activity report 2008 a pessimist sees the … · activity report 2008 a pessimist sees the...

TRANSCRIPT

ACTIVITY REPORT 2008

A pessimist sees the difficulty

in every opportunity.

An optimist sees the opportunity

in every difficulty.

Sir Winston Churchill

We see the opportunities.

Pierre Lebeau

Marc Ooms

Jean Peterbroeck

Pascal Minne

Michel Peterbroeck

Geoffroy d’Aspremont Lynden

Marc Janssens

Erik Verkest

Dirk Van den Broeck

Xavier Van Campenhout

Guy Lerminiaux

Fritz Mertens

Philippe de Broqueville

Eric Struye de Swielande

Johnny Debuysscher

Bart Tishauser

1

1

2

3

5

4

6

7

8

9

10

11

13

12

14

15

16

7

12 13 1415

16

8

10 119

2 3 4 5 6

PETERCAM � activity report 2008 11

LETTER FROM

THE PARTNERS 3

KEY FIGURES 7

FIELDS OF EXPERTISE

Institutional Sales & Research 9

Corporate Finance 13

Private Banking 17

Institutional Asset Management 21

Petercam Private Projects 27

Estate Planning 29

Compliance & Risk Management 31

Macro & Buy-side Research 35

PETERCAM PEOPLE 37

ADDRESSES 38

Table of ContentsTABLE OF

CONTENTS

When written in Chinese,

the word "crisis" is com

posed

of two characters.

One represents danger

and the other represents

opportunity.

John F. Kennedy

PETERCAM � activity report 2008 33

Letter from the PartnersLETTER FROM

THE PARTNERS

Fellow Clients and Colleagues,

The year 2008 was definitely an historic year for the worldwide economy, for the financial markets and

therefore for all investors. Started in the summer of 2007, the subprime crisis became a global credit crisis.

Its contagion on all sectors and the magnitude of its impact have surprised and shaken up the most

experienced investors, business leaders and analysts. Belgian financial institutions have been hit particularly

severely in the current crisis and all the big commercial banks in our country had to rely on government

aid on an unprecedented scale. As of today, some of them continue to search for a stable framework.

On the back of these events it is no surprise that the five-year growth period has been interrupted in 2008,

also at Petercam. According to Belgian GAAPS, we ultimately realized an operating income of 193 million

euro and a current profit before taxes of 60 million euro. Taking into account all negative impacts of the

financial crisis, we ended the year with a net profit for the group of 33 million euro, 65% down compared

to the record year 2007.

The shareholders’equity and hence the solvability and creditworthiness of the group have not been affected

by the crisis. Traditionally, Petercam uses its core equity to finance the operating needs of its international

affiliates and places its excess capital in a very conservative way through bank deposits, treasury bills and

similar instruments. Hence, and notwithstanding the financial turmoil, shareholders’ equity remained stable

at 130 million euro.

Overall, and taking into account the tsunami of alarming financial figures that we have seen elsewhere in

the financial sector, we are more than satisfied that our firm was able to offer such a resistance. Because,

it is in the interest of all our stakeholders – be it staff, clients, suppliers or shareholders – that our firm

proves to be financially strong and resistant even in the most extreme economic environment.

The robustness and strength with which Petercam put up a stubborn defence against this historic period,

shows the success of our model. During its 40 years in existence, Petercam, its partners and staff have

always remained loyal and securely anchored to the pillars upon which the company was founded:

independence of spirit and ownership, internationalization in its natural markets, the relationship of

proximity which puts the client at the heart of priorities, and finally innovation in its work processes and

its services and products.

These are the values which have forged the reputation of Petercam. They enabled us in the past to generate

our growth, and comfort us in the current turmoil that our corporate strategy, based on these values,

continues to be the right way forward. Asset management, corporate finance and brokerage remain at the

core of Petercam, with the focus on research as common driver. All ideas and recommendations we give

to our clients are the result of in-depth analysis. We continue to invest strongly in buy-side and sell-side

research. Numerous international awards and the prominent presence of sophisticated international

investors within the client-base of our activities reflect the quality of this service. We work hard every day

to deserve their trust.

As we are optimists, we see the opportunity in the current difficult market circumstances. In the eye of the

storm, actions to strengthen our systems were triggered: we reinforced our internal audit and risk

management services, we brought in new skills and upgraded our investment teams, we invest in a state-

of-the-art IT platform, we inform our clients in a transparent way through information sessions and

seminars, and we adapted our decision-taking process allowing us to react even faster to the business

opportunities surrounding us.

The stability of our teams allows us to build a long-term relationship with our clients, which is key to better

understand their needs.

At the end of 2008 and at the age of 67, Pierre Drion, who was partner since almost 40 years, retired. His

decision was taken three years ago and Pierre Drion prepared with care his succession. He played a crucial

role at the different stages in the development of Petercam from a pure brokerage house in the seventies

towards the full-fledged investment bank and asset management firm it is today. The partners thank him

for his unparalleled contribution throughout his entire career. We are pleased that Pierre Drion agreed, as

a non-executive director of our group, to continue to support the growth and commercial development of

the firm.

Geert Noels, partner since 2003, who operated as chief economist of the group, decided early 2009 to

leave the company as he wants to discover new challenges in his professional career. We wish him every

success in his new endeavours.

In order to reinforce the partnership, Petercam has the pleasure to welcome Axel Miller as a new partner

as from June, 2nd 2009 onwards. Axel Miller, formerly CEO of Dexia Bank and Dexia Group, is 44 and has

an extensive experience as corporate lawyer and top banker. His legal background and his expertise in

financial matters will allow the group to improve its competences, both managerially and technically.

Conclusion

Despite the financial turmoil, our performance in 2008 was solid and reassuring. Throughout the crisis, we

managed to take the necessary measures and to attract the right people to strengthen our organization.

We are optimistic about our future. Our experience accumulated over more than 40 years and our focus,

especially on our clients’ needs, are the best guarantee for a continuation of our success.

We thank you all, clients and colleagues, for the trust and commitment you put into us.

4 activity report 2008 � PETERCAM

PETERCAM � activity report 2008 55

PARTNERS

MANAGING DIRECTORS (*)

Michel Peterbroeck

Dirk Van den Broeck

Marc Ooms

Eric Struye de Swielande

Fritz Mertens

Pierre Lebeau

Marc Janssens

Philippe de Broqueville

Johnny Debuysscher

Guy Lerminiaux

Pascal Minne

Geoffroy d’Aspremont Lynden

Erik Verkest

Xavier Van Campenhout

Bart Tishauser

CHAIRMAN AND VICE CHAIRMAN OF THE BOARD

Jean Peterbroeck

Petercam et Associés SCRL

NON-EXECUTIVE DIRECTORS

OF GROUP COMPANIES

Pierre Drion

Baudouin du Parc Locmaria

Philippe Huens

(*) Axel Miller as from June 2, 2009.

HONORARY PARTNERS

Jean Peterbroeck

Etienne Van Campenhout

André de Halleux

Pierre Van Dessel

Alain Camu

Georges Caballé-Munill

Léopold d’Oultremont

William Vanderfelt

Philippe Huens

Baudouin du Parc Locmaria

Alexander de Groot

Pierre Drion

Geert Noels

EXECUTIVE DIRECTORS

OF GROUP COMPANIES

Jean-François Bécu

Thijs Berkelder

Christian Bertrand

Philip Bille

Michel Casselman

Marc Debrouwer

Hans de Jonge

Philip De Ridder

Lode De Vrieze

Damien Fontaine

Francis Heymans

Sylvie Huret

Jean de Lambertye

Bertrand Marot

Geoffroy Vermeire

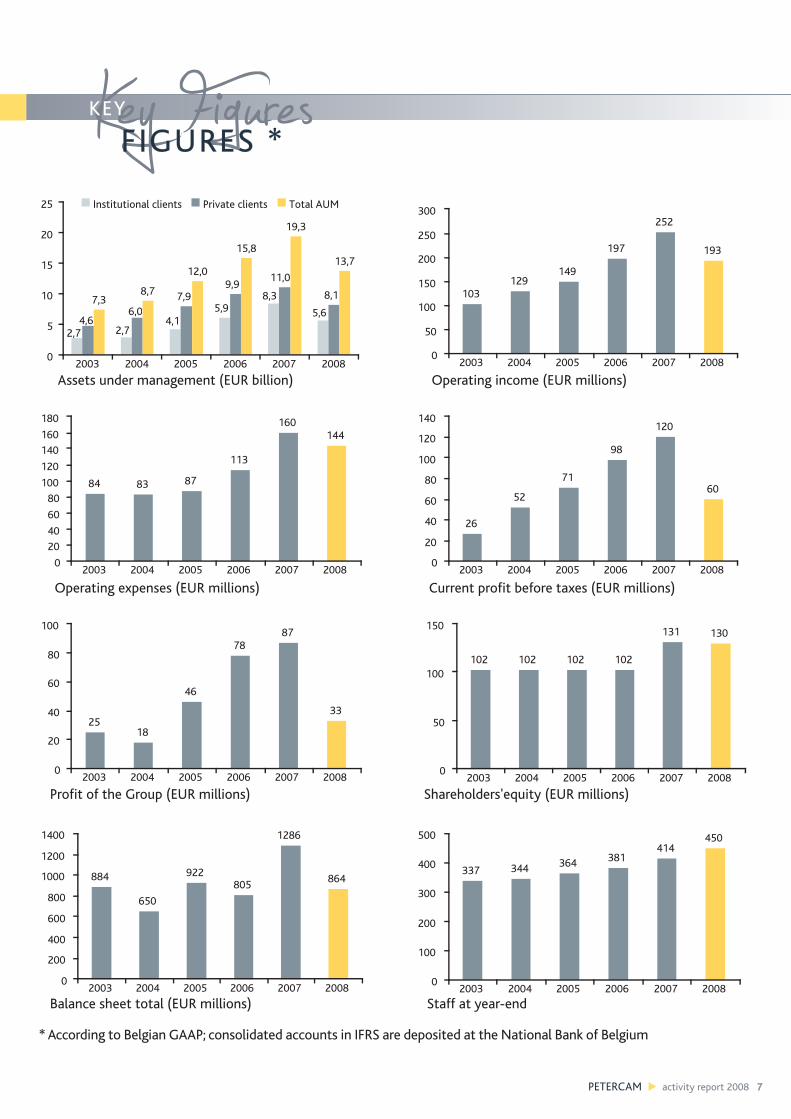

Key Figures

PETERCAM � activity report 2008 77

Key Figures KEY

FIGURES *

7,38,7

12,0

15,8

19,3

13,7

2,7 2,74,1

5,98,3

5,6

8,1

11,09,9

7,96,0

4,6

0

5

10

15

20

25

2003 2004 2005 2006 2007 2008

Institutional clients Private clients Total AUM

84 83 87

113

160144

0

20

40

60

80

100

120

140

160

180

2003 2004 2005 2006 2007 2008

26

52

71

98

120

60

0

20

40

60

80

100

120

140

2003 2004 2005 2006 2007 2008

2518

46

7887

33

0

20

40

60

80

100

2003 2004 2005 2006 2007 2008

884

650

922805

1286

864

0

200

400

600

800

1000

1200

1400

2003 2004 2005 2006 2007 2008

102 102 102 102

131 130

0

50

100

150

2003 2004 2005 2006 2007 2008

Assets under management (EUR billion)

Operating expenses (EUR millions)

Profit of the Group (EUR millions)

Balance sheet total (EUR millions)

337 344 364 381414

450

0

100

200

300

400

500

2003 2004 2005 2006 2007 2008

Staff at year-end

Shareholders'equity (EUR millions)

103129

149

197

252

193

0

50

100

150

200

250

300

2003 2004 2005 2006 2007 2008

Operating income (EUR millions)

Current profit before taxes (EUR millions)

* According to Belgian GAAP; consolidated accounts in IFRS are deposited at the National Bank of Belgium

The difference between per

formance

and outperformance often co

mes

down not to what you buy,

but how you buy it.

Jim Cremer

PETERCAM � activity report 2008 99

Institutional Sales and ResearchINSTITUTIONAL SALES &

RESEARCH

OUR SERVICES

Petercam has for many years been the number one

independent broker on Belgian listed companies. Ten

years ago we started to expand our activities in

brokerage towards the Dutch market. Today as a

member of NYSE-Euronext, we offer an extensive

broking service on the entire Benelux region, based

on in-depth research on all listed Benelux-

companies with a strong emphasis on the local

added value. Institutional investors appreciate the

quality of our services in addition to their global

brokers.

We have a well-established sales force in Brussels,

Amsterdam and New York, which maintains close

contacts with a strong domestic and foreign

institutional client base spread in most of the core

countries of the world. This large domestic and

foreign client base gives us one of the strongest

placing capabilities for Benelux equities.

A team of 15 sell-side financial analysts mainly

specialised by sector offers top-quality research not

only on Benelux blue chip companies but also on

small and mid cap firms, which face lower visibility.

A highly specialised trading team, operating from

both Brussels and Amsterdam, continuously

monitors the market of those small and mid-

capfirms in an order to optimise liquidity for those

stocks.

Petercam has always been the leading specialist of

the Brussels Stock Exchange, but in view of the rapid

internationalisation of the financial markets, our

trading team has developed a pan-European

platform, a combination of direct trading accesses

and dealing relationships in different countries. Our

main focus remains the Paris-Brussels-Amsterdam

axis, symbolised by our NYSE-Euronext Stock

Exchange membership. Last year, we upgraded our

trading platform to allow us to be MIFID-compliant.

For many companies listed on Euronext, Petercam

acts as a corporate broker whose roles are (a) to

enhance the liquidity and reduce intra-day volatility

through a permanent presence in the market, (b) to

increase through constant research and marketing

efforts the knowledge of the company among

international and domestic investors, and (c) to

inform the company of the market evolution of its

share.

The bond desk provides institutional investors with

first-class advice on and access to sovereign and

corporate debt markets across the Euro-zone.

Institutional

Sales

Institutional sales & research

Research Derivatives Fixed

IncomeTrading

10 activity report 2008 � PETERCAM

A specialised model, based on local expertise, is our

effective answer to the growing competition from

the global houses.

RESEARCH AT THE CORE OF BROKERAGE

By covering more than 140 companies, Petercam’s

sell-side research team offers the broadest coverage

of all brokers operating on the Benelux market.

However, our research team is not only the number

1 in terms of quantity but also in terms of quality.

This was highlighted by its election at the top of the

lists of almost all the brokerage surveys that were

carried out in the Benelux.

More particularly the top ranking for the Benelux in

both the surveys organised by Institutional Investor

and Extel highlights Petercam’s sell-side research

quality. These surveys result from interviews with

the leading international institutional investors and

hence we consider them as a vote of confidence by

our clients. All the more as Petercam ranks in these

surveys systematically in the top-three for the

quality of its overall research on the Benelux area,

for its specialised research on small- and midcap

companies, and for the quality of its overall sales

service.

This outstanding performance is realized by a team

of experienced analysts. Most of these analysts have

between 5 and 25 years of sell-side research

experience. The experience and stability of the team

are regarded as our key quality differentiators. Half

the team is located in Brussels, half of it in

Amsterdam. This local presence offers Petercam a

crucial information edge compared to global players.

Knowing the local political, social, management and

networking issues and structures provides crucial

input for high quality research.

MARKET FACTS AND TRENDS 2008

2008 will be remembered as a difficult year on the

financial markets.

The subprime crisis which started in 2007 turned

into a major credit crunch in 2008 with devastating

domino effects on both the equity and the credit

markets. The crisis reached its climax in the fall in

the aftermath of the collapse of Lehman-Brothers

on September 16, which sent the VIX-Index (“fear

gauge” of the equity markets) to an all-time high of

97.

The systemic risk of the banking sector became the

dominant fear, interbank rates soared and the

markets for many asset classes were “de facto”

closed because of lack of liquidity. Belgium came

into the spotlight with the Fortis saga. The

governments had to come to the rescue of the

financial sector with major plans to restore

confidence in the system. The Dow Jones Banks

Index nevertheless plunged 64% and ended 2008

close to its low. The DJ Euro Stoxx 50 (price) closed

at 2,447.62, a whopping 43.6% freefall. Such a

dismal performance has not been seen since the

great depression of the 30’s. No wonder the Bel 20,

heavily weighted towards bank shares, was severely

punished: the index lost 54% and the AEX Index

dropped 51%.

Relatively strong outperformers in the BEL-20 index

were Colruyt (-4.52%), Befimmo (-8.20%) and

Mobistar (-10.42%). On the AEX, Ahold (-7.76%),

Wereldhave (-15.69%) and KPN (-15.56%)

outperformed.

Strong underperformers in Belgium were Fortis (-

94.84%), Dexia (-81.43%) and KBC (-77.70%)

whereas in the Netherlands Tom Tom (-89.90%),

PETERCAM � activity report 2008 111

ING (-72.60%) and Arcelor (-67.94%) were the

worst hit.

At the AEX review, Corio, Fugro, BAM, USG People

and Wereldhave joined the index whereas Corporate

Express, Hagemeyer, Vedior and ABN Amro were

removed.

In 2008, the Belgian Index added Nyrstar as a

component (0.36% weight); Suez became GDF Suez

and increased its weight (19% to 23.68%).

2008 brought significantly lower volumes. Average

daily equities volumes (single count) on the Bel 20

stood at 536.01 million (-14%). The trend was more

pronounced on the Dutch market since average

daily equities volume (single count) reached

2726.46 million, down 34.27%.

PETERCAM INSTITUTIONAL BONDS

Much of our work in the institutional bond markets

over the last 12 months has been based around

finding out what needs to happen to get us back to

a world that was last normal.

Effectively, liquidity was the hot key for corporates

in 2008 while bond markets stayed erratic and

discriminating.

The investor base looked to safer credits and/or very

wide spreads. Issuing corporates accepted these

market conditions and were prepared to issue at the

prevailing market levels.

It was a very difficult environment for investors to

make money. Traditional fundamental analysis was

replaced by analysis of which issuers looked

vulnerable and would be allowed to fail, or what any

type of bail-out might look like.

The global recession was all but unavoidable. A

weak economy and deflation impelled the Fed to

cut interest rates to unprecedented levels (from

4.25% to 0.25%). A sudden shift by the ECB (from

4.00% to 2.50%) occured later in the year.

Very poor market liquidity was given us the

opportunity to increase our dealing revenues in our

specialized niches with more than 65% compared

to 2007. This record amount has demontrated the

benefits of our personalized brokerage approach

developed over the last 15 years.

Electronic trading platforms have shown their

limitations, as pricing and dealing through these

systems have been poor.

With the economy continuing to slow, the focus on

supporting a variety of issuers/asset classes is likely

to continue. The impact of these developments on

the investment process will be critical during 2009.

We are all faced with

a series of great

opportunities brilliantly

disguised as impossible

situations.

Charles R. Swindoll

PETERCAM � activity report 2008 113

THE MARKET

Global Corporate Finance activities suffered

considerably in 2008 from the subprime crisis and

from the deteriorating economy. As one could

expect, the negative environment impacted Equity

Capital Markets transactions as well as M&A

activities in the Benelux, particulary in the second

semester of 2008.

According to Mergermarket, completed M&A

transactions involving Benelux companies

amounted to EUR 177 billion (-20% versus 2007).

Major transactions were the take-over of Anheuser-

Busch by Inbev for an amount of 36,8bn EUR, the

acquisition of Distrigas by ENI (4.8 bn EUR) and the

take-over of Vedior by Randstad (4 bn EUR).

The main Private Equity transactions were the buy-

out of TMF Group, an Amsterdam-based group of

management and accounting outsourcing services,

by Doughty Hanson for 750m EUR and the take-

over of Schuitema by CVC for 253m EUR.

Capital markets recorded few noteworthy transac-

tions. On Euronext Amsterdam, the IPO of Liberty

International raised 600m EUR in February whereas

a few small size IPO’s were recorded in Brussels such

as 4Energy Invest and Immo Moury. On Euronext

Brussels however Inbev managed in this difficult

context to raise 6.36 bn EUR through a rights issue

at a deep discount to refinance part of the acqui-

sition of Anheuser-Busch.

In this context, Petercam’s Corporate Finance team

managed to complete significant M&A related assign-

ments with several capital market transactions.

� M&A

The main transactions advised by Petercam in 2008

were the following:

� Through an LBO transaction MMitiska / Sofindev

took over CCassis and Paprika, a group active in

the retail distribution of textile clothing for

women, together with its management.

Petercam acted as advisor to the shareholders of

Cassis and Paprika

� Telenet, the listed provider of telecom-

munication services closed the acquisition of the

analogue and digital client base of a number of

pure inter-municipalities (PPBE, Integan,

Intermedia, WVEM and Interkabel). The total

deal value was estimated to be around

EUR 427 million, including the value of a long

term lease agreement. Petercam acted as advisor

to Telenet

� Petercam advised SSolvay Pharma in the

acquisition of diagnostics company

Innogenetics. After assisting Solvay Pharma in its

negotiations with Innogenetics co-founder and

main shareholder, Petercam organised the

voluntary public take-over bid on Innogenetics,

which was successfully concluded with Solvay

Pharma owning 100% of the shares. The total

value of the transaction was EUR 201m

� The founding families of CCTB Magemon sold

75% of this leading specialty dry bulk and

general cargo port operator at the inland ports

of Liege and Charleroi to BBenelux Port Holdings,

a vehicle controlled by Babcock and Brown

Infrastructure. Petercam acted as advisor to the

shareholders of CTB Magemon

Corporate FinanceCORPORATE

FINANCE

14 activity report 2008 � PETERCAM

� Petercam advised the shareholders of LLa

Corbeille Groep, a family-owned Belgian

producer of shelf stable food products, in the

sale of their company to the French Group

Bonduelle.

� t-groep, a Belgian staffing services provider,

realized its first foreign acquisition. The company

took over the share capital of LLuba, a

Netherlands based staffing company. Luba is

active in temporary services, as well as

outsourced logistic services. Petercam acted as

financial advisor to t-groep, with the active

collaboration of its Corporate Finance teams in

Brussels and Amsterdam.

� Advice to the Flemish Region

Petercam was appointed as advisor to the Flemish

Region for the financial restructuring of several

important Belgian financial institutions. This mission

included inter alia assistance in valuation of assets,

analysis of possible solutions and in the structuring

of the transactions.

� Ethias came under public scrutiny and had to

cope with a deteriorating solvency and liquidity

situation. The Federal, Flemish and Walloon

governments agreed to jointly increase Ethias’

capital by EUR 1.5 billion (EUR 500 million each).

� Dexia, the Belgo-French banking and insurance

group, had to cope with deteriorating liquidity

and with significant pressure on its share price.

This led the governments of Belgium and France,

together with the Belgian Regions and Dexia’s

stable shareholders to recapitalise the group

with EUR 6 billion of fresh equity.

� Gemeentelijke Holding / Holding Communal, a

holding company comprising inter alia a 14%

participation in Dexia and owned by the Belgian

communities, was facing possible collateral

problems due to the decline of the Dexia share

price. The Federal, Flemish, Walloon and Brussels

governments decided to jointly grant a

guarantee to the Gemeentelijke Holding/

Holding Communal for a total of EUR 800

million.

� Equity capital markets

Reflecting the overall difficult environment in the

capital markets, our activity in ECM significantly

decreased vs. 2007.

� Petercam co-organized the IPO of 44Energy

Invest, a clean energy producer operating a

portfolio of biomass projects including

cogeneration units and solid biofuels and raised

EUR 22m new equity. Petercam acted as co-lead

manager.

� Petercam organised the replacement of several

blocks of listed biotech shares:

� Petercam united a group of investors to

purchase an 11% stake in TThromboGenics

with the intention to form a stable reference

shareholder base. ThromboGenics is a

Belgium-based biopharmaceutical company

focused on the development of therapeutics

for conditions related to the vascular system.

� Petercam placed 2,2% of the capital of

Tigenix, a biotech group active in the field of

cell therapy for cartilage repair, in the hands

of institutional investors.

PETERCAM � activity report 2008 115

� Private Placements

Due to the shut down of the IPO window, several

companies sought to raise cash through private

placements. In this context, Petercam assisted

Cardio3, a specialist of cell therapy for the

regeneration of heart tissue in raising EUR 7,2m new

equity.

� Corporate Finance advisory

Petercam advised DDEME and NNuhma as shareholders

of CC-Power, the first offshore wind park in Belgium,

after co-shareholders Ecotech and Socofe made

clear their intention to reduce their stake in the

park. Petercam’s mission included a valuation of the

park and advice on the right of first refusal and tag-

along right owned by DEME and Nuhma.

The Walloon government through SSOWAER decided

to open the capital of BBrussels South Charleroi

Airport (BSCA), the operator of Wallonia’s main

regional airport, to a private partner by selling a

27,65% stake and a call option on another 21%.

Petercam provided a fairness opinion to the Board of

SOWAER regarding the valuation and the conditions

of the binding offers.

Put not your trust in money,

but put your money in trust.

Olivier Wendell

PETERCAM � activity report 2008 117

OUR SERVICES

Our Private Banking division includes investment

and estate planning services to private individuals,

families and trusts. As of December 31 2008, the

total assets managed for private individuals

amounted to EUR 8.1 billion, which represents a

decrease of 25% over the previous year. This

decrease in assets under management is almost

exclusively the result of the negative performance

of the markets in 2008. New client acquisitions

managed to completely offset the low number of

client departures over the year.

Given the different risk profiles of our clients and

our increasingly large global product offering, this

service has become more than ever tailor-made. We

offer either discretionary, advisory or personal

management services.

Within discretionary management clients give an

investment mandate to Petercam specialists,

allowing them to execute in the best interests of

their clients customized strategies for the

management of their wealth. We believe that

Petercam is currently the only player in the Belgian

market to offer a real tailored approach: all clients

have the ability to give continuous input on how

their portfolio ought to be managed, including

personal preferences with regard to investment

product types or even individual securities.

Within advisory management the Petercam

portfolio manager acts under constant interaction

with the client in view of taking all necessary and

appropriate actions in full agreement. By definition

this service is tailored and because of our experience

and our competence we provide first-class services

within this segment.

Within personal management the client takes all the

investment decisions himself and Petercam limits

its role to the execution and the administrative

follow-up. Naturally, should they request it, we can

provide help to clients with regard to their

investment decisions. Due to our traditional close

links with the financial markets, we are ideally

placed to service this type of clients. We have the

knowledge, the experience and the culture to

provide the best possible execution of private

clients’ orders.

Our Private Banking services within Belgium are

offered from offices in Brussels, Antwerp, Ghent,

Hasselt, Knokke, Liège and Roeselare. Furthermore

our branches in Luxembourg, Geneva, Amsterdam,

Rotterdam and Paris offer Private Banking services

to both on- and offshore clients. Despite the difficult

circumstances of 2008, we have refrained from

cutting staff numbers. In some offices we have even

added new talent, thus confirming that we continue

to invest in Private Banking by further increasing our

capabilities in this activity. Our existing staff stayed

loyal to our company during this difficult period.

They have worked extremely hard in what can only

be described as depressed markets in order to

protect our clients from losses and to stay in

constant communication with them. For these

extraordinary efforts we wish to thank them.

We believe that we have a unique position within

the Private Banking market through a highly

personalised approach. This is a strong reality at

Petercam, which allows us to create a competitive

advantage. Furthermore there is a close relationship

between our clients and their portfolio managers.

These strengths will allow us to remain one of the

strongest players in this market. Private Banking is

one of the core activities of Petercam, and we will

Private BankingPRIVATE

BANKING

18 activity report 2008 � PETERCAM

continue to develop it further in the future. We

experience continued recognition both by older as

well as newer clients of our business model. To

summarise our approach, we put the client at the

centre of attention of our stable, dedicated and

experienced team.

PETERCAM IN THE MARKETS

The year 2008 will be remembered as one of the

worst financial years in history. Stock exchanges

over the world plunged to levels not seen since the

last ten years. Corporate bonds provided no shelter

and liquidity in this market dried up. Banks which

were crucial to the functioning of the economic

system were close to failing and needed

government aid to stay in business. At the end of the

year the atmosphere in the market was such that

the doom scenario of a repeat of the thirties of the

last century seemed almost inevitable.

It is no surprise that working as a Private Banker in

such an environment was not easy. Even though we

were already cautious as far back as 2006 in our

asset allocation, the severity of the downward move

was deeper than expected. The biggest problem

during 2008 was not so much the severity of the

crash, but the fact that there were very few places to

hide. Except for cash, government bonds and to a

lesser extend gold, all asset classes suffered severe

losses.

The fixed income part of our client portfolio’s was

almost exclusively managed through our proprietary

bond funds. We have developed a special skill in

corporate bonds and higher yielding bonds. These

bonds suffered from severe corrections in 2008,

especially in subordinated financials and lower grade

corporates. In these particular products spreads

between bid and offer prices increased to levels

never seen before, which meant that restructuring

these portfolio’s proved extremely difficult. By the

end of the year we managed to bring back the bond

part of our portfolio’s in line with our expectations.

Within our equity allocation we have remained

cautious over the whole year, thus avoiding major

losses for our clients. We have been negative on

financials, thus preventing clients from having major

exposure to the banking stocks which were most

heavily affected by the banking crisis. Our focus

remained on specific themes for which we see a

long-term potential. The hedge fund industry

however was faced with massive redemption

demands, thus being forced to sell all types of

investments, even good ones with long term

potential. This is the main reason why our theme

approach, even though we remain convinced of its

prospects for the future, suffered equally through

the crisis.

In 2008 Petercam has continued to create and

develop tailor-made private equity offerings to our

clients, however at a slower pace. Petercam Private

Projects (“3P”) has been created with a view to

offering products with no correlation with the more

traditional asset classes to our HNWI clients. Some

of these products resisted well with regards to the

more traditional markets.

Even though we suffered the first decrease in assets

under management in seven years, we remain very

efficient and cost conscious. This means that Private

Banking again made a significant contribution to our

net income.

In 2008, we placed our operational focus exclusively

on our clients. Our staff has worked continuously

with only one aim, providing excellent service to our

clients despite the difficult circumstances. Whether

it was through direct communication, managing and

restructuring their portfolio, investigating new

PETERCAM � activity report 2008 119

investment ideas or helping clients better structure

their wealth, all our energy went into helping them

get through this difficult period.

Even though the first months of 2009 have proved

equally challenging, we are starting to see some

silver lining to the clouds. The measures taken by

the governments all over the world are starting to

bear fruit and the volatility in the markets is starting

to recede. Private Banking at Petercam is well

positioned, through its qualified and experienced

staff, its market knowledge and the loyalty of its

clients, to find new opportunities in the market and

to enjoy the huge success it has had in the past.

SPECIAL INVESTMENT ADVICE

Petercam has a long tradition of offering direct

access to global markets to high net worth

individual clients. Taking advantage of Petercam’s

strength in market-related contacts and focus on

special situations, we have developed a specialized

investment advice service. Petercam ‘s direct and

opportunistic approach to the financial markets and

its capacity to analyze the facts in a changing

environment have resulted in a significant increase

in the number of high net worth clients asking for

personalized approach of their portfolio.

With the global downturn of the second part of last

year, the HNWI desk has been able to offer

appropriate solutions for individual clients wishing

to restructure their holdings. Depending on

particular situations, we have been active in equities,

corporate and state guaranteed bonds as well as in

funds, through our third-party funds selection

process.

We strongly believe special attention will be given in

the future to market timing, trend changes, volatility

and liquidity. By understanding the available

indicators, we are able to help clients implement a

suitable asset allocation and to benefit from the

best trading strategies.

Without the stre

ngth to

endure the cri

sis, one will

not see the o

pportunity with

in.

It is within the

process

of endurance

that

opportunity re

veals itself.

Chin-Ning Chu

PETERCAM � activity report 2008 221

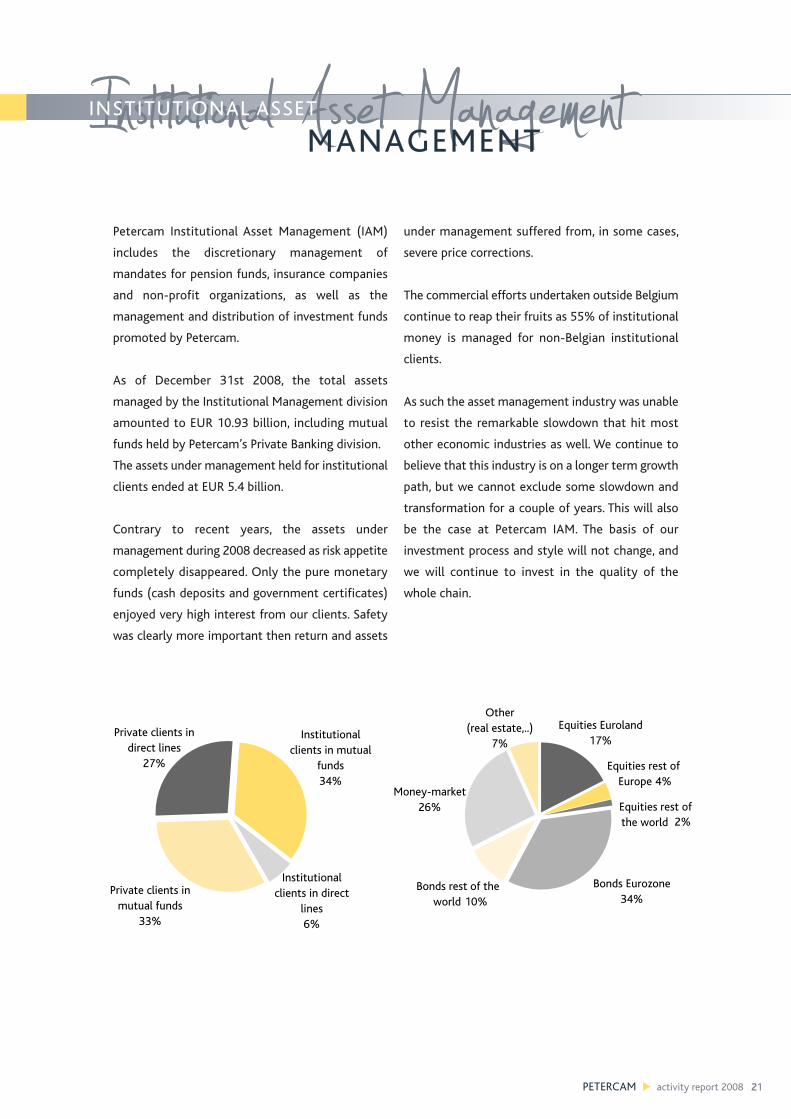

Petercam Institutional Asset Management (IAM)

includes the discretionary management of

mandates for pension funds, insurance companies

and non-profit organizations, as well as the

management and distribution of investment funds

promoted by Petercam.

As of December 31st 2008, the total assets

managed by the Institutional Management division

amounted to EUR 10.93 billion, including mutual

funds held by Petercam’s Private Banking division.

The assets under management held for institutional

clients ended at EUR 5.4 billion.

Contrary to recent years, the assets under

management during 2008 decreased as risk appetite

completely disappeared. Only the pure monetary

funds (cash deposits and government certificates)

enjoyed very high interest from our clients. Safety

was clearly more important then return and assets

under management suffered from, in some cases,

severe price corrections.

The commercial efforts undertaken outside Belgium

continue to reap their fruits as 55% of institutional

money is managed for non-Belgian institutional

clients.

As such the asset management industry was unable

to resist the remarkable slowdown that hit most

other economic industries as well. We continue to

believe that this industry is on a longer term growth

path, but we cannot exclude some slowdown and

transformation for a couple of years. This will also

be the case at Petercam IAM. The basis of our

investment process and style will not change, and

we will continue to invest in the quality of the

whole chain.

Institutional Asset ManagementINSTITUTIONAL ASSET

MANAGEMENT

Bonds rest of the world 10%

Money-market26%

Other(real estate,..)

7%

Bonds Eurozone34%

Equities rest of the world 2%

Equities rest of Europe 4%

Equities Euroland17%

Private clients in mutual funds

33%

Private clients in direct lines

27%

Institutionalclients in mutual

funds34%

Institutionalclients in direct

lines6%

22 activity report 2008 � PETERCAM

MARKET FACTS AND TRENDS 2008

The combination of a banking crisis followed by an

economic crisis, which itself exacerbated the

banking problems, hit the financial markets with full

force during 2008. This “perfect storm” was so

powerful that all financial markets became

correlated to a very high degree and a kind of “black

swan” developed. Something that started as a

problem apparently easy to manage in 2007, the

sub-prime contagion, estimated at around 150

billion USD, became an earthquake beyond

imagination, during which several tens of trillions of

USD have been lost. Something that only happens

once in a century hit all risky assets severly and

investors ran for coverin an unprecedented way.

It is not a surprise that in such a context, risk

appetite has not been rewarded. On the contrary.

2008 was therefore a very atypical year and the

Volkwagen saga probably best illustrates the

dislocation of financial markets in general, both for

equities and for fixed income. This flight to safety

and liquidity has also been witnessed for

government bonds, whereby German bunds profited

from their safe haven status at the expense of

weaker Euro members.

During 2008, two otherwise neglected risks have

been rediscovered: liquidity and counterparty risk.

Liquidity, once taken for granted and a cornerstone

of modern liberal and global capitalism, in some

cases completely disappeared. In certain markets

such as corporate bonds and small cap stocks, forced

selling caused major havoc as the underlying

liquidity disappeared. Going forward, investors will

be asking a premium or pay more expensively for

liquidity. We also believe that organized and

centralizing markets (such as stock exchanges) have

a role to play in replacing other players such as

banks or less regulated OTC markets. More

transparency and regulation are needed to win

investors’ confidence back. It will be a slow process,

but it will change the fundamentals of our industry.

The collapse of Lehman Brothers sent a shockwave

through the whole economy. All market participants

rediscovered the importance of “quality of the

counterparty”. More regulation, better oversight,

stronger balance sheets, less leverage, higher margin

calls, etc. will be the consequences of and the price

to be paid for taking this risk into account. The world

will not be the same anymore and certain segments

of the market, such as hedge funds and issuers and

investors in complicated derivative products and

structured products in general, have to think about

their business model as it was previously based on

assumptions that are no longer valid.

To make things even worse and perhaps as a sign of

the times, investors’ confidence has been further

eroded by a number of scandals and fraud. The

Madoff case dealt a blow to the fund of hedge funds

industry. At Petercam, we decided in September

2008 to eliminate our hedge fund exposure in our

two Irish domiciled funds: Petercam Growth and

Petercam Arbitrage. Here as well, we took into

account the changing landscape to divest from the

hedge fund space. It is not excluded that, under one

form or another, hedge funds in general will make a

come back. In the meantime, we have adopted a

wait and see attitude.

PETERCAM � activity report 2008 223

PETERCAM IN THE MARKETS

The performances of Petercam IAM were below

average during 2008. For years in a row, IAM

performed above average, both compared to the

benchmarks and when compared to its peers, due

to the combination of successful stock and bond

picking, often with a “small cap” bias and with less

barriers to enter into somewhat less liquid

strategies.

This investment style was underpinned by top down

considerations or investment themes such as the

China based global growth story, a reasonable

decoupling potential from US economic weakness

and the positive effect from the European

convergence trends. This enabled IAM to offer good

equity based performances and to develop some

appealing investment products for its clients. Even

though we remain convinced about our longer term

investment themes, 2008 was a challenging year.

We therefore reduced the risk profile of most

portfolios, without however putting into question

the basics of our style and themes. When volatility

returns to more normal levels, we believe that risk

will again be rewarded.

Regarding fixed income, we suffered from our above

average exposure to corporate bonds, especially the

high yield segment and the financial sector,

including subordinated debt. What used to be before

an intelligent “decorrelation trade” in combination

with government bonds failed as forced selling and

the drying up of liquidity forced numerous market

participants to capitulate. Against such a harsh

background, traditional fixed income investment

strategies have been put into question, and this up

to a point where most of the corporate fixed income

universe offers equity-like returns for the future.

Through a strengthening of our fixed income team,

we are well positioned to reap the benefits of this

perhaps “once in a lifetime” opportunity.

BUSINESS DEVELOPMENT

Dispersion of returns across the active asset

managers in the market has increased massively. At

Petercam Institutional Asset Management some

portfolios disappointed in certain asset classes,

especially the corporate fixed income portfolios;

others showed good excess returns, especially in the

equity and balanced portfolios. Therefore, our sales

teams and institutional portfolio managers had a

very important role in explaining the performances

to clients and prospects, financial advisors and

retailers. In more difficult times, communication and

transparency are crucial.

Regarding the fixed income funds, we saw some

important distribution clients switching tactically

out of the more aggressively managed mutual funds

into more defensive asset categories. As a

consequence, important net inflows occurred in

euro government bonds and pure cash funds out of

investment grade corporate and high yield bonds.

Looking forward, the dichotomy between the

revived primary bond marketplace and the

moribund secondary bond market does mean that

new fixed income funds have the advantage of

starting with a clean sheet. We will continue to

focus on our bond picking skills in this new dynamic

credit landscape. In this regard, we strongly support

the distribution of our existing fixed income funds,

even if our historically strong track record suffered

for some funds. Some clients and prospects are now

24 activity report 2008 � PETERCAM

clearly focusing on the potential rebound of

performances. We are also developing new products

to respond to the needs of our clients i.e. inflation

linked bonds, bond funds with fixed maturities, etc.

During 2008, we successfully launched the Petercam

Equities Agrivalue fund and Petercam Equities World

3F (Foundation for the Future), both thematic funds

that caught quite a lot of interest from both private

and institutional investors as long term plays on the

structural challenges in the world. Despite a

temporary set back during the second half of 2008,

we remain convinced that growth will pick up again

first in the emerging markets.

The mandate channel represents 45% of total assets

managed for institutional clients, the remaining part

being mutual funds promoted to distribution clients,

mainly private bankers, life insurers and funds of

funds.

Looking ahead, pension plan managers and insurers

will give greater consideration to the interaction of

the risks of their assets with those of the liabilities.

A complete analysis of the economic drivers of

future return is thus an important part of

establishing an investment strategy. Setting up this

framework will allow us to manage all the

dimensions of risk and return.

We expect pension funds to increase their exposure

to active asset managers which should benefit to

our strategies, namely in traditional active

management of European and worldwide equities

as well as in our different fixed income strategies.

PETERCAM � activity report 2008 225

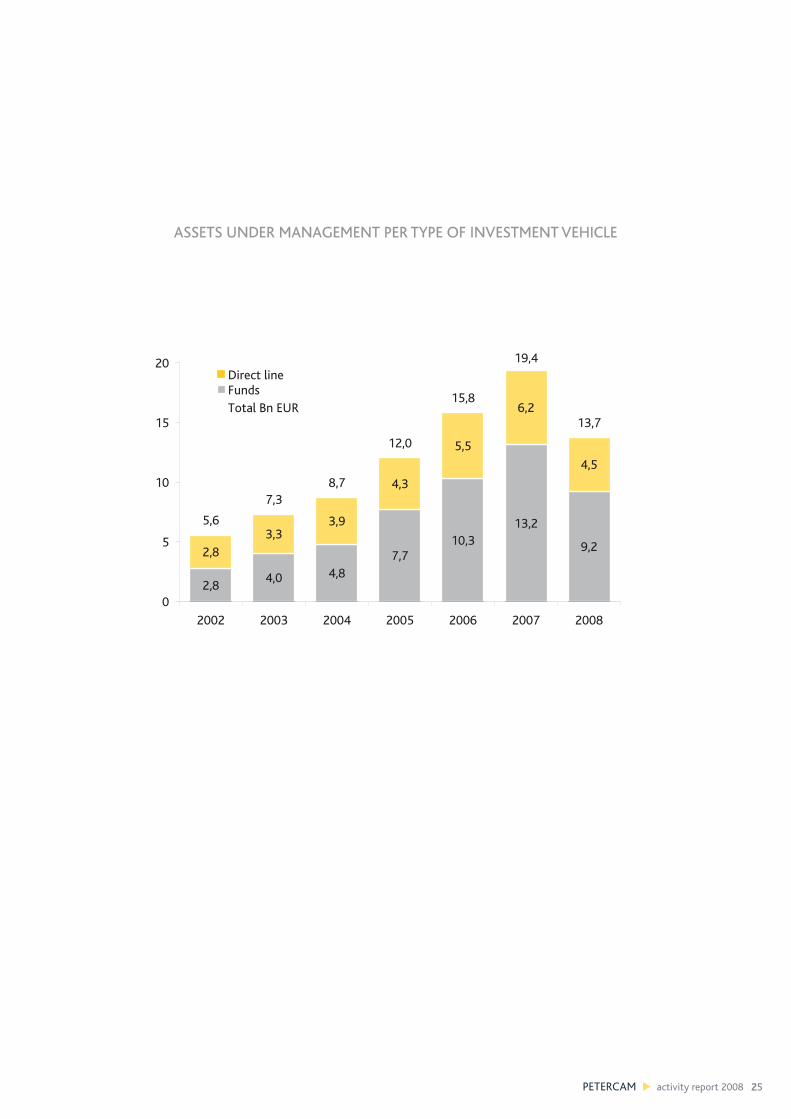

2,84,0 4,8

7,710,3

13,2

9,22,83,3

3,9

4,3

5,5

6,2

4,5

5,6

7,38,7

12,0

15,8

19,4

13,7

0

5

10

15

20

2002 2003 2004 2005 2006 2007 2008

Direct lineFundsTotal Bn EUR

ASSETS UNDER MANAGEMENT PER TYPE OF INVESTMENT VEHICLE

It 's far better to buy awonderful company at a fairprice than a fair companyat a wonderful price.”

Warren Buffet

PETERCAM � activity report 2008 227

3P (Petercam Private Projects) is Petercam’s division

for alternative investments which aims to diversify

the portfolios of Petercam clients. This diversifica-

tion and de-correlation is focused on real economic

diversification, rather than the mathematical de-

correlating effect of different accounting rules for

liquid versus illiquid or less liquid assets.

3P and by extension Petercam is active in real estate,

ships, aircraft, wind farms and other tangible assets

producing regular cash flows. As a consequence

Petercam’s exposure to hedge funds has always

been very limi-ted and has been further reduced

starting in 2007.

Although tangible assets do tend to have a positive

correlation with the global economic climate, many

aspects of such assets diversify these investments

away from traditional investment classes : an

aircraft leased for several years to a first tier

operator produces as much cash in bad economic

circumstances as in good times.

Some observations can be made in this respect.

A first obvious but important factor in 2008 was

that illiquid assets cannot lose a liquidity premium

in terms of valuation. Even if the market situation

in the last quarter of 2008 was exceptional and

probably only temporary, the evaporation of

liquidity in many equity and bond markets has

contributed to increased, mostly one-directional,

volatility over the period.

Furthermore, tangible assets have the typical

characteristic that the predictable cash flow streams

permit the financing of the investment with a

considerable amount of bank debt. 3P structures use

this to enhance the performance of their

investments. After the collapse of Lehman Brothers

in mid-September 08, banks were no longer willing

to engage in any new projects. Nearly all 3Ps

requirements in terms of bank debt had term sheets

in discussion when the market stalled and as a

consequence the discussion was only on the debt to

value ratio and the margin, rather than whether or

not banks would finance the assets.

Higher margins have at least partially been

compensated by lower interest rates, while the

lower debt to value ratio might be enhanced in a

later stage, when banks have settled their internal

problems. The strategy of investing in banking

relationships with the most specialized banks for

each niche in which 3P is present in has paid off :

during the difficult times, only those banks knowing

exactly what risks they were taking on were still able

to act.

3P has in the past also advised its clients on the

selection of closed end but listed private equity

funds in emerging countries. Although we are happy

with the underlying performance of every single

manager, the market price of the funds suffered the

general trend of all equity markets. The de

decoupling of the economies which was widely

expected until late 2007 proved to be illusory in

2008. More realistic expectations are now reflected

in the markets. We continue to be supporters of the

immense opportunities in countries with strong

demographics and ambitions to improve the quality

of life of millions of people.

In terms of fund raising, 2008 was obviously much

quieter than previous years. Nevertheless a second

closing lifted the size of the 3P Tangible Assets Fund

to EUR 126 m. During the fourth quarter New

Paragon Investments Ltd, 3P’s ferry-fund, raised EUR

52 m in mezzanine debt, which together with the

bank debt on the assets, provided the means to take

delivery of its new build roro and ro-pax.

Petercam Private ProjectsPETERCAM PRIVATE

PROJECTS

Planning is bringing the

future into the present

so that you can do

something about it now.

Alan Lakein

PETERCAM � activity report 2008 229

Nobody likes to think about estate planning. Death

is always far away and there will always be enough

time for thinking and planning later. In addition,

many people believe that the mere fact of drafting

a will is a sign that the “bitter end” is approaching:

superstition has not disappeared and these

considerations are a barrier for many persons.

Yet estate planning is of paramount importance for

families: how many times do we see heirs struggling

about the composition or the location of the assets,

or fighting about “who is going to get what”. A

proper advance identification of legacies is clearly

useful. Equally important are the tax considerations:

the different Regions take their toll on the assets of

the deceased and the rates applicable are rather

high.

The tax laws in Belgium allow in many

circumstances to strongly reduce estate duties. It is

the reason why a proper planning must be put in

place. Everybody knows that estate planning of

securities and cash is based on donations: but

people are sometimes reluctant to give away their

assets without being able to benefit from or to

recover them. Yet different techniques exist to

circumvent these fears: donations can be made with

different clauses designed to the wishes of the

donor. These clauses can be standard or specific but

require a lot of attention and care.

Another development which affects estate planning

is the move towards a so-called transparency of the

individuals’ assets. The balance between general

public interest (collection of taxes) and protection

of private life is tipped clearly in favour of the State:

suppression of bearer shares, implementation and

extension of the Directive on savings, future

abolition of banking secrecy : the list is long and

goes on … The recent press announcements on the

fight against tax havens are just examples of the

move towards full transparency. This means that

disclosure of people’s assets will soon become a

reality; hence an additional reason to implement

proper estate tax planning.

Our people in Petercam Estate Tax Planning

department are fully dedicated to assisting our

clients in this environment. With a team of about

10 specialists, the group not only benefits from

extensive experience but its members are also

specialised in certain areas and enjoy a solid

reputation, witnessed by academic activities,

participation as speakers to seminars and

conferences, and advisers to public authorities. They

also regularly inform our clients of the latest

developments in the area of estate planning.

“Planning is bringing the future into the present”:

coming to Petercam’s Estate Planning Group is a

guarantee of estate planning optimisation.

Estate PlanningESTATE

PLANNING

Risk comes fro

m

not knowing wha

t you're doing.

Warren Buffet

PETERCAM � activity report 2008 331

THE IMPORTANCE OF RISK MANAGEMENT AND

COMPLIANCE

The importance of the domains of risk management

and compliance in the financial services sector grew

increasingly over the last years, underlined by some

major milestones. From the various headlines repor-

ting that the unexpected had happened, to the

marked regulatory developments in the areas of

solvency and investor protection, countless clues

pointed over time towards the key role risk mana-

gement has to play in the financial services industry.

But until the recent collapse of the financial

markets, few events underlined how critical it is to

actively manage risks in an integrated way.

Risk management is about developing internal

guidelines interpreting the actual risk challenges of

the current environment – as well as the regulation –

and enforcing their principles, while uncovering new

paths for the business to explore. Identifying,

measuring and monitoring key risks across business

lines allows for a better understanding of the threats

to Petercam and its clients and, ultimately, allows

Petercam to deliver the high added value its clients

have come to expect.

Petercam has been developing for years its approach

to the management of risk and compliance in order

to handle an ever increasing scope of financial risks

as well as to meet increasingly demanding regula-

tory requirements. This development has resulted in

the build-up of risk awareness and the advent of a

robust compliance culture across the group.

THE RISK MANAGEMENT PROCESS OF PETERCAM

Petercam has taken significant steps over the last

years to develop its risk management process –

among which the extension of the risk management

team and the formalisation of roles and

responsibilities in managing risks stand out.

Petercam considers risk management as an ongoing

process, under the responsibility of the Board of

Directors. Communication represents a cornerstone

of this process: risk management is embedded in the

business activities of the Group’s constituent

entities through the establish-ment of a risk

management committee.

The risk management committee acts as a forum

allowing the regular exchange of views between the

risk manager, the risk control officers and the

business managers, thereby continuously enhancing

the risk management process through ongoing

communication – building the risk awareness and

compliance culture established by Petercam as core

values. The risk manager, independent from the

business activities, acts as a link between the

management of Petercam and the business

managers themselves.

Compliance and Risk ManagementCOMPLIANCE AND RISK

MANAGEMENT

32 activity report 2008 � PETERCAM

COMPLIANCE CULTURE

For more than 10 years now, Petercam has put

strong emphasis on CCompliance and has progres-

sively considered all compliance related issues as an

inherent part of its risk management approach. This

has been and still is a challenging exercise since

politicians and regulators have required the finan-

cial industry all over the world to incorporate high

level practices in terms of market integrity, of trans-

parency, of fair treatment of clients, of prevention of

conflicts of interests, of anti-money laundering pro-

cedures, etc…..

Like many other financial institutions, Petercam has

identified the imperative need to implement within

its organization an independent management func-

tion ensuring compliance with internal procedures

and that all products and services offered to clients

comply not only with legal and regulatory require-

ments, but also with its own corporate values and

with the legitimate expectations of its main stake-

holders.

The gradual diffusion of compliance guidelines and

procedures within the different units of the Group

has, over the years, resulted in a broader acceptance

by management and employees of a compliance

culture as an inherent part of our business processes

and behaviour and also as a unique preventative

tool for avoiding reputation failure.

A LOOK IN THE REAR VIEW MIRROR

In the light of the recent collapse of financial

markets, the main focus of the risk management in

2008 was the asset management activity – though

Petercam certainly did not overlook the risks in its

other business lines.

In the area of PPrivate Asset Management, the risk

management accent was set on protecting client

assets, ensuring that discretionary management

decisions were in line with the client profiles – not

only to comply with the requirements of the MiFID

regulation, but first and foremost to ensure that

Petercam’s own internal guidelines are respected.

The main interests of risk management in the area

of IInstitutional Asset Management have been the

follow-up of the institutional mandates and the

control of the fund manager activity. In the recent

context of financial markets breakdown, particular

attention was paid to mitigating the risks arising in

fund management from the lack of liquidity on the

bond markets.

In addition to the direct interest in the business lines

of Petercam, the risk management also ensures the

follow-up of kkey regulatory requirements, among

which the ICAAP1 stands out as a cornerstone of the

risk management process, providing a broad analysis

of the risks the group is exposed to and linking the

potential losses to the capital of Petercam to ensure

the soundness of the group’s business activities.

1 Internal Capital Adequacy Assessment Process, key element of the Basel II framework

PETERCAM � activity report 2008 333

Investing without research

is like playing stud poker

and never looking at the

cards.

Peter Lynch

PETERCAM � activity report 2008 335

MACRO RESEARCH

Top-down research has been a feature of Petercam

Asset Management from the start. The in-depth

analysis of the macro-economic situation is an

important step in our investment process. Our team

follows constantly the flow of economic data, the

fundamentals of the world economy and its regions,

and the valuation of asset markets. Over the last

few years, the focus has been increasingly on

Eastern Europe and Asia. The US and European

economies remain the starting point of the macro-

economic outlook, but over the last decade, the

influence of emerging economies has become crucial.

The team follows important developments in

financial markets, such as the rise of new financial

products, risk transfer, volatility and risk premiums.

Important socio-economic trends also receive atten-

tion, as well as detailed study of the energy challenge.

Economic research and investment strategy are

intrinsically linked, and therefore we call our service

“Ecostrategy”-research.

The role of EcoStrategy can be summarised in three

key points:

� Developing investment themes

Typical investment themes have been the focus

on small and midcaps, US problems, opportuni-

ties in the East, free cash flow, energy and food.

� Analyzing trends: our research is less focused on

the very short term.

Our attention is on how investor consensus is at

a certain moment, and if there are possible

surprises with that general opinion. A stable,

medium term scenario provides a clear

framework for our asset managers.

� Providing unbiased information:

This works in two ways. First, our in-house

research is focused entirely on the interests of

our asset management and eventually our

clients’ interests. Second, outside opinions often

have a bias in investment horizon. We have to

adjust this information to give fair, balanced,

relevant information and views to our asset

managers, adjusted for the typical noise that

accompanies investment opinions.

The Ecostrategy team communicates with e-mails

to the asset managers on important or

marketmoving economic data. They also provide

regular updates on key themes and economic and

financial trends. A monthly summary of economic

headlines provides a clear guide for our economic

convictions with an outline of our strategic asset

allocation.

On a regular basis, there is a forum for asset

managers, with a presentation of the economic and

strategic outlook, with often lively discussions.

But also the day-to-day interaction of market-linked

macro-economists with documented and macro-

interested fund managers creates an environment in

which top-down conviction blends with bottomup

ideas.

Top-down research is an important part of our

investment process. The analysis of the economic

cycle is especially important for our bond

management. Also inflationary expectations are, of

course, crucial for them.

The international political, economic and even

geopolitical outlook is a key element in our inter-

national bond management.

For equity investors, the top-down factor is partially

parallel, as yield and interest rate scenarios

determine an important part of the equity outlook.

The top-down department determines opportu-

nities in investment themes. A knowledge and

in-depth analysis of the stock market valuation,

regionally and by group is also valuable for our

equity management.

Macro and Buy-Side ResearchMACRO & BUY-SIDE

RESEARCH

BUY-SIDE RESEARCH

Over the course of the recent years, Petercam has

continued to invest in its proprietary asset

management research team. The current team

consists of 8 analysts each focused on specific

sectors. Over the last year we refocused our efforts

by decreasing the time allocated to the financial

sector and re-allocating the time to broaden the

geographic (selectively in the United States) and

thematic (launch of Agrivalue) coverage

We put a lot of emphasis on independence and

encourage our people to have an independent

mindset only using broker research as one of the

many sources of information. Going forward we will

increase the utilization of independent and

specialized research organizations who provide us

with a broader perspective on thematic and/or

regional developments

All the information at our disposal (sell-side

research, independent research and database

providers) helps each analyst to build his medium

and long-term sector view. This sector view is very

important as it helps build the framework used to

distinguish the long term winners in each sector.

Analysts are also encouraged to meet with company

management whenever they have the possibility.

Although it does not provide insight into short

termtrends – especially when the visibility of the

company is very low and comments tend to be on

the cautious side – we believe it’s fundamental to

the better understanding ofthe drivers of the

company, its prospects and its future development.

Company meetings also help to better understand

how the sector operates and provide insight into the

evolution of the competitive environment.

Going forward we will continue the path chosen in

2008: working more in depth on a selected universe

of mainly European companies. Having an in-depth

knowledge of sector drivers and the competitive

positioning of companies will also help us to

evaluate relevant companies in other geographical

areas.

All this will contribute to our main goal: selecting

the companies that will outperform their sector and

the market over the medium and long term.

36 activity report 2008 � PETERCAM

PETERCAM � activity report 2008 337

Petercam PeoplePETERCAM

Our people are our main asset.

We strongly believe that the quality of our people

and the creation of an environment where they can

fully deploy their talents are key to the preservation

of our pre-eminent position in the market place.

We pride ourselves on maintaining a strong

corporate culture, notably through our partnership

structure. Shared values, deeply rooted collective

goals and beliefs are at the core of our continued

strength and success.

We reward our people based on their performance,

empowering them to deliver innovative and superior

services to our clients. Petercam has always taken

great care of the quality of the working environment

of its current and future employees. The

preservation of a fair balance between private and

professional life is also a key concern of our firm.

These elements are essential in our determination

to foster motivation, creativity, entrepreneurship

and commitment to excellence.

38 activity report 2008 � PETERCAM

Organigram and AddressesORGANIGRAM AND

ADDRESSES

PETERCAM SA/NV Place Sainte-Gudule 19 B-1000 Brussels +32 2 229 6311Institutional Asset Management +32 2 229 6692Estate Planning +32 2 229 6651Petercam Private Projects +32 2 229 6592Eco Strategy & Buy-side Research +32 2 229 6559Corporate Finance +32 2 229 6555Institutional Sales +32 2 229 6626Trading +32 2 229 6485Sell-side Research +32 2 229 6308

PETERCAM BANK (NEDERLAND) NV De Lairessestraat 180 NL-1075 HM Amsterdam +31 20 573 5555Corporate Finance +31 20 573 5588Institutional Sales +31 20 573 5505Trading +31 20 573 5410Sell-side Research +31 20 573 5472

PETERCAM CAPITAL (UK) Ltd 13 Austin FriarsUK-London EC2N 2JX +44 20 7670 1688

Petercam

Security House

Petercam (Luxembourg)

Private Banking

Petercam Banque Privée (Suisse)

Private Banking

Petercam Capital (UK)

Petercam Bank (Nederland)

Investment Bank

Petercam Institutional Bonds

Bond Dealing

100%

100%100%

100%100%

PETERCAM � activity report 2008 339

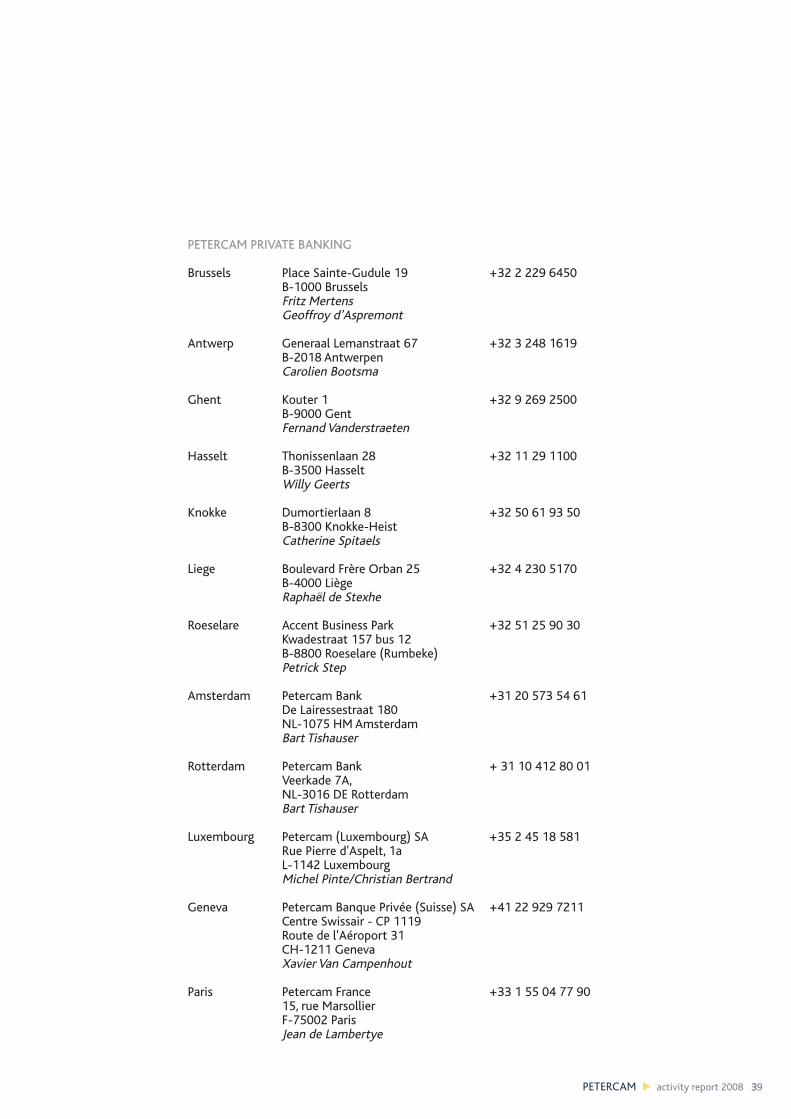

PETERCAM PRIVATE BANKING

Brussels Place Sainte-Gudule 19 +32 2 229 6450B-1000 BrusselsFritz MertensGeoffroy d’Aspremont

Antwerp Generaal Lemanstraat 67 +32 3 248 1619B-2018 AntwerpenCarolien Bootsma

Ghent Kouter 1 +32 9 269 2500B-9000 GentFernand Vanderstraeten

Hasselt Thonissenlaan 28 +32 11 29 1100B-3500 HasseltWilly Geerts

Knokke Dumortierlaan 8 +32 50 61 93 50B-8300 Knokke-HeistCatherine Spitaels

Liege Boulevard Frère Orban 25 +32 4 230 5170B-4000 LiègeRaphaël de Stexhe

Roeselare Accent Business Park +32 51 25 90 30Kwadestraat 157 bus 12B-8800 Roeselare (Rumbeke)Petrick Step

Amsterdam Petercam Bank +31 20 573 54 61De Lairessestraat 180NL-1075 HM AmsterdamBart Tishauser

Rotterdam Petercam Bank + 31 10 412 80 01Veerkade 7A,NL-3016 DE RotterdamBart Tishauser

Luxembourg Petercam (Luxembourg) SA +35 2 45 18 581Rue Pierre d'Aspelt, 1aL-1142 LuxembourgMichel Pinte/Christian Bertrand

Geneva Petercam Banque Privée (Suisse) SA +41 22 929 7211Centre Swissair - CP 1119Route de l'Aéroport 31CH-1211 Geneva Xavier Van Campenhout

Paris Petercam France +33 1 55 04 77 9015, rue MarsollierF-75002 ParisJean de Lambertye

Place Sainte-Gudule 19 Sint-GoedelepleinBruxelles 1000 Brussel

Tel.: +32 2 229 63 11 - Fax: +32 2 229 65 98www.petercam.com