds from its own rights issue, which in turn was subscribed by Sator and Tiepolo for Eu20mn each.

2. Eu92mn share issue (at Eu0.805ps) with payment in kind, without option rights, reserved for Augusto to be paid through the transfer of the entire capital of Praga Holding Real Estate. This share issue was subscribed by Augusto through the transfer by Tiepolo, Prarosa, Agarp, Praviola and Itinera of the entire share capital of Praga Holding Real Estate.

3. Eu49mn share issue (Eu2.30ps) with payment in kind, without option rights, reserved to the group’s banking creditors, paid through the conversion of the outstanding loans issued to Aedes.

4. Eu40mn cash rights issue (Eu0.46ps) with options for Aedes shareholders, who were awarded Warrants. Eu20mn of this issue was underwritten by Augusto shareholders and ViBa, an Aedes shareholder.

5. Eu20mn share issue (strike Eu0.69ps, maturity 07/07/2020) to serve the Warrants, with a ratio of 1 newly issued share for every 3 Warrants (max 28,985,512 shares).

… and the new ownership structure Ownership. Following the restructuring that was launched in 2014, Aedes now has a solid majority owner in Augusto SpA with over 51.2% of the share capital; Augusto is followed by ViBa with 7.3% and Itinera with 5.6%. The remaining 36% or so of the share capital is free float. Along with the rights issues, the company also issued about 87mn warrants that expire in 2020; if all of these are exercised (at one new share for every three warrants), then about 29mn new shares would be issued (ca. 9% of the NOSH). The warrants may be exercised at any time, at a strike price of Eu0.69. Aedes SIIQ – Shareholders Structure

Source: Company data

Aedes ownership Augusto ownership

Tiepolo37%

Prarosa31%

Arepo AD30%

Agarp2%August

o51.20%

ViBa7.31%

Itinera5.30%

Market36.02%

8

Here is a brief description of the group’s main shareholders: Augusto. Aedes’s leading stakeholder with 51.2%, Augusto is governed by a

shareholders’ agreement between its four stakeholders, Arepo AD (Arpe’s Sator Fund), Tiepolo (Amenduni family, noted for its steel manufacturing business), Prarosa and Agarp (both controlled by Aedes CEO Mr. Roveda). Augusto has three classes of shares (A, B and C), assigned to Prarosa, Tiepolo and Arepo AD, respectively. Arepo AD is in turn owned by Luxembourg-based fund Sator, owned by notable Italian businessman Matteo Arpe. Major corporate decisions concerning Augusto or Aedes must be approved by a majority of every share class, effectively giving each of the leading stakeholders veto power. Furthermore, the stakeholders partaking in the agreement cannot sell Augusto shares before 2019. In that year, each stakeholder will be allowed to remove its stake from the agreement and/or sell shares. Because of this setup, no single stakeholder has control of either Augusto or, consequently, of Aedes.

ViBa. A company belonging to the Amenduni family’s industrial group. The Amenduni

family is noted for its steel manufacturing business. Itinera. A company of the ASTM motorway/construction group, Itinera is indirectly

controlled by the Gavio family and does construction business in major works projects. Aedes SIIQ – Ownership Chain

Source: Company Data

Sator

Arepo AD PrarosaTiepolo

Augusto

100%*

37.5%30.6%30.1%

Agarp

1.86%

AEDES

51.2%

Shareholder agreement

Amenduni Family

Mr. Roveda

ViBa (Amenduni It inera (Gavio Family)

5.3%7.31%

Management and governance Management Team The current management team oversaw the restructuring and is now committed to turning the company around. Here are brief profiles of the top executives: Carlo Puri Negri, Chairman. Mr. Puri Negri has been Chairman of both Aedes and its

top stakeholder Augusto since December 2014. He has held upper management positions in various Italian manufacturing and financial companies over the course of his career since 2002, and held various roles in the Pirelli group for 21 years starting in 1988. He is also a member of Harvard University’s International Real Estate Advisory Board.

Giuseppe Roveda, CEO. Roveda has been Aedes’s chief executive since April 2012.

He is also CEO of both Augusto and its leading stakeholder Prarosa. From 2000 to 2014, Roveda was CEO of Praga Holding Real Estate SpA, which was controlling stakeholder in 12 different real estate investment companies, two construction services management companies and two agriculture companies.

9

Gabriele Cerminara, CFO. Chief financial officer Cerminara also manages the group’s equity interests. He is on the boards of several companies within the group and on the advisory committees of real estate funds in which Aedes SIIQ owns stakes. In the past, he gained experience in the telecommunications sector, in the corporate finance department of banks and in auditing for financial companies.

Conflicts of interest. The Aedes group has adopted a procedure for carrying out transactions with associated parties. The key point of the procedure is that prior approval must be given by the Board of Directors for any transactions with associated parties. The definition of associated parties includes all members of the Board of Directors, as well as members of the Board of Statutory Auditors and executives with strategic roles. It also includes all controlling shareholders, both on an individual and combined basis, and those with a stake large enough to allow them to exercise significant influence on the company. Transactions that are relevant for this procedure are broken down into those of lesser and greater magnitude. Normal procedures are applied for smaller transactions that fall under the former case, whereas for the latter case special procedures are used to guarantee that they comply with rules governing transactions with associated parties. According to the rules set by Italian authorities, significant transactions with associated parties are those for which any of the following indices exceeds 5%: Countervalue index; the ratio between the countervalue of the transaction and the

overall shareholders’ equity booked in the most recently filed financial statements. Asset index; the ratio between the total assets of the object of the transaction and

the total assets of the company on the most recently published balance sheet; Liability index; the ratio between the total liabilities of the object of the acquired

entity and the total liabilities of the company on the most recently published balance sheet.

Other transactions that fall under this definition are those with a listed holding company or with associated parties for which any of these indices exceeds 2.5%. The company also plans to introduce an internal audit committee to monitor transactions with associated parties, to be populated by independent Directors. No committee members can have any connection to the transactions scrutinised. If any connection exists, the member in question must be replaced by other independent members without a connection to the transaction Group Strategy Towards a traditional REIT business model in the medium term. Aedes’s strategy is focused on the creation and medium to long term retention of an income-bearing portfolio of commercial property, predominantly in the retail arena, with limited recourse to debt. The portfolio should allow the generation of significant cashflow under the SIIQ model. Aedes is building for the future by further investing in two portfolios, one income-bearing and the other a development portfolio which it already owns. On the one hand it will purchase new rented properties to compete with the performance of European REITs, while on the other it will develop a new generation of shopping and leisure centres through a development pipeline, with the aim of eventually transferring them to the income-bearing portfolio controlled by Aedes SIIQ (hence benefiting from the corporate tax exemption of the SIIQ regime, see Appendix for details).

Aedes SIIQ – Real estate portfolio*: breakdown by use

Source: Company Data *Including JV/Funds

YE'15 YE'19

Assets to be sold5%

Dev elopment Assets25%Rented Assets

70%

Assets to be sold23%

Dev elopment Assets30%

Rented Assets47%

Please note that at the EGM, the shareholders of Aedes SIIQ approved through a majority vote to change Article 21 of the company’s articles of association by creating a statutory reserve to which a portion of annual net earnings (about 3%) will be allocated; the goal

10

of this reserve is to cover annual debt repayments/amortisations and to support the group’s development and growth. This change gives rise to withdrawal rights for shareholders that did not vote in favour of it. Those exercising their rights will have their shares repurchased at a price equivalent to the average for the previous six months, which currently stands at Eu0.43 per share. The new reserve will be created if and only if the amount of withdrawals exercised does not exceed Eu2mn. The company’s property portfolio target beyond the 2019 business plan horizon is for around 80% of its properties to be income-bearing. The latest indications from the company (which are expected to be updated soon) suggest that the group aims to reach a total value for its portfolio of around Eu1.0bn. Aedes plans to do this through: 1) an investment of about Eu200mn in new development projects, which should add about Eu100mn to the portfolio value; 2) the turnover of around Eu150mn worth of assets currently in its portfolio; 3) further re-leverage, bringing LTV to 60%, and thus raising the value of its managed real estate assets to about Eu1bn. The company has nevertheless announced that it intends to provide a business plan update by the end of 3Q16, so the chart below only represents a broad indication of the potential development of the portfolio.

Aedes SIIQ – Expected asset portfolio value trend (Eu mn)

Source: Company Data

426

200 -150 150100

700

300

1000

0

200

400

600

800

1,000

1,200

PortfolioYE'15

Capex Sales Purchase FvAdjusted

PortfolioYE'19E

Releverage Portfoliotarget

LTV 60%

LTV 40%

The table below also shows the key targets from the latest business plan. Once again, it is important to stress that management is working on an update to the plan and some of the targets could therefore be amended (especially EBIT), partly due to the revised timing of development projects (the potential gains from the Caselle project, for example, may well shift by a couple of years).

Aedes SIIQ – Latest business plan targets (to be updated)

(Eu mn) BP Actual BP Intermonte BP Intermonte BP Intermonte BP Intermonte

Ebit 10-12 10 40-45 23 40-45 7 75-80 26 75-80 55

Equity 250-280 275 280-310 313 300-330 314 350-380 330 410-440 369Source: Company data .

2019E2015A 2016E 2017E 2018E

Internally managed group, services only internally focused. Aedes also provides asset management, administration and financing services to companies within the group. Still, it’s important to stress that going forward Aedes SIIQ only wants to focus on property investments, and that services will purely be a tool used to enhance the value of its own real estate portfolio. The companies it offers these services to are: Praga Real Estate: a property services company that is mainly involved in organising

and developing master plans and project management. It also draws up and monitors subsidised building projects, coordinates and implements building permits, oversees commercial authorisation processes and environmental impact assessments, and carries out technical and facilities management.

Praga Construction. This subsidiary predominantly carries out general contracting

services, almost exclusively for other group companies. Aedes Real Estate SGR. The company specialises in the foundation, development and

management of closed-end mutual real estate investment funds, both for the retail market and reserved for qualified investors. As at YE15 the SGR managed four real estate funds (Investietico, Dante Retail, Petrarca and Leopardi), whose combined net asset value was Eu451mn, down Eu41mn from the end of 2014 due to reduced market values of some properties held by those funds. On 11th May, Aedes SIIQ announced that it has signed a contract with Sator Immobiliare SGR for the sale of all the shares held by the former in Aedes Real Estate SGR (95% of the capital). The sale of the fund management business, foreseen in the 2014-19 business plan, is a further

11

step towards the property company model that the Aedes Group adopted when it signed up to the SIIQ regime, which allows the direct management of proprietary assets but not fund management on behalf of third parties. The company should bring in around Eu7.0mn for 95% of the SGR, net of value of the units in the Investietico fund owned by the SGR itself. The contract also stipulates that Aedes receive a preliminary distribution of items of the SGR’s shareholders’ equity amounting to Eu5.5mn, therefore bringing the price of the deal to Eu1.5mn. Moreover, Aedes will receive all of the proceeds from the liquidation of the Investietico fund for an estimated pro-quota value of around Eu2.5mn (Eu2.6mn for all of the units owned by the SGR). Please note that the asset management firm closed 2015 with net income of Eu1.3mn.

Real estate funds: taking advantage of the “Unblock Italy” decree. The acquisition of real estate funds – subsequently to be incorporated in the group’s real estate portfolio - is part of the Aedes group’s SIIQ strategy. It comes on the back of some new options introduced by the Renzi government with the “Unblock Italy” decree, which addressed the issue of real estate funds coming to maturity by trying to create new exit strategies for funds’ shareholders. In summary, the government introduced the two following options:

Listed funds. For listed funds it is possible to transfer units in exchange for shares in the SIIQ,

with exemption from stamp duty / land registry tax at the time of transfer. Moreover, the transfer is not considered to be an act that realises the potential capital gains encapsulated in the fund.

Institutional funds. For these type of funds there is also the possibility to liquidate the shares

of the funds in kind, i.e. by keeping hold of the real estate assets (this is what Aedes is doing with the recently acquired Redwood fund).

12

Portfolio description and statistics RE portfolio: concentrated in northern Italy yet well diversified Aedes’s real estate portfolio at the end of 2015. As at the end of 2015, following the comprehensive restructuring implemented over the last couple of years, Aedes SIIQ boosts a real estate portfolio concentrated in northern Italy, mostly in the regions of Lombardy and Piedmont. In terms of use classes, the portfolio is well diversified. When sizing up how big this portfolio is, it is important to stress that the group reports three different types of figures: 1) the value of the “consolidated” portfolio, which is the number reported on the balance sheet), 2) the “pro-quota” value of the consolidated portfolio, or the balance sheet number minus the portion pertaining to minorities, and 3) the total pro-quota portfolio value, or the pro-quota consolidated value plus the value of Aedes’s stakes in other funds and joint ventures. Key data for the company’s portfolio are as follows: Consolidated portfolio. At the end of 2015 Aedes SIIQ had a consolidated portfolio

GAV of Eu321mn and a NAV of Eu169mn (47.4% LTV). This represents the balance sheet figure and includes all proprietary assets as well as the real estate fund in which Aedes has a controlling stake (the Petrarca fund, in which Aedes owns 65%). When excluding minorities, GAV comes to Eu298mn and NAV Eu162mn, for an LTV ratio of 45.6%.

Total portfolio including JVs and stakes in funds. The group also has a number of

equity interests of 50% or less in other real estate funds and joint ventures. Overall, at the end of 2015 these funds and JVs had a pro-quota GAV of Eu114mn and a NAV of Eu51mn (45% LTV). When adding these to the consolidated assets, Aedes’s total pro-quota portfolio reaches a GAV of Eu412mn and a NAV of Eu214mn (48.2% LTV). The funds are Dante (33% stake, focused on the retail segment in north-central Italy), Leopardi (24.4% stake, retail and office segments in northern and southern Italy), and Investietico (1.9% stake, care homes and office properties). The JV holds assets relating to “phase 6” of the Serravalle Outlet project.

Three main clusters. The company divides its portfolio into three clusters, as follows: Rented assets. at the end of 2015 this portion consisted of 9 consolidated properties

with a GAV of Eu131.5mn and a NAV of Eu54.6mn, although when including funds and JVs the total respective values came to Eu193.5mn (47% of the total) and Eu78.2mn (37% of the total). This is the cash-generating part of the portfolio, and according to the business plan, the company is aiming to increase the weight of this cluster to 80%.

Development assets. Most of these are consolidated assets and represent the

company’s “internal” growth driver. These assets are fully concentrated in the Piedmont region and as at the end of 2015 the total pro-quota GAV was Eu126mn (30% of the total portfolio value) and NAV was Eu100mn (47% of the total).

Aedes SIIQ Portfolio (YE15): breakdown by cluster

Source: Aedes SIIQ, Intermonte SIM elaboration

Total Rented Portfolio

44%Total

Development Assets37%

Total Trading

19%

Consolidated (pro-quota)

Total Rented Portfolio

47%

Total Develop

ment Assets30%

Total Trading

23%

Total (pro-quota)

Aedes SIIQ Portfolio (YE15): breakdown by use

Source: Aedes SIIQ, Intermonte SIM elaboration

Total Retail47%

Total Office33%

Total Other20%

Consolidated (pro-quota)

Total Retail52%Total

Office24%

Total Other24%

Total (pro-quota)

13

A

edes

SIIQ

: Con

solid

ated

por

tfolio

(FY2

015)

(Eu

mn)

GA

VN

AV

GA

V %

of

Tota

lLT

VG

LA (s

qm)

Valu

e (E

u/sq

m)

Pass

ing

Yiel

dM

arke

t Yi

eld

Rent

Rent

/sqm

Occ

up.

Reta

il Re

nted

31.2

17.2

10%

45.0

%17

,048

1,83

07.

1%7.

1%2,

221

130

-O

ffice

Ren

ted

99.1

37.1

33%

62.6

%50

,934

1,94

65.

5%6.

3%5,

486

175

-O

ther

Ren

ted

1.2

0.4

0%66

.7%

1,50

679

77.

5%9.

2%90

60-

Tota

l Ren

ted

Portf

olio

131.

554

.644

%58

.5%

69,4

881,

892

5.9%

6.5%

7,79

715

686

.9%

Reta

il d

evel

op

men

t10

9.1

83.8

37%

23.3

%O

ffice

dev

elo

pmen

t0.

70.

70%

0.0%

Oth

er d

evel

op

men

t0.

00.

0na

naTo

tal D

evel

opm

ent A

sset

s10

9.8

84.4

37%

23.1

%

Tra

ding

Ren

ted

30.8

13.0

10%

57.9

%Tr

adi

ng L

and

26.3

10.3

9%60

.9%

Tota

l Tra

ding

57.1

23.2

19%

59.3

%To

tal (

pro-

quot

a)29

8.4

162.

310

0%45

.6%

Tota

l Re

tail

140.

310

0.9

47%

28.1

%To

tal O

ffice

99.8

37.7

33%

62.2

%To

tal O

the

r58

.323

.620

%59

.4%

Min

orit

ies

22.9

6.8

Tota

l (in

clud

ing

min

oriti

es)

321.

316

9.1

47.4

%

Sour

ce: C

ompa

ny d

ata,

Inte

rmon

te S

IM e

labo

ratio

n

Aed

es S

IIQ: T

otal

por

tfolio

"pro

-quo

ta" i

nclu

ding

fund

s &

JV (F

Y201

5)

(Eu

mn)

Fund

s &

JV

GA

Vas

% o

f fu

nds

& JV

as %

of

tota

l GA

VFu

nds

& JV

N

AV

Tota

l GA

V Pr

o-qu

ota

% o

f to

tal

Tota

l NA

V Pr

o-qu

ota

% o

f to

tal

Tota

l LTV

GLA

(sqm

)Va

lue

(Eu/

sqm

)Pa

ssin

g Yi

eld

Mar

ket

Yiel

dRe

ntRe

nt/s

qmO

ccup

ancy

Reta

il Re

nted

56.5

50%

14%

20.0

87.7

37.1

57.7

%56

,481

1,55

36.

8%7.

8%6,

006

119

-O

ffice

Ren

ted

1.6

1%0%

1.2

100.

738

.262

.0%

52,3

131,

924

6.4%

7.6%

6,42

219

7-

Oth

er R

ente

d3.

93%

1%2.

55.

12.

944

.0%

4,30

31,

185

6.4%

8.0%

329

80-

Tota

l Ren

ted

Portf

olio

62.0

54%

15%

23.6

193.

546

.9%

78.2

36.6

%59

.6%

113,

097

1,71

16.

6%7.

7%12

,757

147

90.5

%

Reta

il d

evel

op

men

t16

.014

%4%

16.0

125.

199

.720

.3%

Offi

ce d

evel

opm

ent

0.0

0%0%

0.0

0.7

0.7

0.0%

Oth

er d

evel

op

men

t0.

00%

0%0.

00.

00.

0na

Tota

l Dev

elop

men

t Ass

ets

16.0

14%

4%16

.012

5.8

30.5

%10

0.4

47.0

%20

.2%

288,

337

436

Tra

ding

Ren

ted

15.6

14%

4%10

.246

.423

.250

.1%

33,7

311,

376

Tra

ding

La

nd20

.418

%5%

1.6

46.7

11.9

74.6

%21

8,97

521

3To

tal T

radi

ng36

.032

%9%

11.8

93.1

22.6

%35

.016

.4%

62.4

%25

2,70

636

9To

tal

114.

010

0%28

%51

.441

2.4

213.

748

.2%

654,

140

630

Tota

l Re

tail

72.5

36.0

212.

951

.6%

136.

935

.7%

344,

818

617

Tota

l Offi

ce1.

61.

210

1.3

24.6

%38

.961

.6%

52,3

131,

937

Tota

l Oth

er

39.9

14.3

98.2

23.8

%37

.961

.4%

257,

009

382

Sour

ce: C

ompa

ny d

ata,

Inte

rmon

te S

IM e

labo

ratio

n

14

Trading assets. This is the smallest cluster, composed of properties that the company intends to sell in the near term . The YE 2015 GAV (total pro-quota) of this cluster was Eu93mn (23% of the total) and its NAV was Eu35mn (16% of the total).

Property classes by use. To analyse the portfolio’s assets based on their use, we can categorise them as follows: Retail properties. This is the largest category, accounting for some 50% of the total

both on a consolidated basis and also when adding in funds and joint ventures. The retail assets included in the rented portfolio are scattered throughout Italy and are mostly shops and medium-sized shopping centers. Among the largest assets are a building in Catania and one near Alba (Piedmont). However, the biggest retail assets are actually in the development portfolio: the Serravalle Outlet extension project and land in Caselle.

Office properties. This category represents some 33% of consolidated assets and 24%

of the total “pro-quota” portfolio. Virtually all of these assets are included in the rented portfolio and all of the major ones are located in or around Milan.

Other assets. These are all the properties in the company’s trading portfolio plus those

that cannot be categorised as either retail or office (mainly residential and healthcare properties). Among the largest assets in this class are: 1) a residential property in Milan; 2) a development area in Via Rubattino, Milan; 3) a retail property in Serravalle Scrivia; 4) a property in Cannes (France) that is in the process of being sold.

Geographical breakdown. From a geographical standpoint the portfolio is heavily concentrated in the richest regions of norther Italy. In particular, Piedmont and Lombardy are the two key regions where over 80% of Aedes’s total pro-forma assets are located. The city that stands out most in the company’s portfolio is Milan, with almost 30% of the total asset value concentrated there. Other key locations are Serravalle and Caselle, both in the north-west region of Piedmont. Aedes SIIQ (YE15): Geographical portfolio breakdown (pro-forma including JVs and funds)

Source: Aedes SIIQ, Intermonte SIM elaboration

Lombardia

38%Piedmont

44%

Sicily5%

Other13%

Milano28%

Serravalle (Alessand

ria)20%

Caselle (Turin)15%

Other37%

Main tenants. The portfolio is also relatively well diversified in terms of tenants, with the largest (information provider and rating agency Cerved) accounting for 22% of total rents and the top five tenants accounting for about 73% of total rents. Besides Cerved, other key tenants include companies such as COIN/Oviesse, NCTM Lawers, BP Property Management, and GS/Esselunga. Aedes SIIQ: Weight of main tenants (YE15), excluding development projects)

Source: Company data, Intermonte SIM elaboration

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Cerved COIN/Oviesse NCTMLawyers

BP PropertyMgmt

GS/Esselunga Other

Lease expiry profile. The lease expiry profile is relatively short as the weighted average lease term (WALT) stands at just 2.6 years (this includes the Redwood portfolio acquired in 1Q16 which has a WALT of about 3 years). Around 50% of total rents are potentially expiring within

15

three years, based on the first potential break-off point, with another 28% in 2019 and the remaining 24% after that. Aedes SIIQ: Average WAULT: 2.6 years* (first expiry)

Source: Company data, Intermonte SIM elaboration * Inc. Redwood

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

2016 2017 2018 2019 after

Income-bearing portfolio: room to work on vacancy rates …. While on the one hand rents have largely stabilised, on the other hand there is potential to improve vacancy rates, which stand at 13% for the fully consolidated portfolio. These vacancies are mostly concentrated in two assets that form part of the Petrarca fund: 1) an office building in Cinisello Balsamo (Milan) with a 92% vacancy rate and a fair value of Eu14.5mn (100%) or just Eu550/m2 (which should make it relatively easy to find new tenants); 2) an office building (the Colleoni office centre) in Agrate Brianza (Monza) with a vacancy rate of 48% and a fair value of Eu18.5mn (100%). … although reversionary potential is limited. There is limited reversionary potential in Aedes’s SIIQ portfolio. Specifically, when looking at the fully consolidated part of the income-bearing portfolio there is slight negative reversionary potential as the 6.5% market yield is lower than the passing yield at full occupancy (6.8%, considering that the vacancy rate stands at 13%). The situation improves slightly when looking at the entire pro-quota portfolio: here the market yield of 7.7% compares to a passing yield at full occupancy of 7.3% suggesting an average 5% reversionary potential. Real estate funds and joint ventures. As mentioned earlier, Aedes’s real estate portfolio contains not just directly owned properties, but also numerous properties held indirectly through stakes in real estate funds. As at 31st December 2015, the company was manager of four different real estate funds, one created for public sector savings and three reserved for qualified institutional investors. Petrarca (fully consolidated): founded in November 2006, this fund specialises in the office

segment and has five residual properties and Eu61.3mn in total assets. Aedes’s stake in Petrarca is 65%, so its pro-quota GAV was Eu38mn at the end of 2015 and its pro-quota NAV was Eu10mn. The other two investors in the fund are IVG Logistic Holding and IMF Italy Office Fund (both German).

Aedes SIIQ: Non-consolidated funds and joint ventures

(Eu mn)Funds & JV

GAVas % of

funds & JVas % of

total GAVFunds & JV

NAVLTV Total GAV

Pro-quota

Retail Rented 56.5 50% 14% 20.0 65% 87.7Office Rented 1.6 1% 0% 1.2 25% 100.7Other Rented 3.9 3% 1% 2.5 37% 5.1Total Rented Portfolio 62.0 54% 15% 23.6 62% 193.5

Retail development 16.0 14% 4% 16.0 0% 125.1Office development 0.0 0% 0% 0.0 0.7Other development 0.0 0% 0% 0.0 0.0Total Development Assets 16.0 14% 4% 16.0 0% 125.8

Trading Rented 15.6 14% 4% 10.2 35% 46.4Trading Land 20.4 18% 5% 1.6 92% 46.7Total Trading 36.0 32% 9% 11.8 67% 93.1Total 114.0 100% 28% 51.4 55% 412.4

Total Retail 72.5 36.0 212.9Total Office 1.6 1.2 101.3Total Other 39.9 14.3 98.2

Source: Company data, Intermonte SIM elaboration Dante Retail (equity participation): established in July 2005, this fund focuses on the retail

segment. Its tenants include supermarket chains Carrefour (ex Billa) and Esselunga. The

16

residual portfolio contains 22 properties (full occupancy) with a total asset value of about Eu140.5mn. Aedes owns 33.33% of this fund through the vehicle Efir S.à r.l. At the end of 2015, the pro-quota GAV was Eu43.5mn while the pro-quota NAV was Eu18.5mn. Two French institutional investors, Caisse Depots et Consignations and the pension fund UMR, own equal stakes to Aedes (also invested through Efir S.à r.l.), while the fund, which matures in 2022, is managed by Aedes SGR.

Leopardi (equity participation): this fund is effectively the distressed assets fund carved out

of Aedes’s old portfolio in the debt restructuring and recapitalisation process (please note that assets were transferred to the fund only after their fair values were adjusted to market prices). This fund has diversified investments in the residential, tertiary, hotel, industrial and commercial segments of the real estate market, as well as in land earmarked for development. As at 31st December 2015, Leopardi owned 20 buildings or portions of buildings plus majority stakes in companies that owned real estate. The fund’s total asset value was about Eu73.9mn, while the total value of all properties held directly or indirectly was Eu172.8mn. Aedes owns 24.4% of the fund’s quotas, so its pro-quota GAV was Eu15.6mn at the end of 2015 and its pro-quota NAV was Eu3mn (or Eu10.7mn including non-consolidated equity stakes). Leopardi’s other stakeholders are A, B and C. The fund is managed by Aedes SGR and it matures in 2022.

Investietico (equity participation): this is a fund listed on the Italian Stock Exchange that

invests mainly in healthcare facilities and offices. Its residual portfolio consisted in 11 buildings and a total asset value of Eu174.8mn. Aedes owns 2% of the fund through Aedes Real Estate SGR. At the end of 2015, the pro-quota GAV was Eu2.9mn and pro-quota NAV was Eu2.2mn. The fund is managed by Aedes SGR and it matures in 2018.

2016 acquisitions: the Redwood portfolio. In March 2016 Aedes SIIQ purchased 100% of the Redwood real estate fund. The acquisition went through in two stages: 1) the purchase of 70% of the fund at a price of Eu16.4mn; 2) the acquisition of financial receivables which had the remaining 30% of the fund as collateral for Eu13.6mn. The upshot of these two deals was that Aedes SIIQ took ownership of 100% of the units in the fund for a total price of Eu30mn, of which Eu25mn for the real estate and trading licences and Eu5mn for the cash position. Based on existing rental contracts (Eu3.6mn), the overall price corresponded to a gross entry yield of 15%. The fund owns 18 retail properties located in various parts of Italy (Unieuro, Metro, etc.) and 9 trading licences held through Redwood S.r.l., a vehicle company controlled in its entirety by the fund itself. The portfolio has a weighted average lease term of three years or slightly higher than the rest of the portfolio.

Redwood portfolio: Key data

City Region GLA (sqm)Avg. Purchase Price (Eu mn)

FV/Sqm (Eu)

OccupancyRent

(Eu mn)Rent/Sqm

(Eu) *Yield

Lamezia Terme (CZ) Calabria 2,814La Spezia Liguria 3,514Brescia Lombardia 1,869Brescia Lombardia 3,460

Rosà (VI) Veneto 2,870Roma Lazio 4,075

Tavagnacco (UD) Friuli-Venezia G. 4,200Trezzano S.N. (MI) Lombardia 10,380

S. Giovanni Teatino (CH) Abruzzo 3,015Castagnito (Cn) Piemonte 3,000

Genola (CN) Piemonte 3,100Genola (CN) Piemonte 2,202Saluzzo (CN) Piemonte 1,914

Castagnito (Cn) Piemonte 1,075Caleppio di Settala (MI) Lombardia 1,950

Bra (CN) Piemonte 1,637Acqui Terme (AL) Piemonte 790

Bassano del Grappa Veneto 4,464

Total 56,329 25 444 73.7% 3.6 87 14.4%Source: Company data, Intermonte SIM elabotation * Rent/sqm calculated on rented space

17

Development portfolio: the organic growth option The development property portfolio is composed chiefly of projects for commercial use. The company expects some of these initiatives to turn into income-generating assets. Financial leverage is on the whole much lower than in the rest of the portfolio, at 20.2%. New financing deals are expected to be reached for the key initiatives in order to ensure that the construction costs can be sustained. Serravalle Designer Outlet: a success story. A number of Aedes’s development initiatives centre around the Serravalle Scrivia “Designer Outlet”. The Serravalle Designer Outlet is the largest outlet in Europe. It was opened in 2001 and managed by UK company McArthur Glen, which together with Giuseppe Roveda’s Praga group subsequently developed the complex, opening the Serravalle Retail Park and the Serravalle shopping centre. Indeed, the project was the first building block in the major requalification of the local area between Serravalle Scrivia and Novi Ligure, a process that continues to this day with other major construction works in progress. The Designer Outlet now covers a total of 45,000m2, and hosts more than 180 stores selling over 300 designer brands. It offers a unique shopping experience to over 4mn annual visitors thanks to the modern services connected to the on-site commercial activities. It is located around one hour from Milan and an hour and a half from Genoa, in Serravalle Scrivia (AL), Piedmont, and can be easily reached from both these cities and Turin, as it has its own junction on the A7 Milan-Genoa motorway and is on the Turin-Genoa railway line. Serravalle Outlet Village – Phase 6 (Pragasei S.r.l.). On 9th June 2015, Aedes Group formed a strategic partnership with major global investment company TH Real Estate and McArthur Glen, a company that runs 20 designer outlets in Europe, five of which in Italy, to begin the executive phase of development at Serravalle Outlet Village. On land owned by Pragasei S.r.l. (50.1% owned by Aedes), 10,577m2 of commercial space will be built. Funding for this project is fully ensured by the cash TH Real Estate is to transfer once works reach an advanced stage, while Aedes’s portion of the funding was allocated when the partnership was established. The residual cost will be covered by a mid/long term loan to be disbursed by Credit Agricole.

Development for rents assets: Serravalle Outlet and Retail Park

Source: Company data * Of which Praga Business Praga total GLA 4,361 sqm

The letting process began in June 2015 and agreements have already been reached to let about 61% of the commercial space, while negotiations are in a final phase for a further 18%. Rents already agreed amount to about Eu630 per square metre plus a variable fee based on revenue. These preliminary agreements will be converted into full leases soon before the shopping centre opens, in accordance with standard market practice. Based on the construction progress made so far, the company estimates that Phase 6 of Serravalle Outlet Village will be inaugurated in late September or early October this year. Serravalle Designer Outlet – Phase 5. Parallel to Phase 6, Phase 5 of the Serravalle Designer Outlet also got underway. In this project, about 2,800m2 of commercial space will be built on proprietary land that belongs to the company that owns Serravalle Outlet, a business partner of Aedes in Pragasei S.r.l. The business agreement between Aedes and TH Real

18

Estate to expand the Serravalle shopping centre foresees increasing the total number of stores to 260 and total retail space to 51,500 square metres. Once the investments have been made, Serravalle will solidify its standing as the biggest luxury outlet in Europe and one of the top fashion destinations on the continent. Serravalle Outlet Village – Phase 7. This represents an extension of Serravalle outlet village Phase 6 and covers an area of around 10,000 sqm of which 50% owned by a subsidiary of Aedes SIIQ. The development plan has been approved and the environmental screening was completed with favourable outcome. The application for full planning permission has been presented. Serravalle Outlet and Caselle geographical position

Source: Intermonte SIM elaboration Caselle Torinese. This project is being put forward by Satac, a SIINQ of Aedes SIIQ. About Eu300mn will be required to build this shopping centre near the Turin airport; it will include a food court, sport facilities (a gym and other establishments), entertainment (a cinema, bowling alley, an adventure land, etc), as well as fashion and design retailers. Road access to the area will be completely overhauled, including a connection between the airport and the shopping village. Management expects to split the project into three phases. Works on phase one are scheduled to start in 2017 (with the site to open at the beginning of 2019) and will relate to around 50k sqm and account for some 40% of the overall investment (i.e. around Eu120mn). JL Lasalle has won the contract for the sale of retail spaces while Aedes is having discussions with two entertainment sector leaders (one of them would run the project’s leisure anchor).

Development for rents assets: Caselle Desiner Village

Source: Company data

19

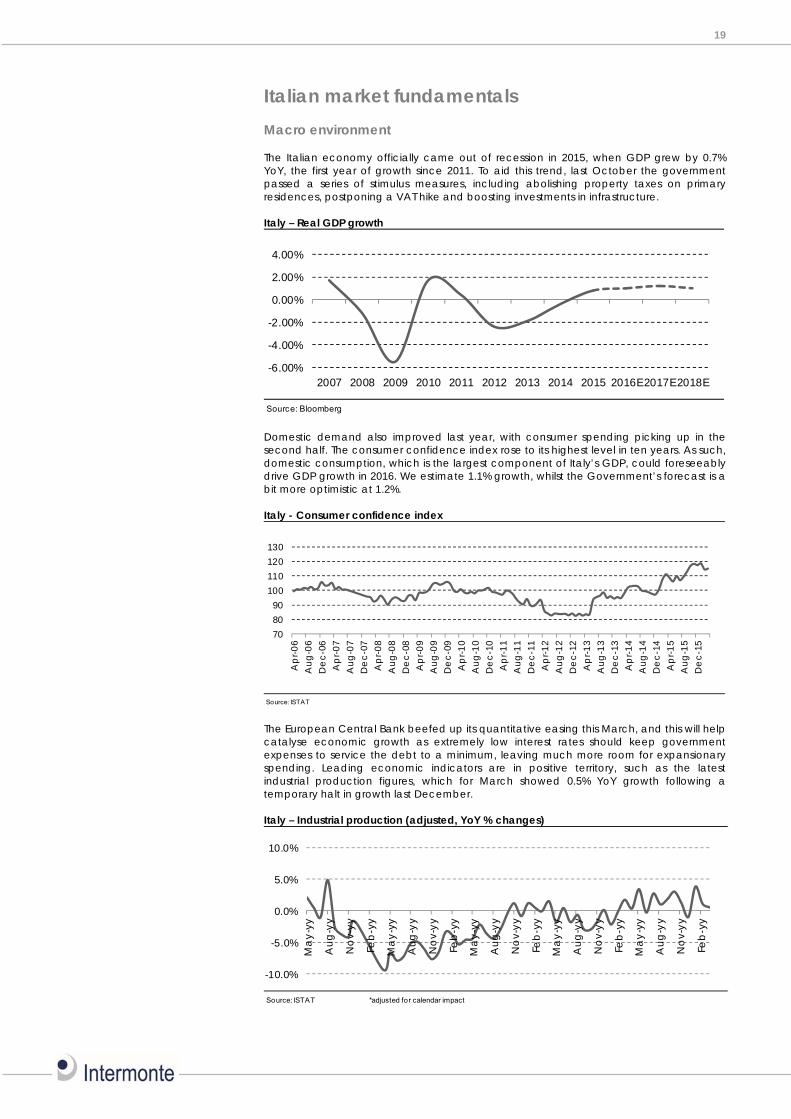

Italian market fundamentals Macro environment The Italian economy officially came out of recession in 2015, when GDP grew by 0.7% YoY, the first year of growth since 2011. To aid this trend, last October the government passed a series of stimulus measures, including abolishing property taxes on primary residences, postponing a VAT hike and boosting investments in infrastructure. Italy – Real GDP growth

Source: Bloomberg

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E

Domestic demand also improved last year, with consumer spending picking up in the second half. The consumer confidence index rose to its highest level in ten years. As such, domestic consumption, which is the largest component of Italy’s GDP, could foreseeably drive GDP growth in 2016. We estimate 1.1% growth, whilst the Government’s forecast is a bit more optimistic at 1.2%. Italy - Consumer confidence index

Source: ISTAT

708090

100110120130

Ap

r-06

Aug

-06

De

c-06

Ap

r-07

Aug

-07

De

c-07

Ap

r-08

Aug

-08

De

c-08

Ap

r-09

Aug

-09

De

c-09

Ap

r-10

Aug

-10

De

c-10

Ap

r-11

Aug

-11

De

c-11

Ap

r-12

Aug

-12

De

c-12

Ap

r-13

Aug

-13

De

c-13

Ap

r-14

Aug

-14

De

c-14

Ap

r-15

Aug

-15

De

c-15

The European Central Bank beefed up its quantitative easing this March, and this will help catalyse economic growth as extremely low interest rates should keep government expenses to service the debt to a minimum, leaving much more room for expansionary spending. Leading economic indicators are in positive territory, such as the latest industrial production figures, which for March showed 0.5% YoY growth following a temporary halt in growth last December. Italy – Industrial production (adjusted, YoY % changes)

Source: ISTAT *adjusted for calendar impact

-10.0%

-5.0%

0.0%

5.0%

10.0%

Ma

y-yy

Aug

-yy

No

v-yy

Feb

-yy

Ma

y-yy

Aug

-yy

No

v-yy

Feb

-yy

Ma

y-yy

Aug

-yy

No

v-yy

Feb

-yy

Ma

y-yy

Aug

-yy

No

v-yy

Feb

-yy

Ma

y-yy

Aug

-yy

No

v-yy

Feb

-yy

20

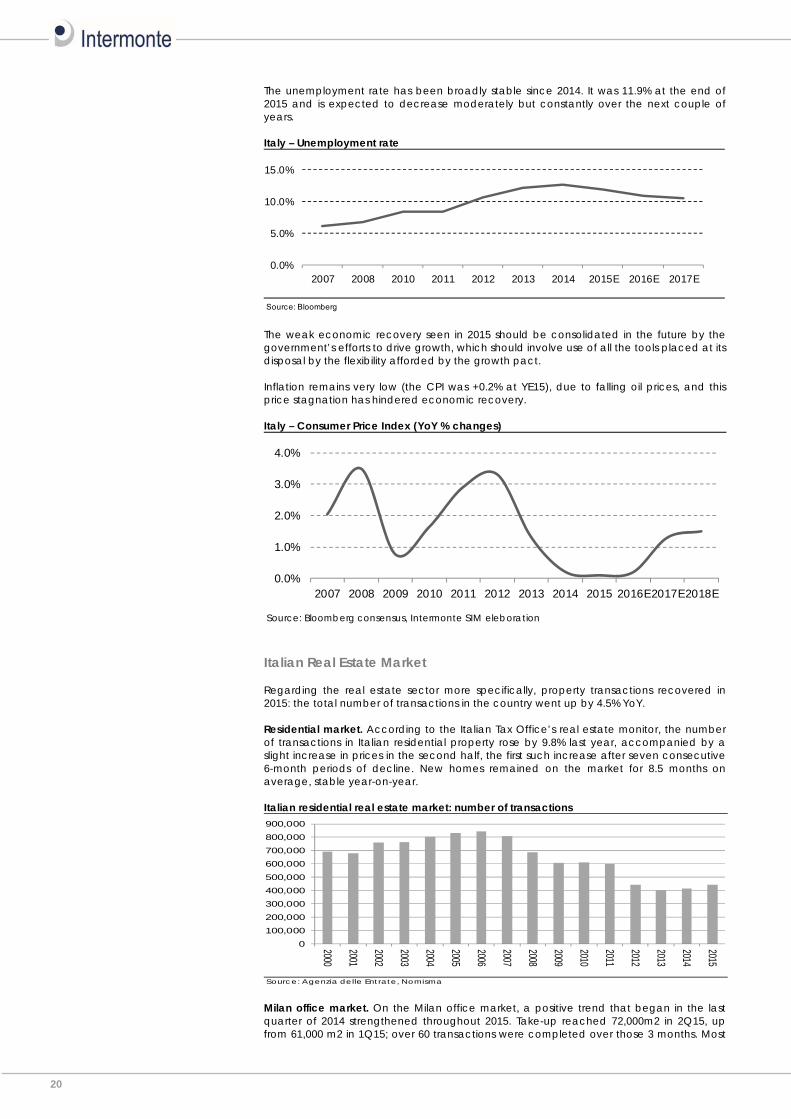

The unemployment rate has been broadly stable since 2014. It was 11.9% at the end of 2015 and is expected to decrease moderately but constantly over the next couple of years. Italy – Unemployment rate

Source: Bloomberg

0.0%

5.0%

10.0%

15.0%

2007 2008 2010 2011 2012 2013 2014 2015E 2016E 2017E

The weak economic recovery seen in 2015 should be consolidated in the future by the government’s efforts to drive growth, which should involve use of all the tools placed at its disposal by the flexibility afforded by the growth pact. Inflation remains very low (the CPI was +0.2% at YE15), due to falling oil prices, and this price stagnation has hindered economic recovery. Italy – Consumer Price Index (YoY % changes)

Source: Bloomberg consensus, Intermonte SIM eleboration

0.0%

1.0%

2.0%

3.0%

4.0%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E2017E2018E

Italian Real Estate Market Regarding the real estate sector more specifically, property transactions recovered in 2015: the total number of transactions in the country went up by 4.5% YoY. Residential market. According to the Italian Tax Office’s real estate monitor, the number of transactions in Italian residential property rose by 9.8% last year, accompanied by a slight increase in prices in the second half, the first such increase after seven consecutive 6-month periods of decline. New homes remained on the market for 8.5 months on average, stable year-on-year. Italian residential real estate market: number of transactions

Source: Agenzia delle Entrate, Nomisma

0100,000200,000300,000400,000500,000600,000700,000800,000900,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Milan office market. On the Milan office market, a positive trend that began in the last quarter of 2014 strengthened throughout 2015. Take-up reached 72,000m2 in 2Q15, up from 61,000 m2 in 1Q15; over 60 transactions were completed over those 3 months. Most

21

of this growth came from the financial sector, which accounted for over 25% of the new leases. Moreover, most of the transactions were small in scale; only five were large-scale deals. According to CBRE estimates, over 370,000 offices were rented out in Milan, a 34% YoY increase. Rental prices remained broadly stable, going up slightly only in high quality offices in central business districts (CBDs), where supply is scarce. Annual rent rates averaged about Eu200/m2 in outlying areas and Eu480/m2 in CBDs. Vacancy rates held rather stable, at about 12.5% in Milan, or 12.8% including the city’s suburbs. Italian residential real estate market: number of transactions

Source: Agenzia delle Entrate

-40%

-25%

-10%

5%

20%

0

25,000

50,000

75,000

100,000

125,000

150,000

175,000

200,000

1Q082Q083Q084Q081Q092Q093Q094Q091Q102Q103Q104Q101Q112Q113Q114Q111Q122Q123Q124Q121Q132Q133Q134Q131Q142Q143Q144Q141Q152Q153Q154Q15

Transactions Change YoY

Milan office market: prime office yields (%) 1Q15 2Q15 3Q15 4Q15 10YH 10YLMilan CBD 4.8 4.8 4.5 4.5 5.3 4.0

Milan Periphery 7.0 7.0 6.8 6.5 7.5 5.0

Source: C&W Milan office Market: prime office rents

Source: DTZ, JLL

0100200300400500600

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

CBD Centre-out of CBD Periphery

Factory Outlets in Italy. The Designer Outlet market in Italy developed much later than in the rest of the world. The first such outlet, the “Fifty Factory Store” in Saronno (VA), was opened in 1995. As things stand, however, Italy is one of the leading countries in the world in terms of the number of open outlet stores. The success of this formula can be explained by the ability of outlets to understand market sectors left uncovered by other formats, benefiting both manufacturers and consumers. In more detail, factory outlets are complex out-of-town shopping centres, which bring together a range of mono-brand stores with a specific commercial offer. This normally involves attractive brands being sold at lower prices than are on offer at traditional town centre retailers. Out-of-town outlet centres generally cover over 10,000m2, and are located close to major roads. These areas must also provide various services in addition to the commercial offers from the outlet stores. The key feature of the centres is the size of the discount to retail prices, which on average comes in at 30-70%. The main actors involved in the construction of outlets are: 1) real estate investors; 2) management companies; and 3) retailers. Investment activity. Investments in Italian real estate rose by 55% in 2015, pushed up by a few major transactions in Milan. Italy’s second largest city in fact accounted for 54% of investments made in the country thanks to three large deals, namely: 1) the Porta Nuova project, purchased by the Qatar Investment Authority for Eu900mn; 2) the purchase of Torre Isozaki by Allianz for Eu367mn; and 3) the sale of Palazzo Broggi, in Piazza Cordusio, to Fosun for Eu345mn. Analysing individual market segments in more detail, one notices that investors were most keen on offices, where investment volumes rose by 139% YoY. On the contrary, residential segment investments collapsed by 44%. These figures highlight how investors have

22

regained interest in the Italian real estate market. Investors are most attracted to ‘core’ assets where supply is scarce. The market is therefore concentrating on properties that can be adapted to tenant and investor demand. In addition to a dearth of good quality properties, there are not a lot of properties worth over Eu100mn on the Italian market. Italian real estate market: investment activity by segment (Eu mn)

Source: BNP Paribas Real Estate, Intermonte SIM eleboration

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Mixed/Other Retail Offices

Specifically regarding Italy’s two leading urban markets, Rome and Milan, the former seems to have returned to the average investment volume level seen in the past decade, although that level is below Milan’s, where the economic recovery is in full swing. Furthermore, the Milan property market is generally considered more liquid than the Rome market.

23

Group Financials & Estimates Group Financials As described earlier, over the past few years the group has gone through an intense process of restructuring and the company’s financials today are very different from what they looked like just a couple of years ago. For this reason, we have limited our ‘historical’ analysis to 2014 and 2015 only. Income statement. In 2015 Aedes earned a net profit and key indicators improved from 2014 after adjusting for non-recurring expenses connected with the 2014 restructuring. 2015 net profit was Eu5.2mn with a non-recurring effect of Eu1.7mn, whereas the net profit of Eu50.5mn achieved in 2014 included a non-recurring gain of Eu73.9mn linked to the restructuring. Gross rents came to Eu7.4mn in 2015, down from Eu10.7mn in 2014 owing to the disposal of some non-core properties to the Leopardi fund. A substantial portion of revenues come from services provided, amounting to Eu13.9mn in 2015 thanks to heightened activity at subsidiary Praga Construction S.r.l. (Eu6.6mn), related to Phase 6 of the Serravalle Outlet Village project as well as a Carrefour shopping centre development project in the town of Nichelino. Aedes SIIQ - Income Statement (Eu mn) 2014A 2015AGross rents 10.7 7.4

direct costs -4.3 -2.4

Net Rents 6.4 5.0Margin on rents 60% 68%

Rev enues from sales 17.1 10.3

Rev enues from serv ices 7.9 13.9

Disposal of participations 4.4 3.8

Other rev enues 2.2 6.7

Gross Revenues 42.4 42.1Net Revenues 22.3 32.1Labour cost -4.7 -5.8

Other costs -9.4 -10.9

Costs for serv ices -10.7 -14.5

Capitalised expenses 1.2 5.5

EBITDA -1.4 6.4Margin on Net rev enues -6.2% 19.9%

Net rev aluation/D&A -2.8 2.0

EBIT -23.1 7.4Financial charges -5.5 -4.3

Income from equity inv estments -1.7 -1.1

Other items 73.9 3.9

Pre tax Profit before minorities 43.6 6.9Total taxes 6.2 -0.9

Tax rate ns -12%

Net result before minorities 49.8 6.1

Minorities -0.7 1.0

Assets held for sale 0.0 0.0

Net Result 50.5 5.1Funds From Operations -10.4 -13.1Source: Company data, Intermonte SIM elaboration Revenues from disposals of properties came down to Eu10mn in 2015 (from Eu17mn in 2014), although the operating margin from such sales increased from Eu1.4mn in 2014 to Eu2.7mn. Other revenue rose from Eu2.2mn to Eu6.7mn, thanks to a Eu3.8mn revaluation of the Petrarca fund based on an expert independent appraisal by Cushman & Wakefield after the company’s acquisition of 50% of the fund’s quotas. With regard to cost items, as well as general expenses they also include the cost of services, including those related to the general contracting activity of subsidiary Praga Construction. In 2015, personnel costs amounted to Eu4mn (or Eu5.8mn when including pension costs) and the cost of executive remuneration amounted to Eu1.9mn. Please note that at the end of 2015

24

the group had a total headcount of 74, around 25 of which were working at the SGR and in other non-core activities. No major write-downs were taken in 2015, in contrast with 2014, when Eu8.2mn in impairments were booked on receivables due from companies sold, another Eu6.2mn on other receivables and Eu1.8mn on goodwill for the equity stake in Aedes Real Estate SGR S.p.A. In 2015, the fair value of real estate investments was actually raised by Eu2.0mn overall (Eu6.0mn in write-ups minus Eu4.0mn in write-downs); by comparison, net value adjustments in 2014 were negative to the tune of Eu2.8mn. In 2015, there were Eu0.9mn write-downs on inventories down from 4.2mn in the previous year. Income from associate companies and joint ventures was in the red to the tune of Eu1.1mn last year, an improvement from the Eu1.7mn loss in 2014. Below the EBIT line, the company had registered a huge one-off gain of Eu74mn due to the debt restructuring and recapitalisation operations, while in 2015, this item was limited to a Eu1.7mn gain (not related to the restructuring). Net financial charges, including fair value adjustments on derivatives used to hedge interest rate risk, came to Eu4.3mn in 2015, down from Eu5.5mn in 2014. This item was the result of Eu0.9mn in gains minus Eu5.3mn in losses. Taxes incurred amounted to Eu0.8mn in 2015, whereas the company had benefited from negative taxes to the tune of Eu6.2mn in 2014. The 2015 figure was the difference between Eu2.6mn in charges (including the exit tax to adjust property values to standard values used for companies in the SIIQ system) and a Eu1.8mn positive entry from deferred taxes. It should be underlined that the group has Eu206mn in carried forward losses, despite which it has not booked any deferred tax assets for losses, other than for a minimal amount (roughly Eu1mn). Balance sheet. The group had Eu326mn in capital assets at the end of 2015, up from Eu165mn a year before, mainly due to higher real estate investments and other tangible assets, which went from Eu106mn to Eu270mn after development assets were reclassified from ‘inventories’ to ‘tangible fixed assets’. More specifically, in keeping with the group’s strategic guidelines, real estate development assets held by subsidiaries under the SIINQ (non-listed real estate investment company) regime were reclassified as at 31st December 2015, and will now be included with property investments. This reclassification did not per se imply any increase in value, as even though they are accounted at fair value in accordance with IAS 40, the group’s accounting policy for properties in the development phase is to use the cost criteria until the related fair value appraisal becomes reliable enough for it to be valued as such on a continuous basis. Other capital assets include equity stakes in associate companies and joint ventures, amounting to Eu53mn as at the end of last year. Net working capital stood at Eu55mn, well below the Eu215mn registered at the end of 2014. This is because inventories fell from Eu188mn to Eu54mn owing to the reclassification of development assets described above. Also, inventories pertaining to Praganove S.r.l. and Pragasei S.r.l. (amounting to Eu25mn) were deconsolidated. Gross debt went from Eu156mn to Eu164mn in 2015. Debt subject to variable interest rates made up 69.6% of the total, down from 100% in 2014, after Aedes signed an interest rate collar contract in November 2015 with a 0% strike rate for the floor and a 1% rate for the cap. The notional amount on this loan contract is Eu50mn and the loan is due to be repaid in full in December 2020. As at 31st December 2015, the average residual loan duration was 2.4 years, but some extensions of short term loans concluded in the first few months of 2016 have brought that average duration up to 3 years, as was the case in 2014. The group ended 2015 with a net debt position of Eu95mn, thanks to gross cash and cash equivalents of Eu68mn. After adding the holding company’s cash and equivalents, the group’s consolidated loan to value (LTV) ratio was 30%, significantly lower than the consolidated real estate portfolio’s LTV ratio of 47%. Aedes SIIQ: Balance Sheet (Eu mn) 2014A 2015AFixed assets 165 326

Working capital 215 56

Invested capital 380 382Group sharehold. equity 239 275Other 17 11

Net debt 124 96

Total Liabilities 380 382Source: Company data

25

1Q 2016 Results 1Q16 results up thanks to higher rents and a write-up of the Redwood portfolio. Aedes SIIQ reported a good set of 1Q16 results, up sharply year-on-year. Gross revenue came in at Eu27mn, much higher than the Eu10.4mn in 1Q15. This increase came thanks to a greater contribution from rent income, which grew from Eu1.4mn to Eu2.6mn mainly as a consequence of the 3Q15 consolidation of the Petrarca fund. Including rents from the Redwood portfolio, which was purchased at the end of 1Q16, total rent income would have been Eu3.4mn. Yet the factor that brought revenue up most of all was higher other income (Eu16.5mn vs. Eu0.7mn in 1Q15), due to a write-up of the Redwood portfolio above the acquisition price. Total costs came to Eu11.4mn, up from Eu8.5mn in 1Q15; this increase is entirely attributable to general contractor costs, which were more than offset by higher corresponding revenues. EBITDA was Eu15.7mn in 1Q16, well above the Eu1.9mn seen in 1Q15, while EBIT was Eu15.6mn (vs. Eu1.5mn) and pre-tax profit was €14.2mn (vs. €0.3mn a year ago). Aedes SIIQ: 1Q16 Profit & Loss (Eu mn) 1Q15A 1Q16AGross rents 1.4 2.6

direct costs -0.5 -0.7

Net Rents 1.0 1.9Margin on rents 68% 73%

Rev enues from sales 4.3 0.5

Rev enues from serv ices 7.9 7.6

Disposal of participations 2.2 0.0

Other rev enues 0.7 16.5

Gross Revenues 16.4 27.1EBITDA 1.9 15.7Net rev aluation/D&A 0.0 -0.3

EBIT 0.0 15.5Financial charges -1.2 -1.4

Income from equity inv estments 0.0 0.1

Other items -0.4 0.0

Pre tax Profit before minorities 0.3 14.2Total taxes na na

Net result before minorities 0.3 14.2

Minorities 0.2 0.1

Assets held for sale 0.0 0.0

Net Result 0.1 14.1Source: Company data, Intermonte SIM elaboration On the balance sheet, shareholders’ equity closed the quarter at Eu289mn, compared to Eu275mn at the end of 2015. Net debt stood at Eu125mn, up from Eu96mn at the end of last year, chiefly as a result of the Redwood fund acquisition. Aedes SIIQ - Invested capital (Eu mn) 1Q15A 1Q16AGroup shareholders equity 275 289

Other 11 11

Net debt 96 125

Invested Capital 382 425Source: Company data

26