acma presentation final

TRANSCRIPT

6-10 June 2011; USA

Auto Component Industry in India: Growing Capabilities & Strengths

Presentation by:Srivats Ram

President, ACMA

Automotive Component Manufacturers Association of India

Objective of the ACMA CEOs’ Delegation

• Strengthen the linkages and enhance relationship with OEMs in the US

• To understand long term plans of OEMs – Global and specific to India

• To understand the sourcing strategies of the OEMs

• Get insights into technology developments crucial to the auto sector

• Present the strengths and capabilities of Indian suppliers and share the perspective of the Indian auto component industry

• Explore opportunities for Indian suppliers to address the requirements of the US OEMs for their domestic and global markets

Automotive Component Manufacturers Association of India

• India: A Vibrant Economy

• Automotive Industry in India

• Auto Component Industry in India

• India – USA Auto Component trade

• Capabilities & Challenges of Component Suppliers

• The Way Forward

• About ACMA

Agenda

Automotive Component Manufacturers Association of India

India: A Vibrant Economy

Automotive Component Manufacturers Association of India

• Largest Democracy in the world – 1.18 billion people

• 4th largest GDP (PPP) and 11th largest GDP (Nominal)

• 2nd fastest growing economy (Estimate 2011-12 – 9%); India’s average growth rate 7.3% over past 10 years and expected to outpace China in next 10 years

• 3rd largest investor base in the World

• Robust Legal and Banking Infrastructure

• Demographics of Youth – 50% under 25 years & 65% under 35 years

• Rural to Urban Migration - 140 million by 2020; 700 million by 2050

• 2nd largest pool of certified professionals and highest number of qualified engineers in the world

India: A Vibrant Economy

Automotive Component Manufacturers Association of India

Automotive Industry in India

Automotive Component Manufacturers Association of India

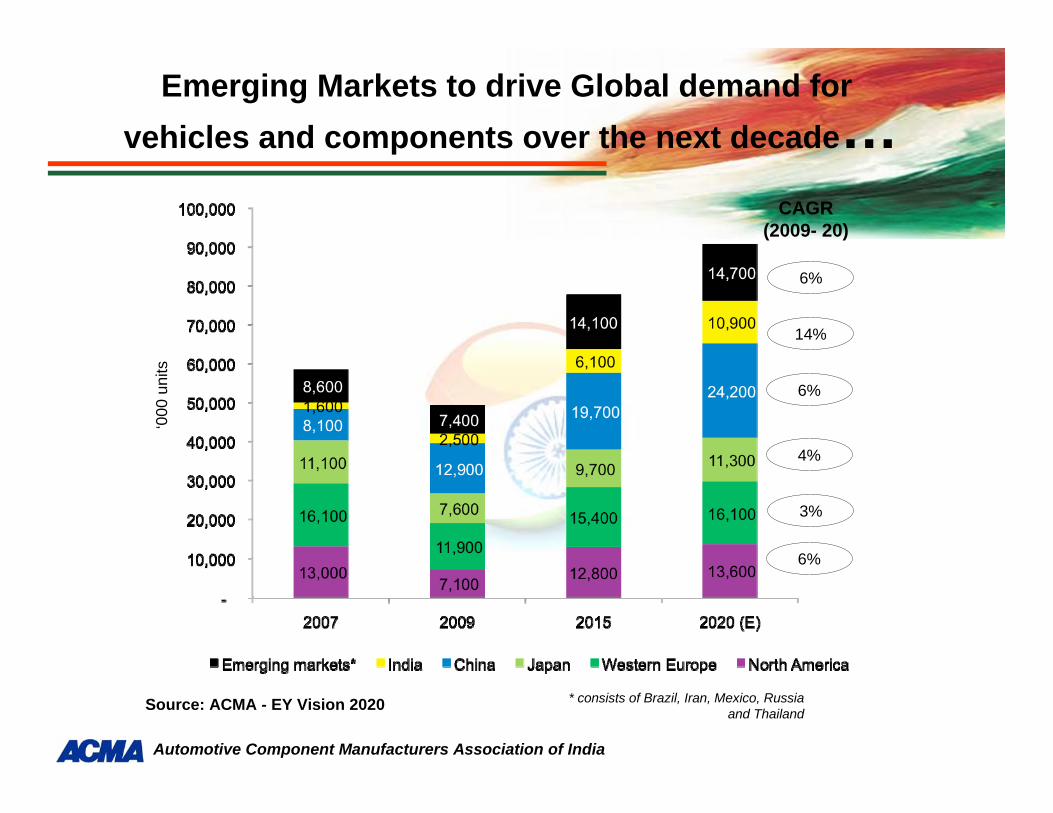

‘000

uni

ts

* consists of Brazil, Iran, Mexico, Russia and Thailand

CAGR (2009- 20)

6%

6%

4%

3%

6%

14%

Emerging Markets to drive Global demand forvehicles and components over the next decade…

Source: ACMA - EY Vision 2020

Automotive Component Manufacturers Association of India

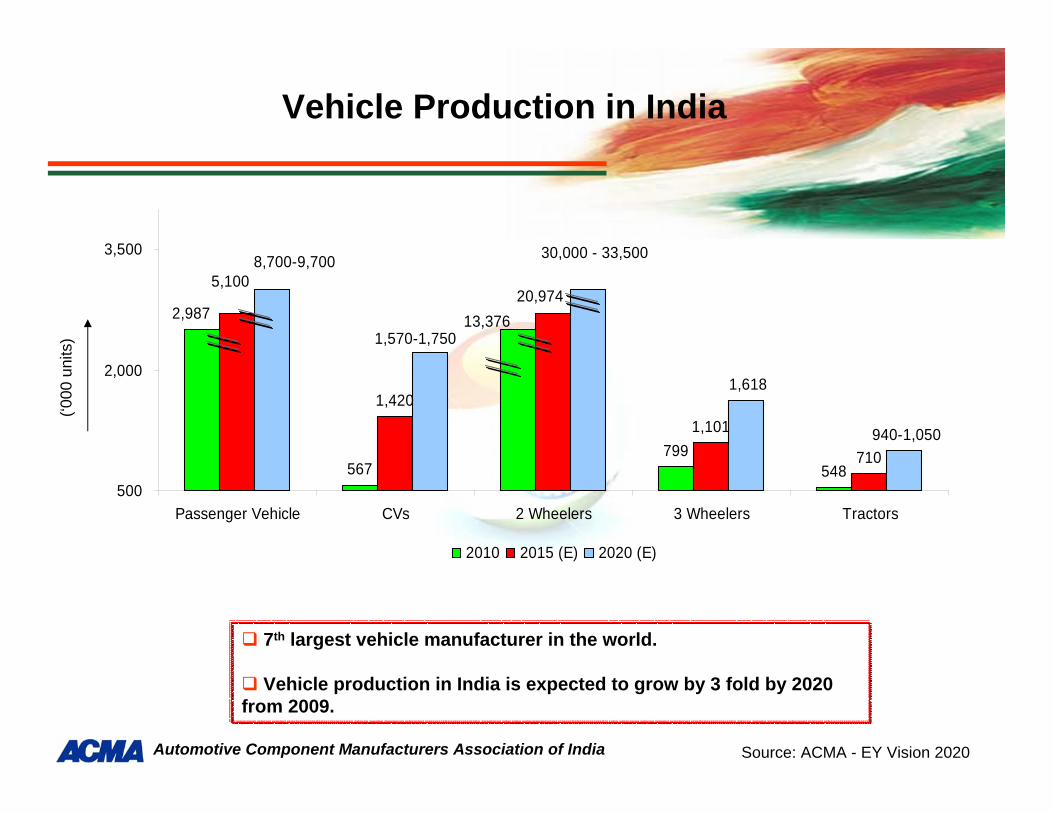

Vehicle Production in India

7th largest vehicle manufacturer in the world.

Vehicle production in India is expected to grow by 3 fold by 2020 from 2009.

Source: ACMA - EY Vision 2020

567799

548

1,4201,101

710

2,987 13,376

5,100 20,974

8,700-9,700

1,570-1,750

30,000 - 33,500

1,618

940-1,050

500

2,000

3,500

Passenger Vehicle CVs 2 Wheelers 3 Wheelers Tractors

2010 2015 (E) 2020 (E)

(‘000

uni

ts)

Automotive Component Manufacturers Association of India 9

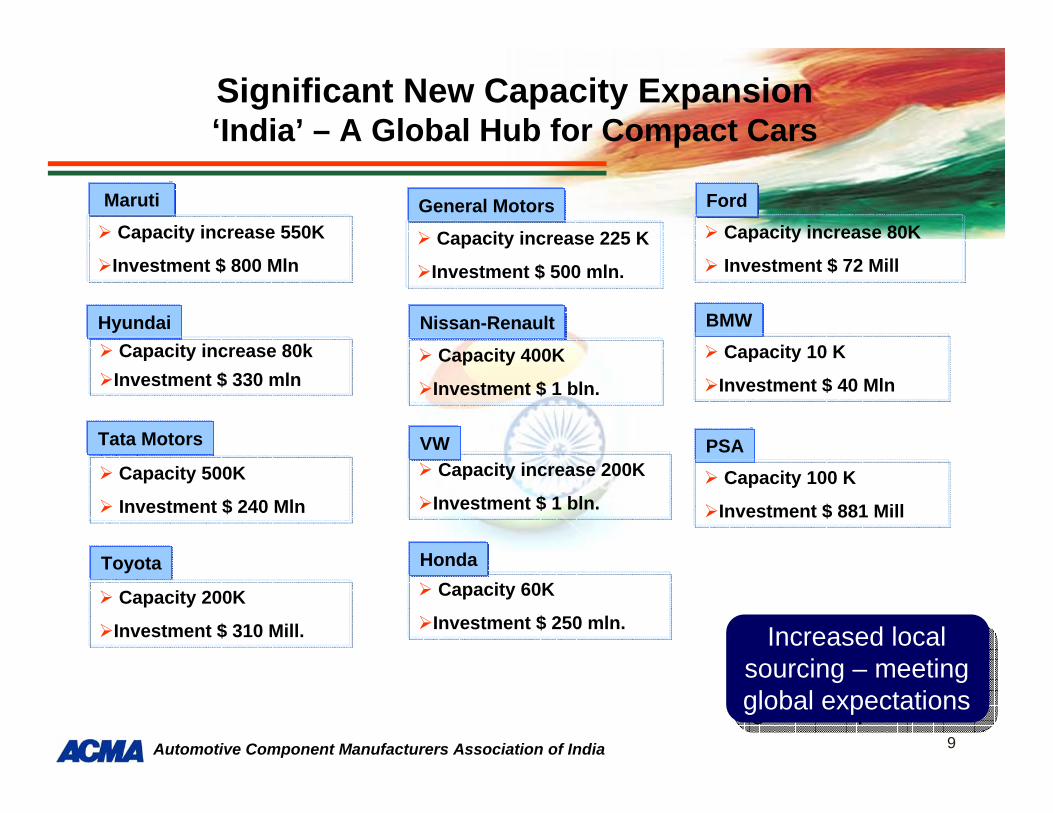

Significant New Capacity Expansion‘India’ – A Global Hub for Compact Cars

Increased local sourcing – meeting global expectations

Increased local sourcing – meeting global expectations

MarutiCapacity increase 550K

Investment $ 800 Mln

HyundaiCapacity increase 80k

Investment $ 330 mln

Tata Motors

Capacity 500K

Investment $ 240 Mln

Toyota

Capacity 200K

Investment $ 310 Mill.

FordCapacity increase 80K

Investment $ 72 Mill

General Motors

Capacity increase 225 K

Investment $ 500 mln.

Nissan-RenaultCapacity 400K

Investment $ 1 bln.

Capacity 60K

Investment $ 250 mln.

BMWCapacity 10 K

Investment $ 40 Mln

PSACapacity 100 K

Investment $ 881 Mill

Capacity increase 200K

Investment $ 1 bln.

VW

Honda

Automotive Component Manufacturers Association of India

Auto Component Industry in India

Automotive Component Manufacturers Association of India

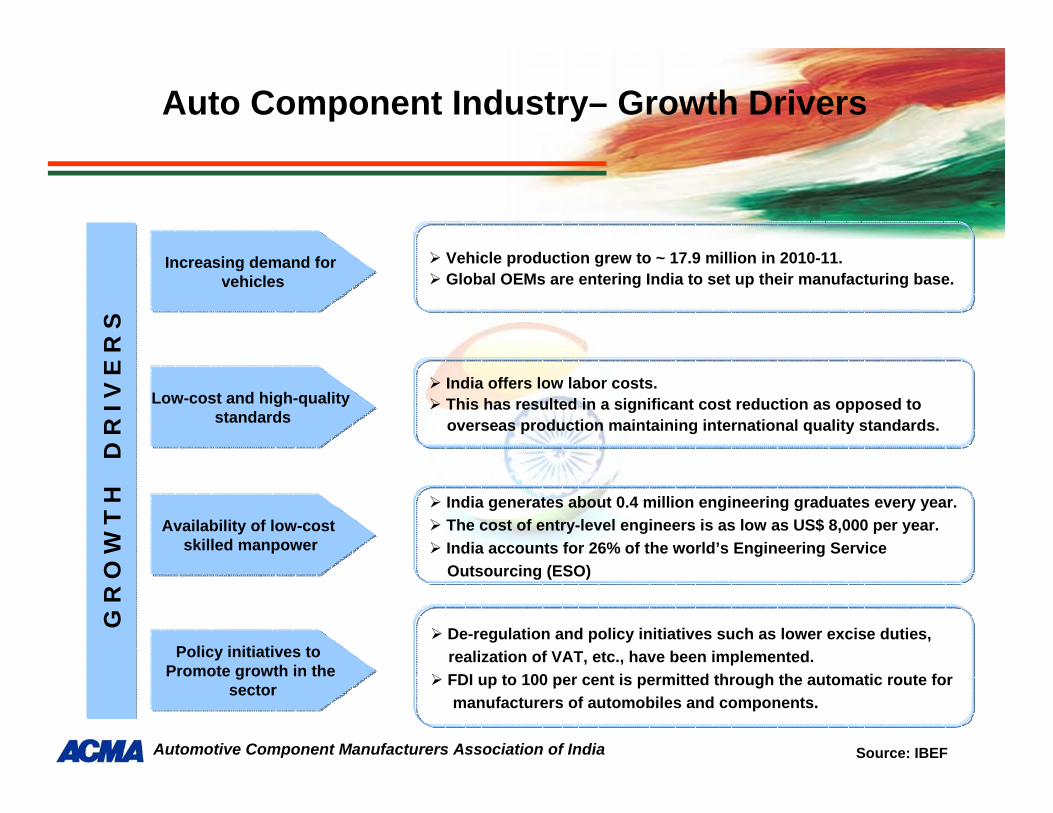

Auto Component Industry– Growth DriversG

R O

W T

H

D R

I V

E R

S

Availability of low-cost skilled manpower

Increasing demand forvehicles

Low-cost and high-qualitystandards

Policy initiatives to Promote growth in the

sector

India generates about 0.4 million engineering graduates every year.The cost of entry-level engineers is as low as US$ 8,000 per year.India accounts for 26% of the world’s Engineering ServiceOutsourcing (ESO)

Vehicle production grew to ~ 17.9 million in 2010-11.Global OEMs are entering India to set up their manufacturing base.

India offers low labor costs.This has resulted in a significant cost reduction as opposed tooverseas production maintaining international quality standards.

De-regulation and policy initiatives such as lower excise duties, realization of VAT, etc., have been implemented.FDI up to 100 per cent is permitted through the automatic route for manufacturers of automobiles and components.

Source: IBEF

Automotive Component Manufacturers Association of India

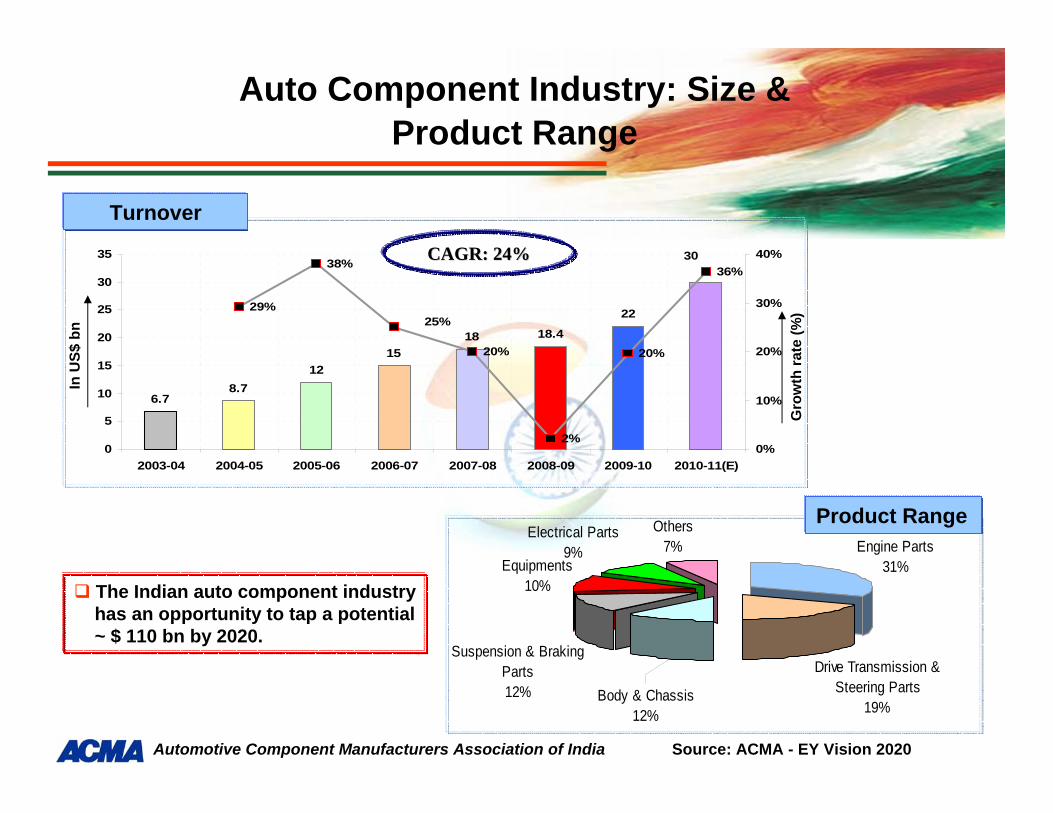

Auto Component Industry: Size & Product Range

Turnover

Product Range

In U

S$ b

n

Source: ACMA - EY Vision 2020

The Indian auto component industryhas an opportunity to tap a potential~ $ 110 bn by 2020.

Engine Parts31%

Drive Transmission & Steering Parts

19%

Equipments10%

Electrical Parts9%

Others7%

Suspension & Braking Parts12% Body & Chassis

12%

CAGR: 24%CAGR: 24%

Gro

wth

rate

(%)

6.78.7

1215

18 18.4

22

30

29%

38%

20%

2%

20%

36%

25%

0

5

10

15

20

25

30

35

2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11(E)0%

10%

20%

30%

40%

Automotive Component Manufacturers Association of India

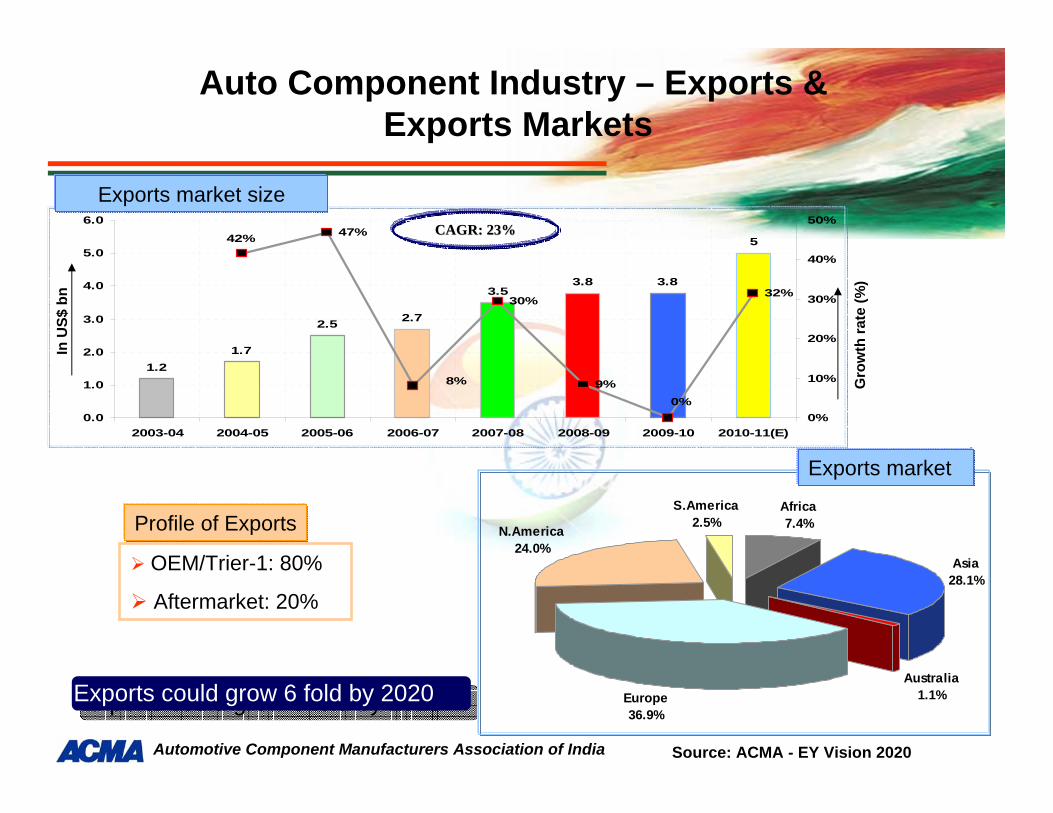

Auto Component Industry – Exports & Exports Markets

Exports market size

OEM/Trier-1: 80%

Aftermarket: 20%

Profile of ExportsAfrica7.4%

Asia28.1%

Australia1.1%Europe

36.9%

N.America24.0%

S.America2.5%

In U

S$ b

n

Source: ACMA - EY Vision 2020

Exports could grow 6 fold by 2020Exports could grow 6 fold by 2020

CAGR: 23%CAGR: 23%

1.21.7

2.5 2.7

3.53.8 3.8

547%

30%

9%

32%

0%

42%

8%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11(E)0%

10%

20%

30%

40%

50%

Gro

wth

rate

(%)

Exports market

Automotive Component Manufacturers Association of India

Increased Component Outsourcing from India(More than 30 IPOs have offices in India)

Indian Components already Driving on your Roads…Indian Components already Driving on your RoadsIndian Components already Driving on your Roads……

Automotive Component Manufacturers Association of India

Auto Component – Imports & Sources ofImports

Imports Sources

Asia54.34%

Australia0.22%

Europe36.03%

N.America8.28%

Africa0.20%

S.America0.92%

Imports market size

Gro

wth

Rat

e (%

)

1.41.9

2.5

3.6

5.2

6.8

8.2

10.045%

23%20%

33%

45%

30%31%

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11(E)0%

10%

20%

30%

40%

50%

CAGR: 32%CAGR: 32%

In U

S $

bn

Automotive Component Manufacturers Association of India

Auto Component Industry Investments

CAGR: 18%

In U

S$ b

n

Source: ACMA - EY Vision 2020

Investments

~$ 2.5 bn Investment is expected annually~$ 2.5 bn Investment is expected annually

Gro

wth

Rat

e (%

)

2.7 3.13.8

5.4

7.2 7.3

9.0

10.3

4.423%

33%

23%

14%

1%

17%17%

21%

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11*0%

10%

20%

30%

40%

* H1 FY 2010-11

Automotive Component Manufacturers Association of India

Vision 2020: The future

Source: ACMA - EY Vision 2020

$ 3.8 bn

$ 9.4 bn

$ 26 - 29 bn

US$

bn

Industry size is expected to grow four-fold by 2020 from 2009

22

50

82

4

9

28

0

20

40

60

80

100

120

2009 2015 (E) 2020 (E)Domestic potential Export potential

$ 26 bn

$ 59 bn

$ 110 bn

US$

bn

CAGR 14%

India’s Potential-Domestic & Exports

India’s Potential-Exports

CAGR 20%

Automotive Component Manufacturers Association of India

India – USA Auto Component Trade

Automotive Component Manufacturers Association of India

India – USA Auto Component trade

Source: GTA

* Estimated

2004 2005 2006 2`007 2008 2009 2010(Jan-Oct) *

India's Exports to USA 410 607 778 809 940 650 975

India's Imports from USA 210 284 346 458 507 437 500

Key Imports from USA

• Spark-Ignition • Gasket• Washers & Other Seals • Gears, Gear Boxes Ball or Roller Screws• Fuel, Lub /Cooling Med Pumps • Tapered Roll Bearing • Air/Gas Pumps, Compressors • Transmission Shafts

Key Exports to USA

• Bumpers and Parts • Drive Axles With Differential • Transmission Shafts • Pipes (riveted) • Parts Of Bearings • Elect Igntn /Start Equip; Generators • Parts Of Bearings • Road Wheels & pts & accessories

USD Million

Automotive Component Manufacturers Association of India

Some major customer in USA

OEMS

Tier 1s

Automotive Component Manufacturers Association of India

Capabilities & Challenges of Component Suppliers

Automotive Component Manufacturers Association of India

Indian Auto Component Industry Focus: Global Best Practices

Largest Deming Prize Award winning companies outside JapanLargest Deming Prize Award winning companies outside Japan

JIPM - 3 Japan Quality Medal - 1Shingo Silver Medallion - 1

Modern shop-floor practices• 5-S; 7-W• Kaizen• TQM• TPM• 6 Sigma• Lean Manufacturing

562 445

208

99

32

0

20

40

60

80

100

120

140

160

ISO 9000 TS 16949 ISO 14001 OHSAS 18001 QS 9000

Deming Award - 12

TPM Award - 15

Automotive Component Manufacturers Association of India

Some Design & Research Centers in India

Automotive Component Manufacturers Association of India

The industry facing challenges typical of a high growth developing country..

1. Raising Capital to meet the growth trajectory

2. Scaling Capacities ahead of the demand

3. Infrastructure Deficit & Cost – Energy & Logistics

4. Maintain productivity gains ahead of inflation

5. Availability of Skilled Manpower

6. Build R&D Competence

7. Develop Managerial Depth across Tiers of the Industry

Automotive Component Manufacturers Association of India

..Despite these challenges India competes strongly with most other cost-effective manufacturing locations

India is less competitiveIndia is more competitive India is comparable

Note: Numbers inside each cell indicate country ranking

Automotive Component Manufacturers Association of India

The Way Forward

Automotive Component Manufacturers Association of India

Areas of Cooperation

1. USA SMEs can invest in green-field manufacturing in India to meet growing domestic demand for auto-components.

2. Opportunities for Partnerships with Indian SMEs at Tier 2/3 level -Product and “Process Technology”.

3. Opportunity for Supply Base discovery.

4. Joint R&D with Indian companies for new product development and designing

Automotive Component Manufacturers Association of India

Conclusion

• Vibrant Indian Economy

• Automotive Industry showing double digit growth in all segments

• India fast becoming Global and Regional hub for vehicle programmes

• Vision 2020: A USD 110 Billion Auto Component Industry

• Growing engineering and IT capability for designing & manufacturing

• Auto Component Industry :Culturally compatible Values

• Opportunity to partner in product & process innovation

India : A Gateway to GrowthIndia : A Gateway to Growth

Automotive Component Manufacturers Association of India

About ACMA

Automotive Component Manufacturers Association of India

Introduction

Automotive Component Manufacturers Association of India

Role

Members

Quality System

Re-Christened

Inception

An apex agency of the Indian Automotive Industry

600+ companies forming majority of the auto component output in the organized sector

ACMA operates on Quality System basedon ISO 9001:2008

In the year 1959 as The All India Automobile & Ancillary IndustriesAssociation (AIA & AIA)

As Automotive Component Manufacturers Association of India in the year 1982

Automotive Component Manufacturers Association of India

Collection &Dissemination of

Information

QualityEnhancement

TechnologyUp-gradation

Promotes IndianAutomotive Component Industry

Trade Promotion

ACMA and Its Services

Vital Catalyst for Industrial Development

Automotive Component Manufacturers Association of India

ACMAThe Capital Court, 6th Floor, Olof Palme Marg, Munirka, New Delhi – 110 067

Tel: 011-26160315, Fax: 011-26160317E-mail: [email protected], Website: www.acmainfo.com

Thank Youfor any assistance contact

7th to 11th January 2012Pragati Maidan, New Delhi

Become a part of it …