accounting clinic vi mcgraw-hill/irwin copyright © 2013 by the mcgraw-hill companies, inc. all...

TRANSCRIPT

Accounting Clinic VI

McGraw-Hill/Irwin Copyright © 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

With contributions by

Stephen H. Penman – Columbia University

Clinic VI-2

Deferred Taxes: Basics

Deferred taxes arise when income tax expense differs from income tax liabilityThe income tax liability is based on income determined under provisions of the United States Internal Revenue Code and foreign, state, and other taxes (including franchise taxes) based on income.The tax expense is the amount of income taxes (whether or not currently payable or refundable) allocable to a period in the determination of net income.Some of these differences are temporary and some are permanent

Clinic VI-3

Why do we need Deferred Taxes?

Main issue: the need to match tax expense to related accounting income so appropriate after-tax income is reported, independent of when taxes on that income is assessed by tax authorities.

Advantages of deferred taxes:Smoothing of earnings

Better relationship between earningsand income tax expense

effective tax rate reflects statutory rate

Clinic VI-4

Temporary and Permanent Differences

TemporaryTemporary difference.difference.Differences between the taxable amount of a revenue or expense and its reported amount in the financial statements that result in taxable or deductible amounts in future years when the revenue or expense enters the tax return.

Permanent differencesPermanent differences.Permanent differences arise from statutory provisions under which specified revenues are exempt from taxation and specified expenses are not allowable as deductions in determining taxable income. Other permanent differences arise from items entering into the determination of taxable income which are not components of pretax accounting income in any period.

Clinic VI-5

Examples of Permanent Differences

Interest received on municipal obligations

premiums paid on officers' life insurance.

Fines and other expenses that result from a violation of law.

Deduction for dividend received from U.S. corporations.

Percentage depletion of natural resources in excess of their cost.

Clinic VI-6

Examples of Temporary differences

1. Revenues or gains that are taxable after they are recognized in financial income. An asset (for example, a receivable from an installment sale) may be recognized for revenues or gains that will result in future taxable amounts when the asset is recovered.

2. Expenses or losses that are deductible after they are recognized in financial income. A liability (for example, a product warranty liability) may be recognized for expenses or losses that will result in future tax deductible amounts when the liability is settled.

Clinic VI-7

Examples of Temporary differences

3. Revenues or gains that are taxable before they are recognized in financial income. A liability (for example, subscriptions received in advance) may be recognized for an advance payment for goods or services to be provided in future years. For tax purposes, the advance payment is included in taxable income upon the receipt of cash. Future sacrifices to provide goods or services (or future refunds to those who cancel their orders) will result in future tax deductible amounts when the liability is settled.

Clinic VI-8

Examples of Temporary differences

4. Expenses or losses that are deductible before they are recognized in financial income. The cost of an asset (for example, depreciable personal property) may have been deducted for tax purposes faster than it was depreciated for financial reporting. Amounts received upon future recovery of the amount of the asset for financial reporting will exceed the remaining tax basis of the asset, and the excess will be taxable when the asset is recovered.

5. A reduction in the tax basis of depreciable assets because of tax credits. Amounts received upon future recovery of the amount of the asset for financial reporting will exceed the remaining tax basis of the asset, and the excess will be taxable when the asset is recovered.

Clinic VI-9

Deferred Tax Liability

A deferred tax liability is recognized for temporary differences that will result in taxable amounts in future years. For example, a temporary difference is created between the reported amount and the tax basis of an installment sale receivable if, for tax purposes, some or all of the gain on the installment sale will be included in the determination of taxable income in future years. Because amounts received upon recovery of that receivable will be taxable, a deferred tax liability is recognized in the current year for the related taxes payable in future years.

Clinic VI-10

Deferred Tax Asset

A deferred tax asset is recognized for temporary differences that will result in deductible amounts in future years and for carryforwards. For example, a temporary difference is created between the reported amount and the tax basis of a liability for estimated expenses if, for tax purposes, those estimated expenses are not deductible until a future year. Settlement of that liability will result in tax deductions in future years, and a deferred tax asset is recognized in the current year for the reduction in taxes payable in future years.

Clinic VI-11

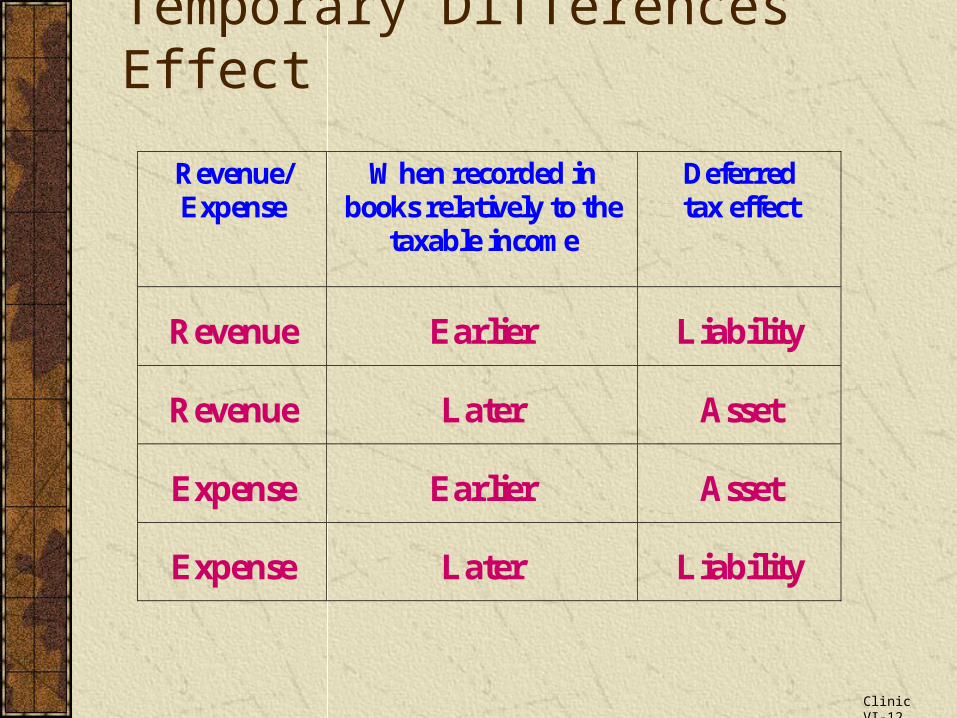

Temporary Differences Effect

Revenue/ Expense

When recorded in books relatively to the

taxable income

Deferred tax effect

Revenue Earlier Liability

Revenue Later Asset

Expense Earlier Asset

Expense Later Liability

Clinic VI-12

Basic Journal Entry to Record Deferred Taxes

Tax LiabilityTax Liability

Income Tax Expense xxxDef.Tax Liability xxx

Taxes Payable xxx

Tax AssetTax Asset

Income Tax Expense xxx Def. Tax Asset xxx Taxes Payable xxx

Clinic VI-13

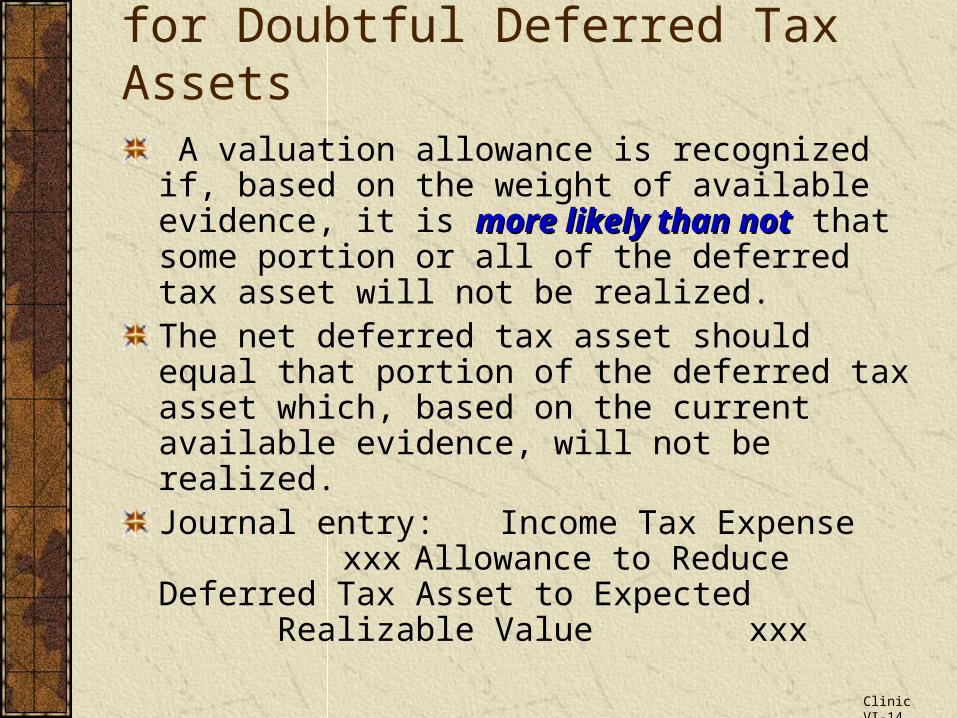

Recording a Valuation Allowancefor Doubtful Deferred Tax Assets

A valuation allowance is recognized if, based on the weight of available evidence, it is more likely more likely than notthan not that some portion or all of the deferred tax asset will not be realized.The net deferred tax asset should equal that portion of the deferred tax asset which, based on the current available evidence, will not be realized.Journal entry:Income Tax Expense xxx

Allowance to ReduceDeferred Tax Asset to Expected

Realizable Value xxx

Clinic VI-14

Example – Deferred Tax Liability - Depreciation

Bryant Corporation purchased a new machine for $100,000 on January 1, 2004.

The machine has a four-year estimated service life and no salvage value.

Bryant’s pretax income for each year 2004 - 2007 is 200,000 before depreciation and taxes.

Clinic VI-15

Bryant Corp. uses straight-line depreciation on its books and MACRS for tax reporting.

For tax purposes the machine is also depreciated over 4 years using MACRS (an accelerated depreciation method).

The depreciation percentages for each of the years are 33%, 44%, 15% and 8%.

Assume a 40% tax rate.

Clinic VI-16

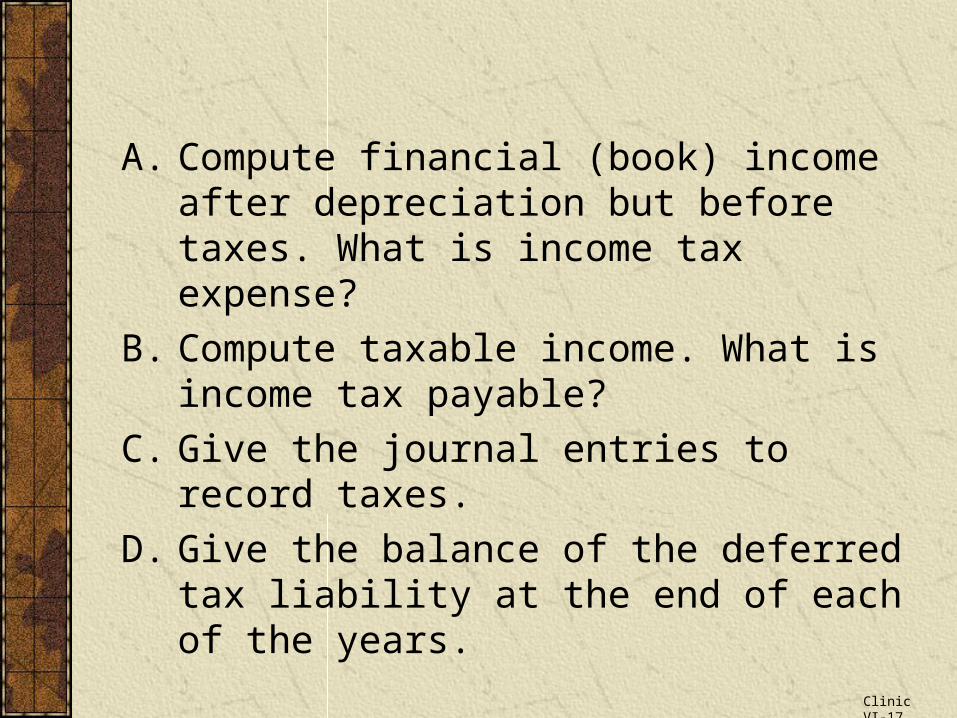

A. Compute financial (book) income after depreciation but before taxes. What is income tax expense?

B. Compute taxable income. What is income tax payable?

C. Give the journal entries to record taxes.

D. Give the balance of the deferred tax liability at the end of each of the years.

Clinic VI-17

Solution

Financial (book) income 2004 2005 2006 2007

Income before Depreciation

Depreciation Expense

($100,000/4)

Income after depreciation but before taxes

Income Tax Expense (40%)

$200,000

(25,000)

$175,000

$70,000

$200,000

(25,000)

$175,000

$70,000

$200,000

(25,000)

$175,000

$70,000

$200,000

(25,000)

$175,000

$70,000

A.

Clinic VI-18

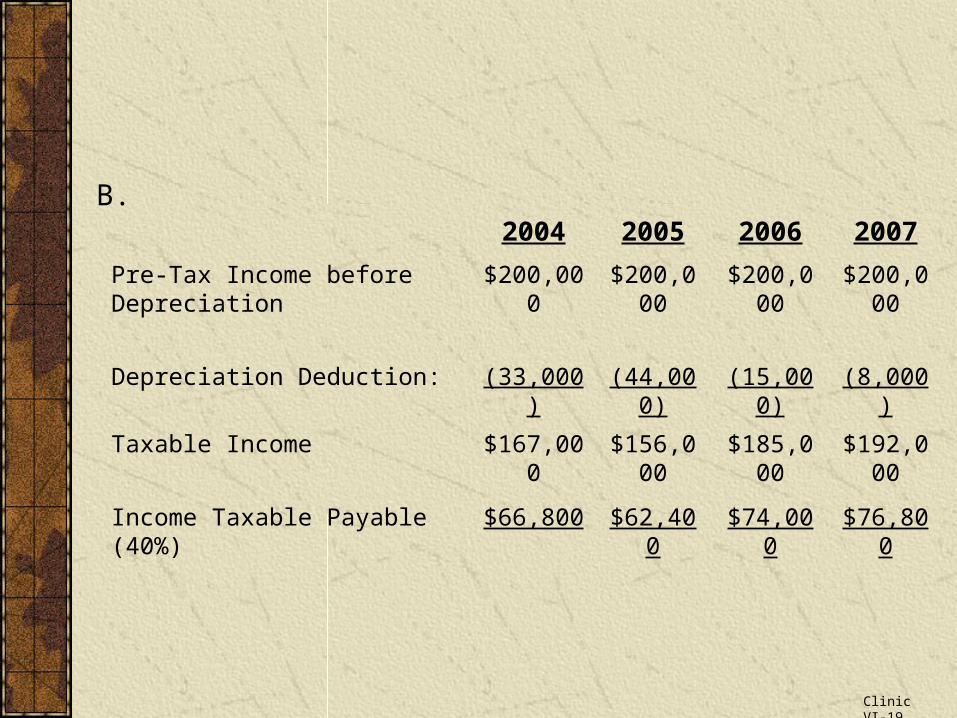

2004 2005 2006 2007

Pre-Tax Income before Depreciation

$200,000 $200,000 $200,000 $200,000

Depreciation Deduction: (33,000) (44,000) (15,000) (8,000)

Taxable Income $167,000 $156,000 $185,000 $192,000

Income Taxable Payable (40%) $66,800 $62,400 $74,000 $76,800

B.

Clinic VI-19

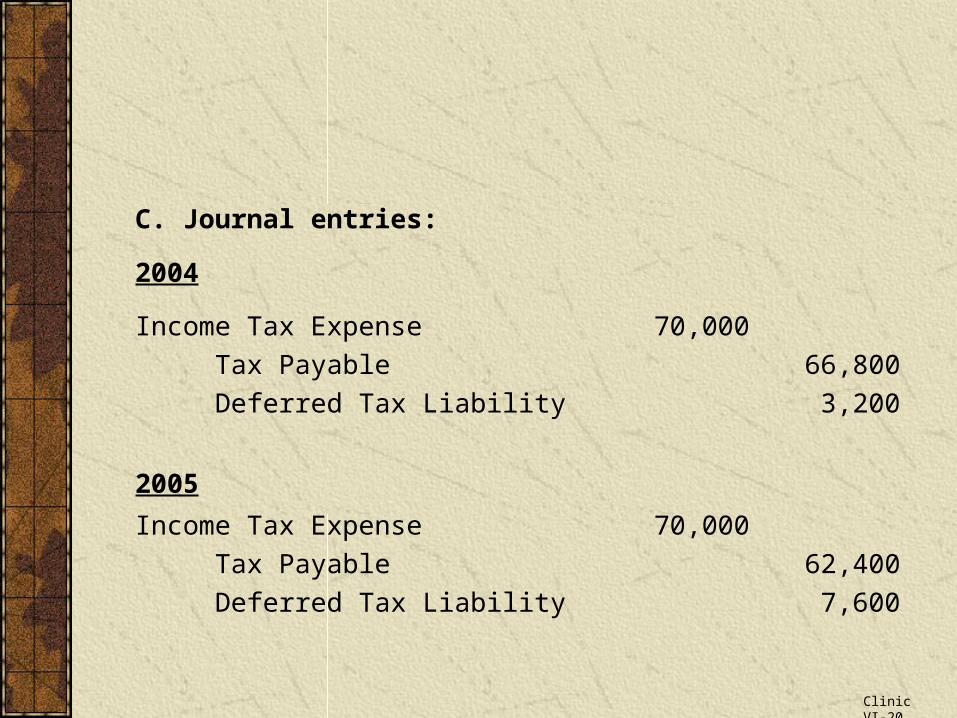

C. Journal entries:

2004

Income Tax Expense

Tax Payable

Deferred Tax Liability

70,000

66,800

3,200

2005

Income Tax Expense

Tax Payable

Deferred Tax Liability

70,000

62,400

7,600

Clinic VI-20

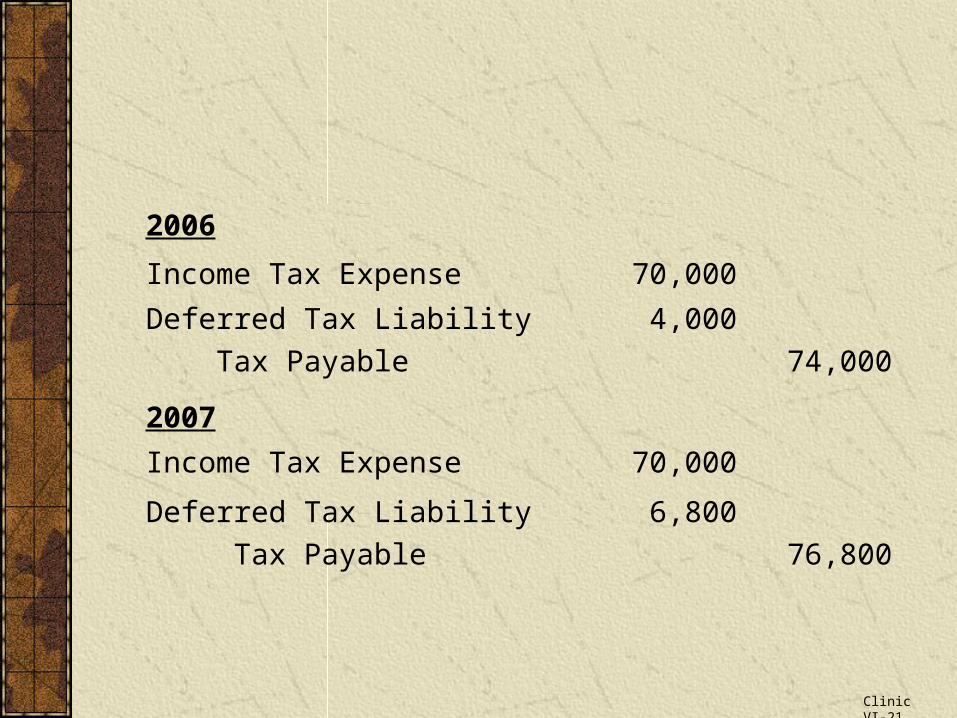

2006

Income Tax Expense 70,000

Deferred Tax Liability

Tax Payable

4,000

74,000

2007

Income Tax Expense 70,000

Deferred Tax Liability

Tax Payable

6,800

76,800

Clinic VI-21

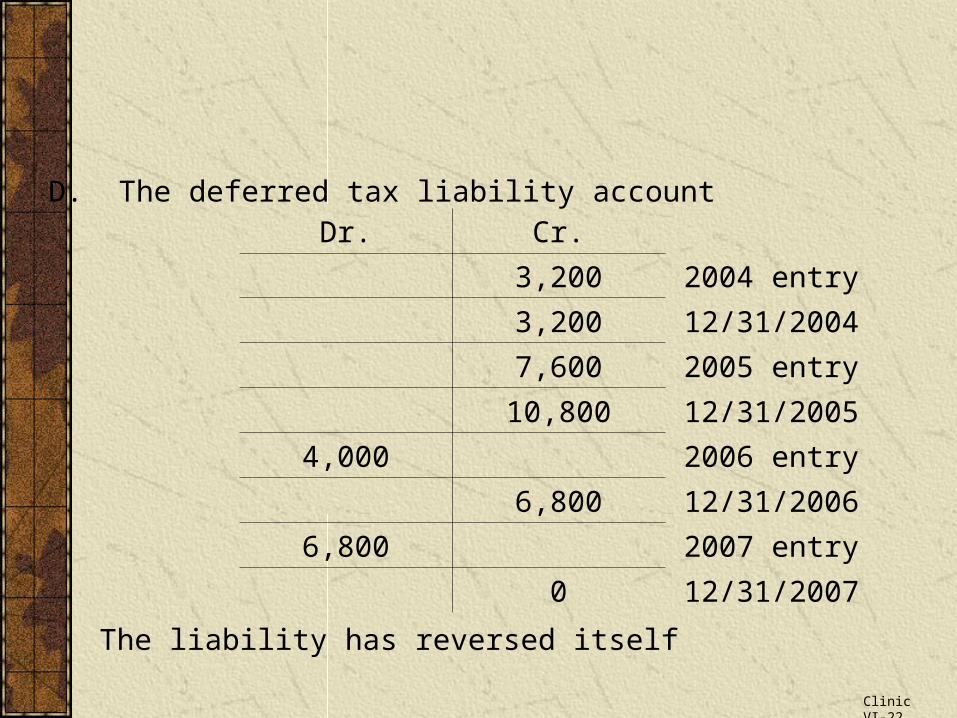

D. The deferred tax liability account

Dr. Cr.

3,200 2004 entry

3,200 12/31/2004

7,600 2005 entry

10,800 12/31/2005

4,000 2006 entry

6,800 12/31/2006

6,800 2007 entry

0 12/31/2007

The liability has reversed itself

Clinic VI-22

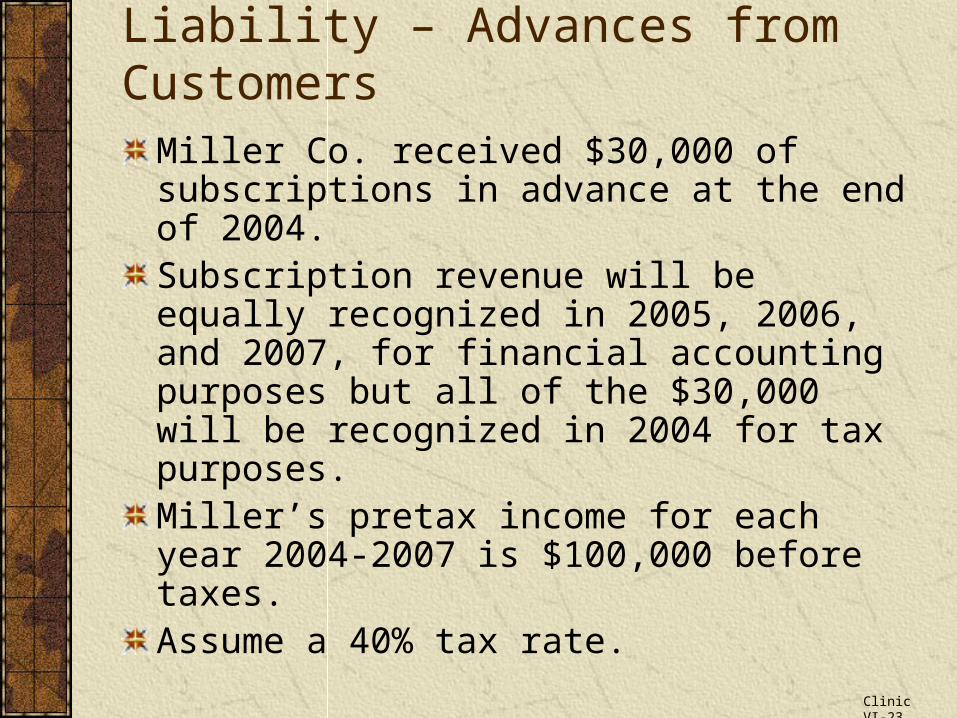

Example - Deferred Tax Liability – Advances from Customers

Miller Co. received $30,000 of subscriptions in advance at the end of 2004. Subscription revenue will be equally recognized in 2005, 2006, and 2007, for financial accounting purposes but all of the $30,000 will be recognized in 2004 for tax purposes. Miller’s pretax income for each year 2004-2007 is $100,000 before taxes.Assume a 40% tax rate.

Clinic VI-23

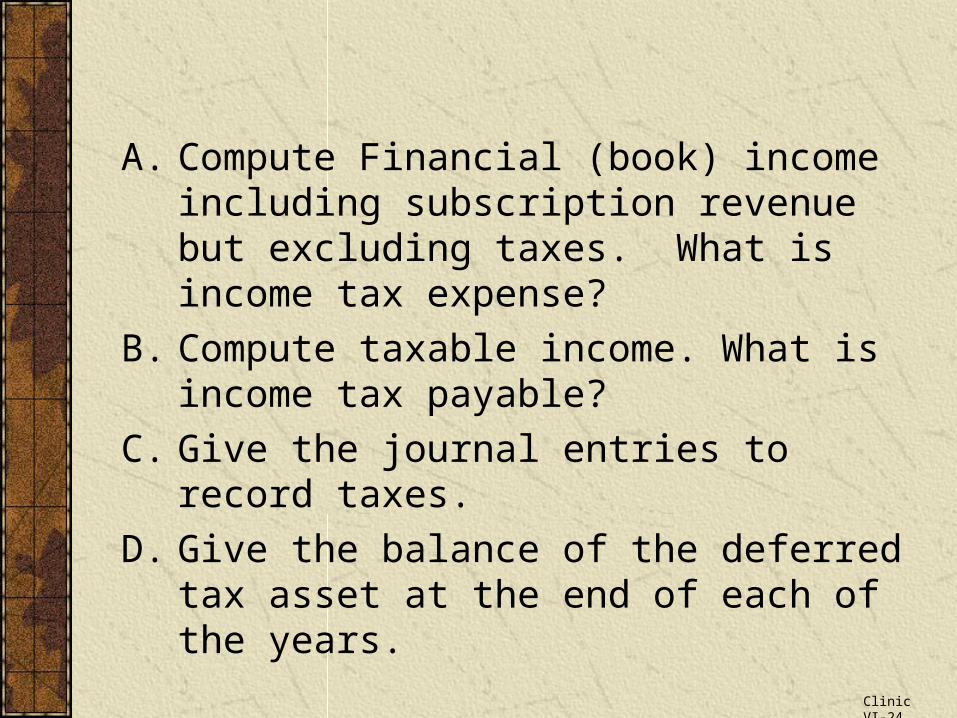

A. Compute Financial (book) income including subscription revenue but excluding taxes. What is income tax expense?

B. Compute taxable income. What is income tax payable?

C. Give the journal entries to record taxes.

D. Give the balance of the deferred tax asset at the end of each of the years.

Clinic VI-24

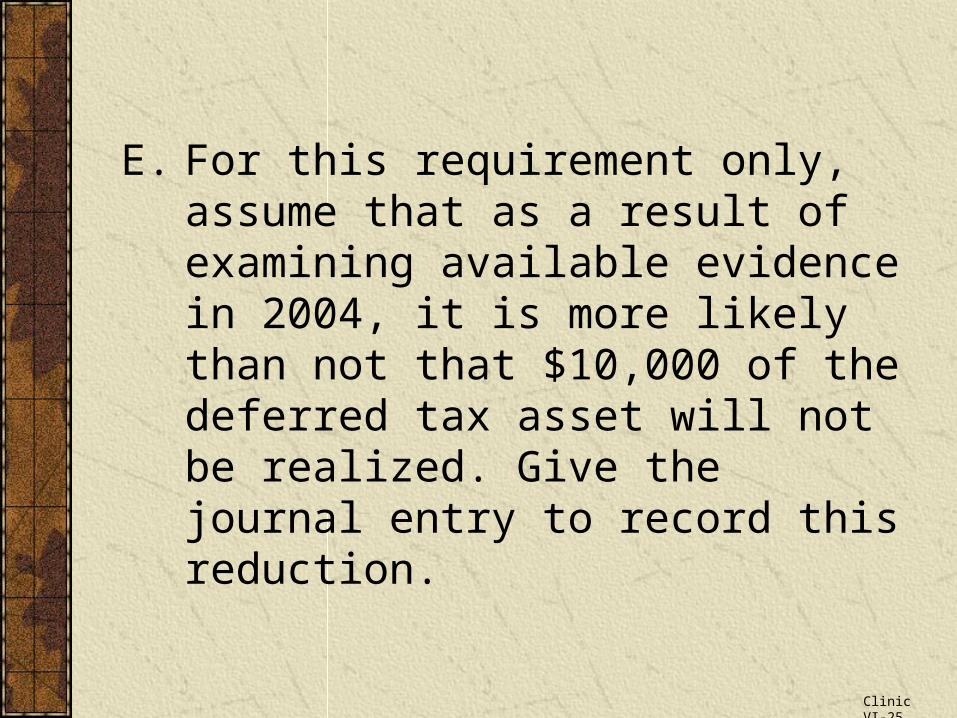

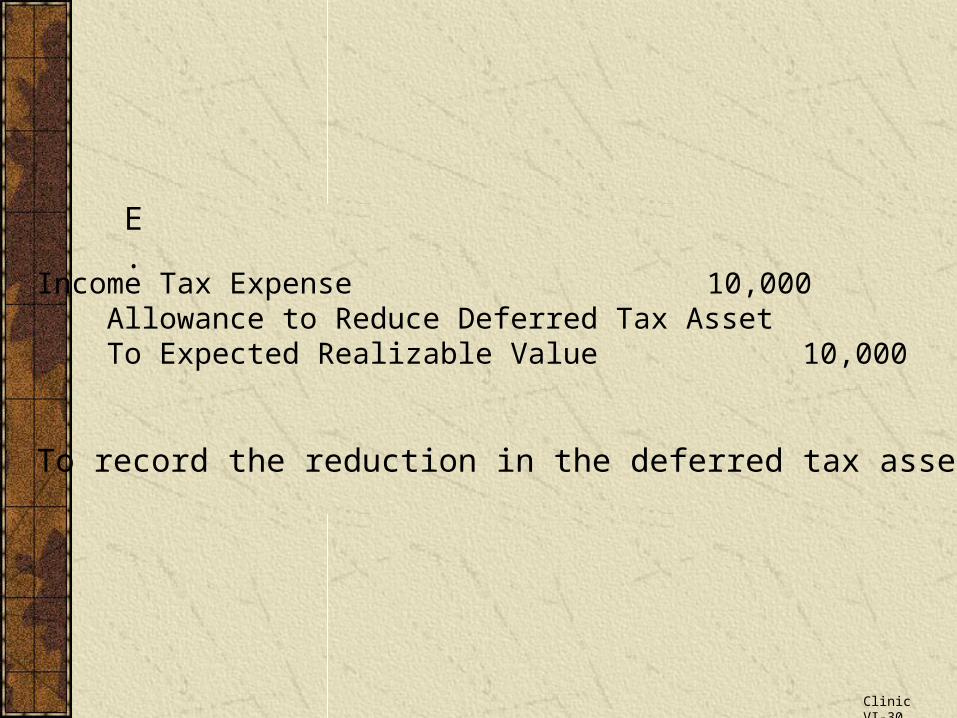

E. For this requirement only, assume that as a result of examining available evidence in 2004, it is more likely than not that $10,000 of the deferred tax asset will not be realized. Give the journal entry to record this reduction.

Clinic VI-25

Solution

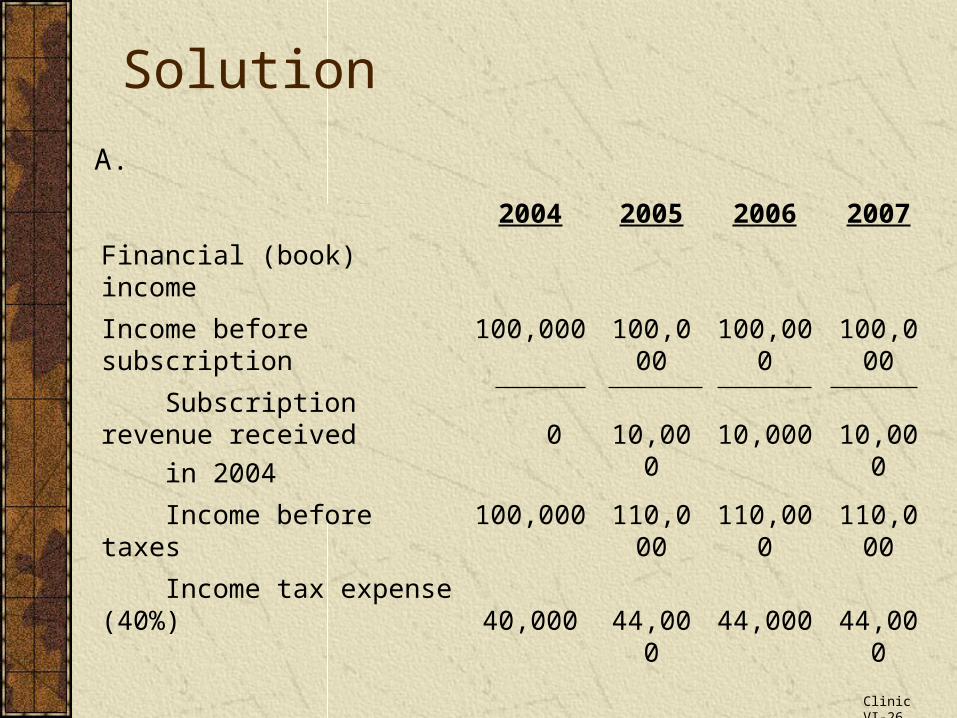

2004 2005 2006 2007

Financial (book) income

Income before subscription 100,000 100,000 100,000 100,000

Subscription revenue received

in 2004

0 10,000 10,000 10,000

Income before taxes 100,000 110,000 110,000 110,000

Income tax expense (40%) 40,000 44,000 44,000 44,000

A.

Clinic VI-26

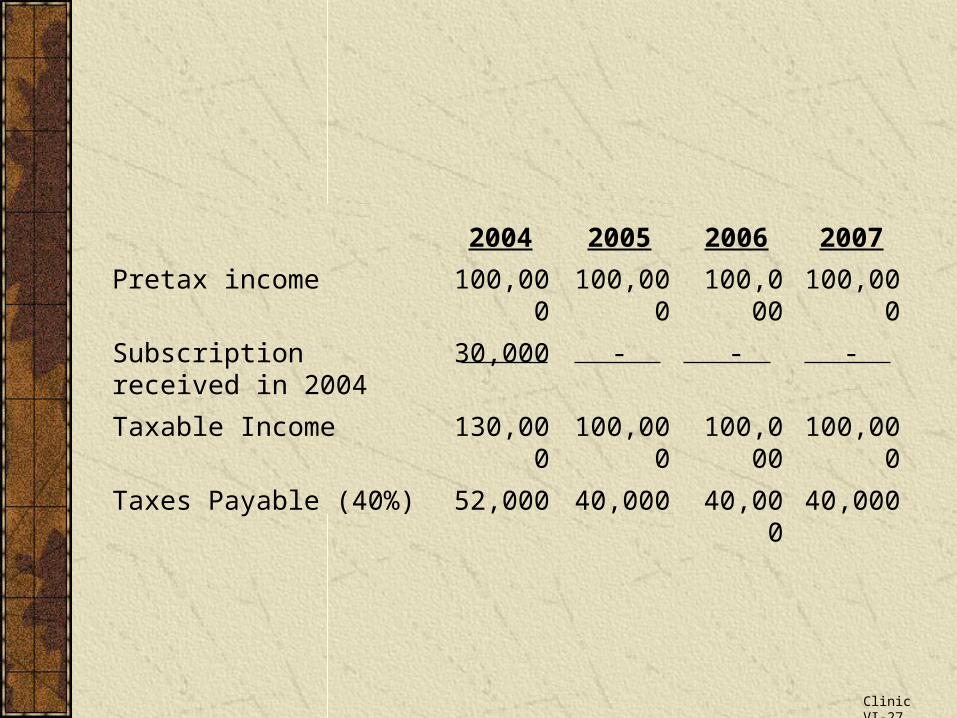

2004 2005 2006 2007

Pretax income 100,000 100,000 100,000 100,000

Subscription received in 2004 30,000 - - -

Taxable Income 130,000 100,000 100,000 100,000

Taxes Payable (40%) 52,000 40,000 40,000 40,000

Clinic VI-27

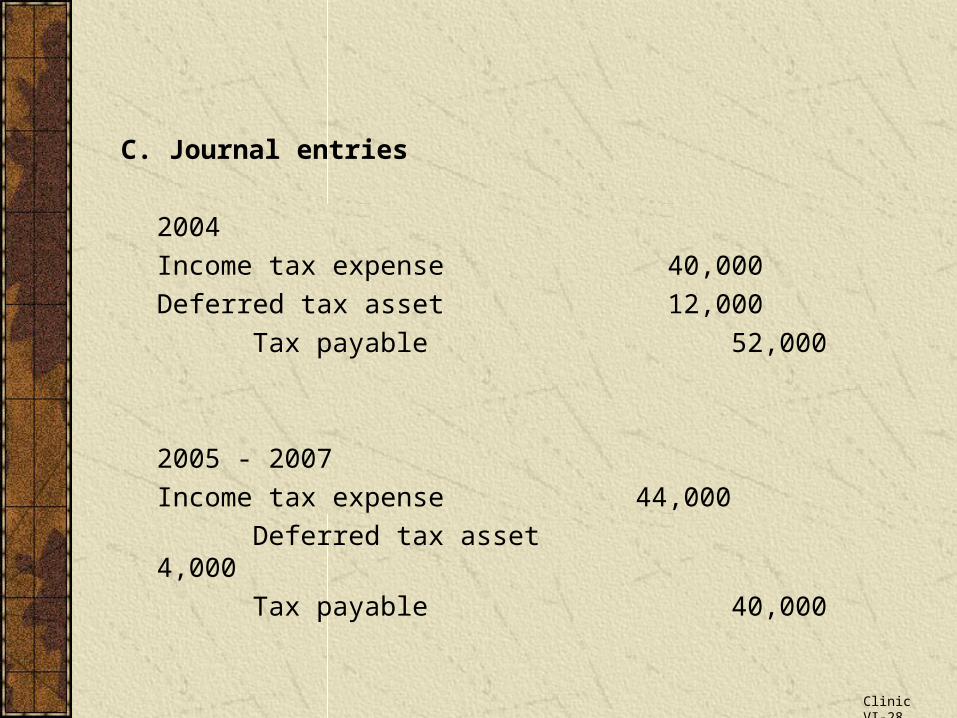

C. Journal entries

2004

Income tax expense 40,000

Deferred tax asset 12,000

Tax payable 52,000

2005 - 2007

Income tax expense 44,000

Deferred tax asset 4,000

Tax payable 40,000

Clinic VI-28

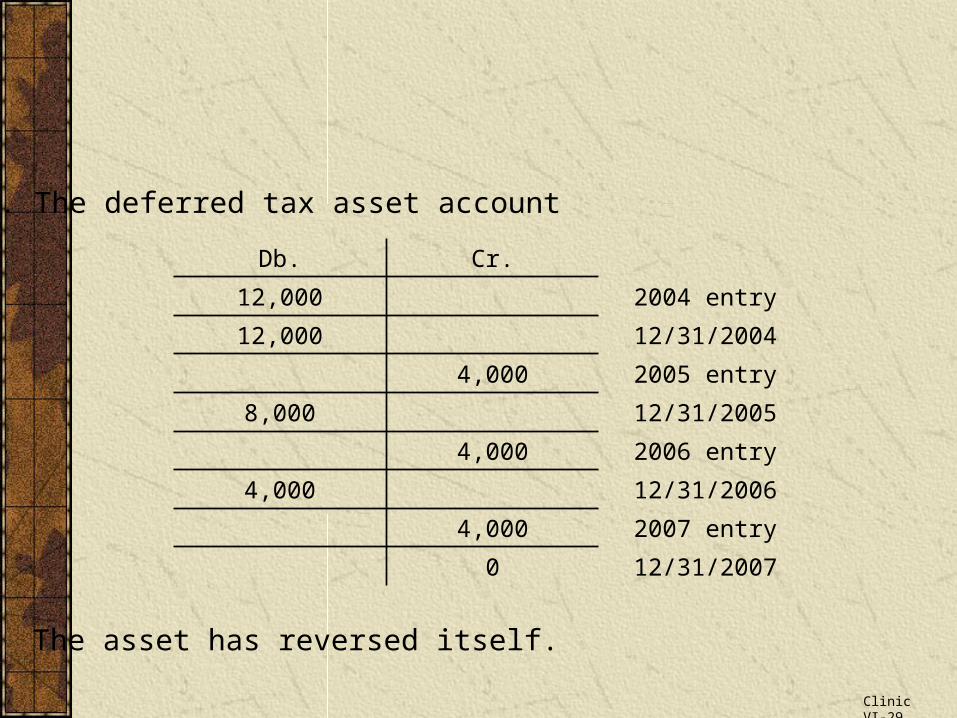

D. The deferred tax asset account

Db. Cr.

12,000 2004 entry

12,000 12/31/2004

4,000 2005 entry

8,000 12/31/2005

4,000 2006 entry

4,000 12/31/2006

4,000 2007 entry

0 12/31/2007

The asset has reversed itself.

Clinic VI-29

Income Tax Expense 10,000 Allowance to Reduce Deferred Tax Asset To Expected Realizable Value 10,000

To record the reduction in the deferred tax asset

E.

Clinic VI-30

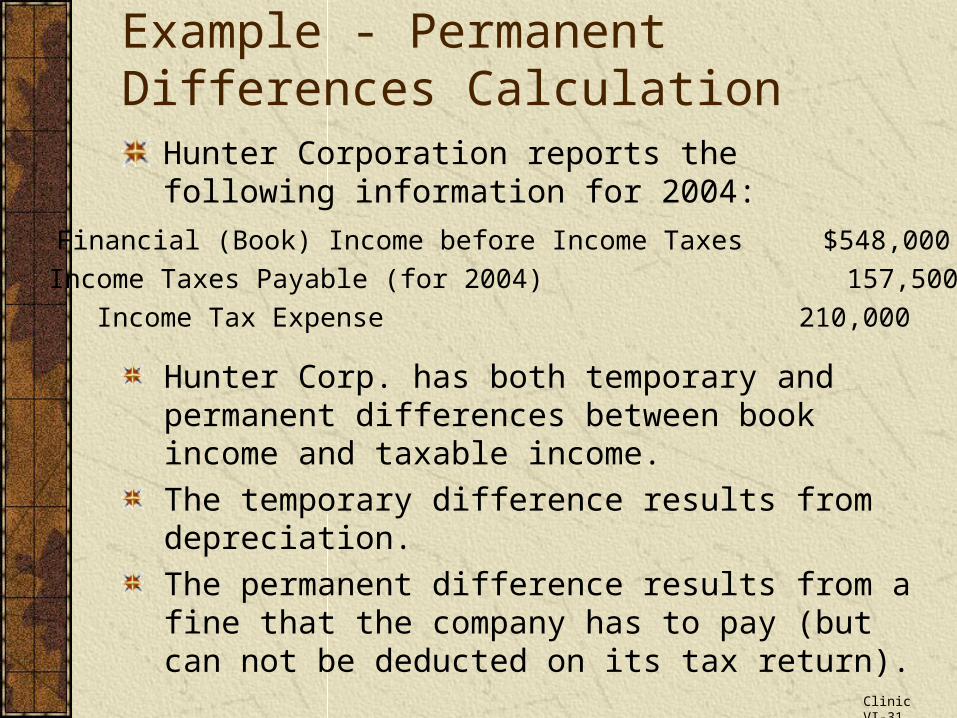

Example - Permanent Differences Calculation

Hunter Corporation reports the following information for 2004:

Financial (Book) Income before Income Taxes $548,000

Income Taxes Payable (for 2004) 157,500

Income Tax Expense 210,000

Hunter Corp. has both temporary and permanent differences between book income and taxable income.

The temporary difference results from depreciation.

The permanent difference results from a fine that the company has to pay (but can not be deducted on its tax return).

Clinic VI-31

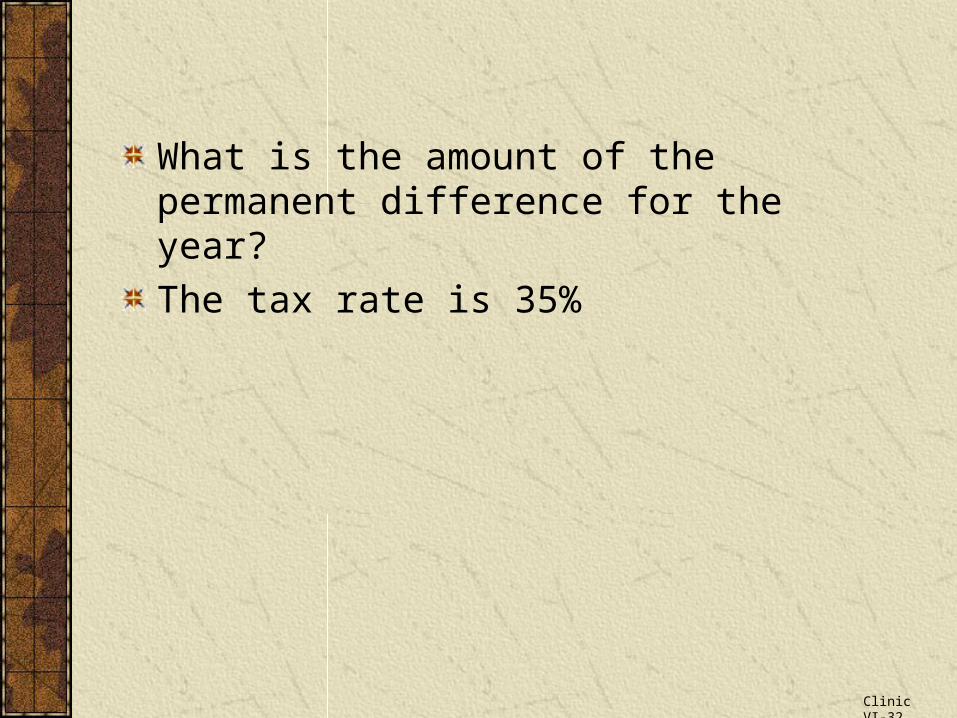

What is the amount of the permanent difference for the year?

The tax rate is 35%

Clinic VI-32

Solution

Step 1: Find the change in the deferred tax liabilityStep 1: Find the change in the deferred tax liability

Income Tax Expense (Book) $210,000

Income Taxes Payable 157,500

∆ Deferred Tax Liability 52,500

Step 2: Find the temporary differenceStep 2: Find the temporary difference

∆ Deferred Tax Liability/0.35 $52,500/0.35=

150,000

Step 3: Find taxable incomeStep 3: Find taxable incomeIncome Taxes Payable (from current year)/0.35

$157,500/0.35= 450,000

Clinic VI-33

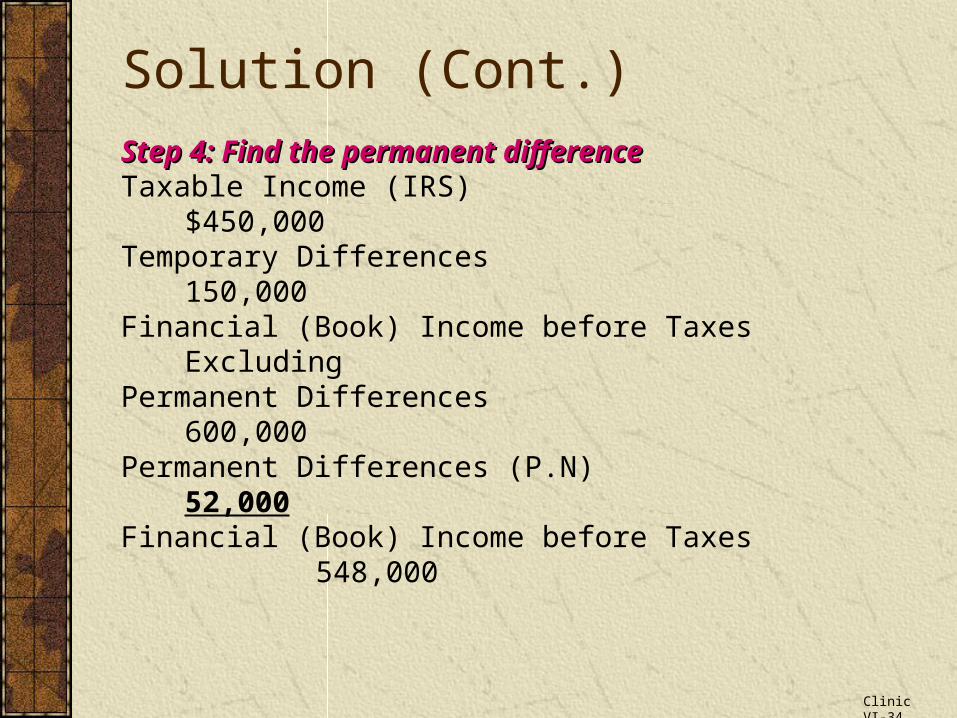

Solution (Cont.)

Step 4: Find the permanent differenceStep 4: Find the permanent differenceTaxable Income (IRS) $450,000Temporary Differences 150,000Financial (Book) Income before Taxes ExcludingPermanent Differences 600,000Permanent Differences (P.N) 52,000Financial (Book) Income before Taxes 548,000

Clinic VI-34

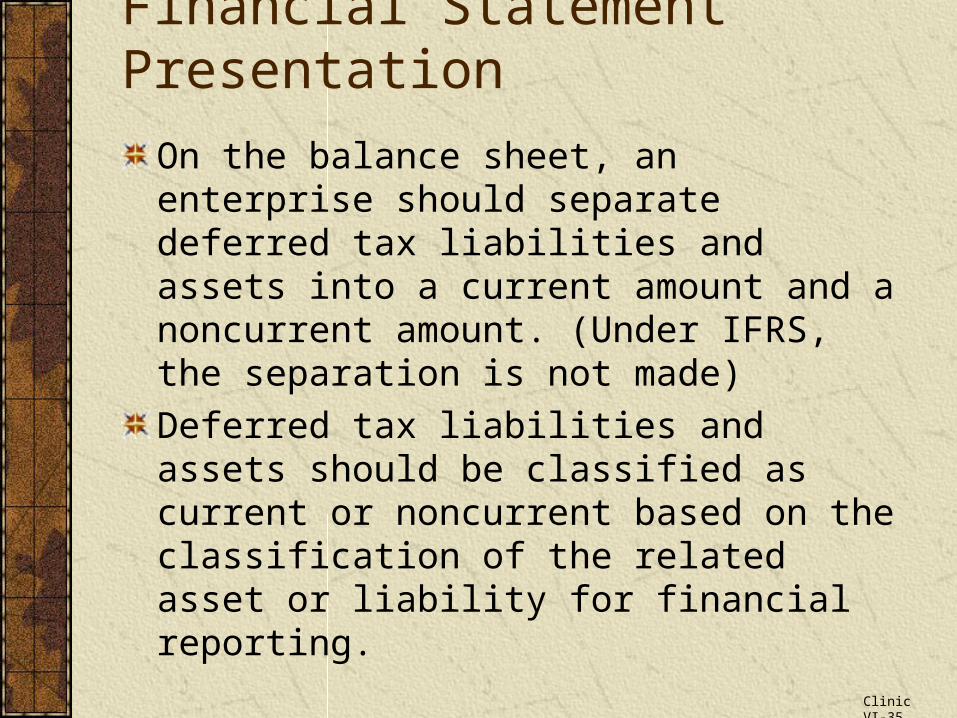

Financial Statement Presentation

On the balance sheet, an enterprise should separate deferred tax liabilities and assets into a current amount and a noncurrent amount. (Under IFRS, the separation is not made)

Deferred tax liabilities and assets should be classified as current or noncurrent based on the classification of the related asset or liability for financial reporting.

Clinic VI-35

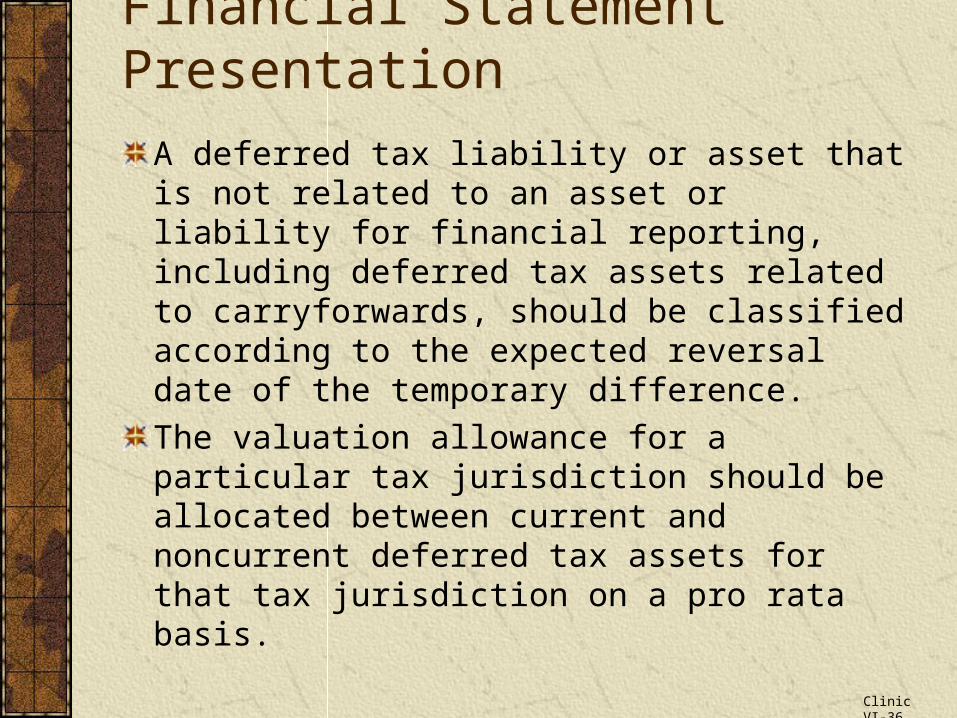

Financial Statement Presentation

A deferred tax liability or asset that is not related to an asset or liability for financial reporting, including deferred tax assets related to carryforwards, should be classified according to the expected reversal date of the temporary difference.

The valuation allowance for a particular tax jurisdiction should be allocated between current and noncurrent deferred tax assets for that tax jurisdiction on a pro rata basis.

Clinic VI-36