adapting in tough times: the growing resilience of uk smes

TRANSCRIPT

Adapting in tough times:The growing resilience of

UK SMEs

Written by

2 Adapting in tough times: The growing resilience of UK SMEs

About this report

In November 2012, the Economist Intelligence Unit, on behalf of Zurich, surveyed 549 small business owners

and directors in the UK to explore what SMEs think about the current economic landscape and how they are

adapting in order to survive and succeed.

In addition, in-depth interviews were conducted with two SME experts. Our thanks are due to the following

for their time and insight:

Mike Cherry, the National Policy Chairman at the Federation of Small Businesses.

Professor Stephen Roper, Director of the Enterprise Research Centre at the University of Warwick.

The report was written by Melissa Carson and edited by Monica Woodley of the Economist Intelligence Unit.

Contents

Foreword 3

Executive summary 4

The impact of stagnation on UK SME survival 6

Winners and losers in the UK’s SME economy 11

Newfound resilience as high-performing SMEs adapt 14

Shifts in SME risk approach and appetite 17

The long-term view: A vicious circle and return to growth 19

3Adapting in tough times: The growing resilience of UK SMEs

The past five years since the financial crisis have presented perhaps the most challenging economic times since the Great Depression and Second World War. The recent World Economic Forum (WEF) Global Risk report1 highlighted economic fragility and resilience as the principal challenge for individuals, businesses and government today. It is no surprise then that the UK small business – whether a sole trader, start-up manufacturer, local pub or hair and beauty salon – has been under constant financial pressure.

This report, Adapting in Tough Times: the growing resilience of UK SMEs, developed in association with the Economist Intelligence Unit (EIU), looks at the general state of fragility within the UK SME sector after five years of challenging economic times; how UK small-medium size enterprises are responding; and what risks are emerging as a result, both for the small business and the larger SME economy.

The good news is that our research demonstrates there are green shoots of recovery already underway. Indeed, many SMEs in the UK are more fit for purpose and in better shape to manage risk and volatility in the future. The long-term nature of this economic crisis has forced SMEs to adapt to the environment. And perhaps the most crucial adaptation is a newfound appreciation for risk; this is a fundamental change in SME business mindset and management behaviour.

UK small businesses are investing and diversifying, building a platform for competitive advantage and resilience in the long-term. Many are moving to a more variable cost business model, providing financial flexibility during times of volatility, tight margins and rising operating costs.

However, our research with EIU also highlights the macro-economic risk of a ‘two-tier SME economy’ emerging in the UK. Whilst many SMEs are adapting, the ongoing financial pressure is eroding the competitive health and vitality of a significant number of small businesses – potentially introducing a turnover gap between ‘winners’ and ‘losers’ in the long-term.

‘Recovery’ and risk, both at the firm and SME economy level, is foremost on the minds of sole traders and small businesses, independent advisers, economists and institutions alike. Indeed, given the broader market context, risk for SMEs is only becoming more complex.

We hope this report will provide further insight into the complex risk dynamics now underway within the UK economy – and help the insurance industry and other stakeholders support a return to stability and growth for SMEs.

Richard ColemanDirector, SMEUK General InsuranceZurich Insurance plc

Foreword

1Global Risks 2013, World Economic Forum (WEF)

4 Adapting in tough times: The growing resilience of UK SMEs

Executive summary

The past five years of economic stagnation and volatility have forced UK small and medium-sized enterprises (SMEs) to undertake the most significant adaptation and shift in management behaviour in decades.

SMEs have become stronger through diversification and deleveraging, in addition to more operationally resilient and better prepared to manage economic challenges and the new risk landscape. But they are also more cautious and risk-averse across the board compared with five years ago, raising concerns that SMEs will not be the engine of economic growth that drags the UK back from the brink of a triple-dip recession.

The economy may never return to the level of stability experienced in the decade prior to the 2008-09 global financial crisis. Although SMEs are better prepared to manage this new economic reality, they are still struggling as operating-cost fundamentals are squeezing business margins. In particular, low-performing businesses appear to be undercutting themselves by taking a short-term approach, increasing the risk to business survival in the long term. There are indications that their Achilles heel might be whether they fully appreciate the long-term market dynamics at hand, and ongoing economic stagnation remains the greatest threat.

In general, SMEs seem cautiously optimistic about the future. In a survey of over 500 UK SMEs conducted by the Economist Intelligence Unit, three-quarters of respondents feel that their company’s position is financially secure – and many for good reason. SMEs have undertaken the biggest management-behaviour shift in a generation – adopting a more strategic approach to risk and taking a longer-term view on financial planning, debt, business continuity preparation and building reserves. The more secure high-performers have been implementing resilience measures such as adapting financial and operational business practices – a lesson from which their low-performing peers must learn. Indeed, a growing and divergent turnover gap between the ‘winners and losers’ may indicate a second economic challenge for low-performers beyond that of stagnation – increasing market competition leading to natural selection within the SME economy.

Experts agree with the picture painted by the survey that SMEs are also much more cautious across the board than was typical of small businesses five years ago, whether consciously or not. Their risk appetite, for example, is no greater today than it was two years ago, as many have been waiting for an economic recovery before returning to ‘business as usual’ – considering re-investment in the business, for example. However, given the continued economic stagnation, SMEs have put risk-taking and opportunism on hold.

The dual issues of a ‘winners and losers’ dichotomy and a conservative, risk-averse business mindset present significant potential challenges to the short-term prospects for SMEs and the broader UK economy.

5Adapting in tough times: The growing resilience of UK SMEs

How are UK SMEs adapting to tough times?

Business threats

High-performing SMEs

Low-performing SMEs

59% of SMEs feel confi dent in the outlook for their business and they have performed better than their less confi dent peers on a range of measures over the past two years.

They have made strategic, long-term adaptations to their businesses such as:

53% Diversifi cation of products and services.

48% Improved productivity.

52% of SMEs now spend more time thinking about their business strategy. But SMEs have also adopted a conservative mindset. 25% rate themselves as risk averse. This raises tough questions about the short-term prospects and long-term strength UK’s SME economy – and thus the UK economy as a whole.

In contrast, low performers have made tactical, short-term changes such as:

What was the greatest threat to your business two years ago?

TOP 5 What is the greatest threat to your business today?

2 YEARS AGO TODAY

Weak demand due to economic stagnation 44% 52%

Operational cost challenge 25% 37%

Inadequate cash reserves 31% 27%

Poor access to fi nance 16% 21%

Failure to manage cash fl ow 22% 17%

37%

Reducing prices

for customers.

51% Working longer hours.

adaptations

53%

48%

TOP

5

Source: Economist Intelligence Unit

6 Adapting in tough times: The growing resilience of UK SMEs

The impact of stagnation on UK SME survival

Table 1: Threats What was the greatest threat to your business...?

2 years ago Today Change

Weak demand due to economic stagnation (a lack of economic growth)

44% 52% Increased

Operational cost challenge (eg sudden rise in energy costs; high fixed costs)

25% 37% Increased

Inadequate cash reserves 31% 27% Decreased

Poor access to finance 16% 21% Increased

Failure to manage cash flow (working capital)

22% 17% Decreased

Supply chain or logistics failure (eg key supplier failure; loss of contract or poor inventory management)

15% 14% Static

Non-compliant business practices (eg data loss; sanctions; tax)

12% 12% Static

Over indebtedness 19% 11% Decreased

Uninsured major loss event (eg fire, flood)

9% 8% Static

Other (please specify) 5% 7% n/a

UK SMEs operate in a high-risk environment. Threats from all sides – the market, operating environment and finances – are squeezing them while the risk environment appears relentlessly unstable. In the short term, this raises questions about the viability of the SME sector to instigate economic growth.

The greatest threats to SMEs are economic stagnation, operating-cost volatility (such as energy costs) and inadequate cash reserves. These, among other related and interconnected pressures, mean that SMEs are stretched to their limits. In this section we look at each of these threats in detail and the implications for SMEs.

Long-term economic stagnation

Economic stagnation is currently the greatest threat to SMEs, according to over one-half (52%) of survey respondents, representing an increase from 44% two years ago. “While aspirations are high,” notes Mike Cherry, the National Policy Chairman at the Federation of Small Businesses (FSB), “there is a lack of confidence in the general economy that is holding [SMEs] back.”

With prolonged economic stagnation, adds Professor Stephen Roper, Director of the Enterprise Research Centre at the University of Warwick: “There is an attrition effect. SMEs inevitably get worn down, not just their resources but also morale. This psychological effect is very important for some. Even if you feel your business is resilient, it is at this point you ask yourself if you have the drive to invest in the future.”

Mike Cherry is the National Policy Chairman for the Federation of Small

Businesses and leads the policy team in Westminster, Whitehall and Brussels.

Stephen Roper is Director of the Enterprise Research Centre, an

independent research centre which conducts policy relevant research on SME growth and development, and Professor

of Enterprise at Warwick Business School.

Source: Economist Intelligence Unit

7Adapting in tough times: The growing resilience of UK SMEs

The impact of stagnation on UK SME survival

Table 2: Top three threats today by Industry What was the greatest threat to your business...?

Weak demand due to economic

stagnation (a lack of

economic growth)

Operational cost challenge (eg sudden rise in energy costs; high fixed costs)

Inadequate cash reserves

Building and construction services 43% 50% 36%

IT services 47% 26% 21%

Manufacturing 38% 42% 36%

Media, marketing or entertainment 54% 33% 24%

Other consumer or business services 53% 35% 31%

Professional or financial services 63% 31% 19%

Property management and rental 28% 32% 32%

Retailing and distribution 50% 32% 37%

There are some industries that are more resistant to long-term economic stagnation. Professional and financial services rate this as their top threat, as their business-to-business transactions mean that they depend on the ability of other businesses to pay. By contrast, property management and rental agencies are less exposed as their business is a necessary requirement for both consumers and other businesses.

Stagnation is also inducing a fundamental shift in the SME business-risk mindset. Mr Cherry says: “While SMEs are more able to take a more realistic approach than they were previously... they are very aware of the economic crisis and risk environment... and now (as a result) they are more cautious.” Greater caution among SMEs will be discussed further in this report.

Rising business operating costs

Operating-cost challenges have increased significantly in the past two years – and have been the most difficult financial metric for SMEs to manage. Over one-third (37%) of those surveyed see these challenges as one of the greatest threats to their business, up from 25% two years ago.

Better-performing SMEs – as we will see later in this report – have not managed this challenge any better than their lower-performing counterparts, in a reflection of operating-cost dynamics, such as rising energy costs, rents and logistics.

The industries most concerned about operating costs are building and construction (50%) and manufacturing (42%), which is not surprising given (for example) the energy requirements in these industries. Information Technology (IT) services is the industry least concerned (26%) among those surveyed.

Source: Economist Intelligence Unit

8 Adapting in tough times: The growing resilience of UK SMEs

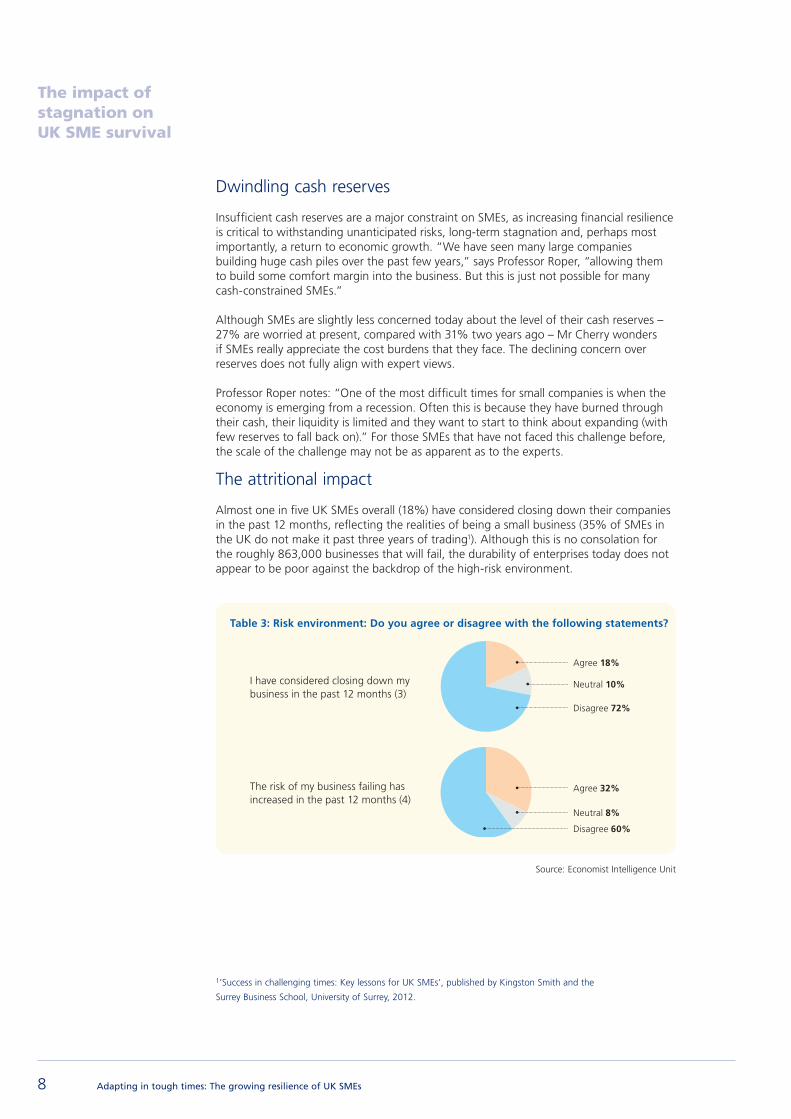

Dwindling cash reserves

Insufficient cash reserves are a major constraint on SMEs, as increasing financial resilience is critical to withstanding unanticipated risks, long-term stagnation and, perhaps most importantly, a return to economic growth. “We have seen many large companies building huge cash piles over the past few years,” says Professor Roper, “allowing them to build some comfort margin into the business. But this is just not possible for many cash-constrained SMEs.”

Although SMEs are slightly less concerned today about the level of their cash reserves – 27% are worried at present, compared with 31% two years ago – Mr Cherry wonders if SMEs really appreciate the cost burdens that they face. The declining concern over reserves does not fully align with expert views.

Professor Roper notes: “One of the most difficult times for small companies is when the economy is emerging from a recession. Often this is because they have burned through their cash, their liquidity is limited and they want to start to think about expanding (with few reserves to fall back on).” For those SMEs that have not faced this challenge before, the scale of the challenge may not be as apparent as to the experts.

The attritional impact

Almost one in five UK SMEs overall (18%) have considered closing down their companies in the past 12 months, reflecting the realities of being a small business (35% of SMEs in the UK do not make it past three years of trading1). Although this is no consolation for the roughly 863,000 businesses that will fail, the durability of enterprises today does not appear to be poor against the backdrop of the high-risk environment.

1’Success in challenging times: Key lessons for UK SMEs’, published by Kingston Smith and the

Surrey Business School, University of Surrey, 2012.

The impact of stagnation on UK SME survival

I have considered closing down my business in the past 12 months (3)

The risk of my business failing has increased in the past 12 months (4)

Table 3: Risk environment: Do you agree or disagree with the following statements?

Agree 18%

Agree 32%

Neutral 10%

Neutral 8%

Disagree 72%

Disagree 60%

Source: Economist Intelligence Unit

9Adapting in tough times: The growing resilience of UK SMEs

The risk environment, however, continues to worsen for a significant proportion of SMEs. On average, one-third (32%) of those surveyed feel that the risk of their businesses failing has increased in the past 12 months, and in many industries it is significantly worse.

Automotive trades and transport, as well as hotels and restaurants, are facing the toughest conditions, with 57% and 46% respectively reporting an increased risk to business failing in the past 12 months. For example, over the past year or so the negative impact on road freight has been exacerbated by significant weather disruptions during the winter of 2011, while the customer base of hotels and restaurants is being affected directly by economic stagnation.

On the other end of the scale, property management and rental, as well as professional and financial services, have experienced a more stable risk environment, with only 24% and 27% respectively reporting an increased risk to business failing over the same period.

Table 4: Risk environment by industry The risk of my business failing has increased in the past 12 months?

Industry Yes NoDon’t know

% Respondents

Note*

Motor trades and transportation 57% 44% 0% 4% indicative

Hotels, restaurants, cafes and pubs 46% 50% 5% 4% indicative

Media, marketing or entertainment 37% 59% 4% 8% representative

Retailing and distribution 37% 53% 10% 11% representative

Building and construction services 36% 57% 7% 5% representative

IT services 33% 54% 14% 8% representative

Manufacturing 30% 62% 8% 9% representative

Child or pet care 30% 60% 10% 2% indicative

Other consumer or business services 29% 59% 12% 9% representative

Not-for-profit organisation 27% 64% 9% 2% indicative

Professional or financial services 27% 65% 8% 29% representative

Property management and rental 24% 72% 4% 5% representative

Healthcare or related services 22% 61% 17% 3% indicative

*Indicates whether the sample size is representative or indicative of a given industry sector based on

sample size in our survey.

The impact of stagnation on UK SME survival

Source: Economist Intelligence Unit

10 Adapting in tough times: The growing resilience of UK SMEs

Economic risks are squeezing UK SMEs over time

The squeeze on UK SMEs can be seen concretely in their financial performance. Over 85% of SMEs have seen shrinking or flat profit margins, cash flows, reserves and investments in the past two years. Furthermore, margins and operating costs have been most difficult to manage owing to external factors such as higher energy costs, anaemic growth in the UK economy, the eurozone crisis, consumers’ focus on price and the growing shift towards online channels, among others. Business operating costs is the one area where all UK SMEs have struggled.

Overall, the survey presents a bleak picture of challenging times experienced in the past two years, and although some metrics, such as debt, have been better managed (see next chapter), SMEs are stretched to their limits in this prolonged environment of elevated risk.

Table 5: Financial performance What has happened to the following financial metrics at your firm over the past two years?

Positive movement

StableNegative

movement

Difference: positive – negative

movement

Business operating costs (7) Positive (Shrinking)/ Negative (Growing)

10% 52% 38% -28%

Profit margin (3) Positive (Growing)/ Negative (Shrinking)

15% 47% 39% -24%

Reserves/savings (6) Positive (Growing)/ Negative (Shrinking)

10% 58% 32% -22%

Cash flow/working capital (1) Positive (Growing)/ Negative (Shrinking)

13% 53% 34% -21%

Investment (2) Positive (Growing)/ Negative (Shrinking)

11% 59% 30% -19%

Turnover (4) Positive (Growing)/ Negative (Shrinking)

27% 42% 31% -4%

Debt (5) Positive (Shrinking)/ Negative (Growing)

28% 62% 10% 18%

The impact of stagnation on UK SME survival

Source: Economist Intelligence Unit

11Adapting in tough times: The growing resilience of UK SMEs

Winners and losers in the UK’s SME economy

Confi dence and performance have a natural correlation; indeed, confi dence is usually born out of performance. The correlation is clearly present among our survey respondents, allowing us to explore the differences and similarities between high and low-performing businesses, and explain the stark performance distinctions between them.

SMEs with high levels of confi dence – the 59% of respondents who are confi dent about their business outlook both 12 months from now and one to two years from now – have demonstrated a dramatically higher level of performance than the other respondents (the 41% that are less confi dent) over the past two years, as measured across seven key fi nancial indicators.

Higher and lower-performers come in all sizes. Although there is a slightly greater proportion of larger SMEs among the high-performers, size is by no means a direct predictor of performance.

Turnover

The most confi dent of those surveyed have achieved admirable growth in turnover in the past two years. Two in fi ve (39%) report growth and only 13% report shrinking turnover, but almost one-half (47%) of the less confi dent report shrinking turnover and just 9% achieved some growth – the polar-opposite trend. The overall performance of these groups could not be more different, and that is unlikely to change. While economic times may help all businesses prosper – a rising tide lifts all boats – in diffi cult times, it is sink or swim.

Table 6: High/low performersChanges in fi nancial metrics over the past two years

Change in fi nancial metrics (positive shift/negative shift) past two years

High-performers/confi dent SMEs*Low-performers/less

confi dent SMEs*

(S=Shrinking, G=Growing)

*Confi dent = confi dent about business outlook 12 months from now and one to two years from now. Less confi dent = all other respondents

Debt (S/G)

Turnover (S/G)

Investment (S/G)

Cash fl ow/working capital (S/G)

Reserves/savings (S/G)

Profi t margin (S/G)

Business operating costs (S/G)

100%80%60%40%20%0% 100%80%60%40%20%0%

Negative shift Positive shift Negative shift Positive shift

Source: Economist Intelligence Unit

12 Adapting in tough times: The growing resilience of UK SMEs

Reserves, working capital (cash fl ow) and investment

The most confi dent of respondents have held stable the core fi nancial metrics: reserves (savings), working capital and investment. A small proportion (less than 20%) report growth – a positive shift – while the same number report a negative shift. Thus, over 60% are holding these core metrics stable, meaning that, overall, the confi dent are performing well despite the economic conditions of the past two years.

However, the majority of the less confi dent (over 50%) have seen a dramatic negative shift across all of the same core metrics and virtually none (4%) have managed to shift these in a positive direction in the past two years. The less confi dent are fundamentally struggling to manage the basics.

Debt

The poor economic environment has meant that debt management has been a requirement of survival for SMEs. In addition, the most confi dent have responded by managing to reduce debt (37%) or keep it stable (58%), with only a few (6%) seeing their debt levels grow.

Although the less confi dent have managed to keep debt relatively stable – 16% report growth in debt, 16% report shrinking debt and the remaining 68% report stable debt – their ability to deleverage is notably much less than their counterparts.

The deleveraging by high-performing SMEs provides two distinct competitive advantages in the long term: fi rst, greater fi nancial fl exibility to manage future revenue volatility, and second, better fi nancial health which can be used to releverage and fi nance expansion – when confi dence and economic growth return. Low-performing SMEs have neither advantage. Indeed, many may be caught in a ‘debt trap’, unable to deleverage and free up cash to survive long-term stagnation, while also unable to access fi nance, invest and grow out of the crisis.

Total

50-249 employees

10-49 employees

1-9 employees

Sole trader

100%80%60%40%20%0%

High-Performers

Low-Performers

Winners and losers in the UK’s SME economy

Source: Economist Intelligence Unit

13Adapting in tough times: The growing resilience of UK SMEs

Zurich Viewpoint

The future prospect of a two-tier SME economyIn every market and economic cycle, there exist winners and losers; a natural process of organic firm failure, mergers and business acquisition. However today’s extended period of economic stagnation may also leave the UK SME economy with an unanticipated, post-recovery challenge as its legacy: two-tiers of SME businesses in vastly different states of financial and business health.

As cited, high-performers and low-performers could not be more different in terms of turnover growth, de-leveraging of debt, ‘cash flow’ and investment metrics. Indeed, there now appears to be a growing and divergent turnover gap between these ‘winners and losers’. High-performers are also adapting their operational business model strategy – increasing potential competitive advantages (for instance, in production, cost base, distribution or marketing) in the long-term. Conversely, the tactical measures of low-performers (such as freezing investment plans) which help to manage business survival today, have the unfortunate feedback loop of undercutting long-term competitive form.

High-performers therefore stand to find themselves in a virtuous future, where investment and business model adaptation places them in a position to acquire share and customers from lower-performers. For the lower-performers, the long-term risk is that even when economic growth returns, many small businesses may find themselves equipped with an outdated business model; lack of reserves to invest and tight access to capital; a fast moving online world and high-street in transformation – and, most importantly, competing against more financial robust (high-performing) and ‘fit-for-purpose’ competitors.

This is the potential long-term dynamic – a new post-recovery economy where low-performing SMEs find themselves at a widening disadvantage and in a market of even higher competitive intensity.

Winners and losers in the UK’s SME economy

14 Adapting in tough times: The growing resilience of UK SMEs

Having survived the past five years of stagnation and volatile pressures, SMEs are fundamentally better prepared to manage the risks of economic instability now than perhaps ever before. They have adopted a range of resilience measures, but most notably they have become more strategic, taking a longer-term view – a shift from how SMEs have traditionally survived and thrived. They are also diversifying and transforming their business operations towards a more flexible (variable) cost model.

Resilience strategies

The dominant resilience strategy has been diversification of products and services, undertaken by almost two-thirds (63%) of SMEs (excluding sole traders). This is the top trend even among sole traders. Similar numbers of SMEs with ten employees or more (62%) have also been diversifying their customer base and market presence.

Although diversification widens revenue opportunities and may reduce turnover risk, it can stretch SMEs operationally or strategically – as well as introduce new business risks and exposures. In particular, businesses must recognise and address the fresh potential liabilities associated with new products, services or markets.

Medium-sized enterprises (50-249 employees) have overwhelmingly adopted a more flexible operating-cost base (68%). For these SMEs, a more variable operating-cost base will allow them to manage future economic volatility in a more flexible and robust manner. (Considering that the very design of sole traders and micro-enterprises is flexibility, it is unsurprising to find that they have been less inclined overall to adopt even more flexibility in their operating-cost base.)

The scale of transformation indicates that SMEs have fundamentally shifted to a more strategic, diverse and operationally flexible business model for the long term – a characteristic that was previously associated more with larger enterprises.

Nonetheless, Professor Roper warns: “It is true that SMEs have been trying to build more resilient responses, but whether that results in SMEs being more resilient is another matter.” The different tactics of high versus low-performers sheds more light on how SMEs can best address resilience.

Newfound resilience as high-performing SMEs adapt

Table 8: Resilience strategies Do you agree/disagree with the following statements?

My company has a more diversified approach to products and service offering.

Sole trader 1-9 10-49 50-249 Total

Agree 40.0% 62.5% 62.6% 63.7% 55.6%

Disagree 24.6% 22.0% 24.3% 30.8% 24.8%

Don’t know / N/A 35.4% 15.5% 13.0% 5.5% 19.7%

Ratio (Agree/Disagree) 1.6 2.8 2.6 2.1 2.2

My company has a more diversified customer base and / or market presence.

Sole trader 1-9 10-49 50-249 Total

Agree 33.7% 49.4% 62.6% 61.5% 49.2%

Disagree 40.6% 35.1% 27.0% 33.0% 34.8%

Don’t know / N/A 25.7% 15.5% 10.4% 5.5% 16.0%

Ratio (Agree/Disagree) 0.8 1.4 2.3 1.9 1.4

My company now has a more flexible operational cost base (eg the ability to reduce costs quickly).

Sole trader 1-9 10-49 50-249 Total

Agree 28.6% 54.2% 52.2% 68.1% 47.9%

Disagree 40.0% 32.7% 42.6% 26.4% 36.1%

Don’t know / N/A 31.4% 13.1% 5.2% 5.5% 16.0%

Ratio (Agree/Disagree) 0.7 1.7 1.2 2.6 1.3

Source: Economist Intelligence Unit

15Adapting in tough times: The growing resilience of UK SMEs

Operationalising resilience: Business adaptation by high-performers

There are clear distinctions between high and low-performers in their approaches to building resilience in the face of the prolonged and volatile economic conditions. Diversification is the number one tactic for high-performers and number two for low-performers, but productivity tactics are where the greatest differences exist between these groups.

Table 9: Operationalising resilience What steps have you taken to make your business more resilient in the face of recession/weak growth?

TotalHigh

performersLower

performers

Percentage point

difference (high-lower performers)

Type of tactic/strategy

Diversification into new product or service areas

48% 52% 42% 10% Diversification

Working longer hours 47% 43% 53% -10% Productivity

Improved productivity (eg finding ways to produce more output with the same inputs)

39% 48% 26% 22% Productivity

Negotiating lower prices with suppliers 32% 34% 29% 5% Operational

Reducing prices for customers30% 24% 39% -15%

Customer base

Cut or freeze wages 22% 17% 29% -12% Operational

Delayed investment 20% 17% 25% -8% Operational

Increased use of part time and/or contract workers

19% 23% 14% 9% Operational

Reducing credit to customers 16% 13% 19% -6% Operational

Cut jobs 11% 6% 17% -11% Operational

Other, please specify 4% 4% 4% 0% Other

Invoice factoring (ie selling invoices to a third party at a discount)

4% 3% 5% -2% Operational

High-performing SMEs have opted for more strategic adaptation, such as improving productivity (their second most preferred tactic), which will have more of a long-term impact. By contrast, this was only the sixth most popular tactic for building resilience among low-performers. Instead, the majority of low-performers opt for a more short-term and reactive tactical approach, electing to make changes such as working longer hours – an important action for both groups, but the top resilience tactic for low-performing SMEs overall.

Newfound resilience as high-performing SMEs adapt

Source: Economist Intelligence Unit

16 Adapting in tough times: The growing resilience of UK SMEs

Chart 10: Operational resilience characteristics of high-performers and low-performers

High-performers clearly hold a more strategic underlying perspective, enabling them to execute tactics that will also strengthen their operational and fi nancial strength for the future. The trend of strategic adaptation by high-performers versus more tactical change by low-performers is consistent. High-performers tend to negotiate lower prices with suppliers and increase the use of part-time or contract workers, whereas low-performers are inclined to take short-term measures – such as cutting or freezing wages, delaying investments and reducing credit to customers – much more so than high-performers.

Perhaps most signifi cantly, although only 11% of all SMEs have shed jobs, high-performers are much less inclined to do so. Broadly, high-performers have elected to continue to invest in the business, potentially securing a long-term future and building competitive advantage – to the detriment of low-performers.

Low-performers look to be undercutting their own long-term performance and sustainability by failing to invest and prioritising temporary gains. They are still operating on the short-term, pre-crisis horizons that once characterised the majority of SMEs.

High-performers Low-performers

Newfound resilience as high-performing SMEs adapt

Diversifi cation into new Diversifi cation into new Diversifi cation into new product/serviceproduct/serviceproduct/service

Negotiating lower prices Negotiating lower prices Negotiating lower prices with supplierswith supplierswith suppliers

Increased use of part-time/Increased use of part-time/Increased use of part-time/contract workerscontract workerscontract workers

Productivity improvementsProductivity improvementsProductivity improvements

Working longer hoursWorking longer hoursWorking longer hours

Working longer hoursWorking longer hoursWorking longer hours

Diversifi cation into new Diversifi cation into new Diversifi cation into new product/serviceproduct/serviceproduct/service

Cut/freeze wagesCut/freeze wagesCut/freeze wages

Delayed investmentDelayed investmentDelayed investment

Reducing prices for customersReducing prices for customersReducing prices for customers

Source: Economist Intelligence Unit

17Adapting in tough times: The growing resilience of UK SMEs

Shifts in SME risk approach and appetite

SMEs have undertaken the biggest risk-management behaviour shift in a generation. They have become more strategic and are taking a longer-term view in financial planning, which bodes well for the future, but they are also more cautious and conservative –painting a mixed picture for the SME economy in the short term.

In this section we look at how SMEs are managing and thinking about risks in their business.

Strategic approach to risk

Historically, a lack of long-term financial planning and strategic planning has been a key reason why SMEs fail. However, in response to the global financial crisis, a significant majority – particularly SMEs with employees – have adopted a greater appreciation of environmental (economic) threats.

Most importantly, they are focusing on increasing investment of time and resources in the management approach to business risk, continuity planning and longer-term financial planning, including building/maintaining reserves, and managing debt – as we saw among both high and low-performers earlier in this report.2

This shift, towards a more strategic view, is a hugely positive step for the long-term resilience and sustainability of SMEs and the UK’s SME economy, and a theme we have seen emerge throughout this report. For most SMEs, it is likely to have started as a tendency towards care and caution. Professor Roper notes: “Naturally, under financial pressure, SMEs are keen to reduce the external financial risks, and so have adopted a conservatism to minimise risks. For example, they are a little less ready to make investments because of the economic environment.” However, under prolonged stress, their behaviour has perhaps changed more permanently. SMEs have to look harder at what they are doing and be more explicit, discerning and strategic about how they approach risk.

Although SMEs highlight their greater attention to reserves, they also feel that insufficient reserves are one of the greatest threats to their business. In this light, the fact that SMEs are generally not looking to their insurance coverage as a form of reserving through risk transfer, and, more strategically, managing cash risks is perhaps a key oversight (or short-termism) that seems incongruous with the tight breathing space that SMEs are operating in, as well as with the possibility of ongoing economic stagnation.

2Sole traders have not had the capacity

to change their approach to risk as

significantly. In fact, over one-half

(57%) say that they have not changed

their risk-management approach at all.

The primary focus for sole traders is

often survival. Even among SMEs

with at least one employee, 22% still

say that they have not changed their

risk-management approach. The risk

environment is continues to be

challenging for many SMEs.

Table 11: Risk management How, if at all, has the financial crisis and recession changed your approach to risk management?

Sole trader

1-9 employees

10-49 employees

50-249 employees

Total

We spend more time thinking about our business strategy (eg managing strategic risks and opportunities)

33% 57% 70% 60% 53%

We pay more attention to maintaining strong reserves/savings

31% 50% 50% 45% 43%

We engage in more long-term financial planning 18% 36% 49% 48% 35%

We consider our business continuity plans more frequently (eg by planning for the failure of key suppliers)

20% 39% 40% 36% 33%

We have increased our insurance coverage 3% 8% 7% 15% 7%

We have not changed our approach to risk management 56% 30% 21% 14% 34%

Source: Economist Intelligence Unit

18 Adapting in tough times: The growing resilience of UK SMEs

Risk appetite, confidence and conservatism

SMEs do not describe their risk appetite today as significantly different compared with two years ago. They have been waiting for more stable and predictable economic times, and have not yet let down their guard when it comes to taking risks.

Nevertheless, SMEs feel that they will be significantly more opportunistic two years from now. Despite “an anticipation on the part of [UK] SMEs that the economic circumstances will remain tough in the years to come,” notes Professor Roper, increasing confidence and opportunism reflect a wider view that we are “through the worst of it”.

Growing confidence in the near term (one to two years from now) also reflects two underlying factors brought on in response to the past five years of challenging economic conditions: better preparedness for volatile economic challenges (through diversification and operating-cost flexibility, stronger strategic and financial management), and a more cautious approach to risk than ever before. Even among the more confident SMEs, Professor Roper has seen “an unconscious conservatism in [response to] economic volatility.”

Table 12: Risk Appetite How would you describe your company’s ‘risk appetite’ compared to other SMEs in your industry?

Two years ago Today Two years from now

Change in risk appetite two years from

now compared to today

Risk averse/highly risk averse

24% 25% 19% -6%

Average 55% 54% 48% -6%

Opportunistic/highly opportunistic

21% 22% 34% +12%

Table 13: Confidence How do you feel about the outlook for your business over the following time periods?

12 months One to two years

Very pessimistic 3.6% 3.5%

Pessimistic 28.2% 18.4%

Confident 50.8% 52.6%

Very confident 11.5% 16.8%

Unsure/don't know 5.8% 8.7%

Shifts in SME risk approach and appetite

Source: Economist Intelligence Unit

Source: Economist Intelligence Unit

19Adapting in tough times: The growing resilience of UK SMEs

The long-term view: A vicious circle and return to growth

Strategic adaptation is the best approach to managing the risks of economic volatility and laying a strong foundation for the future. SMEs – some by design, others by necessity – have done just that after five years of economic stagnation. They are taking a longer-term view on business strategy (53%) and financial planning (35%), deleveraging (28%), diversifying (48%), becoming more agile (48%), working harder (47%) and smarter (39%) – more like the strategies employed by medium to large businesses. They are building confidence despite a tough risk environment that is unlikely to return to pre-2008 norms.

But SMEs have also adopted a notable conservatism that raises tough questions about the long-term strength and growth prospects of the UK’s SME economy. The past five years have put the squeeze on SMEs and many do not have the reserves – cash, resources, morale and other mechanisms – nor perhaps enough awareness of the full cost burdens that they face in order to tackle ongoing stagnation or volatility, despite projecting an overall confidence (75% feel that their company’s financial position is secure).

A return to growth seems inevitable in the overall context of fundamentally stronger SMEs, yet almost unachievable in the face of a potent conservatism today. This vicious circle is likely to play out until either the context for risk-taking decreases for UK SMEs, or the wider economy starts to show signs of rebounding. What role SMEs can play in sparking a return to economic growth is by no means certain – and represents the significant economic and policy challenge today.

Zurich Insurance plc is authorised by the Central Bank of Ireland and subject to limited regulation by the Financial Conduct Authority. Details about the extent of our regulation by the Financial Conduct Authority are available from us on request, FCA registration number 203093. These details can be checked on the FCA’s register by visiting their website www.fca.org.uk or by contacting them on 0845 606 1234.13

5559

A01

(04

/13)

ZC

A