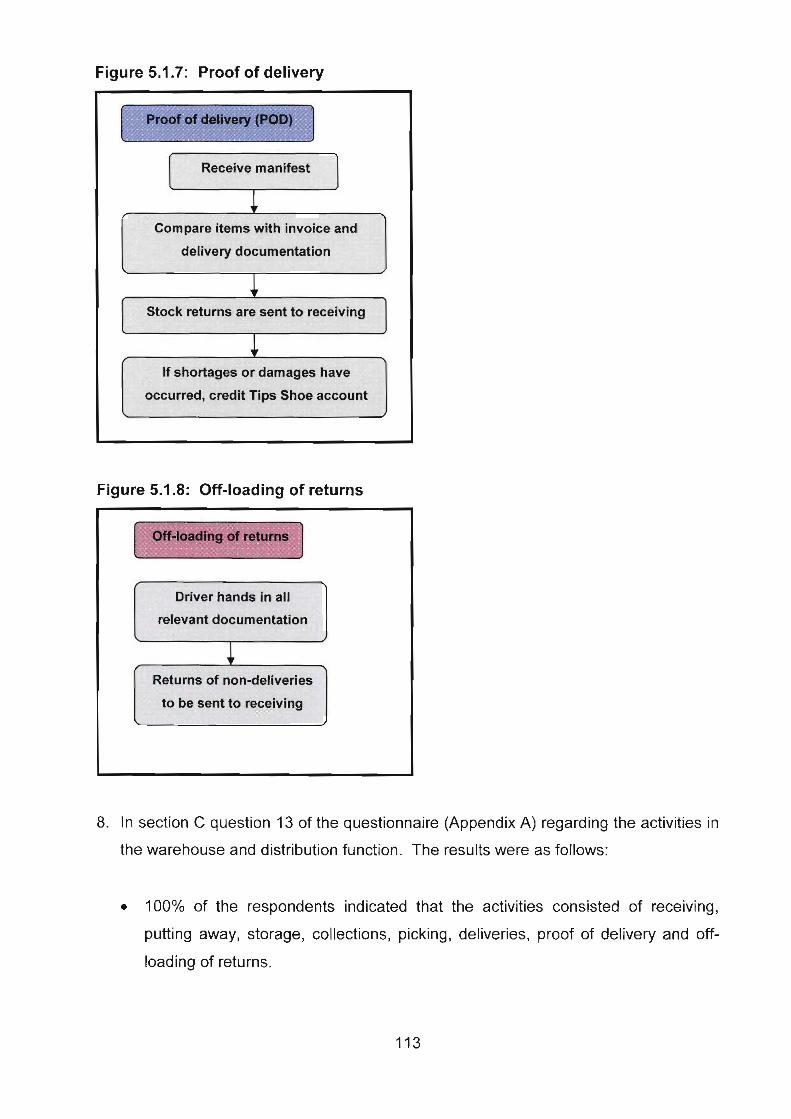

activity-based performance management at strategic

TRANSCRIPT

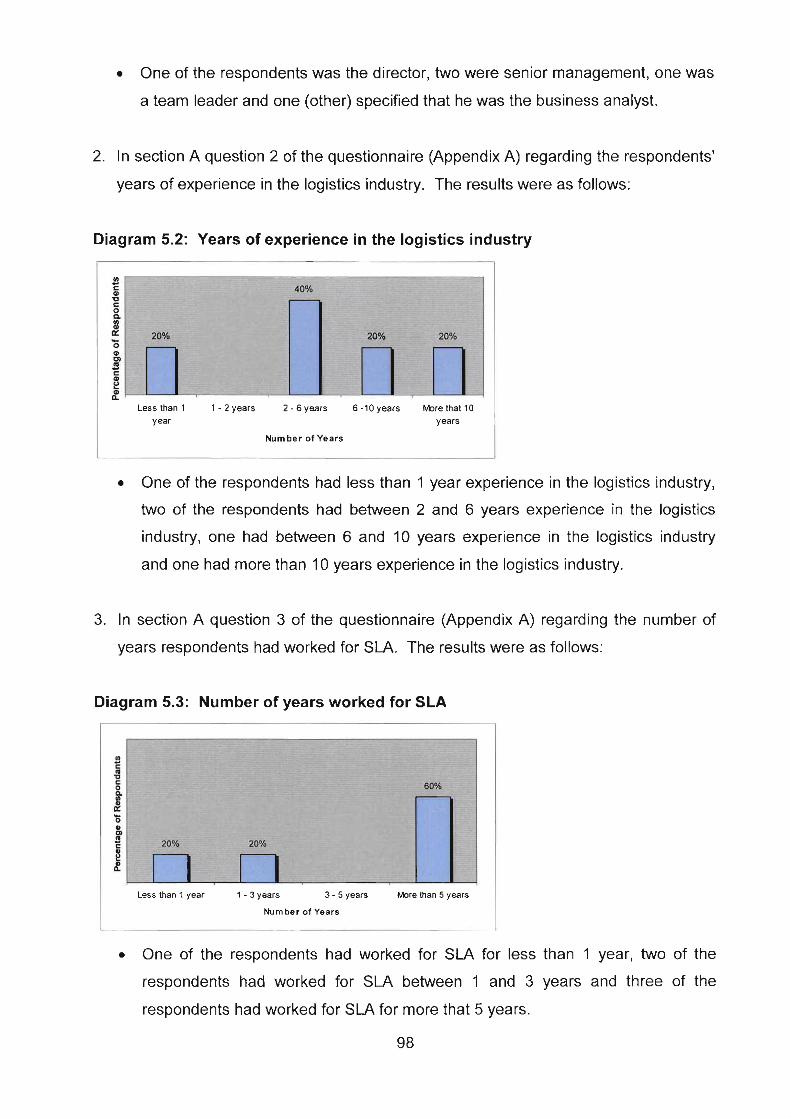

Activity-based performance management at

Strategic Logistical Alliance

SJ Spratt Hons. B. Corn.

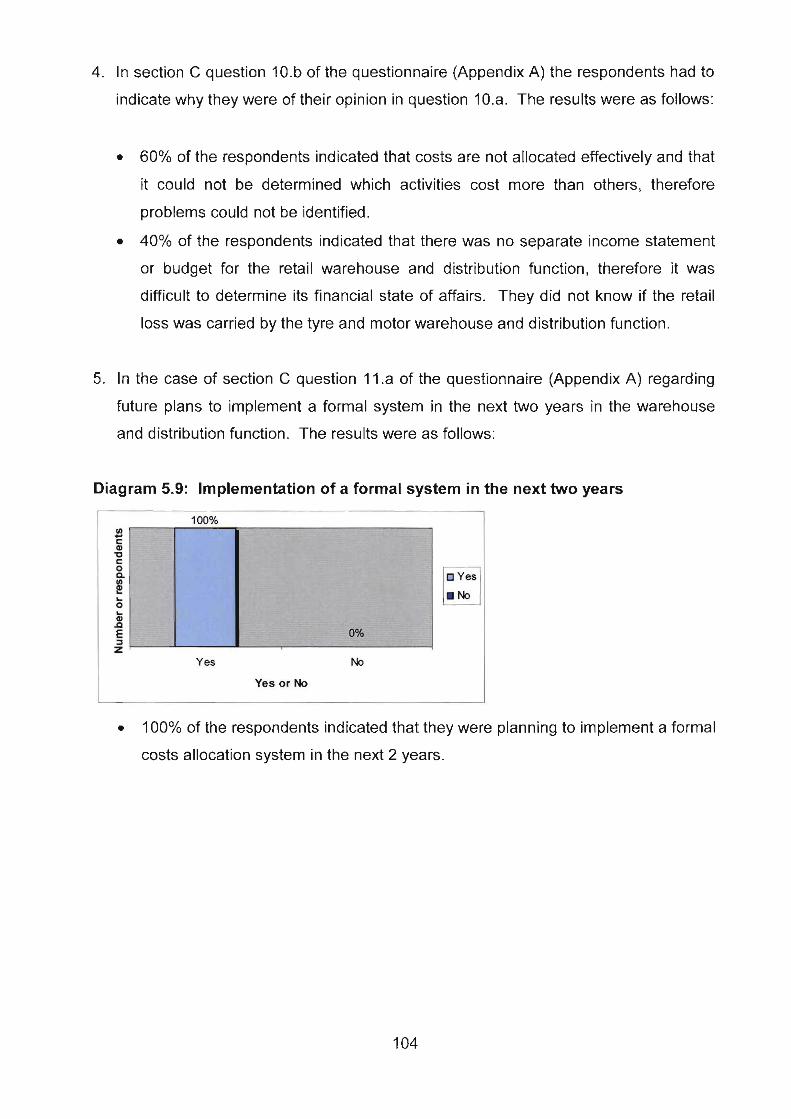

12127841

Mini-dissertation submitted in partial fulfilment of the requirements for the degree

Master of Commerce in Management Accounting at the Potchefstroom Campus of

the North-West University

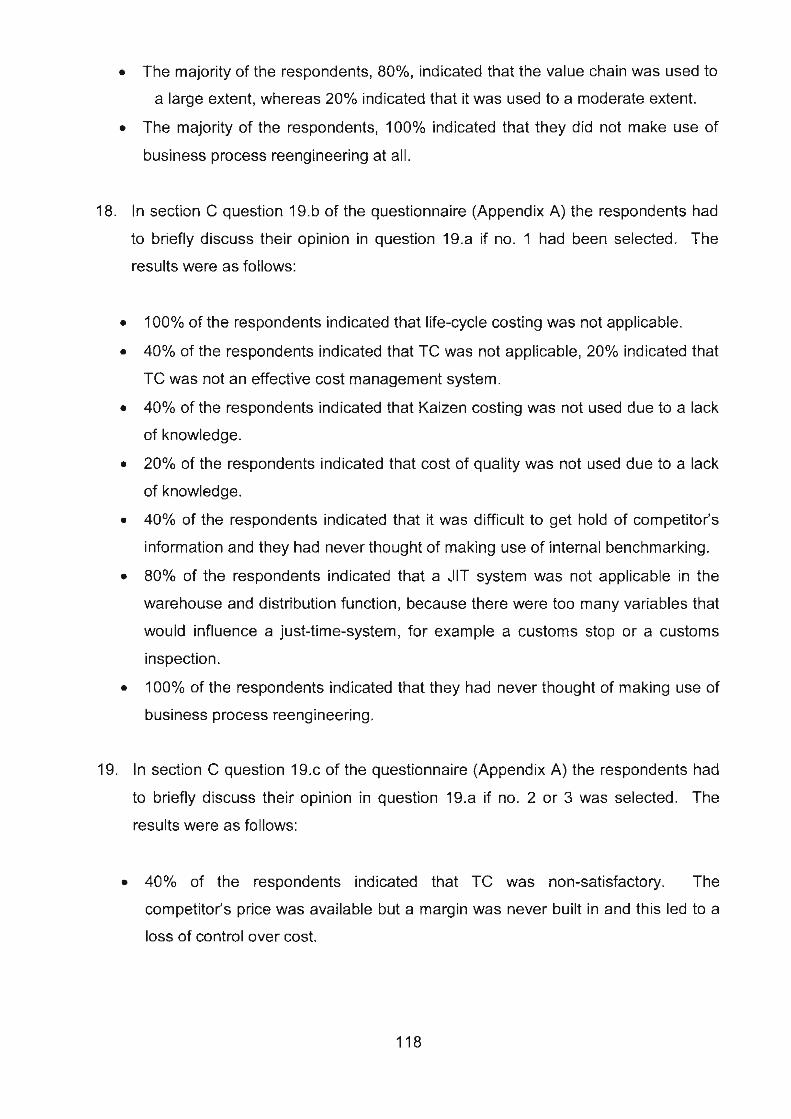

Supervisor: FJ Bibbey

November 2006

Potchefstroom

ACKNOWLEDGEMENTS

I hereby wish to express my sincere appreciation towards:

My Jesus, my Saviour, Lord there is none like You. 'Thank you for your grace

and for granting me with this opportunity. Thank you for blessing me with

wisdom and strength to complete this study. You are my awesome King of Love.

Mr. F.J. Bibbey, my supervisor, for his valuable assistance, guidance, leadership

and encouragement throughout this study. I really appreciate your advice, time

and interest.

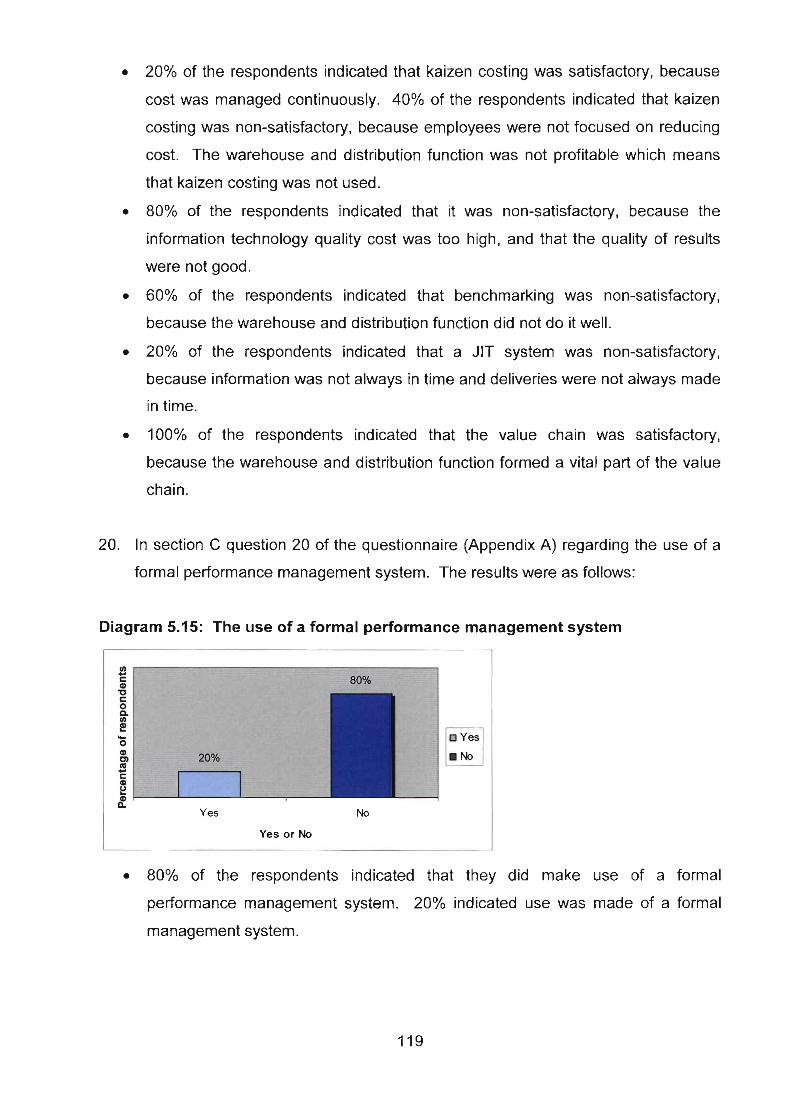

My colleagues at Strategic Logistical Alliance. Thank you for your time during

the structured interviews and thank you for your interest and understanding.

Mr. J. Blaauw for the language editing of the mini-dissertation.

Mrs. E. Roodt of the Ferdinand Postma Library for her friendly assistance with

literature searches.

My parents, Pat and Rina Spratt. Thank you for your love and support and for

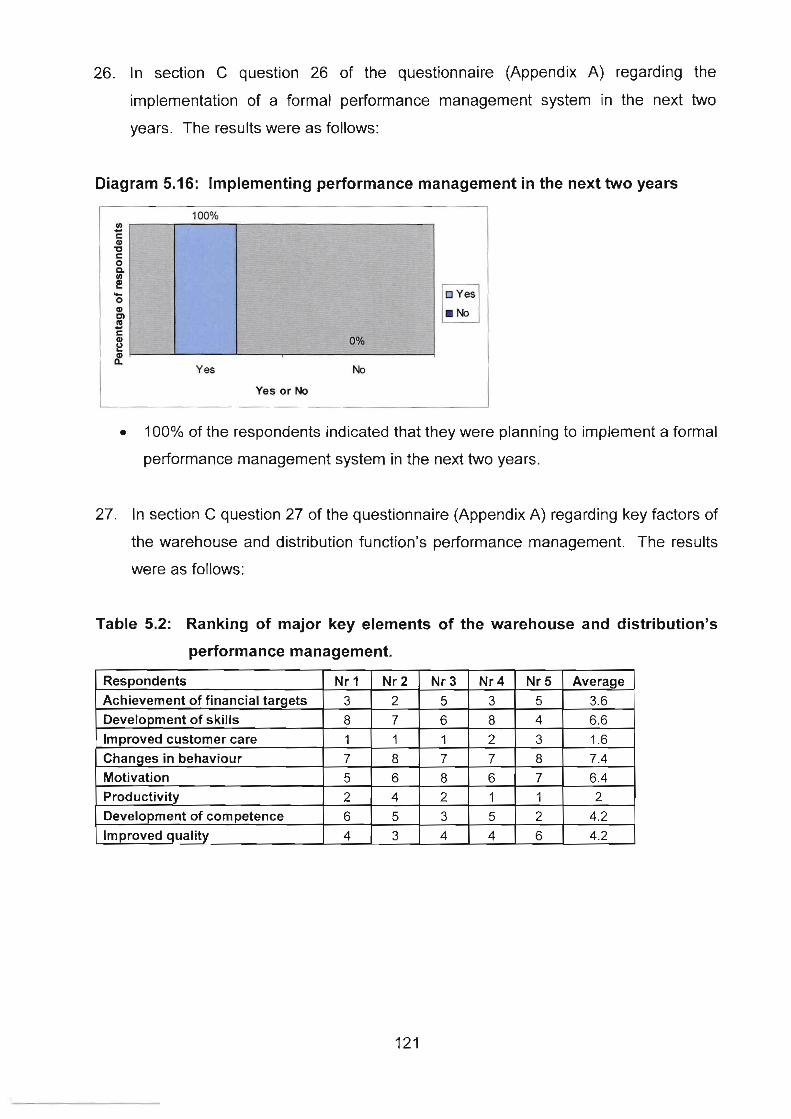

always believing in me. I appreciate your moral and financial support throughout

my studies. I love you.

Antonie, Patrick and Jani for your support, motivation and understanding.

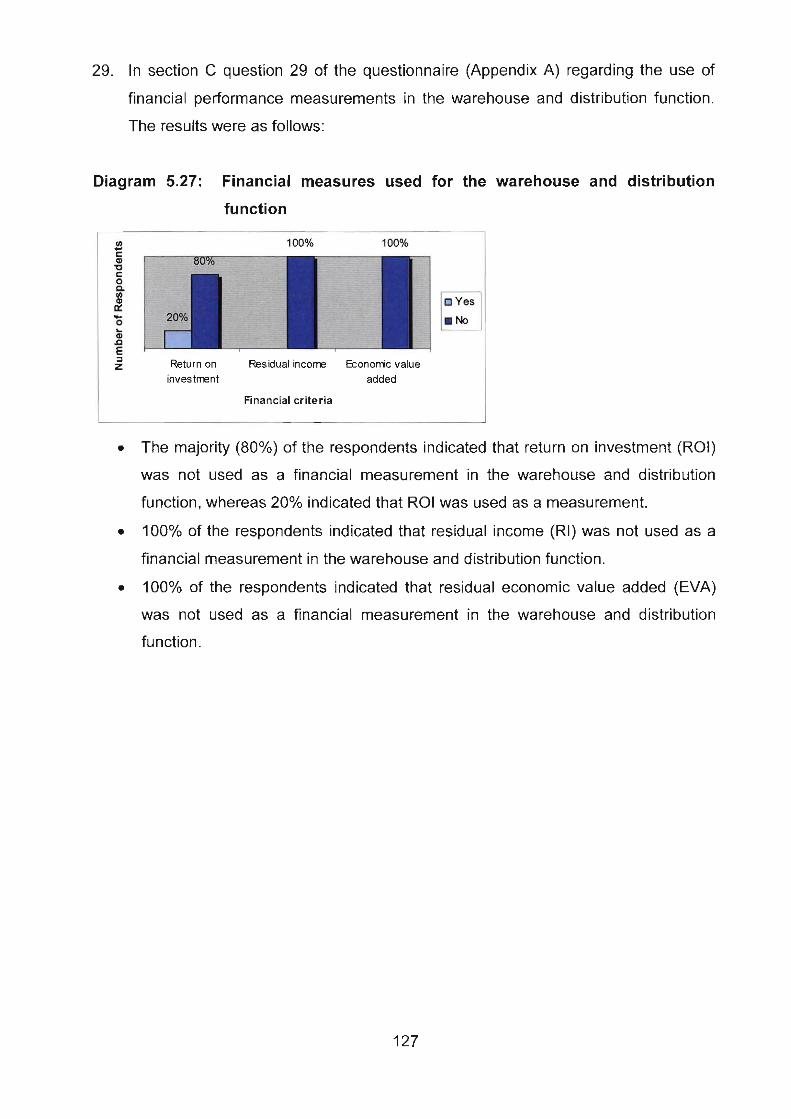

My friends, for your interest, prayers and support.

Psalm 37:3-4

Trust in the LORD and do good; dwell in the land and enjoy safe pasture.

Delight yourself in the LORD and he will give you the desires of your hart.

ABSTRACT

In the era of competitive global environment and technology-based

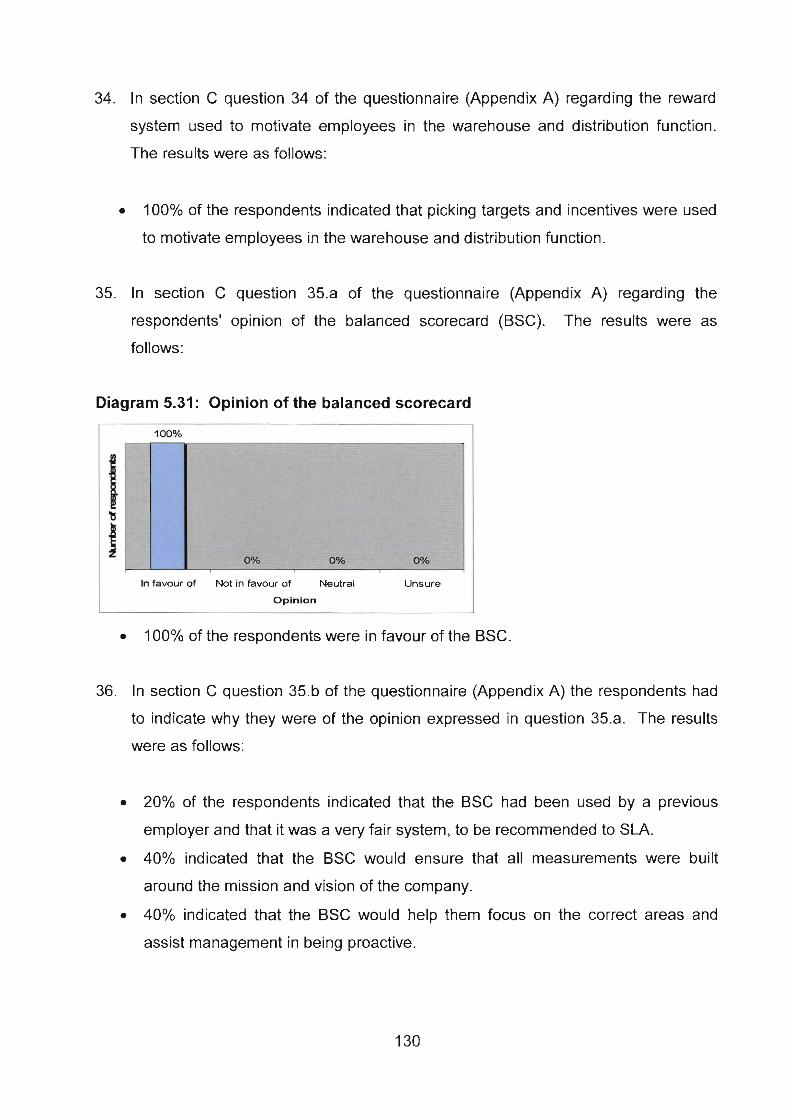

organisations, managers are pressured to find ways to maintain their competitive

advantage. Management has the responsibility to maintain their competitive advantage

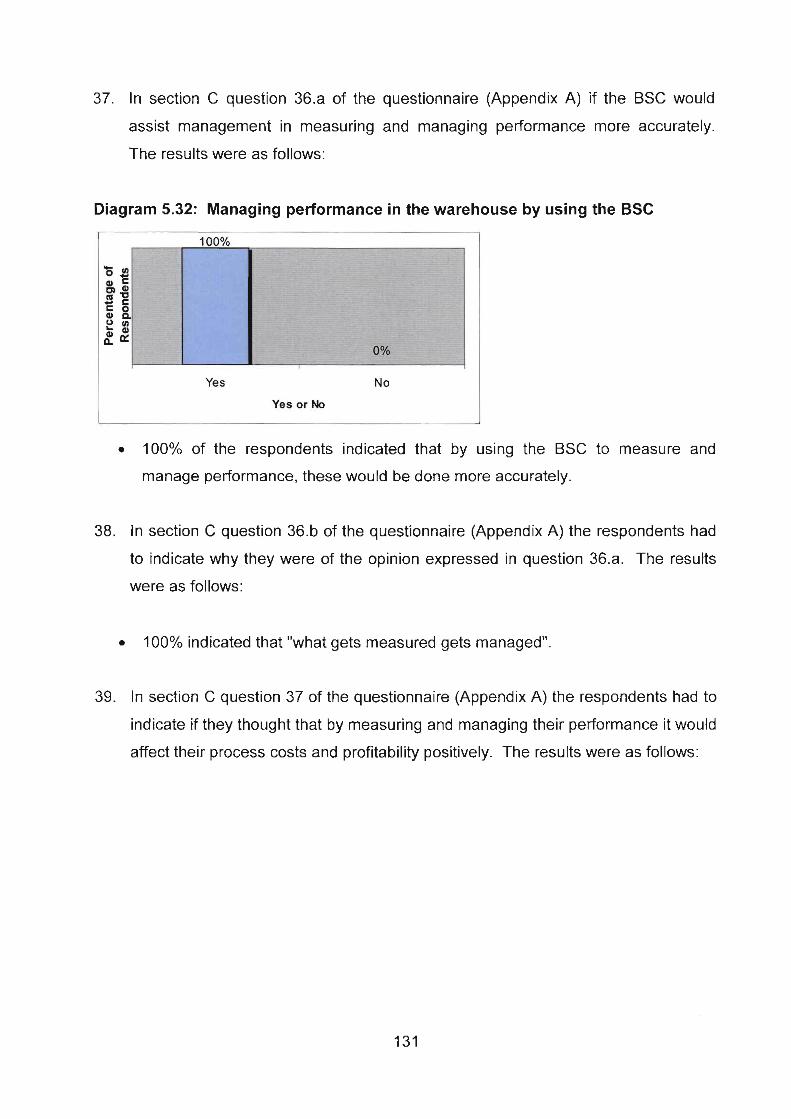

whilst maintaining the profitability of the organisation. This responsibility includes

decisions regarding the retention of profitable customers, and the minimisation of costs

to improve profitability of services. The analysis of cost and profitability of individual

services and customers represents a critical issue with which Strategic Logistical

Alliance (SLA) should be concerned

SLA has proved to be a market leader within the logistics services market whilst

maintaining profitability in most of its core business functions, with the exception of the

warehousing and distribution function. The reasons for a lack of profitability in the

warehousing and distribution function are inadequate planning, controlling and

decision-making within these functions. The main reasons for these problems are

incorrect cost allocations, the non-reflection of the true cost of activities, unprofitable

pricing and the lack of effective performance management.

'The primary objective of this study is to analyse the existing cost allocation system, the

cost management system and the performance management system of SLA, focusing

on the warehousing and distribution functions. The study addresses the shortcomings

of the existing system and recommends activity-based performance management as a

possible solution. To achieve this primary objective, a number of secondary objectives

were relevant.

The research was conducted at SLA in Gauteng. The research comprised a literature

study and an empirical survey using structured interviews to obtain information from

relevant staff and managers. 'The err~pirical study was further extended by obtaining

permission from top management to gather information by observation of activities and

processes carried out by staff in the warehouse and distribution function.

For management of SLA to achieve their goal of becoming a profitable leading

third-party logistical service provider, a combination of tools should be used, which

include activity-based costing, cost management and performance management.

Activity-based performance management will enable management to gain useful

information for decision-making to achieve their goal.

OPSOMMING

In die era van die mededingende wgreldwye omgewing en tegnologiegebaseerde

organisasies is bestuurders onder druk om wyses te vind waarop hulle hul

mededingende voorsprong kan handhaaf. Bestuur is daarvoor verantwoordelik om

hul mededingende voorsprong te behou terwyl hulle terselfdertyd ook die

winsgewendheid van die organisasie handhaaf. Hierdie verantwoordelikheid behels ook

besluite oor die behoud van winsgewende kliente en die minimalisering van koste om

die winsgewendheid van dienste te verbeter. Die ontleding van die koste en

winsgewendheid van individuele dienste en kliente verteenwoordig 'n kritieke kwessie

waarby Strategic Logistical Alliance (SLA) betrokke behoort te wees.

SLA het hulself bewys as 'n markleier in die logistiekdienste-mark terwyl hulle

terselfdertyd winsgewend heid in die meeste van hul kern besig heidsfun ksies hand haaf,

met die uitsondering van hul pakhuis-en-verspreidingsfunksie. Die redes vir die gebrek

aan winsgewendheid in die pakhuis-en-verspreidingsfunksie is ontoereikende

beplanning, beheer en besluitneming binne hierdie funksie. Die hoofrede vir hierdie

probleme is foutiewe kostetoedelings, die nie-weerspieeling van die ware koste van

aktiwiteite, nie-winsgewende prysvasstelling en die gebrek aan doeltreffende

prestasiebestuur.

Die primere doelstelling van hierdie studie is om die bestaande kostetoedelingstelsel,

die kostebestuurstelsel en die prestasiebestuurstelsel van SLA te ontleed, met die fokus

op die pakhuis-en-verspreidingsfunksie. Die studie handel met die tekortkominge van

die bestaande stelsel en beveel aktiwiteitsgebaseerde prestasiebestuur as 'n moontlike

oplossing aan. Om hierdie primere doelstelling te verwesenlik, is daar ook 'n aantal

sekondere doelstellings wat betrokke is.

Die navorsing is gedoen by SLA Gauteng. Die navorsing het bestaan uit 'n

literatuurstudie en 'n empiriese opname met gebruik van gestruktureerde onderhoude

om inligting van toepaslike personeel en bestuurders te verkry. Die empiriese studie is

verder uitgebrei deur toestemming van die topbestuur te verkry om inligting te versamel

deur waarneming van aktiwiteite en prosesse wat personeel in die pakhuis-en-

verspreidingsfunksie uitvoer.

Vir die bestuur van SLA om hul doelstelling te verwesenlik om 'n winsgewende,

toonaangewende derdeparty-verskaffer van logistiekdienste te word, moet 'n

kombinasie van hulpmiddels aangewend word, wat aktiwiteitsgebaseerde

kostebepaling, kostebestu~lr en prestasiebestuur insluit. Aktiwiteitsgebaseerde

prestasiebestuur sal bestuur in staat stel om nuttige inligting in te win met die oog op

besluitneming ten einde hul doelstelling te verwesenlik.

LIST OF ABBREVIKTIONS USED

ABC - Activity-Based Costing

ABM - Activity-Based Management

AGOA - African Growth and Opportunity Act

BPR - Business process reengineering

BSC - Balanced Scorecard

EBlT - Earnings before Interest and Taxes

ED1 - Electronic Data Integration

EDA - Estimated Times of Arrival

ETD - Estimated Times of Departures

EVA - Economic Value Added

GAAP - Generally Accepted Accounting Principles

IS0 - lnternational Standards Organisation

INCO - lnternational Cooperation

ITAC - lnternational Trade Administration Commission

IT - Information Technology

.IIT - Just-in-time

LCC - Life cycle costing

MCE - Manufacturing Cycle Efficiency

NPV - Net Present Value

POD - Proof of delivery

PMS - Performance Measurement System

RI - Residual Income

ROI - Return on Investment

ROS - Return on Sales

SARS - South African Revenue Services

SLA - Strategic Logistical Alliance

TC - Target costing

TQM - Total quality management

USA - United States of America

WACC - Weighted Average Cost of Capital

WIP - Work in progress

vii

-. ---- --

LIST OF FIGURES

Figure 2.1 : Activity-based costing

Figure 2.2: An illustration of the two-stage allocation process for traditional

and activity-based costing systems

Figure 2.3: The activity-based costing model

Figure 3.1 : Product life-cycle phases: relationship between costs

committed and costs incurred.

Figure 3.2: The relationship between target and kaizen costing

Figure 3.3: Warehouse layout before BPR

Figure 3.4: Warehouse layout after BPR

Figure 3.5: The effect of quality costs on quality of compliance

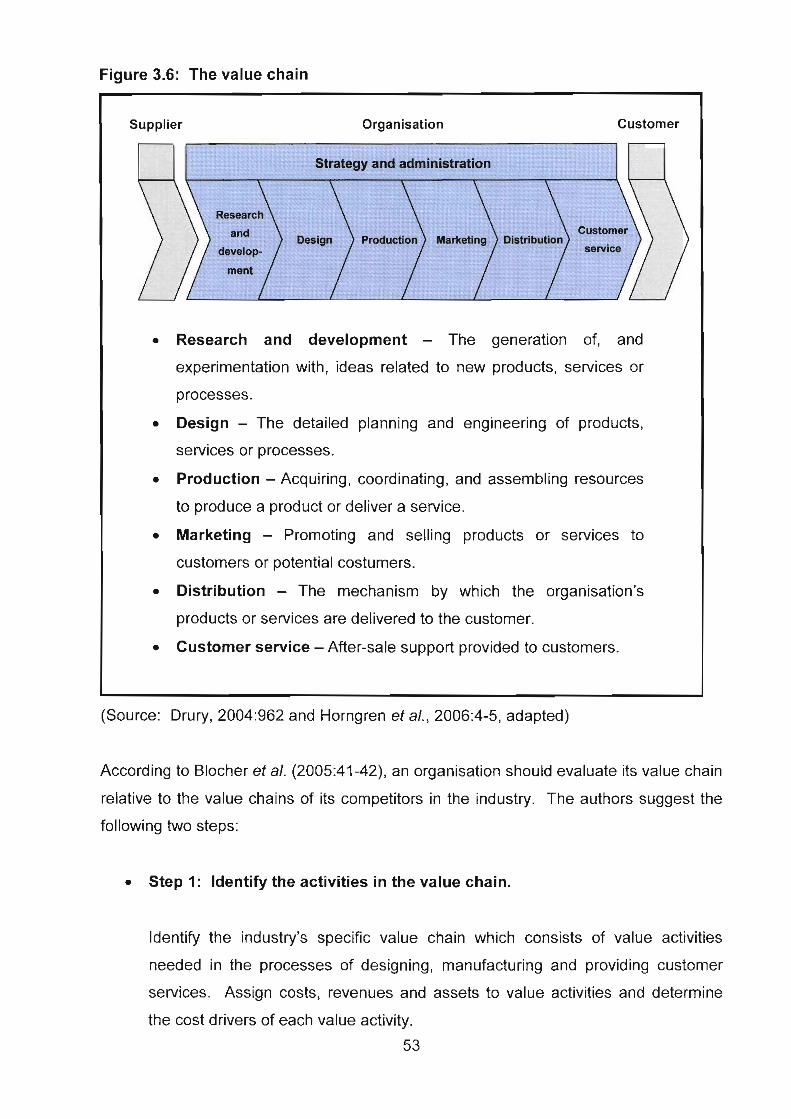

Figure 3.6: The value chain

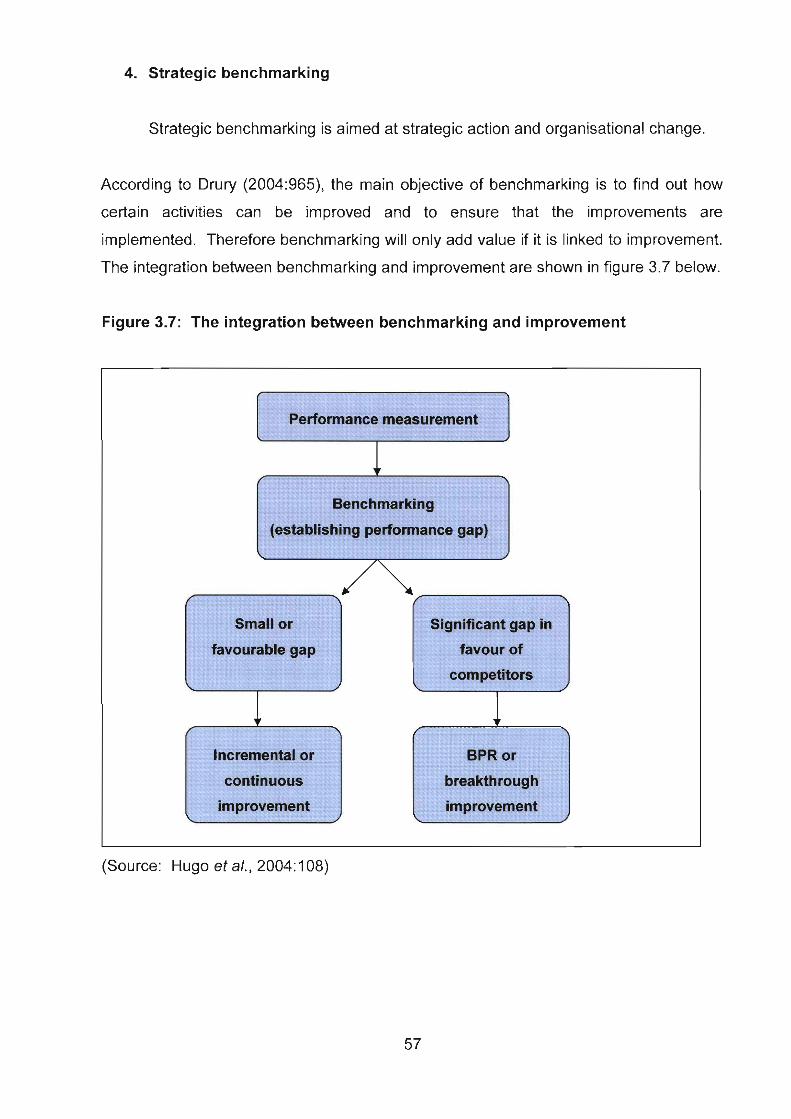

Figure 3.7: The integration between benchmarking and improvement

Figure 4.1 : The balanced scorecard

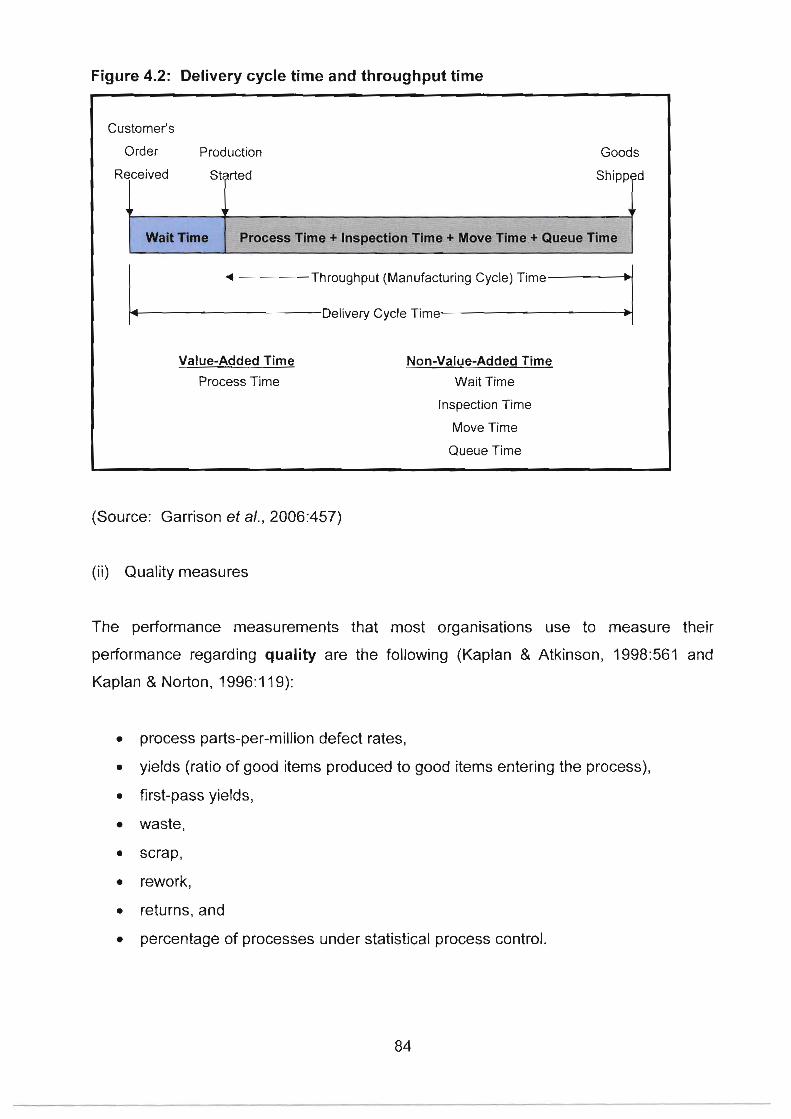

Figure 4.2: Delivery cycle time and throughput time

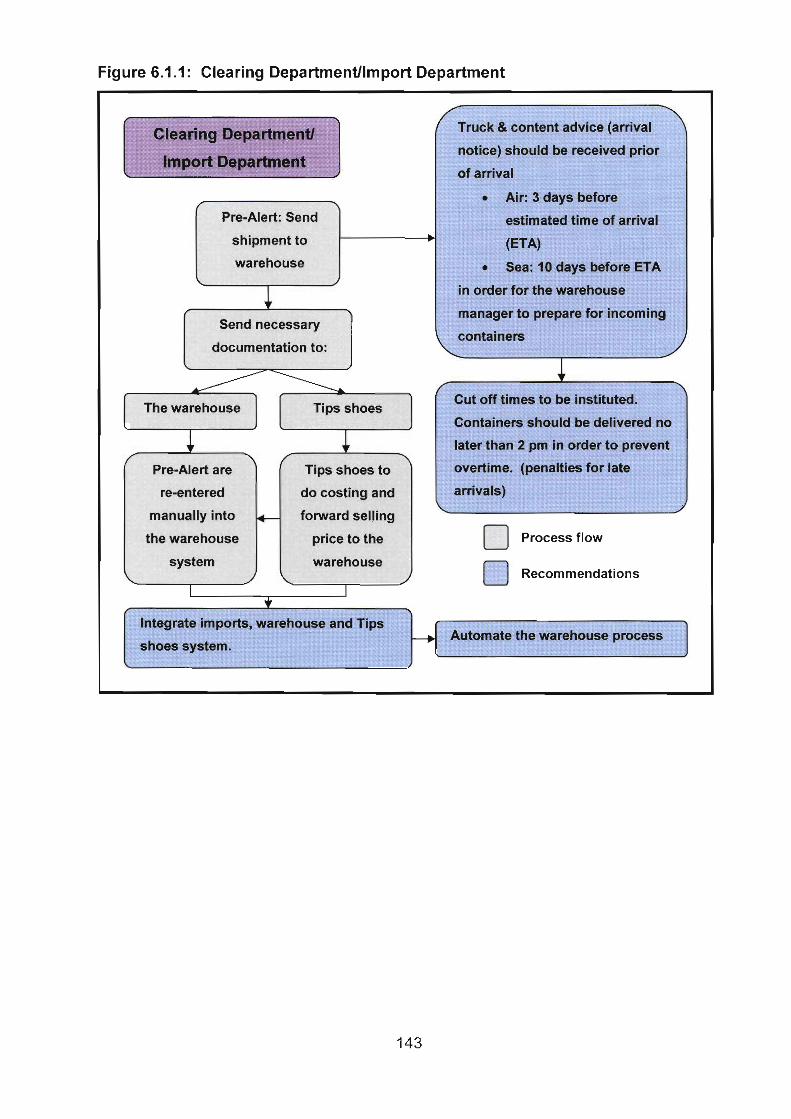

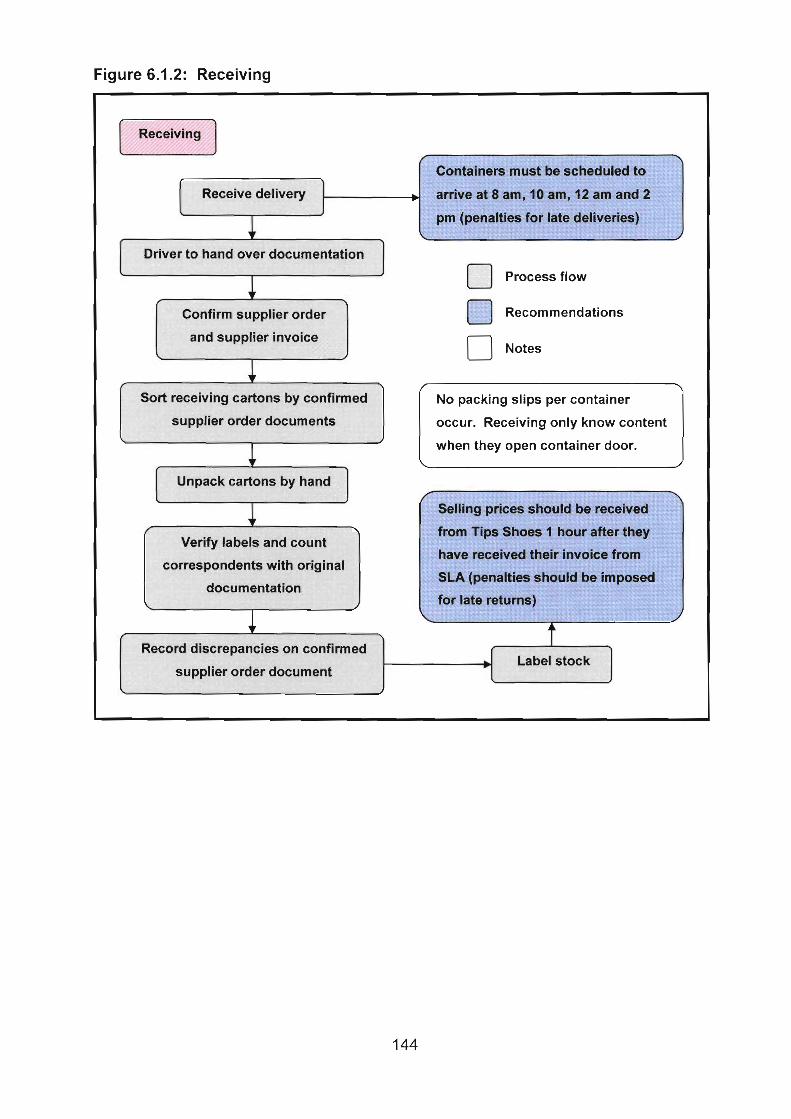

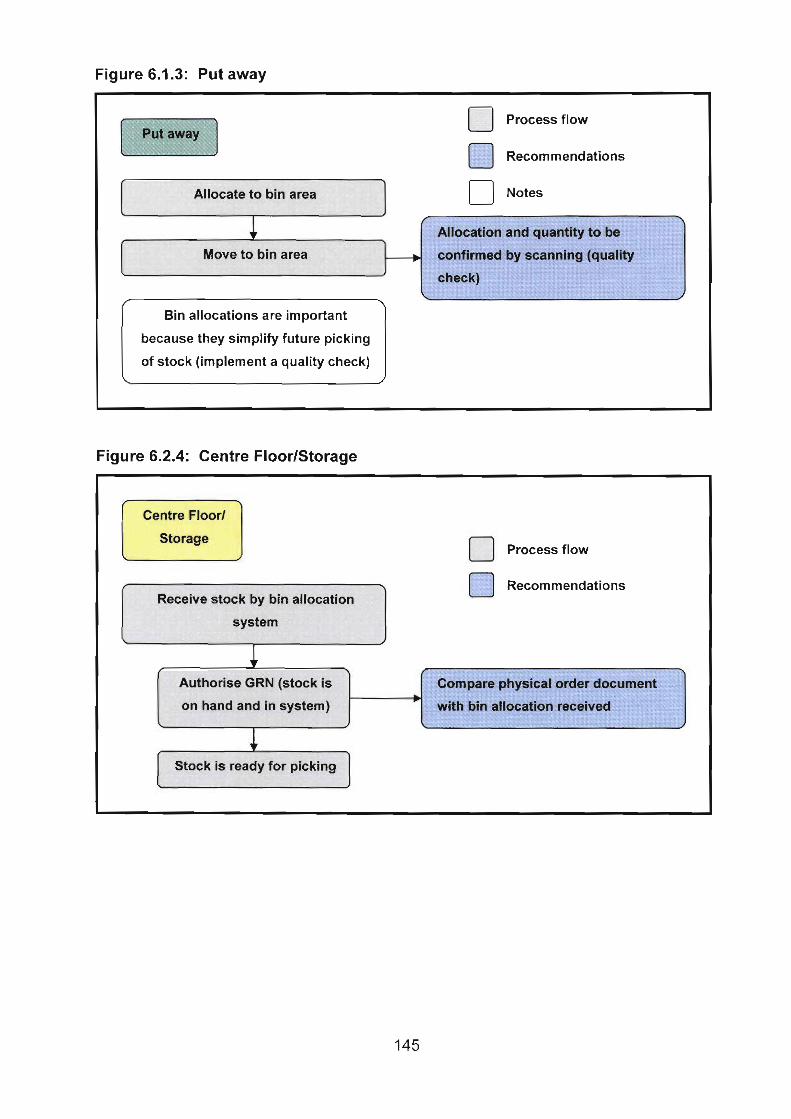

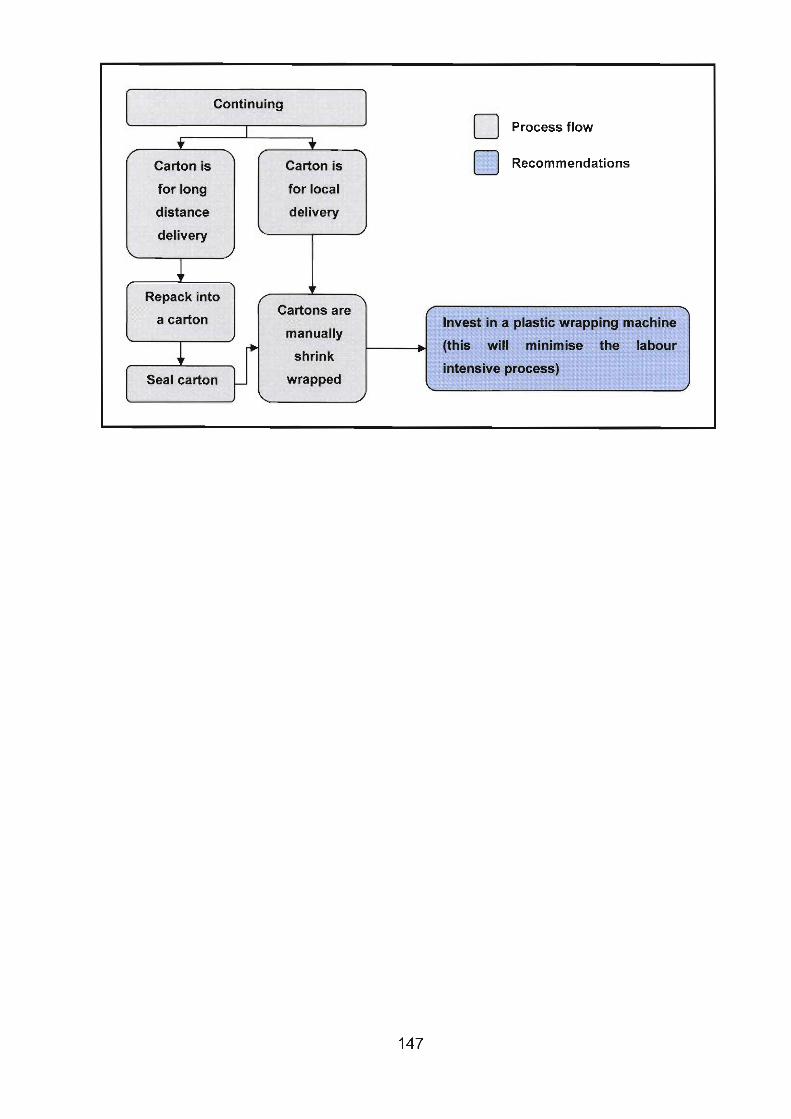

Figure 5.1 : Current process flow of the warehouse and distribution function

Figure 6.1: Process flow of the warehouse and distribution function

Pane

12

. . . Vlll

LIST OF TABLES

Pane

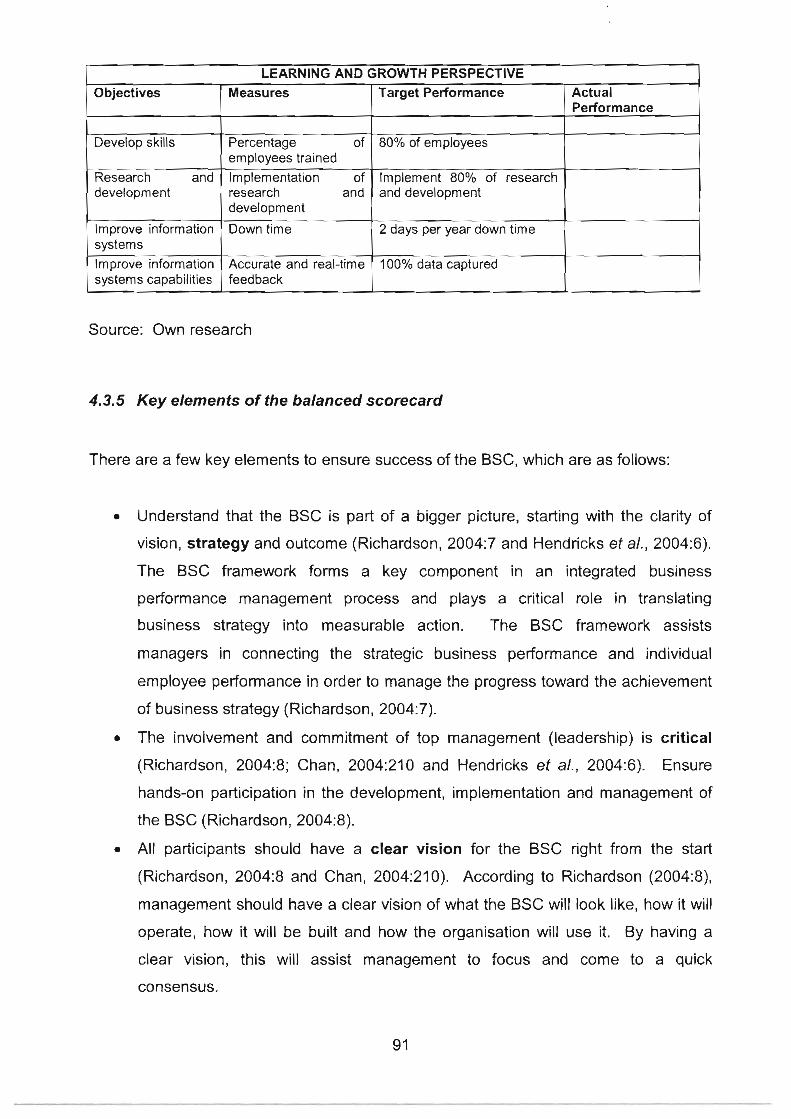

Table 4.1 : Six-dimensional performance matrix: non-financial measures

of performance

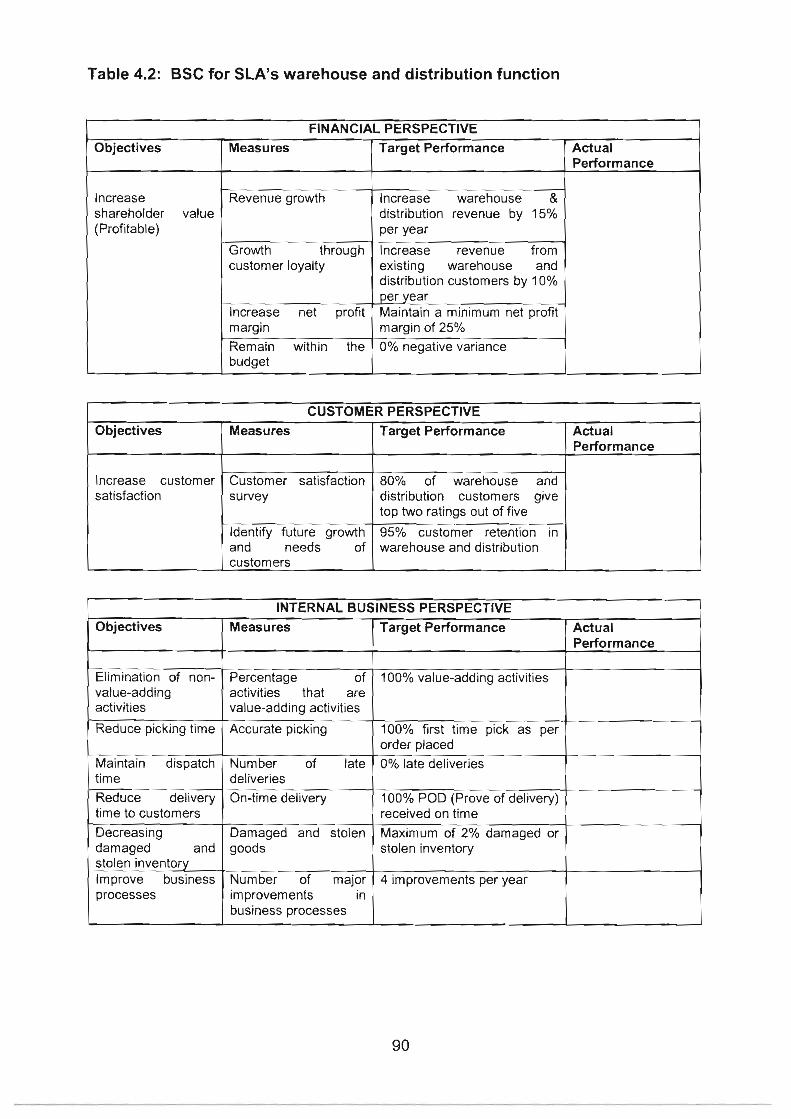

Table 4.2: BSC for SLA's warehouse and distribution function

Table 5.1: Ranking of major elements of the warehouse and

distribution's strategy

Table 5.2: Ranking of major key elements of the warehouse and

distribution's performance management.

LIST OF DIAGRAMS

Diagram 5.1 : The current position of the respondents

Diagram 5.2: Years of experience in the logistics industry

Diagram 5.3: Number of years worked for SLA

Diagram 5.4: Room for improvement regarding the profitability of the

warehouse and distribution function

Diagram 5.5: Number of employees in the warehouse and distribution

function

Diagram 5.6: Current use of an activity-based costing system

Diagram 5.7: The system currently used to allocate costs

Diagram 5.8: Effectiveness of the current cost allocation system

Diagram 5.9: Implementation of a formal system in the next two years

Diagram 5.1 0: Value-adding activities

Diagram 5.1 1 : Opi~iion on whether cost sliould be allocated to activities

Diagram 5.12: The use of ABC to determine the service fee more

accurately

Diagram 5.1 3: Changing to an ABC system

Diagram 5.14: The use of cost management tools

Diagram 5.1 5: 'The use of a formal performance management system

Diagram 5.16: Implementing performance management in the next two

years

Diagram 5.1 7: lmportance of competence

Diagram 5.18: Used as a measurement

Diagram 5.1 9: lmportance of quality of service

Diagram 5.20: Used as a measurement

Diagram 5.21 : lmportance of flexibility

Diagram 5.22: Used as a measurement

Diagram 5.23: lmportance of resource utilisa'tion

Diagram 5.24: Used as a measurement

Diagram 5.25: lmportance of innovation

Diagram 5.26: Used as a measurement

Diagram 5.27: Financial measures used for the warehouse and

distribution function

Pane

97

98

98

LIST OF DIAGRAMS (CONTINUED)

Diagram 5.28: Performance evaluation

Diagram 5.29: Training courses

Diagram 5.30: Employee informed about performance management

Diagram 5.31 : Opinion of the balanced scorecard

Diagram 5.32: Managing performance in the warehouse by using the

BSC

Diagram 5.33: Will performance management affect profitability

positively?

Diagram 5.34: Changing to the balanced scorecard

TABLE OF CONTENT

I . INTRODUCTION AND OBJEC'TIVE OF THE STUDY

1 . 1 SUGGESTED TITLE ............................................................................................... 1

1.2 BACKGROUND AND INTRODUCTION ................................................................. 1

1.2.1 The business vision of SLA .......................................................................... 2 ............................................................................... 1.2.2 Services offered by SLA 2

......................................................................................... 1.2.3 Business process 3 1.2.4 Leveraging technology ................................................................................ 6 1.2.5 SLA 's client approach ................................................................................. 6

1.3 PROBLEM STATEMENT ........................................................................................ 7

1.4 STUDY OBJECTIVE ............................................................................................... 8

1.4.1 Primary objective .......................................................................................... 8 1.4.2 Secondary objectives ................................................................................... 8

1.5 HYPOTHESIS ......................................................................................................... 9

1.6 METHOD OF RESEARCH ...................................................................................... 9

............................................................................................. 1.6.1 Literature study 9 1.6.2 Empirical study and field of research ............................................................ 9

.............................................................................. 1.7 CHAPTER CLASSIFICATION 10

2 . ACTIVITY-BASED COSTING AND ACTIVITY-BASED MANAGEMENT

2.1 INTRODUC'I-ION .................................................................................................. 11

2.2 DEFINI1-ION OF ABC ........................................................................................... 11

2.3 ABC VERSUS TRADITIONAL COSTING ............................................................. 13

2.3.1 Simple example to compare traditional costing with activity-based ........................................................................................................ costing 15

............................................................ 2.4 IMPLEMENTATION OF AN ABC MODEL 17

.................................................................................... 2.4.1 Identifying activities 17 2.4.2 Assigning costs to activity cost centres ...................................................... 19 2.4.3 Selecting appropriate cost drivers for assigning the cost of activities to

................................................................................................ cost objects 19 2.4.4 Assigning the cost of the activities to products or services ......................... 20 2.4.5 An example of implementing activity-based costing ................................... 21

xii

TABLE OF CONTENT (CONTINUED)

2.5 ADVANTAGES AND DISADVANTAGES OF -THE ABC APPROACH .................. 25

2.5. I Advantages of activity-based costing ......................................................... 25 2.5.2 Disadvantages of activity-based costing .................................................... 26

2.6 ACTIVITY-BASED MANAGEMENT ...................................................................... 27

2.6. I Defining activity-based management (ABM) .............................................. 28 2.6.2 Principles of activity-based management ............................................... 29

2.7 THE ACTIVITY-BASED COS'TING AND ACTIVITY-BASED MANAGEMENT MODEL ................................................................................................................. 31

............................................................................................................ 2.8 SUIWMARY 33

3 . COST MANAGEMENT

3.2 DEFINING COST MANAGEMENT ....................................................................... 35

3.2. I Life-cycle costing (LCC) ............................................................................. 36 3.2.2 Target costing (TC) .................................................................................. 39

3.2.2.1 An example of target costing in the warehouse and distribution function ....................................................................... 40

3.2.2.2 Value engineering ......................................................................... 41

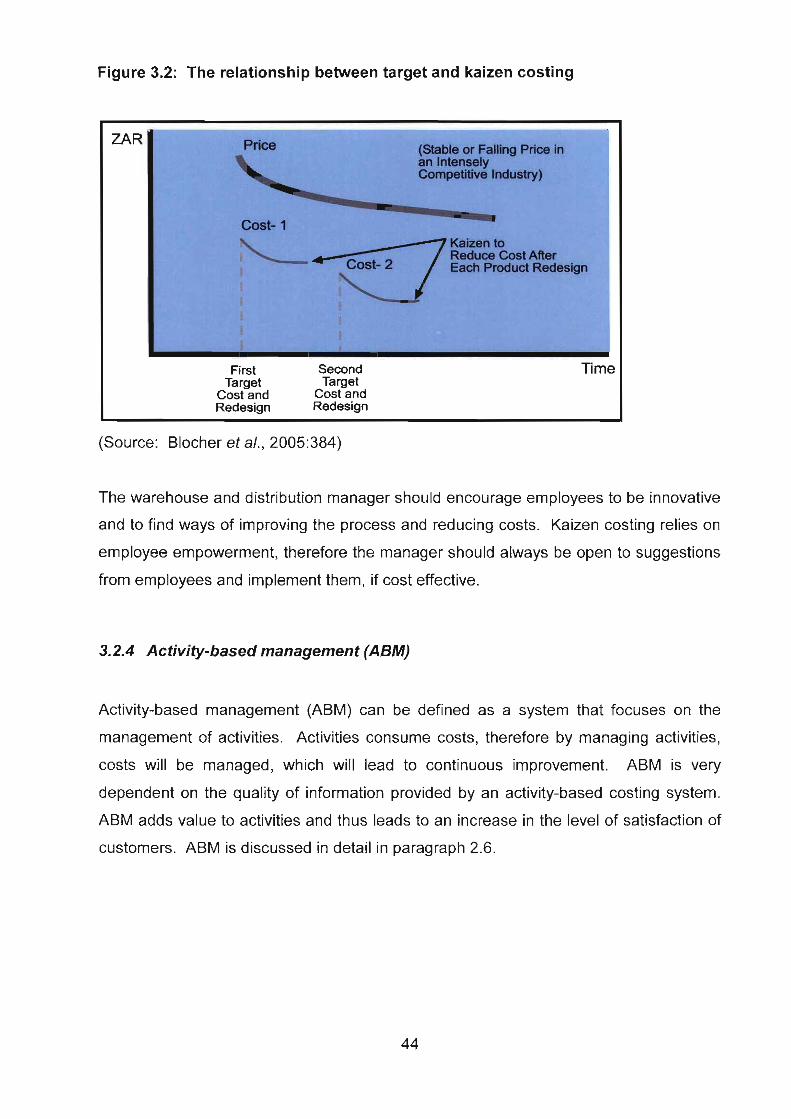

3.2.3 Kaizen costing .......................................................................................... 42 3.2.4 Activity-based management (ABM) ............................................................ 44 3.2.5 Business process reengineering (BPR) ...................................................... 45

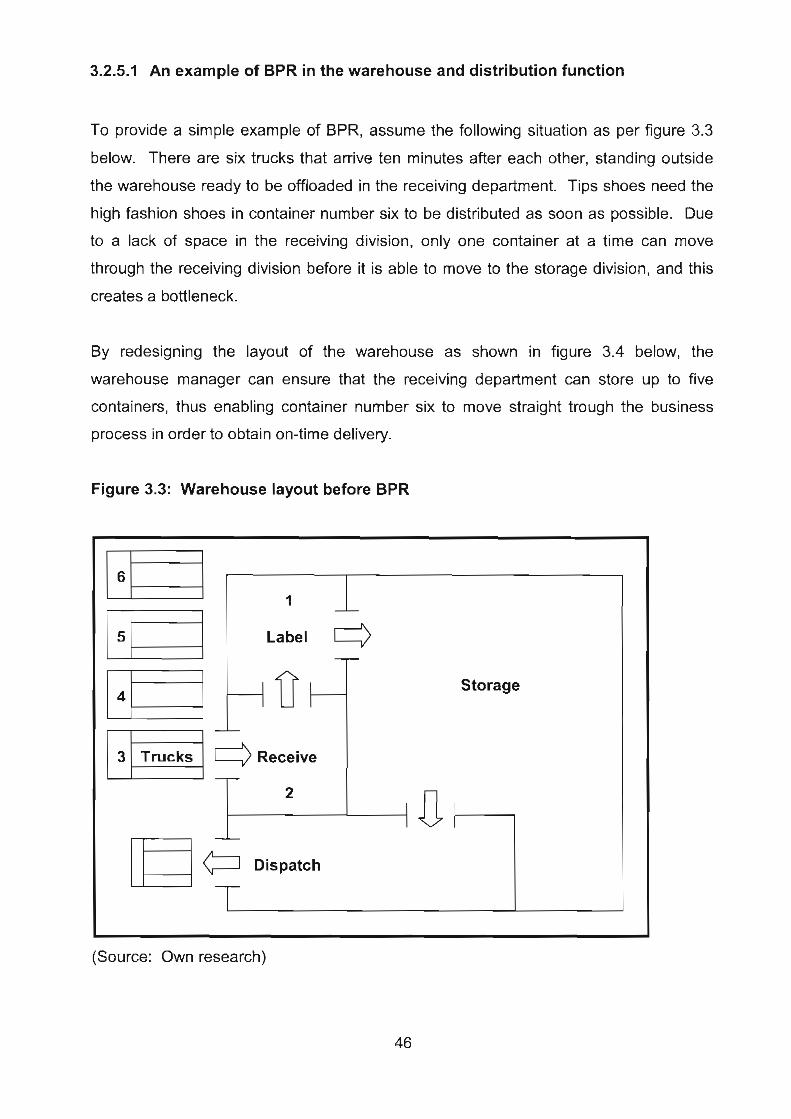

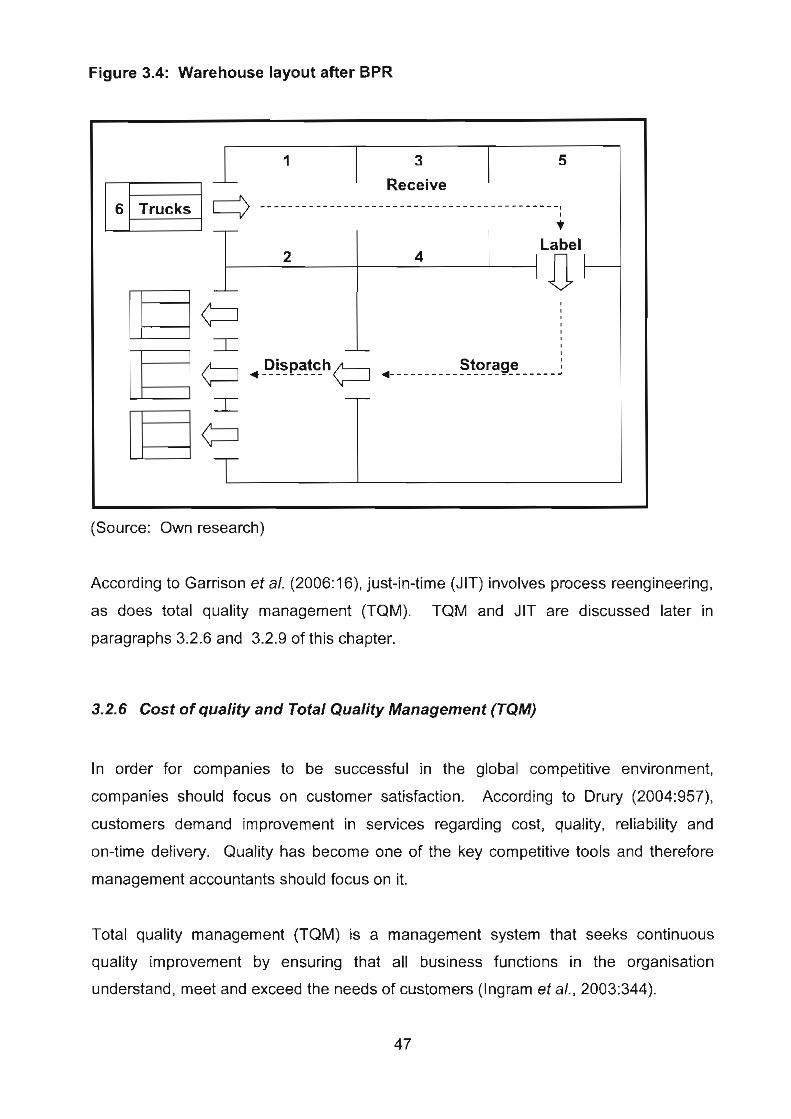

3.2.5.1 An example of BPR in the warehouse and distribution function .... 46

3.2.6 Cost of quality and Total Quality Management (TQM) ............................... 47 3.2.7 Cost management and the value chain ...................................................... 51 3.2.8 Benchmarking .......................................................................................... 55 3.2.9 Just-in-time system (JI T ) ............................................................................ 58

3.2.9.1 Just-in-time and value-adding activities ........................................ 59 3.2.9.2 Just-in-time purchasing arrangements .......................................... 60 3.2.9.3 Just-in-time performance measurement ....................................... 61

3.3 SUIWMARY ............................................................................................................ 62

xiii

TABLE OF CONTENT (CONTINUED)

4 . PERFORMANCE MEASUREMENT AND PERFORMANCE MANAGEMENT

4.2 PERFORMANCE MEASUREMENT ..................................................................... 65

4.2.1 Financial measures .................................................................................... 65

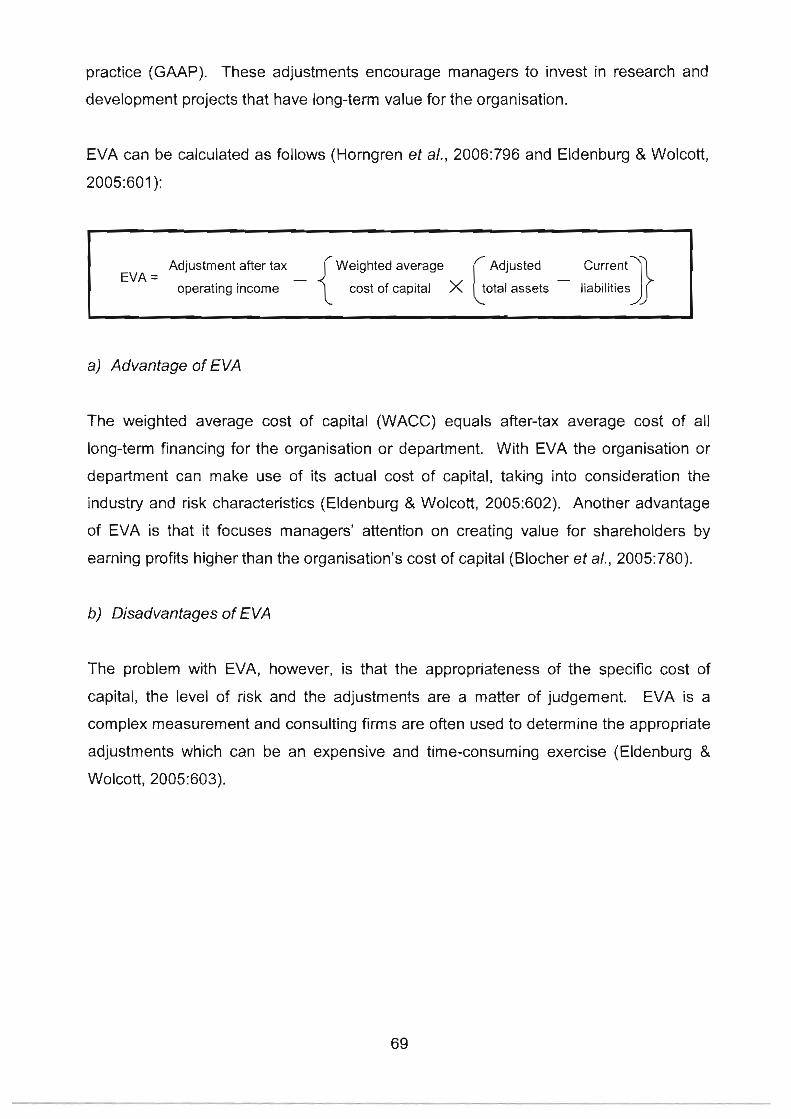

.......................................................... . 4.2.1 1 Return on investment (ROI) 66 4.2.1.2 Residual income (RI) .................................................................... 67 4.2.1.3 Economic value added (EVA) ....................................................... 68 4.2.1.4 Profit-based financial performance measurements ....................... 70

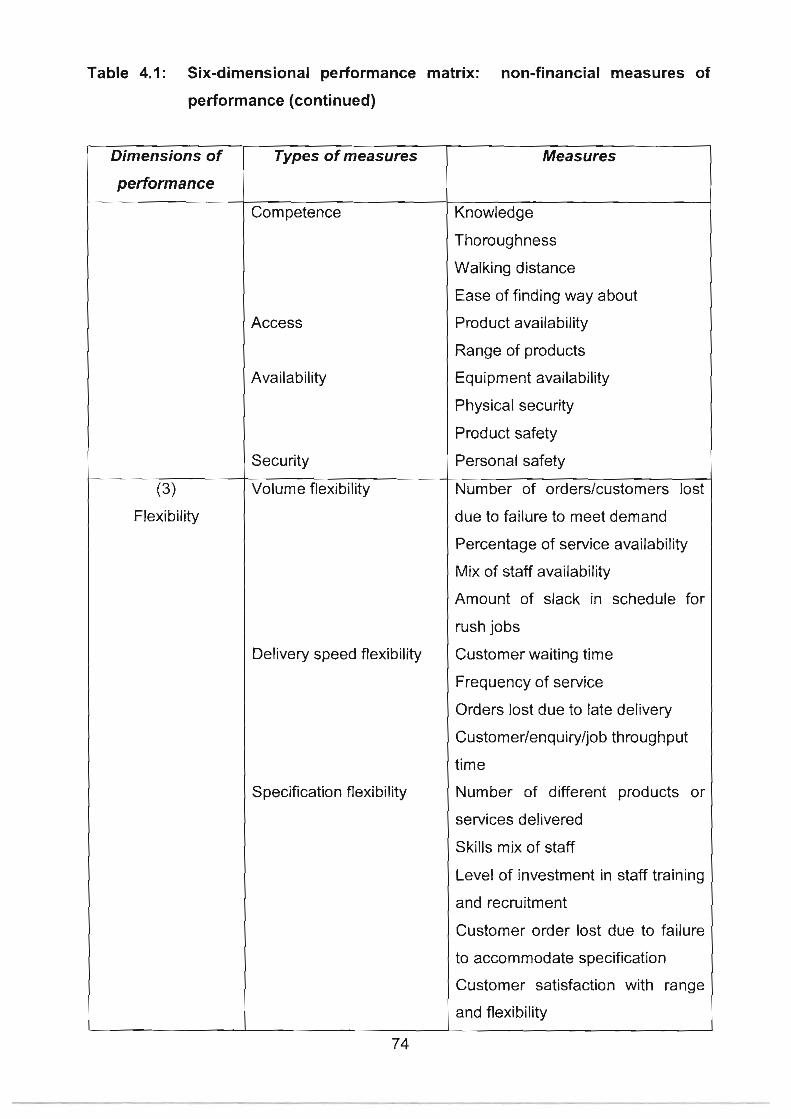

4.2.2 Non-financial measures .............................................................................. 72

4.3 PERFORMANCE MANAGEMENT ....................................................................... 76

4.3. I Defining the Balanced Scorecard ............................................................... 77 4.3.2 The four perspectives of the BSC ............................................................... 79

4.3.2.1 Financial perspective .................................................................... 79 4.3.2.2 Customer perspective ................................................................... 80 4.3.2.3 Internal business perspective ....................................................... 81 4.3.2.4 Post-sales service processes ....................................................... 85 4.3.2.5 Learning and growth perspective .................................................. 85

4.3.3 Implementing the balanced scorecard ........................................................ 87 4.3.4 An example of implementing the balanced scorecard ............................... 89 4.3.5 Key elements of the balanced scorecard ................................................... 91 4.3.6 Critical analysis of using a BSC .................................................................. 92

......................................... 4.3.6.1 Advantages of the balanced scorecard 92 4.3.6.2 Disadvantages of the balanced scorecard .................................... 93

............................................................................................................ 4.4 SUMMARY 94

5 . EMPIRICAL STUDY

5.1 INTRODUC'I'ION .................................................................................................. 96

5.2 ANALYSIS OF THE QUESTIONNAIRE ................................................................ 97

5.2. I Section A - Personal background .............................................................. 97 5.2.2 Section B - Background to the warehouse and distribution function .......... 99 5.2.3 Section C - Fundamentals ....................................................................... 102

.......................................................................................................... 5.3 SUMMARY 133

xiv

TABLE OF CONTENT (CONTINUED)

6 . CONCLUSIONS AND RECOMMENDATIONS

6.1 INTRODUCTION ................................................................................................ 135

6.2 ACTIVITY-BASED COSTING AND ACTIVITY-BASED MANAGEMENT ............ 136

. . ............................................................................... 6.2.1 Actrvrty-based costing 136 6.2.2 Activity-based management ..................................................................... 138

6.3 CONCLUSIONS AND RECOMMENDATIONS REGARDING COST MANAGEMENT .................................................................................................. 139

...................................................................................... 6.3. I Life cycle costing 139 .......................................................................................... 6.3.2 Target costing 140

.................................................................................... 6.3.3 Value engineering 140 .......................................................................................... 6.3.4 Kaizen costing 141

6.3.5 Business process reengineering .............................................................. 141 ......................................... 6.3.6 Cost of quality and Total Quality management 150

........................................................................................ 6.3.7 The value chain 150 .......................................................................................... 6.3.8 Benchmarking 151

............................................................................................... 6.3.9 Just-in-time 151

6.4 CONCLUSIONS AND RECOMMENDATIONS REGARDING PERFORMANCE MEASUREMENT AND PERFORMANCE MANAGEMENT ... 152

...................................................................... 6.4.1 Performance measurement 152

6.4.1 . 1 Financial performance measures ................................................ 153 ......................................... 6.4.1.2 Non-financial performance measures 155

6.4.2 Performance management ...................................................................... 157

6.4.2.1 The balanced scorecard ............................................................. 158

6.5 SUMMARY .......................................................................................................... 161

APPENDIX A: QUESTIONNAIRE .............................................................................. 163

BIBLIOGRAPHY ......................................................................................................... 182

CHAPTER 1

INTRODUCTION AND OBJECTIVE OF THE STUDY

1 .I SUGGESTED TITLE

Activity-based performance management at Strategic Logistical Alliance

1.2 BACKGROUND AND INTRODUCTION

Established in August 1996, Strategic Logistical Alliance (SLA) is a South African-based

third-party logistics provider operating around the globe through a network of more than

130 offices worldwide. Ownership of the business is held equally between management

and listed Italian corrlpany Savino del Bene, which has held interests in SLA since April

1999.

Based on innovation and a determination to deliver, SLA's business activities are

focused on providing an integrated logistics service to a range of business sectors.

Information technology (IT) plays a key role in realising this ambition, enabling full

control of all consignments, from collection (at the factory) to the point of delivery (SLA,

2006).

SLA's approach is one of partnership, ensuring an understanding of clients' needs and

the development of customised solutions. Something that attests to their quest for

quality is the fact that SLA obtained international standards organisation (ISO) 9002

listing in 1997, and they have maintained this status ever since (SLA, 2006).

SLA state ,that they strive to deliver the right logistics answer for every business they

serve. They are not constrained by traditional methodologies and conventions.

Instead, they thrive on thinking outside the box, applying the intellectual capital within

the business to design and irr~plement the best solution for every situation (SLA, 2006)

1.2.1 The business vision of SLA

SLA is committed to become and remain the number one third-party logistics service

provider in the local South Africa market. To this end they offer a range of standard-

setting logistics services that consistently exceed customer expectations, whether

implemented independently or as part of an integrated logistics solution (SLA, 2006).

1.2.2 Services offered by SLA

Collection

SLA controls the client's consignment through the whole of the logistics chain,

from the supplier to the recipient.

Expediting and forwarding (irnportlexport)

SLA's advanced computer-tracking system ensures the visibility of every

consignment throughout the logistics chain - a system that can be viewed on-line

24 hours a day, seven days a week. SLA also handles all the requisite

doc~~mentation - including instructions to expedite orders; routing orders; packing

lists/commercial invoices; ELIRllcertificates of origin; African Growth and

Opportunity Act (AGOA) registration in the United States of America (USA);

export clearances in countries of origin; air waybillslocean bills of lading; import

clearances; and statements of landed cost per unit.

Customs clearance

SLA has extensive clearing expertise. This, they say, together with a reputation

for compliance with customs and excise rules and regulations, has earned SLA

the trust and respect of customs offices across South Africa. SLA handles all

customs and excise matters, including obtaining clearances and permits,

applications, registrations, payments and rebates (SLA, 2006).

SLA also has experience in issues relating to the Department of Trade and

lndustry and the South African Revenue Service - including managing the

formalities and applying for refunds and drawbacks on behalf of importers. SLA

is familiar with the Motor lndustry Development Programme, and has the

know-how to manage the paperwork and administration for eligible exporters of

motor vehicles.

Warehouse management

SLA controls inventory in both their bonded warehouse (a warehouse at SLA's

premises, but under customs control) and their non-bonded warehouse (a

warehouse at SLA's premises, but not under customs control) by bar-coding and

scanning all consignments received, storage bins and consignments issued.

This allows for electronic management of the documentation and enables goods

to be tracked and traced at any stage in the process.

Local distribution

SLA delivers imports to their client's doors, striving to do so promptly and

cost-effectively.

1.2.3 Business process

Leg 1 : Origin Pick-Up

As the pick-up and placement of cargo at the relevant airport or port is the first

and vital step in the seamless flow of a shipment, SLA assumes responsibility for

this leg. SLA's extensive global presence allows them to co-ordinate shipments

according to each individual customer's tailor-made needs (SLA, 2006).

SLA also state (SLA, 2006) that they ensure that they understand their client's

country of origin pick-up requirement. SLA's central database is kept up to date

with each supplier's address details and any special requests which need to be in

place to stack cargo. SLA oversees that all the necessary equipment is in place

at the supplier's premises to load any abnormal cargo. SLA provides their

customers with relevant information regarding ETD (estimated times of

departure) for all carriers and ensure that the placement of cargo for export will

meet the required service level.

Leg 2: Origin Handling

SLA's overseas are responsible for processing overseas export formalities and

shipping documentation. SLA's overseas network was founded more than 90

years ago and it has achieved a high level of acknowledgement among customs

and port authorities in the relevant countries. Likewise, SLA respects their

partners for their high standards and expertise, which allow SLA complete peace

of mind.

Leg 3: Carrier Air and Sea

Whether SLA's clients require shipment by air, sea or road, containerised,

breakbulk (when a co~isolidated shipment arrives at the destination terminal, the

carrier must break down the many shipments in the vehicle for dispatch to the

individual consignees) or specialised, SLA advises on a continuous basis

regarding the features and benefits of the different modes of transport (SLA,

2006). SLA's priority is to ensure that their clients' uniq~re requirements are met

and that they are guided with regard to costs, risks factors and the relevant

shipping terms. Through the global network and secure relationships with

leading carriers, SLA offers its clients the buying power to manage ,their total

landing costs. Whilst their cargo is on the road, in the air or at sea, clients have

the benefit of track and trace systems that enable access to the status of

shipments (SLA, 2006).

Leg 4: Destination Handling

SLA is accredited with the South African Revenue Services (SARS). SLA has

expert knowledge of local airline procedures and South African Port Authority

requirements. SLA branches are strategically placed in Elandsfontein, Durban,

Cape Town and Port Elizabeth. Their operational staff specialises in and are

acknowledged for their dedication and hands-on approach. All premises boast

de-grouping, unpacking and bonded warehousing facilities (SLA, 2006).

Leg 5: Customs Clearing

SLA has extensive expertise in Customs Clearance (SLA, 2006). SLA records a

complete database of products and tariff codes, ensuring the accurate

processing of clearance documentation. SLA is EDI-compliant (electronic data

integration-compliant) which means that SLA guarantee entry release within 24

hours from submission. SLA has vast experience in managing

refundsldrawbacks (like customs stop or customs examination) and other

complex procedures with the International Trade Administration Commission of

SA (ITAC) or SARS. SLA is proud to have been chosen by SARS to be part of

the export pilot initiative regardirrg paperless F178 (SLA, 2006).

Leg 6: Warehousing

SLA operates beyond traditional boundaries to customise warehousing

requirements. SLA's information technology professionals design unique,

integrated electronic management system to streamline ordering and distribution

processes. SLA is the first logistics specialist in South Africa to obtain

permission from SARS to operate their computerised record-keeping system for

bonded warehouses. This system manages bonded warehouses and allows for

goods to be traded out of the bonded store on demand, whilst still complying with

SARS requirements (SLA, 2006).

Leg 7: Delivery

State of the art dispatch radios, cellular communication and satellite vehicle

tracking facilitate constant contact with SLA's fleet of vehicles, ensl-ring absolute

and time-bound efficiency (SLA, 2006).

1.2.4 Leveraging technology

Advanced information technology, developed by SLA, holds the key to the efficient

rendering of their services (SLA, 2006). Their extensive in-house information

technology department has the proven capacity and skill to develop proprietary

systems, both for SLA's purposes and to fulfil their client's specific needs.

1.2.5 SLA '3 client approach

SLA's approach is to understand their client's

required service levels and cycle times,

the volumes they move,

suppliers and end users,

lncoterms (developed by the Paris-based International Chamber of Commerce in

1936, lncoterms are internationally accepted rules defining trade terms (Coyle et

a/., 2003:388)), and

existing and potential problem areas, before devising the best solution for its

clients.

Only by understanding their clients' needs (as listed above) can SLA provide a

comprehensive door-to-door logistics service, complete with all the required paperwork,

leaving their clients to focus on their core business (SLA, 2006).

SLA currently serves a broad cross-section of industries, including 'the motor industry

(Nissan, Fiat, Ford, etc.), textiles, information technology, earthmoving equipment,

chemicals and plastics, tyres (Michelin, Pirelli, Yokohama), food products, paper,

cosmetics, catering equipment, petrochemicals, paper pulp, white goods, aviation,

ammunition, gaming and forklifts.

1.3 PROBLEM STATEMENT

SLA (2006) is committed to become and remain the number one third-party logistics

provider in the South African market. To this end SLA offers a range of standard-setting

logistics services that consistently exceed customer expectations, whether implemented

independently or as part of an integrated logistics solution. SLA is also committed to

delivering imports to their client's doors promptly and cost-effectively. SLA sets high

standards for itself, but these standards can only be achieved if the company is

profitable and financially successful.

In the era of competitive global environment and technology-based

organisations, managers are press~~red to find ways to maintain their competitive

advantage. Management has the responsibility to maintain their competitive advantage

whilst maintaining the profitability of the organisation. This responsibility includes

decisions regarding the retention of profitable customers, and the minimisation of costs

to improve profitability of services. The analysis of cost and profitability of individual

services and customers represents a critical issue with which SLA should be concerned

SLA has proved to be a market leader within the logistics services market whilst

maintaining profitability in most of its core business functions, with the exception of the

warehousing and distribution function. The reasons for a lack of profitability in the

warehousing and distribution function are inadequate planning, controlling and

decision-making within these functions. The main reasons for these problems are

incorrect cost allocations, the non-reflection of the true cost of activities, unprofitable

pricing and the lack of effective performance management.

1.4 STUDY OBJECTIVES

1.4.1 Primary objective

The primary objective of this study is to analyse the existing cost allocation system, the

cost management system and the performance management system of SLA, focusing

on the warehousing and distribution functions. The study will address the shortcomings

of the existing system and recommend Activity-Based Performance Management as a

solution.

1.4.2 Secondary objectives

Secondary objectives include the following:

1. To implement activity-based performance management systems effectively and

efficiently so as to ensure business success through continuous improvement.

2. To improve existing cost management systems and measure performance in

order to achieve an overall competitive advantage. (How can existing cost

management systems be modified and improved to optimise their effectiveness?)

3. To implement an activity-based performance management system to assist

management in decision-making, planning and controlling, by providing timely

and useful information to ensure accurate cost allocation, the ability to determine

the true cost of activities and facilitating performance management.

1.5 HYPOTHESIS

With the goal of becoming and remaining the number one third-party logistical services

provider in South Africa, SLA should focus on two strategic means to achieve and

sustain competitive advantage. The first of these is the achievement of high-quality

service levels, and the second a competitive pricing structure.

For management of SLA to achieve their goal of becoming a profitable leading

third-party logistical service provider, a combination of tools should be used, which

include activity-based costing, cost management and performance management.

Activity-based performance management will enable management to gain useful

information for decision-making to achieve their goal.

1.6 METHOD OF RESEARCH

1.6.1 Literature study

The study involved in-depth literature research of activity-based and performance

management systems, tools and relevant aspects by consulting books, journal articles,

the internet and other relevant sources.

1.6.2 Empirical study and field of research

Relevant information was obtained from SLA by means of an empirical study.

Structured interviews were used to obtain information from relevant staff and managers.

Permission to gather information by observation of activities and processes carried out

by staff in the warehouse was obtained from top management.

After completion of the questionnaires, information was analysed, followed by final

conclusions and recommendations for SLA.

1.7 CHAPTER CLASSIFICATION

Chapter 1: Introduction and objective of study. This chapter sets the background

for the study, giving a scenario for SLA. The problem statement, objective of the study,

hypothesis and method of research is set out.

Chapter 2: Activity-based costing and Activity-based management. A theoretical

framework of activity-based costing as a system is provided. A comparison between

activity-based costing and traditional costing is made. 'The steps necessary to

implement an activity-based costing system are explained and the advantages and

disadvantages of an activity-based costing system evaluated. Lastly the activity-based

costing and activity-based nianagement model is explained.

Chapter 3: Cost Management. A theoretical consideration of cost management is

provided. Different types of cost management tools are defined and evaluated.

Chapter4: Performance measurement and performance management. A

theoretical framework of Performance measurement; focussing on financial and

non-financial performance measurement, is provided. A theoretical framework for

performance mansrgement is discussed, foc~~ssing on the balanced scorecard in order

to link financial and non-financial measures. The steps necessary to implement the

balanced scorecard will be explained, key elements of the balanced scorecard will be

discussed and the advantages and disadvantages of the balanced scorecard will be

evaluated. The need to manage performance within SLA will be emphasised.

Chapter 5: Empirical study. The empirical study is set out. Findings are set out

and analysed.

Chapter 6: Conclusions and recommendations. Conclusions and

recommendations are made with regards to the activity-based performance

management in SLA.

Appendix

Bibliography

CHAPTER 2

ACTIVITY-BASED COSTING AND ACTIVITY-BASED MANAGEMENT

2.1 INTRODUCTION

The analysis of cost and profitability of individual products, services, and customers

represents a critical issue with which companies should be concerned and one where

activity-based costing (ABC) tries to help.

The shortcomings of traditional costing systems, in terms of validity, accuracy,

completeness, consistency, understanding and relevance, increased the need of

companies to refine their costing system. ABC evolved from the 1960s and the 1980s

and became one of the main ways in which companies around the globe refined their

costing systems.

ABC focuses on what is important for the organisation, and on what information is

needed to help management understand cost behaviour and absorption by

productlservices in order to make better decisions about pricing and to understand

exactly where to take actions that will drive profits. ABC does not only focus on

financial information for internal reporting but also focuses on non-financial information.

2.2 DEFINITION OF ABC

ABC is a costing method based on the principle that products and/or services require an

organisation to carry out activities and that those activities require of an organisation to

incur costs. In ABC, systems are designed so that any costs that cannot be directly

accredited to a product or service flow into the activities that makes ,the cost necessary.

The cost of each activity then flows to the product(s) or service(s) that make the activity

necessary, based on their particular use of that activity (Hicks, 1999:6 and

Griful-Miquela, 2001 :I 35).

ABC is a method of measuring the cost and performance of activities, and cost objects.

ABC assigns costs to business processes, also called activities, based on their use of

resources. The costs incurred by business processes are assigned to cost objects (i.e.

products, services, customers, etc.) based on their consumption of these processes

(activities). ABC recognises the fundamental relationship between cost drivers and

business processes (Sedgley & Jackiw, 2001 :369).

According to Horngren et a/. (2006:144-145), ABC refines a costing system by focusing

on individual activities as the essential cost objects. An activity is an event, task or unit

of work with a particular purpose; for example, designing products, setting up machines,

operating machines, and distributing products. ABC systems calculate the costs of

individual activities and assign costs by making use of cost drivers to cost objects such

as product and services on the basis of the activities needed to produce each product or

service:

Figure 2.1 : Activity-based costing

Fundamental Cost Objects Assignment to Other Cost

(Source: Horngren et a/., 2006:145)

ABC can therefore be defined as a system that calculates the costs of individual

activities and assigns costs by making use of cost drivers to cost objects such as

products and services on the basis of the activities undertaken to create each product or

service. ABC is designed to provide managers with cost information for strategic and

other decisions.

In essence, ABC uncovers the true cost of a product or service of a business.

2.3 ABC VERSUS TRADITIONAL COS'TING

Historically, companies used a traditional method of costing but during the 1980s the

limitations of traditional costing caused major publicity. These systems were realistic

when labour and materials were the two major costs involved in creating a narrow range

of products. Overhead costs were relatively small and problems which arose from

inaccurate overhead allocation were not important (Drury, 2004:374 and Beheshti,

2004:377).

Today, companies make use of modern technology and they produce many products

and services, therefore direct labour and material represent only a small portion of total

costs, while overhead costs became more important. The traditional method of costing

became insufficient for effective decision-making, whereas an ABC system generates a

more representative exarrlination of how costs are actually consumed by a product or

service within the organisation.

An overview of the major differences between traditional costing and ABC is illustrated

in figure 2.2 below.

Both these systems make use of a two-stage allocation process. In traditional costing

systems, overheads are first grouped into one or more cost pools by allocating the

overheads to production and/or service department. In the second stage it reallocates

service department costs to the production departments using an allocation base such

as direct labour cost or hours, machine hours, or number of units (Drury, 2004:372 and

Eldenburg & Wolcott, 2005:260).

In the first stage of an ABC system, the overhead costs of resources are assigned to

activity cost pools, and then activity costs are allocated to individual products or

services, using cost drivers that are chosen to reflect the use of resources (Drury,

2004:372 and Eldenburg & Wolcott, 2005:260).

The two processes are therefore very comparable, but the first stage is different as an

ABC system uses activities instead of functional departments or cost centres on which

to base costing.

Figure 2.2: An illustration of the two-stage allocation process for traditional and

activity-based costing systems

a) Traditional costing systems

(Source: Kaplan & Cooper, 1998:83 and Drury, 2004:373, adapted)

r Overhead ' f- 'l

b) Activity-based costing systems

Cost Centre "f'tb'$ "-" , b ' ~ b b e i E ; i * I h", y%. it=- 7-tZC I

Activitv Cost Drivers

Direct Materials

(Source: Kaplan & Cooper, 1998183 and Drury, 2004:373, adapted)

Overhead

Cost Centre

K

Cost Centre

2 i J

Allocations f \

4) 4,

Production

Cost Centre

1 L 1 \ 1 \ /'

Machine Hours Direct /

Direct Materials- ' Labour Products Hours

Direct Labour -\ ,

Production

Cost Centre o 2

41

Production

Cost Centre

N

2.3.1 Simple example to compare traditional costing with activity-based costing

The following example is a simple introduction to ABC. The number of departments and activities is coincidental and is used just for simplicity in this demonstration.

An organisation produces three products for which the standard quantities per unit are as follows:

Source: Wilks & Burke (2005272-273) (adapted)

Production overhead analysis per department:

Department 1 R 1,400,000.00 Department 2 R 1,800,000.00

R 3,200,000.00

Department 1 is labour intensive and department 2 is machine intensive

Total labour hours in department 7 : Total machine hours in department 2:

Production overhead analysed by activity:

Inspection R 1,400,000.00 Production scheduling/machine set-up R 1,200,000.00

R 2,600,000.00

Number of batches inspected Number of batches for scheduling and set-up

Traditional costing

Absorption rates:

Department 1 = R1,400,000.00 1 75,000

- - R 8.00 per labour hour

Department 2 = R1,800,000.00 450,000

- - R 4.00 per machine hour

Product cost statement

Activity- based costing

Cost driver rates:

Inspection = R1,600,000.00 5000

R 280.00 per inspection

Production scheduling/ machine set-up - - R1,500,000.00

800

- - R 1,500.00 per set-up

Product cost statement

Should management have applied the traditional way of costing, Product Z (Rl80lunit)

would have appeared to be more expensive than if ABC had been used. Product X

(R152lunit) would appear to be cheaper when the traditional system is used and more

expensive (R172lunit) when ABC is used. The effect of making a decision not to use

ABC (with the assumption that ABC is more accurate) will lead management to over-

price product Z (R1801unit) and under-price product X (Rl52lunit). This can lead to

major failure in an organisation. The selling price of product Z will not be market related

and will lead to low selling volumes. Product X will be sold in high volumes, but the

organisation will unknowingly be making a loss per unit of product X.

Based on the above case it is extremely important to every company to achieve and

sustain a competitive advantage. The importance of ABC and the implementation of

ABC will form the content of the rest of this chapter.

2.4 IMPLEMENTATION OF AN ABC MODEL

2.4.1 identifying activities

An ABC system makes use of activities and not cost centres or departments, like in the

case of traditional costing systems. Activities are defined as a collection of actions (or

work) performed within an organisation to produce an output. Activities are described

by verbs related to objects (Glad & Becker, 1994:18; Beheshti, 20041378 and Turney,

1996:99).

A cost hierarchy is used to identify activities and to assign costs to these activities

(Eldenburg & Wolcott, 2005:261; Drury, 2004:382-383; Lere, 2000:24-25 and Garrison

ef a!., 2006:321-322). The following are the various activities.

Unit-level activities

Unit-level activities are the activities performed for every unit of product or

service produced. The quantity of unit-level activities should be proportional to

production and sales volumes, for example direct labour and direct material.

Typical examples of cost drivers for unit-level activities will be labour hours and

machine hours.

Batch-level activities

Batch-level activities are the activities that have to be performed for a collection

of products or services, regardless of how many units are in the batch. For

example processing a customer order and arranging for a shipment to a client.

The cost of batch-related activities varies from the number of batches, but is a

fixed cost for all units within the batch. For example, the cost of processing a

customer order will be the same regardless of whether the batch contains two or

50 items.

Product-sustaining activities or service-sustaining activities

Product-sustaining activities are the activities performed to enable the production

and sales of individual products or services. These activities are not unit- or

batch-related, but are related to individual products or services. For example,

inspection of individual products or services, and technical support for individual

products or services.

Facility-sustaining or business-sustaining activities

These activities occur regardless of how many customers are served, which

products are produced, how many batches are processed or how many units are

produced. Many of these costs are fixed and typically assigned to the facility or

business as a whole, for example insurance, depreciation, arranging for loans

and providing a computer network.

2.4.2 Assigning costs to activity cost centres

Once the activities are identified, the cost of resources consumed by these activities

can be determined. The aim of ABC is to determine the "true cosr of the organisation's

activities (Closs & Goldsby, 2000:500). The activities do not involve only production

costs, but rather all costs related to the activities, for example inspection of individual

products or services and development costs should be taken into consideration. This

includes fixed and variable costs. By identifying activities in paragraph 2.4.1 and the

cost of activities, ABC seeks a greater level of detail to understand how an organisation

uses its resources.

2.4.3 Selecting appropriate cost drivers for assigning the cost of activities to

cost objects

According to Stapleton et a/. (2004:586), activities and cost objects are linked by cost

drivers, therefore a cost driver is a unit of activity that causes or influences costs (Lin

eta/., 2001 :708).

According to Drury (2004:380-381) and Kaplan & Cooper (1998:95-97), activity cost

drivers consist of three types:

1. Transaction drivers

Transaction drivers, such as the number of purchase orders and the number of

customer orders processed, provide a count of how often an activity is

performed. Transaction drivers are the least expensive cost driver and are also

expected to be the least accurate cost driver because they expect that the same

quantity of resources is necessary every time an activity is performed.

2. Duration drivers

Duration drivers represent the amount of time necessary to perform an activity.

Duration drivers are useful when significant variation exists in the amount of

activity that is required for different outputs. For example the set-up hours for a

simple product will be 20-25 minutes, but complex products can require quite a

few hours. Using a transaction driver like number of set-ups will cause an over-

costing of simple products and an under-costing of complex products. Therefore

using set-up hours as a cost driver will overcome this problem.

3. Intensity drivers

Intensity drivers directly charge for the resources used every time an activity is

performed. A complex product may require skilled personnel for set-up.

Duration drivers will determine an average hourly rate to calculate the cost of the

activity, whereas intensity drivers would record the time required from skilled

personnel and assign the specific resources directly to the product.

2.4.4 Assigning the cost of the activities to products or services

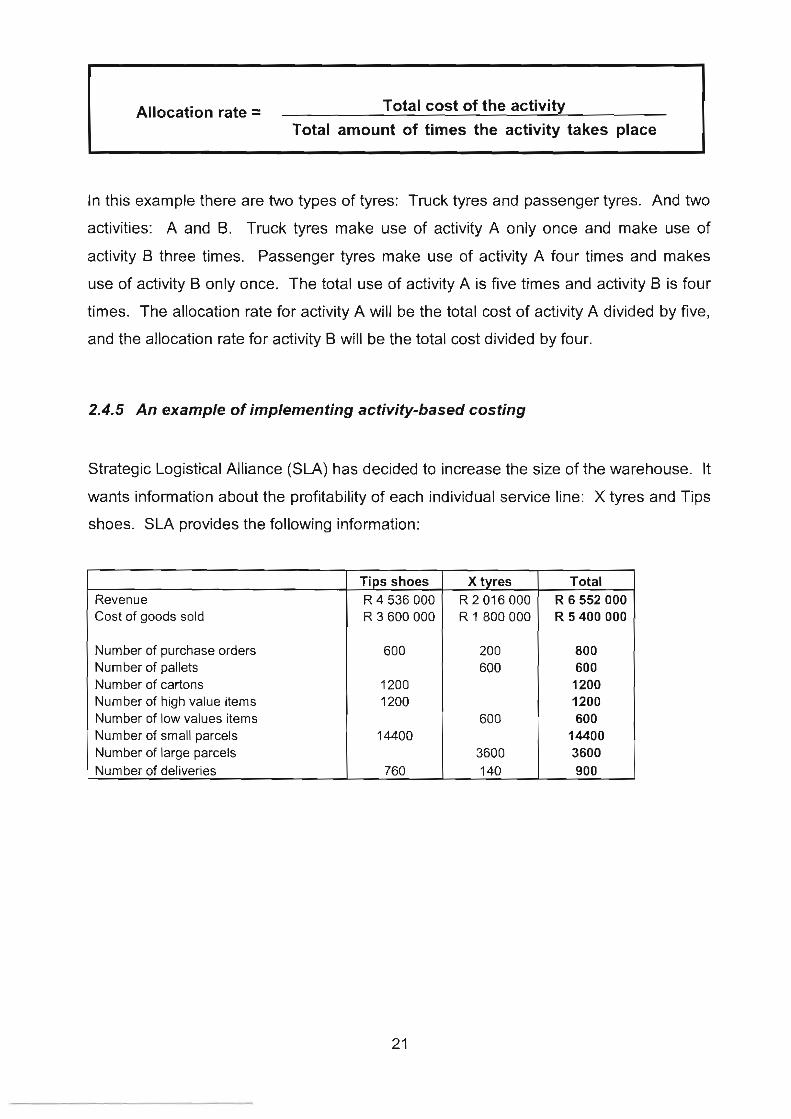

The fourth step is also known as second-stage ailocation. Activity rates are used fo

apply costs to products and customers (Garrison et a/., 2006:328-330). The allocation

rate is determined by dividing the total cost of the activity by the total amount of times

the activity takes place (Eldenburg & Wolcott, 2005265).

Allocation rate = Total cost of the activity

Total amount of times the activity takes place

In this example there are two types of tyres: Truck tyres and passenger tyres. And two

activities: A and 6. Truck tyres make use of activity A only once and make use of

activity B three times. Passenger tyres make use of activity A four times and makes

use of activity B only once. The total use of activity A is five times and activity 5 is four

times. The allocation rate for activity A will be the total cost of activity A divided by five,

and the allocation rate for activity B will be the total cost divided by four.

2.4.5 An example of implementing activity-based costing

Strategic Logistical Alliance (SLA) has decided to increase the size of the warehouse. It

wants information about the profitability of each individual service line: X tyres and Tips

shoes. SLA provides the following information:

Revenue Cost of goods sold

Number of purchase orders Number of pallets Number of cartons Number of high value items Number of low values items Number of small parcels Number of large parcels Number of deliveries

Tips shoes R4536000 R 3 600 000

600

1200 1200

14400

760

X tyres R2016000 R I 800 000

200 600

600

3600 140

Total R 6 5 5 2 0 0 0 R 5 400 000

800 600 1200 1200 600

14400 3600 900

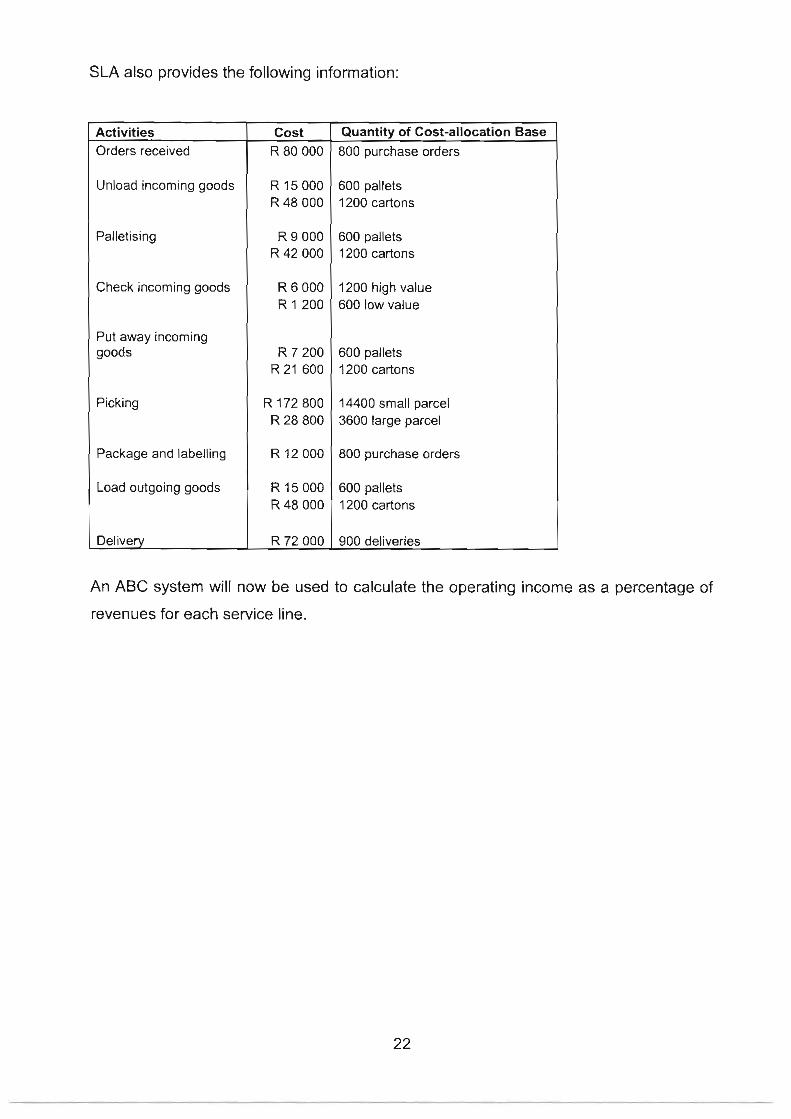

SLA also provides the following information:

Activities Orders received

Palletising

Unload incoming goods

Cost R 80 000

Put away incoming goods

Quantity of Cost-allocation Base

800 purchase orders

R 15 000 R 48 000

Check incoming goods

Picking

600 pallets 1200 cartons

R 6 000 R 1 200

1200 high value 600 low value

R 7 200 R 21 600

I Package and labelling I R 12 000 800 purchase orders I I

600 pallets 1200 cartons

R 172 800 R 28 800

14400 small parcel 3600 large parcel

1 Delivery ( R 72 000 1 900 deliveries

Load outgoing goods

An ABC system will now be used to calculate the operating income as a percentage of

revenues for each service line.

R 15 000 R 48 000

600 pallets 1200 cartons

Step 1 is to determine the activities in the warehouse as discussed in paragraph 2.4.1.

Step 2 is to assign cost to activity centres as discussed in paragraph 2.4.2. Step 3 is

selecting appropriate cost drivers for assigning the cost of activities to cost objects as

discussed in paragraph 2.4.3. Step 4 is assigning the cost of the activities to products

or service as discussed in paragraph 2.4.4; here SLA calculates cost-allocation rates for

each activity area. The activity rates are as follows:

Cost centres Receiving

Centre floor

Dispatch

identifying activities

(Step 1)

Activities Order received

Unload incoming goods

Palletising

Check incoming goods

Put away incoming goods

Picking

Package and labelling

Load outgoing goods

Delivery

Total cost

(Step 2)

Cost R 80 000

R 15 000

R 48 000

R 9 000

R 42 000

R 6 000

R 1 200

R 7 200

R 21 600

R 172 800

R 28 800

R 12 000

R 15 000

R 48 000

R 72 000

Cost drivers

(Step 3)

Cost Driver Number of purchase orders Quantity and packaging (pallets or cartons)

Quantity of pallets or cartons

Quantity and quality of supplier

Quantity and number of returns

Size of parcel picked

Num ber of orders picked

Quantity and packaging (pallets or cartons)

Quantity of deliveries

Assigning the cost of activities

(Step 4) Quantity of cost-

allocation base

800 purchase orders 600 pallets

1200 cartons

600 pallets

1200 cartons

7200 high value

600 low value

600 pallets

1200 cartons

14400 small parcel

3600 large parcel

800 purchase orders

600 pallets

1200 cartons

900 deliveries

Overhead allocation

rate Rl00 per order R25 per pal let R40 per carton R15 per pallet R35 per carton R5 per quantity R2 per quantity R12 per pallet R18 per carton R12 per parcel R8 per parcel R15 per purchase order R25 per pallet R40 per carton R80 delivery

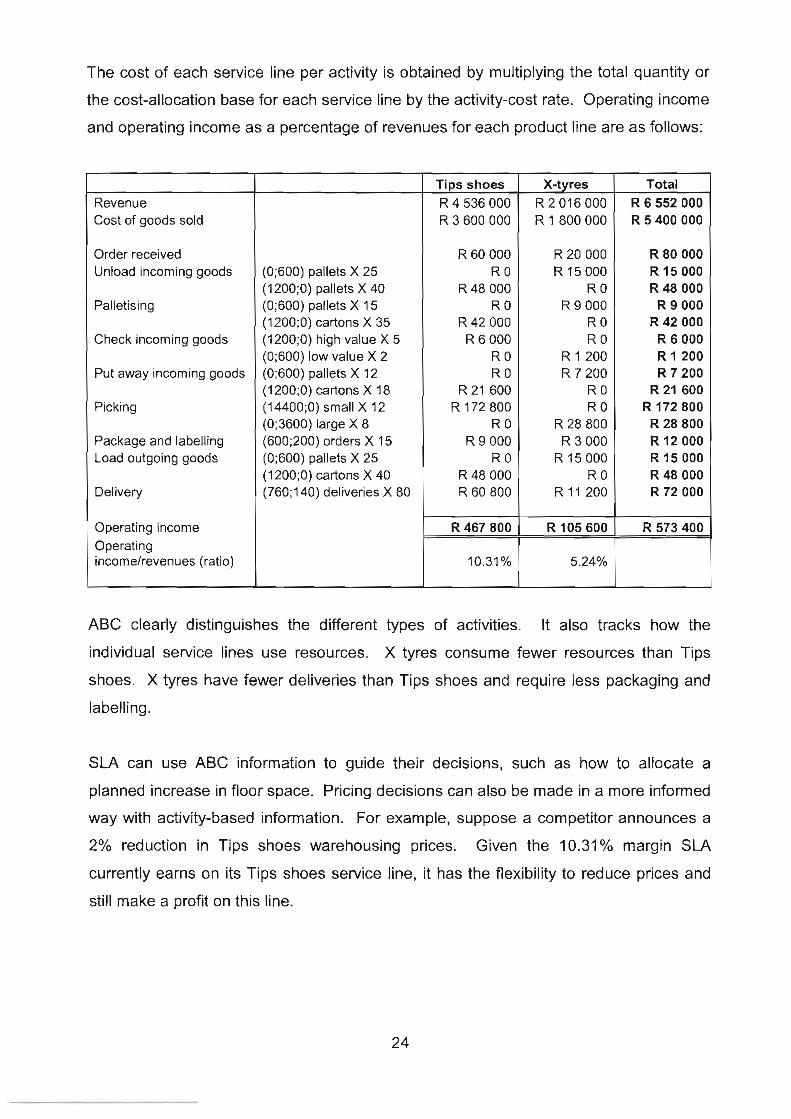

The cost of each service line per activity is obtained by multiplying the total quantity or

the cost-allocation base for each service line by the activity-cost rate. Operating income

and operating income as a percentage of revenues for each product line are as follows:

ABC clearly distinguishes the different types of activities. It also tracks how the

individual service lines use resources. X tyres consume fewer resources than Tips

shoes. X tyres have fewer deliveries than Tips shoes and require less packaging and

labelling.

Revenue Cost of goods sold

Order received Unload incoming goods

Palletising

Check incoming goods

Put away incoming goods

Picking

Package and labelling Load outgoing goods

Delivery

Operating income Operating incornelrevenues (ratio)

SLA can use ABC information to guide their decisions, such as how to allocate a

planned increase in floor space. Pricing decisions can also be made in a more informed

way with activity-based information. For example, suppose a competitor announces a

2% reduction in Tips shoes warehousing prices. Given the 10.31% margin SLA

currently earns on its Tips shoes service line, it has the flexibility to reduce prices and

still make a profit on this line.

(0;600) pallets X 25 (1 200;O) pallets X 40 (0;600) pallets X 15 (1 200;O) cartons X 35 (1200;O) high value X 5 (0;600) low value X 2 (0;600) pallets X 12 (1 200;O) cartons X 18 (1 4400;O) small X 12 (0;3600) large X 8 (600;200) orders X I S (0;600) pallets X 25 (1 200;O) cartons X 40 (760;140) deliveries X 80

Tips shoes R4536000 R 3 600 000

R 60 000 RO

R 48 000 RO

R 42 000 R 6 000

RO RO

R 21 600 R 172 800

R 0 R 9 000

RO R 48 000 R 60 800

R 467 800

10.31 %

X-tyres

R2016000 R I 800 000

R 20 000 R 15 000

RO R 9 000

RO RO

R 1 200 R 7 200

RO RO

R 28 800 R 3 000

R 15 000 RO

R 11 200

R 105 600

5.24%

Total R 6 5 5 2 0 0 0 R 5 400 000

R 80 000 R 15 000 R 48 000

R 9 000 R 42 000

R 6 000 R I 200 R 7 200

R 21 600 R 172 800 R 28 800 R 12 000 R 15 000 R 48 000 R 72 000

R 573 400

2.5 ADVANTAGES AND DISADVANTAGES OF THE ABC APPROACH

During the discussion of traditional costing systems versus ABC systems in paragraph

2.3, it became clear that traditional costing does not allocate cost accurately to

individual products or services. It is especially so where organisations:

Produce more than one product and service and where all products or services

do not make use of all the resources in the production or service line, or

make use of more indirect cost in the production or service line.

ABC has been developed to overcome the shortcomings of traditional costing systems.

It has certain advantages, and certain disadvantages, and these are discussed below.

2.5.1 Advantages of activity-based costing

ABC provides a clear picture of where resources are spent in an organisation.

ABC reduces the unpredictability in cost measurement by closely matching cost

allocations to the actual use of resources by operating activities (Stapleton ef a/.,

2004:591 and Eldenburg & Wolcott, 2005:276).

ABC helps managers focus on activity level measurement. After identifying

activities and cost drivers, managers are more aware of the cause-and-effect

relationships. This awareness motivates managers and employees to look for

ways to advance performance simply because they have more information

about the cost effects of an activity (Eldenburg & Wolcott, 2005:276).

ABC relies on a greater number of cost drivers to allocate overheads on a

cause-and-effect basis and therefore organisations can trace cost more

accurately and determine the areas andior customers that generate the greatest

profit or loss. Product and customer profitability analysis performed by the

organisation using activity-based management may significantly alter

management perceptions of the status of operations, as a more accurate and

effective allocation of costs is obtained (Drury, 2004:372-374 and Stapleton

et a/., 2004:591).

ABC identifies value-adding activities. Value-adding activities are those

activities that add value from the customer's point of view (Griful-Miquela,

2001 :I 36).

ABC helps managers identify non-value-adding activities so that they can be

improved to add value from the customer's point of view or so that the activity

can be eliminated (Stapleton et a/., 2004:591).

ABC identifies many activity costs that are not directly linked to production at all

but are traditionally allocated to products as production cost. On the other hand,

it identifies many marketing, selling and administrative costs that should be

included to establish better pricing estimates (Stapleton et at., 2004:592).

2.5.2 Disadvantages of activity-based costing

According to Horngren ef a/. (2006:157), the main costs and limiting factors of an

ABC system are the measurements necessary to implement the system. Cost-

allocation bases require management to estimate costs of activity pools and to

identify and measure cost drivers for these pools. ABC systems require many

calculations to determine costs of products and services. These measurements

are costly and rates need to be updated regularly.

Due to the lengthy procedures which ABC entails, it can be a very

time-consuming procedure (Stapleton et al., 2004:592).

It is not appropriate for every organisation; firms with low overhead costs will not

benefit from an ABC system (Stapleton eta/., 2004:592).

ABC is a very complex system, due to the near impossibility of tracking and

attaching every resource cost to a particular activity. Hundreds and possibly

thousands of activities take place in organisations every day. Some activities

may not be identifiable or quantifiable without a great amount of effort (Lin et a/.,

2001 :710).

Most organisations ask the following question: Are the costs of implementing an ABC

system worth the benefits achieved? ABC is clearly a more complicated and expensive

costing approach but the benefits of this system definitely justify these inputs.

2.6 ACTIVITY-BASED MANAGEMENT

To achieve continuous improvement, managers should remain informed. Managers

need timely and accurate information about the activities (work) done and the objects of

these activities (the products and the customers). This is what ABC is all about as

discussed throughout chapter 2. Obtaining good quality information is only one half of

the challenge. The key to success is putting ABC information to work to identify

appropriate strategies, improve product design, and remove waste from operating

activities (Turney, 1996: 139).

Using ABC to improve an organisation is called activity-based management (ABM) and

will form the content of the rest of this chapter.

2.6.7 Defining activity-based management (ABM)

According to Horngren et a/. (2006:A 52-1 55), activity-based management (ABM)

describes management decisions that use ABC information to please customers and

advance profitability, and more broadly defines ABM to include decisions about:

pricing and product mix,

how to reduce costs,

how to improve processes, and

product design.

According to Eldenburg & Wolcott (2005:270), ABM makes use of ABC information to

calculate the costs and benefits of production and internal activities and to identify and

implement opportunities for improvement in profitability, efficiency and quality within an

organisation.

ABC can be used to identify areas that would gain from process improvement, and

when ABC is used in this manner it is called ABM. ABM focuses on managing activities

to eliminate waste and reducing delays or defects (Garrison et a/., 2006:335).

ABM can be defined as a system that focuses on the management of activities.

Activities consume costs, therefore by managing activities, cost will be managed, which

leads to continuous improvement. ABM is very dependent on the quality of information

provided by ABC. ABM adds value to activities and thus leads to an increase in the

level of satisfaction of customers.

2.6.2 Principles of activity-based management

ABM is directly aimed at two goals. The first goal is to satisfy customers' needs by

improving the value of the product or service received by the customer. The second

goal is to improve profits by making fewer demands on organisational resources. These

goals will be obtained by managing activities (Drury, 2004:951 and Turney, 1996:141).

Knowing the cost of activities highlights those activities with the highest cost so that

management can prioritise the analysis of these activities so that they can be eliminated

or performed more efficiently.

Turney (1996:146) recommend using a Pareto rule to identify the activities with the

greatest potential for improvement. Pareto's rule or the 80120 rule states that 20% of

the activities cause 80% of the cost (Turney, 1996:146 and Wayne & Searcy, 2004:51).

This will help management identify activities that need to be analysed. Another way of

dealing with activities is to classify them as either value-adding or non-value-adding

activities.

Value-adding activities

A value-adding activity is an activity that customers recognise as adding value to

the product or service they purchase. For example, on-time deliveries of the right

quality and quantity will be a value-adding activity for the client. Other definitions

include an activity that is performed as efficiently as possible and/or an activity

that is in line with the primary objective of producing outputs (Drury, 2004:955

and Griful-Miquela, 2001 :I 36).

Non-value-adding activities

A non-value-adding activity is an activity that does not add value to a

product/service and therefore is unnecessary and can be reduced or eliminated.

This is an opportunity for cost reduction, without fotfeiting the value or quality of

the product or service to the customer (Drury, 2004:955 and

Griful-Miquela, 2001:136). For example, a third hundred percent audit check

(inspection) of inventory that has been previously picked and audited will be a

non-value adding activity in the warehouse.

According to Drury (2004:955), a value-adding or non-value-adding activity can be

classified in terms of the following five point scale.

1 Highly efficient, with little opportunity for improvement

2. Moderately efficient, with a few opportunities for improvement

3. Of average efficiency, with reasonable opportunity for improvement

4. Inefficient, with plenty of opportunities for improvement

5. Highly inefficient, should maybe not be done at all, opportunity for improvement

By identifying the cost of activities that make up the organisation and classifying them

into the above five categories, opportunities for cost reduction can be identified and

prioritised. Cost reduction can be achieved by eliminating the activities, performing

them more efficiently with fewer resources or redesigning them so that they are

performed entirely differently and more efficiently, also in terms of cost.

2.7 THE ACTIVITY-BASED COSTING AND ACTIVITY-BASED MANAGEMENT

MODEL

Figure 2.3 below illustrates a graphical model of activity-based performance

measurement. This model is defined by Turney (1 996:81) as second-generation ABC.

This model has three main views:

Figure 2.3: The activity-based costing model

Cost assignment

(Source: Turney, 1996:81 and Drury, 2004:392, adapted)

ABM view (indicated by the circle) illustrates the interrelationship between ABC

and ABM. ABC provides the information needed to manage activities. ABM

uses the information provided by activity-based costing as the route to

continuous improvement.

The cost assignment view (indicated by the vertical box). The vertical box

relates to product or customer costing, where costs are first assigned to

activities, and then to cost objects. The resources and activity drivers within the

model reflect the total time or other resources consumed in performing a specific

activity (La Londe & Ginter, 1999:17). Thus the vertical box focuses on financial

information. This information is important in order to analyse critical decisions.

These decisions include pricing, product mix, sourcing, product-design decisions

and setting priorities for improvement efforts.

The process view (indicated by the horizontal box). The horizontal box reflects

information about events that influence the performance of activities and activity

performance. What causes work and how well it is done? Thus the horizontal

box focuses on non-financial information. Organisations use this information to

help improve performance and the value received by customers.

This model indicates the connection between financial and non-financial information.

This connection enables performance to be translated into cost information and into

how performance affects process costs or profitability. Improved performance can also

be translated into a revised activity cost that requires fewer resources. The vertical box

or cost view of ABC allows the activity cost to be translated into changes in necessary

resources or into customer or product or service cost (La Londe & Ginter, 1999:17).

The aim of this chapter was to look at how ABC can be used to provide relevant

information for decision-making by more accurately assigning costs to cost objects.

ABM was also discussed to see how the information provided by ABC is used by ABM

to manage activities. Cost management and performance measurementtmanagement

are considered more valuable than pure financial evaluation to evaluate overall

organisational performance (Burk & Douglas, 1994:17). This statement will be

explained in Chapters 3 and 4.

2.8 SUMMARY

Knowledge of product cost or service cost is critical for any organisation that hopes to

maintain, or improve, its competitive advantage. This is especially true in small and

mid-sized organisations that face ever-increasing pressure from their key customers

continually to reduce the price of their products and services.

Traditional cost accounting methods suffer from several defects that can result in

distorted cost for decision-making purposes. All manufacturing costs - even those that

are not caused by any specific product - are allocated to products. Traditional methods

also allocate the costs of idle capacity to products. In effect, products or services are

charged for resources that they don't use. And finally, traditional methods tend to place

too much reliance on unit-level allocation bases, such as direct labour and

machine-hours. This results in over-costing high-volume products and under-costing

low-volume products and can lead to mistakes when making decisions.

ABC estimates the costs of the resources consumed by cost objects such as products

and customers. The approach taken in ABC assumes that cost objects generate

activities that in turn consume costly resources. Activities form the link between costs

and cost objects. ABC is concerned with overhead costs. The accounting for direct

labour and direct material is usually unaffected.

To build an ABC system, managers should choose a set of activities that summarises

much of the work performed in overhead departments and associate that with each

activity-cost pool. The remaining overhead costs are assigned to the activity-cost pools

in the first-stage allocation.

An activity rate is computed for each cost pool by dividing the costs assigned to the cost

pool by the measure of activity for the cost pool. Activity rates provide useful

information to managers concerning the costs of carrying out overhead activities. A

particularly high cost for an activity may trigger efforts to improve the way the activity is

carried out in the organisation.

In the second-stage allocation, the activity rates are used to apply costs to cost objects

such as products and customers. The costs computed under ABC are often quite

different from the costs generated by a company's traditional cost accounting system.

While the activity-based costing system is almost certainly more accurate, managers

should nevertheless exercise caution before making decisions based on activity-based

costing data. A vital part of any activity-based analysis of product or customer

profitability is an action analysis that identifies who is ultimately responsible for each

cost and the ease with which the cost can be adjusted.

CHAPTER 3

COST MANAGEMENT

3.1 INTRODUCTION

The aim of chapter 2 was to look at how activity-based costing can be used to provide

relevant information for decision-making by more accurately assigning costs to cost

objects. According to Drury (2004:391), activity-based costing can be used for a range

of cost management applications. The vertical box as illustrated in figure 2.3 in

paragraph 2.7 relates to product or customer costing, where costs are first assigned to

activities and then to cost objects. According to Drury (2004:391), the horizontal box as

illustrated in figure 2.3 in paragraph 2.7 relates to cost management, where a process

approach is adopted and costs are allocated to activities. This represents the basis for

cost management applications.

Therefore activity-based costing should not only be used to provide relevant information

for decision-making, but should also represent the basis for cost management

applications. Cost management will be discussed in this chapter.

3.2 DEFINING COST MANAGEMENT

According to Horngren et a/. (2006:Z-3), cost management describes the activities of

managers in the short- and long-term in which they

(i) implement programmes to control decisions that minimise costs of products or

services, and

(ii) increase the value or quality of the products or services to ensure customer

satisfaction.

Cost management forms an important part of management strategies and their

implementation.

Cost management focuses on cost reduction rather than cost control. Traditional

cost-control systems are applied on a continuous basis, while cost management tends

to be applied on an ad hoc basis when cost reduction opportunities are identified.

Cost-control systems rely heavily on accounting techniques, whereas cost management