accounting chapter 24

TRANSCRIPT

Cost Allocation and

Responsibility Accounting

Chapter 24

24-1Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall

Learning Objectives

1. Assign direct costs and allocate indirect costs using predetermined overhead allocation rates with single and multiple allocation bases

2. Explain why companies decentralize and use responsibility accounting

24-2Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall

Learning Objectives

3. Describe the purpose of performance evaluation systems and how the balanced scorecard helps companies evaluate performance

4. Use responsibility reports to evaluate cost, revenue, and profit centers

24-3Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall

Learning Objectives

5. Use return on investment (ROI) and residual income (RI) to evaluate investment centers

6. Determine how transfer pricing affects decentralized companies (Appendix 24A)

24-4Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall

Learning Objective 1

Assign direct costs and Assign direct costs and allocate indirect costs allocate indirect costs using predetermined using predetermined overhead allocation overhead allocation rates with single and rates with single and

multiple allocation multiple allocation basesbases

24-5Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall

Ways to Allocate Indirect Costs

• Plantwide rate

• Multiple department rates

• Activity-based costing

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-6

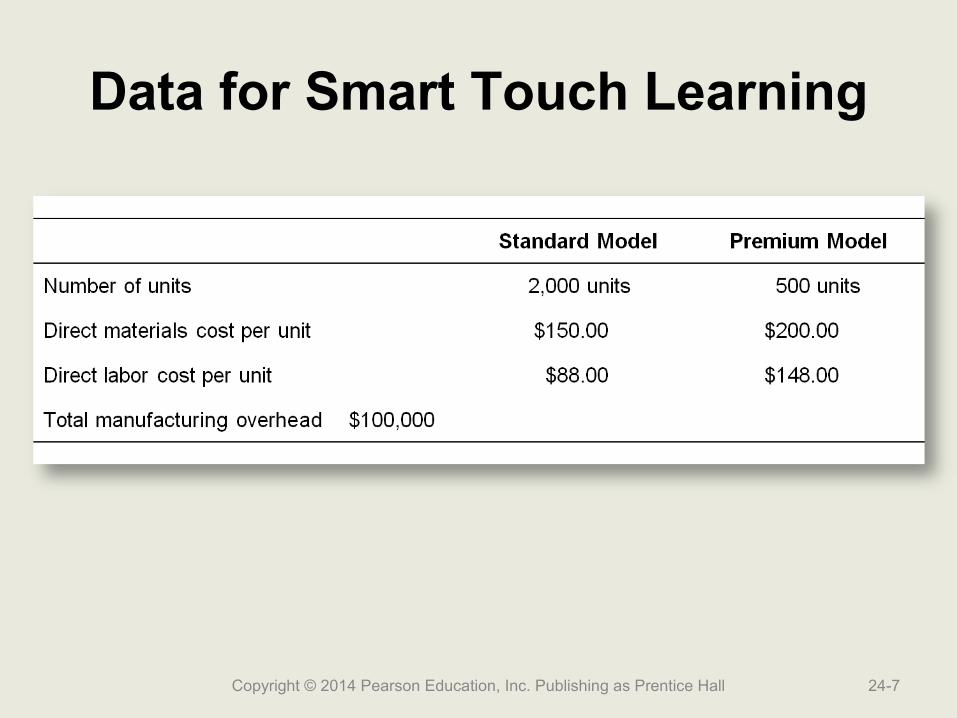

Data for Smart Touch Learning

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-7

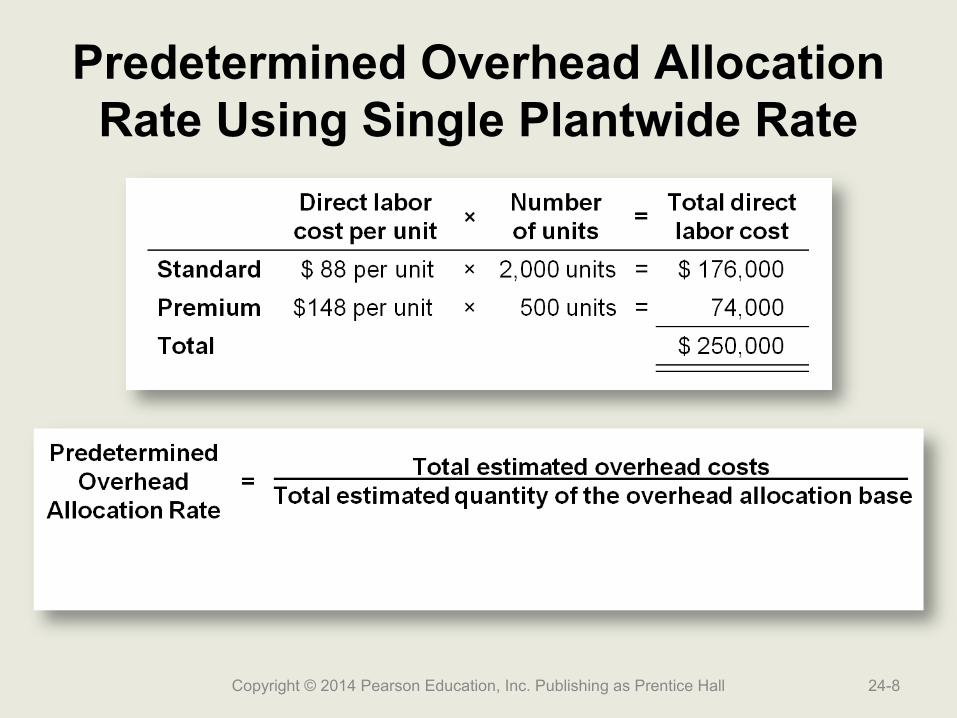

Predetermined Overhead Allocation Rate Using Single Plantwide Rate

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-8

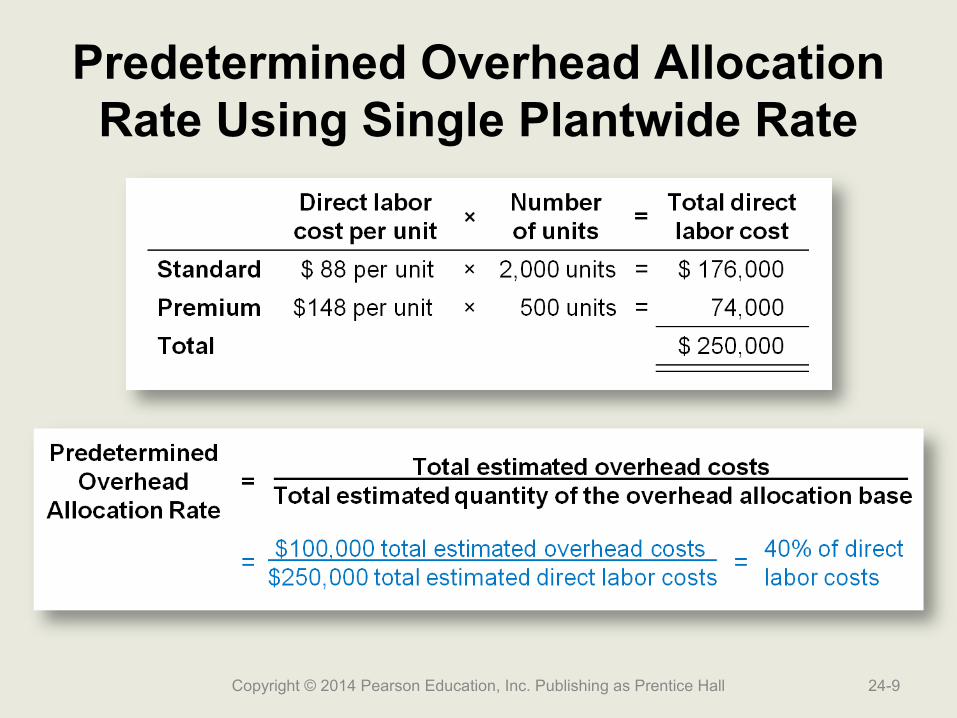

Predetermined Overhead Allocation Rate Using Single Plantwide Rate

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-9

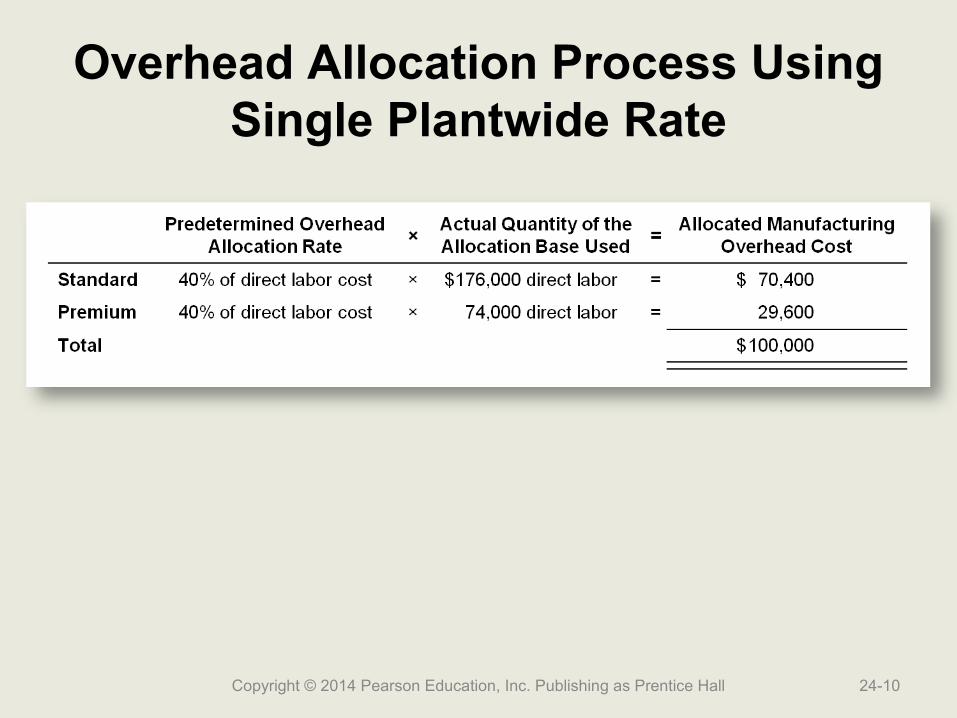

Overhead Allocation Process UsingSingle Plantwide Rate

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-10

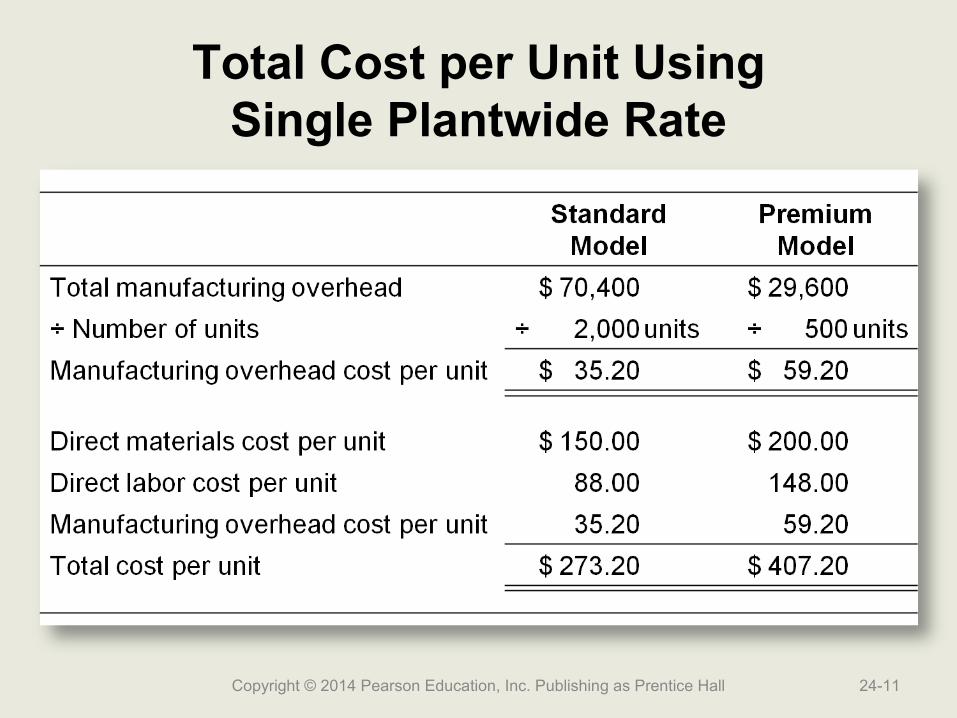

Total Cost per Unit UsingSingle Plantwide Rate

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-11

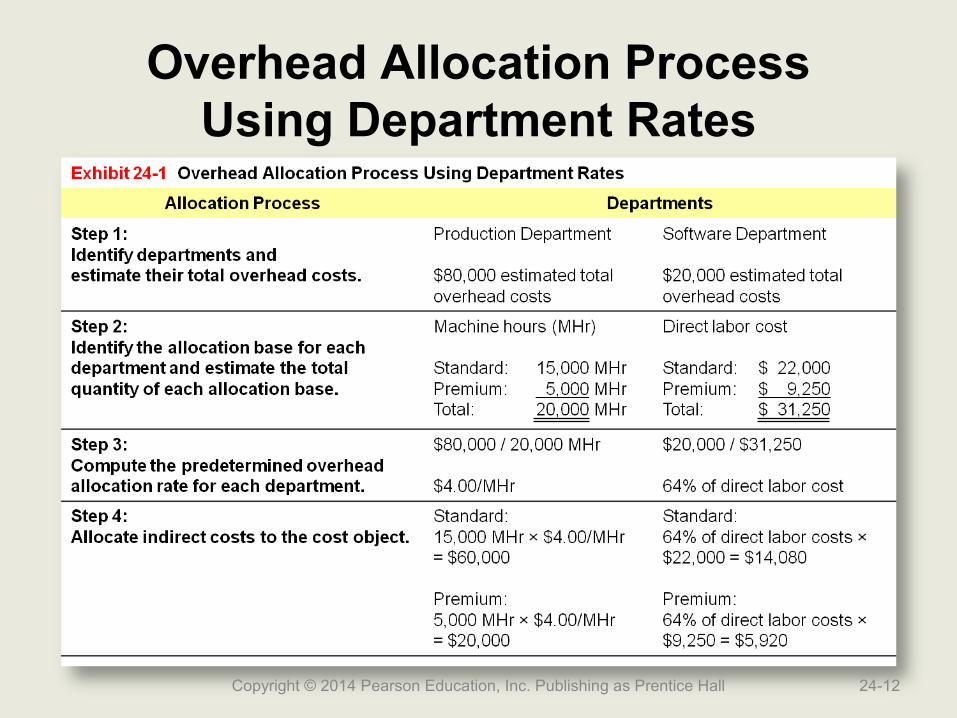

Overhead Allocation ProcessUsing Department Rates

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-12

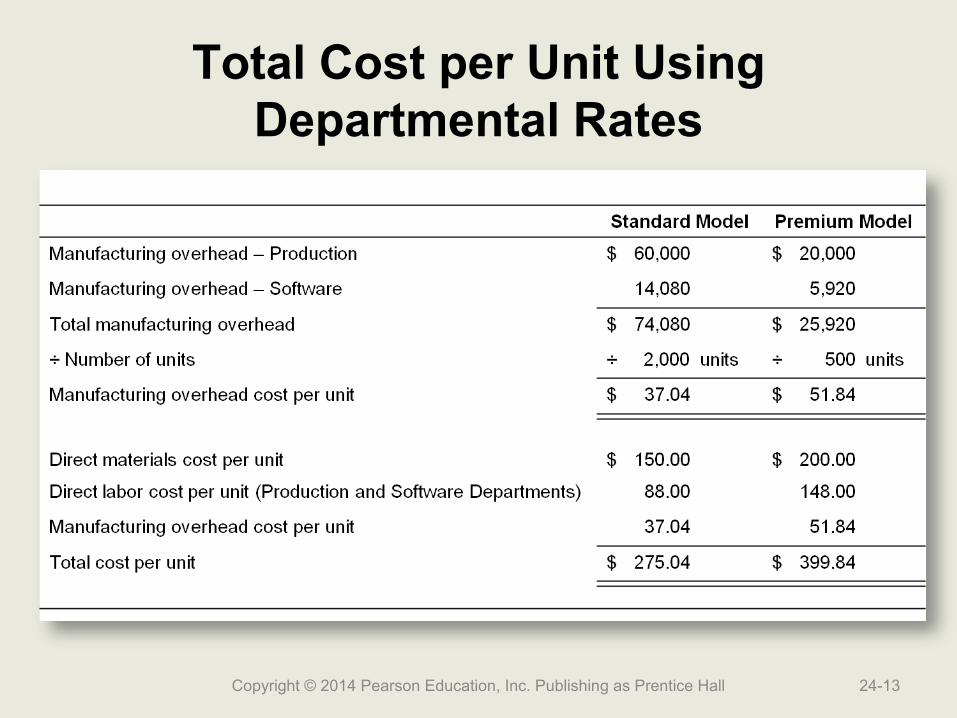

Total Cost per Unit Using Departmental Rates

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-13

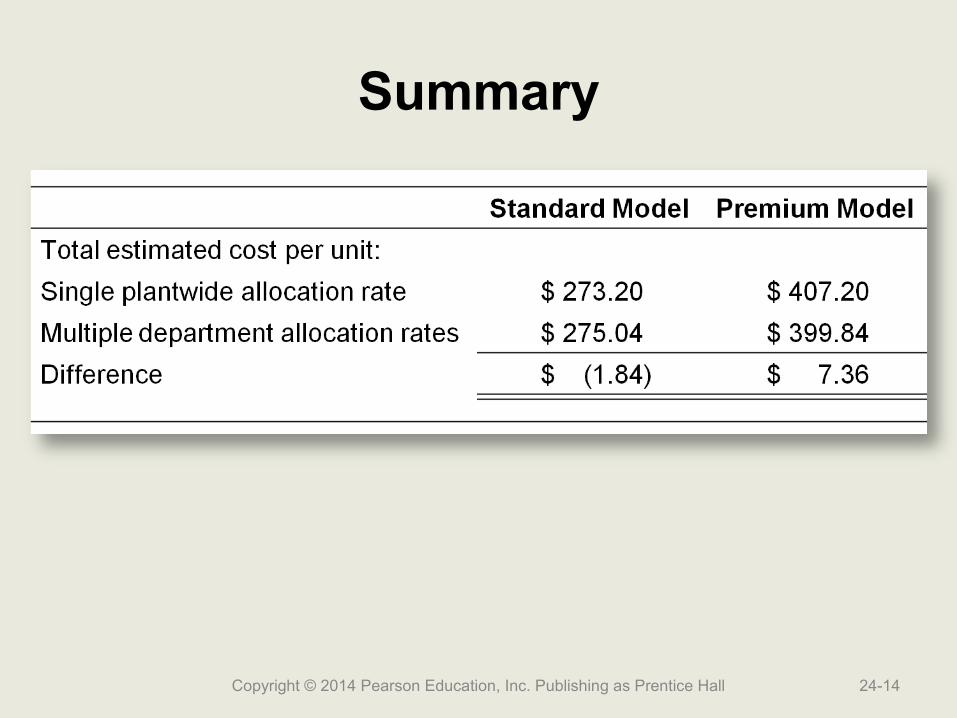

Summary

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-14

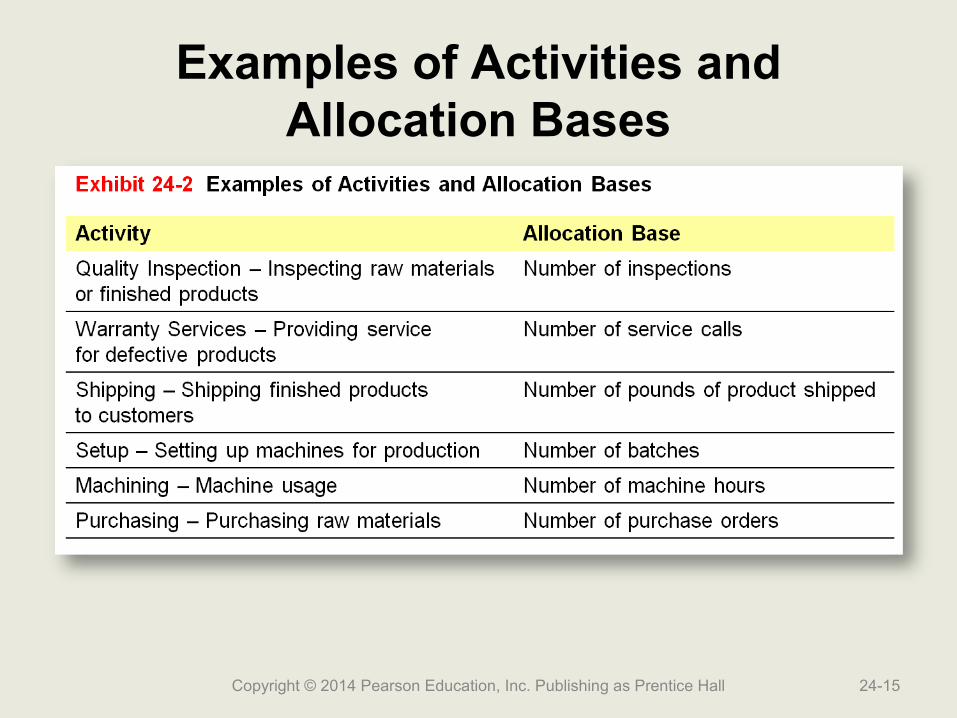

Examples of Activities and Allocation Bases

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-15

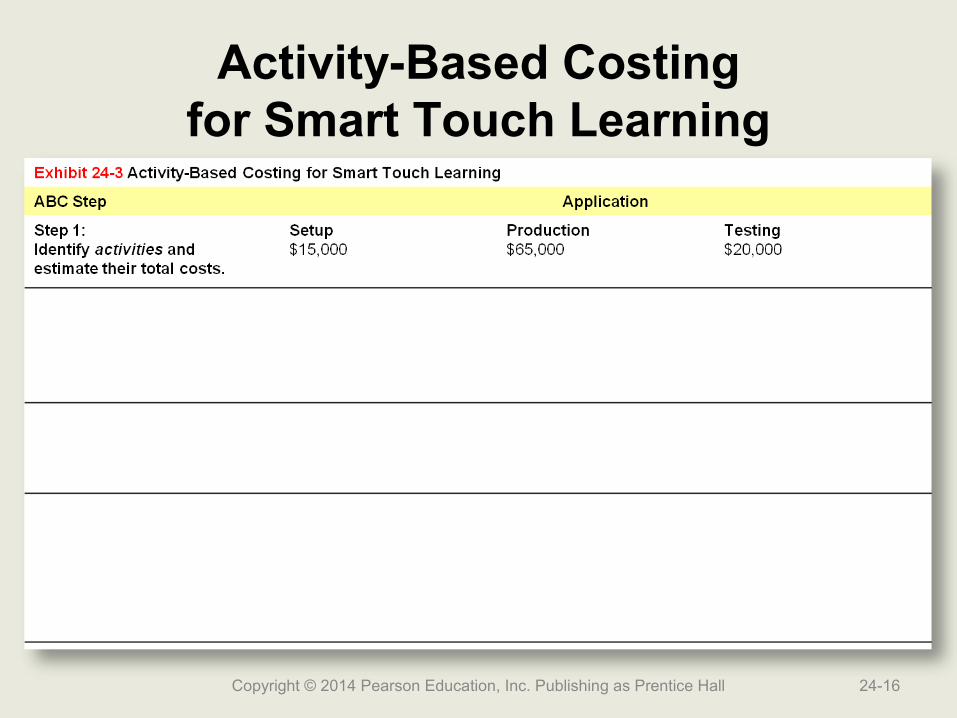

Activity-Based Costingfor Smart Touch Learning

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-16

Smart Touch Learning’sEstimated Manufacturing Overhead

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-17

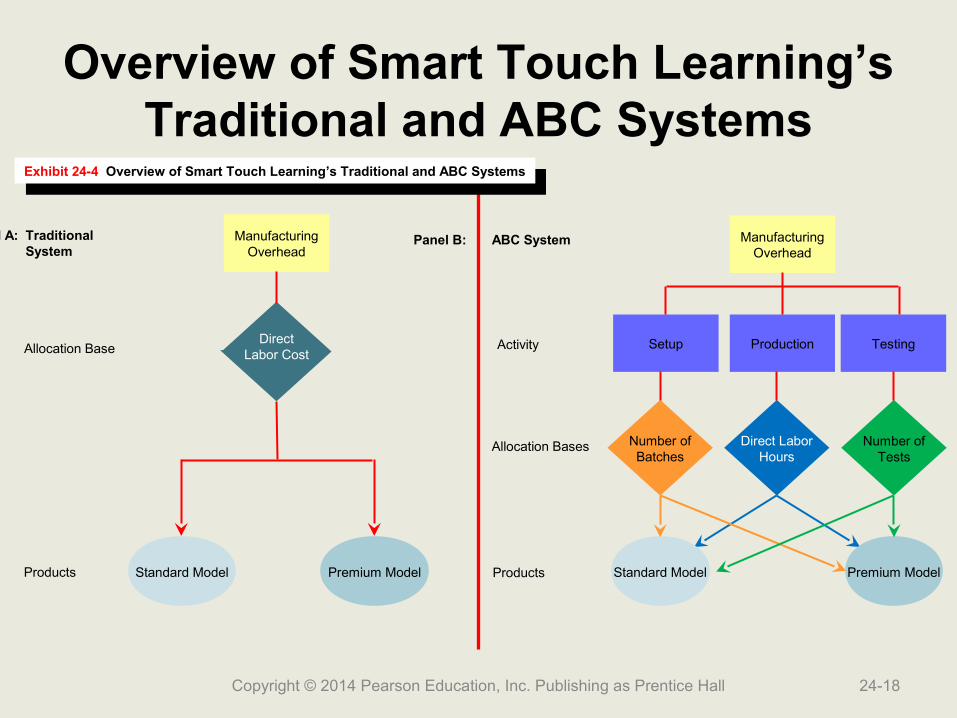

Overview of Smart Touch Learning’s Traditional and ABC Systems

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-18

ManufacturingOverhead

Panel A: TraditionalSystem

DirectLabor CostAllocation Base

ManufacturingOverhead

ProductionSetup

Panel B: ABC System

Activity Testing

Number ofBatches

Direct LaborHours

Number ofTests

Standard Model Premium ModelStandard Model Premium Model

Allocation Bases

ProductsProducts

Exhibit 24-4 Overview of Smart Touch Learning’s Traditional and ABC SystemsExhibit 24-4 Overview of Smart Touch Learning’s Traditional and ABC Systems

Activity-Based Costingfor Smart Touch Learning

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-19

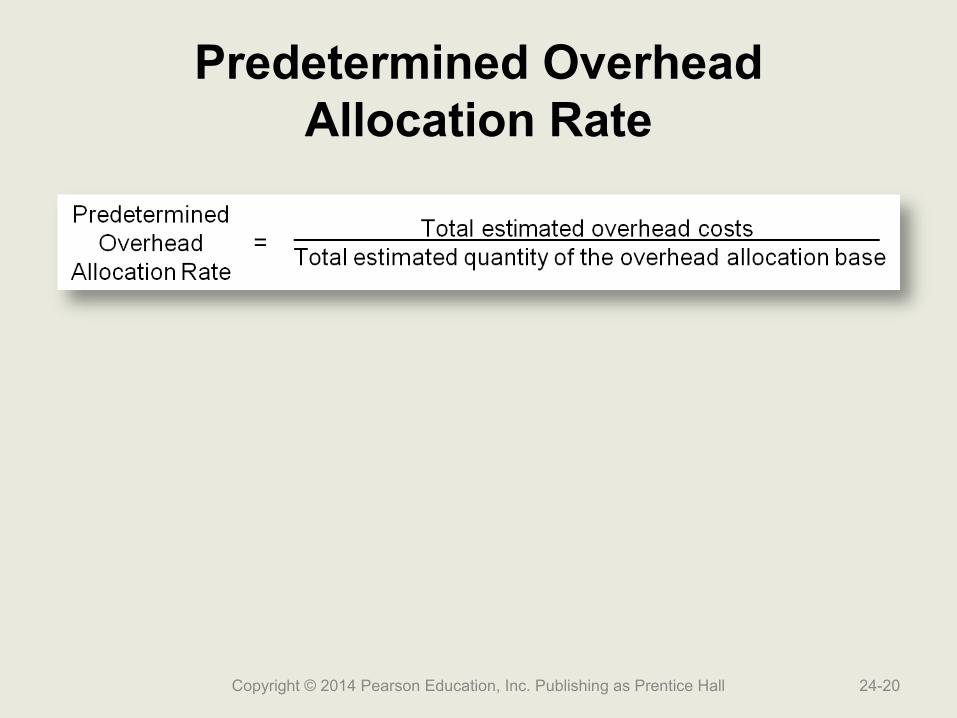

Predetermined OverheadAllocation Rate

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-20

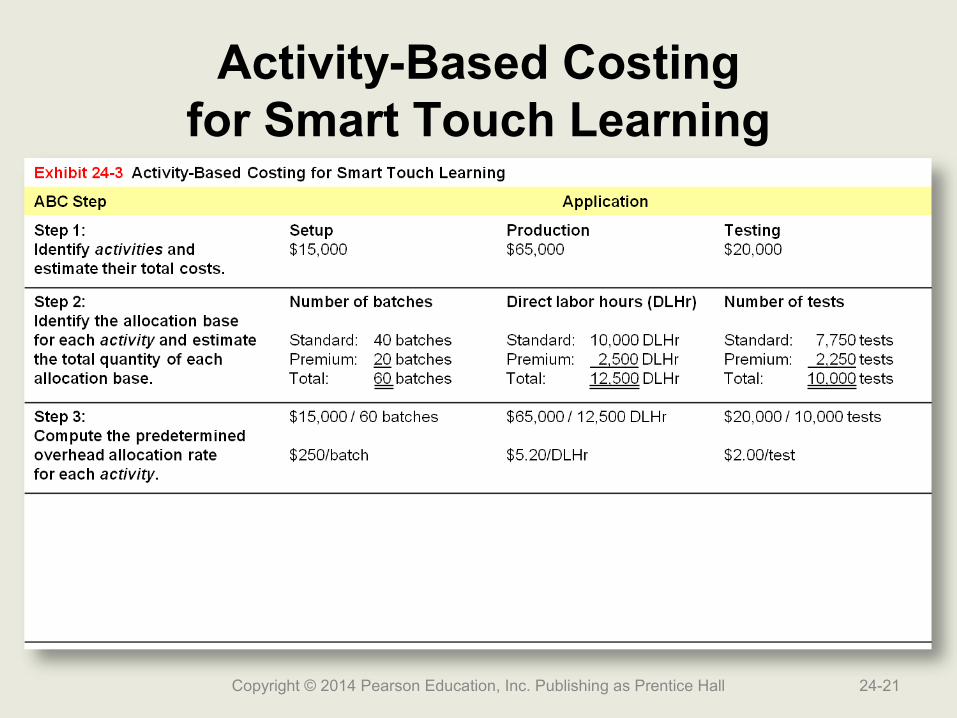

Activity-Based Costingfor Smart Touch Learning

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-21

Activity-Based Costingfor Smart Touch Learning

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-22

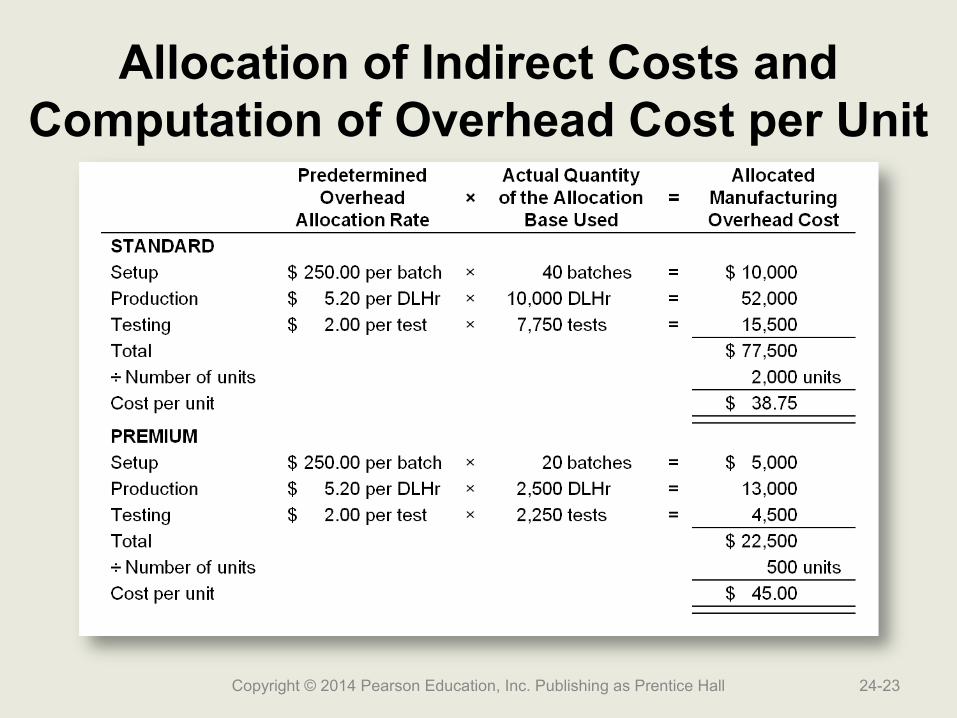

Allocation of Indirect Costs and Computation of Overhead Cost per Unit

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-23

Total Cost per Unit

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-24

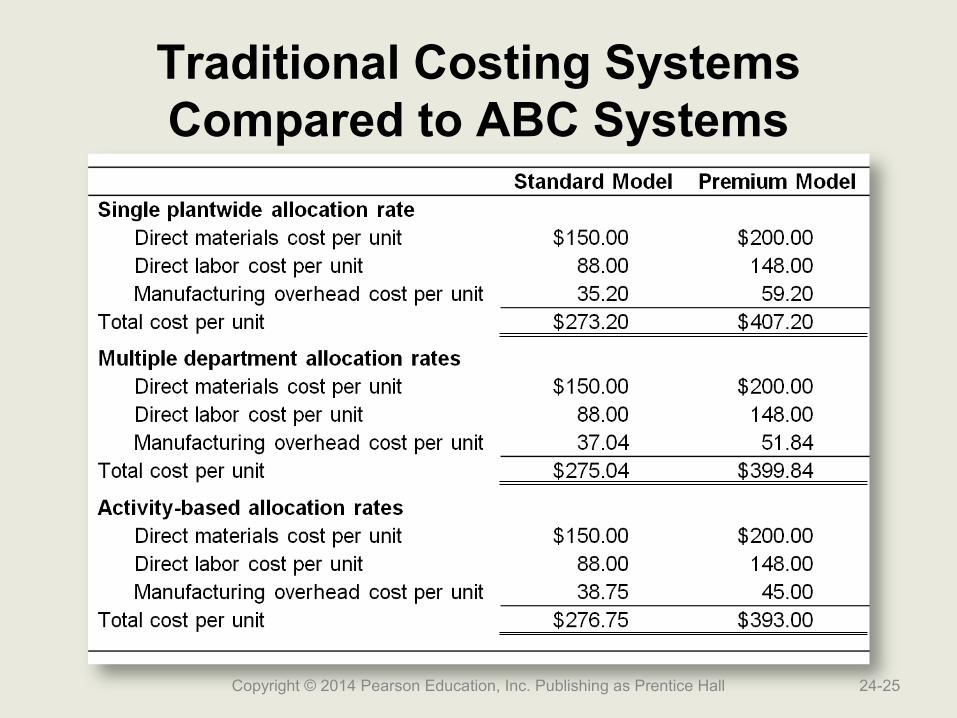

Traditional Costing Systems Compared to ABC Systems

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-25

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-26

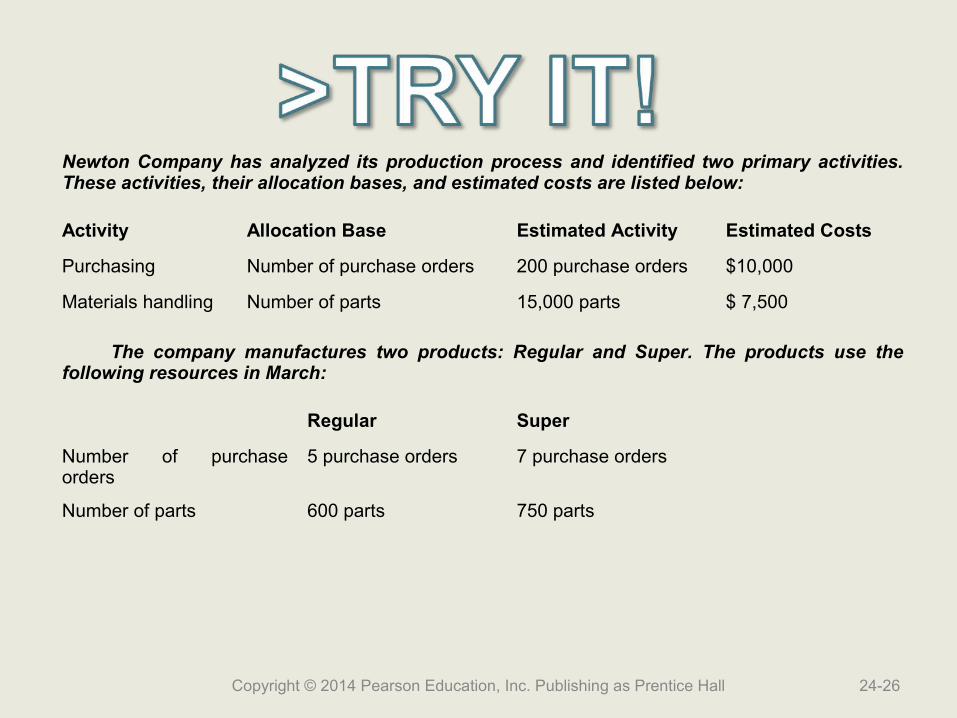

Newton Company has analyzed its production process and identified two primary activities. These activities, their allocation bases, and estimated costs are listed below:

Activity Allocation Base Estimated Activity Estimated Costs

Purchasing Number of purchase orders 200 purchase orders $10,000

Materials handling Number of parts 15,000 parts $ 7,500

The company manufactures two products: Regular and Super. The products use the following resources in March:

Regular Super

Number of purchase orders

5 purchase orders 7 purchase orders

Number of parts 600 parts 750 parts

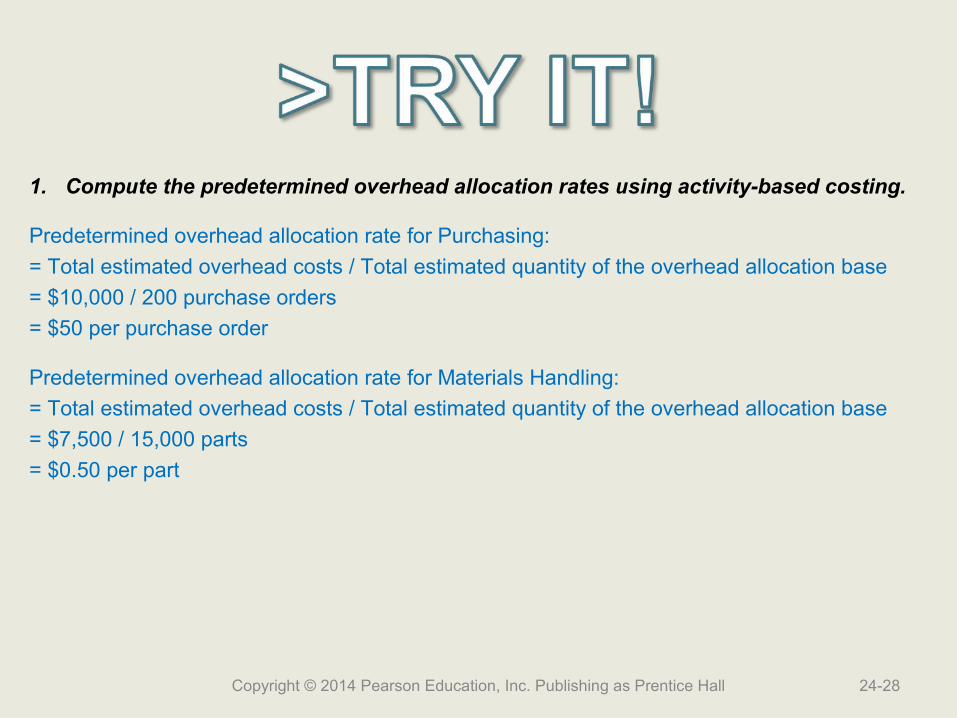

1. Compute the predetermined overhead allocation rates using activity-based costing.

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-27

1. Compute the predetermined overhead allocation rates using activity-based costing.

Predetermined overhead allocation rate for Purchasing:

= Total estimated overhead costs / Total estimated quantity of the overhead allocation base

= $10,000 / 200 purchase orders

= $50 per purchase order

Predetermined overhead allocation rate for Materials Handling:

= Total estimated overhead costs / Total estimated quantity of the overhead allocation base

= $7,500 / 15,000 parts

= $0.50 per part

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-28

2. Determine the amount of overhead allocated to Regular in March.

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-29

2. Determine the amount of overhead allocated to Regular in March.

Allocated Manufacturing Overhead Cost for Regular for Purchasing:

= Predetermined overhead allocation rate × Actual quantity of the allocation base used

= $50 per purchase order × 5 purchase orders

= $250

Allocated Manufacturing Overhead Cost for Regular for Materials Handling:

= Predetermined overhead allocation rate × Actual quantity of the allocation base used

= $0.50 per part × 600 parts

= $300

Total overhead allocated to Regular

= $250 + $300

= $550

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-30

3. Determine the amount of overhead allocated to Super in March.

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-31

3. Determine the amount of overhead allocated to Super in March.

Allocated Manufacturing Overhead Cost for Super for Purchasing:

= Predetermined overhead allocation rate × Actual quantity of the allocation base used

= $50 per purchase order × 7 purchase orders

= $350

Allocated Manufacturing Overhead Cost for Super for Materials Handling:

= Predetermined overhead allocation rate × Actual quantity of the allocation base used

= $0.50 per part × 750 parts

= $375

Total overhead allocated to Super

= $350 + $375

= $725

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-32

Learning Objective 2

Explain why Explain why companies companies

decentralize and use decentralize and use responsibility responsibility

accountingaccounting

24-33Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall

Organization of a Business

• Centralized

• Decentralized

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-34

Advantages of Decentralization

• Frees top management time

• Supports use of expert knowledge

• Improves customer relations

• Provides training

• Improves motivation and retention

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-35

Disadvantages of Decentralization

• Duplication of costs

• Problems achieving goal congruence

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-36

Responsibility Centers

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-37

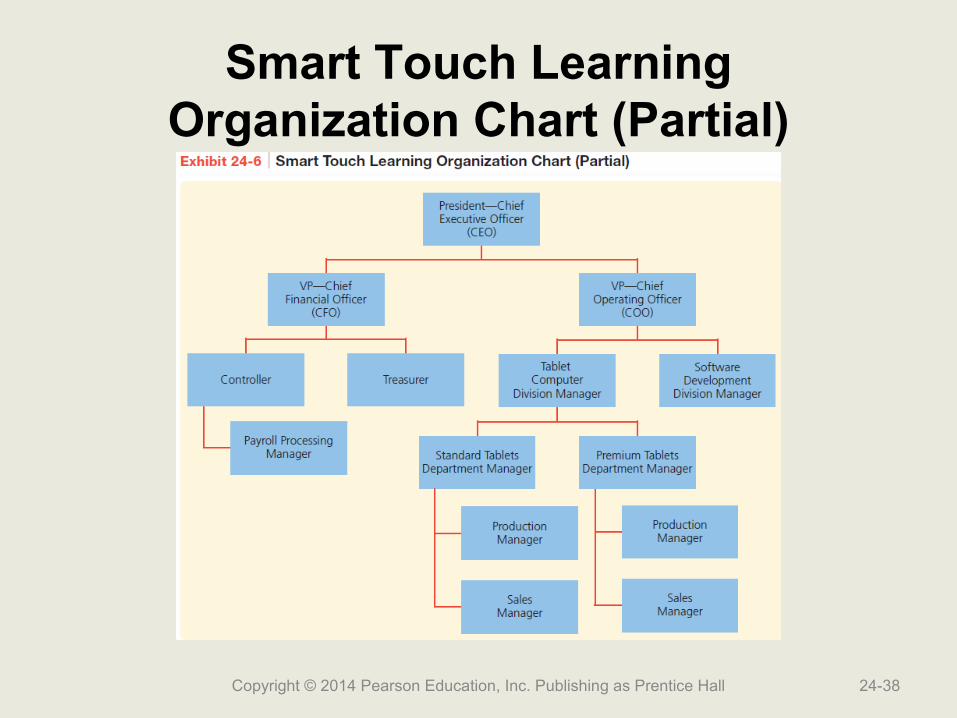

Smart Touch LearningOrganization Chart (Partial)

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-38

Fill in the blanks with the phrase that best completes the sentence. Some phrases may be used more than once and some not at all.

Phrases:

cost center revenue center

investment center lower

profit center higher

responsibility center

4. The maintenance department at the local zoo is a(n)

_______________.

5. The concession stand at the local zoo is a(n) _______________.

6. The menswear department of a department store, which is

responsible for buying and selling merchandise, is a(n) _______________.

7. The production line at a manufacturing plant is a(n)

_______________.Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-39

Fill in the blanks with the phrase that best completes the sentence. Some phrases may be used more than once and some not at all.

Phrases:

cost center revenue center

investment center lower

profit center higher

responsibility center

4. The maintenance department at the local zoo is a(n)

_______________.

5. The concession stand at the local zoo is a(n) _______________.

6. The menswear department of a department store, which is

responsible for buying and selling merchandise, is a(n) _______________.

7. The production line at a manufacturing plant is a(n)

_______________.Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-40

cost center

Fill in the blanks with the phrase that best completes the sentence. Some phrases may be used more than once and some not at all.

Phrases:

cost center revenue center

investment center lower

profit center higher

responsibility center

4. The maintenance department at the local zoo is a(n)

_______________.

5. The concession stand at the local zoo is a(n) _______________.

6. The menswear department of a department store, which is

responsible for buying and selling merchandise, is a(n) _______________.

7. The production line at a manufacturing plant is a(n)

_______________.Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-41

cost center

profit center

Fill in the blanks with the phrase that best completes the sentence. Some phrases may be used more than once and some not at all.

Phrases:

cost center revenue center

investment center lower

profit center higher

responsibility center

4. The maintenance department at the local zoo is a(n)

_______________.

5. The concession stand at the local zoo is a(n) _______________.

6. The menswear department of a department store, which is

responsible for buying and selling merchandise, is a(n) _______________.

7. The production line at a manufacturing plant is a(n)

_______________.Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-42

cost center

profit center

profit center

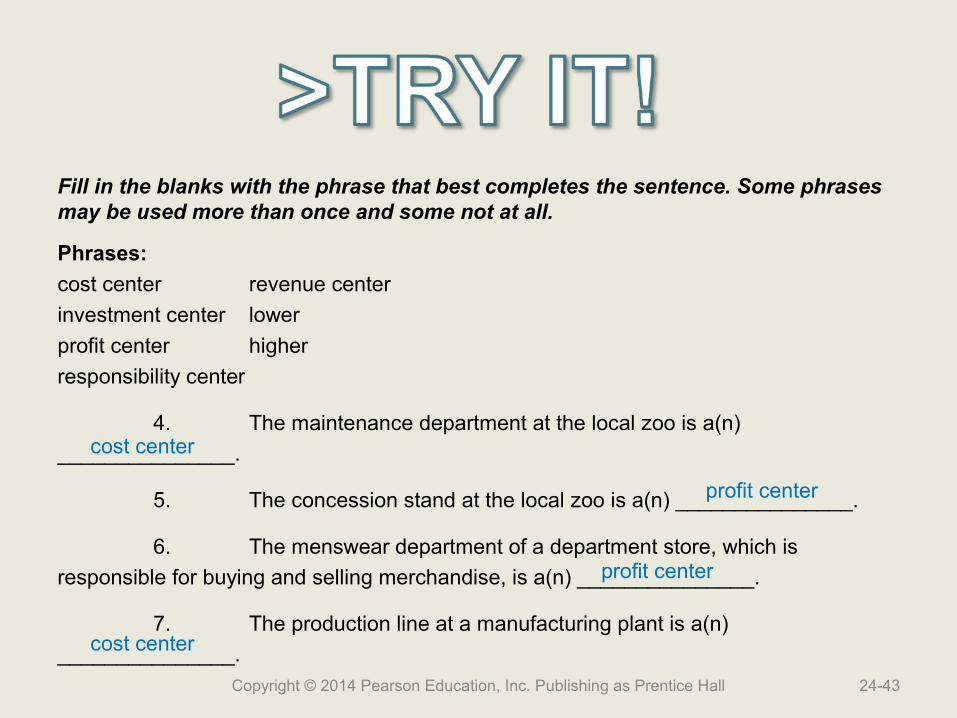

Fill in the blanks with the phrase that best completes the sentence. Some phrases may be used more than once and some not at all.

Phrases:

cost center revenue center

investment center lower

profit center higher

responsibility center

4. The maintenance department at the local zoo is a(n)

_______________.

5. The concession stand at the local zoo is a(n) _______________.

6. The menswear department of a department store, which is

responsible for buying and selling merchandise, is a(n) _______________.

7. The production line at a manufacturing plant is a(n)

_______________.Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-43

cost center

profit center

profit center

cost center

Fill in the blanks with the phrase that best completes the sentence. Some phrases may be used more than once and some not at all.

Phrases:

cost center revenue center

investment center lower

profit center higher

responsibility center

8. A(n) _________________ is any segment of the business whose manager is accountable for specific activities.

9. A brand of soft drink, a division of a beverage manufacturing company, is a(n) _________________.

10.The sales manager in charge of a shoe company’s northwest sales territory oversees a(n) _______________.

11. Managers of cost and revenue centers are at _______________ levels of the organization than are managers of profit and investment centers.

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-44

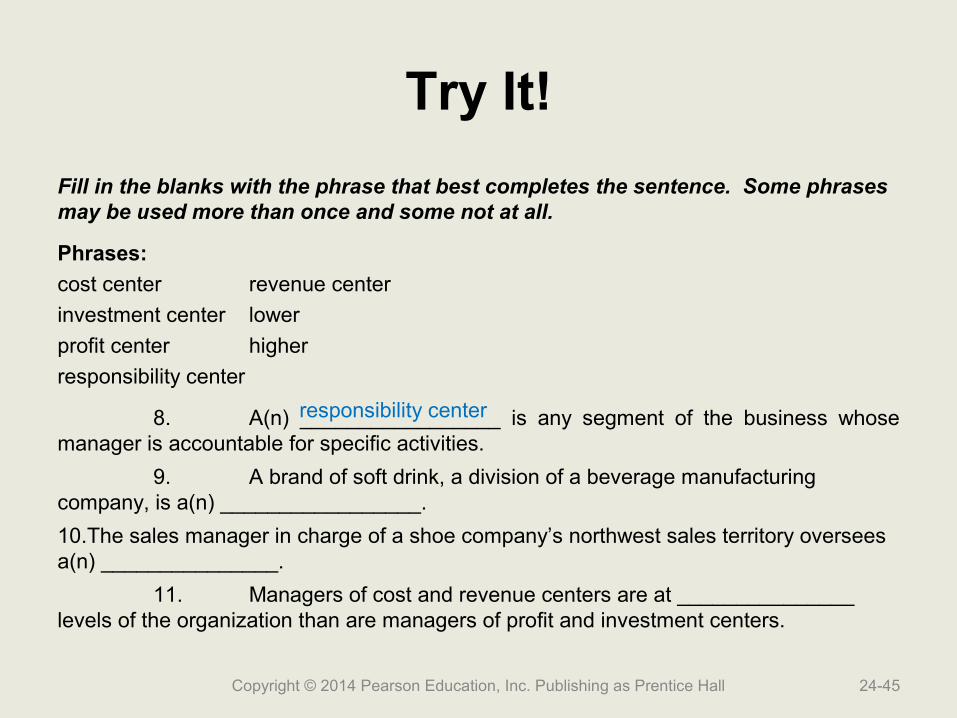

Try It!

Fill in the blanks with the phrase that best completes the sentence. Some phrases may be used more than once and some not at all.

Phrases:

cost center revenue center

investment center lower

profit center higher

responsibility center

8. A(n) _________________ is any segment of the business whose manager is accountable for specific activities.

9. A brand of soft drink, a division of a beverage manufacturing company, is a(n) _________________.

10.The sales manager in charge of a shoe company’s northwest sales territory oversees a(n) _______________.

11. Managers of cost and revenue centers are at _______________ levels of the organization than are managers of profit and investment centers.

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-45

responsibility center

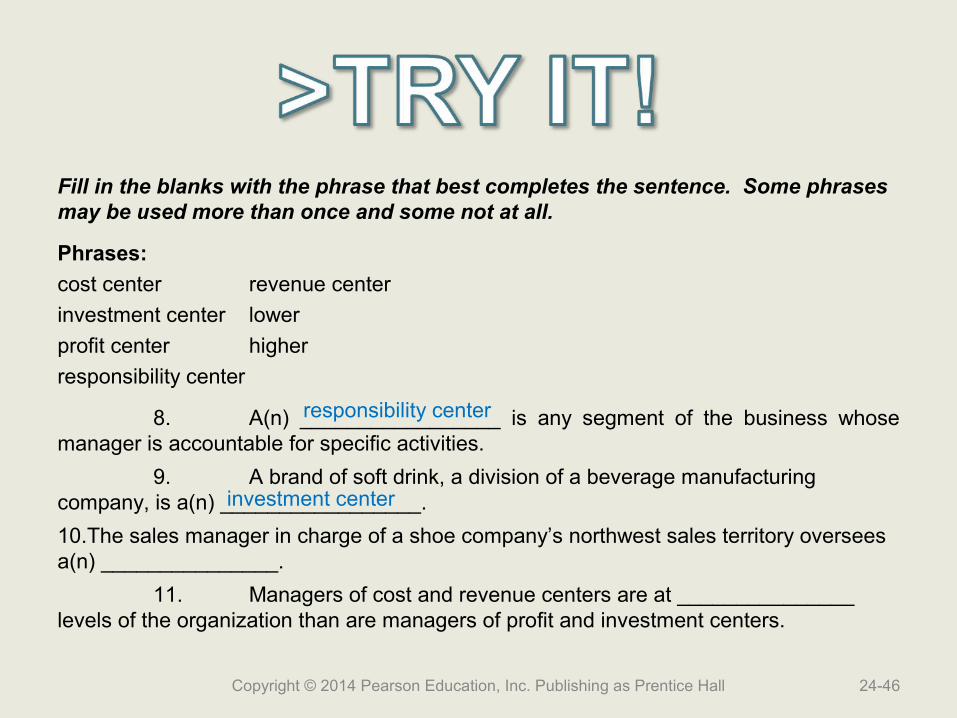

Fill in the blanks with the phrase that best completes the sentence. Some phrases may be used more than once and some not at all.

Phrases:

cost center revenue center

investment center lower

profit center higher

responsibility center

8. A(n) _________________ is any segment of the business whose manager is accountable for specific activities.

9. A brand of soft drink, a division of a beverage manufacturing company, is a(n) _________________.

10.The sales manager in charge of a shoe company’s northwest sales territory oversees a(n) _______________.

11. Managers of cost and revenue centers are at _______________ levels of the organization than are managers of profit and investment centers.

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-46

responsibility center

investment center

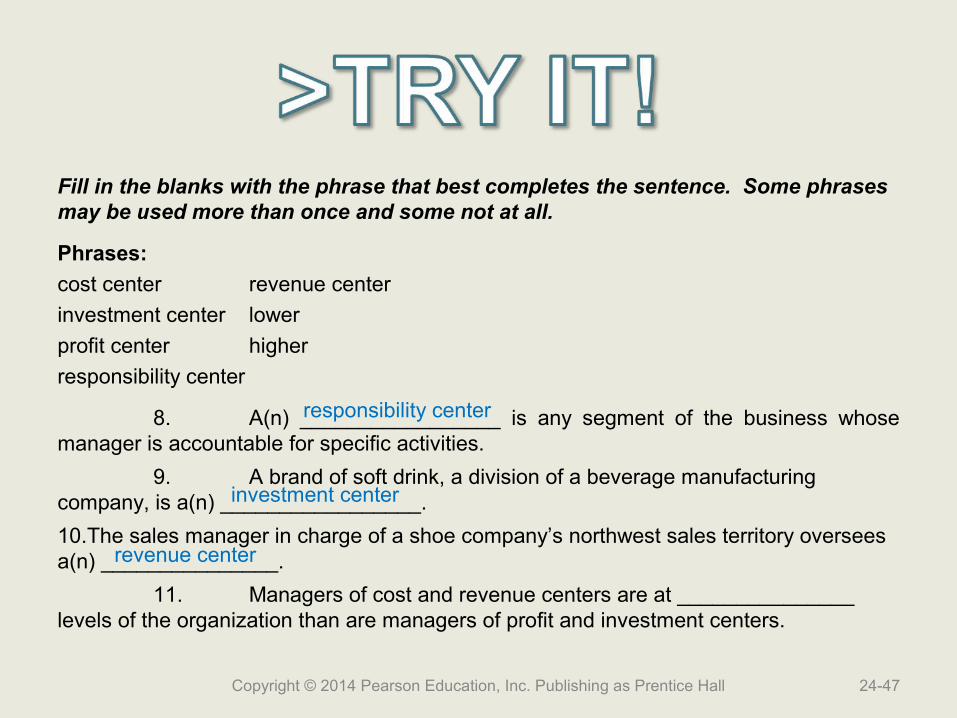

Fill in the blanks with the phrase that best completes the sentence. Some phrases may be used more than once and some not at all.

Phrases:

cost center revenue center

investment center lower

profit center higher

responsibility center

8. A(n) _________________ is any segment of the business whose manager is accountable for specific activities.

9. A brand of soft drink, a division of a beverage manufacturing company, is a(n) _________________.

10.The sales manager in charge of a shoe company’s northwest sales territory oversees a(n) _______________.

11. Managers of cost and revenue centers are at _______________ levels of the organization than are managers of profit and investment centers.

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-47

responsibility center

investment center

revenue center

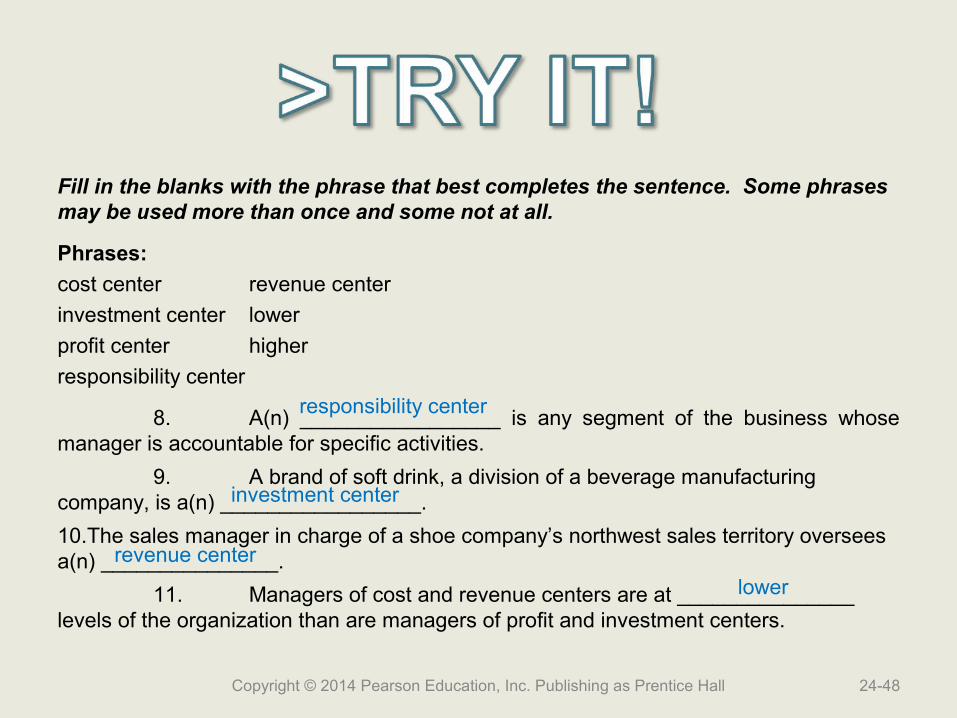

Fill in the blanks with the phrase that best completes the sentence. Some phrases may be used more than once and some not at all.

Phrases:

cost center revenue center

investment center lower

profit center higher

responsibility center

8. A(n) _________________ is any segment of the business whose manager is accountable for specific activities.

9. A brand of soft drink, a division of a beverage manufacturing company, is a(n) _________________.

10.The sales manager in charge of a shoe company’s northwest sales territory oversees a(n) _______________.

11. Managers of cost and revenue centers are at _______________ levels of the organization than are managers of profit and investment centers.

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-48

responsibility center

investment center

revenue center

lower

Learning Objective 3

Describe the purpose Describe the purpose of performance of performance

evaluation systems evaluation systems and how the balanced and how the balanced

scorecard helps scorecard helps companies evaluate companies evaluate

performanceperformance

24-49Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall

Goals of PerformanceEvaluation Systems

• Promoting goal congruence and coordination

• Communicating expectations

• Motivating segment managers

• Providing feedback

• Benchmarking

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-50

Limitations of FinancialPerformance Measures

• Lag indicators

• Focus on short-term achievements

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-51

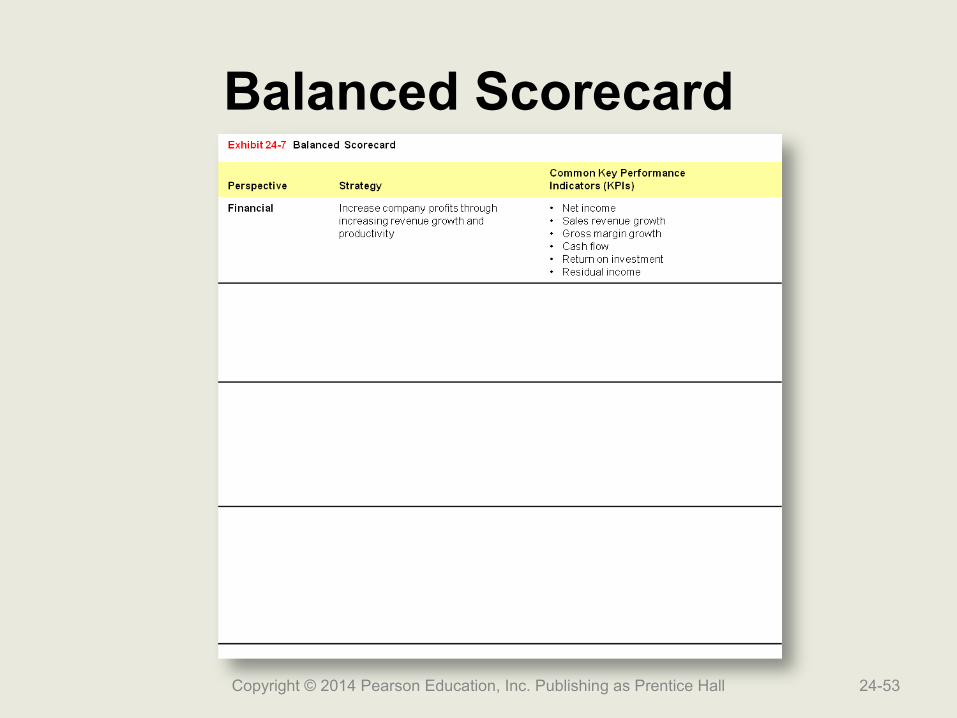

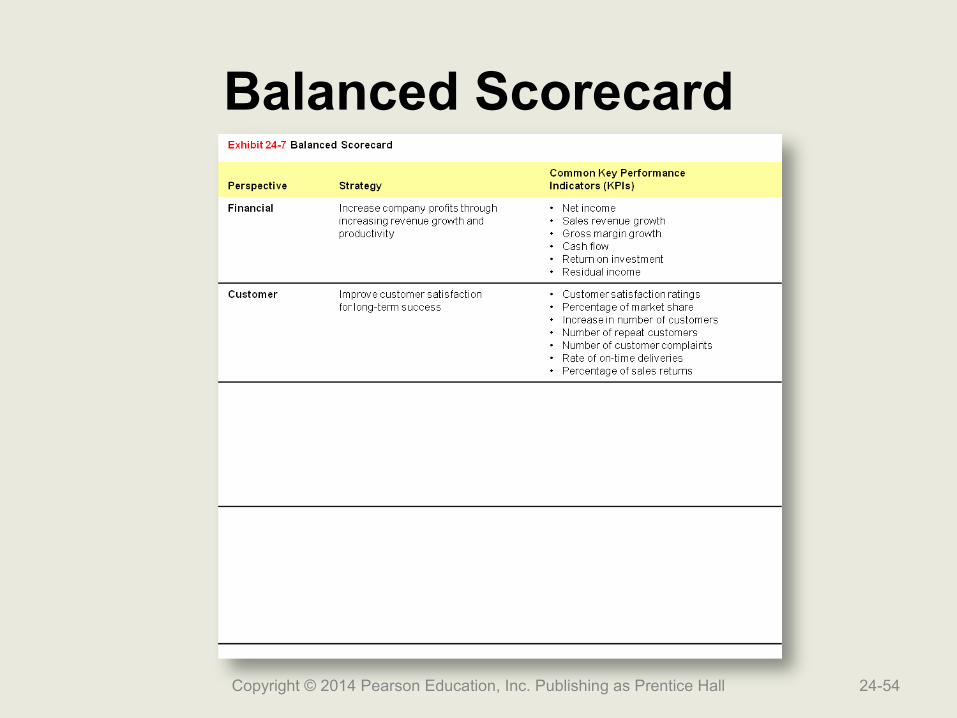

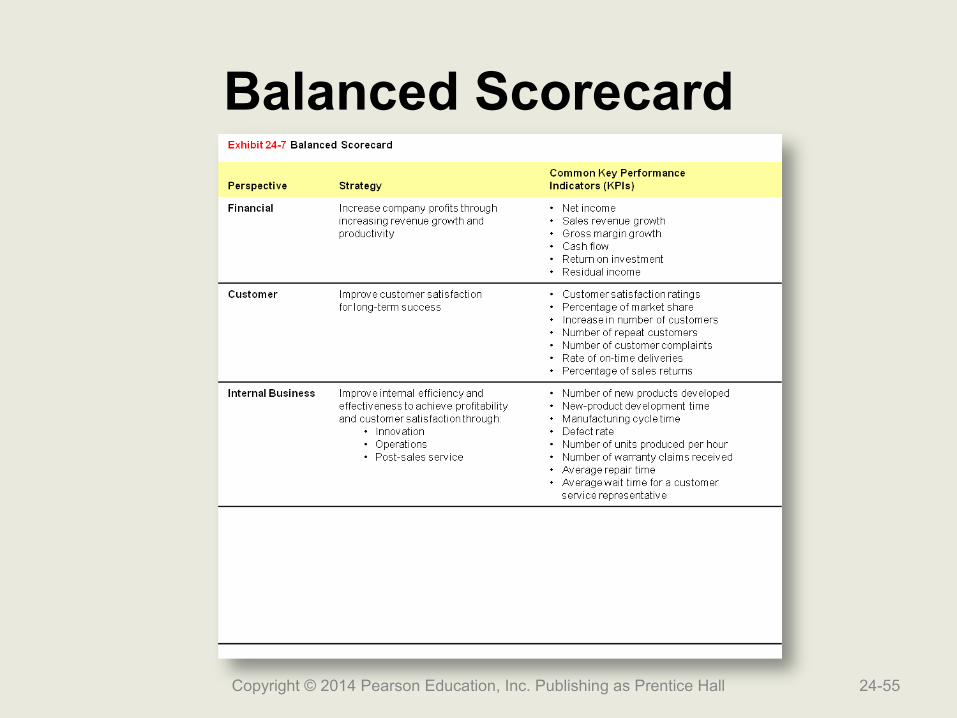

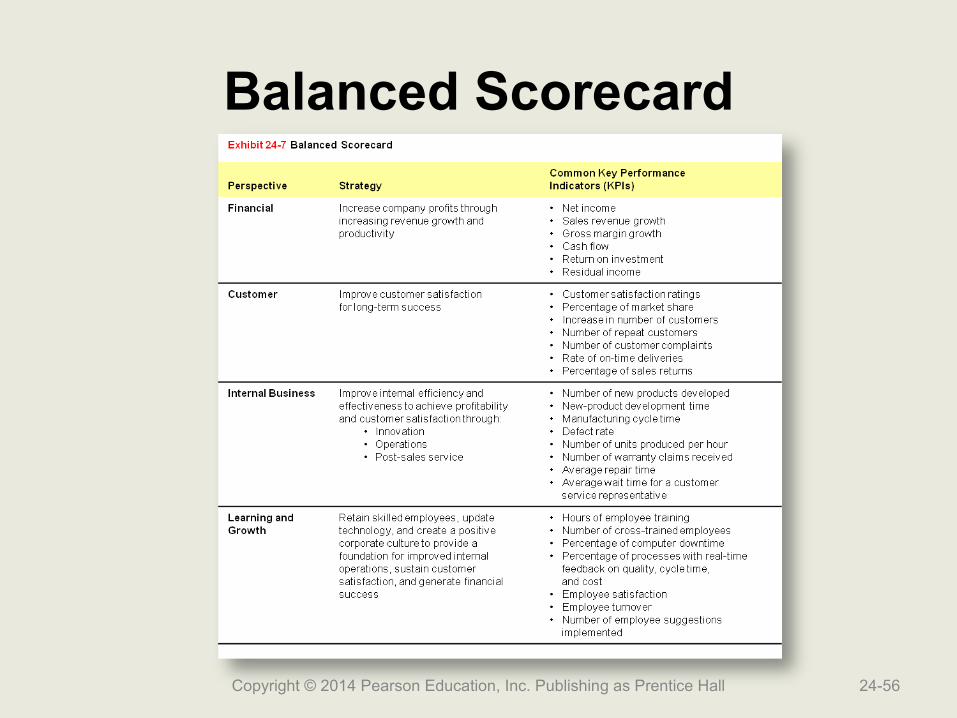

Balanced Scorecard

• Performance evaluation system that requires management to consider:– Financial performance measures (lag

indicators)– Operational performance measures (lead

indicators)• Should link these measures with the company’s:

– Goals– Strategy for achieving those goals

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-52

Balanced Scorecard

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-53

Balanced Scorecard

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-54

Balanced Scorecard

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-55

Balanced Scorecard

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-56

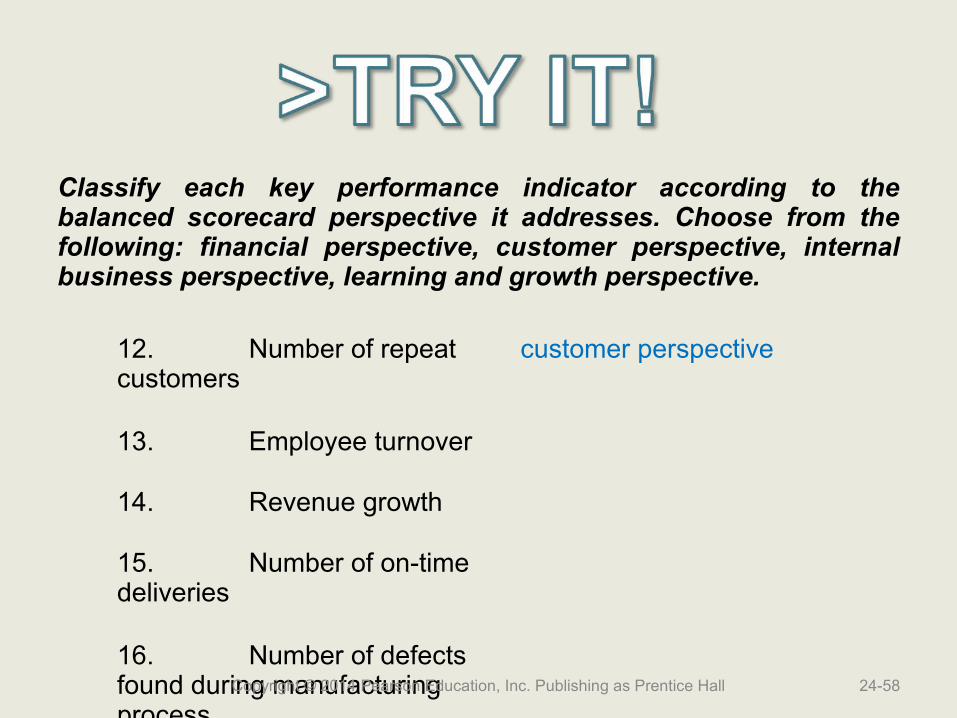

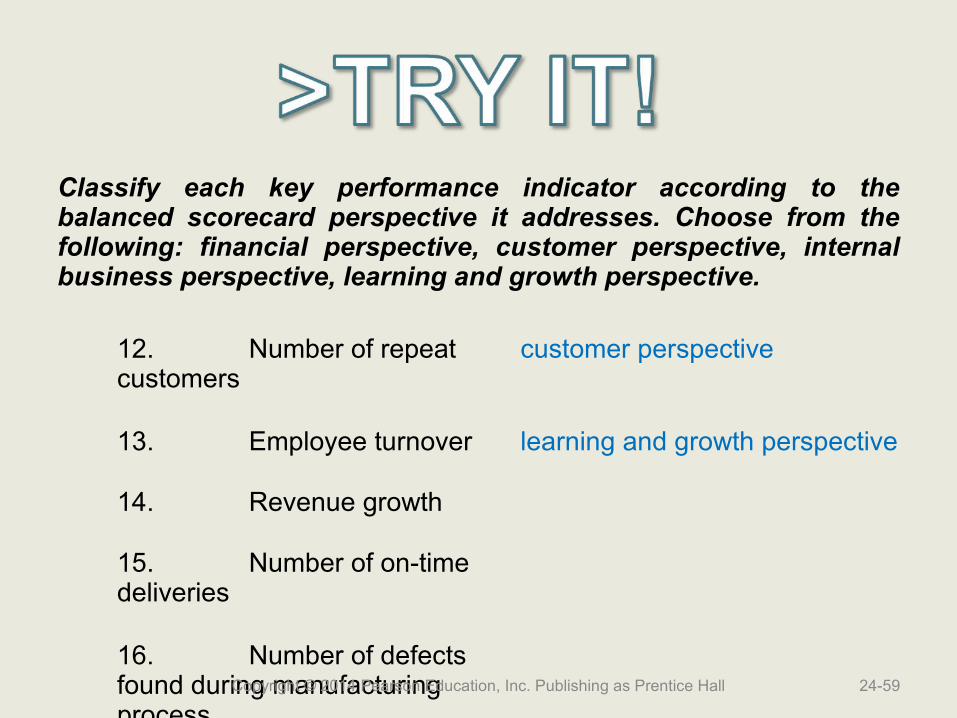

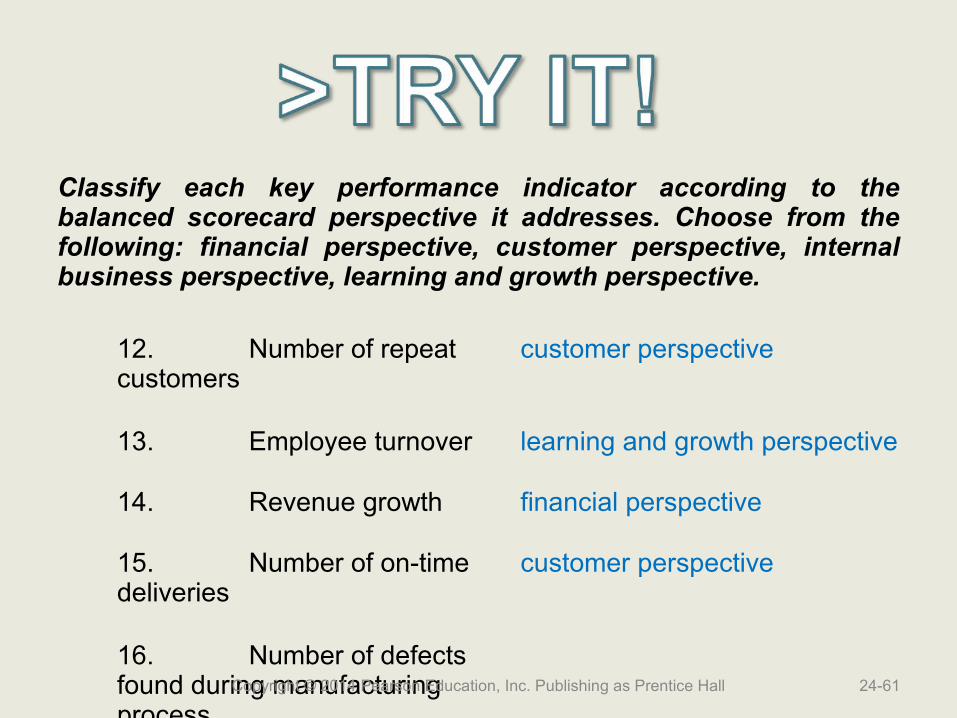

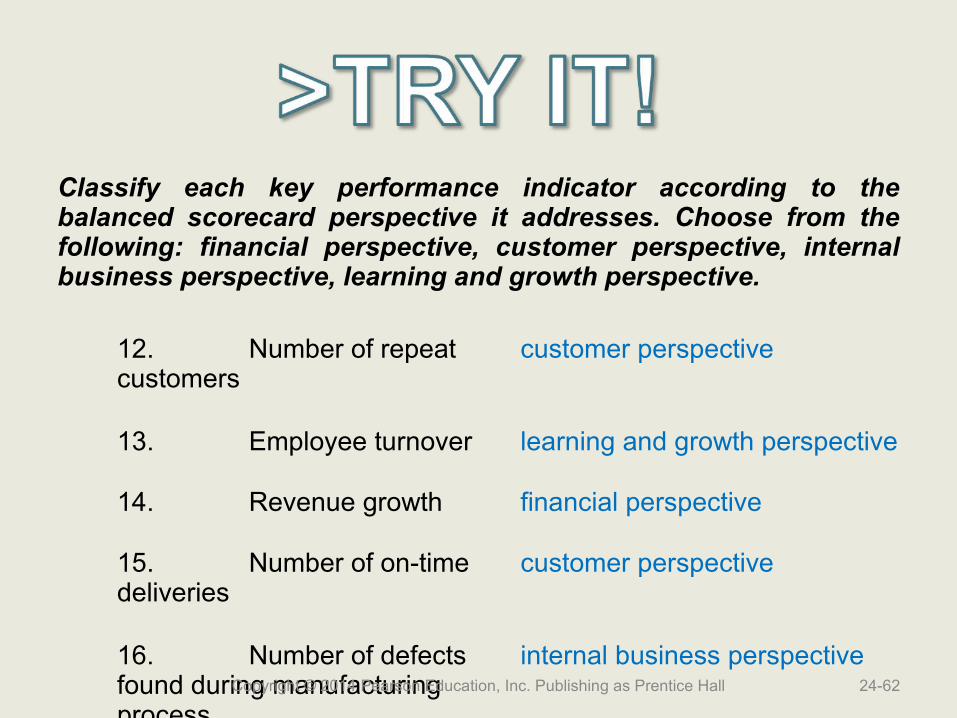

Classify each key performance indicator according to the balanced scorecard perspective it addresses. Choose from the following: financial perspective, customer perspective, internal business perspective, learning and growth perspective.

12. Number of repeat customers

13. Employee turnover

14. Revenue growth

15. Number of on-time deliveries

16. Number of defects found during manufacturing process

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-57

Classify each key performance indicator according to the balanced scorecard perspective it addresses. Choose from the following: financial perspective, customer perspective, internal business perspective, learning and growth perspective.

12. Number of repeat customers

customer perspective

13. Employee turnover

14. Revenue growth

15. Number of on-time deliveries

16. Number of defects found during manufacturing process

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-58

Classify each key performance indicator according to the balanced scorecard perspective it addresses. Choose from the following: financial perspective, customer perspective, internal business perspective, learning and growth perspective.

12. Number of repeat customers

customer perspective

13. Employee turnover learning and growth perspective

14. Revenue growth

15. Number of on-time deliveries

16. Number of defects found during manufacturing process

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-59

Classify each key performance indicator according to the balanced scorecard perspective it addresses. Choose from the following: financial perspective, customer perspective, internal business perspective, learning and growth perspective.

12. Number of repeat customers

customer perspective

13. Employee turnover learning and growth perspective

14. Revenue growth financial perspective

15. Number of on-time deliveries

16. Number of defects found during manufacturing process

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-60

Classify each key performance indicator according to the balanced scorecard perspective it addresses. Choose from the following: financial perspective, customer perspective, internal business perspective, learning and growth perspective.

12. Number of repeat customers

customer perspective

13. Employee turnover learning and growth perspective

14. Revenue growth financial perspective

15. Number of on-time deliveries

customer perspective

16. Number of defects found during manufacturing process

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-61

Classify each key performance indicator according to the balanced scorecard perspective it addresses. Choose from the following: financial perspective, customer perspective, internal business perspective, learning and growth perspective.

12. Number of repeat customers

customer perspective

13. Employee turnover learning and growth perspective

14. Revenue growth financial perspective

15. Number of on-time deliveries

customer perspective

16. Number of defects found during manufacturing process

internal business perspectiveCopyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-62

Learning Objective 4

Use responsibility Use responsibility reports to evaluate reports to evaluate cost, revenue, and cost, revenue, and

profit centersprofit centers

24-63Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall

Responsibility Accounting Performance Reports

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-64

Controllable Cost

• Cost that the manager has the power to influence by his or her decisions

• All costs are ultimately controllable at the upper levels of management

• Controllability decreases as responsibility decreases

• Responsibility accounting performance report (responsibility report) is completed for each manager of a business segment

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-65

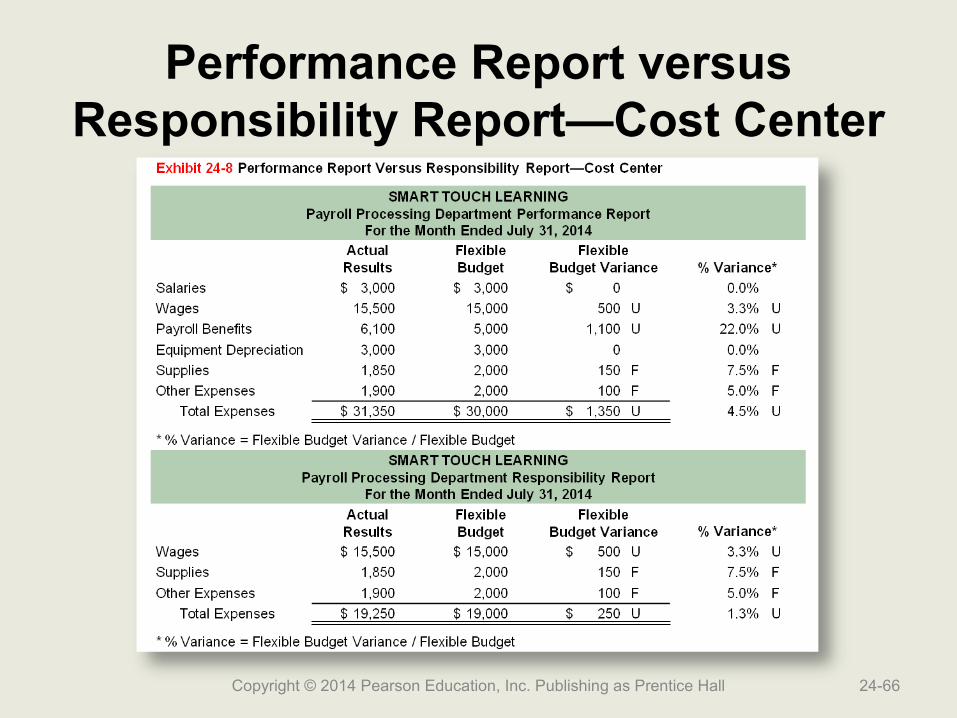

Performance Report versus Responsibility Report—Cost Center

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-66

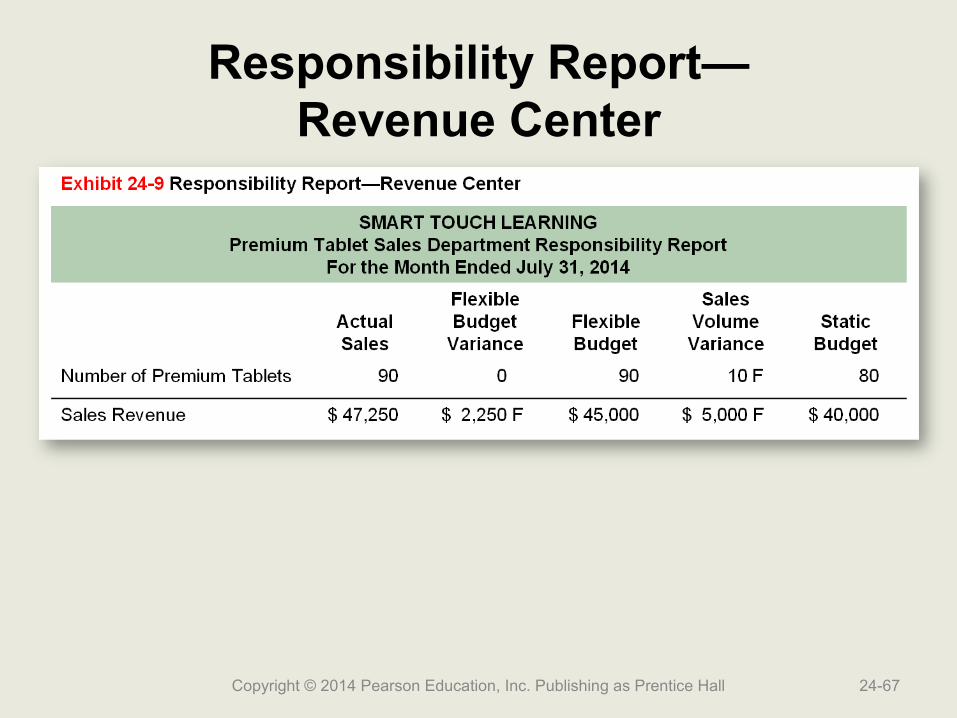

Responsibility Report—Revenue Center

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-67

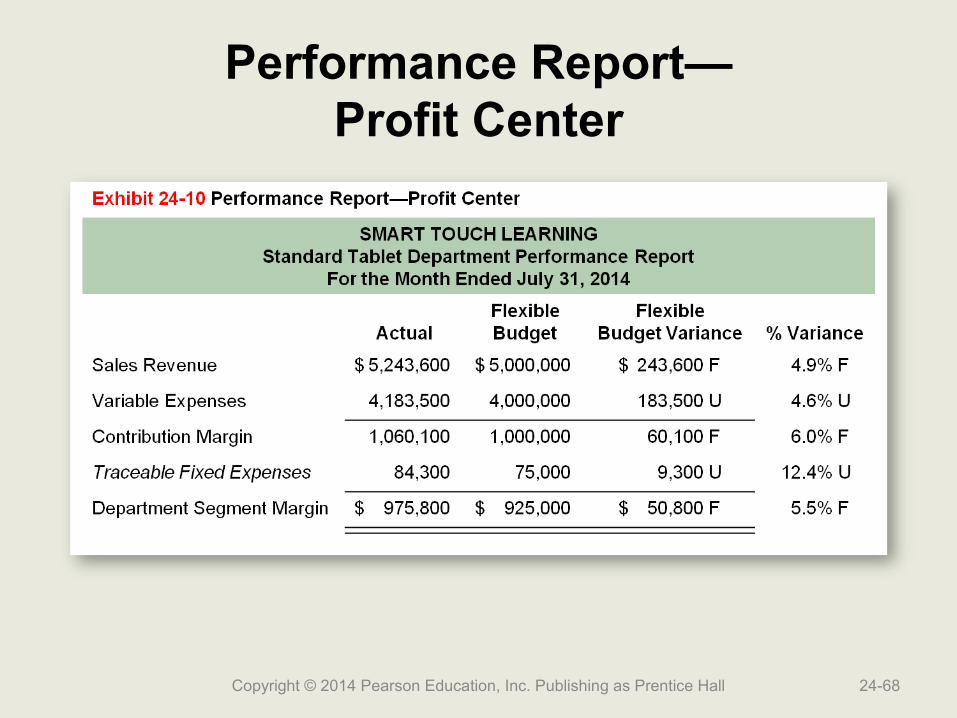

Performance Report—Profit Center

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-68

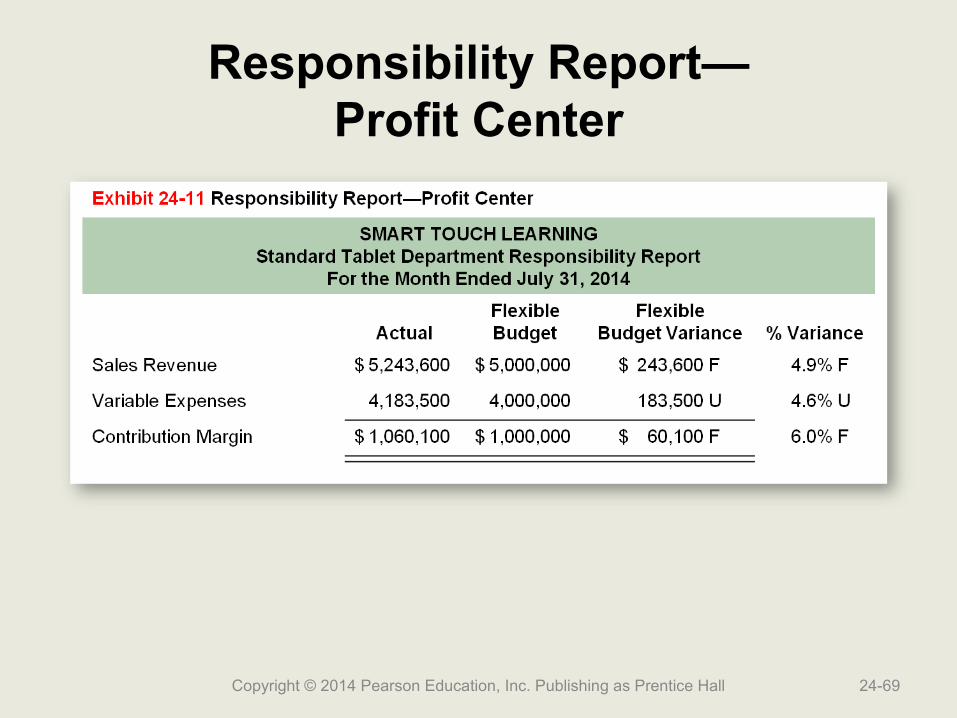

Responsibility Report—Profit Center

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-69

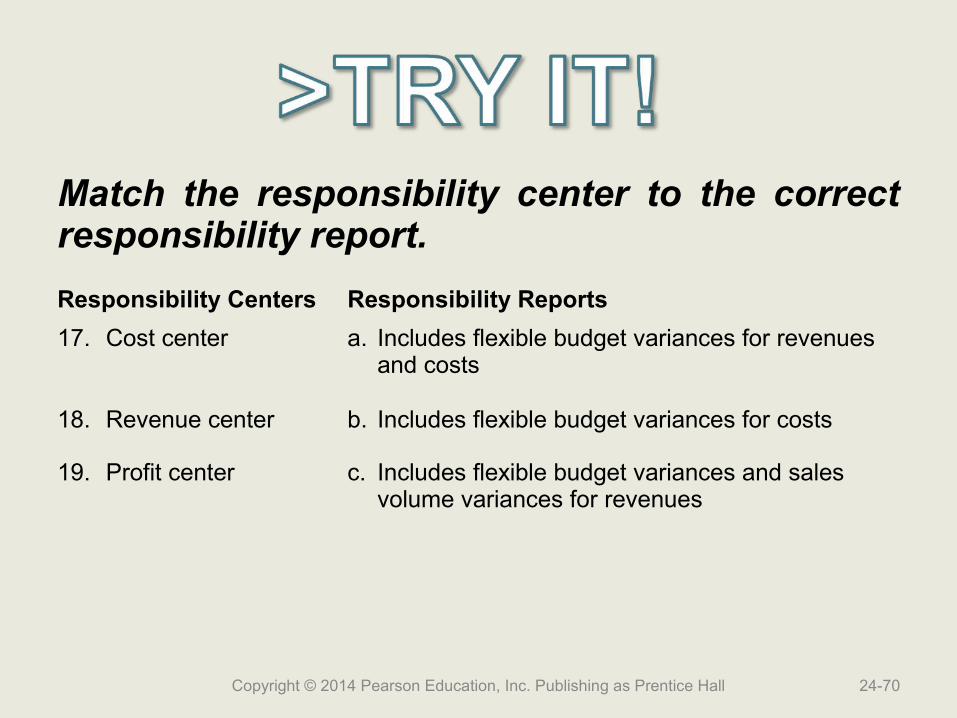

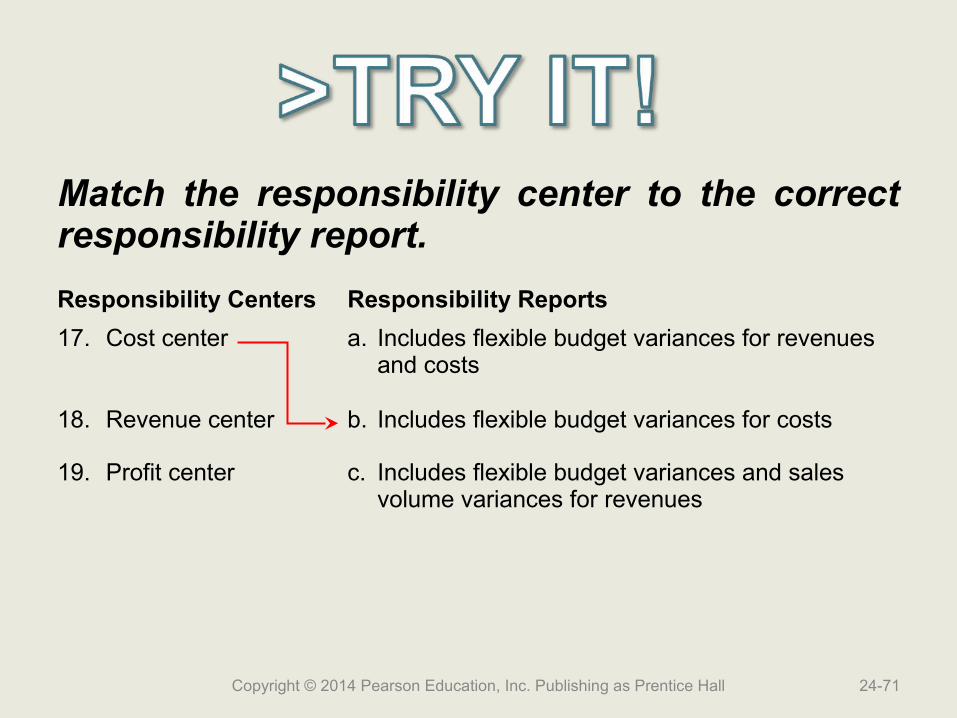

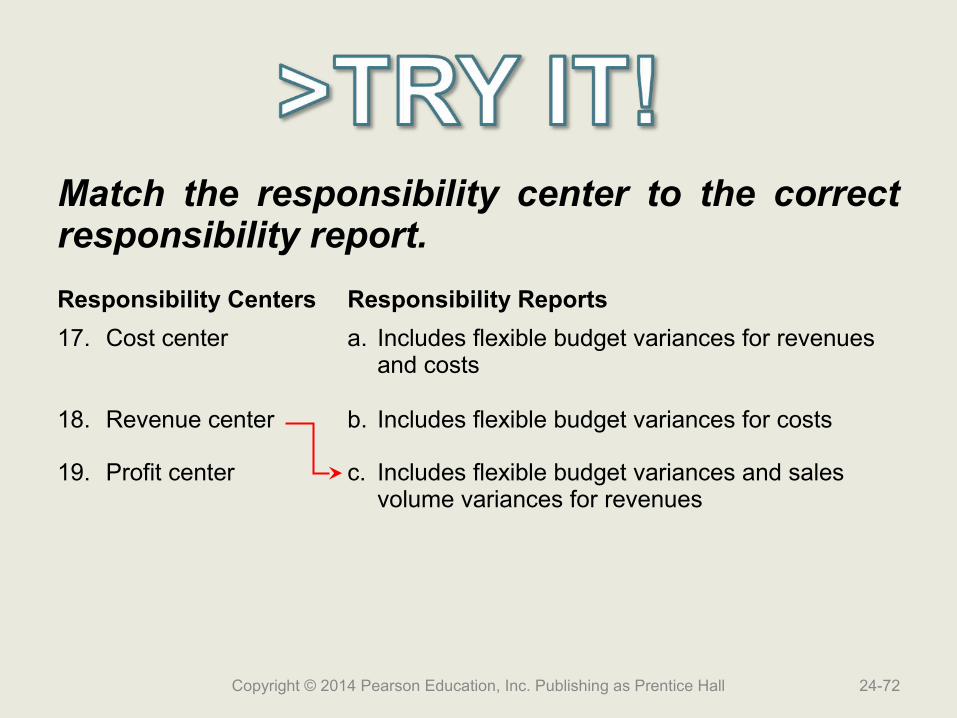

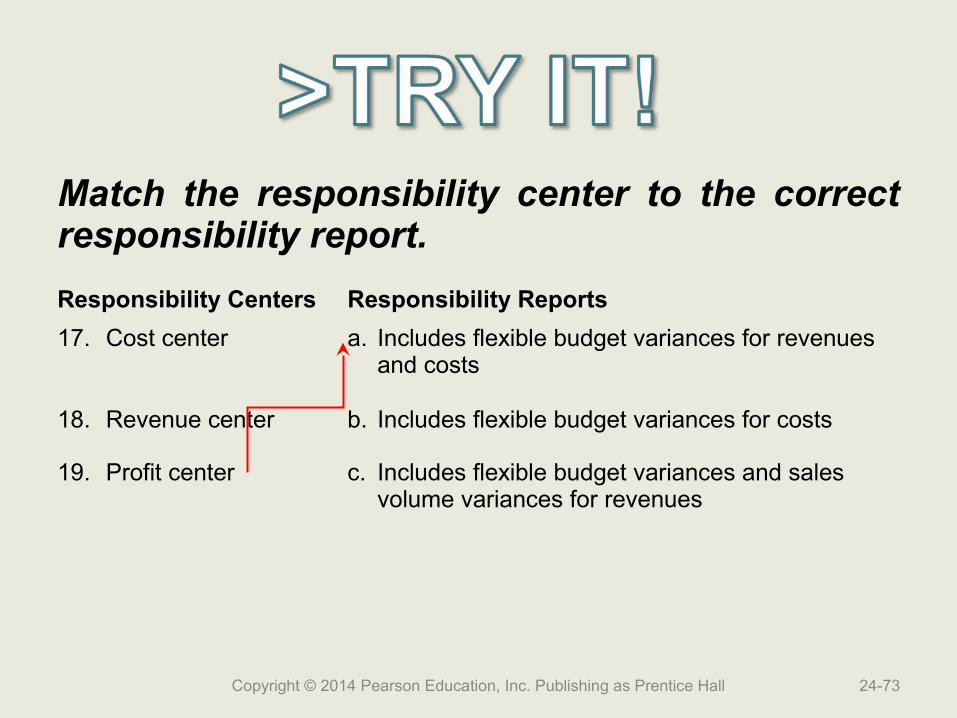

Match the responsibility center to the correct responsibility report.

Responsibility Centers Responsibility Reports

17. Cost center a. Includes flexible budget variances for revenues and costs

18. Revenue center b. Includes flexible budget variances for costs

19. Profit center c. Includes flexible budget variances and sales volume variances for revenues

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-70

Match the responsibility center to the correct responsibility report.

Responsibility Centers Responsibility Reports

17. Cost center a. Includes flexible budget variances for revenues and costs

18. Revenue center b. Includes flexible budget variances for costs

19. Profit center c. Includes flexible budget variances and sales volume variances for revenues

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-71

Match the responsibility center to the correct responsibility report.

Responsibility Centers Responsibility Reports

17. Cost center a. Includes flexible budget variances for revenues and costs

18. Revenue center b. Includes flexible budget variances for costs

19. Profit center c. Includes flexible budget variances and sales volume variances for revenues

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-72

Match the responsibility center to the correct responsibility report.

Responsibility Centers Responsibility Reports

17. Cost center a. Includes flexible budget variances for revenues and costs

18. Revenue center b. Includes flexible budget variances for costs

19. Profit center c. Includes flexible budget variances and sales volume variances for revenues

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-73

Learning Objective 5

Use return on Use return on investment (ROI) and investment (ROI) and

residual income (RI) to residual income (RI) to evaluate investment evaluate investment

centerscenters

24-74Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall

Investment Centers

• Large divisions of a company• Manager’s duties are similar to those of a CEO

– Generate profit– Make the best use of the assets

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-75

Financial Evaluation of Investment Centers Must Measure:

• How much operating income the segment is generating

• How efficiently the segment is using its assets

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-76

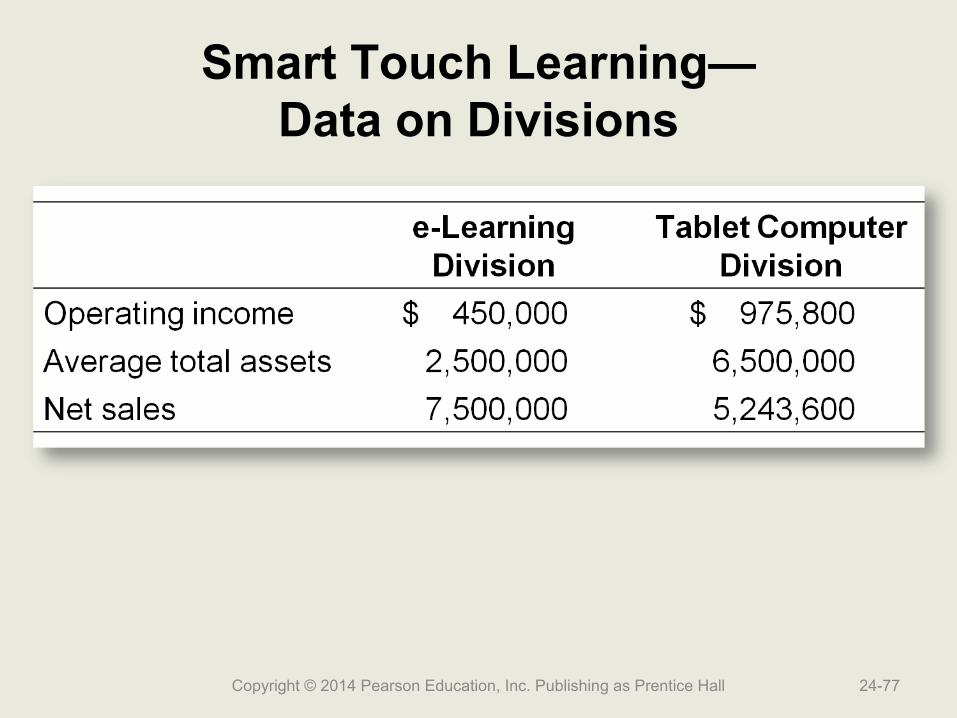

Smart Touch Learning—Data on Divisions

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-77

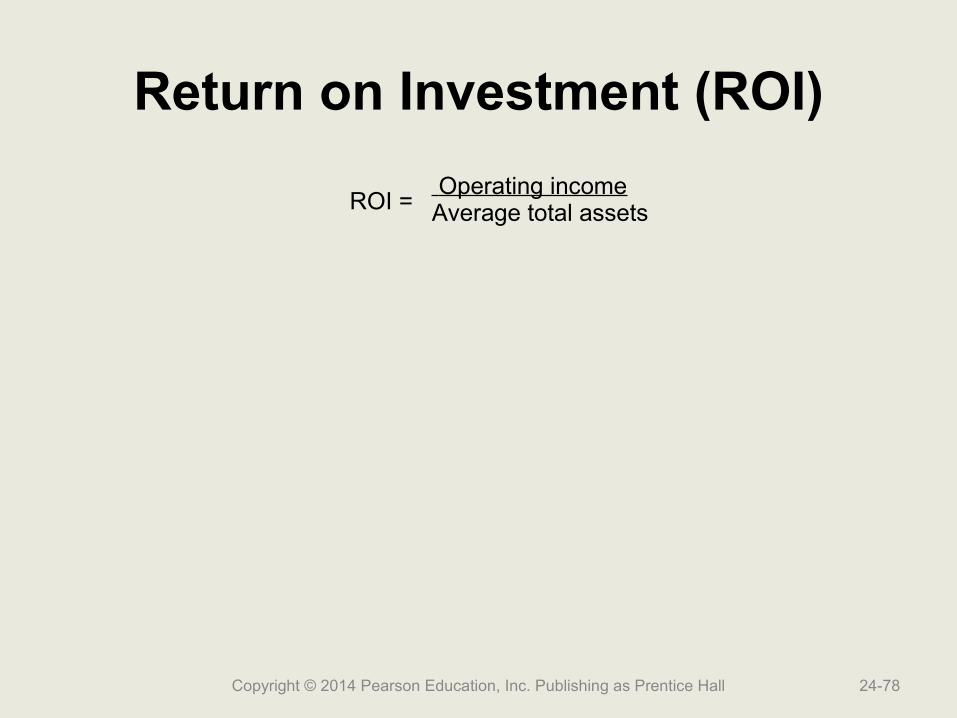

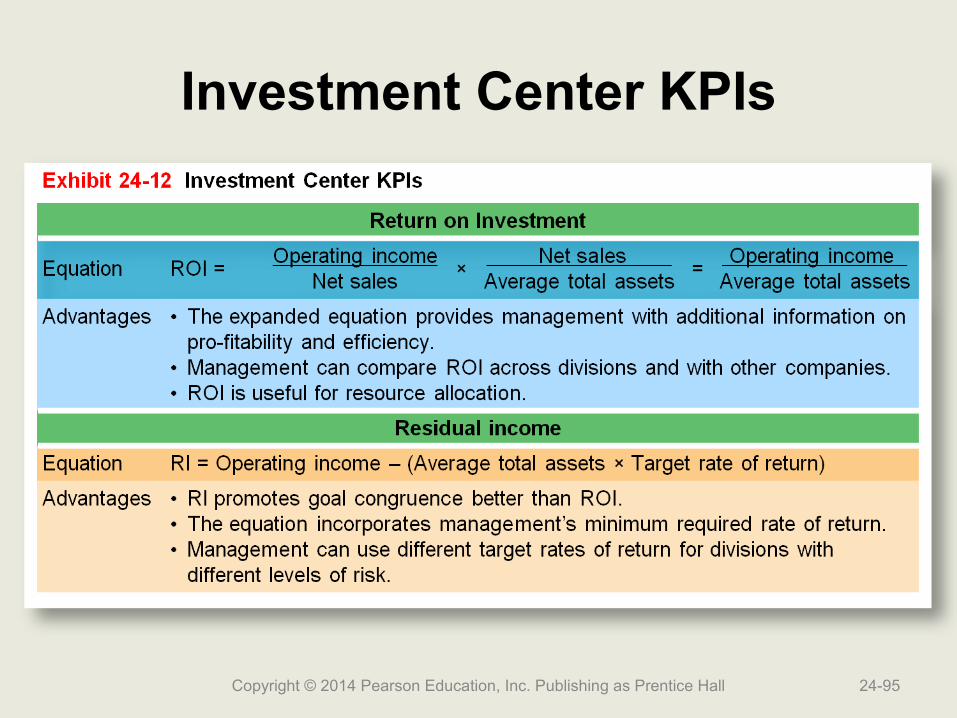

Return on Investment (ROI)

ROI = Operating incomeAverage total assets

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-78

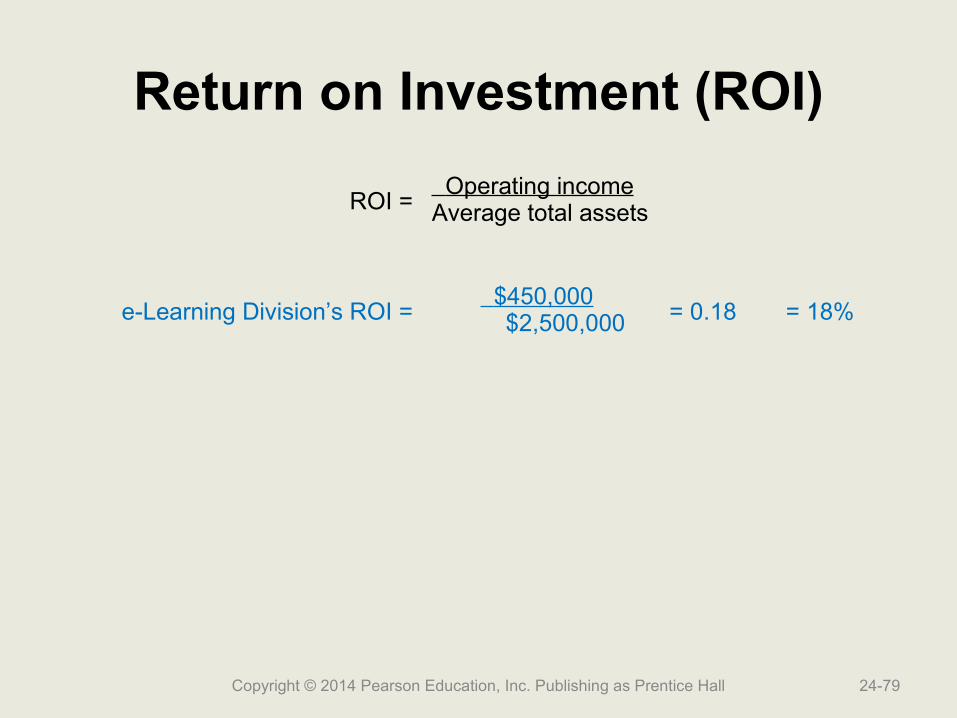

Return on Investment (ROI)

ROI = Operating incomeAverage total assets

e-Learning Division’s ROI = $450,000

$2,500,000 = 0.18 = 18%

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-79

Return on Investment (ROI)

ROI = Operating incomeAverage total assets

e-Learning Division’s ROI = $450,000

$2,500,000 = 0.18 = 18%

Tablet Computer Division’s ROI = $975,800

$6,500,000 = 0.15 = 15%

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-80

Expanded ROI Equation

ROI = Operating incomeNet sales

×Net sales

Average total assets= Operating income

Average total assets

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-81

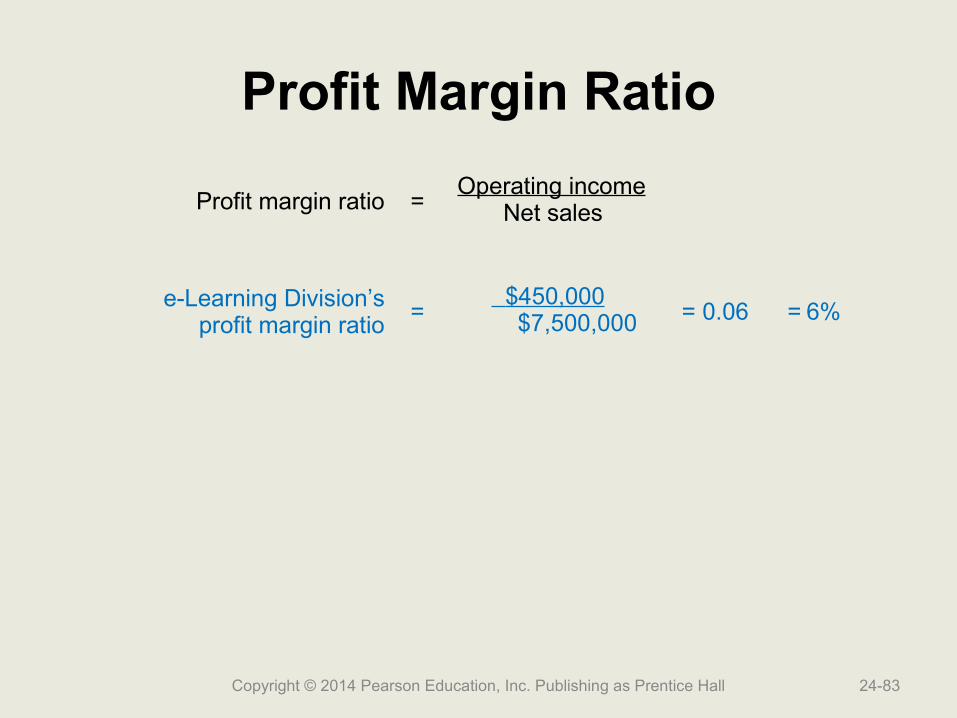

Profit Margin Ratio

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-82

Profit margin ratio =Operating income

Net sales

Profit Margin Ratio

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-83

Profit margin ratio =Operating income

Net sales

e-Learning Division’sprofit margin ratio

= $450,000

$7,500,000 = 0.06 = 6%

Profit Margin Ratio

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-84

Profit margin ratio =Operating income

Net sales

e-Learning Division’sprofit margin ratio

= $450,000

$7,500,000 = 0.06 = 6%

Tablet Computer Division’sprofit margin ratio

= $975,800

$5,243,600 = 0.19 =19%

Asset Turnover Ratio

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-85

Asset turnover ratio =Net sales

Average total assets

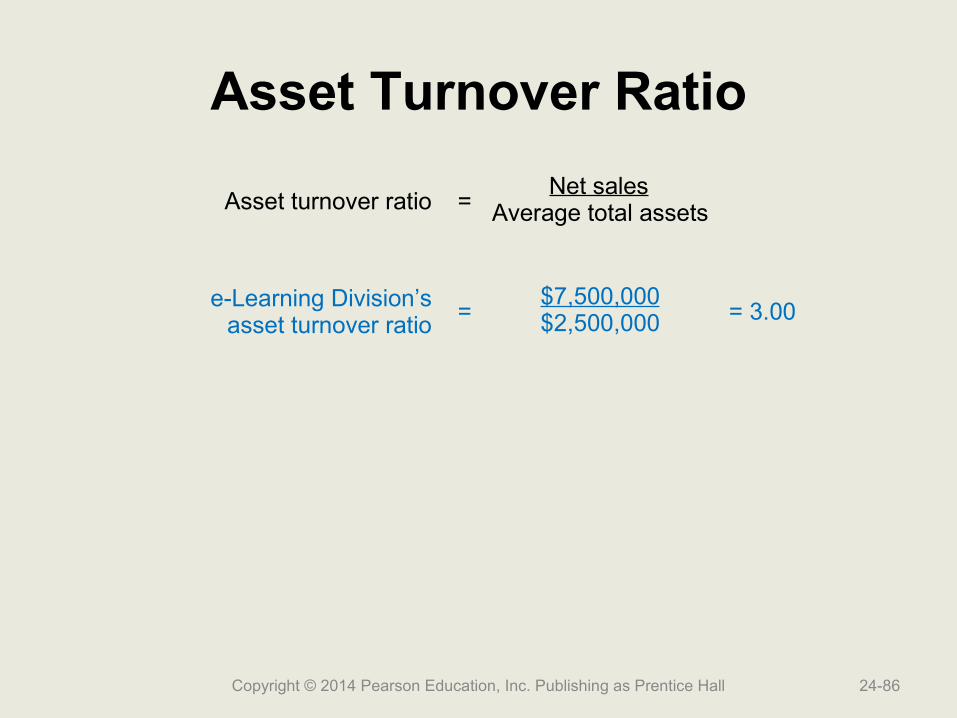

Asset Turnover Ratio

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-86

Asset turnover ratio =Net sales

Average total assets

e-Learning Division’sasset turnover ratio

=$7,500,000$2,500,000 = 3.00

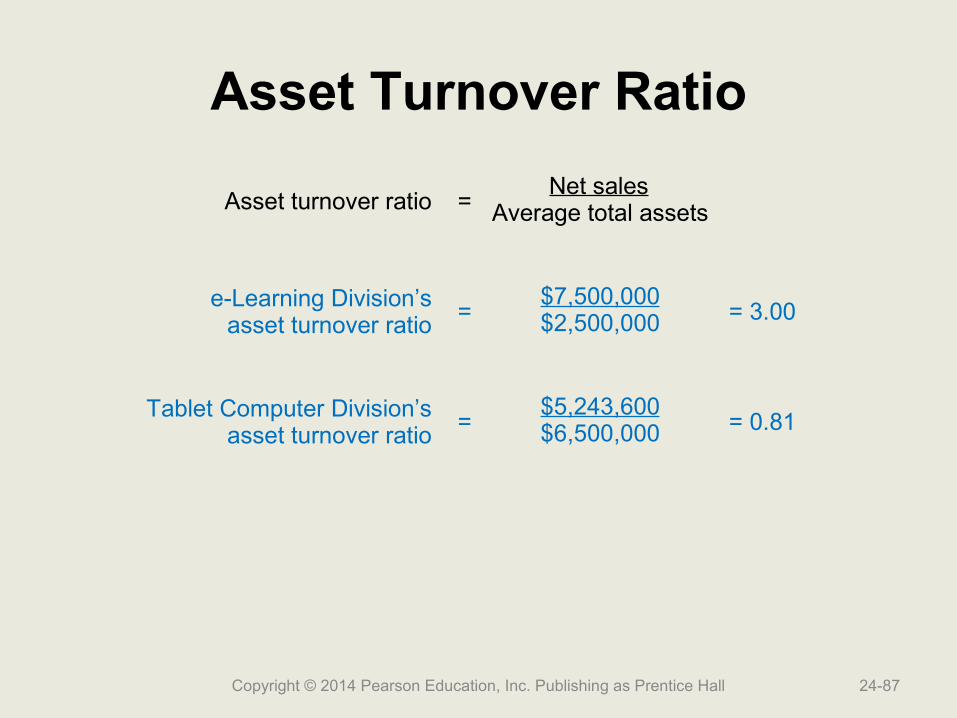

Asset Turnover Ratio

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-87

Asset turnover ratio =Net sales

Average total assets

e-Learning Division’sasset turnover ratio

=$7,500,000$2,500,000 = 3.00

Tablet Computer Division’sasset turnover ratio

=$5,243,600$6,500,000 = 0.81

Expanded ROI Equation

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-88

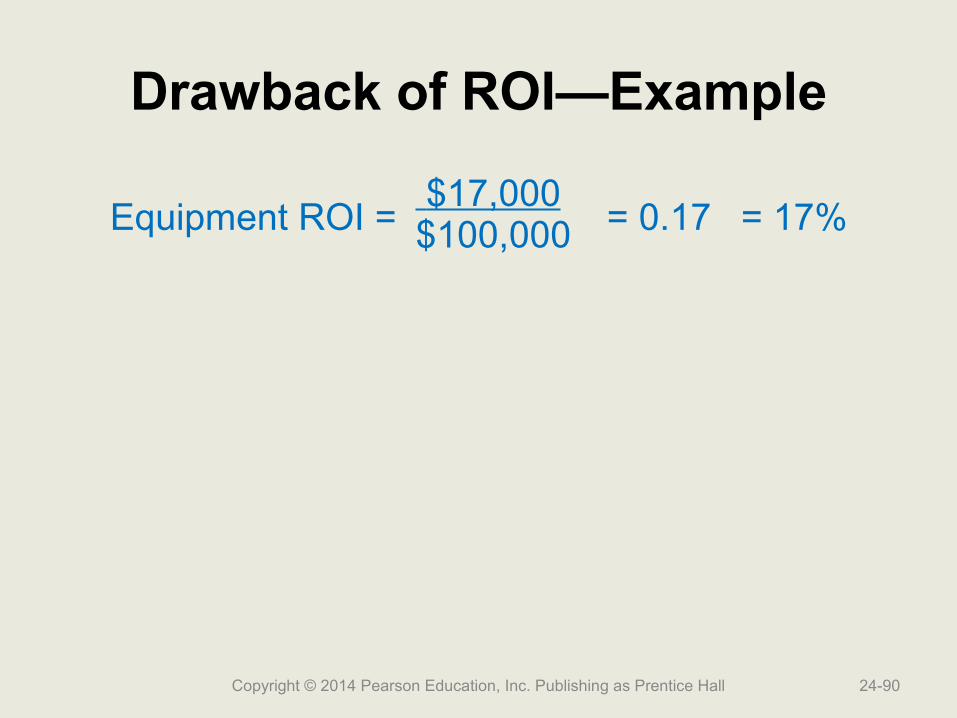

Drawback of ROI—Example

• Companywide target ROI of 16%• Both divisions are considering investing in

in-store video display equipment that shows customers how to use featured products– Cost is $100,000– Expected annual operating income is

$17,000

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-89

Drawback of ROI—Example

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-90

Equipment ROI = $17,000$100,000 = 0.17 = 17%

Residual Income

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-91

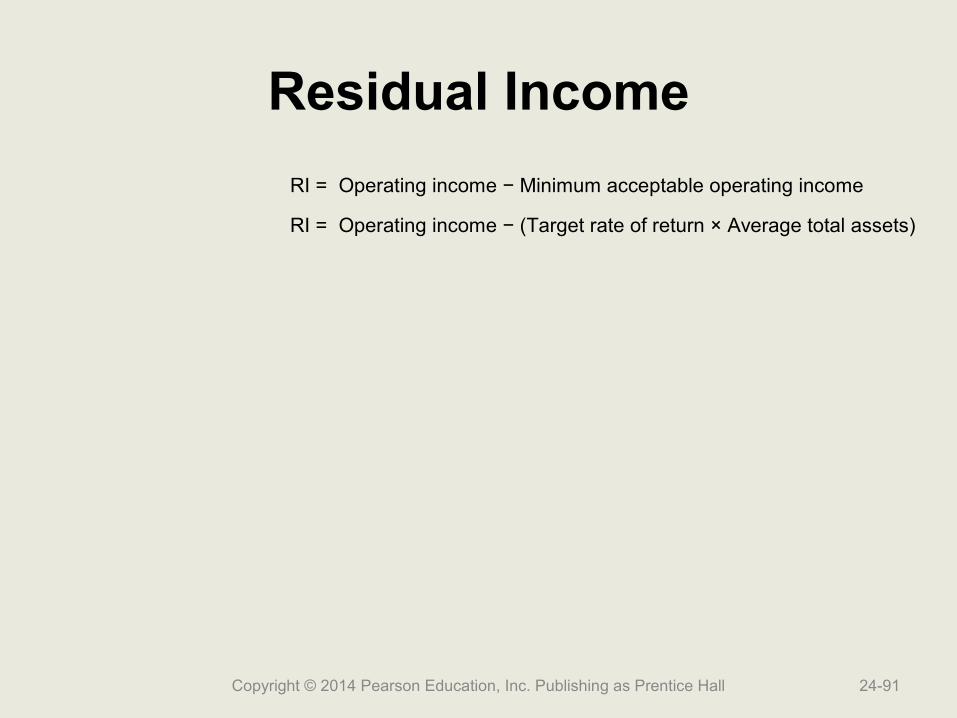

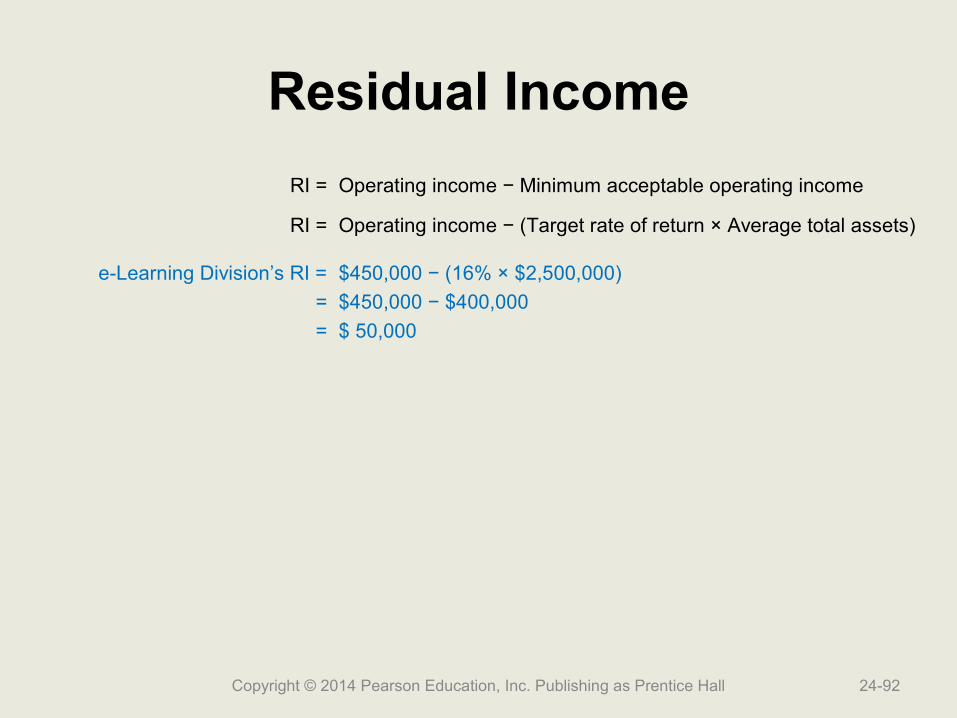

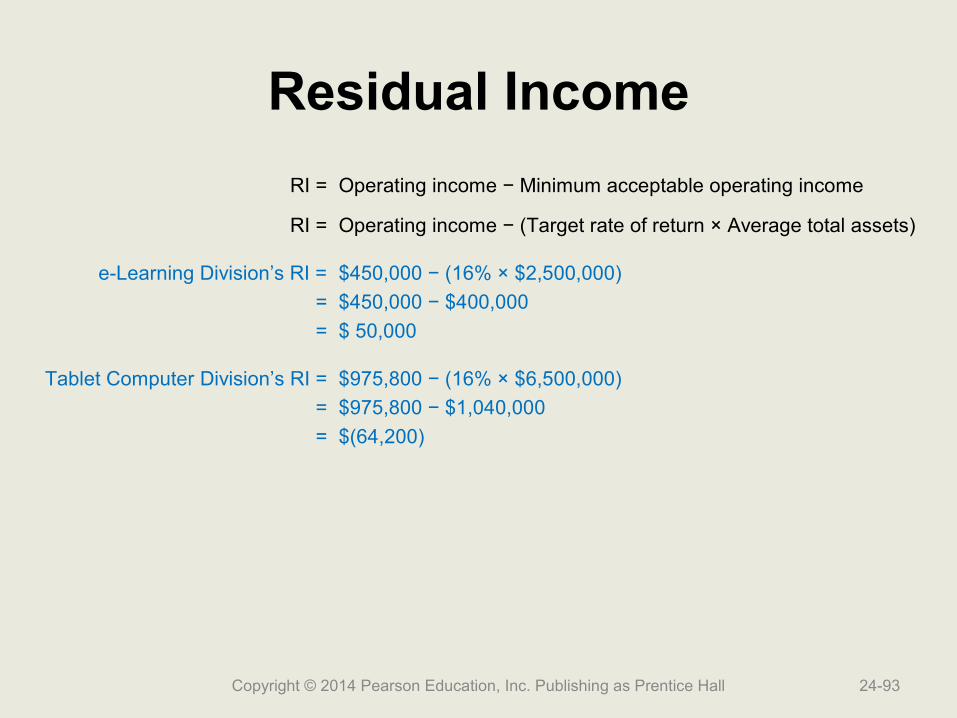

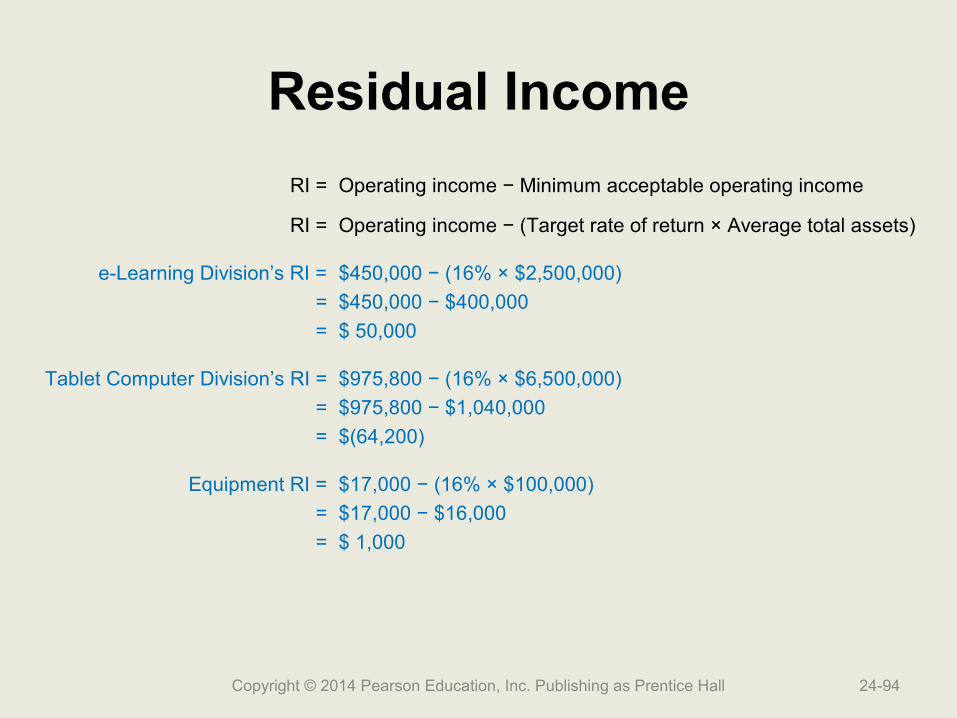

RI = Operating income − Minimum acceptable operating income

RI = Operating income − (Target rate of return × Average total assets)

Residual Income

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-92

RI = Operating income − Minimum acceptable operating income

RI = Operating income − (Target rate of return × Average total assets)

e-Learning Division’s RI = $450,000 − (16% × $2,500,000)

= $450,000 − $400,000

= $ 50,000

Residual Income

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-93

RI = Operating income − Minimum acceptable operating income

RI = Operating income − (Target rate of return × Average total assets)

e-Learning Division’s RI = $450,000 − (16% × $2,500,000)

= $450,000 − $400,000

= $ 50,000

Tablet Computer Division’s RI = $975,800 − (16% × $6,500,000)

= $975,800 − $1,040,000

= $(64,200)

Residual Income

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-94

RI = Operating income − Minimum acceptable operating income

RI = Operating income − (Target rate of return × Average total assets)

e-Learning Division’s RI = $450,000 − (16% × $2,500,000)

= $450,000 − $400,000

= $ 50,000

Tablet Computer Division’s RI = $975,800 − (16% × $6,500,000)

= $975,800 − $1,040,000

= $(64,200)

Equipment RI = $17,000 − (16% × $100,000)

= $17,000 − $16,000

= $ 1,000

Investment Center KPIs

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-95

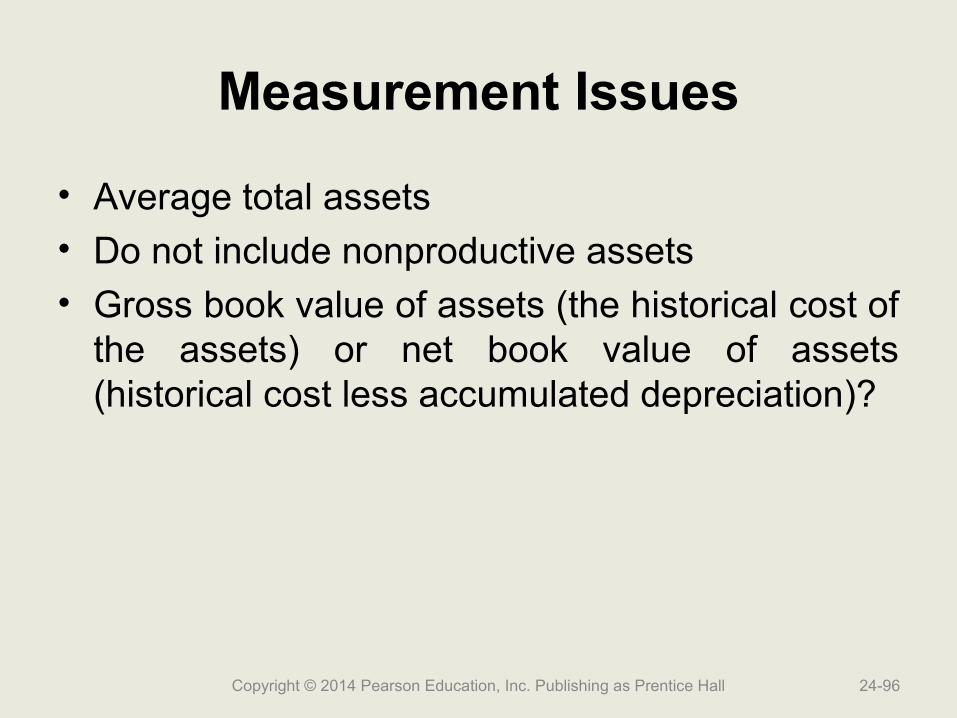

Measurement Issues

• Average total assets• Do not include nonproductive assets• Gross book value of assets (the historical cost of

the assets) or net book value of assets (historical cost less accumulated depreciation)?

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-96

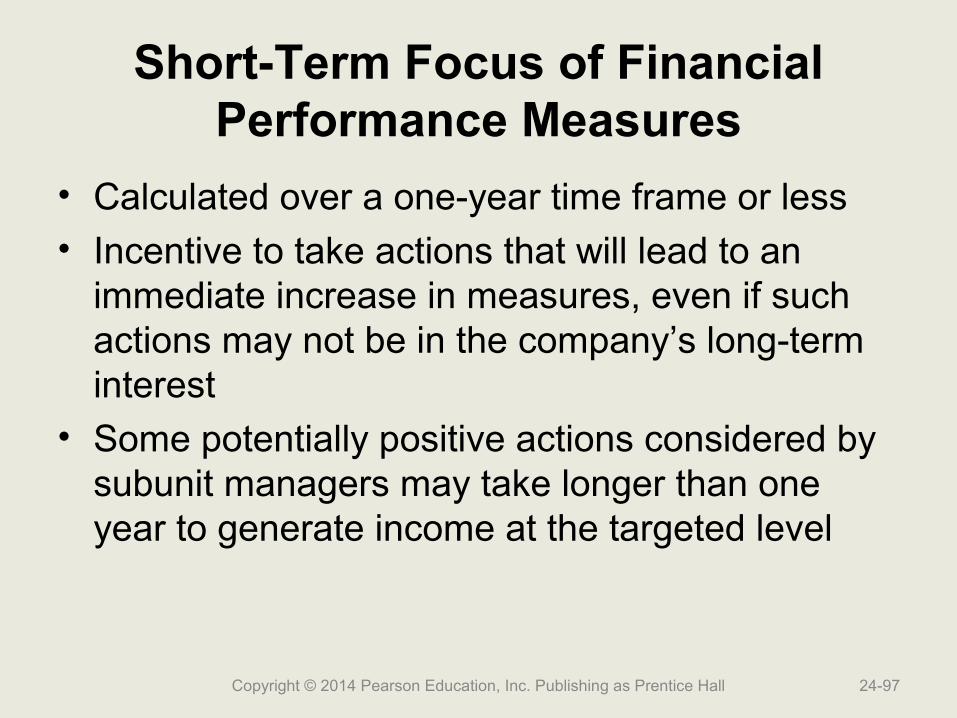

Short-Term Focus of Financial Performance Measures

• Calculated over a one-year time frame or less• Incentive to take actions that will lead to an

immediate increase in measures, even if such actions may not be in the company’s long-term interest

• Some potentially positive actions considered by subunit managers may take longer than one year to generate income at the targeted level

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-97

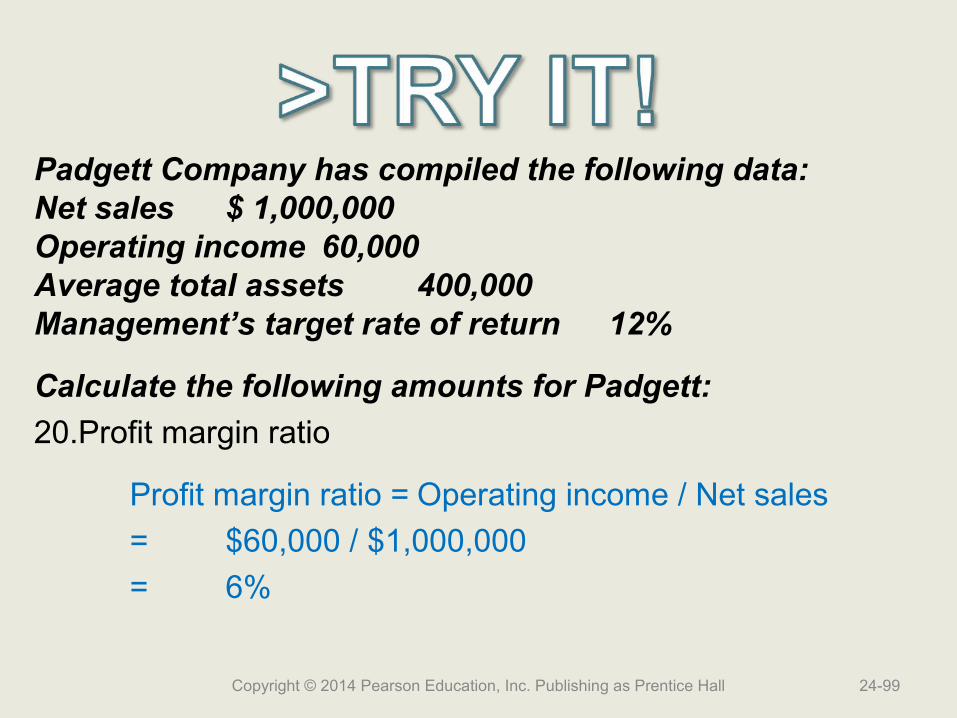

Padgett Company has compiled the following data:Net sales $ 1,000,000Operating income 60,000Average total assets 400,000Management’s target rate of return 12%

Calculate the following amounts for Padgett:

20.Profit margin ratio

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-98

Padgett Company has compiled the following data:Net sales $ 1,000,000Operating income 60,000Average total assets 400,000Management’s target rate of return 12%

Calculate the following amounts for Padgett:

20.Profit margin ratio

Profit margin ratio = Operating income / Net sales

= $60,000 / $1,000,000

= 6%

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-99

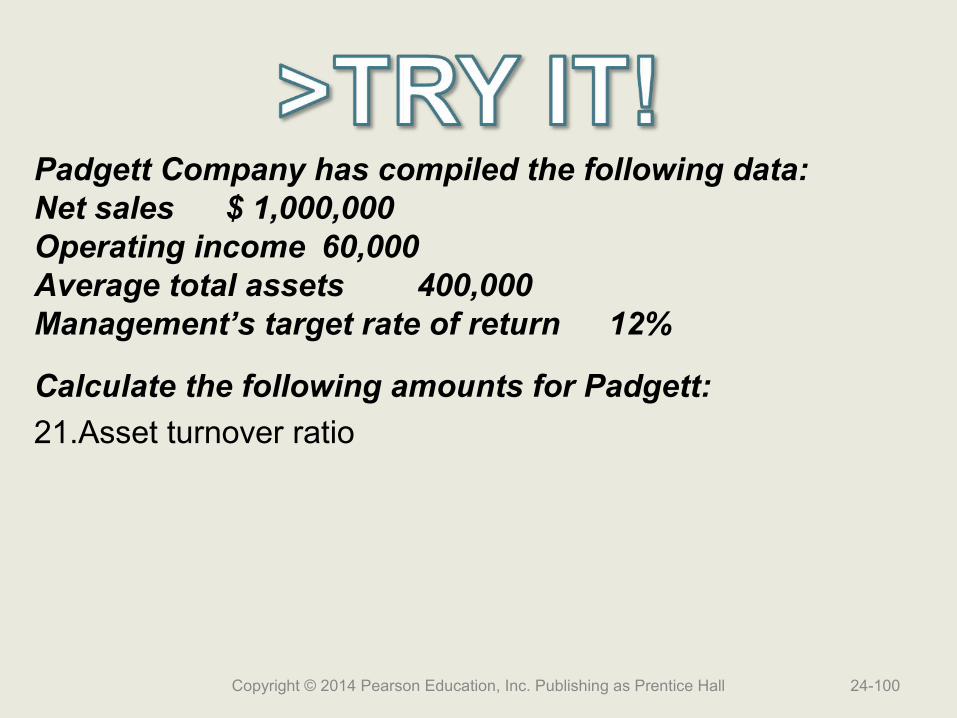

Padgett Company has compiled the following data:Net sales $ 1,000,000Operating income 60,000Average total assets 400,000Management’s target rate of return 12%

Calculate the following amounts for Padgett:

21.Asset turnover ratio

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-100

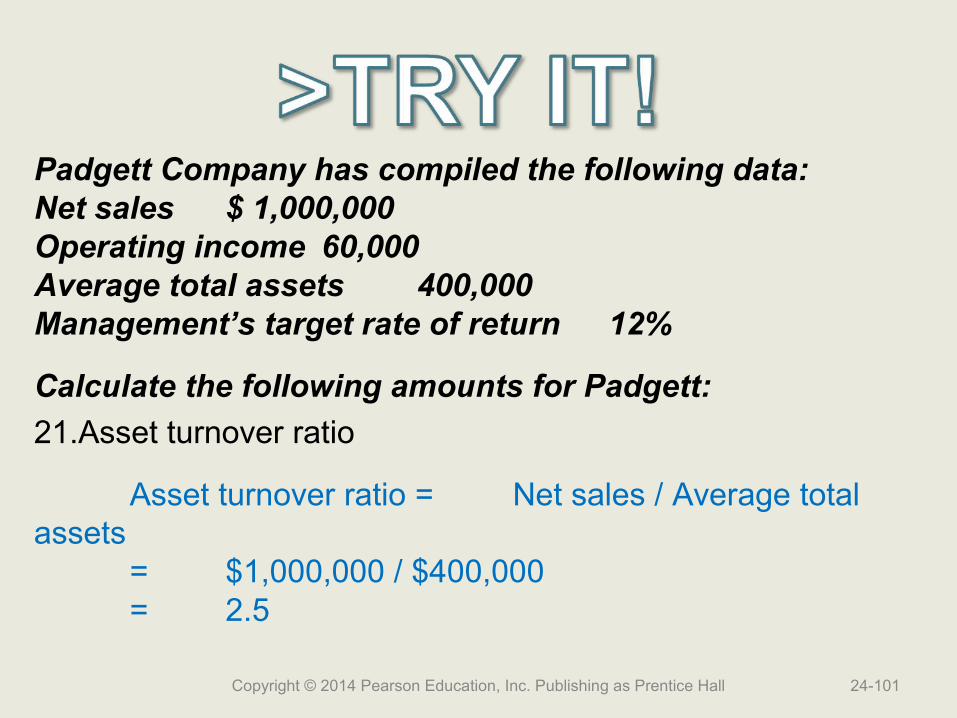

Padgett Company has compiled the following data:Net sales $ 1,000,000Operating income 60,000Average total assets 400,000Management’s target rate of return 12%

Calculate the following amounts for Padgett:

21.Asset turnover ratio

Asset turnover ratio = Net sales / Average total assets

= $1,000,000 / $400,000= 2.5

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-101

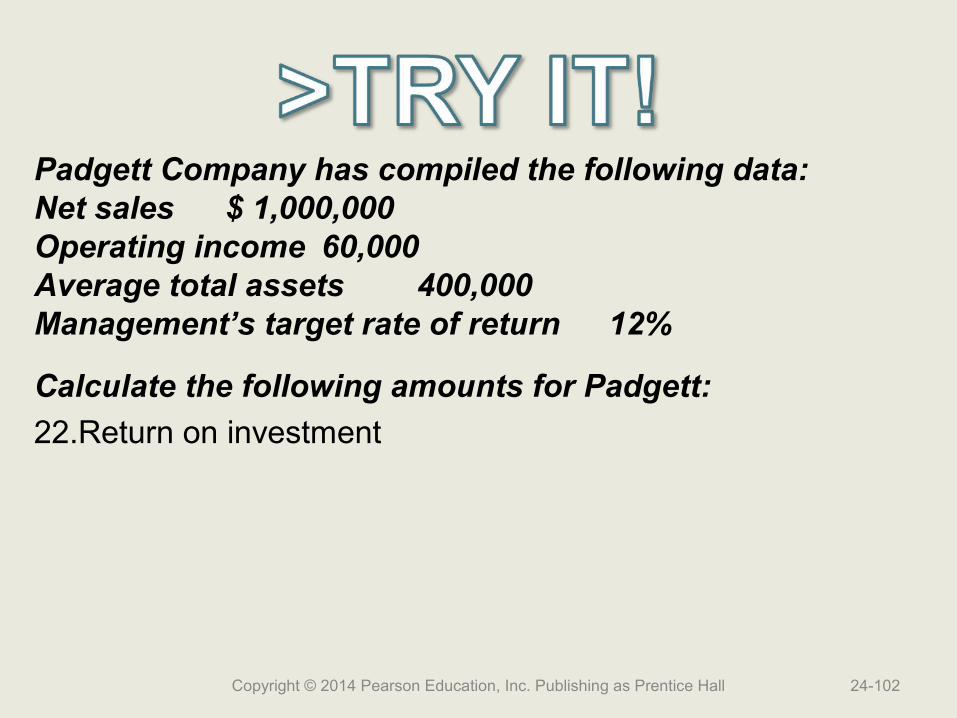

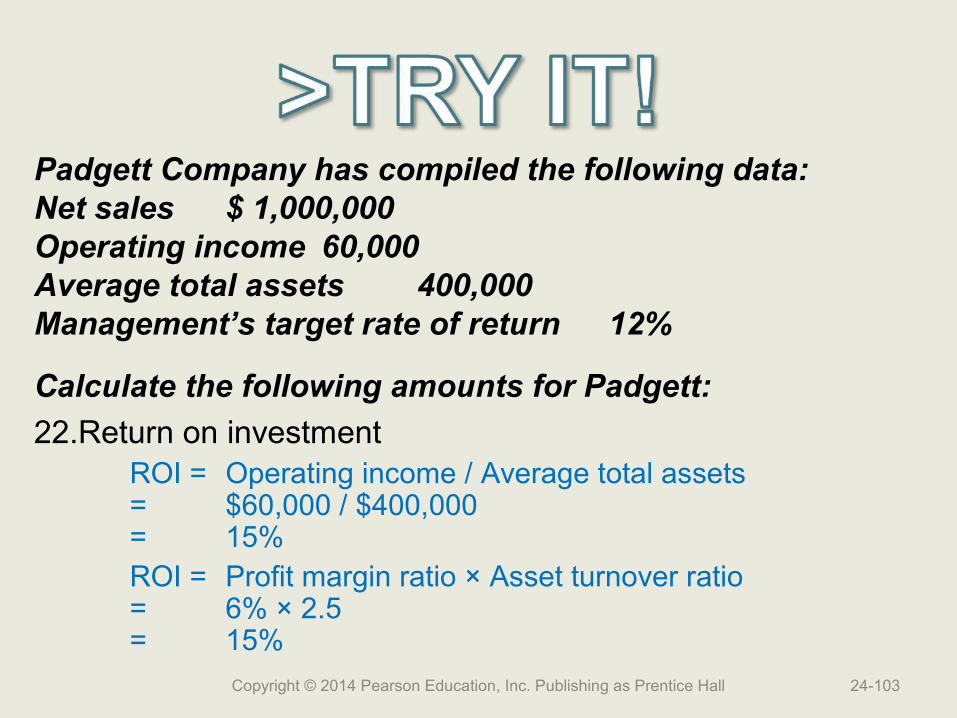

Padgett Company has compiled the following data:Net sales $ 1,000,000Operating income 60,000Average total assets 400,000Management’s target rate of return 12%

Calculate the following amounts for Padgett:

22.Return on investment

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-102

Padgett Company has compiled the following data:Net sales $ 1,000,000Operating income 60,000Average total assets 400,000Management’s target rate of return 12%

Calculate the following amounts for Padgett:

22.Return on investmentROI = Operating income / Average total assets= $60,000 / $400,000= 15%ROI = Profit margin ratio × Asset turnover ratio= 6% × 2.5= 15%

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-103

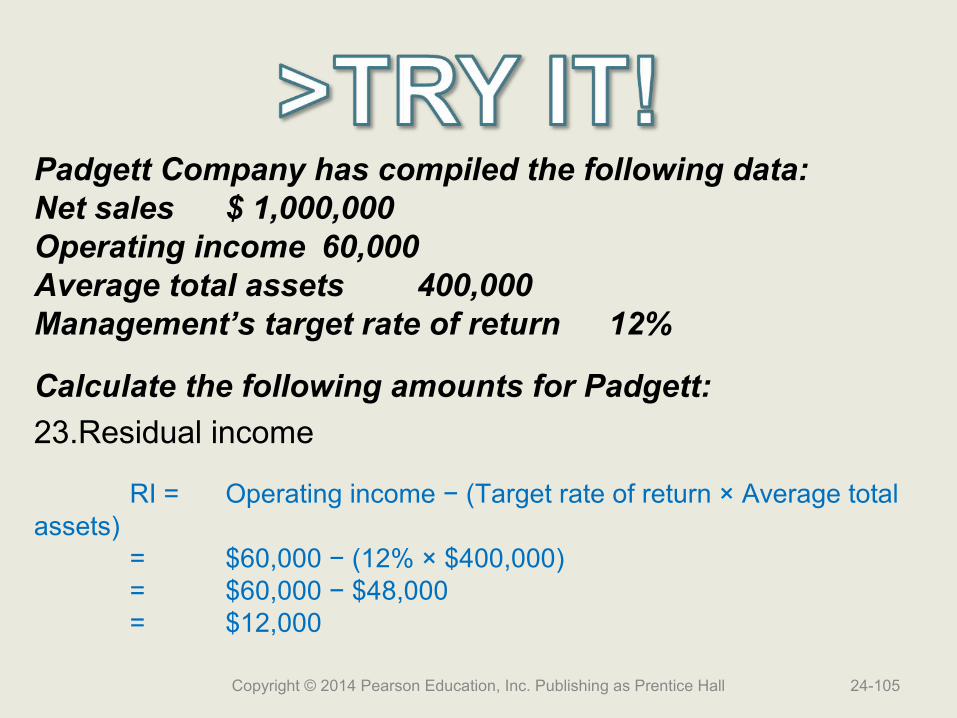

Padgett Company has compiled the following data:Net sales $ 1,000,000Operating income 60,000Average total assets 400,000Management’s target rate of return 12%

Calculate the following amounts for Padgett:

23.Residual income

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-104

Padgett Company has compiled the following data:Net sales $ 1,000,000Operating income 60,000Average total assets 400,000Management’s target rate of return 12%

Calculate the following amounts for Padgett:

23.Residual income

RI = Operating income − (Target rate of return × Average total assets)

= $60,000 − (12% × $400,000)= $60,000 − $48,000= $12,000

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-105

Learning Objective 6

Determine how transfer Determine how transfer pricing affects pricing affects decentralized decentralized

companiescompanies

(Appendix 24A)(Appendix 24A)

24-106Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall

Objectives in Setting Transfer Prices

• To achieve goal congruence by selecting a price that will maximize overall company profits

• To evaluate the managers of the responsibility centers involved

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-107

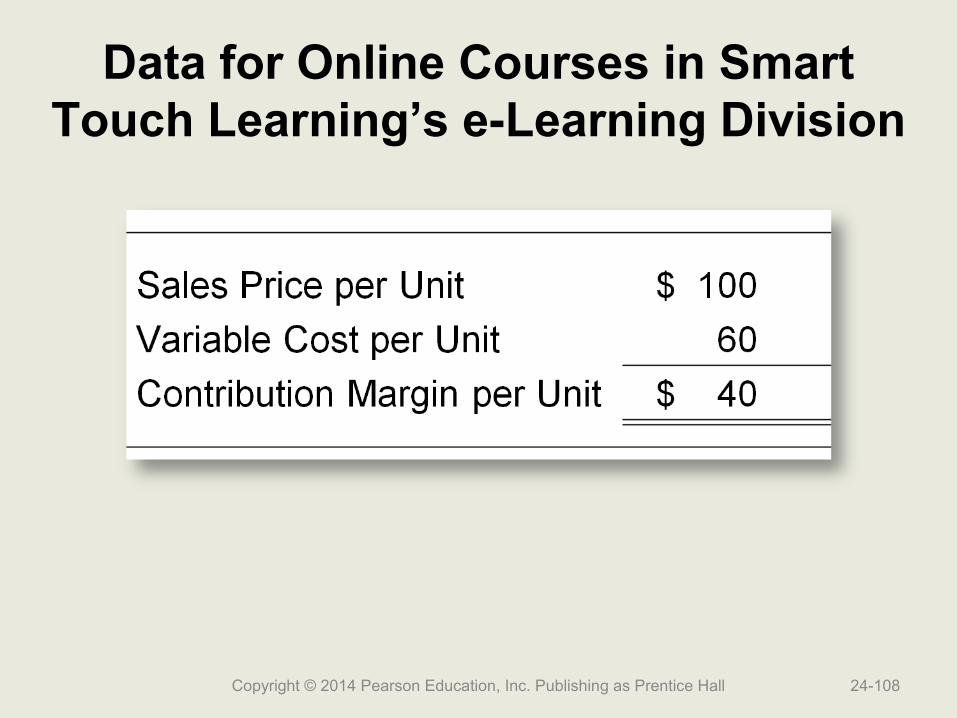

Data for Online Courses in Smart Touch Learning’s e-Learning Division

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-108

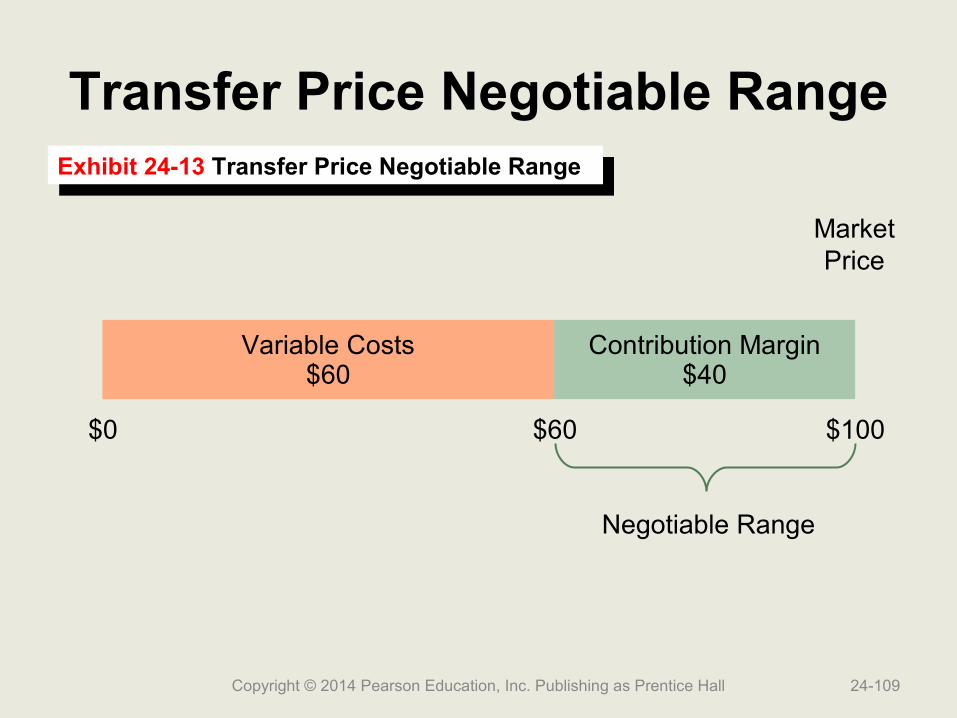

Transfer Price Negotiable Range

Variable Costs$60

Contribution Margin$40

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-109

Exhibit 24-13 Transfer Price Negotiable RangeExhibit 24-13 Transfer Price Negotiable Range

$0 $60 $100

Negotiable Range

MarketPrice

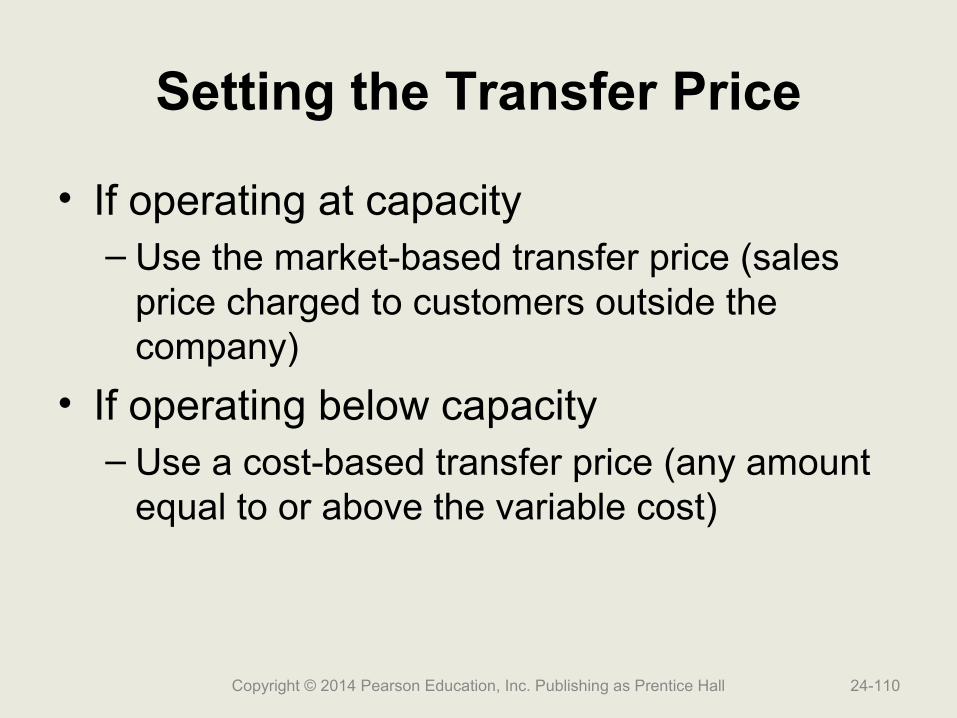

Setting the Transfer Price

• If operating at capacity– Use the market-based transfer price (sales

price charged to customers outside the company)

• If operating below capacity– Use a cost-based transfer price (any amount

equal to or above the variable cost)

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-110

Other Issues

• International issues

• Legal and ethical issues

• Difficult to determine a market price

• Nonfinancial issues

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-111

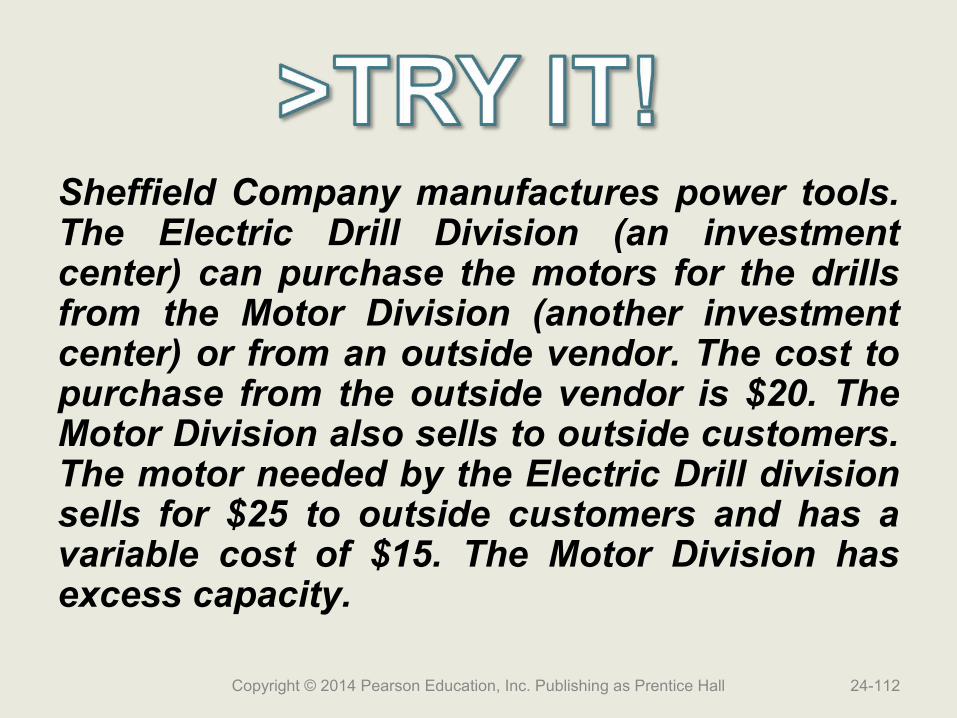

Sheffield Company manufactures power tools. The Electric Drill Division (an investment center) can purchase the motors for the drills from the Motor Division (another investment center) or from an outside vendor. The cost to purchase from the outside vendor is $20. The Motor Division also sells to outside customers. The motor needed by the Electric Drill division sells for $25 to outside customers and has a variable cost of $15. The Motor Division has excess capacity.

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-112

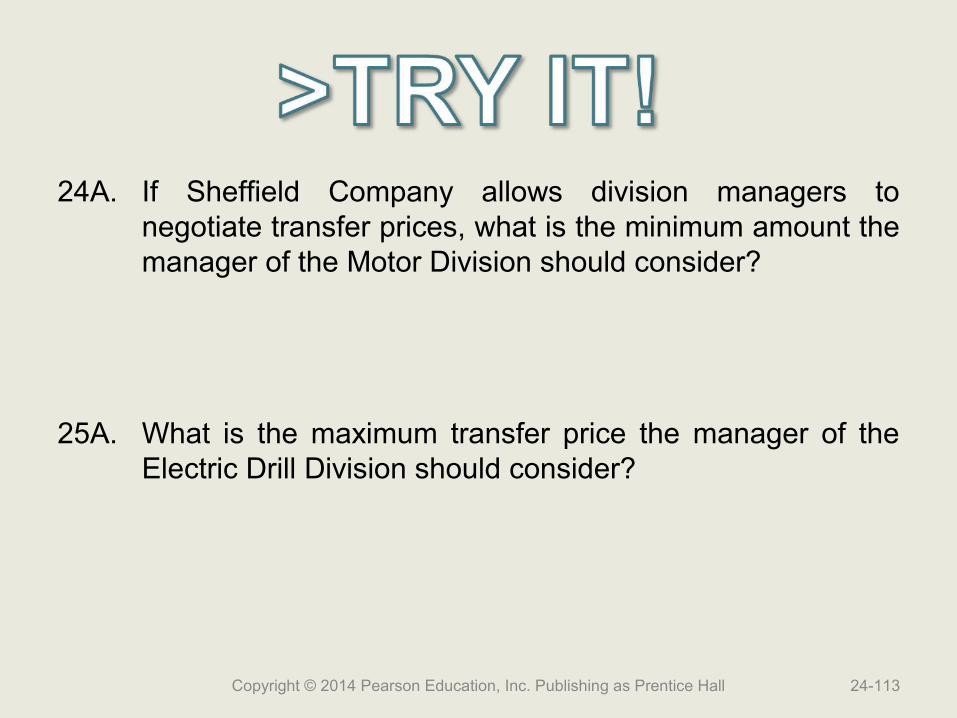

24A. If Sheffield Company allows division managers to negotiate transfer prices, what is the minimum amount the manager of the Motor Division should consider?

25A. What is the maximum transfer price the manager of the Electric Drill Division should consider?

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-113

24A. If Sheffield Company allows division managers to negotiate transfer prices, what is the minimum amount the manager of the Motor Division should consider?

The Motor Division has excess capacity, so the manager should consider the variable cost of $15 for the minimum transfer price.

25A. What is the maximum transfer price the manager of the Electric Drill Division should consider?

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-114

24A. If Sheffield Company allows division managers to negotiate transfer prices, what is the minimum amount the manager of the Motor Division should consider?

The Motor Division has excess capacity, so the manager should consider the variable cost of $15 for the minimum transfer price.

25A. What is the maximum transfer price the manager of the Electric Drill Division should consider?

The Electric Drill Division can purchase the motors from an outside vendor for $20, so that is the maximum amount the manager should consider.

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-115

Key Terms

• Decentralized Company• Goal Congruence• Investment Center• Key Performance Indicator (KPI)• Lag Indicator• Lead Indicator• Market-Based Transfer Price• Opportunity Cost

Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall 24-116

End of Chapter 24

24-117Copyright © 2014 Pearson Education, Inc. Publishing as Prentice Hall