accounting information systems, investor … information systems, investor learning, and stock...

TRANSCRIPT

Accounting Information Systems, Investor Learning, and Stock

Return Regularities∗

Kai DuSmeal College of Business

Penn State [email protected]

Steven HuddartSmeal College of Business

Penn State [email protected]

Nov 2016

∗VERY PRELIMINARY. We thank Jianhong Chen, Pingyang Gao, Robert Gox, Jeremiah Green,Jia Li, Pierre Liang, John Liechty, Hong Qu, Jack Stecher, Lingzhou Xue and workshop participants atPenn State, University of Southern Denmark, Michigan State, Carnegie Mellon, and University of Zurich forhelpful comments. Financial support from Penn State Smeal College of Business is gratefully acknowledged.

Accounting Information Systems, Investor Learning, and Stock

Return Regularities

Abstract

This paper examines the implications of investor learning based on accounting information

systems for the relationship between accounting information and stock returns. We propose

a stochastic model in which the underlying states of a company follow a Markov process

and are only imperfectly measured through accounting information systems, based on which

Bayesian investors form beliefs about the underlying states of the company. The model

delivers several predictions that are consistent with empirical regularities on the relationship

between accounting information and stock returns, including market reactions to earnings

signals and to breaks of earnings strings, and stock return regularities based on the difference

of two accounting signals. We also discuss how these predictions vary with two characteristics

of accounting information systems, informativeness and conservatism.

1 Introduction

Empirical research in accounting and finance has identified a plethora of regularities in

stock prices in relation to accounting information (for reviews of the literature, see Kothari

2001; Richardson et al. 2010). Such regularities include market reactions to contempora-

neous earnings reports and to time-series patterns of earnings, and the predictive ability of

various accounting signals. Researchers have attributed these phenomena to various eco-

nomic, psychological, and institutional factors. However, little consensus exist with respect

to the explanations of the regularities. In this paper, we propose a simple stochastic model

of investor learning that can accommodate a battery of accounting-based stock return reg-

ularities, including market reactions to earnings reports and to breaks in strings of earnings

surprises, and anomalies based on earnings-cash flow difference (the accruals anomaly) and

book-tax differences.

Our model features an accounting information system (AIS), a measurement function that

generates accounting signals from underlying states (e.g., profitability, or cash generating

activities) which follow a Markov process and are unobservable to investors. Even though

the representative investor does not observe the underlying states, she understands the law

of motion of the underlying states and the way how the states are mapped into accounting

reports, based on which she attempts to infer underlying states in a Bayesian fashion. The

recursive feature of the belief function enables an examination of investor learning, i.e., how

investor beliefs evolve with the the growing history of accounting signals.

Our study focuses on the implications of investor learning on various regularities docu-

mented by practitioners and empiricists who examine a large number of firms. Understand-

1

ing these empirical regularities requires analysis from a frequentist’s perspective outside the

model that any investor faces, in contrast to conventional equilibrium analysis which derives

implications based on the behavior of the economic agents within the model. Departing from

the world of the representative investor, much of our analysis seeks to imitate the way how

empiricists detect patterns of return regularities. While the average belief of the investor

clientele of each firm may be characterized by Bayesian learning, the return regularities de-

tected by empiricists represent the distributional behavior of a large number of idiosyncratic

firms. The Bayesian investor can only condition her belief on a certain history of realized

signals, but an empiricist would draw inferences from a large number of idiosyncratic firm

histories which collectively approximate the true data-generating process. This argument is

built on the distinction between the Bayesian perspective and the frequentist’s view of the

world first noted in statistical decision theories (Berger 1985) and later introduced to asset

pricing research (Lewellen and Shanken 2002).

Unlike prior asset pricing models which assume stationary dividend processes, our model

assumes that states follow a Markov process, which is nonstationary. With nonstationary

states, expected returns from a Bayesian investor’s perspective are not typically zero, because

prices do not revert to a long-run mean. If the investor’s probability assessment of the state is

more pessimistic than what is implied by the stationary distribution of the Markov process,

price is temporarily deflated and will rise in the future, and vice versa. From an empiricist’s

perspective, however, expected returns will be determined by distributional properties. For

example, the average subsequent return of a group of firms with low signal will be different

from a group with high signal, because different signals imply different updating dynamics

in individual investors’ beliefs, which collectively cause systematic differences in the average

2

returns.

Our analysis predicts that market reaction to the break of a string of earnings increases

is more negative as the length of the string increases, but approaches a lower bound as the

length of the string approaches infinity. The intuition is that as the length of the earnings

string increases, investor beliefs are updated toward an upper or lower bound. For example,

even though observing the first low signal causes investors to revise her belief of the state

being bad upward by a lot, observing more signals of the same nature will only cause smaller

and smaller revisions.

With dual information systems, our model yields predictions on the relationship be-

tween differential informativeness and return regularities based on the differences between

the accounting signals generated by the two information systems. This result has strong

implications for two accounting-based anomalies: the accruals anomaly (Sloan 1996) and

the return predicability of book-tax-differences (e.g., Lev and Nissim 2004).

Simulating the model for a large number of idiosyncratic histories and for a large number

of periods, we are able to produce empirical patterns as predicted by the model. What is

more, we are able to study how these patterns vary with different parameters of the AIS.

Several findings emerge:

Our study makes several contributions to the literature of accounting-based return regu-

larities, theories on investor learning and asset prices, and studies of accounting information

systems. First, our study contributes to the vast literature on accounting-based return reg-

ularities by proposing learning-based explanations to several regularities. By investigating

the impact of AIS on market reactions, this paper is also related to studies on the earnings-

return associations (for a review of the literature, see Kothari 2001) and stock price reactions

3

to breaks of earnings strings (e.g., Ke et al. 2003), as well as other accounting-based return

regularities (for a review, see Richardson et al. 2010).

Second, by examining the impact of investor learning in a model with nonstationary

dividends, our study complements studies on investor learning and expectations in capital

markets (e.g., Lewellen and Shanken 2002).

Lastly, our notion of AIS follows from theories of information systems in the economics

and accounting literature. Marschak and Miyasawa (1968) and Marschak (1971) examine

the economics of information systems, drawing on the informativeness criterion by Blackwell

(1953). The accounting literature on AIS has primarily focused on its decision usefulness

(e.g., Demski 1973). The focus of our study is distinct from these studies: Instead of studying

the decision-usefulness of the AIS, we examine its implications for stock return regularities.

We contribute to this literature by proposing a theoretical framework for understanding the

role of AIS in stock market reactions to accounting signals, and by formally studying the

role of informativeness and conservatism, two important properties of accounting information

systems, in asset price formation.

The rest of the paper is organized as follows. Section 2 introduces a simple model of

Bayesian learning by a representative investor, and characterizes investor’s belief updating

process. Section 3 analyzes empirical tests of return regularities from a frequentist’s per-

spective. Section 4 conducts simulation analysis and discusses the connections to empirical

research. market reactions to accounting signals, and discusses the connections to prior

empirical findings. Section 5 concludes.

4

2 Model

2.1 Accounting Information System

Our main analysis is based on a 2 by 2 setup in which both the underlying states and

accounting signals take binary values. However, the model can be readily extended to a

general case as detailed in Appendix A.

Suppose a firm operates in a stochastic environment, and there are two possible states

for the firm’s fundamental profitability xt in each period t: bad state (B) and good state

(G), where 0 < B < G, i.e., xt ∈ X = {B,G}. The state evolves according to a Markov

chain summarized by a 2 by 2 transition matrix:

P =

Pr(xt+1 = B|xt = B) Pr(xt+1 = G|xt = B)

Pr(xt+1 = B|xt = G) Pr(xt+1 = G|xt = G)

=

a 1− a

1− b b

(2.1)

where 0 ≤ a, b ≤ 1. We further impose the following condition:

Condition 1 a+ b ≥ 1.

Condition 1 implies a relatively persistent process, whereas a + b < 1 implies a mean-

reverting process.

Following Marschak and Miyasawa (1968) and Marschak (1971), we introduce an ac-

counting information system denoted by the 3-tuple < X, Y, η >, where Y = {L,H} is the

set of possible signals (“low” (L) and “high” (H)), and η is a measurement matrix which

maps the states to accounting signals for each period.1 After observing state xt, a firm man-

1The ordering of possible values for states and signals warrants some discussion. Even though the labelingof event/signal values does not affect the implications of the information system2, we assume ordinal valuesfor x and y so that we may study certain properties of the information system, such as conservatism, whichinvolves ordinal values of events/signals.

5

ager uses the accounting information system to generate a signal yt ∈ Y , which is a noisy

representation of xt. AIS can be described by a 2 by 2 measurement matrix η:

η =

Pr(yt = L|xt = B) Pr(yt = H|xt = B)

Pr(yt = L|xt = G) Pr(yt = H|xt = G)

=

c 1− c

1− d d

(2.2)

where 0 ≤ c, d ≤ 1. The structure of the model is illustrated by Figure 1.

The following condition ensures that the AIS is sufficiently informative.

Condition 2 c+ d ≥ 1.

Based on Marschak (1971), some special cases of the information system are easy to define.

An information system η is said to be a null information system if its rows are identical, i.e.,

c + d = 1; η is said to be a perfect information system if η is a permutation matrix3, i.e., if

c = d = 1 or c = 1− d = 1.

AIS in our model refers to the firm-specific technology/practice of applying accounting

rules to measure underlying economic transactions. Two key features characterize the AIS:

the economic states that the AIS measures evolve in a stochastic fashion; accounting mea-

surement introduces noise which randomizes the mapping from states to signals. The second

statement is an abstraction of numerous accounting estimates which require accountants’

assessment of uncertain economic positions. For example, accounting for loss contingencies

(recognition vs. disclosure) requires accountants’ subjective evaluation of whether a contin-

gent loss is probable and/or estimable; impairment of long-lived assets involves a recover-

ability test based on expectations of future cash flows; accounting for bad debt provisions

require estimates of uncertain future collections.4 Scott (1979) provide a theoretic account

3A permutation matrix is obtained by permuting the rows of an identify matrix, and contains exactlyone entry of 1 in each row and each column and 0s elsewhere.

4Even though law of large numbers stipulate that estimates based on large sample of transactions (such as

6

on the probabilistic nature of AIS. As a result, these estimates are inevitably subject to ran-

domness, and the overall AIS can be understood as a probabilistic mapping from underlying

states to accounting signals. The attributes of the mapping are influenced by a variety of

factors, such as accounting rules, industry norms, innate firm characteristics, and above all,

discretion of managers and accountants.

In some later analysis we study the market pricing consequences of the properties of

accounting information systems, including informativeness and conservatism. In this paper,

we do not provide formal definitions of these concepts. Essentially, informativeness is a

concept based on the decision usefulness of the information system (Blackwell 1953), while

conservatism captures the extent to which the the mapping from B (“bad”) state to L

(“low”) signal is less noisy than the mapping from G (“good”) state to H (“high”) signal

(e.g., Antle and Lambert 1988; Gigler et al. 2009). It is important to note that rigorous

definitions of both concepts cannot typically be reduced to scalars. For the purpose of the

main analysis, the following two observations suffice.

Remark 1 Considering two information systems η = [c, 1 − c; 1 − d, d] and η′ = [c′, 1 −

c′; 1 − d′, d′]. A sufficient condition for η to be more informative than η′ is that c ≥ c′ and

d ≥ d′.

Remark 2 Considering two information systems η = [c, 1 − c; 1 − d, d] and η′ = [c′, 1 −

c′; 1−d′, d′]. A sufficient condition for η to be more conservative than η′ is c ≥ c′ and d ≤ d′.

2.2 Investor Beliefs

In this section, we study the learning process of a Bayesian investor who updates her

posterior about the underlying state given the growing history of the accounting signals.

warranty expenses) are predictable with certain precision, abundant other transactions are non-diversifiablein nature.

7

We assume that she is a representative investor whose beliefs reflect consensus forecasts of

heterogenous investors in the real world.

Denote investor posterior at t after observing the history by µt = Pr{xt = B|yt}, where

yt = {y0, ..., yt} is the history of earnings reports. Using Bayes’ Rule, it is easy to show that

the updating process of investor beliefs is given by the following proposition.

Lemma 1 Given investor belief of the previous period (µt−1) and the accounting signal of

this period (yt), the belief at the end of period t is given by the following:

µt|yt=L =c(a+ b− 1)µt−1 + c(1− b)

(c+ d− 1)(a+ b− 1)µt−1 + (1− d)b+ c(1− b), (2.3)

µt|yt=H =(1− c)(a+ b− 1)µt−1 + (1− c)(1− b)

(1− c− d)(a+ b− 1)µt−1 + db+ (1− c)(1− b). (2.4)

The recursion of investor beliefs implies that investor beliefs and stock prices depend on

the patterns of earnings sequences. The following proposition discusses the implications of

such recursion.

Proposition 1 Suppose Conditions 1-2 hold. (i) If µt ∈ [µ, µ], then µt+s ∈ [µ, µ] for ∀s ≥ 1;

(ii) if the investor starts with prior µ0 /∈ [µ, µ], then with probability one, µt will eventually

jump into [µ, µ] and stay in this interval forever, where

µ =1

2

(a(c− 1) + b(2c+ d− 2)− 2c+ 2

(a+ b− 1)(c+ d− 1)−

√a2(c− 1)2 − 2a(b− 2)(c− 1)d+ d (b2d+ 4b(c− 1)− 4c+ 4)

(a+ b− 1)2(c+ d− 1)2

),

and

µ =1

2

(√c (a2c+ 4a(d− 1)− 4d+ 4)− 2(a− 2)bc(d− 1) + b2(d− 1)2

(a+ b− 1)2(c+ d− 1)2+

(a− 2)c+ b(2c+ d− 1)

(a+ b− 1)(c+ d− 1)

).

Intuitively, if the investor sees a long series of L signals, µt increases toward µ; if the

investor sees a long series of H signals, µt decreases toward µ. In other words, if we focus

on the long-run behavior of investor belief which is not influenced by priors, we can be sure

8

that the belief is bounded by µ and µ. The following corollary discusses the properties of

the bounds.

Corollary 1 The lower bound µ and upper bound µ exhibit the following relationships with

parameters of AIS:

(i)∂µ

∂a≥ 0,

∂µ

∂b≤ 0,

∂µ

∂c≤ 0, and

∂µ

∂d≤ 0.

(ii) ∂µ∂a≥ 0, ∂µ

∂b≤ 0, ∂µ

∂c≥ 0, and ∂µ

∂d≥ 0.

Intuitively, the more persistent the B state is, the higher investor’s probabilistic assessment of

the state being indeed B is (signified by higher lower and upper bounds); the more persistent

the G state is, the opposite is true. More informative accounting signals will enlarge the

possible range for possible investor beliefs, because more informative signals induce more

substantive revisions.

2.3 Two-Signal Information System

In the preceding analysis we have defined an information system with one signal (in-

terpreted as earnings) for each period. In the real world, however, earnings are usually

not the only indicator of firm profitability (e.g., Antle et al. 1994). There are various in-

stitutional contexts in financial reporting in which different channels of public information

provide noisy information about the underlying state. The most proverbial example of such

two-signal systems is one that reports cash flows and earnings. According to Christensen

and Demski (2003), cash flows and earnings (accrual basis measurement) are “simply two

different ways of doing the accounting, and both, in principle, are sources of information”

(p. 128), and “the typical financial report contains accrual and cash basis renderings, two

different partitions so to speak” (p. 115). Another example is book income and tax income

9

(Hanlon 2005; Graham et al. 2012). Therefore, it is of interest to augment the model to

include a second signal about the same state.

Suppose the underlying state xt is imperfectly revealed by an information system with

two information channels, < X, Y, Z, η1, η2 > for every state xt, η1 generates a signal yt, and

η2 generates a different signal zt. Specifically, let

η1 =

c1 1− c1

1− d1 d1

, η2 =

c2 1− c2

1− d2 d2

(2.5)

Figure 2 illustrates the structure of the two-signal information system. The following condi-

tion ensures that both signals are sufficiently informative.

Condition 3 c1 + d1 ≥ 1, c2 + d2 ≥ 1.

We can derive the beliefs of investor who observes two sequences of signals, yt and zt, as

given by Lemma 2.

Lemma 2 Given investor belief of the previous period (µt−1) and the signals of this period

(yt and zt), the belief at the end of period t is given by the following:

µt|yt=L,zt=L =c1c2((a+ b− 1)µt−1 + 1− b)

c1c2((a+ b− 1)µt−1 + 1− b) + (1− d1)(1− d2)((1− a− b)µt−1 + b), (2.6)

µt|yt=L,zt=H =c1(1− c2)((a+ b− 1)µt−1 + 1− b)

c1(1− c2)((a+ b− 1)µt−1 + 1− b) + (1− d1)d2((1− a− b)µt−1 + b), (2.7)

µt|yt=H,zt=L =(1− c1)c2((a+ b− 1)µt−1 + 1− b)

(1− c1)c2((a+ b− 1)µt−1 + 1− b) + d1(1− d2)((1− a− b)µt−1 + b), (2.8)

µt|yt=H,zt=H =(1− c1)(1− c2)((a+ b− 1)µt−1 + 1− b)

(1− c1)(1− c2)((a+ b− 1)µt−1 + 1− b) + d1d2((1− a− b)µt−1 + b). (2.9)

The recursion of investor beliefs implies that investor beliefs depend on the patterns of

the two sequences of signals. The following proposition provides the lower bound and upper

bound for investor beliefs.

10

Proposition 2 Suppose Conditions 1 and 3 hold. (i) If µt ∈ [µ∗, µ∗∗], then µτ ∈ [µ∗, µ∗∗]for ∀τ > t; (ii) if the investor starts with prior µ0 /∈ [µ∗, µ∗∗], then with probability one, µtwill eventually jump into this interval and stay in this interval forever, where

µ∗ =1

2

(a(c1 − 1)(c2 − 1) + b(2c1(c2 − 1)− 2c2 − d1d2 + 2) + 2(c1(−c2) + c1 + c2 − 1)

(a+ b− 1)(c1(c2 − 1)− c2 − d1d2 + 1)

−

√a2(c1 − 1)2(c2 − 1)2 + 2a(b− 2)(c1 − 1)(c2 − 1)d1d2 + d1d2 (b2d1d2 + 4b(c1(−c2) + c1 + c2 − 1) + 4(c1 − 1)(c2 − 1))

(a+ b− 1)2(c1(−c2) + c1 + c2 + d1d2 − 1)2

),

(2.10)

and

µ∗∗ =1

2

(√c1c2 (a2c1c2 + 4a(d1(−d2) + d1 + d2 − 1) + 4(d1 − 1)(d2 − 1)) + 2(a− 2)bc1c2(d1 − 1)(d2 − 1) + b2(d1 − 1)2(d2 − 1)2

(a+ b− 1)2(c1c2 − d1d2 + d1 + d2 − 1)2

+(a− 2)c1c2 + b(2c1c2 − d1d2 + d1 + d2 − 1)

(a+ b− 1)(c1c2 − d1d2 + d1 + d2 − 1)

). (2.11)

The following corollary discusses the properties of the bounds. The intuitions underlying

the corollary are similar to those of Corollary 1.

Corollary 2 The lower bound µ∗ and upper bound µ∗∗ exhibit the following relationships

with parameters of AIS:

(i) ∂µ∗

∂a≥ 0, ∂µ∗

∂b≤ 0, ∂µ∗

∂cj≤ 0, and ∂µ∗

∂dj≤ 0 for j = 1, 2.

(ii) ∂µ∗∗

∂a≥ 0, ∂µ∗∗

∂b≤ 0, ∂µ∗∗

∂cj≥ 0, and ∂µ∗∗

∂dj≥ 0 for j = 1, 2.

2.4 Stock Prices

We interpret xt as the underlying cash flows of period t, and assume investors price the

firm based on risk-neutral expectation of discounted future cash flows of all future periods.

The post-accounting-signal price is the cum-dividend price, pt, which as a function of investor

beliefs is given by the following lemma.5

5We abstract from institutional contexts which may justify such pricing functions. The pricing functioncan be motivated by an economic setting in which investors trade on future claims to the entire discounteddividend stream of the company, without ever receiving (and thereby observing) the dividends. We make thissimplified assumption without formally modeling the institutions of dividends and trading in an over-lappinggeneration model (e.g., De Long et al. 1990) because our focus is to examine the implications of investorlearning for asset prices in a representative investor setting, instead of the equilibrium behavior of price.

11

Lemma 3 After observing accounting signals in each period t, stock price pt is given by

pt =1 + δ

δ(2− a− b+ δ)

(G(1− a+ δ) +B(1− b)− δ(G−B)µt

)(2.12)

where δ is the discount rate, and I is the identity matrix of size 2.

It follows immediately that the price change from period t to period t+ 1 is given by

pt+1 − pt = − 1 + δ

2− a− b+ δ(G−B)(µt+1 − µt). (2.13)

where µt+1 is given by (2.3) and (2.4) for the one-signal case and (2.6-2.9) for the two-signal

case, updating time subscripts by one period.6

The Markov process of underlying states (dividends) dictates that the dividend process

is nonstationary. With changing dividend process, learning does not lead the belief to a

long-run mean. However, in the extreme case of entirely uninformative AIS, price change is

given by pt+1 − pt = 1+δ2−a−b+δ (G − B)((2 − a − b)µt − (1 − b)). Note that even though the

investor rationally ignores the signal, there is still updating due to the nature of Markov

process: As long as 0 < a < 1 and 0 < b < 1, the two-state Markov process will yield the

unique stationary distribution (πB, πG):

(πB, πG) =

(1− b

2− a− b,

1− a2− a− b

). (2.16)

6If we work instead with ex-dividend prices, the price function would be:

pt =G(1− a) +B(1− b+ δ)− (G−B)δ ((a+ b− 1)µt − b)

δ(2− a− b+ δ), (2.14)

and the price change would be:

pt+1 − pt = − a+ b− 1

2− a− b+ δ(G−B)(µt+1 − µt). (2.15)

The intuitions remain the same as the case of cum-dividend prices.

12

3 Empirical Tests of Return Regularities

3.1 Bayesian Investor versus Freqentist Empiricist

In this section, we discuss the different expectations of a Bayesian investor who updates

her belief based on a history of earnings reports and an empiricist who attempts to detect

return regularities in the data (i.e., a sample of earnings and stock prices). We use Eit [·]

to denote the subjective expectation of a Bayesian investor, and use Eet [·] to denote the

expectation of an empiricist who observes the entire sample of firms. For the investor, the

probability that the underlying state is B is random and fluctuates over time as new earnings

reports arrive. However, from an empiricist’s perspective, the average price change in the

sample depends on the distribution of a large number of Bayesian investors.

The following lemma derives the expectations from the Bayesian investor and the em-

piricist’s perspectives.

Lemma 4 (i) From a Bayesian investor’s perspective,

Eit [pt] = pt =

1 + δ

δ(2− a− b+ δ)

(G(1− a+ δ) +B(1− b)− δ(G−B)µt

)(3.1)

Eit [pt+1 − pt] =

1 + δ

2− a− b+ δ(G−B)

((2− a− b)µt − 1 + b

)(3.2)

Eit [pt − pt−1] = − 1 + δ

2− a− b+ δ(G−B)

(µt − µt−1

)(3.3)

(ii) From an empiricist’s perspective,

Eet [pt] =

1 + δ

δ(2− a− b+ δ)

(G(1− a+ δ) +B(1− b)− δ(G−B)πB

)(3.4)

Eet [pt+1 − pt] = 0 (3.5)

Eet [pt − pt−1] = 0 (3.6)

13

As we can see from equation (3.1),

sign(Eit [pt+1 − pt]

)= sign

(µt −

1− b2− a− b

)(3.7)

With changing dividend process, expected price change is positively related to lagged belief

µt, and price does not revert to a long-run mean. This feature is unlike models with stationary

dividend processes (e.g., Lewellen and Shanken 2002). The intuition behind equation (3.4)

is as follows. If the current probability assessment of the state being B is greater than the

probability implied by the stationary distribution, price is temporarily deflated and will rise

in the future. On the other hand, if the current probability assessment of the state being

B is lower than the probability implied by the stationary distribution, price is temporarily

inflated and will decline in the future. Expected price change is zero only when if µt = 1−b2−a−b ,

i.e., investor belief is consistent with the stationary distribution of the underlying states.

According to an empiricist, the expectation of next-period price revision is taken over all

possible investor beliefs µt in the empirical sample examined, which we assume to consist of

a large number of i.i.d. firms. The key to the proof is that∫µtµtdF (µt) = 1−b

2−a−b . In other

words, the average belief perceived by the empiricist is 1−b2−a−b . Therefore, the empiricist

perceives no return predictability in the sample. The distinction between the Bayesian

perspective and the empiricist (frequentist) perspective has been discussed by Berger (1985)

and Lewellen and Shanken (2002) in greater lengths.

We then show why asset pricing tests from an empiricist’s perspective could detect return

predictabilities conditional on certain accounting signals, when individual firms’ prices are

determined by Bayesian investors who must infer the underlying states from accounting

signals. We show this through both analytical characterization (this section) and simulations

14

(Section 4).

3.2 Market Reactions to Earnings and Breaks in Earnings Strings

Our model can be used to examine the behavior of stock prices in relation to accounting

signals. The following proposition characterizes how the differential market reactions to

earnings signals depend on investor belief µt.

Proposition 3

Eet [pt|yt = H]− Ee

t [pt|yt = L] ≥ 0 (3.8)

The expectation operator Eet [·] denotes the mean of the sample for which yt is equal to

certain signal, based on the unconditional distribution of beliefs. Proposition 3 essentially

states that the earnings response coefficient (ERC) is positive.

We then examine the average market reactions to earnings strings, defined as a series of

the same earnings signals. The following proposition characterizes the comparative statics

of the average market reaction with respect to breaks in earnings strings.

Proposition 4 (i) The average market reaction to breaks in earnings strings is negative; the

average market reaction becomes more negative as the string of H signals becomes longer if ei-

ther of the following conditions is met: (1) 0 ≤ b ≤ b∗, where b∗ =c(

(2c+d−1)−√

(1−d)(4c+3d−3))

2(c+d−1)2;

(2) b∗ ≤ b ≤ 1 and 0 ≤ a ≤ a∗, where a∗ = b2(c+d−1)2−bc(2c+d−1)+c(c−d+1)c(1−d)

;

(ii) As the earnings string (of H signals) becomes long enough,

lims→∞

Eet [pt − pt−1|yt = L, yt−1 = ... = yt−s = H]

=− 1 + δ

2− a− b+ δ(G−B)

( c(a+ b− 1)µ+ c(1− b)(c+ d− 1)(a+ b− 1)µ+ (1− d)b+ c(1− b)

− µ)

(3.9)

Notice that as the string of H signals becomes longer, because of gH(µ) ≤ 0 for µ ∈ [µ, µ],

it must be the case that µt−1 is on average lower. Therefore, a sufficient condition for the

15

above statement is gL′(µ) ≤ 0, which is easily shown to hold when any of the following three

conditions (in addition to Conditions 1 and 2) is true:

Intuitively, after observing a string of H signals, if information system is sufficiently

informative, µt will be walked down, so the price change upon the break of earnings string

will be negative. The longer the string, the more negative the reaction to the break. More

nuanced comparative statics could show that the magnitude of market reaction to break will

increase with informativeness.

Analogously, if the earnings strings are defined as consecutive low (L) signals, the average

market reaction to breaks in earnings strings is positive, and the magnitude of the average

market reaction becomes greater as the string of L signals becomes longer under certain

conditions. If the investor observes a sequence of L signals before seeing a break,

lims→∞

Eet [pt − pt−1|yt = H, yt−1 = ... = yt−s = L]

=− 1 + δ

2− a− b+ δ(G−B)

( (1− c)(a+ b− 1)µ+ (1− c)(1− b)(1− c− d)(a+ b− 1)µ+ db+ (1− c)(1− b)

− µ)

(3.10)

3.3 Return Predictability Based on Earnings

Now we would like to discuss how sampling based on current period ’s earnings signal

could generate a hedge return in the next period, and why such anomaly is consistent with

Bayesian learning.

Proposition 5 Earnings signal negatively predicts stock returns in the next period. In other

words, a trading strategy that buys stocks with bad signals and sells stocks with good signals

and holds them for one period is profitable. Formally, the hedge return for the next period

by trading on earnings signals is negative:

Eet (pt+1 − pt|yt = H)− Ee

t (pt+1 − pt|yt = L) ≤ 0 (3.11)

16

where the expectation operator denotes the mean over the unconditional distribution of beliefs.

Note that the proofs of the main propositions are not typical analytical proofs in the

context of the model assumptions, but rather outside the model: the proofs rely on arguments

based on the distributional knowledge which is not available to investors within the model.

The intuition behind the finding that future price change conditional on a good signal is

smaller than future price change conditional on a bad signal involves two arguments. First,

future price change is an increasing function of µt. Second, in the whole population, on

average, µt with a L signal is greater than µt with a H signal.

The following corollary examines the comparative statics of hedge returns with respect

to parameters of the AIS.

Corollary 3 (Hedge return and information system.)

∂

∂c

(Eet (pt+1 − pt|yt = H)− Et(pt+1 − pt|yt = L)

)≥ 0 (3.12)

∂

∂d

(Eet (pt+1 − pt|yt = H)− Et(pt+1 − pt|yt = L)

)≥ 0 (3.13)

The intuition is that when c = d = 1/2 (uninformative), there is no learning and no

predictability.

3.4 Return Predictability Based on Differential Accounting Signals

We now study return regularities based on two AIS. Various accounting-based regulari-

ties based on accounting accruals (which are difference between cash flows and accounting

earnings) and the book-tax difference can be studied in this framework. The commonality

of these return regularities is that a signal defined as the difference between two other infor-

mation signals predict future stock returns. The following proposition formalizes this notion

17

and provides conditions for hedging strategies based on differential signals to be profitable.

Proposition 6 Consider a trading strategy that buys stocks with with negative accruals (yt =

L, zt = H) and sells stocks with positive accruals (yt = H, zt = L) and hold them for 1 period.

A sufficient condition for the strategy to be profitable is, in addition to Conditions (1) and

(3),c2d2(1− d1)

d1(1− d2) + c2(d2 − d1)≤ c1 ≤ 1. (3.14)

Proposition 6 states that accruals negatively predict future returns if the AIS that gen-

erates earnings is sufficiently informative and conservative.

4 Simulation and Connections to Empirical Findings

As discussed above, our model can be applied to reexamine empirical regularities of

market reactions to earnings surprises and breaks in earnings strings. In this section, we use

simulations to gauge how well is model is able to explain empirical findings. Simulation is

a faithful representation of empirical tests (as studied above) because both of them are in a

frequentist sense.

Making connections between the model and real world data requires the interpretation

of model “period” in terms of real world time intervals, such as quarters and years. We

interpret the model period as a quarter when we study market reactions to earnings strings,

but interpret a model period as a year when we study return predictabilities. This seemingly

inconsistent choice is driven by considerations to align the model intuitions with real world

phenomena, i.e., choosing the real-world interpretation that makes most sense in each con-

text. For example, for earnings strings, it is customary to define strings based on quarterly

reports, because anecdotes and empirical evidence shows that investors can make salient

18

comparisons across adjacent quarters.

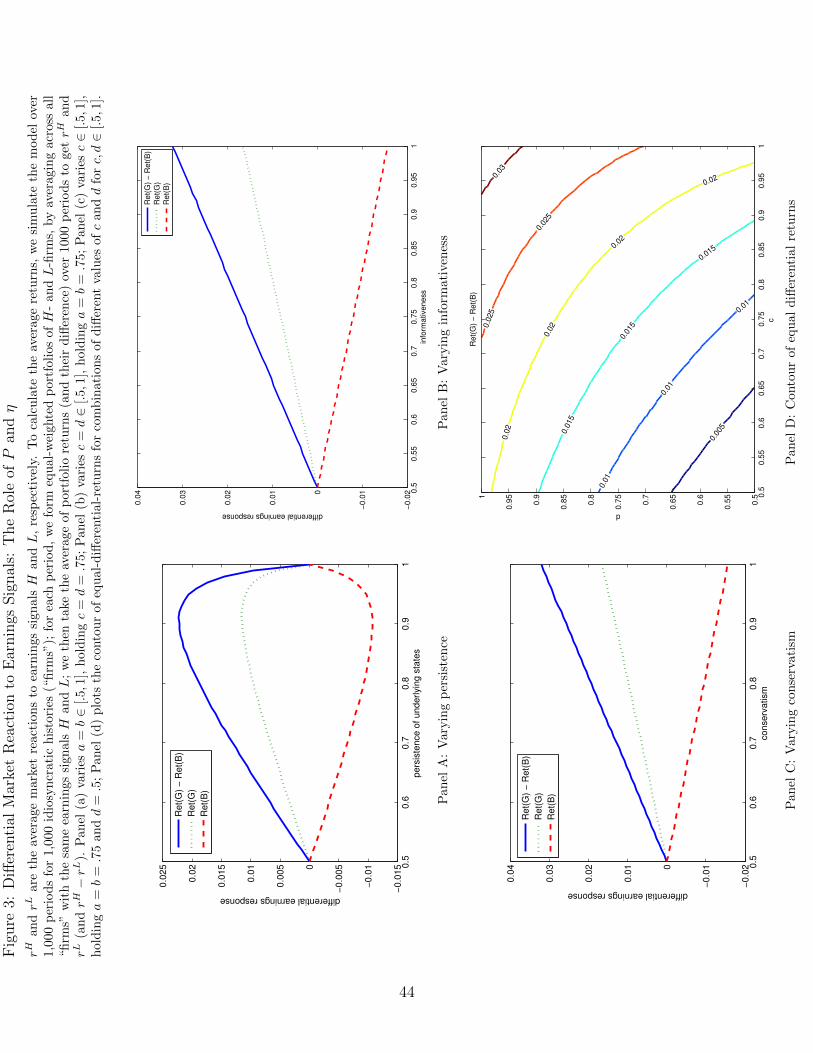

4.1 Average market reactions to earnings signals

To calculate the average returns, we simulate the model over T = 100 periods for N =

10, 000 idiosyncratic histories (“firms”)7. We calibrate the three nonessential parameters as

(L,H, δ) = (1, 2, .06), which will be maintained throughout the simulation analysis8. For

each period, we form equal-weighted portfolios of H- and L-firms, by averaging across all

“firms” with the same earnings signals H and L; we then take the average of portfolio returns

(and their difference) over 1,000 periods to get the average market reactions (stock returns)

to earnings signals H and L and their difference, rH , rL, and rH − rL respectively.

Figure 3 presents the results. When we vary the persistence of underlying state, the

differential reaction first increases then decreases (Panel (a)). The differential reaction in-

creases with both informativeness and conservatism (Panels (b) and (c)). This pattern is

also evident in Panel (d), the contour plot in which both c and d vary from .5 to 1.

4.2 Market reaction to breaks in earnings strings

Prior studies have documented a strong negative market reaction to a break in a string

of consecutive earnings increases (e.g., Barth et al. 1999; Ke et al. 2003). For example, Ke

et al. (2003) document a mean abnormal return is -1.77% for the three-trading-day window

[-2,1] and -4.29% for the 32-trading-day [-30,1] window relative to the announcement of a

break. We revisit this regularity by examining how the length of the string and parameters

of the transition matrix and AIS affect the market reaction to breaks.

7In order to determine M(t), we will need to specify the initial belief M(0). The choice of initial beliefwill not affect the simulation analysis given long enough histories simulated.

8The qualitative patterns of the results are not sensitive the choice of these variables.

19

To calculate the market reaction to breaks, we simulate the model over T periods9 for

N idiosyncratic histories (“firms”). We define a sequence of consecutive good signals as a

“string”, which follows a bad signal and is followed by a bad signal. For example, a string of

length 3 looks like “...LHHHL...”. For each period, we form an equal-weighted portfolio of

all firms with a L signal following exactly s consecutive H signals, where s=1, 2, ..., 8 is the

length of earnings strings. We plot the average of portfolio returns (and their difference) over

1,000 periods for different lengths of the earnings strings. Panel (a) of Figure 4 shows that

the longer the string, the more negative is the reaction, but the effect of increased length on

amplifying the market reaction diminishes as the length increases.

We compare the model prediction with real data. We measure actual reaction as the

average reaction to breaks of earnings strings of lengths 1 to 8, based on a sample of 1,143,863

firm-quarters over 1963-2013 on Compustat, after excluding firms with fiscal year changes.

Earnings strings are defined as consecutive earnings increases, where “earnings increase” is

defined as earnings per share (EPS) before extraordinary items in the observation quarter

being higher than EPS for the same quarter of the previous year. Earnings announcement

return is measured as the cumulative abnormal return starting 2 trading days before to 1

trading day after the earnings announcement date, where returns are adjusted by value-

weighted market or risk, which is measured by market beta estimated using daily returns

of the previous month. We find that the predicted pattern and actual pattern are similar

(Panel (b) of Figure 4).

Figure 5 simulates the market reaction to string breaks for alternative parameter values

9The number of periods is greater than the previous simulation to ensure the existence of a large numberof earnings strings of various lengths, but comes at a cost of computing time.

20

of the transition matrix and AIS. When we vary the persistence of underlying state, the

market reaction first decreases then increases (Panel (a)). This is due to the diminishing

weight investors assign to the accounting signal as persistence increases from .5 to 1: When

persistence close to 1, investors put little weight on the break signal (L), which they attribute

to noise in the AIS. Therefore, they do not revise their expectation downward by a lot. The

reaction decreases with both informativeness and conservatism (Panels (b) and (c)). This

is intuitive because more informative/conservative AIS makes investors react more strongly

negative to a bag signal which they believe is less likely to be due to noise. This pattern is

also evident in Panel (d), the contour plot in which both c and d vary from .5 to 1.

4.3 Dual Information Systems

The setting with dual information systems shed lights on empirical findings that involve

the comparison between two reported numbers, such as accruals (earnings vs. cash flows)

and book-tax differences. In the following, we discuss how the model can offer testable

predictions regarding each.

4.3.1 The accruals anomaly

The accruals component of earnings negatively predicts future returns (Sloan 1996).

Researchers have proposed various explanations for the accruals anomaly, including investor

fixation on accruals (e.g., Sloan 1996), earnings persistence (e.g., Richardson et al. 2005),

and investment (e.g., Wu et al. 2010). By incorporating both earnings and cash flows, our

model of AIS and investors’ Bayesian learning may be able to yield new insights on factors

underlying the return predictability based on accruals. Let the dual information systems

21

correspond to earnings and cash flows, respectively: < X, Y, Z, ηE, ηCF > for every state xt,

ηE generates an earnings signal yt, and ηCF generates a cash flow signal zt, where

Our main variables of interest are the relative informativeness and relative conservatism

of cash flows compared with earnings. Accruals are defined as the difference between earnings

and cash flows, i.e.,

Accrualst = yt − zt ∈ {−(H − L), 0, (H − L)}. (4.1)

To study the accruals anomaly, we simulate N idiosyncratic firms for T periods, and form

portfolios based on the level of accruals, Accrualst. Specifically, for each period, we form a

zero-investment portfolio by buying all firms with negative accruals in the previous period

(i.e., Accrualst−1 = −(H − L)) and shorting all firms with positive accruals in the previous

period (i.e., Accrualst−1 = H − L). We use the equal-weighted returns as portfolio return.

The existence of accruals anomaly would be indicated by a positive return to the hedge

portfolio over some forecasting horizon.

Figure 6 reports the simulation results. Panel A reports the return to an average hedging

portfolio formed based on the accruals τ periods earlier, where τ = 1, 2, ..., 7 is on the x-

axis. The parameters are (a, b, cE, dE, cCF, dCF) = (.75, .75, .75, .75, .6, .6). Panels B, C, and

D report the variations of the one-period ahead accruals-based portfolio returns with respect

to: (B) the persistence of the state process, i.e., a = b ∈ [.5, .95], for (cE, dE, cCF, dCF) =

(.75, .75, .6, .6); (C) the relative informativeness of cash flows, i.e., ∆ = cCF−cE = dCF−dE ∈

[−.25, .25], for (a, b, cE, dE) = (.75, .75, .75, .75); and (D) the relative conservatism of cash

flows, i.e., ∆ = cCF − cE = dE − dCF ∈ [0, .25], for (a, b, cE, dE) = (.75, .75, .75, .75).

Figure 6 shows that when cash flows are less informative about the underlying states

22

than earnings (which is consistent with the central tenet of the accrual-based accounting),

the accruals anomaly exists. Panel A reports the buy-and-hold return to an average hedging

portfolio formed at a certain period based on the accruals of the last period, and held for

τ = 1, 2, ..., 7 periods. The return predictability diminishes as we hold the portfolios for

more periods into the future. The accruals anomaly first increases but then decreases as

the underlying state process is more persistent (Panel B); it decreases with the relative

informativeness and conservatism of cash flows benchmarked against earnings (Panels C and

D).

Panel C suggests that the accruals anomaly only exists when cash flows are less informa-

tive than earnings about the underlying states. This is consistent with the basic notion that

net income is considered a better indicator of future operating cash flows than is current net

operating cash flow (Spiceland et al. 2013, p.7).

Over time, the accruals anomaly has become less significant (Green et al. 2011). Based

on our model prediction, this could be explained by the increasing relative informativeness

of cash flows relative to earnings, which have been shown to be lower quality in recent years,

partially due to large numbers of write-offs and other one-time items.

4.3.2 Book-tax differences (BTDs) and future stock returns

Prior studies document that return predictability based on book-tax differences (e.g., Lev

and Nissim 2006). Our model can also shed light on how BTDs predict future stock returns.

Let the dual information systems correspond to book income (earnings) and taxable income,

respectively: < X, Y, Z, ηBook, ηTax > for every state xt, ηBook generates an earnings signal

yt, and ηTax generates a cash flow signal zt.

23

A higher BTD relative to other firms indicates that taxable income is more conservative

than book income, which could be due to either lower conservatism in book income (Pratt

2005)10 or greater conservatism in taxable income (Heltzer 2009). To the extent that more

conservative tax income also partially means more informative tax income relative to book

income, the model predicts that BTDs are positively associated with future stock returns.

5 Concluding Remarks

This paper proposes a framework for understanding the role of AIS in accounting-based

stock return regularities. The model generate predictions on the market reactions to ac-

counting signals and return predictabilities which are consistent with a battery of empirical

regularities on the relationship between accounting information and stock returns.

There are several limitations to the current framework. First, this paper does not address

the discretionary reporting decisions. Instead, our focus is to study the properties and

implications of an exogenous AIS. Second, even though the Bayesian belief of investors is

consistent various empirical regularities, we acknowledge that other schemes of learning,

including seemingly irrational beliefs such as , such as limited memory and regime-shifting

beliefs (e.g., Barberis et al. 1998), may also produce empirical regularities.

10This statement is based on the assumption that book income is more susceptible to reporting discretion.As Pratt (2005) notes, “the extent to which reported income before taxes exceeds (or is less than) taxableincome indicates how conservative reported income is. Ratios (of reported book income before taxes totaxable income) around 1 or less indicate relatively conservative levels, while reported income becomesincreasingly less conservative as the ratio grows.”

24

Appendix A. General Model Setup

In Appendix A, we extend the 2 by 2 case to more general cases with nx states and ny

(and nz) signals.

A.1 Single Accounting Information System

Suppose a firm’s underlying state (e.g., profitability) xt can take one of the nx values

from X, the set of all possible states by X = {Xi : i = 1, ..., nx}. The law of motion for xt

is described by a Markov transition matrix P = (Pij)nx×nx with

Pij = Pr(xt+1 = Xj|xt = Xi) (A.1)

The sum of each row of P is 1, namely,∑nx

j=1 Pij = 1.

Following Marschak and Miyasawa (1968) and Marschak (1971), we introduce accounting

information system as < X, Y, η >, where Y = {Yi : i = 1, ..., ny} is the set of possible signals,

and η is a measurement matrix which maps the states to accounting signals. After observing

state xt, a firm manager use the accounting information system to generate a signal yt ∈ Y ,

which is a noisy function of xt. AIS can be described by η = (ηij)nx×ny , where

ηij = Pr(yt = yj|xt = xi) (A.2)

The sum of each row of η is 1, namely,∑ny

j=1 ηij = 1. We assume Xi and Yi are in ascending

order with respect to the subscript.

Some special cases of the information system are easy to define. An information system

η is said to be a null information system if its rows are identical, i.e., ηij = ζj for all i, where∑ny

j=1 ζj = 1; when nx = ny, η is said to be a perfect information system if η is a permutation

matrix.

Denote investor belief at t by M(t) = [M1(t), ..., Mnx(t)]′, where Mi(t) = Pr{xt =

Xi|yt}, yt = {yt, ..., y0} is the history of accounting signals. The following proposition

characterizes the law of motion for investor beliefs.

Lemma A.1 Upon observing yt+1 = yj, an investor’s belief is given by the following

25

recursive formula:

M(t+ 1) =M(t+ 1)

M(t+ 1) · 1(A.3)

where M(t+ 1) ≡ diag(ηj)P′M(t), ηj = [η1j, ..., ηnxj]

′ is the j-th column of η.

A.2 Dual Information Systems

Suppose the underlying state xt is imperfectly revealed by an information system with

two information channels, < X, Y, Z, η1, η2 > for every state xt, η1 generates a signal yt, and

η2 generates a different signal zt ∈ Z, where Z = {Zi : i = 1, ..., nz} and Zi are in ascending

order with respect to the subscript.

Lemma A.2 Upon observing yt+1 = Yj and zt+1 = Zk, an investor’s belief is given by the

following recursive formula:

M(t+ 1) =M(t+ 1)

M(t+ 1) · 1(A.4)

where M(t+ 1) ≡ diag(η1j ◦ η2

k)P′M(t), with η1

j = [η11j, ..., η

1nxj]

′ being the j-th column of η1

and η2k = [η2

1k, ..., η2nxk

]′ being the k-th column of η2. Here, η1j ◦ η2

k denotes their Hadamard

Product.

A.3 Stock Prices

Interpreting xt as the underlying cash flows of period t, the post-accounting-signal price

is the cum-dividend price, pt is given by the following lemma.

Lemma A.3 After observing accounting signals in each period t, stock price pt is given by

pt = M ′t

(I − 1

1 + δP)−1

X (A.5)

where δ is the discount rate and I is the identity matrix of size nx, and X is the vector of

possible values for xt ordered by subscripts.

26

Appendix B: Proofs

Proof of Lemma 1.

For brevity, we only prove the expression for µt|yt=L. µt|yt=H can be derived analogously.

By Bayes’ Rule,

µt|yt=L = Pr(xt = B|yt = L,yt−1)

=Pr(yt = L|xt = B)Pr(xt = B|yt−1)

Pr(yt = L|xt = B,yt−1)

=

∑xt−1=B,G Pr(yt = L|xt = B)Pr(xt = B|xt−1)Pr(xt−1|yt−1)∑xt=B,G

∑xt−1=B,G Pr(yt = L|xt)Pr(xt|xt−1)Pr(xt−1|yt−1)

=caµt−1 + c(1− b)(1− µt−1)

(caµt−1 + c(1− b)(1− µt−1)) + ((1− d)(1− a)µt−1 + (1− d)b(1− µt−1))

=c(a+ b− 1)µt−1 + c(1− b)

(c+ d− 1)(a+ b− 1)µt−1 + (1− d)b+ c(1− b)(B.1)

Proof of Proposition 1. For notational brevity, let gL(µ) and gH(µ) denote the belief

updating functions given the belief from last period being µt = µ:

gL(µ) = µt+1|yt+1=L,µt=µ (B.2)

gH(µ) = µt+1|yt+1=H,µt=µ (B.3)

Suppose Conditions 1-2 are met, i.e., a + b ≥ 1 and c + d ≥ 1. It is straightforward to

show that both gL(µ) and gH(µ) are increasing functions for µ ∈ [0, 1]:

g′L =c(1− d)(a+ b− 1)

(c((a− 1)µ+ 1) + (a− 1)(d− 1)µ+ b(µ− 1)(c+ d− 1))2≥ 0 (B.4)

g′H =(1− c)d(a+ b− 1)

(acµ+ adµ− aµ+ b(µ− 1)(c+ d− 1)− cµ+ c− dµ+ µ− 1)2≥ 0 (B.5)

Additionally, we can show that gL(µ) is a concave function for µ ∈ [0, 1], i.e.,

g′′L =2c(d− 1)(a+ b− 1)2(c+ d− 1)

(c((a− 1)µ+ 1) + (a− 1)(d− 1)µ+ b(p− 1)(c+ d− 1))3≤ 0; (B.6)

and that gH(µ) is a convex function for µ ∈ [0, 1], i.e.,

g′′H(µ) =2(c− 1)d(a+ b− 1)2(c+ d− 1)

(acµ+ adµ− aµ+ b(µ− 1)(c+ d− 1)− cµ+ c− dµ+ µ− 1)3≥ 0. (B.7)

27

It is also easy to show that gL(µ) ≥ µ is equivalent to

0 ≤ µ ≤ µ (B.8)

where µ = 12

(√c(a2c+4a(d−1)−4d+4)−2(a−2)bc(d−1)+b2(d−1)2

(a+b−1)2(c+d−1)2+ (a−2)c+b(2c+d−1)

(a+b−1)(c+d−1)

). and that gH(µ) ≤

µ is equivalent to

µ ≤ µ ≤ 1 (B.9)

where µ = 12

(a(c−1)+b(2c+d−2)−2c+2

(a+b−1)(c+d−1)−√

a2(c−1)2−2a(b−2)(c−1)d+d(b2d+4b(c−1)−4c+4)(a+b−1)2(c+d−1)2

). It is also easy

to show that µ ≤ µ holds.

Therefore, for ∀µ ∈ [µ, µ], we have µ ≤ gL(µ) ≤ µ and µ ≤ gH(µ) ≤ µ. In other words,

if we start from µt ∈ [µ, µ], µt+1 will always stay within the range [µ, µ].

For ∀µ ∈ [0, µ), we have gL(µ) > µ and gH(µ) > µ. In other words, if we start from

µt ∈ [0, µ), µt+1 will eventually rise to the range [µ, µ].

For ∀µ ∈ (µ, 1], we have gL(µ) < µ and gH(µ) < µ. In other words, if we start from

µt ∈ (µ, 1], µt+1 will eventually fall to the range [µ, µ].

Proof of Corollary 1. Omitted for brevity. It can be easily verified by checking the sign

of the derivatives given Conditions 1 and 2.

Proof of Lemma 2. For brevity, we only prove the expression for µt|yt=L,zt=L. By Bayes’

Rule,

µt|yt=L,zt=L = Pr(xt = B|yt = L, zt = L,yt−1, zt−1)

=Pr(yt = L, zt = L|xt = B)Pr(xt = B|yt−1, zt−1)

Pr(yt = L, zt = L|xt = B,yt−1, zt−1)

=

∑xt−1=B,G Pr(yt = L, zt = L|xt = B)Pr(xt = B|xt−1)Pr(xt−1|yt−1)∑xt=B,G

∑xt−1=B,G Pr(yt = L, zt = L|xt)Pr(xt|xt−1)Pr(xt−1|yt−1)

=c1c2aµt−1 + c1c2(1− b)(1− µt−1)

(c1c2aµt−1 + c1c2(1− b)(1− µt−1)) + ((1− d1)(1− d2)(1− a)µt−1 + (1− d1)(1− d2)b(1− µt−1))

=c1c2((a+ b− 1)µt−1 + 1− b)

c1c2((a+ b− 1)µt−1 + 1− b) + (1− d1)(1− d2)((1− a− b)µt−1 + b)(B.10)

The proofs for the other three scenarios (µt|yt=L,zt=H , µt|yt=H,zt=L, and µt|yt=H,zt=H) are

analogous.

Proof of Proposition 2. Define gij(µ) ≡ µt+1|yt+1=i,zt+1=j,µt=µ, where i, j ∈ {L,H}.

28

It is easy to show that given Conditions 1 and 3, i.e., for (a, b, c1, d1, c2, d2) such that

a, b, c1, d1, c2, d2 ∈ (0, 1), a + b > 1, c1 + d1 > 1 and c2 + d2 > 1, the following two in-

equalities always hold:

gHH(µ) < gLH(µ) < gLL(µ) (B.11)

gHH(µ) < gHL(µ) < gLL(µ) (B.12)

Therefore, in order to bound the value of µt, we only need to consider the bounds of

gLL(µ) and gHH(µ).

We can show that gLL(µ) ≥ µ is equivalent to

0 ≤ µ ≤ µ∗∗ (B.13)

where µ∗∗ is given by (2.11), and that gHH(µ) ≤ µ is equivalent to

µ∗ ≤ µ ≤ 1 (B.14)

where µ∗ is given by (2.10). These conditions ensure that if yt+1 = L and zt+1 = L, then

µt+1 ≥ µt; if yt+1 = H and zt+1 = H, then µt+1 ≤ µt.

It is also easy to show that the second order conditions for concavity/convexity are met.

For ∀a, b, c, d such that Conditions 1 and 3 are met, we have

g′′LL(µ) = −2c1c2(d1 − 1)(d2 − 1)(a+ b− 1)2(c1c2 − d1d2 + d1 + d2 − 1)

(c1c2((a− 1)µ+ 1)− (a− 1)(d1 − 1)(d2 − 1)µ+ b(p− 1)(c1c2 − d1d2 + d1 + d2 − 1))3≤ 0 (B.15)

g′′HH(µ) =2(c1 − 1)(c2 − 1)d1d2(a+ b− 1)2(c1(−c2) + c1 + c2 + d1d2 − 1)

(c1(c2 − 1)((a− 1)µ+ 1)− ac2µ− ad1d2µ+ ap+ b(µ− 1)(c1(c2 − 1)− c2 − d1d2 + 1) + c2µ− c2 + d1d2µ− µ+ 1)3

≥ 0 (B.16)

The rest of the proof is analogous to that of Proposition 1.

Proof of Corollary 2. Analogous to that of Corollary 1.

Proof of Lemma 3. The risk-neutral cum-dividend price is equal to the discounted ex-

pected future cash flows. Given that that 11+δ

< 1 ensures the convergence of I + 11+δ

P +

1(1+δ)2

P 2 + ... = (I − 11+δ

P )−1, we have

pt = (µt, 1− µt)(I − 1

1 + δP

)−1

X (B.17)

29

where X = (B,G)′.

Equation (B.17) can be easily rewritten as

pt =1 + δ

δ(2− a− b+ δ)

(G(1− a+ δ) +B(1− b)− δ(G−B)µt

). (B.18)

Proof of Lemma 4. For a Bayesian investor, equation (3.1) follows directly from the fact

that Eit [µt] = µt. To prove equation (3.2), we need to derive an expression for Ei

t [µt+1|µt].

Note that

Eit [µt+1|µt] = Pr(yt+1 = L|µt) · µt+1|yt+1=L + Pr(yt+1 = H|µt) · µt+1|yt+1=H (B.19)

where

Pr(yt+1 = L|µt) =∑

xt+1∈{B,G}

∑xt∈{B,G}

Pr(yt+1 = L|xt+1)Pr(xt+1|xt)Pr(xt|µt)

=(µta+ (1− µt)(1− b)

)c+

(µt(1− a) + (1− µt)b

)(1− d) (B.20)

Pr(yt+1 = H|µt) =∑

xt+1∈{B,G}

∑xt∈{B,G}

Pr(yt+1 = L|xt+1)Pr(xt+1|xt)Pr(xt|µt)

=(µta+ (1− µt)(1− b)

)(1− c) +

(µt(1− a) + (1− µt)b

)d (B.21)

µt+1|yt+1=L =c(a+ b− 1)µt + c(1− b)

(c+ d− 1)(a+ b− 1)µt + (1− d)b+ c(1− b)(B.22)

µt+1|yt+1=H =(1− c)(a+ b− 1)µt + (1− c)(1− b)

(1− c− d)(a+ b− 1)µt + db+ (1− c)(1− b)(B.23)

It follows that

Eit [µt+1|µt] = aµt + (1− b)(1− µt). (B.24)

Based on equation (2.13), it is straightforward to show that the expected price change from

an investor’s perspective is:

Eit [pt+1 − pt] =

1 + δ

2− a− b+ δ(G−B)

((2− a− b)µt − 1 + b

)(B.25)

For an empiricist, the expectation of current period belief is

Eet [µt] =

∫µt

µtdF (µt) = πB =1− b

2− a− b(B.26)

30

Therefore,

Eet [pt] =

1 + δ

δ(2− a− b+ δ)

(G(1− a+ δ) +B(1− b)− δ(G−B)πB

)(B.27)

Eet [pt+1 − pt] =

1 + δ

2− a− b+ δ(G−B)

((2− a− b)πB − 1 + b

)= 0 (B.28)

Proof of Proposition 3.

Eet [pt|yt = H]− Ee

t [pt|yt = L] = − 1 + δ

2− a− b+ δ(G−B)

(Et[µt|yt = H]− Et[µt|yt = L]

)= − 1 + δ

2− a− b+ δ(G−B)

∫µt−1

(µt|yt=H − µt|yt=L

)dF (µt−1)

≥ 0 (B.29)

The last inequality obtains because the integrand is negative for µt−1 ∈ (µ, µ).

Proof of Proposition 4. Suppose the earnings string is of length s = 1, i.e., yt = L, yt−1 =

H. The conditional expectation of price change for an empiricist is

Eet [pt − pt−1|yt = L, yt−1 = H]

=− 1 + δ

2− a− b+ δ(G−B)Ee

t [µt − µt−1|yt = L, yt−1 = H]

=− 1 + δ

2− a− b+ δ(G−B)

∫µt−1

(gL(µt−1)− µt−1

)dF (µt−1|yt−1 = H)

≤0 (B.30)

because gL(µt−1) ≥ µt−1 for µt−1 ∈ [µ, µ].

Suppose the earnings string is of length s = 2, i.e., yt = L, yt−1 = yt−2 = H. The

conditional expectation of price change for an empiricist is

Eet [pt − pt−1|yt = L, yt−1 = yt−2 = H]

=− 1 + δ

2− a− b+ δ(G−B)Ee

t [µt − µt−1|yt = L, yt−1 = yt−2 = H]

=− 1 + δ

2− a− b+ δ(G−B)

∫µt−1

(gL(µt−1)− µt−1

)dF (µt−1|yt−1 = yt−2 = H) (B.31)

≤0 (B.32)

31

Now we would like to find conditions for

Eet [pt − pt−1|yt = L, yt−1 = H] ≥ Ee

t [pt − pt−1|yt = L, yt−1 = yt−2 = H] (B.33)

This is equivalent to∫µt−1

(gL(µt−1)− µt−1) dF (µt−1|yt−1 = H) ≤∫µt−1

(gL(µt−1)− µt−1) dF (µt−1|yt−1 = yt−2 = H)

(B.34)

Define FH(µt−1) = F (µt−1|yt−1 = H) and FHH(µt−1) = F (µt−1|yt−1 = yt−2 = H). By

integration by parts, the left hand side of (B.34) is∫µt−1

(gL(µt−1)− µt−1) dF (µt−1|yt−1 = H)

= (gL(µ)− µ)︸ ︷︷ ︸=0

FH(µ)︸ ︷︷ ︸=1

−(gL(µ)− µ

)FH(µ)︸ ︷︷ ︸

=0

−∫ µ

µ

FH(µt−1) (g′L(µt−1)− 1) dµt−1

=−∫ µ

µ

(g′L(µt−1)− 1)FH(µt−1)dµt−1 (B.35)

Similarly, the right hand side is∫µt−1

(gL(µt−1)− µt−1) dF (µt−1|yt−1 = yt−2 = H) = −∫ µ

µ

(g′L(µt−1)− 1)FHH(µt−1)dµt−1

(B.36)

Therefore, inequality (B.34) becomes∫ µ

µ

(g′L(µt−1)− 1)FH(µt−1)dµt−1 ≥∫ µ

µ

(g′L(µt−1)− 1)FHH(µt−1)dµt−1 (B.37)

A sufficient condition for (B.36) is

(g′L(µt−1)− 1)FH(µt−1) ≥ (g′L(µt−1)− 1)FHH(µt−1) (B.38)

for ∀µt−1. In the following, we first prove

FH(µt−1) ≤ FHH(µt−1), (B.39)

and derive a sufficient condition for the above inequality to hold.

32

By definition, for a given µt−3,

FH(µt−1) =F (µt−1|yt−1 = H) = Pr(gH(µt−2) ≤ µt−1) = Pr(µt−2 ≤ g−1H (µt−1))

=γPr(gL(µt−3) ≤ g−1H (µt−1)) + (1− γ)Pr(gH(µt−3) ≤ g−1

H (µt−1)) (B.40)

where γ = Pr(yt−2 = L);

FHH(µt−1) =F (µt−1|yt−1 = yt−2 = H) = Pr(gH(gH(µt−3)) ≤ µt−1)

=Pr(gH(µt−3) ≤ g−1H (µt−1)) (B.41)

Because gL(µt−3) ≥ gH(µt−3) for ∀µt−3, it follows that

Pr(gL(µt−3) ≤ g−1H (µt−1)) ≤ Pr(gH(µt−3) ≤ g−1

H (µt−1)) (B.42)

and therefore

FH(µt−1) ≤ FHH(µt−1) (B.43)

for ∀µt−1 ∈ [µ, µ]. In other words, FH first-order stochastically dominates (f.o.s.d.) FH .

Given (B.43), a sufficient condition for (B.38) to hold is

g′L(µt−1)− 1 ≤ 0. (B.44)

for ∀µt−1. It is easy to show that (B.44) is met when either of the following two conditions

(in addition to Conditions 1 and 2) is true:

(i) 0 ≤ b ≤ b∗, where b∗ =c(

(2c+d−1)−√

(1−d)(4c+3d−3))

2(c+d−1)2;

(ii) b∗ ≤ b ≤ 1 and 0 ≤ a ≤ a∗, where a∗ = b2(c+d−1)2−bc(2c+d−1)+c(c−d+1)c(1−d)

;

Now let us consider longer earnings strings. Note that based on the proof of (), analogous

arguments for longer sequences of H signals can be proved by induction. For example, FHH

first-order stochastically dominates (f.o.s.d.) FHHH , and so forth. As the earnings string

becomes infinitely long, we have

lims→∞

µt−1 = µ (B.45)

and

lims→∞

FHH...H(µt−1) = 1 (B.46)

33

As a result,

lims→∞

Eet [pt − pt−1|yt = L, yt−1 = ... = yt−s = H] = Ee

t [pt − pt−1|yt = L, µt−1 = µ]

=− 1 + δ

2− a− b+ δ(G−B)

( c(a+ b− 1)µ+ c(1− b)(c+ d− 1)(a+ b− 1)µ+ (1− d)b+ c(1− b)

− µ)

(B.47)

Analogously, if the investor observes a sequence of bad news before seeing a break, the

market reaction will be

lims→∞

Eet [pt − pt−1|yt = H, yt−1 = ... = yt−s = L] = Ee

t [pt − pt−1|yt = H,µt−1 = µ]

=− 1 + δ

2− a− b+ δ(G−B)

( (1− c)(a+ b− 1)µ+ (1− c)(1− b)(1− c− d)(a+ b− 1)µ+ db+ (1− c)(1− b)

− µ)

(B.48)

Proof of Proposition 5. Recall the price change is given by

pt+1 − pt = − 1 + δ

2− a− b+ δ(G−B)(µt+1 − µt). (B.49)

where µt+1 is given by (2.3) and (2.4). Before we derive the expression for ht, it is useful to

observe

Prob(yt+1 = H|yt = H) =∑

xt+1∈{B,G}

∑xt∈{B,G}

Prob(yt+1 = H|xt+1)Prob(xt+1|xt)Prob(xt|yt = H)

= µt(a(1− c) + (1− a)d) + (1− µt)(bd+ (1− b)(1− c))

= (µta+ (1− µt)(1− b))(1− c) + (µt(1− a) + (1− µt)b)d (B.50)

Prob(yt+1 = L|yt = H) =∑

xt+1∈{B,G}

∑xt∈{B,G}

Prob(yt+1 = L|xt+1)Prob(xt+1|xt)Prob(xt|yt = H)

= µt(ac+ (1− a)(1− d)) + (1− µt)(b(1− d) + (1− b)c)

= (µta+ (1− µt)(1− b))c+ (µt(1− a) + (1− µt)b)(1− d) (B.51)

34

Et(pt+1 − pt|yt = H,µt = µ)

=− 1 + δ

2− a− b+ δ(G−B)Et(µt+1 − µt|yt = G, µt = µ)

=− 1 + δ

2− a− b+ δ(G−B)

[(µ[ac+ (1− a)(1− d)] + (1− µ)[b(1− d) + (1− b)c]

)gB(µ)

+(µ[a(1− c) + (1− a)d] + (1− µ)[bd+ (1− b)(1− c)]

)gG(µ)

]=

1 + δ

2− a− b+ δ(G−B)

((2− a− b)µ− 1 + b

)(B.52)

Similarly,

Et(pt+1 − pt|yt = L, µt = µ) =1 + δ

2− a− b+ δ(G−B)

((2− a− b)µ− 1 + b

)(B.53)

Let φ(µ) = 1+δ2−a−b+δ (G − B)

((2 − a − b)µ − 1 + b

). Note that φ(µ) is a linear increasing

function of µ:

φ′(µ) =(1 + δ)(2− a− b)

2− a− b+ δ(G−B) > 0 (B.54)

Therefore,

Eet (pt+1 − pt|yt = H) =

∫µt

φ(µt)dF (µt|yt = H) (B.55)

Eet (pt+1 − pt|yt = L) =

∫µt

φ(µt)dF (µt|yt = L) (B.56)

This is the key to the return predictability: the distribution of µt conditional on signals

are different between L and H.

Note that with probability 1, µt ∈ [µ, µ]. Therefore, evaluating the integration over the

full support of [0, 1] is equivalent to evaluating the integration over [µ, µ]. Denote FH(µt) =

F (µt|yt = H) and FL(µt) = F (µt|yt = L), we know that FH(µ) = FL(µ) = 0 and FH(µ) =

FL(µ) = 1.

∫µt

µtdFH(µt) =

∫ µ

µ

µtdFH(µt) = µ · FH(µ)− µ · FH(µ)−

∫ µ

µ

FH(µt)dµt

= µ−∫ µ

µ

FH(µt)dµt (B.57)

The inequality∫µtµtdF

H(µt) <∫µtµtdF

L(µt) is equivalent to∫ µµFH(µt)dµt ≥

∫ µµFL(µt)dµt.

In the following, we prove a sufficient condition of the above inequality, namely, FH(µt) ≥

35

FL(µt) for ∀µt.

By definition, for a given µt−1,

FH(µ) = F (µt|yt = H) = Pr(gH(µt−1) ≤ µ) (B.58)

FL(µ) = F (µt|yt = L) = Pr(gL(µt−1) ≤ µ) (B.59)

Given that gL(µt−1) ≥ gH(µt−1) for ∀µt−1, it follows that FH(µ) ≥ FL(µ) for ∀µ.

Proof of Corollary 3. Define

h(µ) = φ(µt|yt=H,µt−1=µ

)− φ(µt|yt=L,µt−1=µ

)= φ

(gH(µ)

)− φ(gL(µ)

), (B.60)

It is easy to show that ∂gL(µ)∂c≥ 0 and ∂gH(µ)

∂c≤ 0 for ∀µ. Therefore,

∂h(µ)

∂c=

(1 + δ)(2− a− b)2− a− b+ δ

(G−B)

(∂gH(µ)

∂c− ∂gL(µ)

∂c

)≤ 0 (B.61)

Therefore,

∂h(µ)

∂c=

∂

∂c

∫ µ

µ

h(µ)dF (µ)

= h(µ)︸︷︷︸−

· ∂µ∂c︸︷︷︸+

−h(µ)︸︷︷︸−

·∂µ

∂c︸︷︷︸−

+

∫ µ

µ

∂h(µ)

∂c︸ ︷︷ ︸−

dF (µ) ≤ 0 (B.62)

Similarly, we can prove that

∂h(µ)

∂d≤ 0. (B.63)

Proof of Proposition 6. The hedge return obtained by trading on the two signals is

Eet (pt+1 − pt|yt = H, zt = L)− Ee

t (pt+1 − pt|yt = L, zt = H) (B.64)

Note that

Eet (pt+1 − pt|µt = µ) =

1 + δ

2− a− b+ δ(G−B)

((2− a− b)µ− 1 + b

)≡ φ(µ) (B.65)

Therefore,

Eet (pt+1 − pt|yt = H, zt = L) =

∫µ

φ(µ)dF (µ|yt = H, zt = L) (B.66)

36

Eet (pt+1 − pt|yt = L, zt = H) =

∫µ

φ(µ)dF (µ|yt = L, zt = H) (B.67)

Recall:

µt|yt=H,zt=L =(1− c1)c2((a+ b− 1)µt−1 + 1− b)

(1− c1)c2((a+ b− 1)µt−1 + 1− b) + d1(1− d2)((1− a− b)µt−1 + b),

(B.68)

µt|yt=L,zt=H =c1(1− c2)((a+ b− 1)µt−1 + 1− b)

c1(1− c2)((a+ b− 1)µt−1 + 1− b) + (1− d1)d2((1− a− b)µt−1 + b),

(B.69)

Note that with probability 1, µt ∈ [µ∗, µ∗∗]. Therefore, evaluating the integration over

the full support of [0, 1] is equivalent to evaluating the integration over [µ∗, µ∗∗]. Denote

FHL(µt) = F (µt|yt = H, zt = L) and FLH(µt) = F (µt|yt = L, zt = H), we know that

FHL(µ∗) = FLH(µ∗) = 0 and FHL(µ∗∗) = FLH(µ∗∗) = 1. Therefore, analogous to (), we

have ∫µt

µtdFHL(µt) = µ∗∗ −

∫ µ∗∗

µ∗FHL(µt)dµt (B.70)

The inequality∫µtµtdF

HL(µt) ≥∫µtµtdF

LH(µt), is equivalent to∫ µ∗∗µ∗

FHL(µt)dµt ≤∫ µ∗∗µ∗

FLH(µt)dµt. In the following, we prove a sufficient condition of the above inequality,

namely, FHL(µt) ≤ FLH(µt) for ∀µt.

By definition, for a given µt−1,

FHL(µ) = Pr(µHL(µt−1) ≤ µ) (B.71)

Assume a, b, c1, d1, c2, d2 ∈ [0, 1], a + b ≥ 1, c1 + d1 ≥ 1, and c2 + d2 ≥ 1. It is easy to show

that

µt|yt=H,zt=Lµt−1=µ ≥ µt|yt=L,zt=H,µt−1=µ (B.72)

iff

1− d1 ≤ c1 ≤c2d2(1− d1)

d1(1− d2) + c2(d2 − d1)(B.73)

But we know that ∀µt−1, µHL(µt−1) ≥ µLH(µt−1) given the assumptions. Therefore,

Pr(µHL(µt−1) ≤ µ) ≤ Pr(µLH(µt−1) ≤ µ)

37

Given that φ(µ) is a linear increasing function of µ, we have

Eet (pt+1 − pt|yt = H, zt = L)− Ee

t (pt+1 − pt|yt = L, zt = H) ≥ 0 (B.74)

iff

1− d1 ≤ c1 ≤c2d2(1− d1)

d1(1− d2) + c2(d2 − d1)(B.75)

where it can be shown that 1− d1 ≤ c2d2(1−d1)d1(1−d2)+c2(d2−d1)

always hold.

Proof of Lemma A.1. This is a standard result for the hidden Markov model, and is also

proved in other texts. Using Bayes’ rule,

Mi(t+ 1) =αi(t+ 1)∑nx

i′=1 αi′(t+ 1)

where αi(t + 1) ≡ Pr(yt+1, xt+1 = Xi) is the joint probability of yt+1 and xt+1 = Xi. We

know that

αi(t+ 1) =nx∑k=1

Pr(y1, y2, ..., yt+1, xt+1 = Xi, xt = Xk)

=nx∑k=1

Pr(y1, y2, ..., yt, xt = Xk) · Pr(yt+1, xt+1 = Xi|xt = Xk, y1, y2, ..., yt)

=nx∑k=1

αk(t) · Pr(yt+1, xt+1 = Xi|xt = Xk)

=nx∑k=1

αk(t) · Pr(yt+1|xt+1 = Xi, xt = Xk) · Pr(xt+1 = Xi|xt = Xk)

=nx∑k=1

αk(t) · Pr(yt+1|xt+1 = Xi) · Pr(xt+1 = Xi|xt = Xk) (B.76)

where the third equality is based on the fact that given xt, xt+1 is independent of all xτ ,

τ = 1, ..., t− 1, and hence yτ . In addition, xt+1 is independent of yt because xt is given.

Therefore, upon observing yt+1 = Yj,

Mi(t+ 1) =

∑k ηijPkiMk(t)∑

i′∑

k ηi′jPki′Mk(t)(B.77)

which is equivalent to the matrix form of the posterior.

38

Proof of Lemma A.2. Using Bayes’ rule, we have

Mi(t+ 1) =αi(t+ 1)∑nx

i′=1 αi′(t+ 1)(B.78)

where αi(t+ 1) ≡ Pr(yt+1, zt+1, xt+1 = Xi) is the joint probability of yt+1, zt+1 and xt+1 =

Xi.

We know that

αi(t+ 1) =nx∑k=1

Pr(yt, yt+1, zt, zt+1, xt+1 = Xi, xt = Xk)

=nx∑k=1

Pr(yt, zt, xt = Xk) · Pr(yt+1, zt+1, xt+1 = Xi|xt = Xk,yt, zt)

=nx∑k=1

αk(t) · Pr(yt+1, zt+1, xt+1 = Xi|xt = Xk)

=nx∑k=1

αk(t) · Pr(yt+1, zt+1|xt+1 = Xi, xt = Xk) · Pr(xt+1 = Xi|xt = Xk)

=nx∑k=1

αk(t) · Pr(yt+1|xt+1 = Xi) · Pr(zt+1|xt+1 = Xi) · Pr(xt+1 = Xi|xt = Xk)

(B.79)

where the third equality is based on the fact that given xt, xt+1 is independent of all xτ ,

τ = 1, ..., t − 1, and hence yτ and zτ , and the last equality uses the fact that yt+1 and zt+1

are conditionally independent given xt+1. In addition, xt+1 is independent of yt because xt

is given.

Therefore, upon observing yt+1 = Yj and zt+1 = Zl,

Mi(t+ 1) =

∑k ηijξilPkiMk(t)∑

i′∑

k ηi′jξi′lPki′Mk(t)(B.80)

which is equivalent to the matrix form of the posterior.

Proof of Lemma A.3. See the proof of Lemma 3.

39

References

[1] Antle, R., J. Demski, and S. Ryan. 1994. Multiple sources of information, valuation, and

accounting earnings. Journal of Accounting, Auditing and Finance 9, 675-696.

[2] Antle, R., and R. Lambert. 1988. Accountants’ loss functions and induced incentives

for conservatism. In Economic Analysis of Information and Contracts: Essays in Honor

of John Butterworth, edited by G. Feltham, A. Amershi, and W. Ziemba. Boston, MA:

Kluwer Academic Publishers.

[3] Barberis, N., A. Shleifer, and R. Vishny. 1998. A model of investor sentiment. Journal of

Financial Economics 49, 307-345.

[4] Barth, M. E., J. A. Elliott, and M. W. Finn. 1999. Market rewards associated with

patterns of increasing earnings. Journal of Accounting Research 37, 387-413.

[5] Berger, J. 1985. Statistical Decision Theory and Bayesian Analysis. New York: Springer-

Verlag.

[6] Blackwell, D. 1953. Equivalent comparisons of experiments. Annals of Mathematical

Statistics, 24, 265-72.

[7] Christensen, J., and J. Demski. 2003. Accounting Theory: An Information Content Per-

spective. McGraw-Hill/Irwin.

[8] Demski, J. 1973. The general impossibility of normative accounting standards. The Ac-

counting Review 48, 718-723.

[9] Gigler, F., C. Kanodia, H. Sapra, and R. Venugopalan. 2009 Accounting conservatism

and the efficiency of debt contracts. Journal of Accounting Research 47, 767-797.

[10] Heltzer, W. 2009. Conservatism and Book-Tax Differences. Journal of Accounting, Au-

diting and Finance 24, 469-504.

[11] Ke, B., S. Huddart, and K. Petroni. 2003. What insiders know about future earnings

and howthey use it: Evidence from insider trades. Journal of Accounting and Economics

35, 315-346.

[12] Kothari, S.P. 2001. Capital market research in accounting. Journal of Accounting Eco-

nomics 31, 105-231.

[13] Lev, B., and D. Nissim. 2004. Taxable income, future earnings, and equity values. The

Accounting Review 79, 1039-1074.

[14] Lewellen, J., and J. Shanken. 2002. Learning, asset-pricing tests, and market efficiency.

Journal of Finance 57, 1113-1145.

40

[15] Marschak, J. 1971. Economics of information systems. Journal of the American Statis-

tical Association 66, 192-219.

[16] Marschak, J., and K. Miyasawa. 1968. Economic comparability of information systems.

International Economic Review 9, 137-174.

[17] Pratt, J. 2005. Financial Accounting in an Economic Context. 6th ed. Hoboken, NJ:

John Wiley & Sons.

[18] Richardson, S., R. Sloan, M. Soliman, and I. Tuna. 2005. Accrual reliability, earnings

persistence and stock prices. Journal of Accounting and Economics 39, 437-485.

[19] Richardson, S., I. Tuna, and P. Wysocki. 2010. Accounting anomalies and fundamental

analysis: A review of recent research advances. Journal of Accounting and Economics

50, 410-454.

[20] Scott, W. 1979. Scoring Rules for Probabilistic Reporting. Journal of Accounting Re-

search 17, 156-178.

[21] Sloan, R. 1996. Do stock prices fully reflect information in accruals and cash flows about

future earnings? The Accounting Review 71, 289-315.

[22] Spiceland, J., J. Sepe, and M. Nelson. 2013. Intermediate Accounting. 7th ed. New York,

NY: McGraw-Hill Irwin.

[23] Wu, J., L. Zhang, and X. Zhang. 2010. The q-theory Approach to Understanding the

Accrual Anomaly. Journal of Accounting Research 48, 177-223.

41

Figure 1: Accounting Information System

Panel A illustrates the time-series structure of the model. Panel B illustrates the law of motion (a Markovprocess) for the underlying state xt and the information system which maps the state to an accounting signalyt.

xt−1 xt xt+1

yt−1 yt yt+1

(a) The time-series structure of the model

B L

G H

c

1−c

1−d

d

a

b

1− a 1− b

(b) The law of motion for xt and the information system

42

Figure 2: Dual Accounting Information Systems

Panel A illustrates the time-series structure of the two-AIS model. Panel B illustrates the law of motion(a Markov process) for the underlying state xt and the information systems which map the state to anaccounting signals yt and zt.

xt−1 xt xt+1

yt−1 yt yt+1

zt−1 zt zt+1

(a) The time-series structure of the model

B LL

G HH

c1

1−c1

1−d 1

d1

c2

1−c 2

1−d2

d2

a

b

1− a 1− b

(b) The law of motion for xt and the information system43

Fig

ure

3:D

iffer

enti

alM

arke

tR

eact

ion

toE

arnin

gsSig

nal

s:T

he

Rol

eofP

andη

rHan

drL

are

the

aver

age

mar

ket

reac

tion

sto

earn

ings

sign

alsH

an

dL

,re

spec

tive

ly.

To

calc

ula

teth

eav

erage

retu

rns,

we

sim

ula

teth

em

od

elov

er1,

000

per

iod

sfo

r1,

000

idio

syn

crat

ich

isto

ries

(“fi

rms”

);fo

rea

chp

erio

d,

we

form

equ

al-

wei

ghte

dp

ort

foli

os

ofH

-an

dL

-firm

s,by

aver

agin

gacr

oss

all

“firm

s”w

ith

the

sam

eea

rnin

gssi

gnal

sH

andL

;w

eth

enta

keth

eav

erage

of

port

foli

ore

turn

s(a

nd

thei

rd

iffer

ence

)ov

er1000

per

iod

sto

getrH

an

drL

(an

drH−rL

).P

anel

(a)

vari

esa

=b∈

[.5,

1],

hold

ingc

=d

=.7

5;

Pan

el(b

)va

riesc

=d∈

[.5,

1],

hold

inga

=b

=.7

5;

Panel

(c)

vari

esc∈

[.5,

1],

hol

din

ga

=b

=.7

5an

dd

=.5

;P

anel

(d)

plo

tsth

eco

nto

ur

of

equ

al-

diff

eren

tial-

retu

rns

for

com

bin

ati

on

sof

diff

eren

tva

lues

ofc

an

dd

forc,d∈

[.5,

1].

0.5

0.6

0.7

0.8

0.9

1−

0.0

15

−0.0

1

−0.0

050

0.0

05

0.0

1

0.0

15

0.0

2

0.0

25

pers

iste

nce o

f underlyin

g s

tate

s

differential earnings response

Ret(

G)

− R

et(

B)

Ret(

G)

Ret(

B)

Pan

elA

:V

aryin

gp

ersi

sten

ce

0.5

0.5

50.6

0.6

50.7

0.7

50.8

0.8

50.9

0.9

51

−0.0

2

−0.0

10

0.0

1

0.0

2

0.0

3

0.0

4

info

rmativeness

differential earnings response

Ret(

G)

− R

et(

B)

Ret(

G)

Ret(

B)

Pan

elB

:V

ary

ing

info

rmati

ven

ess

0.5

0.6

0.7

0.8

0.9

1−

0.0

2

−0.0

10

0.0

1

0.0

2

0.0

3

0.0

4

conserv

atism

differential earnings response

Ret(

G)

− R

et(

B)

Ret(

G)

Ret(

B)

Pan

elC

:V

aryin

gco

nse

rvati

sm

0.00

5