addendum revisions of product brochure · health” on page 5 of the product brochure of metlife...

TRANSCRIPT

1

ADDENDUM REVISIONS OF PRODUCT BROCHURE

This addendum should be read in conjunction with the product brochures of MetLife Health Navigator Critical Illness Protector, MetLife Oasis Savings Plan, MetLife Precious Savings Plan, MetLife Retirement Enricher Income Plan and MetLife Sunshine Eternity Plus Savings Plan (collectively, the “Relevant Plans”).

With effect from May 16, 2020 (the “Effective Date”), the premium payment term options available under the Relevant Plans will be revised as follows:

Plan Name Premium Payment Term Options

Suspended from the Effective Date

Remain Available from the Effective Date

MetLife Health Navigator Critical Illness Protector

- 10 years - 15 years - 25 years

- 20 years

MetLife Oasis Savings Plan - 5 years (including premium prepayment option)

- 10 years

- 15 years - 20 years

MetLife Precious Savings Plan - 2 years (including premium prepayment option)

- 10 years - 15 years

- 20 years

MetLife Retirement Enricher Income Plan

- 5 years (including premium prepayment option)

- 10 years - 15 years

- 20 years

MetLife Sunshine Eternity Plus Savings Plan

- 3 years (including premium prepayment option)

- 5 years

- 10 years

1) Product Brochures of Relevant Plans

From the Effective Date, all references and relevant information in relation to the suspended premium payment term options and premium prepayment option (if applicable) shall be deleted from the product brochure of the corresponding Relevant Plans.

2

2) Product Brochure of MetLife Precious Savings Plan

The policy anniversary / policy year when Annual Dividend and Terminal Dividend start to be available varies across different premium payment term options. With the suspension of the premium payment term options of 2 years, 10 years and 15 years, the section of “Annual Dividends and Terminal Dividend” on page 2 and the sections of “Annual Dividend (non-guaranteed)3” and “Terminal Dividend (non-guaranteed) 3” under the Plan Summary on page 7 of the product brochure of MetLife Precious Savings Plan shall be amended in the following manner from the Effective Date: Annual Dividends and Terminal Dividend (on page 2) Your wealth accumulation is given a further boost with annual dividends (non-guaranteed)3, plus a terminal dividend (non-guaranteed)3 which may also be awarded if the policy has remained in force for 2 years or more.

Plan Summary (on page 7) Annual Dividend (non-guaranteed)3

Available during the policy term, starting from the 2nd policy anniversary date.

Annual dividend options: (i) Withdraw it when it is distributed; or (ii) Leave it in the policy for wealth accumulation

Terminal Dividend (non-guaranteed)3

Available for policies which have been in force for 2 years or more and payable upon policy termination during or at the end of the policy term.

3) Product Brochure of MetLife Retirement Enricher Income Plan

The policy anniversary when terminal dividend starts to be available varies across different premium payment term options. With the suspension of the premium payment term options of 5 years, 10 years and 15 years, the section of “Build Your Retirement Reserve” on page 2 of the product brochure of MetLife Retirement Enricher Income Plan shall be amended in the following manner from the Effective Date: Build Your Retirement Reserve (on page 2) • The Plan has built-in capability to grow your retirement reserve with guaranteed cash

value5. • Your retirement fund accumulation is given a further boost with a terminal dividend (non-

guaranteed)6 which is payable upon policy termination on or after the 2nd policy anniversary date.

1

ADDENDUM REVISIONS OF PRODUCT BROCHURE

This addendum should be read in conjunction with the product brochures of MetLife Health Navigator Critical Illness Protector and MetLife Health-is-Wealth Medical Plan, and the rider leaflet of MetLife Health-is-Wealth Medical Benefit.

1) Product Brochure of MetLife Health Navigator Critical Illness Protector

• With immediate effect, the following sentence will be added as the last sentence of the sub-section of “Vision Care Benefit9” under the section of “Value-add Services to Upgrade Your Health” on page 5 of the product brochure of MetLife Health Navigator Critical Illness

Protector: “To be eligible for the Vision Care Benefit, the policy of the Plan must be approved and issued by MetLife Limited on or before June 30, 2020 and such policy must remain in force after the cooling-off period.”

• With effect from July 1, 2020, all references and relevant information in relation to the Vision Care Benefit shall be deleted from the product brochure of MetLife Health Navigator Critical Illness Protector.

2) Product Brochure of MetLife Health-is-Wealth Medical Plan • With immediate effect, the following sentence will be added as the 4th paragraph of the

section of “‘Vision Care Benefit’ – Better Management of Diabetes” on page 4 of the product brochure of MetLife Health-is-Wealth Medical Plan: “To be eligible for the Vision Care Benefit, the policy of the Plan must be approved and issued by MetLife Limited on or before June 30, 2020 and such policy must remain in force after the cooling-off period.”

• With effect from July 1, 2020, all references and relevant information in relation to the Vision Care Benefit shall be deleted from the product brochure of MetLife Health-is-Wealth Medical Plan.

3) Rider Leaflet of MetLife Health-is-Wealth Medical Benefit • With immediate effect, the following sentence will be added as the 4th paragraph of the

section of “‘Vision Care Benefit’ – Better Management of Diabetes” on page 3 of the rider leaflet of MetLife Health-is-Wealth Medical Benefit: “To be eligible for the Vision Care Benefit, the policy of the basic plan to which the Optional Rider is attached must be approved and issued by MetLife Limited on or before June 30, 2020 and such policy along with the Optional Rider must remain in force after the cooling-off period.”

• With effect from July 1, 2020, all references and relevant information in relation to the Vision Care Benefit shall be deleted from the rider leaflet of MetLife Health-is-Wealth Medical Benefit.

MetLife Health Navigator Critical Illness ProtectorMetLife Extra Love Benefit (Optional Rider)

MetLife Extra Love Plus Benefit (Optional Rider)

Navigate Your Healthcare Journey with Extra Love and Protection

Did you know?

StrokeAround 25,000 people suffer

from stroke each year (vii)

Heart AttackAbout 77,600 inpatients

in 2015(vi)

Liver cancer patients have a high risk of tumor recurrence at

30-40%(iii) in the first year after

surgical resection

Cancer is the number one killer disease in Hong Kong(i). However, with early detection and treatment, there could be a higher survival rate. The 5-year survival rate for prostate cancer

and breast cancer can be as high as 99%(ii)

Cancers may recur multiple times despite a higher survival rate with early detection and treatment.

Targeted therapies give cancer patients new hope by turning cancers into chronic diseases, but patients may not be able to afford expensive medical expenses in the long run.

Heart disease and stroke are amongst the top 5 killer diseases in Hong Kong(i). Their morbidity rates continue to rise.

Targeted therapy can double the progression-free survival time(iv) compared to the current standard treatment for lung cancer patients

Medical expenses of targeted therapies for each lung cancer patient can be as high as HK$200,000 a year (v)

Sources:(i) Center for Health Protection, HKSAR (2015 Figure)(ii) American Cancer Society, Cancer Facts & Figures, 2006-2012 statistics, 5-year relative survival rates for local cancers at diagnosis (as of

March 2017)(iii) Cancer Fund Website, HKSAR (as of August 2017)(iv) The New England Journal of Medicine (June 2017)(v) Cancer Fund Website, HKSAR (as of August 2017)(vi) Figure includes heart attack inpatient discharges and inpatient deaths. Source: Center for Health Protection, HKSAR (2015 Figure) (vii) Stroke Fund Website, HKSAR (as of August 2017)

1

Your Journey, Your HealthHealth protection starts from here

Along life’s journey, we may face sudden dangers, such that life does not follow our plans or schedule. MetLife Health Navigator Critical Illness Protector (“MetLife Health Navigator”) together with an optional rider, MetLife Extra Love Benefit or MetLife Extra Love Plus Benefit (the “Optional Rider”) are available to provide comprehensive protection for your healthcare journey:

Ready to begin your healthy journey? Start now!

Upon diagnosis of a late stage critical illness: All future premiums are waived 3

We know that suffering from a Late Stage Critical Illness is already a great blow to you, so we will waive future premiums3 for you, while providing you with continuous protection.

4

Waiver of Premium

When suffering from an early stage critical illness: Receive up to 50% of the sum assured2,4,5 (if MetLife Extra Love Benefit is selected) or up to 100% of the sum assured2,4,5 (if MetLife Extra Love Plus Benefit is selected)

We understand early treatment may increase the chances of recovery. That is why we go beyond the typical market practice and offer a higher benefit amount for an Early Stage Critical Illness, giving you adequate funds for early treatment.

5

Early Stage Critical

Illness Benefit

When a critical illness persists, recurs or spreads: Multiple claims may be honored

Critical illnesses such as cancer may recur, spread or persist. And it is getting more common for individuals to suffer from more than one critical illness in a lifetime. We understand your worries and with the Optional Rider, we offer multiple claims for Early Stage and Late Stage Critical Illnesses. The optional rider offers up to 300% of its sum assured as benefit for Cancer, and allows up to 2 times cover for Heart Attack and Stroke each.

2

Multiple Claims

Unconventional customized protection

We have gone beyond the market norm by allowing you to choose the sum assured for the Optional Rider at as much as the sum assured of 150% of the basic plan, MetLife Health Navigator in order to provide greater protection against Early Stage Critical Illnesses and greater amounts for multiple claim coverage. With MetLife Health Navigator and the Optional Rider, you can enjoy total coverage of up to 1450%* of sum assured of the basic plan.

1

Flexibility

* The figure is for illustrative purpose only and based on the assumption that the amount of sum assured of the Optional Rider is 150% of the sum assured of MetLife Health Navigator and the amounts of sum assured of MetLife Health Navigator and the Optional Rider remain unchanged throughout the policy term, and all claims made fulfill claims conditions under MetLife Health Navigator and the Optional Rider. Please refer to the respective Policy Provisions for details.

Upon the first instance of suffering from a late stage critical illness: You are protected by dual coverage

Why is the dual coverage1,2 so important? Because we understand that this could be your most helpless, destitute time, we want to give you double the support, and provide sufficient resources to help you face the challenge.

3

Dual Coverage

2

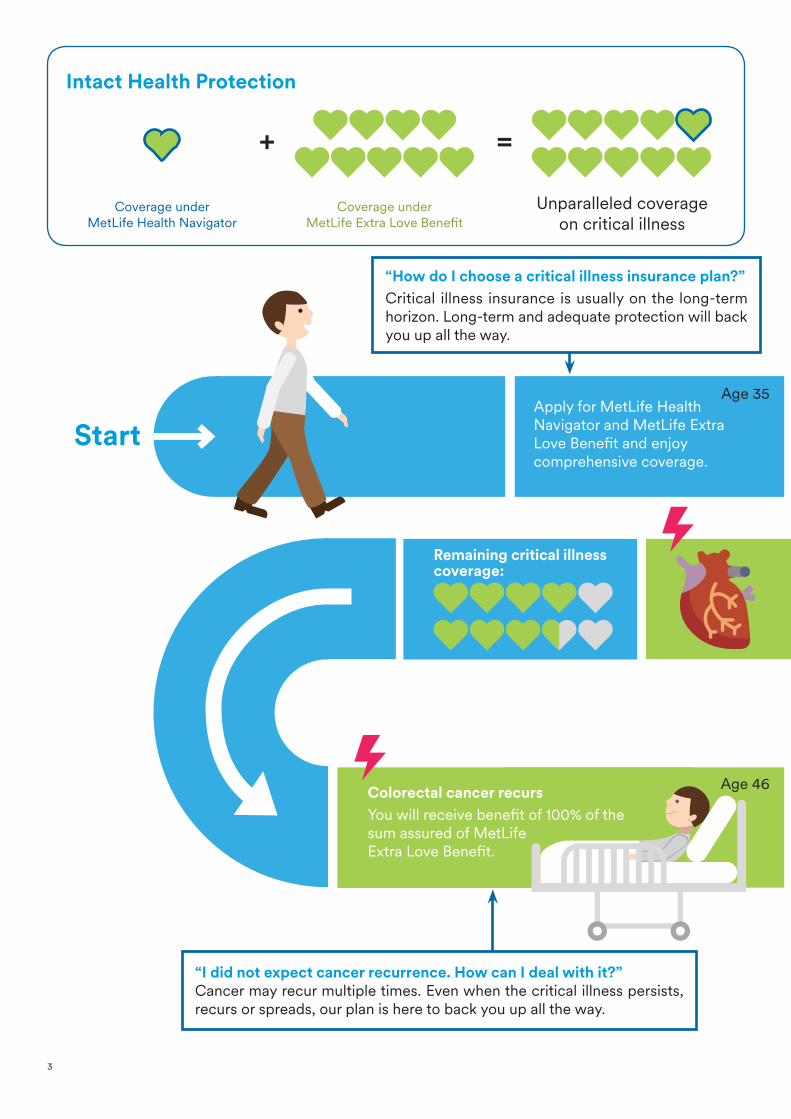

Intact Health Protection

Coverage under MetLife Health Navigator

Coverage under MetLife Extra Love Benefit

Unparalleled coverage on critical illness

+ =

“How do I choose a critical illness insurance plan?”Critical illness insurance is usually on the long-term horizon. Long-term and adequate protection will back you up all the way.

Apply for MetLife Health Navigator and MetLife Extra Love Benefit and enjoy comprehensive coverage.

Remaining critical illness coverage:

Colorectal cancer recurs You will receive benefit of 100% of the sum assured of MetLife Extra Love Benefit.

StartAge 35

Age 46

“I did not expect cancer recurrence. How can I deal with it?” Cancer may recur multiple times. Even when the critical illness persists, recurs or spreads, our plan is here to back you up all the way.

3

Continuous protectionIn case you are diagnosed

with any other covered critical illness, you will be equipped with coverage up to 5.5 times of the

sum assured of MetLife Extra Love Benefit

up to age 85.

Each represents 100% of sum assured

Each represents 50% of sum assuredRemark: The sum assured of MetLife Health Navigator and

MetLife Extra Love Benefit may not be the same.

Diagnosed with colorectal cancer You will receive:- Dual coverage1,2

- All future premiums waived3

Diagnosed with early stage heart diseaseYou will receive 50% of the sum assured4,5 of MetLife Extra Love Benefit for timely treatment.

Diagnosed with lung cancer You will receive benefit of 100% of the sum assured of MetLife Extra Love Benefit.

Your critical illness coverage:

Remaining critical illness coverage:

Remaining critical illness coverage:

Remaining critical illness coverage:

Age 40

Age 45

Age 48

“It is my first time suffering from a late stage critical illness. Is it an incurable disease?”Upon the first instance of suffering from a critical illness, your life goals may be disrupted. This could be your most helpless time. We give you dual coverage1,2 for medical expenses or other needs.

“If the Early Stage Critical Illness strikes, will I be eligible for claims immediately?”We understand early treatment may increase the chances of recovery. When you are destitute, coverage on Early Stage Critical Illness Benefit gives you financial support for timely treatment.

“I am well prepared. But do I have sufficient support for treatment?” No one could foresee recurrence of illness. You can obtain timely treatment with prompt protection. With the waiting period as short as 1 year, you will receive timely support if you are diagnosed with new cancer(s).

4

MetLife Health Navigator Critical Illness Protector

We all care about our health, but are you sure you have the right coverage that really looks after your needs at every stage of your life? MetLife Health Navigator here to back you up all the way.

Comprehensive Lifelong ProtectionMetLife Health Navigator offers coverage for 79 critical illnesses up to the age of 100, including minor critical illnesses, specialized protection against certain childhood, female and male illnesses, and Late Stage Critical Illnesses6.

If the insured person is diagnosed with any covered Minor Critical Illnesses7 or Severe Child Critical Illnesses7,8, 25% of the sum assured will be paid. As for confirmed diagnosis of any one of the covered Late Stage Critical Illnesses6, 100% of the current sum assured will be paid.

To give you an effective first line of defense, Minor Critical Illness7 coverage includes Carcinoma-in-situ and Coronary Angioplasty. A maximum of 2 claims are available for Coronary Angioplasty and Carcinoma-in-situ respectively7.

Value-add Services to Upgrade Your HealthVision Care Benefit9 — Underlying conditions such as hypertension, high cholesterol and diabetes may be identified at the earliest opportunity through thorough eye examinations. That's why we offer the Vision Care Benefit9 under MetLife Health Navigator. You can enjoy full coverage for a comprehensive eye examination in the first policy year, which includes intra-ocular pressure measurement, ocular health assessment and fundus examination, consultation and recommendation, and more. A summary of the optometrist’s clinical findings and observations from the examination, including retinal photos, will be provided upon request, free of charge.

Second Medical Opinion Service10 — MetLife Health Navigator also provides the Second Medical Opinion Service10 giving the insured person access to a designated medical network for a free consultation.

Adding Value to Your Policy over TimeMetLife Health Navigator provides guaranteed cash value11. It also offers non-guaranteed accumulated dividends and interest12 (if any) and a non-guaranteed terminal dividend13 (if any) — increasing the value of your savings while you are in good health.

Life Benefit Protecting Your Loved OnesIn the unfortunate event of the death of the insured person during the policy term, the beneficiary(ies) will receive a Life Benefit14 equivalent to 100% of the current sum assured, plus non-guaranteed accumulated dividends and interest12 (if any) and non-guaranteed terminal dividend13 (if any).

Various Payment Terms for Financial FlexibilityYou can choose from a premium payment term of 10 years, 15 years, 20 years or 25 years to enjoy protection up to the age of 1008, so that you can plan your finances ahead.

5

MetLife Extra Love Benefit / MetLife Extra Love Plus Benefit (Optional Rider)The Optional Rider helps further reinforce your safeguard against critical illnesses by offering multiple claims against Early Stage Critical Illnesses and Late Stage Critical Illnesses. Extra peace of mind comes with extra protection!

Unconventional Customized Protection

We understand you want insurance coverage customized to your protection needs. That’s we have gone beyond the market norm by allowing you to choose the sum assured for the Optional Rider at as much as 150% of the sum assured of the basic plan, MetLife Health Navigator. That means you can enjoy higher protection for Early Stage Critical Illnesses and greater multiple claim coverage without increasing the sum assured and premium for the basic plan. Through innovation, we provide you with unparalleled protection to back up your health along the way.

With MetLife Health Navigator and the Optional Rider, you can enjoy dual coverage1,2 for the first instance of confirmed diagnosis of a covered Late Stage Critical Illness. You will receive benefit under both MetLife Health Navigator and the Optional Rider. This stands out from the typical market practice, providing you with the peace of mind that comes from simplicity.

With MetLife Health Navigator and the Optional Rider, you can enjoy total coverage of up to of sum assured of the basic plan

Flexibility

Dual Coverage

* The figure is for illustrative purpose only and based on the assumption that the amount of sum assured of the Optional Rider is 150% of the sum assured of MetLife Health Navigator, the amounts of sum assured of MetLife Health Navigator and the Optional Rider remain unchanged throughout the policy term, and all claims made fulfill claims conditions under MetLife Health Navigator and the Optional Rider. Please refer to the respective Policy Provisions for details.

Maximum Benefit under the Optional Rider (based on the percentage of its sum assured)

Group 1Cancer300%

Up to 900% Total Coverage under the Optional Rider

Group 5Diseases related to neurological degeneration

100%

Group 2Diseases related to

organ failure 100%

Group 6Diseases

related to the musculoskeletal

system 100%

Group 3Diseases related to the heart and

blood vessels 100%

(Maximum benefit for Heart Attack is 200%)

Group 7Other diseases

100%

Group 4Diseases related to the nervous

system 100%

(Maximum benefit for Stroke is 200%)

Multiple Claims for Intact Defense

Critical illnesses may recur, spread or persist. And it is getting more common for individuals to suffer more than one critical illness in a lifetime. The Optional Rider allows multiple claims for Early Stage and Late Stage Critical Illnesses of up to 900% of the sum assured.

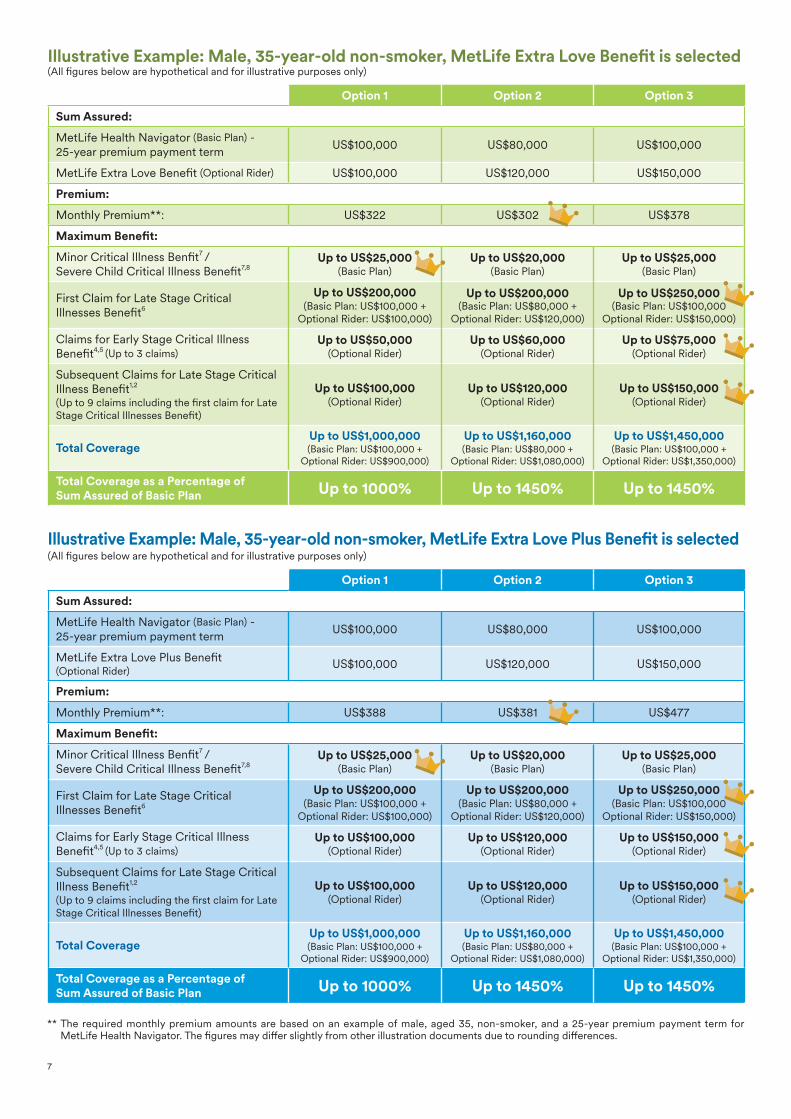

Illustrative Example: Male, 35-year-old non-smoker, MetLife Extra Love Plus Benefit is selected(All figures below are hypothetical and for illustrative purposes only)

Option 1 Option 2 Option 3

Sum Assured:

MetLife Health Navigator (Basic Plan) - 25-year premium payment term US$100,000 US$80,000 US$100,000

MetLife Extra Love Plus Benefit (Optional Rider)

US$100,000 US$120,000 US$150,000

Premium:

Monthly Premium**: US$388 US$381 US$477

Maximum Benefit:

Minor Critical Illness Benfit7 /Severe Child Critical Illness Benefit7,8

Up to US$25,000(Basic Plan)

Up to US$20,000(Basic Plan)

Up to US$25,000(Basic Plan)

First Claim for Late Stage Critical Illnesses Benefit6

Up to US$200,000(Basic Plan: US$100,000 +

Optional Rider: US$100,000)

Up to US$200,000(Basic Plan: US$80,000 +

Optional Rider: US$120,000)

Up to US$250,000(Basic Plan: US$100,000

Optional Rider: US$150,000)

Claims for Early Stage Critical Illness Benefit4,5 (Up to 3 claims)

Up to US$100,000(Optional Rider)

Up to US$120,000(Optional Rider)

Up to US$150,000(Optional Rider)

Subsequent Claims for Late Stage Critical Illness Benefit1,2 (Up to 9 claims including the first claim for Late Stage Critical Illnesses Benefit)

Up to US$100,000(Optional Rider)

Up to US$120,000(Optional Rider)

Up to US$150,000(Optional Rider)

Total CoverageUp to US$1,000,000(Basic Plan: US$100,000 +

Optional Rider: US$900,000)

Up to US$1,160,000(Basic Plan: US$80,000 +

Optional Rider: US$1,080,000)

Up to US$1,450,000(Basic Plan: US$100,000 +

Optional Rider: US$1,350,000)

Total Coverage as a Percentage of Sum Assured of Basic Plan Up to 1000% Up to 1450% Up to 1450%

** The required monthly premium amounts are based on an example of male, aged 35, non-smoker, and a 25-year premium payment term for MetLife Health Navigator. The figures may differ slightly from other illustration documents due to rounding differences.

Illustrative Example: Male, 35-year-old non-smoker, MetLife Extra Love Benefit is selected(All figures below are hypothetical and for illustrative purposes only)

Option 1 Option 2 Option 3

Sum Assured:

MetLife Health Navigator (Basic Plan) - 25-year premium payment term US$100,000 US$80,000 US$100,000

MetLife Extra Love Benefit (Optional Rider) US$100,000 US$120,000 US$150,000

Premium:

Monthly Premium**: US$322 US$302 US$378

Maximum Benefit:

Minor Critical Illness Benfit7 /Severe Child Critical Illness Benefit7,8

Up to US$25,000(Basic Plan)

Up to US$20,000(Basic Plan)

Up to US$25,000(Basic Plan)

First Claim for Late Stage Critical Illnesses Benefit6

Up to US$200,000(Basic Plan: US$100,000 +

Optional Rider: US$100,000)

Up to US$200,000(Basic Plan: US$80,000 +

Optional Rider: US$120,000)

Up to US$250,000(Basic Plan: US$100,000

Optional Rider: US$150,000)

Claims for Early Stage Critical Illness Benefit4,5 (Up to 3 claims)

Up to US$50,000(Optional Rider)

Up to US$60,000(Optional Rider)

Up to US$75,000(Optional Rider)

Subsequent Claims for Late Stage Critical Illness Benefit1,2 (Up to 9 claims including the first claim for Late Stage Critical Illnesses Benefit)

Up to US$100,000(Optional Rider)

Up to US$120,000(Optional Rider)

Up to US$150,000(Optional Rider)

Total CoverageUp to US$1,000,000(Basic Plan: US$100,000 +

Optional Rider: US$900,000)

Up to US$1,160,000(Basic Plan: US$80,000 +

Optional Rider: US$1,080,000)

Up to US$1,450,000(Basic Plan: US$100,000 +

Optional Rider: US$1,350,000)

Total Coverage as a Percentage of Sum Assured of Basic Plan Up to 1000% Up to 1450% Up to 1450%

7

Early Stage Critical Illnesses Maximum Number of ClaimsPer Disease Group Overall

Group 1: Cancer 3

3Group 2: Diseases related to organ failure 1

Group 3: Diseases related to the heart and blood vessels

1

Group 4: Diseases related to the nervous system

1

Group 5: Diseases related to neurological degeneration

1

Group 6: Diseases related to the musculoskeletal system

1

Group 7: Other diseases 1

Today, many forms of critical illnesses can be treated successfully if properly diagnosed at an early stage. That’s why the Optional Rider provides the Early Stage Critical Illness Benefit2,4,5.

Two options of the Optional Rider are available, being MetLife Extra Love Benefit and MetLife Extra Love Plus Benefit. Upon confirmed diagnosis of any of the 60 covered Early Stage Critical Illnesses, 50% of the sum assured (if MetLife Extra Love Benefit is selected) or 100% of the sum assured (if MetLife Extra Love Plus Benefit is selected) will be offered.

Early Stage Critical Illness

Benefit

When it comes to Late Stage Critical Illnesses, the diagnosis can be devastating. But with greater protection comes greater peace of mind. That’s why the Optional Rider provides the Late Stage Critical Illness Benefit2,4,5,15, which allows a maximum of 9 total claims for 70 Late Stage Critical Illnesses on top of MetLife Health Navigator. This benefit offers up to 300% of the sum assured of the Optional Rider for Cancer, and allows up to 2 times cover for Heart Attack and Stroke each.

Late Stage Critical Illnesses Maximum Number of ClaimsPer Disease Group Overall

Group 1: Cancer 3

9Group 2: Diseases related to organ failure 1

Group 3: Diseases related to the heart and blood vessels

1(1 extra claim is available

for Heart Attack)

Group 4: Diseases related to the nervous system

1(1 extra claim is available

for Stroke)

Group 5: Diseases related to neurological degeneration

1

Group 6: Diseases related to the musculoskeletal system

1

Group 7: Other diseases 1

Late Stage Critical Illness

Benefit

8

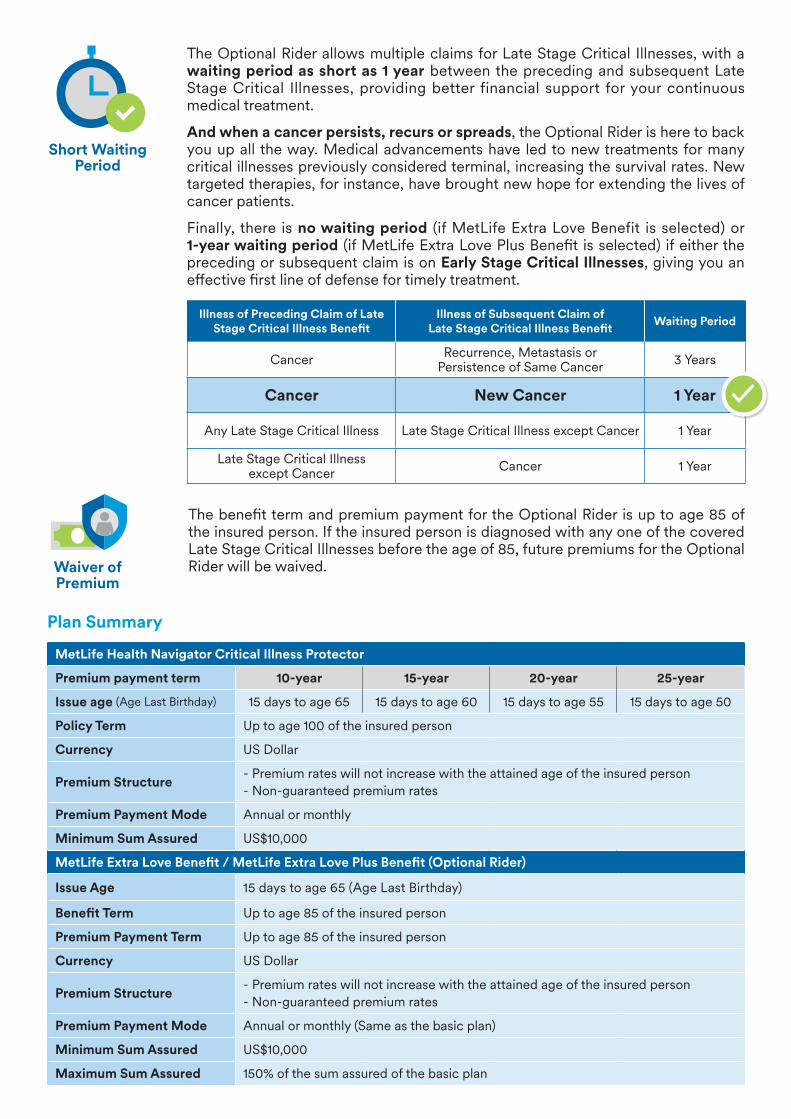

The Optional Rider allows multiple claims for Late Stage Critical Illnesses, with a waiting period as short as 1 year between the preceding and subsequent Late Stage Critical Illnesses, providing better financial support for your continuous medical treatment.

And when a cancer persists, recurs or spreads, the Optional Rider is here to back you up all the way. Medical advancements have led to new treatments for many critical illnesses previously considered terminal, increasing the survival rates. New targeted therapies, for instance, have brought new hope for extending the lives of cancer patients.

Finally, there is no waiting period (if MetLife Extra Love Benefit is selected) or 1-year waiting period (if MetLife Extra Love Plus Benefit is selected) if either the preceding or subsequent claim is on Early Stage Critical Illnesses, giving you an effective first line of defense for timely treatment.

Illness of Preceding Claim of Late Stage Critical Illness Benefit

Illness of Subsequent Claim of Late Stage Critical Illness Benefit Waiting Period

Cancer Recurrence, Metastasis or Persistence of Same Cancer 3 Years

Cancer New Cancer 1 Year

Any Late Stage Critical Illness Late Stage Critical Illness except Cancer 1 Year

Late Stage Critical Illness except Cancer Cancer 1 Year

The benefit term and premium payment for the Optional Rider is up to age 85 of the insured person. If the insured person is diagnosed with any one of the covered Late Stage Critical Illnesses before the age of 85, future premiums for the Optional Rider will be waived.

✓

Short Waiting Period

Waiver of Premium

Plan Summary

MetLife Health Navigator Critical Illness Protector

Premium payment term 10-year 15-year 20-year 25-year

Issue age (Age Last Birthday) 15 days to age 65 15 days to age 60 15 days to age 55 15 days to age 50

Policy Term Up to age 100 of the insured person

Currency US Dollar

Premium Structure- Premium rates will not increase with the attained age of the insured person- Non-guaranteed premium rates

Premium Payment Mode Annual or monthly

Minimum Sum Assured US$10,000

MetLife Extra Love Benefit / MetLife Extra Love Plus Benefit (Optional Rider)

Issue Age 15 days to age 65 (Age Last Birthday)

Benefit Term Up to age 85 of the insured person

Premium Payment Term Up to age 85 of the insured person

Currency US Dollar

Premium Structure- Premium rates will not increase with the attained age of the insured person- Non-guaranteed premium rates

Premium Payment Mode Annual or monthly (Same as the basic plan)

Minimum Sum Assured US$10,000

Maximum Sum Assured 150% of the sum assured of the basic plan

Mr. ChanAccountant, married with a son, non-smoking

As the primary breadwinner, Mr. Chan decided, at age 40, to apply for MetLife Health Navigator and MetLife Extra Love Plus Benefit, each with the sum assured of US$100,000 for health protection. The monthly premium is US$466#.

Case Studies (All figures below are hypothetical and for illustrative purposes only)

Case 1 - Multiple claims with a short waiting period

# The required monthly premium amounts are based on an example of non-smoking male, aged 40, with a sum assured of US$100,000 for both MetLife Health Navigator and MetLife Extra Love Plus Benefit, and a 25-year premium payment term for MetLife Health Navigator. The figures may differ slightly from other illustration documents due to rounding differences.

Mr. Chan was diagnosed with Stroke at age 48. He was then diagnosed with Tumor of the Prostate. Later, he was unfortunately diagnosed as having suffered from Heart Attack. All the way, MetLife Health Navigator and MetLife Extra Love Plus Benefit provide a strong backup for Mr. Chan, by offering multiple claims with a short waiting period.

Diagnosed with Stroke

15 months later

Diagnosed with Tumor of the

Prostate

13 months later

Diagnosed with Heart

Attack

Age 48 Age 50 Age 51

Received treatment for Stroke

Underwent timely surgery to remove the tumor

Undertook cardiac surgery

Received US$200,000 (100% of the sum assured under both MetLife Health

Navigator and MetLife Extra Love Plus Benefit)

Future Premiums are Waived

Received US$100,000(100% of the sum assured under MetLife Extra Love

Plus Benefit)

Received US$100,000(100% of the sum assured under MetLife Extra Love

Plus Benefit)

10

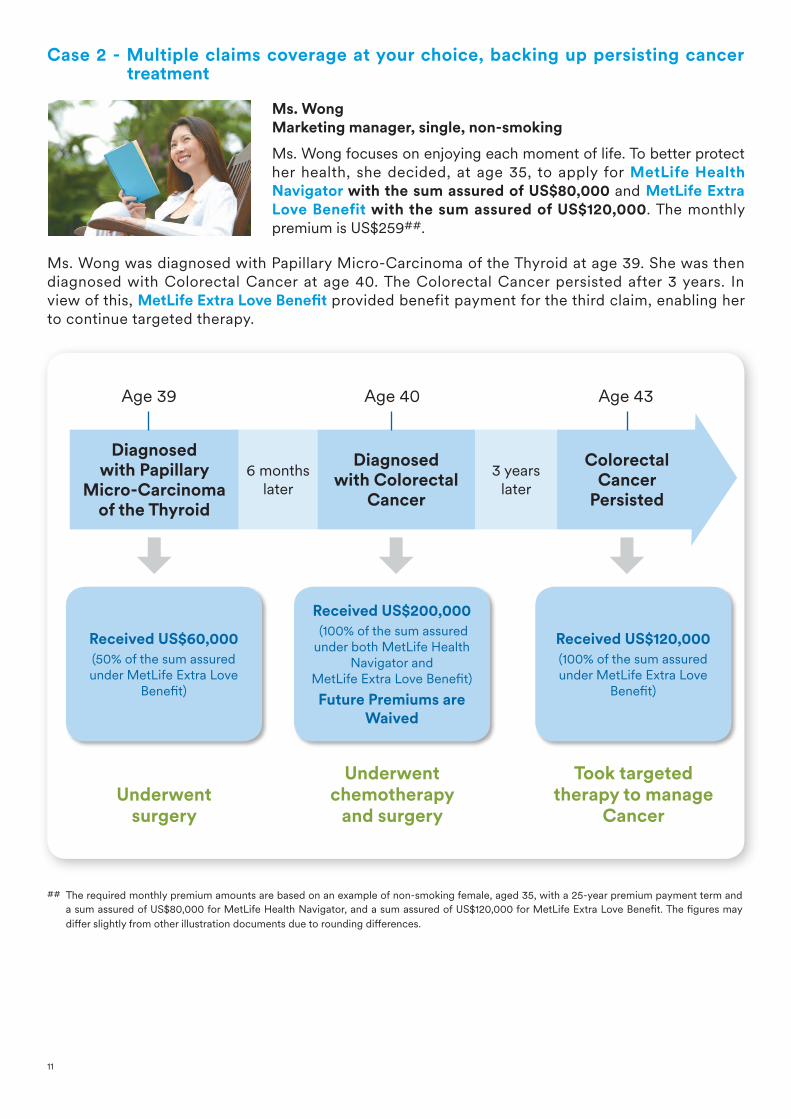

Ms. WongMarketing manager, single, non-smoking

Ms. Wong focuses on enjoying each moment of life. To better protect her health, she decided, at age 35, to apply for MetLife Health Navigator with the sum assured of US$80,000 and MetLife Extra Love Benefit with the sum assured of US$120,000. The monthly premium is US$259##.

Case 2 - Multiple claims coverage at your choice, backing up persisting cancer treatment

## The required monthly premium amounts are based on an example of non-smoking female, aged 35, with a 25-year premium payment term and a sum assured of US$80,000 for MetLife Health Navigator, and a sum assured of US$120,000 for MetLife Extra Love Benefit. The figures may differ slightly from other illustration documents due to rounding differences.

Ms. Wong was diagnosed with Papillary Micro-Carcinoma of the Thyroid at age 39. She was then diagnosed with Colorectal Cancer at age 40. The Colorectal Cancer persisted after 3 years. In view of this, MetLife Extra Love Benefit provided benefit payment for the third claim, enabling her to continue targeted therapy.

Diagnosed with Papillary

Micro-Carcinoma of the Thyroid

6 months later

Diagnosed with Colorectal

Cancer

3 years later

Colorectal Cancer

Persisted

Age 39 Age 40 Age 43

Underwent surgery

Underwentchemotherapy

and surgery

Took targeted therapy to manage

Cancer

Received US$60,000(50% of the sum assured under MetLife Extra Love

Benefit)

Received US$200,000 (100% of the sum assured under both MetLife Health

Navigator and MetLife Extra Love Benefit)

Future Premiums are Waived

Received US$120,000(100% of the sum assured under MetLife Extra Love

Benefit)

11

Table 1: Early Stage Critical Illnesses and Late Stage Critical Illnesses Covered

MetLife Extra Love BenefitMetLife Extra Love Plus Benefit

MetLife Health NavigatorMetLife Extra Love Benefit

MetLife Extra Love Plus Benefit60 Early Stage Critical Illnesses Covered 70 Late Stage Critical Illnesses Covered

Group 1Cancer

1. Early Stage Malignancy- Tumor of the Prostate- Chronic Lymphocytic Leukaemia - Papillary Micro-Carcinoma of the Thyroid- Papillary Micro-Carcinoma of the Bladder- Non-melanoma Skin Cancer

1. Cancer

Group 2Diseases related to organfailure

2. Biliary Tract Reconstruction Surgery 2. Acquired Immune Deficiency Syndrome (AIDS) Due to Blood Transfusion

3. Chronic Auto-immune Hepatitis 3. Acute Necrohemorrhagic Pancreatitis4. Chronic Lung Disease 4. Aplastic Anaemia5. Hepatitis with Cirrhosis 5. Cardiomyopathy6. Less Severe Aplastic Anaemia 6. Chronic Liver Failure7. Less Severe Coma 7. Coma8. Less Severe Kidney Disease 8. End Stage Lung Disease9. Less Severe Systemic Lupus

Erythematosus 9. Fulminant Viral Hepatitis

10. Liver Surgery 10. Kidney Failure11. Moderately Severe Crohn’s Disease 11. Loss of Independent Existence+

12. Moderately Severe Ulcerative Colitis 12. Major Organ Transplantation13. Secondary Pulmonary Hypertension 13. Medullary Cystic Disease14. Surgical Removal of One Lung 14. Occupationally Acquired Human

Immunodeficiency Virus (HIV)15. Pulmonary Arterial Hypertension (Primary)16. Resection of the Whole Small Intestine (duodenum, jejunum and ilium)17. Severe Crohn’s Disease18. Severe Ulcerative Colitis19. Systemic Lupus Erythematosus (SLE) with Lupus Nephritis20. Total Pancreatectomy

Group 3Diseases related to the heartand blood vessels

15. Angioplasty or Endarterectomy for Carotid Arteries

21. Brugada Syndrome Requiring Defibrillator Insertion

16. Cardiac Pacemaker or Defibrillator Insertion 22. Coronary Artery By-pass Surgery17. Emergency Intravenous Anti-arrhythmic Therapy for Ventricular Tachycardia or Fibrillation

23. Dissecting Aortic Aneurysm

18. Endovascular Treatments of Aortic Disease or Aortic Aneurysm 24. Eisenmenger’s Syndrome

19. Endovascular Treatment of Peripheral Arterial Disease 25. Heart Attack

20. Insertion of a Veno-cava Filter 26. Heart Valve Replacement21. Less Invasive Treatments of Heart Valve

Disease 27. Infective Endocarditis

22. Minimally Invasive Direct Coronary Artery By-pass 28. Other Serious Coronary Artery Disease

23. Moderately Severe Infective Endocarditis 29. Surgery for Disease of Aorta24. Pericardiectomy 30. Temporal Arteritis or Cranial Arteritis25. Cerebral Shunt Insertion 31. Accidental Fracture of Spinal Column++

Group 4Diseases related to the nervous system

26. Early Amyotrophic Lateral Sclerosis 32. Amyotrophic Lateral Sclerosis27. Early Motor Neurone Disease 33. Apallic Syndrome28. Early Multiple Sclerosis 34. Bacterial Meningitis29. Early Progressive Bulbar Palsy 35. Benign Brain Tumor30. Early Progressive Supranuclear Palsy^ 36. Cerebral Aneurysm Requiring Surgery31. Early Spinal Muscular Atrophy^ 37. Encephalitis32. Early Tuberculous Myelitis 38. Major Head Trauma

MetLife Extra Love BenefitMetLife Extra Love Plus Benefit

MetLife Health NavigatorMetLife Extra Love Benefit

MetLife Extra Love Plus Benefit60 Early Stage Critical Illnesses Covered 70 Late Stage Critical Illnesses Covered

33. Endovascular Treatment for Cerebral Aneurysm 39. Motor Neurone Disease

34. Less Severe Bacterial Meningitis 40. Multiple Sclerosis35. Less Severe Encephalitis 41. Paralysis36. Moderately Severe Brain Damage 42. Poliomyelitis37. Moderately Severe Paralysis 43. Progressive Bulbar Palsy38. Moderately Severe Poliomyelitis 44. Progressive Supranuclear Palsy39. Severe Epilepsy 45. Spinal Muscular Atrophy^

40. Surgery for Subdural Haematoma 46. Stroke47. Tuberculous Meningitis

Group 5Diseases related toneurological degeneration

41. Moderately Severe Creutzfeld-Jacob Disease (CJD)

48. Advanced Dementia (including Alzheimer’s Disease)

42. Moderately Severe Parkinson’s Disease 49. Creutzfeld-Jacob Disease50. Parkinson’s Disease

Group 6Diseases related to themusculoskeletal system

43. Early Systemic Scleroderma 51. Muscular Dystrophy44. Moderate Severe Ankylosing Spondylitis 52. Necrotising Fasciitis

45. Moderately Severe Muscular Dystrophy^ 53. Psoriasis Arthritis

46. Moderately Severe Rheumatoid Arthritis 54. Severe Ankylosing Spondylitis47. Osteoporosis with Fractures 55. Severe Myasthenia Gravis

56. Severe Osteoporosis57. Severe Rheumatoid Arthritis58. Systemic Scleroderma

Group 7Other diseases

48. Adrenalectomy for Adrenal Adenoma 59. Amputation of Feet Due to Complication from Diabetes

49. Amputation of Four Fingers of Both Hands 60. Blindness

50. Cochlear Implant Surgery 61. Chronic Adrenal Insufficiency (Addison’s Disease)

51. Diabetic Retinopathy 62. Deafness52. Facial Burns Due to Accident 63. Ebola53. Grade 4 Hypertensive Retinopathy 64. Elephantiasis54. Loss of Hearing in One Ear 65. Loss of Limbs55. Loss of One Limb 66. Loss of Speech56. Loss of Sight in One Eye 67. Major Burns57. Loss of Speech Due to Vocal Cord Paralysis 68. Pheochromocytoma58. Optic Nerve Atrophy with Low Vision 69. Severe Primary Thrombocythaemia59. Surgical Removal of Pituitary Tumor 70. Terminal Illness60. Wegener’s Granulomatosis

Table 2: Minor Critical Illnesses and Severe Child Critical Illnesses CoveredMetLife Health Navigator

Minor Critical Illnesses Covered Severe Child Critical Illnesses Covered8

1. Carcinoma-in-situ (breast, uterus or cervix uteri, ovary and/or fallopian tube, vagina or vulva, colon and rectum, penis, testis, lung, liver, stomach and esophagus, urinary tract, and nasopharynx)

1. Insulin Dependent Diabetes Mellitus

2. Coronary Angioplasty 2. Kawasaki Disease with Heart Complications3. Facial Reconstructive Surgery for Injury Due to Accident 3. Osteogenesis Imperfecta – Type III4. Major Organ Transplantation (on Waiting List) 4. Still's Disease5. Skin Transplantation Caused by Accidental Burning

^ Only an insured person aged above 5 on the confirmed diagnosis of this critical illness is eligible to claim for the relevant benefit.+ Only an insured person aged below 65 on the confirmed diagnosis of this critical illness is eligible to claim for the relevant benefit.++ Only an insured person aged between 65 and 80 on the confirmed diagnosis of this critical illness is eligible to claim for the relevant benefit.

Remarks

1. Benefit payments for the first late stage critical illness will be made under both MetLife Health Navigator and MetLife Extra Love Benefit / MetLife Extra Love Plus Benefit (if any) at the same time, at the amount equivalent to 100% of the respective sum assureds.

2. If MetLife Extra Love Plus Benefit is selected and the insured person suffers from late stage critical illness, the policyowner will be paid the Late Stage Critical Illness Benefit under MetLife Extra Love Plus Benefit, being an amount equal to 100% of the sum assured of MetLife Extra Love Plus Benefit.

If MetLife Extra Love Benefit is selected and the insured person suffers from late stage critical illness, the policyowner will be paid the Late Stage Critical Illness Benefit under MetLife Extra Love Benefit, being an amount equal to 100% of the sum assured of MetLife Extra Love Benefit less the amount of the immediately preceding claim of Early Stage Critical Benefit paid or payable (if any) to the policyowner if: (a) the respective conditions for which Early Stage Critical Illness Benefit is paid or payable (if any) and for which Late Stage Critical Illness Benefit is claimed both fall within the same group of Conditions which is not Group 1; (b) the respective conditions for which Early Stage Critical Illness Benefit is paid or payable (if any) and for which Late Stage Critical Illness Benefit is claimed both fall within Group 1 with diagnosis in the same organ or the cancer for which Late Stage Critical Illness is claimed is caused by the same malignant cells in the preceding claim of Early Stage Critical Illness Benefit. For the avoidance of doubt, if the relevant organ has both a left and a right component (such as, but not limited to, the lungs or breasts), the left side and right side of the organ shall be considered 1 and the same organ.

3. When the Late Stage Critical Illness Benefit becomes payable, MetLife Health Navigator will automatically terminate. MetLife Extra Love Benefit / MetLife Extra Love Plus Benefit will remain inforce and its future premium payments will be waived. Premiums shall continue to be payable until the approval of claim for this benefit. Following such approval, any premiums which are supposed to be waived but paid after the date the confirmed diagnosis of a condition shall be refunded.

4. If MetLife Extra Love Benefit is selected, 50% of the sum assured under MetLife Extra Love Benefit will be payable for the confirmed diagnosis of any covered Early Stage Critical Illnesses suffered by the insured person. If the condition for which subsequent claim(s) for Early Stage Critical Illness Benefit is made falls within groups other than Group 1, it must be in a group different from the groups that Conditions for which the preceding payment(s) for Early Stage Critical Illness Benefit (if any) and Late Stage Critical Illness Benefit (if any) has been made belong to. In respect of claims for conditions under Group 1 under MetLife Extra Love Benefit, if preceding payment(s) of Early Stage Critical Illness Benefit or Late Stage Critical Illness Benefit is paid or payable, a subsequent claim of Early Stage Critical Illness Benefit will only be allowed if (i) the Condition for such claim is diagnosed in an organ that is different from the organ(s) concerned in the preceding claim(s) of Early Stage Critical Illness Benefit or Late Stage Critical Illness Benefit, or (ii) the condition for such claim is caused by malignant cells different from the ones concerned in the preceding claim(s) of Early Stage Critical Illness Benefit or Late Stage Critical Illness Benefit.

If MetLife Extra Love Plus Benefit is selected, 100% of the sum assured under MetLife Extra Love Plus Benefit will be payable for the confirmed diagnosis of any covered Early Stage Critical Illnesses suffered by the insured person. If the condition for which subsequent claim(s) for Early Stage Critical Illness Benefit is made falls within groups other than Group 1, it must be in a group different from the groups that Conditions for which the preceding payment(s) for Early Stage Critical Illness Benefit (if any) and Late Stage Critical Illness Benefit (if any) has been made belong to. In respect of claims for conditions under Group 1 under MetLife Extra Love Plus Benefit, if preceding payment(s) of Early Stage Critical Illness Benefit or Late Stage Critical Illness Benefit is paid or payable, a subsequent claim of Early Stage Critical Illness Benefit or Late Stage Critical Illness Benefit will only be allowed if (i) the Condition for such claim is diagnosed in an organ that is different from the organ(s) concerned in the preceding claim(s) of Early Stage Critical Illness Benefit or Late Stage Critical Illness Benefit, or (ii) the condition for such claim is caused by malignant cells different from the ones concerned in the preceding claim(s) of Early Stage Critical Illness Benefit or Late Stage Critical Illness Benefit, unless the subsequent claim of Late Stage Critical Illness Benefit is for persistent cancer or recurrence of cancer.

5. The aggregate amount of payments of Early Stage Critical Illness Benefit and Late Stage Critical Illness Benefit payable for conditions that fall within Group 1 under MetLife Extra Love Benefit / MetLife Extra Love Plus Benefit shall not exceed 300% of the sum assured of MetLife Extra Love Benefit / MetLife Extra Love Plus Benefit. The aggregate amount of payments of Early Stage Critical Illness Benefit and Late Stage Critical Illness Benefit payable for Conditions that falls within any group other than Group 1 under MetLife Extra Love Benefit / MetLife Extra Love Plus Benefit shall not exceed 100% of the sum assured of MetLife Extra Love Benefit / MetLife Extra Love Plus Benefit, save that (a) the aggregate amount of payments of Early Stage Critical Illness Benefit and Late Stage Critical Illness Benefit payable for conditions that fall within Group 3 can be up to 200% of the sum assured of MetLife Extra Love Benefit / MetLife Extra Love Plus Benefit, provided that once the aggregate amount of payments made reaches 100% of the sum assured of MetLife Extra Love Benefit / MetLife Extra Love Plus Benefit, the remaining claim can only be for the Condition of Heart Attack; and (b) the aggregate amount of payments of Early Stage Critical Illness Benefit and Late Stage Critical Illness Benefit payable for conditions that fall within Group 4 can be up to 200% of the sum assured of MetLife Extra Love Benefit / MetLife Extra Love Plus Benefit provided that once the aggregate amount of payments made reaches 100% of the sum assured of MetLife Extra Love Benefit / MetLife Extra Love Plus Benefit, the remaining claim can only be for the condition of Stroke. The aggregate amount of payments of Early Stage Critical Illness Benefit and Late Stage Critical Illness Benefit under MetLife Extra Love Benefit / MetLife Extra Love Plus Benefit shall not exceed 900% of the sum assured of MetLife Extra Love Benefit / MetLife Extra Love Plus Benefit. MetLife Extra Love Benefit / MetLife Extra Love Plus Benefit will be terminated automatically once the aggregate amount of payments of Early Stage Critical Illness Benefit and Late Stage Critical Illness Benefit has reached 900% of sum assured of MetLife Extra Love Benefit / MetLife Extra Love Plus Benefit.

14

6. If the insured person is confirmed diagnosed with Late Stage Critical Illness, an amount equal to 100% of the current sum assured under MetLife Health Navigator plus non-guaranteed accumulated dividends plus interest (if any) and non-guaranteed terminal dividend (if any) will be paid to the policyowner. The Late Stage Critical Illness Benefit under MetLife Health Navigator will be paid once only. MetLife Health Navigator will be terminated automatically after the payment of Late Stage Critical Illness Benefit is made.

7. Current sum assured, premium, guaranteed cash value, annual dividend and terminal dividend thereafter shall be reduced proportionally accordingly once the Minor Critical Illness Benefit or Severe Child Critical Illness Benefit is paid under MetLife Health Navigator. MetLife Limited shall pay the Minor Critical Illness Benefit or Severe Child Critical Illness Benefit being an amount equal to 25% of the sum assured of MetLife Health Navigator (the aggregate of any and all benefits paid or payable under this basic plan and other policies, supplementary benefit(s) and endorsements issued by MetLife Limited in respect of any condition within the same meaning and scope of the relevant condition of the Minor Critical Illness Benefit shall not exceed US$50,000 per insured person), plus a proportionate non-guaranteed terminal dividend (if any) to the policyowner in respect of such condition. Except for Coronary Angioplasty and Carcinoma-in-situ, the Minor Critical Illness Benefit and Severe Child Critical Illness Benefit will only be paid once for each of conditions falling thereunder. A maximum of 2 claims are available for Coronary Angioplasty and Carcinoma-in-situ respectively. Once Carcinoma-in-situ is diagnosed in one covered organ, the relevant organ is excluded for purposes of a second claim for Carcinoma-in-situ under the Minor Critical Illness Benefit. For the avoidance of doubt, if the relevant organ has both a left and a right component (such as, but not limited to, the lungs or breasts), the left side and right side of the organ shall be considered one and the same organ. This is subject to terms, conditions and exclusions of this benefit. Please refer to the Policy Provisions for details.

8. Severe Child Critical Illness Benefit under MetLife Health Navigator shall cease on the insured person’s 18th birthday.

9. MetLife Limited has engaged VSP Asia Private Limited (“VSP® Vision Care”) to provide the relevant services. MetLife Limited shall not be liable for any matters in respect of any services provided by VSP® Vision Care and its network provider, OPTICAL 88. MetLife Limited reserves the right to change the service provider and its service content at any time or withdraw the services by giving no less than 1 month’s prior written notice to policyowners.

10. The Second Medical Opinion Service is provided for the first claim of the Late Stage Critical Illness Benefit only. It is currently provided by Inter Partner Assistance Hong Kong Ltd. (“IPA”). MetLife shall not be liable for any matters in respect of any services provided therein including but not limited to the quality and/or appropriateness and/or suitability of the medical prescriptions, supplies, procedures, treatments, facilities and services as suggested, recommended or offered by IPA. MetLife Limited reserves the right to change the service provider and its scope of service by giving no less than 1 month’s prior written notice to policyowners.

11. For the guaranteed cash value you are entitled to, please refer to the relevant illustration document of MetLife Health Navigator.

12. The non-guaranteed annual dividends will be declared annually (if any) and the policyowner may choose to withdraw them in cash or leave them in the policy. Dividends (including the annual dividends and terminal dividend), and the annual dividend accumulation rate are not guaranteed and may change from time to time. Once the annual dividend is declared, it will be vested and cannot be removed, while the terminal dividend does not form a permanent addition to the policies and may be reduced or increased at subsequent declarations. Please refer to the Bonus Philosophy for details.

13. The non-guaranteed terminal dividend will be payable when the policy of MetLife Health Navigator has been in-force for 10 years or more upon the payment of Minor Critical Illness Benefit, Severe Child Critical Illness Benefit or Late Stage Critical Illness Benefit of MetLife Health Navigator or death of the insured person, or upon surrender or maturity of the policy.

14. If the insured person commits suicide within the first 13 months from the issue date or the effective date of reinstatement, no Life Benefit shall be payable. For the amount payable in such event, please refer to the Policy Provisions of MetLife Health Navigator for details.

15. If the condition for which a preceding payment of Late Stage Critical Illness Benefit is made is prostate cancer and any subsequent claim(s) of Late Stage Critical Illness Benefit is for a Persistent Cancer of such prostate cancer which is confirmed diagnosed after the insured person’s 70th birthday, the subsequent claim(s) of Late Stage Critical Illness Benefit for the condition of prostate cancer shall be payable only if the insured person has received or has been receiving Active Treatment on the recommendation of a Physician in the relevant field, and the Active Treatment must be Medically Necessary and performed during the period between the date of confirmed diagnosis of the condition of prostate cancer for which the immediately preceding benefit payment is made and the date of confirmed diagnosis of the condition of prostate cancer for which the subsequent claim of Late Stage Critical Illness Benefit is made.

15

Bonus Philosophy for MetLife Health Navigator Critical Illness ProtectorParticipating insurance plans are designed to be held long-term, giving policyholders an opportunity to participate in the financial performance of our life insurance participating business by way of non-guaranteed bonus (i.e. annual dividends, terminal dividends, interest on dividend/coupon accumulation, if applicable for the product) with the prospect of potential attractive long-term return.

To determine our bonus scales, we consider both past experience and long-term assumptions of factors pertaining to the product groups, in which the policies belong to. The factors include, without limitation, the following:

● Investment factors: include the interest earnings and the capital gains and losses generated from the products' backing assets. As we invest in different types of assets in the financial market, we are exposed to various investment risks, such as interest rate risk, credit risk, equity risk, liquidity risk and currency risk.

● Claim factors: include the cost of providing insurance benefits for the product, e.g. death benefits, critical illness benefits (where applicable)

● Persistency factors: include the lapse or surrender of policies, reduction in sum assured / principal amount; and the corresponding impact on investments

● Expense factors: include the direct expenses which are specifically related to a policy (e.g. commission, underwriting, issue and premium collection expense) and indirect expenses which are allocated to the product groups (e.g. general overhead costs)

If the actual experiences and/or latest outlook are more favorable than previously expected, the bonus scales would increase; if the actual experiences and/or latest outlook are less favorable, the bonus scales would decrease. At times, the actual experiences and/or latest outlook are volatile and unpredictable, so the impact on bonus scales may be smoothed out over a few years such that a more stable bonus scales can be achieved.

With the Appointed Actuary's recommendation, the Board of Directors, which includes at least one Independent Non-Executive Director, will review and declare the bonus scales at least annually. The actual declared bonus scales may be different from those illustrated previously. Should there be any changes in the bonus scales, the policyholders will be informed about the details and the potential impact of the changes.

For the historical fulfillment ratio, please visit MetLife's website at http://www.metlife.com.hk/fulfillment-ratios.

Investment Philosophy for MetLife Health Navigator Critical Illness ProtectorWe employ a balanced investment approach for the underlying portfolio of the Participating products, with the objective to deliver long-term value to policyholders and the MetLife Limited.

The current long-term strategy is to allocate assets in fixed income instruments (e.g. government bonds, corporate bonds and commercial mortgage related instruments), and equity-like instruments (e.g. private equities, mutual funds and hedge funds). The objective is to invest 10% to 20% of collected premium to equity-like instruments with main exposure in the United States and Europe. The remaining premium will be invested in fixed income instruments of different regions, including the United States, Asia and Europe, to achieve geographic diversification. The fixed income portfolio invests mainly in investment grade bonds, while high yield bonds may be invested in with limited exposure to enhance the long-term portfolio return. In addition, other market instruments (such as securities lending) may be utilized to generate additional returns.

Currency exposure of the portfolio is mitigated by closely matching either through direct investments in the same currency denomination or the use of currency hedging instruments. On top of hedging, the portfolio may also use derivative instruments for efficient portfolio management purposes.

Investment for insurance products with similar characteristics will be pooled together to achieve higher efficiency. Depending on the market conditions (e.g. availability of assets, liquidity, market outlook) at the time of the purpose of asset, the actual asset mix may differ from the target asset mix temporarily.

To cope with the changing financial environment and in reflection of emerging experiences, MetLife Limited will review the investment strategy regularly. Should there be any changes in the long-term investment strategy, policyholders will be informed about the details and the potential impact of the changes.

16

Key Product Risks for MetLife Health Navigator Critical Illness Protector (the “Plan”)

Key Exclusions

MetLife Limited shall not be liable to pay any Minor Critical Illness Benefit, Severe Child Critical Illness Benefit, and/or Late Stage Critical Illness Benefit in respect of any conditions that result from any of the following events:

● any pre-existing medical condition● any congenital anomaly which has manifested or was diagnosed before the insured person attains age 16, infertility or

sterilization.Please refer to the Policy Provisions of this Plan for the complete list and details of exclusions.

Early Surrender

The savings element of this Plan is designed for long term savings purpose. Early surrender of your policy may result in a significant loss of premium paid.

Premium Adjustment

Premium shall be determined by reference to the issue age, sex and smoking habit of the insured person at policy inception. The premium rate is non-guaranteed. MetLife Limited reserves the right to adjust the rate of premium by giving 1 month's prior written notice to the policyowner if, in pursuant to the underwriting policy of MetLife Limited, MetLife Limited has decided to adjust the premium rate applicable to a category of insured persons and the insured person falls within that category.

Any premium adjustment will reflect the past experience and long-term assumptions of a number of factors in respect of the relevant policies including but not limited to (a) operating expenses; (b) policy persistency; (c) cost of claim; and (d) performance of the investment of the assets.

Non-payment of Premium during Premium Payment Term

You should pay premium(s) on time and according to the selected premium payment schedule during the premium payment term. If you do not pay the premium within 60 days of the premium due date, the premium will be deducted from the nonguaranteed accumulated annual dividends and interest (if any). If the non-guaranteed accumulated annual dividends and interest in the policy are insufficient to fully pay the due premium, such outstanding premium will be covered by a loan taken out on the policy automatically. Interest will be charged at a rate as determined by MetLife Limited from time to time on this automatic premium loan. Interest accrued shall become part of indebtedness. If the due premium is not paid by the applicable loan or if the sum of the applicable loan and the indebtedness under the policy is greater than or equal to the guaranteed cash value, the policy will be terminated and the insured person will lose the coverage.

Credit Risk

The Plan is an insurance plan underwritten by MetLife Limited. The benefits payable under your policy are subject to the credit risk of MetLife Limited. If MetLife Limited is unable to satisfy the financial obligations of the policy of the Plan, the insured person may lose the coverage and you may lose the premium paid.

Foreign Exchange Risk

You should be aware that any transaction which is denominated in a currency other than that of your home currency is subject to foreign exchange risks.

Inflation Risk

The benefits under the policy of the Plan may not be sufficient for the increasing protection needs in the future as the future cost of living may be higher than now due to the effects of inflation.

The above information is intended for reference only. Please refer to the Policy Provisions of MetLife Health Navigator Critical Illness Protector for definitions, detailed terms, conditions and exclusions.

17

Key Product Risks for MetLife Extra Love Benefit and MetLife Extra Love Plus Benefit (the “Optional Riders”)

Key Exclusions

The Optional Riders will not cover conditions that result from any of the following events:

● any pre-existing medical condition● any congenital anomaly which has manifested or was diagnosed before the insured person attains age 16, infertility or

sterilization.Please refer to the Policy Provisions of the Optional Riders for the complete list and details of exclusions.

Premium Adjustment

Premium shall be determined by reference to the issue age, sex and smoking habit of the insured person on the rider date of the Optional Riders. The premium rate is non-guaranteed. MetLife Limited reserves the right to adjust the rate of premium by giving 1 month's prior written notice to the policyowner if, in pursuant to the underwriting policy of MetLife Limited, MetLife Limited has decided to adjust the premium rate applicable to a category of insured persons and the insured person falls within that category.

Any premium adjustment will reflect the past experience and long-term assumptions of a number of factors in respect of the relevant policies including but not limited to (a) operating expenses; (b) policy persistency; (c) cost of claim; and (d) performance of the investment of the assets.

Non-payment of Premium

You should pay premium(s) on time and according to the selected premium payment schedule while the Optional Riders are in force. If you do not pay the premium within 60 days of the premium due date, the Optional Riders will be terminated and the insured person will lose the coverage.

Credit Risk

The Optional Riders are underwritten by MetLife Limited. The benefits payable under your Optional Riders are subject to the credit risk of MetLife Limited. If MetLife Limited is unable to satisfy the financial obligations of the Rider, the insured person may lose the coverage and you may lose the premium paid.

Foreign Exchange Risk

You should be aware that any transaction which is denominated in a currency other than that of your home currency is subject to foreign exchange risks.

Inflation Risk

The benefits under the Optional Riders may not be sufficient for the increasing protection needs in the future as the future cost of living may be higher than now due to the effects of inflation.

The above information is intended for reference only. Please refer to the Policy Provisions of MetLife Extra Love Benefit and MetLife Extra Love Plus Benefit for definitions, detailed terms, conditions and exclusions.

18

Important Notes● MetLife Limited reserves the right to accept or reject any application for MetLife Health Navigator, MetLife Extra Love

Benefit and MetLife Extra Love Plus Benefit.● MetLife Limited reserves the right to make payment of the surrender value within a period not exceeding 6 months from

the effective date of surrender.● MetLife Health Navigator is an insurance plan with a savings element. Part of the premium pays for the insurance and

related costs. The savings component of MetLife Health Navigator is subject to risk and possible loss. MetLife Extra Love Benefit and MetLife Extra Love Plus Benefit are the optional riders with no savings element. All premiums pay for the insurance and related costs.

● If you are not happy with your policy, you have the right to cancel it within the Cooling-off Period and obtain a refund of any premiums paid provided that you have not made any claims under the policy. A written notice signed by you together with the policy must be received by the Customer Service Centre of MetLife Limited at Level 57, Hopewell Centre, 183 Queen's Road East, Wan Chai, Hong Kong within the Cooling-off Period (that is, 21 days after the delivery of the policy or the issue of a Notice informing you/your representative about the availability of the policy and the expiry date of the Cooling-off Period, whichever is earlier). After the expiration of the Cooling-off Period, if you cancel the policy before the end of the policy term as set out in the policy document, the projected total cash value payable (if any) may be less than the total premiums you have paid.

● MetLife Limited is the insurance underwriter of MetLife Health Navigator, MetLife Extra Love Benefit and MetLife Extra Love Plus Benefit, and is solely responsible for all content, approvals, coverage and benefit payment. MetLife Limited is a wholly-owned subsidiary of MetLife, Inc. in Hong Kong and operates under the “MetLife” brand. MetLife Limited is a company incorporated and registered as a private company limited by shares under the applicable laws in Hong Kong.

Foreign Tax Reporting and Withholding Obligations● MetLife Limited may from time to time be subject to various tax reporting and withholding obligations imposed by the

foreign laws, intergovernmental agreements, and agreements with foreign governments or tax authorities, including the Foreign Account Tax Compliance Act of 2010 and the United States Treasury Regulations promulgated thereunder.

● For the purpose of compliance with the above, MetLife Limited may be required to disclose any and all of your policy information to any governments or tax authorities, including your citizenships and tax residency. MetLife Limited would therefore require you (and any other person who is entitled to access the policy value, change a beneficiary, or claim or receive a benefit payment) to provide MetLife Limited with all necessary information, update MetLife Limited promptly of any changes thereto, and complete and sign such documents as MetLife Limited may require. If you or any such other person fails to do so, MetLife Limited will have the right to deduct or withhold such amount(s) from any payment under the policy, or provide your policy information to such government or tax authorities as may be required.

● If you have any doubt on the impact on you or your tax position, you should seek independent professional advice.

Automatic Exchange of Financial Account Information for Tax Purposes between JurisdictionsHong Kong has now legislation in place for the implementation of automatic exchange of financial account information for tax purposes. Under the rules, financial institutions in Hong Kong including MetLife Limited are required to implement due diligence procedures to identify account holders (i.e. policyowners and certain beneficiaries in case where the financial institution is an insurance company) and in the case where the account holder is a passive non-financial entity, its "controlling persons", who are foreign tax residents, and report certain information about them (including but not limited to their name, date of birth, jurisdiction(s) of tax residence and tax identification numbers in that jurisdiction(s), account balance/value and investment income) to the Inland Revenue Department (“IRD”) if required. When agreements are in place between Hong Kong and the relevant countries or jurisdictions, the IRD will transfer this information with the country of tax residence of such account holders and controlling persons. This information exchange will be conducted on a regular, annual basis. To fulfill such legal obligations, MetLife Limited will ask you to submit a self-certification form that would include your country of tax residence, tax identification number in that country, date and place of birth, and in the case where the policyowner is an entity, the classification of the entity that holds the policy, and information regarding "controlling persons" of a passive non-financial entity. You may also be asked to provide additional information and documents. Where required under the legislation, any and all such information may then be reported to the IRD which may transfer this information to foreign tax authorities and governments. Please see the IRD website for more details.

MetLife Limited is not permitted to and does not provide you with any legal or tax advice. We encourage all existing and prospective policyowners to obtain independent legal and tax advice.

HK-

MK

T-A

G/I

A/C

DC

-CC

7PB0

2-03

18

MetLife Limited Customer Service Centre: Level 57, Hopewell Centre, 183 Queen’s Road East, Wan Chai, Hong Kong

Tel: (852) 2199 1000 Fax: (852) 8101 3977 www.metlife.com.hk(This brochure is for distribution in Hong Kong only.)