advisory board meeting fall 2013 - university of … · advisory board meeting – fall 2013...

TRANSCRIPT

Advisory Board Meeting – Fall 2013

December 2, 2013

Figures in millions USD (NYSE/NASDAQ-listed) or CAD (TSX-listed) except for share price or as noted

Agenda

2

Fall 2013 Student Team

Overview

Portfolio

Sell Recommendations

Hold Recommendations

Buy Recommendations

Future Initiatives

Macro Outlook

Portfolio Today

Click to edit Master title style

FALL 2013 TEAM

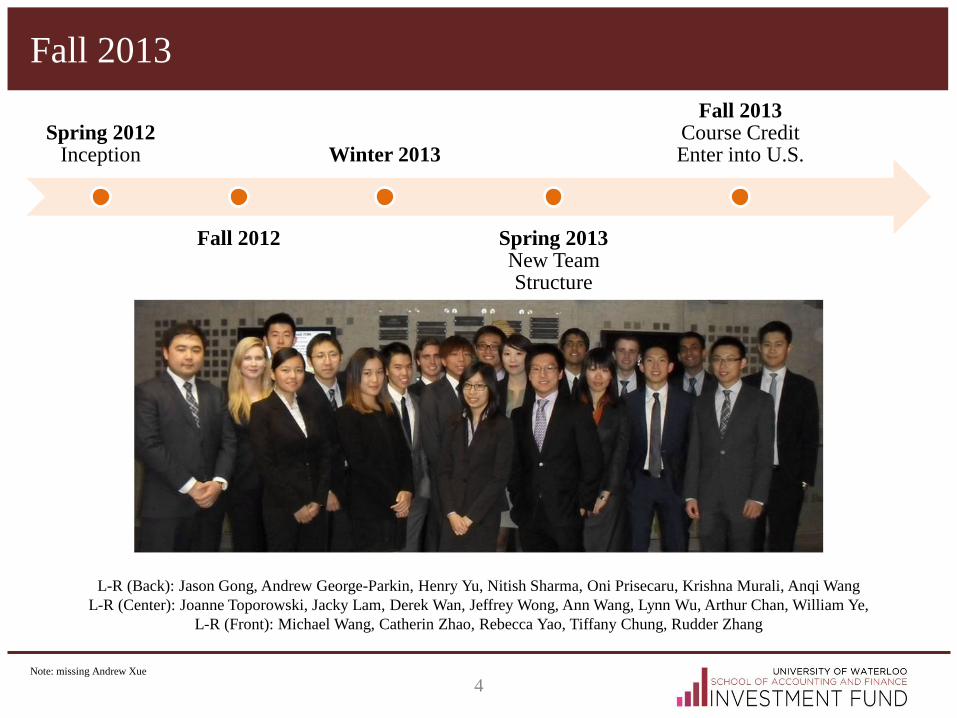

Fall 2013

4

Spring 2012 Inception

Fall 2012

Winter 2013

Spring 2013 New Team Structure

Fall 2013 Course Credit Enter into U.S.

L-R (Back): Jason Gong, Andrew George-Parkin, Henry Yu, Nitish Sharma, Oni Prisecaru, Krishna Murali, Anqi Wang

L-R (Center): Joanne Toporowski, Jacky Lam, Derek Wan, Jeffrey Wong, Ann Wang, Lynn Wu, Arthur Chan, William Ye,

L-R (Front): Michael Wang, Catherin Zhao, Rebecca Yao, Tiffany Chung, Rudder Zhang

Note: missing Andrew Xue

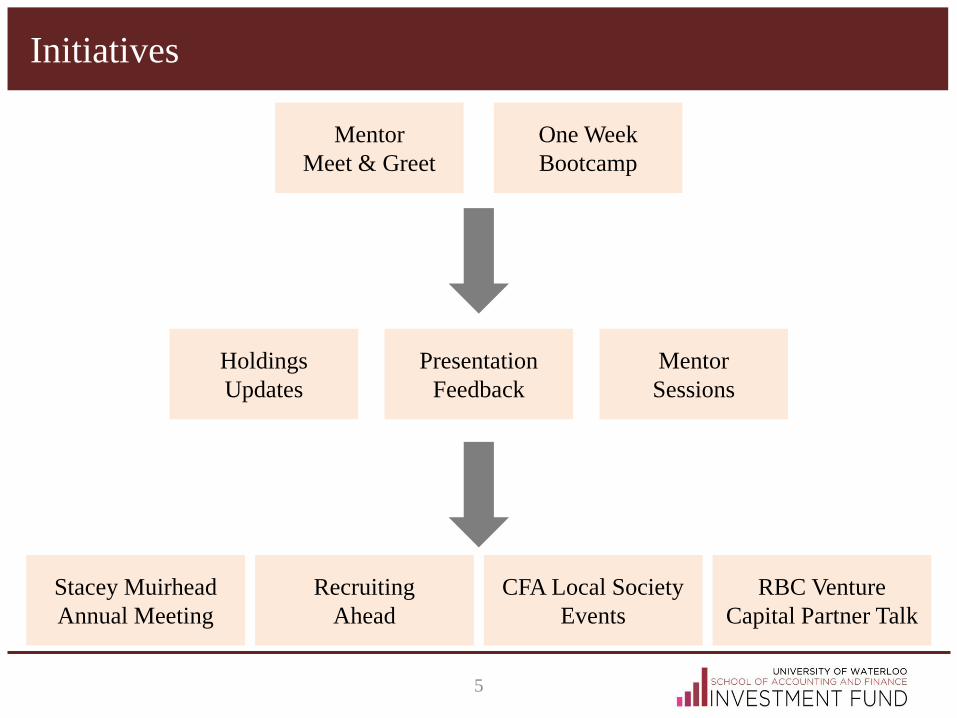

Initiatives

5

One Week

Bootcamp

Mentor

Meet & Greet

Presentation

Feedback

Holdings

Updates

Mentor

Sessions

Recruiting

Ahead

Stacey Muirhead

Annual Meeting

CFA Local Society

Events

RBC Venture

Capital Partner Talk

Click to edit Master title style

OVERVIEW

The Fund

7

Purpose

Objective

“To provide students with an investment management experience in an

institutional setting. Specifically, it will provide students hands-on-

training in equity valuation and portfolio management with guidance

from industry experts and with supervision by finance faculty.”

“To generate long-term growth of the Fund’s assets. The Fund will invest

in a broadly diversified portfolio of mid-to-large capitalization stocks of

Canadian1 issuers that may provide capital gains or income.”

1 The Fund is opening up to all North American issuers this term 2 A mix of S&P/TSX and S&P 500 going forward due to U.S stocks

Benchmark S&P / TSX Total Return Index2

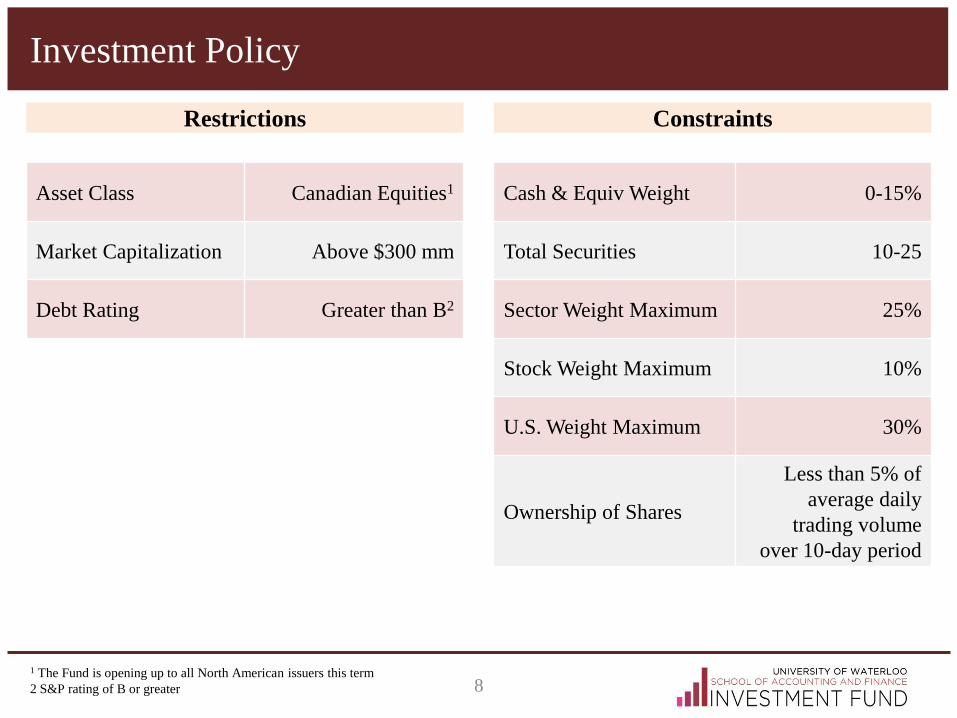

Investment Policy

8

Restrictions Constraints

Asset Class Canadian Equities1

Market Capitalization Above $300 mm

Debt Rating Greater than B2

Cash & Equiv Weight 0-15%

Total Securities 10-25

Sector Weight Maximum 25%

Stock Weight Maximum 10%

U.S. Weight Maximum 30%

Ownership of Shares

Less than 5% of

average daily

trading volume

over 10-day period

1 The Fund is opening up to all North American issuers this term

2 S&P rating of B or greater

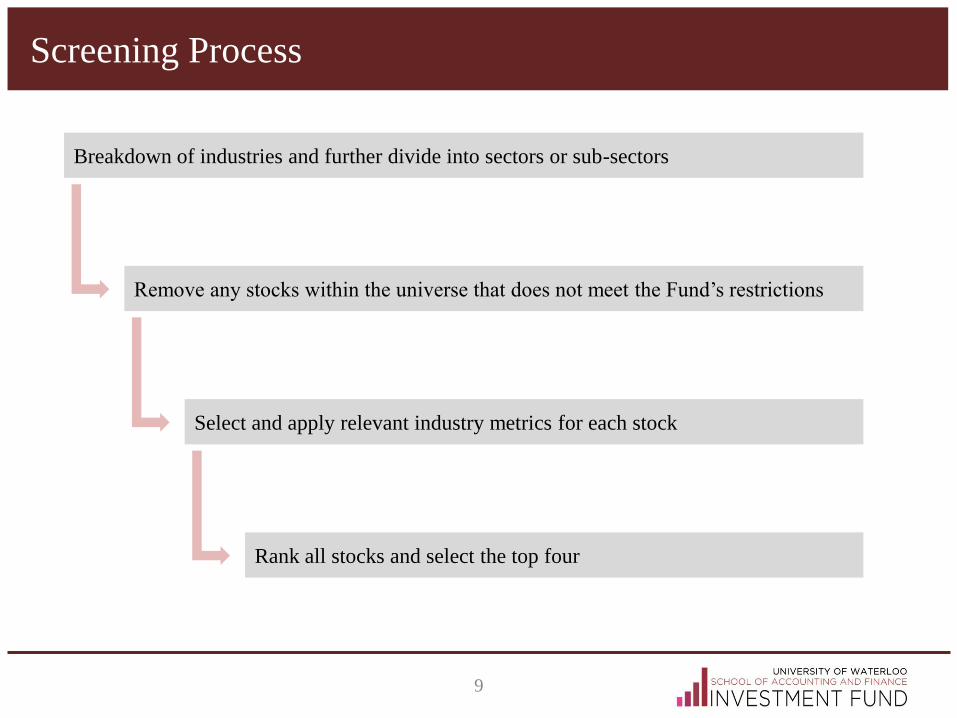

Screening Process

9

Breakdown of industries and further divide into sectors or sub-sectors

Select and apply relevant industry metrics for each stock

Remove any stocks within the universe that does not meet the Fund’s restrictions

Rank all stocks and select the top four

Click to edit Master title style

PORTFOLIO & MACRO

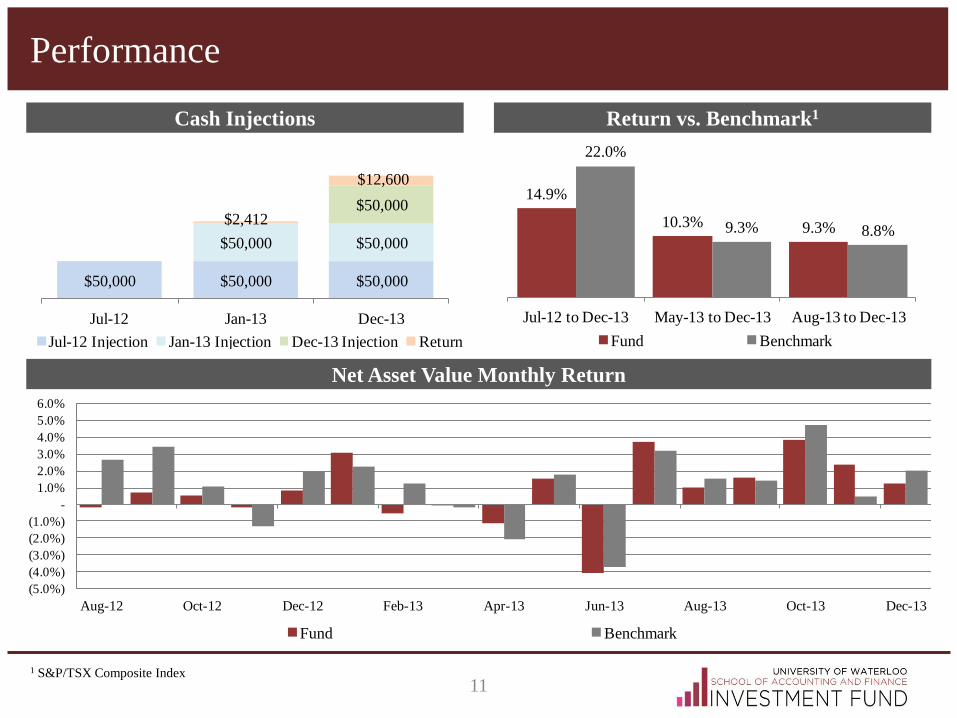

Performance

11

Net Asset Value Monthly Return

Cash Injections Return vs. Benchmark1

$50,000 $50,000 $50,000

$50,000 $50,000

$50,000$2,412

$12,600

Jul-12 Jan-13 Dec-13

Jul-12 Injection Jan-13 Injection Dec-13 Injection Return

1 S&P/TSX Composite Index

14.9%

10.3% 9.3%

22.0%

9.3% 8.8%

Jul-12 to Dec-13 May-13 to Dec-13 Aug-13 to Dec-13

Fund Benchmark

(5.0%)

(4.0%)

(3.0%)

(2.0%)

(1.0%)

-

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Aug-12 Oct-12 Dec-12 Feb-13 Apr-13 Jun-13 Aug-13 Oct-13 Dec-13

Fund Benchmark

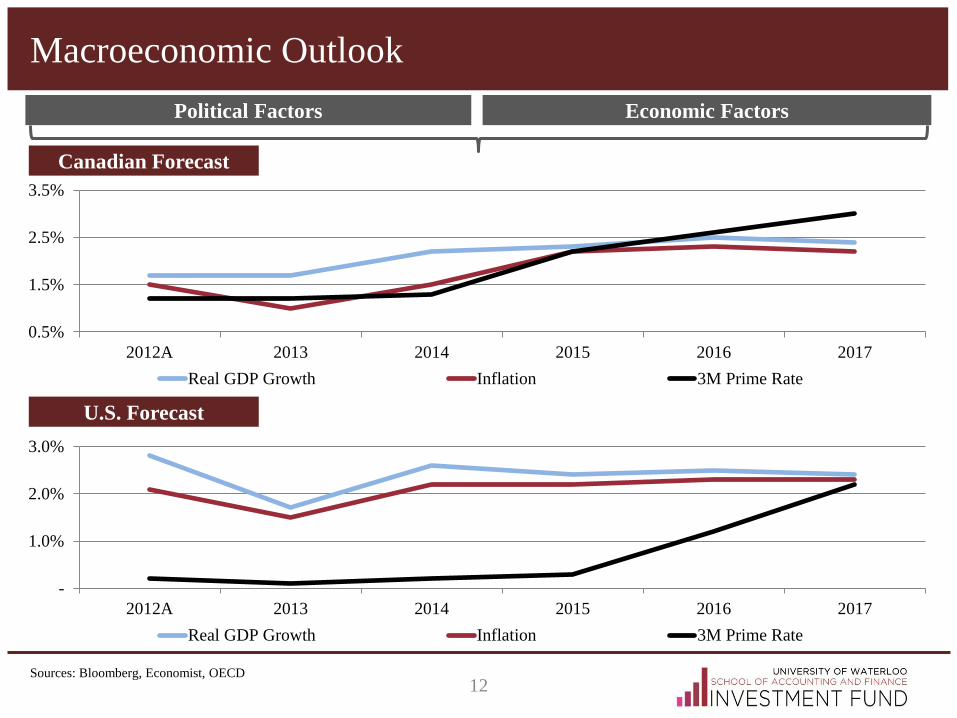

Macroeconomic Outlook

12

Political Factors Economic Factors

U.S. Forecast

Sources: Bloomberg, Economist, OECD

0.5%

1.5%

2.5%

3.5%

2012A 2013 2014 2015 2016 2017

Real GDP Growth Inflation 3M Prime Rate

-

1.0%

2.0%

3.0%

2012A 2013 2014 2015 2016 2017

Real GDP Growth Inflation 3M Prime Rate

Canadian Forecast

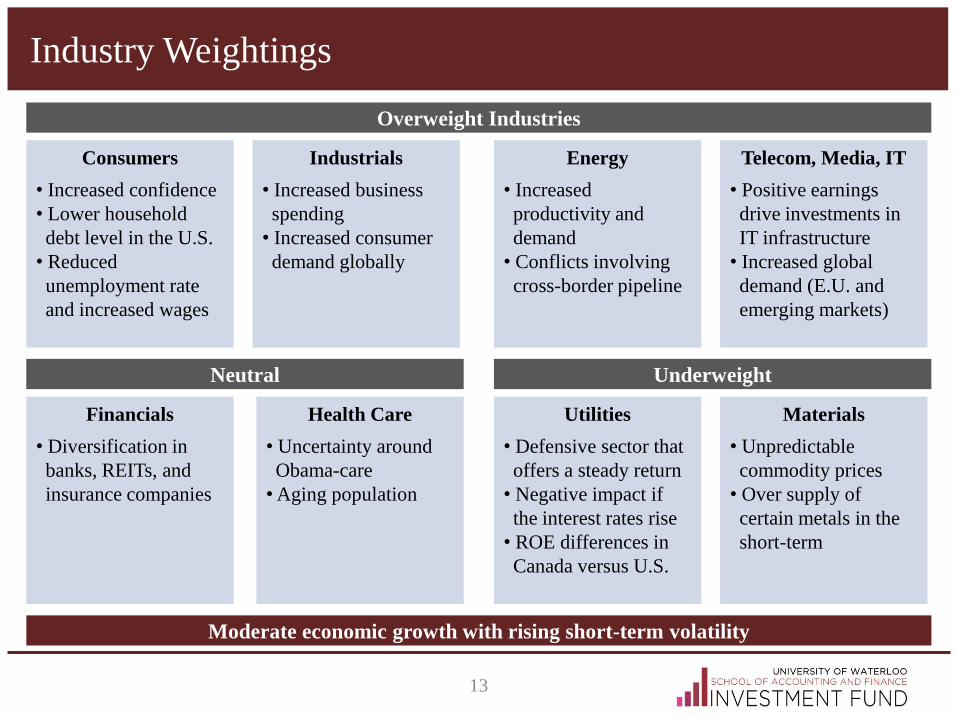

Industry Weightings

13

Overweight Industries

Consumers

• Increased confidence

• Lower household

debt level in the U.S.

• Reduced

unemployment rate

and increased wages

Neutral Underweight

Industrials

• Increased business

spending

• Increased consumer

demand globally

Energy

• Increased

productivity and

demand

• Conflicts involving

cross-border pipeline

Telecom, Media, IT

• Positive earnings

drive investments in

IT infrastructure

• Increased global

demand (E.U. and

emerging markets)

Financials

• Diversification in

banks, REITs, and

insurance companies

Utilities

• Defensive sector that

offers a steady return

• Negative impact if

the interest rates rise

• ROE differences in

Canada versus U.S.

Materials

• Unpredictable

commodity prices

• Over supply of

certain metals in the

short-term

Moderate economic growth with rising short-term volatility

Health Care

• Uncertainty around

Obama-care

• Aging population

Click to edit Master title style

SELL RECOMMENDATIONS

-

1

2

3

4

5

6

(40%)

(30%)

(20%)

(10%)

-

10%

20%

Aug-13 Sep-13 Oct-13 Nov-13

Volu

me

(mm

)

Ret

urn

MRE Volume MRE Return Sector Return

Martinrea International (TSX:MRE)

15

Stock Performance

Events Sell Rationale

A B

C

A

B

C

Aug 7, 2013 – Martinrea International announced

Q2 results slightly below expectations

Sept 27, 2013 – Ex Vice Chairman, Natale Rea

sues Martinrea on fraudulent management

Nov 7, 2013 – Martinrea International announced

Q3 results in line with expectations

Governance issues with respect to management as

current CEO was highly involved with alleged activity

Lower expected growth if Rea is successful in taking

over Martinrea given existing management expertise

High uncertainty with respect to timing and cost on

resolution of lawsuit

Nov 22, 2013 – Rea responds to counterclaim with

specific alleged magnitude of fraud D

D

1

1 S&P/TSX Composite Auto Parts & Equipment Index

Market Cap $750

Beta 0.94

Debt/Equity 47.3%

S&P Rating NR

Cost Value $4,953

Sold Value $3,773

Capital Gains (23.6%)

Dividend 0.3%

-

1

2

3

(10%)

(5%)

-

5%

Aug-13 Sep-13 Oct-13 Nov-13

Volu

me

(mm

)

Ret

urn

FTS Volume FTS Return Sector Return

Fortis (TSX:FTS)

16

Stock Performance

Events Sell Rationale

A

B

A

B Nov 1, 2013 – Q3 Earnings below expectations

with year-over-year decline of ROE due to

regulatory changes and continued issues from CH

Group

Continued issues integrating CH Group acquisition (i.e.

not capitalizing on higher allowed ROE within U.S.)

Revenue growth expected to be curbed significantly

limiting value with a target price of $31.75 (upside 2.4%)

Macro outlook moderately positive, underweight yield

stocks

Aug 1, 2013 – Q2 Earnings significantly below

expectations due to implementation issues with

respect to CH Group post-acquisition integration as

significant credits offered to U.S. customers

1

1 Dow Jones Canada Select Utility Index

Note: FTS is still in the portfolio with a limit sell of $31.75 GTC Dec 30, 2013

Market Cap $6,617

Beta 0.52

Debt/Equity 96.2%

S&P Rating A-

Cost Value $8,879

Sold Value $8,414

Capital Gains (5.2%)

Dividend 3.4%

-

1

2

3

(10%)

-

10%

20%

Aug-13 Sep-13 Oct-13 Nov-13

Volu

me

(mm

)

Ret

urn

NA Volume NA Return Sector Return

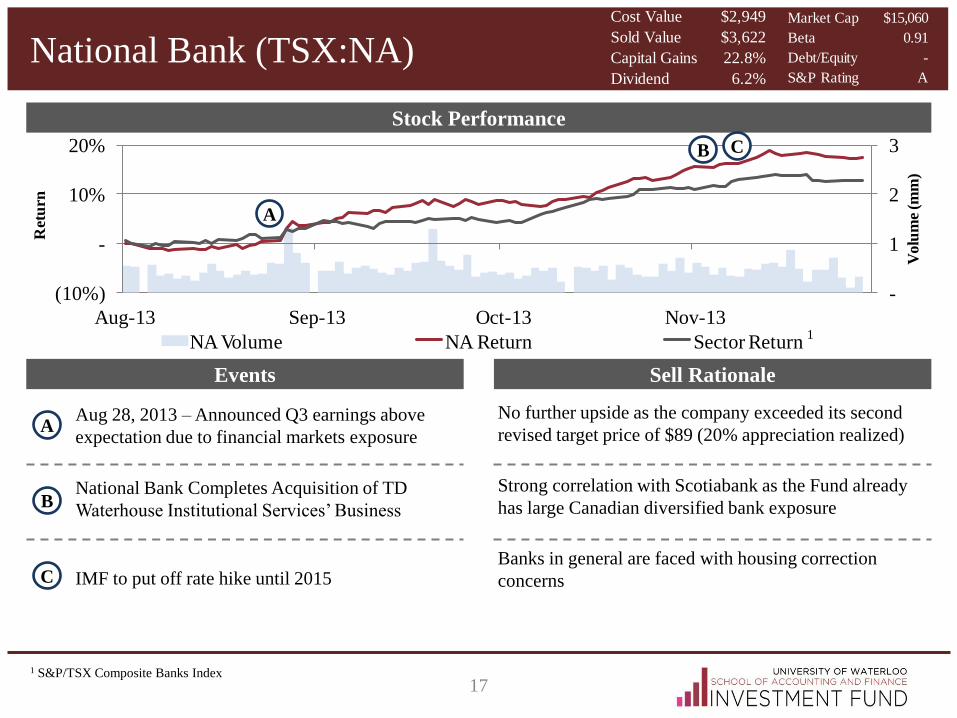

National Bank (TSX:NA)

17

Stock Performance

Events Sell Rationale

A

B National Bank Completes Acquisition of TD

Waterhouse Institutional Services’ Business

No further upside as the company exceeded its second

revised target price of $89 (20% appreciation realized)

Strong correlation with Scotiabank as the Fund already

has large Canadian diversified bank exposure

Banks in general are faced with housing correction

concerns

Aug 28, 2013 – Announced Q3 earnings above

expectation due to financial markets exposure

A

B

IMF to put off rate hike until 2015 C

C

1

1 S&P/TSX Composite Banks Index

Market Cap $15,060

Beta 0.91

Debt/Equity -

S&P Rating A

Cost Value $2,949

Sold Value $3,622

Capital Gains 22.8%

Dividend 6.2%

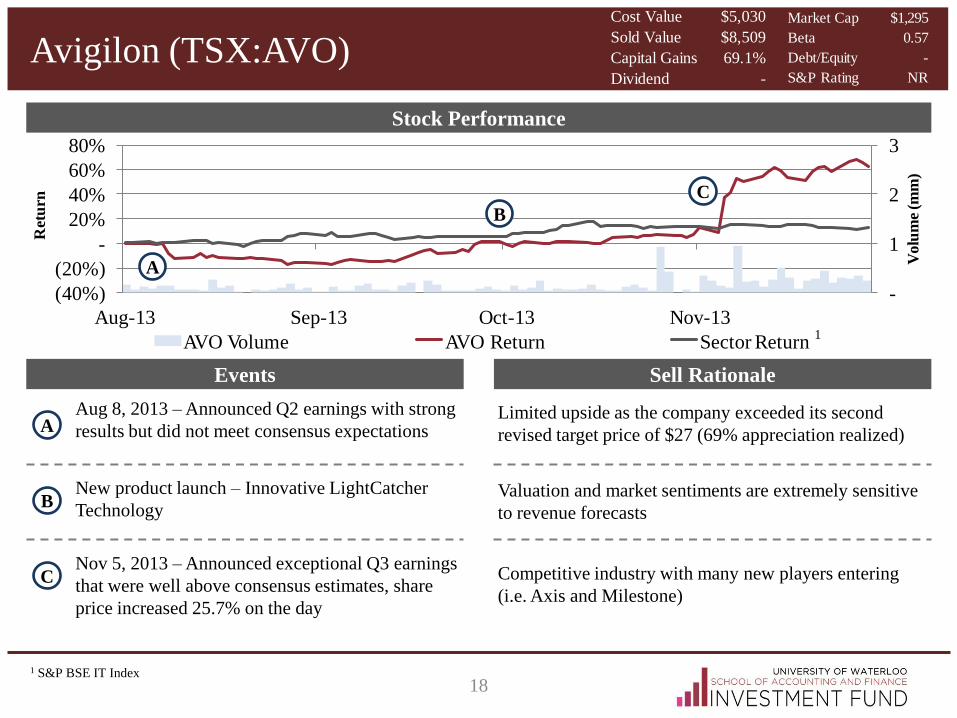

Avigilon (TSX:AVO)

18

Stock Performance

Events Sell Rationale

A

B New product launch – Innovative LightCatcher

Technology

Limited upside as the company exceeded its second

revised target price of $27 (69% appreciation realized)

Valuation and market sentiments are extremely sensitive

to revenue forecasts

Competitive industry with many new players entering

(i.e. Axis and Milestone)

Aug 8, 2013 – Announced Q2 earnings with strong

results but did not meet consensus expectations

Nov 5, 2013 – Announced exceptional Q3 earnings

that were well above consensus estimates, share

price increased 25.7% on the day

C

-

1

2

3

(40%)

(20%)

-

20%

40%

60%

80%

Aug-13 Sep-13 Oct-13 Nov-13

Volu

me

(mm

)

Ret

urn

AVO Volume AVO Return Sector Return1

1 S&P BSE IT Index

A

C

Market Cap $1,295

Beta 0.57

Debt/Equity -

S&P Rating NR

Cost Value $5,030

Sold Value $8,509

Capital Gains 69.1%

Dividend -

B

Baytex Energy (TSX:BTE)

19

Stock Performance

Events Sell Rationale

A

B Oct 2013 – Widening WSC-WTI differential where

WCS declined 12% but WTI declined 5.4% in

October

Significant production growth built into current price,

limited upside with high risk of not meeting targets

Sustainability of dividend reliant on realizing production

growth and WTI/WCS spread

History of earnings misses except in periods of

significant derivative gains of asset sales

Aug 30, 2013 – Baytex reaffirms production

outlook for year at 56k to 58k BOE/D

Reached updated target price which represents capital

gains of 4.1% and dividends of 1.6%

Oct 30, 2013 – Baytex reported above expected Q3

earnings results

C

-

1

2

3

4

5

(15%)

(10%)

(5%)

-

5%

10%

Aug-13 Sep-13 Oct-13 Nov-13

Volu

me

(mm

)

Ret

urn

BTE Volume BTE Return Sector Return1

1 S&P TSX Composite Oil and Gas Exploration Index

C

A

Market Cap $5,329

Beta 1.65

Debt/Equity 10.4%

S&P Rating BB

Cost Value $5,583

Sold Value $5,814

Capital Gains 4.1%

Dividend 1.6%

B

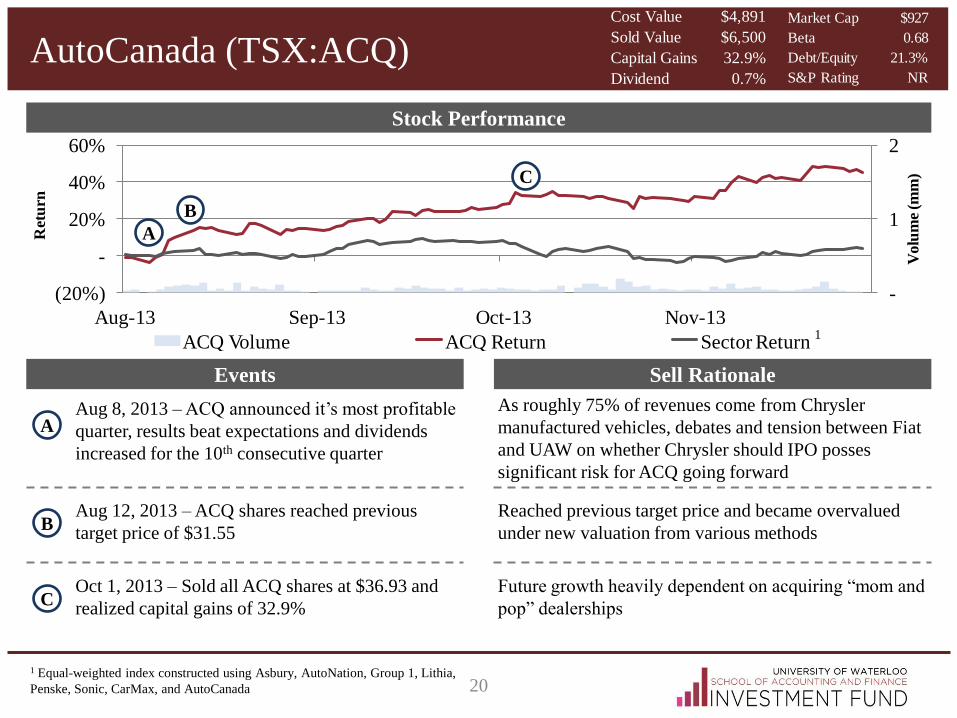

AutoCanada (TSX:ACQ)

20

Stock Performance

Events Sell Rationale

-

1

2

(20%)

-

20%

40%

60%

Aug-13 Sep-13 Oct-13 Nov-13

Volu

me

(mm

)

Ret

urn

ACQ Volume ACQ Return Sector Return1

1 Equal-weighted index constructed using Asbury, AutoNation, Group 1, Lithia,

Penske, Sonic, CarMax, and AutoCanada

A

B

C

A

B Aug 12, 2013 – ACQ shares reached previous

target price of $31.55

Aug 8, 2013 – ACQ announced it’s most profitable

quarter, results beat expectations and dividends

increased for the 10th consecutive quarter

Oct 1, 2013 – Sold all ACQ shares at $36.93 and

realized capital gains of 32.9% C

As roughly 75% of revenues come from Chrysler

manufactured vehicles, debates and tension between Fiat

and UAW on whether Chrysler should IPO posses

significant risk for ACQ going forward

Reached previous target price and became overvalued

under new valuation from various methods

Future growth heavily dependent on acquiring “mom and

pop” dealerships

Market Cap $927

Beta 0.68

Debt/Equity 21.3%

S&P Rating NR

Cost Value $4,891

Sold Value $6,500

Capital Gains 32.9%

Dividend 0.7%

Click to edit Master title style

HOLD RECOMMENDATIONS

Hold Recommendations

22

Click to edit Master title style

BUY RECOMMENDATIONS

AGCO (NYSE:AGCO)

24

Valuation

Company Overview Share Performance

Drivers & Risks

Manufacturer and distributor of agricultural equipments and parts

Revenue by Geography Revenue by Segment

N.A.

26%

S.A.

19%

EM

EA

51%

APJ

5%

EMEA51%

Drivers

Risks

Russian joint-venture to capitalize on growing market

Progress on 2015 goal of 10% operating margins

Strategic partnership in India

Increasing storage and consumption

High correlation with row crop prices

Dependent on size and nature of government subsidies

Acquisitions have negatively impacted margins

Country risk – expected to have operations in Russia

Financing heavily dependent on partner, Radobank

Base Bear Bull

WACC 8.6% 8.6% 8.6%

Revenue CAGR 7.3% 4.3% 7.9%

Exit Multiple 5.5x 5.5x 5.5x

Perpetuity Growth 2.0% 2.0% 2.0%

Implied Share Price $68.34 $54.48 $85.77

Weighting 80% 10% 10%

Target price $68.70

Current Price $58.28

Upside 17.9%

-

2

4

6

8

(80%)

(40%)

-

40%

80%

2008 2009 2010 2011 2012 2013

Vo

lum

e (m

m)

Ret

urn

AGCO Volume AGCO Return Sector Return1

1 SPDR Industrial Sector Select Index

Market Cap $5,674

Beta 1.27

Debt/Equity 8.9%

S&P Rating BBB-

Parts

13%

Mac

hinar

y …

Othe

r

14% Tractors

59%

Other

14%

Machi-

nery

14%

Alaska Air Group (NYSE:ALK)

25

Valuation

Company Overview Share Performance

Drivers & Risks

Legacy airline company operating primarily in the U.S.

Revenue by Segment Financials

Drivers

Risks

Mai

nline

76%

Regi

onal

16%

Hori

zon

7%

Mainline

76%

Horizon

7%Regional

16%

UAL merger opens East Coast slots due to Department of

Justice settlement on anti-trust lawsuit

Improving margins generated by year-over-year

decreases in cost per available seat mile

CEO transition – William Ayers expected to step down in

early 2014

Significant decreases in hedge profile for fuel

Salaries and wages continue to rise with industry

Delta Airlines expanding into core route offerings

-

2

4

6

8

(200%)

-

200%

400%

600%

2008 2009 2010 2011 2012 2013

Vo

lum

e (m

m)

Ret

urn

Alaska Volume Alaska Return Sector Return1

1 NYSE ARCA Airline Index

DCF EV/EBITDA P/E

WACC 7.6%

Revenue CAGR 6.2%

Exit Multiple 5.5x

Terminal Growth 2.5%

Multiple 5.9x 20.7x

Share Price $86.81 $88.07 $140.00

Weighting 85.0% 7.5% 7.5%

Target Price $91.00

Current Price $77.74

Upside 17.1%

Market Cap $5,402

Beta 1.05

Debt/Equity -

S&P Rating BB

Enterprise Value $4,902

52 Week Range $42.05-$78.53

EV/EBITDA 5.6x

P/E 11.7x

Beta 5Y 0.96

Revenue CAGR 5Y 6.20%

Dundee REIT (TSX:D.UN)

26

Valuation

Company Overview Share Performance

Drivers & Risks

One of the largest Canadian REITs renting office buildings

Gross Leasable Area (24mm Sq. Ft)

Drivers

Risks

High quality portfolio

Consistently above average occupancy rates

Stable dividend yield

Lease rollover

Oversupply of office property

Increase in interest rate

Calgary

16%Ottawa

5%

Montreal

4%GTA

39%

KW

4%

Edmonton

6%

Other

26%

-

1

2

3

4

(100%)

(50%)

-

50%

100%

2008 2009 2010 2011 2012 2013

Vo

lum

e (m

m)

Ret

urn

Dundee Volume Dundee Return Sector Return1

1 iShares S&P TSX Capped REIT Index

Net Asset Value P/FFO P/AFFO

Capitalization Rate 6.9%

Multiple 11.9x 12.9x

Share Price $33.75 $31.76 $31.76

Weighting 50% 25% 25%

Target Price $33.49

Purchased Price $28.00

Upside 19.6%

Dividend Yield 7.8%

Market Cap $3,035

Beta 0.37

Debt/Equity 90.8%

S&P Rating BBB-

ProAssurance (NYSE:PRA)

27

Valuation

Company Overview Share Performance

Drivers & Risks

Medical Malpractice Insurer operating in the U.S.

Drivers

Risks

Diversified insurer with a low combined ratio

Tort reform and legal developments

History of successful acquisition growth

Consolidation in the Industry

Unpredictability of Reserve Developments

Decrease in interest rates

Physicians

78%

Healthcare

5%

Legal

3%

Other

14%

Premiums by Segment ($554 mm)

-

1

2

3

4

5

(100%)

(50%)

-

50%

100%

150%

2008 2009 2010 2011 2012 2013

Vo

lum

e (m

m)

Ret

urn

ProAssurance Volume ProAssurance Return Sector Return

DCF P/TBV P/BV P/E

Cost of Equity 7.2%

Terminal Growth 1.0%

Multiple 1.4x 1.2x 15.0x

Share Price $57.67 $53.30 $46.16 $49.01

Weighting 50% 17% 17% 17%

Target Price $53.58

Current Price $48.08

Upside 11.44%

Dividend Yield 2.10%

Market Cap $2,965

Beta 0.49

Debt/Equity 0.2%

S&P Rating BBB+

11.4%

1

1 iShares Dow Jones U.S. Insurance Index ETF

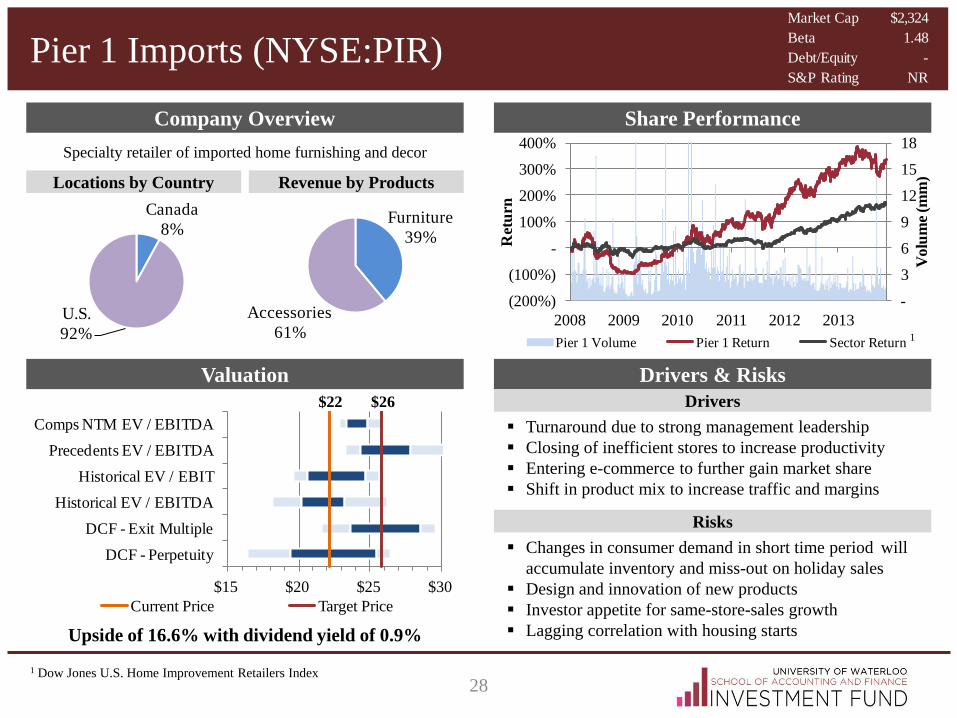

Pier 1 Imports (NYSE:PIR)

28

-

3

6

9

12

15

18

(200%)

(100%)

-

100%

200%

300%

400%

2008 2009 2010 2011 2012 2013

Vo

lum

e (m

m)

Ret

urn

Pier 1 Volume Pier 1 Return Sector Return

Valuation

Company Overview Share Performance

Drivers & Risks

Specialty retailer of imported home furnishing and decor

Drivers

Risks

Turnaround due to strong management leadership

Closing of inefficient stores to increase productivity

Entering e-commerce to further gain market share

Shift in product mix to increase traffic and margins

Changes in consumer demand in short time period will

accumulate inventory and miss-out on holiday sales

Design and innovation of new products

Investor appetite for same-store-sales growth

Lagging correlation with housing starts

1

1 Dow Jones U.S. Home Improvement Retailers Index

U.S.

92%

Canada

8%

Locations by Country Revenue by Products

$22 $26

$15 $20 $25 $30

DCF - Perpetuity

DCF - Exit Multiple

Historical EV / EBITDA

Historical EV / EBIT

Precedents EV / EBITDA

Comps NTM EV / EBITDA

Current Price Target Price

Upside of 16.6% with dividend yield of 0.9%

Furniture

39%

Accessories

61%

Market Cap $2,324

Beta 1.48

Debt/Equity -

S&P Rating NR

Cogeco Cable (TSX:CCA)

29

Valuation Drivers & Risks

11th largest hybrid fiber coaxial cable operator in North America

Ownership Breakdown Revenue by Products

Drivers

Risks

Strong organic and acquisition growth in the industry

Exclusive partnerships will lead to competitive advantage

Effective cost management to steadily increase margins

Unique ownership structure and solid management team

Competitive industry with rapid technological

developments (i.e. over-the-top content)

Regulation changes in Canada and the U.S.

Switch from landline to mobile telephony

Incremental increases in integration cost

Company Overview Share Performance

1

1 S&P Global Telecom Index

-

1

2

3

4

5

(60%)

(40%)

(20%)

-

20%

40%

2008 2009 2010 2011 2012 2013

Vo

lum

e (m

m)

Ret

urn

Cogeco Volume Cogeco Return Sector Return

Cabl

e

U.…

Cable

Canada

72%

Cable

U.S.

16%

Services

12%

Market Cap $2,339

Beta 0.58

Debt/Equity 97.3%

S&P Rating BB+

Major DCF Assumptions (100% DCF Value)

5-year revenue CAGR 5.5%

5-year EBITDA CAGR 5.0%

WACC 5.9%

Terminal Multiple 5.5x

Target price $54.00

Current Price $47.88

Upside 12.8%

Dividend Yield 2.2%

Letk

o

Br…

Othe

r

18%Cogeco

32%

Other

14%

Letko

Brosseau

10%Rogers

40%

Click to edit Master title style

OTHER STOCK PITCHES

Other Stock Pitches

31

Click to edit Master title style

PORTFOLIO TODAY

Portfolio Today (December 2, 2013)

33

Limit Sell

Sell Fortis at $31.75 ($31.15 as of Nov 29, 2013)

U.S. Stocks

Currently awaiting approval on W8-BEN form to purchase

U.S. listed stocks. High likelihood of trade execution

Alaska Air Group

AGCO

ProAssurance

Pier 1 Imports

Ticker Name Shares Price Value Return

AGU Agrium 50 $95.61 $4,781 (4.1%)

AX.UN Artis REIT 350 $14.40 $5,040 1.7%

BNS Scotiabank 124 $65.21 $8,086 18.5%

BDI Black Diamond 239 $29.50 $7,051 44.3%

CCO Cameco 238 $21.54 $5,127 2.9%

CPX Capital Power 453 $20.90 $9,468 0.7%

CCA Cogeco Cable 105 $48.04 $5,044 0.2%

D.UN Dundee REIT 180 $28.00 $5,040 (0.1%)

FTS Fortis 265 $31.15 $8,255 (2.8%)

G Goldcorp 240 $23.65 $5,676 (34.1%)

NA National Bank 54 $92.46 $4,993 21.6%

SU Suncor Energy 260 $36.42 $9,469 17.9%

VRX Valeant 53 $114.46 $6,066 21.4%

Market Value $84,096

Cash $27,064

Total Portfolio $111,160

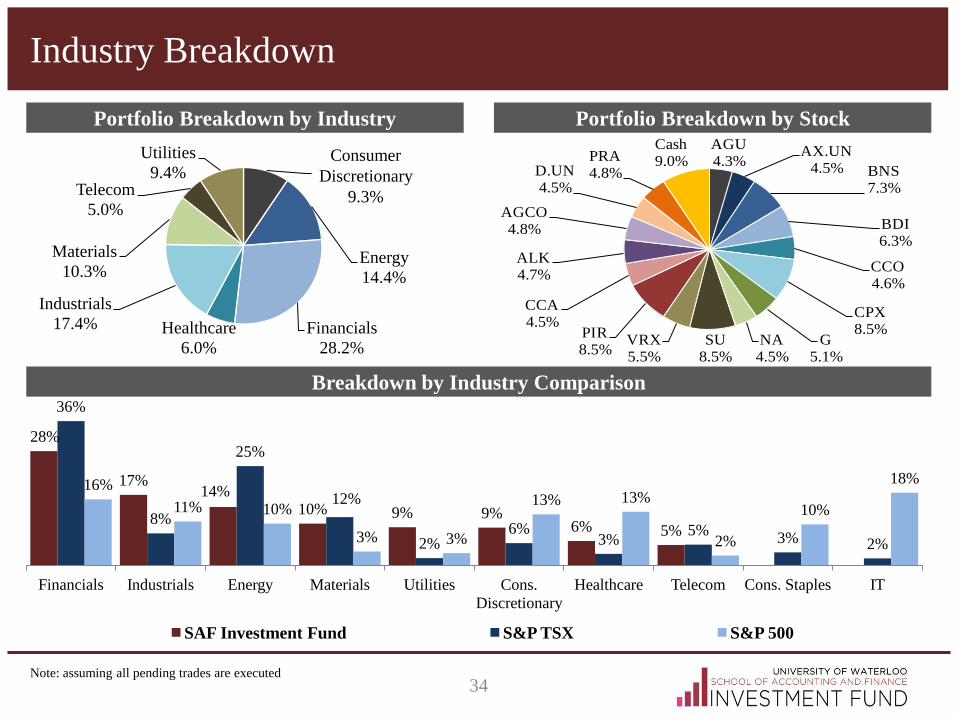

AGU4.3%

AX.UN4.5%

BNS7.3%

BDI6.3%

CCO4.6%

CPX8.5%

CCA4.5%

D.UN4.5%

FTS7.4%

G5.1%

NA4.5%

SU8.5%

VRX5.5%

Cash24.3%

Unexecuted Trades

Portfolio Breakdown

Industry Breakdown

34 Note: assuming all pending trades are executed

AGU4.3%

AX.UN4.5% BNS

7.3%

BDI6.3%

CCO4.6%

CPX8.5%

G5.1%

NA4.5%

SU8.5%

VRX5.5%

PIR8.5%

CCA4.5%

ALK4.7%

AGCO4.8%

D.UN4.5%

PRA4.8%

Cash9.0%

28%

17% 14%

10% 9% 9% 6% 5%

36%

8%

25%

12%

2% 6%

3% 5%

3% 2%

16%

11% 10%

3% 3%

13% 13%

2%

10%

18%

Financials Industrials Energy Materials Utilities Cons.

Discretionary

Healthcare Telecom Cons. Staples IT

SAF Investment Fund S&P TSX S&P 500

Consumer

Discretion

ary

9.3%

Energy

14.4%

Financials

28.2%

Healthcare

6.0%

Industrials

17.4%

Materials

10.3%

Telecom

5.0%

Utilities

9.4% Consumer

Discretionary

9.3%

Portfolio Breakdown by Industry Portfolio Breakdown by Stock

Breakdown by Industry Comparison

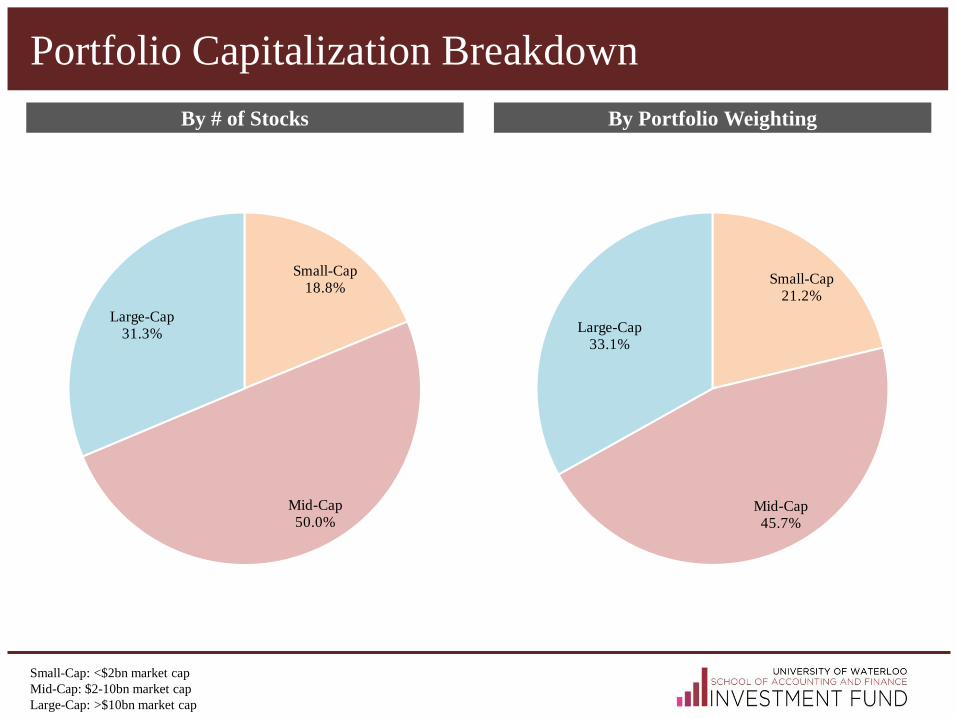

Portfolio Capitalization Breakdown

By # of Stocks By Portfolio Weighting

Small-Cap18.8%

Mid-Cap50.0%

Large-Cap31.3%

Small-Cap21.2%

Mid-Cap45.7%

Large-Cap33.1%

Small-Cap: <$2bn market cap

Mid-Cap: $2-10bn market cap

Large-Cap: >$10bn market cap

Portfolio Breakdown by Sub-sector

Versus S&P / TSX Versus S&P 500

Sub-Sector Index Fund

Oil, Gas and Consumable Fuels 24.0% 14.4%

Commercial Banks 20.3% 13.0%

Real Estate Investment Trusts (REITs) 2.2% 9.9%

Independent Power Producers and

Energy Traders 0.6% 9.4%

Specialty Retail 0.1% 9.4%

Commercial Services and Supplies 0.4% 6.9%

Pharmaceuticals 2.1% 6.1%

IT Services 0.8% 5.6%

Insurance 8.6% 5.3%

Machinery 0.1% 5.3%

Airlines 0.3% 5.2%

Media 3.2% 5.0%

Chemicals 2.7% 4.7%

Sub-Sector Index Fund

Oil, Gas and Consumable Fuels 8.2% 14.4%

Commercial Banks 2.8% 13.0%

Real Estate Investment Trusts (REITs) 1.9% 9.9%

Independent Power Producers and

Energy Traders 0.1% 9.4%

Specialty Retail 2.3% 9.4%

Commercial Services and Supplies 0.5% 6.9%

Pharmaceuticals 5.7% 6.1%

IT Services 3.8% 5.6%

Insurance 3.0% 5.3%

Machinery 1.7% 5.3%

Airlines 0.2% 5.2%

Media 3.7% 5.0%

Chemicals 2.5% 4.7%

Risk & Return

Note: assuming Fortis is sold and U.S. stocks are purchased

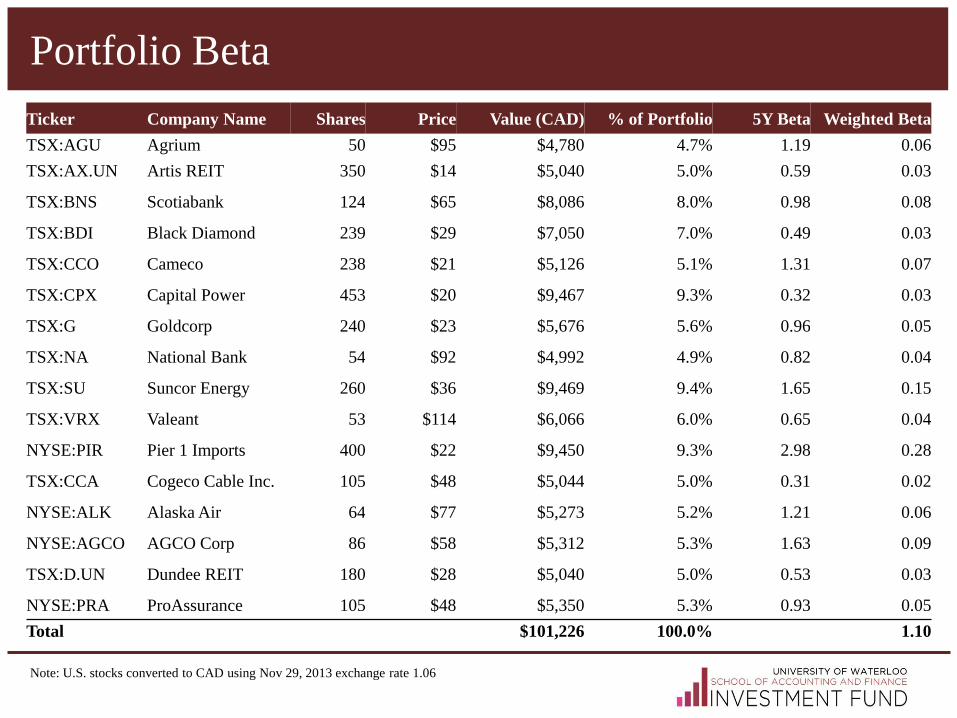

Beta 1.10

Variance 5.5%

Expected Return 11.0%

Sharpe 0.35

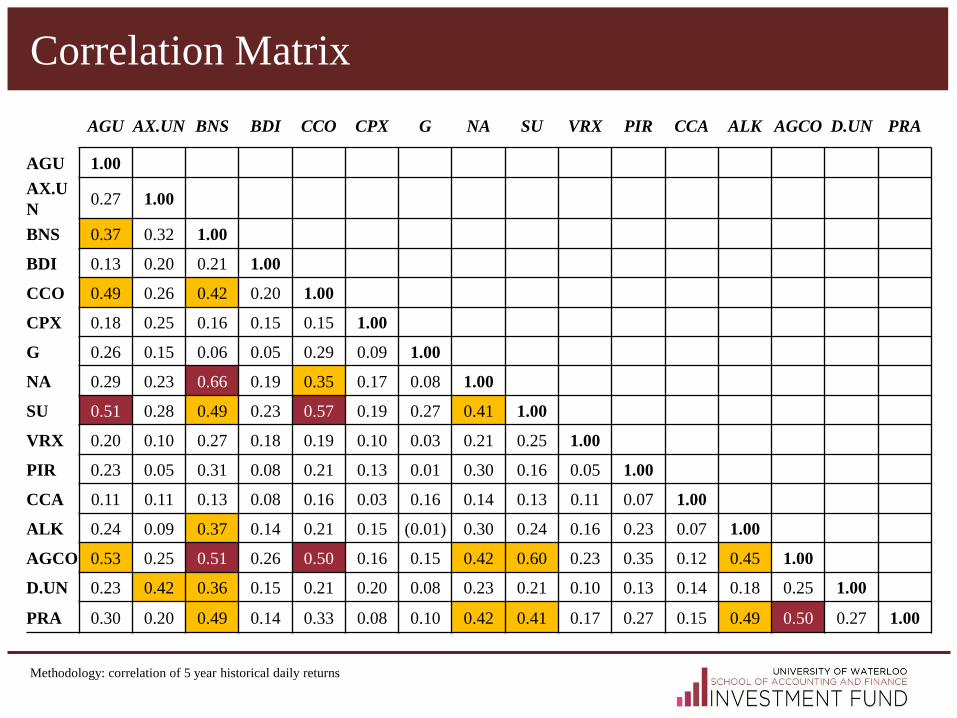

NA & BNS 0.66

SU & CCO 0.57

AGCO & AGU 0.53

SU & AGU 0.51

Canadian

Equities

74.9%

U.S.

Equities

25.1%

Total Return Breakdown by Listing Country

Correlation Analysis

Cumulative NAV Return

(5.0%)

-

5.0%

10.0%

15.0%

20.0%

25.0%

Jul-12 Sep-12 Nov-12 Jan-13 Mar-13 May-13 Jul-13 Sep-13 Nov-13

Fund Benchmark

Pipeline of Initiatives

38

Factor Analysis Analyst Sector

Allocation Executive Transition

Capital IQ Templates Alerts

Industry Mentors

39

Mike Williams Jin Li

Dan Lavric Lu Jiang

Niall Glynn Aly Hadibhai

Ohad Lederer

Kevin Huynh

Simon Kwan

David Middleton

Dorena Tu

Meng Wang

Ian Gutwinski Derek Chu

Ray Wan Joey Zhang

Partners

Faculty

Alan Douglas Craig Geoffrey Ranjini Jha Andrew Ecclestone

Advisory Board

Anish Chopra John Gort Jeffrey Stacey Aazar Zafar Thomas Scott Dennis Huber

Final Questions

Click to edit Master title style

APPENDIX

Correlation Matrix

AGU AX.UN BNS BDI CCO CPX G NA SU VRX PIR CCA ALK AGCO D.UN PRA

AGU 1.00

AX.U

N 0.27 1.00

BNS 0.37 0.32 1.00

BDI 0.13 0.20 0.21 1.00

CCO 0.49 0.26 0.42 0.20 1.00

CPX 0.18 0.25 0.16 0.15 0.15 1.00

G 0.26 0.15 0.06 0.05 0.29 0.09 1.00

NA 0.29 0.23 0.66 0.19 0.35 0.17 0.08 1.00

SU 0.51 0.28 0.49 0.23 0.57 0.19 0.27 0.41 1.00

VRX 0.20 0.10 0.27 0.18 0.19 0.10 0.03 0.21 0.25 1.00

PIR 0.23 0.05 0.31 0.08 0.21 0.13 0.01 0.30 0.16 0.05 1.00

CCA 0.11 0.11 0.13 0.08 0.16 0.03 0.16 0.14 0.13 0.11 0.07 1.00

ALK 0.24 0.09 0.37 0.14 0.21 0.15 (0.01) 0.30 0.24 0.16 0.23 0.07 1.00

AGCO 0.53 0.25 0.51 0.26 0.50 0.16 0.15 0.42 0.60 0.23 0.35 0.12 0.45 1.00

D.UN 0.23 0.42 0.36 0.15 0.21 0.20 0.08 0.23 0.21 0.10 0.13 0.14 0.18 0.25 1.00

PRA 0.30 0.20 0.49 0.14 0.33 0.08 0.10 0.42 0.41 0.17 0.27 0.15 0.49 0.50 0.27 1.00

Methodology: correlation of 5 year historical daily returns

Portfolio Beta

Note: U.S. stocks converted to CAD using Nov 29, 2013 exchange rate 1.06

Ticker Company Name Shares Price Value (CAD) % of Portfolio 5Y Beta Weighted Beta

TSX:AGU Agrium 50 $95 $4,780 4.7% 1.19 0.06

TSX:AX.UN Artis REIT 350 $14 $5,040 5.0% 0.59 0.03

TSX:BNS Scotiabank 124 $65 $8,086 8.0% 0.98 0.08

TSX:BDI Black Diamond 239 $29 $7,050 7.0% 0.49 0.03

TSX:CCO Cameco 238 $21 $5,126 5.1% 1.31 0.07

TSX:CPX Capital Power 453 $20 $9,467 9.3% 0.32 0.03

TSX:G Goldcorp 240 $23 $5,676 5.6% 0.96 0.05

TSX:NA National Bank 54 $92 $4,992 4.9% 0.82 0.04

TSX:SU Suncor Energy 260 $36 $9,469 9.4% 1.65 0.15

TSX:VRX Valeant 53 $114 $6,066 6.0% 0.65 0.04

NYSE:PIR Pier 1 Imports 400 $22 $9,450 9.3% 2.98 0.28

TSX:CCA Cogeco Cable Inc. 105 $48 $5,044 5.0% 0.31 0.02

NYSE:ALK Alaska Air 64 $77 $5,273 5.2% 1.21 0.06

NYSE:AGCO AGCO Corp 86 $58 $5,312 5.3% 1.63 0.09

TSX:D.UN Dundee REIT 180 $28 $5,040 5.0% 0.53 0.03

NYSE:PRA ProAssurance 105 $48 $5,350 5.3% 0.93 0.05

Total $101,226 100.0% 1.10