ache ms panel discussion 031815 final

TRANSCRIPT

1

Upstart Alliances: How New Strategic Partnerships and Joint Venturing Will Reshape U.S. Healthcare

Managed Services & Enterprise PartnershipsA luncheon symposium hosted by Philips Healthcare March 18, 2014

2

Session AgendaOverview: The Future of provider‐vendor models

Panel introductions

Panel discussion / Q & A period

3

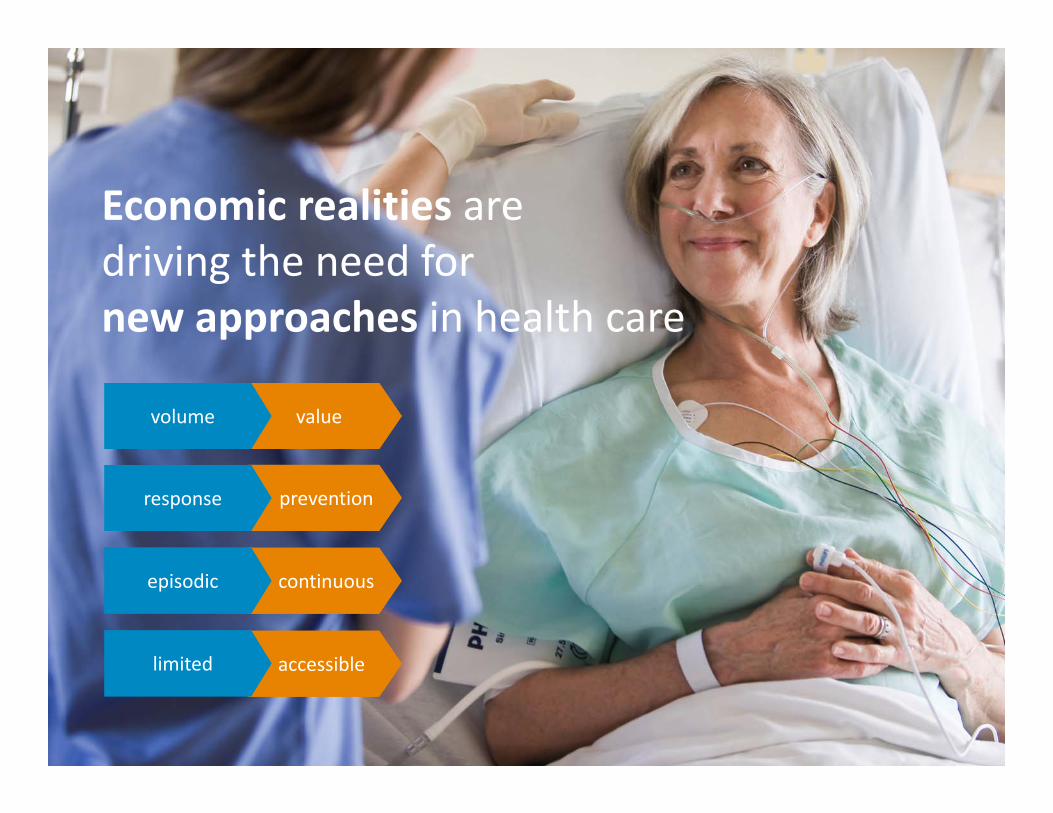

Economic realities are driving the need for new approaches in health care

valuevaluevolumevolume

preventionprevention

continuouscontinuous

accessible accessible

responseresponse

episodicepisodic

limitedlimited

4

To survive, thrive and add value to the communities we serve, we’ve all had to change.To survive, thrive and add value to the communities we serve, we’ve all had to change.

new business models and services to transform care deliverynew business models and services to transform care delivery

technologies, programs focused on personal health & wellnesstechnologies, programs focused on personal health & wellness

digital platform to connect care across the health continuum digital platform to connect care across the health continuum

hospital‐to‐home telehealth and population health solutions hospital‐to‐home telehealth and population health solutions

valuevalue

preventionprevention

continuouscontinuous

accessibleaccessible

volumevolume

responseresponse

episodicepisodic

limitedlimited

5

Traditional model Shared accountability modelJoint focus on partnership goals with shared

risk and performance incentives

Business Model Evolution

SupplierCustomer

Payments for Equipment and services at discounted pricing

SupplierCustomer

Common GoalsPredictabilityShared riskContinuous improvementReduced OpExInnovation

Equipment and Service delivery with Service Level Agreements

Joint Commitment to Quality, Efficiency, and Cost Metrics =VALUE FOR PATIENTS

The changing health care environment requires new business models and partnership strategies

6

Creating an “outcomes‐based‐ecosystem” – driven by global best practices – with the patient at the center

Hospital or health care provider

Design/buildpartner

Facilities/Operations partnerICAT partner

Business Model Partnership Options

Hospital or health care provider

Design/buildpartner

Facilities/Operations partner

ICAT partner

Managed Services Extend managed services business model across hospital operations

Enterprise Partnerships, ConsortiumsEstablish multi‐party consortium to design, build, finance and manage new hospital

8

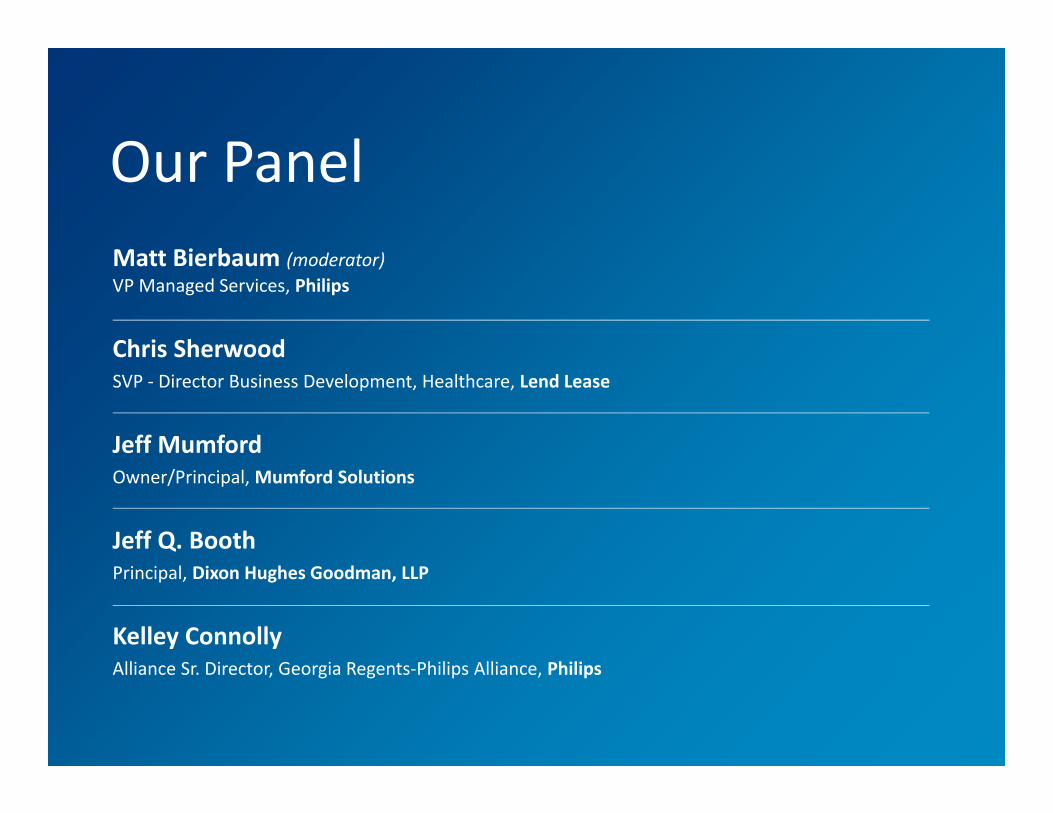

Matt Bierbaum (moderator)VP Managed Services, Philips

Chris SherwoodSVP ‐ Director Business Development, Healthcare, Lend Lease

Jeff MumfordOwner/Principal, Mumford Solutions

Jeff Q. BoothPrincipal, Dixon Hughes Goodman, LLP

Kelley ConnollyAlliance Sr. Director, Georgia Regents‐Philips Alliance, Philips

Our Panel

9

Chris Sherwood, SVPDirector Business Development, Healthcare, Lend Lease

14

Jeff Mumford, Owner/PrincipalMumford Solutions

Mumford Solutions• Contract Management Services• Public Private Partnership (PPP) Advisor Services• Project Management • Facility Management and Optimization

Honeywell Limited – Canadian Vice President HBS• Total Asset Management (TAM) – Honeywell’s PPP offering• Life Cycle Management• Energy Management

Jeff Mumford, P.Eng.

• PPP’s are an alternative procurement model for public infrastructure to traditional design / construction

• Single entity (“Project Company”) contracts with public sector entity and in turn contracts with consortium partners

• PPP’s involve private sector accepting responsibility for Design, Construction, Financing, Maintenanceand in some cases Operations

• Facilities management over a long term concession period (25 ‐ 35 years) with pre‐defined hand back conditions

What is a PPP or P3?

• Risk transfer, innovation, competition provides Value for Money

• PPP’s are performance‐based contracting arrangements

– Payment from public sector begins only upon completion of construction

– Ongoing payments remain subject to deduction for failures in service delivery

Partnership structure

Public Sector Agency

Project Co Developer/Equity Provider

Design & ConstructionGeneral Contractor

Operator & Life cyclee.g., Honeywell

Senior Debt Providere.g., RBC

DBFM/O Agreement

Sub Contracts Senior Debt Agreements

AvailabilityPayment

18

Jeff Q. Booth, PrincipalDixon Hughes Goodman LLP

19

Connecting the transformational dialogue

Guiding Our Clients to Risk Readiness & Value‐Driven SuccessIn an evolving healthcare environment moving towards clinical integration and population management, DHG Healthcare works with providers and payers to move from volume to value at a pace dictated by local market conditions and organizational readiness

20

Connecting the transformational dialogue

Clinical Enterprise Maturity (CEM)A concept unique to DHG Healthcare, the CEM is a qualitative evaluation that measures numerous characteristics associated (among other things) with the state of an organization’s physician enterprise in combination with its overall clinical integration accomplishments and planning.

Market StagingAn evaluation of an individual market’s level of evolution with respect to resident payment models. This concept, which DHC Healthcare has developed and applies in our business planning practice, considers evolutionary facts such as depth of non‐FFS transition, level of consolidation, employer base, and similar characteristics.

21

Connecting the transformational dialogue

Risk CapabilityHealthcare providers are preparing to accept greater risk for payment of services. Increasing an organization’s risk capability requires a focus on three critical success factors: Enterprise Intelligence, Revenue Transformation and Clinical Enterprise Maturity.

22

Kelley ConnollyAlliance Sr. Director, Philips HealthcareGR Health‐Philips Alliance

Sweden15 years

USA15 years

Netherlands10 years

Belfast15 years

KUBIN CLINICAustria8 yearsNetherlands

15 years

Spain8 years

Spain10 years

Philips has deep experience partneringwith leading healthcare systems

Care transformation and care redesign Enterprise quality and care management Consumerism and patient engagement Co‐develop and pilot new technologies

Collaboration for higher equipment utilization Managed services and business model Shared performance metrics and risk sharing

Long‐term managed services and innovation partnerships

Transforming healthcareover a large network

ChallengeBetter, faster, less expensive care for the 4 million patients served in primary and secondary markets.

“It's no longer a simple supply‐and‐demand business model. Our goal with the Philips alliance is to foster an atmosphere of meaningful innovation that will have a significant and positive impact on the health of our patients. This is the future of healthcare.”

‐David S. HefnerFormer CEO, GRHealth

Solution15‐year partnership focused on patient‐centered approaches to care that include medical equipment and systems, workflow re‐design, clinical education, and professional services. Addresses current and future clinical, operational, and equipment needs at predictable costs over a 15‐year term.

BenefitsFleet management, increased utilization and ROI, cost containment, improved quality, enhanced overall competencies of technicians, radiologists, nurses, and clinicians.

25

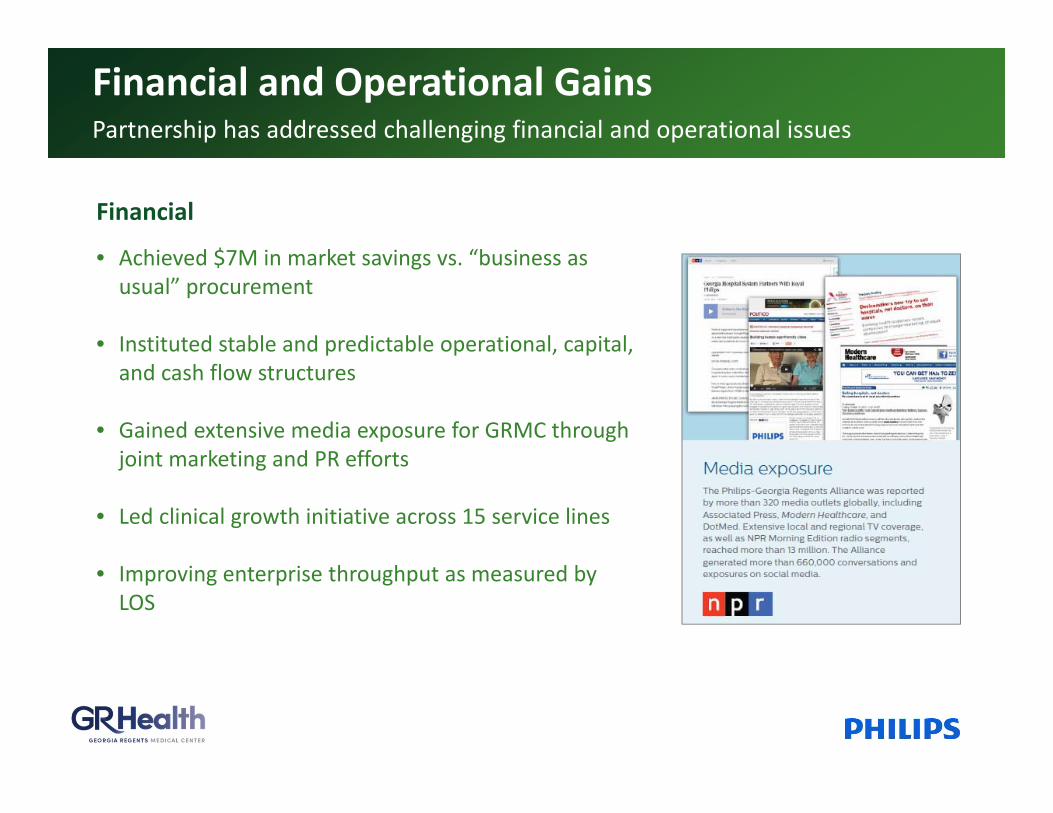

Financial

• Achieved $7M in market savings vs. “business as usual” procurement

• Instituted stable and predictable operational, capital, and cash flow structures

• Gained extensive media exposure for GRMC through joint marketing and PR efforts

• Led clinical growth initiative across 15 service lines

• Improving enterprise throughput as measured by LOS

Financial and Operational GainsPartnership has addressed challenging financial and operational issues

26

Clinical

• Transformed from aging to state‐of‐the‐art technology in monitoring systems to drive safer, faster in‐patient environment

• Switch from analogue to digital radiology systems driving significant workflow efficiencies and corresponding volume

• Reallocated imaging resources to support growth and improve utilization

• Improved the patient and staff experience

• Supported substantial quality re‐programming initiative

Year One AccomplishmentsClinical transformation and a new, collaborate way of addressing challenges

27

Panel Discussion/Q&A

28