accounting practices 501 chapter 8 balance day adjustments (allowance for doubtful debts) cathy...

TRANSCRIPT

Accounting Practices 501

Chapter 8

Balance Day Adjustments

(Allowance for Doubtful Debts)

Cathy Saenger, Senior Lecturer, Eastern Institute of Technology © Pearson 2011

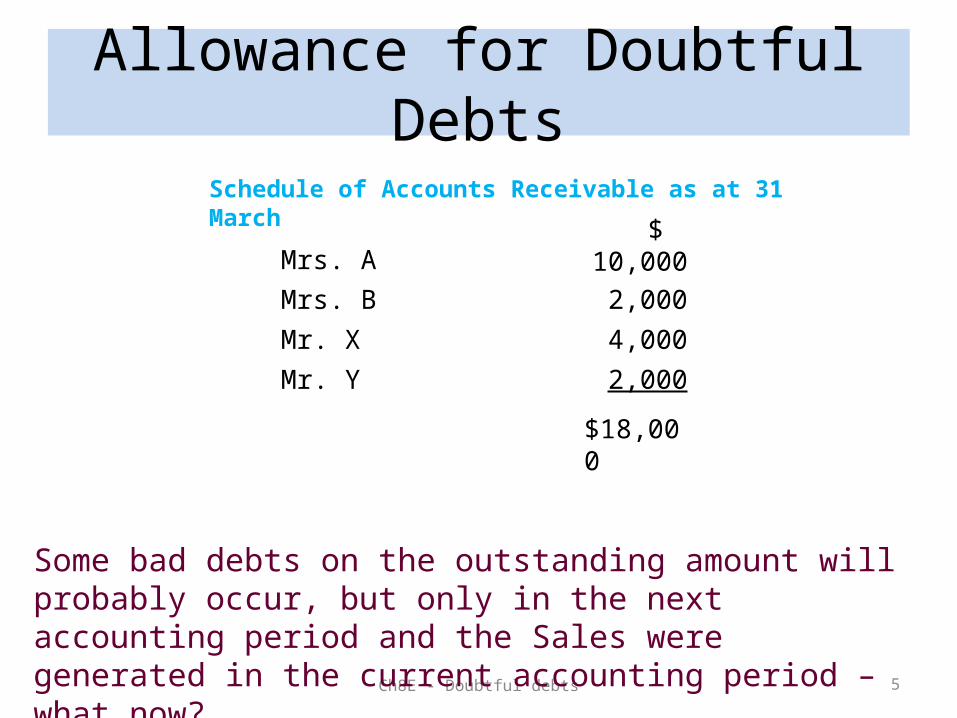

Allowance for Doubtful Debts

Ch8E - Doubtful debts 2

Let’s say we have the following Accounts Receivable schedule at balance date (31 March)

Schedule of Accounts Receivable as at 31 March

10,0002,000

4,000

2,000

$18,000

Mrs. A

Mrs. B

Mr. X

Mr. Y

$

Allowance for Doubtful Debts

Ch8E - Doubtful debts 3

Schedule of Accounts Receivable as at 31 March

10,0002,000

4,000

2,000

$18,000

Mrs. A

Mrs. B

Mr. X

Mr. Y

$

The outstanding $18,000 will only be received in the next accounting period

Allowance for Doubtful Debts

Ch8E - Doubtful debts 4

Schedule of Accounts Receivable as at 31 March

10,0002,000

4,000

2,000

$18,000

Mrs. A

Mrs. B

Mr. X

Mr. Y

$

From experience, the accountant would know that a certain percentage of the outstanding Accounts Receivable amount will not be recovered

Allowance for Doubtful Debts

Ch8E - Doubtful debts 5

Schedule of Accounts Receivable as at 31 March

10,0002,000

4,000

2,000

$18,000

Mrs. A

Mrs. B

Mr. X

Mr. Y

$

Some bad debts on the outstanding amount will probably occur, but only in the next accounting period and the Sales were generated in the current accounting period – what now?

Ch8E - Doubtful debts 6

This is what happens ……..

interesting stuff!!

Allowance for Doubtful Debts

Allowance for Doubtful Debts

Ch8E - Doubtful debts 7

Schedule of Accounts Receivable as at 31 March

10,0002,000

4,000

2,000

$18,000

Mrs. A

Mrs. B

Mr. X

Mr. Y

$

Let’s say we estimate that 5% of the outstanding Accounts Receivable amount will not be recovered in the next accounting period

Allowance for Doubtful Debts

Ch8E - Doubtful debts 8

Schedule of Accounts Receivable as at 31 March

10,0002,000

4,000

2,000

$18,000

Mrs. A

Mrs. B

Mr. X

Mr. Y

$

We then need to push the Accounts Receivable amount down by 5% ($900) to provide a more realistic value

Allowance for Doubtful Debts

Ch8E - Doubtful debts 9

Schedule of Accounts Receivable as at 31 March

10,0002,000

4,000

2,000

$18,000

Mrs. A

Mrs. B

Mr. X

Mr. Y

$

The question is - which account will we write the $900 off from?

?

Don’t know!

- 900

Allowance for Doubtful Debts

Ch8E - Doubtful debts 10

Schedule of Accounts Receivable as at 31 March

10,0002,000

4,000

2,000

$18,000

Mrs. A

Mrs. B

Mr. X

Mr. Y

$

The solution is to create an account called Allowance for Doubtful Debts which will be used to push down the total of Accounts Receivable in the Balance Sheet to show a more realistic figure

?- 900

Allowance for Doubtful Debts

Ch8E - Doubtful debts 11

Schedule of Accounts Receivable as at 31 March

10,0002,000

4,000

2,000

$18,000

Mrs. A

Mrs. B

Mr. X

Mr. Y

$

?- 900

General JournalDate

Account Titles

Ref no Debit Credit31/3

Allowance for Doubtful Debts 900

Allowance for Doubtful Debts

Ch8E - Doubtful debts 12

General JournalDate

Account Titles

Ref no Debit Credit31/3

Allowance for Doubtful Debts 900

The Allowance for Doubtful Debts account is a negative asset (used to push down Acc Rec) and is therefore credited

The million dollar question – what will it balance with?

Allowance for Doubtful Debts

Ch8E - Doubtful debts 13

General JournalDate

Account Titles

Ref no Debit Credit31/3

Allowance for Doubtful Debts 900

A Doubtful Debts expense account is created to balance the amount

Doubtful Debts expense 900

Being entry to create an allowance for doubtful debts (5% of Acc Rec)

The Doubtful Debts expense account will in turn push down the profit to show a more realistic profit

Allowance for Doubtful Debts

Ch8E - Doubtful debts 14

Schedule of Accounts Receivable as at 31 March

10,0002,000

4,000

2,000

$18,000

Mrs. A

Mrs. B

Mr. X

Mr. Y

$

General JournalDate

Account Titles

Ref no Debit Credit31/3 Doubtful Debts expense 900

Allowance for Doubtful Debts 900

Being entry to create an allowance for doubtful debts (5% of Acc Rec)

Ch8E - Doubtful debts 15

The Doubtful Debts Expense will be classified as a Finance Expense in the Income Statement

The Allowance for Doubtful Debts account is classified as a Current Asset (negative) in the Balance Sheet

This means that the Profit will decrease and the Current Assets will decrease, which gives a truer picture of the financial position and performance of the business

Let’s look at the financial statements

Week 7 (E) - Doubtful Debts 16

……….

Less Expenses

Finance Expenses

Doubtful Debts $900

……….

Current Assets

Accounts Receivable $18,000Less Allowance for Doubtful Debts 900 17,100

Extract from the Income Statement for the year ended ……..

Extract from the Balance Sheet as at …