accessing commercial capital markets

TRANSCRIPT

CommerCialaCCessing

marketsCapital

bESt PractIcES

Povertyisaglobalphenomenon.AccordingtotheWorldTradeOrganization,thenumberofpeoplelivingonlessthanUS$2perdayhasrisenbyalmost50percentsince1980toalmostonehalfoftheworld’spopulation.Inaddition,thenumberofpeoplelivinginextremepov-erty,lessthanUS$1perday,isalsogrowinginallregionsoftheworldexceptChina.

Infifty-ninecountries,theaverageincomeislowertodaythanitwastwentyyearsago.From1980to1996,onlythirty-threeofonehundredandthirtydevelopingcountriesincreasedgrowthbymorethan3percentpercapita,whilethegrossnationalproductpercapitaoffifty-ninecountriesdeclined.Around1.6billionpeopleareeconomicallyworseofftodaythanfifteenyearsago.

Overthelastfortyyears,thegapbetweentherichandthepoorhasdoubled.Therichestfifthoftheworld’spop-ulationhas80percentoftheworld’sincome,whilethepoorestfifthhaveonly1percentoftheworld’sincome,accordingtotheWorldTradeOrganization.Manypeopleseemicrofinanceasaviableandsustainablemethodtocombatpoverty.Microfinanceistheextensionofsmallloanstoimpoverishedindividuals,typicallywomen,toprovidethemwiththecapitaltostartupsmallbusinessesandtoliftthemselvesandtheirfamiliesoutofpoverty.ThesizeofmicrofinanceloanstendstobebetweenUS$50andUS$100.

DeMAND For MICroFINANCe

Seventy-fivepercentoftheworld’s550millionpoorfami-liesdonothavesufficientaccesstoaffordableandappro-priatefinancialservices.MarketdemandformicrofinanceservicesisestimatedatmorethanUS$300billionwhilemarketsupplyisonlyUS$15billion.Formicrofinancetocontinuegrowingataverageratesof15to30percent,US$2.25toUS$5billioninnewportfoliofinancing

andUS$300toUS$400millioninnewequitywillberequiredannually.Tomeetthisdemand,microfinanceinstitutions(MFIs)willneedtoaccesscapitalmarketstoclosethesupply-demandgap.MFIleadersandpotentialinvestorsneedtoknowaboutthemarketmechanismsthatareemergingtohelpthemlearnacommonlanguagethatwillfacilitatefunding.

INForMAtIoN INterMeDIArIeS

BridgingthegapbetweenMFIsandcapitalmarketsarethreemainintermediaries:ratinginstitutions,theMIXMarket,andfinancialintermediaries.RatinginstitutionshelpidentifyandassessthestateofMFIoperations.TheMIXMarketisaglobal,Web-basedmicrofinanceinforma-tionplatformthatlinksMFIswithinvestorsanddonors.MFIfinancialintermediariesarespecializedprivateinvest-mentfundsthatspecificallytargetMFIs.

Rating Institutions

OneofthegreatestchallengesMFIsencounterwhenseekingaccesstocapitalmarketsislegitimacyandproofofstability.ItisthereforenecessaryforMFIstoutilizereliableratingandassessmentserviceslikethefinancialmarkets.TheMicrofinanceRatingandAssessmentFundwasestablishedin2001asajointinitiativeoftheInter-AmericanDevelopmentBank(IDB)andtheConsultativeGrouptoAssistthePoor(CGAP).TheprimaryobjectivesoftheRatingFund,aslistedonitsWebsite,are:

• TobuildmarketsforMFIratingandassessmentservicesbyencouraginggreaterdemandfromMFIsforprofessionalexternalevaluations,aswellasbystrengthen-ingthequalityofsupply.

• ToimprovetransparencyofMFIfinancialperfor-manceasabasisforimprovedperformanceandincreasedflowofcommercialfunding.

by Isaac H. Smith, Michael A. Broderick, and Richard G. Winsor

��

Thefundwillfinance80percentofthecostofarat-ing/assessmentofanMFIbyapreapprovedinstitution(SeeTable1).

ForanMFItoqualifyforrating/assessmentfunds,ithastohaveprovidedfinancialservicesforclientsforatleastthreeyears.HundredsofMFIshavealreadyreceivedratingsandassessments—lendingcredencetothenotionofMFIsasanemergingassetclassbyimprovingthe

reliabilityandavailabilityofinformationontheriskandperformanceofMFIs.

The MIX Market

TheMIXMarketservesasaWeb-basedlinkbetweenMFIsandthepublicatlarge.Itprovidesinformationonpublicandprivatefundsthatinvestinmicrofinance,MFInetworks,ratersandexternalevaluators,advisory

Table 1: ApprovedRatingAgencies[1]

NameofAgency PrimaryProduct Regions

apoyo & asociados Internacionales

Saccredit rating Latin america

brc Investor Services credit rating Latin america

class & asociados S.a. credit rating Latin america

crISIL credit rating, risk assessment South asia

Ecuability credit rating Latin america

Equilibrium credit rating Latin america

Feller rate credit rating Latin america

Fitch ratings credit rating Latin america

Global credit rating co. credit rating Sub-Saharan africa

Jcr-VIS credit rating company

Limitedcredit rating South asia

M-crIL credit rating, risk assessment Europe, asia, and the Pacific

Microfinanza Srl risk assessmentSub-Saharan africa, Europe,

asia, and Latin america

Microfinanza Srl (ES) risk assessmentSub-Saharan africa, Europe,

asia, and Latin america

Microfinanza Srl (Fr) risk assessmentSub-Saharan africa, Europe,

asia, and Latin america

Microrate risk assessmentSub-Saharan africa, Europe,

asia, and Latin america

Microrate Latin america credit rating, risk assessmentSub-Saharan africa, Europe,

asia, and Latin america

Pacific credit rating Holding Inc. credit rating Latin america

Planet rating afrique risk assessmentSub-Saharan africa, Europe,

asia, and Latin america

Planet rating Perú Sa risk assessmentSub-Saharan africa, Europe,

asia, and Latin america

Planet rating SaS risk assessmentSub-Saharan africa, Europe,

asia, and Latin america

Standard & Poor’s credit rating Latin america

[1] agencies are approved by the rating Fund. See http://www.ratingfund.org/rater_compare.aspx for more information.

�� ESR— Fall 2007

firms,andgovernmentalandregulatoryagencies.ThegoaloftheMIXMarket,aswordedontheirWebsite,is

“toattractmorepublicandcommercially-orientedinves-torstomicrofinancebypromotingfinancialtransparency,accountability,andincreaseddisclosurestandards.”ItprovidesMFIswithanopportunitytopostaprofileontheWebtomarkettheirorganizationtoinvestorsanddonors.Likewise,investorsanddonorscanpostprofilesinanefforttodeveloppotentialmicrofinanceinvestmentopportunities.AsofJuly2007,theMIXMarkethaspro-filesof973MFIs,93investors,and163partners.

Financial Intermediaries

MFIfinancialintermediariesarespecializedinvestmentfundsthatspecificallytargetMFIs.Privateinvestorsaregiventheopportunitytoinvestinafund,whichinturn,ismanagedbyathird-partyorganizationthatinvestsinmultipleMFIs.

TheACCIONBridgeFundandtheWisconsinCoordinatingCommitteeforNicaraguaFundwerepioneeringMFIfinancialintermediaries,providingdebtfinancingtopartnerMFIsbysellingpromissorynotestothepublic.Later,in1995,ProFundwascreatedasaprivateequity,venturecapitalfundthatinvestsinfifteenLatinAmericanMFIs.In1999,LA-CIFwascreatedandismanagedbyCyranoManagement.CyranohassincelaunchednumerousfundsthatofferdifferenttypesofcapitaltoMFIsanddifferentinvestmentriskportfoliostoinvestors.

AnotherinnovativeMFIfinancialintermediaryisBlueOrchardFinance.Itwasincorporatedastheworld’sfirstinvestmentcompanythattargetedMFIsexclu-sively.Bysolicitinginvestmentsfromsocialinvestors,BlueOrchardmanagesmillionsofdollars,whichitisabletoinvestinMFIs.

OneofthemajorconstraintsofanMFIinreachingtheestimated2billionpeoplelivingbelowthepovertythresholdisthelackofcapital.Historically,capitalwasonlyaccessedthroughprivateorgovernmentdonations.Inthelastdecade,MFIshavepushedtolimitthedepen-dencyondonorcapitalandtoaccessfundingthroughthecapitalmarkets.

FUNDING veHICLeS

Microfinance Funds

Approximatelyseventy-fiveprivatesocialinvestmentfundsraisemoneytodistributetoMFIs.Manyfundsareaffiliated,invaryingdegrees,withestablisheddevel-opmentorganizations—mostlyNGOs.

Historically,thesefundsreliedsolelyonphilanthropicfunding.Currently,mostfundsarenotanddonotseektobeself-sustaining.However,afewsuccessfulfundsareemergingthatofferreturnsatornearmarketrates,andanotherfifteentotwentyoffermodestorbelow-marketreturns.

Theleadingexampleofamarket-sustainablemicrofi-nancefundistheDexiaMicro-CreditFund.DexiaBankInternationalofLuxemburgcreatedthefundin1998;itwasthefirstcommercialinvestmentfunddesignedtorefinancemicrofinanceinstitutions.Investorsinthefundrangefromretailbankingcustomerstoinstitutionalinves-tors.ThefundisactiveintwentydevelopingcountriesinLatinAmerica,Asia,andEasternEurope,andfinanc-esfortyinstitutions.

Tomanageitsmicrofinanceportfolio,DexiaAssetManagementreliesontheSwissfirmBlueOrchardFinance.BlueOrchardselectstheMFIsthroughacompre-hensivenetworkofcontacts.InorderforBlueOrchardtoselectanMFI,theMFIfirstmusthaveanindependentexternalrating.ThenBlueOrchardinitiatesafieldvisitandadatacollectionprocessfortheprospectiveMFI.OnthebasisofBlueOrchard’son-siteevaluation,thefinanc-ingcommitteedecidestoinvestornot.Iftheydoinvest,theselectedinstitutionreportsonamonthlybasisoverthewholelifeoftheinvestmentandisvisitedeveryyear.

Asset-Backed Securities

Anotheremergingassetclassinmicrofinanceisasset-backedsecurities.Amicrocreditasset-backedsecurityisabondthatiscollateralizedbythefuturecashflowsofprin-cipalandinterestrepaymentsfromanMFI’sclients.Thenatureofthisfinancinginstrumentdoesrequiretheset-tingupofanewspecialpurposecompanytomanagetheloanportfoliothathasbeensetasidetomakepayments.

OnesuchspecialpurposecompanyisBlueOrchardMicrofinanceSecurities(BOMFS)I,formedbyDevelopingWorldMarketsandBlueOrchard.InwhatwasthelargesttransactionintheUnitedStatescapitalmarketstofundmicrofinance,BOMFSI,inJuly2004,issuedaUS$40MMbondtosupportMFIsinninedevelopingcountries.InFebruary2005,BOMFSIIraisedanotherUS$47MMinthecapitalmarkets.

JPMorganhelpedplaceBOMFSIsecuritiesonWallStreet.Microfinancedebt,aswithothernewassetclasses,allowsWallStreettoprofithandsomelyfromunderwrit-ingthesenewsecuritiesandsellingthemtobrokerageclients.BOMFSIwasnoexceptionandpaidfeesaround3percent,fallinginthemiddleofthetypicalspandemandedbyinvestmentbanks.

��

best practices

Bond Issues

In2002,threemicrofinanceinstitutionsinthreedif-ferentcountriesinLatinAmericaissuedbondsinlocalcapitalmarkets,raisingapproximatelyUS$25millioninnewdebtfinancingontermsmorefavorablethanthoseavailablefrombanks.OneoftheseMFIs,Compartamos,issueda100millionMXP(approximatelyUS$10MM),three-year,13.1percentcouponbond.In2004,CompartamostappedthecapitalmarketswithaUS$44MMbondratedAAbyFitchandS&P.Bothbondplace-mentswereissuedtoindividualandinstitutionalinvestorsandbothplacementswereoversubscribed(i.e.,investordemandexceededthesupplyofbonds).

Strategic Partnerships with Commercial Banks

In2003,CASHPOR,anMFIworkinginthepoorestregionofIndia,andICICIBank,India’ssecondlargestbankandlargestprivatebank,enteredintoamutuallybeneficial,strategicpartnershipagreementtoprovidemicrofinanceservicestothepoor.CASHPOR,withitsmarketknowledgeofpoorcustomers,originatesandservicesloans,whileICICI,withitsstrongbalancesheetandvastfinancialresources,providescapital—includingworkingcapital—forCASHPORtocarryoutitswork.UnderpinningthisagreementisCASHPOR’sapprovalofloanproposals.Inthefirstyearofjointpartner-ship,CASHPORrecruitedsixthousandnewcustomersanddistributedUS$650,000.Theat-riskportfolio(i.e.,greaterthanthirtydayspastdue)was0.02percent.ForICICI,thisinvestmenthasbeenveryadvantageous,andICICIplanstocommittheequivalentofUS$1billiontothissectoroverthenextfiveyears.

LooKING ForWArD

“Wearechangingtheperceptionthatmicrofinanceinstitu-tionsarefundedonlybycharitabledonations,”saidDrewTulchin,managerofGF-USA’scapitalmarketprograms.Currently,onlyanestimated20percentofmicrofinancefundingismadebycommercialoperators,accordingtoGF-USA.“Thissuccessexpandstheequationtoincludeinvestorsasviablepartnersthroughcommercialfinancing.”

For INveStorS: A UNIQUe CoMBINAtIoN

of SoCIAL and FINANCIAL retUrNS

Oneimportantdistinctionbetweenmicrofinancedebtandotherassetclassesisthatmicrofinancedebtofferswhatiscalleddoublebottomlinereturns—whichmeansthatmicrofinancenotonlyoffersanattractivefinancialrisk-returnprofile,butitalsooffersasignificantsocialreturn.Microfinanceiswidelyrecognizedasoneofthemosteffectivepovertyreductiontools.In2005,theUnitedNationsdeclared2005astheYearofMicrocredit.

Social Returns

Microfinancehasproventobeaveryefficientwaytoalleviatepoverty.Ithasstimulatedgrassrootsentrepre-neurship,jobcreation,andcommunityandfinancialinfrastructuredevelopment;ithasraisedfamilylivingstandardsandgrowthofsmallbusinesses;andithasenhancedsocialandeconomicdevelopmentbyfacilitatingaccesstocapitalmarkets.

Appealing Financial Risk-Return Profile

WallStreetisknowntobeheartlesswhenitcomestoinvestmentdecisions.Investorslookforhighreturnsbalancedwithpotentialriskforaninvestment.Inordertointerestinvestors,microfinancedebtmustprovideanattractivereturnbasedonitsrisk.

BlueOrchardestimatesthatmicrofinancedebtoffersabetterreturnthanmonetaryinstruments.Specifically,itestimatesmicrofinancedebttohaveearnedanadditional150to200basispointswithonlyaslightlyhigherlevelofriskandconcludesitisanexcellentalternativetofiduciarydepositsorcertificatesofdeposits.

Theasset-backedsecurityBOMFSIisanexampleofavariedrisk-returnprofileinthemicrofinanceinvestmentclass.BOMFSIissuedaseven-yeardealthathasfourlayersofvariousrisksortranches.TheseniordebtportionaccountsforUS$30MM,or75percent,andisguaran-teedbyOverseasPrivateInvestmentCorporation(OPIC),

Table 2: S&P�00ReturnonInvestment[1]

SharePrice ��0�.��

CumulativeReturn ��%

2000 roI -2%

2001 roI -17%

2002 roI -24%

2003 roI 32%

2004 roI 4%

2005 roI 2%

[1] Statistics found on Yahoo!Finance in april 2006.

�0 ESR— Fall 2007

anagencyoftheU.S.federalgovernment—thusmakingthisportionarisk-freeinvestment.Thereturnontheseniortrancheisbetween0.25percentand0.5percenthigherthansimilarrisk-freetreasurysecurities.

Weak Correlation

Anotherattractiveprospectofmicrofinancedebtisthelowcorrelationthereturnshavewithotherassets.Akeystrategyforinvestorsistotrytodiversifytheirinvestmentportfoliosinanefforttoreducetheiroverallrisk.Astheworldbecomesmoreglobal,marketsbecomemoreheavilycorrelated—thusmakingitincreasinglydifficultforinves-torstodiversifytheirportfoliorisk.

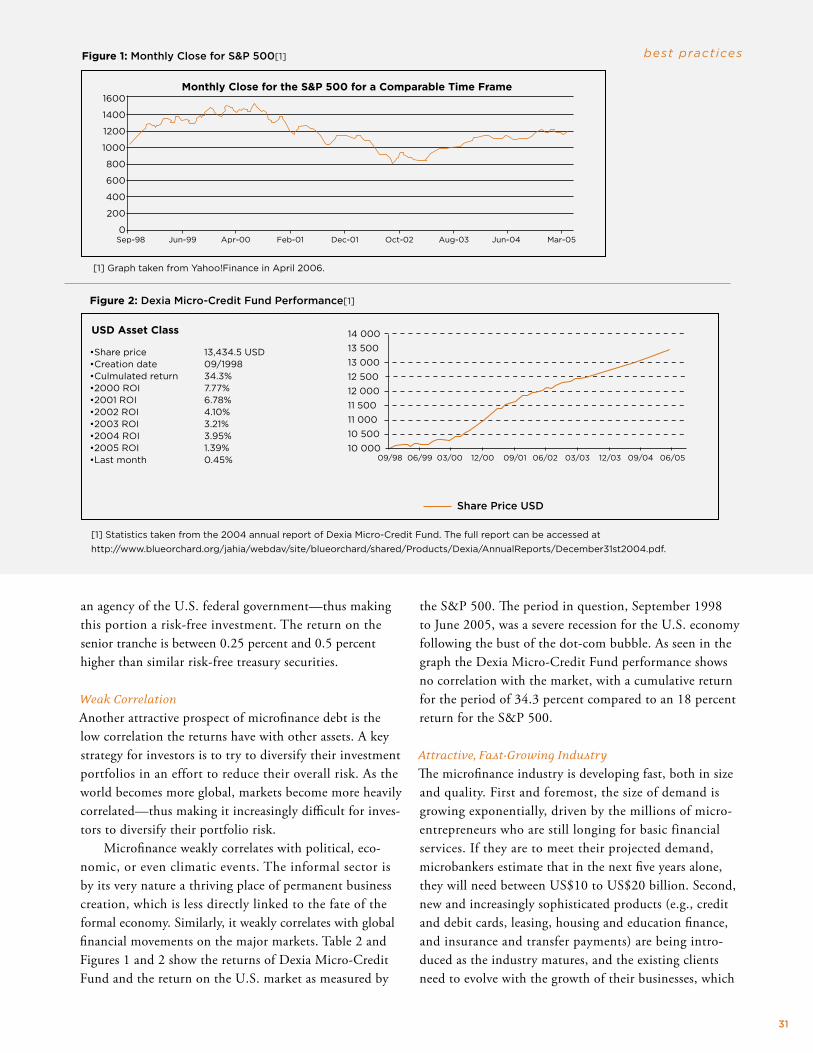

Microfinanceweaklycorrelateswithpolitical,eco-nomic,orevenclimaticevents.Theinformalsectorisbyitsverynatureathrivingplaceofpermanentbusinesscreation,whichislessdirectlylinkedtothefateoftheformaleconomy.Similarly,itweaklycorrelateswithglobalfinancialmovementsonthemajormarkets.Table2andFigures1and2showthereturnsofDexiaMicro-CreditFundandthereturnontheU.S.marketasmeasuredby

theS&P500.Theperiodinquestion,September1998toJune2005,wasasevererecessionfortheU.S.economyfollowingthebustofthedot-combubble.AsseeninthegraphtheDexiaMicro-CreditFundperformanceshowsnocorrelationwiththemarket,withacumulativereturnfortheperiodof34.3percentcomparedtoan18percentreturnfortheS&P500.

Attractive, Fast-Growing Industry

Themicrofinanceindustryisdevelopingfast,bothinsizeandquality.Firstandforemost,thesizeofdemandisgrowingexponentially,drivenbythemillionsofmicro-entrepreneurswhoarestilllongingforbasicfinancialservices.Iftheyaretomeettheirprojecteddemand,microbankersestimatethatinthenextfiveyearsalone,theywillneedbetweenUS$10toUS$20billion.Second,newandincreasinglysophisticatedproducts(e.g.,creditanddebitcards,leasing,housingandeducationfinance,andinsuranceandtransferpayments)arebeingintro-ducedastheindustrymatures,andtheexistingclientsneedtoevolvewiththegrowthoftheirbusinesses,which

��

best practices

pushesstillfurtherthefundingrequirementsofthisindustry.Competitioniscurrentlylimitedornon-existentinmostmarkets,particularlyinAsiaandAfrica,creatingauniqueshort-termgrowthopportunityformicrofinanceserviceproviderstocapitalizeontheindustry’sattractivereturns.

Theindustryhasadocumentedtrackrecordofmorethanfifteenyearsthatshowsaglobalassetqualitystrongerthanotherfinancialassetclasses.Overthelastfiveyears,

“winners”haveemergedfromtheindustry’sfragmentedmarketplace,settingstandardsforbestpractice.

reASoN Not to INveSt

Withanyuniqueemergingassetclassthereisalwayssomeuncertainty.Investorsanduncertaintydonotlikeeachother,andthereexistrealquestionsaboutthequalityandsafetyofmicrofinanceinvestments.

Someofthecriticismsofmicrofinancedebtinclude:• Themajorityofmicrofinancedebtisnottradedin

aliquidmarketandisthereforedifficulttoprice.• Thereiscurrentlynotalargeenoughamountof

microfinancedebtforinstitutionalinvestorstouseasakeyinvestmenttodiversifyrisk.

• Thelevelofformalfinancialdisclosureisnotasfor-malizedasothertypesofinvestments,whichcouldleadtoexaggeratedperceptionofdefaultrisk.

• InvestorsdonothaveanyexpertisewithMFIsandmicrofinancedebt.

Thelistpinpointsareasofconcernmainlyfromaninstitutionalinvestor’sperspective.Thepositivenewsisthattherearenotunderlyingweaknessesintheessentialsofthemicrofinanceindustry.Rather,mostitemscanbeovercomethroughbettercommunicationofthemarket’sfundamentalsandthroughchangesinthewaytheindus-trypresentsitselftoinvestors.

For MFIS: BreAKING into the GAMe

MFIstraditionallyhavereliedondonorstoprovidefundingformicrocredit.Manyarenotsurehowtoaccesscapitalmarketsthemselvesandmaynotevenseeareasontopursuethissourceoffunding.

reASoNS to ACCeSS CAPItAL MArKetS

ThemerenotionofaccessingcapitalmarketsmaybecompletelyforeigntomanyMFIs.Whatisthepurposeofaccessingcapitalmarkets?MFIsarecurrentlysatisfyingonlyanestimated10percentofthedemandformicro-

credit.ThefullsizeofthemarketisroughlyUS$300bil-lion,whiledonorsonlyaccountforlessthanUS$1billionperyear.Meetingdemandwillrequireanever-increasinginfluxofcashflows.Privateinvestorsviacapitalmarketsarethemostrealisticsourceforsuchanimmenseamountofneededfunds.

AsecondaryreasonforMFIstoworktowardsaccessingcapitalmarketsisthatitwillinevitablyleadtoincreasedoperationalefficiency,financialaccountability,andtrans-parency.Justtobeconsideredbyprivateinvestors,anMFIwouldneedtoproveitselfasaviableorganizationwithcompetentmanagementandsustainableoperations.

HoW to GAIN ACCeSS

WeofferfourkeyrecommendationsforMFIsseek-ingtoaccesscapitalmarkets.First—andmostdiffi-cult—anMFImustbecomeprofitableandself-sufficient.Otherwise,privateinvestorswillbereluctanttorisktheircapital.Second,getaratingandassessmentfromanaccreditedorganization.Third,registerontheMIXMarket.Fourth,network.

Become profitable:FormanyMFIs,thenotionofprofitabilitymaybedaunting,intimidating,andseeminglyoutofreach.Toeffectivelyaccesscapitalmarkets,however,MFIsmustbecomesustainableorganizationsthatinvestorscanhaveconfidencein.Thefirststeptowardprofitabilityislearningthelanguageofbusiness.MFIsmustbecomefamiliarwithbasicbusinessterminologytoleveltheplay-ingfieldwithinvestors.Thesecondstepistoincorporatebasicbusinesspractices(e.g.,financialmanagement)intostandardoperations.AsimpleInternetsearchcanpro-videcountlesssourcesofinformationtohelpMFIsbetter

�� ESR— Fall 2007

ABOUTTHEAUTHORS

Issac H. Smith, Michael A. Broderick, and Richard G.

Winsor put their minds together for a field study in early

2006. For an academic course available to MBa and MPa

students at Brigham young university, smith, Broderick,

and Winsor conducted research for the EsR Center. as part

of their research they gathered many key players in the

field of microfinance together for a focus group—including

John hatch of FINCa, Ellen Vor der Bruegge of Freedom

From hunger, Mushtaque Chowdhury of BRaC, and louis

Pope and troy holmberg of yehu Microfinance. smith

and Broderick earned MBa degrees from Brigham young

university in 2007, and Winsor graduated from Brigham

young university’s MPa program in 2006.

managetheirorganizationandworktowardprofitability.Forexample,athttp://www.managementhelp.org/finance/fp_fnce/fp_fnce.htm,aWebsitetitled“BasicGuidetoFinancialManagementInFor-Profits,” adviceisgivenonbasicbookkeeping,budgetmanagement,financialstate-mentdevelopment,andmuchmore.

Thereisarisktofocusingonprofitability:atheorycalledmissiondrift.Asthetheorygoes,assoonasanon-profitorganizationbeginstofocusonsustainabilityandprofitability,theybegintolosesightoftheverymissionandpurposeforwhichtheycameintoexistence.Itmustbeunderstood,however,thatifthelong-termgoalofmicrofinanceistohelpalleviatepovertybyprovidingthepoorwithaccesstocapital,thenbillionsmoredollarsneedtoberaisedtomeetthemassivedemand.Becomingprofitableandmorebusiness-likeinordertoaccesscapitalmarketsisoneofthemostpromisingoptionsfortheMFIcommunitytomeetitsultimategoalofofferingcapitaltoallwhoneedit.MFIsmaythereforelookataccessingcapitalmarketsascentraltotheirmission,notasadetrac-torfromit.

Get a rating: Informationaboutratingandassessmentscanbefoundathttp://www.ratingfund.org,theofficialWebsiteoftheMicrofinanceRatingandAssessmentFund.Aformalratingandassessmentfromapreapprovedratingorganizationservestwopurposes.Firstofall,anassessmentcanincreasethelikelihoodofanMFIbecom-ingprofitable.Theratingandassessmentwillhelpidentifyareasofconcernandareasofneededimprovement.Forexample,inDecember2004,FINCAMexicoreceivedaratingfromMicroRate,amicrofinanceratingagency.Theratingincludedathirteen-pagereportdetailingtheoperations,portfolioquality,managementandorganiza-tion,personnelandproductivity,operatingefficiency,governanceandstrategicpositioning,andfinancialdata.Aratingandassessmentcanprovideinvaluableinforma-tionforanMFIthatisonthebrinkofprofitability.

Second,foraprofitableMFIthatisseekingcapitalmarketfunding,aratingprovidesinvestorswithneededinformationtomakeanestimateoftheriskassociatedwithinvestinginthatMFI.Reliableratingsallowinves-torstobenchmarkMFIsagainsteachotherandmakeinformedinvestmentdecisions.OvertwohundredMFIratingandassessmentreportsarepostedontheMicrofinanceRatingandAssessmentFundWebsite.

Register on the MIX Market:AnMFIcanregisterontheMIXMarketthroughitsWebsite:http://www

.mixmarket.org.AccordingtotheWebsite,“TheMIXMarketstrivestofacilitateexchangeandinvestmentsflows,promotetransparency,andimprovereportingstandardsinthemicrofinanceindustry.”Byregistering,MFIsexposetheirorganizationtopotentialdonorsandinvestors.

Network:Althoughobvious,itshouldnotbeunderem-phasizedthatoneofthebestwaystoaccomplishagoalistolearnfromsomeonewhohasalreadyaccomplishedthatgoal.NumerousMFIshavesuccessfullyaccessedcapi-talmarkets.Networkingwiththeseorganizationsisanimportantopportunitytolearnfrompastfailuresandsuc-cesses.TheConsultativeGrouptoAssistthePoor(CGAP)regularlypoststheMicrofinanceCapitalMarketsUpdateonitsWebsite.ThereportliststherecentdebtandequitydealsbetweenMFIsandinvestors.NetworkingwithorganizationscurrentlyintheprocessofaccessingcapitalmarketscanalsoprovideMFIswithvaluableinformation.

CoNCLUSIoN

Povertyamidstgreatprosperityhasalwaysexisted,inlargemeasurebecausemanyoftheworld’spoorwereshutoutofthesamemarketsthatmadeotherswealthy.Microfinancerepresentsatoolthatcanbringtheworld’spoormorefullyintoexistingmarkets.Wehavesuggestedhereanumberofreasonsandwaysthatmicrofinanceorganizationsandinvestorscanworktogethertobringthevirtuesandfruitsoffinancialmarketstomicrofi-nanceinstitutions.

��

best practices