accumulation default investment strategy qsuper …€¦ · accumulation default investment...

TRANSCRIPT

Accumulation Default Investment Strategy

QSuper Case Study

Rosemary Vilgan – CEO

ICPM Discussion Forum

October 2013

2

1. Understanding risks from a member perspective

2. 1st and 2nd generation investment strategy responses

3. QSuper’s response – 3rd generation ALM and supporting

influences

4. Investment process and principles

5. The first cohorts

6. Conclusion

Agenda

3

• QSuper’s objective for Default Option was CPI + 4% pa over ten years.

• Little relevance to members

− longer or shorter horizons than 10 years

− risk tolerances change with age and account balance

− accrue an IRR not a time-weighted return

• They will understand an objective to accrue a dollar amount

− Fixed dollar amount (e.g. $500,000)

− “ASFA (Industry Association) Comfortable” income level (e.g.

$40,000 pa).

− Individual replacement rate (e.g. 70% of salary)

• The Trustee will set a specific target for each cohort of default

members

Understanding members’objectives

4

Sequence of returns matter

1930-50: 2.0 %/yr

Source: New York Times 01/02/11, “In Investing, It’s When You Start and When You Finish”

Best 20 year return 1948-68: 8.4 %/yr

Worst 20 year return 1961-81: -2.0 %/yr

2nd best 20 years 1979-99: 8.2 %/yr

Expectations are 7% pa real (areas in green) This is rare over 20 years or longer Stable returns over 60 or 70 year periods

0% +3% +7% +10%

Average real annual return for S&P500 (includes dividends and taxes)

Australia is no different! 10 years average real returns since 1980: • minimum of 1.3% (2010) • maximum of 9.2%

(1992)

Outline squares show investment returns after 20 years

5

• The Board endorsed the Lifetime Accumulation strategy

• First steps: changed Balanced (Default) Option (objective and

strategy) and withdrawn from surveys

• Subsequent steps:

− Segment default Accumulation members into meaningful cohorts

− Developing investment strategy for each cohort using asset-

liability management (ALM) principles

− Strategies will be managed dynamically into the future as cohorts

and risks change

− A range of complementary non-investment initiatives

• Goal: exercise fiduciary authority to accumulate assets and transition

to maintain retirement income

The path QSuper is following

6

• Use age as a starting point. Age is a good proxy for:

− Investment horizons

− Member risk tolerance around adequacy vs. certainty

• But it is imperative to also include other factors:

Account balance Contribution rate

Salary Variable retirement dates (later)

• Make assumptions regarding unknown data

• Establish homogeneous cohorts with reasonably narrow distributions.

Accept and understand the shortcomings of averages.

• Similar in some concepts to a DB Fund measure of solvency.

Segmenting cohorts of default members

Funded status

7

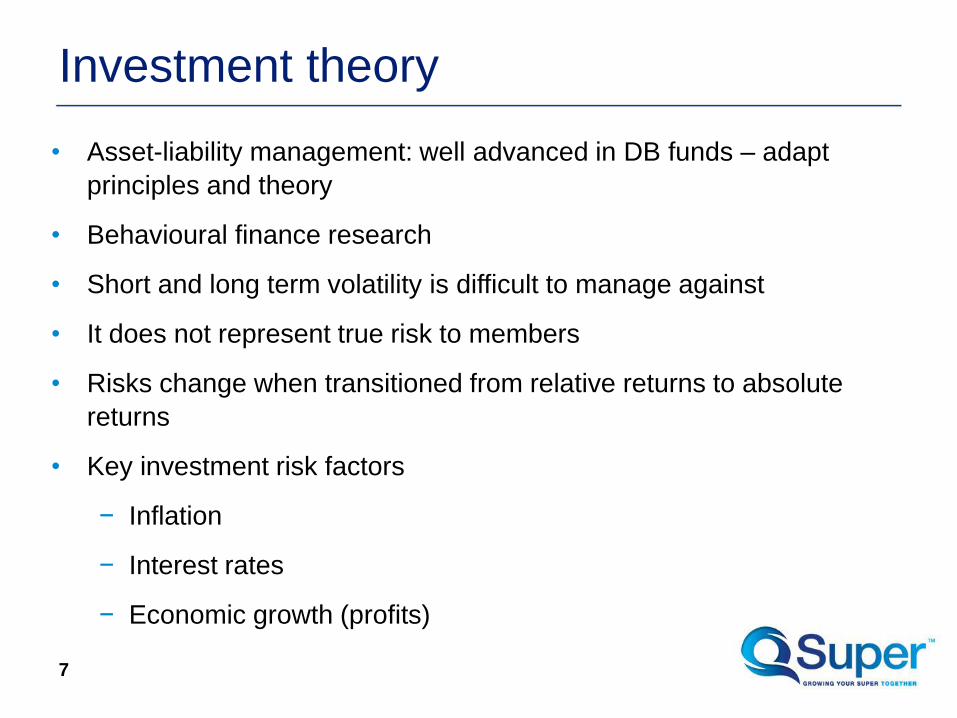

Investment theory

• Asset-liability management: well advanced in DB funds – adapt

principles and theory

• Behavioural finance research

• Short and long term volatility is difficult to manage against

• It does not represent true risk to members

• Risks change when transitioned from relative returns to absolute

returns

• Key investment risk factors

− Inflation

− Interest rates

− Economic growth (profits)

8

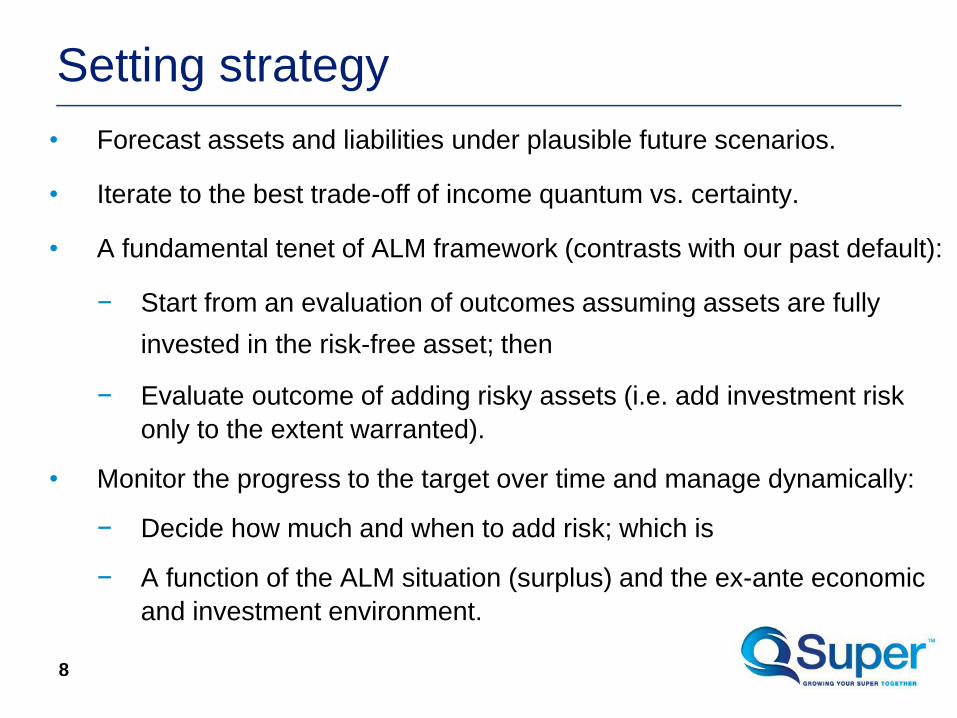

• Forecast assets and liabilities under plausible future scenarios.

• Iterate to the best trade-off of income quantum vs. certainty.

• A fundamental tenet of ALM framework (contrasts with our past default):

− Start from an evaluation of outcomes assuming assets are fully

invested in the risk-free asset; then

− Evaluate outcome of adding risky assets (i.e. add investment risk

only to the extent warranted).

• Monitor the progress to the target over time and manage dynamically:

− Decide how much and when to add risk; which is

− A function of the ALM situation (surplus) and the ex-ante economic

and investment environment.

Setting strategy

9

• Invest “to” not “through” retirement.

• Define risk as not achieving the retirement income objective, rather

than volatility of asset returns.

• Respond to changing investment environment and cohort

characteristics. Not a static lifetime glide-path.

• Default members have asymmetric risk preferences.

− Adopt a conservative bias for default members, with opt-out

provision.

− Emphasise short-fall and down-side risk metrics.

• Use the risk-free strategy as an ALM benchmark. Add investment risk

(quantity and timing) when it appears to be rewarding.

Some emerging ALM principles

“When” not “if”

• In 10 years time, would you ignore what you know about your

members?

• Funds will become advice engines; even to default members

• This will invert current business plans

10

Investment and Administration platform

Education and marketing

segmentation

Advice

Personal advice

Mass Fund

Driven Advice

Investment and Administration platform

11

• Cohort 1 is underway:

− 2,100 default members

− Contacted in February 2013

• Outcomes:

− Very few negative comments

− About 25% elected to opt-out

− New strategy executed in April 2013

• Australian MySuper licensing obtained

− A further 51,000 default members in Cohort 2

− Will be executed in December 2013

• Next six cohorts for younger members in 2014

The First Cohorts

12

Membership Profile and Analysis

Cohort No# MembersTotal FUMMed Age

Med Balance

30 40 50 60 70 80

$100,000 $100,000

$50,000 $50,000

$500,000 $500,000

$300,000 $300,000

$250,000 $250,000

Cohort 8177,167

$6,002.2m31

$18,012

Cohort 640,125

$4,573.0m45

$95,636

44 Cohort 7$7,900 83,916

$1,123.3m

Cohort 567,158

$1,882.6m53

$16,729

Cohort 414,710

$2,209.6m53

$140,682

Cohort 12,956

$1,574.3m61

$453,572Cohort 33,304

$1,349.8m54

$345,960

Cohort 251,169

$2,580.4m62

$19,522

13

Summary of strategies

Age

$100,000

$50,000 H20

H0

40 50 58

Account B

ala

nce

H80

H40 $300,000

$250,000

H20

H30 H60

H0

• The industry often analyses lifecycle strategies using glidepaths.

• While QSuper Lifetime is not a traditional glidepath product we should

remain aware of how it will be perceived by stakeholders.

• The paths of this for the age/account balance cohort structure:

Glidepaths (stylised)

0

20

40

60

80

100

20 25 30 35 40 45 50 55 60 65 70

% G

row

th A

sse

ts

Age

Low Balance Med Balance High Balance Typical Balanced

14

15

• This is a material change to the way we manage default

accumulation members’ assets.

• Initially applied to cohorts and based on average factors (age and

account balance) and investment expectations.

• Not a perfect solution but we start here and improve over time.

Remains flexible (e.g. to incorporate Australian MySuper rules) and

we will move through cohorts methodically.

• Limited number of initial cohorts allows us to test decision making

process and make administrative adjustments.

• Similar ALM methodology has been used in DB fund since 2006.

Summary and conclusion