active lifestyle sector - d. a. davidson & co.davidsoncompanies.com/advertising/ecm/ib... ·...

TRANSCRIPT

Strictly Private & Confidential

Active Lifestyle Sector Quarterly Review | Spring 2016 Merger, acquisition, and valuation trends in the public

and private active lifestyle markets

BALTIMORE – CHICAGO – DENVER – GREAT FALLS – ORANGE COUNTY – PORTLAND – SALT LAKE CITY – SEATTLE

Private and Confidential | 2 www.davidsoncompanies.com/ecm/ Page 2

DAVIDSON TEAM

Active Lifestyle Execution Team

Mike Smith Managing Director, Co-Head of Active Lifestyle Investment Banking

(206) 903-8679 [email protected]

Jason Lippenberger Vice President Investment Banking

(206) 903-8672 [email protected]

Nathan Neubauer Analyst Investment Banking

(206) 903-8675 [email protected]

Kirk Swanson Analyst Investment Banking

(206) 903-8676 [email protected]

Private Equity Coverage Bryan Cummings Managing Director, Head of Private

Equity Coverage

(714) 850-8339 [email protected]

Brien Rowe Managing Director, Co-Head of Active Lifestyle Investment Banking

(714) 850-8335 [email protected]

Raya Raphael Analyst Investment Banking

(714) 850-8353 [email protected]

Jacqueline Millen Associate, Private Equity Coverage

(714) 850-8336 [email protected]

Selected Transactions

Sell-Side Advisor

has been acquired by

Sell-Side Advisor*

has been acquired by

has entered a strategic

partnership with

Sell-Side Advisor

Co-Manager

$1.0 billion

Secondary Offering

Sell-Side Advisor*

has been acquired by

Shanghai Acquisition

Corporation

Sell-Side Advisor

has been acquired by

Kanders & Company

Sell-Side Advisor

has been acquired by

Co-Manager

$126.5 million

Secondary Offering

Sell-Side Advisor

has been acquired by

Sell-Side Advisor

has been acquired by

Sell-Side Advisor*

has been acquired by

Sell-Side Advisor

has been acquired by

Sell-Side Advisor*

has completed a

recapitalization with

Sell-Side Advisor*

has completed a

recapitalization with

Buy-Side Advisor*

together with

Acquired

Fox Head, Inc.

* Transactions completed by current D.A. Davidson professional prior to joining the firm.

Sell-Side Advisor

have been acquired by

Private Investors

Buy-Side Advisor

has acquired

Co-Manager

$132.1 million

Initial Public Offering

has been acquired by

Sell-Side Advisor

a portfolio company of

Co-Manager

$76.6 million

Secondary Offering

Private and Confidential | 3 www.davidsoncompanies.com/ecm/ Page 3

SECTOR SCORECARD: COMPARABLE PUBLIC COMPANIES

Stock Performance(1)

TEV/LTM EBITDA

Valuation(2)

Source: S&P Capital IQ, data as of 3/14/16.

(1) Detail on public companies on pages 12 – 14.

(2) Enterprise value / LTM EBITDA (median and range) Note: Enterprise value is defined as market capitalization plus net debt .

17.1x

4.8x

11.9x

6.6x

20.1x

7.4x

12.4x

18.3x

5.4x

9.5x

18.0x

6.2x

12.2x

19.7x

6.7x

10.2x

19.3x

3.6x

7.1x

24.2x

7.6x

9.8x

S&P 500 Accessories Active Apparel Fashion Apparel Equipment Footwear Retail Tactical

90 Days (1.0)% 11.5% 5.8% 13.3% (3.2)% 3.9% 6.4% 2.6%

180 Days 1.3% 3.0% (11.2)% (0.4)% (11.6)% (11.4)% (4.1)% 1.2%

1-Year (1.5)% (9.7)% (5.4)% (3.4)% (14.8)% (1.4)% (12.5)% 5.7%

3-Year 29.4% 0.5% 58.8% 27.3% 27.1% 35.5% 2.8% 64.1%

Private and Confidential | 4 www.davidsoncompanies.com/ecm/ Page 4

CURRENT EVENT INSIGHTS & COMMENTARY

Active Lifestyle stocks appreciate in February, beating the S&P 500(1) – On average, Active Lifestyle stocks increased 3.5% in February,

beating both the S&P 500, which decreased 0.4%, and the S&P 500 Consumer Index, which rose 0.2%. Year-to-date, Active Lifestyle stocks

are up 0.8%, outperforming both the S&P 500 (-5.5%), and the broader Consumer Index (-5.1%). On a 12 month rolling basis, the

Active Lifestyle space has declined 7.2% on average, outpacing the S&P 500’s 8.2% loss, but trailing the S&P 500 Consumer Index’s

1.9% decline.

The retail landscape is rapidly evolving and forward looking retailers are the winners – Retailers will continue to adopt and deploy new

technology in order to remain competitive. Cloud technology will be one of the technologies that retailers will embrace in the coming few years.

Additionally, the Internet of Things (IoT) is set to disrupt the retail industry even further by enabling the collection and analysis of data. This

technology will equip retailers with a powerful tool that will allow them to create, collect, and act upon new sorts of data, giving them the

opportunity to alter future action in valuable ways.

Currency translation headwinds remain, but paused in February – During the month of February, the USD appreciated against the GBP

(+3.0%) and EUR (+0.1%), and depreciated against the AUD (-1.0%), CAD (-3.3%), and JPY (-6.8%). The strong dollar is boosting U.S.

consumers' purchasing power, yet exerting pressure on the sales of companies who export, manufacture overseas, or sell to large multinational

companies.

Macroeconomic pressures hit luxury stores in the U.S. – A volatile stock market, weak global growth, and a stronger U.S. dollar have

hampered luxury stores’ sales. As the new year begins, the U.S. dollar continues to appreciate against major currencies, discouraging

foreigners from visiting and spending in the United States. Additionally, China’s slowdown has also adversely affected luxury stores’ sales.

According to China Daily, consumers in China spent $116.8 billion (or 46% of the global volume of high-end goods) on luxury goods abroad in

2015. With a less than ideal start to 2016 for the U.S. stock market and continued volatility in the Chinese stock market, luxury

retailers will be challenged in the year ahead.

(1) Active Lifestyle space based on D.A. Davidson research coverage: BDE, CAB, COLM, ELY, FOXF, GIL, HBI, JAH, LULU, NKE, NLS , PSG, SKUL, SPWH, UA, VFC, WWW. Data as of 3/1/16.

Source: D.A. Davidson Equity Research, Women’s Wear Daily, Deloitte, China Daily.

Industry Insights

Private and Confidential | 5 www.davidsoncompanies.com/ecm/ Page 5

INDUSTRY INSIGHT & TRENDS: OVERVIEW

Middle market M&A continues improvement – Middle market M&A activity increased for the third consecutive quarter, with the

number of transactions and dollar volume rising 8.6% and 7.3%, respectively, in Q4 2015 versus Q3 2015. However, middle

market M&A activity for 2015 is down significantly from 2014 - dollar volume is down 25.6% and overall transactions are down

32.3%.

Consumer M&A beating overall market – While overall middle market M&A activity has dropped significantly in 2015 compared to

2014, middle market consumer M&A activity has only dipped slightly. Deal count is down 9.9% and dollar volume is down 5.5%

in 2015 compared to 2014.

Leisure Products industry outperforms – Leisure Products has been one of the best performing industries since the start of the

2016, up 18.8%. The YTD worst performing industries include Real Estate Management and Development, Biotechnology, and

Banks.

IPO market lost momentum – Continued volatility in the equity markets resulted in a significant slowdown in public offering activity,

with the IPO market experiencing the steepest declines. In 2014 $57.8 billion was raised through 233 IPOs, compared to 2015

where these figures dropped to $32.5 billion raised through 149 IPOs.

Major indices continue struggle – Tepid economic data and company earnings coupled with commodity price fluctuations

contributed to further volatility in the U.S. equity markets. YTD as of March 14, 2016 the S&P 500 Index and the Russell 2000 Index

are down 1.2% and 4.5%, respectively.

Debt and equity levels – The debt proportion of deals completed during the final quarter of 2015 was 58.0%, a significant jump

compared to the 49.7% figure clocked in 3Q and exceeding any other quarter of the year. This reinforces the point that dealmakers

are still willing to pay premiums for certain transactions, as well as the availability of debt higher up in the quality spectrum.

Leverage for large deals challenging – Industry conversations suggest debt syndication is down, which makes financing for large

deals more challenging. Middle market transactions are less affected.

Note: Middle-market defined as transactions between $10 and $500 million where pricing is disclosed.

Source: D.A. Davidson “DealMaker” Report, PitchBook, S&P Capital IQ.

M&A and Public Offering Trends

Private and Confidential | 6 www.davidsoncompanies.com/ecm/ Page 6

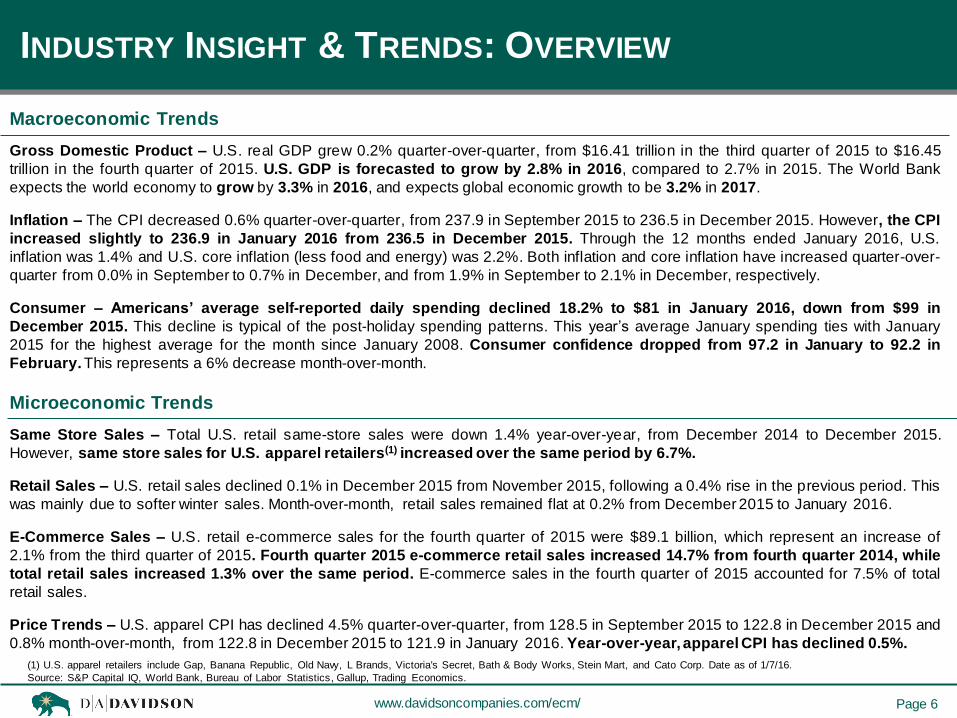

INDUSTRY INSIGHT & TRENDS: OVERVIEW

Gross Domestic Product – U.S. real GDP grew 0.2% quarter-over-quarter, from $16.41 trillion in the third quarter of 2015 to $16.45

trillion in the fourth quarter of 2015. U.S. GDP is forecasted to grow by 2.8% in 2016, compared to 2.7% in 2015. The World Bank

expects the world economy to grow by 3.3% in 2016, and expects global economic growth to be 3.2% in 2017.

Inflation – The CPI decreased 0.6% quarter-over-quarter, from 237.9 in September 2015 to 236.5 in December 2015. However, the CPI

increased slightly to 236.9 in January 2016 from 236.5 in December 2015. Through the 12 months ended January 2016, U.S.

inflation was 1.4% and U.S. core inflation (less food and energy) was 2.2%. Both inflation and core inflation have increased quarter-over-

quarter from 0.0% in September to 0.7% in December, and from 1.9% in September to 2.1% in December, respectively.

Consumer – Americans’ average self-reported daily spending declined 18.2% to $81 in January 2016, down from $99 in

December 2015. This decline is typical of the post-holiday spending patterns. This year’s average January spending ties with January

2015 for the highest average for the month since January 2008. Consumer confidence dropped from 97.2 in January to 92.2 in

February. This represents a 6% decrease month-over-month.

Same Store Sales – Total U.S. retail same-store sales were down 1.4% year-over-year, from December 2014 to December 2015.

However, same store sales for U.S. apparel retailers(1) increased over the same period by 6.7%.

Retail Sales – U.S. retail sales declined 0.1% in December 2015 from November 2015, following a 0.4% rise in the previous period. This

was mainly due to softer winter sales. Month-over-month, retail sales remained flat at 0.2% from December 2015 to January 2016.

E-Commerce Sales – U.S. retail e-commerce sales for the fourth quarter of 2015 were $89.1 billion, which represent an increase of

2.1% from the third quarter of 2015. Fourth quarter 2015 e-commerce retail sales increased 14.7% from fourth quarter 2014, while

total retail sales increased 1.3% over the same period. E-commerce sales in the fourth quarter of 2015 accounted for 7.5% of total

retail sales.

Price Trends – U.S. apparel CPI has declined 4.5% quarter-over-quarter, from 128.5 in September 2015 to 122.8 in December 2015 and

0.8% month-over-month, from 122.8 in December 2015 to 121.9 in January 2016. Year-over-year, apparel CPI has declined 0.5%.

Macroeconomic Trends

Microeconomic Trends

(1) U.S. apparel retailers include Gap, Banana Republic, Old Navy, L Brands, Victoria's Secret, Bath & Body Works, Stein Mart, and Cato Corp. Date as of 1/7/16.

Source: S&P Capital IQ, World Bank, Bureau of Labor Statistics, Gallup, Trading Economics.

Private and Confidential | 7 www.davidsoncompanies.com/ecm/ Page 7

$6.0

$4.1 $4.3

$2.5

$5.6

$3.3

$6.1

$2.8

$6.5

$2.1

$4.6

$5.3

$4.5

$3.8

$8.2

$2.1

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

$8.0

$9.0

Consumer Energy &Utilities

Financials Healthcare Industrials& Materials

Real Estate Technology& Telecom

Other

Q4 2014 Q4 2015

Middle Market Consumer M&A Deal Activity

Middle Market M&A Transactions

MIDDLE MARKET MERGER & ACQUISITION TRENDS

Middle Market M&A by Industry

Middle Market Consumer EV/EBITDA Multiples

U.S. COMPANIES

Note: Middle-market defined as transactions between $10 and $500 million where pricing is disclosed. Deals in this report are for announced transactions in the quarter of interest involving U.S. based companies. Source: S&P Capital IQ.

($ in billions) ($ in billions)

($ in billions)

$3

4.4

$4

2.6

$3

9.1

$5

0.8

$2

9.0

$3

7.9

$4

5.0

$5

2.6

$4

0.0

$5

2.3

$3

7.4

$3

4.7

$2

5.0

$2

5.6

$3

4.6

$3

7.1

461

541 588

678

438

513

655 680

567

680

365 337

283 312

347 377

0

100

200

300

400

500

600

700

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2012 2013 2014 2015

Volume ($B) Deal Count

11.3x

12.7x

9.1x

13.1x 13.6x

9.3x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

2010 2011 2012 2013 2014 2015

$2

2.5

$2

7.9

$3

0.7

$2

8.8

$3

1.4

$2

9.7

308

347 366 376

393

354

0

100

200

300

400

500

$10.0

$15.0

$20.0

$25.0

$30.0

$35.0

2010 2011 2012 2013 2014 2015

Volume ($B) Deal Count

Private and Confidential | 8 www.davidsoncompanies.com/ecm/ Page 8

4.2x 4.3x 4.5x

4.8x

5.3x 5.3 5.1x

4.7x

5.2x 5.3x 5.4x

5.8x 5.7

5.2x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

2010 2011 2012 2013 2014 2015 Q4 2015

Middle Market Large Corporate

$1

4.1

$9

.3

$3

.8

$7

.5

$5

.8

$2

3.2

$3

.9

$8

.5

$8

.8

$1

2.9

$1

1.8

$2

2.8

$1

0.9

$1

7.3

$1

2.8

$1

6.8

$6

.0

$1

2.9

$7

.6

$6

.0

0

10

20

30

40

50

60

70

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2011 2012 2013 2014 2015

$ Value of IPOs # of IPOs

$1

78

.0

$2

26

.0

$1

99

.0

$1

14

.0

$1

07

.0

$1

41

.0

$1

46

.0

$1

79

.0

$1

84

.0

$1

28

.0

178

226

199

114 107

141 146

179 184

128

0

50

100

150

200

250

$0.0

$50.0

$100.0

$150.0

$200.0

$250.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Capital Raised # of Funds Closed

LBO Leverage Multiples

Middle Market* Private Equity Fundraising

MIDDLE MARKET MERGER & ACQUISITION TRENDS CONT.

IPO Offering Breakdown

Median Debt-to-Equity Breakdown

U.S. COMPANIES

Note: *PitchBook defines middle market as transactions between $25 million and $1 billion, where pricing is disclosed, for U.S. based companies.

Source: Dealogic, PitchBook, S&P LCD.

($ in billions)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

20

13

20

14

20

15

Debt % Equity %

($ in billions)

Private and Confidential | 9 www.davidsoncompanies.com/ecm/ Page 9

MERGER & ACQUISITION SELECTED TRANSACTIONS

Seattle, WA Confidential

Develops and produces apparel,

outerwear, headwear and handwear

products for outdoor activities

Union Bay Capital Partners has finalized the sale of POW Gloves, Holden

Outerwear, and Spacecraft Collective, three brands under the POW

Holdings umbrella, to various buyers

D.A. Davidson & Co. acted as exclusive sell-side financial advisor to

POW Holdings in this transaction

Minnetonka, MN Sharon Hill, PA

El Paso, TX Bend, OR

The company offers hydration vests,

belts, handhelds, bottles, running

packs

Acquisition provides Shock Doctor and McDavid channel growth within

run specialty retailers

United Sports Brands is majority-owned by investment firm Bregal

Partners

D.A. Davidson & Co. acted as exclusive sell-side financial advisor to

NATHAN Sports in this transaction

Manufactures double wall vacuum

insulated stainless steel water bottles

The purchase price is expected to be approximately $210 million in cash,

implying a pre-synergy multiple of approximately 11.5x projected calendar

year 2016 adjusted EBITDA

Hydro Flask has more than quadrupled in size since the beginning of

calendar year 2014, grew over 50% in calendar year 2015, and has been

the key driver behind the majority of the growth of the category itself

Source: S&P Capital IQ, SportsOneSource.

Tustin, CA Midvale, UT

Provides battery cases, battery and

storage products, universal batteries,

belt clips, docks, and cables and

adapters

Transaction was announced at $105.0 million

Mophie CEO Daniel Huang and COO Shawn Dougherty will maintain their

current responsibilities and will report directly to ZAGG CEO Randy Hales

D.A. Davidson & Co. acted as exclusive buy-side financial advisor to

ZAGG in this transaction

Target Acquirer Target Description Deal Notes

RECENT M&A DEAL ACTIVITY

London, UK London, UK

Operates as a retailer of luxury shoes

and accessories for men, women, and

kids

Transaction was announced at £245.0 million, resulting in a multiple of

8.2x last year’s earnings

Kurt Geiger, which operates in 80 countries and employs 1,700 people,

had sales of £260 million in 2014

The sale represents another step in the break-up of Jones Group, a

sprawling US fashion group, by Sycamore Partners

Separate Private

Investors

Private and Confidential | 10 www.davidsoncompanies.com/ecm/ Page 10

MERGER & ACQUISITION SELECTED TRANSACTIONS

Brooklyn Park, MN Vancouver, WA

Manufactures fitness equipment,

including standing, recumbent, and

lateral elliptical machines; and zero

runner equipment

Transaction was announced at approximately $115.0 million

The acquisition funded with a combinations of cash on hand and from

proceeds of a new $80 million term loan

The transaction adds a leading fitness brand, unique products and

technologies, broadens distribution and deepens Nautilus’ talent pool

Sante Fe Springs, CA San Diego, CA

Atlanta, GA Boca Raton, FL

Designs and manufactures protective

gear, including helmets, kneepads,

gloves, armpads, and ankle braces for

skateboarding, biking, BMX,

watersports, and other extreme

sporting activities

Pro-Tec is the first major acquisition since Transom Capital Group has

been at the helm of Bravo Sports

Pro-Tec will be moving day-to-day operations to Bravo Sports’ South

Orange County campus

Other Bravo Sports action sports brands include SixSixOne and ONE

Industries

Designs, manufactures, markets, and

distributes consumer products

worldwide

Transaction was announced at approximately $13.2 billion, or 2.1x LTM

revenue and 20.0x LTM EBITDA multiple

Substantial revenue synergies and $500 million cost synergies over four

years

New company to be called Newell Brands

Source: S&P Capital IQ, SportsOneSource.

Scotts Valley, CA Clearfield, UT

Engages in the design, development,

and marketing of branded sports

equipment, protective products, and

related accessories worldwide

Transaction was announced at $400.0 million, resulting in a effective

multiple of approximately 10x the expected calendar year 2016 EBITDA

The Bell, Giro, C-Preme and Blackburn brands will be integrated into

Vista's Outdoor Products segment

The acquisition of BRG Sports’ Action Sports division will include more

than 600 employees

Target Acquirer Target Description Deal Notes

RECENT M&A DEAL ACTIVITY

Ontario, CA Buffalo, NY

Operates as a retailer and distributor

of equipment, tactical gear and

uniforms for law enforcement and

public safety professionals

With the acquisition of United Uniform, Safariland enhances its position

as a leading global provider of safety and survivability products

Safariland has expanded its geographic footprint to 11 retail stores,

establishing itself as the premier provider of law enforcement equipment

to institutions and retail customers in the Eastern U.S.

Transaction is Safariland Group’s third acquisition since January 2015

Action Sports Division

Private and Confidential | 11 www.davidsoncompanies.com/ecm/ Page 11

MERGER & ACQUISITION SELECTED TRANSACTIONS

New York City, NY Toronto, ON

Online, membership-based retailer of

luxury goods, such as fashion

apparel, home décor, footwear,

jewelry, and handbags

Represents Hudson Bay’s ongoing focus on advancing its all-channel

model while continuing to grow its off-price business

Hudson Bay expects Gilt to contribute approximately $40 million of

adjusted EBITDA by FY 2017

Transaction funded with cash on hand

Lake Forest, IL Medway, MA

Columbus, OH San Diego, CA

Developer and manufacturer of

strength, cardiovascular, and fitness

equipment products

Acquisition made as part of efforts to double Brunswick Fitness segment

revenue by 2020

Addition of premium brand will provide broader product portfolio, growth

synergies, and cost reduction efficiencies

Retailer of shoes for women, men,

and children

Acquisition made to expand online presence while growing international

business

Ebuys will operate as a distinct business within DSW and will continue to

be led by its chief executive, David Duong

Source: S&P Capital IQ, SportsOneSource.

Newport Beach, CA Aliso Viejo, CA

Develops and manufactures polarized

eyewear products for athletes ranging

from sailing to golf, and from baseball

to fishing

Kaenon will remain a separate entity, led by its Co-Founder and President

Darren Rosenberg

Kaenon designs its products in Orange County and manufactures them in

Italy

Target Target Description Deal Notes

RECENT M&A DEAL ACTIVITY

New York, NY New York, NY

Manufactures and distributes designer

footwear and bags for men and

women

Transaction was announced at approximately $574.0 million or 1.8x LTM

revenue multiple

The largest acquisition ever made by Coach

Acquisition is part of an effort to revamp the Coach’s image amid

declining sales and increased competition

Acquirer

Private and Confidential | 12 www.davidsoncompanies.com/ecm/ Page 12

PUBLIC EQUITY OFFERINGS SELECTED TRANSACTIONS

Source: Dealogic, S&P Capital IQ.

RECENT EQUITY OFFERING ACTIVITY

Belleville, WI

William Blair; Baird; Raymond James; BMO Capital Markets

Offer Date Deal Type Issuer Underwriters Gross Proceeds

$80.0mm Initial Public

Offering 11-19-15

Boca Raton, FL

$490.0mm Follow-On

Offering 10-15-15

$76.6mm Follow-On

Offering 9-24-15

$248.4mm Initial Public

Offering 8-5-15

$1.0bn Follow-On

Offering 7-16-15

Barclays; Credit Suisse; UBS Investment Bank; RBC Capital

Markets; SunTrust Robinson Humphrey; Wells Fargo

Securities; Deutsche Bank Securities; Citigroup; CJS

Securities; BTIG; Raymond James; D.A. Davidson & Co.;

KeyBanc Capital Markets

Credit Suisse; Goldman, Sachs & Co.; Baird; William Blair;

Piper Jaffray; Wells Fargo Securities; D.A. Davidson & Co.;

Sterne Agee CRT

J.P. Morgan; BofA Merrill Lynch; Jefferies; Credit Suisse;

Guggenheim Securities; Baird; William Blair; Piper Jaffray;

Cowen and Company

Barclays; Credit Suisse; UBS Investment Bank; RBC Capital

Markets; SunTrust Robinson Humphrey; Wells Fargo

Securities; Citigroup; CJS Securities; Deutsche Bank

Securities; Jefferies; William Blair; BTIG; D.A. Davidson &

Co.; KeyBanc Capital Markets; Raymond James

Midvale, UT

Newington, NH

Boca Raton, FL

Private and Confidential | 13 www.davidsoncompanies.com/ecm/ Page 13

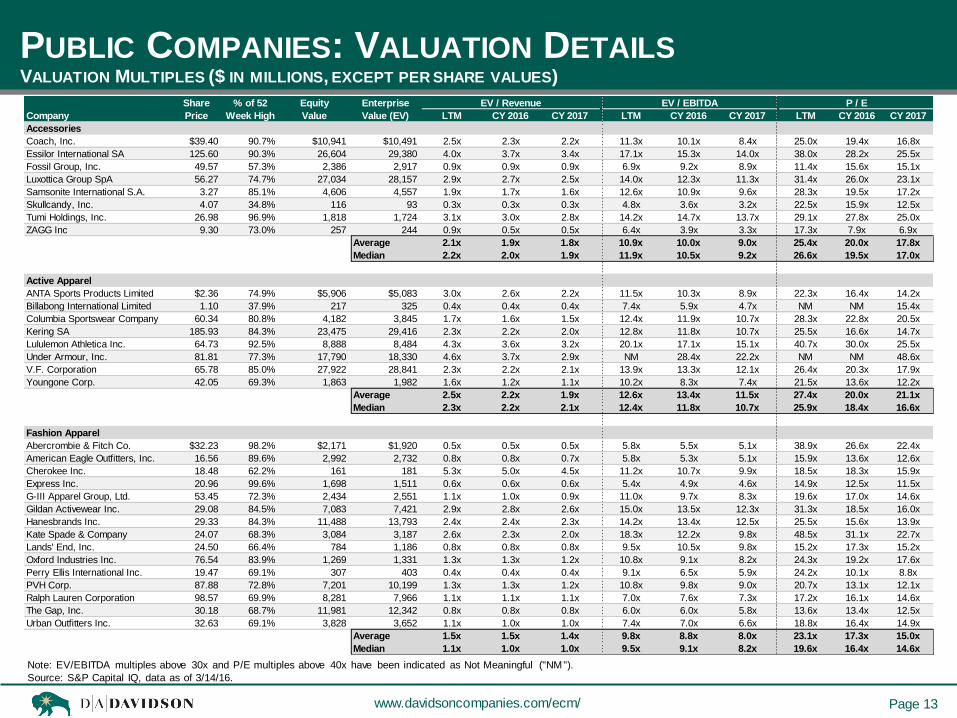

Accessories

Coach, Inc. $39.40 90.7% $10,941 $10,491 2.5x 2.3x 2.2x 11.3x 10.1x 8.4x 25.0x 19.4x 16.8x

Essilor International SA 125.60 90.3% 26,604 29,380 4.0x 3.7x 3.4x 17.1x 15.3x 14.0x 38.0x 28.2x 25.5x

Fossil Group, Inc. 49.57 57.3% 2,386 2,917 0.9x 0.9x 0.9x 6.9x 9.2x 8.9x 11.4x 15.6x 15.1x

Luxottica Group SpA 56.27 74.7% 27,034 28,157 2.9x 2.7x 2.5x 14.0x 12.3x 11.3x 31.4x 26.0x 23.1x

Samsonite International S.A. 3.27 85.1% 4,606 4,557 1.9x 1.7x 1.6x 12.6x 10.9x 9.6x 28.3x 19.5x 17.2x

Skullcandy, Inc. 4.07 34.8% 116 93 0.3x 0.3x 0.3x 4.8x 3.6x 3.2x 22.5x 15.9x 12.5x

Tumi Holdings, Inc. 26.98 96.9% 1,818 1,724 3.1x 3.0x 2.8x 14.2x 14.7x 13.7x 29.1x 27.8x 25.0x

ZAGG Inc 9.30 73.0% 257 244 0.9x 0.5x 0.5x 6.4x 3.9x 3.3x 17.3x 7.9x 6.9x

Average 2.1x 1.9x 1.8x 10.9x 10.0x 9.0x 25.4x 20.0x 17.8x

Median 2.2x 2.0x 1.9x 11.9x 10.5x 9.2x 26.6x 19.5x 17.0x

Active Apparel

ANTA Sports Products Limited $2.36 74.9% $5,906 $5,083 3.0x 2.6x 2.2x 11.5x 10.3x 8.9x 22.3x 16.4x 14.2x

Billabong International Limited 1.10 37.9% 217 325 0.4x 0.4x 0.4x 7.4x 5.9x 4.7x NM NM 15.4x

Columbia Sportswear Company 60.34 80.8% 4,182 3,845 1.7x 1.6x 1.5x 12.4x 11.9x 10.7x 28.3x 22.8x 20.5x

Kering SA 185.93 84.3% 23,475 29,416 2.3x 2.2x 2.0x 12.8x 11.8x 10.7x 25.5x 16.6x 14.7x

Lululemon Athletica Inc. 64.73 92.5% 8,888 8,484 4.3x 3.6x 3.2x 20.1x 17.1x 15.1x 40.7x 30.0x 25.5x

Under Armour, Inc. 81.81 77.3% 17,790 18,330 4.6x 3.7x 2.9x NM 28.4x 22.2x NM NM 48.6x

V.F. Corporation 65.78 85.0% 27,922 28,841 2.3x 2.2x 2.1x 13.9x 13.3x 12.1x 26.4x 20.3x 17.9x

Youngone Corp. 42.05 69.3% 1,863 1,982 1.6x 1.2x 1.1x 10.2x 8.3x 7.4x 21.5x 13.6x 12.2x

Average 2.5x 2.2x 1.9x 12.6x 13.4x 11.5x 27.4x 20.0x 21.1x

Median 2.3x 2.2x 2.1x 12.4x 11.8x 10.7x 25.9x 18.4x 16.6x

Fashion Apparel

Abercrombie & Fitch Co. $32.23 98.2% $2,171 $1,920 0.5x 0.5x 0.5x 5.8x 5.5x 5.1x 38.9x 26.6x 22.4x

American Eagle Outfitters, Inc. 16.56 89.6% 2,992 2,732 0.8x 0.8x 0.7x 5.8x 5.3x 5.1x 15.9x 13.6x 12.6x

Cherokee Inc. 18.48 62.2% 161 181 5.3x 5.0x 4.5x 11.2x 10.7x 9.9x 18.5x 18.3x 15.9x

Express Inc. 20.96 99.6% 1,698 1,511 0.6x 0.6x 0.6x 5.4x 4.9x 4.6x 14.9x 12.5x 11.5x

G-III Apparel Group, Ltd. 53.45 72.3% 2,434 2,551 1.1x 1.0x 0.9x 11.0x 9.7x 8.3x 19.6x 17.0x 14.6x

Gildan Activewear Inc. 29.08 84.5% 7,083 7,421 2.9x 2.8x 2.6x 15.0x 13.5x 12.3x 31.3x 18.5x 16.0x

Hanesbrands Inc. 29.33 84.3% 11,488 13,793 2.4x 2.4x 2.3x 14.2x 13.4x 12.5x 25.5x 15.6x 13.9x

Kate Spade & Company 24.07 68.3% 3,084 3,187 2.6x 2.3x 2.0x 18.3x 12.2x 9.8x 48.5x 31.1x 22.7x

Lands' End, Inc. 24.50 66.4% 784 1,186 0.8x 0.8x 0.8x 9.5x 10.5x 9.8x 15.2x 17.3x 15.2x

Oxford Industries Inc. 76.54 83.9% 1,269 1,331 1.3x 1.3x 1.2x 10.8x 9.1x 8.2x 24.3x 19.2x 17.6x

Perry Ellis International Inc. 19.47 69.1% 307 403 0.4x 0.4x 0.4x 9.1x 6.5x 5.9x 24.2x 10.1x 8.8x

PVH Corp. 87.88 72.8% 7,201 10,199 1.3x 1.3x 1.2x 10.8x 9.8x 9.0x 20.7x 13.1x 12.1x

Ralph Lauren Corporation 98.57 69.9% 8,281 7,966 1.1x 1.1x 1.1x 7.0x 7.6x 7.3x 17.2x 16.1x 14.6x

The Gap, Inc. 30.18 68.7% 11,981 12,342 0.8x 0.8x 0.8x 6.0x 6.0x 5.8x 13.6x 13.4x 12.5x

Urban Outfitters Inc. 32.63 69.1% 3,828 3,652 1.1x 1.0x 1.0x 7.4x 7.0x 6.6x 18.8x 16.4x 14.9x

Average 1.5x 1.5x 1.4x 9.8x 8.8x 8.0x 23.1x 17.3x 15.0x

Median 1.1x 1.0x 1.0x 9.5x 9.1x 8.2x 19.6x 16.4x 14.6x

PUBLIC COMPANIES: VALUATION DETAILS

Note: EV/EBITDA multiples above 30x and P/E multiples above 40x have been indicated as Not Meaningful ("NM").

Source: S&P Capital IQ, data as of 3/14/16.

VALUATION MULTIPLES ($ IN MILLIONS, EXCEPT PER SHARE VALUES)

Share % of 52 Equity Enterprise EV / Revenue EV / EBITDA P / E

Company Price Week High Value Value (EV) LTM CY 2016 CY 2017 LTM CY 2016 CY 2017 LTM CY 2016 CY 2017

Private and Confidential | 14 www.davidsoncompanies.com/ecm/ Page 14

Equipment

Accell Group NV $21.66 92.4% $547 $770 0.7x 0.7x 0.6x 9.8x 9.4x 8.6x 15.3x 13.9x 11.1x

Amer Sports Corp. 27.65 88.7% 3,180 3,691 1.3x 1.2x 1.2x 12.9x 11.2x 10.1x 27.3x 18.8x 16.5x

Arctic Cat Inc. 16.08 41.2% 209 198 0.3x 0.3x 0.3x NM 7.5x 5.0x NM 46.0x 13.3x

Black Diamond, Inc. 4.67 43.4% 153 137 0.9x 0.9x 0.9x NM 24.9x 14.3x NM NM NM

Brunswick Corporation 44.94 80.2% 4,091 3,868 0.9x 0.9x 0.8x 7.5x 6.5x 5.7x 16.5x 13.0x 11.3x

Callaway Golf Co. 8.85 85.9% 830 795 0.9x 0.9x 0.9x 17.9x 16.1x 12.6x NM 37.1x 24.9x

Dorel Industries Inc. 20.14 70.4% 652 1,191 0.4x 0.4x 0.4x 7.3x 6.5x 5.9x 15.4x 9.7x 8.0x

Escalade Inc. 12.73 63.7% 181 202 1.3x 1.2x NA 11.2x 8.1x NA 18.5x 12.0x NA

Fox Factory Holding Corp 16.10 82.1% 596 638 1.7x 1.6x 1.5x 11.4x 9.2x 8.0x 23.4x 14.6x 12.7x

Giant Manufacturing Co. Ltd. 6.52 69.2% 2,446 2,499 1.3x 1.3x 1.2x 13.7x 12.8x 11.7x 23.5x 19.0x 17.4x

GoPro, Inc. 12.27 18.7% 1,679 1,205 0.7x 0.9x 0.7x 14.4x NM NM NM NM NM

Jarden Corp. 55.83 96.3% 12,278 17,360 2.0x 1.7x 1.7x 18.0x 11.4x 10.5x 37.0x 17.8x 16.1x

Johnson Outdoors Inc. 22.69 64.3% 226 209 0.5x 0.5x NA 6.2x NA NA 16.0x 13.5x NA

Marine Products Corp. 7.60 84.5% 292 276 1.3x 1.2x 1.2x 12.8x 11.6x 9.9x 21.5x 16.7x 14.8x

Mizuno Corporation 4.75 80.4% 599 771 0.5x 0.4x 0.4x 12.1x 10.1x 9.5x 29.6x 21.4x 19.1x

Nautilus Inc. 18.41 80.2% 571 590 1.8x 1.4x 1.2x 12.2x 8.8x 7.7x 20.8x 16.3x 14.2x

Performance Sports Group Ltd. 3.95 20.2% 180 653 1.1x 1.1x 1.0x 11.5x 12.8x 9.2x NM 25.9x 7.3x

Polaris Industries Inc. 97.55 62.4% 6,336 6,644 1.4x 1.4x 1.3x 7.7x 8.0x 7.3x 15.4x 15.3x 13.7x

Shimano Inc. 157.84 88.8% 14,632 13,054 4.1x 3.8x 3.6x 15.6x 14.3x 13.2x 27.8x 24.6x 22.7x

Vista Outdoor Inc. 51.09 94.8% 3,122 3,738 1.7x 1.5x 1.4x 12.2x 9.5x 9.2x 24.2x 18.0x 16.5x

Average 1.3x 1.2x 1.1x 11.9x 11.0x 9.3x 22.1x 19.6x 15.0x

Median 1.2x 1.1x 1.1x 12.2x 9.8x 9.2x 21.5x 17.3x 14.5x

Footwear

Adidas AG $113.22 99.8% $22,666 $23,063 1.3x 1.1x 1.1x 15.3x 12.7x 11.2x 31.1x 25.4x 21.6x

ASICS Corp. 17.93 50.9% 3,404 3,430 0.9x 0.9x 0.8x 9.4x 10.1x 8.8x 19.0x 21.2x 16.9x

Caleres, Inc. 29.21 86.3% 1,276 1,391 0.5x 0.5x 0.5x 7.9x 6.6x 6.1x 16.6x 13.1x 11.8x

Crocs, Inc. 9.77 60.9% 713 752 0.7x 0.7x 0.6x NM 10.6x 7.4x NM 39.9x 17.9x

Deckers Outdoor Corp. 56.59 72.6% 1,835 1,628 0.9x 0.9x 0.9x 6.8x 6.2x 6.4x 16.2x 12.7x 13.3x

Li Ning Company Limited 0.48 67.0% 688 644 0.6x 0.5x 0.4x 15.5x 4.9x 3.7x NM 17.8x 11.7x

NIKE, Inc. 60.81 89.2% 103,569 99,629 3.2x 2.9x 2.6x 19.7x 17.5x 14.4x 37.9x 26.9x 22.1x

PUMA SE 216.12 89.6% 3,228 2,848 0.8x 0.7x 0.7x 17.1x 13.9x 10.7x NM NM 32.2x

Rocky Brands, Inc. 12.92 56.2% 98 118 0.4x 0.4x 0.4x 6.7x 6.0x 5.7x 16.2x 12.3x 11.2x

Skechers U.S.A., Inc. 31.53 57.8% 4,929 4,554 1.4x 1.2x 1.1x 11.3x 8.7x 7.5x 27.0x 15.0x 12.3x

Steven Madden, Ltd. 36.28 81.1% 2,242 2,137 1.5x 1.5x 1.4x 10.9x 10.9x 9.9x 20.3x 17.7x 15.6x

Weyco Group Inc. 25.24 81.4% 270 280 0.9x NA NA 8.4x NA NA 15.0x NA NA

Wolverine World Wide Inc. 18.70 53.1% 1,868 2,500 0.9x 1.0x 0.9x 8.7x 9.3x 8.8x 14.7x 13.9x 12.7x

Average 1.1x 1.0x 0.9x 11.5x 9.8x 8.4x 21.4x 19.6x 16.6x

Median 0.9x 0.9x 0.8x 10.2x 9.7x 8.1x 17.8x 17.7x 14.4x

PUBLIC COMPANIES: VALUATION DETAILS CONT.

Note: EV/EBITDA multiples above 30x and P/E multiples above 40x have been indicated as Not Meaningful ("NM").

Source: S&P Capital IQ, data as of 3/14/16.

VALUATION MULTIPLES ($ IN MILLIONS, EXCEPT PER SHARE VALUES)

Share % of 52 Equity Enterprise EV / Revenue EV / EBITDA P / E

Company Price Week High Value Value (EV) LTM CY 2016 CY 2017 LTM CY 2016 CY 2017 LTM CY 2016 CY 2017

Private and Confidential | 15 www.davidsoncompanies.com/ecm/ Page 15

Retail

Amazon.com, Inc. $573.37 82.3% $269,967 $267,706 2.5x 2.1x 1.7x NM 18.8x 14.2x NM NM NM

ASOS Plc 45.33 74.3% 3,763 3,592 2.0x 1.8x 1.4x NM 27.4x 21.0x NM NM NM

Big 5 Sporting Goods Corp. 11.41 73.8% 250 302 0.3x 0.3x 0.3x 6.4x 6.4x 5.9x 15.6x 16.7x 13.3x

Cabela's Incorporated 48.22 81.9% 3,270 7,867 2.0x 1.9x 1.8x 17.3x 15.6x 14.4x 17.7x 15.1x 13.6x

Dick's Sporting Goods Inc. 46.71 77.4% 5,371 5,258 0.7x 0.7x 0.6x 7.1x 7.0x 6.2x 16.2x 15.7x 13.4x

eBay Inc. 24.28 36.4% 28,619 29,267 3.4x 3.4x 3.2x 9.9x 8.5x 7.9x 21.5x 13.0x 11.8x

Finish Line Inc. 18.45 63.5% 818 763 0.4x 0.4x 0.4x 5.7x 4.8x 4.6x 14.5x 11.7x 10.6x

Foot Locker, Inc. 64.28 83.2% 8,823 7,932 1.1x 1.0x 1.0x 7.3x 6.7x 6.3x 15.4x 13.5x 12.2x

Gaiam Inc. 5.81 75.0% 142 127 0.7x 0.6x NA 16.4x 6.1x NA NM 16.6x NA

Genesco Inc. 65.96 89.7% 1,457 1,436 0.5x 0.5x 0.5x 6.0x 5.8x 5.3x 15.5x 13.4x 12.1x

Hibbett Sports, Inc. 35.72 64.1% 814 782 0.8x 0.8x 0.7x 6.1x 6.0x 5.7x 12.3x 11.9x 11.2x

Overstock.com Inc. 14.79 57.0% 374 218 0.1x NA NA 19.3x NA NA NM NA NA

Pacific Sunwear of California Inc. 0.15 5.0% 11 131 0.2x 0.2x 0.2x NM NA NA NM NM NM

Sportsman's Warehouse 13.11 87.9% 551 776 1.1x 0.9x 0.9x 13.8x 8.7x 8.2x 34.6x 17.5x 14.2x

Tilly's, Inc. 8.29 48.8% 236 162 0.3x 0.3x 0.3x 3.6x 3.9x 4.3x 16.7x 21.1x 20.6x

Wayfair Inc. 42.87 75.4% 3,617 3,231 1.4x 1.0x 0.7x NM NM NM NM NM NM

West Marine Inc. 9.17 82.8% 227 179 0.3x 0.2x 0.2x 6.3x 4.8x NA NM 26.6x 14.1x

Winmark Corp. 99.15 91.6% 407 473 6.8x NA NA 12.6x NA NA 20.9x NA NA

Zumiez, Inc. 19.70 48.5% 506 431 0.5x 0.5x 0.5x 5.6x 6.1x 5.4x 19.0x 19.0x 15.8x

Average 1.3x 1.0x 0.9x 9.6x 9.1x 8.4x 18.3x 16.3x 13.6x

Median 0.7x 0.7x 0.7x 7.1x 6.4x 6.2x 16.5x 15.7x 13.3x

Tactical

BAE Systems plc $7.12 90.6% $22,553 $24,533 1.0x 0.9x 0.9x 9.0x 8.1x 7.7x 23.3x 12.5x 11.8x

The Boeing Company 126.34 81.0% 83,701 81,713 0.9x 0.9x 0.8x 9.1x 7.8x 7.5x 19.2x 14.9x 13.5x

Cobham plc 3.06 65.5% 3,470 5,200 1.7x 1.8x 1.7x 8.4x 9.2x 8.5x 32.2x 11.5x 10.4x

General Dynamics Corporation 134.21 87.3% 41,761 42,375 1.3x 1.3x 1.3x 9.1x 9.0x 8.7x 17.1x 14.3x 13.3x

Honeywell International Inc. 108.51 97.0% 82,612 87,570 2.3x 2.2x 2.1x 11.4x 10.4x 9.7x 21.2x 16.4x 15.0x

Lockheed Martin Corporation 216.60 95.0% 66,169 80,340 1.7x 1.6x 1.6x 12.8x 11.6x 10.7x 20.3x 18.4x 15.8x

MSA Safety Incorporated 46.81 85.8% 1,749 2,114 1.9x 1.8x 1.7x 12.0x 10.5x 10.0x 20.4x 17.3x 15.6x

Orbital ATK, Inc. 78.26 82.4% 4,604 5,950 1.5x 1.3x 1.2x 13.7x 8.5x 7.8x 33.6x 14.5x 12.7x

Oshkosh Corporation 37.23 66.9% 2,722 3,674 0.6x 0.6x 0.6x 7.6x 8.4x 7.5x 15.7x 15.6x 12.3x

Smith & Wesson 28.37 99.0% 1,563 1,632 2.4x 2.2x 2.3x 9.1x 8.3x 8.7x 20.1x 16.4x NA

Sturm, Ruger & Co. Inc. 74.66 97.8% 1,415 1,345 2.4x 2.3x 2.2x 10.5x 8.6x 8.3x 24.1x 18.8x 18.0x

TASER International Inc. 19.33 53.8% 1,038 928 4.7x 4.0x 3.2x 24.2x NM 17.8x NM NM 29.9x

Average 1.9x 1.7x 1.6x 11.4x 9.1x 9.4x 22.5x 15.5x 15.3x

Median 1.7x 1.7x 1.6x 9.8x 8.6x 8.6x 20.4x 15.6x 13.5x

Agg. Average 1.5x 1.4x 1.3x 11.0x 10.0x 9.0x 22.4x 18.2x 15.9x

Agg. Median 1.1x 1.1x 1.1x 10.9x 9.2x 8.6x 20.7x 16.5x 14.6x

PUBLIC COMPANIES: VALUATION DETAILS CONT.

* Aggregate average and median of all 7 public equity comparables groups.

Note: EV/EBITDA multiples above 30x and P/E multiples above 40x have been indicated as Not Meaningful ("NM").

Source: S&P Capital IQ, data as of 3/14/16.

*

*

VALUATION MULTIPLES ($ IN MILLIONS, EXCEPT PER SHARE VALUES)

Share % of 52 Equity Enterprise EV / Revenue EV / EBITDA P / E

Company Price Week High Value Value (EV) LTM CY 2016 CY 2017 LTM CY 2016 CY 2017 LTM CY 2016 CY 2017

Private and Confidential | 16 www.davidsoncompanies.com/ecm/ Page 16

ABOUT D.A. DAVIDSON & CO.

D.A. DAVIDSON & CO.

INVESTMENT BANKING OFFICE LOCATIONS

Baltimore 111 S. Calvert Street, Suite 2830

Baltimore, Maryland 21202

(443) 610-6217

Chicago 30 N. LaSalle, Suite 1600

Chicago, Illinois 60602

(312) 525-2777

Denver 1550 Market Street, Suite 300

Denver, Colorado 80202

(303) 571-6100

Great Falls 8 Third Street North

Great Falls, Montana 59401

(406) 268-3029

Orange County 611 Anton Boulevard, Suite 600

Costa Mesa, California 92626

(714) 327-8800

Portland Two Centerpointe, Suite 450

Lake Oswego, Oregon 97035

(503) 603-3060

Salt Lake City 110 S. Regent Street, Suite 410

Salt Lake City, Utah 84111

(801) 333-3123

Seattle 701 5th Ave. Suite 4050

Seattle, Washington 98104

(206) 903-8669

This material is for your information, and w e are not soliciting any action based

upon it. This material should not be read as advice or recommendations. It has

not been prepared taking into account any person’s particular objectives or

needs. Any person should consider w hether the information is appropriate to

their needs or seek advice before making a decision based on this information.

The material is based upon information that w e consider reliable, but w e do not

represent that it is accurate or complete, and it should not be relied upon as

such. Opinions expressed, unless otherw ise indicated, are our current opinions

as of the date appearing on this material only. No part of this material may be

copied, photocopied or duplicated in any form by any means or redistributed

w ithout D.A. Davidson & Co.’s prior w ritten consent.

D.A. Davidson & Co.'s Investment Banking Group is dedicated to helping

its clients achieve their strategic and financial objectives, while maximizing

stakeholder value. With highly experienced investment banking

professionals, we bring world class skills and senior-level attention to every

transaction. D.A. Davidson’s Active Lifestyle Group is dedicated to

delivering these services to companies in the following sectors:

Accessories, Active Apparel, Fashion Apparel, Equipment, Footwear,

Retail, and Tactical.

For more information visit www.davidsoncompanies.com/ecm.

About D.A. Davidson Investment Banking

About D.A. Davidson Companies

Founded in 1935, D.A. Davidson Companies has approximately $41.5

billion in assets under management and administration and employs over

1,300 people across 24 states. D.A. Davidson & Co.’s Investment Banking

group provides full-service underwriting and advisory services for

corporations and institutions globally, including public offerings, mergers

and acquisitions, and private placements. D.A. Davidson & Co.’s full-

service platform allows investment banking clients to benefit from the firm’s

capital market capabilities, including research, corporate services, and

institutional sales and trading. D.A. Davidson & Co. is a member of SIPC.