adopted annual budget - montrose high school ... teacher salary schedules ... superintendent’s...

TRANSCRIPT

INTRODUCTORY SECTION 2014 – 2015 BUDGET

Montrose County School District RE-1J | INTRODUCTORY SECTION 1

MONTROSE COUNTY SCHOOL DISTRICT RE-1J

2014-15

Adopted Annual Budget For the Fiscal Year Ended June 30, 2015

Submitted by the Superintendent and the Finance Department

P O B O X 1 0 , 0 0 0 | M O N T R O S E | C O L O R A D O | U S A | 8 1 4 0 2 W W W . M C S D . O R G

Montrose County School District RE-1J | i

Table of Contents

INTRODUCTORY SECTION ................................................................................... 1

Board of Education / District Office Administration ........................................................................ 2

Superintendent’s Budget Transmittal Letter ................................................................................... 3

The District Strategic Plan ................................................................................................................ 5

Executive Budget Summary ............................................................................................................. 6

Introduction ........................................................................................................................ 6

Demographics ..................................................................................................................... 6

Overview ............................................................................................................................. 6

Economic Outlook ............................................................................................................... 6

Financial Budgeting and Accounting ................................................................................... 8

Budget Goals and Objectives .............................................................................................. 8

General Fund Budget .......................................................................................................... 9

Other District Funds .......................................................................................................... 15

Budget Forecasts............................................................................................................... 16

Budget Compliance Statements .................................................................................................... 17

ORGANIZATIONAL SECTION .............................................................................. 19

School District Organizational Chart .............................................................................................. 20

District Map ................................................................................................................................... 21

Fund Accounting ............................................................................................................................ 22

Fund Organization Chart ................................................................................................................ 24

Chart of Accounts ........................................................................................................................... 25

Budget Procedures ......................................................................................................................... 25

Significant Budget Development Statutes, Policies, and Guidelines ............................................. 26

Budget Development Calendar ...................................................................................................... 29

FINANCIAL SECTION .......................................................................................... 31

Budget Revenue Assumptions ....................................................................................................... 32

Budget Expenditure Assumptions .................................................................................................. 32

Summary Budget Schedule – All Funds ......................................................................................... 34

Graphs ............................................................................................................................................ 36

Revenue Distribution Summary ........................................................................................ 36

Expenditure Distribution Summary .................................................................................. 36

Governmental Funds...................................................................................................................... 37

General Fund (Fund 10) .................................................................................................... 37

Insurance Reserve Fund (Fund 18) ................................................................................... 50

ii | Montrose County School District RE-1J

Nutritional Services Fund (Fund 21) ................................................................................. 52

Special Grants Fund (Fund 22) .......................................................................................... 54

Student Activity Fund (Fund 23) ....................................................................................... 58

Fee-in-Lieu Fund (Fund 26) ............................................................................................... 59

Debt Funds ........................................................................................................................ 61

Capital Projects Funds ....................................................................................................... 66

Proprietary Fund ............................................................................................................................ 70

Employee Medical Internal Service Fund (Fund 65) ......................................................... 70

Fiduciary Funds .............................................................................................................................. 72

Scholarship Trust Fund (Fund 79) ..................................................................................... 72

Charter School Component Unit Budgets ...................................................................................... 74

Passage Charter School ..................................................................................................... 74

Vista Charter School .......................................................................................................... 75

2014-2015 Summary Budget (CDE-18) .......................................................................................... 76

INFORMATIONAL SECTION ................................................................................ 77

Demographic Information ............................................................................................................. 78

Property Tax Information............................................................................................................... 79

October 2013 Student Count by School ........................................................................................ 80

Personnel Resource Allocation History .......................................................................................... 81

Bond Amortization Schedule ......................................................................................................... 82

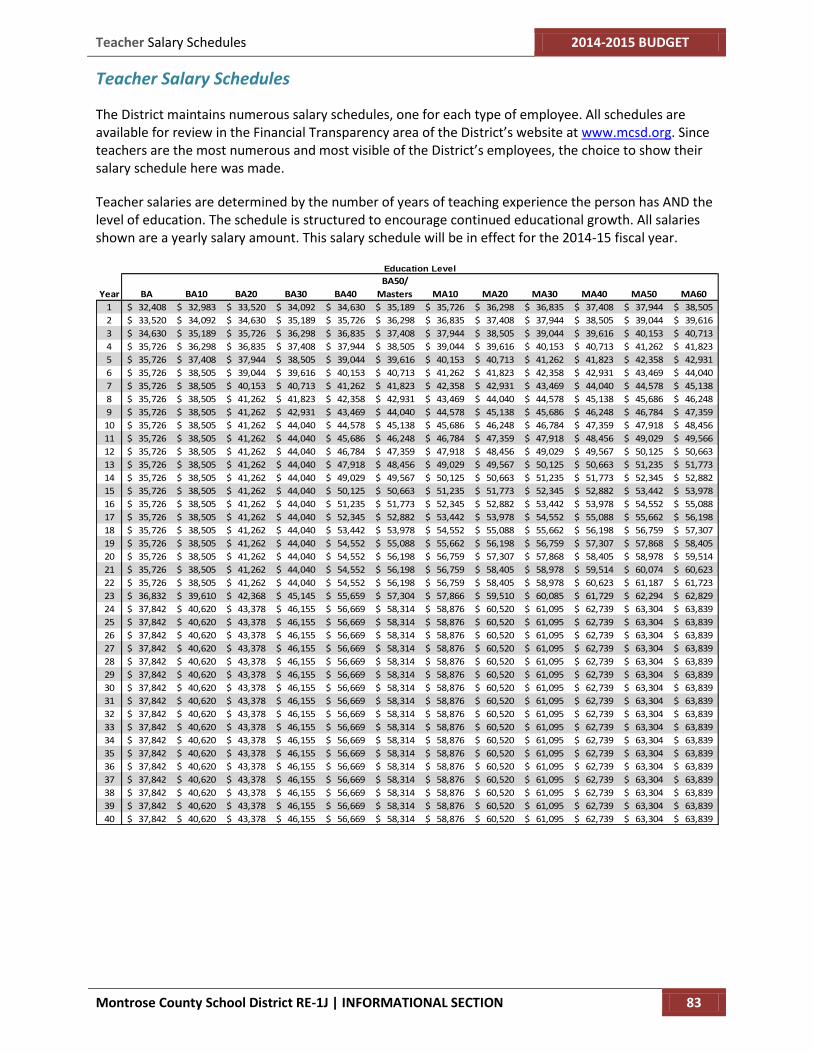

Teacher Salary Schedules ............................................................................................................... 83

Performance Measurements ......................................................................................................... 84

Glossary .......................................................................................................................................... 88

INTRODUCTORY SECTION 2014 – 2015 BUDGET

Montrose County School District RE-1J | INTRODUCTORY SECTION 1

INTRODUCTORY SECTION

2014 – 2015 BUDGET Board of Education / District Office Administration

2 INTRODUCTORY SECTION | Montrose County School District RE-1J

Board of Education / District Office Administration

Board of Education

Leann Tobin, District G ............................................................................. President

Tom West, District D ........................................................................ Vice-President

Mark Bray, District E ................................................................................ Secretary

Stu Tolen, District A ................................................................................. Treasurer

Seth Felix, District B ................................................................................... Director

Gayle Johnson, District C ............................................................................ Director

Phoebe Benziger, District F ........................................................................ Director

District Office Administration

Mark MacHale ................................................................................ Superintendent

Karin Slater ........................................................................... Chief Financial Officer

Marilyn Stahn ....................................................................................... Accountant

John Omohundro, CPA .......................................................................... Accountant

Superintendent’s Budget Transmittal Letter 2014-2015 BUDGET

Montrose County School District RE-1J | INTRODUCTORY SECTION 3

Superintendent’s Budget Transmittal Letter

From: Mark MacHale, Superintendent of Schools

Date: May 30, 2014

To: RE-1J Governing Board

The 2014-2015 budget has been prepared in accordance with the following Board adopted budget goals:

1. Student achievement and learning are top priority.

2. The District recognizes that staff is our most valuable asset.

3. As good stewards, we must maintain the district facilities to the best of our ability.

This year we are budgeting revenues to take into account a forecasted decline in student enrollment. The decline is expected to be 85 students, which using the declining enrollment averaging that CDE allows, converts to 83 FTE (full-time equivalent). The decline is entirely due to a large graduating senior class .The budget will be based on this expected declining enrollment. This is a projected loss of revenue of $577,800.

As in the past, the state is requiring the District to budget a State Budget Stabilization Negative Factor. The current year amount is $6,188,600. This is the amount the District will realize as reduction in the state revenues. The negative factor actually reduced by $954,300 from the 2013-2014 budgeted amount of $7,142,900. The State is projecting higher revenue for the 2014-15 year which equates to an increase in the base student per pupil revenue of 2.8%, and the decrease in the Negative Factor.

Coming from our fund balance account will be the funding for: (same as 2013-2014)

Continuing steps and educational credits from the 12-13 negotiations: $1,125,000 which has been reduced from $1,256,900 due to staff attrition

Steps for eligible employees from 13-14 negotiations: $500,000

Educational credits in the form of lanes and clock hours for eligible employees from 13-14 negotiations: $150,000

Additional costs expected for the 2014-15 year which will be funded from new state revenues:

Mandatory PERA increase for all employees .09%: $233,600

5% increase in the District’s contribution to employee medical: $184,500

Transfer of three Title I teachers to General Fund (includes benefits): $156,000

Add four teachers to elementary classrooms (includes benefits): $249,200

Addition of a custodial supervisor (includes benefits): $58,000

1% across-the-board salary increase for all employees: $242,800

Increase hourly salaries an additional 25 cents per hour: $100,000

Increase salaries of exempt (salaried) staff $500 per year (includes all teachers): $234,500

Increase hourly wages of custodial crew leaders by $1 per hour: $27,000

Allow steps, lanes, and clock hours for eligible employees: $422,460

2014 – 2015 BUDGET Superintendent’s Budget Transmittal Letter

4 INTRODUCTORY SECTION | Montrose County School District RE-1J

Additional work days during the year for head school secretaries: $15,000

Additional amounts for staff professional development(includes benefits): $80,000

Negotiated additions to discretionary school spending budgets: $70,000

Positions that are vacated during the year due to attrition and limited term positions will be refilled as needed.

Almost all of the points above relate in some way to employee compensation. We live in a community with a higher-than-average cost of living, yet we historically have offered compensation at a lower rate than other similar school districts. In able to hire and retain top talent, we must offer competitive compensation in order to do so.

We acknowledge that funding ongoing expenditures such as salaries and benefits from fund balance is not a sustainable approach to budgeting. We anticipate that the unassigned fund balance in the General Fund will remain as a positive amount through the 2015-2016 year, but additional revenue will be required in future years in order to sustain current spending patterns.

While revenues appear to be increasing, the District still is operating below full funding. Our limited resources will be focused on increasing student achievement, recognizing our employees and maintaining our facilities to the best of our ability.

The District Strategic Plan 2014-2015 BUDGET

Montrose County School District RE-1J | INTRODUCTORY SECTION 5

The District Strategic Plan

2014 – 2015 BUDGET Executive Budget Summary

6 INTRODUCTORY SECTION | Montrose County School District RE-1J

Executive Budget Summary

Introduction This document provides a comprehensive summary of budgeting for the Montrose County School District. It includes the following information:

An organizational overview

District mission and objectives

Current budget assumptions

Long-term outlook

Staffing and enrollment summaries

Performance data

Statistical data

Demographics Montrose County School District RE-1J (MCSD) is a rural school district located in west-central Colorado. It serves approximately 6,000 students in 11 schools, an Early Childhood Center, and an online Virtual Academy. The City of Montrose and the Town of Olathe are the major communities served by these schools. Student levels range from preschool through 12th grade.

The District is the largest employer in Montrose County with over 800 full- and part-time employees. Detailed staffing information is presented later in this document.

Overview As with all school districts in Colorado, MCSD faces continuing budget challenges. K-12 public education funding has been reduced over the last five years due to declining state revenues resulting from the recession. The outlook statewide is improving as the economy recovers, but western Colorado, and Montrose County in particular, are lagging in this recovery, and the long-term outlook is guarded. The following document will address the local, state, and national economic situation and the impacts on this school district.

Economic Outlook

Local Economy Montrose County was particularly hard hit by the recent recession. While farming and ranching play a large part in the local economy, tourism and recreation and the energy industry are also quite important to the local scene. As the recession took hold, spending by the public on recreation and travel declined, and jobs in the tourism industry were put in jeopardy. A decline in the local energy industry, both in oil/gas and coal mining, spill over into Montrose County due to workers who commute to nearby jobs in those fields. Unemployment rates, which hit its lowest rate in 2008 at just over 3%, jumped to just under 13% in 2010. As a result, families with school-age children have moved out of the area, and the local student population declined. A student count increase between 2012 and 2013 was the result of opening the District’s online virtual academy. This brought in local students who historically enrolled in other districts’ on-line programs.

As of the end of 2013, unemployment came down to about 8.5%, and assessed property values declined by 13%. The student population decline appears to have bottomed out, but long-term forecasting by the State Demography office indicates that Montrose County will see a very modest 1% to 2% per-year growth for the next 25 years.

Executive Budget Summary 2014-2015 BUDGET

Montrose County School District RE-1J | INTRODUCTORY SECTION 7

State Economy As a whole, the State of Colorado fared well through the recent recession. The agricultural market (which greatly affects Montrose County) remained strong. Drought conditions contributed to lower production, which boosted prices and actually increased overall revenue.

School districts in Colorado are funded via the School Finance Act (the Act). The Act prescribes total program funding using a per-pupil funding formula. To accommodate state revenue challenges, the state incorporated what has been titled as a negative factor into the school finance funding formula. The negative factor is a factor that proportionately reduces prescribed funding levels for each school district. This negative factor is the mechanism the state has implemented to reduce the level of K-12 funding while remaining within acceptable legal limits of the funding formula.

This negative factor has created a deficit funding gap of 16 percent or more than $1 Billion statewide. This means that school districts across the state have been receiving $1 Billion less than they should be receiving under a fully funded school finance formula. The reduction of funding has been spread across districts in Colorado. The following chart shows the District’s share of the Negative Factor, which topped out in school year 2012-13 at $7.37 million. The District’s 2014-15 share is anticipated to be in excess of $6.2 million.

$-

$2

$4

$6

$8

Mill

ion

s

MCSD Negative Factor Share

In calendar year 2013, the State had a budget surplus, which should positively affect school budgets going forward. For the 2014-15 school year, the negative factor is about 13% (down from about 15.4% in 2013-14), resulting in a per-pupil funding amount of $6,961, an increase of $371 or 6% over 2013-14.

$6,833

$7,169

$6,501 $6,430 $6,462 $6,590

$6,961

$6,000

$6,400

$6,800

$7,200

$7,600

MCSD Per-Pupil Funding by Year

2014 – 2015 BUDGET Executive Budget Summary

8 INTRODUCTORY SECTION | Montrose County School District RE-1J

National Economy The graph on the following page shows the percent change in Gross Domestic Product (GDP), which is commonly used as a benchmark to indicate the general health of the economy. Values over zero indicate growth in the economy. The graph indicates that the U.S. economy has been in a slow growth phase since early 2010. This should be encouraging in the near term.

Another concern to government entities such as MCSD has been the inability of the U.S. Legislature to pass budgets and thereby fund education programs. The sequestration cuts that took effect in March 2013 resulted in substantial cuts to a number of Federal education programs. The Consolidated Appropriations Act of 2014, signed into law in January 2014, restores this sequestration and should result in increased Federal Grant funding for the coming school year.

Financial Budgeting and Accounting The District follows generally accepted accounting principles (GAAP) established by the Governmental Accounting Standards Board (GASB) for both accounting and budgeting. The majority of the day-to-day operations of the school district are accounted for in the General Fund. Definitions of each of the funds maintained by the District are presented later in this executive summary. In addition, budgeting and accounting is governed by Administrative Policy.

In the late winter, the administration develops pupil enrollment forecasts. This forecast is used to develop other key budget assumptions as well as determine allocations for school staffing equivalents and financial resources. During April and early May, the finance department works with information taken from salary negotiations, student count projections, and Colorado Department of Education estimates for per-pupil funding to formulate the budget. The Board must adopt and appropriate a budget annually by formal resolution no later than June 30 of each year.

Budget Goals and Objectives The vision of the District is to ensure that all students have a safe and academically rigorous environment in which to learn, and that all students will graduate with life skills and knowledge required to enter into the workforce, to begin a career, and to attend college or other post-secondary education opportunities of their choice, without remediation. All budget monies that this district spends are dedicated toward that vision. To that end, the budget will be designed to (1) support this vision and the Board goals, (2) recognize that staff is our most valuable asset, and (3) promote good stewardship of our public funds.

Executive Budget Summary 2014-2015 BUDGET

Montrose County School District RE-1J | INTRODUCTORY SECTION 9

The District has made great strides in the past several years in improving student achievement. The District is no longer on an improvement plan and has attained full accreditation status. While we are happy with the improvements made, we still see room for growth.

In order to support the Strategic Plan, the following items have been identified as budget priorities for 2014-15:

1. Develop and maintain a staff compensation package that maintains or enhances the District’s competitive position relative to other school districts in the area, recognizing that staff is our most valuable asset.

2. Provide necessary resources to facilitate attainment of the two major goals noted above.

3. Continue to provide resources that maintain jobs in the district, maintain reasonable class sizes to the extent possible, and ensure that current student programs can continue.

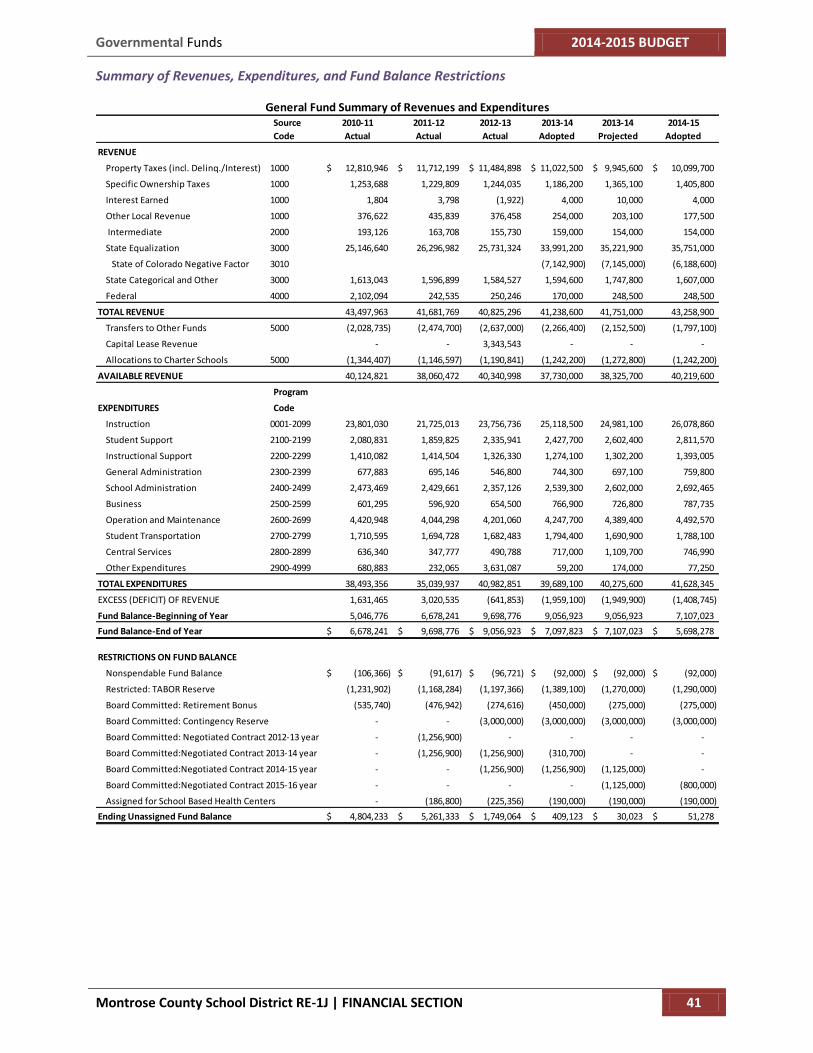

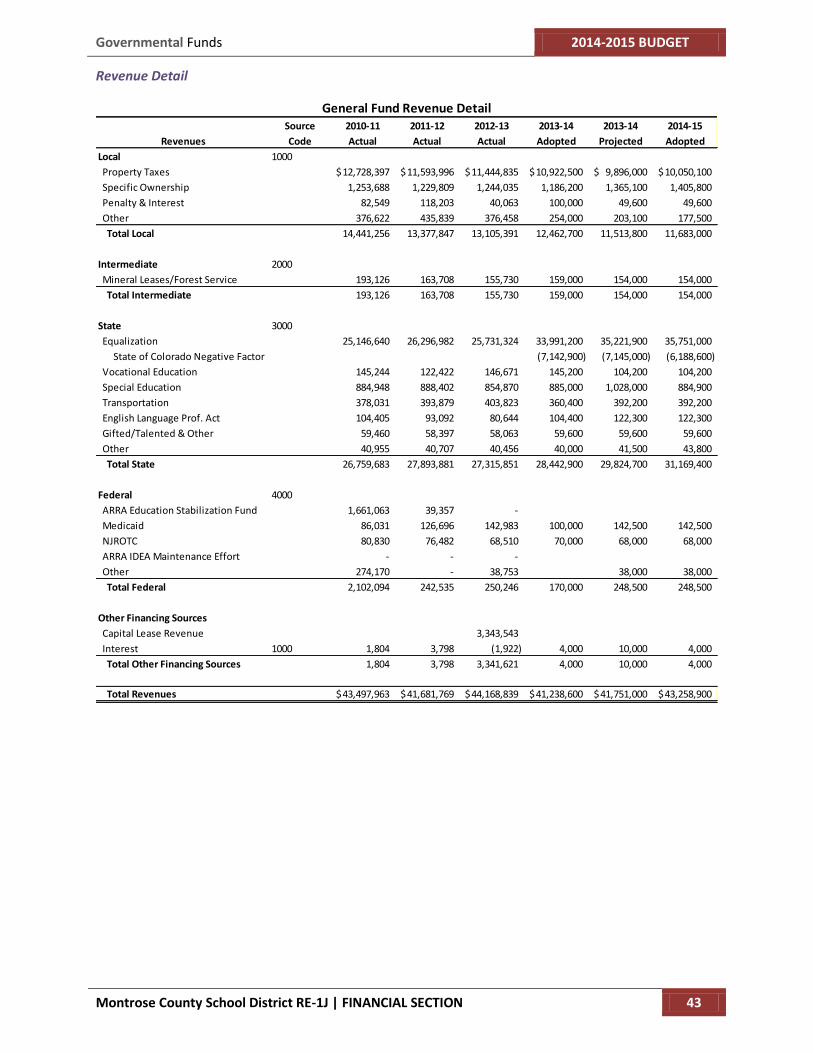

General Fund Budget

Total Appropriation The General Fund adopted budget appropriation for FY2014-15 is $41,628,345, an increase of $1,939,245 or 4.9% from the prior year final adjusted budget of $39,689,100. The total appropriation is comprised of the beginning fund balance plus revenues projected to be received during the fiscal year. Increases in the appropriation are projected to result mainly from increases in per-pupil funding from the State.

Beginning Fund Balance Colorado Statutes require that certain reserves must be funded while other designations may be approved by the Board of Education. The District has fully funded their liability for accrued salary and benefits ($4,428,461) as noted in the Financial Statements for FY2012-13. The adopted budget anticipates the resources necessary to maintain the accrual at a fully funded level. Excluding accruals, the total beginning fund equity, restricted, committed, assigned, and unassigned balances going into FY2014-15 are estimated to be $7,107,023 or 17.6% of total appropriated resources.

Sources of Revenue Approximately 95% of the revenue anticipated to be received by the General Fund is determined by the School Finance Act of 1994 as amended during the 2014 legislative session and the provisions of section 17 of Article IX of the state constitution (Amendment 23). The Act and Constitution determine per pupil funding levels for each Colorado public school district. Property taxes, specific ownership taxes (vehicle tax) and state aid provide the required funding for the Act.

The largest source of total revenue for the General Fund, 68%, is from state aid equalization. Local property taxpayers provide a total of 27%. Other sources of revenue include specific ownership taxes from vehicle registrations, other local sources, and other state sources.

Major revenue source changes for FY2014-15 are anticipated to include the following:

Legislation at the State level has increased per-pupil funding, resulting in an estimated total increase in District revenue of about $1.9 million.

The District’s student count is expected to drop by about 85 full-time students.

2014 – 2015 BUDGET Executive Budget Summary

10 INTRODUCTORY SECTION | Montrose County School District RE-1J

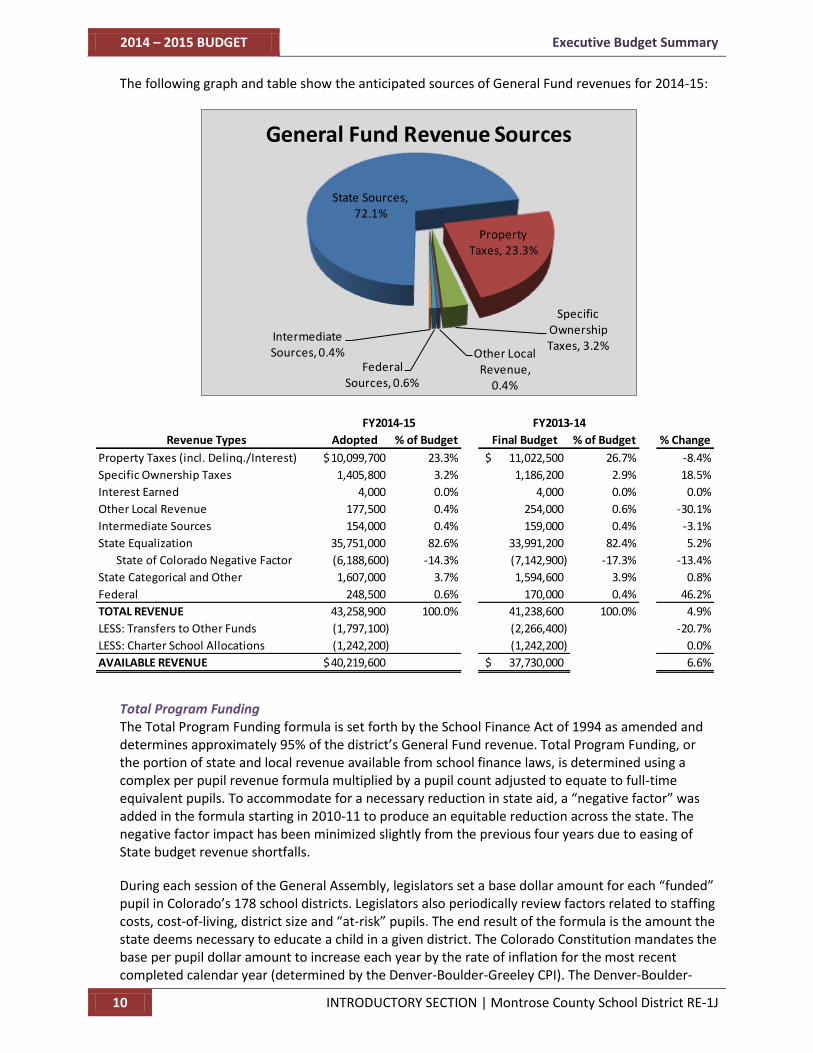

The following graph and table show the anticipated sources of General Fund revenues for 2014-15:

State Sources, 72.1%

Property Taxes, 23.3%

Specific Ownership Taxes, 3.2%

Other Local Revenue,

0.4%

Federal Sources, 0.6%

Intermediate Sources, 0.4%

General Fund Revenue Sources

Revenue Types Adopted % of Budget Final Budget % of Budget % Change

Property Taxes (incl. Delinq./Interest) 10,099,700$ 23.3% 11,022,500$ 26.7% -8.4%

Specific Ownership Taxes 1,405,800 3.2% 1,186,200 2.9% 18.5%

Interest Earned 4,000 0.0% 4,000 0.0% 0.0%

Other Local Revenue 177,500 0.4% 254,000 0.6% -30.1%

Intermediate Sources 154,000 0.4% 159,000 0.4% -3.1%

State Equalization 35,751,000 82.6% 33,991,200 82.4% 5.2%

State of Colorado Negative Factor (6,188,600) -14.3% (7,142,900) -17.3% -13.4%

State Categorical and Other 1,607,000 3.7% 1,594,600 3.9% 0.8%

Federal 248,500 0.6% 170,000 0.4% 46.2%

TOTAL REVENUE 43,258,900 100.0% 41,238,600 100.0% 4.9%

LESS: Transfers to Other Funds (1,797,100) (2,266,400) -20.7%

LESS: Charter School Allocations (1,242,200) (1,242,200) 0.0%

AVAILABLE REVENUE 40,219,600$ 37,730,000$ 6.6%

FY2014-15 FY2013-14

Total Program Funding The Total Program Funding formula is set forth by the School Finance Act of 1994 as amended and determines approximately 95% of the district’s General Fund revenue. Total Program Funding, or the portion of state and local revenue available from school finance laws, is determined using a complex per pupil revenue formula multiplied by a pupil count adjusted to equate to full-time equivalent pupils. To accommodate for a necessary reduction in state aid, a “negative factor” was added in the formula starting in 2010-11 to produce an equitable reduction across the state. The negative factor impact has been minimized slightly from the previous four years due to easing of State budget revenue shortfalls.

During each session of the General Assembly, legislators set a base dollar amount for each “funded” pupil in Colorado’s 178 school districts. Legislators also periodically review factors related to staffing costs, cost-of-living, district size and “at-risk” pupils. The end result of the formula is the amount the state deems necessary to educate a child in a given district. The Colorado Constitution mandates the base per pupil dollar amount to increase each year by the rate of inflation for the most recent completed calendar year (determined by the Denver-Boulder-Greeley CPI). The Denver-Boulder-

Executive Budget Summary 2014-2015 BUDGET

Montrose County School District RE-1J | INTRODUCTORY SECTION 11

Greeley inflation rate for Calendar Year 2013 was 2.8%. Therefore, the base amount per FTE student in Colorado for 2014-15 is $6,121, an increase of $166, or 2.77%, over 2013-14, before application of the negative factor. The addition of the negative factor reduces statewide funding of pre K-12 education by $894,302,068 from the amount otherwise required by the current School Finance Act. The impact of the negative factor on the district is a reduction to Total Program Funding of $6,223,454 or $1,054 per pupil below what the current School Finance Act should provide.

Student Enrollment As stated above, State per-pupil funding accounts for the largest percentage of revenue for the District. The funded pupil count is equal to the number of students enrolled in the District on October 1, and is adjusted for characteristics of certain student groups, such as half-day kindergarten students. The following graph shows historical and projected pupil counts for the District.

5,500

5,700

5,900

6,100

2006 2007 2008 2009 2010 2011 2012 2013EST.

2014EST.

2015EST.

2016

Count 5,672 5,856 6,010 6,011 5,971 5,859 5,768 5,804 5,748 5,740 5,745

Stu

de

nt

Co

un

t

MCSD October Student CountsFull Time Equivalents (FTE)

The Colorado Demography Office predicts that Montrose County will grow at a rate of 1% - 2% through 2040. However, in the short term, the District foresees student counts dropping in the current year, based on current enrollments. The graduating class of 2014 is particularly large, so a drop is expected for 2014-15, but slight increases are predicted for the next couple years thereafter.

Property Tax Revenues The District receives approximately 26% of total revenues from property taxes collected by Montrose, Ouray, and Gunnison counties. Each county’s assessor’s office establishes the taxable value of real estate for various types of properties, and periodically reassesses values based on market activity from the previous assessment period. A reassessment was done in 2013 in Montrose County that resulted in a 13% decrease to the District’s expected tax revenues, a drop of about $1,495,000. Fortunately, this loss of local revenue is replaced by an increase in state revenue to equal total program funding.

Expenditures Expenditures for the General Fund are first allocated by programs that identify specific activities such as classroom education, special education, maintenance, etc. Within each program, expenditures are further allocated to specific objects such as salaries, benefits, purchased services, etc.

2014 – 2015 BUDGET Executive Budget Summary

12 INTRODUCTORY SECTION | Montrose County School District RE-1J

Major Changes in Budgeted Expenditures by Program The changes in budgeted expenditures by program for FY2014-15 result from salary and benefit increases for staff.

The General Fund budget by program is shown in the following chart.

Instruction, 62.6%

Student Support, 6.8%

Instructional Support, 3.3%

General Admin, 1.8%

School Admin, 6.5%Business, 1.9%

Operations & Maintenance,

10.8%

Student Transportation,

4.3%

Central Services, 1.8%

Other, 0.2%

General Fund Expenditures by Program

Changes in budgeted expenditures by program in the General Fund from FY2013-14 to FY2014-15 are shown below.

Programs Adopted % of Budget Final Budget % of Budget % Change

Instruction 26,078,860$ 62.6% 25,118,500$ 63.3% 3.8%

Student Support 2,811,570 6.8% 2,427,700 6.1% 15.8%

Instructional Support 1,393,005 3.3% 1,274,100 3.2% 9.3%

General Administration 759,800 1.8% 744,300 1.9% 2.1%

School Administration 2,692,465 6.5% 2,539,300 6.4% 6.0%

Business 787,735 1.9% 766,900 1.9% 2.7%

Operations & Maintenance 4,492,570 10.8% 4,247,700 10.7% 5.8%

Student Transportation 1,788,100 4.3% 1,794,400 4.5% -0.4%

Central Services 746,990 1.8% 717,000 1.8% 4.2%

Other 77,250 0.2% 59,200 0.1% 30.5%

Total 41,628,345$ 100.0% 39,689,100$ 100.0% 4.9%

Fund Balances

Nonspendable 92,000$ 92,000$ 0.0%

Restricted 1,290,000 1,389,100 -7.1%

Committed 3,275,000 5,017,600 -34.7%

Assigned 190,000 190,000 0.0%

Unassigned 51,278 409,123 -87.5%

Total Reserves 4,898,278 7,097,823 -31.0%

Total Expenditures and

Reserves 46,526,623$ 46,786,923$ -0.6%

FY2014-15 FY2013-14

Executive Budget Summary 2014-2015 BUDGET

Montrose County School District RE-1J | INTRODUCTORY SECTION 13

Expenditures by Object In addition to budgeting expenditures by program, expenditures are also budgeted into groupings referred to as objects. Objects refer to the service or item that is being purchased. There are eight major object groups required by the state. Those groups include salaries, benefits, purchased professional services, purchased property services, other purchased services, supplies, property and other uses. Salary costs include regular employee wages, overtime pay, supplemental pay and substitute employee pay. Benefits include health, vision and dental premiums as well as contributions to the state mandatory retirement system (PERA). Purchased professional services include non-employee costs for services provided by attorneys, auditors, bankers and consultants. Purchased property services include non-employee costs for repair of buildings and equipment, rental of facilities or equipment and water and trash services. Other purchased services include costs related to field trips, tuition paid to other entities, communications, printing, postage, insurance premiums and travel. Supplies include natural gas and electric utilities in addition to typical office and classroom supply items. Property costs include non-capital assets (unit cost between $500 and $5,000) and capital assets (unit cost greater than $5,000). Other uses include inter-fund transfers and payments of principal and interest on short-term notes and long-term debts.

The following chart depicts adopted budgeted expenditures in the General Fund by object. Employee compensation and benefits account for 87% of budgeted expenditures.

Salaries, 65.5%

Benefits, 21.1%Purchased

Services, 8.1%Supplies, 4.2%

Capital Outlay, 0.3%

Other, 0.7%

General Fund Expenditures by Object

2014 – 2015 BUDGET Executive Budget Summary

14 INTRODUCTORY SECTION | Montrose County School District RE-1J

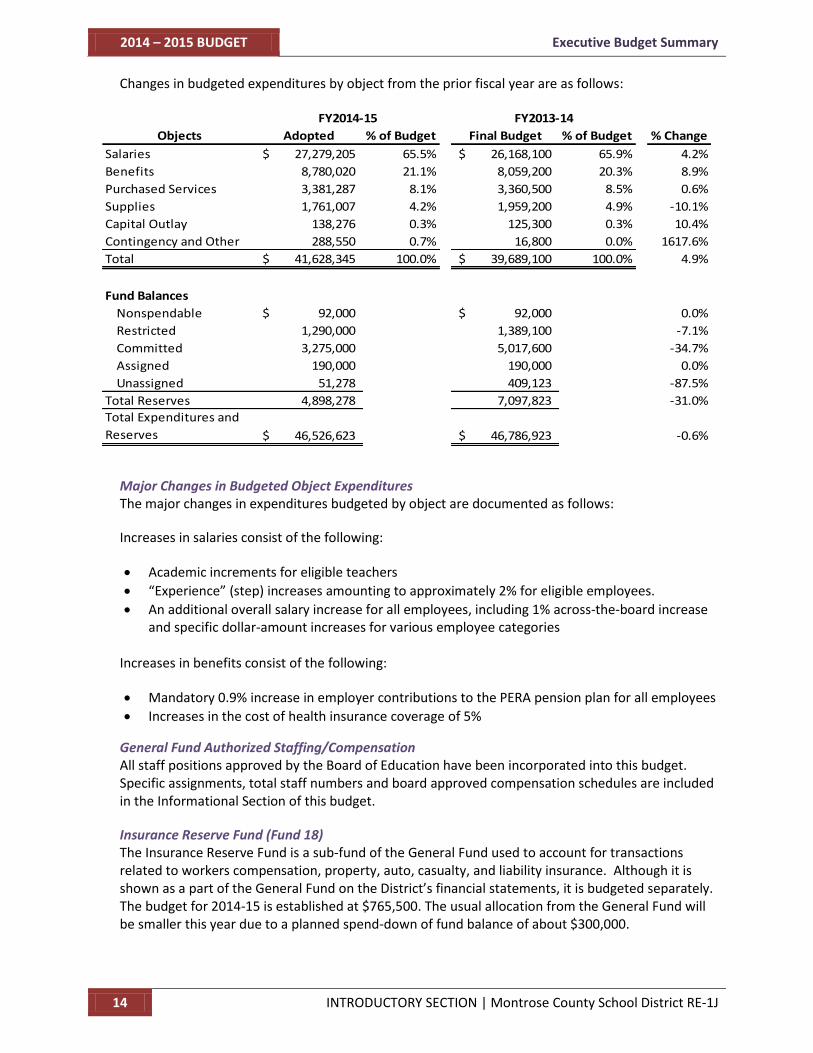

Changes in budgeted expenditures by object from the prior fiscal year are as follows:

Objects Adopted % of Budget Final Budget % of Budget % Change

Salaries 27,279,205$ 65.5% 26,168,100$ 65.9% 4.2%

Benefits 8,780,020 21.1% 8,059,200 20.3% 8.9%

Purchased Services 3,381,287 8.1% 3,360,500 8.5% 0.6%

Supplies 1,761,007 4.2% 1,959,200 4.9% -10.1%

Capital Outlay 138,276 0.3% 125,300 0.3% 10.4%

Contingency and Other 288,550 0.7% 16,800 0.0% 1617.6%

Total 41,628,345$ 100.0% 39,689,100$ 100.0% 4.9%

Fund Balances

Nonspendable 92,000$ 92,000$ 0.0%

Restricted 1,290,000 1,389,100 -7.1%

Committed 3,275,000 5,017,600 -34.7%

Assigned 190,000 190,000 0.0%

Unassigned 51,278 409,123 -87.5%

Total Reserves 4,898,278 7,097,823 -31.0%

Total Expenditures and

Reserves 46,526,623$ 46,786,923$ -0.6%

FY2014-15 FY2013-14

Major Changes in Budgeted Object Expenditures The major changes in expenditures budgeted by object are documented as follows:

Increases in salaries consist of the following:

Academic increments for eligible teachers

“Experience” (step) increases amounting to approximately 2% for eligible employees.

An additional overall salary increase for all employees, including 1% across-the-board increase and specific dollar-amount increases for various employee categories

Increases in benefits consist of the following:

Mandatory 0.9% increase in employer contributions to the PERA pension plan for all employees

Increases in the cost of health insurance coverage of 5%

General Fund Authorized Staffing/Compensation All staff positions approved by the Board of Education have been incorporated into this budget. Specific assignments, total staff numbers and board approved compensation schedules are included in the Informational Section of this budget.

Insurance Reserve Fund (Fund 18) The Insurance Reserve Fund is a sub-fund of the General Fund used to account for transactions related to workers compensation, property, auto, casualty, and liability insurance. Although it is shown as a part of the General Fund on the District’s financial statements, it is budgeted separately. The budget for 2014-15 is established at $765,500. The usual allocation from the General Fund will be smaller this year due to a planned spend-down of fund balance of about $300,000.

Executive Budget Summary 2014-2015 BUDGET

Montrose County School District RE-1J | INTRODUCTORY SECTION 15

Other District Funds

Special Revenue Funds Funds used to account for the proceeds from special revenue sources that are legally restricted to expenditure for specified purposes are referred to as Special Revenue Funds.

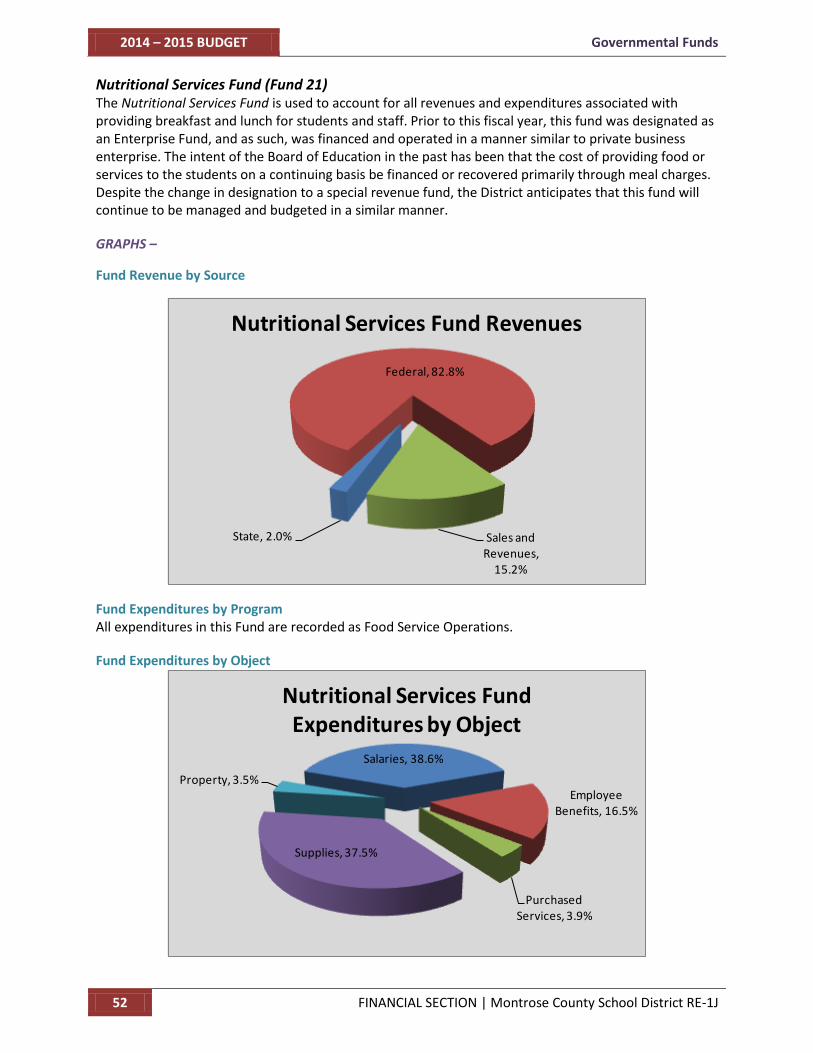

Nutritional Services Fund (Fund 21) The Nutritional Services Fund was accounted for as an Enterprise Fund (Fund 51) in prior years. CDE changed the fund type for this fund effective with this fiscal year. This fund accounts for the activities of the District’s school breakfast and lunch programs. The Fund has operated in the past as a business enterprise with a revenue-based budget using a profit and loss format, due to its Enterprise designation. While the fund type designation has changed, the District’s philosophy regarding operation and budgeting will not change. The budget for 2014-15 is established at $1,977,150.

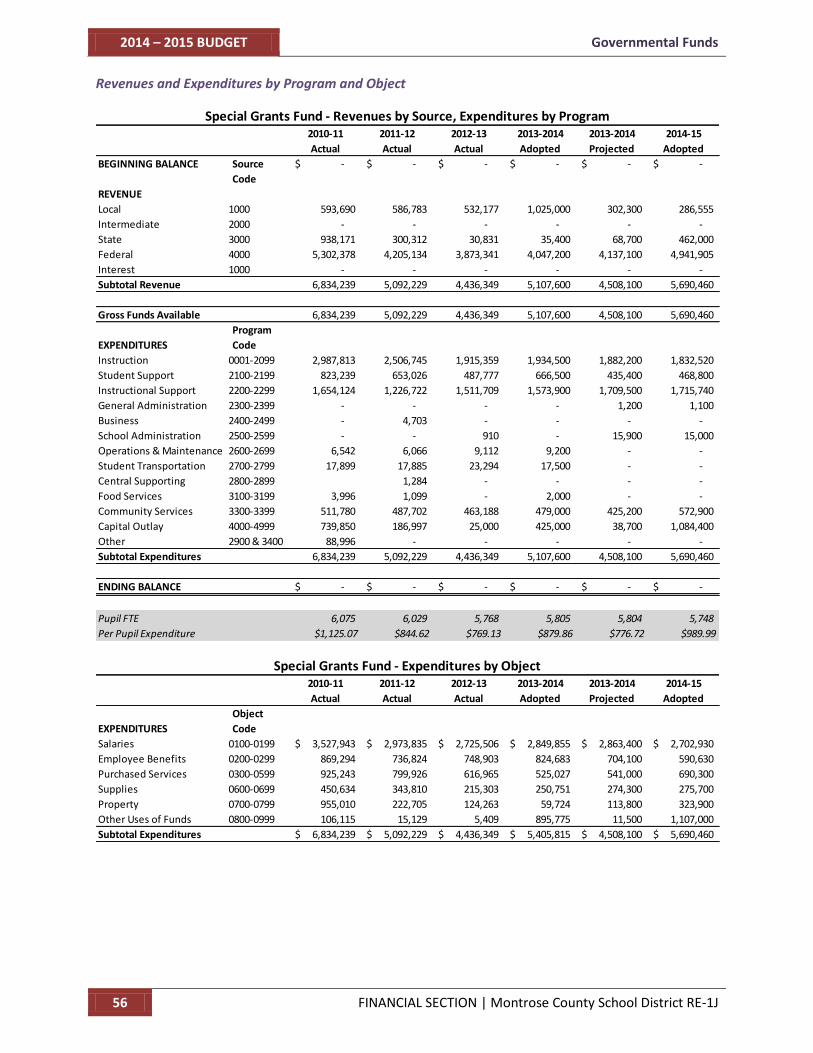

Designated Purpose Grant Fund (Fund 22) Designated purpose grants are external funds that are received mostly from the U.S. Department of Education to provide for a particular group or need. Generally, the funds must supplement the district’s expenditures for these activities/needs and should not be used to supplant district responsibilities. The fund is used to account for a variety of grants that are detailed in the specific budget section. Title I, II, III, IV, and V grants, IDEA, Perkins, S.W.A.P, and other state and local grants are recorded in the Designated Purpose Grant Fund. Federal budget sequestration reduced grant reimbursement for 2013-14, but sequestration was rescinded in early 2014, so funding levels are expected to rise for the coming year. The budget for 2014-15 is established at $5,690,460.

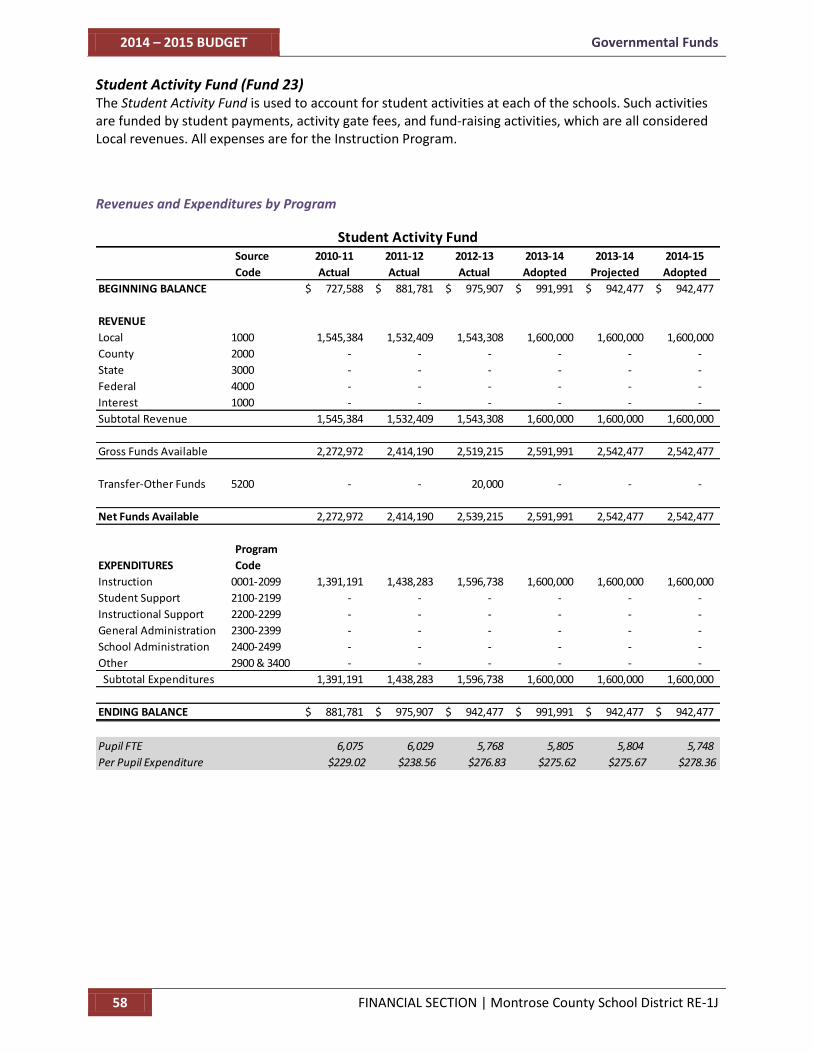

Student Activities Fund (Fund 23) The Student Activities Fund is used to record the financial transactions related to approved academic and sports activities within the schools. Each school has its own set of activity funds. Revenues to support these activities come primarily from fees charged to the students and from fundraising donations. The budget for 2014-15 is established at $1,600,000.

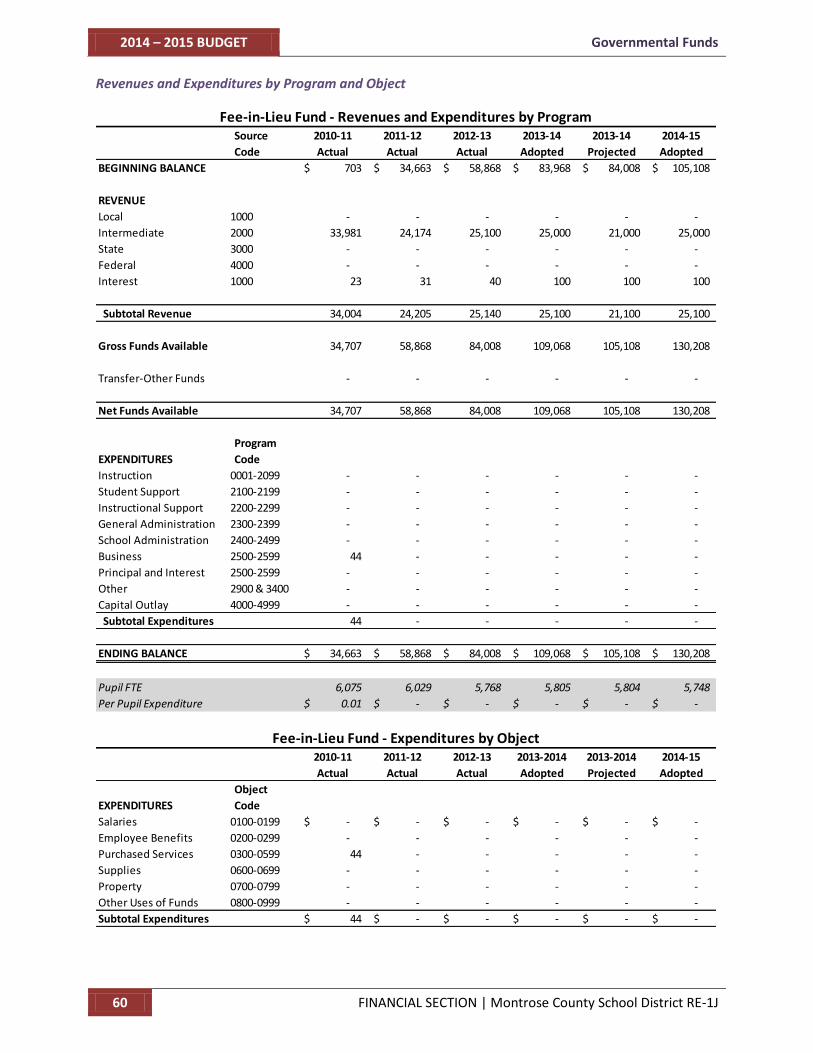

Fee in Lieu Fund (Fund 26) The Fee in Lieu Fund is used to record revenues from new real estate development in Montrose County and is used to fund future capital projects. Currently, no expenditures from this fund have been budgeted.

Debt Service Funds Debt Service Funds are used to service the long-term debts of the District, including principal, interest, and related expenses.

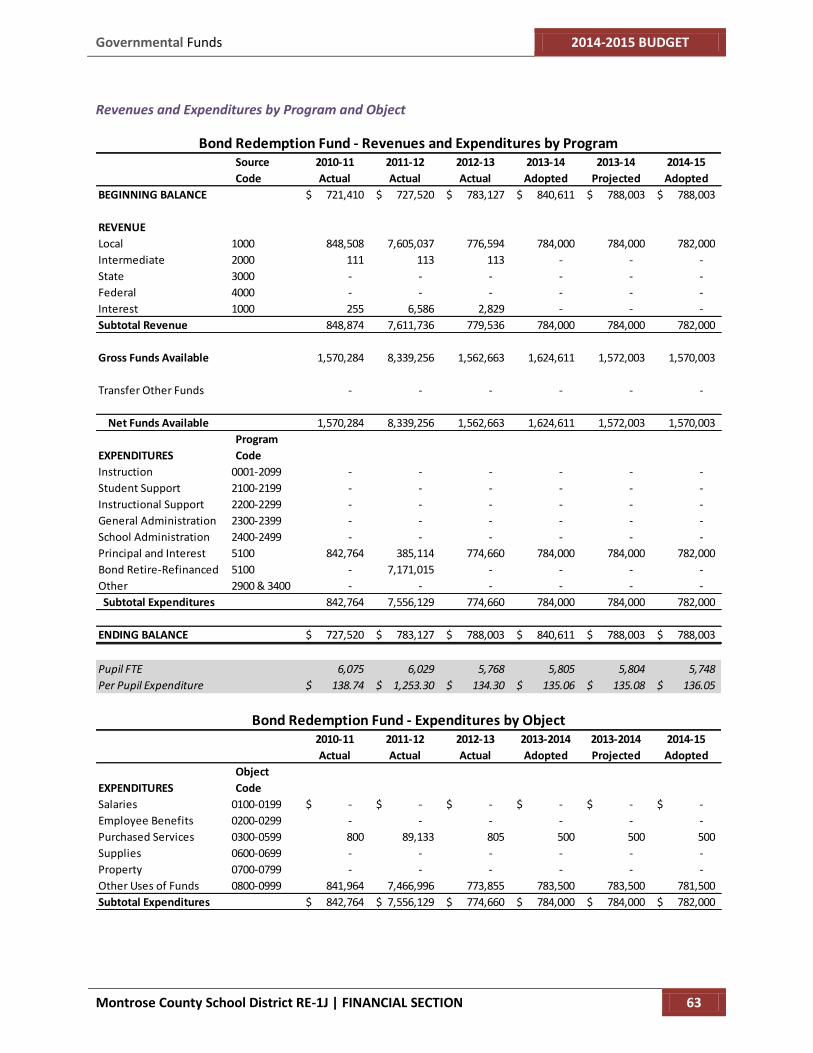

Bond Redemption Fund (Fund 31) The district utilizes the Bond Redemption Fund, as specified in C.R.S. 22-45-103(b), to finance and account for the payment of principal and interest on all long-term bonded debt of the district. The budget for 2014-15 is established at $782,000, which covers payments for bonded debt already currently in existence.

Capital Lease/QZAB Fund (Fund 39) The Capital Lease/QZAB Fund accounts for resources to be used to repay the Qualified Zone Academy Bond (QZAB) debt and other long-term debt obligations. The budget for 2014-15 is established at $400,000.

2014 – 2015 BUDGET Executive Budget Summary

16 INTRODUCTORY SECTION | Montrose County School District RE-1J

Capital Projects Funds The District maintains two funds related to capital expenditures.

Building Fund (Fund 41) The Building Fund is used to account for the construction of large projects and large repairs to facilities. No such current projects are anticipated in the current year, and this fund is not currently budgeting any expenditures. A $200,000 transfer from the General Fund is budgeted to allow for future construction projects and emergency repairs.

Capital Reserve Capital Projects Fund (Fund 43) The Capital Reserve Capital Projects Fund was reclassified in 2011 from the Special Projects Fund, Capital Reserve. This fund is used to account for the purposes and limitations specified by Section 22-45-103(1)(c), C.R.S., including the acquisition of sites, buildings, equipment, and vehicles. The majority of revenues to this fund come from transfers from other funds. The budget for 2014-15 is established at $1,187,500.

Internal Service Funds Internal Service Funds account for operations undertaken by District Staff that primarily support the District and/or its employees. The District’s only internal service fund is the Employee Medical Benefit Program Fund (Fund 65), which services the District’s self-funded medical insurance program. The budget for 2014-15 is established at $5,956,200.

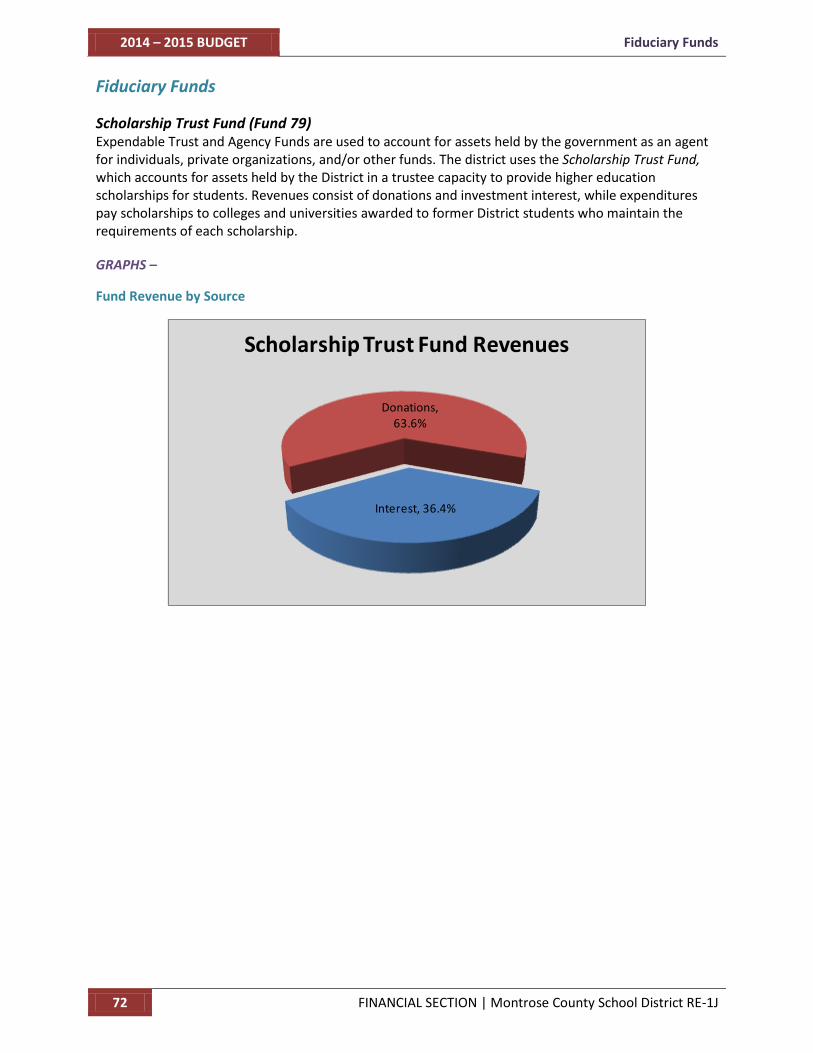

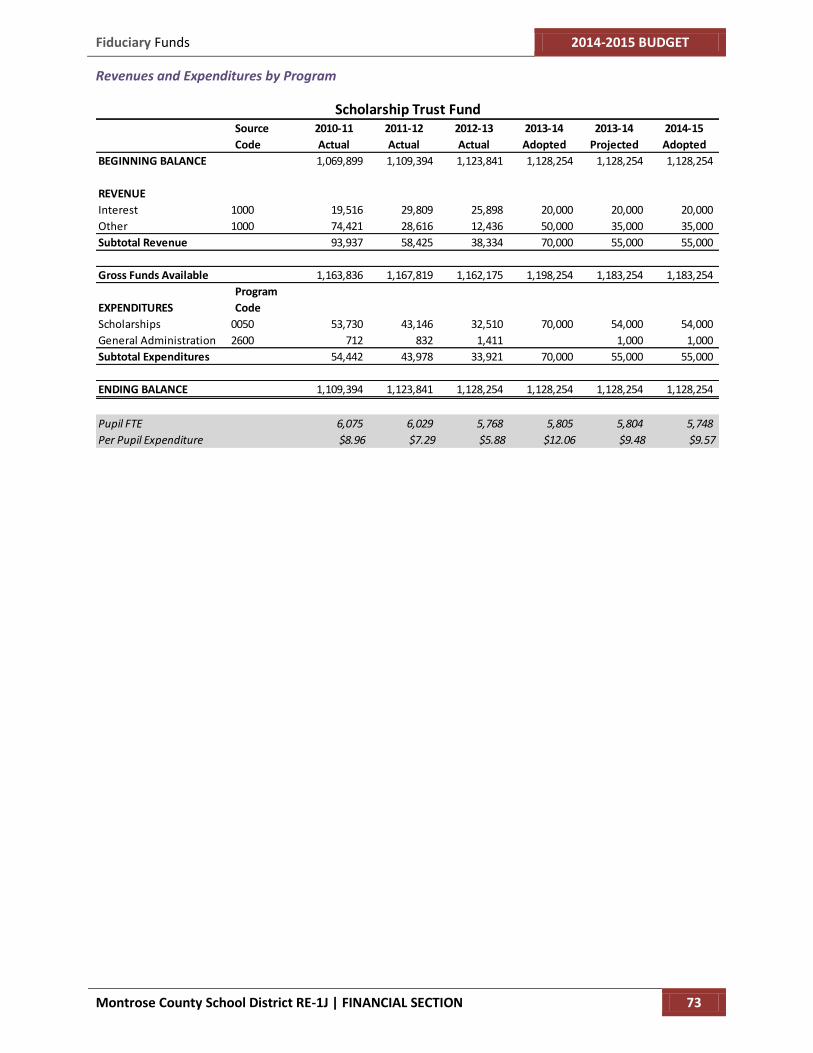

Fiduciary Funds Fiduciary Funds are used to account for funds held by the District in a trustee capacity for others. The District’s only fiduciary fund is the Scholarship Trust Fund (Fund 79), which accounts for scholarship funds held by the District for students. The budget for 2014-15 is established at $55,000.

Budget Forecasts The District foresees a stabilization in student counts for the next few years, which will translate into a more even funding stream. We expect that the Negative Factor will reduce slowly over the next several years as well, which should mean an increase in per-pupil funding. We are aware that we are currently operating in an overspent situation, as is evidenced by the use of fund balance. The majority of the overspending is related to salaries and benefits, which are ongoing expenses. We realize that any Negative Factor reduction which results in additional State funding must first be applied to reducing and eliminating overspending. A concerted effort must be made to no budget any further use of existing fund balances.

The District plans to introduce a mill levy override proposition on the November 2014 ballot. The yearly proceeds of approximaately $2,913,000 would be used to fund personnel, teaching and learning materials, technology, and learning environment. The override would have an initial life of five years. Since passage of this issue is uncertain, the curent budget does not reflect this additional amount.

Budget Compliance Statements 2014-2015 BUDGET

Montrose County School District RE-1J | INTRODUCTORY SECTION 17

Budget Compliance Statements

In Compliance with C.R.S. 22-44-105, this budget’s revenue projections were prepared using information provided by the Colorado Department of Education, the County Assessor, the Federal government, and other sources using methods recommended in the Colorado School District Financial Policies and Procedures Handbook. This budget’s expenditure estimates were prepared based on program needs, enrollment projections, mandated requirements, employee contracts, contracted services and anticipated changes in economic conditions using methods described in the Financial Policies and Procedures Handbook. Beginning fund balances and revenues equal or exceed budgeted expenditures and reserves.

In compliance with C.R.S. 22-44-105, this budget includes actual audited revenues, expenditures and fund balances for the last completed fiscal year. The figures are contained in the District’s audited financial statement report that is available online at www.mcsd.org under the “Business Office and Finance -> Financial Transparency” link or through the Colorado Department of Education or the Colorado State Auditor’s Office. Also, this budget includes the budgeted and estimated actual expenditures for the current fiscal year for comparison to the Fiscal Year 2013-2014 budget.

In compliance with C.R.S. 22-44-105, the fiscal year 2014-2015 budget has been prepared in accordance with the revenue, expenditures, tax limitation and reserve requirements of Article X, Section 20 of the Colorado State Constitution.

Lastly, this budget was developed and is presented in accordance with Meritorious Budget criteria established by the Association of School Business Officials International (ASBO).

2014 – 2015 BUDGET Budget Compliance Statements

18 INTRODUCTORY SECTION | Montrose County School District RE-1J

This page left intentionally blank.

ORGANIZATIONAL SECTION 2014 – 2015 BUDGET

Montrose County School District RE-1J | ORGANIZATIONAL SECTION 19

ORGANIZATIONAL SECTION

2014 – 2015 BUDGET School District Organizational Chart

20 ORGANIZATIONAL SECTION | Montrose County School District RE-1J

School District Organizational Chart

District Map 2014-2015 BUDGET

Montrose County School District RE-1J | ORGANIZATIONAL SECTION 21

District Map

2014 – 2015 BUDGET Fund Accounting

22 ORGANIZATIONAL SECTION | Montrose County School District RE-1J

Fund Accounting

The accounts of the district are organized on the basis of funds, each of which is considered a separate accounting entity. The operations of each fund are accounted for with a separate set of self-balancing accounts that comprise its assets, liabilities, fund balance, revenues, and expenditures. Government resources are allocated to and accounted for in individual funds based upon the purposes for which they are to be spent and the means by which spending activities are controlled. The various funds can be grouped into the following three categories. Basis of accounting is modified accrual in compliance with Generally Accepted Accounting Principles (GAAP) governmental reporting requirements.

1. GOVERNMENTAL FUNDS

General Fund (Fund 10) —As the district’s major operating fund, the General Fund accounts for the ordinary operating expenditures financed by property taxes, state equalization payments, service charges, and other sources. The fund includes all resources and expenditures not legally or properly accounted for in other funds as directed by C.R.S 22- 45-103(1)(a). The General Fund balance is available to the district for any purpose provided it is expended or transferred according to Colorado Revised Statutes.

The General Fund operating budget contains over 70% of the District’s total expenditures, and will therefore be shown in greater detail in the Financial section.

Special Revenue Funds —Special Revenue Funds are used to account for the proceeds of specific revenue sources (other than expendable trusts or for major capital projects) that are restricted to expenditures for specific purposes. The district maintains three Special Revenue Funds:

1. The Nutritional Services Fund (Fund 21) is used to account for all revenues and expenditures associated with providing breakfast and lunch for students and staff. Prior to this fiscal year, this fund was designated as an Enterprise Fund, and as such, was financed and operated in a manner similar to private business enterprise. Despite the change in designation to a special revenue fund, the District anticipates that this fund will continue to be managed and budgeted in the same manner.

2. The Designated Purpose Grant Fund (Fund 22) is used to account for the various federal, state and local grants awarded to the district to accomplish specific activities.

3. The Student Activity Fund (Fund 23) is used to account for student activities at each of the schools. Such activities are funded by student payments, activity gate fees, and fund-raising activities.

4. The Fee-in-Lieu Fund (Fund 26) is used to account for monies received from new developments and is used for future capital projects.

Debt Service Funds —Debt Service Funds account for the accumulation of resources and payment of long-term debt used to finance capital construction and land acquisition. The District uses two funds to account for debt service, which are combined for purposes of the District’s audited financial statements:

1. The district utilizes the Bond Redemption Fund (Fund 31), as specified in C.R.S. 22-45-103(b), to finance and account for the payment of principal and interest on all long-term bonded general obligation debt of the district.

Fund Accounting 2014-2015 BUDGET

Montrose County School District RE-1J | ORGANIZATIONAL SECTION 23

2. The Capital Lease/QZAB Fund (Fund 39) is utilized to finance and account for the payment of principal and interest on long-term leases and Qualified Zone Academy Bonds (QZAB).

Capital Projects Funds –Capital Project Funds are used to account for and report financial resources that are restricted, committed, or assigned to expenditure for capital outlays, acquisition or construction of major capital facilities and other capital assets (other than those financed by proprietary funds and trust funds). The District uses two funds to account for capital projects, which are combined for purposes of the District’s audited financial statements:

1. The Building Fund (Fund 41) is used to account for capital construction.

2. The Capital Reserve Capital Projects Fund (Fund 43) was reclassified in 2011 from the Special Projects Fund, Capital Reserve. This fund is used to account for the purposes and limitations specified by Section 22-45-103(1)(c), C.R.S., including the acquisition of sites, buildings, equipment, and vehicles.

2. PROPRIETARY FUNDS

Internal Service Fund – Internal Service Funds are used to account for the financing, on a cost-reimbursement basis of goods and services provided by one department or agency to other departments or agencies within the same government or to other governments or not-for-profit organizations. The Employee Medical Benefit Program Fund (Fund 65) is used to account for all revenues and expenses related to the District’s self funded medical/dental/vision insurance plan.

3. FIDUCIARY FUNDS

Expendable Trust and Agency Funds are used to account for assets held by the government as an agent for individuals, private organizations, and/or other funds. The district uses the Scholarship Trust Fund (Fund 79), which accounts for assets held by the District in a trustee capacity to provide higher education scholarships for students.

2014 – 2015 BUDGET Fund Organization Chart

24 ORGANIZATIONAL SECTION | Montrose County School District RE-1J

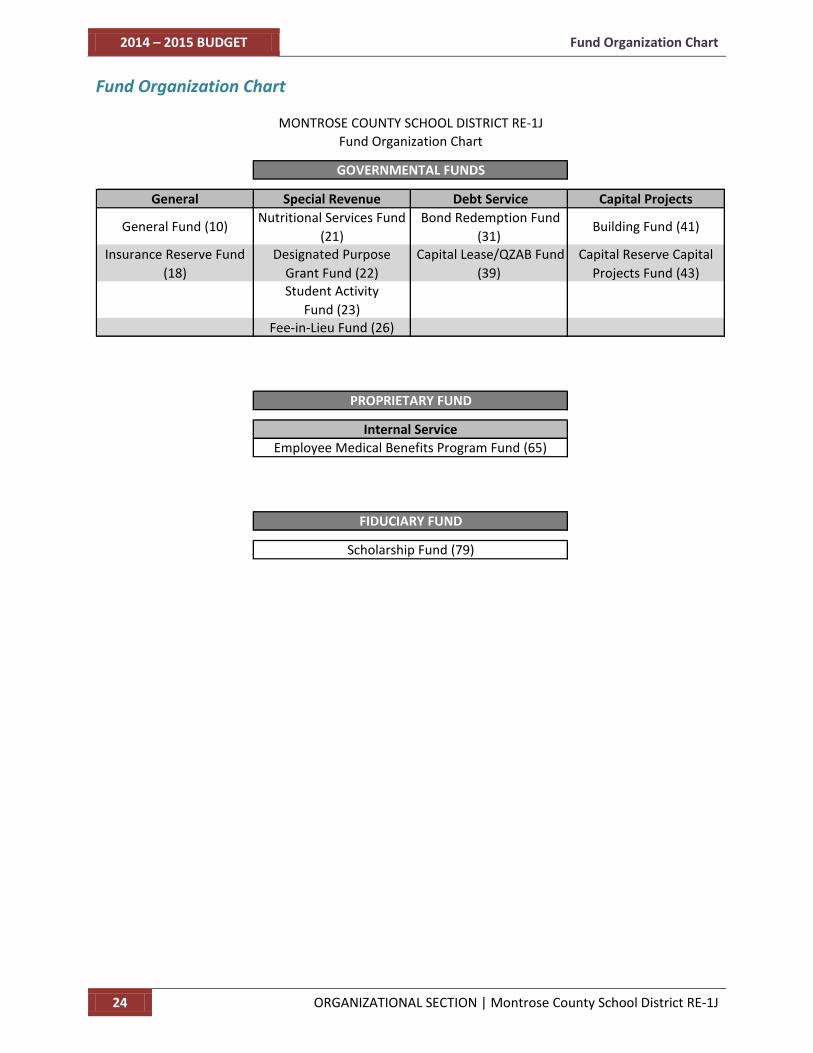

Fund Organization Chart

General Special Revenue Debt Service Capital Projects

General Fund (10)Nutritional Services Fund

(21)

Bond Redemption Fund

(31) Building Fund (41)

Insurance Reserve Fund

(18)

Designated Purpose

Grant Fund (22)

Capital Lease/QZAB Fund

(39)

Capital Reserve Capital

Projects Fund (43)Student Activity

Fund (23)Fee-in-Lieu Fund (26)

Scholarship Fund (79)

MONTROSE COUNTY SCHOOL DISTRICT RE-1J

Fund Organization Chart

GOVERNMENTAL FUNDS

PROPRIETARY FUND

FIDUCIARY FUND

Internal Service

Employee Medical Benefits Program Fund (65)

Chart of Accounts 2014-2015 BUDGET

Montrose County School District RE-1J | ORGANIZATIONAL SECTION 25

Chart of Accounts

Colorado Revised Statutes (C.R.S), Colorado Code of Regulations (C.C.R.), and Code of Federal Regulations (C.F.R.) stipulate the requirements for the funds and accounts used by school districts. The following information is provided to assist the readers of this document to identify revenue sources and program expenditures. This document provides only a brief overview of the required chart of accounts. Individuals seeking more detail may contact the Business Office for a complete chart of accounts document.

The following diagram illustrates the format and sequencing of the dimensions of the required reporting for revenues, expenditures, and balance sheet accounts.

XX - XXX - XX - XXXX - XXXX - XXX - XXXX Fund

Location SRE

Program Source

Equity/Liability/Asset Job

Classification Grant/Project

Budget Procedures

The district adheres to the following procedures in establishing the budgetary data reflected in the financial statements:

1. Budgets are required by state law, except fiduciary fund types. Annual appropriated budgets are adopted for all funds. During May, the Superintendent of Schools submits to the Board of Education a proposed budget for the fiscal year commencing the following July 1. The budget includes proposed expenditures and the means of financing them.

2. Public hearings are conducted by the Board of Education to obtain taxpayer comments on the proposed budget.

3. Prior to June 30 the budget is adopted and appropriated by formal resolution.

4. Expenditures may not legally exceed appropriations at the fund level. Authorization to transfer budgeted amounts between departments within any fund and the reallocation of budget line items within any department in the General Fund rests with administration. Revisions that alter the total expenditures of any fund must be approved by the Board of Education.

5. Budgets for all fund types are adopted on a basis consistent with generally accepted accounting principles.

6. All original and supplemental unencumbered appropriations for all funds lapse at the end of the fiscal year. (Certain uncommitted general fund school allocations are re-appropriated in the succeeding fiscal year by administrative policy).

2014 – 2015 BUDGET Significant Budget Development Statutes, Policies, and Guidelines

26 ORGANIZATIONAL SECTION | Montrose County School District RE-1J

7. Formal budgetary integration is employed as a management control device during the year for all funds consistent with the general obligation bond indenture and other statutory provisions. All funds must complete the year within the amount of their legally authorized appropriation.

8. Appropriation amounts are as originally adopted, or as amended by the Board of Education throughout the year by supplemental appropriations.

Significant Budget Development Statutes, Policies, and Guidelines

The Purpose of a Budget

The purpose of a budget is to provide a plan of financial operation, incorporating an estimate of proposed expenditures for a given period and a purpose that includes the proposed means of financing that plan. To achieve this basic purpose, a comprehensive budget system must be integrated with the financial accounting system. Detailed budget planning allows the district to reflect educational values and needs. The structure and format provided by a well-designed budget promotes rational decision-making regarding the importance of various school district services. In this way, administrators and the Board of Education are assisted in educational planning as well as the prioritization and planning of all district operations through the allocation of resources.

BLong Range Planning

The District’s long range planning process assures that department and school site plans align closely with the district’s mission and belief statements. Each site has developed objectives and detailed action plans that are intended to improve student achievement and the overall effectiveness of the district’s operations.

Budgets are reviewed on an ongoing basis for accomplished actions and costs. An annual review process assures that each plan reflects the changing needs of the site. For example, schools might revise elements in their site plan to reflect priorities identified during the accreditation process.

The Budget Process

The budget process involves multiple steps, which includes identification of district goals, budget calendar, budget projections, budget content, program budgeting, and the utilization and presentation of prescribed forms. In addition to the preparation of the operating budget, the capital budget must be prepared. The capital budget is based on a long-range plan, prioritized based on useful life of systems maintenance, safety and improvements to district buildings. The impact of capital projects is considered when developing the operating budget.

A. Budgetary Accounting

The budget serves as the basis for information appearing on required reports, as an integral part of the accounting records and as a tool for management control of expenditures during the fiscal year. The district’s budget is prepared on Generally Accepted Accounting Principles (GAAP) basis. A GAAP budget includes all expenditures incurred and revenue earned during the period, regardless of the timing when cash is actually received or paid.

Significant Budget Development Statutes, Policies, and Guidelines 2014-2015 BUDGET

Montrose County School District RE-1J | ORGANIZATIONAL SECTION 27

B. Budget Projections

In order to prepare budget projections for the ensuing fiscal year, the district has developed underlying assumptions, aligned with the Board’s objectives and goals, administrative policies, and the district’s mission statement, for use in forecasting sources and uses of funds.

1. Beginning Fund Balance

The district determines an estimate of year-end fund balances to be carried forward to the ensuing year as beginning balances. Governmental Accounting Standards Board (GASB) issued Statement No. 54 dictates the categories and terminology used to describe fund balance components, including constraints on the specific purposes for which the fund balance can be spent. Restricted Fund Balance is governed by laws through constitutional provisions or enabling legislation. Committed Fund Balance has limitations imposed at the highest level of decision making authority of the entity. Assigned Fund Balance can be established by the superintendent or a designee. Classification of Fund Balance requires projection of accounts payable and receivable, expenditures, and revenues for the remaining portion of the current budget year.

2. Revenues

For a review of the major revenue sources and the projection process, see detailed “Revenue Assumptions” presented in the Financial Section of this document.

3. Expenditures

For a review of the major expenditures and the projection process, see detailed “Expenditure Assumptions” presented in the Financial Section of this document.

4. Budget Transfers

Administrative Policy and state statutes govern budget transfers. The Board of Education approves all budget transfers through the budget process or by resolution during the fiscal year.

Operating subsidies to other funds must be approved by the Board of Education.

Budget Publication and Adoption

The Board of Education of the district must adopt a budget and an appropriation resolution for each fund that presents a complete financial plan for the ensuing fiscal year. In accordance with state budget law, the budget shall include actual revenues and expenditures/expenses in detail for the last completed fiscal year, revenues and expenditures/expenses anticipated/budgeted or both for the current fiscal year and proposed revenues and expenditures/expenses for the ensuing fiscal year.

A. Notice of Budget Publication

1. Proposed Budget/Notice to Public

The proposed budget shall be submitted to the Board of Education at least 30 days prior to the beginning of the fiscal year. Per statute, “Within 10 days after the submission of the proposed budget, The Board of Education must publish a notice stating that the proposed budget is on file at the principal administrative offices of the district; that the

2014 – 2015 BUDGET Significant Budget Development Statutes, Policies, and Guidelines

28 ORGANIZATIONAL SECTION | Montrose County School District RE-1J

proposed budget is available for inspection during reasonable business hours; that any person paying school taxes in the district may file or register an objection thereto at any time prior to its adoption; and that the Board of Education of the district will consider adoption of the proposed budget for the ensuing fiscal year on the date, time and place specified in the notice.”

2. Budget Consideration by the public

State law requires that a public meeting be held at which the proposed budget will be considered by the Board of Education.

B. Budget Adoption

The Board of Education must adopt a budget for each fiscal year prior to the beginning of the fiscal year (July1).

After adoption, the Board of Education may modify the budget prior to January 31 of the current fiscal year. Changes to the budget after that date may be authorized only under supplemental budget provisions.

C. Appropriation Resolution

The Board of Education must adopt a budget and an appropriation resolution for each fiscal year prior to the beginning of such year. The appropriation resolution must specify the amount of money appropriated to each fund. The amounts appropriated to a fund must not exceed the amount as specified in the adopted budget.

The Board of Education may not expend any monies in excess of the amount appropriated by resolution for a particular fund in the absence of a supplemental budget resolution.

D. Budget Filing

A copy of the budget is to remain on file at the main administrative office of the district throughout the year and must be open for public inspection during business hours. It must also be posted online on the District website.

E. Failure to Adopt a Budget

If either the budget or appropriation resolution is not properly adopted as required by statute, then 90% of the last duly adopted budget and appropriation resolution shall be deemed to be budgeted and appropriated.

F. Financial Transparency

Certain financial information must be posted online as prescribed by Article 44, Title 22 of the Colorado Revised Statutes.

Budget Development Calendar 2014-2015 BUDGET

Montrose County School District RE-1J | ORGANIZATIONAL SECTION 29

TABOR Constitutional Amendment

In November 1992, a majority of voters in the State of Colorado passed a constitutional amendment commonly referred to as Amendment 1 or the Taxpayers Bill of Rights (TABOR). The intent of the amendment is to restrict the growth of government in the state. Property tax revenue and total spending are restricted to increase by no more than the rate of population growth plus the Denver/Boulder Consumer Price Index for the calendar year immediately preceding the fiscal year.

Budget Development Calendar

Mid-December Mill Levy Certification of property tax collection for the calendar year

January 31 Deadline for amending final adjusted budget

February Denver-Boulder-Greeley CPI announced

April-May Salary negotiations with Uncompahgre Valley Education Association (UVEA)

Early May Schools informed of the per-pupil allocation

May 31 Proposed Budget transmitted to Board of Education

June 1-7 Publish Notice to the Public that the Proposed Budget is available for review per C.R.S. 22-44-109(1)

Mid-June Public hearing to review budget

June 30 Budget Adoption by Board of Education

Late August Initial district-wide assessed value received from County Assessor

October Preparation of Certified Enrollment, review of adopted budget based on student counts

November 3 Transmittal of Certified Pupil Count to CDE

2014 – 2015 BUDGET Budget Development Calendar

30 ORGANIZATIONAL SECTION | Montrose County School District RE-1J

This page left intentionally blank.

FINANCIAL SECTION 2014 – 2015 BUDGET

Montrose County School District RE-1J | FINANCIAL SECTION 31

FINANCIAL SECTION

2014 – 2015 BUDGET Budget Revenue Assumptions

32 FINANCIAL SECTION | Montrose County School District RE-1J

Budget Revenue Assumptions

Colorado’s Public School Finance Act of 1994 determines the per-pupil funding for the District. For the 2014-2015 year, total per-pupil funding will increase 2.8 % from $7,797 to $8,012. The State Budget Stabilization Negative Factor brings the per-pupil funding to $6,961. The budget reflects a decrease of 83 student FTE (full-time equivalent); therefore, General Fund per-pupil revenue is based on the $8,012 times 5,871 FTE students or $47 million. Including the Negative Factor results in net per-pupil revenue of $40.8 million. Approximately 25% of this will be received from school district property taxes, 3% from specific ownership tax, and 73% from state equalization funding. This year the ratio between local and state increased from 65% to 73% for the state portion, due to declining property valuations. Additional revenue is received for state categorical programs and from federal sources.

The state established a State Budget Stabilization Negative Factor in the amount of 13.16% of total program funding ($6,188,600) which in the budget has been included in State Equalization and as a separate line item as an offset to revenue.

Budget Expenditure Assumptions

Approximately 87% of General Fund expenditures are spent on salaries and benefits. The 2014-2015 budget for salaries and benefits reflects increases of 0.9% in PERA; 5% increase in Employee Medical; steps; and educational credits for lanes and clock hours. $.25 per hour was added to all classified positions, and $500 per year for each licensed/certified position. Positions that were vacated due to attrition will be carefully reviewed and refilled as needed.

Six separate amounts are acknowledged and set aside as committed and restricted as shown on the separate Fund Balance and Reserves Schedule (pg 20). While required to be budgeted, it is not intended that these six amounts will be expended: (1) Fund Balance in Non-Spendable form; (2) 3% for the TABOR emergency reserve (3) An amount for irrevocably-committed retirement bonuses; (4) Board reserve; (5) Board commitment for the third year of expenditures on the UVEA negotiated Contract; and (6) Assigned for the School Based Health Center.

Budget Expenditure Assumptions 2014-2015 BUDGET

Montrose County School District RE-1J | FINANCIAL SECTION 33

This page left intentionally blank.

2014 – 2015 BUDGET Summary Budget Schedule – All Funds

34 FINANCIAL SECTION | Montrose County School District RE-1J

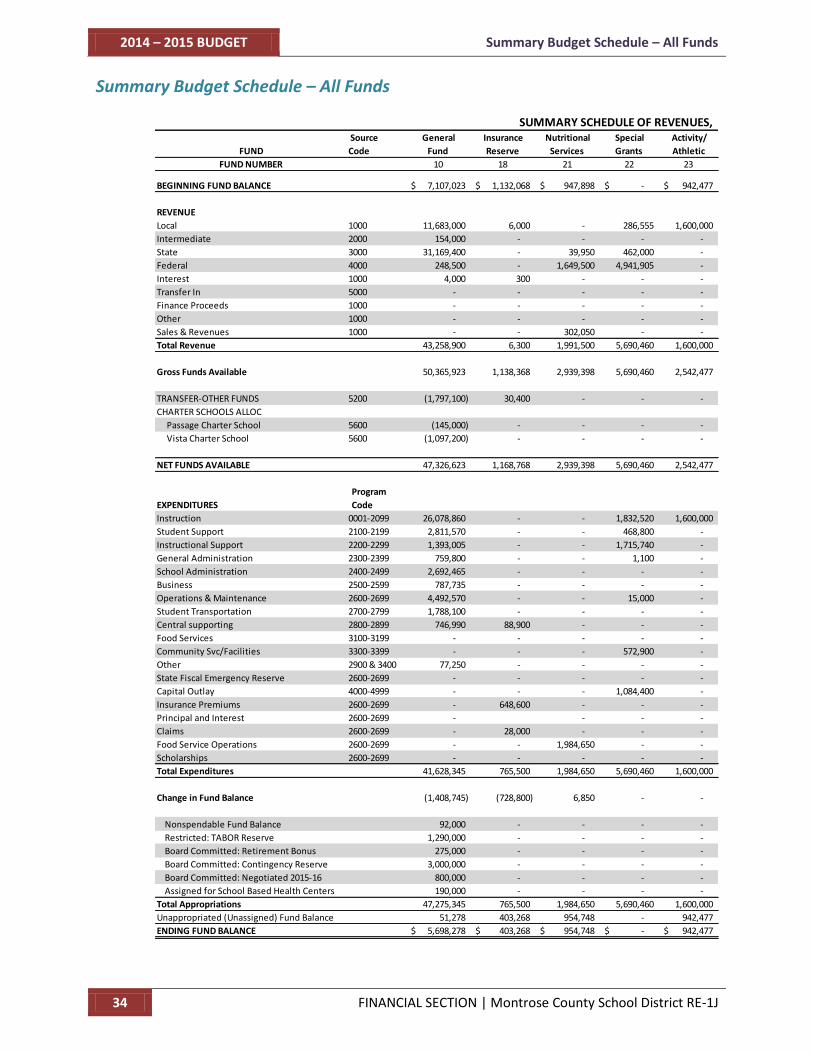

Summary Budget Schedule – All Funds

SUMMARY SCHEDULE OF REVENUES,

FUND

Source

Code

General

Fund

Insurance

Reserve

Nutritional

Services

Special

Grants

Activity/

Athletic

FUND NUMBER 10 18 21 22 23

BEGINNING FUND BALANCE 7,107,023$ 1,132,068$ 947,898$ -$ 942,477$

REVENUE

Local 1000 11,683,000 6,000 - 286,555 1,600,000

Intermediate 2000 154,000 - - - -

State 3000 31,169,400 - 39,950 462,000 -

Federal 4000 248,500 - 1,649,500 4,941,905 -

Interest 1000 4,000 300 - - -

Transfer In 5000 - - - - -

Finance Proceeds 1000 - - - - -

Other 1000 - - - - -

Sales & Revenues 1000 - - 302,050 - -

Total Revenue 43,258,900 6,300 1,991,500 5,690,460 1,600,000

Gross Funds Available 50,365,923 1,138,368 2,939,398 5,690,460 2,542,477

TRANSFER-OTHER FUNDS 5200 (1,797,100) 30,400 - - -

CHARTER SCHOOLS ALLOC

Passage Charter School 5600 (145,000) - - - -

Vista Charter School 5600 (1,097,200) - - - -

NET FUNDS AVAILABLE 47,326,623 1,168,768 2,939,398 5,690,460 2,542,477

Program

EXPENDITURES Code

Instruction 0001-2099 26,078,860 - - 1,832,520 1,600,000

Student Support 2100-2199 2,811,570 - - 468,800 -

Instructional Support 2200-2299 1,393,005 - - 1,715,740 -

General Administration 2300-2399 759,800 - - 1,100 -

School Administration 2400-2499 2,692,465 - - - -

Business 2500-2599 787,735 - - - -

Operations & Maintenance 2600-2699 4,492,570 - - 15,000 -

Student Transportation 2700-2799 1,788,100 - - - -

Central supporting 2800-2899 746,990 88,900 - - -

Food Services 3100-3199 - - - - -

Community Svc/Facilities 3300-3399 - - - 572,900 -

Other 2900 & 3400 77,250 - - - -

State Fiscal Emergency Reserve 2600-2699 - - - - -

Capital Outlay 4000-4999 - - - 1,084,400 -

Insurance Premiums 2600-2699 - 648,600 - - -

Principal and Interest 2600-2699 - - - -

Claims 2600-2699 - 28,000 - - -

Food Service Operations 2600-2699 - - 1,984,650 - -

Scholarships 2600-2699 - - - - -

Total Expenditures 41,628,345 765,500 1,984,650 5,690,460 1,600,000

Change in Fund Balance (1,408,745) (728,800) 6,850 - -

Nonspendable Fund Balance 92,000 - - - -

Restricted: TABOR Reserve 1,290,000 - - - -

Board Committed: Retirement Bonus 275,000 - - - -

Board Committed: Contingency Reserve 3,000,000 - - - -

Board Committed: Negotiated 2015-16 800,000 - - - -

Assigned for School Based Health Centers 190,000 - - - -

Total Appropriations 47,275,345 765,500 1,984,650 5,690,460 1,600,000

Unappropriated (Unassigned) Fund Balance 51,278 403,268 954,748 - 942,477

ENDING FUND BALANCE 5,698,278$ 403,268$ 954,748$ -$ 942,477$

Summary Budget Schedule – All Funds 2014-2015 BUDGET

Montrose County School District RE-1J | FINANCIAL SECTION 35

EXPENDITURES,AND FUND BALANCE -- ALL FUNDS Fee In

Lieu

Bond

Fund

Lease/QZAB

Fund

Building

Fund

Capital

Projects

Employee

Medical

Scholarship

Fund TOTAL

26 31 39 41 43 65 79

105,108$ 788,003$ 2,663,486$ 936,631$ 1,501,586$ 771,519$ 1,128,254$ 18,024,053$

- 782,000 - - - - - 14,357,555

25,000 - - - - - - 179,000

- - - - - 31,671,350

- - - - - - - 6,839,905

100 - - 300 800 1,300 20,000 26,800

- - - - 20,000 6,071,500 - 6,091,500

- - - - - - - -

- - - - - - 35,000 35,000

- - - - - - - 302,050

25,100 782,000 300 20,800 6,072,800 55,000 59,503,160

130,208 1,570,003 2,663,486 936,931 1,522,386 6,844,319 1,183,254 77,527,213

- - 400,000 200,000 1,166,700 - - -

- - - - - - - (145,000)

- - - - - - - (1,097,200)

130,208 1,570,003 3,063,486 1,136,931 2,689,086 6,844,319 1,183,254 76,285,013

- - - - 819,000 - - 30,330,380

- - - - - - - 3,280,370

- - - - - - - 3,108,745

- - - - - - - 760,900

- - - - - - - 2,692,465

- - - - - - - 787,735

- - - - 5,000 - - 4,512,570

- - - - 10,000 - - 1,798,100

- - - - - - - 835,890

- - - - - - - -

- - - - - - - 572,900

- - - - - - - 77,250

- - - - - - - -

- - - - 353,500 - - 1,437,900

- - - - - 600,000 - 1,248,600

- 782,000 400,000 - - - - 1,182,000

- - - - - 5,356,200 - 5,384,200

- - - - - - - 1,984,650

- - - - - - 55,000 55,000

- 782,000 400,000 - 1,187,500 5,956,200 55,000 60,049,655

25,100 - - 200,300 - 116,600 - (1,788,695)

- - - - - - - 92,000

- - - - - - - 1,290,000

- - - - - - - 275,000

- - - - - - - 3,000,000

- - - - - - - 800,000

- - - - - - - 190,000

- 782,000 400,000 - 1,187,500 5,956,200 55,000 65,696,655

130,208 788,003 2,663,486 1,136,931 1,501,586 888,119 1,128,254 10,588,358

130,208$ 788,003$ 2,663,486$ 1,136,931$ 1,501,586$ 888,119$ 1,128,254$ 16,235,358$

2014 – 2015 BUDGET Graphs

36 FINANCIAL SECTION | Montrose County School District RE-1J

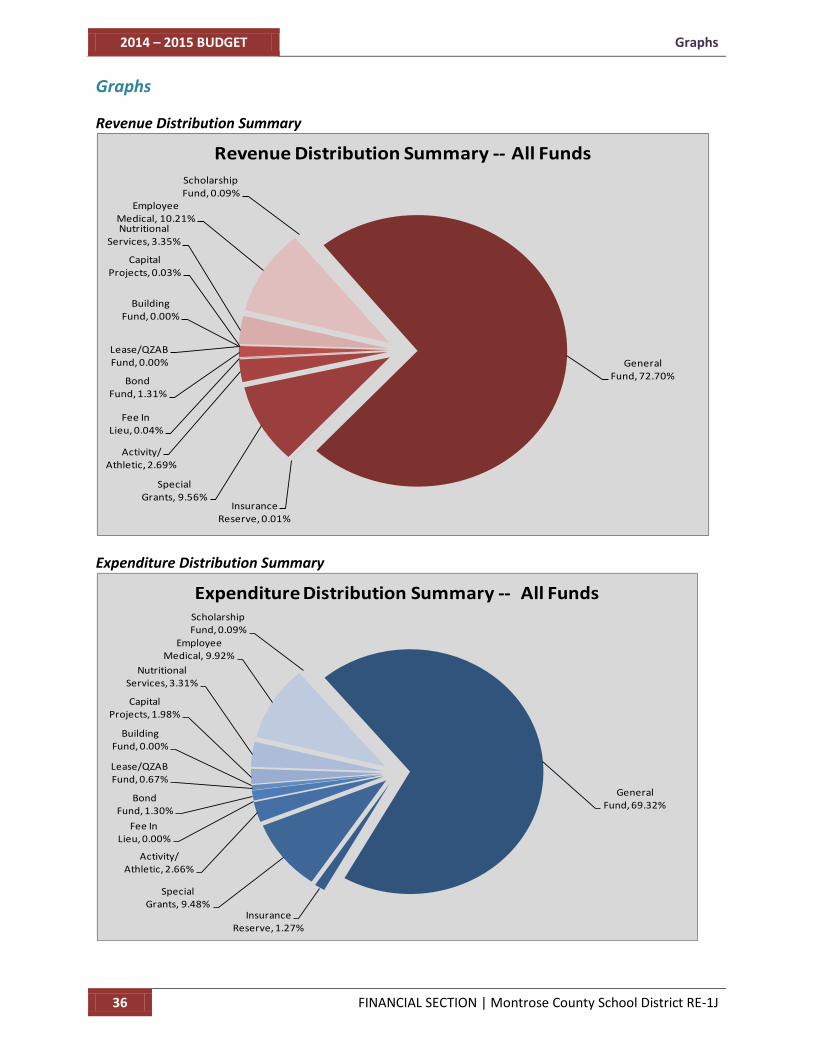

Graphs

Revenue Distribution Summary

GeneralFund, 72.70%

InsuranceReserve, 0.01%

SpecialGrants, 9.56%

Activity/Athletic, 2.69%

Fee InLieu, 0.04%

BondFund, 1.31%

Lease/QZABFund, 0.00%

BuildingFund, 0.00%

CapitalProjects, 0.03%

NutritionalServices, 3.35%

EmployeeMedical, 10.21%

ScholarshipFund, 0.09%

Revenue Distribution Summary -- All Funds

Expenditure Distribution Summary

GeneralFund, 69.32%

InsuranceReserve, 1.27%

SpecialGrants, 9.48%

Activity/Athletic, 2.66%

Fee InLieu, 0.00%

BondFund, 1.30%

Lease/QZABFund, 0.67%

BuildingFund, 0.00%

CapitalProjects, 1.98%

NutritionalServices, 3.31%

EmployeeMedical, 9.92%

ScholarshipFund, 0.09%

Expenditure Distribution Summary -- All Funds

Governmental Funds 2014-2015 BUDGET

Montrose County School District RE-1J | FINANCIAL SECTION 37

Governmental Funds

General Fund (Fund 10) As the district’s major operating fund, the General Fund accounts for the ordinary operating expenditures financed by property taxes, state equalization payments, service charges, and other sources. The fund includes all resources and expenditures not legally or properly accounted for in other funds as directed by C.R.S 22- 45-103(1)(a). The General Fund balance is available to the district for any purpose provided it is expended or transferred according to Colorado Revised Statutes.

The General Fund operating budget contains almost 70% of the District’s total expenditures, and will therefore be shown in greater detail in this section.

Pupil Count Projections In recent years the total student population in the District has fluctuated between 6,100 and 6,500 students. These fluctuations were a product of economic expansion and contraction in the area. The western slope area of Colorado, including Montrose County, tends to lag behind the State and National economies. While the National economy bottomed out in 2009 during the recent recession, Montrose County experienced a slow slide that bottomed out in 2011-12. The local economy appears to have stabilized, but there are currently no reasons to expect another boom or a large influx of population. In fact, the Colorado State Demography Office projects an annual growth rate of 1%-2% for Montrose County through 2040. However, in the short term, the District foresees student counts dropping for the 2014-15 year, due to a particularly large graduating senior class in 2013-14. The District forecasts a flattening of the trend in future years.

It is necessary to note that the graph below represents the actual pupil count as of October 1st for the given year. For funding purposes, the state uses a complex averaging formula that covers the 5 prior years, so the “funded pupil count” is not necessarily the same as the actual count.

5,500

5,700

5,900

6,100

2006 2007 2008 2009 2010 2011 2012 2013EST.

2014EST.

2015EST.

2016

Count 5,672 5,856 6,010 6,011 5,971 5,859 5,768 5,804 5,748 5,740 5,745

Stu

de

nt

Co

un

t

MCSD October Student CountsFull Time Equivalents (FTE)

Per Pupil Allocations Total Program Funding is the revenue available to the district as determined by the School Finance Act of 1994 (as amended for 2014-15) and accounts for approximately 95% of the district’s General Fund Revenue. Each year since passage of the Act, the Colorado Legislature has modified the formula in order to provide funding for public education in the state. Amendment 23, approved by voters statewide in November 2000, requires an annual inflationary increase to the statewide base per pupil amount. For

2014 – 2015 BUDGET Governmental Funds

38 FINANCIAL SECTION | Montrose County School District RE-1J

the 2014-15 budget year the base will be increased by the 2013 Denver-Boulder-Greeley CPI, which was 2.8%, resulting in an increase to the base per pupil amount from $5,954.28 to $6,121, for a change of $167 for FY 2014-15.

Complementary to the state-wide base amount, the Act includes several other multiplying factors that are used to determine the district’s total per pupil funding level before and after at-risk funding. Several years of budget shortfall of revenue forced the state to modify the School Finance Act for the fiscal years 2010-11 through 2013-14. This modification was termed “The Negative Factor” and set the statewide funding level for Colorado school districts below FY2009-2010 funding, which resulted in a 15.5% reduction in revenue compared to the unadjusted School Finance Act funding level. The State experienced a budget surplus during calendar year 2013, and the Negative Factor has been reduced for the 2014-15 school year to 13.2%.

Montrose County School District receives funding in excess of the State’s base per-pupil amount, based on a formula that considers district size, local cost factors, and the percentage of students considered to be “at risk” (i.e. low-income, broken homes, etc.). The district’s adopted budget is based upon the following school finance act factors:

State Averages

Funded Pupil Count 5,748.0 4,687

Base Per Pupil Funding 6,121.00$ 6,121.00$

Cost of Living Factor 1.222 1.166

District Size Factor 1.030 1.423

Personnel Cost Factor 0.881 0.838

Non-Personnel Cost Factor 0.119 0.162

At-Risk Funded Pupil Count 2,880.0 640.4

State Budget Negative Factor -13.2% -13.2%

Anticipated Per Pupil Amount 6,960.63$ 8,963.90$

Anticipated Statutory Formula

Per-Pupil Funding Factors (per CDE)

After the State Legislature has established the funding level per pupil, which usually is not completed until near the end of the session in early May, the amount is multiplied by the projected October funded pupil count to estimate the district’s total program funding. Total program funding will be adjusted by the Colorado Department of Education in December to reflect the actual pupil count; “at-risk” funding based upon actual free lunch and ELL (English Language Learner) counts; the district’s actual assessed valuation; and the actual specific ownership tax collected during the previous fiscal year. The sum of FY2013-14 state aid, local property tax collections estimated at 100%, and specific ownership taxes collected during the fiscal year comprise total program funding projected in the budget.

Full Time Equivalent Employees by Program Montrose County School District hires and assigns workers based on current and anticipated needs at each school site. The following table shows the numbers and types of employees by program across the District that are budgeted for FY2014-15.

Governmental Funds 2014-2015 BUDGET

Montrose County School District RE-1J | FINANCIAL SECTION 39

Position Inst

ruct

ion

al

Stu