accounting systems - e-learning · 202 chapter 5 accounting systems basic accounting systems in...

TRANSCRIPT

C H A P T E R

I N T U I T I N C.

5

Accounting Systems

Whether you realize it or not, you likely interact with

accounting systems. For example, your checkbook

register is a type of accounting system. When you make a

deposit, you record an addition to your cash; when you

write a check, you record a reduction in your cash. Such a

simple accounting system works well for a person with just

a few transactions per month. However, over time, you

may find that your financial affairs will become more com-

plex and involve many different types of transactions,

including investments and loan payments. At this point, a

simple checkbook register may not be sufficient for man-

aging your financial affairs. Personal financial planning

software, such as Intuit’s Quicken®, can be useful when your

financial affairs reach this level of complexity.

What happens if you decide to begin a small business?

Now the transactions occurring every month have expanded

and involve customers, vendors, and employees. As a

result, the accounting system will need to grow with this

complexity. Thus, many small businesses will use small-

business accounting software, such as Intuit’s QuickBooks®,

as their first accounting system. As a business grows, more

sophisticated accounting systems will be needed.

Companies such as SAP, Oracle, NetSuite Inc., and SageSoftware, Inc. offer accounting system solutions for busi-

nesses that become larger with more complex accounting

needs.

Accounting systems used by large and small busi-

nesses employ the basic principles of the accounting cycle

discussed in the previous chapters. However, these account-

ing systems include features

that simplify the recording and

summary process. In this chap-

ter, we will discuss these sim-

plifying procedures as they

apply to both manual and

computerized systems.

© P

ixla

nd

/Ju

pit

erIm

ages

202 Chapter 5 Accounting Systems

Basic Accounting SystemsIn Chapters 1–4, an accounting system for NetSolutions was described and illustrated. Anaccounting system is the methods and procedures for collecting, classifying, summarizing,and reporting a business’s financial and operating information. Most accounting systems,however, are more complex than NetSolutions’. For example, Southwest Airlines’ accountingsystem not only records basic transaction data, but also records data on such items as ticketreservations, credit card collections, frequent-flier mileage, and aircraft maintenance.

As a business grows and changes, its accounting system also changes in a three-stepprocess. This three-step process is as follows:

Step 1. Analyze user information needs.

Step 2. Design the system to meet the user needs.

Step 3. Implement the system.

For NetSolutions, our analysis determined that Chris Clark needed financial state-ments for the new business. We designed the system, using a basic manual system thatincluded a chart of accounts, a two-column journal, and a general ledger. Finally, weimplemented the system to record transactions and prepare financial statements.

Define and describe anaccounting system.

Journalize and posttransactions in amanual accountingsystem that usessubsidiary ledgers andspecial journals.

Subsidiary Ledgers

Special Journals

Revenue Journal

E-Commerce

Describe and giveexamples of othersubsidiary ledgers andmodified specialjournals.

ComputerizedAccounting Systems

Additional SubsidiaryLedgers

Modified SpecialJournals

Describe and illustratethe use of acomputerizedaccounting system.

Manual AccountingSystems

Describe the basic features ofe-commerce.

After studying this chapter, you should be able to:

1

At a Glance Menu Turn to pg 223

2 3 4 5

Cash Payments Journal

Basic AccountingSystems

Cash Receipts Journal

Adapting ManualAccounting Systems

EE 5-5(page 218)

EE 5-1(page 208)

Purchases JournalEE 5-3(page 213)

Accounts PayableControl Account andSubsidiary LedgerEE 5-4

(page 217)

Accounts ReceivableControl Account andSubsidiary LedgerEE 5-2

(page 211)

Define and

describe an

accounting system.

1

Chapter 5 Accounting Systems 203

Once a system has been implemented, feedback, or input, fromusers is used to analyze and improve the system. For example, in laterchapters NetSolutions expands its chart of accounts to record morecomplex transactions.

Internal controls and information processing methods are essen-tial in an accounting system. Internal controls are the policies andprocedures that protect assets from misuse, ensure that business infor-mation is accurate, and ensure that laws and regulations are being fol-lowed. Internal controls are discussed in Chapter 8.

Processing methods are the means by which the system collects, sum-marizes, and reports accounting information. These methods may beeither manual or computerized. In the following sections, manual account-ing systems that use special journals and subsidiary ledgers are describedand illustrated. This is followed by a discussion of computerized account-ing systems.

Manual Accounting SystemsAccounting systems are manual or computerized. Understanding a manual accountingsystem is useful in identifying relationships between accounting data and reports. Also,most computerized systems use principles from manual systems.

In prior chapters, the transactions for NetSolutions were manually recorded in anall-purpose (two-column) journal. The journal entries were then posted individually tothe accounts in the ledger. Such a system is simple to use and easy to understand whenthere are a small number of transactions. However, when a business has a large num-ber of similar transactions, using an all-purpose journal is inefficient and impractical.For example, in a given day, a company might earn fees on account from 20 customers.Recording each fee earned by debiting Accounts Receivable and crediting Fees Earnedwould be inefficient. Also, a record of the amount each customer owes must be kept. Insuch cases, subsidiary ledgers and special journals are useful.

Subsidiary LedgersAn accounting system should be designed to provide information on the amounts duefrom various customers (accounts receivable) and amounts owed to various creditors(accounts payable). A separate account for each customer and creditor could be addedto the ledger. However, as the number of customers and creditors increases, the ledgerwould become awkward.

A large number of individual accounts with a common characteristic can be groupedtogether in a separate ledger called a subsidiary ledger. The primary ledger, which con-tains all of the balance sheet and income statement accounts, is then called the generalledger. Each subsidiary ledger is represented in the general ledger by a summarizingaccount, called a controlling account. The sum of the balances of the accounts in a sub-sidiary ledger must equal the balance of the related controlling account. Thus, a subsidiaryledger is a secondary ledger that supports a controlling account in the general ledger.

Two of the most common subsidiary ledgers are as follows:

1. Accounts receivable subsidiary ledger

2. Accounts payable subsidiary ledger

The accounts receivable subsidiary ledger, or customers ledger, lists the individual cus-tomer accounts in alphabetical order. The controlling account in the general ledger that sum-marizes the debits and credits to the individual customer accounts is Accounts Receivable.

The accounts payable subsidiary ledger, or creditors ledger, lists individual creditoraccounts in alphabetical order. The related controlling account in the general ledger isAccounts Payable.

The relationship between the general ledger and the accounts receivable andaccounts payable subsidiary ledgers is illustrated in Exhibit 1.

Journalize

and post

transactions in a

manual accounting

system that uses

subsidiary ledgers

and special journals.

2

. . .

. . .

. . .

. . .

.

Implementation

Design

Analysis

Feedback

204 Chapter 5 Accounting Systems

Special JournalsOne method of processing data more efficiently in a manual accounting system is toexpand the all-purpose two-column journal to a multicolumn journal. Each column in amulticolumn journal is used only for recording transactions that affect a certain account.

For example, a special column could be used only for recording debits to the cashaccount. Likewise, another special column could be used only for recording credits to thecash account. The addition of the two special columns would eliminate the writing of Cashin the journal for every receipt and every payment of cash. Also, there would be no needto post each individual debit and credit to the cash account. Instead, the Cash Dr. and CashCr. columns could be totaled periodically and only the totals posted. In a similar way, spe-cial columns could be added for recording credits to Fees Earned, debits and credits to

Accounts Receivable and Accounts Payable, and for other entries thatare repeated.

An all-purpose multicolumn journal may be adequate for asmall business that has many transactions of a similar nature.However, a journal that has many columns for recording many dif-ferent types of transactions is impractical for larger businesses.

The next logical extension of the accounting system is to replace the single multi-column journal with several special journals. Each special journal is designed to beused for recording a single kind of transaction that occurs frequently. For exam-ple, since most businesses have many transactions in which cash is paid out, they willlikely use a special journal for recording cash payments. Likewise, they will use anotherspecial journal for recording cash receipts. Special journals are a method of summariz-ing transactions, which is a basic feature of any accounting system.

Exhibit 1

General Ledger and Subsidiary Ledgers

Chris Clark, Drawing 32

Chris Clark, Capital 31

Accts. Payable 21(Controlling Account)

AccountsReceivableSubsidiary

Ledger

AccountsPayable

SubsidiaryLedger

Customer D

Customer C

Customer B

Customer A

Creditor D

Creditor C

Creditor B

Creditor A

General LedgerSupplies 14

Accts. Rec. 12(Controlling Account)

Cash 11

Special journals are a method ofsummarizing transactions.

Chapter 5 Accounting Systems 205

The format and number of special journals that a business uses depends on thenature of the business. A business that gives credit might use a special journal designedfor recording only revenue from services provided on credit. In contrast, a business thatdoes not give credit would have no need for such a journal.

The transactions that occur most often in a small service business and the specialjournals in which they are recorded are as follows:

Revenue journal

Cash receipts journal

Purchases journal

Cash payments journal

Providing services on account

recorded in

Receipt of cash from any source

recorded in

Purchase of items on account

recorded in

Payment of cash for any purpose

recorded in

The all-purpose two-column journal, called the general journal or simply the journal,can be used for entries that do not fit into any of the special journals. For example,adjusting and closing entries are recorded in the general journal.

Next, the following types of transactions, special journals, and subsidiary ledgersare described and illustrated for NetSolutions:

Transaction Special Journal Subsidiary Ledger

Fees earned on Revenue journal Accounts receivable account subsidiary ledger

Cash receipts Cash receipts journal Accounts receivable subsidiary ledger

Purchases on Purchases journal Accounts payable subsidiaryaccount ledger

Cash payments Cash payments journal Accounts payable subsidiary ledger

As shown above, transactions that are recorded in the revenue and cash receiptsjournals will affect the accounts receivable subsidiary ledger. Likewise, transactionsthat are recorded in the purchases and cash payments journals will affect the accountspayable subsidiary ledger.

We will assume that NetSolutions had the following selected general ledger bal-ances on March 1, 2010:

Account Number Account Balance

11 Cash $6,20012 Accounts Receivable 3,40014 Supplies 2,50018 Office Equipment 2,50021 Accounts Payable 1,230

Revenue JournalFees earned on account would be recorded in the revenue journal. Cash fees earned wouldbe recorded in the cash receipts journal.

206 Chapter 5 Accounting Systems

To illustrate the efficiency of using a revenue journal, an example for NetSolutionsis used. Specifically, assume that NetSolutions recorded the following four revenuetransactions for March in its general journal:

Mar.2010

2,200

1,750

2,650

3,000

2

6

18

27

12/✓

41

12/✓

41

12/✓

41

12/✓

41

Accounts Receivable––Accessories By Claire

Fees Earned

Accounts Receivable––RapZone

Fees Earned

Accounts Receivable––Web Cantina

Fees Earned

Accounts Receivable––Accessories By Claire

Fees Earned

2,200

1,750

2,650

3,000

For the above entries, NetSolutions recorded eight account titles and eightamounts. In addition, NetSolutions made twelve postings to the ledgers—four toAccounts Receivable in the general ledger, four to the accounts receivable subsidiaryledger (indicated by each check mark), and four to Fees Earned in the general ledger.

The preceding revenue transactions could be recorded more efficiently in a revenuejournal, as shown in Exhibit 2. In each revenue transaction, the amount of the debit toAccounts Receivable is the same as the amount of the credit to Fees Earned. Thus, onlya single amount column is necessary. The date, invoice number, customer name, andamount are entered separately for each transaction.

Revenues are normally recorded in the revenue journal when the company sendsan invoice to the customer. An invoice is the bill that is sent to the customer by the com-pany. Each invoice is normally numbered in sequence for future reference.

To illustrate, assume that on March 2 NetSolutions issued Invoice No. 615 toAccessories By Claire for fees earned of $2,200. This transaction is entered in therevenue journal, shown in Exhibit 2, by entering the following items:

1. Date column: Mar. 22. Invoice No. column: 6153. Account Debited column: Accessories By Claire4. Accts. Rec. Dr./Fees Earned Cr. column: 2,200

The process of posting from a revenue journal, shown in Exhibit 3, is as follows:

1. Each transaction is posted individually to a customer account in the accountsreceivable subsidiary ledger. Postings to customer accounts should be made on a

Revenue Journal Page 35

Mar.2010

2,200

1,750

2,650

3,000

9,600

Accessories By Claire

RapZone

Web Cantina

Accessories By Claire

2

6

18

27

31

615

616

617

618

Date Account DebitedInvoice

No.Post.Ref.

Accts. Rec. Dr.Fees Earned Cr.

Exhibit 2

RevenueJournal

Chapter 5 Accounting Systems 207

regular basis. In this way, the customer’s account will show a current balance. Sincethe balances in the customer accounts are usually debit balances, the three-columnaccount form is shown in Exhibit 3.

To illustrate, Exhibit 3 shows the posting of the $2,200 debit to Accessories By Claire in theaccounts receivable subsidiary ledger. After the posting, Accessories By Claire has a debitbalance of $2,200.

2. To provide a trail of the entries posted to the subsidiary and general ledger, thesource of these entries is indicated in the Posting Reference column of each accountby inserting the letter R (for revenue journal) and the page number of the revenuejournal.

To illustrate, Exhibit 3 shows that after $2,200 is posted to Accessories By Claire’s account,R35 is inserted into the Post. Ref. column of the account.

3. To indicate that the transaction has been posted to the accounts receivable sub-sidiary ledger, a check mark (✓) is inserted in the Post. Ref. column of the revenuejournal, as shown in Exhibit 3.

✓

R35

Date ItemPost.Ref. Debit Credit

Mar. 1

31

2010

Debit Credit

Balance

Account No. 12Account Accounts Receivable

R35

R35

2,200

3,000

Date ItemPost.Ref. Debit Credit

Mar. 2

27

2010

2,200

5,200

Balance

Name: Accessories By Claire

R35 1,750 1,750

Date ItemPost.Ref. Debit Credit

Mar. 62010

Balance

Name: RapZone

Date Account DebitedPost.Ref.

Accts. Rec. Dr.Fees Earned Cr.

Balance

R35 9,600 9,600

9,600

Date ItemPost.Ref. Debit Credit

Mar. 312010

3,400

13,000

Debit Credit

Balance

Account No. 41Account Fees Earned

Balance

✓

R35 2,650

3,400

6,050

Date ItemPost.Ref. Debit Credit

Mar. 1

18

2010

Balance

Name: Web Cantina

Revenue Journal

Mar.2010

2

6

18

27

31

General Ledger Accounts Receivable Subsidiary Ledger

2,200

1,750

2,650

3,000

9,600

(12) (41)

✓

✓

✓

✓

Page 35

InvoiceNo.

Accessories By Claire

RapZone

Web Cantina

Accessories By Claire

615

616

617

618

Exhibit 3

Revenue Journal and Postings

208 Chapter 5 Accounting Systems

To illustrate, Exhibit 3 shows that a check mark (✓) has been inserted in the Post. Ref. col-umn next to Accessories By Claire in the revenue journal to indicate that the $2,200 hasbeen posted.

4. A single monthly total is posted to Accounts Receivable and Fees Earned in thegeneral ledger. This total is equal to the sum of the month’s debits to the individualaccounts in the subsidiary ledger. It is posted in the general ledger as a debit toAccounts Receivable and a credit to Fees Earned, as shown in Exhibit 3. Theaccounts receivable account number (12) and the fees earned account number (41)are then inserted below the total in the revenue journal to indicate that the postingis completed.

To illustrate, Exhibit 3 shows the monthly total of $9,600 was posted as a debit to AccountsReceivable (12) and as a credit to Fees Earned (41).

Exhibit 3 illustrates the efficiency gained by using the revenue journal rather thanthe general journal. Specifically, all of the transactions for fees earned during the monthare posted to the general ledger only once—at the end of the month.

Example Exercise 5-1 Revenue JournalThe following revenue transactions occurred during December:

Dec. 5. Issued Invoice No. 302 to Butler Company for services provided on account, $5,000.9. Issued Invoice No. 303 to JoJo Enterprises for services provided on account, $2,100.

15. Issued Invoice No. 304 to Double D Inc. for services provided on account, $3,250.

Record these transactions in a revenue journal as illustrated in Exhibit 2.

Follow My Example 5-1

REVENUE JOURNAL

Accts. Rec. Dr. Date Invoice No. Account Debited Post. Ref. Fees Earned Cr.

Dec. 5 302 Butler Company 5,0009 303 JoJo Enterprises 2,100

15 304 Double D Inc. 3,250

For Practice: PE 5-1A, PE 5-1B

2

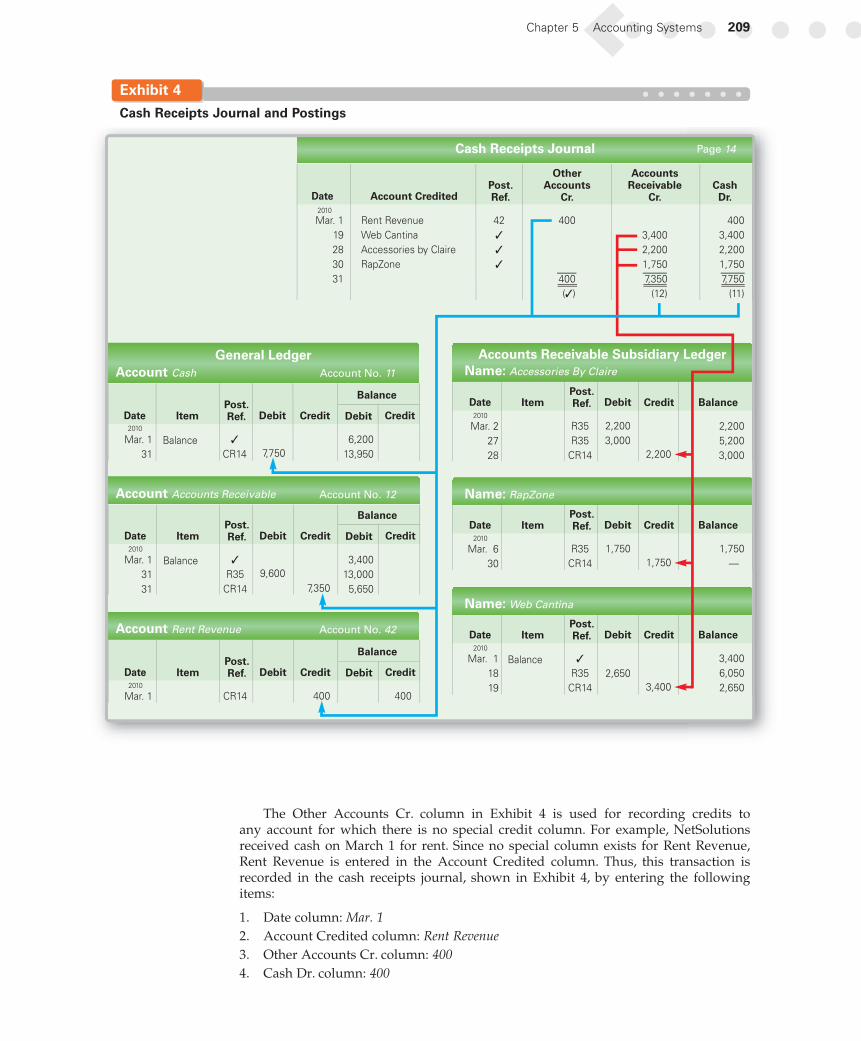

Cash Receipts JournalAll transactions that involve the receipt of cash are recorded in a cash receipts journal.The cash receipts journal for NetSolutions is shown in Exhibit 4.

The cash receipts journal shown in Exhibit 4 has a Cash Dr. column. The kinds of trans-actions in which cash is received and how often they occur determine the titles of the othercolumns. For example, NetSolutions often receives cash from customers on account. Thus,the cash receipts journal in Exhibit 4 has an Accounts Receivable Cr. column.

To illustrate, on March 28 Accessories By Claire made a payment of $2,200 on itsaccount. This transaction is recorded in the cash receipts journal, shown in Exhibit 4, byentering the following items:

1. Date column: Mar. 282. Account Credited column: Accessories By Claire3. Accounts Receivable Cr. column: 2,2004. Cash Dr. column: 2,200

Chapter 5 Accounting Systems 209

The Other Accounts Cr. column in Exhibit 4 is used for recording credits toany account for which there is no special credit column. For example, NetSolutionsreceived cash on March 1 for rent. Since no special column exists for Rent Revenue,Rent Revenue is entered in the Account Credited column. Thus, this transaction isrecorded in the cash receipts journal, shown in Exhibit 4, by entering the followingitems:

1. Date column: Mar. 12. Account Credited column: Rent Revenue3. Other Accounts Cr. column: 4004. Cash Dr. column: 400

Exhibit 4

Cash Receipts Journal and Postings

R35

R35

CR14

2,200

3,000

Date ItemPost.Ref. Debit Credit

Mar. 2

27

28

2010

2,200

5,200

3,0002,200

Balance

Name: Accessories By Claire

R35

CR14

1,750 1,750

— 1,750

Date ItemPost.Ref. Debit Credit

Mar. 6

30

2010

Balance

Name: RapZone

Date Account CreditedPost.Ref.

OtherAccounts

Cr.

AccountsReceivable

Cr.CashDr.

Balance ✓

R35

CR14

2,650

3,400

6,050

2,6503,400

Date ItemPost.Ref. Debit Credit

Mar. 1

18

19

2010

Balance

Name: Web Cantina

Cash Receipts Journal

Rent Revenue

Web Cantina

Accessories by Claire

RapZone

2010

Mar. 1

19

28

30

31

Accounts Receivable Subsidiary Ledger

3,400

2,200

1,750

7,350

(12)

400

3,400

2,200

1,750

7,750

(11)

42

✓

✓

✓

400

400

(✓)

Page 14

✓

R35

CR14

9,600

Date ItemPost.Ref. Debit Credit

Mar. 1

31

31

2010

7,350

3,400

13,000

5,650

Debit Credit

Balance

Account No. 12Account Accounts Receivable

Balance

CR14 400 400

Date ItemPost.Ref. Debit Credit

Mar. 12010

Debit Credit

Balance

Account No. 42Account Rent Revenue

✓

CR14

Date ItemPost.Ref. Debit Credit

Mar. 1

31

2010

Debit Credit

Balance

Account No. 11Account Cash

Balance7,750

6,200

13,950

General Ledger

210 Chapter 5 Accounting Systems

At the end of the month, all of the amount columns are totaled. The debits mustequal the credits. If the debits do not equal the credits, an error has occurred. Before pro-ceeding further, the error must be found and corrected.

The process of posting from the cash receipts journal, shown in Exhibit 4, is as follows:

1. Each transaction involving the receipt of cash on account is posted individually toa customer account in the accounts receivable subsidiary ledger. Postings to cus-tomer accounts should be made on a regular basis. In this way, the customer’saccount will show a current balance.

To illustrate, Exhibit 4 shows on March 19 the receipt of $3,400 on account from WebCantina. The posting of the $3,400 credit to Web Cantina in the accounts receivable sub-sidiary ledger is shown in Exhibit 4. After the posting, Web Cantina has a debit balance of$2,650. If a posting results in a customer’s account with a credit balance, the credit balanceis indicated by an asterisk or parentheses in the Balance column. If an account’s balance iszero, a line may be drawn in the Balance column.

2. To provide a trail of the entries posted to the subsidiary ledger, the source of theseentries is indicated in the Posting Reference column of each account by inserting theletter CR (for cash receipts journal) and the page number of the cash receipts journal.

To illustrate, Exhibit 4 shows that after $3,400 is posted to Web Cantina’s account in theaccounts receivable subsidiary ledger, CR14 is inserted into the Post. Ref. column of the account.

3. To indicate that the transaction has been posted to the accounts receivable sub-sidiary ledger, a check mark (✓) is inserted in the Posting Reference column of thecash receipts journal, as shown in Exhibit 4.

To illustrate, Exhibit 4 shows that a check mark (✓) has been inserted in the Post. Ref. col-umn next to Web Cantina to indicate that the $3,400 has been posted.

4. A single monthly total of the Accounts Receivable Cr. column is posted to theaccounts receivable general ledger account. This is the total cash received onaccount and is posted as a credit to Accounts Receivable. The accounts receivableaccount number (12) is then inserted below the Accounts Receivable Cr. column toindicate that the posting is complete.

To illustrate, Exhibit 4 shows the monthly total of $7,350 was posted as a credit to AccountsReceivable (12).

5. A single monthly total of the Cash Dr. column is posted to the cash general ledgeraccount. This is the total cash received during the month and is posted as a debit toCash. The cash account number (11) is then inserted below the Cash Dr. column toindicate that the posting is complete.

To illustrate, Exhibit 4 shows the monthly total of $7,750 was posted as a debit to Cash (11).6. The accounts listed in the Other Accounts Cr. column are posted on a regular basis

as a separate credit to each account. The account number is then inserted in thePost. Ref. column to indicate that the posting is complete. Because accounts in theOther Accounts Cr. column are posted individually, a check mark is placed belowthe column total at the end of the month to show that no further action is needed.

To illustrate, Exhibit 4 shows that $400 was posted as a credit to Rent Revenue (42). Also,at the end of the month a check mark (✓) is entered below the Other Accounts Cr. column toindicate that no further action is needed.

Accounts Receivable Control Account and Subsidiary LedgerAfter all posting has been completed for the month, the balances in the accounts receiv-able subsidiary ledger should be totaled. This total should then be compared with thebalance of the accounts receivable controlling account in the general ledger. If the con-trolling account and the subsidiary ledger do not agree, an error has occurred. Beforeproceeding further, the error must be located and corrected.

Chapter 5 Accounting Systems 211

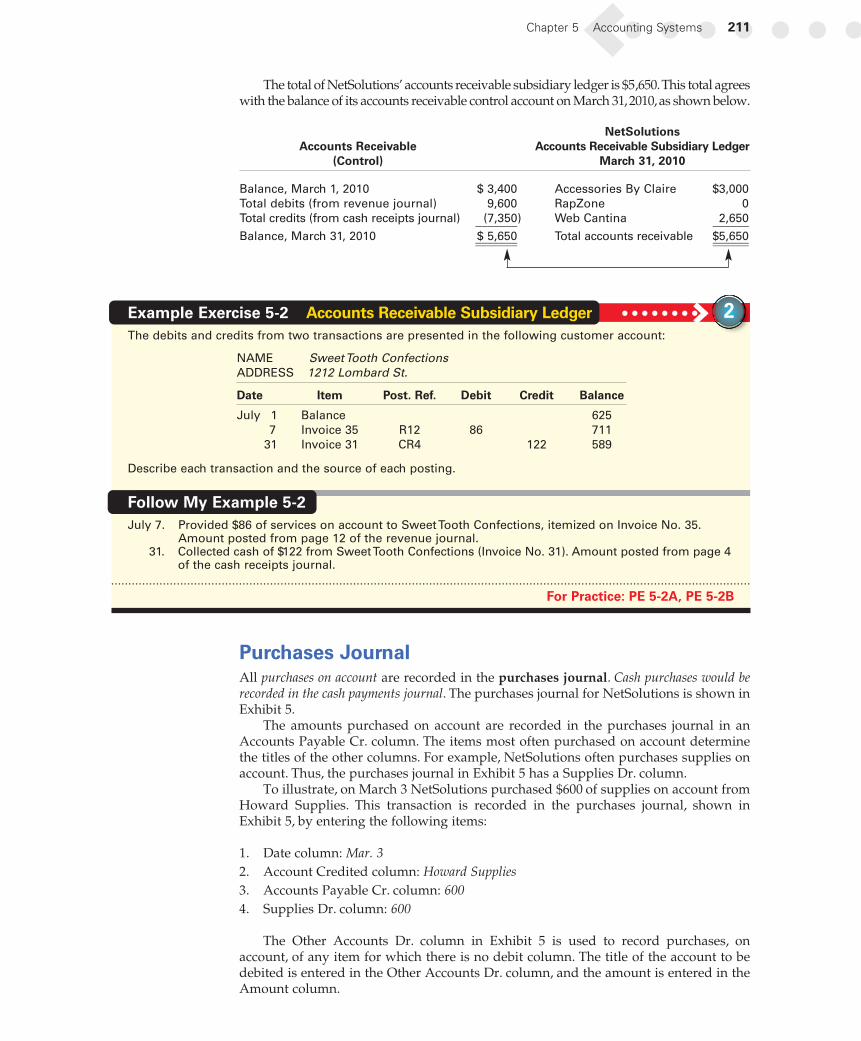

The total of NetSolutions’ accounts receivable subsidiary ledger is $5,650.This total agreeswith the balance of its accounts receivable control account on March 31,2010,as shown below.

NetSolutionsAccounts Receivable Accounts Receivable Subsidiary Ledger

(Control) March 31, 2010

Balance, March 1, 2010 $ 3,400 Accessories By Claire $3,000Total debits (from revenue journal) 9,600 RapZone 0Total credits (from cash receipts journal) (7,350) Web Cantina 2,650_______ _______Balance, March 31, 2010 $ 5,650 Total accounts receivable $5,650_______ ______________ _______

Example Exercise 5-2 Accounts Receivable Subsidiary LedgerThe debits and credits from two transactions are presented in the following customer account:

NAME Sweet Tooth Confections ADDRESS 1212 Lombard St.

Date Item Post. Ref. Debit Credit Balance

July 1 Balance 6257 Invoice 35 R12 86 711

31 Invoice 31 CR4 122 589

Describe each transaction and the source of each posting.

Follow My Example 5-2July 7. Provided $86 of services on account to Sweet Tooth Confections, itemized on Invoice No. 35.

Amount posted from page 12 of the revenue journal.31. Collected cash of $122 from Sweet Tooth Confections (Invoice No. 31). Amount posted from page 4

of the cash receipts journal.

For Practice: PE 5-2A, PE 5-2B

2

Purchases JournalAll purchases on account are recorded in the purchases journal. Cash purchases would berecorded in the cash payments journal. The purchases journal for NetSolutions is shown inExhibit 5.

The amounts purchased on account are recorded in the purchases journal in anAccounts Payable Cr. column. The items most often purchased on account determinethe titles of the other columns. For example, NetSolutions often purchases supplies onaccount. Thus, the purchases journal in Exhibit 5 has a Supplies Dr. column.

To illustrate, on March 3 NetSolutions purchased $600 of supplies on account fromHoward Supplies. This transaction is recorded in the purchases journal, shown inExhibit 5, by entering the following items:

1. Date column: Mar. 32. Account Credited column: Howard Supplies3. Accounts Payable Cr. column: 6004. Supplies Dr. column: 600

The Other Accounts Dr. column in Exhibit 5 is used to record purchases, onaccount, of any item for which there is no debit column. The title of the account to bedebited is entered in the Other Accounts Dr. column, and the amount is entered in theAmount column.

212 Chapter 5 Accounting Systems

To illustrate, on March 12 NetSolutions purchased office equipment on accountfrom Jewett Business Systems for $2,800. This transaction is recorded in the purchasesjournal shown in Exhibit 5 by entering the following items:

1. Date column: Mar. 12

2. Account Credited column: Jewett Business Systems

3. Accounts Payable Cr. column: 2,800

4. Other Accounts Dr. column: Office Equipment

5. Amount column: 2,800

Exhibit 5

Purchases Journal and Postings

P11

P11

P11

P11

P11

Date ItemPost.Ref. Debit Credit

Mar. 7

19

2010

420

1,870420

1,450

Balance

Name: Donnelly Supplies

✓ 1,230

Date ItemPost.Ref. Debit Credit

Mar. 12010

Balance

Name: Grayco Supplies

Date Account CreditedPost.Ref.

AccountsPayable

Cr.Supplies

Dr.

OtherAccounts

Dr. Amount

600

1,560600

960

Date ItemPost.Ref. Debit Credit

Mar. 3

27

2010

Balance

Name: Howard Supplies

Mar.2010

3

7

12

19

27

31

Balance

2,8002,800

Date ItemPost.Ref. Debit Credit

Mar. 122010

Balance

Name: Jewett Business Systems

Accounts Payable Subsidiary Ledger

✓

✓

✓

✓

✓

Page 11

600

420

2,800

1,450

960

6,230

(21)

600

420

1,450

960

3,430

(14)

Post.Ref.

Purchases Journal

Howard Supplies

Donnelly Supplies

Jewett Business Systems

Donnelly Supplies

Howard Supplies

Office Equipment 18 2,800

2,800

(✓)

✓

P11 6,230

1,230

7,460

Date ItemPost.Ref. Debit DebitCredit Credit

Mar. 1

31

2010

Balance

Account No. 21Account Accounts Payable

Balance

General Ledger

✓

P11 3,430

2,500

5,930

Date ItemPost.Ref. Debit Credit

Mar. 1

31

2010

Account No. 14Account Supplies

Balance

Debit Credit

Balance

✓

P11 2,800

2,500

5,300

Date ItemPost.Ref. Debit Credit

Mar. 1

12

2010

Account No. 18Account Office Equipment

Balance

Debit Credit

Balance

Chapter 5 Accounting Systems 213

At the end of the month, all of the amount columns are totaled. The debits mustequal the credits. If the debits do not equal the credits, an error has occurred. Beforeproceeding further, the error must be found and corrected.

The process of posting from the purchases journal shown in Exhibit 5 is as follows:

1. Each transaction involving a purchase on account is posted individually to a cred-itor’s account in the accounts payable subsidiary ledger. Postings to creditoraccounts should be made on a regular basis. In this way, the creditor’s account willshow a current balance.

To illustrate, Exhibit 5 shows on March 3 the purchase of supplies of $600 on account fromHoward Supplies. The posting of the $600 credit to Howard Supplies accounts payablesubsidiary ledger is shown in Exhibit 5. After the posting, Howard Supplies has a creditbalance of $600.

2. To provide a trail of the entries posted to the subsidiary and general ledger, the sourceof these entries is indicated in the Posting Reference column of each account by insert-ing the letter P (for purchases journal) and the page number of the purchases journal.

To illustrate, Exhibit 5 shows that after $600 is posted to Howard Supplies’ account, P11is inserted into the Post. Ref. column of the account.

3. To indicate that the transaction has been posted to the accounts payable subsidiaryledger, a check mark (✓) is inserted in the Posting Reference column of the pur-chases journal, as shown in Exhibit 5.

To illustrate, Exhibit 5 shows that a check mark (✓) has been inserted in the Post. Ref. col-umn next to Howard Supplies to indicate that the $600 has been posted.

4. A single monthly total of the Accounts Payable Cr. column is posted to the accountspayable general ledger account. This is the total amount purchased on account andis posted as a credit to Accounts Payable. The accounts payable account number (21) isthen inserted below the Accounts Payable Cr. column to indicate that the posting iscomplete.

To illustrate, Exhibit 5 shows the monthly total of $6,230 was posted as a credit to AccountsPayable (21).

5. A single monthly total of the Supplies Dr. column is posted to the supplies generalledger account. This is the total supplies purchased on account during the monthand is posted as a debit to Supplies. The supplies account number (14) is theninserted below the Supplies Dr. column to indicate that the posting is complete.

To illustrate, Exhibit 5 shows the monthly total of $3,430 was posted as a debit to Supplies (14).6. The accounts listed in the Other Accounts Dr. column are posted on a regular basis

as a separate debit to each account. The account number is then inserted in the Post.Ref. column to indicate that the posting is complete. Because accounts in the OtherAccounts Dr. column are posted individually, a check mark is placed below the col-umn total at the end of the month to show that no further action is needed.

To illustrate, Exhibit 5 shows that $2,800 was posted as a debit to Office Equipment (18).Also, at the end of the month, a check mark (✓) is entered below the Amount column to indi-cate that no further action is needed.

Example Exercise 5-3 Purchases Journal The following purchase transactions occurred during October for Helping Hand Cleaners:

Oct. 11. Purchased cleaning supplies for $235, on account, from General Supplies. 19. Purchased cleaning supplies for $110, on account, from Hubble Supplies. 24. Purchased office equipment for $850, on account, from Office Warehouse.

Record these transactions in a purchases journal as illustrated at the top of Exhibit 5.

2

(continued)

214 Chapter 5 Accounting Systems

Follow My Example 5-3

PURCHASES JOURNAL

Accounts Cleaning OtherPost. Payable Supplies Accounts Post.

Date Account Credited Ref. Cr. Dr. Dr. Ref. Amount

Oct. 11 General Supplies 235 23519 Hubble Supplies 110 11024 Office Warehouse 850 Office Equipment 850

For Practice: PE 5-3A, PE 5-3B

Cash Payments JournalAll transactions that involve the payment of cash are recorded in a cash payments jour-nal. The cash payments journal for NetSolutions is shown in Exhibit 6.

The cash payments journal shown in Exhibit 6 has a Cash Cr. column. The kinds oftransactions in which cash is paid and how often they occur determine the titles of theother columns. For example, NetSolutions often pays cash to creditors on account. Thus,the cash payments journal in Exhibit 6 has an Accounts Payable Dr. column. In addi-tion, NetSolutions makes all payments by check. Thus, a check number is entered foreach payment in the Ck. No. (Check Number) column to the right of the Date column.The check numbers are helpful in controlling cash payments and provide a useful cross-reference.

To illustrate, on March 15 NetSolutions issued Check No. 151 for $1,230 to GraycoSupplies for payment on its account. This transaction is recorded in the cash paymentsjournal shown in Exhibit 6 by entering the following items:

1. Date column: Mar. 152. Ck. No. column: 1513. Account Debited column: Grayco Supplies4. Accounts Payable Dr. column: 1,2305. Cash Cr. column: 1,230

The Other Accounts Dr. column in Exhibit 6 is used for recording debits to anyaccount for which there is no special debit column. For example, NetSolutions issuedCheck No. 150 on March 2 for $1,600 in payment of the March rent. This transaction isrecorded in the cash payments journal, shown in Exhibit 6, by entering the followingitems:

1. Date column: Mar. 22. Ck. No. column: 1503. Account Debited column: Rent Expense4. Other Accounts Dr. column: 1,6005. Cash Cr. column: 1,600

At the end of the month, all of the amount columns are totaled. The debits mustequal the credits. If the debits do not equal the credits, an error has occurred. Before pro-ceeding further, the error must be found and corrected.

The process of posting from the cash payments journal, shown in Exhibit 6, is asfollows:

1. Each transaction involving the payment of cash on account is posted individuallyto a creditor account in the accounts payable subsidiary ledger. Postings to creditoraccounts should be made on a regular basis. In this way, the creditor’s account willshow a current balance.

Chapter 5 Accounting Systems 215

To illustrate, Exhibit 6 shows on March 22 the payment of $420 on account to DonnellySupplies. The posting of the $420 debit to Donnelly Supplies in the accounts payable sub-sidiary ledger is shown in Exhibit 6. After the posting, Donnelly Supplies has a credit bal-ance of $1,450.

2. To provide a trail of the entries posted to the subsidiary and general ledger, thesource of these entries is indicated in the Posting Reference column of each account

P11

P11

CP7 420

Date ItemPost.Ref. Debit Credit

Mar. 7

19

22

2010

420

1,870

1,450

420

1,450

Balance

Name: Donnelly Supplies

✓

CP7 1,230

1,230

—

Date ItemPost.Ref. Debit Credit

Mar. 1

15

2010

Balance

Name: Grayco Supplies

Date Account DebitedPost.Ref.

OtherAccounts

Dr.

AccountsPayable

Dr.Cash

Cr.Ck. No.

Balance

P11

CP7 2,800

2,800

— 2,800

Date ItemPost.Ref. Debit Credit

Mar. 12

21

2010

Balance

Name: Jewett Business Systems

P11

P11

CP7 600

600

1,560

960

600

960

Date ItemPost.Ref. Debit Credit

Mar. 3

27

31

2010

Balance

Name: Howard Supplies

Cash Payments Journal

Mar.2010

Accounts Payable Subsidiary Ledger

1,230

2,800

420

600

5,050

(21)

1,600

1,230

2,800

420

1,050

600

7,700

(11)

52

✓

✓

✓

54

✓

1,600

1,050

2,650

(✓)

Page 7

Rent Expense

Grayco Supplies

Jewett Business Systems

Donnelly Supplies

Utilities Expense

Howard Supplies

2

15

21

22

30

31

31

150

151

152

153

154

155

Date ItemPost.Ref. Debit Credit

2010

Balance

Debit Credit

Account No. 52Account Rent Expense

Mar. 2 CP7 1,600 1,600

Date ItemPost.Ref. Debit Credit

2010

BalanceDebit Credit

Account No. 54Account Utilities Expense

Mar. 30 CP7 1,050 1,050

6,230

1,230

7,460

2,410

Date ItemPost.Ref. Debit Credit Debit Credit

2010

Balance

Balance

General Ledger

Mar. 1

31

31

✓

P11

CP7 5,050

7,700

6,200

13,950

6,250

Date ItemPost.Ref. Debit Credit

2010

BalanceDebit Credit

Account No. 11Account Cash

BalanceMar. 1

31

31

✓

CR14

CP77,750

Account No. 21Account Accounts Payable

Exhibit 6

Cash Payments Journal and Postings

216 Chapter 5 Accounting Systems

by inserting the letter CP (for cash payments journal) and the page number of thecash payments journal.

To illustrate, Exhibit 6 shows that after $420 is posted to Donnelly Supplies’ account, CP7is inserted into the Post. Ref. column of the account.

3. To indicate that the transaction has been posted to the accounts payable subsidiaryledger, a check mark (✓) is inserted in the Posting Reference column of the cashpayments journal, as shown in Exhibit 6.

To illustrate, Exhibit 6 shows that a check mark (✓) has been inserted in the Post. Ref. col-umn next to Donnelly Supplies to indicate that the $420 has been posted.

4. A single monthly total of the Accounts Payable Dr. column is posted to the accountspayable general ledger account. This is the total cash paid on account and is postedas a debit to Accounts Payable. The accounts payable account number (21) is theninserted below the Accounts Payable Dr. column to indicate that the posting iscomplete.

To illustrate, Exhibit 6 shows the monthly total of $5,050 was posted as a debit to AccountsPayable (21).

5. A single monthly total of the Cash Cr. column is posted to the cash general ledgeraccount. This is the total cash payments during the month and is posted as a creditto Cash. The cash account number (11) is then inserted below the Cash Cr. columnto indicate that the posting is complete.

To illustrate, Exhibit 6 shows the monthly total of $7,700 was posted as a credit to Cash (11).6. The accounts listed in the Other Accounts Dr. column are posted on a regular

basis as a separate debit to each account. The account number is then inserted inthe Post. Ref. column to indicate that the posting is complete. Because accounts inthe Other Accounts Dr. column are posted individually, a check mark is placedbelow the column total at the end of the month to show that no further action isneeded.

To illustrate, Exhibit 6 shows that $1,600 was posted as a debit to Rent Expense (52) and $1,050was posted as a debit to Utilities Expense (54). Also, at the end of the month, a check mark (✓)is entered below the Other Accounts Dr. column to indicate that no further action is needed.

Accounts Payable Control Account and Subsidiary LedgerAfter all posting has been completed for the month, the balances in the accountspayable subsidiary ledger should be totaled. This total should then be compared withthe balance of the accounts payable controlling account in the general ledger. If the con-trolling account and the subsidiary ledger do not agree, an error has occurred. Beforeproceeding, the error must be located and corrected.

The total of NetSolutions’ accounts payable subsidiary ledger is $2,410. This totalagrees with the balance of its accounts payable control account on March 31, 2010, asshown below.

NetSolutions Accounts Payable Accounts Payable Subsidiary Ledger

(Control) March 31, 2010

Balance, March 1, 2010 $ 1,230 Donnelly Supplies $1,450Total credits (from purchases journal) 6,230 Grayco Supplies 0Total debits Howard Supplies 960

(from cash payments journal) (5,050) Jewett Business Systems 0_______ ______Balance, March 31, 2010 $ 2,410 Total $2,410_______ _____________ ______

Chapter 5 Accounting Systems 217

Adapting Manual Accounting SystemsIn the prior sections of this chapter, we illustrated subsidiary ledgers and special jour-nals that are common for small businesses. Many businesses use subsidiary ledgers forother accounts, in addition to Accounts Receivable and Accounts Payable. Also, specialjournals are often adapted or modified in practice.

Additional Subsidiary LedgersSubsidiary ledgers are often used for accounts that consist of a large number of indi-vidual items. For example, businesses often use a subsidiary equipment ledger to keeptrack of each item of equipment purchased, its cost, location, and other data. Suchledgers are similar to the accounts receivable and accounts payable subsidiary ledgersillustrated in this chapter.

Modified Special JournalsA business may modify its special journals by adding one or more columns for record-ing transactions that occur frequently. For example, a business may collect sales taxesthat must be remitted to taxing authorities. Thus, the business may add a special col-umn for Sales Taxes Payable Cr. in its revenue journal, as shown below.

Example Exercise 5-4 Accounts Payable Subsidiary Ledger

The debits and credits from two transactions are presented in the following creditor’s (supplier’s) account:

NAME Lassiter Services Inc. ADDRESS 301 St. Bonaventure Ave.

Date Item Post. Ref. Debit Credit Balance

Aug. 1 Balance 32012 Invoice No. 101 CP36 200 12022 Invoice No. 106 P16 140 260

Describe each transaction and the source of each posting.

Follow My Example 5-4Aug. 12. Paid $200 to Lassiter Services Inc. on account (Invoice No. 101). Amount posted from page 36 of

the cash payments journal.22. Purchased $140 of services on account from Lassiter Services Inc. itemized on Invoice No. 106.

Amount posted from page 16 of the purchases journal.

For Practice: PE 5-4A, PE 5-4B

2

Describe

and give

examples of other

subsidiary ledgers

and modified special

journals.

3

Revenue Journal

Nov. 2

3

2010

Page 40

FeesEarned

Cr.

Accts.Rec.Dr.

Post.Ref.

Sales TaxesPayable

Cr.DateInvoice

No. Account Debited

270

66

4,500

1,100

4,770

1,166

Litten Co.

Kauffman Supply Co.

842

843✓

✓

Other examples of how special journals may be modified for different types of busi-nesses include the following:

• Farm—The purchases journal may be modified to include columns for various typesof seeds (corn, wheat), livestock (cows, hogs, sheep), fertilizer, and fuel.

218 Chapter 5 Accounting Systems

• Automobile Repair Shop—The revenue journal may be modified to includecolumns for each major type of repair service. In addition, columns for warrantyrepairs, credit card charges, and sales taxes may be added.

• Hospital—The cash receipts journal may be modified to include columns for receiptsfrom patients on account, from Blue Cross/Blue Shield or other major insurancereimbursers, and Medicare.

• Movie Theater—The cash receipts journal may be modified to include columns forrevenues from admissions, arcade, and concession sales.

• Restaurant—The purchases journal may be modified to include columns for food,linen, silverware and glassware, and kitchen supplies.

Regardless of how a special journal is modified, the basic procedures discussed inthis chapter apply. For example, the columns in special journals are normally totaled atperiodic intervals. The totals of the debit and credit columns are then compared to ver-ify their equality before the totals are posted to the general ledger accounts.

Example Exercise 5-5 Modified Revenue Journal The state of Tennessee has a 7% sales tax. Volunteer Services, Inc., a Tennessee company, had two revenuetransactions as follows:

Aug. 3. Issued Invoice No. 58 to Helena Company for services provided on account, $1,400, plus sales tax.19. Issued Invoice No. 59 to K-Jam Enterprises for services provided on account, $900, plus sales tax.

Record these transactions in a revenue journal as illustrated in this section.

Follow My Example 5-5

REVENUE JOURNAL

Sales Taxes Invoice Post. Accts. Rec. Fees Earned Payable

Date No. Account Debited Ref. Dr. Cr. Cr.

Aug. 3 58 Helena Company 1,498 1,400 98*

19 59 K-Jam Enterprises 963 900 63**

* 98 � 1,400 � 7%

** 63 � 900 � 7%

For Practice: PE 5-5A, PE 5-5B

3

Computerized Accounting SystemsComputerized accounting systems are widely used by even the smallest of companies.Computerized accounting systems have the following three main advantages overmanual systems:

1. Computerized systems simplify the record-keeping process in that transactions arerecorded in electronic forms and, at the same time, posted electronically to generaland subsidiary ledger accounts.

2. Computerized systems are generally more accurate than manual systems.

3. Computerized systems provide management with current account balance infor-mation to support decision making, since account balances are posted as the trans-actions occur.

The popular QuickBooks® accounting software for small- to medium-sized businessesis used to illustrate a computerized accounting system for NetSolutions. To simplify,the illustration is limited to transactions involving the earning of revenue on account

Describe and

illustrate the

use of a computerized

accounting system.

4

Chapter 5 Accounting Systems 219

and the subsequent recording of cash collections. Exhibit 7 illustrates the use ofQuickBooks® for NetSolutions to record transactions as follows:

Step 1. Record fees by completing an electronic invoice form.

Sales transactions are entered onto the computer screen using an electronicinvoice form. The electronic form appears like a paper form with spaces, orfields, to input transaction data. The data spaces may have pull-down lists toease data entry. After the form is completed, it is printed out and mailed, or e-mailed, to the customer.

To illustrate, on March 2, NetSolutions earned $2,200 on account from Accessories ByClaire. As shown in Exhibit 7, Invoice No. 615 was created using an electronic form.Upon submitting the invoice form, QuickBooks® automatically posts a $2,200 debit tothe Accessories By Claire customer account and the credit to Fees Earned. An invoiceis also printed for mailing to Accessories By Claire.

Step 2. Record collection of payment by completing a “receive payment” form.

Upon collection from the customer, a “receive payment” electronic form isopened and completed. As with the “invoice form,” data are input into thevarious spaces directly or by using pull-down lists.

To illustrate, a $2,200 payment was collected from Accessories By Claire on March 28.As shown in Exhibit 7, the $2,200 was applied to Invoice No. 615, as shown bythe check mark (✓) next to the March 2 date at the bottom of the form. As shownat the bottom of the form, the March 27 invoice of $3,000 remains uncollected. Whenthe screen is completed, a debit of $2,200 is automatically posted to the cash account,and a credit for $2,200 is posted to the Accessories By Claire account. This causes thebalance of the Accessories By Claire account to be reduced from $5,200 to $3,000.

Step 3. Prepare reports.

At any time, managers may request reports from the software. Three suchreports include the following:

1. “Accounts Receivable Subsidiary Ledger” lists as of a specific date theaccounts receivable balances by customer.

To illustrate, the Accounts Receivable Subsidiary Ledger shown in Exhibit 7 forNetSolutions was generated as of March 31, 2010. The total of the AccountsReceivable Subsidiary Ledger of $5,650 agrees with the accounts receivablesubsidiary balance total we illustrated using a manual system for NetSolutions onpage 211.

ACCOUNTING SYSTEMS AND PROFITMEASUREMENT

A Greek restaurant owner in Canada had his own systemof accounting. He kept his accounts payable in a cigar box onthe left-hand side of his cash register, his daily cash returnsin the cash register, and his receipts for paid bills in anothercigar box on the right. A truly “manual” system.

When his youngest son graduated as an accountant,he was appalled by his father’s primitive methods. “I don’t

know how you can run a business that way,” he said.“How do you know what your profits are?”

“Well, son,” the father replied, “when I got off the boatfrom Greece, I had nothing but the pants I was wearing.Today, your brother is a doctor. You are an accountant. Yoursister is a speech therapist. Your mother and I have a nicecar, a city house, and a country home. We have a good busi-ness, and everything is paid for . . . .”

“So, you add all that together, subtract thepants, and there’s your profit!”

220 Chapter 5 Accounting Systems

1. Record fees by completing an electronic invoice form.

Mail invoiceto customer.

2. Record collection of payment by completing a “receive payment” form.

3. Prepare reports.

Accessories By Claire244 Grand Ave.Des Moines, IA 50310

37¢

Receive payment

Automatic Postings Dr. Cr.Accounts Receivable— Accessories By Claire Fees Earned

Cash Accounts Receivable— Accessories By Claire

Net 302,200

2,200

2,200

2,200

Dr. Cr.

03/02/2010

Exhibit 7

Revenue and Cash Receipts in QuickBooks®

Chapter 5 Accounting Systems 221

2. “Fees Earned by Customer” lists revenue by customer for the month. Thisis similar to the revenue journal in the manual system. It is created from theelectronic invoice form used in step 1.

To illustrate, the Fees Earned by Customer shown in Exhibit 7 for NetSolutions isfor the month of March 2010. The total of the Fees Earned by Customer of $9,600agrees with the total of the revenue journal we illustrated using a manual systemfor NetSolutions in Exhibits 2 and 3.

3. “Cash Receipts” lists the cash receipts during the month. This report is similarto the cash receipts journal in the manual system.

To illustrate, the Cash Receipts shown in Exhibit 7 for NetSolutions is for themonth of March 2010. The total of the Cash Receipts of $7,750 agrees with the totalof the Cash Dr. column of the cash receipts journal we illustrated using a manualsystem for NetSolutions in Exhibit 4.

The computer does not make journalizing, posting, and mathematical errors. Forexample, a computerized accounting system will not process a transaction unless thetotal debits for the transaction equal the total credits for a transaction. Instead, an errorscreen will notify the user that the transaction data must be corrected. Likewise, thecomputer will not make posting or mathematical errors.

The discovery and correction of errors, however, is important in a computerizedsystem. Errors that can occur in a computerized system include the following:

1. Failing to record a transaction.

2. Recording a transaction more than once.

3. Recording a transaction in incorrect accounts.

4. Entering an incorrect number in both the debit and credit parts of the transaction.

The preceding errors are often discovered by reviewing the computerized trialbalance for any account balances that are unusual or unreasonable. For example, acredit balance for Supplies indicates that an error has occurred. In addition, errors areoften discovered when parties affected by the incorrect transaction complain. Forexample, an employee would likely complain about a missed or incorrect payroll check.

Incorrectly recorded transactions can be corrected in computerized accountingsystems by deleting the incorrect entries and replacing them with correct entries.When a transaction is deleted in a computerized system, the postings to theaccounts are automatically deleted. This also removes the effect of the incorrect entryfrom the accounts. Alternatively, correcting entries may also be used as described inChapter 2.

In this section, we illustrated revenue and cash receipt transactions forNetSolutions using QuickBooks® accounting software. Similar illustrations could beprovided for purchases and cash payment transactions. A complete illustration of acomputerized accounting system is beyond the scope of this text. However, this chap-ter provides a solid foundation for applying accounting system concepts in either amanual or a computerized system.

ONLINE FRAUD

Fraud accounted for over $3.6 billion in e-commerce lossesin 2007, or approximately 1.4% of all online revenue. Asa result, online retailers are using address verificationand credit card security codes as additional securitymeasures. Address verification matches the customer’s

address to the address on file with the credit cardcompany, while the security code is the additional four-digit code designed to reduce fictitious credit card trans-actions.

Source: 9th Annual CyberSource fraud survey, CyberSource,November 13, 2007.

222 Chapter 5 Accounting Systems

E-CommerceThe U.S. Census Bureau indicates that e-commerce sales are growing at a rate of 21%per year to over $120 billion in retail sales. This represents over 3% of all retail sales.1

Using the Internet to perform business transactions is termed e-commerce. When trans-actions are between a company and a consumer, it is termed B2C (business-to-consumer) e-commerce. Examples of companies engaged in B2C e-commerce includeAmazon.com, Priceline.com Inc., and Dell Inc.

The B2C business allows consumers to shop and receive goods at home, rather thangoing to the store. For example, Whirlpool Corporation allows consumers to use itsWeb site to order appliances, selecting color and other features. After paying with acredit card, customers can receive delivery of the appliance from the Whirlpool factory.

When transactions are conducted between two companies, it is termed B2B(business-to-business) e-commerce. Examples of companies engaged in B2B e-commerceinclude Cisco Systems, Inc., an Internet equipment manufacturer, and Bristol-Myers Squibb Company (BMS) , a pharmaceutical company. BMS, for example, usese-commerce to purchase supplies and equipment from its suppliers. E-commercestreamlines purchases and payments by automating transactions and eliminatingpaperwork. BMS claims over $90 million in savings by placing its purchase/paymentcycle on the Internet.

The Internet creates opportunities for improving the speed and efficiency oftransactions. Many companies are realizing these benefits of using e-commerce asillustrated above. Three additional areas where the Internet is being used for businesspurposes are as follows:

1. Supply chain management (SCM): Internet applications to plan and coordinatesuppliers.

2. Customer relationship management (CRM): Internet applications to plan andcoordinate marketing and sales effort.

3. Product life-cycle management (PLM): Internet applications to plan and coordi-nate the product development and design process.

E-commerce also provides opportunities for faster business processes that operateat lower costs. New Internet applications are continually being introduced as theInternet develops into a preferred method of conducting business.

Describe

the basic

features of

e-commerce.

5

1 Estimated Quarterly U.S. Retail Sales: Total and E-commerce, U.S. Census Bureau, May 18, 2007.

A new trend is toward appli-cation service provider (ASP)software solutions wherebythe accounting system ismanaged and distributedover the Internet by a thirdparty. Under this model, thesoftware is “rented,” whileanalysis, design, and imple-mentation are largely pro-vided by the ASP vendor.

Chapter 5 Accounting Systems 223

Financial Analysis and InterpretationAccounting systems often use computers to collect, clas-sify, summarize, and report financial and operating infor-mation in many different ways. One way is to reportrevenue earned by different segments of business. A seg-ment of business may include regions, products or serv-ices, or customers. For example, Delta Air Lines uses theaccounting system to determine the amount of revenueearned by different regions, shown as follows from thenotes to its financial statements:

2006 2005(in millions) (in millions)

North America $12,931 $13,030

Trans Atlantic 2,997 2,255

Trans Pacific 164 150

Latin America 1,079 756_______ _______Total revenues $17,171 $16,191_______ ______________ _______

This regional information can be used to perform a hori-zontal analysis using 2005 for the base year, as illustratedin Chapter 2, as follows:

Increase

2006 2005 (Decrease)

(in millions) (in millions) Amount Percent

North America $12,931 $13,030 $ (99) �0.8%

Trans Atlantic 2,997 2,255 742 32.9

Trans Pacific 164 150 14 9.3

Latin America 1,079 756 323 42.7_______ _______ _____ ____Total revenues $17,171 $16,191 $980 6.1_______ _______ _____ ___________ _______ _____ ____

As can be seen from this analysis, Delta Air Linesincreased total revenue by 6.1% from 2005 to 2006.However, this increase came mostly from increases inTrans Atlantic (32.9%) and Latin America (42.7%) reve-nues. The domestic North America revenues actuallydeclined during the period.

In addition, a vertical analysis as shown in Chapter 3could also be performed on the segment disclosures asfollows:

2006 2005

Amount Percent Amount Percent(in millions) (in millions)

North America $12,931 75.3% $13,030 80.5%

Trans Atlantic 2,997 17.4 2,255 13.9

Trans Pacific 164 1.0 150 0.9

Latin America 1,079 6.3 756 4.7_______ ______ _______ ______Total $17,171 100.0% $16,191 100.0%_______ ______ _______ _____________ ______ _______ ______

This analysis shows that revenue of North America flightsdeclined from 80.5% of total revenue in 2005 to 75.3% oftotal revenue in 2006. Both the Trans Atlantic and LatinAmerica revenues as a percent of the total revenuesincreased during the two-year period. Both analyses to-gether indicate that Delta is benefiting from revenue growthin the Trans Atlantic and Latin America markets.

An accounting system is the methods andprocedures for collecting, classifying, summarizing,and reporting a business’s financial information.The three steps through which an accountingsystem evolves are: (1) analysis of informationneeds, (2) design of the system, and (3) implementation of the system design.

• Define an accounting system.

• Describe the three steps fordesigning an accounting sys-tem: (1) analysis, (2) design,and (3) implementation.

1 Define and describe an accounting system.

Key Points Key Learning OutcomesExample PracticeExercises Exercises

At a Glance 5

224

5-1 5-1A, 5-1B

5-2 5-2A, 5-2B

5-3 5-3A, 5-3B

5-4 5-4A, 5-4B

Subsidiary ledgers may be used to maintainseparate records for customers and creditors(vendors). A controlling account summarizes thesubsidiary ledger accounts. The sum of the sub-sidiary ledger must agree with the balance in therelated controlling account.

Special journals efficiently summarize a largenumber of similar transactions as follows:

The revenue journal is used to record the sale ofservices on account.

The cash receipts journal is used to record thecollection of accounts and other cash receipts.

The purchases journal is used to record pur-chases on account.

The cash payments journal is used to record thepayments of creditor accounts and other cashpayments.

• Define subsidiary ledgeraccounts for customers andcreditors.

• Prepare a revenue journal andpost services provided onaccount to individual customeraccounts and the accountsreceivable control account.

• Prepare a cash receipts journaland post collections to individ-ual customer accounts and theaccounts receivable controlaccount.

• Prepare a purchases journal andpost amounts owed to individ-ual creditor accounts and theaccounts payable controlaccount.

• Prepare a cash payments journaland post the amounts paid toindividual creditor accounts andthe accounts payable controlaccount.

Journalize and post transactions in a manual accounting system that uses subsidiary ledgers and special journals.

Key Points Key Learning OutcomesExample PracticeExercises Exercises

2

3 Describe and give examples of other subsidiary ledgers and modified special journals.

Key Points Key Learning OutcomesExample PracticeExercises Exercises

Subsidiary ledgers may be maintained for a variety of accounts, such as fixed assets,accounts receivable, and accounts payable.Special journals may be modified by addingcolumns for frequently occurring transactions.

• Prepare modified special jour-nals that incorporate additionalcolumns for frequently occur-ring transactions.

5-5 5-5A, 5-5B

Computerized accounting systems are simi-lar to manual systems. The main advantages of acomputerized accounting system are the simulta-neous recording and posting of transactions, highdegree of accuracy, and timeliness of reporting.

• Differentiate between a manualand a computerized accountingsystem.

• Illustrate revenue and cashreceipts transactions usingQuickBooks®.

Describe and illustrate the use of a computerized accounting system.

Key Points Key Learning OutcomesExample PracticeExercises Exercises

4

225

Using the Internet to perform businesstransactions is termed e-commerce. B2C e-commerce involves Internet transactionsbetween a business and consumer, while B2B e-commerce involves Internet transactionsbetween businesses. More elaborate e-commerce involves planning and coordinatingsuppliers, customers, and product design.

• Define e-commerce anddescribe the major trends in e-commerce.

Describe the basic features of e-commerce.

Key Points Key Learning OutcomesExample PracticeExercises Exercises

5

accounting system (202)

accounts payable subsidiaryledger (203)

accounts receivable subsidiaryledger (203)

cash payments journal (214)

cash receipts journal (208)

controlling account (203)

e-commerce (222)

general journal (205)

general ledger (203)

internal controls (203)

invoice (206)

purchases journal (211)

revenue journal (205)

special journals (204)

subsidiary ledger (203)

Key Terms

Selected transactions of O’Malley Co. for the month of May are as follows:

a. May 1. Issued Check No. 1001 in payment of rent for May, $1,200.b. 2. Purchased office supplies on account from McMillan Co., $3,600.c. 4. Issued Check No. 1003 in payment of freight charges on the supplies

purchased on May 2, $320.d. 8. Provided services on account to Waller Co., Invoice No. 51, $4,500.e. 9. Issued Check No. 1005 for office supplies purchased, $450.f. 10. Received cash for office supplies sold to employees at cost, $120.g. 11. Purchased office equipment on account from Fender Office Products,

$15,000.h. 12. Issued Check No. 1010 in payment of the supplies purchased from

McMillan Co. on May 2, $3,600.i. 16. Provided services on account to Riese Co., Invoice No. 58, $8,000.j. 18. Received $4,500 from Waller Co. in payment of May 8 invoice.k. 20. Invested additional cash in the business, $10,000.l. 25. Provided services for cash, $15,900.m. 30. Issued Check No. 1040 for withdrawal of cash for personal use, $1,000.n. 30. Issued Check No. 1041 in payment of electricity and water invoices,

$690.o. 30. Issued Check No. 1042 in payment of office and sales salaries for May,

$15,800.p. 31. Journalized adjusting entries from the work sheet prepared for the fis-

cal year ended May 31.

O’Malley Co. maintains a revenue journal, a cash receipts journal, a purchases journal,a cash payments journal, and a general journal. In addition, accounts receivable andaccounts payable subsidiary ledgers are used.

Illustrative Problem

226 Chapter 5 Accounting Systems

Instructions

1. Indicate the journal in which each of the preceding transactions, (a) through (p),would be recorded.

2. Indicate whether an account in the accounts receivable or accounts payable sub-sidiary ledgers would be affected for each of the preceding transactions.

3. Journalize transactions (b), (c), (d), (h), and (j) in the appropriate journals.

Solution

1. Journal 2. Subsidiary Ledger

a. Cash payments journalb. Purchases journal Accounts payable ledgerc. Cash payments journald. Revenue journal Accounts receivable ledgere. Cash payments journalf. Cash receipts journalg. Purchases journal Accounts payable ledgerh. Cash payments journal Accounts payable ledgeri. Revenue journal Accounts receivable ledgerj. Cash receipts journal Accounts receivable ledgerk. Cash receipts journall. Cash receipts journalm. Cash payments journaln. Cash payments journalo. Cash payments journalp. General journal

3.

Transaction (b):

Purchases Journal

OfficeSupplies

Dr.

AccountsPayable

Cr.Post.Ref.

Post.Ref.

OtherAccounts

Dr.Date Account Credited Amount

3,600 3,600McMillan Co.May 2

3,600

Cash Payments Journal

OtherAccounts

Dr. Post.Ref.

AccountsPayable

Dr.Date Account DebitedCash

Cr.Ck.No.

May 4

12

1003

1010

Freight Expense

McMillan Co.320 320

3,600

Transactions (c) and (h):

Chapter 5 Accounting Systems 227

Cash Receipts Journal

OtherAccounts

Cr.Post.Ref.

AccountsReceivable

Cr.Date Account CreditedCashDr.

Waller Co. 4,5004,500May 18

Date Account DebitedPost.Ref.

InvoiceNo.

Accts. Rec. Dr.Fees Earned Cr.

Revenue JournalRevenue Journal

4,500May 8 Waller Co.51

Transaction (d):

Transaction (j):

1. The initial step in the process of developing anaccounting system is called:

A. analysis. C. implementation.B. design. D. feedback.

2. The policies and procedures used by managementto protect assets from misuse, ensure accuratebusiness information, and ensure compliancewith laws and regulations are called:

A. internal controls.B. systems analysis.C. systems design.D. systems implementation.

3. A payment of cash for the purchase of servicesshould be recorded in the:

A. purchases journal.B. cash payments journal.

C. revenue journal.D. cash receipts journal.

4. When there are a large number of individualaccounts with a common characteristic, it is com-mon to place them in a separate ledger called a(n):

A. subsidiary ledger.B. creditors ledger.C. accounts payable ledger.D. accounts receivable ledger.

5. Which of the following would be used in a com-puterized accounting system?

A. Special journalsB. Accounts receivable control accountsC. Electronic invoice formD. Month-end postings to the general ledger

Self-Examination Questions (Answers at End of Chapter)

1. Why would a company maintain separate accounts receivable ledgers for each cus-tomer, as opposed to maintaining a single accounts receivable ledger for all customers?

2. What are the major advantages of the use of special journals?3. In recording 400 fees earned on account during a single month, how many times

will it be necessary to write Fees Earned (a) if each transaction, including feesearned, is recorded individually in a two-column general journal; (b) if each trans-action for fees earned is recorded in a revenue journal?

Eye Openers

228 Chapter 5 Accounting Systems

4. How many postings to Fees Earned for the month would be needed in Eye Opener 3if the procedure described in (a) had been used; if the procedure described in (b)had been used?

5. During the current month, the following errors occurred in recording transactionsin the purchases journal or in posting from it.a. An invoice for $1,875 of supplies from Kelly Co. was recorded as having been

received from Kelley Co., another supplier.b. A credit of $420to Blackstone Company was posted as $240 in the subsidiary ledger.c. An invoice for equipment of $4,800 was recorded as $4,000.d. The Accounts Payable column of the purchases journal was overstated by $3,600.How will each error come to the bookkeeper’s attention, other than by chance dis-covery?

6. The Accounts Payable and Cash columns in the cash payments journal were unknow-ingly overstated by $900 at the end of the month. (a) Assuming no other errors inrecording or posting, will the error cause the trial balance totals to be unequal? (b) Willthe creditors ledger agree with the accounts payable control account?

7. Assuming the use of a two-column general journal, a purchases journal, and a cashpayments journal as illustrated in this chapter, indicate the journal in which eachof the following transactions should be recorded:a. Purchase of office supplies on account.b. Purchase of supplies for cash.c. Purchase of store equipment on account.d. Payment of cash on account to creditor.e. Payment of cash for office supplies.

8. What is an electronic form, and how is it used in a computerized accounting system?9. Do computerized systems use controlling accounts to verify the accuracy of the

subsidiary accounts?10. What happens to the special journal in a computerized accounting system that uses

electronic forms?11. How would e-commerce improve the revenue/collection cycle?

The following revenue transactions occurred during February:

Feb. 6. Issued Invoice No. 78 to Howard Co. for services provided on account, $490.9. Issued Invoice No. 79 to Hitchcock Inc. for services provided on account, $240.

15. Issued Invoice No. 80 to David Inc. for services provided on account, $515.

Record these three transactions into the following revenue journal format:

REVENUE JOURNAL

Post. Accts. Rec. Dr. Date Invoice No. Account Debited Ref. Fees Earned Cr.

EE 5-1 p. 208

PE 5-1ARevenue journal

obj. 2

Practice Exercises

The following revenue transactions occurred during August:

Aug. 7. Issued Invoice No. 121 to Lincoln Co. for services provided on account, $5,410.15. Issued Invoice No. 122 to Triple A Inc. for services provided on account, $2,360.21. Issued Invoice No. 123 to Bailey Co. for services provided on account, $4,140.

Record these three transactions into the following revenue journal format:

REVENUE JOURNAL

Post. Accts. Rec. Dr. Date Invoice No. Account Debited Ref. Fees Earned Cr.

EE 5-1 p. 208

PE 5-1BRevenue journal

obj. 2

Chapter 5 Accounting Systems 229

The debits and credits from two transactions are presented in the following customeraccount:

NAME XTREME Products Inc. ADDRESS 46 W. Main St.

Post.Date Item Ref. Debit Credit Balance

Mar. 1 Balance ✓ 1,20010 Invoice 127 R29 920 2,12019 Invoice 106 CR52 690 1,430

Describe each transaction and the source of each posting.

EE 5-2 p. 211

PE 5-2AAccounts receivablesubsidiary ledger

obj. 2

The debits and credits from two transactions are presented in the following customeraccount:

NAME Airwave Communications Inc.ADDRESS 76 Oak Ridge Rd.

Post.Date Item Ref. Debit Credit Balance

May 1 Balance ✓ 28014 Invoice 564 CR92 125 15522 Invoice 527 R127 90 245

Describe each transaction and the source of each posting.

EE 5-2 p. 211

PE 5-2BAccounts receivablesubsidiary ledger

obj. 2

The following purchase transactions occurred during October for Rehoboth Inc.:

Oct. 4. Purchased office supplies for $105, on account from Office-to-Go Inc.16. Purchased office equipment for $2,460, on account from Zell Computer Inc.23. Purchased office supplies for $190, on account from Office Mate Inc.

Record these transactions in the following purchases journal format:

PURCHASES JOURNAL

Accounts Office Other Post. Payable Supplies Accounts Post.

Date Account Credited Ref. Cr. Dr. Dr. Ref. Amount

EE 5-3 p. 213

PE 5-3APurchases journal

obj. 2

The following purchase transactions occurred during May for Amy’s Catering Service:

May 11. Purchased party supplies for $420, on account from Party Zone Supplies Inc.19. Purchased party supplies for $290, on account from Party Time Supplies Inc.21. Purchased office furniture for $2,160, on account from Office Space Inc.

Record these transactions in the following purchases journal format:

PURCHASES JOURNAL

Accounts Party Other Post. Payable Supplies Accounts Post.

Date Account Credited Ref. Cr. Dr. Dr. Ref. Amount

EE 5-3 p. 213

PE 5-3BPurchases journal

obj. 2

The debits and credits from two transactions are presented in the following supplier’s(creditor’s) account:

NAME Carnation Inc.ADDRESS 5000 Grand Ave.

Post. Date Item Ref. Debit Credit Balance

Nov. 1 Balance 9211 Invoice 128 CP71 47 4518 Invoice 139 P43 88 133

Describe each transaction and the source of each posting.

EE 5-4 p. 217

PE 5-4AAccounts payablesubsidiary ledger

obj. 2

The debits and credits from two transactions are presented in the following supplier’s(creditor’s) account:

NAME Da Vinci Computer Services Inc. ADDRESS 2199 Technology Avenue

Post. Date Item Ref. Debit Credit Balance

July 1 Balance 9,40019 Invoice 75 P21 3,520 12,92021 Invoice 43 CP46 5,960 6,960

Describe each transaction and the source of each posting.

EE 5-4 p. 217

PE 5-4BAccounts payablesubsidiary ledger

obj. 2

The state of Ohio has a 5.5% sales tax. Buckeye Services Inc., an Ohio company, had tworevenue transactions as follows:

Aug. 7. Issued Invoice No. 121 to Manly Inc. for services provided on account,$1,200, plus sales tax.

21. Issued Invoice No. 122 to Tel Optics Inc. for services provided on account,$2,200, plus sales tax.

EE 5-5 p. 218

PE 5-5AModified revenuejournal