aec management solutions, inc. - codewriters...

TRANSCRIPT

AEC Management Solutions, Inc. 183 Higgins Road Matawan, NJ 07747

Matawan 732-705-5098 San Francisco 415-462-0840 www.aecmanagementsolutions.com

Pathway to Profit Seminar™

Society for Design Administration American Institute of Architects

October 2, 2008

Akron, Ohio

AEC Management Solutions, Inc. 183 Higgins Road Matawan, NJ 07747

Matawan 732-705-5098 San Francisco 415-462-0840 www.aecmanagementsolutions.com

Herbert M. Cannon President Herb Cannon is one of the nations leading experts in the management of A/E firms. With over 25 years of “hands on” experience in the A/E Industry, Herb has held top management positions in a number of high profile firms. Prior to founding AEC Management Solutions, Inc., he held senior executive positions at Robert A.M. Stern Architects, Ehrenkrantz Eckstut & Kuhn Architects, Burns & Roe Engineering. Mr. Cannon has served these organizations in a variety of executive roles including Chief Operating Officer, Chief Financial Officer and Director of Project Management. Throughout his 25-year career he recognized that design professionals create an extraordinary value for their clients. To a large extent the extraordinary value these design professionals create is not rewarded with a fair economic return. Herb founded AEC Management Solutions in 2000 with the simple goal helping A/E firms of all sizes earn and keep the money they deserve. To achieve this goal, he conducts numerous seminars and workshops throughout North America on Strategic Planning, Mergers and Acquisitions, Incentive Compensation, Project Management, Ownership Transition, Financial Management and Firm Valuation. He helps firms to develop and implement strategic plans, incentive compensation programs and project management systems that dramatically improve profitability. He provides consulting services on valuation and ownership transition issues to facilitate a smooth transition to the next generation of owners. Through his extensive contacts in the A/E industry and professional organizations, he also assists firms in identifying potential merger and acquisition candidates. Herb is an accomplished speaker, speaking to hundreds of A/E professionals each year at seminars and professional association events. He has been a featured speaker for the American Institute of Architects, Society for Marketing Professional Services, Society for Design Administration, NSPE Chief Financial Officer Roundtable, NSPE Principals Forum, Axium Software, American Society for Heating Refrigeration and Air Conditioning Engineers, Ontario Association of Architects, Texas Council of Engineering Companies Leadership Forum and is a guest lecturer at New York University. Herb is the publisher of AEC Managing Partner, a monthly newsletter for the design professional. He also has a long-term consulting relationship with Robert A.M. Stern Architects, a 265-person architecture firm in New York City, acting as the part-time CFO and Director of Project Management.

AEC Management Solutions, Inc. 183 Higgins Road Matawan, NJ 07747

Matawan 732-705-5098 San Francisco 415-462-0840 www.aecmanagementsolutions.com

AEC Management Solutions, Inc. Company Profile

At AEC Management Solutions, Inc., we recognize that architects, engineers and related industry professionals create extraordinary value through their creative efforts. To a large extent, the extraordinary value these design professionals create is not rewarded with a fair economic return. Our simple goal is to help these design professionals earn and keep the money they deserve.

In order to achieve this goal we provide a variety of seminars and consulting services on:

• Strategic Planning • Incentive Compensation • Project Management • Financial Management • Cash Flow and Collections • Ownership Transition • Valuation Services • Management Audits • Marketing

Whether it is customized seminars, workshops or consulting solutions, you can be assured that only top level instructors and consultants will be provided. All of our consultants are exclusive to the A/E industry and have 15 to 25+ years of experience working with many of the country’s top A/E firms. They are licensed professionals and have held top-level positions such as Chief Executive Officer, President, Chief Operating Officer, Director of Project Management, Chief Financial Officer, Director of Marketing and Director of Information Technology.

By tapping into our decades of knowledge and experience, you can jump start your companies performance and avoid years of costly mistakes figuring it out on your own. Whether your needs are strategic or tactical, long or immediate, we look forward to helping you solve your problem – so you can start earning the money you deserve.

Contact Information: Herbert M. Cannon AEC Management Solutions, Inc. 183 Higgins Road Matawan, NJ 07747 732.705.5098 [email protected] www.aecmanagementsolutions.com

AEC Management Solutions, Inc. 183 Higgins Road Matawan, NJ 07747

Matawan 732-705-5098 San Francisco 415-462-0840 www.aecmanagementsolutions.com

Herbert M. Cannon 2007 Speaking Engagements SMPS Southern Region Conference January 25th San Antonio Strategic Planning Axium Webinar February 8th Project Management for 20%+ Profit Pathway to Profit Seminar™ March 15-16 New York 2-day Seminar on Achieving a 20%+ Profit

NSPE – Principals Forum February 23rd Tampa Top Ten Ways to Connect and Communicate with your Employees

Pathway to Profit Seminar™ April 12-13 Chicago 2-day Seminar on Achieving a 20%+ Profit

SMPS Philadelphia April 18th Incentive Compensation Society for Design Administration National Convention May 4th San Antonio Administrator’s Survival Guide to the A/E Industry Axium Webinar May 10th Incentive Compensation Deltek Convention May 16 – 18 Las Vegas Session #1 Secrets of Creating a 20%+ Profit Machine Session #2 Incentive Compensation

Pathway to Profit Seminar™ June 7-8 Portland 2-day Seminar on Achieving a 20%+ Profit

Pathway to Profit Seminar™ June 21-22 Las Vegas 2-day Seminar on Achieving a 20%+ Profit

NSPE National Convention July 26-27 Denver Secrets of Creating a 20%+ Profit Machine SDA Webinar August 16th 2007 Incentive Compensation Texas Council of Engineering Companies August 23rd San Antonio Business Management Skills SDA Western States Conference September 28th Orange County, CA Incentive Compensation

AEC Management Solutions, Inc. 183 Higgins Road Matawan, NJ 07747

Matawan 732-705-5098 San Francisco 415-462-0840 www.aecmanagementsolutions.com

Axium Software National Convention October 18 – 20 Portland Keynote Address

2006 and Prior Speaking Engagements Build Business National Convention Incentive Compensation - 1 Hour Presentation, August 2006 Society for Design Administration National Convention Incentive Compensation – 1.5 Hour Presentation June 2006 Axium Software National Convention Incentive Compensation – 1.5 Hour Presentation October 2006 Axium Software Webinar Maximize Productivity – A Principal’s Guide – 1 Hour Presentation August 2006 American Society of Heating Refrigeration and Air Conditioning Engineers – Houston The Seven Habits of Highly Ineffective Engineering Firms – 1 Hour Presentation September 2006 Project Management – A Profit Perspective – 1 Hour Presentation September 2006 National Society of Professional Engineers CFO Roundtable Incentive Compensation – 1 Hour Presentation, May 2005 Texas Council of Engineering Companies Incentive Compensation - 3 Hour Presentation November 6 & 7, 2004 American Institute of Architects – Jersey Shore Chapter Incentive Compensation - 1 Hour Presentation, March 2005 Kansas Council of Engineering Companies Incentive Compensation – Full Day Presentation, October 2004 Society for Marketing Professional Services – NY Chapter Developing a Business Plan – 3 Hour Presentation, November 2005 Society for Marketing Professional Services – NJ Chapter Strategic Planning Techniques – An emphasis on Marketing – 1 ½ Hour Presentation, November 2005 American Institute of Architects – NY Chapter Marketing Committee Giving Away the Store – 2 Hour Panel March 2001 Texas Council of Engineering Companies Leadership Forum Business Management Skills - 4 Hour Presentation Annual Event 2001 - 2006 New York University Guest Lecturer on Public Speaking – 1 Hour Presentation Bi-Annual Event 2002-2006

AEC Management Solutions, Inc. 183 Higgins Road Matawan, NJ 07747

Matawan 732-705-5098 San Francisco 415-462-0840 www.aecmanagementsolutions.com

Singer Nelson Chalmers Ownership Transition and Valuing Your Design Firm - 3 Hour Presentation 2004-2006 Institute for Classical Architecture and Classical America Profit by Design: Successful Management for the Architectural Firm - Full Day April 2005 American Society of Heating Refrigeration and Air Conditioning Engineers Improving Cash Flow – 1 Hour Presentation February 2003 Ownership Transition – 1 Hour Presentation March 2004 PSMJ Resources Financial Management Bootcamp 2 day Seminars 2000 - 2003 Project Management Bootcamp 2 day Seminars 2000 - 2003 Principals Bootcamp 2 day Seminars 2000 – 2003 Annual Software Summit 2 day event 2001 CEO Ownership Transition Roundtable 3 day Annual Event 2000-2003

AEC Management Solutions, Inc. 183 Higgins Road Matawan, NJ 07747

Matawan 732-705-5098 San Francisco 415-462-0840 www.aecmanagementsolutions.com

References Rob Buford Robert A.M. Stern Architects 460 West 34th St. New York, NY 10001 212.967.5100 Joeseph Tomaino Tomaino Tomaino Iamello & Associates 136 Brighton Avenue Deal, NJ 07723 732.531.2282 Kenneth Camp KDC Architects and Engineers 7442 South Tucson Way Centennial, CO 80112 303.750.6999 Jeffrey Venezia NJ K-12 Architects 104 Bayard St. New Brunswick, NJ 08901 732.296-6545 Steve Stagner Texas Council of Engineering Companies 1001 Congress Austin, Texas 78701 512.474.1474 Kevin Newman Bucher Willis Ratliff 601 Shelley Drive Tyler, TX 75701 903.581.7844 Charles Becht Becht Engineering 22 Church St. Liberty Corner, NJ 07938 908.580.1119

Rolf Kielman Truex Cullins and Partners 209 Battery St. Burlington, VT 05401 802.658.2775 Wally Gordon Deems Lewis McKinley 12 Gough St. San Francisco, CA 94103 415.255.1811 Scott Gaudineer Flewelling and Moody 141 South Lake Avenue Pasadena, CA 91101 626.449.6787 Paul Stoller Atelier Ten 45 East 20th St. New York, NY 10003 212.254.4500 Peter Biber The Biber Partnership 422 Morris Avenue Summit, NJ 07901 908.273.8877 Fred Shen Shen Milsom Wilke 417 5th Avenue New York, NY 10016 212.725.6800

Sharyn Yorio Sustainable Marketing 170 Kinnelon Road Kinnelon, NJ 07405 973.492.1040

1

Pathway to Profit™

2-Day Seminarfor 20%+ Profit

AEC Management Solutions, Inc.

Who is Here Today

NamePositionCompany Name, LocationSpecialty & Size

The Next 2 Days

LogisticsParticipationNetworkingReinforcement New Ideas

2

Gross Fees 27,622,778$ Other Income 55,239 Reimbursables & Directs (10,011,033) Net Revenues 17,666,985$ A

Minimum Profit% 20.0% BProfit Increase 3,533,397$ AxB

What Do We Mean by20%+ Profit?

Elements of a 20%+ Profit

Understanding the financial fundamentalsTimely & accurate project informationStrategic PlanningCommunicationsCash flowProject managementIncentive compensation

The Core Secret of 20%+ Profit

Stop Admiring the Problem!

3

The Core Secret of 20%+ Profit

Start Taking Action!

Pathway to Profit™

Financial Fundamentalsfor 20%+ Profit

AEC Management Solutions, Inc.

Elements of a 20%+ Profit

Understanding the Financial FundamentalsProduce Timely & Accurate Project InformationStrategic PlanningCommunicationsCash FlowProject ManagementIncentive Compensation

4

Definitions

Utilization Rate – the percentage of staff dollars or hours charged to projectsNet Multiplier – net revenues divided by direct labor dollarsOverhead Rate – indirect expenses divided by direct labor dollars

Definitions

Net Revenues – total revenue less all non-labor direct expenses (Consultants, Project Travel, Postage…)Direct Labor – labor dollars charged to client projectsIndirect Labor – labor dollars not charged to client projects

Key Indicators

Utilization:

Direct Labor $ Total Labor $

Net Multiplier: Net Revenues $ Direct Labor $

Overhead Rate:

Total Indirect Expenses Total Direct Labor $

Accounts Receivable In Days:

Accounts Receivable (Annual Sales/365 days)

Backlog in Days Uncompleted Work under Contact (Annual Sales/365 days)

5

AssetsCash in Bank 1,500,000$ Accounts Receivable 4,300,000 Other Current Assets 200,000 Total Current Assets 6,000,000

Furniture Fixtures & Equipment (Net) 2,600,000 Investments 250,000 Total Fixed Assets 2,850,000

Total Assets 8,850,000$ +

LiabilitiesAccounts Payable 1,800,000$ Retainers 500,000 Total Current Liabilities 2,300,000

Loans Payable 1,900,000 Total Liabilities 4,200,000 -

CapitalCommon Stock 10,000$ Retained Earnings 2,938,267 Current Years Profit 1,701,733 Total Capital 4,650,000 =

Total Liablilities & Capital 8,850,000$

San Antonio EngineersBalance Sheet

December 31, 2006

San Antonio EngineersIncome Statement

12 Months Ended December 31, 2006

Gross Fees 27,622,778$ Other Income 55,239 Reimbursables & Directs 10,469,001

Net Revenues 17,209,017 ADirect Labor Expense 5,833,565 BGross Profit 11,375,452

Overhead 9,673,719 COperating Profit 1,701,733$ D

Overhead SummaryIndirect Labor 3,679,200$ ETotal Overhead 9,673,719$

Overhead Rate 165.8% (C/B)Net Multiplier 2.95 (A/B)Utilization 61.3% (+B/(B+E))Profit% 9.9% (+D/A)

Key Statistic

Utilization RateAverage A/E Firm • 61.3% Utilization Rate

Top Performing A/E Firm• 70.0% Utilization Rate

6

Increased Utilization in a10-person Firm

Assumptions:Assumptions:$45,000 Salary, 10 Employees, 8.7% Increase in Utilization$45,000 Salary, 10 Employees, 8.7% Increase in Utilization

Difference in Direct Labor =Difference in Direct Labor = $ 39,150$ 39,150Net Multiplier =Net Multiplier = 2.902.90Total increase in profits = $113,535Total increase in profits = $113,535

Increased Utilization Scenarios

20 Employees $ 227,07030 Employees $ 340,60540 Employees $ 454,14050 Employees $ 567,67560 Employees $ 681,21070 Employees $ 794,74580 Employees $ 908,28090 Employees $1,021,815100 Employees $1,135,350

12 Months Ended December 31, 2006

Gross Fees 27,622,778$ Other Income 55,239 Reimbursables & Directs 10,011,033

Net Revenues 19,643,861 ADirect Labor Expense 6,658,936 BGross Profit 12,984,925

Overhead 8,848,349 COperating Profit 4,136,576$ D

Overhead SummaryIndirect Labor 2,853,830$ ETotal Overhead 8,848,349$

Overhead Rate 132.9% (C/B)Net Multiplier 2.95 (A/B)Utilization 70.0% (+B/(B+E))Profit% 21.1% (+D/A)Profit Increase 2,434,843$

San Antonio EngineersIncome Statement with Increased Utilization

7

Ideas to Increase Utilization

1.

2.

3.

4.

5.

6.

7.

Key Statistic

Net MultiplierAverage A/E Firm • 2.90 Net Multiplier

Top Performing A/E Firm• 3.25 Net Multiplier

Impact of Multiplier Differences In a 10-person Firm

Assumptions:$45,000 Salary, 10 Employees, 61.3% Utilization

Direct Labor $275,850

Revenue Achieved with a 2.90 Multiplier $799,965Revenue Achieved with a 3.25 Multiplier $896,513Total Increase in Revenue $ 96,548

8

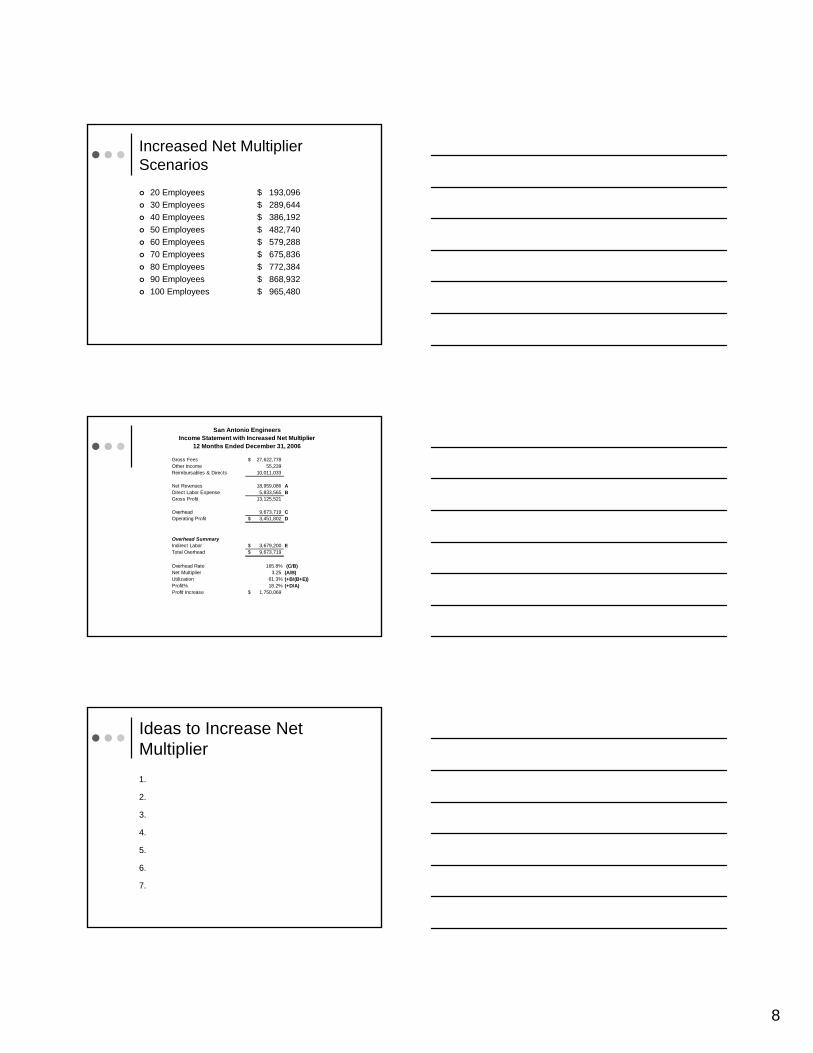

Increased Net Multiplier Scenarios

20 Employees $ 193,09630 Employees $ 289,64440 Employees $ 386,19250 Employees $ 482,74060 Employees $ 579,28870 Employees $ 675,83680 Employees $ 772,38490 Employees $ 868,932100 Employees $ 965,480

12 Months Ended December 31, 2006

Gross Fees 27,622,778$ Other Income 55,239 Reimbursables & Directs 10,011,033

Net Revenues 18,959,086 ADirect Labor Expense 5,833,565 BGross Profit 13,125,521

Overhead 9,673,719 COperating Profit 3,451,802$ D

Overhead SummaryIndirect Labor 3,679,200$ ETotal Overhead 9,673,719$

Overhead Rate 165.8% (C/B)Net Multiplier 3.25 (A/B)Utilization 61.3% (+B/(B+E))Profit% 18.2% (+D/A)Profit Increase 1,750,069$

San Antonio EngineersIncome Statement with Increased Net Multiplier

Ideas to Increase Net Multiplier1.

2.

3.

4.

5.

6.

7.

9

12 Months Ended December 31, 2006

Gross Fees 27,622,778$ Other Income 55,239 Reimbursables & Directs 10,011,033

Net Revenues 21,641,542 ADirect Labor Expense 6,658,936 BGross Profit 14,982,606

Overhead 8,848,349 COperating Profit 6,134,257$ D

Overhead SummaryIndirect Labor 2,853,830$ ETotal Overhead 8,848,349$

Overhead Rate 132.9% (C/B)Net Multiplier 3.25 (A/B)Utilization 70.0% (+B/(B+E))Profit% 28.3% (+D/A)Profit Increase 4,432,524$

San Antonio EngineersIncome Statement with Increased Net Multiplier & Utilization

Income Low HighOriginal Company 1,701,733$ 6,806,932$ 8,508,666$ Increased Utilization 4,136,576 16,546,305 20,682,882 Increased Net Multiplier 3,451,802 13,807,208 17,259,011 Increased Utilization & Net Multiplier 6,134,257 24,537,028 30,671,286

San Antonio EngineersRule of Thumb Valuation Implications

December 31, 2006

Valuation Range

Pathway to Profit™

Strategic Planningfor 20%+ Profit

AEC Management Solutions, Inc.

10

Elements of a 20%+ Profit

Understanding the financial fundamentalsTimely & accurate project informationStrategic PlanningCommunicationsCash flowProject managementIncentive compensation

Why Strategic Planning?

Raises the bar of expectationsCreates a common vision for all employeesDerails the Wishful Thinking™SyndromeCreates commitment and accountabilityEnables ordinary people to do extraordinary things

Strategic Plan or Business Plan?

Strategic PlanEstablished businessesHelp build competitive advantageCommunicates to staffPrioritizes financesAction OrientedIdea & Goal Oriented

Business PlanNew businessesDefines business purposePlans operational needsCritical for financingAssesses opportunitiesProvides structure to ideas

11

Successful Planning Retreats

Limited number of participantsHeld offsite (No distractions)PreparationOutside facilitatorOpen communicationFocus on the big pictureAction oriented

Strategic Planning Key Elements

Where are we now?Where are we going?How will we get there?

Where are We Now?

BenchmarkingEmployee SurveysEmployee InterviewsSWOT Analysis

StrengthsWeaknessesOpportunitiesThreats

12

Strengths, Weaknesses, Opportunities, and Threats AnalysisStrengths My Company Competitor 1 Competitor 2 Competitor 3What are your business advantages?What are your core competencies?Where are you making the most money?What are you doing well?WeaknessesWhat areas are you avoiding?Where do you lack resources?What are you doing poorly?Where are you losing money?What needs improvement?OpportunitiesAny beneficial trends?Niches that competitors are missing?New technologies?New needs of customers?ThreatsObstacles to overcome?Aggressive competitors?Successful competitors?Negative economic conditions?Government regulation?Changing business climate?Vulnerabilities?

Where are We Going?

MissionGoal SettingCapitalize on StrengthsFix the WeaknessesCapitalize on OpportunitiesRecognize and Avoid the Threats

Goal Setting

Where do we want to be in 3 yearsMarkets served

• Services• Geographic area• Client type

RevenuesProfitsEmployees

13

Achieving our Goals

MarketingProject DeliveryFinancesOrganizational StructureInformation TechnologyHuman ResourcesOwnership Transition

Action items from Planning Retreat on October 15-16, 2007Action Needed Owner Due Date

Contact Axium Software to arrange a Demonstration of their Portfolio Software H Cannon 12.16.07

Get competitive proposals for in-house Project Management Training R. Titsch 12.28.07

Prepare a detailed plan for the financial turnaround of Houston Office. Goal of profitability by April 30, 2008 R.Titsch 11.30.07

Investigate the need for upgrade of IT Infrastructure and make recommendations to the executive committee D.Laun 1.08.08

Pathway to Profit™

Communicationsfor 20%+ Profit

AEC Management Solutions, Inc.

14

Elements of a 20%+ Profit

Understanding the Financial FundamentalsProduce Timely & Accurate Project InformationStrategic PlanningCommunicationsCash FlowProject ManagementIncentive Compensation

Internal Communications

Divergence of OpinionOwners/Management think there is good communication with employeesOwners/Management think there is poor communication within management groupEmployees think there is poor communication at all levelsLack of communication is the #1 complaint

What I have discovered

People want to feelConnectedPart of a Team

They want to knowWhat is the vision for the firmHow can they fit inHow can they help achieve that visionWhat’s in it for me

15

Human Resources AuditOutside Facilitator with Industry ExperienceSurveyReportIn-Person InterviewsFinal Report and Recommendations

More about the survey

Completed on-lineCombination of Question types

Multiple choice rankingsOpen-Ended Questions

Compare Management Responses to Rank & File

Management always has a rosier view of communicationStaff views lack of communication as the lack of a plan

Ranking Your Staff

1. Hold a mock draft2. If you had to start all over which

employees would you keep?3. Who are the first ones chosen4. Who are the last ones chosen5. Actually write it down

16

1

2

3

4

Ranking Your Staff

Core Group

Leaders

Top Performers

On the Bubble

Who is in Your Core Group?

What qualities do the bring?Can do attitudeWillingness to do whatever it takesTalentLeadershipMarketingIdentityFollowing

Should they be Owners?

Who are Your Leaders?

What qualities do the bring?Can they eventually become part of your core group?Client followingWho views them as leadersCan the become part of your core group and how?

17

Who are Your Top Performers?

Compare to their peer groupCan be at any level of the companyTechnical SkillsDesign SkillsMarketing SkillsCan they become a leader?

Who is on the Bubble?

What can they improve?Can they improve and can we help them?What feedback can we give them?What training or motivation can we provide?Should we help with a transition?

Who is on the Bubble?

Why are they not a top performer?What can they improve?Can they improve and can we help them?What feedback can we give them?What training or motivation can we provide?

18

Annual Review

Hold it on TimeHold it on TimeHold it on Time

Don’t put the burden on the employee to make it happenIf we are communicating throughout the year, the review is easy

Monthly E-Mail Newsletter

State of the FirmNew Projects

How we wonBrief overviewProject Team

PromotionsAwardsMilestones

Monthly E-Mail Newsletter

Individual RecognitionTeam RecognitionExpansion PlansUpcoming Events

19

Quarterly Meeting for Staff

Owners can talk about any topic they choose

Firm HistoryNew initiativesQ & A

Others can give a talkMarketingAdministration

Retreat Activities

Quarterly ½ day or full dayTheme Based

Improved CommunicationExpand into new marketsOpen new officesOffer new services

A facilitator would help the process

Project Related Communication

New project e-mail announcement to the entire firmBulletin Board PostingsIn-house presentations

Improves presentation skillsElectronic Photo Gallery

20

In-House Seminars/Training

All Attendees hear the same informationTechnology ToolsAchieving a 20%+ ProfitProject ManagementClient CommunicationsCollections

Do Something Just For Fun

BarbecueSponsor Team SportsActivities that include familiesMuseum ToursBaseball Games

Pathway to Profit™

Cash Flow & Collectionsfor 20%+ Profit

AEC Management Solutions, Inc.

21

Elements of a 20%+ Profit

Understanding the Financial FundamentalsProduce Timely & Accurate Project InformationStrategic PlanningCommunicationsCash Flow & CollectionsProject ManagementIncentive Compensation

Key Indicators

Utilization:

Direct Labor $ Total Labor $

Net Multiplier: Net Revenues $ Direct Labor $

Overhead Rate:

Total Indirect Expenses Total Direct Labor $

Accounts Receivable In Days:

Accounts Receivable $ (Annual Sales/365 days)

Backlog in Days Uncompleted Work under Contact (Annual Sales/365 days)

Annual Sales 1,000,000$ 5,000,000$ 10,000,000$ Sales Per Day 2,740$ 13,699$ 27,397$

Days A/R Additional Additional Additional Outstanding Cash Flow Cash Flow Cash Flow

120 Baseline Baseline Baseline115 13,699$ 68,493$ 136,986$ 110 27,397$ 136,986$ 273,973$ 105 41,096$ 205,479$ 410,959$ 100 54,795$ 273,973$ 547,945$ 95 68,493$ 342,466$ 684,932$ 90 82,192$ 410,959$ 821,918$ 85 95,890$ 479,452$ 958,904$ 80 109,589$ 547,945$ 1,095,890$ 75 123,288$ 616,438$ 1,232,877$ 70 136,986$ 684,932$ 1,369,863$ 65 150,685$ 753,425$ 1,506,849$ 60 164,384$ 821,918$ 1,643,836$

How Much Money do you Want?

22

Month 1 Month 2 Month 3 Month 4 Month 5 Month 6Invoices 20,000$ 20,000$ 20,000$ 20,000$ 20,000$ 20,000$ Reimbursables & Directs 2,000 2,000 2,000 2,000 2,000 2,000 Net Revenue 18,000 18,000 18,000 18,000 18,000 18,000

Direct Labor 6,000 6,000 6,000 6,000 6,000 6,000 Gross Profit 12,000 12,000 12,000 12,000 12,000 12,000

Overhead 8,400 8,400 8,400 8,400 8,400 8,400 Profit 3,600$ 3,600$ 3,600$ 3,600$ 3,600$ 3,600$

Monthly Disbursements 16,400$ 16,400$ 16,400$ 16,400$ 16,400$ 16,400$ Colledtions at 60 Days 20,000 20,000 20,000 20,000 Monthly Cash Flow (16,400) (16,400) 3,600 3,600 3,600 3,600 Culmulative Cash Flow (16,400)$ (32,800)$ (29,200)$ (25,600)$ (22,000)$ (18,400)$

Collections at 90 days 20,000 20,000 20,000 Monthly Disbursements 16,400 16,400 16,400 16,400 16,400 16,400 Monthly Cash Flow (16,400) (16,400) (16,400) 3,600 3,600 3,600 Culmulative Cash Flow (16,400)$ (32,800)$ (49,200)$ (45,600)$ (42,000)$ (38,400)$

Cash Flow with 20% Profit60 and 90 Day Collection Periods

10,000,000$ Annual Sales365 Days in the Year

27,397$ Average Sales per Day

2,602,740$ Outstanding Receivables684,932$ Work In Progress (WIP)

3,287,671$ Total Work Completed and not Paid

95 Outstanding Receivables Measured in Days25 Outstanding WIP Measured in Days

120 Total Days of Work Completed and not Paid

500,000$ Profit at 5% of Annual Sales6.58 Years of Profit in Work Completed and Not Collected

1,000,000$ Profit at 10% of Annual Sales3.29 Years of Profit in Work Completed and Not Collected

1,500,000$ Profit at 15% of Annual Sales2.19 Years of Profit in Work Completed and Not Collected

2,000,000$ Profit at 20% of Annual Sales1.64 Years of Profit in Work Completed and Not Collected

How Much Profit Are You Owed?

Collection Process

Proposal/ContractKick-off MeetingInvoicingFollow-up for Payment

23

Ideas for Proposal/Contract

1.

2.

3.

4.

5.

6.

7.

Ideas for Start-up Meeting

1.

2.

3.

4.

5.

6.

7.

Ideas for Invoicing

24

Ideas for Payment Follow-up

Pathway to Profit™

Project Managementfor 20%+ Profit

AEC Management Solutions, Inc.

Elements of a 20%+ Profit

Understanding the Financial FundamentalsProduce Timely & Accurate Project InformationStrategic PlanningCommunicationsCash FlowProject ManagementIncentive Compensation

25

Proposal/Contract Language

FeesDeliverablesSchedulesMeetingsClient Responsibilities

Fees

Don’t be afraid to ask what you are worthYou can always lower your feeMost clients do not leave over priceTie the fee to specific assumptions

Construction CostMeetingsProgram

Fees

Escalation clauses for hourly servicesDo not give a fixed fee for an unknown quantity of work

ApprovalsUndefined Program

Proposal/Contract termination dateProject Suspension Fee

26

Deliverables

Include a Drawing ListInclude a Responsibility Matrix

ClientConsultant (You)Other Consultants

What is not includedSurveysApprovals

Schedules

Schedule by PhaseCalendar DatesNumber of weeks or monthsLonger/Shorter schedule will result in fee increaseClient approval schedule

Meetings

Limit the number and frequency of meetings

Explicitly state the number of meetingsQuote a flat rate for additional meetings

Attend only the portion of the meeting that requires your participation

27

Meetings

Limit the number of attendeesSubstitute the proactive weekly report

Client Responsibilities

Designated Point of ContactProvide all of the needed informationTimely decisionsKeep up with their paper-work

ContractsChange ordersPayments

Bottom-Up BudgetingProposed Fee

Contingency

Project Expenses

Billing Rate

Estimated Hours

Deliverables/Task List

28

Top-Down BudgetingProposed Fee

Contingency

Project Expenses

Billing Rate

Estimated Hours

Deliverables/Task List

Circular BudgetingMaximum Fee

Contingency

Project Expenses

Billing Rate

Estimated Hours

What Can We Deliver?

Budgeting Reality Check

Percentage of Construction CostDesign Dollars per S.FPrevious ProjectsHours Per Drawing x Billing RateDollars Per Drawing

29

Client Communications

Be Proactive – Not ReactiveYou initiate most of the communication

Regular ScheduleAs far in advance as reasonably possibleTelephone call that you initiateRegular e-mail status reports

Status Report

Every week for active projects

Every 2-weeks to 1 month for less active projects

Status Report

Project Activity since last meetingMeetings attendedMilestone submissionsNew information Receive

Upcoming EventsMeetingsMilestone submissions

30

Status Report

Schedule IssuesIssues that may impact schedule

Client IssuesInformation needed from clientDecisions needed from client

Business IssuesApprovals neededAccounts Receivable

Project Progress Report

31

How Hard is this Job?

Staff

ConsultantsInterestGroups

Partners

Client

Project Manager

Project Business Reviews

Little or no preparation needed by project managerAccounting prepares the financial informationThe Project Manager, Partner in Charge, Controller, Managing Partner attend the MeetingFrequency is every two weeks

Same day of the weekSame time of the dayPut it in your calendar 1 year in advance

Project Business Reviews

At the meeting we reviewPercent Complete vs. Percent SpentOut of Scope WorkStaffingScheduleInvoicingAccounts Receivable

32

Percent Complete Vs. Percent Spent

Project as a whole or by phaseIf there is a variance, find out whyDevelop an action plan (who, what, when) to turn things aroundReview the action plan at next meeting

Out of Scope Work?

If yes, ask to see the contract so we can adjust budget.If no signed contract, ask what action the project manager intends to takeAsk when they intend to take actionAdd to the action list

Is Project on Schedule

If not why?Is the schedule delay beyond our control?What does the contract say about the schedule?How do we intend to notify the client that we need to be paid for our added time due to delaysAdd the intended action to the action list

33

Staffing?

What is the current level of project staffing?How long will we maintain this level?How can we adjust staffing to bring in line with budget?When will we adjust the staffing?Add to the action list

Accounts Receivable

Invoices over 45 days oldI ask the project manager to contact the client

Invoices over 60 days oldWhy hasn’t the client paid?What reason did the client give for not paying?

Invoicing

For projects invoiced as a percentage of completion

What percentage of completion will we be invoicing at month endIf near month end I will ask accounting to prepare the invoice

For hourly projectsHow much do you estimate we will invoice this month?

34

Accounts Receivable

Project Review Action List

Fee is 302k.35 weeks to go – 6 hours per week. Must keep involvement to a minimum.

Partner – Will put in claim for delays by Feb. 9th. $30 - $40k

60% CDHMCDeville Company3032.02

30% Complete DD & 36% Spent. Need DD decisions to be made. PM will submit a revised work plan by 2/12 to get us back on track

Will call consultants to submit their invoices

30% DDGFMUniversity Hall Basic Services

3022.02

RemarksInvoicingManagerProject NameProject #

Pathway to Profit™

Incentive Compensationfor 20%+ Profit

AEC Management Solutions, Inc.

35

Elements of a 20%+ Profit

Understanding the Financial FundamentalsProduce Timely & Accurate Project InformationStrategic PlanningCommunicationsCash Flow & CollectionsProject ManagementIncentive Compensation

The Big Question

Why Have Incentive Compensation?

Typical Reasons for Incentive Compensation

Lack of Firm-Wide ProfitabilityWide Disparity of Profits Between Partners Offices or Project ManagersSome are Consistently ProfitableSome are Consistently Losing MoneySome are In-BetweenAs a Whole there is Dissatisfaction With Financial Results

36

Pre-Requisites to an Effective Incentive Compensation Program

Confidence in Financial InformationTimely and Accurate Financial ReportingConfidence in Financial/Project Management SoftwareOpen Communication Between the PartnersRegular Project Financial Reviews Where Open Communication is EncouragedConfidence in Accounting Personnel

Issues Addressed

Bad DebtBilling RatesWorking Without ContractsAmbiguous Contract Language on FeesNot Getting Paid for Additional WorkLack of Real Incentive at the Partner LevelLack of Accountability at All Levels of CompanyInexperienced Project Managers

Big Picture

Differentiate Contribution as an Employee vs. Benefits of being an OwnerOwnership Provides a Return on Investment Such as an Increase in Capital Account or DividendEmployee Contribution is Rewarded with Salary, Benefits and Incentive Bonus

37

Benefits of Ownership

TitlePrestigePerksReturn on InvestmentInfluence on Direction of CompanyMore Control Over Career

Benefits of Employment

SalaryAnnual Increases in Salary on MeritBenefitsNo Risk of Investment

Successful Incentive Plans

Everyone Must Understand What Results are RewardedEconomic Contributions Receive Economic RewardsNon-Economic Efforts Receive Non-Economic Rewards100% Objective CriteriaConsistent Reinforcement of Rewarded ResultsRewards Must be Significant

38

Successful Incentive Plans-2

Should Encourage Recruitment & RetentionSimple to AdministerDoes not Encourage Counter Productive BehaviorOpportunity Exists for all Key Personnel to Earn an IncentiveDon’t Make it a Stealth PlanMake Sure Quality of Design is not CompromisedDon’t Limit the Incentive Amount!

Incentive Compensation Does Not Reward

EffortLong HoursSeniorityHow Much We Like YouHow Badly You Need the MoneyNon-Economic Contributions to the CompanyMeeting Minimum Performance Standards

Incentive Compensation Does Reward

Positive Economic ResultsProfitabilityIncreasing Value for the Stockholders

39

Distributing the Profits

Suggested Distribution for Initial Calculations

1/3 Stays in the Company to Fuel Growth1/3 Distributed to Partners as an Incentive1/3 Goes to Employees as a Bonus

Distribution of Profits

Company Profits

1/3 to RetainedEarnings

1/3 PartnersIncentive

1/3 to EmployeeIncentive Pool

Profit Pools

PartnerPool

Non-RevenuePartner Pool

RevenuePartner Pool

Rewarded forExceeding Target Profit

Rewarded on Pct.Of Relative Profit

40

Partners Incentive Pool

Non-Revenue Partners Not responsible for Revenue Producing Projects

Revenue PartnersResponsible for Revenue Producing Projects

Non-Revenue Partners

Responsible for Creating an Environment that Provides the Greatest Opportunity for the Long-Term Financial Success of the CompanyThey are Rewarded on the Basis of Firm-Wide ProfitsMinimum Profitability Standard Must be Exceeded Before a Bonus Distribution is Made

Non-Revenue Partner

A Minimum Expectation of Profit Percentage is Established

• We call this percentage the target profit• To the extent that profits exceed the

target profit, the non-revenue partner (typically the managing partner) receives a percentage of the excess.

• This percentage should be substantial• 50% for example

41

Non-Revenue Partner

Company Profits

Deduct Target Profit

Multiply Excess Profit by NR Partner Participation %

Revenue Partners

Rewarded on the Basis of Their Profit Centers Results as it Relates to the Firm-Wide Profit

• Partner A has a $20,000 profit• Partner B has a $50,000 profit• Partner C has a $30,000 profit

Therefore• Partner A is entitled to 20% of the revenue

partner profit pool• Partner B is entitled to 50% of the revenue

partner profit pool• Partner C is entitled to 30% of the revenue

partner profit pool

Revenue Partners

RevenuePartner

Pool

Partner A$20,000 Profit

Partner B$50,000 Profit

Partner C$30,000 Profit

20% of Profit Pool 50% of Profit Pool 30% of Profit Pool

42

Revenue Partners

In Making this Calculation Profit Center Losses are Ignored

• Partner A has a $30,000 profit• Partner B has a $70,000 profit• Partner C has a $50,000 loss

Therefore:• Partner A is entitled to 30% of the

revenue partner profit pool• Partner B is entitled to 70% of the

revenue partner profit pool• Partner C does not participate in the

distribution

Revenue Partners

RevenuePartner

Pool

Partner A$30,000 Profit

Partner B$70,000 Profit

Partner C$50,000 Loss

30% of Profit Pool 70% of Profit Pool Participates asEmployee

Revenue Partners

A Partner’s Bonus Will Not be Less Than They Would Earn as an Employee

43

Add Additional Modules as Needed

Project Manager Plan• Handle the same as the partner level plan• Establish a bonus pool• Project Managers compete for distributions

based upon their relative profitability

Location Based Plan• Handle the same as the non-revenue partner

level plan• Establish a target profit• Reward the person in charge of the office for

exceeding the target profit

Employee Bonus Pool

Divided into Sub-Pools for Employee CategoriesSenior AssociateAssociates & Project ManagersAll Other EmployeesWithin these Pools, Bonuses are Distributed According to Relative Salaries Earned During the Quarter

Employee Profit PoolsExample # 1

Employee Pool

Senior Staff Pool Project Managers Technical & Administrative Staff

Rewarded on Basis ofRelative Salaries

Rewarded on Basis ofRelative Salaries

Rewarded on Basis ofRelative Salaries

44

Employee Profit PoolsExample # 2

Employee Pool

Senior Staff Pool Project Managers Technical & Administrative Staff

Rewarded on SameBasis as Non-Rev.

Partner

Rewarded on SameBasis as

Revenue Partner

Rewarded on Basis ofRelative Salaries

Benefits of Incentive Plans

Employee RecruitmentEmployee RetentionEmployee MoraleGolden Handcuffs (Well Maybe Silver)Increased Contributions to Retirement Plan

What to Expect

Increased ProfitsIncreased Net MultiplierReduction of Unpaid Out of Scope ServicesIncreased RevenuePossible Change in Overhead

45

Rules to Live by

Company Must be Profitable Year to Date Before any Distributions are MadeIndividual Profit Centers Must be Profitable Year to Date Before any Distributions are Made to the PartnerAny Accounts Receivable Over 120 Days is Considered a Bad Debt for Purposes of the Incentive Bonus Plan

Rules to Live by

Collection of Accounts Receivable Over 120 Days Counts as Revenue in the Period it is CollectedIncentive Distributions are Made by the End of the Following QuarterEmployee Must be with Company when Bonus is Distributed

FAQ

Won’t This Cause Competition Among the Partners?Won’t this Cause Competition Among the Project Managers?Won’t This Cause Competition Among the Employees?Won’t Some Employees Leave the Company?

46

FAQ

What about Partners that don’t Manage Projects –but Make a Significant Contribution to the Company?Aren’t Some Markets/Clients Inherently Less Profitable?What about Project Managers that are Stuck with Lousy Clients, Contracts, Projects, Staff, Contractors, Associate Architects…..?

Implementation

Review Seminar Materials and Philosophy with Partners & Get Their Buy-InClean-up Your Financial ReportingStart Project Financial/Business ReviewsCalculate What Distributions Would Look Like Based Upon Past PerformanceStart Implementation at the Highest Level of Company

AEC Managrment Solutions, Inc.138

Implementation

Fine-Tune System to Meet Your Individual NeedsAfter Success at the Partner Level, Implement other levels of Accountability (Project Managers)Remember to Reward Economic Results With

Economic Rewards

47

Profit by Design Series

Incentive Compensation

Real World Examples© AEC Management Solutions, Inc.

All rights reserved. No part of this presentation may be reproduced or used in any form without the express written permission of the publisher

Company Profile # 1

Full Service Firm offering a range of Engineering and Architectural ServicesMultiple Offices (More than 5)Located Across Midwest and SouthEmployees 200+Ownership is Widely Dispersed with No One Person Owning More than 15%Profits were Historically 8% of Net Revenues

Challenges

Change the Firm Culture to Rewarding Results Rather that EffortProvide a Real Opportunity for Employees to Earn Significant Financial RewardsConvince a Majority of Shareholder’s to Approve the Plan

48

Incentive Pool

Non-Revenue PrincipalsNot responsible for Revenue Producing Projects

Revenue EmployeesResponsible for Revenue Producing Projects

Non-Revenue Principals

Responsible for Creating an Environment that Provides the Greatest Opportunity for the Long-Term Financial Success of the CompanyThey are Rewarded on the Basis of Firm-Wide ProfitsMinimum Profitability Standard Must be Exceeded Before a Bonus Distribution is Made

Non-Revenue Principals - 2

A Minimum Expectation of Profit Percentage is Established

• We call this percentage the target profit• To the extent that profits exceed the

target profit, the non-revenue employees receive a percentage of the excess.

• This percentage should be substantial

49

Distributing the Profits

1st 5% of Net Profit Stays in the Company to Fuel GrowthBalance of Profits is Divided into Pools

Non-Revenue Principals Office ManagersDiscipline LeadersProject ManagersEmployees

Distributing the Profits

Non-Revenue Partners receive 20% of profit in excess of 5%The remaining profit is then divided into equal pools of 25% each for

Office Managers (OM)Discipline Leaders (DL)Project Managers (PM)Employees (NT for non-titled)

Distributing the Profits

Each employee in the OM, DL, PM categories compete for their share of the profit distribution –Based upon Relative Profits

50

Profit Pools

Company Profits

1st 5% ProfitRemains in Company

Non-RevenuePrincipal Pool

Revenue Employee Profit Pool

Profit Pools

NR PrincipalsReceives 20% of Profit

In Excess of Target

CEO

55%

COO

35%

CFO

10%

Profit Pools

RevenueEmployees

Office Managers25% of ProfitDistribution

Discipline Leaders25% of ProfitDistribution

Project Managers25% of ProfitDistribution

Non-Titled25% of ProfitDistribution

51

Revenue Employees

Rewarded on the Basis of Their Profit Groups Results as it Relates to the Firm-Wide Profit

• Office Manager A has a $20,000 profit• Office Manager B has a $50,000 profit• Office Manager C has a $30,000 profit

Therefore• OM A is entitled to 20% of the Office Manager

profit pool• OM B is entitled to 50% of the Office Manager

profit pool• OM C is entitled to 30% of the Office Manager

profit pool

Revenue Employees

In Making this Calculation Profit Center Losses are Ignored

• Office Manager A has a $30,000 profit• Office Manager B has a $70,000 profit• Office Manager C has a $50,000 loss

Therefore:• OM A is entitled to 30% of the OM profit pool• OM B is entitled to 70% of the OM profit pool• OM C does not participate in the distribution

Revenue Employee

The Discipline Leader and Project Managers will compete for their share of the Incentive Distribution on the same basis as the Office Managers

An Non-Revenue Employee, Office Manager, Discipline Leaders or Project Managers Distribution, Will Not be Less Than They Would Earn as an Employee

52

Office Manager Profit PoolExample # 1

Office Managers

Office Mgr. A Office Mgr. B Office Mgr. C

$20,000 Profit $50,000 Profit $30,000 Profit

20% of Profit Pool 50% of Profit Pool 30% of Profit Pool

Office Manager Profit PoolExample # 2

Office Managers

Office Mgr. A Office Mgr. B Office Mgr. C

$30,000 Profit $70,000 Profit $50,000 Loss

30% of Profit Pool 70% of Profit Pool Participates as Employee

Employee Bonus Pool

Bonuses are Divided According to Relative Salaries Earned During the Quarter

53

Spot Bonuses

In order to recognize contributions to the company – that cannot be easily quantified, a spot bonus program was also adoptedExamples – Taking over a problem project, Helping to turn around an under performing office, landing a major new clientSpot bonuses are at the sole discretion of the Board of Directors

Rules to Live by

Company Must be Profitable Year to Date Before any Distributions are MadeIndividual OM, DL & PM Must be Profitable Year to Date Before any Distributions are Made to the PartnerAny Accounts Receivable Over 120 Days is Considered a Bad Debt for Purposes of the Incentive Bonus Plan

Rules to Live by

Collection of Accounts Receivable Over 120 Days Counts as Revenue in the Period it is CollectedIncentive Distributions are Made by the End of the Following QuarterEmployee Must be with Company when Bonus is Distributed

54

Results

The first quarter that this program was adopted, profits doubled when compared to the prior yearProfits rose from 8% of net revenues to 16% of net revenuesThe second quarter profits exceeded 20% of net revenues.

Company Profile #2

Architecture Firm serving a wide range of markets both domestic and internationalOne office175 EmployeesOwnership is somewhat dispersed.2 employees own a controlling interestProfits were historically low – less than 5% of net revenues

Challenges - 2

Differentiate Contribution as an Employee vs. Benefits of being an Owner

Convincing the majority owners to receive profits less than their percentage of ownership

55

Distribution of Profits

Company Profits

1/3 to RetainedEarnings

1/3 PartnersIncentive

1/3 to EmployeeIncentive Pool

Profit Pools

PartnerPool

Non-RevenuePartner Pool

RevenuePartner Pool

Rewarded forExceeding Target Profit

Rewarded on Pct.Of Relative Profit

Non-Revenue Partner

Company Profits

Deduct Target Profit

Multiply Excess Profit by NR Partner Participation %

56

Revenue Partners

RevenuePartner

Pool

Partner A$20,000 Profit

Partner B$50,000 Profit

Partner C$30,000 Profit

20% of Profit Pool 50% of Profit Pool 30% of Profit Pool

Revenue Partners

RevenuePartner

Pool

Partner A$30,000 Profit

Partner B$70,000 Profit

Partner C$50,000 Loss

30% of Profit Pool 70% of Profit Pool Participates asEmployee

Employee Profit PoolsExample # 1

Employee Pool

Senior Associates Associates &Project Managers

Technical & Administrative Staff

Rewarded on Basis ofRelative Salaries

Rewarded on Basis ofRelative Salaries

Rewarded on Basis ofRelative Salaries

Sr. AssociateAverage is

2 X Associate

Associate IncentiveAverage is

2 X Technical

Technical Incentive Average is

½ Associates

57

Results

The first quarter this program was implemented the profits increased to 16% of net revenuePlan has been in place for 4 years and annual profits have been well in excess of 20% of net revenuesBad Debt has virtually been eliminatedEvery Partner is now profitable

Results

Quarterly bonuses in excess of $100,000 to individual partners is now routineQuarterly bonuses to technical, associates and senior associates have been as high as $2,000, $4,000 and $8,000 respectivelyRetained profits in the company have enabled them to invest in the best equipment and software.

Taking Action

Review the materialsDecide which 3 actions would produce the most immediate benefitDecide on who is responsible and set a deadlineImplement those ideasRepeat the process

58

Contact Information

Herbert M. CannonAEC Management Solutions, Inc.183 Higgins RoadMatawan, NJ 07747

Phone: 732-705-5098

E-Mail: [email protected]

Subscribe to our free e-mail newsletterwww.aecmanagementsolutions.com