acn 125 931 964 financial report 30 june 20152015/09/14 · 2 the directors of chrysalis resources...

TRANSCRIPT

ACN 125 931 964

FINANCIAL REPORT

30 JUNE 2015

For

per

sona

l use

onl

y

COMPANY DIRECTORY

DIRECTORS

Dr Neale Fong Non-Executive Chairman

Mr Jian Hua Sang Non-Executive Director

Mr Leigh Ryan Managing Director

COMPANY SECRETARY Mr Kevin Hart

REGISTERED OFFICE

Suite 20 7 The Esplanade Mt Pleasant WA 6153

Telephone: +61(8) 6180 9290 Facsimile: +61(8) 9316 1314 Website: www.chrysalisresources.com.au

SHARE REGISTRY

Computershare Investor Services Pty Ltd Level 11 172 St Georges Terrace

PERTH WA 6000 GPO Box D182 Perth WA 6840

Telephone: +61(8) 9323 2000 Facsimile: +61(8) 9323 2033

AUDITORS

HLB Mann Judd Level 4, 130 Stirling Street PERTH WA 6000

Telephone: +61(8) 9227 7500 Facsimile: +61(8) 9227 7533

AUSTRALIAN SECURITIES EXCHANGE

Chrysalis Resources Limited shares (CYS) are listed on the Australian Securities Exchange.

The home exchange is Perth, Western Australia.

For

per

sona

l use

onl

y

CONTENTS

DIRECTORS’ REPORT 2 AUDITOR’S INDEPENDENCE DECLARATION 23 STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME 24 STATEMENT OF FINANCIAL POSITION 25 STATEMENT OF CHANGES IN EQUITY 26 STATEMENT OF CASH FLOWS 27 NOTES TO THE FINANCIAL STATEMENTS 28 DIRECTORS’ DECLARATION 53 INDEPENDENT AUDITOR’S REPORT 54

For

per

sona

l use

onl

y

DIRECTORS’ REPORT

2

The Directors of Chrysalis Resources Limited (“the Company”) present their report for the financial year ended 30 June 2015. In order to comply with the provisions of the Corporations Act 2001, the directors report as follows: Directors

The names of directors, who held office during or, since the end of the year and up until the date of this report, are as follows:

Dr Neale Fong Non-Executive Chairman

Mr Leigh Ryan1 Managing Director Appointed 23 September 2014

Mr Jian Hua Sang Non-Executive Director

Mr Michael Griffiths2 Non-Executive Director Resigned 23 September 2014

Ms Jing Wang3 Executive Director Resigned 23 September 2014 Notes: 1. Mr Leigh Ryan was appointed as Managing Director on 23 September 2014.

2. Mr Michael Griffiths was appointed as Alternate Director to Mr Bradley Marwood on 5 April 2013, subsequently appointed as Non-

Executive director on 26 July 2013 and resigned on 23 September 2014.

3. Ms Jing Wang was appointed Executive Director on the 1 November 2013 and resigned on the 23 September 2014.

Directors were in office for this entire period unless otherwise stated.

The particulars of the qualifications, experience and special responsibilities of each director as at year end and until the date of this report are as follows: Dr Neale Fong – MBBS Dip CS MTS MBA FAICD FACHSM (Hon) Non-Executive Chairman

Dr Fong has extensive experience in management of large and complex organisations, especially in the health and human services field. He is a qualified medical practitioner holding Bachelors Degrees in Medicine and Surgery from the University of Western Australia as well as a Masters in Business Administration from the UWA Business School. He also holds a Masters Degree in Theological Studies from Regent College, University of British Columbia.

Dr Fong is a Fellow of the Australian Institute of Company Directors and is an experienced chairman and director. He is also a non-executive director of Sleep Studies Australia Pty Ltd and Chairman of Bethesda Hospital Inc.

Dr Fong has served as a director and chairman of the West Australian Football Commission and acts as adviser and consultant to a number of other companies.

During the past three years, Dr Fong has served as a Director of the following listed companies.

Company Date appointed Date ceased

Realm Resources Limited 10 December 2009 17 September 2013 Mr Leigh Ryan – BSc Geology, MAIG Managing Director (Appointed 23 September 2014)

Mr Ryan is a highly qualified geologist with 28 years of experience in the exploration and resources industry, specifically in project management and executive management throughout Australia and Africa. He has been involved in the targeting, evaluation, discovery and resource definition of numerous gold and base metal deposits and has successfully negotiated many purchase option and joint venture agreements. Mr Ryan was previously the Managing Director of Boss Resources Limited, and prior to that was employed by Resolute Mining Limited as the Group Exploration Manager for Africa and Australia. He has worked extensively in Queensland, WA, Tanzania, Burkina Faso, Mali, and Cote d’Ivoire. On the 2 December 2013 Mr Ryan was appointed as Chief Executive Officer of the Company, which preceded his appointment as Managing Director.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT (continued)

3

During the past three years Mr Ryan has also served as a Director of the following listed companies:

Company Date appointed Date ceased

Attila Resources Limited 23 January 2012 21 January 2013 Boss Resources Limited 4 May 2011 24 July 2013

Mr Jian Hua Sang Non-Executive Director

Mr Sang trained in China and also was the first Chinese postgraduate student studying Economic Geology in Western Australia. He has more than 25 years of international exploration, mining and corporate experience in Asia, Australia and Africa.

Mr Sang has held senior executive positions as the Chief Representative China of several ASX-listed companies, Vice President China of Ivanhoe Mines Inc., Director of Minerals China with Hatch Associates, General Manager – Commercial Services of Citic Pacific Mining and CEO of an ASX mining company. During the past two years, he has played an instrumental role in successfully bringing a significant amount of Chinese capital investment to several ASX-listed minerals exploration companies.

During the past three years Mr Sang has also served as a Director of the following listed companies:

Company Date appointed Date ceased

Emergent Resources Limited 17 September 2012 - Vector Resources Limited 13 September 2012 28 November 2013

Mr Sang is entitled to a benefit for the provision of corporate advisory services in relation to the Term Sheet executed with Eagle Brilliant Holdings Limited (“EBH”). The corporate advisory agreement executed between Mr Sang’s consulting entity and the Company entitles Mr Sang to receive, by way of a consulting fee, 5% of any amount of direct equity investment in the Company by the TDL Group (or any of its associates). The contract was executed at arms length and on commercial terms. Company Secretary

Mr Kevin Hart – FCA, B Com

Mr Hart is a Partner at Endeavour Corporate Pty Ltd, an advisory firm that specialises in the provision of Company Secretarial services to ASX listed entities. Kevin has over 28 years of professional experience with various public companies, mostly in the exploration and mining industry. Interests in shares and options of the company and related bodies corporate The following relevant interests in shares and options of the Company were held by the directors or their associates as at the date of this report:

Number of fully paid

ordinary shares

Number of listed options over

ordinary shares Unissued employee

share plan rights Directors Neale Fong 7,611,480 - - Leigh Ryan 1,000,000 - 2,000,000 Jian Hua Sang - - -

No share options were granted to the directors of the Company during or since the end of the financial year as part of their remuneration. Listed options There were no ordinary shares issued by the company during or since the end of the financial year as a result of the exercise of an option. At the date of this report, the Company had no listed options over ordinary shares on issue.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT (continued)

4

Dividends No dividends were paid during the year and no recommendation is made as to dividends. Principal Activity The principal activity of the Group was exploration for minerals. Review of Operations Zambian Copper Projects Exploration continued in Zambia throughout the year, with the company entering into a legally binding Letter Agreement with FQM Exploration (Zambia) Limited (“FQM”) whereby FQM agreed to fund exploration across Chrysalis’ Shikila and Kabwima Projects for a minimum 6 month period prior to earning the right to enter an Earn-in phase, and subsequent Joint Venture, Put/Call and/or Net Smelter Royalty options. The Letter Agreement includes licences 8194-HQ-LPL, 13404-HQ-LPL, and 13405-HQ-LPL (Kabwima and Shikila projects).

Kabwima Project

During the year exploration within the Kabwima Project included one trench and an additional 13 pits excavated within the Kimabwe Prospect returning maximum copper results of 1m @ 266ppm Cu from the trench, and 0.5m@359ppm Cu, 0.5m@346ppm Cu and 0.5m @ 483ppm Cu from pits KIPT007, KIPT008 and KIPT014 respectively (refer to ASX release dated 31 July 2014, June Quarterly Activities Report and 27 October 2014, September Quarterly Activities Report).

A 122 hole, 5,234m aircore (AC) drilling program was then completed at the Kimabwe Prospect in order to identify the potential for economic copper mineralisation within the >200ppm areas of the Kimabwe Prospect 5.5 kilometre long, up to 1.6km wide, continuous >100ppm copper-in-soil anomaly. Significant intercepts from the aircore program included (refer to ASX release dated 10 November 2014):

• 44m @ 0.7% Cu from 6m (KIAC108) incl. 6m @ 2.15% Cu, 1.1g/t Ag from 44m • 28m @ 0.26% Cu, 0.034% Co from 12m (KIAC021) • 16m @ 0.29% Cu from 25m to EOH (KIAC105) incl. 4m @ 0.43% Cu, 0.033% Co from 33m • 24m @ 0.18% Cu from 2m (KIAC107) • 17m @ 0.20% Cu from 14m (KIWB001)

The holes intercepted gabbro intrusives at the northern edge of the Cu-in-soil anomaly, and interbedded black shale, grey shale, silicified siltstone and biotite-muscovite-quartz schist to the south. Significant amounts of quartz veining and gossan development was encountered both at the gabbro / sediment and sediment / mica- quartz schist contacts. Lithologies and mineralised structures appear to dip at ~400 to the north-northwest and with all holes drilled at -600 all intercepts are interpreted to be close to true widths. Nine aircore holes ended in Cu mineralisation at <50m (down hole) depth, with saprolitic and gossanous mineralised zones suggesting surficial copper leaching and better copper grades at depth possible.

A regional 500m x 500m spaced soil sampling program was completed during the year as part of the FQM Joint Venture Option Agreement with a total of 7,140 samples collected plus an additional 314 laboratory standards and blank samples inserted into the sample submission. All samples were sieved to a -80# fraction and submitted for 4 acid digest and ICP-MS analysis in order to obtain low detection limits for 48 elements. Final multi-element soil sample results confirmed previous copper in soil anomalies identified by Chrysalis and have identified several new significant copper in soil anomalies, including one very large anomaly located ~6km NNE of the previously drilled Kimabwe Prospect in the south-western part of the Kabwima Project (Fig. 1), (refer to ASX announcement dated 23rd July 2015).

For

per

sona

l use

onl

y

DIRECTORS’ REPORT (continued)

5

Review of Operations (continued) The regional soil results included 30 soil samples >200ppm Cu, to a maximum of 500ppm Cu from a sample collected ~17 kilometres along strike to the NW of the Mutenda prospect. The largest and most significant Cu-in-soil anomaly from within the Kabwima Project (Target H) is up to 2 kilometres wide and runs discontinuously for a distance of more than 10 kilometres. Apart from checking the residual nature of the soil in the area, the anomaly has been confirmed and characterised by plotting the Cu/Sc ratio in soil which removes the effect of Cu anomalism due to naturally elevated copper levels in mafic rock types (e.g. gabbro which are very common in this region). Figure 1 shows an image produced from the Kabwima soils Cu/Sc ratio data and confirms the Cu-in-soil anomalism associated with Target H, and various other areas including Target B, Target D, and the previously identified and drilled Kimabwe Prospect. Elevated Fe and Ti levels (typically high in soils derived from mafic rock types) have also been used to discriminate between true Cu-in-soil anomalism and rock type related elevated copper (e.g. the strong linear anomaly in the NW corner of the project appears to be gabbro related, but ground checking is obviously required).

FQM are planning to drill the Target H anomaly and also conduct additional drilling at the Kimabwe Prospect. Drilling preparation is underway.

Figure 1: Kabwima Project 500m x 500m spaced soil sample results (Cu ppm) over Cu/Sc ratio image.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT (continued)

6

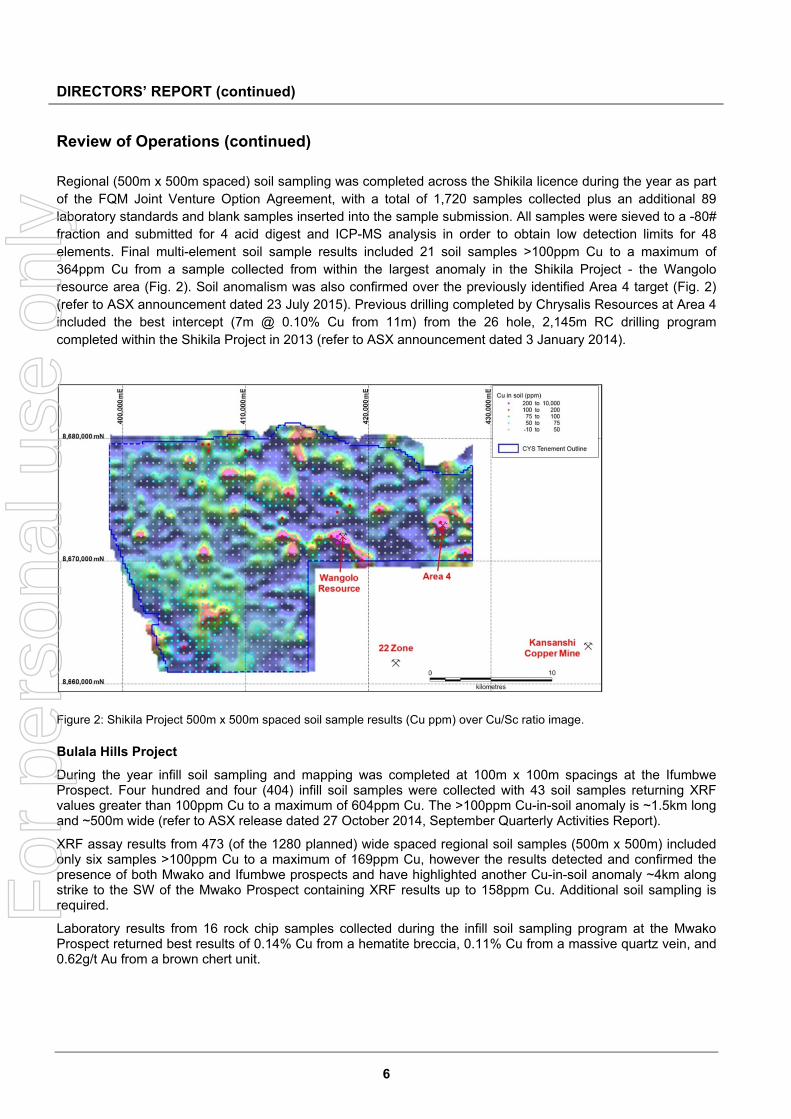

Review of Operations (continued) Regional (500m x 500m spaced) soil sampling was completed across the Shikila licence during the year as part of the FQM Joint Venture Option Agreement, with a total of 1,720 samples collected plus an additional 89 laboratory standards and blank samples inserted into the sample submission. All samples were sieved to a -80# fraction and submitted for 4 acid digest and ICP-MS analysis in order to obtain low detection limits for 48 elements. Final multi-element soil sample results included 21 soil samples >100ppm Cu to a maximum of 364ppm Cu from a sample collected from within the largest anomaly in the Shikila Project - the Wangolo resource area (Fig. 2). Soil anomalism was also confirmed over the previously identified Area 4 target (Fig. 2) (refer to ASX announcement dated 23 July 2015). Previous drilling completed by Chrysalis Resources at Area 4 included the best intercept (7m @ 0.10% Cu from 11m) from the 26 hole, 2,145m RC drilling program completed within the Shikila Project in 2013 (refer to ASX announcement dated 3 January 2014).

Figure 2: Shikila Project 500m x 500m spaced soil sample results (Cu ppm) over Cu/Sc ratio image.

Bulala Hills Project

During the year infill soil sampling and mapping was completed at 100m x 100m spacings at the Ifumbwe Prospect. Four hundred and four (404) infill soil samples were collected with 43 soil samples returning XRF values greater than 100ppm Cu to a maximum of 604ppm Cu. The >100ppm Cu-in-soil anomaly is ~1.5km long and ~500m wide (refer to ASX release dated 27 October 2014, September Quarterly Activities Report).

XRF assay results from 473 (of the 1280 planned) wide spaced regional soil samples (500m x 500m) included only six samples >100ppm Cu to a maximum of 169ppm Cu, however the results detected and confirmed the presence of both Mwako and Ifumbwe prospects and have highlighted another Cu-in-soil anomaly ~4km along strike to the SW of the Mwako Prospect containing XRF results up to 158ppm Cu. Additional soil sampling is required.

Laboratory results from 16 rock chip samples collected during the infill soil sampling program at the Mwako Prospect returned best results of 0.14% Cu from a hematite breccia, 0.11% Cu from a massive quartz vein, and 0.62g/t Au from a brown chert unit.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT (continued)

7

Review of Operations (continued) A nine hole, 1,634m reverse circulation (RC) drilling program was completed at the Mwako Prospect. The program was aimed at identifying the potential for economic copper mineralisation beneath >200ppm copper-in-soil XRF results within a semi-continuous 1km wide x 4.5km long >100ppm Cu-in-soil anomaly containing 107 >200ppm Cu-in-soil XRF values, including 1100ppm Cu, 1066ppm Cu, 971ppm and 818ppm Cu (Fig. 3).

Drilling results included three broad low grade copper intercepts including 39m @ 0.28% Cu from 97m (including 17m @ 0.32% Cu from 114m) in hole MKRC003, 36m @ 0.26% Cu from 150m in MKRC007, and 38m @ 0.19% Cu from 174m to EOH in MKRC008, all from the northern zone of copper mineralisation and all associated with an intensely silica altered sedimentary “chert” unit. Two of these holes (MKRC007 and MKRC008) ended in copper mineralisation. Disseminated pyrite, minor malachite staining and minor disseminated chalcopyrite was observed within the chert unit. The chert is located immediately above an interpreted structural contact with a strongly altered (argillic) felsic quartz-porphyry unit. The porphyry is interpreted to have intruded into a steep (~800) SE-dipping NE-striking shear zone which contains a hematite ironstone breccia unit on its northern contact (refer to ASX release dated 13 November 2014).

Gold analysis was only conducted on samples that looked prospective for gold mineralisation. Of the fifty one 1m samples selected, six returned values >0.1g/t Au to a maximum of 0.28g/t Au from a hematite ironstone breccia with minor pyrite from 104m to 105m in MKRC001. Other elevated gold values included 0.24g/t Au in a hematitic chert from 76m to 77m in MKRC004, 0.12g/t Au in magnetic chert from 25m to 26m in MKRC009, and 0.20g/t Au in magnetic chert from 184m to 185m in MKRC008. Additional gold analysis is required in order to determine the average width and grade of gold within the zones of Cu mineralisation. This will enable copper equivalent (CuEq) intercepts to be calculated.

Figure 3: Mwako Prospect RC drilling location plan with copper intercepts, major structures, and >100ppm and >200ppm Cu-in-soil anomaly contours over grey scale 1st Vertical Derivative (1VD) aeromagnetic image.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT (continued)

8

Review of Operations (continued) During the year 435 infill soil samples were collected at 50m x 100m spacings at the Kasonkomona Prospect in the central north of the Project (refer to ASX release dated 27 October 2014, September Quarterly Activities Report). XRF analysis of the soil samples included only 3 samples >90ppm Cu to a maximum of 126ppm Cu (Fig. 4). No further work is currently planned for this area.

Infill soil sampling was also completed at the Chitampira Prospect as a follow-up to anomalous regional soil sampling results. Three hundred and sixty seven (367) soil samples were collected at a 100m x 100m spacing. XRF analysis of the soil samples included 27 samples >100ppm Cu to a maximum of 147ppm Cu (Fig. 4). Further infill sampling will be required over the Cu-in-soil anomaly in the NE of the prospect area.

XRF assay results from 753 (100m x 100m spaced) infill soil samples collected during the last quarter from the area surrounding the workings and trenches at the Mulyongo Prospect included 18 samples >100ppm Cu to a maximum of 182ppm Cu (Fig. 4). Additional work is required at Mulyongo to more closely determine the residual or transported nature of the soils in the area. Reverse circulation (RC) drilling to test for sulphide copper mineralisation at depth beneath the Mulyongo gossan and Cu-Au workings is warranted.

Three hundred and sixty six (366) infill soil samples were collected at 100m x 100m spacings at the Kaporoso Prospect in the southern corner of the Project. XRF analysis of the soil samples included only 3 samples >100ppm Cu to a maximum of 325ppm Cu (Fig. 4). The program is not complete with an additional 235 infill samples planned for the eastern side of the prospect area.

Figure 4: Mwongo Project infill soil sample locations (coloured dots), rock chip samples (coloured triangles), tracks, drainage and prospects.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT (continued)

9

Review of Operations (continued) During the year licence renewals for all 5 Zambian large-scale prospecting licences were approved without reduction for a further 2 years commencing 1st July 2014. The total area covered by the Zambian prospecting licences remains at 3,023km2.

Corporate Social Responsibility

During the year a motorbike was purchased for the Mumbwa District Hospital (Mwongo Project) for medical deliveries, water sampling, child growth/health monitoring and supervision of community volunteers, and paint, sports equipment and writing materials were supplied to the Mulyango Primary School (Mwongo Project).

Australian Projects

During the 12 month period to 30 June 2015, Chrysalis continued its divestment push on the Australian Exploration Projects.

Halloween West Project (Cu/Au)

No field work was completed on this project, and after a thorough review of the Halloween West exploration data the Halloween West 37% Joint Venture equity in the project (E52/2275) was sold to the new Joint Venture farm-in partner Sandfire Resources NL for a consideration of $85,000.

Pioneer Project (Au)

No field work was completed on this project during the year. After a thorough review of the Pioneer exploration data exploration licences E63/1413 and E63/1413 were relinquished due to a perceived lack of prospectivity, and the remaining licences (E63/1117, M63/329, M63/368, P63/1429 and P63/1468) were sold to Metals-X Limited for a consideration of $30,000.

Gregory Range (U/Fe/Base Metals)

No field work was completed on this project during the year. After another thorough review of the Gregory Range exploration data and as part of the Company’s exploration divestment strategy, exploration licences E45/3120, 3E45/3313 and E45/3313 were surrendered.

West Angelas Project (Fe)

During the year Chrysalis Resources (“Chrysalis”) entered a legally binding agreement with FMG Pilbara Pty Ltd (“Fortescue”) whereby Chrysalis agreed to grant Fortescue exclusive exploration access to, and an option to purchase, the West Angelas Project Tenements (E47/1838-I and P47/1538).

In consideration, Fortescue paid Chrysalis $100,000 on the Commencement Date, and if not terminated beforehand, were to pay the sum of $100,000 on the first and second anniversaries of the Commencement Date; and if Fortescue exercised the Purchase Option, Fortescue agreed to pay Chrysalis a 1% Gross Revenue Royalty which reduces to a 0.1% GR Royalty after 10 million tonnes were mined and sold.

On 3 June 2015, Fortescue withdrew from the West Angelas Iron Ore Project Purchase Option Agreement. Prior to withdrawal all environmental rehabilitation was completed by Fortescue and the two tenements are now free of any environmental liability or any other encumbrances. Chrysalis will resume management of the project going forward. F

or p

erso

nal u

se o

nly

DIRECTORS’ REPORT (continued)

10

Corporate

Fully Underwritten Non-Renounceable Entitlement Issue (NREI)

On 8 July 2014 the company announced a fully underwritten Non-Renounceable Entitlement Issue on the basis of one new share for every two shares held on 15 July 2014 (the record date) at one cent each.

A total of 114,494,709 shares were allotted under the NREI which comprised:

• 26,200,957 shares to existing shareholders; and

• 88,293,752 shares to the Underwriter (Mr Adrian Paul), being the balance of the NREI shortfall.

Total funds raised from the NREI were $1,144,947 (before costs).

The capital raised was used to fund the costs associated with further exploration across the Zambian Copper Projects, together with meeting general working capital requirements.

First Quantum Joint Venture Option Agreement (Zambia)

On 23 October 2014 Chrysalis entered a legally binding Letter Agreement (“Agreement”) with FQM Exploration (Zambia) Limited (“FQM”) whereby FQM agreed to fund exploration across Chrysalis’ Shikila and Kabwima Projects for a 6 month period prior to earning the right to enter a two stage Earn-in phase, and subsequent Joint Venture, Put/Call and/or Net Smelter Royalty options (refer to ASX announcement dated 18 November 2014). The Letter Agreement includes licences 8194-HQ-LPL, 13404-HQ-LPL, and 13405-HQ-LPL) and includes the following terms:

• 6 month “Option Period” whereby FQM shall sole fund regional soil sampling programs across the Shikila and Kabwima Projects with a minimum spend of US$450,000. The 6 months can be shortened by completion of the soil programs and receipt of results, or extended if the wet season delays the completion of soil sampling.

• Chrysalis to manage Option Period exploration program in conjunction with technical input from FQM.

• If FQM spends $450,000 or more, and are satisfied with the soil sampling results, FQM can advance to a “First Earn-in” period.

• During the “First Earn-in” period FQM may spend an additional US$5 million within 2 years in order to earn a 51% interest and enter a formal Joint Venture Agreement.

• The Farm-in Manager will be responsible for maintaining the Licenses, including ensuring compliance with all related statutory and compliance obligations.

• FQM can then advance to a “Second Earn-in” period to earn a total 80% interest by generating an NI 43-101 compliant resource report (at FQM’s cost) for the purpose of making an application for a large scale mining licence under the Zambian Mines Act, and obtaining the successful grant of one or more large scale mining licence(s).

• Chrysalis will be carried through to production with all development costs to be paid back from production cash-flow (at LIBOR+4%).

• Within 30 days of the completion of the Second Earn-in Requirements a Put/Call option will allow FQM to force Chrysalis to sell their Joint Venture interest, or enable Chrysalis to force FQM to buy Chrysalis’ Joint Venture interest, at US$0.04c/lb. CuEq multiplied by the amount of Cu in the combined Measured, Indicated & Inferred (MII) Resource multiplied by the Joint Venture percentage of the seller.

• If either party are unable or unwilling to contribute to prorata share of cash requirements then the Joint Venture interest is diluted by an industry standard dilution formula.

• If diluted below 15% the diluting parties interest will be converted to a 1% net smelter royalty subject to a US$20,000,000 cap.

• A first right of refusal will apply to both FQM and Chrysalis.

• The Agreement was subject to due diligence on the 3 licences involved. On 12 January 2015 Chrysalis announced that it had received notification from FQM that the Due Diligence condition had been satisfied.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT (continued)

11

Corporate (continued)

On the 17 July 2015, FQM Exploration (Zambia) Limited (“FQM”) satisfied all conditions associated with the Agreement and, subsequent to reviewing the final multi-element soil sample results from the Kabwima and Shikila projects in Zambia, have elected to execute the Option and advance to the “Earn-in” period (refer to ASX announcement dated 23 July 2015). The following modifications to the “Letter Agreement” have been accepted by both parties via the execution of the “Earn-in Notice”:

• A formal drafting of the joint venture agreement may be postponed for up to 12 months whilst initial drill testing is carried out. During this time all aspects of the joint venture will continue to be governed by the Letter Agreement.

• The parties are agreed that the “First Earn-In” stage of the letter agreement will be removed altogether leaving FQM with the right to earn an undivided interest of 80% in the project by completing all necessary conditions defined as the “Second Earn-In” (clause 3d of the Letter Agreement) within four years of the Earn-in Notice, dated 17 July 2015.

• The parties acknowledge that FQM will act as Farm-in Manager and carry out all exploration activities itself (by its employees, agents or contractors) as Farm-in Manager.

Peppermint Innovation Limited Acquisition

During the year Chrysalis Resources Limited was granted an option to acquire all the issued share capital in Peppermint Innovation Limited ("Peppermint") subject to due diligence and shareholder approval. Peppermint operates a Mobile Banking, Payments and Remittance Platform (“Platform”) in the Philippines which it intends to expand throughout Asia, Australia, the Middle East, Europe and Tunisia (refer to ASX announcement dated 21 May 2015).

The Mobile Banking, Payments and Remittance market is a rapidly expanding industry with significant market potential as the prevalence and reliance on mobile telecommunication continues to increase. Peppermint operate an established Platform and develop new and innovative mobile phone applications aimed at improving business efficiency and deriving revenue for commercial clients and agent networks. A key aspect of the Platform is to provide a mechanism, via a mobile phone, to the global unbanked population to bridge the financial inclusion gap. Peppermint already have a highly qualified and experienced technical development and management team in place.

On 23 July 2015 Chrysalis announced that the Due Diligence requirements had been satisfied and the Option to Acquire was exercised. On 21 July 2015 both Chrysalis and Peppermint elected not to enter into a Definitive Agreement as originally stated in the Binding Term Sheet (BTS) dated 20 May 2015, instead using the terms and conditions of an amended BTS. The key acquisition terms and conditions precedent including the recent amendments to the BTS include:

• Chrysalis is to obtain all regulatory approvals for the Acquisition, including in particular ASX approval for the readmission of Chrysalis to the official list of the ASX in connection with its change in nature and scale of activities.

• the removal of the 1 for 5 consolidation of Chrysalis share capital prior to the Acquisition. The parties agree that subject to Chrysalis obtaining a waiver from Listing Rule 2.1, Condition 2 (20c Rule Waiver) in respect of Chrysalis’ proposed recompliance with Chapters 1 and 2 of the ASX Listing Rules, Chrysalis will not undertake a consolidation of its share capital in respect of the Acquisition of all the Peppermint shares.

• the allotment and issue of 350,000,000 Acquisition Shares by Chrysalis to the Vendors (the Peppermint Shareholders) in consideration for the Acquisition.

• the issue of 100,000,000 Performance Shares. Performance Shares shall not vest until the Milestones to which they attach are achieved and the Acquisition Shares shall be escrowed in accordance with ASX requirements. Each (1) Performance Share shall be issued on completion and is convertible into one (1) ordinary share in the capital of Chrysalis, upon the following milestones being achieved.

o Milestone 1: 50 million Performance shares will vest upon Chrysalis or its subsidiaries generating cumulative revenue of $15,000,000 from the Mobile Banking, Payments and Remittance Business operated by Peppermint (MBPRB) or in the event of a Change of Control within 5 years of the date of the Term Sheet.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT (continued)

12

Corporate (continued)

o Milestone 2: 50 million Performance shares will vest upon Chrysalis or its subsidiaries generating cumulative revenue of $50,000,000 from the MBPRB or in the event of a Change of Control within 5 years of the date of the Term Sheet.

o Conversion is subject to the following:

- the issue of Shares on conversion of Performance Shares on a Change of Control shall at all times be limited to 10% of the total shares on issue at the date of the Change of Control; and

- a “Change of Control” occurs where a third party becomes entitled to more than 50% of the Chrysalis shares or where all those shares are either cancelled or transferred to a third party under Court Order.

• the replacement of the Transaction Timetable with the following clause; “The parties agree they will use their best endeavours to ensure that the transaction proceeds and completes as soon as possible.”

• Chrysalis must successfully complete a capital raising under a prospectus to raise sufficient funds to meet the ASX Chapter 1 and 2 readmission requirements and satisfactorily deliver the business plan and objectives of PEP in connection with its readmission. The capital required is currently estimated at $3,500,000.

The Acquisition remains subject to the necessary shareholder and regulatory approvals, and satisfaction of the remaining conditions precedent under the BTS. A general meeting has been convened for 2 October 2015 at which shareholders will have the opportunity to vote on the Acquisition and other related matters.

In light of the above, the updated indicative effect of the Acquisition on the capital structure of Chrysalis is expected to be as follows:

Ordinary Shares

Performance Shares

Existing Shares 345,484,128 Ordinary Shares as Consideration 350,000,000 Performance Shares as Consideration - 100,000,000Shares issued under Prospectus* 175,000,000 TOTAL 870,484,128 100,000,000

* Assumes a minimum capital raise of $3.5m at an issue price of $0.02 per Share.

Subject to the receipt of shareholder approval, Chrysalis will undertake a capital raising under a prospectus to raise sufficient funds to meet the ASX Chapter 1 and 2 readmission requirements and deliver the business plan and objectives of Peppermint in connection with its readmission. The current estimated funding required is $3,500,000. The majority of the funds will be used to establish and expand the existing Peppermint subscriber base.

On completion of the Acquisition of Peppermint and readmission of Chrysalis, the Board of Chrysalis shall comprise three directors nominated by PEP and a maximum of one existing director of Chrysalis.

ASX Listing Rules Re-compliance and Financial Information

The Acquisition of Peppermint will result in a change to the nature and scale of Chrysalis (“the Company”) and will require shareholder approval under Chapter 11 of the ASX Listing Rules and will also require the Company to re-comply with Chapters 1 and 2 of the ASX Listing Rules. The Company has dispatched a notice of meeting to shareholders seeking all of the relevant approvals. F

or p

erso

nal u

se o

nly

DIRECTORS’ REPORT (continued)

13

Corporate (continued)

DJ Carmichael Corporate Advisors and Lead Manager

Chrysalis has announced that DJ Carmichael Pty Ltd (DJC) have been appointed as Corporate Advisors for Chrysalis in order to assist in raising up to $3.5 million of additional equity funding as part of the Company’s proposed re-compliance with Chapters 1 and 2 of the ASX Listing Rules (Re-listing). As disclosed above Chrysalis proposes to place 175 million ordinary fully paid shares at an issue price of $0.02 pursuant to a Re-Listing prospectus to be lodged with the Australian Securities and Investments Commission as soon as practicable. DJC will assist the Company in meeting its objectives on a best endeavours basis with regards to the issue of new Shares pursuant to the Re-Listing, and are named as Lead Manager, on the terms and conditions set out in the Corporate Advisory Services Mandate signed by Chrysalis and DJC.

Board Changes

Mr Michael Griffiths and Ms Jing Wang resigned as Non-Executive and Executive Director respectively on 23 of September 2014. Mr Leigh Ryan assumed the role of Managing Director on 23 of September 2014. Financial At 30 June 2015, the Company had cash reserves of $159,446 (2014: $694,497). Capitalised exploration and evaluation expenditure is $1,059,896 (2014: $3,772,954). Exploration expenditure during the year was $1,224,011 (2014: $1,448,713). The net loss for the year was $4,353,904 (2014: $2,788,971) which included a Zambian loss of $3,744,821 (2014: $819,014) which supports the delivery of the exploration program in Zambia. Included in the net loss for the year is an impairment of exploration assets for $3,938,589 following a Board review of existing tenements as detailed in Note 8.

In the past year there has been a strong focus on reducing administration costs with reductions in director and employee costs $543,707 (2014: $1,139,207), other expenses $391,343 (2014: $756,847) and accounting fees $61,615 (2014: $135,250). Significant changes in the state of affairs In the opinion of the directors, there were no other significant changes in the state of affairs of the Group that occurred during the financial year not otherwise disclosed in this report or in the financial report. Matters Subsequent to the End of the Financial Year

There has not been any matter or circumstance that has arisen after balance date that has significantly affected, or may significantly affect, the operations of the Group, the results of those operations, or the state of affairs of the Group in future financial years, other than those detailed below:

• Further to the announcement on 21 May 2015 in which the Company announced that it had been granted an option to acquire all the issued capital in Peppermint Innovation Limited (“Peppermint”), the following events have been announced.

o On 3 July 2015 the Company advised that it had agreed with Peppermint to extend the Due Diligence period for the acquisition of Peppermint to 18 July 2015.

o On 23 July 2015 the Company announced that the Due Diligence requirements had been satisfied and that the Company had exercised the Option to acquire Peppermint. DJ Carmichael Pty Ltd had been appointed Corporate Advisors and Lead Manager to assist in raising up to $3,500,000 of additional equity funding. The acquisition remains conditional upon the Company obtaining necessary shareholder and regulatory approvals, together with satisfaction of the remaining conditions precedent under the binding term sheet.

• On 23 July 2015 the Company advised that FQM Exploration (Zambia) Limited (“FQM”) had satisfied all conditions associated with the exclusive option period within the “Letter Agreement” dated 23 October 2014, (refer to ASX announcement dated 18th November 2014), and have elected to execute the Option and advance to the “Earn-in” period.

• On 11 September 2015 the Company executed a short-term unsecured loan agreement for up to $200,000 to complete the Peppermint transaction pursuant to the binding term sheet between the Company and Peppermint dated 20 May 2015.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT (continued)

14

Financial (continued) Likely developments and expected results

The Group will undertake a capital raising under a prospectus to raise sufficient funds to meet the ASX Chapter 1 and 2 readmission requirements and deliver the business plan and objectives of Peppermint in connection with its readmission. Environmental legislation

The Group’s exploration activities are subject to environmental regulations under both Commonwealth of Australia and Western Australian State legislation as well as Zambian Government legislation.

The Board believes the Group has adequate systems in place for the management of its environmental requirements and is not aware of any breach of those environmental requirements as they apply to the Group during 2015 and up until the date of this report. Remuneration Report

This report outlines the remuneration arrangements in place for key management personnel of the Company and its controlled entities for the financial year ended 30 June 2015. The information provided in this remuneration report has been audited as required by Section 308(3C) of the Corporations Act 2001.

The remuneration report details remuneration arrangements for key management personnel (“KMP”) who are defined as those persons having authority and responsibility for planning, directing and controlling the major activities of the Company and its controlled entities, directly or indirectly, including any director (whether executive or otherwise) of the Company. Key Management Personnel Directors

Dr Neale Fong Non-Executive Chairman

Mr Leigh Ryan1 Managing Director Appointed 23 September 2014

Mr Jian Hua Sang2 Non-Executive Director

Mr Michael Griffiths3 Non-Executive Director Resigned 23 September 2014

Ms Jing Wang Executive Director Resigned 23 September 2014 Notes: 1. Mr Leigh Ryan was appointed as Managing Director on 23 September 2014.

2. Mr Michael Griffiths was appointed as Alternate Director to Mr Bradley Marwood on 5 April 2013, subsequently appointed as Non-

Executive director on 26 July 2013 and resigned 23 September 2014.

3. Ms Jing Wang was appointed Executive Director on the 1 November 2013 and resigned on the 23 September 2014.

Executives

Mr Kevin Hart Company Secretary

Mr Patrick Soh Chief Financial Officer

Mr John Noakes Director (Sedgwick Resources Limited)

Mr Christopher Simasiku Director / Company Secretary (Sedgwick Resources Limited)

Mr Jeremy Hawksworth Exploration Manager Resigned 31 January 2014

For

per

sona

l use

onl

y

DIRECTORS’ REPORT (continued)

15

Financial (continued) Details of KMP remuneration are set out under the following main headings: A Principles used to determine the nature and amount of remuneration B Details of remuneration including share-based compensation remuneration C Employment contracts of key management personnel D Remuneration of key management personnel E Shareholdings of key management personnel F Share-based compensation - share plan shares G Option holdings of key management personnel H Transactions with related parties of key management personnel A Principles used to determine the nature and amount of remuneration The objective of the Company’s reward framework is to ensure reward for performance is competitive and appropriate for the results delivered. The framework aims to align reward with the creation of value for shareholders. The Board ensures that employee reward satisfies the following key criteria for good reward governance practices: • competitiveness and reasonableness • acceptability to shareholders • performance incentives • transparency • capital management The framework provides a mix of fixed fee, consultancy agreement based remuneration, and share-based incentives. Company performance and link to remuneration Mr Ryan has been granted 3,000,000 performance shares of which 2,000,000 of these relate to market performance as detailed in the performance rights holdings table. Below is a table showing the Group’s performance and EPS over the last 4 financial years.

30 June 2012 30 June 2013 30 June 2014 30 June 2015

Financial year profit / (loss) - $ (1,207,470) (3,905,006) (2,788,971) (4,353,904)

EPS / (Loss per share) - cents (2.13) (2.90) (1.29) (1.35)

Share price - cents 8 5.5 1.5 3.5

B Details of remuneration

Remuneration structure In accordance with best practice corporate governance, the structure of non-executive director and executive remuneration is separate and distinct.

Non-executive directors The Board seeks to set aggregate remuneration at a level that provides the Company with the ability to attract and retain directors of the highest calibre, whilst incurring a cost that is acceptable to shareholders.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT (continued)

16

Financial (continued) The ASX Listing Rules specify that the aggregate remuneration of non-executive directors shall be determined from time to time by a general meeting. The latest determination was at the Annual General Meeting held on 20 November 2009 when shareholders approved an aggregate remuneration of $300,000 per year as a base salary. The amount of aggregate remuneration sought to be approved by shareholders and the manner in which it is apportioned amongst directors is reviewed annually. The Board considers advice from external shareholders as well as the fees paid to non-executive directors of comparable companies when undertaking the annual review process. Each director receives a fee for being a director of the Company. The remuneration of non-executive directors for the year ended 30 June 2015 is detailed in section D of this report. Employee share plan Non-executive directors are encouraged by the Board to hold shares in the Company (purchased on market and in accordance with the Company’s approved policies to ensure there is no insider trading). It is considered good governance for directors of a company to have a stake in that company. The non-executive directors of the Company may also participate in the share and option plans as described in this report. The objective of the Chrysalis Employee Share Plan is to ensure that the Company has appropriate mechanisms in place to continue to attract and retain the services of suitable directors, consultants and employees. The plans provide an incentive for participants to participate in the future growth of the Company and, upon becoming shareholders in the Company, to participate in the Company’s profits and development. There are no performance criteria attached to shares given the Company’s projects are currently within an exploration phase. The key features of the schemes are set out below. Executive director remuneration The Company aims to reward executives with a level and mix of remuneration commensurate with their position and responsibilities within the Company and so as to:

reward executives for Company, business team and individual performance;

align the interests of executives with those of shareholders; and

ensure total remuneration is competitive by market standards. Remuneration consists of fixed annual remuneration and variable remuneration (comprising short-term and long-term incentive schemes). Fixed annual remuneration Fixed remuneration is reviewed annually by the Board of directors. The process consists of a review of relevant comparative remuneration in the market and internally and, where appropriate external advice on policies and practices. The Board of directors has access to external and independent advice where necessary. Variable annual remuneration Short-term incentives The Performance Rights of Mr Ryan include rights that vested upon completion of 12 months service and were issued on 4 December 2014.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT (continued)

17

Financial (continued) Long-term incentives Retirement allowances for directors Apart from superannuation payments paid on base director fees there are no retirement allowances for directors. Employee share plan To ensure that the Company has appropriate mechanisms in place to continue to attract and retain the services of suitable directors, consultants and employees, the Company established an Employee Share Plan (the “Plan”), which was approved by the Shareholders on 20 November 2009 at the Company’s Annual General Meeting. The Plan was not renewed at the Company’s 2012 Annual General Meeting and as such should the Company issue shares to directors, consultants and employees under the Plan, the issue will impact the Company’s 15% placement capacity under ASX listing rule 7.1.

The number of Ordinary Shares that may be offered to a Participant is entirely within the discretion of the Board. The Company does not intend to offer more than 5% of the issued share capital of the Company under the Plan.

The Board’s policy is to remunerate directors at market rates for time, commitment and responsibilities. The board determines payments to the directors and reviews their remuneration annually, based on market practice, duties and accountability. During the year no independent external advice was utilised, but it is sought when required. The maximum aggregate amount of directors’ fees that can be paid is subject to approval by shareholders in general meeting, from time to time. Fees for non-executive directors are not linked to the performance of the Company. However, to align directors’ interests with shareholders’ interests, the directors are encouraged to hold securities in the Company.

The Company’s aim is to remunerate at a level that will attract and retain high-calibre directors and employees. Company officers and directors are remunerated to a level consistent with the size of the company. All remuneration paid to directors and executives is valued at the cost to the Company and expensed.

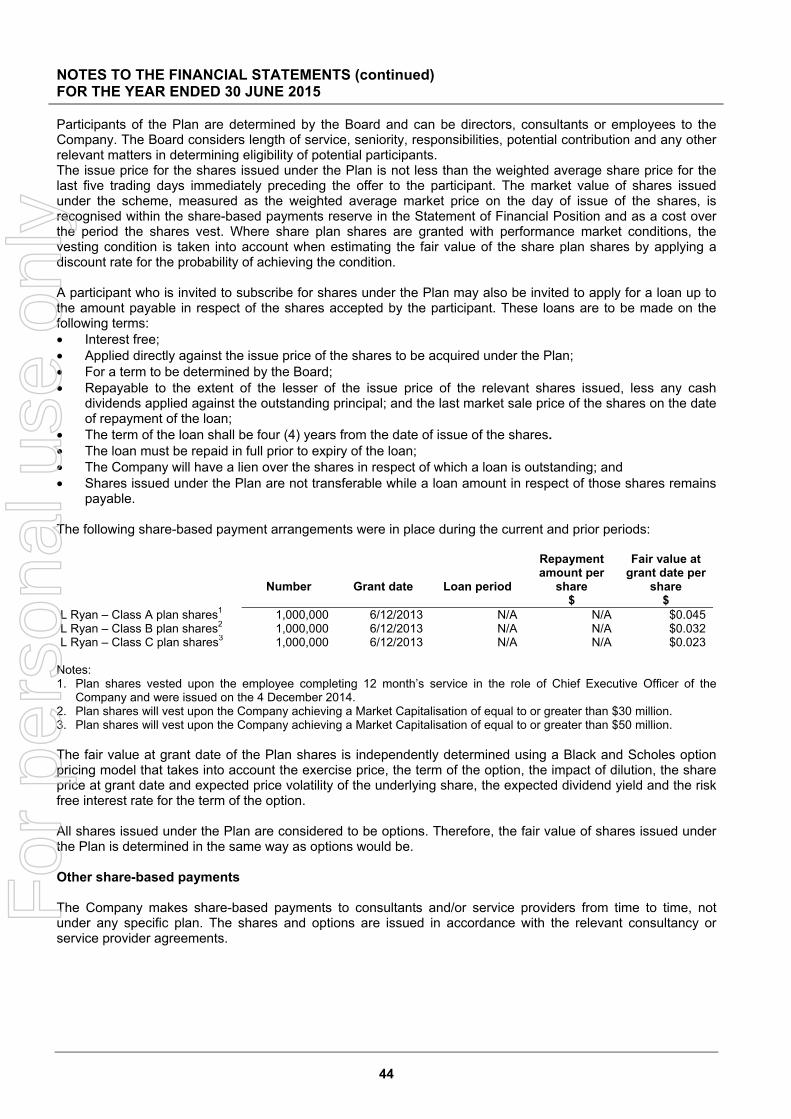

Participants of the Plan are determined by the Board and can be employees and directors of, or consultants to, the Company or a controlled entity. The Board considers length of service, seniority, responsibilities, potential contribution and any other relevant matters in determining eligibility of potential participants.

The issue price for the shares issued under the Plan are not less than the weighted average share price for the last five trading days immediately preceding the offer to the participant.

A participant who is invited to subscribe for shares under the Plan may also be invited to apply for a loan up to the amount payable in respect of the shares accepted by the participant. These loans are to be made on the following terms:

• Applied directly against the issue price of the shares to be acquired under the Plan; • For a term to be determined by the Board; • Repayable to the extent of the lesser of the issue price of the relevant shares issued, less any cash

dividends applied against the outstanding principal; and the last market sale price of the shares on the date of repayment of the loan;

• The loan must be repaid in full prior to expiry of the loan; and • The Company will have a lien over the shares in respect of which a loan is outstanding. The market value of the option implicit in the share issued under the Plan (funded by way of a loan on the conditions noted above), measured using the Black and Scholes option pricing model, is recognised in the financial statements as an equity benefit reserve and as employee benefit costs in the period over which the shares vest. The Employee Share Plan shares were issued by the Company during the year ended 30 June 2014 and are detailed in section F of the Remuneration Report.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT (continued)

18

Financial (continued) C Employment contracts of key management personnel Agreements with Directors The employment arrangements of the non-executive directors are formalised in a contract for services. Agreements with Executives The employment arrangements of executives formalised in a contract of employment are listed below: Chief Executive Officer

On 10 December 2013 the Company announced the appointment of Mr Leigh Ryan as Chief Executive Officer effective from the 2 December 2013.

An agreement executed on the 6 December 2013 does not have a fixed contract period. It requires that:

i) the Company may terminate the employment contract at any time by giving three months notice; or

ii) Mr Ryan may terminate the employment contract at any time by providing the Company with three months notice.

iii) Fixed remuneration in the form of a base salary at $220,000 plus superannuation which was reduced by 25% from December 2014 and reduced by a further 25% from May 2015.

iv) Employee Share Plan Participation

a. 1,000,000 plan shares vesting on completion of 12 month’s service in the role of Chief Executive Officer were issued on the 4 December 2014.

b. 1,000,000 plan shares will vest upon the Company achieving a Market Capitalisation of equal to or greater than $30,000,000.

c. 1,000,000 plan shares will vest upon the Company achieving a Market Capitalisation of equal to or greater than $50,000,000.

Contracted key management personnel are engaged on standard commercial terms. D Remuneration of key management personnel

Key management personnel remuneration for the year ended 30 June 2015 and 30 June 2014

Short-term employee benefits

Post-employment

benefits

Other long-term benefits

Share-based

payments

Salary & Fees

$

Bonuses

$

Other

$

Super-annuation

$

Long-service leave

$

Equity-settled

$

Total

$

Perform-ance

Related

% 2015 Directors

Dr Neale Fong 49,584 - - 4,710 - - 54,294 -

Mr Leigh Ryan1 180,563 - - 17,154 - 25,851 223,568 11.6%

Mr Jian Hua Sang 35,416 - 2,000 3,365 - - 40,781 -

Mr Michael Griffiths2 12,500 - - 1,188 - - 13,688 -

Ms Jing Wang3 33,333 - 900 3,167 - - 37,400 -

Key Management Personnel

Mr Kevin Hart 58,864 - - - - - 58,864 -

Mr Patrick Soh 56,250 - - - - - 56,250 -

Mr John Noakes - - - - - - - -

Mr Christopher Simasiku 50,472 - - - - - 50,472 -

For

per

sona

l use

onl

y

DIRECTORS’ REPORT (continued)

19

Financial (continued)

Short-term employee benefits

Post-employment

benefits

Other long-term benefits

Share-based

payments

Salary & Fees

$

Bonuses

$

Other

$

Super-annuation

$

Long-service leave

$

Equity-settled

$

Total

$

Perform-ance

Related

% 2014 Directors

Dr Neale Fong 82,500 - - 7,631 - - 90,131 -

Mr Jian Hua Sang 133,765 - 6,386 2,698 - - 142,849 -

Mr Trevor Benson4 21,331 - - 1,973 - - 23,304 -

Mr Michael Griffiths2 48,316 - - 4,469 - - 52,785 -

Mr Grant Kidner5 41,667 - - 3,854 - - 45,521 -

Mr Bradley Marwood6 50,328 - - - - - 50,328 -

Mr Adrian Paul7 22,917 - - 2,120 - - 25,037 -

Ms Jing Wang3 62,917 - 9,118 5,820 - - 77,855 -

Key Management Personnel

Mr Leigh Ryan1 188,923 - - 11,740 - 40,254 240,917 16.7%

Mr Kevin Hart 24,524 - - - - - 24,524 -

Mr Patrick Soh 39,500 - - - - - 39,500 -

Mr John Noakes - - - - - - - -

Mr Christopher Simasiku 62,052 - 7,462 - - - 69,514 -

Ms Melanie Cotterell8 12,500 - - 1,156 - - 13,656 -

Mr Jeremy Hawksworth9 154,493 - - - - - 154,493 - Notes: 1. Appointed as Chief Executive Officer from 2 December 2013 and subsequently appointed as Managing Director on 23 September 2014. 2. Appointed as Alternate Director to Mr Bradley Marwood on 5 April 2013, subsequently appointed as Non-Executive director on

26 July 2013. 3. Appointed as Executive Director from 1 November 2013 and resigned on the 23 September 2014. 4. Resigned 29 November 2013 5. Resigned 29 November 2013 6. Resigned 29 July 2013 7. Resigned 29 November 2013 8. Resigned as Company Secretary 2 December 2013 9. Resigned 31 January 2014 E Shareholdings of key management personnel

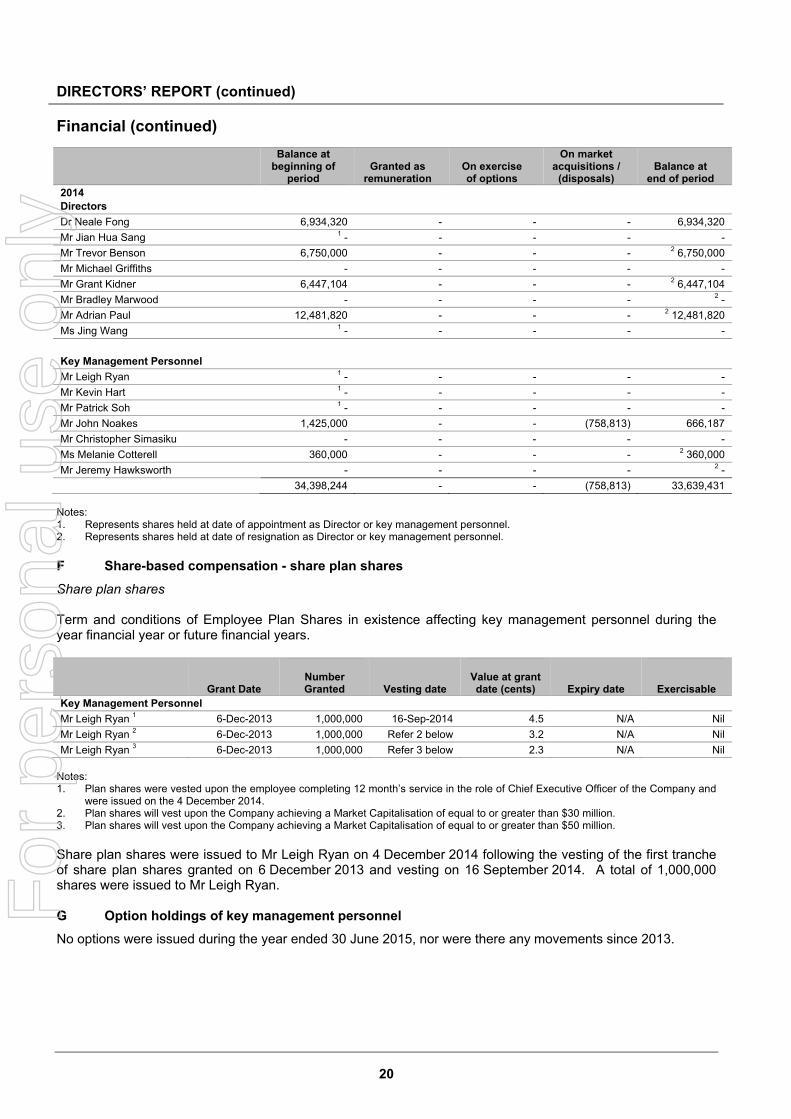

Balance at beginning of

period Granted as

remuneration On exercise of options

On market acquisitions /

(disposals) Balance at

end of period 2015 Directors

Dr Neale Fong 6,934,320 - - 677,160 7,611,480

Mr Leigh Ryan - 1,000,000 - - 1,000,000

Mr Jian Hua Sang - - - - -

Mr Michael Griffiths - - - - 2 -

Ms Jing Wang - - - - 2 -

Key Management Personnel

Mr Kevin Hart - - - - -

Mr Patrick Soh - - - - -

Mr John Noakes 666,187 - - (333,095) 333,092

Mr Christopher Simasiku - - - - -

7,600,507 1,000,000 - 344,065 8,944,572

For

per

sona

l use

onl

y

DIRECTORS’ REPORT (continued)

20

Financial (continued)

Balance at beginning of

period Granted as

remuneration On exercise of options

On market acquisitions /

(disposals) Balance at

end of period 2014 Directors

Dr Neale Fong 6,934,320 - - - 6,934,320

Mr Jian Hua Sang 1 - - - - -

Mr Trevor Benson 6,750,000 - - - 2 6,750,000

Mr Michael Griffiths - - - - -

Mr Grant Kidner 6,447,104 - - - 2 6,447,104

Mr Bradley Marwood - - - - 2 -

Mr Adrian Paul 12,481,820 - - - 2 12,481,820

Ms Jing Wang 1 - - - - -

Key Management Personnel

Mr Leigh Ryan 1 - - - - -

Mr Kevin Hart 1 - - - - -

Mr Patrick Soh 1 - - - - -

Mr John Noakes 1,425,000 - - (758,813) 666,187

Mr Christopher Simasiku - - - - -

Ms Melanie Cotterell 360,000 - - - 2 360,000

Mr Jeremy Hawksworth - - - - 2 -

34,398,244 - - (758,813) 33,639,431 Notes: 1. Represents shares held at date of appointment as Director or key management personnel. 2. Represents shares held at date of resignation as Director or key management personnel. F Share-based compensation - share plan shares

Share plan shares Term and conditions of Employee Plan Shares in existence affecting key management personnel during the year financial year or future financial years.

Grant Date

Number Granted

Vesting date

Value at grant date (cents)

Expiry date

Exercisable Key Management Personnel

Mr Leigh Ryan 1 6-Dec-2013 1,000,000 16-Sep-2014 4.5 N/A Nil

Mr Leigh Ryan 2 6-Dec-2013 1,000,000 Refer 2 below 3.2 N/A Nil

Mr Leigh Ryan 3 6-Dec-2013 1,000,000 Refer 3 below 2.3 N/A Nil Notes: 1. Plan shares were vested upon the employee completing 12 month’s service in the role of Chief Executive Officer of the Company and

were issued on the 4 December 2014. 2. Plan shares will vest upon the Company achieving a Market Capitalisation of equal to or greater than $30 million. 3. Plan shares will vest upon the Company achieving a Market Capitalisation of equal to or greater than $50 million. Share plan shares were issued to Mr Leigh Ryan on 4 December 2014 following the vesting of the first tranche of share plan shares granted on 6 December 2013 and vesting on 16 September 2014. A total of 1,000,000 shares were issued to Mr Leigh Ryan. G Option holdings of key management personnel

No options were issued during the year ended 30 June 2015, nor were there any movements since 2013.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT (continued)

21

Financial (continued) H Transactions with related parties of key management personnel

The following table provides the total amount of transactions that were entered into with related parties for the relevant financial year:

Income from

Related Parties Expenditure to Related Parties

Amounts Owed by Related

parties at year end

Amounts Owed to Related

parties at year end

$ $ $ $

Craigstone Pty Ltd 1 2015 - - - -

2014 - 64,906 - 78,000

Equiti partners 2 2015 - - - -

2014 - 138,429 - 30,430

Yangtze Trust 3 2015 - 2,000 - -

2014 - 165,356 - - Notes: 1. Mr J Noakes, a director of Sedgwick Resources Limited, is a director of Craigstone Pty Ltd. During the financial year 2014, Mr Noakes

received geological exploration consultancy fees from the Company. 2. Mr G Kidner was an Executive director, is a director of Equiti Partners. During the 2014 financial year, Equiti Partners received fees for

accounting, secretarial, executive consultancy fees, administration services and reimbursement of car parking facilities from the Company.

3. Mr Jian Hua Sang, a Non-Executive directors is a beneficiary of Yangtze Trust. During the financial year Mr Sang received a consulting fee and in 2014 received a commission on funds raised from EBH.

For the year ended 30 June 2015, the Group has not made any allowance for doubtful debts relating to amounts owed by related parties due to solid payment history (2013: $nil). An impairment assessment is undertaken each financial year by examining the financial position of the related party and the market in which the related party operates to determine whether there is objective evidence that a related party receivable is impaired. When such objective evidence exists, the Group recognises an allowance for the impairment loss. End of Remuneration Report Directors’ Meetings

The Board has not established separate committees and performs the roles of these committees in separately identified meetings.

The number of meetings of directors (including meetings of committees of directors) held during the year and the number of meetings attended by each director was as follows:

Directors’ meetings Audit committee

Nomination and remuneration

committee

Attended Held Attended Held Attended Held

Number of meetings attended:

Dr Neale Fong 7 7 2 2 1 1

Mr Leigh Ryan1 4 4 2 2 1 1

Mr Jian Hua Sang 6 7 2 2 1 1

Mr Michael Griffiths2 3 3 - - - -

Ms Jing Wang3 2 3 - - - -

Notes: 1. Appointed as Chief Executive Officer from 2 December 2013 and subsequently appointed as Managing Director on 23 September 2014. 2. Appointed as Alternate Director to Mr Bradley Marwood on 5 April 2013, subsequently appointed as Non-Executive director on

26 July 2013. 3. Appointed as Executive Director from 1 November 2013 and resigned on the 23 September 2014.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT (continued)

22

Directors’ Meetings (continued)

Indemnification and insurance of Directors and Officers The Company has agreed to indemnify all the directors of the Company for any liabilities to another person (other than the Company or related body corporate) that may arise from their position as directors of the Company, except where the liability arises out of conduct involving a lack of good faith. During the financial year the Company paid a premium in respect of a contract insuring the directors and officers of the company and its controlled entities against any liability incurred in the course of their duties to the extent permitted by the Corporations Act 2001. The contract of insurance prohibits disclosure of the nature of the liability and the amount of the premium. Proceedings on behalf of the company No person has applied for leave to the Court to bring proceedings on behalf of the Company or intervene in any proceedings to which the Company is a party for the purpose of taking responsibility on behalf of the Company for all or any part of those proceedings. The Company was not a party to any such proceedings during the year. Auditor Independence and Non-Audit Services Section 307C of the Corporations Act 2001 requires our auditors, HLB Mann Judd, to provide the directors of the Company with an Independence Declaration in relation to the audit of the annual report. This Independence Declaration is set out on page 22 and forms part of this Directors’ Report for the year ended 30 June 2015. Non-Audit Services The Company’s auditors provided tax compliance services during the financial year ended 30 June 2015. The directors are satisfied that the provision of non-audit services by the auditor did not compromise the auditor independence requirements of the Corporations Act 2001. Signed in accordance with a resolution of the directors.

Dr Neale Fong Non-Executive Chairman Perth, 14 September 2015 Competent Person’s Statement The information in this report that relates to exploration results is based on information compiled by Mr Leigh Ryan, CEO employed by Chrysalis, who is a Member of the Australian Institute of Geoscientists (MAIG). Mr Ryan has sufficient experience relevant to the style of mineralisation and type of deposit under consideration and to the activity he is undertaking to qualify as a Competent Person as defined in the 2012 Edition of the “Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves”. Mr Ryan consents to the inclusion in the report of the matters based on information in the form and context in which it appears. Mr Ryan participates in the Company’s Employee Share Plan. The Company confirms that it is not aware of any new information or data that materially affects the information included in the original market announcement and, in the case of estimates of Mineral Resources that all material assumptions and technical parameters underpinning the estimate in the relevant market announcement continue to apply and have not materially changed. The Company confirms that the form and context in which the Competent Person’s findings are presented have not materially modified from the original market announcement.

For

per

sona

l use

onl

y

AUDITORS INDEPENDENCE DECLARATION

23

For

per

sona

l use

onl

y

STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 30 JUNE 2015

24

Consolidated

Note 2015

$ 2014

$ Interest income 2 11,054 43,943 Gain from sale of tenements 2 100,000 Other income 2 630,064 2,002 Accounting fees (61,615) (135,250) Audit fees (44,937) (35,258) Depreciation and amortisation (54,473) (65,749) Directors’ remuneration (143,263) (449,590) Employee benefits expense (400,444) (689,617) Stock exchange and registry fees (40,774) (44,968) Corporate social responsibility (19,584) (28,740) Tenement management fees - (6,304) Costs associated with Zambian Copper Project - (26,159) Impairment of exploration costs 8 (3,938,589) (596,434) Other expenses 2 (391,343) (756,847) Loss before income tax expense (4,353,904) (2,788,971)Income tax expense 3 - - Net loss for the year

(4,353,904)

(2,788,971)

Other comprehensive income / (loss) Items that may be reclassified to profit or loss Exchange difference on translation of foreign operations 87,509 (396,731) Total comprehensive loss for the year (4,266,395) (3,185,702) Earnings per share Basic loss per share (cents) 5 (1.35) (1.29)Diluted earnings per share (cents) 5 (1.35) (1.29)

The accompanying notes form part of this financial statement.

For

per

sona

l use

onl

y

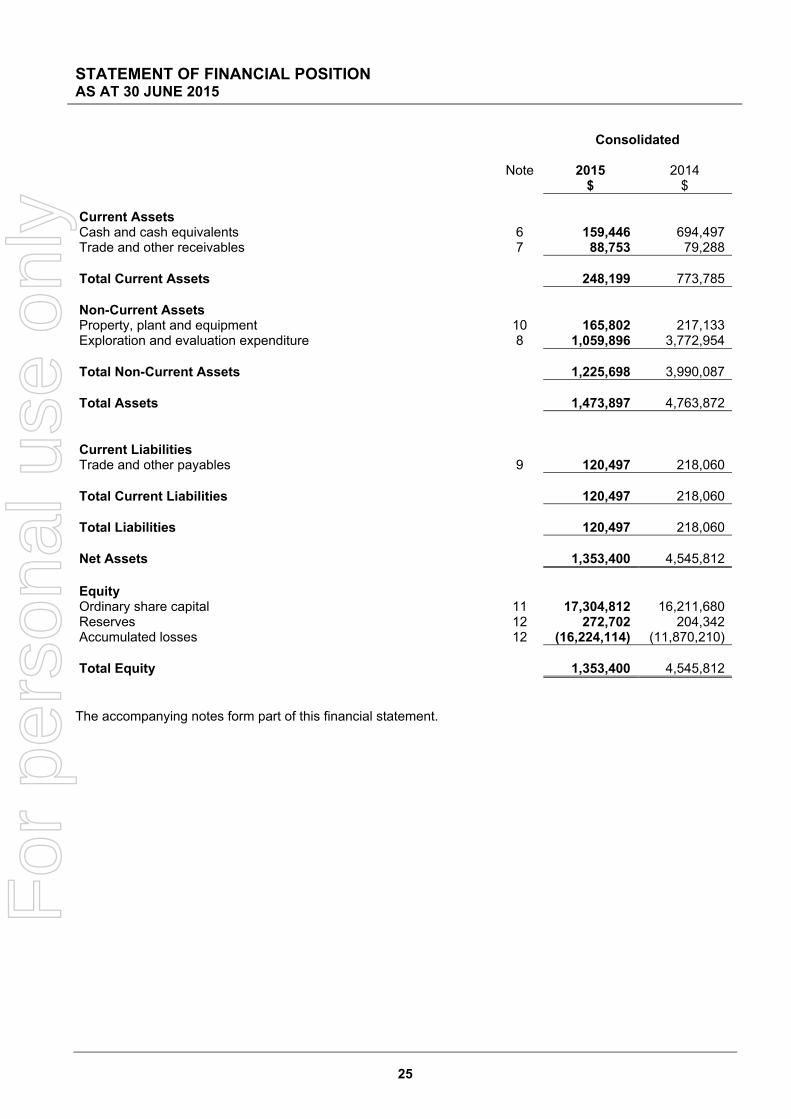

STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE 2015

25

Consolidated

Note 2015

$ 2014

$ Current Assets Cash and cash equivalents 6 159,446 694,497Trade and other receivables 7 88,753 79,288 Total Current Assets 248,199 773,785 Non-Current Assets Property, plant and equipment 10 165,802 217,133Exploration and evaluation expenditure 8 1,059,896 3,772,954 Total Non-Current Assets 1,225,698 3,990,087 Total Assets 1,473,897 4,763,872 Current Liabilities Trade and other payables 9 120,497 218,060 Total Current Liabilities 120,497 218,060 Total Liabilities 120,497 218,060 Net Assets 1,353,400 4,545,812 Equity Ordinary share capital 11 17,304,812 16,211,680Reserves 12 272,702 204,342Accumulated losses 12 (16,224,114) (11,870,210) Total Equity 1,353,400 4,545,812

The accompanying notes form part of this financial statement.

For

per

sona

l use

onl

y

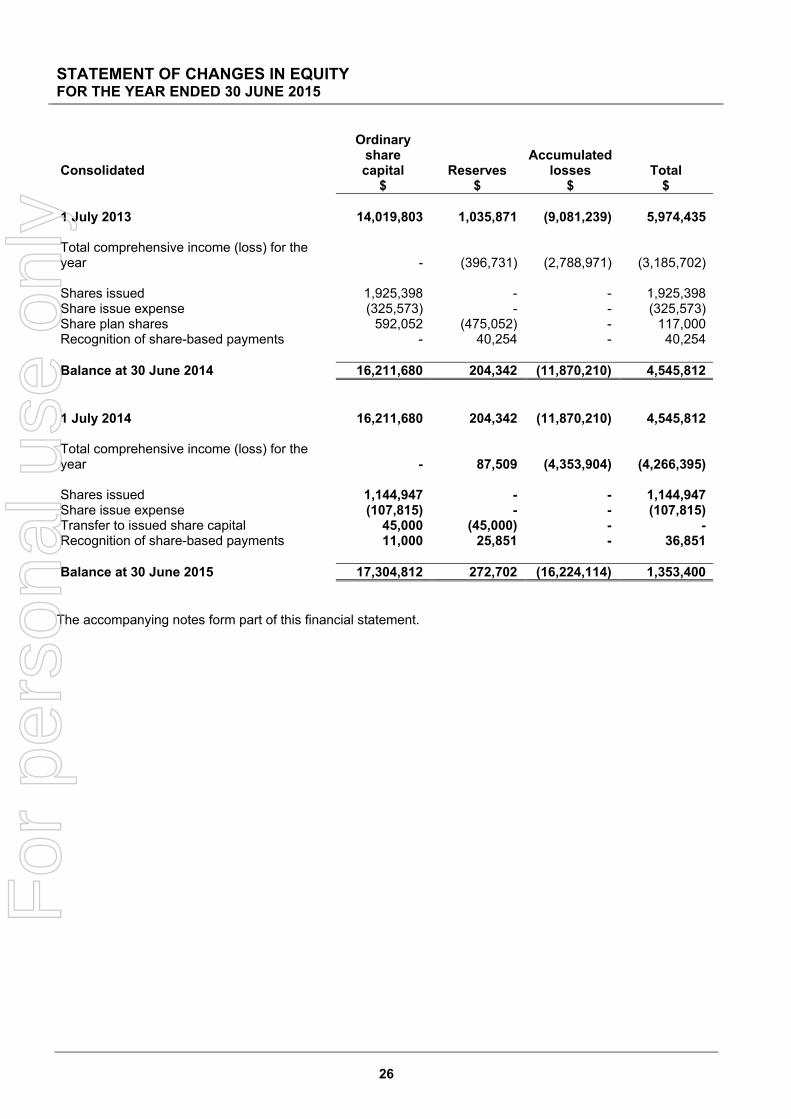

STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 30 JUNE 2015

26

Consolidated

Ordinary share capital

$ Reserves

$

Accumulated losses

$ Total

$ 1 July 2013

14,019,803 1,035,871 (9,081,239) 5,974,435

Total comprehensive income (loss) for the year - (396,731) (2,788,971) (3,185,702) Shares issued 1,925,398 - - 1,925,398Share issue expense (325,573) - - (325,573)Share plan shares 592,052 (475,052) - 117,000Recognition of share-based payments - 40,254 - 40,254 Balance at 30 June 2014 16,211,680 204,342 (11,870,210) 4,545,812 1 July 2014

16,211,680 204,342 (11,870,210) 4,545,812

Total comprehensive income (loss) for the year - 87,509 (4,353,904) (4,266,395) Shares issued 1,144,947 - - 1,144,947Share issue expense (107,815) - - (107,815)Transfer to issued share capital 45,000 (45,000) - -Recognition of share-based payments 11,000 25,851 - 36,851 Balance at 30 June 2015 17,304,812 272,702 (16,224,114) 1,353,400

The accompanying notes form part of this financial statement.

For

per

sona

l use

onl

y

STATEMENT OF CASH FLOWS FOR THE YEAR ENDED 30 JUNE 2015

27

Consolidated

Note 2015

$

2014 $

Cash flows from operating activities Payments to suppliers and employees (742,214) (1,787,420)Exploration overheads (403,401) (630,641)Proceeds from farm in option 626,246 -Interest received 11,307 43,496GST received 17,385 116,618Interest paid - (164)Net cash (used in) operating activities 6 (490,677) (2,258,111) Cash flows from investing activities Purchase of plant and equipment (560) (127,072)Proceeds from sale of plant and equipment 1,068 -Proceeds from sale of prospects 196,253 -Exploration & evaluation expenditure (1,269,161) (1,448,713)Net cash (used in) investing activities (1,072,400) (1,575,785) Cash flows from financing activities Proceeds from issue of shares 1,144,947 4,405,191Payment of capital raising costs (107,816) (325,573)Net cash provided by financing activities 1,037,131 4,079,618 Net increase/(decrease) in cash held (525,946) 245,722 Cash at beginning of the financial year 694,497 456,885

Effect of exchange fluctuations on cash held (9,105) (8,110)

Cash at end of the financial year 6 159,446 694,497

The accompanying notes form part of this financial statement.

For

per

sona

l use

onl

y

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2015

28

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (a) Basis of Preparation The financial report is a general purpose financial report, which has been prepared in accordance with the requirements of the Corporations Act 2001, Accounting Standards and Interpretations and complies with other requirements of the law.

The accounting policies detailed below have been consistently applied to all of the years presented unless otherwise stated. The financial statements are for the consolidated entity of Chrysalis Resources Limited and its subsidiaries.

The financial report has also been prepared on a historical cost basis. Cost is based on the fair values of the consideration given in exchange for assets.

The financial report is presented in Australian dollars. The Company is a listed company incorporated in Australia and operating in Australia and the Republic of Zambia. The Group’s principal activities are the exploration for mineral resources. The Company is a for profit entity.

Where appropriate prior year disclosures have been reclassified for consistency with current year classifications. The re-classification has not impacted the net profit / (loss) for the prior year. (b) Adoption of new and revised standards Standards and Interpretations applicable to 30 June 2015 In the year ended 30 June 2015, the Directors have reviewed all the new and revised standards and interpretations issued by the AASB that are relevant to the Group’s operations and effective for the current annual reporting period.

As a result of this review, the directors have determined that there is no material impact of the new and revised Standards and Interpretations on the Company and, therefore, no material change is necessary to Group accounting policies.

Standards and Interpretations in issue not yet adopted The Directors have also reviewed all new Standards and Interpretations that have been issued but are not yet effective for the year ended 30 June 2015. As a result of this review the directors have determined that there is no material impact, of the new and revised Standards and Interpretations on the Group and, therefore, no change is necessary to Group accounting policies. (c) Statement of Compliance The financial report was authorised for issue on 14 September 2015.

The financial report complies with Australian Accounting Standards, which include Australian equivalents to International Financial Reporting Standards (“AIFRS”). Compliance with AIFRS ensures that the financial information, comprising the financial statements and notes thereto, comply with International Financial Reporting Standards (IFRS). (d) Basis of consolidation The consolidated financial statements incorporate the assets and liabilities of all subsidiaries of Chrysalis Resources Limited (“Company”) as at 30 June 2015 and the results of all subsidiaries for the year then ended. Chrysalis Resources Limited and its subsidiaries are referred to in this financial report as the Group or consolidated entity.

The financial statements of the subsidiaries are prepared for the same reporting period as the parent entity, using consistent accounting policies.

In preparing the consolidated financial statements, all intercompany balances and transactions, income and expenses and profit and losses resulting from intra-group transactions have been eliminated in full.

Subsidiaries are fully consolidated from the date on which control is transferred to the Group and cease to be consolidated from the date on which control is transferred out of the Group. Control exists where the Company has the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities. The existence and effect of potential voting rights that are currently exercisable or convertible are considered when assessing when the Group controls another entity.

For

per

sona

l use

onl

y

NOTES TO THE FINANCIAL STATEMENTS (continued) FOR THE YEAR ENDED 30 JUNE 2015

29

Unrealised gains or transactions between the Group and its associates are eliminated to the extent of the Group’s interests in the associates. Unrealised losses are also eliminated unless the transaction provides evidence of an impairment of the asset transferred.

Non-controlling interests represent the portion of profit or loss and net assets in subsidiaries not held by the Group and are presented separately in the Statement of Profit or Loss and Other Comprehensive Income and within equity in the Consolidated Statement of Financial Position. Losses are attributed to the non-controlling interests even if that results in a deficit balance.

The Group treats transactions with non-controlling interests that do not result in a loss of control as transactions with equity owners of the Group. A change in ownership interest results in an adjustment between the carrying amounts of the controlling and non-controlling interests to reflect their relative interests in the subsidiary. Any difference between the amount of the adjustment to the non-controlling interests and any consideration paid or received is recognised within equity attributable to owners of Chrysalis Resources Limited.

When the Group ceases to have control, joint control or significant influence, any retained interest in the entity is remeasured to its fair value with the change in carrying amount recognised in profit or loss. The fair value is the initial carrying amount for the purposes of subsequently accounting for the retained interest as an associated, joint controlled entity or financial asset. In addition, any amounts previously recognised in other comprehensive income in respect of that entity are accounted for as if the Group had directly disposed of the related assets or liabilities. This may mean that amounts previously recognised in other comprehensive income are reclassified to profit or loss. (e) Critical accounting judgements and key sources of estimation uncertainty The application of accounting policies requires the use of judgements, estimates and assumptions about carrying values of assets and liabilities that are not readily apparent from other sources. The estimates and associated assumptions are based on historical experience and other factors that are considered to be relevant. Actual results may differ from these estimates.

The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions are recognised in the period in which the estimate is revised if it affects only that period or in the period of the revision and future periods if the revision affects both current and future periods.

Share-based payment transactions: The Group measures the cost of equity-settled transactions with employees and consultants by reference to the fair value of the equity instruments at the date at which they are granted. The fair value of options and share plan shares with limited recourse loans where applicable is determined by using a Black and Scholes model, using the assumptions detailed in Note 13.

Exploration and evaluation costs carried forward The Group assesses impairment at each reporting date by evaluating conditions specific to the Group that may lead to impairment of assets. Where an impairment trigger exists, the recoverable amount of the asset is determined. Value-in-use calculations performed in assessing recoverable amounts incorporate a number of key estimates. The ultimate recoupment of value is dependent on the successful development and commercial exploitation or sale of the respective areas.

The recoverability of the carrying amount of exploration and evaluation costs carried forward has been reviewed by the directors and an impairment expense of $3,938,589 has been recognised in the Statement of Profit or Loss and Other Comprehensive Income in relation to the Zambian projects, Shikila, Kabwima North, Bulala Hills and Mwongo. Please refer to Note 8 for more details. (f) Foreign currency translation Both the functional and presentation currency of the Company and its Australian controlled entity is Australian dollars (A$). Each entity in the Group determines its own functional currency and items included in the financial statements of each entity are measured using that functional currency.

The functional currency of the foreign operations is Zambian Kwacha (KWA).

Transactions in foreign currencies are initially recorded in the functional currency by applying the exchange rates ruling at the date of the transaction. Monetary assets and liabilities denominated in foreign currencies are retranslated at the rate of exchange ruling at the balance date.

All exchange differences in the consolidated financial report are taken to profit or loss with the exception of differences on foreign currency borrowings that provide a hedge against a net investment in a foreign entity.

For

per

sona

l use

onl

y

NOTES TO THE FINANCIAL STATEMENTS (continued) FOR THE YEAR ENDED 30 JUNE 2015

30

These are taken directly to equity until the disposal of the net investment, at which time they are recognised in profit or loss.

Tax charges and credits attributable to exchange differences on those borrowings are also recognised in equity.