acknowledgements - aidc studies/automotiveexportmanual2014 (2).pdf · acknowledgements the...

TRANSCRIPT

1

ACKNOWLEDGEMENTS

The information and analysis in this report were produced and compiled by Dr Norman Lamprecht on behalf of the Automotive Industry Export Council. The contributions and assistance by NAAMSA, NAACAM and the Department of Trade and Industry are hereby gratefully acknowledged. The data processing and editing by Dr Alet Tolmay, design and outlay of the publication by Dr Selma Schiller and photography by Mr Paul Parsons are also acknowledged with appreciation.

AIECP O Box 40611

Arcadia0007

Tel: +27 12 807 0086Fax: +27 12 807 0054

Website: www.aiec.co.za

2

CONTENTS

Foreword ............................................................................................................................... 4

The Automotive Industry Export Council (AIEC) ........................................................................ 5

The South African automotive industry operating environment ................................................ 7

South Africa and its automotive clusters .................................................................................. 9

South Africa’s automotive policy regime ................................................................................ 13

South African new vehicle market features ............................................................................ 17

Automotive exports and imports – methodology .................................................................... 23

Exports to regions ................................................................................................................. 24

Exports to countries .............................................................................................................. 42

Exports of vehicles ................................................................................................................ 46

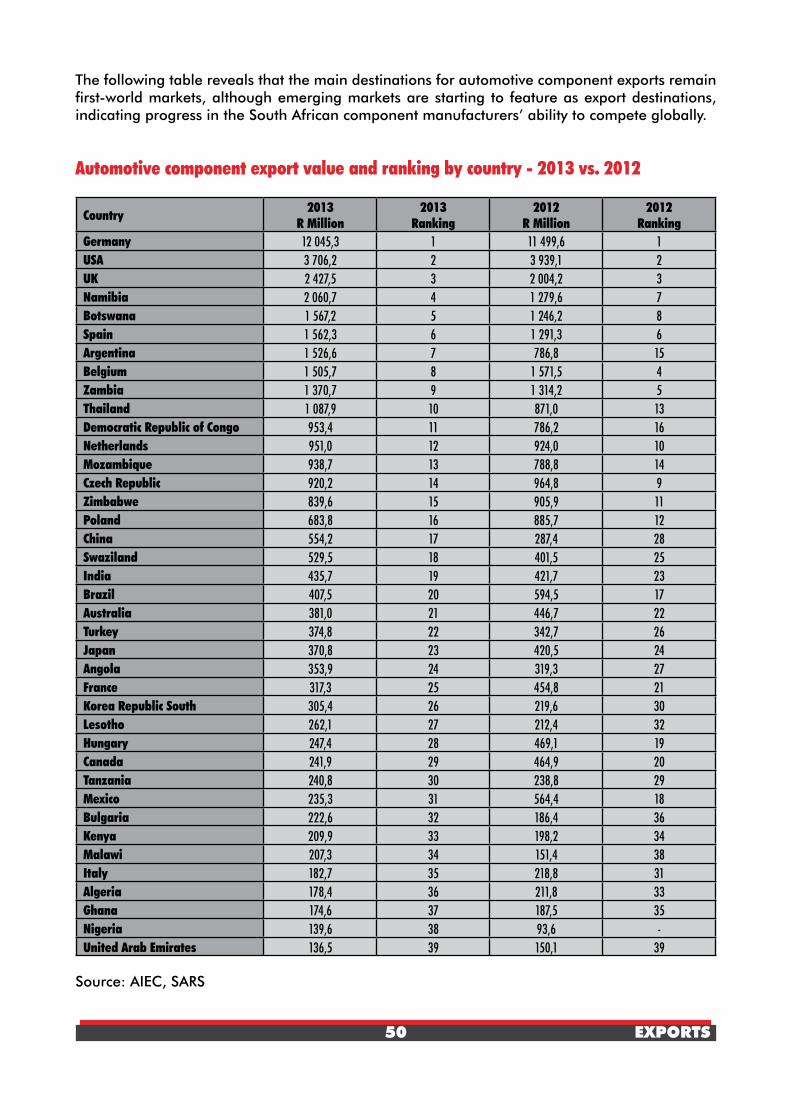

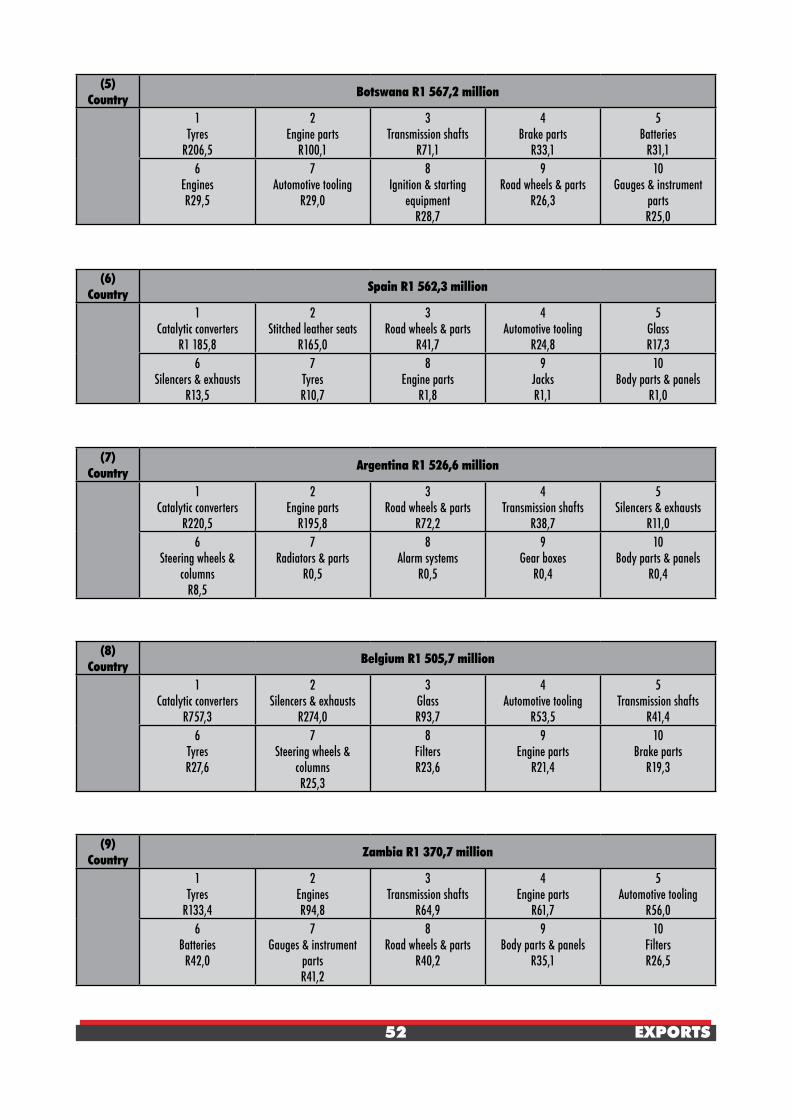

Automotive components – exports by country ........................................................................ 48

Automotive components – exports by product ....................................................................... 59

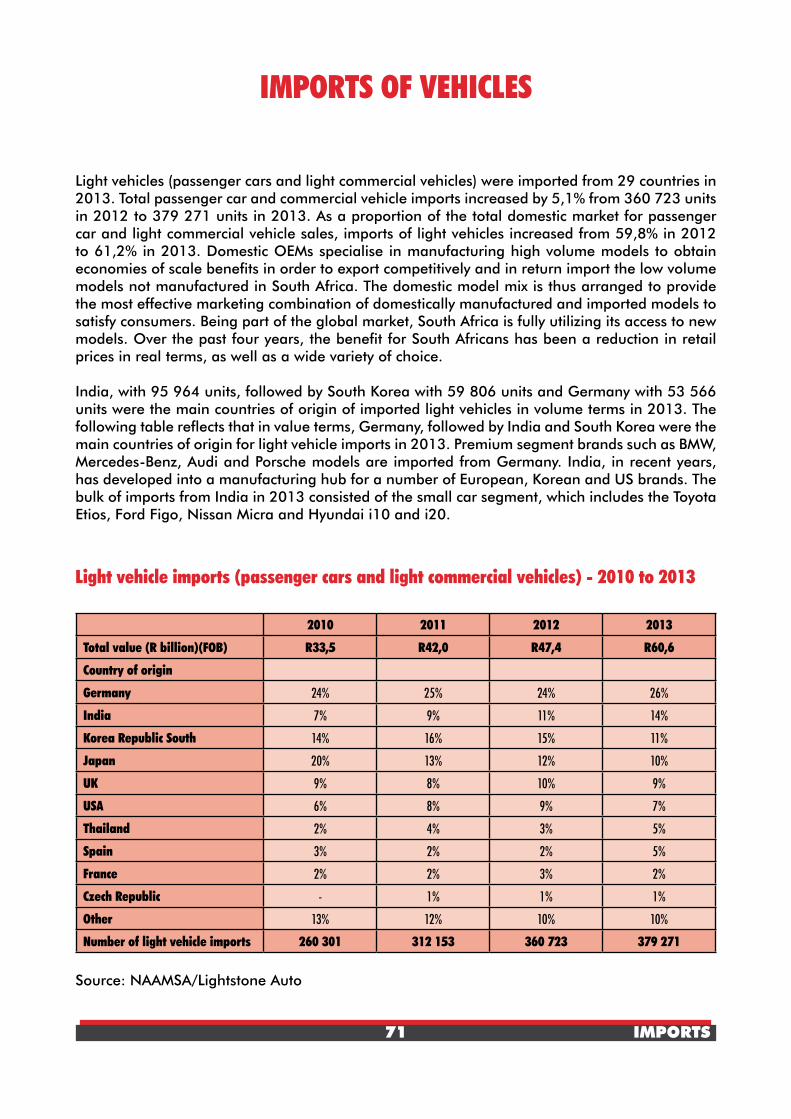

Imports by country of origin .................................................................................................. 68

Imports of vehicles ............................................................................................................... 71

Automotive parts and components – imports ......................................................................... 73

Main automotive trading partners ......................................................................................... 75

Automotive industry trade balance ........................................................................................ 79

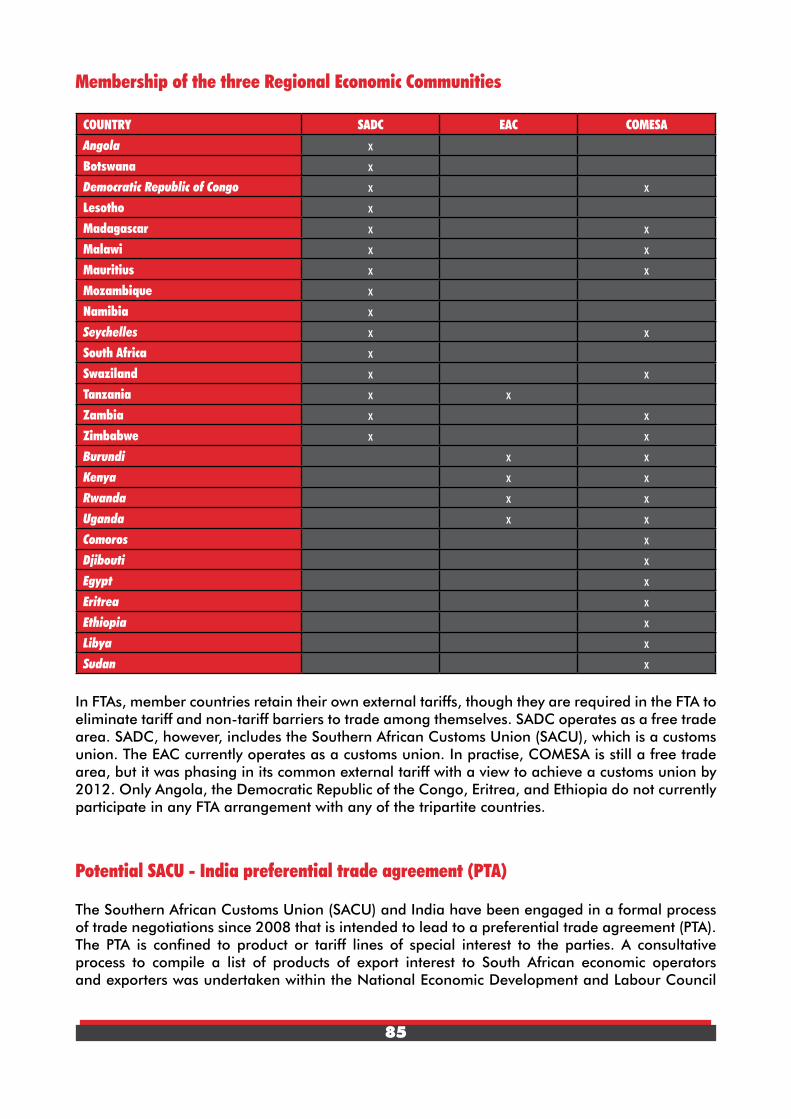

Potential opportunities via trade and co-operation arrangements .......................................... 82

General information ............................................................................................................. 87

South African automotive industry – prospects and imperatives to grow ................................. 88

Key motor industry addresses ............................................................................................... 91

3

ABBREVIATIONS

AGOA African Growth and Opportunity Act

AIEC Automotive Industry Export Council

AIS Automotive Investment Scheme

APDP Automotive Production Development Programme

BLNS Botswana, Lesotho, Namibia and Swaziland

BRICS Brazil, Russia, India, China and South Africa

CBU Completely Built Up

CKD Completely Knocked Down

COMESA Common Market for Southern and Eastern Africa

CPI Consumer Price Index

DTI The Department of Trade and Industry

EAC East African Community

EU European Union

FDI Foreign Direct Investment

FTA Free Trade Agreement

GDP Gross Domestic Product

IDZ Industrial Development Zone

MERCOSUR Mercado Común del Sur – Common Market of South America

MIDP Motor Industry Development Programme

NAACAM National Association of Automotive Component and Allied Manufacturers

NAAMSA National Association of Automobile Manufacturers of South Africa

NAFTA North American Free Trade Area

OEM Original Equipment Manufacturer (Vehicle Manufacturer)

SADC Southern African Development Community

SARS South African Revenue Service

WTO World Trade Organisation

4

FOREWORD

The Automotive Export Manual – 2014 – South Africa publication is an annual publication produced and compiled by the Automotive Industry Export Council (AIEC) – the key source of South African automotive trade data. The 2014 publication, as well as the previous publications since 2006, represent a comprehensive guide on the export and import performance of the South African automotive industry under the previous Motor Industry Development Programme (MIDP) and current Automotive Production Development Programme (APDP). The aim of the manual is to identify and prioritise the major automotive export destinations, the major countries of origin, the main automotive export trade blocs, the most important automotive products exported and imported, the top growth markets and products as well as the impact of the trade arrangements enjoyed by South Africa.

Over the past two decades the South African automotive industry has been transformed into an internationally more competitive, globally integrated industry supplying high quality automotive products to the domestic and global markets. The South African vehicle manufacturing and associated industries have grown to become the major contributors to manufacturing output in South Africa and currently accounts for about one third of all manufacturing activity in the country. The APDP, which commenced 1st January 2013, is designed to take the industry to the next level by doubling vehicle production in the country to 1,2 million units per annum by 2020.

The value and insight which data has to offer and the role that data plays is absolutely key and integral in formulating policy and defining business strategies. Market intelligence provides companies with a competitive edge. Accurate and timeous data gives insight into current trading conditions, acts as an indicator as to where the market is headed and assists companies to develop better and appropriate strategies. A recent development relating to South African trade statistics is that the Minister of Finance, during 2013, approved that South Africa’s trade statistics should include data in respect of Botswana, Lesotho, Namibia and Swaziland (BLNS) in order to provide a more accurate reflection of South Africa’s trade. BLNS country trade statistics have previously not been included in South Africa’s trade statistics because of the free flow of trade from a customs point of view within the Southern African Customs Union (SACU). The automotive industry’s trade performance has subsequently been revised with BLNS country data in the 2014 publication, and where applicable, with retrospective effect.

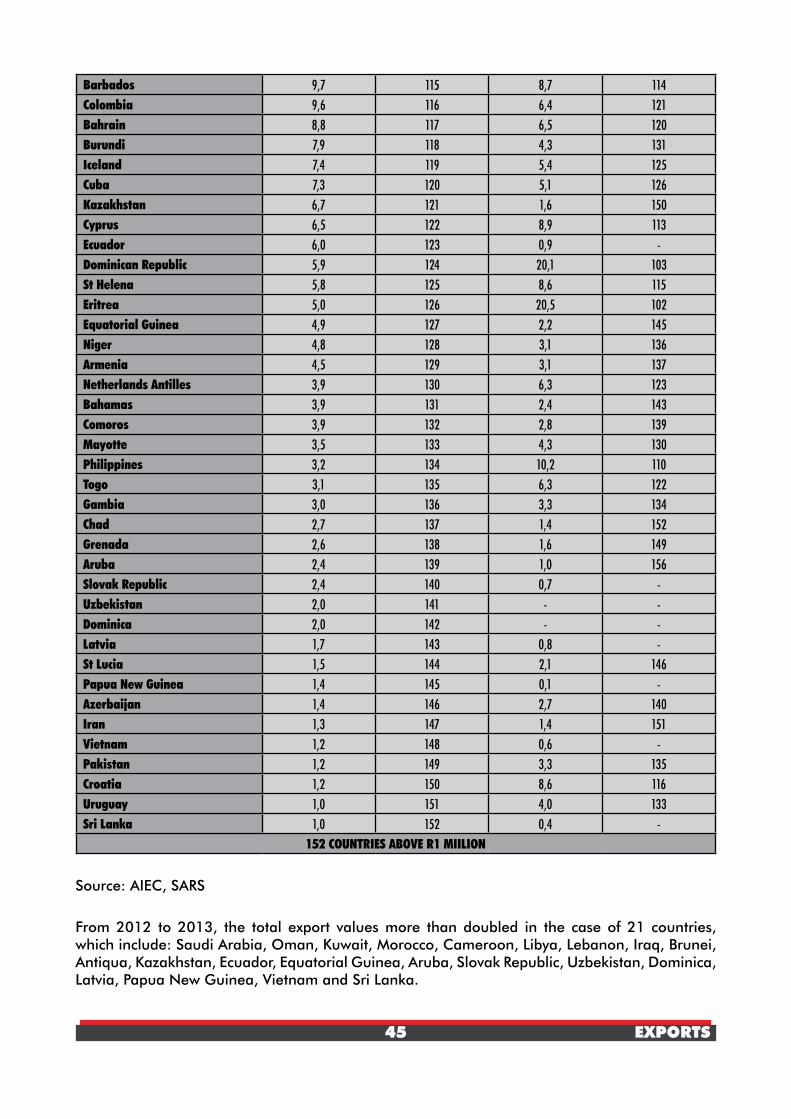

The South African automotive industry has enjoyed sustained growth in both domestic sales and exports since the downturn in 2009, despite the uncertain international climate. During 2013, total automotive industry exports increased by R7,8 billion or 8,2% to R102,7 billion from the revised R94,9 billion in 2012. The economic challenges in Europe and the US are forcing South African companies to look at alternative markets and partners to diversify risk and create new avenues for growth. Indicative of this trend, the export value to 21 of the 152 country export destinations more than doubled from 2012 to 2013.

The performance of exports remains a function of the performance and direction of global markets. There are, however, increasing positive signs that economic conditions are improving in important regions for the domestic automotive industry, including Europe and North America. The accelerating recovery in the world’s major developed economies, which, together with a weaker exchange rate, should enhance South Africa’s manufacturing and exports during 2014. The domestic automotive sector’s significance is premised on its contribution to export earnings, employment and GDP growth. In recognition of the importance of the automotive sector to the country’s economy, the South African government remains committed to fast track the growth and development of the domestic automotive industry which it regards as strategically significant.

5

THE AUTOMOTIVE INDUSTRY EXPORT COUNCIL (AIEC)

Export Councils are the prime delivery vehicles that stimulate export growth and deepen the export base. This format was initiated by Trade and Investment South Africa in a number of key sectors, and is also aimed at assisting Small Medium and Micro Enterprises (SMMEs) and Black Economic Empowerment (BEE) companies to enter the export market successfully.

The Automotive Industry Export Council (AIEC) was established at the end of 1999 and serves as the umbrella body for the South African automotive industry’s export promotion and development activities. The purpose was to provide a cost effective administered central body to assist companies in the automotive sector that are currently exporting, may be interested in exporting in the future, or may become capable of exporting in the future. The AIEC represents the interests of seven motor vehicle manufacturers/exporters namely BMW, Ford, General Motors, Mercedes-Benz, Nissan, Toyota and Volkswagen as well as manufacturers/exporters of trucks and buses, and over 500 component suppliers in South Africa.

The AIEC is operated from the NAAMSA offices in Pretoria and the activities and administration are coordinated by the AIEC Board. The AIEC Board of Directors consists of Mr Robert Houdet (Executive Director – NAACAM – Chairperson), Mr Nico Vermeulen (Director – NAAMSA), Dr Norman Lamprecht (Executive Manager – NAAMSA) as well as two ex-officio members from the Department of Trade and Industry, Mr Mzwakhe Mbatha and Mr Jacob Moatshe.

Mr Robert HoudetExecutive Director

NAACAM

Dr Norman LamprechtExecutive Manager

NAAMSA

Mr Nico VermeulenDirectorNAAMSA

6

The domestic automotive industry is a vital contributing element to the success of the national economy and the sustainable growth of the country at large. Manufacturing output accounts for 15% of the country’s GDP and the automotive industry accounts for about 30% of manufacturing output. Continuous efforts to grow the South African automotive industry’s export business are imperative, especially in view of the vision of doubling vehicle production in the country to 1,2 million units per annum by 2020. The focus of the South African automotive industry is to build on existing exports and to explore and exploit new opportunities. The domestic market is generally not large enough to generate sufficient economies of scale for world-class competitiveness/production; consequently exporting needs to be viewed as a necessary step towards international competitiveness. Failure to rise to the challenge by finding new markets and products could result in stagnation of exports. The current global economic environment is dominated by intense competition for export markets, investment and technology. This makes it important to gain and maintain access to these markets.

The Dti plays an important role in the promotion of economic development and meaningful participation in the global economic and trade environment. The Export Promotion Directorate of the Dti is responsible for developing and promoting South African goods and services, including specific technical interventions in the form of Export Marketing and Investment Assistance (EMIA) financial support, matchmaking, market intelligence, trade lead facilitation and in-market support. For the automotive industry, a flagship tool and successful platform to showcase and promote the South African automotive industry’s world-class capabilities is participation by means of National Pavilions at major world events.

During 2013, financial assistance under the EMIA scheme was provided to automotive manufacturing company exhibitors to participate in the Automechanika Middle East, United Arab Emirates (UAE) National Pavilion from 11 to 13 June 2013, the Johannesburg International Motor Show National Pavilion from 16 to 27 October 2013 as well as the South African National Pavilion at Midest, France from 19 to 23 November 2013.

The two automotive National Pavilions approved for 2014 include the Automechanika Middle East, UAE National Pavilion from 3 to 5 June 2014 (www.automechanikadubai.com) and the Automechanika Frankfurt, Germany National Pavilion from 16 to 20 September 2014 (www.automechanika.messefrankfurt.com). Automotive manufacturing companies will also be invited to participate in the Midest, France South African National Pavilion from 4 to 7 November 2014 (www.midest.com). The 2014 national automotive event is the South African Automotive Week (SAAW) scheduled to take place from 13 to 17 October 2014 in Midrand, Johannesburg (www.saaw.co.za).

The customers and stakeholders of the AIEC are all the domestic automotive industry stakeholders as well as the Dti Head Office, Dti foreign economic representatives, and global players abroad. The needs of members are primarily twofold, namely: (i) research and information, and (ii) practical assistance with exhibitions and missions. These needs form the basis for the assistance provided.

More information on the Automotive Industry Export Council can be accessed at www.aiec.co.za.

7

THE SOUTH AFRICAN AUTOMOTIVE INDUSTRY OPERATING ENVIRONMENT

Globally, major automotive manufacturing regions include the North American Free Trade Area (NAFTA), Western Europe, Japan, Asia-Pacific, Eastern Europe, South America and South Africa. 2009 was a pivotal year for the global motor industry. It marked the parting of ways between mature and emerging countries. The latter continued to grow while the global financial crisis hit Europe and the US particularly hard. The next two years saw an improvement in production and sales, especially in Asia, where China became the sector’s driver. The situation again changed in 2012 when the EU car market once more went into crisis, while the US market experienced a rebirth.

In 2013, the automotive industry reached its fourth production record since 2009, with 87,3 million vehicles produced. The year-on-year vehicle production growth of 3,7% was supported for the most part by strong growth in developing countries and the continued recovery of the North American market. The gloomy climate in Western Europe continued with year-on-year vehicle production remaining stagnant. The Triad economies of North America, Europe and Japan, although declining, still comprised 42,3 million or 48,5% of global vehicle production in 2013. Developing countries and regions, providing lower cost manufacturing and huge growth potential for both the global automotive supply and demand sides, are increasingly becoming important focus areas. A case in point is the BRICS coalition which increased its global market share from 35,2% in 2012 to 37,2% in 2013. The year-on-year increases could mainly be attributed to production gains of 14,8% in the case of China and 9,9% in the case of Brazil. China accounted for 25,3% of global vehicle production in 2013 and since 2012 has become the global number 1, both in terms of sales and vehicles produced.

Developing countries have to cope and incorporate not only the direct impact of the major global trends on their automotive operations, but also have to compete with each other for sourcing and outsourcing opportunities. It is within this fast changing environment that many developing countries, such as South Africa, are seeking to create for themselves a role as producer of vehicles and automotive components. When the domestic market is not large enough to absorb the production, the focus is on exports. The South Africa automotive industry possesses unique qualities and a natural ability to add value to global strategies of parent companies and multinationals. The industry has capitalised on the wealth of experience brought about by the presence of all the major European, American, Japanese and other Asian motor vehicle manufacturers in the country. South Africa’s attractiveness as an investment destination of choice and production base for products to be exported to global markets is increasing.

The South African automotive industry, as in many other countries in the world, is strongly influenced by the OEMs. The industry’s structure and evolutionary path are therefore closely aligned with OEMs’ strategies in both domestic and global markets. Key decisions about South Africa’s automotive business are made in Europe, the USA and Japan. South Africa’s participation in the World Trade Organisation (WTO), its competitive advantages and its special relationships with the EU and other trading regions have facilitated the industry’s integration into the global sourcing strategies of the multinational automotive corporations.

On a global stage, an automotive industry must be able to handle industry-wide factors such as social contributions, taxes, currency volatility, market competition, and difficulties in passing raw

8

material costs increases to the end consumer, amongst others. As in the other leading automotive manufacturing countries, public authorities are important partners in South Africa. At a national level, the National Association of Automobile Manufacturers of South Africa (NAAMSA) and the National Association of Automotive Component and Allied Manufacturers (NAACAM) are regularly involved in discussions with government on issues affecting the automotive industry. In this regard, a recent development is the introduction of the Automotive Supply Chain Competitiveness Initiative (ASCCI), a joint initiative between the major national stakeholders, namely NAAMSA, NAACAM, the National Union of Metalworkers of South Africa (NUMSA) and the Department of Trade and Industry (Dti). One main objective is to implement the national strategic imperative of sustained and progressive competitiveness improvement. Other key focus areas of the initiative include: improving component supplier operational capabilities, increasing levels of localisation, achieving increased manufacturing value addition in South Africa as well as other strategic issues affecting local supply chain competitiveness in support of the vision to manufacture 1,2 million vehicles per annum by 2020. The initiative should have a positive impact on employment creation, enabling domestic supplier capabilities and an increase in value addition, thus ensuring the long term sustainability of the South African automotive industry.

9

SOUTH AFRICA AND ITS AUTOMOTIVE CLUSTERS

South Africa is an open and globally integrated market-oriented economy with a Gross Domestic Product (GDP) of R3 385 billion, at current prices, in 2013. As the continent’s most sophisticated economy, South Africa is regarded as one of the most diversified exporting countries in the world and its increasing trade liberalisation is contributing significantly to the country’s growth and future prosperity. South Africa has a substantial mineral resource base to support an economy that generates a third of sub-Saharan Africa GDP. The country has an abundance of natural resources, well developed financial, legal and transport sectors as well as modern infrastructure supporting the distribution of goods throughout the fast developing southern African region.

South Africa is one of the world’s richest countries in mineral reserves and production. With access to large aluminium and steel resources and the world’s largest deposits of platinum group metals (PGMs), the country’s vehicle and parts industry has plenty of growth potential. The Columbus stainless steel facility is the largest in the world as is the Alusaf aluminium-smelting facility at Richards Bay. New manganese smelters are scheduled to be built at Coega. South Africa currently supplies in the order of 10% of the global demand for catalytic converters. The country is also home to over 70% of the world’s chromium, which is an essential ingredient in the stainless steel used to house the catalyst and to produce modern auto exhausts.

The improving and modernisation of various border systems and processes to facilitate increased trade with South Africa and the sustained investments in refining its infrastructure will no doubt have a significant positive impact on the region’s trade as a whole. The country’s ports provide a natural stopover for shipping to and from Europe, the Americas, Asia, Australia and both coasts of Africa. South Africa is not only an attractive investment destination in its own right but also provides entry to investments in other African countries. The country is ideally positioned for easy access to the countries of the Southern African Development Community (SADC), a free trade area, which consists of 15 countries with a total population of about 280 million. The country’s inclusion in the BRICS economies substantiates its reputation as a globally competitive destination for foreign investment.

South Africa consists of nine provinces, namely Western Cape, Eastern Cape, Northern Cape, North West, Free State, KwaZulu-Natal, Gauteng, Mpumalanga and Limpopo, each with its own premier, executive council and legislature. Cape Town is the legislative capital and is where parliament sits. Pretoria is the executive capital where the government administration is housed while the Constitutional Court of South Africa is based in Bloemfontein, the judicial capital. The country has a population of 52,98 million people with 11 official languages. While most South Africans can communicate in more than one language, English is the most commonly spoken and is the official language in business and commerce. The country occupies the southernmost part of the African continent and shares boundaries with Namibia, Botswana, Zimbabwe, Mozambique, Swaziland and Lesotho.

South Africa’s vehicle manufacturing industry is concentrated in three of the country’s nine provinces, namely Gauteng, the Eastern Cape and KwaZulu-Natal, and in close proximity to its suppliers. However, increasingly, some automotive development is also taking place in the Western Cape and North West provinces. Provincial and local governments have trade, investment and tourism offices to promote economic activity in their regions, many of which have their own Industrial Development Zones (IDZs) and development programmes.

10

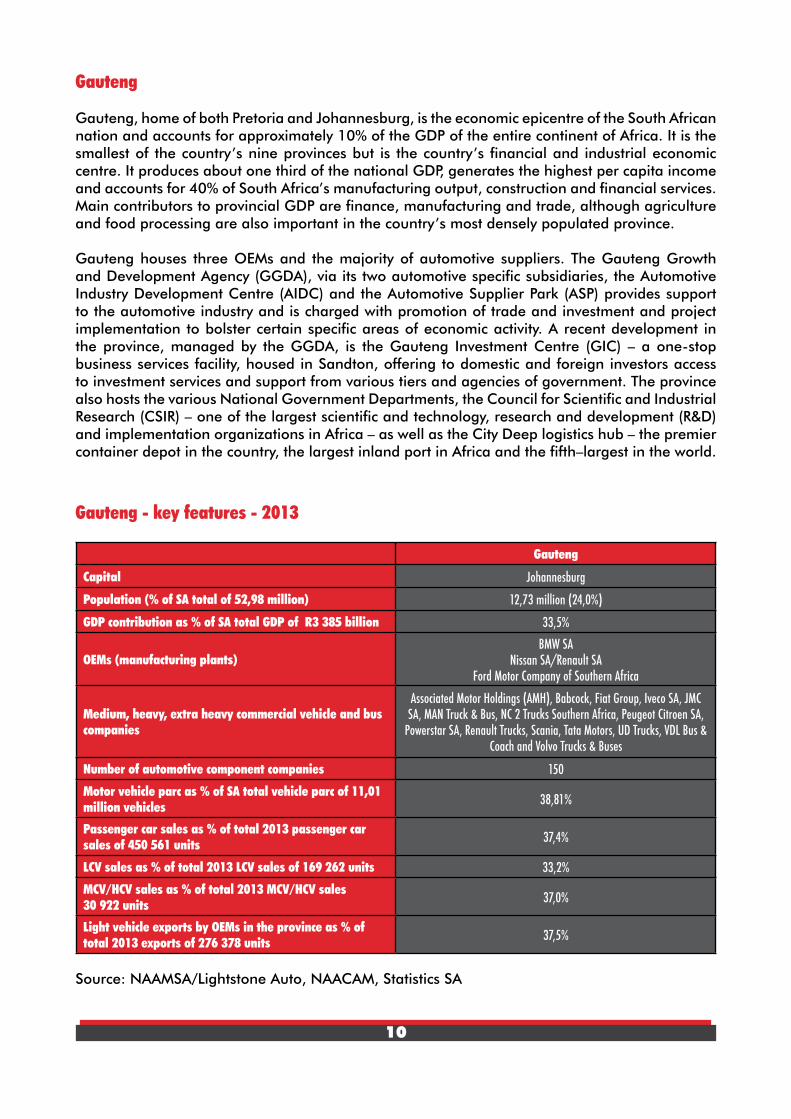

Gauteng

Gauteng, home of both Pretoria and Johannesburg, is the economic epicentre of the South African nation and accounts for approximately 10% of the GDP of the entire continent of Africa. It is the smallest of the country’s nine provinces but is the country’s financial and industrial economic centre. It produces about one third of the national GDP, generates the highest per capita income and accounts for 40% of South Africa’s manufacturing output, construction and financial services. Main contributors to provincial GDP are finance, manufacturing and trade, although agriculture and food processing are also important in the country’s most densely populated province.

Gauteng houses three OEMs and the majority of automotive suppliers. The Gauteng Growth and Development Agency (GGDA), via its two automotive specific subsidiaries, the Automotive Industry Development Centre (AIDC) and the Automotive Supplier Park (ASP) provides support to the automotive industry and is charged with promotion of trade and investment and project implementation to bolster certain specific areas of economic activity. A recent development in the province, managed by the GGDA, is the Gauteng Investment Centre (GIC) – a one-stop business services facility, housed in Sandton, offering to domestic and foreign investors access to investment services and support from various tiers and agencies of government. The province also hosts the various National Government Departments, the Council for Scientific and Industrial Research (CSIR) – one of the largest scientific and technology, research and development (R&D) and implementation organizations in Africa – as well as the City Deep logistics hub – the premier container depot in the country, the largest inland port in Africa and the fifth–largest in the world.

Gauteng - key features - 2013

Gauteng

Capital Johannesburg

Population (% of SA total of 52,98 million) 12,73 million (24,0%)

GDP contribution as % of SA total GDP of R3 385 billion 33,5%

OEMs (manufacturing plants)BMW SA

Nissan SA/Renault SAFord Motor Company of Southern Africa

Medium, heavy, extra heavy commercial vehicle and bus companies

Associated Motor Holdings (AMH), Babcock, Fiat Group, Iveco SA, JMC SA, MAN Truck & Bus, NC 2 Trucks Southern Africa, Peugeot Citroen SA,

Powerstar SA, Renault Trucks, Scania, Tata Motors, UD Trucks, VDL Bus & Coach and Volvo Trucks & Buses

Number of automotive component companies 150

Motor vehicle parc as % of SA total vehicle parc of 11,01 million vehicles 38,81%

Passenger car sales as % of total 2013 passenger car sales of 450 561 units 37,4%

LCV sales as % of total 2013 LCV sales of 169 262 units 33,2%

MCV/HCV sales as % of total 2013 MCV/HCV sales30 922 units 37,0%

Light vehicle exports by OEMs in the province as % of total 2013 exports of 276 378 units 37,5%

Source: NAAMSA/Lightstone Auto, NAACAM, Statistics SA

11

Eastern Cape

The Eastern Cape has a sound manufacturing base, primarily in the automotive sector. Finance, government services and manufacturing are the leading sectors in the Eastern Cape economy. The province is well served logistically, with airports situated in Port Elizabeth, East London, Mthatha and Bisho and with ports in Port Elizabeth, Coega and East London. The allocation of two of South Africa’s five industrial development zones (IDZs) to the province is confirmation of the potential generated by the shipping traffic that operates between Europe, Asia and the Far East. The Coega IDZ is the largest IDZ in the country and is the main catalyst for Eastern Cape socio-economic development and the gateway to global markets. The East London IDZ has also established an Automotive Supplier Park.

The Automotive Industry Development Centre, the Eastern Cape Development Corporation, the Nelson Mandela Bay Metropolitan Municipality and the Cacadu District Municipality are among the several organisations promoting the Eastern Cape as a preferred destination for trade and investment. Three Spatial Development Initiatives (SDIs) – Fish River, Wild Coast and East London/Coega – are also located in the Eastern Cape.

Eastern Cape - key features - 2013

Automotive clusters Eastern Cape

Capital Bisho

Population (% of SA total of 52,98 million) 6,62 million (12,5%)

GDP contribution as % of SA total GDP of R3 385 billion 7,6%

OEMs (manufacturing plants)

Volkswagen Group SAMercedes-Benz SA

General Motors Southern AfricaFord Motor Company of Southern Africa engine plant

Medium, heavy, extra heavy commercial vehicle and bus companies

FAW Trucks, General Motors/Isuzu, Mercedes-Benz SA and Volkswagen Group SA

Number of automotive component companies 100

Motor vehicle parc as % of SA total vehicle parc of 11,01 million vehicles 6,67%

Passenger car sales as % of total 2013 passenger car sales of 450 561 units 3,7%

LCV sales as % of total 2013 LCV sales of 169 262 units 5,1%

MCV/HCV sales as % of total 2013 MCV/HCV sales of 30 922 units 4,0%

Light vehicle exports by OEMs in the province as % of total 2013 exports of 276 378 units 32,7%

Source: NAAMSA/Lightstone Auto, NAACAM, Statistics SA

12

KwaZulu-Natal

KwaZulu-Natal represents the second largest economy in the country after Gauteng. With two of Africa’s busiest ports supported by world-class road and rail infrastructure, the province enjoys the strategic and competitive advantage of being a global gateway for trade into Africa and to the world. Durban is South Africa’s second largest city and busiest port. Richards Bay, originally developed as a coal exporting port, is now South Africa’s busiest bulk port and the centrepiece of the Richards Bay IDZ and Spatial Development Initiative (SDI). Richards Bay and Durban ports handle about 75% of the country’s tonnage. Manufacturing – dominated by pulp and paper, chemicals and food and beverages – is the largest sector in the province, followed by finance, trade, tourism and agriculture. The new King Shaka international airport at La Mercy provides easy access to Durban.

Trade and Investment KwaZulu-Natal, Tourism KwaZulu-Natal, the Durban Investment and Promotion Agency and the Durban Automotive Cluster promote the province’s trade and investment opportunities. These institutions have been supplemented by the new Durban KwaZulu-Natal Convention Bureau which has been established to promote the city and province as top conference destinations in Africa.

KwaZulu-Natal - key features - 2013

Automotive clusters KwaZulu-Natal

Capital Mzunduzi (Pietermaritzburg)

Population (% of SA total of 52,98 million) 10,46 million (19,7%)

GDP contribution as % of SA total GDP of R3 385 billion 16,1%

OEMs (manufacturing plants) Toyota SA Motors

Medium, heavy, extra heavy commercial vehicle and bus companies

Bell Equipment Co SA, Hino, MAN Truck & Bus (SA) and Toyota SA Motors

Number of automotive component companies 80

Motor vehicle parc as % of SA total vehicle parc of 11,01 million vehicles 13,53%

Passenger car sales as % of total 2013 passenger car sales of 450 561 units 12,8%

LCV sales as % of total 2013 LCV sales of 169 262 units 12,5%

MCV/HCV sales as % of total 2013 MCV/HCV sales of 30 922 units 17,0%

Light vehicle exports by OEMs in the province as % of total 2013 exports of 276 378 units 29,0%

Source: NAAMSA/Lightstone Auto, NAACAM, Statistics SA

13

SOUTH AFRICA’S AUTOMOTIVE POLICY REGIME

Most countries with vehicle markets similar to or larger than South Africa protect their automotive industries with significantly higher tariffs and governments provide substantial support to their industries, recognizing the benefits of the sector to a country’s economy. Each job in manufacturing normally supports a multiple of jobs elsewhere in the economy.

The automotive industry in South Africa is regarded as a strategic asset. The Motor Industry Development Programme (MIDP) was implemented with effect from 1 September, 1995 to reshape the future direction of the South African automotive and associated industries. The MIDP was established to entrench the outward orientation of the industry, thereby restructuring it to achieve global competitiveness, whilst at the same time maintaining its employment level and output contributions to the South African economy.

Since the introduction of the MIDP, significant structural changes have taken place in the South African automotive industry. The sector has grown in stature to become the leading manufacturing sector in the country’s economy. Other industries, due to their strong linkages with the automotive industry, have also benefited from the growth in the automotive sector. Input industries include aluminium, chemicals, electronics, leather and textiles, platinum group metals, plastics, rubber, steel, machinery and equipment, as well as service industries such as engineering, logistics, tooling and others such as financial, wholesale, retail and advertising.

The MIDP has to a large extent achieved its stated objectives and, in general, its contribution to the domestic automotive industry has been regarded as positive. Key achievements under the MIDP between 1995 and 2012 may be summarised as follows:

• Totalnominalexportvalueofvehiclesandautomotivecomponents–R772,2billion

• Totalnumberofvehiclesexported–2411376units

• TotalnominalcapitalexpenditurebytheOEMs–R48,6billion

• TotalnominalexpenditureontrainingbytheOEMs–R1,85billion

• Acompoundedannualgrowthrateof19,5%innominalRandvaluetermsforcompletely

built-up vehicles (CBUs) and automotive component exports has been achieved since 1995,

through to 2012

• Totalautomotiveindustryexports(CBUsandcomponents)inRandvaluetermsincreased

more than twenty fold from the R4,2 billion in 1995 to R86,9 billion (excluding BLNS

countries) in 2012.

The MIDP ended on 31 December 2012 and was succeeded by the Automotive Production Development Programme (APDP), with effect from 1st January, 2013.

The vision is to double vehicle production in South Africa by 2020 to 1,2 million vehicles per annum, pushing the country’s automotive industry up to an anticipated global market share of over 1%. The increase in market share will trigger additional interest and investment and generate additional export business. The APDP will seek to shift the emphasis away from an export focus to one that emphasises value addition and scale in the production of vehicles. In

14

addition, the programme is intended to be supportive of the further development of world-class automotive component manufacturing. The APDP will incentivise automotive-related production, investment and large-scale vehicle manufacturing, while the investment incentive will also be accessible to more companies than was the case under the MIDP. The programme should generate a quantum leap in terms of processes, technologies and the scale on which the domestic industry has operated. The APDP focus is to ensure the sector has a greater impact on the economy and on national employment levels by increasing local component manufacturing, and sourcing more semi-finished goods in the domestic market.

The APDP consists of four pillars that will drive the programme:

1. Import Duty

2. Vehicle Assembly Allowance (VAA) (rebate mechanism)

3. Production Incentive (PI) (rebate mechanism)

4. Automotive Investment Scheme (AIS) (cash grant)

The four key elements of the APDP may be described as follows:

Tariffs: Import duties on vehicles and automotive components will remain at 2012 levels (25% on light vehicles and 20% on original equipment components) through to 2020. A preferential agreement will result in imported vehicles from the EU paying only 18% duty. These tariffs are meant to provide just enough protection to justify continued local vehicle manufacturing.

Vehicle Assembly Allowance (VAA): This support will be in the form of duty-free import credits issued to vehicle manufacturers based on 20% of the ex-factory vehicle price in 2013, reducing to 19% in 2014 and in 2015 to 18% of the value of light motor vehicles produced domestically. The equivalent value of this to the OEMs will be the allowance multiplied by the duty rate; so this represents 4% of the ex-factory vehicle price in 2013 and will reduce to 3,6% in 2015. This support is effectively providing a lower duty rate for local vehicle manufacturers and should provide enough encouragement for high volume vehicle production in line with the target of doubling production.

Production Incentive (PI): From 2013 this support will start at 55% reducing progressively by 1% annually to 50% of value added, in the form of duty-free import credits. The equivalent value will be the incentive multiplied by the component duty rate; so this represents 11% of value added in 2013, and will reduce to 10% by 2018. There will be an additional amount for “vulnerable products” which will earn a PI of 80% in 2013 and 2014, reducing thereafter by 5% annually to 50% in 2020. Value added has been defined in simple terms as the manufacturer’s selling price less the value of non-qualifying material and components. The incentive will flow through the supply chain to the end producer, which will be the OEM or, in the case of component exports or replacement parts, the component manufacturer. The value-add support is planned to encourage increasing levels of local value addition along the automotive value chain with positive spin-offs for employment creation. A 25% Standard Value is regarded as local value added on the following qualifying raw materials originating in the Southern African Customs Union (SACU) which have been beneficiated to suit automotive specifications:

• Aluminium • Brass• Leather

• Platinum Group Metals (PGMs)

15

• Stainlesssteel

• Steel

With regard to vulnerable products, these high material content products will receive additional support to avoid a sudden and significant loss of export business. In this regard 40% of the standard materials listed above and applicable to the following list of products will be regarded as local value added:

• Alloywheels

• Aluminiumproducts (engineand transmission components,heat exchangersand tubes,

suspension components and heat shields)

• Alloywheels

• Castironcomponents(engine/axle/brake/transmissionandrelatedtypesofcomponents)

• Catalyticconverters

• Flexiblecouplings

• Leatherinteriors

• Machinedbrasscomponents

• Steeljacks

The 40% level will be reduced by 5 percentage points per annum from 1 January 2015 to reach 25% from 1 January 2017 onwards.

Automotive Investment Scheme (AIS): Effective from July 2009, this assistance replaces the Productive Asset Allowance (PAA) and provides for a taxable cash grant of 20% of the value of qualifying investment in productive assets by light motor vehicle manufactures and 25% of the value of qualifying investment in productive assets by component manufactures and tooling companies as approved by the Dti. In addition, by achieving certain performance objectives, companies will be able to earn an additional 5% or 10%. This support is available to encourage investments by OEMs and component manufacturers in a manner that supports productive capacity upgrading. A competitiveness improvement cost grant of 20% of qualifying costs will also be available for automotive component manufacturers. The objective of this benefit is to enhance the competitiveness of component manufacturers through the improvement of processes, products, quality standards and related skills development through the use of business development services. The grant is a function of expenditure incurred by component suppliers to improve competitiveness and must be linked to a new or replacement model of a light vehicle manufacturer.

A first review of the APDP has commenced in the first quarter of 2014 to consider the effectiveness of current support measures for the industry and identify shortcomings and recommend possible changes or enhancements to the programme. Recommendations in this regard are expected towards the end of 2014.

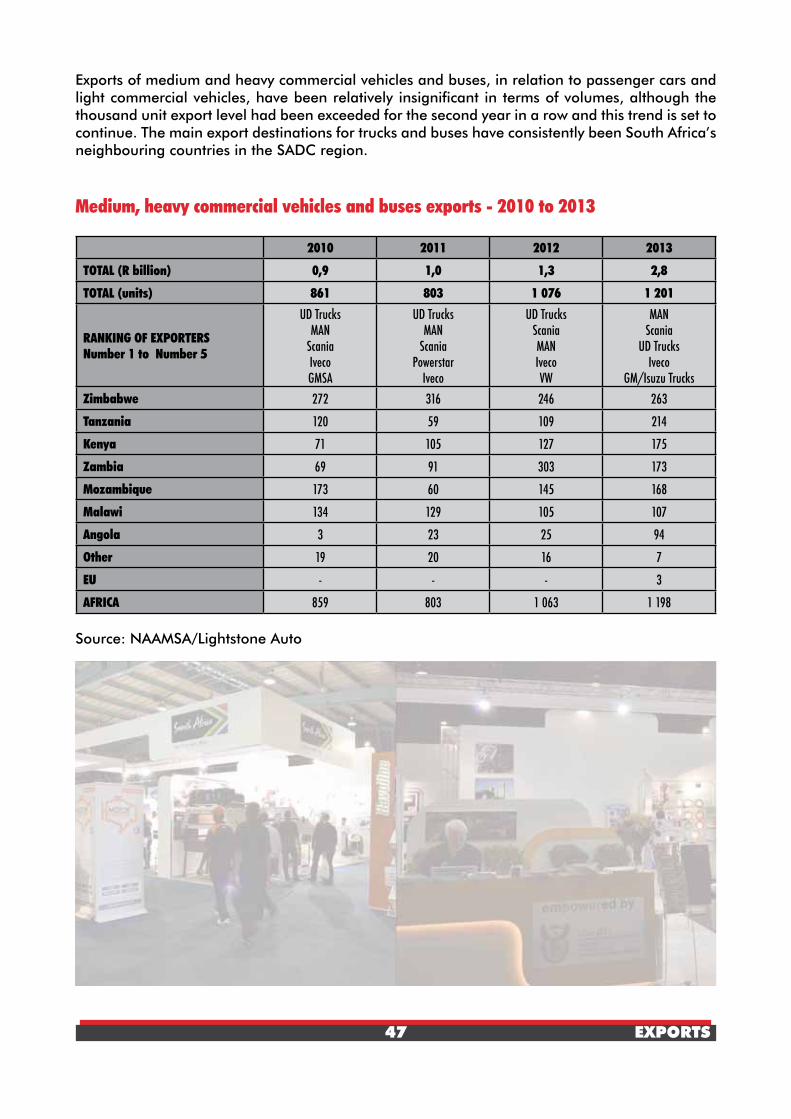

The APDP applies to light vehicles (passenger cars and light commercial vehicles) only. In terms of support to the medium and heavy commercial vehicle (MCV/HCV) sector, including the country’s truck, bus, capital equipment and agricultural vehicle manufacturing industries, government acknowledges that the sector has not received adequate policy attention. A review by the Department of Trade and Industry of developmental policy options for the South African

16

medium and heavy truck industry, bus manufacturing and associated sectors has been completed and recommendations in this regard are expected during 2014. There is the potential to enhance bus production in South Africa, as well as the production of other MHCVs, through leveraging opportunities, such as the roll-out of the bus rapid transit system and the growing demand for MHCVs in areas such as infrastructure, construction, mining and, possibly, agriculture. The rationale behind this review is the fact that the MHCV sector is labour intensive in terms of assembly, while a more active sector could also broaden South Africa’s component manufacturing industry. It is believed that this could be an opportunity for the component sector to grow its base and create additional jobs. Components produced for the heavy vehicle sector already receive the same benefits as light vehicle components under the APDP.

The way forward for the South African automotive industry has been indicated clearly under the APDP. There is certainty through to 2020, which will assist long-term strategic planning, while the programme requires each OEM manufacturing plant to produce at least 50 000 units per year, thus bringing reasonable economies of scale. As was the case under the MIDP, those companies able to comply with the new policy regime the quickest will be able to reap the most benefits.

17

SOUTH AFRICAN NEW VEHICLE MARKET FEATURES

For the fourth year in succession, new vehicle sales in South Africa recorded year-on-year gains. Aggregate sales grew by 3,2% in volume terms in 2013 following annual growth in total sales of 24,7% year-on-year in 2010, 16,1% in 2011 and 9,0% in 2012. Industry trading conditions remained intensely competitive in the new car and light commercial vehicle sectors. According to the Lightstone Auto/NAAMSA database, 51 brands and 2 295 passenger car model derivatives and 28 LCV brands and 510 model derivatives were available for consumers to choose from in 2013, the biggest ratio compared to its market size in the world.

Toyota SA Motors has maintained its overall market leadership position in South Africa for 34 consecutive years since 1980. In 2013, Toyota SA Motors had an overall market share of 19,5%, followed by Volkswagen Group of SA, Associated Motor Holdings, Ford Motor Company of Southern Africa and General Motors Southern Africa. The following graph reveals the overall market shares of the top 10 OEMs/Importers in the country in 2013.

Overall new vehicle market share – 2013Source: NAAMSA/Lightstone Auto

Domestic new vehicle sales growth is expected to remain modest at best during 2014. The key factors that contributed to an expansion in domestic sales over the years from 2010 through to 2013 have turned negative. Specifically, economic growth has slowed, with expected growth in real terms of about 2,3% in 2014, new vehicle price inflation has risen largely as a result of the Rand exchange rate depreciation and the interest rate cycle has turned upwards with a 0,5% increase in the repo rate early in 2014. As a result of the unfavourable current macro-environment, the general industry consensus is that the domestic market in 2014 is likely to remain stagnant.

18

19

Vehicle exports should benefit from improving global economic conditions and could well show substantial growth particularly in respect of vehicle exports to Asia, Africa and Europe. Factoring in the expected improvement in exports, total domestic production of motor vehicles in South Africa during 2014 is expected to rise from the 545 913 vehicles produced in 2013 to about 591 000 vehicles in 2014 – an improvement in vehicle production of about 8,3%.

Production of passenger car and light commercial vehicles - 2010 to 2013

PASSENGER CARS LIGHT COMMERCIAL VEHICLES

Market Exports as a % of total

Market Exports as a % of total Domestic Exports Total Domestic Export Total

2010 113 740 181 654 295 394 61,5 96 823 56 950 153 773 37,0

2011 124 736 187 529 312 265 60,1 108 704 84 125 192 829 43,6

2012 120 417 151 659 272 076 55,7 121 638 123 443 245 081 50,4

2013 113 364 151 893 265 257 57,3 127 188 121 345 248 533 48,8

2014* 110 000 160 000 270 000 59,3 127 000 160 000 287 000 55,7

* projected figuresSource: NAAMSA/Lightstone Auto

In 2013, new vehicle sales turnover has grown by about 11%, based on volume increases and a weighted average estimated increase of about 8% in new vehicle prices, to reach R205 billion for the year.

The OEMs in South Africa specialize in one or two high volume models, obtain economies of scale benefits via exports and in turn import those models not manufactured in the country to complement their domestic model mixes. This approach also assisted the component suppliers in obtaining higher volumes. The passenger car models manufactured by the OEMs during 2013 included the following:

Passenger cars (2013):

BMW 3-Series 4-door

General Motors Chevrolet Spark

Mercedes-Benz C-Class 4-door

Nissan Livina and Tiida

Renault Sandero

Toyota Corolla 4-door and Fortuner

Volkswagen Polo new and previous series

Colour is a customer’s most memorable sense, as the first point of interaction is shaped by the vehicle’s colour. According to the 2012 DuPont Automotive Colour Popularity Report, white/white pearl continued to dominate the global automotive colour popularity ranks. Overall, white/white pearl represented 23% of the global market and was in the leading position as the most popular car colour in North America, Japan, South Korea, Russia, South Africa and Mexico. Black/black effect led among vehicle colour popularity in China, but took second place in the global ranks

20

with 21% of the world’s share of automotive colour. Silver rounded off the top three global colour choices, topping the ranks in South America, Brazil and India with a global market share of 18%. South Africa has the world’s highest market share of white/white pearl of any region or country analysed, with those vehicles representing more than 38% of local market share. Silver followed and black/black effect and grey tied in third place.

Colour of passenger cars sold in South Africa – 2013Source: DuPont

The light commercial vehicle models manufactured by the OEMs in 2013 included the following:

Light commercial vehicles (2013):

Ford Ranger

Mazda BT-50

General Motors Chevrolet Utility and Isuzu KB

Nissan NP300 Hardbody, NP200

Toyota Hilux

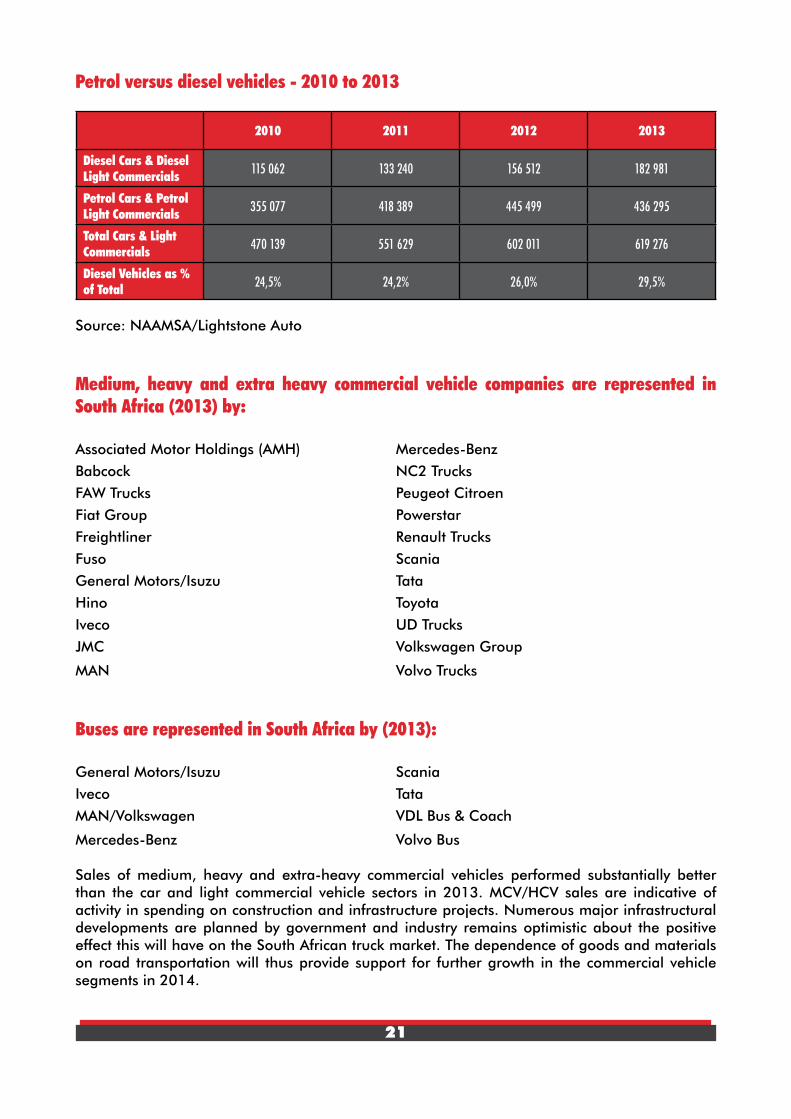

The popularity of diesel engine models has been increasing and in 2013 the market share for new diesel light vehicle (passenger car and light commercial vehicle) sales accounted for 29,5% of total light vehicle sales, up from the 26,0% level in 2012. The following table – showing the split between sales of new petrol and diesel vehicles in South Africa – for 2010 through to 2013 - will prove of interest.

0%

5%

10%

15%

20%

25%

30%

35%

40%

White Silver Black Grey Red Blue Other

38%

20%

13% 13%

5% 5% 6%

21

Petrol versus diesel vehicles - 2010 to 2013

2010 2011 2012 2013

Diesel Cars & Diesel Light Commercials 115 062 133 240 156 512 182 981

Petrol Cars & Petrol Light Commercials 355 077 418 389 445 499 436 295

Total Cars & Light Commercials 470 139 551 629 602 011 619 276

Diesel Vehicles as % of Total 24,5% 24,2% 26,0% 29,5%

Source: NAAMSA/Lightstone Auto

Medium, heavy and extra heavy commercial vehicle companies are represented in South Africa (2013) by:

Associated Motor Holdings (AMH) Mercedes-Benz

Babcock NC2 Trucks

FAW Trucks Peugeot Citroen

Fiat Group Powerstar

Freightliner Renault Trucks

Fuso Scania

General Motors/Isuzu Tata

Hino Toyota

Iveco UD Trucks

JMC Volkswagen Group

MAN Volvo Trucks

Buses are represented in South Africa by (2013):

General Motors/Isuzu Scania

Iveco Tata

MAN/Volkswagen VDL Bus & Coach

Mercedes-Benz Volvo Bus

Sales of medium, heavy and extra-heavy commercial vehicles performed substantially better than the car and light commercial vehicle sectors in 2013. MCV/HCV sales are indicative of activity in spending on construction and infrastructure projects. Numerous major infrastructural developments are planned by government and industry remains optimistic about the positive effect this will have on the South African truck market. The dependence of goods and materials on road transportation will thus provide support for further growth in the commercial vehicle segments in 2014.

22

Assembly of medium and heavy commercial vehicles and buses - 2010 to 2013

MEDIUM AND HEAVY COMMERCIALS

MarketExports as a % of total

Domestic Exports Total

2010 22 021 861 22 882 3,8

2011 26 656 803 27 459 2,9

2012 27 841 1 076 28 917 3,7

2013 30 922 1 201 32 123 3,7

2014* 33 000 1 400 34 400 4,1

* projected figuresSource: NAAMSA/Lightstone Auto

Medium and heavy commercial vehicles are regarded as productive assets and major cost drivers to the entire economy. Therefore the level of protection on these vehicles has been set at 20% ad valorem, which is lower than the level on light commercial vehicles and passenger cars. Assembly operations of these vehicles are characterized by the duty-free importation of all the drive line components, which include the engines, transmissions, drive-axles and gear boxes. Tyres, which are manufactured domestically, are excluded and attract a 15% import duty. The physical transfer of goods exported by a country is a reflection of economic competitiveness. The demand for freight transport is therefore closely linked to the economy of a country and its interactions with other countries.

Automotive parts and accessories

A diverse range of original equipment components, parts and accessories are manufactured in the country by about 500 automotive component suppliers, including 120 first tier suppliers. The profiles and contact details of the major automotive component suppliers in South Africa can be accessed in the NAACAM Directory at www.naacam.co.za.

23

AUTOMOTIVE EXPORTS AND IMPORTS -METHODOLOGY

The trade data in this publication is reflected for South Africa. A significant change in South Africa’s trade statistics, as approved by the Minister of Finance on 14 November 2013, is that South African trade with member countries of the Southern African Customs Union (SACU), namely Botswana, Lesotho, Namibia and Swaziland (BLNS), would now be included in South Africa’s trade data to provide a more accurate reflection of the country’s trade. BLNS country trade data has previously not been included in the country’s trade statistics because of the free interchange of goods between member countries from a customs point of view within SACU. The automotive industry’s trade performance has subsequently been revised with BLNS country data, with retrospective effect to 2010, where applicable.

The trade data in the Automotive Export Manual – 2014 – South Africa publication is based on the detailed Customs and Excise statistics for products eligible under the APDP, obtained from the South African Revenue Service (SARS). The Customs and Excise export values reflect free on board (FOB) values in nominal terms. The export values of the latest year (2013) are used to rank the countries in order of priority, from the most to the least important export country destination. The same principle is applied so as to prioritise the export data regarding regions, vehicles and component categories. Approximately 263 country export destinations are listed by SARS. For purposes of relevance, one million Rand (R1 million) is used in the Automotive Export Manual – 2014 – South Africa publication as a cut off level to determine the top 152 South African export country destinations. For ease of reference and for comparison purposes, the data with respect to the component categories and for countries, where applicable, is placed in alphabetical order. Percentages are rounded off.

The main purpose of this publication is to discern and highlight export and import trends, to prioritise export country destinations, to prioritise countries of origin, to identify opportunities via potential growth country and region destinations as well as to identify growth in products exported to specific country destinations. The publication also serves as a guide to track the export and import performance of the South African automotive industry under the new APDP. Due to certain limitations, Customs and Excise statistics cannot always distinguish between automotive components eligible in terms of the APDP and non-APDP components and certain categories may contain a small percentage of non-APDP components.

24 EXPORTS

EXPORTS TO REGIONS

Global economic growth is projected to strengthen from 3% in 2013 to 3,6% in 2014 and to 3,9% in 2015, with emerging markets and developing economies growth projected to pick up gradually from 4,7% in 2013 to about 5% in 2014 and 5,25% in 2015. The anticipated growth is shifting from traditional developed regions to the emerging markets of Asia, Africa and Latin America, where the growth rates over the past two decades have raised income and consumption to unprecedented levels.

Due to changes in the balance of power, it is becoming an imperative goal to diversify trade and investment towards these new emerging markets offering vast opportunities and rapid growth, while still actively maintaining and expanding relations with traditional trading partners. The demand side for vehicles, which is declining in the mature Triad markets, is problematic since supply is exceeding demand. The rush for cost savings by the OEMs is therefore a priority area to increase vehicle sales. The offensive strategies of a few dominant OEMs to win market share, in an intensely competitive global environment, also impact significantly on the developments of the automotive component suppliers on the supply side. Developing countries and regions, providing lower cost manufacturing and huge growth potential for both the global automotive supply and demand sides, are increasingly important focus areas.

South Africa forms an important part of international automotive supply chains and has escalated the importance of trading with new poles of economic growth over recent years. China, Thailand, India and South Korea recently count amongst South Africa’s main automotive trading partners. The EU, however, still remains the South African automotive industry’s largest trading bloc worldwide, absorbing 34,2% of the automotive industry’s exports in 2013.

25 EXPORTS

European Union

Europe remained the South African automotive industry’s most important trading partner, accounting for R35,1 billion or 34,2% of the country’s total automotive exports of R102,7 billion in 2013. Developments in the EU therefore have a direct and measurable impact on the local automotive industry’s overall performance.

South Africa’s trade relations with the EU are governed by the Trade, Development and Co-operation Agreement (TDCA). The main objective of the TDCA was to create a free-trade area between South Africa and the European Union (EU). The SA-EU Free Trade Agreement on trade, development and co-operation became effective on 1 January 2000. The agreement was based on preferential rates of import duties for certain products having been deemed to originate in the partner country. South Africa had granted duty-free status to 86% of its EU imports by 1 January 2012, while the EU had provided duty-free status to 95% of South Africa’s exports since 1 January 2010.

Initially the EU consisted of just six countries: Belgium, Germany, France, Italy, Luxembourg and the Netherlands. Denmark, Ireland and the United Kingdom joined in 1973, Greece in 1981, Spain and Portugal in 1986 and Austria, Finland and Sweden in 1995. In May 2004, the biggest ever enlargement took place with ten countries joining: Czech Republic, Cyprus, Estonia, Hungary, Latvia, Lithuania, Malta, Poland, Slovenia and Slovakia. On 1 January 2007, the EU welcomed its 26th and 27th members, Bulgaria and Romania. These new countries are also bound by the current free trade agreement. The eastern European countries which are significant in terms of vehicle production include the Czech Republic, Poland, Slovakia and Romania.

Passenger cars into the EU attract an import duty of 10% while original equipment components an import duty of 3% and aftermarket automotive parts an import duty of 4,5%. Effectively from 1 January 2000, when the SA-EU Free Trade agreement was signed, the applied tariffs for automotive components into the EU were reduced by 50% below normal EU duty rates. On 1 January 2002, the EU improved the preference extended to South Africa under its Generalised System of Preference (GSP) to 3,5%. This meant that South African passenger car exports into the EU only attracted an import duty of 6,5% while original equipment components as well as aftermarket automotive components could be exported duty-free. As from 15 December 2006, with the finalisation of the automotive part of the SA-EU Free Trade Agreement, the 10% import duty on passenger cars was reduced to 3,5% on 15 December 2006, to 1,5% on 1 January 2007 and fell away completely in January 2008. South African commercial vehicle exports to the EU were already duty-free and unaffected by the agreement. South Africa returned the compliment with a 7% preference to the EU on passenger cars and light commercial vehicles and an 8% preference on medium and heavy commercial vehicles and buses. Original equipment components will get no preference but a large number of aftermarket automotive parts will qualify for lower import duties. In order to qualify for zero tariff into the EU, South African vehicles and components must contain at least 60% local content. The definition of local content includes South African raw materials, labour, parts, transport, manufacturing costs and profit margins, as well as the value of components and subcomponents originally sourced from Europe.

For South Africa, the success of its relationship with the EU has shown the value of a pragmatic, interest-based foreign policy. Total automotive exports (vehicles and components) to the EU increased by R1,07 billion or 3,1% to R35,1 billion in 2013 from the R34,0 billion in 2012,

26 EXPORTS

with notable increases in exports to the UK, Germany, Belgium and Spain. Exports to the 12 new member countries forming part of the expanded EU amounted to R2,60 billion or 7,4% of the R35,1 billion export value in 2013, declining from the R3,41 billion export value in 2012. Total automotive exports in Rand value terms increased by 3,1% year-on-year, but in Euro terms declined by 15,1%, in line with the 21,5% depreciation of the Rand against the Euro during 2013.

Exports to the European Union (EU) - 2010 to 2013

Component 2010 2011 2012 2013TOTAL (R million) 33 116,4 38 577,4 34 030,7 35 096,2TOTAL (average Euro million) 3 410,5 3 827,1 3 225,7 2 737,6Air conditioners 4,4 17,7 22,1 22,1Alarm systems 41,0 35,0 29,6 39,0Automotive tooling 56,7 104,0 160,6 161,5Axles 34,8 125,7 92,5 186,6Batteries 20,8 35,5 28,7 68,8Body parts / panels 28,2 25,8 22,1 30,9Brake parts 31,9 37,4 21,7 21,7Car radios 11,0 30,0 36,1 0,5Catalytic converters 11 886,1 16 013,7 12 389,9 13 288,6Clutches / shaft couplings 198,0 143,8 140,1 169,8Engines 17,6 6,1 16,3 7,5Engine parts 728,1 741,0 834,0 1 019,3Filters 143,0 165,3 131,7 157,0Gaskets 31,5 29,6 34,2 42,7Gauges / instruments / parts 38,1 45,2 42,9 44,7Gear boxes 7,0 68,8 14,8 4,5Glass 284,1 256,0 210,6 324,9Ignition / starting equipment 35,5 22,2 15,4 21,7Jacks 20,4 14,2 22,8 10,6Lighting equipment 137,7 139,2 131,4 154,7Radiators / parts 489,2 642,3 577,3 74,4Road wheels / parts 323,3 401,4 251,5 123,7Seats 0,3 0,6 0,3 0,5Seat belts 0,5 1,1 0,7 0,4Stitched leather seats 2 871,1 2 157,3 1 693,4 1 499,3Shock absorbers / suspension parts 296,6 373,8 366,5 386,6Silencers / exhausts 1 415,9 1 790,4 1 326,8 839,7Springs 21,3 21,5 7,8 7,3Steering wheels / columns 131,0 110,0 123,9 131,8Transmission shafts 159,6 230,5 247,0 217,1Tyres 381,3 624,3 392,5 274,4Wiring harnesses 40,4 61,1 63,9 75,9Other parts 714,2 1 423,5 1 250,0 1 838,9Light vehicles 12 446,2 12 619,2 13 327,2 13 841,6Medium / Heavy vehicles 69,6 64,2 4,4 7,5

Source: AIEC, SARS

27 EXPORTS

Top export destinations in the EU with export value - 2013

28 EXPORTS

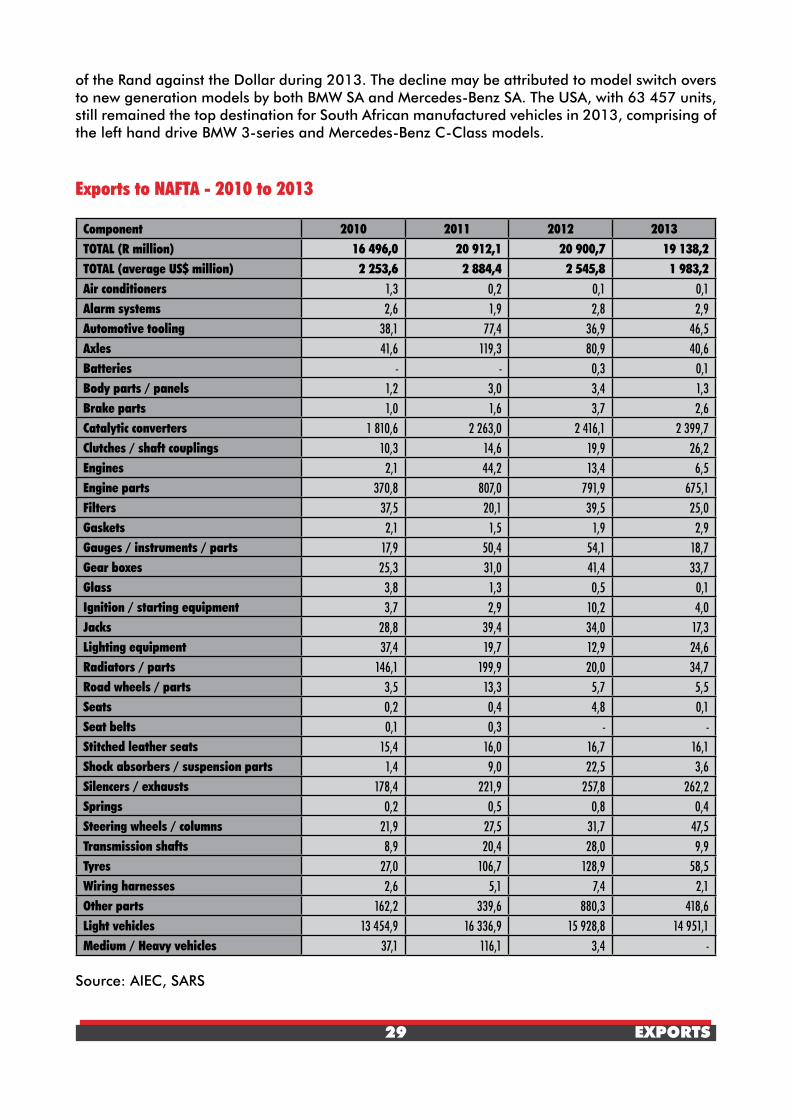

NAFTA (North American Free Trade Area)

The North American Free Trade Area consists of the USA, Canada and Mexico and was South Africa’s second largest trading region. Exports amounted to R19,1 billion or 18,6% of total automotive exports of R102,7 billion in 2013.

South Africa is a beneficiary of the USA’s Generalised System of Preference (GSP), which was instituted on 1 January 1976 and grants duty-free status to some goods. Since 2001 trade with the USA has significantly increased under the African Growth and Opportunity Act (AGOA), which is an extension of the GSP and allows duty-free access of additional products into the USA. AGOA represents a non-reciprocal gesture by the USA aimed at liberalizing trade and assisting the growth and development of sub-Saharan African countries by extending duty-free and quota-free access into the USA market in respect of a broad range of products. South Africa, together with 39 other African countries, have been designated as eligible countries in terms of the Act. The effective commencement date of the duty-free access provisions in terms of AGOA was 1 January 2001. The first expiry date was until 30 September 2008, which was subsequently extended until 30 September 2015. AGOA provides three important benefits to sub-Saharan African exporters. Firstly, it extends the duty-free treatment under the GSP programme to September 2015. Secondly, AGOA eliminates most of the limitations of the GSP programme for sub-Saharan African countries. Thirdly, AGOA expands the product coverage of the GSP programme exclusively for products of sub-Saharan Africa. The Rule of Origin requirement is that 35% of the value added on the output should come from the production activities in the country claiming AGOA preference. The 35% value added can be met by including the production of raw materials from other AGOA beneficiaries.

Under AGOA, 98% of South African exports to the US enter the country without tariffs or quotas. Various automotive components and, importantly, motor cars as well as motor vehicles for the transportation of persons and of goods now qualify for a duty-free and quota-free access into the USA. Duty rates into the USA normally range from 2,5% to 25% in respect of various types of vehicles.

Under AGOA, trade in automotive products between the United States and South Africa has grown substantially in recent years as American consumers benefit from the reduced import duties. Imports of vehicles, original equipment components as well as replacement parts into South Africa have also increased substantially. The interests of American automotive corporations are well represented in South Africa. Ford Motor Company and General Motors are long established, leading automotive producing corporations in South Africa. Moreover, most of the top American automotive parts suppliers are represented in South Africa, including Johnson Controls, Lear, TRW Automotive, Tenneco, Federal Mogul, Delphi, Visteon and ArvinMeritor, amongst others. All of these companies have built strong business links between their South African operations and other international stakeholders, including those in the US. AGOA and its extension beyond 2015 will be good for Africa’s growth and development and will also be beneficial to US companies hoping to tap into new growth markets in Africa. It is important for South Africa to share the same treatment under AGOA as all countries in the region otherwise if preferences were to be offered only to certain countries, this could be counterproductive because they would inhibit the natural development of integrated value chains in the region. AGOA needs to be optimised within an investor and exporter friendly long term framework.

In 2013 exports to NAFTA amounted to R19,1 billion, a decline of 8,4% from the R20,9 billion exported in 2012, and declined by 22,1% in US Dollar terms, in line with the 17,5% depreciation

29 EXPORTS

of the Rand against the Dollar during 2013. The decline may be attributed to model switch overs to new generation models by both BMW SA and Mercedes-Benz SA. The USA, with 63 457 units, still remained the top destination for South African manufactured vehicles in 2013, comprising of the left hand drive BMW 3-series and Mercedes-Benz C-Class models.

Exports to NAFTA - 2010 to 2013

Component 2010 2011 2012 2013TOTAL (R million) 16 496,0 20 912,1 20 900,7 19 138,2TOTAL (average US$ million) 2 253,6 2 884,4 2 545,8 1 983,2Air conditioners 1,3 0,2 0,1 0,1Alarm systems 2,6 1,9 2,8 2,9Automotive tooling 38,1 77,4 36,9 46,5Axles 41,6 119,3 80,9 40,6Batteries - - 0,3 0,1Body parts / panels 1,2 3,0 3,4 1,3Brake parts 1,0 1,6 3,7 2,6Catalytic converters 1 810,6 2 263,0 2 416,1 2 399,7Clutches / shaft couplings 10,3 14,6 19,9 26,2Engines 2,1 44,2 13,4 6,5Engine parts 370,8 807,0 791,9 675,1Filters 37,5 20,1 39,5 25,0Gaskets 2,1 1,5 1,9 2,9Gauges / instruments / parts 17,9 50,4 54,1 18,7Gear boxes 25,3 31,0 41,4 33,7Glass 3,8 1,3 0,5 0,1Ignition / starting equipment 3,7 2,9 10,2 4,0Jacks 28,8 39,4 34,0 17,3Lighting equipment 37,4 19,7 12,9 24,6Radiators / parts 146,1 199,9 20,0 34,7Road wheels / parts 3,5 13,3 5,7 5,5Seats 0,2 0,4 4,8 0,1Seat belts 0,1 0,3 - -Stitched leather seats 15,4 16,0 16,7 16,1Shock absorbers / suspension parts 1,4 9,0 22,5 3,6Silencers / exhausts 178,4 221,9 257,8 262,2Springs 0,2 0,5 0,8 0,4Steering wheels / columns 21,9 27,5 31,7 47,5Transmission shafts 8,9 20,4 28,0 9,9Tyres 27,0 106,7 128,9 58,5Wiring harnesses 2,6 5,1 7,4 2,1Other parts 162,2 339,6 880,3 418,6Light vehicles 13 454,9 16 336,9 15 928,8 14 951,1Medium / Heavy vehicles 37,1 116,1 3,4 -

Source: AIEC, SARS

30 EXPORTS

Top export destinations in NAFTA with export value - 2013

31 EXPORTS

Africa

Africa is the youngest continent in terms of age of its population with more than 50% of the continent’s population being younger than 20, compared with only 28% of China’s population, underlining the continent’s huge comparative advantage and growth potential. African companies are attracting increasing investor attention due to the spending power of the rising middle class and expansion of its natural resources sector. Unsurprisingly, Africa is the second fastest growing continent in the world, after Asia, and offers the highest return on investment than any other region.

Africa’s challenge is to move off an economic growth path built on consumption and commodity exports onto a more sustainable developmental path based on industrialisation. Africa’s ongoing initiatives to advance regional integration and infrastructural development are vital in this respect. With a potential of one billion consumers, Africa’s ascension into one of the fastest growing economies has created massive demand for infrastructure, goods and services. The International Monetary Fund (IMF) predicts that over the next five years, Africa will surpass Asia and seven African nations will be in the top 10 fastest growing economies. These include Ethiopia, Mozambique, Tanzania, Republic of Congo, Ghana, Zambia and Nigeria. Many African countries were in a different state of economic and political development but over the next five to 10 years an increasing number of people on the continent will have sufficient disposable income to purchase a vehicle, which would thus drive industry sales.

South Africa continues to actively participate in African processes and continues to work together with other African countries in pursuing the development of the continent along the lines of the New Partnership for Africa’s Development (Nepad), including the pursuit of an economically integrated Africa. The vision of Nepad is for a self-reliant, innovative and enterprising Africa through the building of export capacity for African companies, attracting new investments from around the world and growing inter-African trade to facilitate faster economic growth on the African continent.

South Africa, as the economic powerhouse of the continent, is well positioned as a base from which investors can access the aggressively growing economies of the rest of Africa. South Africa is a key investment location, both for the market opportunities that lie within its borders and for the possibility to use the country as a gateway to the rest of the continent. Several global companies have accordingly chosen to locate their African headquarters in South Africa and have used the capabilities developed in the country to expand into the region. South Africa therefore serves as a platform to access the broader African opportunity, which underpins the choice of the country as a gateway into the continent.

South Africa represented the biggest domestic market for vehicles in Africa and accounted for 72% of the continent’s vehicle production in 2013. Africa remained South Africa’s main export region for commercial vehicles in 2013. Due to the limited levels of vehicle production on the rest of the continent, a diverse range of automotive components are exported by South Africa to the majority of countries in Africa, but the bulk of these exports consists of aftermarket replacement parts.

The following table reflects South African automotive exports to the African continent. Annual comparisons should take account of the following – the 2013 total automotive export data to Africa provides two comparisons: one comparison includes exports to Botswana, Lesotho,

32 EXPORTS

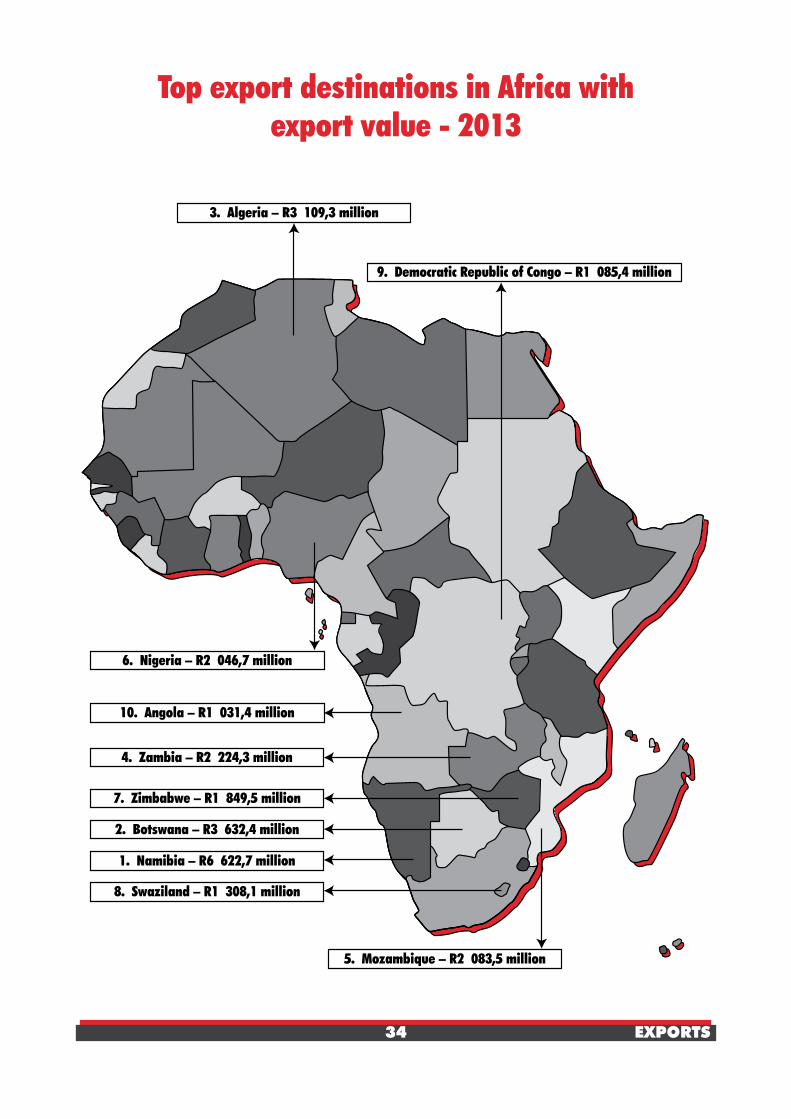

Namibia and Swaziland (BLNS countries) in line with the new publishing format of South African trade data provided by SARS, and the other comparison excludes exports to BLNS countries in order to facilitate historical comparisons. Total automotive exports to Africa, excluding BLNS country data, increased only by 0,5% or R91 million, following the significant 53,6% increase of the previous year. Total automotive exports, including BLNS country data, increased by 16,8% or R4,3 billion, mainly due to an increase in export sales to Namibia and Botswana. Vehicle exports to 42 African countries declined from 80 293 units in 2012 to 78 787 units in 2013.

33 EXPORTS

Exports to Africa - 2010 to 2013

Component 2010 2011 2012 2013 2013TOTAL (R million)Including BLNS country data 17 707,4 19 997,2 25 862,2 30 194,5**

TOTAL (R million) Excluding BLNS country data 8 719,2 11 588,9 17 796,9 17 887,9*

Air conditioners 10,7 12,6 18,6 18,1 30,1Alarm systems 22,3 14,7 21,4 21,6 36,6Automotive tooling 88,5 99,7 314,8 291,1 396,8Axles 13,7 20,9 42,9 61,4 87,3Batteries 94,3 106,3 146,7 166,6 209,8Body parts / panels 26,2 23,6 80,8 77,6 144,9Brake parts 49,1 33,6 54,4 70,6 145,7Car radios 8,6 5,8 9,9 8,2 24,2Catalytic converters 29,2 63,8 90,2 86,1 107,0Clutches / shaft couplings 16,2 20,9 31,9 29,6 72,5Engines 97,8 104,7 194,2 187,3 238,8Engine parts 181,2 182,5 339,5 334,1 585,0Filters 99,1 110,4 162,4 154,7 207,7Gaskets 35,0 33,1 59,1 79,1 106,7Gauges / instruments / parts 126,1 164,6 210,5 244,7 312,8Gear boxes 16,7 19,3 31,6 41,2 74,3Glass 10,8 11,9 13,4 15,7 54,6Ignition / starting equipment 37,1 61,1 73,3 64,5 136,2Jacks 7,8 14,3 15,0 24,0 26,9Lighting equipment 22,7 25,6 34,5 42,6 53,8Radiators / parts 16,4 22,2 32,4 29,5 58,4Road wheels / parts 21,0 21,3 70,8 68,3 110,3Seats 2,9 2,0 3,7 4,3 9,7Seat belts 1,2 1,5 1,5 1,7 4,2Stitched leather seats 3,4 10,0 2,4 4,7 11,0Shock absorbers / suspension parts 19,3 31,7 33,1 33,8 58,5Silencers / exhausts 6,4 4,6 8,7 5,7 15,5Springs 2,2 4,7 6,8 10,2 16,9Steering wheels / columns 7,3 5,9 11,0 12,1 20,1Transmission shafts 172,6 219,7 267,2 322,9 448,6Tyres 583,4 685,6 810,8 725,3 1 352,6Wiring harnesses 2,9 2,8 12,3 12,2 33,2Other parts 1 494,4 1 768,4 2 517,2 2 846.8 5 325,8Light vehicles 4 627,5 6 917,7 10 857,2 10 598,9 16 958,1Medium / Heavy vehicles 765,2 761,4 1 216,7 1 192,7 2 719,9

Source: AIEC, SARS* Comparison excluding BLNS (Botswana, Lesotho, Namibia and Swaziland) country exports** Comparison including BLNS (Botswana, Lesotho, Namibia and Swaziland) country exports

34 EXPORTS

Top export destinations in Africa with export value - 2013

35 EXPORTS

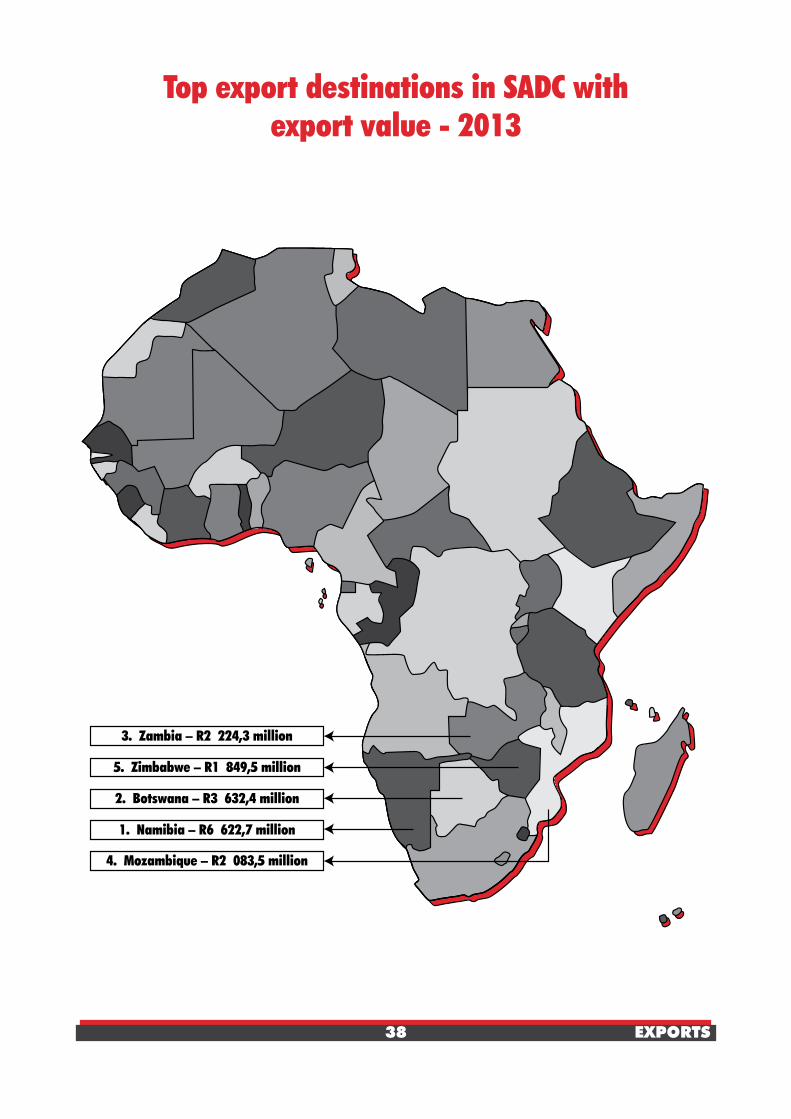

Southern African Development Community (SADC)

Within Africa, automotive exports to SADC comprised 72,4% of the continent’s automotive exports and 21,3% of total South African automotive exports of R102,7 billion in 2013.

Sub-Saharan Africa represents 1,6% of the world’s economy. Over the next 20 to 30 years, sub-Saharan Africa’s urban population is expected to more than double, creating lucrative demand opportunities for domestic and international manufacturers of goods. The region’s growth remains positive on the back of increased investment flows, rising consumer spending and the coming on stream of new mineral exports in a number of countries within the region. It is, however, important for sub-Saharan Africa, as a global growth frontier, to move away from its current economic growth path that relies almost exclusively on resource extraction and exports, towards a more sustainable development path that promotes industrialisation and value addition. Industrialisation offers the best chance for generating jobs and income, creating a middle class and improving individual lives. In this regard, infrastructure development is important, as it is not only an enabler of competitiveness and trade, but also a stimulant of economic growth.

South Africa’s participation in the Southern African Development Community (SADC), comprising of 15 sub-Saharan African countries, allows access to a market of approximately 280 million people and a regional GDP of US$471 billion. SADC operates as a Free Trade Area. The 15 SADC countries include Angola, Botswana, Democratic Republic of Congo, Lesotho, Madagascar, Malawi, Mauritius, Mozambique, Namibia, Seychelles, South Africa, Swaziland, Tanzania, Zambia and Zimbabwe. South Africa joined the SADC in August 1994. The SADC Protocol on Trade was signed on 24 August 1996 and came into force on 25 January 2000. The SADC FTA was launched in 2008 when 85% of tariff lines became duty-free. The remaining 15% tariff lines were deemed sensitive and were accorded a longer liberalisation time frame up to 2012, except for Mozambique, which would complete its tariff phase down with respect to imports from South Africa by 2015. Eleven members implemented the Protocol in September 2000 after ratification. Currently Angola, Seychelles and the Democratic Republic of Congo remain outside the agreement. To date, all signatories except for Zimbabwe have translated their commitments into domestic enabling legislation. Angola has not yet made an offer or implemented the SADC Trade Protocol, while the Democratic Republic of Congo and Seychelles, even though members of SADC, are not party to the SADC Trade Protocol. The Seychelles is in the process of becoming a party to the Trade Protocol. Its tariff offer was recently accepted on a technical level, and will in June 2014 be submitted to the Committee of Ministers of Trade for approval. Thereafter, the Seychelles would be in a position to complete its internal processes to ratify its accession and implement the tariff phase down schedule. The intention is that the agreement encourages economies of scale, creating competitive SADC-wide industries and thereby increasing intra-regional trade and enhancing foreign investment in the region. Given the high level of competition for foreign direct investment among emerging markets, South Africa has placed great importance on forming strong economic trading blocs in order to gain access to key markets. The SADC agreement consists of general objectives rather than specific obligations. The key policy objective is to strengthen trade and development linkages between South Africa and other SADC countries. By 2012, about 98% of SADC merchandise trade will be subject to zero tariffs. The phase-down offers are country-specific, on the principle of reciprocity. For example, tariff preferences will be extended only to member states that have submitted their instruments of implementation.

36 EXPORTS

Several SADC countries have consistently remained amongst the South African automotive industry’s top export destinations over the past two decades. The SADC is a major export region for the country’s commercial vehicles as well as automotive components. Since no vehicles are manufactured from completely disassembled/completely knocked down parts in the SADC region, except for South Africa, a wide range of automotive components are exported from South Africa to the region but the bulk of these exports consists of aftermarket replacement parts.

The following table reflects South Africa’s automotive exports to SADC. Annual comparisons should take account of the following – the 2013 total automotive exports (vehicles and automotive components) to SADC provides two comparisons: one comparison which includes exports to Botswana, Lesotho, Namibia and Swaziland (BLNS countries), in line with the new publishing format of South African trade data provided by SARS, and the other comparison which excludes exports to BLNS countries in order to facilitate historical comparisons. Total automotive exports to SADC, excluding BLNS country data, increased by only 1,1% or R102 million, following the significant 59,5% increase of the previous year. Total automotive exports, including BLNS country data, increased by 24,8% or R4,3 billion, mainly due to an increase in export sales to Namibia and Botswana.

37 EXPORTS

Exports to Southern African Development Community (SADC) - 2010 to 2013

Component 2010 2011 2012 2013 2013

TOTAL (R million)Including BLNS country data 13 880,7 14 331,4 17 521,8 21 865,2**

TOTAL (R million) Excluding BLNS country data 4 907,1 5 930,9 9 456,4 9 558,6*