actuary india oct 2011

TRANSCRIPT

8/3/2019 Actuary India Oct 2011

http://slidepdf.com/reader/full/actuary-india-oct-2011 1/32

O C T O B E R 2

0 1 1

V O L . I I I I S S U E

1 0`20

For Private Circulation Only

INDIAN ACTUARIAL PROFESSION

Serving the Cause of Public Interest

8/3/2019 Actuary India Oct 2011

http://slidepdf.com/reader/full/actuary-india-oct-2011 2/32

8/3/2019 Actuary India Oct 2011

http://slidepdf.com/reader/full/actuary-india-oct-2011 3/32

3Indian Actuarial Profession Serving the Cause of Public Interest The Actuary India October 2011

C O N T E N T S

ENQUIRIES ABOUT PUBLICATION OF ARTICLES OR NEWS

Please address all your enquiries with regard to the magazine by e-mail at [email protected] do not send it to editor or any other functionaries.

For circulation to members, connected

individuals and organizations only.

Chief Editor

Taket, Nick

Editor

Sharma, Sunil

Puzzle Editor

Mainekar, Shilpa

Manager (Library and Publishing)Rautela, Binita

COUNTRY REPORTERS

Smith, John Laurence

Kakar, Gautam

Chung, Phuong Ba

Sharma, Rajendra Prasad

USA

Cheema, Nauman

Pakistan

Leung, Andrew

Thailand

Krishen, Sukdev

South Africa

a.co.za

4

C O N T E N T S

FROM THE CHIEF EDITOR

NICK TAKET

FROM THE PRESIDENT

LIYAQUAT KHAN

ANNOUNCEMENT

FEATURES

Disclosures

CAREER CORNER

INTERVIEW

FROM THE PRESS DNA

for general insurers

IAA and ISSA

Understanding in Geneva IAA

Geneva

IAIS

IAA

FROM THE DESK OFChairperson

Social Security (PEBSS)

BOOK REVIEW

The Fundamentals of Pension

SHILPA'S PUZZLES

ENTRY EXAM

5

6

Disclaimer :

The tariff rates for advertisement in the Actuary India are as under:

Back Page colour ` 35,000/- Full page colour ` 30,000/- Half Page colour ` 20,000/-

7

22

29

30

28

25

9

31

8/3/2019 Actuary India Oct 2011

http://slidepdf.com/reader/full/actuary-india-oct-2011 4/32

4 Indian Actuarial Profession Serving the Cause of Public InterestThe Actuary India October 2011

FROM THE CHIEF EDITOR

T he work carried out by actuaries has changed very signicantly over the last few decades. Today we

routinely carry out investigations and analyses that would have been unheard of 25 years ago. It might

be thought that this is a measure of how much actuarial science has developed in that time. However, in

practice I believe that the application of actuarial science has developed little. Most of the changes brought

about in actuarial practice have come about because of the huge amount of cheap computing power that

actuaries have at their disposal today.

It is not that our predecessors were not aware of the issues that we deal with today or that they ignored them, it

was just that they could not tackle them by the use of brute computing power as we do today. Instead they had

to rely more on their insights and judgement to nd solutions. I believe this made them more rounded actuaries,

who were better equipped to face the challenges that our profession will face in the future. By which I mean

they were forced to spend more time thinking deeply about and understanding the nancial risks and problems

they faced.

By contrast, today if a problem is complicated we tend to take the easy way out and simply write or run a

programme to show us the possible answers.

There are a number of dangers for the profession in this approach. It allows the belief to grow that actuaries are

simply people who use actuarial software, and it fails to promote the development and application of the skill

of judgement within our members.

There are already people outside the profession who think that actuaries are just number crunchers. In addition,

we must all at some point of time have heard employers or clients wonder why they have to have so many

actuaries, surely they could manage by buying some actuarial software and get the IT department to run it.

At a simple level this suggestion can be refuted by employing the old computer adage “Garbage in, garbage out”,which is true of any software. However, this does not address the fundamental problem which is as actuaries

what is our unique selling proposition?

To my mind our USP is our ability to use judgement and insight to simplify and nd solutions to complex nancial

and risk problems. Yes, we use actuarial software, but this is just one of the tools of our trade.

We add value not by running the software but using our judgement to decide

• when to use the software, and when not;

• what needs to be modelled, and what does not;

• what scenarios will be important, and which less so;

• what modications need to be made to products or schemes to achieve the result

required by the client; and so on.

Our use of judgement is a signicant value addition to our employers and clients, and we must

do all we can to promote this skill amongst the members of the profession. We need to ensure

that our education and examination system not only teaches the use of software tools, but alsoplaces a major emphasis on the development of the skills of judgement and insight. These

constitute our main USP and we ignore them at our peril.

Will we as a profession always be able to rely on these skills? This is a difcult question to

answer, but a simple analogy with chess gives some food for thought.

Many years ago it was believed that the number of possible moves in a chess game was just so large that a

computer would never be able to beat a human at chess.

But then computing power grew exponentially, and it was not long before the very best chess computers could

beat all but the very best chess grandmasters.

It was then believed that this situation would remain unchanged because although grandmasters do analyse

a huge number of possible future moves, their unique strength lies in their ability to discount future moves

that lead to ”weak” positions and focus only on those that lead to “strong” positions. If asked to dene “weak”

and “strong” positions grandmasters would become somewhat vague, but in essence it was a matter of them

exercising their judgement.

There the matter rested for a number of years, until computing moved on, not in computing power, but in the

ability to teach computers to judge “strong” and “weak” positions, so that now even the very best chess players

in the world can be beaten by the very best chess computers.

So does the same fate await the actuarial profession?

Possibly, but the analogy with chess is not perfect since chess is a game with

• a xed set of rules,

• a limited number of pieces with clearly dened roles,

• an unambiguous denition of victory.

Whereas actuaries operate in an environment in which

• the rules keep changing,

• there are a large number of stakeholders whose roles continue to evolve over time, and

• even the denition of victory varies between players!

This leads to sufcient complexity and uncertainty to ensure that actuaries should be able to hold the computers

at bay for a good few years to come.

Nick Taket

T H E C H I E F E D I T O R

F R O M

8/3/2019 Actuary India Oct 2011

http://slidepdf.com/reader/full/actuary-india-oct-2011 5/32

5Indian Actuarial Profession Serving the Cause of Public Interest The Actuary India October 2011

FROM THE PRESIDENT he 16th East Asian Actuarial Conference – lessons to learn from:

As I write (13 th Oct., 2011) in Kuala Lumpur the 16 th East Asian Actuarial Conference (16 th EAAC) is on

and will come to an end this evening. Organised by the East Asian Actuarial Congress (eaac), it’s the

16 th one held biennially and the very rst one too was in Kula Lumpur. For the Actuarial Society of Malaysia

it was a nostalgic memory to recall, one of the then Organising Committee members from Malaysia is still

around: he was “recognised” during the inaugural function on 11 th Oct., 2011.

Mr. Donald Joshua Jaganathan, Assistant Governor, Bank Negara Malaysia was there to inaugurate and deliver

Key Note address.

A bit of a nostalgia for us in IAI too -- Years 2003/04 were hectic for us as we worked hard to become a member

of the eaac and were admitted to it in the year 2005 during the 13 th EAAC in BALI, Indonesia. The eaac opened

its door for the rst time beyond the original NINE founding members. This was followed by Australia, thus the

eaac is now ELEVEN members TEAM.

Things are changing fast – the Global Economic down-turn triggered by US Subprime mortgage defaults in the

years 2007/08 ended in global debate and dialogue including the Actuarial Community lead by International

Actuarial Association (IAA). Was there a voice in this global debate and dialogue amongst the actuarial

community from Asia/Asia Pacic? Can not think of one! Not surprising to me atleast!

In the Asia/Asia Pacic we have to move fast: our economies are interlinked, social and cultural values are

intertwined as well.

A small though important step: the eaac Board of Eleven members met on 10 th

Oct., to decide amongst othermatters to have the EAAC once a year after the next one in Singapore in year 2013. The circle moves in

alphabetical order so the 18 th EAAC will be in Taiwan and probably India ill get its turn in the year 2018.

The 16 th EAAC, at the last count amongst 508 participants, had its member associations contributing;

Malaysia: 162, Singapore: 85, Indonesia: 62, Hong Kong: 54, South Korea: 44, Japan: 14,

Taiwan: 12 Thailand: 12, India: 11, Australia: 11, The Philippines: 8 Total eaac members:

475 Others: 33

India with student population of 12,000+, the highest amongst the eaac member countries,

surely could have done better.

The Appointed Actuary in India:

The IRDA circular dt. 5 th Sept., 2011 proposing changes to the IRDA (Appointed Actuary)

Regulation, 2000 has brought quite lot of agitative application of mind amongst the stakeholders: the Insurers, the IAI members particularly those who are Appointed Actuaries

and are adversely affected and hopefuls to serve as Appointed Actuaries. The position of

Appointed Actuary is and as much perceived as a position of importance and power within

the corporate structure of an Insurer. The Introduction of the Appointed Actuary system in the

year 2000 concurrently with the opening up of the insurance sector to private participation was

somewhat of an historical importance. It was aimed at as an effective system of regulatory instrument so as to

ensure nancial stability of the insurer: having enough money to enable it to pay policyholder liabilities as and

when these fall due and the insurer required to hold on to solvency level with adequate capital for writing new

business, fell on the shoulders of the Appointed Actuary. Neither the AA system implies that the insurers would

not have actuarial staff other than those required to support the role of the Appointed Actuary nor does it mean

that the insurance regulator, IRDA would not have actuarial staff to perform its regulatory role. The Appointed

Actuary concept sits rmly on the belief that the regulatory roles expected of the Appointed Actuary could not

be performed well if such person were not part of the corporate structure of the insurer, not even if he/she

were to operate from within the ofce of the Insurance regulator. Nevertheless such Appointed Actuary has his/

her primary loyalties to the insurance regulator. A sound legal structure for this to happen is essential besides

ensuring that professional standards required of the professional body of the Appointed Actuary are complied

with and strictly enforced. This latter role of the actuarial body has to be demonstrative so as to ensure public

and the regulator of required level of comfort on ongoing basis. In case of India has this happened?

Questions have been raised. Aside from the circular from IRDA proposing changes to the provisions of the

(Appointed Actuary) Regulations, after about a decade do we not sit up and examine;

i) the framework of rules against which we issue certicate of Practice,

ii) the adequacy of Actuarial Practice Standards (earlier called Guidance Notes) that Appointed Actuaries are

required to observe,

iii) the compliance mechanism to ensure that the Actuarial Practice Standards are indeed complied with and

disciplinary actions that should follow in case of non-compliance,

iv) capacity building programmes to support the Appointed Actuary on ongoing basis, and that the ethical

standards are understood and followed.

Last but not the least the IRDA proposal, the “Appointed Actuary shall not function in any capacity other

than Appointed Actuary in the ofce of the insurer” should in my view be a welcome proposal. The CFO and

T T H E P R E S I D E N T

F R O M

8/3/2019 Actuary India Oct 2011

http://slidepdf.com/reader/full/actuary-india-oct-2011 6/32

6 Indian Actuarial Profession Serving the Cause of Public InterestThe Actuary India October 2011

MARK YOUR DATES FOR THE UPCOMING EvENTS

Eent Organised by Date Place

6 th Current Issues in Retirement Benets PEBSS Advisory Group November 18-19, 2011 Mumbai

7 th Current Issues in Life Assurance Life Insurance Advisory Group November 24-25, 2011 Mumbai

1st Current Issues in General Insurance General Insurance Advisory Group December 2, 2011 Mumbai

16 th India Fellowship Seminar PEC Advisory Group December 15-17, 2011 Mumbai

6 th Current Issues in Health & Care Insurance Health & Care Insurance Advisory Group January, 19-20, 2012 Gurgaon

14 th Global Conference of Actuaries PSIR Advisory Group February 19-21, 2012 Mumbai

Contact Person: Aparajita Mitra ([email protected] )

The Institute of

Actuaries

of

India

announces

“IAI Connect”

Organised by:

Social, Cultural and Youth Affairs adisory group (SC&YA)

Date: 3rd Dec 2011

Time: 10 am to 3 pm

venue:

Sai Palace Hotels, Mahakali Caves Road, Chakala,Andheri East, Mumbai - 400093.

A N N O U N C E M E N T

the Appointed Actuary denitely have conicts of interest: Appointed Actuary determines the capital required for doing

or holding certain amount of business and the CFO has to ensure that such capital is available. The CRO identies and

measures all the risks that the insurers holds within, the Appointed Actuary measures some of these (but not all) and

reserves for. The conict of interest of the CEO with the role of the Appointed Actuary is obvious. The question is not that

these conicts of interest exist; of course these do but the question is that the role boundaries of these positions should

be designed to be non-overlapping and thus non-frictional. Responsibility for dening such role boundaries, which have

serious regulatory implications, can’t be left to the Board of Insurance Companies alone.

Liyauat Khan

Vide notication dated 26 July 2011 the Government of India has nominated

Shri Arind Kumar, Joint Secretary (Pension & Insurance)

as a member of the Council of the Institute of Actuaries of India to represent the

Ministry of Finance vice Mr. Tarun Bajaj, Ex- Joint Secretary (Banking and Insurance).Mr. Arind Kumar

• Bringing Institute closer to the student members through series of

interactive sessions

• Talk by a senior Fellow

• Exam dealing techniques by a recently qualied Fellow

• Industry overview or talk by an actuarial employer

For more details about the workshop and downloading the registra-

tion form, please visit www.actuariesindia.org . There are limited seats

for the event, so registration will be done on rst come rst serve basis.

For any other queries, please email [email protected] .

8/3/2019 Actuary India Oct 2011

http://slidepdf.com/reader/full/actuary-india-oct-2011 7/32

7Indian Actuarial Profession Serving the Cause of Public Interest The Actuary India October 2011

(Courtsey the Chartered Accountant Journal of ICAI.July 2011)

DIFFERENCES BETwEEN IFRSs aND Ind aS

T his note is issued by the Institute

of Chartered Accountants of India

(ICAI) to bring out the differences

between the IFRSs1 as applicable on

1st April, 2011 and the corresponding

Indian Accounting Standards (Ind ASs)

placed by the Ministry of Corporate

Affairs (MCA), Government of India,

on its website after recommendation

of the same by the National Advisory

Committee on Accounting Standards

(NACAS) and the ICAI.

The Ind ASs placed on the MCA website

when notied under Section 211 (3) (c)

of the Companies Act, 1956 by the MCA

will be applicable to the companies

from the date specied in the said

notication. Section I of the note

contains IFRSs deferred by the MCA.

Section II contains carve outs from

IFRSs in the relevant Ind ASs. Section III

contains ‘Other major changes in Indian

Accounting Standards vis-à-vis IFRSs

not resulting in carve outs’. Section IV

contains a comparative chart of IFRSs

and corresponding Ind ASs indicating,

inter alia, IFRSs in respect of which

no corresponding Ind AS has been

formulated and reasons therefor.

I. IFRSs deferred by the MCA

1. Ind AS 11, Construction Contracts

IFRIC 12 and SIC 29, Service

Concession Arrangements and

Service Concession Arrangements:

Disclosures, respectively, which are

included as Appendices A and B to

Ind AS 11, Construction Contracts,

respectively, would not be notied along

with the other standards and their

application has been deferred.

Reasons

MCA received feedback regarding the

adverse consequences which may

ensue to the Indian companies in the

event of immediate adoption of the

IFRIC 12. Hence, MCA decided that

Appendix A to Ind AS 11, corresponding

to IFRIC 12, Service Concession

Arrangements should be deferred and

the same may be examined and applied

with or without modication later. Appendix B to Ind AS 11, corresponding

to SIC 29, Service Concession

Arrangements: Disclosures, is related

to IFRIC 12. Therefore, it has also been

deferred.

2. Ind AS 17, Leases

IFRIC 4 Determining Whether an

Arrangement contains a Lease, which

is included as Appendix C to Ind AS 17,

Leases would not be notied alongwith

the other standards and its application

has been deferred.

Reasons

MCA received feedback regarding the

adverse consequences which may

ensue to the Indian companies in theevent of immediate adoption of the

Appendix C to Ind AS 17, corresponding

to IFRIC 4. Hence, MCA decided that

the Appendix should be deferred and

the same may be examined and applied

with or without modication later.

3. Ind AS 106, Exploration for and

Evaluation of Mineral Resources

Ind AS 106 corresponding to IFRS

6, Exploration for and Evaluation

of Mineral Resources, would not be

notied immediately as it is under

consideration of the Government.

Reasons

MCA is of view that the standard is open-

ended offering freedom to companies

to follow virtually any policy they like.

The standard does not prescribe any

standardisation. In such circumstances,

the standard does not serve any

useful purpose and may create a

wrong impression in the mind of the

stakeholders that the entity concernedhas complied with a strict standard

when in fact, the company is free to apply

any accounting treatment it wants. This

may even be counter productive from a

regulatory point of view by giving a false

sense of correctness. Hence, this Ind AS

may not be notied immediately.

II Care Outs

A. Carve-outs which are due to

differences in application of

accounting principles and practicesand economic conditions prevailing in

India.

1. Ind AS 21, The Effects of Changes

in Foreign Exchange Rates As per IFRS

IAS 21 requires recognition of exchange

differences arising on translation of monetary items from foreign currency

to functional currency directly in prot

or loss.

Care out

Ind AS 21 permits an option to

recognise exchange differences arising

on translation of certain long-term

monetary items from foreign currency

to functional currency directly in equity.

In this situation, Ind AS 21 requires

the accumulated exchange differences

to be amortised to prot or loss in an

appropriate manner. IAS 21 does not

permit such a treatment.

Reasons

(i) There is signicant uctuation in

the value of US dollar vis-à-vis rupee.

India plans for a large expenditure on

infrastructure. This may need a very

large inow in the foreign borrowings.

These borrowings are denominated in

foreign currencies unlike developed

countries where borrowings aredenominated in localcurrencies.

(ii) Unlike currencies of many advanced

countries, rupee is not fully convertible.

(iii) Hedging is not possible for the

full period for which the loan is taken.

Hedging is available for shorter periods

but not for longer periods, and the

duration of the borrowings is very long.

(iv) Indian companies are not permitted

to prepay the foreign currency loans.

(v) Other countries such as South Korea

have also been raising these issues.

(vi) It is not appropriate to recognise the

exchange differences immediately which

arise as a result of items which are to be

paid/realised in foreign currency, after a

long term nature.

2. Ind AS 28, Investment in Associates

As per IFRS

IAS 28 requires that difference between

the reporting period of an associate and that of the investor should not be more

than three months, in any case.

1 The term ‘IFRS’ includes not only the International Financial Reporting Standards (IFRSs) issued by the IASB, it also includes the International Accounting Standards

(IASs), IFRICs and SICs.

F E A T U R E S

8/3/2019 Actuary India Oct 2011

http://slidepdf.com/reader/full/actuary-india-oct-2011 8/32

8 Indian Actuarial Profession Serving the Cause of Public InterestThe Actuary India October 2011

Care out

The phrase ‘unless it is impracticable’

has been added in the relevant

requirement i.e., paragraph 25 of Ind

AS 28.

Reasons

Since the investor does not have control

over the associate, it may not be able

to inuence the associate to changeits accounting period if it does not fall

within 3 months.

Apart from this, another reason can

be a situation, e.g., where an entity

is an associate of two investors and

difference between the reporting dates

of the associate and the investors

is more than three months and the

reporting dates of the two investors are

also different. In that case a problem

will arise that in respect of which

investor the associate will have tochange its reporting period.

3. Ind AS 28, Investment in Associates

As per IFRS

IAS 28 requires that for the purpose of

applying equity method of accounting in

the preparation of investor’s nancial

statements, uniform accounting policies

should be used. In other words, if the

associate’s accounting policies are

different from those of the investor, the

investor should change the nancial

statements of the associate by using

same accounting policies.

Care out

The phrase, ‘unless impracticable to

do so’ has been added in the relevant

requirements i.e., paragraph 26 of Ind

AS 28.

Reasons

Since the investor has signicant

inuence and not control over theassociate, it may not be able to inuence

the associate to change its accounting

policies.

4. Ind AS 32, Financial Instruments:

Presentation

Care out

An exception has been included to

the denition of ‘nancial liability’

in paragraph 11 (b) (ii), Ind AS 32 to

consider the equity conversion option

embedded in a convertible bonddenominated in foreign currency to

acquire a xed number of entity’s

own equity instruments as an equity

instrument if the exercise price is xed

in any currency. This exception is not

provided in IAS 32.

Reasons

This position is not appropriate in

instruments such as FCCBs since the

number of shares convertible on the

exercise of the option remains xed and

the amount at which the option is to be

exercised in terms of foreign currency is

also xed; merely the difference in thecurrency should not affect the nature of

derivative, i.e., the option.

5. Ind AS 39, Financial Instruments:

Recognition and Measurement

As per IFRS

IAS 39 requires all changes in fair values

in case of nancial liabilities designated

at fair value through Prot and Loss at

initial recognition shall be recognised in

prot or loss. IFRS 9 which will replaceIAS 39 requires these to be recognised

in ‘other comprehensive income’.

Care out

A proviso has been added to paragraph

48 of Ind AS 39 that in determining the

fair value of the nancial liabilities which

upon initial recognition are designated

at fair value through prot or loss, any

change in fair value consequent to

changes in the entity’s own credit risk

shall be ignored.

Reasons

It is felt that recognition of gain in prot

or loss or in ‘other comprehensive

income’ on deterioration of own

credit risk is not proper because such

deterioration ordinarily occurs when

an entity is incurring losses. Thus, if an

entity is allowed to recognise gain on

deterioration of its own credit risk, it will

book gains when its performance is not

upto the mark. In the recent nancial

crisis in USA, it was noted that somebanks booked gains while they were

incurring losses due to the crisis.

6. Ind AS 103, Business Combinations

As per IFRS

IFRS 3 requires bargain purchase gain

arising on business combination to be

recognised in prot or loss.

Care out

Ind AS 103 requires the same to be

recognised in other comprehensiveincome and accumulated in equity

as capital reserve, unless there is

no clear evidence for the underlying

reason for classication of the business

combination as a bargain purchase,in

which case, it shall be recognised

directly in equity as capital reserve.

Reasons

It is felt that recognition of such gains

in prot or loss would result into

recognition of unrealised gains as the

value of net assets is determined on

the basis of fair value of net assets

acquired.

7. Ind AS 101, First-time Adoption of

Indian Accounting Standards

(i) Presentation of comparaties in

the First-time Adoption of Indian

Accounting Standards (Ind AS) 101

(corresponding to IFRS 1)

As per IFRS

IFRS 1 denes transitional date as

beginning of the earliest period for which

an entity presents full comparativeinformation under IFRS. It is this date

which is the starting point for IFRS and

it is on this date the cumulative impact

of transition is recorded based on

assessment of conditions at that date by

applying the standards retrospectively

except to the extent specically provided

in this standard as optional exemptions

and mandatory exceptions. Accordingly,

the comparatives, i.e., the previous year

gures are also presented in the rst

nancial statements prepared under

IFRS on the basis of IFRS.

Care out

Ind AS 101, requires an entity to provide

comparatives as per the existing

notied Accounting Standards. It is

provided that, in addition to aforesaid

comparatives, an entity may also

provide comparatives as per Ind AS on

a memorandum basis.

Reason

This would facilitate smooth

convergence with IFRS as comparatives

are not required to be in accordance

with the Ind ASs. It is also felt that since

Ind AS 101 would not be considered

to be in existence for the comparative

period, requiring comparatives to be

prepared on the basis of Ind AS may not

be legally defensible.

(ii) Presentation of reconciliation

As per IFRS

IFRS 1 requires reconciliations for

opening equity, total comprehensive

income, cash ow statement and

closing equity for the comparative

period to explain the transition to IFRS

from previous GAAP.

F E A T U R E S

8/3/2019 Actuary India Oct 2011

http://slidepdf.com/reader/full/actuary-india-oct-2011 9/32

9Indian Actuarial Profession Serving the Cause of Public Interest The Actuary India October 2011

Jobprole

• Designation – Senior Manager Actuarial• Department - Actuary• Location – Prabhadevi, Mumbai

Qualication/Experience/Competencies(Noofyears&type)/Age

• Engineer/MBA/CA• Should have cleared most of the CT papers• Strong analytical and innovative problem solving skills;• Excellent written and oral communication skills;• At least 4 years in actuarial department of a life ofce

• Should have sound knowledge of Embedded Value Reporting / Valuation agency• Should be procient in Prophet and excel

Key Accountabilities of the Role Manage and delier

• Quarterly Embedded Value Reporting process including Analysis of Movements. It consists of a. Market Consistent Basisb. Traditional Basis

- for our Board and- for incorporation into Prudential Corporation Asia disclosures.

c. Traditional Basis channel (sub business unit) level Analysis of Movements

Monthly Ne Business Reporting Process

•User Acceptance Testing of the Embedded Value / Market Consistent Embedded Value models•Investigating various Experience Variances and providing inputs to the Assumption Setting Process

About ICICI Prudential life Insurance

ICICI Prudential Life Insurance Company is a joint venture between ICICI Bank - one of India’s foremost nancial ser-vices companies-and Prudential plc - a leading international nancial services group headquartered in the UnitedKingdom.Further information about us can be explored at – www.iciciprulife.com. Pls e-mail resumes to [email protected] with “Senior Manager Actuarial” as the subject.

Care out

Ind AS 101 provides an option to

provide a comparative period nancial

statements on memorandum basis.

Where the entities do not exercise this

option and, therefore, do not provide

comparatives, they need not provide

reconciliation for total comprehensive

income, cash ow statement and

closing equity in the rst year of transition but are expected to disclose

signicant differences pertaining to

total comprehensive income. Entities

that provide comparatives would have to

provide reconciliations which are similar

to IFRS.

Reason

This would facilitate smooth

convergence with IFRS.

(iii) Cost of Non-current Assets Held

for Sale and Discontinued Operations

on the date of transition on First-

time Adoption of Indian Accounting

Standards (Ind AS)

Care out

Ind AS 101 provides transitional relief

that while applying Ind AS 105 - Non-

current Assets Held for Sale and

Discontinued Operations, an entity may

use the transitional date circumstances

to measure such assets or operations

at the lower of carrying value and fair

value less cost to sell.

Reason

This would facilitate smooth

convergence with IFRS.

(i) Foreign currency gains/losses

on translation of long term monetary

items

Care out

Ind AS 101 provides that on the date

of transition, if there are long-term

monetary assets or long- term monetary

liabilities mentioned in paragraph

29A of Ind AS 21, an entity may

exercise the option mentioned in that

paragraph regarding spreading over

the unrealised Gains/Losses over

the life of Assets/Liabilities either

retrospectively or prospectively. If this

option is exercised prospectively, the

accumulated exchange differences in

respect of those items are deemed to

be zero on the date of transition.

Reason

Exemption given as a consequence of

optional treatment prescribed in Ind AS

21, The Effects of Changes in Foreign

Exchange Rates, in context of exchange

differences arising on account of certain

long-term monetary assets or long-term

monetary liabilities.

(v) Financial instruments existing on

transition date

Care out

Ind AS 101 provides that the nancial

instruments carried at amortised cost

should be measured in accordance with

Ind AS 39 from the date of recognition

of nancial instruments unless it is

impracticable (as dened in Ind AS 8)

for an entity to apply retrospectively the effective interest method or the

impairment requirements of Ind AS 39.

If it is impracticable to do so then the fair

value of the nancial asset at the date

of transition to Ind-ASs shall be the new

amortised cost of that nancial asset at

the date of transition to Ind ASs.

Ind AS 101 provides another exemption

that nancial instruments measured at

fair value shall be measured at fair value

as on the date of transition to Ind AS.

Reason

This exemption would facilitate smooth

convergence with IFRS.

(vi)DenitionofpreviousGAAPunder

Ind AS 101 First-time Adoption of

Indian Accounting Standards

As per IFRS

IFRS 1 denes previous GAAP as the

basis of accounting that a rst-time

adopter used immediately before

adopting IFRS.

F E A T U R E S

Continued on next page..

C A R E E R O

P P O R T

U N I T Y

8/3/2019 Actuary India Oct 2011

http://slidepdf.com/reader/full/actuary-india-oct-2011 10/32

10 Indian Actuarial Profession Serving the Cause of Public InterestThe Actuary India October 2011

Care out

Ind AS 101 denes previous GAAP as

the basis of accounting that a rst-

time adopter used immediately before

adopting Ind ASs for its reporting

requirements in India. For instance,

for companies preparing their nancial

statements in accordance with the

existing Accounting Standards notied

under the Companies (Accounting Standards) Rules, 2006 shall consider

those nancial statements as previous

GAAP nancial statements.

Reason

The change makes it mandatory

for Indian companies to consider

the nancial statements prepared

in accordance with existing notied

Indian accounting standards as was

applicable to them as under Companies

(Accounting Standards)

Rule, 2006 as previous GAAP when

it transitions to Ind AS as the law

prevailing in India does not recognise

the nancial statements prepared in

accordance with Accounting Standards

other than those prescribed under the

Companies Act.

(ii) Cost of Property, Plant and

Euipment (PPE), Intangible Assets,

Inestment Property, on the date of

transition of First-time Adoption of

Indian Accounting Standards.

Ind AS 101 provides an entity an option

to use carrying values of all assets as

on the date of transition in accordance

with previous GAAP as an acceptable

starting point under Ind AS

Reasons

The existing Indian notied Accounting

Standards are not signicantly different

from IFRS as all the standards have

been based on IFRS. It will minimise the

cost of convergence.

B.Carve-outs for specic industries

1. Ind AS 18, Revenue

As per IFRS

On the basis of principles of the

IAS 18, IFRIC 15 on Agreement for

Construction of Real Estate, prescribes

that construction of real estate should

be treated as sale of goods and

revenue should be recognised when

the entity has transferred signicant

risks and rewards of ownership and has

retained neither continuing managerial

involvement nor effective control.

Care out

IFRIC 15 has not been included in Ind

AS 18, Revenue. Such agreements

have been scoped out from Ind AS 18

and have been included in Ind AS 11,

Construction Contracts.

Reasons

(i) IFRIC 15, would have required the

real estate developers to recognise therevenue in their nancial statements

based on the completion method i.e.,

only in the last year of the completion

of the project. In that case, the prot

and loss account of the developers will

not truly reect the performance of the

business, as during the years the real

estate project continues, no revenue

will be recognised. In other words, prot

and loss account will not reect proper

measure of performance of business.

(ii) Some countries such as Malaysiahave also decided not to apply IFRIC

15 for the time being. Similarly, while

Singapore has decided to issue IFRIC

15, it has provided specic guidance in

the context of legal situations prevailing

in that country.

2. Ind AS 18, Revenue

Care out

A footnote has been added in paragraph

1 to Ind AS 18, Revenue, that for rate

regulated entities, this standard shall

stand modied, where and to the extent

the recognition and measurement of

revenue of such entities is affected

by recognition and measurement of

regulatory assets/liabilities as per the

Guidance Note on the subject being

issued by the Institute of Chartered

Accountants of India.

Reason

Rate regulated entities such as

electricity companies are subject to tariff xation by the relevant

authorities. Tariff is xed on the basis

of certain costs which are different

from the expenses recognised in

nancial statements. Such differences

may result into certain regulatory

assets and regulatory liabilities which

are presently not recognised as per

the IFRS. Such entities feel that

such assets and liabilities exist and,

therefore, should be recognised in

nancial statements. IASB had earlier

taken up a project on this subject which

has been dropped from its Agenda. ICAI

is developing a Guidance Note on the

subject.

3. Indian Accounting Standard on

Agriculture (Corresponding to IAS 41)

As per IFRS

IAS 41, Agriculture, requires

measurement of biological assets, viz.,

living animals and plants at fair value

and recognising gains and losses arising

on such measurement in prot or loss,

unless ascertainment of fair value is

unreliable.

Care out

It has been decided to revise the

Standard and not to issue the standard

as it is.

Reasons

(i) There is difculty in identifying the

attributes of biological assets, the cost

of fair valuation, and high volatility of

signicant qualitative factors (not within

the control of the entity) leads to greatersubjectivity in estimating fair value.

(ii) The quoted market price for bearer

biological assets (e.g. long-term assets

that produce each year such as tea,

coffee, rubber and palm oil trees) is

not easily available, since these are not

traded in the open market.

(iii) Present value (PV) method is to

be adopted for estimating fair value

of biological assets such as forests.

Making appropriate estimates of futureprice and costs levels are key factors

for a reliable fair value measurement

of standing forests. Due to the long-

term nature of the period of cash ows,

small uctuations in the assumptions

may have a signicant effect on the

calculated fair value.

(iv) Fair value of biological assets may not

be relevant because most plantations

are rarely sold. Fair valuation may give

the impression that the value of the

company increases when in reality

nothing has changed.

(v) Considering the high volatility of

prices for the end products, the fair

value adopted as cost as per IAS 41,

may result in very signicant impact on

the protability of the companies.

III Other major changes in Indian

Accounting Standards is-a-is IFRSs

not resulting in care-outs

1. Ind AS 1, Presentation of Financial Statements

1. With regard to preparation of

Statement of prot and loss, IAS 1,

F E A T U R E S

8/3/2019 Actuary India Oct 2011

http://slidepdf.com/reader/full/actuary-india-oct-2011 11/32

11Indian Actuarial Profession Serving the Cause of Public Interest The Actuary India October 2011

Presentation of Financial Statements,

provides an option either to follow the

single statement approach or to follow

the two statement approach. While

in the single statement approach,

all items of income and expense

are recognised in the statement of

profit and loss, in the two statements

approach, two statements are

prepared, one displaying components

of profit or loss (separate incomestatement) and the other beginning

with profit or loss and displaying

components of other comprehensive

income. Ind AS 1 allows only the single

statement approach.

2. IAS 1 requires preparation of a

Statement of Changes in Equity as a

separate statement. Ind AS

1 requires the Statement of Changes

in Equity to be shown as a part of the

balance sheet.

3. IAS 1 gives the option to individual

entities to follow different terminology

for the titles of nancial statements. Ind

AS 1 is changed to remove alternatives

by giving one terminology to be used by

all entities.

4. IAS 1 permits the periodicity, for

example, of 52 weeks for preparation of

nancial statements. Ind AS 1 does not

permit it.

5. IAS 1 requires an entity o present

an analysis of expenses recognised in

prot or loss using a classication based

on either their nature or their function

within the equity. Ind AS 1 requires only

nature-wise classication of expenses.

6. IAS 1 contains Implementation

Guidance. Ind AS 1 does not include

the same because various enactments

have prescribed formats,e.g., Schedule

VI to the Companies Act, 1956.

2. Ind AS 7, Statement of Cash Flows

1. In case of other than nancial entities,

IAS 7 gives an option to classify the

interest paid and interest and dividends

received as item of operating cash

ows. Ind AS 7 does not provide such an

option and requires these items to be

classied as items of nancing activity

and investing activity, respectively.

2. IAS 7 gives an option to classify the

dividend paid as an item of operating

activity. However, Ind AS 7 requires it to be classied as a part of nancing

activity only.

3. Ind AS 8, Accounting Policies,

Changes in Accounting Estimates and

Errors

Ind AS 8 has been amended to provide

that in absence of specic Ind AS

on the subject, management may

also rst consider the most recent

pronouncements of International

Accounting Standards Board and in

absence thereof those of the other

standard-setting bodies that usea similar conceptual framework to

develop accounting standards, other

accounting literature and accepted

industry practices.

4. Ind AS 16, Property, Plant and

Equipment

Language of paragraph 8 has been

changed to clarify more precisely that

‘servicing equipment’ also qualies as

property, plant and equipment when an

entity expects to use them during more than one period.

5. Ind AS 19, Employee Benets

1. According to Ind AS 19 the rate to

be used to discount post-employment

benet obligation shall be determined

by reference to the market yields on

government bonds, whereas under IAS

19, the government bonds can be used

only where there is no deep market of

high quality corporate bonds.

2. To illustrate treatment of gratuitysubject to ceiling under Indian Gratuity

Rules, an example has been added in

Ind AS 19.

3. IAS 19 permits various options for

treatment of actuarial gains and losses

for post- employment dened benet

plans whereas Ind AS 19 requires

recognition of the same in other

comprehensive income, both for post-

employment dened benet plans and

other long-term employment benet

plans. The actuarial gains recognisedin other comprehensive income should

be recognised immediately in retained

earnings and should not be reclassied

to prot or loss in a subsequent period.

6. Ind AS 20, Accounting for

Government Grants and Disclosure of

Government Assistance

1. IAS 20 gives an option to measure

non-monetary government grants either

at their fair value or at nominal value.

Ind AS 20 requires measurement of such grants only at their fair value. Thus,

the option to measure these grants at

nominal value is not available under Ind

AS 20.

2. IAS 20 gives an option to present

the grants related to assets, including

non-monetary grants at fair value in

the balance sheet either by setting

up the grant as deferred income or

by deducting the grant in arriving at

the carrying amount of the asset. Ind

AS 20 requires presentation of such

grants in balance sheet only by setting

up the grant as deferred income. Thus,

the option to present such grants bydeduction of the grant in arriving at

the carrying amount of the asset is not

available under Ind AS 20.

7. Ind AS 21, The Effects of Changes in

Foreign Exchange Rates

1. When there is a change in functional

currency of either the reporting currency

or a signicant foreign operation, IAS

21 requires disclosure of that fact

and the reason for the change in

functional currency. Ind AS 21 requires

an additional disclosure of the date of

change in functional currency.

2. The following examples have been

included in Ind AS 21, The Effects of

Changes in Foreign Exchange Rates, as

Appendix B:

1) An example to clarify the provisions of

paragraph 14.

2) An example to clarify impairment loss

in Paragraph 25.

3) An example to clarify paragraphs 33and 37.

4) The date of change of functional

currency should also be disclosed in

paragraph 57.

8. Ind AS 23, Borrowing Costs

IAS 23 provides no guidance as to how

the adjust-ment prescribed in paragraph

6(e) is to be deter-mined. Ind AS 23

provides guidance in this regard.

9. Ind AS 24, Related Party Disclosures

1. In Ind AS 24, disclosures which conict

with condentiality requirements of

statute/regulations are not required to

be made since Accounting Standards

cannot override legal/regulatory

requirements.

2. Paragraph 24A (reproduced below)

has been included in the Ind AS 24.

It provides additional claricatory

guidance regarding aggregation of

transactions for disclosure.“24A Disclosure of details of particular

transactions with individual related

parties would frequently be too

voluminous to be easily understood.

F E A T U R E S

8/3/2019 Actuary India Oct 2011

http://slidepdf.com/reader/full/actuary-india-oct-2011 12/32

12 Indian Actuarial Profession Serving the Cause of Public InterestThe Actuary India October 2011

Accordingly, items of a similar nature

may be disclosed in aggregate by type

of related party. However, this is not

done in such a way as to obscure the

importance of signicant transactions.

Hence, purchases or sales of goods are

not aggregated with purchases or sales

of xed assets. Nor a material related

party transaction with an individual

party is clubbed in an aggregated

disclosure.”

3. In the denition of the ‘close members

of the family of a person’ , relatives as

specied under the meaning of ‘relative’

under the Companies Act, 1956, has

been included.

10. Ind AS 27, Consolidated and

Separate Financial Statements

1. Paragraphs 8, 10 and 42 have

been deleted and paragraphs 9, 11,

39 and 43 have been modied as the

applicability or exemptions to the IndianAccounting Standards is governed by

the Companies Act and the Rules made

thereunder.

2. A sentence has been added in

paragraph 9 of Ind AS 27, Consolidated

and Separate Financial Statements

requiring that for companies the form

of consolidated nancial statements as

given in Appendix C to this standard shall

be applied to the extent circumstances

admit.

11. Ind AS 29, Financial Reporting in

Hyperination- ary Economies

Ind AS 29 requires an additional

disclosure regarding the duration of the

hyperinationary situation existing in

the economy.

12. Ind AS 33, Earnings per Share

1. IAS 33 provides that when an entity

presents both consolidated nancial

statements and separate nancial

statements, it may give EPS related

information in consolidated nancial

statements only, whereas, the Ind AS 33

requires EPS related information to be

disclosed both in consolidated nancial

statements and separate nancial

statements.

2. Paragraph 2 of IAS 33 requires that

the entire standard applies to :

(a) the separate or individual nancial

statements of an entity:

(i) whose ordinary shares or potential

ordinary shares are traded in a public

market (a domestic or foreign stock

exchange or an over-the-counter market,

including local and regional markets) or

(ii) that les, or is in the process of

ling, its nancial statements with a

Securities Regulator or other regulatory

organisation for the purpose of issuing

ordinary shares in a public market; and

(b) the consolidated nancial statements

of a group with a parent:

(i) whose ordinary shares or potential

ordinary shares are traded in a publicmarket (a domestic or foreign stock

exchange or an over-the-counter

market, including local and regional

markets) or

(ii) that les, or is in the process of

ling, its nancial statements with a

Securities Regulator or other regulatory

organisation for the purpose of issuing

ordinary shares in a public market.

It also requires that an entity that

discloses earnings per share shallcalculate and disclose earnings

per share in accordance with this

Standard.

The above have been deleted in the Ind

AS as the applicability or exemptions

to the Indian Accounting Standards is

governed by the Companies Act and the

Rules made there under.

3. Paragraph 4 has been modied in

Ind AS 33 to clarify that an entity shall

not present in separate nancial sta tements,earningspersharebasedont

heinformation given in consolidated

nancial statements, besides requiring

as in IAS 33, that earnings per share

based on the information given in

separate nancial statements shall

not be presented in the consolidated

nancial statements.

4. In Ind AS 33, a paragraph has been

added after paragraph 12 on the

following lines -

“Where any item of income or expense

which is otherwise required to be

recognised in prot or loss in accordance

with accounting standards is debited or

credited to securities premium account/

other reserves, the amount in respect

thereof shall be deducted from prot or

loss from continuing operations for the

purpose of calculating basic earnings

per share.”

5. In Ind AS 33 paragraph 15 has

been amended by adding the phrase,‘irrespectie of hether such discount

or premium is debited or credited to

securities premium account’ to further

clarify that such discount or premium

shall also be amortised to retained

earnings.

13. Ind AS 34, Interim Financial

Reporting

A footnote has been added to paragraph

1of Ind AS 34, Interim Financial

Reporting that Unaudited Financial

Results required to be prepared and

presented under Clause 41 of Listing Agreement with stock exchanges is not

an ‘Interim Financial Report’ as dened

in paragraph 4 of this Standard.

14. Ind AS 40, Investment Property

IAS 40 permits both cost model and fair

value model (except in some situations)

for measurement of investment

properties after initial recognition. Ind

AS 40 permits only the cost model.

15. Ind AS 101 First-time Adoption of Indian Accounting Standards

1. Paragraph 3 of Ind AS 101 species

that an entity’s rst Ind AS nancial

statements are the rst annual

nancial statements in which the entity

adopts Ind ASs in accordance with

Ind ASs notied under the Companies

Act, 1956 whereas IFRS 1 provides

various examples of rst IFRS nancial

statements.

2. Paragraph 4 of IFRS 1 providesvarious examples of instances when an

entity does not apply this IFRS. Ind AS

101 does not provide the same.

3. IFRS 1 requires specic disclosures

if the entity provides non-IFRS

comparative information and historical

summaries. Such disclosures are not

required under Ind AS 101.

16. Ind AS 103, Business Combinations

IFRS 3 excludes from its scope businesscombinations of entities under common

control. Appendix C of Ind AS 103 gives

guidance in this regard.

Notes:

1. Differences between Indian

Accounting Standards (Ind-ASs)

and corresponding IFRSs are given

in Appendix 1 at the end of each

Indian Accounting Standard.

2. Apart from the changes in IFRSs

as a result of carve- outs and otherchanges as described in above

section, changes consequential

thereto have also been made in all

Ind ASs, wherever required.

F E A T U R E S

8/3/2019 Actuary India Oct 2011

http://slidepdf.com/reader/full/actuary-india-oct-2011 13/32

13Indian Actuarial Profession Serving the Cause of Public Interest The Actuary India October 2011

Iv. Comparison of IFRS as applicable on 1st April 2011 ith Ind AS, placed at MCA’s ebsite

S

No.

IFRS /

IAS No.

Corresponding

Indian Accounting

Standard

Name

1. IAS 1 Ind AS 1 Presentation of Financial Statements

2. IAS 2 Ind AS 2 Inventories

3. IAS 7 Ind AS 7 Statement of Cash Flows

4. IAS 8 Ind AS 8 Accounting Policies, Changes in Accounting Estimates and Errors5. IAS 10 Ind AS 10 Events after the Reporting Period

6. IAS 11 Ind AS 11 Construction Contracts

7. IAS 12 Ind AS 12 Income Taxes

8. IAS 16 Ind AS 16 Property, Plant and Equipment

9. IAS 17 Ind AS 17 Leases

10. IAS 18 Ind AS 18 Revenue

11. IAS 19 Ind AS 19 Employee Benefts

12. IAS 20 Ind AS 20 Accounting for Government Grants and Disclosure of Government Assistance

13. IAS 21 Ind AS 21 The Effects of Changes in Foreign Exchange Rates

14. IAS 23 Ind AS 23 Borrowing Costs

15. IAS 24 Ind AS 24 Related Party Disclosures

16. IAS 26 * Accounting and Reporting by Retirement Beneft Plans

17. IAS 27 Ind AS 27 Consolidated and Separate Financial Statements

18. IAS 28 Ind AS 28 Investments in Associates

19. IAS 29 Ind AS 29 Financial Reporting in Hyperinationary Economies

20. IAS 31 Ind AS 31 Interests in Joint Ventures

21. IAS 32 Ind AS 32 Financial Instruments: Presentation

22. IAS 33 Ind AS 33 Earnings per Share

23. IAS 34 Ind AS 34 Interim Financial Reporting

24. IAS 36 Ind AS 36 Impairment of Assets

25. IAS 37 Ind AS 37 Provisions, Contingent Liabilities and Contingent Assets

26. IAS 38 Ind AS 38 Intangible Assets

27. IAS 39 Ind AS 39 Financial Instruments: Recognition and Measurement

28. IAS 40 Ind AS 41 Investment Property

29. IAS 41 ** Agriculture

30. IFRS 1 Ind AS 101 First-time Adoption of Indian Accounting Standards

31. IFRS 2 Ind AS 102 Share based Payment

32. IFRS 3 Ind AS 103 Business Combinations

33. IFRS 4 Ind AS 104 Insurance Contracts

34. IFRS 5 Ind AS 105 Non current Assets Held for Sale and Discontinued Operations

35. IFRS 6 Ind AS 106 Exploration for and Evaluation of Mineral Resources

36. IFRS 7 Ind AS 107 Financial Instruments: Disclosures

37. IFRS 8 Ind AS 108 Operating Segments

38. IFRS 9 *** Financial Instruments

* Ind AS corresponding to IAS 26 Accounting and Reporting by Retirement Benet Plans has not been placed on MCA’s website

as this standard is not applicable to companies

** Ind AS corresponding to IAS 41, Agriculture, is being redrafted.

*** It has been decided that Ind AS corresponding to IFRS 9, Financial Instruments, should not be issued since it was felt that it was

incomplete; instead of this standard, Ind AS 39 has been issued.

F E A T U R E S

8/3/2019 Actuary India Oct 2011

http://slidepdf.com/reader/full/actuary-india-oct-2011 14/32

14 Indian Actuarial Profession Serving the Cause of Public InterestThe Actuary India October 2011

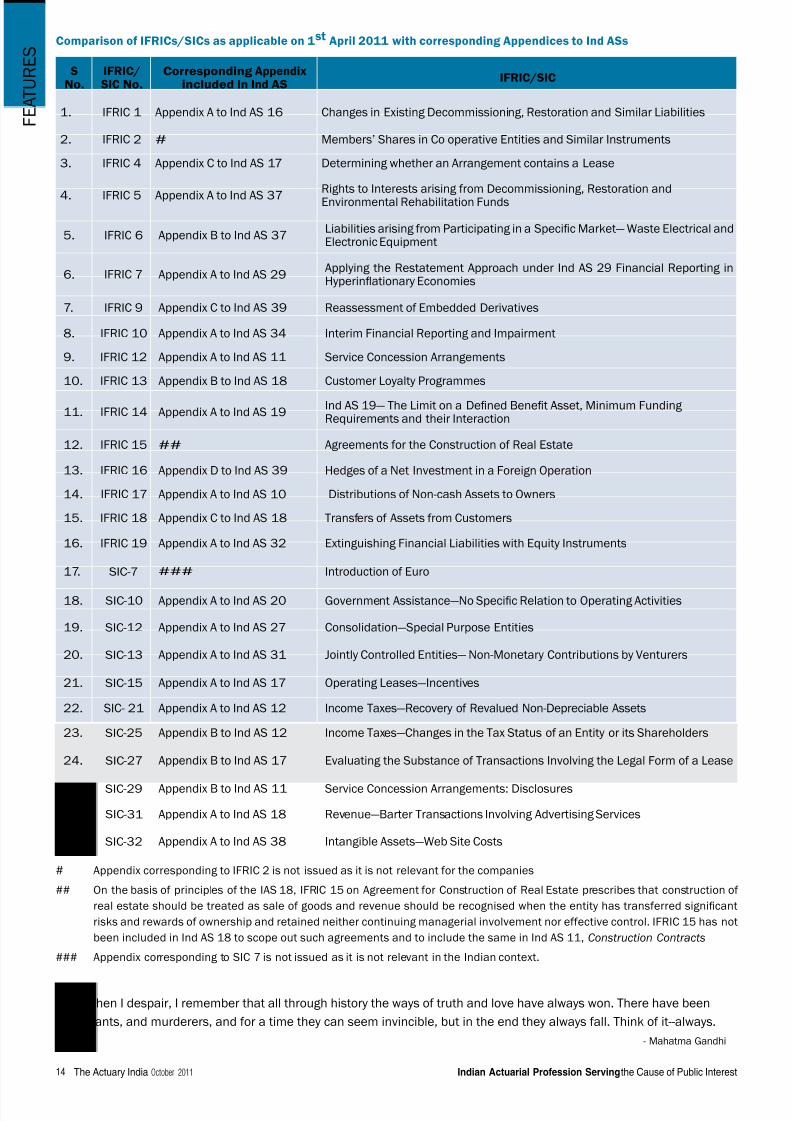

Comparison of IFRICs/SICs as applicable on 1st April 2011 ith corresponding Appendices to Ind ASs

SNo.

IFRIC/SIC No.

Corresponding Appendixincluded in Ind AS

IFRIC/SIC

1. IFRIC 1 Appendix A to Ind AS 16 Changes in Existing Decommissioning, Restoration and Similar Liabilities

2. IFRIC 2 # Members’ Shares in Co operative Entities and Similar Instruments

3. IFRIC 4 Appendix C to Ind AS 17 Determining whether an Arrangement contains a Lease

4. IFRIC 5 Appendix A to Ind AS 37Rights to Interests arising from Decommissioning, Restoration andEnvironmental Rehabilitation Funds

5. IFRIC 6 Appendix B to Ind AS 37Liabilities arising from Participating in a Specic Market— Waste Electrical andElectronic Equipment

6. IFRIC 7 Appendix A to Ind AS 29Applying the Restatement Approach under Ind AS 29 Financial Reporting inHyperinationary Economies

7. IFRIC 9 Appendix C to Ind AS 39 Reassessment of Embedded Derivatives

8. IFRIC 10 Appendix A to Ind AS 34 Interim Financial Reporting and Impairment

9. IFRIC 12 Appendix A to Ind AS 11 Service Concession Arrangements

10. IFRIC 13 Appendix B to Ind AS 18 Customer Loyalty Programmes

11. IFRIC 14 Appendix A to Ind AS 19Ind AS 19— The Limit on a Dened Benet Asset, Minimum Funding Requirements and their Interaction

12. IFRIC 15 ## Agreements for the Construction of Real Estate

13. IFRIC 16 Appendix D to Ind AS 39 Hedges of a Net Investment in a Foreign Operation

14. IFRIC 17 Appendix A to Ind AS 10 Distributions of Non-cash Assets to Owners

15. IFRIC 18 Appendix C to Ind AS 18 Transfers of Assets from Customers

16. IFRIC 19 Appendix A to Ind AS 32 Extinguishing Financial Liabilities with Equity Instruments

17. SIC-7 ### Introduction of Euro

18. SIC-10 Appendix A to Ind AS 20 Government Assistance—No Specic Relation to Operating Activities

19. SIC-12 Appendix A to Ind AS 27 Consolidation—Special Purpose Entities

20. SIC-13 Appendix A to Ind AS 31 Jointly Controlled Entities— Non-Monetary Contributions by Venturers

21. SIC-15 Appendix A to Ind AS 17 Operating Leases—Incentives

22. SIC- 21 Appendix A to Ind AS 12 Income Taxes—Recovery of Revalued Non-Depreciable Assets

23. SIC-25 Appendix B to Ind AS 12 Income Taxes—Changes in the Tax Status of an Entity or its Shareholders

24. SIC-27 Appendix B to Ind AS 17 Evaluating the Substance of Transactions Involving the Legal Form of a Lease

25. SIC-29 Appendix B to Ind AS 11 Service Concession Arrangements: Disclosures

26. SIC-31 Appendix A to Ind AS 18 Revenue—Barter Transactions Involving Advertising Services

27. SIC-32 Appendix A to Ind AS 38 Intangible Assets—Web Site Costs

# Appendix corresponding to IFRIC 2 is not issued as it is not relevant for the companies

## On the basis of principles of the IAS 18, IFRIC 15 on Agreement for Construction of Real Estate prescribes that construction of

real estate should be treated as sale of goods and revenue should be recognised when the entity has transferred signicant

risks and rewards of ownership and retained neither continuing managerial involvement nor effective control. IFRIC 15 has not

been included in Ind AS 18 to scope out such agreements and to include the same in Ind AS 11, Construction Contracts

### Appendix corresponding to SIC 7 is not issued as it is not relevant in the Indian context.

F E A T U R E S

when I despair, I remember that all through history the ways of truth and love have always won. There have been

tyrants, and murderers, and for a time they can seem invincible, but in the end they always fall. Think of it--always.

- Mahatma Gandhi

8/3/2019 Actuary India Oct 2011

http://slidepdf.com/reader/full/actuary-india-oct-2011 15/32

15Indian Actuarial Profession Serving the Cause of Public Interest The Actuary India October 2011

A PEEP INTO IND AS 19: THE NEw wAY FOR PENSION LIABILITY

MEASURES AND DISCLOSURES

By R Arunachalam FIA ; FIAI and

Nasrat Kamal FIA ; FIAI

I ntroduction

The requirement for a uniform

accounting framework across the

world, the emergence of International

Financial Reporting Standards (IFRS)

and its growing signicance has been

phenomenal during the past few years.

In pursuance of this requirement, India

has started the process of convergence

of Indian Accounting Standards with

IFRS.

The International Accounting Standards

Board (IASB) is an independent, privately

funded accounting standard setter

based in London. The IASB was founded

on 1 April 2001 as the successor to the International Accounting Standards

Committee (IASC).

International Financial Reporting

Standards (IFRS) are principles

based Standards, Interpretations and

Framework developed, adopted and

promoted for use and application

across various companies.

IASB is responsible for setting the

IFRS. Many of the standards forming

part of IFRS are known by the older

name of International Accounting Standards (IAS). IASs were issued

between 1973 and 2001 by the

erstwhile IASC. The IASB adopted all

these existing IASs in its rst meeting

and continued to develop new

standards calling them as IFRS.

IFRS are used in many parts of the world,

including the European Union, Hong

Kong, Australia, Malaysia, Pakistan, Gulf

Countries, Russia, South

Africa, Singapore and Turkey. As of

2008, more than 113 countries around the world, including all of Europe

require or permit IFRS reporting. The

Securities and Exchange Commission

(SEC) in the US is slowly but

progressively shifting from requiring

only US Generally Accepted Accounting

Principles (US GAAP) to accepting

IFRS and will most likely accept IFRS

standards in the long term.

It is expected that IFRS adoptionworldwide will be benecial to investors

and other users of nancial statements,

by reducing the costs of comparing

alternative investments and increasing

the quality of information. Companies

are also expected to benet, as investors

will be more willing to provide nancing.

IndianotiesIndAS19

The Institute of Chartered Accountants

of India (ICAI), set up by an Act of

Parliament in 1949, is a statutory body

aimed at regulating the profession of Chartered Accountants in India. The

ICAI is also responsible for specifying

and recommending the accounting

standards to be followed by companies

conducting business in India. While

formulating accounting standards,

the ICAI takes into consideration the

applicable laws, customs, usages and

business environment prevailing in the

country.

As per the Companies Act, 1956, ICAI

would recommend the accounting

standards which may then be prescribed

by the Central Government in consultation

with the National Advisory Committee

on Accounting Standards (NACAS) for

adoption by companies. The section

further claries that the accounting

standards specied by the ICAI shall be

deemed to be the accounting standards

until such prescription by the Central

Government.

The Central Government constituted

the National Advisory Committee on

Accounting Standards (NACAS) in 2001.The NACAS have been reviewing the

accounting standards and working

closely with the ICAI since its constitution.

The accounting standards specied

by the ICAI were deemed to be the

accounting standards until 2006,

by when the Ministry of Corporate

Affairs started notifying the prescribed

accounting standards in consultation

with NACAS.

The Ministry of Corporate Affairs (MCA)

notied thirty ve Indian Accounting

Standards, referred to as “Ind AS”, on

25 February 2011 as part of the IFRS

convergence process. The MCA will

implement the IFRS converged Indian

Accounting Standards in a phased

manner after various issues including

tax related issues are resolved with the

concerned departments. It would be

ensured that the implementation of the

converged standards is smooth for all the stakeholders.

The date of implementation of the Ind

AS will be notied by the MCA at a later

date. Although the MCA is yet to nalize

and declare the exact implementation

date/s, notication of Ind AS is a

signicant step towards convergence

with IFRS.

In the ensuing sections of this article, we

have atempted to capture the synopsis

of areas of divergence between Ind AS

19 as notied by the MCA, the existing standard AS 15 (rev 2005) as adopted

by ICAI and the existing International

Accounting Standard IAS 19 as adopted

by IASB. We have also included the Ind

AS 19 impact for the companies and the

role of the Actuarial Profession.

Ind AS19changes from the existing

standard AS 15 (reised 2005)

ICAI issued the existing Accounting

Standard AS 15 (revised 2005) in March

2005 effective from accounting periods

commencing on or after 1 April 2006.This existing standard was regarded as an

improvement over the earlier standard.

It is a ‘market based’ standard that

measures employee benet liabilities on

a basis that is consistent with nancial

markets. The Table 1 summarizes the

key changes from this existing standard.

Table1DifferencesbetweenIndAS19andexistingstandardAS15(revised2005)

Constructive Obligations Ind AS 19 covers employee benets arising from constructive obligations. The existing standard does

not deal explicitly with the same. (Paragraph 3(c) of Ind AS 19)

Employees include all Direc- tors

As per the existing standard the term employee includes only whole time directors whereas under IndAS 19, the term includes directors. (Paragraph 6 of Ind AS 19)

Changes in Denitions The denitions of short-term employee benets, other long-term employee benets, and return on plan

assets and past service cost as per the existing standard have been changed in Ind AS 19. (Paragraph

7 of Ind AS 19)

F E A T U R E S

8/3/2019 Actuary India Oct 2011

http://slidepdf.com/reader/full/actuary-india-oct-2011 16/32

16 Indian Actuarial Profession Serving the Cause of Public InterestThe Actuary India October 2011

Multi-Employer Plan and

Contractual Agreement

Ind AS 19 deals with situations where there is a contractual agreement between a multi-employer plan

and its participants that determine how the surplus in the plan will be distributed to the participants (or

the decit funded). The existing standard does not deal with it. (Paragraph 32A of Ind AS 19)

Multi-Employer Plan and

Contingent Liabilities

Cross-reference to recognition of, or disclosure of information, of contingent liabilities (under AS 29), in

the case of multi-employer plans, appearing in the existing standard has been amended in Ind AS 19

as disclosure only, since, contingent liabilities should not be recognized (under Ind AS 37). (Paragraph

32 B of Ind AS 19)

Entities under Common

Control

As per Ind AS 19, participation in a dened benet plan sharing risks between various entities under

common control is a related party transaction for each group entity and some disclosures are required

in the separate or individual nancial statements of an entity. The existing standard does not containsimilar provisions. (Paragraph 34 B of Ind AS 19)

Actuary’s Involvement Ind AS 19 encourages (but does not require) an entity to involve a qualied actuary in the measurement

of all material postemployment benet obligations. The existing standard though does not require in-

volvement of a qualied actuary, does not specically encourage the same. (Paragraph 57 of Ind AS 19)

Asset Ceiling As per Ind AS 19, one of the limits for ‘asset ceiling’ is the total of (i) any cumulative unrecognized past

service cost and (ii) the present value of economic benets available in the form of refunds from the

plan or reductions in future contributions to the plan. As per the existing standard, the said limit is only

(ii) as above. (Paragraph 58(b) of Ind AS 19)

Financial Assumptions Ind AS 19 makes it clear that nancial assumptions shall be based on market expectations at the end

of the reporting period (for the period over which the obligations are to be settled). The existing stand-

ard does not clarify the same. (Paragraph 77 of Ind AS 19)

Negative Past Service Cost Ind AS 19 claries that negative past service cost arises when an entity changes the benets attribut-

able to past service so that the present value of the dened benet obligation decreases. The existing

standard does not clarify the same. (Paragraph 97 of Ind AS 19)

Curtailments Ind AS 19 provides the following clarications in the context of curtailments. (i) A curtailment may

arise from a reduction in the extent to which future salary increases are linked to the benets payable

for past service. (ii) When a plan amendment reduces benets, only the effect of reduction for future

service is a curtailment. The effect of any reduction for past service is a negative past service cost. The

existing standard does not provide these clarications.

Further Ind AS 19 requires ‘demonstrable commitment in respect of reduction in the number of employ-

ees’ as against the requirement of ‘present obligation’ in the existing standard. Also, the terms ‘mate-

rial reduction in the number of employees’ and ’material element of future service’ appearing in the ex-

isting standard have been replaced by the terms ‘signicant reduction in the number of employees’ and

’signicant element of future service’ respectively in Ind AS 19. (Paragraph 111 and 111 A of Ind AS 19)

Termination Benets Ind AS 19 provides more guidance on timing of recognition of termination benets. The measurement

criteria have also been expanded to deal with voluntary redundancy. The recognition criteria under the

revised standard differ from the criteria prescribed in the existing standard. (Paragraphs 133, 134 and

140 of Ind AS 19)

Recognition of Actuarial

Gains and Losses

Ind AS 19 requires recognition of the actuarial gains and losses in other comprehensive income, which

in turn to be immediately recognized in retained earnings. They should not be reclassied as prot or

losses in a subsequent period. The existing standard requires the recognition of the actuarial gains and

losses immediately in the statement of prot and loss as income or expense. (Paragraphs 92 and 93

of Ind AS 19)

Dened Benet Asset /

Minimum Funding Require-

ment

Appendix A of Ind AS19 provides guidance on the Limit on a Dened Benet Asset, Minimum Funding

Requirements and their Interaction. This provision compares with the IFRIC 14 of the IASB. This guid-

ance is not available in the existing standard. (Appendix A of Ind AS 19)

Inter Valuation Period The existing standard says that the detailed actuarial valuation may be made at intervals not exceeding

three years unlike Ind AS 19.

Ind AS 19 Impact for the Companies

The above changes and clarications in

the Ind AS 19 will help the companies

improve their disclosure and better align

with their IAS 19 reporting if any. The

signicant impact for the companies

would be:

• Inclusion of Directors: Thecompanies would now need to

include part time directors. Though

they could be few in numbers, their

pension cost could be signicant.

This would increase the expense

and the net liability provisions.

• Actuarial Gains and Losses: The

actuarial gains and losses will now

be immediately recognized in the

other comprehensive income and

not ow into the prot and loss. This

will remove the volatility in the prot

and loss which in turn improves

the credibility and understanding

of the nancial statements by

the investors. This will also help

achieve closer compatibility with the

amended IAS 19 as the amended

standard has similar provisions. The

other comprehensive income would

be adjusted against the retained

earnings and the net liability

provisions in the balance sheet

would not change.

• Termination Benets: The timing of

recognition of termination benets

including voluntary redundancy

could potentially impact the

expenses if there is a termination or

redundancy plan.

F E A T U R E S

8/3/2019 Actuary India Oct 2011

http://slidepdf.com/reader/full/actuary-india-oct-2011 17/32

17Indian Actuarial Profession Serving the Cause of Public Interest The Actuary India October 2011

F E A T U R E S

• Asset Ceiling: The cumulative

unrecognized past service cost

could now be included in the assets

which could potentially lower the net

liability for companies who have such

a provision.

The impact would be uniform across all

the sectors of the business. However the

impact would be higher for companies

who have consistently and signicantlyunder / overestimated their assumptions

such as salary increases or withdrawals.

The actuarial gains or losses from such

an under / overestimation will not ow

through the prot or loss as per Ind AS

19 and hence would have a signicant

impact in their reported prot or loss

gures.

IndAS19comparisonwiththeexisting

standard IAS 19

IASB issued the accounting standardIAS 19 for Employee Benets originally

in 1983. This has been amended

subsequently many times, the last

signicant amendments being in

December 2004 and June 2011. IAS

19 applies to all employee benets

offered by an employer to employees

and their dependents and beneciaries.

The Table 2 captures the signicant

differences between Ind AS 19 as

notied by the MCA and the existing

standard IAS 19 in practice (before June2011 amendment).

Table 2 Differences beteen Ind AS 19 and IAS 19 (before June 2011 amendment)

Topic Ind AS 19 IAS 19

Actuarial Gains and

Losses

Ind AS 19 provides a single option for recognition of